Three-way choice Option Price Option Value Real Options Calls & Puts Endogenous/Exogenous

Three-way choice Option Price Option Value Real Options Calls & Puts Endogenous/Exogenous Option Price Option Value Real Options Calls & Puts Endogenous/Exogenous.

Dec 18, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Three-way choice

Option PriceOption ValueReal OptionsCalls & PutsEndogenous/Exogenous

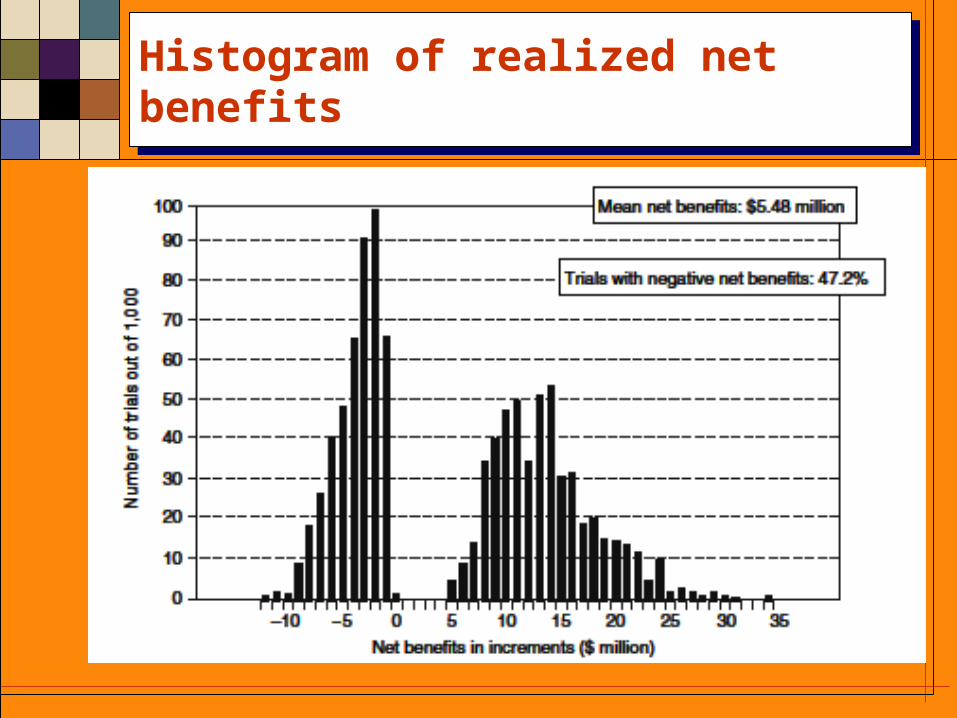

Histogram of realized net benefitsHistogram of realized net benefits

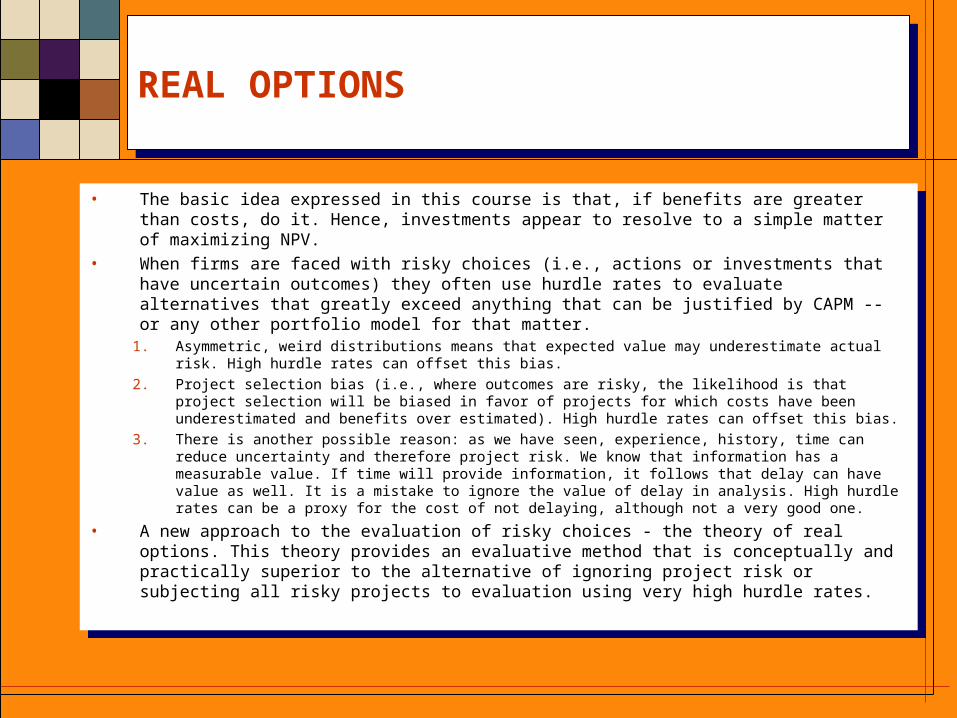

REAL OPTIONSREAL OPTIONS

• The basic idea expressed in this course is that, if benefits are greater than costs, do it. Hence, investments appear to resolve to a simple matter of maximizing NPV.

• When firms are faced with risky choices (i.e., actions or investments that have uncertain outcomes) they often use hurdle rates to evaluate alternatives that greatly exceed anything that can be justified by CAPM -- or any other portfolio model for that matter. 1. Asymmetric, weird distributions means that expected value may underestimate actual

risk. High hurdle rates can offset this bias.

2. Project selection bias (i.e., where outcomes are risky, the likelihood is that project selection will be biased in favor of projects for which costs have been underestimated and benefits over estimated). High hurdle rates can offset this bias.

3. There is another possible reason: as we have seen, experience, history, time can reduce uncertainty and therefore project risk. We know that information has a measurable value. If time will provide information, it follows that delay can have value as well. It is a mistake to ignore the value of delay in analysis. High hurdle rates can be a proxy for the cost of not delaying, although not a very good one.

• A new approach to the evaluation of risky choices - the theory of real options. This theory provides an evaluative method that is conceptually and practically superior to the alternative of ignoring project risk or subjecting all risky projects to evaluation using very high hurdle rates.

• The basic idea expressed in this course is that, if benefits are greater than costs, do it. Hence, investments appear to resolve to a simple matter of maximizing NPV.

• When firms are faced with risky choices (i.e., actions or investments that have uncertain outcomes) they often use hurdle rates to evaluate alternatives that greatly exceed anything that can be justified by CAPM -- or any other portfolio model for that matter. 1. Asymmetric, weird distributions means that expected value may underestimate actual

risk. High hurdle rates can offset this bias.

2. Project selection bias (i.e., where outcomes are risky, the likelihood is that project selection will be biased in favor of projects for which costs have been underestimated and benefits over estimated). High hurdle rates can offset this bias.

3. There is another possible reason: as we have seen, experience, history, time can reduce uncertainty and therefore project risk. We know that information has a measurable value. If time will provide information, it follows that delay can have value as well. It is a mistake to ignore the value of delay in analysis. High hurdle rates can be a proxy for the cost of not delaying, although not a very good one.

• A new approach to the evaluation of risky choices - the theory of real options. This theory provides an evaluative method that is conceptually and practically superior to the alternative of ignoring project risk or subjecting all risky projects to evaluation using very high hurdle rates.

Option PriceOption Price

• Maximum an individual would pay for an option (right to participate in a lottery) prior to the event (drawing), given the ex ante probabilities of each of the SONs that might occur.

• Option Price is the certainty equivalent of the lottery (price you pay is certain, payoff uncertain)

• Where the option reduces risk, this is a premium; where it increases risk, a discount.

• The following diagrams reflect both cases using the examples of a dam and a bridge

• Maximum an individual would pay for an option (right to participate in a lottery) prior to the event (drawing), given the ex ante probabilities of each of the SONs that might occur.

• Option Price is the certainty equivalent of the lottery (price you pay is certain, payoff uncertain)

• Where the option reduces risk, this is a premium; where it increases risk, a discount.

• The following diagrams reflect both cases using the examples of a dam and a bridge

A Risk Reducing ProjectA Risk Reducing Project

Contingency No Da m Da m Probability Dry 50 1 0 0 .5 W et 1 0 0 1 1 0 .5

Ex pe cte d Va lu e ( ) 75 1 0 5

Va rian c e ( 2 ) 6 2 5 25

Payoff and option value of risk reducing investmentPayoff and option value of risk reducing investment

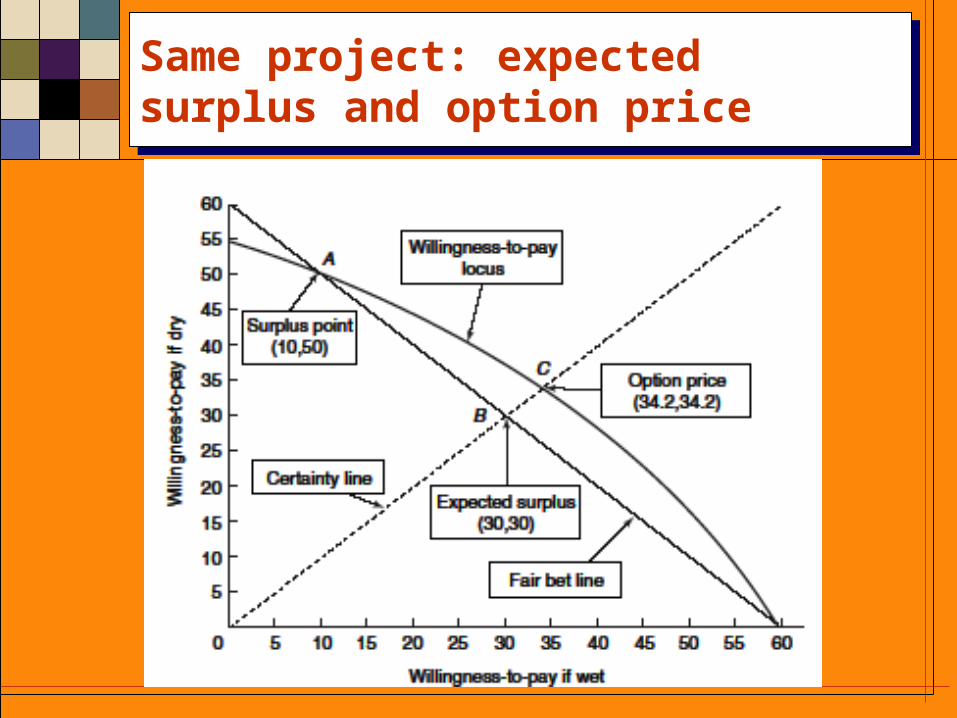

Same project: expected surplus and option priceSame project: expected surplus and option price

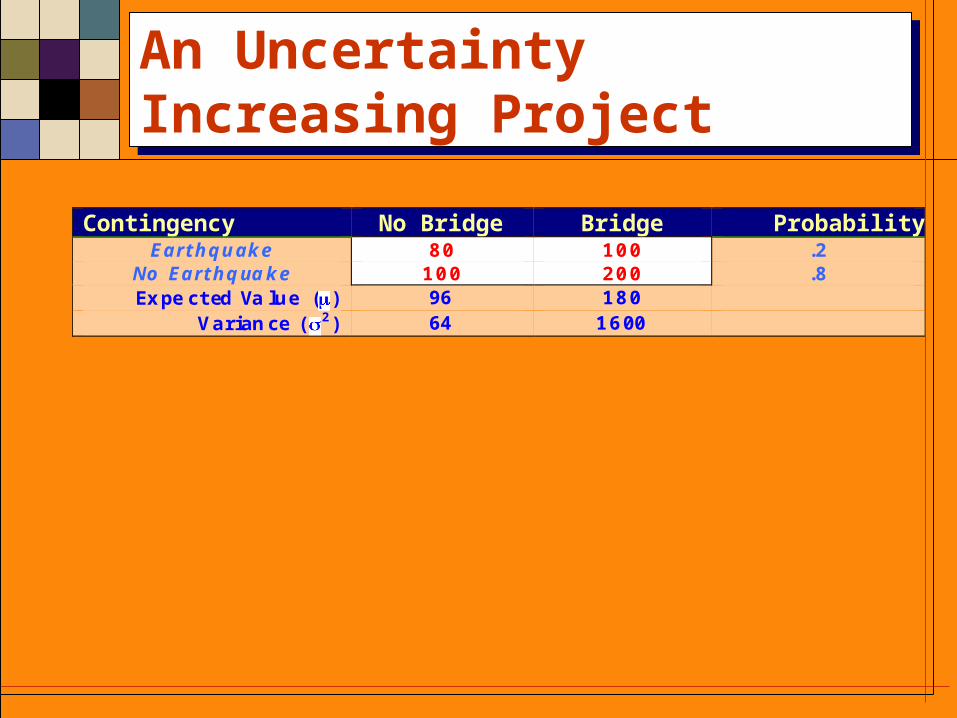

An Uncertainty Increasing ProjectAn Uncertainty Increasing Project

Contingency No Bridge Bridge Probability Ea rt h q u a k e 8 0 1 0 0 .2

No Ea rt h q ua k e 1 0 0 2 0 0 .8 Ex pe cte d Va lu e ( ) 96 1 8 0

Va rian c e ( 2 ) 64 1 6 00

Risk increasing project: expected surplus and option priceRisk increasing project: expected surplus and option price

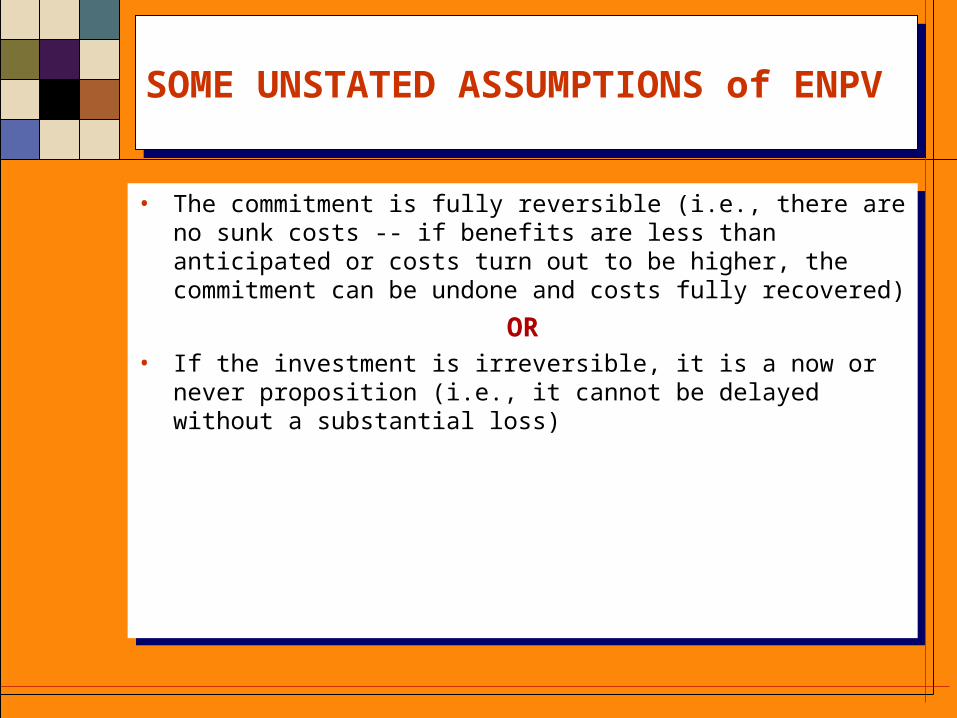

SOME UNSTATED ASSUMPTIONS of ENPVSOME UNSTATED ASSUMPTIONS of ENPV

• The commitment is fully reversible (i.e., there are no sunk costs -- if benefits are less than anticipated or costs turn out to be higher, the commitment can be undone and costs fully recovered)

OR• If the investment is irreversible, it is a now or

never proposition (i.e., it cannot be delayed without a substantial loss)

• The commitment is fully reversible (i.e., there are no sunk costs -- if benefits are less than anticipated or costs turn out to be higher, the commitment can be undone and costs fully recovered)

OR• If the investment is irreversible, it is a now or

never proposition (i.e., it cannot be delayed without a substantial loss)

THE ABILITY TO DELAY AN IRREVERSIBLE INVESTMENT UNDERMINES THE SIMPLE NPV RULE

THE ABILITY TO DELAY AN IRREVERSIBLE INVESTMENT UNDERMINES THE SIMPLE NPV RULE

WHY? • Holding an investment opportunity that can be

postponed is analogous to holding a call option; it gives you the right but not the obligation to exercise it at a future time.

• When an entity makes an irreversible investment, it "kills" its option to invest. That means that it sacrifices the possibility that waiting would provide information that would affect the desirability or timing of the investment.

• This "opportunity cost" (lost option value) should be included as part of the cost of the investment.

WHY? • Holding an investment opportunity that can be

postponed is analogous to holding a call option; it gives you the right but not the obligation to exercise it at a future time.

• When an entity makes an irreversible investment, it "kills" its option to invest. That means that it sacrifices the possibility that waiting would provide information that would affect the desirability or timing of the investment.

• This "opportunity cost" (lost option value) should be included as part of the cost of the investment.

The right decision ruleThe right decision rule

Where commitments are both irreversible and postponable, the NPV rule should be amended to read:

PROJECT BENEFITS MUST EXCEED COSTS BY AN AMOUNT EQUAL TO THE BENEFIT OF

KEEPING THE INVESTMENT OPTION ALIVE OR YOU SHOULDN’T DO IT

Where commitments are both irreversible and postponable, the NPV rule should be amended to read:

PROJECT BENEFITS MUST EXCEED COSTS BY AN AMOUNT EQUAL TO THE BENEFIT OF

KEEPING THE INVESTMENT OPTION ALIVE OR YOU SHOULDN’T DO IT

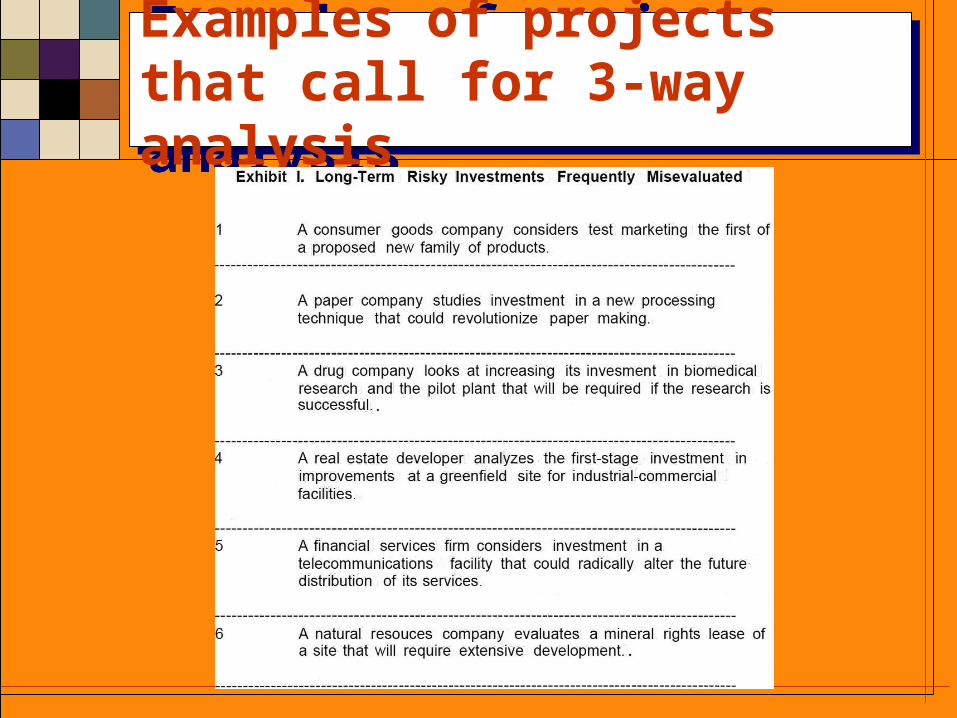

Examples of projects that call for 3-way analysisExamples of projects that call for 3-way analysis

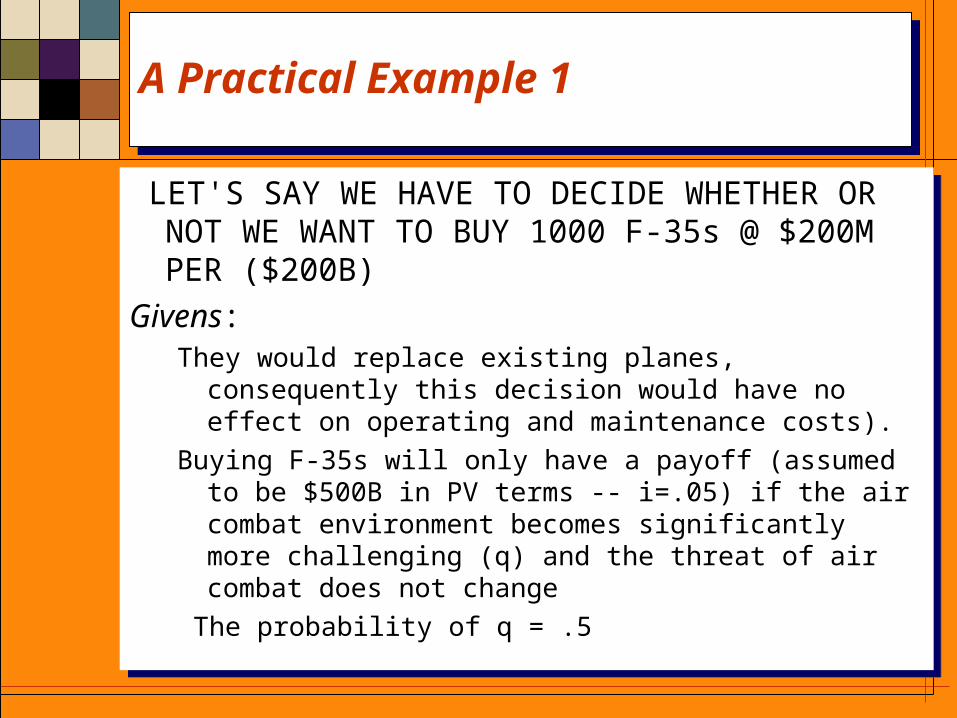

A Practical Example 1A Practical Example 1

LET'S SAY WE HAVE TO DECIDE WHETHER OR NOT WE WANT TO BUY 1000 F-35s @ $200M PER ($200B)

Givens:They would replace existing planes, consequently this decision would have no effect on operating and maintenance costs).

Buying F-35s will only have a payoff (assumed to be $500B in PV terms -- i=.05) if the air combat environment becomes significantly more challenging (q) and the threat of air combat does not change

The probability of q = .5

LET'S SAY WE HAVE TO DECIDE WHETHER OR NOT WE WANT TO BUY 1000 F-35s @ $200M PER ($200B)

Givens:They would replace existing planes, consequently this decision would have no effect on operating and maintenance costs).

Buying F-35s will only have a payoff (assumed to be $500B in PV terms -- i=.05) if the air combat environment becomes significantly more challenging (q) and the threat of air combat does not change

The probability of q = .5

A Practical Example 2A Practical Example 2

If we buy now we get an NPV of $50 BIf we buy now we get an NPV of $50 B

A Practical Example 3A Practical Example 3

If we delay for ten years it would cost $400B in current dollars to buy the equivalent of 200 F-35s (@ $200 M/PER), hence the PV cost = $246 M

However, in ten years we would buy the F-35 only if the more dangerous SON eventuates. Hence,

EV = .5 (0) + .5 (500 -246) = $127 B

The value of the option to wait is, in this case, = $127B - $50B = $77 B.

If we delay for ten years it would cost $400B in current dollars to buy the equivalent of 200 F-35s (@ $200 M/PER), hence the PV cost = $246 M

However, in ten years we would buy the F-35 only if the more dangerous SON eventuates. Hence,

EV = .5 (0) + .5 (500 -246) = $127 B

The value of the option to wait is, in this case, = $127B - $50B = $77 B.

Exogenous learningExogenous learning

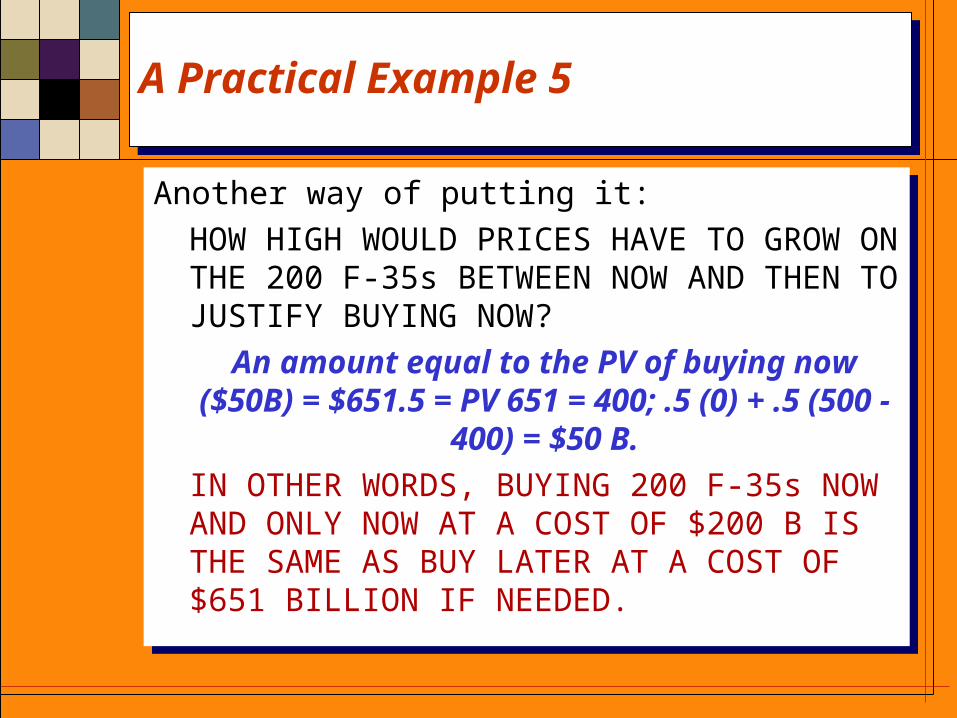

A Practical Example 5A Practical Example 5

Another way of putting it: HOW HIGH WOULD PRICES HAVE TO GROW ON THE 200 F-35s BETWEEN NOW AND THEN TO JUSTIFY BUYING NOW? An amount equal to the PV of buying

now ($50B) = $651.5 = PV 651 = 400; .5 (0) + .5 (500 - 400) = $50 B.IN OTHER WORDS, BUYING 200 F-35s NOW AND ONLY NOW AT A COST OF $200 B IS THE SAME AS BUY LATER AT A COST OF $651 BILLION IF NEEDED.

Another way of putting it: HOW HIGH WOULD PRICES HAVE TO GROW ON THE 200 F-35s BETWEEN NOW AND THEN TO JUSTIFY BUYING NOW? An amount equal to the PV of buying

now ($50B) = $651.5 = PV 651 = 400; .5 (0) + .5 (500 - 400) = $50 B.IN OTHER WORDS, BUYING 200 F-35s NOW AND ONLY NOW AT A COST OF $200 B IS THE SAME AS BUY LATER AT A COST OF $651 BILLION IF NEEDED.

A practical example: endogenous learningA practical example: endogenous learning

Results of project learningResults of project learning

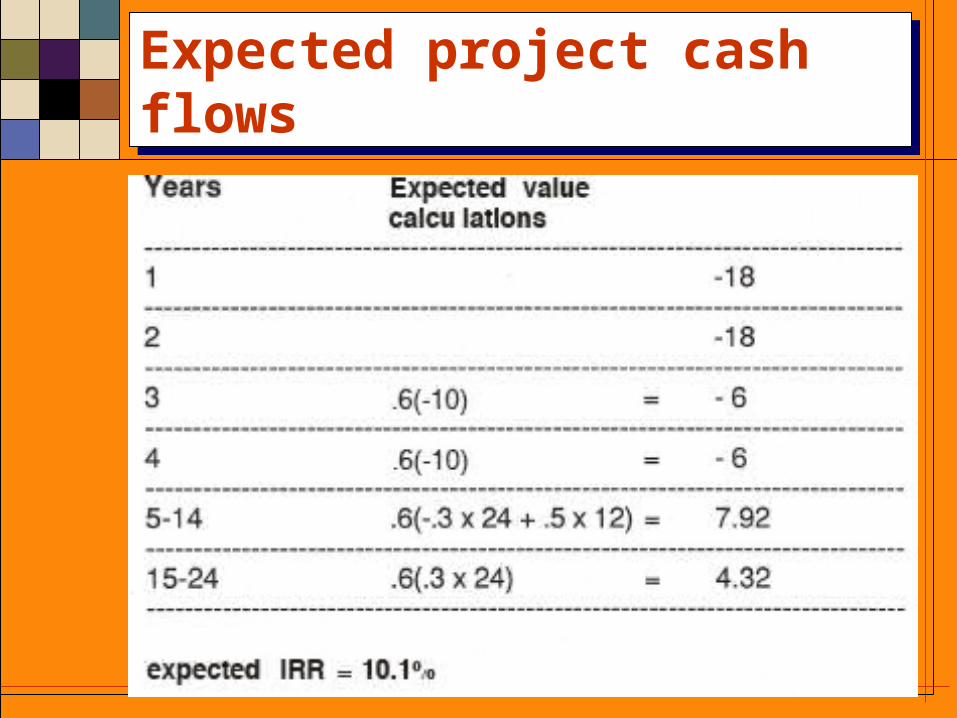

Expected project cash flowsExpected project cash flows

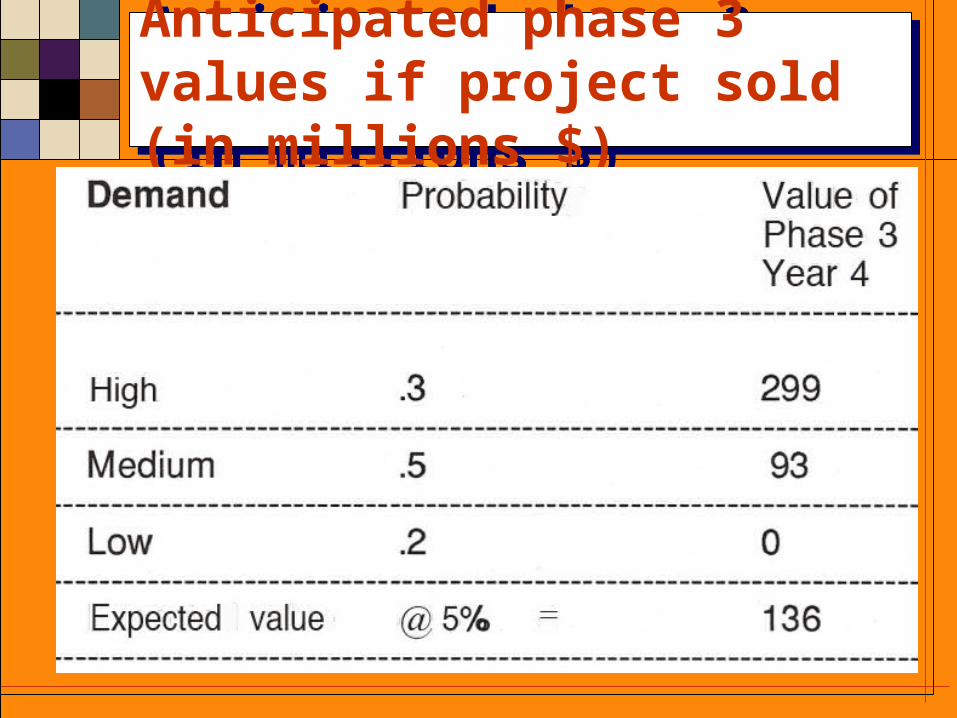

Anticipated phase 3 values if project sold (in millions $)Anticipated phase 3 values if project sold (in millions $)

Expected cash flow with phase three sale (in millions $)Expected cash flow with phase three sale (in millions $)

Related Documents