Topic 8 Accounting for Partnership Part 1

Topic 8 -_partnership_part_i

Jul 15, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Topic 8

Accounting for Partnership

Part 1

8.1 Nature of Partnership

• A partnership is an unincorporated

association of two or more people to pursue a

business for profit as co-owners. In Malaysia,

this business form is governed under the

Partnership Act 1961.

• A partnership is defined as:

“the relation which subsists between personscarrying on business in common with a view ofprofit”.

[Para II, Section 3(1) of the Partnership Act 1961]

BKAF3063 A141

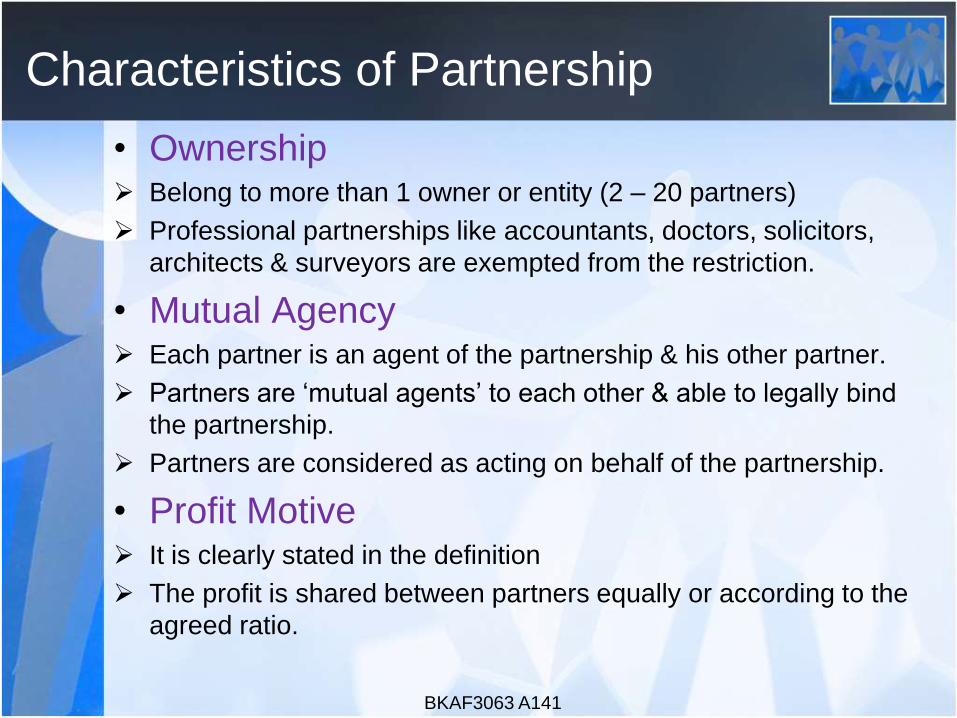

Characteristics of Partnership

• Ownership Belong to more than 1 owner or entity (2 – 20 partners)

Professional partnerships like accountants, doctors, solicitors,

architects & surveyors are exempted from the restriction.

• Mutual Agency Each partner is an agent of the partnership & his other partner.

Partners are ‘mutual agents’ to each other & able to legally bind

the partnership.

Partners are considered as acting on behalf of the partnership.

• Profit Motive It is clearly stated in the definition

The profit is shared between partners equally or according to the

agreed ratio.

BKAF3063 A141

Characteristics of Partnership

• Partnership Agreement Not required by law but making partners clear regarding their

mutual rights & duties.

Also as an evidence & reference for any future issues & conflict.

• Limited Life Will dissolve by itself if any of the partners withdraw, insane,

bankrupt or dies.

Some dissolve with or without court order.

Case of death – the descendant has the right upon the share of

the late partner.

• Share of Liability Every partner (except for limited partners) has unlimited liability –

liable for partnership debts, including the use of personal assets.

BKAF3063 A141

Characteristics of Partnership

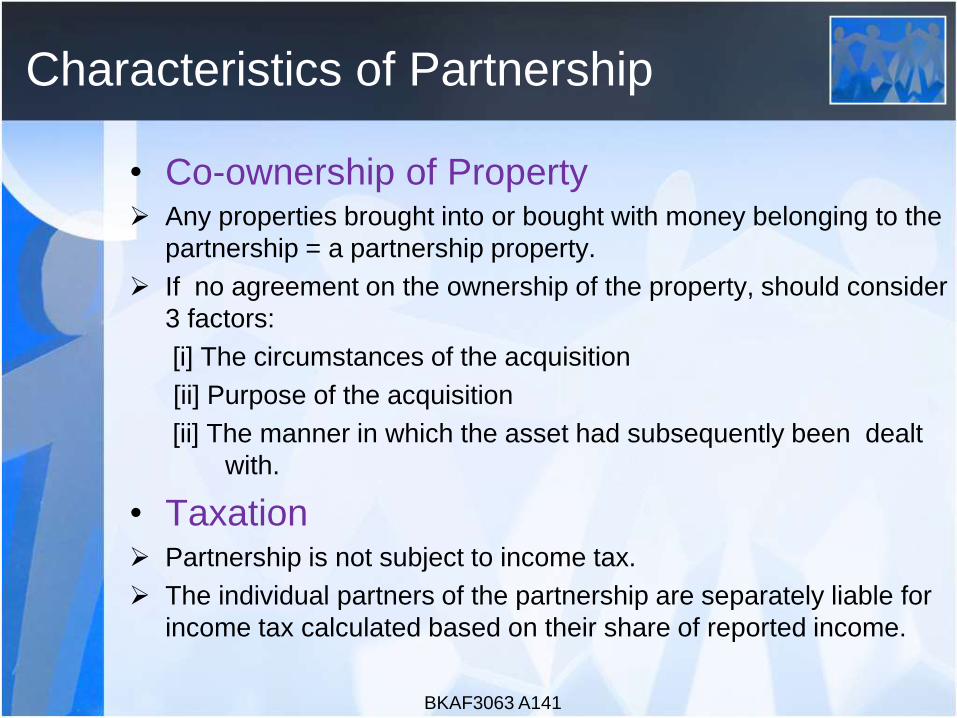

• Co-ownership of Property Any properties brought into or bought with money belonging to the

partnership = a partnership property.

If no agreement on the ownership of the property, should consider

3 factors:

[i] The circumstances of the acquisition

[ii] Purpose of the acquisition

[ii] The manner in which the asset had subsequently been dealt

with.

• Taxation Partnership is not subject to income tax.

The individual partners of the partnership are separately liable for

income tax calculated based on their share of reported income.

BKAF3063 A141

Advantages of Partnership

Ability to share knowledge, expertise, and experience among co-

partners in the business.

Easy to form the partnership firm and lower cost of formation as

compared to the other types of business organizations.

Enables firm to get additional sources of investment capital from

each partner since more than one partner is within the partnership

firm.

Possible tax advantages where a partnership has the same tax

status as a sole proprietorship and is, therefore, not subject to

taxes on its income.

Easy to manage and decisions can be made with less

bureaucracy since the owners of the partnership firm are usually

its managers.

BKAF3063 A141

Disadvantages of Partnership

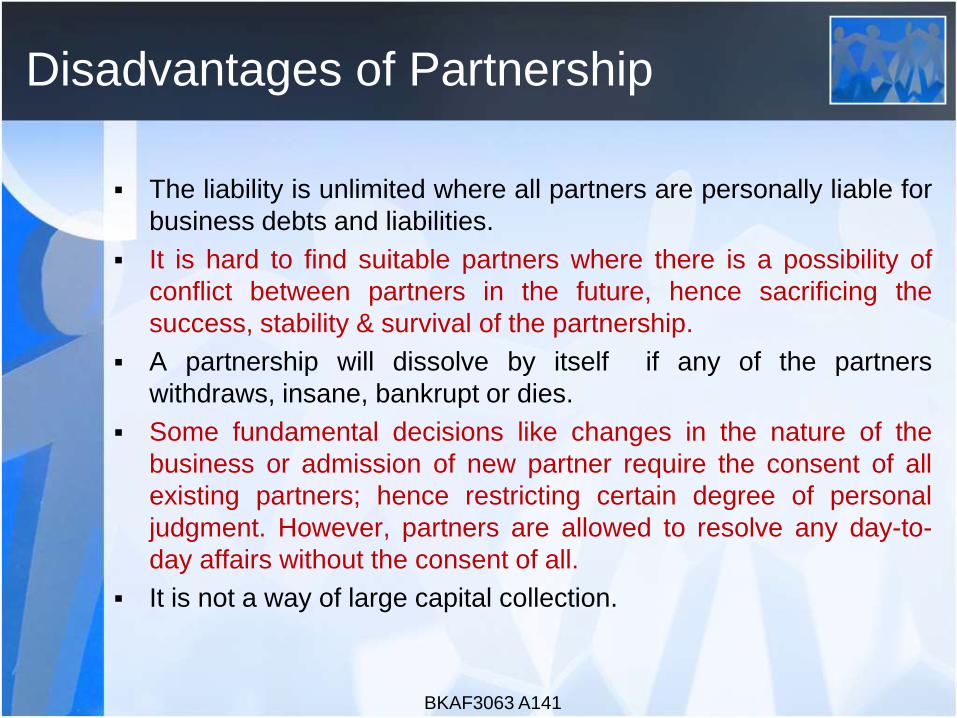

The liability is unlimited where all partners are personally liable for

business debts and liabilities.

It is hard to find suitable partners where there is a possibility of

conflict between partners in the future, hence sacrificing the

success, stability & survival of the partnership.

A partnership will dissolve by itself if any of the partners

withdraws, insane, bankrupt or dies.

Some fundamental decisions like changes in the nature of the

business or admission of new partner require the consent of all

existing partners; hence restricting certain degree of personal

judgment. However, partners are allowed to resolve any day-to-

day affairs without the consent of all.

It is not a way of large capital collection.

BKAF3063 A141

8.2 Partnership Agreement

• A partnership is based on a contract between

individuals. It is an agreement among the members of

a firm for sharing the profits of the business carried on

by all or any of them acting for all.

• Partnership agreements normally include the following

details:

1. Name of the firm.

2. Name of all partners and contributions made by each

partner.

3. Nature of the business.

4. Date of commencement of partnership.

5. Duration of partnership, if any.

BKAF3063 A141

Partnership Agreement

6. Rights and duties of all partners.

7. Sharing of profit and losses.

8. Interest charged on capital.

9. Withdrawal arrangement and interest charged on

drawings.

10. Salaries, bonus, commissions, etc to the partners.

11. Interest on loan by the partner(s) of the firm.

12. Dispute procedures.

13. Admission and withdrawal of partners.

14. Rights and duties in the event of partner dies.

15. Dissolution of partnership.

BKAF3063 A141

In the Absence of a Partnership

Agreement

• Need to comply with the rules under S. 26 of the

Partnership Act 1961:

1. Every partner may take part in the management of the

partnership business.

2. No partner shall be entitled to remuneration or salary for acting in

the partnership business.

3. No change may be made in the nature of the partnership

business without the consent of all the existing partners but a

majority of the partners are entitled to resolve differences of

opinion concerning day-to-day business affairs.

4. The partnership books are to be kept at the place of business of

partnership, and every partner have access to inspect and copy

any of them.

5. Partners are entitled to share equally in profit or losses of the

business.

BKAF3063 A141

In the Absence of a Partnership

Agreement

6. A partner is not entitled to interest on the capital subscribed by

him.

7. A partner making payment or advance beyond the amount of

capital subscribed is entitled to interest at the rate of 8% per

annum from the date of the payment or advance.

8. No interest will be charged on drawings made by partners.

9. No person may be introduced as a partner without the consent of

all existing partners.

BKAF3063 A141

8.3 Partnership Accounts

• Capital Accounts Opened for each partner to record the capital contributed when

the partnership is formed.

When partners invest in a partnership, their capital accounts arecredited for the invested amounts.

Each partner’s investment is recorded at an agreed-on value,normally the market values of the contributed assets and liabilitiesat the date of contribution.

Journal entry is:

Cash/ Bank/ Assets Accounts XX

Partner’s Capital Accounts XX

Generally remain unchanged from year to year [also referred as

fixed capital ac]

Current ac is needed to show the changes in transactions etc.

BKAF3063 A141

Partnership Accounts

• Current Accounts Recording frequent transactions between the partners & the firm.

Increase when partners receive interest on capital, interest on

loan, salary & the remaining profits made by the business.

Decrease if the partners make any drawings, or are charged

interests on the drawings during the year…can even get a debit

balance if any partners withdraw more than their share of profits.

• Fluctuating Capital Accounts Include all the relevant transactions (interests, drawings etc),

hence fluctuating throughout the accounting period.

Disadvantage ‘coz cannot ascertain which partner has made

drawings in excess of his share of profits.

BKAF3063 A141

Partnership Accounts

• Profit Appropriation Account Showing net profit appropriated to each of the partners.

Also shows any other allocation of profits to the partners (eg.

salaries, interest on capital and interest on drawings).

The following adjustments are needed to prepare the ac:

1. Interest on Capital

Partners can agree to allocate “interest allowance (or interest on

capital)” based on the amounts invested by each partner.

Journal entry for crediting interest on capital to the Partner’s

Capital/Current Ac:

Profit Appropriation Ac XX

Partners' Capital/Current Account XX

BKAF3063 A141

Profit Appropriation Account

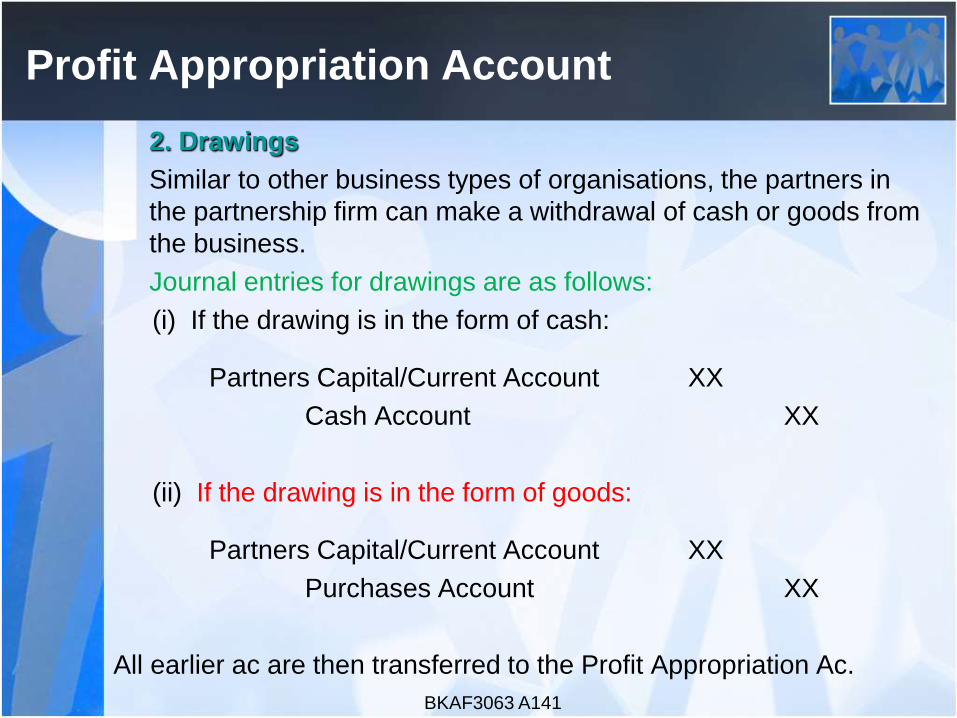

2. Drawings

Similar to other business types of organisations, the partners in

the partnership firm can make a withdrawal of cash or goods from

the business.

Journal entries for drawings are as follows:

(i) If the drawing is in the form of cash:

Partners Capital/Current Account XX

Cash Account XX

(ii) If the drawing is in the form of goods:

Partners Capital/Current Account XX

Purchases Account XX

All earlier ac are then transferred to the Profit Appropriation Ac.

BKAF3063 A141

Profit Appropriation Account

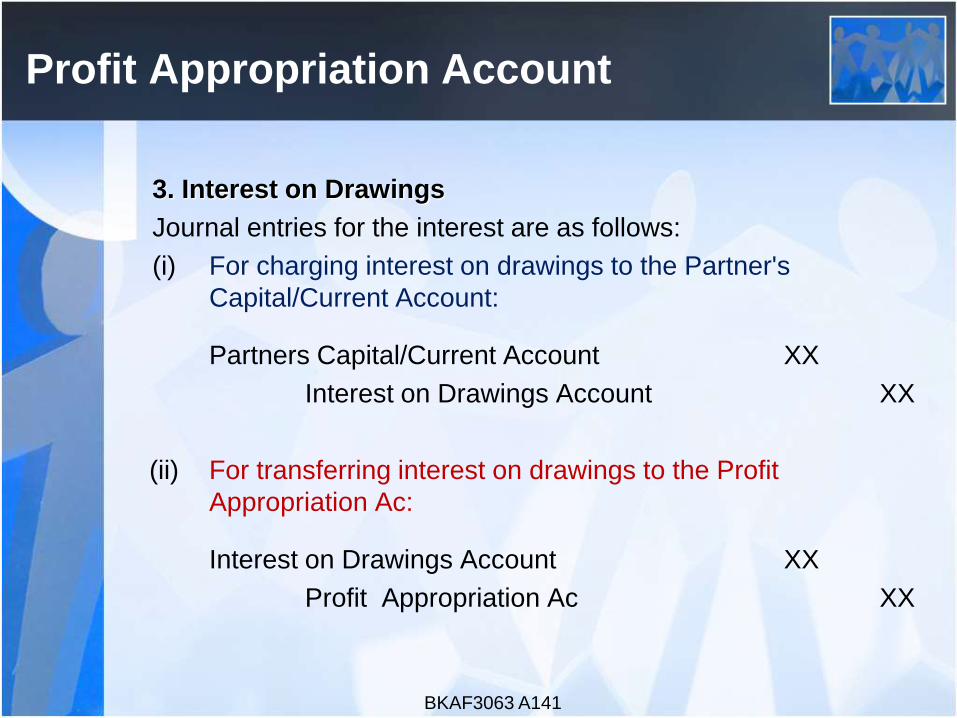

3. Interest on Drawings

Journal entries for the interest are as follows:

(i) For charging interest on drawings to the Partner's

Capital/Current Account:

Partners Capital/Current Account XX

Interest on Drawings Account XX

(ii) For transferring interest on drawings to the Profit

Appropriation Ac:

Interest on Drawings Account XX

Profit Appropriation Ac XX

BKAF3063 A141

Profit Appropriation Account

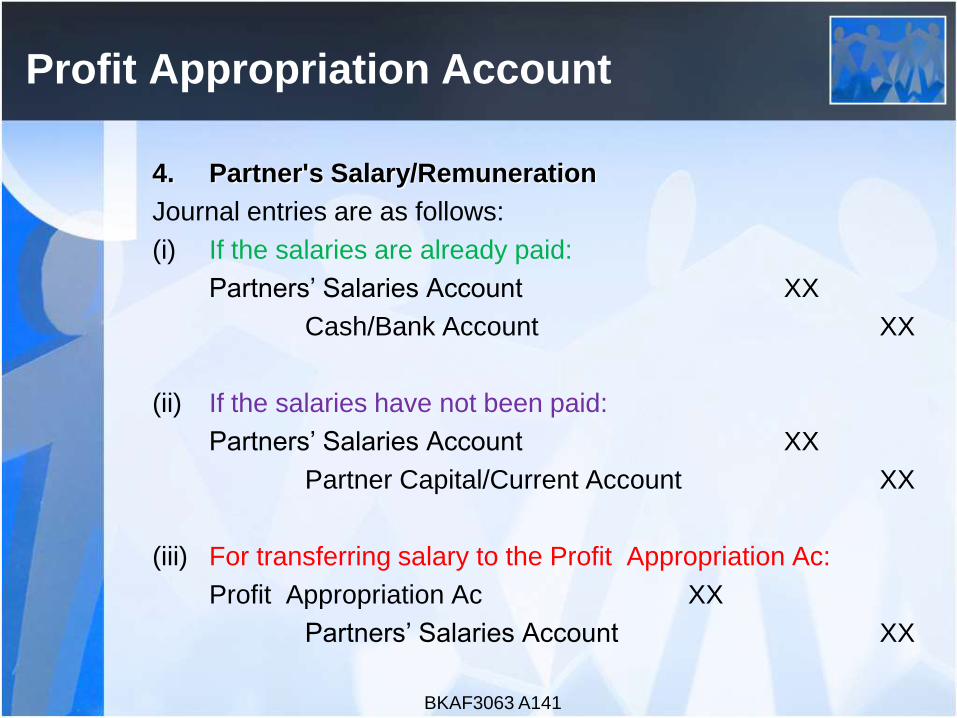

4. Partner's Salary/Remuneration

Journal entries are as follows:

(i) If the salaries are already paid:

Partners’ Salaries Account XX

Cash/Bank Account XX

(ii) If the salaries have not been paid:

Partners’ Salaries Account XX

Partner Capital/Current Account XX

(iii) For transferring salary to the Profit Appropriation Ac:

Profit Appropriation Ac XX

Partners’ Salaries Account XX

BKAF3063 A141

Profit Appropriation Account

5. Partner's Commission

Any commission paid to the partners is a gain to partners but an

expense to the partnership firm. When this happens, the following

journal entry is made:

Commission to Partner’s Account XX

Partner's Capital/Current Account XX

The commission paid to a partner is then charged to Profit

Appropriation Ac by recording the following entry:

Profit Appropriation Ac XX

Commission to Partner’s Account XX

6. Transfer to Reserve

Profit Appropriation Ac XX

Reserve XXBKAF3063 A141

Profit Appropriation Account

7. Share of Profits or Losses

Partners can agree to any method of dividing profits or losses.

In the absence of an agreement, the law says that the partners

share profits or losses of a partnership equally.

• If the resulting balance in the Profit and Loss Appropriation is

profits, the entry is:

Profit Appropriation Ac XX

Partner's Capital/Current Account XX

If the resulting balance in the Profit and Loss Appropriation is

losses, the entry is:

Partner's Capital/Current Account XX

Profit and Loss Appropriation XX

BKAF3063 A141

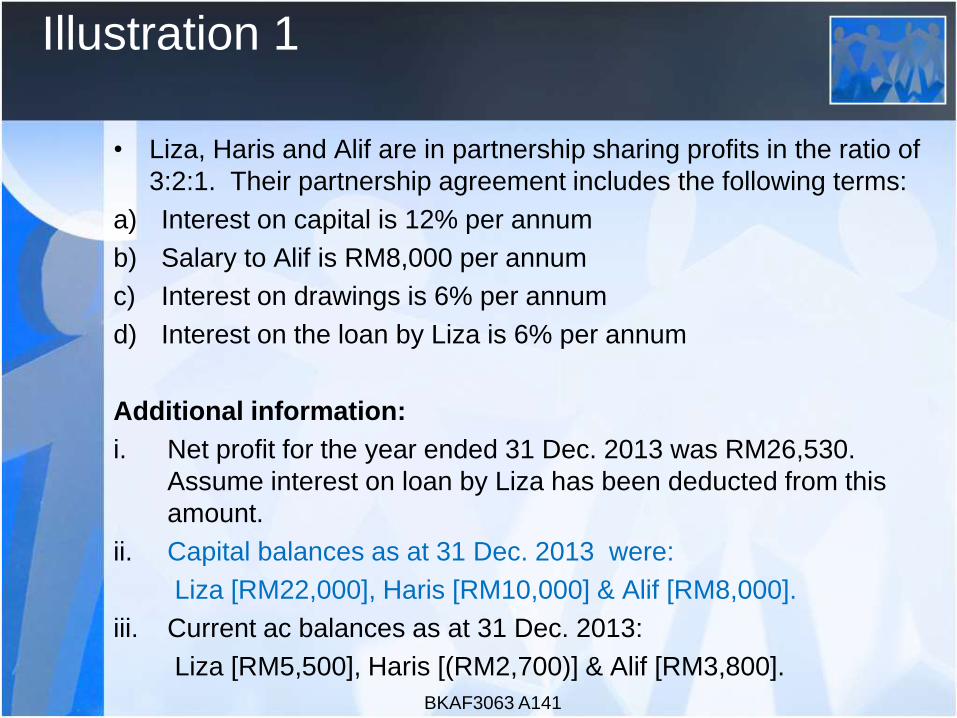

Illustration 1

• Liza, Haris and Alif are in partnership sharing profits in the ratio of

3:2:1. Their partnership agreement includes the following terms:

a) Interest on capital is 12% per annum

b) Salary to Alif is RM8,000 per annum

c) Interest on drawings is 6% per annum

d) Interest on the loan by Liza is 6% per annum

Additional information:

i. Net profit for the year ended 31 Dec. 2013 was RM26,530.

Assume interest on loan by Liza has been deducted from this

amount.

ii. Capital balances as at 31 Dec. 2013 were:

Liza [RM22,000], Haris [RM10,000] & Alif [RM8,000].

iii. Current ac balances as at 31 Dec. 2013:

Liza [RM5,500], Haris [(RM2,700)] & Alif [RM3,800].

BKAF3063 A141

Illustration 1

iv. Drawings by the partners during the year were:

Liza [RM8,000], Haris [RM6,000] & Alif [RM9,000].

v. Loan from Liza RM8,000.

Required:

Prepare profit appropriation ac, capital ac, current ac and a statement

of financial position as at 31 Dec. 2013 .

Suggested Solution & Explanatory Notes:

[1] The net profit balance is RM26,530. Note that all the

transactions recorded in the profit appropriation ac have a

corresponding double entry in the current ac.

[2] Interest on capital. The following interests are calculated based

on the balance in the capital ac & not in the current ac.

However, the interests are recorded in the current ac.

BKAF3063 A141

Illustration 1

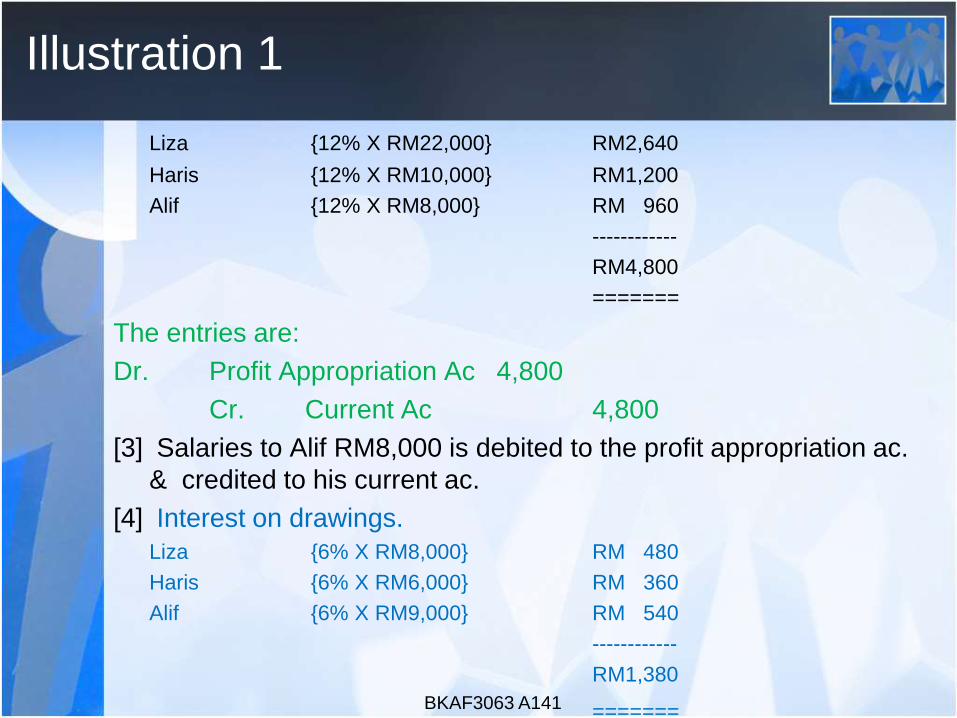

Liza {12% X RM22,000} RM2,640

Haris {12% X RM10,000} RM1,200

Alif {12% X RM8,000} RM 960

------------

RM4,800

=======

The entries are:

Dr. Profit Appropriation Ac 4,800

Cr. Current Ac 4,800

[3] Salaries to Alif RM8,000 is debited to the profit appropriation ac.

& credited to his current ac.

[4] Interest on drawings.

Liza {6% X RM8,000} RM 480

Haris {6% X RM6,000} RM 360

Alif {6% X RM9,000} RM 540

------------

RM1,380

======= BKAF3063 A141

Illustration 1

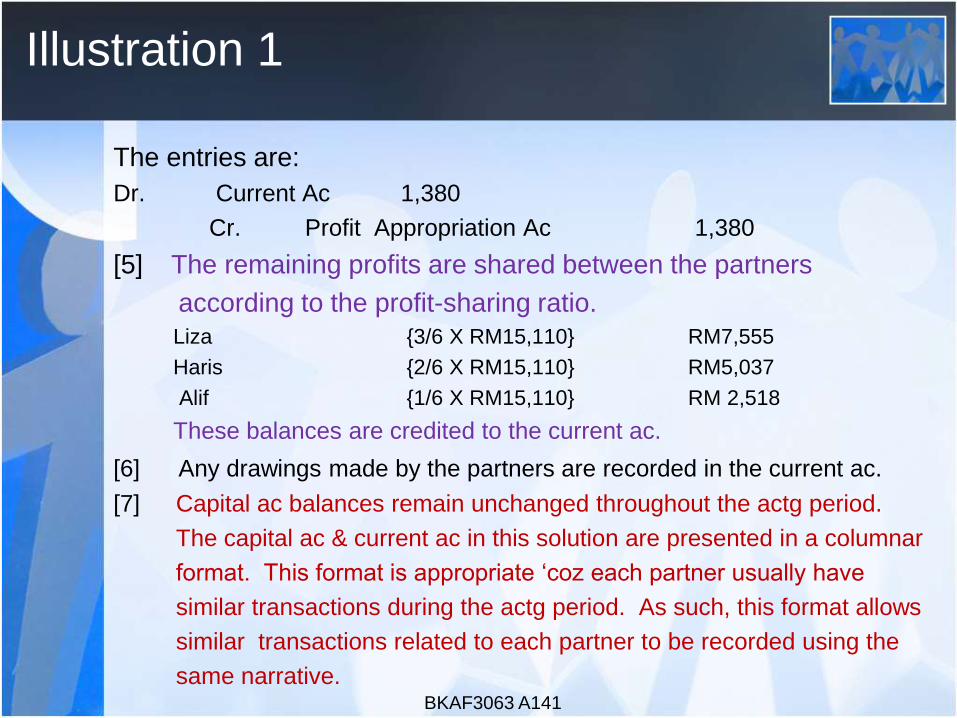

The entries are:

Dr. Current Ac 1,380

Cr. Profit Appropriation Ac 1,380

[5] The remaining profits are shared between the partners

according to the profit-sharing ratio.

Liza {3/6 X RM15,110} RM7,555

Haris {2/6 X RM15,110} RM5,037

Alif {1/6 X RM15,110} RM 2,518

These balances are credited to the current ac.

[6] Any drawings made by the partners are recorded in the current ac.

[7] Capital ac balances remain unchanged throughout the actg period.

The capital ac & current ac in this solution are presented in a columnar

format. This format is appropriate ‘coz each partner usually have

similar transactions during the actg period. As such, this format allows

similar transactions related to each partner to be recorded using the

same narrative.BKAF3063 A141

Illustration 1

[8] Haris’s ac shows a debit balance since he has overdrawn his current ac.

[9] Net assets calculation.

Balance as at 31 Dec. 2013: RM

Capital ac (22,000 + 10,000 + 8,000) 40,000

Current ac (5,500 – 2,700 + 3,800) 6,600

Loan – Liza 8,000

---------

54,600

Net profit 26,530

Drawings (23,000)

---------

58,130

=====

BKAF3063 A141

Liza Haris Alif

Profit Appropriation Account

BKAF3063 A141

RM RM RM RM

Interest on capital [2] Net profit b/d [1] 26,530

Liza 2,640 Interest on drawings [4]

Haris 1,200 Liza 480

Alif 960 Haris 360

--------- 4,800 Alif 540

Salaries – Alif [3] 8,000 ------- 1,380

Remaining profits [5]

Liza 7,555

Haris 5,037

Alif 2,518

--------- 15,110

----------- ----------

27,910 27,910

======= ======

Current Accounts

Liza Haris Alif Liza Haris Alif

RM RM RM RM RM RM

Balance b/d - 2,700 - Balance b/d 5,500 - 3,800

Drawings [6] 8,000 6,000 9,000 Interest on capital

[2]

2,640 1,200 960

Interest on

drawings [4]

480 360 540 Salary [3] - - 8,000

Balance c/d [8] 7,215 - 5,738 Remaining profit [5] 7,555 5,037 2,518

Balance c/d [8] - 2,823 -

-------- -------- ------- --------- -------- --------

15,695 9,060 15,278 15,695 9,060 15,278

===== ==== ===== ===== ==== =====

BKAF3063 A141

Liza Haris Alif Liza Haris Alif

RM RM RM RM RM RM

Balance c/d 22,000 10,000 8,000 Balance b/d [7] 22,000 10,000 8,000

===== ===== ===== ===== ===== ====

Capital Accounts

Liza Haris Alif

Statement of Financial Position as at 31 December 2013

RM RM

Net assets [9] 58,130

Financed by:

Capital Accounts

Liza 22,000

Haris 10,000

Alif 8,000

40,000

Current Accounts

Liza 7,215

Haris (2,823)

Alif 5,738

10,130

Loan: Liza 8,000

58,130BKAF3063 A141

Related Documents