<Presenter’s name> <date> There’s never been a better time to realise the true potential of your superannuation Your logo here

There’s never been a better time to realise the true potential of your superannuation Your logo here.

Dec 20, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

<Presenter’s name><date>

There’s never been a better time to realise the true potential of

your superannuation

Your logo here

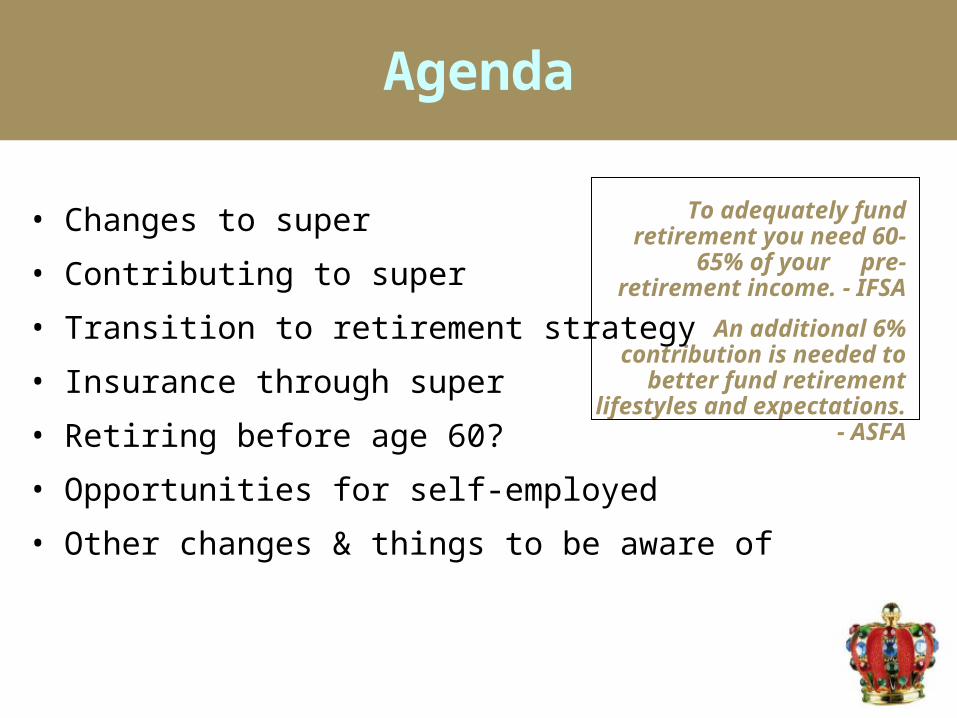

Agenda

To adequately fund retirement you need 60-65% of your

pre-retirement income. - IFSA

An additional 6% contribution is needed to better fund

retirement lifestyles and expectations. - ASFA

• Changes to super

• Contributing to super

• Transition to retirement strategy

• Insurance through super

• Retiring before age 60?

• Opportunities for self-employed

• Other changes & things to be aware of

Hasn’t Super always been a good investment?

Super already has characteristics that make it a tax effective investment:

• Compared to paying marginal tax rates on investments outside of super…

– In super – maximum tax on earnings is 15% – In pensions – zero tax on earnings

So, why is Super changing?

• Federal Budget 2006

• Aim is to simplify super

• Encourages people to save for retirement throughout working life

• Old complex system

• Australians typically only thought of super towards retirement, and even then, found it confusing

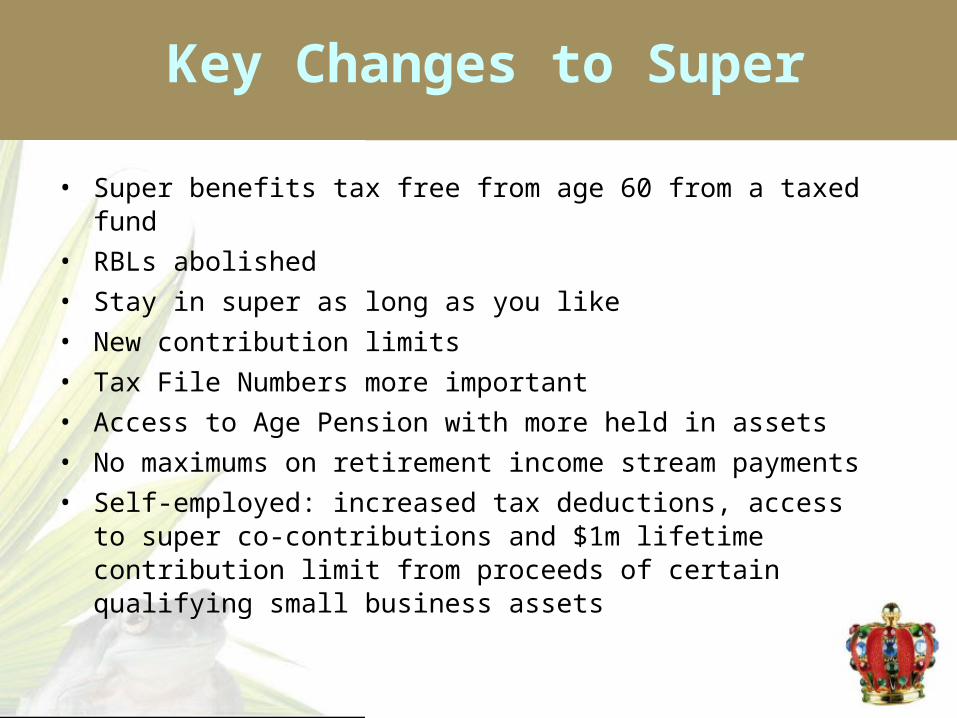

Key Changes to Super

• Super benefits tax free from age 60 from a taxed fund

• RBLs abolished

• Stay in super as long as you like

• New contribution limits

• Tax File Numbers more important

• Access to Age Pension with more held in assets

• No maximums on retirement income stream payments

• Self-employed: increased tax deductions, access to super co-contributions and $1m lifetime contribution limit from proceeds of certain qualifying small business assets

New Lower Contribution Limits

Your contributions to super

After-tax contribution Pre-tax contribution

New rules from 1 July

Limits on how much you can contribute per annum before

penalty tax is payable

Limits on how much of the contribution will be eligible for the 15% contributions tax rate

After-tax Contributions

10 May 2006 30 June 2007

Contribute up to $1 million

After-tax contributions capped at $150,000 pa* before penalty tax applies

You are here!

• or $450,000 brought forward over 3 years if you’re under age 65

Opportunity alert!Use it or lose it!

After-tax Contributions before 30 June 2007

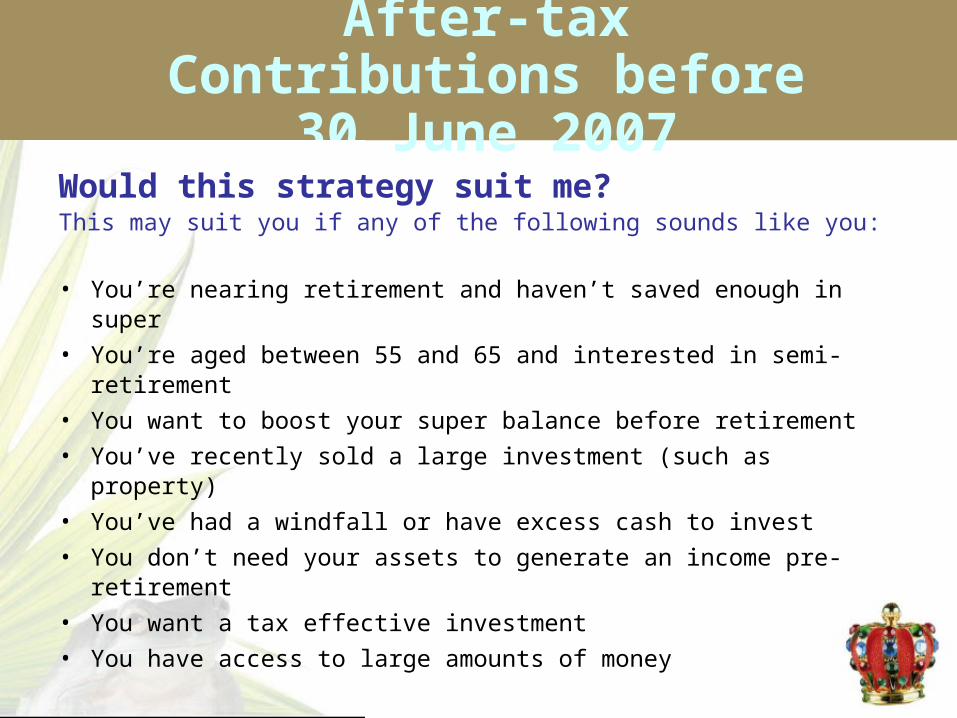

Would this strategy suit me? This may suit you if any of the following sounds like you:

• You’re nearing retirement and haven’t saved enough in super

• You’re aged between 55 and 65 and interested in semi-retirement

• You want to boost your super balance before retirement

• You’ve recently sold a large investment (such as property)

• You’ve had a windfall or have excess cash to invest

• You don’t need your assets to generate an income pre-retirement

• You want a tax effective investment

• You have access to large amounts of money

Case Study 1:

John is 63 and plans to retire at age 65. He has $500,000 to invest and is considering investing in super before 1 July 2007. John would like to know how investing in super compares with investing the $500,000 outside of super.

Before retirementIf John had invested outside of super and re-invested the earnings, he would end up with an after tax income that is $9,338 less than if he’d invested within super.

John’s retirement incomeIn his first year of retirement, John’s net income is $56,587. If he had invested outside of super and drawn the same gross income, he would have ended up with net income of $48,534. The pension strategy delivers $8,053 more to John in his first year of retirement due to the tax advantages of being in a pension.

For the first ten years of his retirement, John will receive $86,597 more in after tax income from the pension option, compared with drawing the same gross income from the non super strategy.

After-tax Contributions before 30 June 2007

Case Study 2:

• Graeme & Carol are both aged 64 and started an allocated pension a few years ago when Graeme retired. They decide they no longer want the hassle of looking after their investment property and have their pension as income anyway. They sell and invest the proceeds into super.

• The capital grows in a concessional environmentand Graeme and Carol do not have to draw on themoney even after age 65 (but they can of course dip into it as they wish after age 65 –it is a more liquid investment and easier to look after than aproperty).

After-tax Contributions before 30 June 2007

It is especially important to seek advice on strategies involving sale of assets so CGT and other costs can be factored in. Ensure you meet the work test from age 65 years to contribute to super.

After-tax Contributions before 30 June 2007

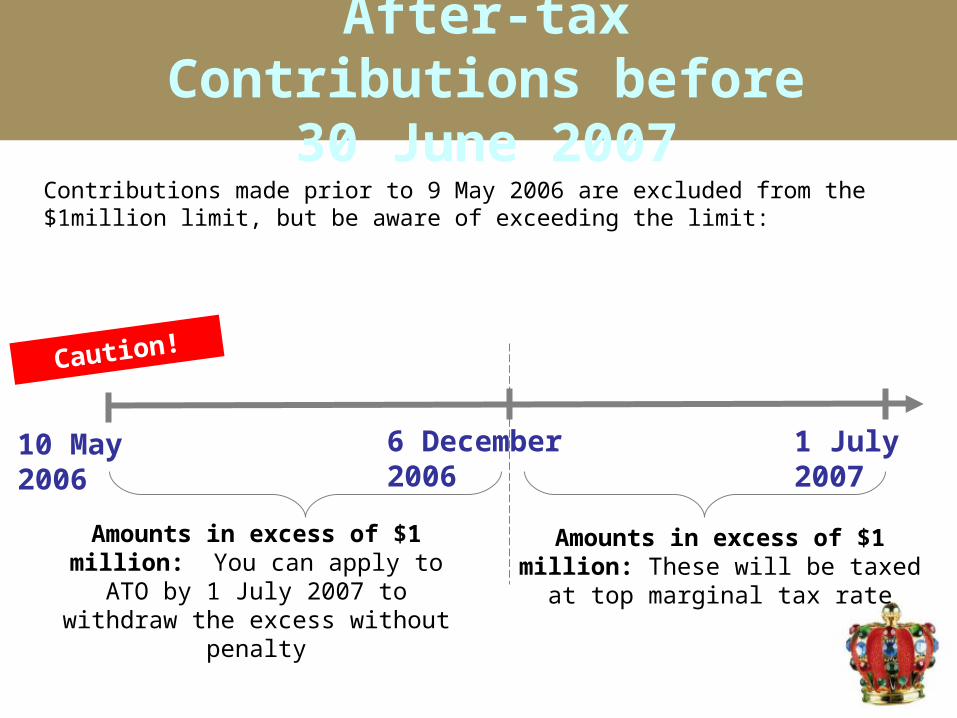

Contributions made prior to 9 May 2006 are excluded from the $1million limit, but be aware of exceeding the limit:

Amounts in excess of $1 million: You can apply to ATO by 1 July 2007

to withdraw the excess without penalty

Amounts in excess of $1 million: These will be taxed at top marginal

tax rate

1 July 2007

Caution!

10 May 2006 6 December 2006

After-tax Contributions after 30 June 2007

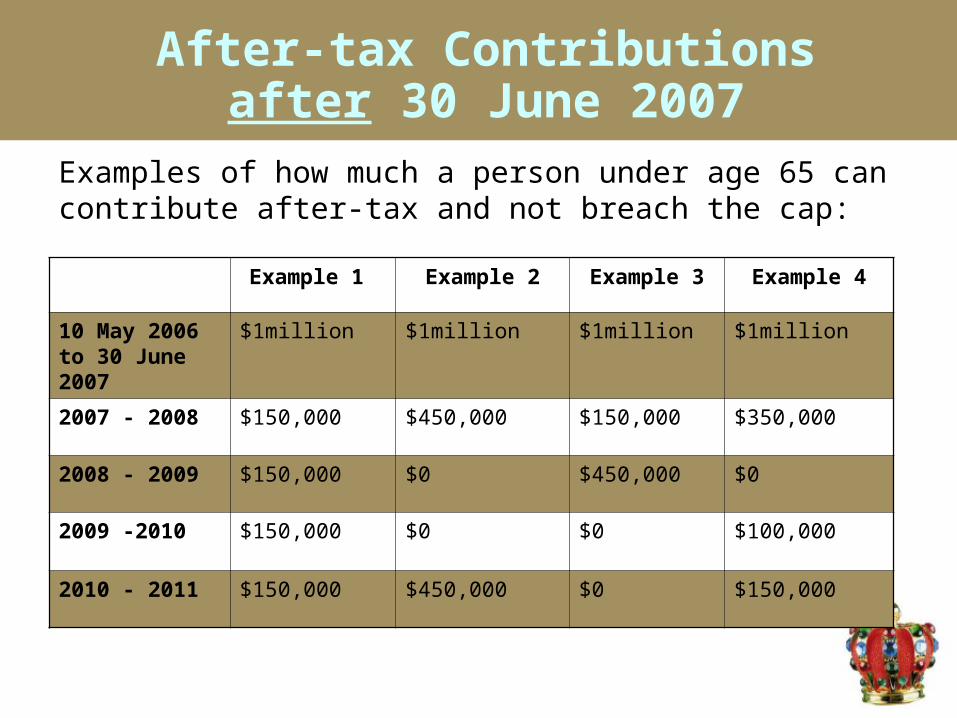

Examples of how much a person under age 65 can contribute after-tax and not breach the cap:

Example 1 Example 2 Example 3 Example 4

10 May 2006 to 30 June 2007

$1million $1million $1million $1million

2007 - 2008 $150,000 $450,000 $150,000 $350,000

2008 - 2009 $150,000 $0 $450,000 $0

2009 -2010 $150,000 $0 $0 $100,000

2010 - 2011 $150,000 $450,000 $0 $150,000

New Lower Contribution Limits

Your contributions to super

After-tax contribution Pre-tax contribution

New rules from 1 July

Limits on how much you can contribute per annum before

penalty tax applies

Limits on how much of the contribution will be eligible for the 15% contributions tax rate

Before-tax Contributions

• 15% tax on employer contributions (including salary sacrifice).

• Currently, there are aged-based limits on how much you can salary sacrifice based on how much an employer can claim as a tax deduction from salary sacrifice + employer contributions.

• From 1 July 2007, these will be replaced by “universal limits” on how much will be eligible for the 15% tax on entry– up to $50,000 p.a. taxed at 15% (employer and salary sacrifice

contributions) – above this, an extra 31.5% tax levied on the individual

• However, if you’re over age 50, up to $100,000 p.a. will be eligible for the 15% contributions tax until 30 June 2012, when the limit will revert to $50,000 p.a. for everyone.

• Review your salary sacrifice limits to maximise opportunities

Before-tax Contributions

2006/07

Aged 50+

2007/08

2006/07

Aged under 35

$100,000

$50,000

$0

Em

plo

yer

Co

ntr

ibu

tio

ns

(in

clu

din

g s

ala

ry

sac

rifi

ce)

elig

ible

fo

r co

nce

ssio

nal

ta

x tr

eatm

ent

$42,385

$15,260

$105,113

2007/08

2006/07

Aged 35 to 49

2007/08 until 2011/12

2012 onwards

If you’re under 50, you benefit from being able to

salary sacrifice more

If you’re over 50, consider salary sacrifice to maximise ability to contribute large pre-tax amounts while you still can

What does this mean?

Transition to Retirement

Did you know it’s possible to draw an income from your super while you’re still working?

Since 2005, access laws have been relaxed to allow people from age 55 to access their super in the form of a non-commutable income stream.

Who would that suit? • People keen to reduce their working hours and just wanting to use the income from super to top up their reduced salary from work. OR • People keen to increase salary sacrifice to boost their nest egg, without sacrificing their lifestyle.

How does it relate to the new changes? • This strategy is even more attractive from 1 July 2007 with the prospect of tax-free super after age 60. Coupled with salary sacrifice, it can boost your retirement savings.

Transition to Retirement

Case Study 1

• Joshua is aged 55 and recently sold an investment. He has $750,000 to invest somewhere. He has also previously under-invested in super and has only accrued $250,000 in his super account. He would like to scale back his work hours but not sacrifice his lifestyle.

• Joshua invests the $750,000 into super before 30 June 2007 (using the $1million cap) and reduces his work hours. He then commences a Transition to Retirement pension to supplement his new lower salary.

• If Joshua didn’t need the extra income, he could also consider salary sacrificing into super, contributing more to super than he withdraws.

• By the time Joshua turns age 60, he can draw the income from his non-

commutable pension tax-free.

Insurance through Super

With the abolition of RBLs from 1 July 2007, insurance through super is even more attractive.

• Under the current rules death benefits are tax-free up to the deceased’s RBL• Under the new rules, death benefits paid to dependants* for tax purposes will be completely tax free.

Insurance through super is attractive because: • Premiums are paid from super balance, which can be built from pre-tax

money• Cover may be available at group premium rates• Automatic acceptance may remove need for medical tests and

underwriting

Review your insurance levels AND your nominated beneficiaries

* Death benefits paid to non-dependants for tax purposes (e.g: an adult child not financially dependant) will still be taxable after 1 July 2007

Retiring Before age 60?

Do you have super dating prior to 1 July 1983?

This component has traditionally been taxed concessionally upon accessing super. From 1 July 2007, it will form part of a tax-free component. But if you retire prior to age 60, some of your super may be taxable, so its desirable to maximise the tax-free component of your super.

Consolidate accounts before 30 June 2007 to achieve the earliest start date across all of your super, resulting in a higher tax-free component

Self-employed Opportunities

Tax deductions• From 1 July 2007, self-employed can claim a full

tax deduction on contributions instead of a 75% deduction after the first $5,000.

• Note that the 15% contributions tax concession is subject to pre-tax contribution limits - which are $50,000 p.a. or $100,000 until 2011/2012 if you are over age 50. Amounts over this will incur extra tax 31.5%

•

Co-contributions • Self-employed people are not currently eligible for the Government Co-

contribution scheme• The scheme pays up to $1.50 for every after-tax dollar contributed - up to

$1,500 p.a.• From 1 July 2007, self-employed people with an income less than

$58,000 p.a. may be eligible.

Other Changes

Changes to pensions• No maximum on income you can draw down• However, maximums still apply on transition to retirement

Changes to assets test for age pensionFrom 20 September 2007:

• the pension assets taper rate will halve from $3.00 to $1.50 per fortnight• more people will be eligible for the age pension based on assets test• Term Allocated Pensions (TAPs) and Annuities purchased from super

benefits on or after 20 September 2007 will no longer receive a 50% exemption from the assets test

• customers who purchased before 19 September 2007 will retain their 50% assets test exemption

• no new TAPs will be available after this date

Tax File Numbers

Check to ensure your super funds have a valid TFN recorded

From 1 July 2007, penalties will apply:

– Where no valid TFN is recorded on a super fund members will incur 46.5% tax on pre-tax contributions for new members joining after 1.7.07.

– For existing members, more than $1,000 has to be contributed before the penalty tax applies. It then applies to the total distribution.

– Funds will not be able to accept post-tax contributions without a TFN.

What else should I think about?

Summary

Super is a tax attractive way to save and receive an income in retirement because compared to paying marginal tax rates outside super:

• In super – contributions and earnings are taxed at a maximum of 15%• In pensions - earnings are tax free

Budget changes will make it even more so:

For people aged over 60 the income drawn from a pension, as well as benefits cashed out from a taxed fund, will also be tax free from 1 July 2007

RBLs will be abolished, meaning you can take a greater level of super savings out of the super system on a concessionally taxed basis

Seek Advice

Financial advice can assist with all aspects of retirement planning and investing:

• Contribution strategies • Asset allocation strategies • Tax structures • Social security issues • Estate planning• Insurance

More Help?

• <Contact details> “I also note that there are some

people who think the new rules are too good to be true.

Let me assure you, they confirm

superannuation as the perfect investment vehicle”

Noel Whittaker, 14 February 2007

Disclaimer

• <adviser to insert legal disclaimer here>

Related Documents