Corporate Financial Policy Semester A 2012-13 City University of Hong Kong AC4331 – Topic 6

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 1/108

Corporate Financial Policy

Semester A 2012-13City University of Hong Kong

AC4331 – Topic 6

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 2/108

Topic 7

.

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 3/108

1-2

Introduction to Financial Management

Free Cash Flow

Financial Planning and Forecasting

Financial Assets and Time Value of Money

Risk and Return Bond and Stock Valuation

Cost of Capital

Cash Flow Estimation and Risk Analysis Capital Structure and Leverage Treasury and Valuation

Enterprise Risk Management Dividends and Share Repurchase

Merger and Acquisitions

Working Capital Management

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 4/108

Extra Ref: Smart,Chapter 13

Financial Management, Theory and Practice, 12e Eugene and

Brigham

Topic 7:Capital Structure and Leverage

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 5/108

Chapter 15

Business vs. Financial Risk

Optimal Capital Structure

Operating Leverage Capital Structure Theory

15-4

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 6/108

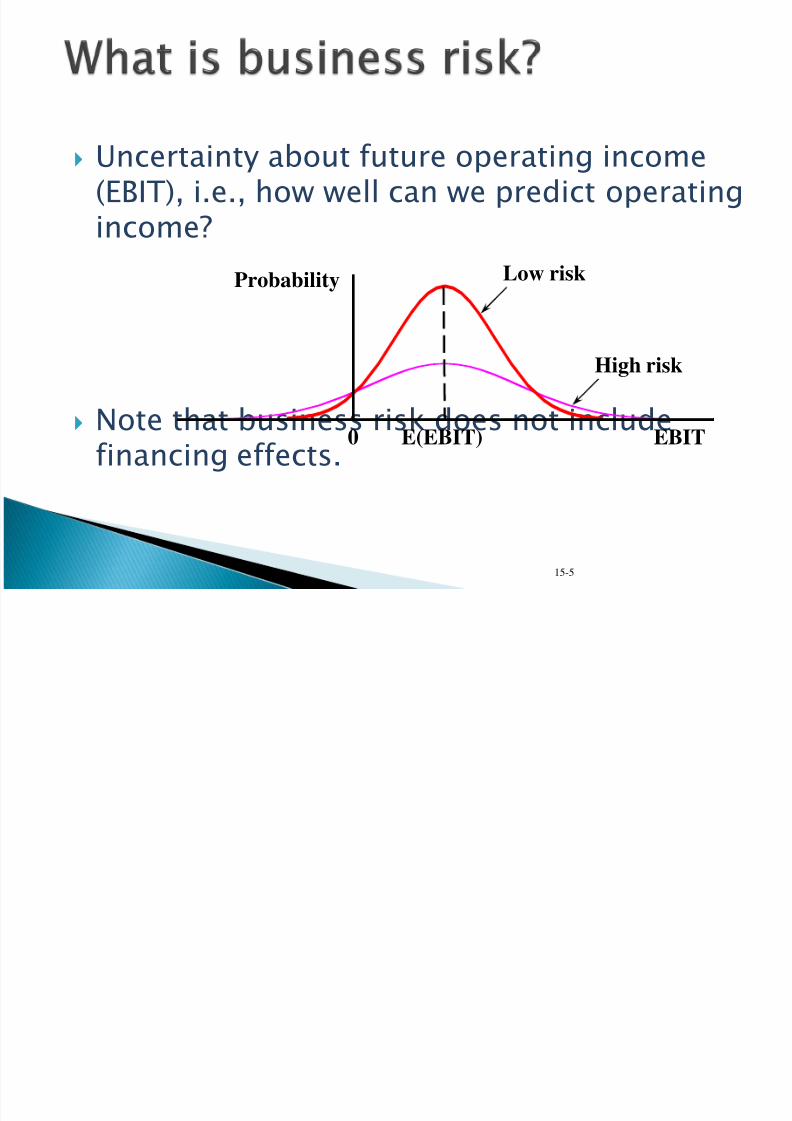

Uncertainty about future operating income(EBIT), i.e., how well can we predict operatingincome?

Note that business risk does not includefinancing effects.

Probability

EBITE(EBIT)0

Low risk

High risk

15-5

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 7/108

Uncertainty about demand (sales)

Uncertainty about output prices

Uncertainty about costs

Product, other types of liability Operating leverage

15-6

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 8/108

Operating leverage is the use of fixed costsrather than variable costs.

If most costs are fixed, hence do not decline

when demand falls, then the firm has highoperating leverage.

15-7

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 9/108

More operating leverage leads to morebusiness risk, for then a small sales declinecauses a big profit decline.

What happens if variable costs change?Sales

$ Rev.TC

FCQ BE Sales

$ Rev.

TC

FC

Q BE

} Profit

15-8

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 10/108

Typical situation: Can use operating leverageto get higher E(EBIT), but risk also increases.

Probability

EBITL

Low operating leverage

High operating leverage

EBITH

15-9

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 11/108

Financial leverage is the use of debt andpreferred stock.

Financial risk is the additional risk

concentrated on common stockholders as aresult of financial leverage.

15-10

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 12/108

Business risk depends on business factorssuch as competition, product liability, andoperating leverage.

Financial risk depends only on the types of securities issued.◦ More debt, more financial risk.

◦ Concentrates business risk on stockholders.

15-11

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 13/108

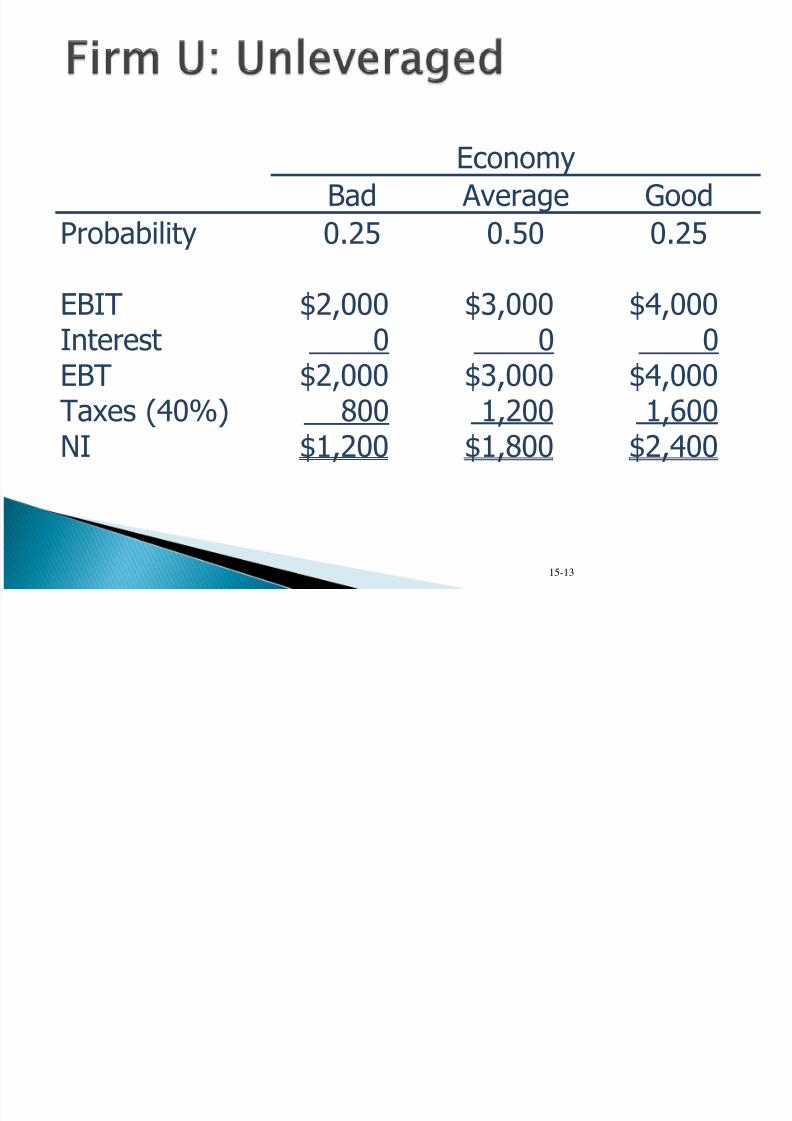

Two firms with the same operating leverage,business risk, and probability distribution of EBIT.

Only differ with respect to their use of debt(capital structure).

15-12

Firm U Firm L

No debt $10,000 of 12% debt$20,000 in assets $20,000 in assets40% tax rate 40% tax rate

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 14/108

15-13

Economy

Bad Average Good

Probability 0.25 0.50 0.25

EBIT $2,000 $3,000 $4,000Interest 0 0 0EBT $2,000 $3,000 $4,000

Taxes (40%) 800 1,200 1,600NI $1,200 $1,800 $2,400

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 15/108

15-14

Economy

Bad Average Good

Probability* 0.25 0.50 0.25

EBIT* $2,000 $3,000 $4,000Interest 1,200 1,200 1,200EBT $ 800 $1,800 $2,800

Taxes (40%) 320 720 1,120NI $ 480 $1,080 $1,680

*Same as for Firm U.

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 16/108

15-15

Firm U Bad Average Good

BEP 10.0% 15.0% 20.0%ROE 6.0 9.0 12.0

TIE

Firm L Bad Average Good

BEP 10.0% 15.0% 20.0%

ROE 4.8 10.8 16.8TIE 1.67× 2.50x 3.30x

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 17/108

15-16

Expected values:Firm U Firm L

E(BEP) 15.0% 15.0%

E(ROE) 9.0% 10.8%E(TIE) 2.5×

Risk measures:Firm U Firm L

σROE 2.12% 4.24%CVROE 0.24 0.39

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 18/108

For leverage to raise expected ROE, musthave BEP > rd.

Why? If rd > BEP, then the interest expense

will be higher than the operating incomeproduced by debt-financed assets, soleverage will depress income.

As debt increases, TIE decreases because

EBIT is unaffected by debt, but interestexpense increases (Int Exp = rdD).

15-17

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 19/108

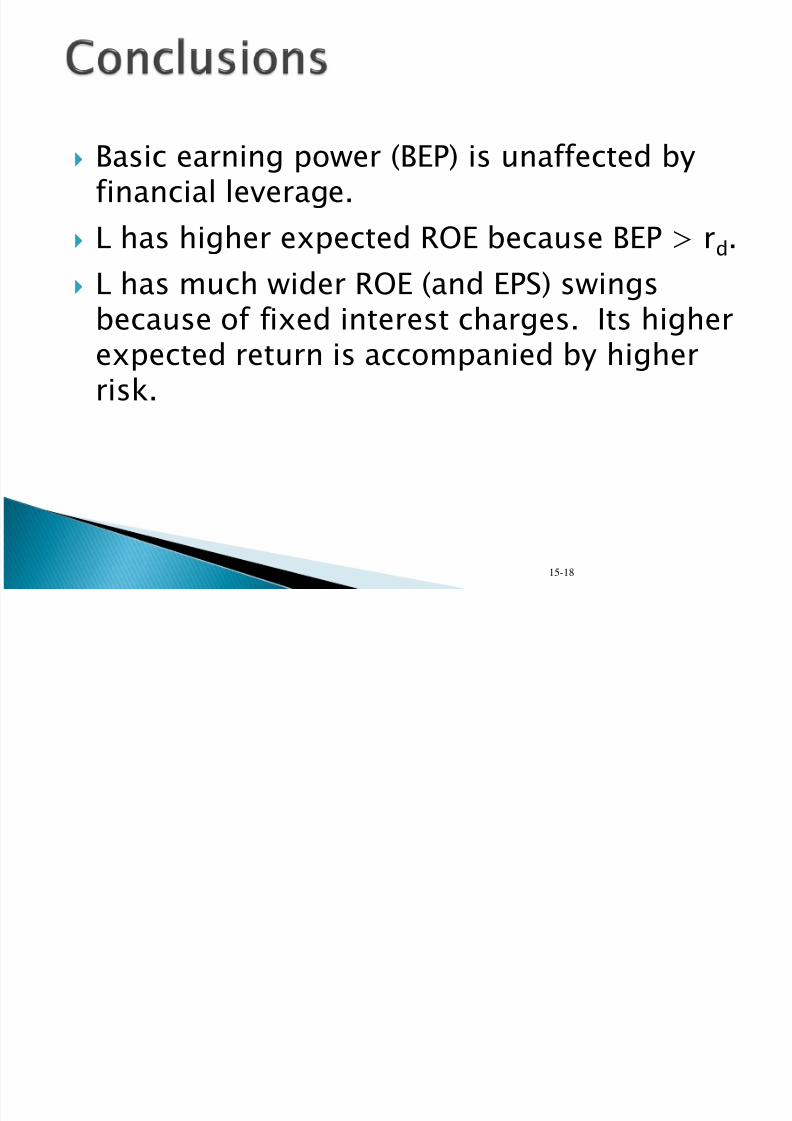

Basic earning power (BEP) is unaffected byfinancial leverage.

L has higher expected ROE because BEP > rd.

L has much wider ROE (and EPS) swingsbecause of fixed interest charges. Its higherexpected return is accompanied by higherrisk.

15-18

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 20/108

The capital structure (mix of debt, preferred,and common equity) at which P0 ismaximized.

Trades off higher E(ROE) and EPS againsthigher risk. The tax-related benefits of leverage are exactly offset by the debt’s risk-related costs.

The target capital structure is the mix of debt, preferred stock, and common equitywith which the firm intends to raise capital.

15-19

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 21/108

Firm announces the recapitalization.

New debt is issued.

Proceeds are used to repurchase stock.◦

The number of shares repurchased is equal to theamount of debt issued divided by price per share.

15-20

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 22/108

AmountBorrowed

D/A Ratio

D/ERatio

BondRating rd

$ 0 0 0 -- --

250 0.125 0.143 AA 8.0%

500 0.250 0.333 A 9.0%

750 0.375 0.600 BBB 11.5%

1,000 0.500 1.000 BB 14.0%

15-21

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 23/108

As the firm borrows more money, the firmincreases its financial risk causing the firm’sbond rating to decrease, and its cost of debtto increase.

15-22

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 24/108

$3.00

80,000

(0.6)($400,000)

goutstandinSharesT)D)(1r(EBIT EPS

$0D

d

15-23

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 25/108

20x$20,000

$400,000

ExpInt

EBIT TIE

$3.26

10,00080,000

000))(0.6)0.08($250,($400,000

goutstandinShares

T)D)(1r(EBIT EPS

10,000$25

$250,000 drepurchaseShares

d

15-24

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 26/108

8.9x$45,000

$400,000

ExpInt

EBIT TIE

$3.55

20,00080,000

000))(0.6)0.09($500,($400,000

goutstandinShares

T)D)(1r(EBIT EPS

20,000$25

$500,000 drepurchaseShares

d

15-25

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 27/108

4.6x$86,250

$400,000

ExpInt

EBIT TIE

$3.77

30,00080,000

),000))(0.60.115($750($400,000

goutstandinShares T)D)(1r(EBIT EPS

30,000$25

$750,000 drepurchaseShares

d

15-26

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 28/108

2.9x$140,000

$400,000

ExpInt

EBIT TIE

$3.90

40,00080,000

6)0,000))(0.0.14($1,00($400,000

goutstandinSharesT)D)(1r(EBIT EPS

40,000$25

$1,000,000 drepurchaseShares

d

15-27

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 29/108

sss

10

r

DPS

r

EPS

gr

D P̂

If all earnings are paid out as dividends,E(g) = 0.

EPS = DPS.

To find the expected stock price ( ),we must find the appropriate rs at each of the debt levels discussed.

15-28

Pˆ0

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 30/108

If the level of debt increases, the firm’s riskincreases.

We have already observed the increase in thecost of debt.

However, the risk of the firm’s equity alsoincreases, resulting in a higher rs.

15-29

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 31/108

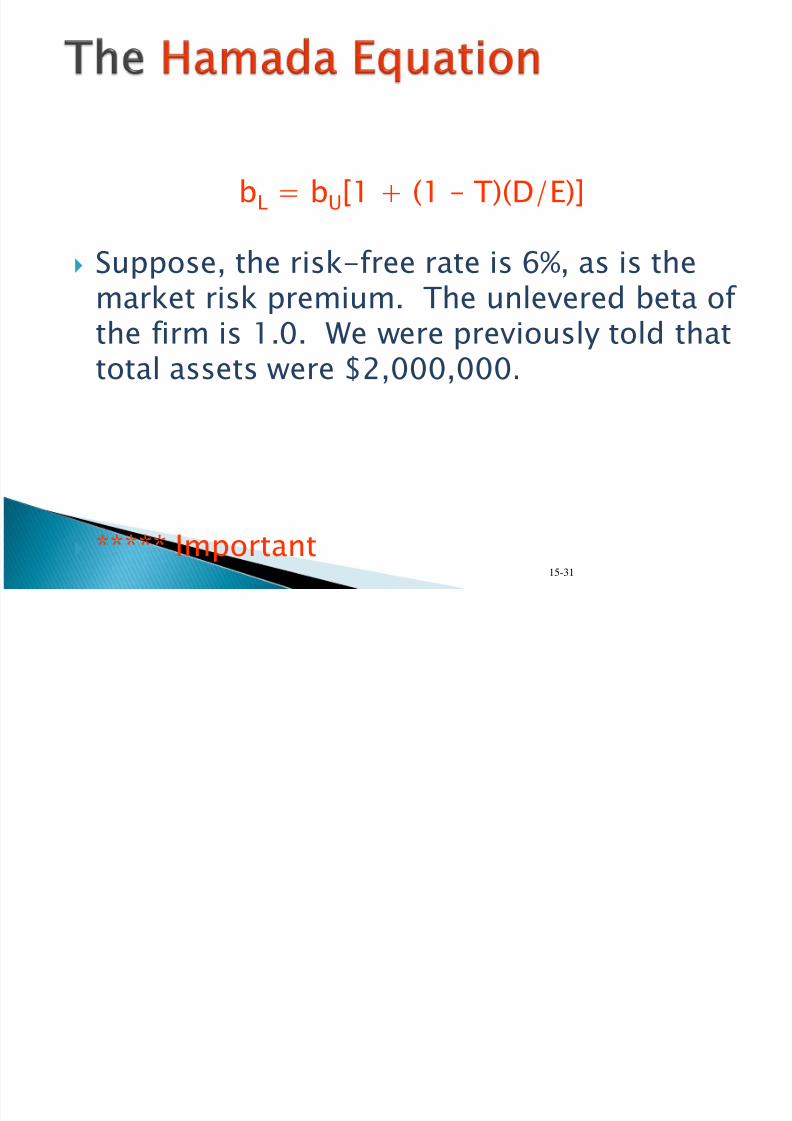

Because the increased use of debt causesboth the costs of debt and equity to increase,we need to estimate the new cost of equity.

The Hamada equation attempts to quantifythe increased cost of equity due to financialleverage.

Uses the firm’s unlevered beta, which

represents the firm’s business risk as if ithad no debt.

15-30

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 32/108

bL = bU[1 + (1 – T)(D/E)]

Suppose, the risk-free rate is 6%, as is themarket risk premium. The unlevered beta of the firm is 1.0. We were previously told thattotal assets were $2,000,000.

***** Important 15-31

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 33/108

If D = $250,

bL = 1.0[1 + (0.6)($250/$1,750)]= 1.0857

rs = rRF + (rM – rRF)bL = 6.0% + (6.0%)1.0857

= 12.51%

15-32

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 34/108

AmountBorrowed

D/A Ratio

D/ERatio

LeveredBeta rs

$ 0 0% 0% 1.00 12.00%

250 12.50 14.29 1.09 12.51

500 25.00 33.33 1.20 13.20

750 37.50 60.00 1.36 14.16

1,000 50.00 100.00 1.60 15.60

15-33

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 35/108

15-34

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 36/108

The firm’s optimal capital structure can bedetermined two ways:◦ Minimizes WACC.

◦ Maximizes stock price.

Both methods yield the same results.

15-35

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 37/108

36

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 38/108

37

Homogeneous Expectations Homogeneous Business Risk Classes

Perpetual Cash Flows

Perfect Capital Markets:◦ Perfect competition

◦ Firms and investors can borrow/lend at the samerate

◦

Equal access to all relevant information◦ No transaction costs

◦ No taxes

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 39/108

38

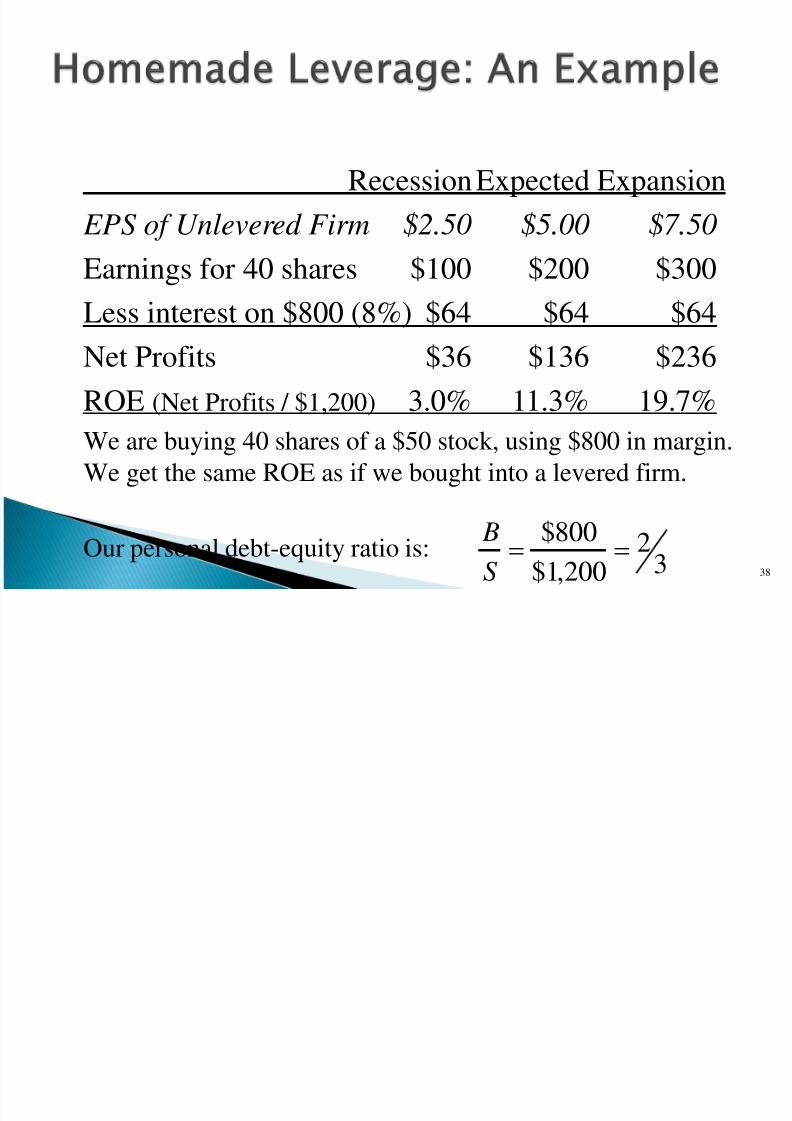

Recession Expected Expansion

EPS of Unlevered Firm $2.50 $5.00 $7.50

Earnings for 40 shares $100 $200 $300Less interest on $800 (8%) $64 $64 $64

Net Profits $36 $136 $236

ROE (Net Profits / $1,200) 3.0% 11.3% 19.7%

We are buying 40 shares of a $50 stock, using $800 in margin.

We get the same ROE as if we bought into a levered firm.

Our personal debt-equity ratio is: 32

200,1$

800$S

B

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 40/108

39

RecessionExpected ExpansionEPS of Levered Firm $1.50 $5.67 $9.83 Earnings for 24 shares$36 $136 $236

Plus interest on $800 (8%)$64 $64 $64Net Profits $100 $200 $300ROE (Net Profits / $2,000) 5% 10% 15%Buying 24 shares of an otherwise identical levered

firm along with some of the firm’s debt gets us to theROE of the unlevered firm.

This is the fundamental insight of M&M

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 41/108

40

We can create a levered or unlevered positionby adjusting the trading in our own account.

This homemade leverage suggests thatcapital structure is irrelevant in determining

the value of the firm:

V L = V U

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 42/108

41

Proposition II◦ Leverage increases the risk and return to

stockholders

R s = R 0 + (B / S ) (R 0 - R B)R B is the interest rate (cost of debt)

R S is the return on (levered) equity (cost of equity)

R 0 is the return on unlevered equity (cost of capital)

B is the value of debt

S is the value of equity

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 43/108

42

The derivation is straightforward:

S BWACC R

S B

S R

S B

B R

0setThen R RWACC

0 R RS B

S RS B

BS B

S

S B bysidesbothmultiply

0 RS

S B R

S B

S

S

S B R

S B

B

S

S B

S B

0 RS

S B R R

S

B

S B

00 R RS

B R R

S

B

S B )( 00 BS

R R

S

B R R

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 44/108

43

Debt-to-equity Ratio

C o s t o f c a p i t a l : R ( % )

R0

R B

S BWACC R

S B

S R

S B

B R

)( 00 BS R R

S

B R R

R B

S

B

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 45/108

44

Proposition I (with Corporate Taxes)◦ Firm value increases with leverage

V L = V U + t C B

Proposition II (with Corporate Taxes)◦ Some of the increase in equity risk and return is

offset by the interest tax shield

R S = R 0 + (B/S )×(1-t C )×(R 0 - R B ) R B is the interest rate (cost of debt)

R S is the return on equity (cost of equity)

R 0 is the return on unlevered equity (cost of capital)

B is the value of debt

S is the value of equity

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 46/108

45 Bt V V C U L

B Rt B R EBIT BC B

)1()(

isrsstakeholdealltoflowcashtotalThe

The present value of this stream of cash flows is V L

B Rt B R EBIT BC B

)1()(Clearly

The present value of the first term is V U

The present value of the second term is t C B

B Rt B Rt EBIT BC BC

)1()1(

B R Bt R B Rt EBIT BC B BC )1(

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 47/108

46

Start with M&M Proposition I with taxes:

)()1( 00 BC S R Rt S

B

R R

Bt V V C U L

Since BS V L

The cash flows from each side of the balance sheet must equal:

BC U BS BRt RV BRSR 0

B Rt Rt BS BRSR BC C BS

0)]1([

Divide both sides by S

BC C BS Rt

S

B Rt

S

B R

S

B R 0)]1(1[

Bt V BS C U

)1( C U

t BS V

Which quickly reduces to

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 48/108

47Debt-to-equityratio ( B / S )

Cost of capital: R (%)

R0

R B

)()1( 00 BC S R Rt

S

B R R

S C BWACC R

S B

S t RS B

B R

)1(

)( 00 BS R R

S

B R R

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 49/108

48

Recession Expected Expansion

EBIT $1,000 $2,000 $3,000

Interest 0 0 0

EBT $1,000 $2,000 $3,000

Taxes (t c = 35%) $350 $700 $1,050

Total Cash Flow to S/H $650 $1,300 $1,950

Recession Expected Expansion

EBIT $1,000 $2,000 $3,000

Interest ($800 @ 8% ) 640 640 640

EBT $360 $1,360 $2,360

Taxes (t c = 35%) $126 $476 $826

Total Cash Flow $234+640 $884+$640 $1,534+$640

(to both S/H & B/H): $874 $1,524 $2,174

EBIT(1-t c )+t C R B B $650+$224 $1,300+$224 $1,950+$224

$874 $1,524 $2,174

A

l l E q u i t y

L e v e r e d

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 50/108

49

The levered firm pays less in taxes than does the all-equity firm.

Thus, the sum of the debt plus the equity of the levered firm is

greater than the equity of the unlevered firm.

This is how cutting the pie differently can make the pie “larger.”

-the government takes a smaller slice of the pie!

S G S G

B

All-equity firm Levered firm

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 51/108

50

In a world of no taxes, the value of the firm isunaffected by capital structure.

This is M&M Proposition I:

V L = V U Proposition I holds because shareholders can

achieve any pattern of payouts they desire withhomemade leverage.

In a world of no taxes, M&M Proposition II statesthat leverage increases the risk and return tostockholders.

)( 00 BS R R

S

B R R

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 52/108

51

In a world of taxes, but no bankruptcy costs, thevalue of the firm increases with leverage.

This is M&M Proposition I:

V L = V U + t C B Proposition I holds because shareholders can

achieve any pattern of payouts they desire withhomemade leverage.

In a world of taxes, M&M Proposition II states thatleverage increases the risk and return tostockholders.

)()1( 00 BC S R Rt

S

B R R

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 53/108

Life Corporation has 7 million shares of ordinary equityoutstanding, 1 million shares of 6 percent preferred stockoutstanding and 100,000 9 percent semi-annual bondsoutstanding, par value $1,000 each. Current market value of stock is $35 per share and its beta is 1.0, the preferred stock

currently sells at $60 per share, and the bond has 15 years tomaturity and is currently selling for $890. The market riskpremium is 8%, T-bills are yielding 3 %, and the company’stax rate is 16%.

(i) Find the market value capital structure of the firm

(ii)If the firm is evaluating a project that has same risk asthe firm’s existing projects, what rate should the firm use todiscount the project’s future cash flows? If the project hashigher risk than the firm’s existing projects, what should thefirm do in order to evaluate the project?

52

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 54/108

53

T di Off D bt’ B fit d C t

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 55/108

• The optimal capital structure occurs where the marginal benefit of

additional debt is equal to the marginal cost.• How do managers trade-off the benefits and costs of debt to

establish a target capital structure that maximizes firm value?

54

Trading Off Debt’s Benefits and Costs

Figure 1 Weighing Debt’s Benefits and

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 56/108

55

Figure 1 Weighing Debt s Benefits andCosts to Find Optimal Capital Structure

A manager facing these cost and benefit

curves would choose a debt level where thetwo curves intersect.

Figure 2 Weighing Debt’s Benefits and

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 57/108

56

Figure 2 Weighing Debt s Benefits andCosts to Find Optimal Capital Structure

If a firm has no debt, its value equals Vu.

From there, if the firm adds debt to itscapital structure, its value begins to rise,

reaches a peak, and from there, adding more

debt decreases firm value.

Figure 3 Weighing Debt’s Benefits and

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 58/108

57

Figure 3 Weighing Debt s Benefits andCosts to Find Optimal Capital Structure

Managers want to find the debt ratio that

minimizes the cost of capital because itmaximizes firm value. The optimum point

in Panel C is the same optimum debt ratio as

in Panels A & B.

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 59/108

AmountBorrowed

D/A Ratio

E/A Ratio rs rd(1 – T) WACC

$ 0 0% 100% 12.00% -- 12.00%

250 12.50 87.50 12.51 4.80% 11.55

500 25.00 75.00 13.20 5.40% 11.25

750 37.50 62.50 14.16 6.90% 11.44

1,000 50.00 50.00 15.60 8.40% 12.00

15-58

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 60/108

AmountBorrowed DPS rs P0

$ 0 $3.00 12.00% $25.00

250 3.26 12.51 26.03

500 3.55 13.20 26.89

750 3.77 14.16 26.59

1,000 3.90 15.60 25.00

15-59

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 61/108

Maximum EPS = $3.90 at D = $1,000,000,and D/A = 50%. (Remember DPS = EPSbecause payout = 100%.)

Risk is too high at D/A = 50%.

15-60

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 62/108

P0 is maximized ($26.89) at D/A =$500,000/$2,000,000 = 25%, so optimalD/A = 25%.

EPS is maximized at 50%, but primaryinterest is stock price, not E(EPS).

The example shows that we can push upE(EPS) by using more debt, but the risk

resulting from increased leverage more thanoffsets the benefit of higher E(EPS).

15-61

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 63/108

15-62

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 64/108

If there were higher business risk, then theprobability of financial distress would begreater at any debt level, and the optimalcapital structure would be one that had less

debt.

However, lower business risk would lead toan optimal capital structure with more debt.

15-63

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 65/108

1.Sales stability?2.High operating leverage?

3.Increase in the corporate tax rate?

4.Increase in the personal tax rate?5.Increase in bankruptcy costs?

6.Management spending lots of money onlavish perks?

15-64

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 66/108

Value of Stock

0 D1 D2 D/A

MMresult

Actual

Noleverage

15-65

Example: PV of Tax Debt Shield

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 67/108

66

Example: PV of Tax Debt Shield

Debt Tax Shields and Firm Profitability

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 68/108

Interest deductions only lower taxes to theextent that the firm is profitable.

Using more debt financing increases the

probability that the firm will experiencelosses.

67

Debt Tax Shields and Firm Profitability

Costs of Bankruptcy and Financial

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 69/108

Bankruptcy costs are distinct from thedecline in firm value that leads to financialdistress.

Poor management, unfavorable movementsin input and output prices, and recessionscan push a firm into bankruptcy, but theyare not examples of bankruptcy costs.

Bankruptcy costs refer to direct andindirect costs of the bankruptcy process

itself.

68

p yDistress

Bankruptcy Costs

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 70/108

69

It is not the event of going bankrupt that matters; it is thecosts of going bankrupt that matter.

If ownership of the firm’s assets were transferred costlesslyto its creditors in the event of bankruptcy…

The optimal capital structure would still be 100% debt.

When the firm incurs costs in bankruptcy that it would otherwise avoid, bankruptcy costs become a deterrent to using leverage.

Bankruptcy Costs

Example

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 71/108

70

Firm 1 Firm 2

Market value of assets $100,000,000 $100,000,000

Debt $0 $50,000,000Equity $100,000,000 $50,000,000

– Assume if firm goes bankrupt, $10 million in assets

are lost in the process of transferring ownership fromstockholders to bondholders:

$30,000,000$40,000,000$0$0

$30,000,000$40,000,000

Firm 2 will calculate the tax advantage of debt and weigh that againstthe cost of bankruptcy times the probability of bankruptcy at each

debt level.

When the recession hits, Firm 1 has $40 million in assets, but Firm 2has $30 million in assets.

We are now looking not at bankruptcy costs per se, but at expected

bankruptcy costs.

Example

Bankruptcy Costs

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 72/108

71

Direct Costs Costs of bankruptcy-related litigation (e.g.legal, auditing, and administrative costs)

Indirect

Costs

Cost of management time diverted tobankruptcy process

Loss of customers who don’t want to deal witha distressed firm

Loss of employees who switch to healthier firms

Strained relationships with suppliers

Lost investment opportunities

Bankruptcy Costs

Bankruptcy Costs

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 73/108

72

Indirect costs are likely to be much larger, and are likely tovary a great deal depending on the type of firm in distress.

Indirect costs may be high:

When the firm’s product requires that the firm stay inbusiness (e.g., when warranties or service are important)

When the firm must make additional investments in productquality to maintain customers

For example, think of customers worrying that a bankruptairline might try to save $ by cutting spending on safety.

Bankruptcy Costs

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 74/108

73

V L = V U + PV(Tax shields) – PV(Bankruptcy costs)

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 75/108

Producers of complex products or servicestend to use less debt than do firmsproducing nondurable goods or basicservices.

Companies whose assets are mostlytangible and have well-establishedsecondary markets should be less fearful of financial distress than companies whose

assets are mostly intangible.

74

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 76/108

75

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 77/108

Jensen and Meckling (1976): agency costtheory of financial structure

Agency costs of outside equity◦ Managers who own less than 100% of the firm

have an incentive to expropriate wealth from the

firm’s investors. Excessive perquisite consumption

Less effort devoted to increasing firm’s value

76

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 78/108

77

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 79/108

Using debt means a firm can sell lessexternal equity and still finance itsoperations.

Using debt reduces managerial perquisiteconsumption.

External debt serves as a bonding mechanism .

Debt subjects managers to directmonitoring by public capital markets.

78

Agency Costs of Outside Debt

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 80/108

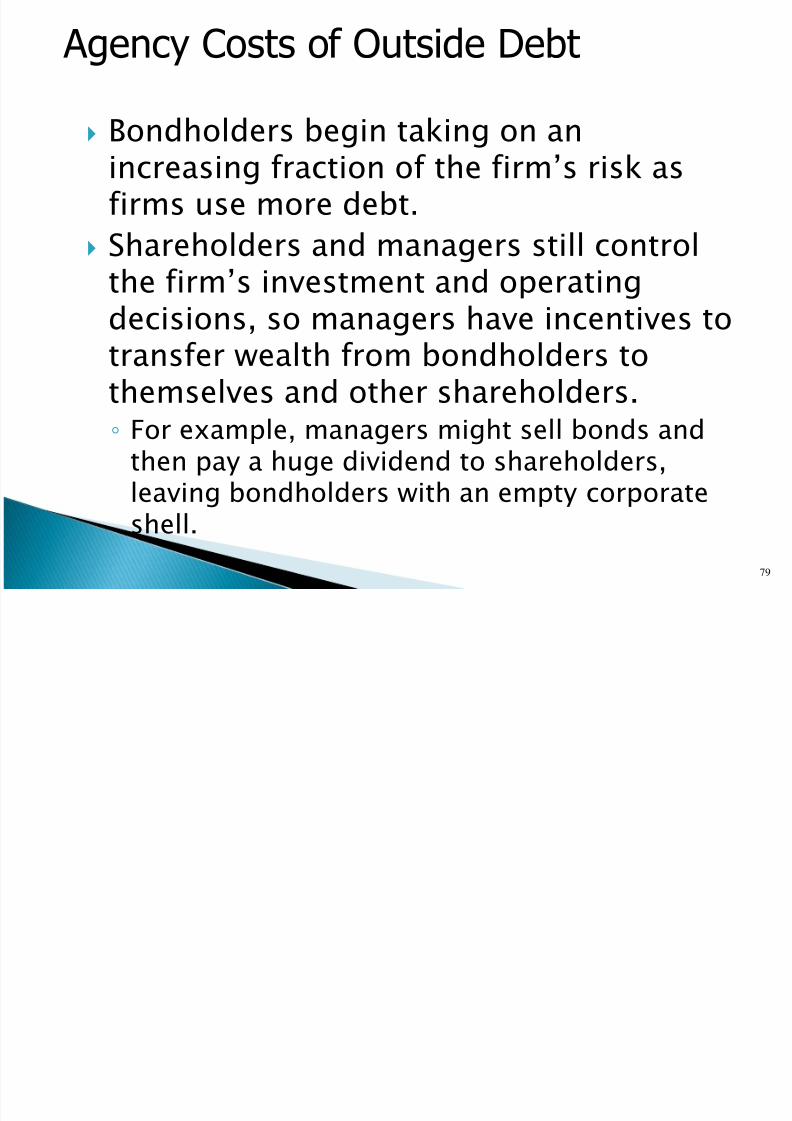

Bondholders begin taking on anincreasing fraction of the firm’s risk asfirms use more debt.

Shareholders and managers still control

the firm’s investment and operatingdecisions, so managers have incentives totransfer wealth from bondholders tothemselves and other shareholders.◦ For example, managers might sell bonds and

then pay a huge dividend to shareholders,leaving bondholders with an empty corporateshell.

79

Agency Costs of Outside Debt

Agency Costs of Outside Debt

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 81/108

80

g y o o Ou d b

Problems withoutside debt

Asset substitution (bait and switch)

Underinvestment

Bondholders protect themselves with positive and negativecovenants in lending contracts.

Agency costs of debt are burdensome, but so are solutions.

Agency Costs of Outside Debt

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 82/108

Asset substitution is the promise to invest ina safe asset to obtain an interest ratereflecting low risk, and then substituting ariskier asset promising a higher expected

return. Underinvestment occurs when a firm’s

shareholders refuse to invest in a positive-NPV project because most of the benefits

would be realized by bondholders.

81

g y

Smart Figure 13.5The Trade off Model Revisited

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 83/108

82

The Trade-off Model Revisited

V L = V U + PV(Tax shields) – PV(Bankruptcy costs) – PV(Agency costs)

Implications of the Trade-off Model

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 84/108

Profitable firms should borrow more thanunprofitable firms because they are morelikely to benefit from interest tax shields.

Firms that own tangible, marketable

assets should borrow more than firmswhose assets are intangible or highlyspecialized.

Safer firms should borrow more than

riskier firms. Companies should have a target debt

ratio.

83

Implications of the Trade off Model

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 85/108

Some studies find that the mostprofitable firms in an industry have thelowest debt ratios.

Leverage-increasing events, such as

stock repurchases and debt-for-equityexchange offers, almost always increasestock prices, while leverage-decreasingevents reduce stock prices.

Firms issue debt securities frequently, butseasoned equity issues (equity issuesfrom firms that already have stock) arerare.

84

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 86/108

85

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 87/108

The graph shows MM’s tax benefit vs.bankruptcy cost theory.

Logical, but doesn’t tell whole capitalstructure story. Main problem--assumes

investors have same information asmanagers.

15-86

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 88/108

Signaling theory suggests firms should useless debt than MM suggest.

This unused debt capacity helps avoid stocksales, which depress stock price because of

signaling effects.

15-87

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 89/108

Assumptions:◦ Managers have better information about a firm’s

long-run value than outside investors.

◦ Managers act in the best interests of current

stockholders. What can managers be expected to do?

◦ Issue stock if they think stock is overvalued.

◦ Issue debt if they think stock is undervalued.

◦ As a result, investors view a stock offeringnegatively ─ managers think stock is overvalued.

15-88

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 90/108

Issue stock if they think stock is overvalued. Issue debt if they think stock is undervalued. As a result, investors view a common stock

offering as a negative signal ─ managers think

stock is overvalued.

15-89

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 91/108

Intuitively appealing model, but relativelylittle empirical support

Leverage ratios are, if anything, negatively related to profitability in almost every

industry.◦ Signaling models predict a positive relationship!!!

Asset-rich companies use far more debtthan do growth companies with intangibleassets.◦ Information asymmetry is more severe for growth

companies, which thus should have a greaterneed to signal.

90

Smart Figure 13.5The Trade-off Model Revisited

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 92/108

91

The Trade off Model Revisited

V L = V U + PV(Tax shields) – PV(Bankruptcy costs) – PV(Agency costs)

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 93/108

92

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 94/108

• Dividend policy is “sticky .”

• Firms prefer internal financing (retainedearnings and depreciation) to externalfinancing of any sort, debt or equity.

• If a firm must obtain external financing, it willissue the safest security first.

• As a firm requires more external financing, itwill work down the “pecking order” of securities:1. Safe debt2. Risky debt3. Convertible securities4. Preferred stock5. Common stock (as a last resort)

93

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 95/108

94

Assumptions

Manager acts in best interests of

existing shareholders.

Information asymmetry between managersand investors.

Two key predictions about managerial behavior

Firms hold financial slack so they don’t have toissue securities.

Firms follow pecking order when issuingsecurities: sell low-risk debt first, equity only as

last resort.

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 96/108

It implies that firms have no target capitalstructure and that the debt ratios observedin the real world ought to fluctuaterandomly.

95

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 97/108

96

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 98/108

•

Taxes – Since interest is tax deductible, highly profitable firmsshould use more debt (i.e., greater tax benefit).

• Types of Assets – The costs of financial distress depend on the types of

assets the firm has.

• Uncertainty of Operating Income – Even without debt, firms with uncertain operating

income have a high probability of experiencingfinancial distress.

• Pecking Order and Financial Slack – Theory stating that firms prefer to issue debt rather

than equity if internal financing is insufficient.

15-97

Trading Off Debt’s Benefits and Costs

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 99/108

• The optimal capital structure occurs where the marginal benefit of additional debt is equal to the marginal cost.

• How do managers trade-off the benefits and costs of debt toestablish a target capital structure that maximizes firm value?

98

Smart Figure 13.5The Trade-off Model Revisited

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 100/108

99

The Trade off Model Revisited

V L = V U + PV(Tax shields) – PV(Bankruptcy costs) – PV(Agency costs)

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 101/108

• Most corporations have low Debt-Asset ratios.

• Changes in financial leverage affect firm value. – Stock price increases with increases in leverage and vice-

versa; this is consistent with M&M with taxes.

– Another interpretation is that firms signal good news when

they lever up.• There are differences in capital structure across

industries.

• There is evidence that firms behave as if they had atarget Debt-Equity ratio. As more debt is added andthe probability of losses increases, the marginal

benefit of debt curve slopes downward.

38

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 102/108

10

1

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 103/108

102

What Companies Do GloballySmart Figure 13.6 Target Capital Structure

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 104/108

103

Smart Figure 13.6 Target Capital Structure

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 105/108

10

4

Smart Figure 13.5The Trade-off Model Revisited

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 106/108

10

5

V L = V U + PV(Tax shields) – PV(Bankruptcy costs) – PV(Agency costs)

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 107/108

Need to make calculations as we did, butshould also recognize inputs are“guesstimates.”

As a result of imprecise numbers, capital

structure decisions have a large judgmentalcontent.

We end up with capital structures varyingwidely among firms, even similar ones in

same industry.

15-106

7/29/2019 Topic 7 (2012-13A)MP

http://slidepdf.com/reader/full/topic-7-2012-13amp 108/108

Eugene Chapter 15 Self-test Questions and Problems, ST-1,2,3

Questions: 15-3, 15-6, 15-7, 15-11

Problems: 15-1,15-2,15-3, 15-6,15-8, 15-

10,15-11 Comprehensive Question: 15-14

Related Documents