THE VIABILITY OF ASSET BACKED SECURITISATION IN EMERGING MARKETS WITH REFERENCE TO SOUTH AFRICA. STEWART MAKURA A research report submitted in partial fulfillment of the requirements for the degree of MASTER OF BUSINESS ADMINISTRATION in the INSTITUTE OF FINANCIAL MANAGEMENT UNIVERSITY OF WALES BANGOR AND UNIVERSITY OF MANCHASTER OCTOBER 2002 1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

THE VIABILITY OF ASSET BACKED SECURITISATION IN EMERGING MARKETS

WITH REFERENCE TO SOUTH AFRICA.

STEWART MAKURA

A research report submitted in partial fulfillment of the requirements for the degree of

MASTER OF BUSINESS ADMINISTRATION

in the

INSTITUTE OF FINANCIAL MANAGEMENT

UNIVERSITY OF WALES BANGOR AND

UNIVERSITY OF MANCHASTER

OCTOBER 2002

1

ACKNOWLEDGEMENT

I wish to express my appreciation and gratitude to the following persons and without

whom this project would not have been completed:

• Colleagues at Standard Corporate and Merchant Bank for the provision of data,

discussions and support provided towards the success of this research report.

• Mr Ismail Erturk of the Manchester Business School, my supervisor for his guidance

and support.

• My family and friends especially my late sister Gennis Varaidzo for their

encouragement and support during my period of study.

2

TABLE OF CONTENTS

1. THE MECHANICS OF ASSET BACKED SECURITISATION 6

1.1 Research Objectives and Methodology 7

1.2 The parties and processes in Asset Backed Securitisation 7

1.3 Development of Asset Backed Securitisation 14

1.3.1 The United States of America 14

1.3.2 Europe 15

1.3.3 South Africa and Other Emerging markets 17

2 REGULATORY ENVIRONMENT 21

2.1 Regulatory framework in the Developed World 21

2.1.1 United States of America 21

2.1.2 Developed markets in Europe 22

2.1.2.1 United Kingdom 22

2.1.2.2 Germany 24

2.1.2.3 France 26

2.2 Regulatory Environment in Emerging markets 27

2.2.1 Malaysia 27

2.2.2 Hong Kong 28

2.2.3 South Africa 30

3 LEGAL,TAXATION AND ACCOUNTING FRAMEWORK 34

3.1 Legal and Taxation 34

3.1.1 United Kingdom 34

3.1.1.1 Legal 34

3.1.1.2 Taxation 36

3.1.2 The French Credit Foncier de France (“FCC”) 38 3.1.3 Australia 38

3

3.1.4 Hong Kong 39

3.1.5 Malaysia 40

3.1.6 South Africa 41

3.1.6.1 Legal 41

3.1.6.2 Taxation 45

3.2 Accounting 49

3.2.1 United Kingdom 49

3.2.2 Australia 50

3.2.3 South Africa 50

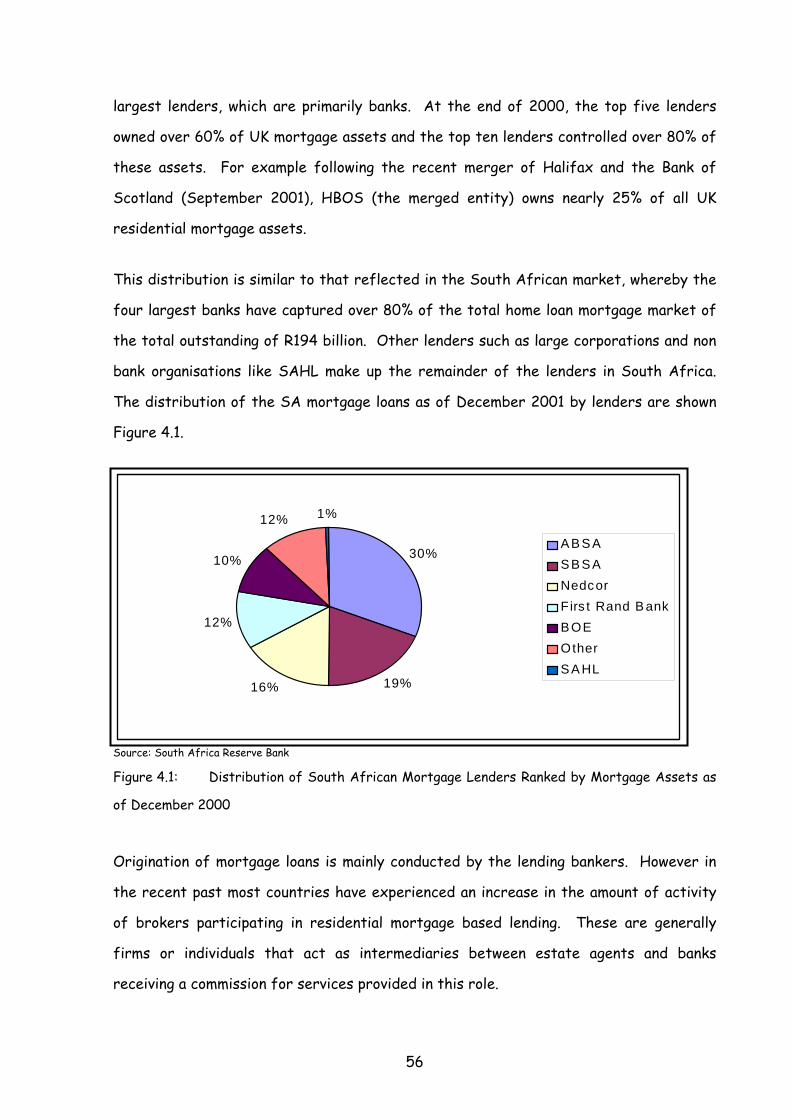

4 ASSET AND ORIGINATOR CHARACTERISTICS 54

4.1 Residential Mortgage Loans 54

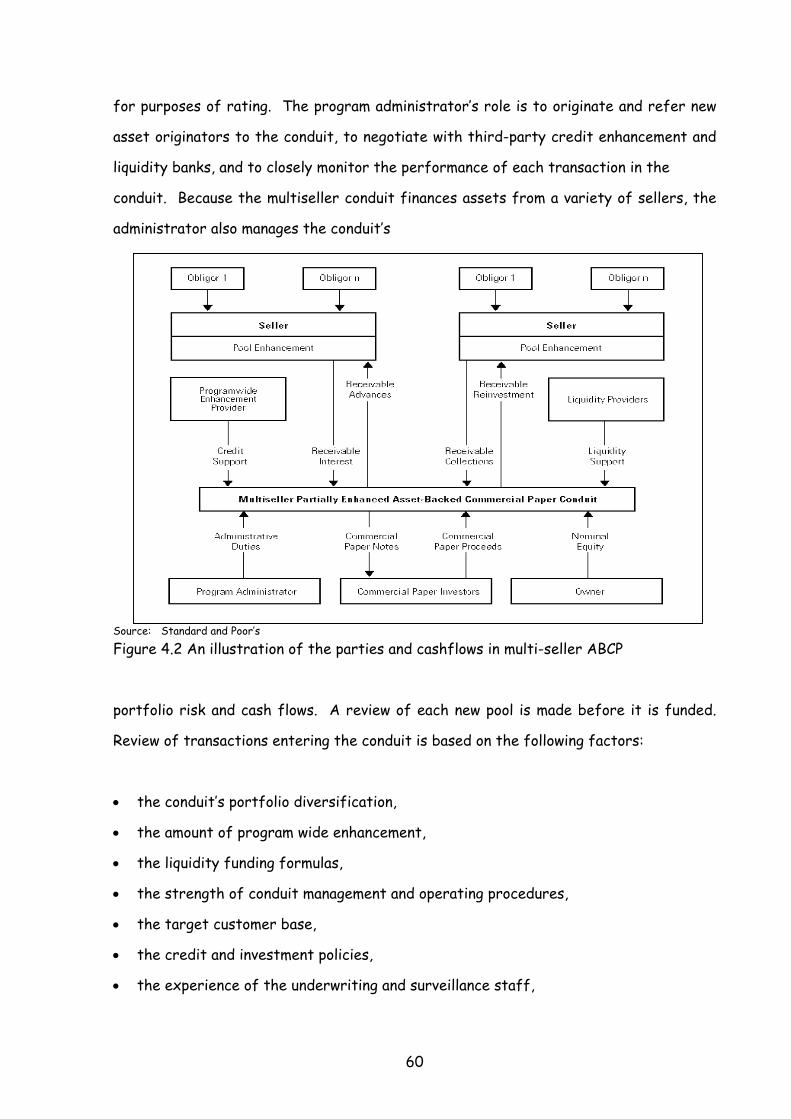

4.2 Asset Backed Commercial Paper (ABCP) Conduits 58

4.2.1 Credit Enhancement in ABCP 61 4.2.2 Non eligible assets 64

4.3 Commercial Mortgage Backed Securitisation (CMBS) 65

5 MARKET INFRASTRUCTURE AND INVESTORS 69

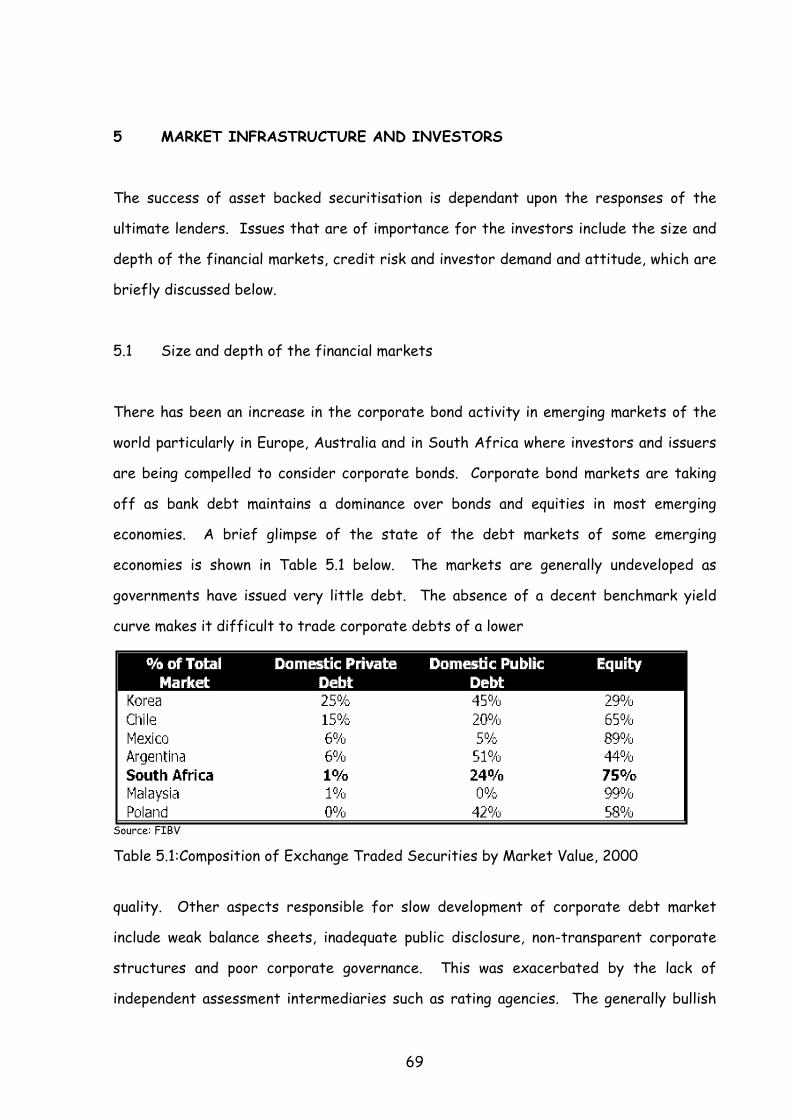

5.1 Size and depth of the financial markets 69

5.2 Credit risk and Investor demand and attitude 71 6 CONCLUSION 78

7. REFERENCES 81

4

TABLE OF FIGURES AND TABLES

Figure 1.1 A typical asset backed securitisation transaction

Figure 1.2. European MBS/ABS Issuance by Asset Type, 1997 and 1998

Figure 2.1 Growth of the UK ABS Market

Figure 2.3: Risk weighting applicable to banks investing in ABS in South Africa

Figure 4.1: Distribution of South African Mortgage Lenders Ranked by Mortgage

Assets as of December 2000

Figure 4.2 An illustration of the parties and cashflows in multi-seller ABCP

Table 5.1:Composition of Exchange Traded Securities by Market Value, 2000

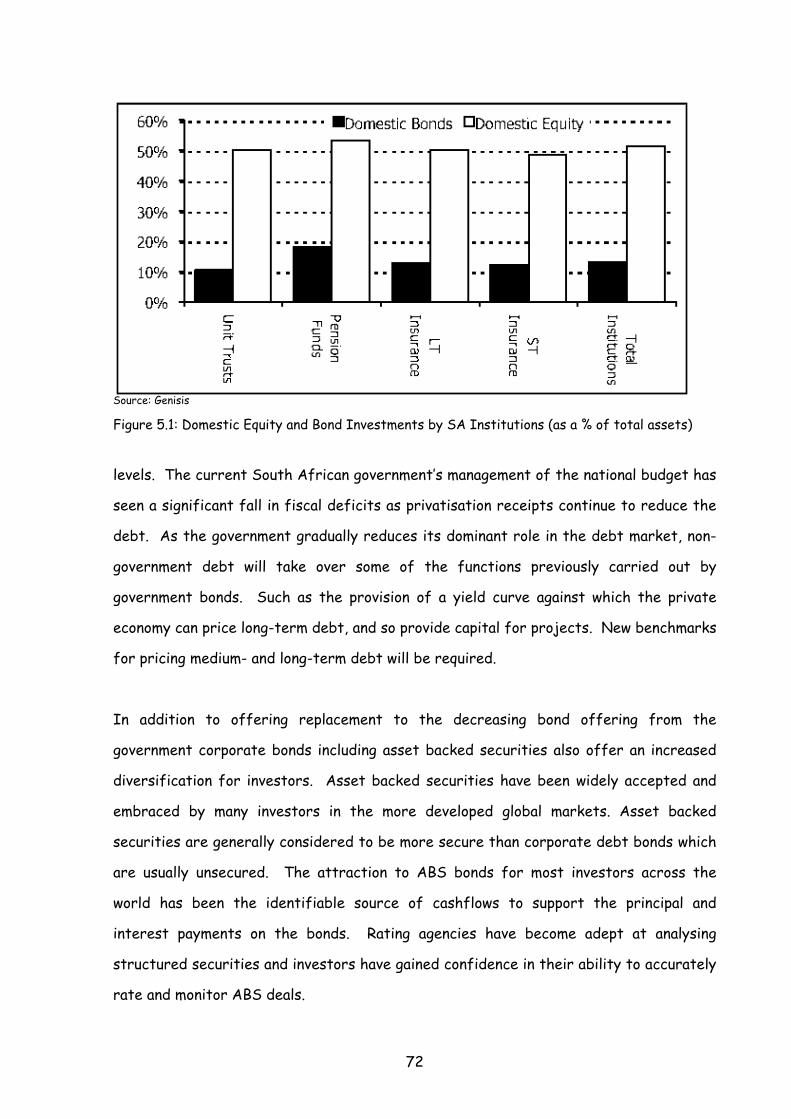

Figure 5.1: Domestic Equity and Bond Investments by SA Institutions

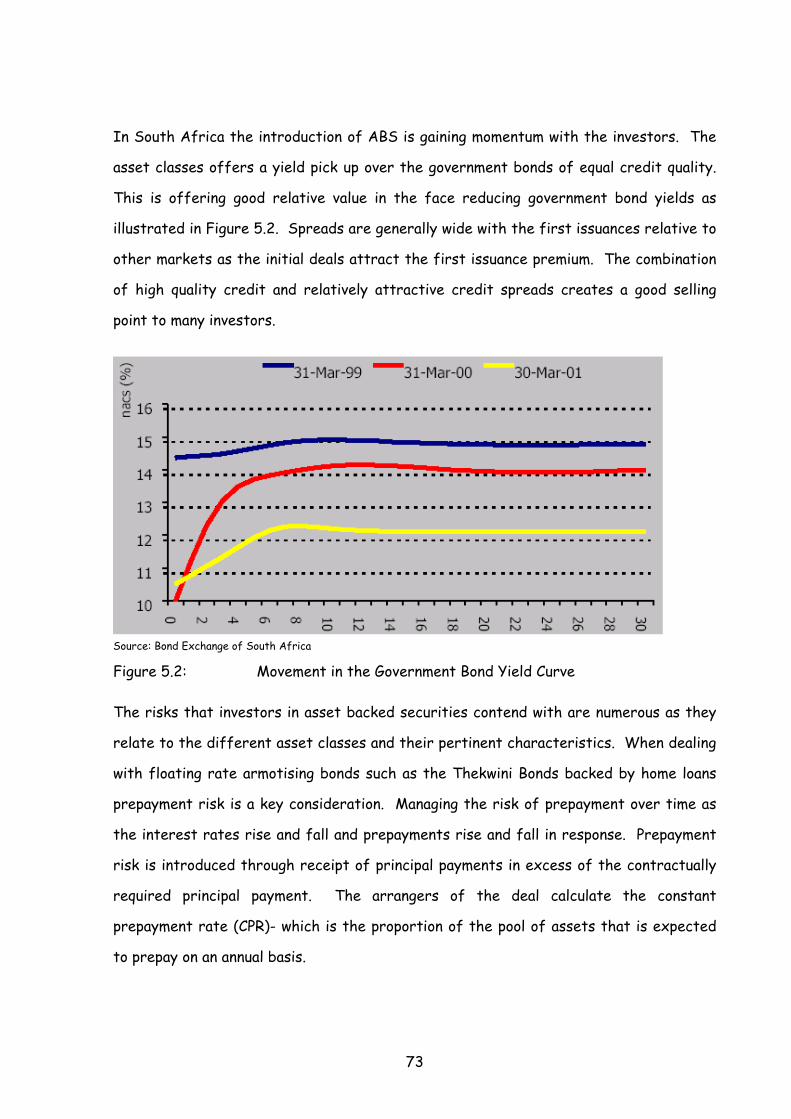

Figure 5.2: Movement in the Government Bond Yield Curve

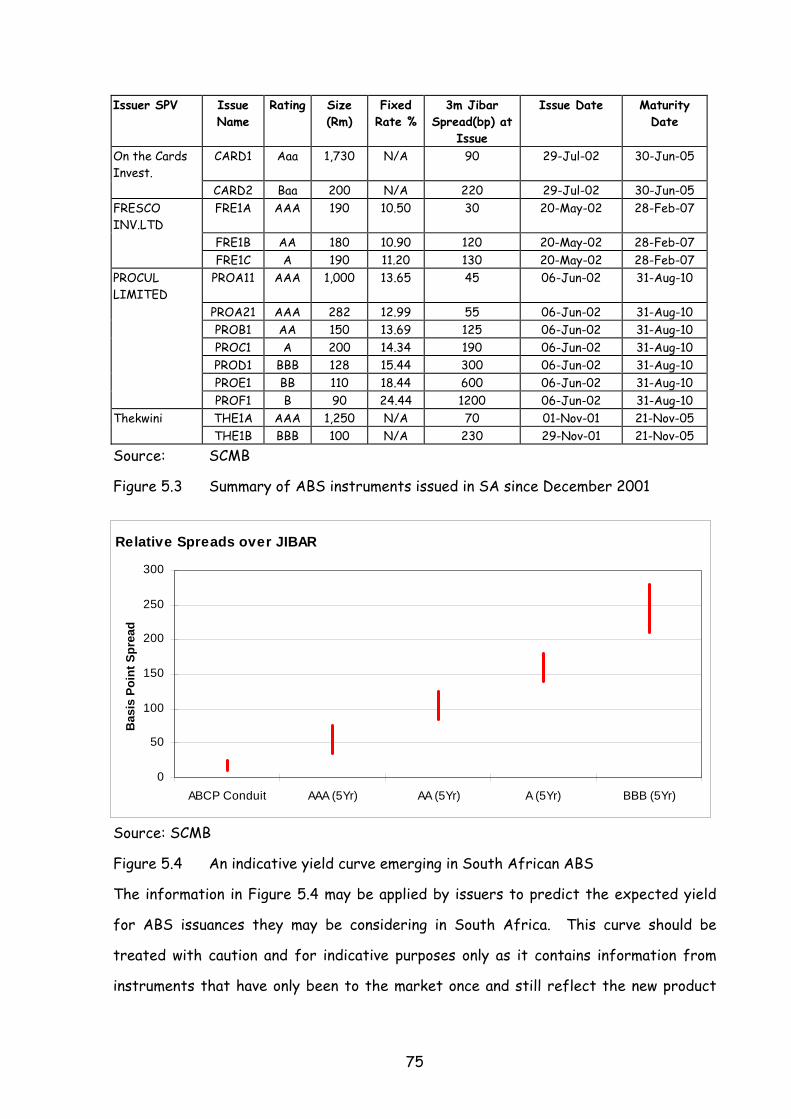

Figure 5.3 Summary of ABS instruments issued in SA since December 2001

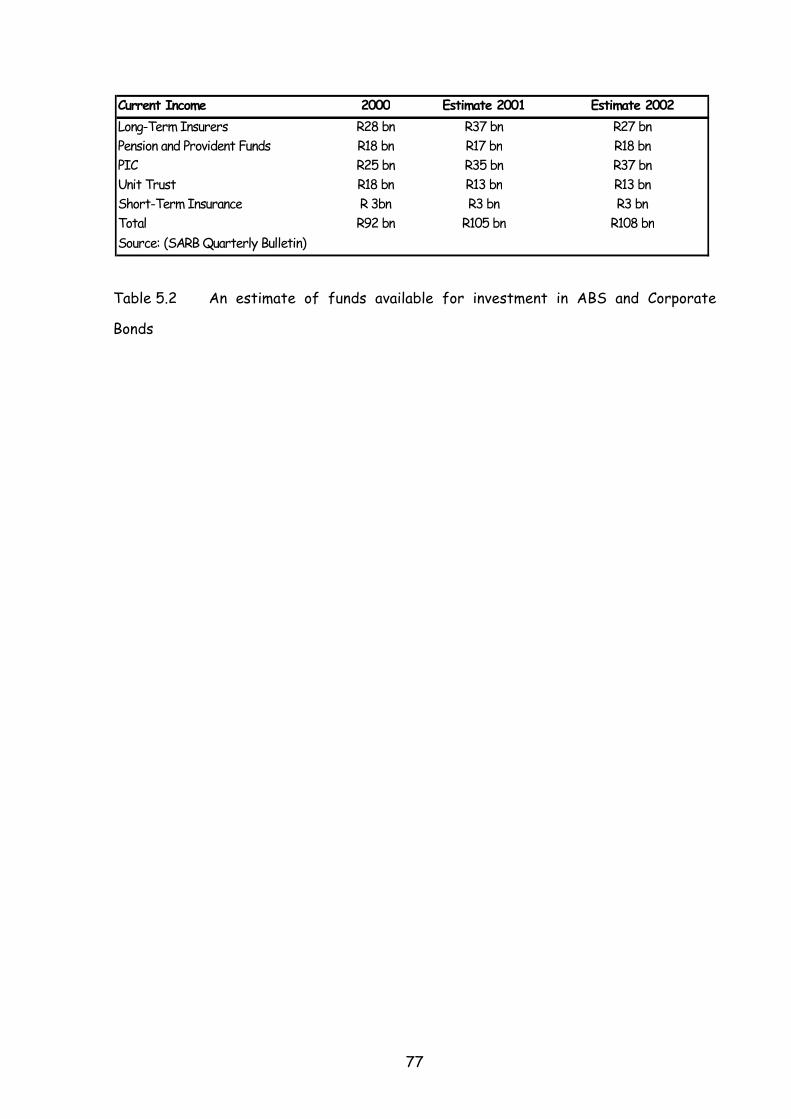

Table 5.2 An estimate of funds available for investment in ABS and Corporate

Bonds

5

1. THE MECHANICS OF ASSET BACKED SECURITISATION

Before presenting the research methodology and findings a literature review was

considered appropriate to provide readers with the necessary background to the

concepts and components of asset backed securitisation (“ABS”). In the context of

this report ABS will be applied to mean all forms of asset backed securitisation

including mortgage backed securitisation (“MBS”) which of are distinguished in most

American literature. In this chapter a broad overview will be given outlining the

processes and parties involved in concluding an ABS transaction. A brief overview of

the historical development of ABS in the USA, Europe and more recently in emerging

markets will be discussed. Further an introduction into the various asset classes that

can be securitised and the benefits sought after by those who participate in

securitisation will be made.

Several definitions have been suggested to describe ABS amongst the more prominent

are the following:

”A device of structured financing where an entity seeks to pool together it’s interest in

identifiable cashflows over time, transfer the same to investors either with or without

the support of further collaterals and thereby achieve the purpose of financing”(V

Kothari, 1999).

“ a means by which providers of finance fund a specific block of assets rather than the

general business of a company”(Accounting Standards Board, 1994).

“Asset securitisation is the structured process, whereby interests in loans and other

receivables are packaged, underwritten, and sold in the form of “asset backed

securities….”(US Office of Comptroller, 1997).

6

In essence the process of ABS entails transformation of illiquid financial assets into

securities that can be traded. Put another way the assets are monetised through the

issuance of asset backed securities. The assets in question can be in theory be any

assets that provide a predictable stream of cashflows, amongst the most common types

of assets that are used in ABS transactions are; residential mortgage loans, credit card

receivables, loans and trade receivables.

1.1 Research Objectives and Methodology

Asset backed securitisation is rapidly becoming a financial tool and concept in the South

African funding and investor scene. The main objective of this report is to predict the

viability and extent to which the application of this tool will be put to use in the South

African market and other emerging markets given the experience in the developed

world.

The research methodologies employed to meet the objectives of this report comprise;

• A review of the available literature to trace and highlight the developments of

securitisation in emerging markets relative to the developed world.

• In particular an in-depth comparison of the regulatory environment, legal and

regulatory framework, asset types and originator characteristics, as well as investor

and market characteristics.

• Input of my experiences as an arranger of asset backed securitisation deals in

South Africa over the last two years.

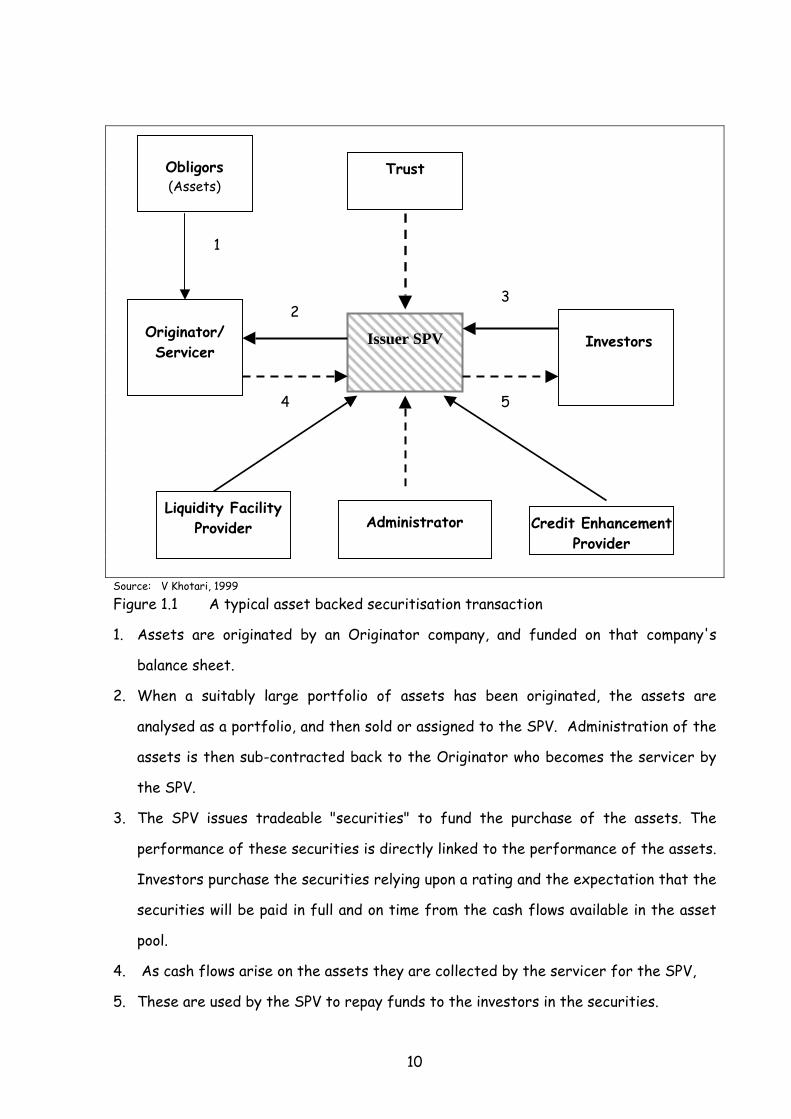

1.2 The parties and processes in Asset Backed Securitisation

The main parties to an ABS are the originator, servicer, issuer, credit enhancers and

liquidity providers, rating angecies, placement agents and the investors. Each of these

party’s role in the ABS transaction will be discussed briefly in turn.

7

The originator also referred to as the seller or transferor is the entity that owns the

asset prior to conducting an ABS. They have a need to raise funding generally at

attractive rates and or a need to free up their balance sheet. The main characteristics

sought in the assets is a predictable stream of cashflows that are capable of being

pooled and securitised.

The issuer usually takes the form of a bankruptcy remote special purpose vehicle (SPV)

owned by and independent trust. The SPV is specially created to perform solely the

functions of buying and pooling of assets from one or more originators. It then raises

funding in the capital markets, money markets or by private placement through issuing

securities backed by or representing and interest on such assets. Generally the SPV is

designed to have limited powers which permit only the needs of the ABS transaction.

It is made bankruptcy remote to ensure that it is sufficiently separate from the

originator and holds the assets that have been transferred to it by way of a “true sale”.

When the sale and transfer of assets to the issuer is completed, the issuer appoints a

servicer to monitor the performance of assets. His main tasks also include collecting

cashflows and ensuring that they are properly distributed. Quite often the originator

is appointed as the servicer usually with a backup/fallback servicer in the event of the

originator not keeping up with the prescribed servicing requirements.

Depending on the required credit rating on the assets, credit enhancers are usually

employed to provide credit enhancement so that the assets can attain the required

rating. The credit enhancement comes in various forms including guarantees issued by

appropriately rated and acceptable institutions, pool insurance policies and special

harzard policies. In some cases the originator provides the first level of credit

enhancement through either selling goods at a discount or a deferred purchase price

arrangement. Asset backed securities can also be credit enhanced through insurance

wraps provided for either certain classes of paper issued or for entire issuances. All

providers of credit enhancement are called credit enhancers.

8

Liquidity providers may also be required in ABS transactions. The main purpose for

liquidity facilities are to provide for liquidity in the event of cashflow mismatches

between the receipt of cashflows from the assets and the payments due on the asset

backed securities on a payment date. In transactions, which are funded through the

issuance of short dated securities on a rolling basis, liquidity facilities are often used to

provide liquidity if there are market disruptions during the rollover period.

The other important party in ABS transactions is the rating agency. There will be at

least one but usually two rating agencies per transaction. They rate the asset backed

securities issued by the issuer on the basis of the credit quality of the underlying

assets, the structural features of the transaction and any credit enhancements

(including the credit quality of the credit enhancer) of the underlying assets or the

asset-backed securities themselves.

When asset backed securities are being distributed into the capital markets, money

market or in the private market, underwriters and or placement agents will purchase

and distribute/place the securities in the markets. Interaction between the various

parties is generally initiated and co-ordinated by the arranger hired usually by the

originator. Other parties that are involved include auditors and lawyers.

There are a number of varieties of "securitisation" and a number of different

structures. However, there is a common theme and process to all of these transactions,

which is illustrated in Figure 1.1 and briefly explained below.

9

Originator/ Servicer

Issuer SPV

Trust

Investors

Administrator Liquidity Facility

Provider

4 5

2

1

Obligors (Assets)

3

Source: V Khotari, 1999 Figure 1.1 A typical asset backed securitisation transactio

1. Assets are originated by an Originator company, and f

balance sheet.

2. When a suitably large portfolio of assets has been o

analysed as a portfolio, and then sold or assigned to the S

assets is then sub-contracted back to the Originator wh

the SPV.

3. The SPV issues tradeable "securities" to fund the pur

performance of these securities is directly linked to the p

Investors purchase the securities relying upon a rating an

securities will be paid in full and on time from the cash f

pool.

4. As cash flows arise on the assets they are collected by th

5. These are used by the SPV to repay funds to the investor

10

Credit EnhancementProvider

n

unded on that company's

riginated, the assets are

PV. Administration of the

o becomes the servicer by

chase of the assets. The

erformance of the assets.

d the expectation that the

lows available in the asset

e servicer for the SPV,

s in the securities.

There are generally seven reasons why companies consider securitisation:

• to improve their return on capital, since securitisation normally requires less

capital than traditional on-balance sheet funding;

• to raise finance when other forms of finance are unavailable (in a recession

banks are often unwilling to lend - and during a boom, banks often cannot keep up

with the demand for funds);

• to improve return on assets - securitisation can be a cheap source of funds, but

the attractiveness of securitisation for this reason depends primarily on the

costs associated with alternative funding sources;

• to diversify the sources of funding which can be accessed, so that dependence

upon banking or retail sources of funds is reduced;

• to reduce credit exposure to particular assets (for instance, if a particular class

of lending becomes large in relation to the balance sheet as a whole, then

securitisation can remove some of the assets from the balance sheet);

• to match-fund (liquidity) certain classes of asset - mortgage assets are

technically 25 year assets, a proportion of which should be funded with long

term finance; securitisation normally offers the ability to raise finance with a

longer maturity than is available in other funding markets;

• to achieve a regulatory advantage, since securitisation normally removes certain

risks which can cause regulators some concern, there can be a beneficial result

in terms of the availability of certain forms of finance (for example, banks are

increasingly using securitisation as a means of managing the restriction on their

wholesale funding abilities).

Establishing the primary rationale for the securitisation activity, is a vital part of the

preparation for a securitisation transaction, since it influences the sorts of

administrative tasks which need to be developed as well as the transaction structures

themselves.

11

Assets, which can be securitised easily generally, have a number of characteristics,

which include:

• Cash-flow- A principal part of the asset is the right to receive a cash flow from

a debtor in certain amounts (or amounts defined by reference to a market or

administered rate) on certain dates i.e.: the asset can be analysed as a series of

cash flows.

• Security-If the security available to collateralise the cash flows is valuable,

then this security can be realised by the SPV. For instance, for a mortgage loan,

there is security over the property and other collateral, which will make a

significant contribution towards recovering any losses, which might otherwise

arise. Consequently, if there is default, an effective method of ensuring that the

SPV can gain the benefit of the security will be required (otherwise

securitisation will be an uneconomic way of arranging funding).

• Concentration risk-Assets should be well diversified. For instance a single

retail loan should be relatively small in value in the context of the available

supply of retail loans. Generally limitations are placed on the acceptable

maximum exposure to a single person/entity within a given portfolio of assets.

This way, the performance of a single asset is not likely to distort the

performance of the entire portfolio. Consequently, the entire portfolio can be

considered as a single asset, with a predictable performance.

• Homogeneity-Assets have to be relatively homogeneous - this means that there

are not wide variations in documentation, product type or origination

methodology. Otherwise, it again becomes more difficult to consider the assets

as a single portfolio.

• No executory clauses-The contracts to be securitised must work, even if the

Originator goes bankrupt. Certain clauses are therefore difficult to include in a

securitisable contract –for example in equipment leasing, the inclusion of a clause

stating that the Originator will maintain the equipment would make that lease

difficult to securitise. These sorts of contract are normally referred to as

"executory contracts".

12

• Capacity-It must be possible for the necessary transactions which are needed

for the securitisation to take place in relation to the assets concerned - for

instance, if the assets contain specific prohibitions against assignment, then

they will not be securitisable in the traditional sense.

• Independence from Originator-The on-going performance of the assets must

be independent of the existence of the Originator. This tends to be a wider

restriction than the example given above about executory contracts. A number

of technical matters can arise, for instance, if asset yields are quoted only by

reference to the Originator (eg; as the Originator's rate), then this will cause a

structural difficulty in the event of the Originator's insolvency.

13

1.3 Development of Asset Backed Securitisation

1.3.1 The United States of America

The United States of America is currently the largest asset backed securitisation

market in the World. It is the only market in the World where ABS market draws

participation from both institutional as well as individual investors. This market also has

the most number of securitisation applications than any other. In terms of global

volumes in ABS three-quarters are originated from the USA. This indicates the

tremendous significance of USA in global securitisation market, which extends to issues

originating from other countries, including Japan, Europe and some of the emerging

markets. The total volume of securitisation in USA was estimated at over $2.8 trillion

at the end of 2000. With the bulk of it ($1.9 trillion) dominated by the government-

sponsored programmes popularly known as Ginnie Mae, Fannie Mae, and Freddie Mac,

which support housing finance and account for almost $9 out of every $10 in the MBS

market. Other major components of the ABS market include commercial mortgages

($200 billion), credit-card receivables and home-equity loans ($220 billion), and

automobile loans ($75 billion). Secondary trading in mortgage backed securities in the

US has recorded average daily volumes of over $70,9 billion in 1998.

The main causes of the establishment of the ABS market in the US include, the need

and willingness of the government to channel funds from the securities market to the

home loans market by providing guarantees on the mortgage backed securities

generated by regional and local government agencies. The technology and expertise

developed in the mortgage backed securities led to the development and packaging of

other bank assets. There was an increased significance in ABS during the 1970’s and

1980’s due to the debt crises in the US which emanated from debts extended to

developing countries which were being poorly serviced by the borrowers. In an attempt

14

to manage the pending liquidity crises most banks sold their assets in the form of asset

backed securitisation schemes.

The main key drivers for growth of ABS in the US include; the associated saving in

regulatory capital required for normal bank funded loans. The increased possibilities in

earning fee-based income generated as banks participated in these asset backed

securitisation transactions in various roles such as sponsors, arrangers or underwriters.

Other key attractions included cheaper and diversified sources of funding for the

originators and better returns for the investors.

1.3.2 Europe

There is evidence that schemes similar in nature to the modern United States form of

asset backed securitisation existed in Denmark where a mortgage credit system has

existed in Denmark for over 20 years now. There is also pfandbrief market in Germany,

which is a secondary mortgage market. Although a form of securitisation has been in

existence in the German and Danish mortgage markets for a long time, securitisation in

the modern sense only emerged in Europe in the mid- 1980s. Growth of asset backed

securitisation in Europe has progressed at a slow pace and has only recently evolved into

a viable and rapidly advancing sector.

The number and value of European issues in the ABS market increased significantly in

1999, as a result of favourable regulatory changes, and the introduction of the Euro.

According to estimates by Moody's Investors Services, annual issuance of European

MBS/ABS was less than $10 billion until 1996, when it jumped to $30 billion, then

further increased to $45.4 billion in 1997. Volume for 1998, however, was about the

same as 1997, at $46,6 billion, as the flight to quality towards the end of 1998 due to

the Asian and Russian crises led to widening in ABS spreads and reduced issuance. The

total outstanding volume of European ABSs has been estimated to be about $130 billion,

15

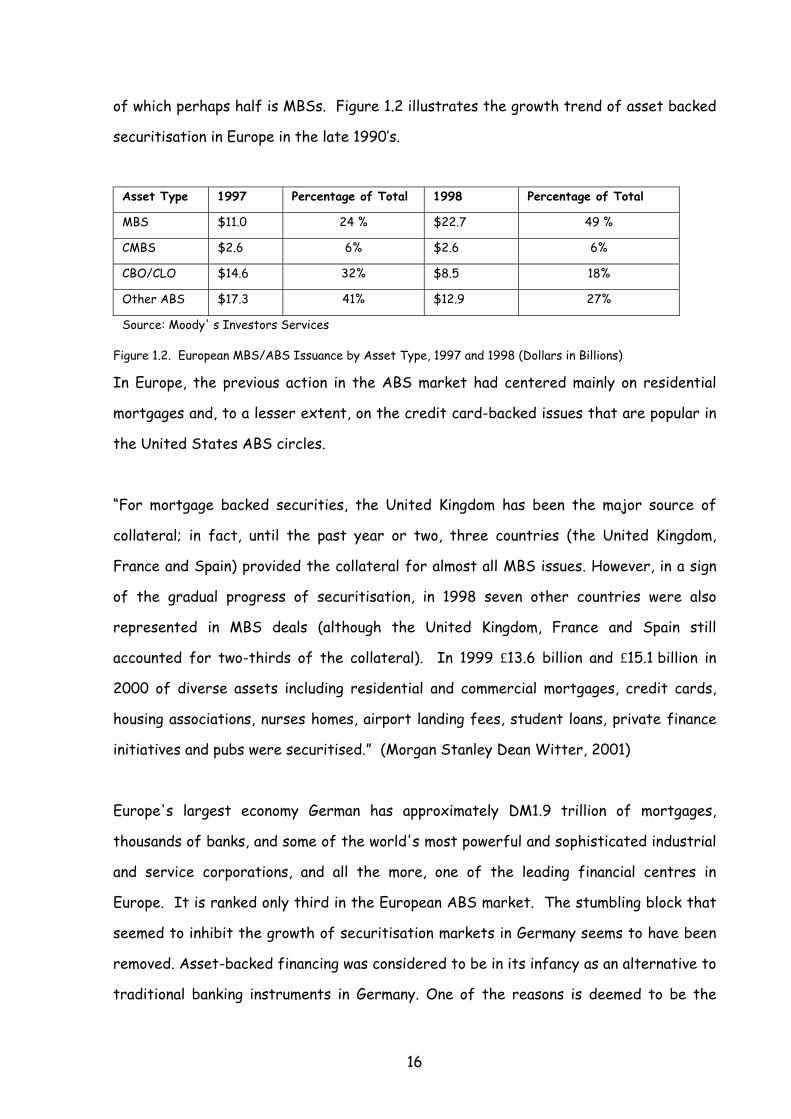

of which perhaps half is MBSs. Figure 1.2 illustrates the growth trend of asset backed

securitisation in Europe in the late 1990’s.

Asset Type 1997 Percentage of Total 1998 Percentage of Total MBS $11.0 24 % $22.7 49 % CMBS $2.6 6% $2.6 6% CBO/CLO $14.6 32% $8.5 18% Other ABS $17.3 41% $12.9 27% Source: Moody' s Investors Services

Figure 1.2. European MBS/ABS Issuance by Asset Type, 1997 and 1998 (Dollars in Billions)

In Europe, the previous action in the ABS market had centered mainly on residential

mortgages and, to a lesser extent, on the credit card-backed issues that are popular in

the United States ABS circles.

“For mortgage backed securities, the United Kingdom has been the major source of

collateral; in fact, until the past year or two, three countries (the United Kingdom,

France and Spain) provided the collateral for almost all MBS issues. However, in a sign

of the gradual progress of securitisation, in 1998 seven other countries were also

represented in MBS deals (although the United Kingdom, France and Spain still

accounted for two-thirds of the collateral). In 1999 £13.6 billion and £15.1 billion in

2000 of diverse assets including residential and commercial mortgages, credit cards,

housing associations, nurses homes, airport landing fees, student loans, private finance

initiatives and pubs were securitised.” (Morgan Stanley Dean Witter, 2001)

Europe's largest economy German has approximately DM1.9 trillion of mortgages,

thousands of banks, and some of the world's most powerful and sophisticated industrial

and service corporations, and all the more, one of the leading financial centres in

Europe. It is ranked only third in the European ABS market. The stumbling block that

seemed to inhibit the growth of securitisation markets in Germany seems to have been

removed. Asset-backed financing was considered to be in its infancy as an alternative to

traditional banking instruments in Germany. One of the reasons is deemed to be the

16

uncertainty regarding the legal structure, validity, and enforceability of the many

transactions involved in a securitisation program. The Bundesaufsichtsamt fhr das

Kreditwesen, the German Supervisory Authority for the Banking and Capital Markets

Industry has recently passed a rule which gives securitisations their official blessing

and will contribute to the acceptance of securitisation as an effective commercial law

financing instrument under German law.

1.3.3 South Africa and Other Emerging markets

The history of securitisation in South Africa dates back to 1989 when the first

securitisation issue a R250 million mortgage-backed issue by the then Allied Building

Society (United Bank of South Africa Limited). Another public issue took place in 1991

offered by Sasfin Limited comprising the securitisation of lease rentals from leasing of

machinery and equipment for R30 million. In South Africa, the concept of

securitisation was not widely accepted despite the two issues, noted above and the

other worth an estimated R3,5bn placed on the market in the late 1980s and early

1990s through private placements. The limited success of the earlier securitisation

transactions was due to little interest from the banks. Most of the banks felt no need

to securitise their assets, as they were not faced with capital constraints and had little

or no pressure from shareholders to improve on returns.

In addition a weak regulatory environment, significant limited sovereign issuance and a

generally illiquid and undeveloped corporate debt market hindered the development of

asset backed securitisation in South Africa.

Toward the end of 1997 The National Housing Finance Corporation, (NHFC) a South

African Government sponsored body decided to employ securitisation to provide

liquidity to the mortgage market to support home ownership in the medium to lower end

of the market. The ideas were based on a structure similar in nature to the Fannie Mae

structure of the United States. The intention was to have the securitised assets

17

housed in Gateway (Pty) Ltd a subsidiary of NHFC formed to create housing

opportunities for low and moderate income borrowers in 1999, from where funding

would be sourced directly from the capital markets. Several originators were

identified, generally tier two banks to originate a pool of qualifying loans using funding

provided by the NHFC. By the end of 1999 approximately R750 million worth of home

loans were in the special purpose vehicle and the originating banks were facing large

constraints in attracting deposits to write further loans. This was mainly due to the

lack of confidence in tier two banks. The need to access the capital markets funding

was more crucial than ever before. An arranger was mandated by the NFHC, who

managed to put in place the various parties to the transaction. It was however felt that

an additional amount of money would be required to increase the pool value to about R1

billion to reduce the liquidity premium associated with smaller issuances. However the

national government was not willing to issue guarantees to possible “warehouse” funding

providers (funders that facilitate building of a portfolio prior to approaching investor

markets). This led to the collapse of the Gateway program as some large banks, which

held shareholdings in the tier two banks ended up purchasing the assets from the pool

as the originator banks were closed or absorbed into their parent entities.

South African Home Loans (SAHL) commenced operations in 1999 as the first non-bank

securitised mortgage loan provider. The business model is based on an Australian

equivalent.

The business strategy is to capture a share of the homeloan market by offering low

cost mortgages to highly creditworthy borrowers. The current portfolio of SAHL is

less than 0,5% in a market where over 90% of the country’s mortgage market is

controlled by the country’s largest five banks. At the end of 2001 The Thekwini Fund 1

Limited a securitisation SPV issued R1,2 billion worth of asset backed bonds. The notes

were structured into three tranches 92% Class A notes, 6% Class B notes supported by

a 2% reserve/equity fund and were heavily oversubscribed in the capital markets

despite the absence of major bank investors due to the lack of regulatory stimulation.

18

Shortly after the issuance of SAHL securities the South African Reserve Bank (SARB)

issued regulations which designate securitisation as an activity not falling within the

meaning of "the business of a bank", and gives guidelines as regards securitisation

schemes in December 2001. These mandatory guidelines form the first step towards

the prospect of creating asset backed securities which would in turn attract large

amounts of capital, which they would otherwise not have been able to attract, from

countries such as the United States of America and Japan. Although demand for

securitised assets from large institutional investors is already immense and growing,

there are many features, such as, transfer duties, value-added tax ("VAT") at the

special-purpose vehicle level and VAT on custodial and trustee services which continue

to impede development of asset backed securitisation in emerging markets. Other

regulators in South Africa are clearly faced with a challenge to review the impediments

to legitimate and prudent securitisation within their jurisdiction and to work towards

removing such impediments where appropriate. Other limitations include ignorance on

the part of investors who prefer to invest in listed companies with established track

records. There are also legislative and accounting problems.

In most emerging markets in Asia asset backed securitisations have been characterised

by novel, one –off means of fund raising. The main characteristics responsible for the

limited growth include uncertain or unhelpful legal and regulatory environments.

In Korea for example the Act on Asset Backed Securitisation came into being in

September 1998 prior to this act issues by Korean companies and banks were few and

restricted to non-Korean assets. Many attempts to securitise loan and lease

receivables were unsuccessful due to practical and legal issues particularly security

issues. Korea has taken the first step towards providing certainty for the development

of asset backed securitisation. It is hoped that increased utilisation of this alternative

funding method will be the result contrary to Thailand where an equivalent

securitisation decree was issued but remains largely unused in 1997.

19

Activity of ABS has been slow to develop in New Zealand in comparison to other

jurisdictions. This is partly due to the small size of the New Zealand market, but

however new entrants are building significant asset pools suitable for securitisation.

And increasingly New Zealand originated assets are being sold into international

portfolios. There are few regulatory issues in this country and it is unlikely to be

required since there are no regulatory agencies that restrict the origination of assets.

20

2 REGULATORY ENVIRONMENT

Regulators’ understanding of the concepts and their facilitation through regulations

particularly pertaining to the financial industry with emphasis on the banking regulator

have a strong influence on the state of the development of securitisation markets

across the world. In this chapter brief description of the various changes experienced

in the US, Europe and some emerging markets are discussed and comparisons drawn

including the environment and other events which influenced such decisions.

2.1 Regulatory framework in the Developed World

2.1.1 United States of America

As previously alluded to in Chapter 1, the onset of securitisation in the US where it was

first used as a major source of funding was fully backed by the US government. Central

to the regulatory requirements regarding securitisation in the US is the Securities Act

of 1933. It provides that public offerings of securities including ABS must be

registered with the Securities and Exchange Commission (“SEC”). As such the

prospectus used to offer these securities must meet specified disclosure standards.

Private placements can also be made under the guidance of Rule 144 of the SEC, which

stipulates that the level of disclosure is dependent on the number of issuers and the

number of investors. It also takes into consideration the level of sophistication of the

investors also known as accredited investors who have the necessary knowledge to

judge the offered securities without the level of disclosure required in a registered

offering. This rule is complemented by Rule 144a, which provides the framework for

promoting secondary trading of the securities including ABS.

21

2.1.2 Developed markets in Europe

However in Europe the development of ABS was slow and cumbersome in most countries

prior to the introduction of laws, regulations and guidelines from the respective bank

supervisors. The absence of such guidelines excluded and restricted the participation

of regulated entities such as banks that now form the largest group of originators of

assets used in ABS. Spectacular growth has been witnessed post 1998 as various

securitisation techniques have emerged across Europe. Some of the more important

developments in specific countries and their impact on the development of the ABS

markets in Europe are discussed in turn below.

2.1.2.1 United Kingdom

The UK, which is the largest securitisation jurisdiction in Europe and has also, hatched

exotic applications of securitisation. Guidance for securitisation regulations affecting

financial institutions emanates from the capital adequacy requirements in relation to

the transfer of assets. The Financial Services Authority (“FSA”) has issued a number

of notes relating to the use of securitisation by regulated entities. The most recent

being the chapter on “Securitisation and Loan Transfers”, which forms part of a new

Guide to Banking Supervisory Policy. As the capital requirements in financial

institutions have become very important partly due to the increased regulatory capital

prescriptions. And the trend towards increased emphasis on return on capital employed

as opposed to asset building. The guidelines as provided by FAS allow the structuring

of transactions in ABS to restructure the risk profiles of assets and consequently

lower risk weighting for these assets.

It also makes provision for allowing for the assets to be removed from the regulatory

balance sheet of the financial institution, in accordance with the guidelines, thus leaving

the institution with more capital for new lending activities. This is all done without any

serious implications for the underlying customers since the originator would continue to

service and collect these assets. The guideline sets out a number of primary and

22

secondary conditions that must be met to effect a securitisation. These also include

requirements in relation to the provision of swaps and the pricing thereof.

In addition bank originators of mortgage loans for example also have to comply with the

Department of Environment Statement of Practice on the transfer of mortgages issued

in November 1989. This deals with the issue of obtaining consent of the underlying

borrowers to the securitisation scheme. It lays down rules relating to whether a

general or specific consent would be required from the underlying mortgagors. In

instances were the underlying borrowers are individuals consumer protection legislation

and data protection legislation may be relevant and transactions would have to be

structured to ensure compliance with relevant regulations.

Two of the most common statutes in the UK are the Consumer Credit Act, 1974 and the

Data Protection Act, 1998.

In the case of revolving assets such as credit card backed securitisation increased legal

and moral risks have attracted additional requirements which are stipulated in section 7

of the “Securitisation and Loan Transfers” structure. These include guidelines for

ensuring equal terms of interest, principal, expenses, losses, and recoveries between

the originator and the investors in securities backed by credit card receivables. Such

schemes may be eligible for off balance sheet treatment by the FSA on meeting

predetermined regulations. In addition the FSA requires conviction that the originator

has proper plans to manage it’s liquidity to cope with funding requirements on the

occurrence of scheduled or early termination of the scheme.

The introduction of the guidelines and regulations amongst other factors contributed to

the jump starting of significant securitisation in the UK in 1988. Subsequent changes in

the guidelines and the introduction of FAS has largely been responsible for the

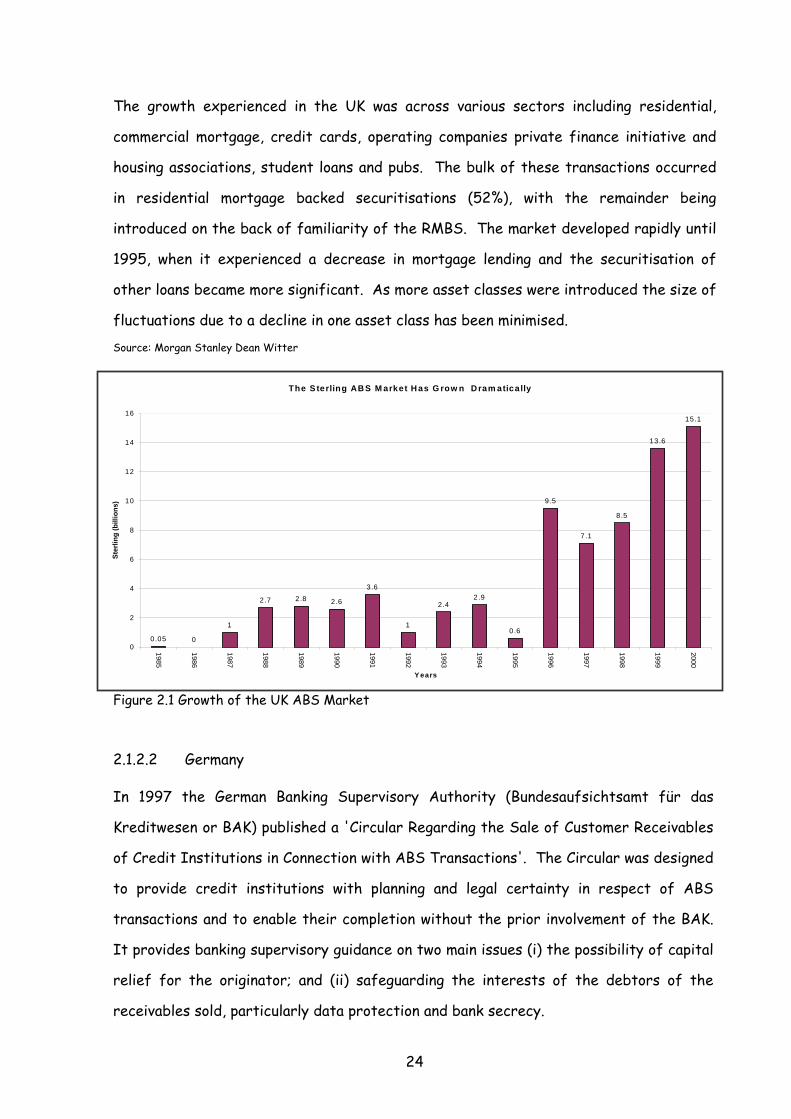

exponential growth experienced in the ABS market in the UK between 1996 and present

as illustrated in Figure 2.1.

23

The growth experienced in the UK was across various sectors including residential,

commercial mortgage, credit cards, operating companies private finance initiative and

housing associations, student loans and pubs. The bulk of these transactions occurred

in residential mortgage backed securitisations (52%), with the remainder being

introduced on the back of familiarity of the RMBS. The market developed rapidly until

1995, when it experienced a decrease in mortgage lending and the securitisation of

other loans became more significant. As more asset classes were introduced the size of

fluctuations due to a decline in one asset class has been minimised.

Source: Morgan Stanley Dean Witter

Figure 2.1 Growth of the UK ABS Market

The S terling AB S M arket H as G row n D ram atica lly

0.05 0

1

2.7 2.8 2.6

3.6

1

2.42.9

0.6

9.5

7.1

8.5

13.6

15.1

0

2

4

6

8

10

12

14

16

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

Y ears

Ster

ling

(bill

ions

)

2.1.2.2 Germany

In 1997 the German Banking Supervisory Authority (Bundesaufsichtsamt für das

Kreditwesen or BAK) published a 'Circular Regarding the Sale of Customer Receivables

of Credit Institutions in Connection with ABS Transactions'. The Circular was designed

to provide credit institutions with planning and legal certainty in respect of ABS

transactions and to enable their completion without the prior involvement of the BAK.

It provides banking supervisory guidance on two main issues (i) the possibility of capital

relief for the originator; and (ii) safeguarding the interests of the debtors of the

receivables sold, particularly data protection and bank secrecy.

24

Other important factors that are highlighted in the German regulations include,

• a legal valid transfer of the receivables to the SPV (a 'true sale');

• limited recourse against the originator;

• repurchase of the receivables sold to the SPV is only permitted for the purposes of

finalising the transaction and is limited to a rest-portfolio of less than 10% of the

receivables sold to the SPV at their then current value (the clean up call option).

• restrictions for the originator nor any of its affiliates to participate in the

financing of the SPV during the transaction. And purchases of ABS by the

originator in the secondary market must be at the current market price and must

not involve the granting of credit to the SPV.

• to avoid the deterioration of the originators’ risk profile due to the sale and

transfer of high quality receivables in ABS transactions, the BAK requires that the

receivables be selected randomly from the originator's receivables portfolio. The

auditor's report on the audit of the annual accounts of the originator must comment

on any material deterioration of the portfolio caused by an ABS transaction. This

may lead the BAK to assess whether 'special circumstances exist, requiring a

revision of the own funds assessment; and

• To facilitate ABS transactions by credit institutions, the Circular provides that no

consent from the debtor of the receivable is required for the transmission of data.

The introduction of the regulations in Germany saw an increase in the assets being

securitised. In particular diversification to a range of assets comprising mainly trade

receivables, credit card transactions and other ‘exotic’ assets. The clear guidelines and

resultant transactions catapulted Germany into second place behind the UK,

contributing 17% and 18% in ABS issuance in Europe for 1999 and 2000 respectively.

This excludes the residential mortgage issuances, which are mainly in the form of the

traditional Pfandbrief.

25

With an outstanding of almost DEM 2 trillion, the overall German Pfandbrief market is

the largest capital market segment in the world's non-government sector.

2.1.2.3 France

Recent legal developments have taken place aimed at advancing securitisation markets in

France. The original French legislation on securitization was implemented by the Act of

1988. Under this legislation, credit institutions, insurance companies and the Caisse des

dépôts et consignations (a public entity) were permitted to sell their receivables to a

vehicle, the fonds commun de créances or FCC (equivalent of the SPV known in other

markets), which would be financed by issuing units on the market. Amendments in 1997

extended the scope of the legislation by taking into account most of the objections of

market practitioners. It allowed an FCC to purchase and issue from time to time any

type of receivables (including doubtful receivables or receivables of different types),

whether denominated in French francs or in other currencies. The 1998 amendments

have further expanded the scope of securitisation by making it possible for commercial

companies to also use FCC to securitise their assets - earlier, the facility was limited to

financial intermediaries such as credit institutions and insurance companies alone.

Second, the originator is no longer required to notify the debtors of the assigned

receivables of the transfer of their receivables - which was required earlier and was

found to be detrimental to the interests of the originator.

Until 1993 securitisation of bank to bank loans dominated the French market accounting

for up to 70% of total transactions. The securitisation law was adopted with the main

objective of promoting the securitisation of mortgage loans. However the market has

been dominated by personal loan transactions. These assets are easier to securitise

mainly due to high margins that could afford to pay transaction fees and still offer the

underlying investors a good spread. With issuers gaining experience and modifications

in the law in 1995. FFr 5 billion worth of residential mortgage backed securities were

issued. Up to 1998 more than 120 FCC's had been set up by way of public offering,

representing approximately 150 billion French francs. The market has continued to grow

accounting for about 10% of the ABS issuance in Europe 1999.

26

2.2 Regulatory Environment in Emerging markets

The introduction of regulations and their subsequent influence in the developed world

on ABS advancement as discussed above has generally been positive. Evolvement of

similar regulations in emerging markets is examined and discussed below with the aim of

establishing influence on the development of securitisation in these markets.

Regulators’ attitudes and levels of understanding of ABS is on the increase in most

emerging markets. Basic securities laws are being passed, a trend is emerging to

redefine laws governing capital reserve requirements for lenders and investors. Most

regulators also perceive securitisation as the tool that will add impetus to the

development of capital and money markets, especially increasing the size of corporate

loans.

2.2.1 Malaysia

Securitisation started in Malaysia in 1986 with the establishment of the government-

owned National Mortgage Corporation. This is a secondary mortgage market agency,

which issues debt securities commonly known as Cagamas Bonds. Cagamas is by far the

largest issuer of ABS in Malaysia. The Malaysian government presented Budget 2000,

which was hailed as expansionary, and growth oriented. Among a number of measures to

boost capital markets, there is a proposal to encourage companies to opt for

securitisation. The budget 2000 proposed that the instrument used in the transfer of

assets be exempted from stamp duty. Subsequently ABS guidelines were released in

April 2001.

The regulations seek to provide clear and transparent criteria for securitisation

transactions. Some of the key aspects include;

27

• Requirement for all securities issued to be approved by the Malaysian Securities

Commission based on standards setout in the guidelines on the Offering of Private

Debt Securities;

• The originator should have had at least six months interest in the debts prior to

securitising them.

• Transfer of assets to the SPV should be by way of a true sale to ensure a

bankruptcy remote characteristic.

• ABS guidelines prohibit an originator from, holding a direct or indirect equity stake

in the SPV.

• Purchase of securities by originators in a securitisation transaction without

Malaysian Securities Commission permission is limited to10%.

The positive developments in terms of the regulatory environment in Malaysia and the

region have been met with limited action. There was increased interest and mandates in

the period leading up to the Asian financial crisis, however most of these deals had to

be abandoned. Since 1999 there has been a re-invigoration of the market. Like in the

UK over 50% of the deals completed are backed by mortgages and new asset classes

are being introduced. However, largely due to the macro economic environment

potential remains far greater than the activity. The pullback in lending during the Asian

crisis produced strong bank liquidity. In Malaysia there is also a concern over the

potential for the unexpected reintroduction of capital controls similar to the foreign

exchange controls recently introduced. More changes are in the pipeline from the

regulators to facilitate securitisation. Another important factor is that whilst the

regulations are in place, most issuers tend to see securitisation as a sign of weakness,

as the market will think they are under pressure to sell assets.

2.2.2 Hong Kong The Hong Kong Monetary Authority's (“HKMA”) supervisory policy towards asset

securitisation and mortgage backed securities enacted in 1990 includes policy guidelines

that set out;

28

• the supervisory tests applied to asset securitisation schemes to decide if the assets

concerned can be excluded from the seller's balance sheet for capital adequacy

purposes; and

• the criteria for MBS to qualify for a 50% risk weight;

• Authorised institutions intending to conduct any securitisation transaction have to

inform the HKMA of their intention well in advance.

• How to determine whether the assets have transferred in the form of a “clean

sale”;

• An institution may undertake the role of servicing the pool of assets held under the

securitisation scheme.

• It is the HKMA’s view that the concessionary risk weighting of 50% should not be

applied to the subordinated tranches of any MBS issue. The purpose of

subordinated tranches of MBS is to absorb the credit losses, which may arise in the

mortgage portfolio which support the MBS. They should accordingly be weighted at

100%.

Whilst Hong Kong clearly has an advantageous regulatory environment, issuance levels

are much less than in the developed world. There is a significant lack of issuers in Hong

Kong due to the strong balance sheets that corporates generally have, and can

therefore fund at relatively low cost in the traditional bank market. In Hong Kong

securitisation began with a few residential mortgage backed security issuances and

some credit card deals. This was later complemented by several commercial mortgage

deals after the Asian crisis. Hong Kong has managed to generate approximately 60% of

the Asian market.

Many analyst believe that the Hong Kong market has reached stagnation as most of the

banks now look at property securitisation mainly for liquidity management as opposed to

capital reserve reduction since the passing of the new laws which prescribe a 50% risk

weighting for mortgage backed securities.

29

2.2.3 South Africa

In many respects development of asset backed securitisation in South Africa followed

in the framework of the European securitisation market particularly that of the UK. In

1991 the Office For Deposit Taking Institutions at the South African Reserve Bank

issued a paper on the Guidelines Regarding Securitisation. This paper acknowledged the

need for a proper regulatory framework for securitisation stating that, “securitisation

is a desirable financial market development tool in that it broadens the funding base

and profitability of deposit taking institutions whilst enhancing liquidity in the market

through the creation of negotiable asset backed instruments.” The key issues

discussed in these guidelines related to the legal status of transfer of the assets,

outlining of the risks associated with a securitisation scheme, recourse with respect to

the assets transferred to the SPV and the general management aspects of the SPV.

Following the paper discussed in the above paragraph, a Securitisation Schedule, Notice

153 of 3 January 1992 was gazetted under paragraph cc within the Banks Act 94/90

under the definition of the business of the bank. Whilst the general reference in the

Act implied that the business of securitisation was not limited to banks alone, the

definition of the originator only made reference to banks. The associated amendment

to the Banks Act under the same paragraph cc further enforced the limitation of

securitisation to banks. It stated that a finance entity other than a bank is not

permitted to issue debt instruments to fund its operations. The net result was that

securitisation had to be routed through a bank.

During the early 1990s the South African financial sector was characterised by

majority shareholders that are corporate conglomerates. This structurally resulted in

easier and greater accessibility to capital for the banks, making securitisation a less

attractive option to raise capital. The general measure for competitiveness for banks in

South Africa was relative size and headline earnings. This again discouraged the

development of securitisation, which results in a reduction of the size of the balance

30

sheet. Further the strict foreign exchange regulations restricted the outflow of

capital from South Africa with the result that the banking industry as a whole was

adequately capitalised. Securitisation was also considered as off balance sheet

financing for the bank involved, therefore attracting 100% risk weighting for

calculating capital adequacy. This provided no incentives for bank to securitise their

mortgage loan assets for example, which were risk weighted 50% on the balance sheet.

Similar to most European countries, the introduction of legislation managed to stimulate

discussions and interest in the subject in South Africa. But due to the economic

arguments presented above and the technical nature of the regulations which were

cumbersome to interpret no public transactions were completed after the introduction

of the regulations. By the end of the 1990s, SARB realised that the existing regulatory

criteria were diverging from the standardised approach being adopted by the majority

of the G10 countries. For example, an originating bank was restricted in providing

credit enhancement and liquidity facilities to securitisation schemes. In addition, the

growth in demand for credit-related instruments, particularly short-dated credit linked

notes and deposits, had led to market participants requesting regulatory action to help

increase the liquidity of the South African corporate debt market. The new capital

adequacy framework of 1999 from Basle Accord (Bank of International Settlements)

introduced a new impetus for securitisation in South Africa. Of particular interest was

the guidance on the treatment of capital relief derived from the application of

different risk weightings on rated financial assets. A working group including

interested and affected parties was established to make the necessary changes to the

existing legislation to stimulate and facilitate asset backed securitisation.

On 13 December 2001, the South African Reserve Bank ("SARB") published in the

Government Gazette (Vol. 438, No. 22948) new regulations governing securitisation in

South Africa (the "Regulations"). The Regulations were developed and agreed after a

detailed review by SARB of different international regimes, including the draft capital

adequacy proposals of the Bank of International Settlement ("BIS") in June 1999.

31

The Regulations encompass all institutions, whether or not within a banking group.

Nevertheless, where an institution, which is a member of a banking group, is involved in

a securitisation scheme, there are a number of additional rules, which apply. The main

aspects of these regulations are highlighted below:

• Provisions under which institutions within a banking group and other institutions not

within a banking group may participate in securitisation schemes are clearly outlined.

• no transactions other than transactions directly relating to the securitisation

scheme shall be entered into by, or on behalf of, the special-purpose institution.

• Conditions relating to limitation of association with assets for the originator

particularly with respect to banking institutions.

• Conditions relating to the provision of liquidity facilities and credit enhancement

facilities as well as underwriting.

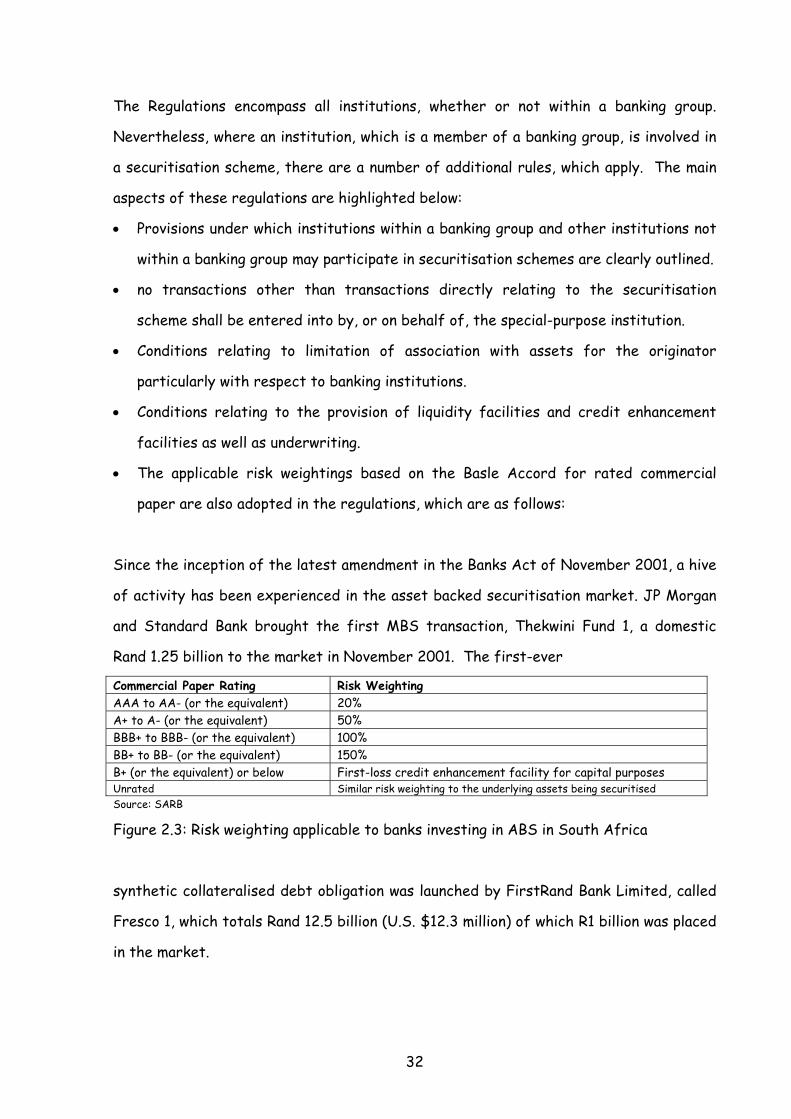

• The applicable risk weightings based on the Basle Accord for rated commercial

paper are also adopted in the regulations, which are as follows:

Since the inception of the latest amendment in the Banks Act of November 2001, a hive

of activity has been experienced in the asset backed securitisation market. JP Morgan

and Standard Bank brought the first MBS transaction, Thekwini Fund 1, a domestic

Rand 1.25 billion to the market in November 2001. The first-ever

Commercial Paper Rating Risk Weighting AAA to AA- (or the equivalent) 20% A+ to A- (or the equivalent) 50% BBB+ to BBB- (or the equivalent) 100% BB+ to BB- (or the equivalent) 150% B+ (or the equivalent) or below First-loss credit enhancement facility for capital purposes Unrated Similar risk weighting to the underlying assets being securitised Source: SARB

Figure 2.3: Risk weighting applicable to banks investing in ABS in South Africa

synthetic collateralised debt obligation was launched by FirstRand Bank Limited, called

Fresco 1, which totals Rand 12.5 billion (U.S. $12.3 million) of which R1 billion was placed

in the market.

32

The two deals took more time to complete than in other markets because they were of

the first in the jurisdiction and also because there were some issues that had not been

previously encountered in the local market. The South African asset backed

securitisation market has become very active and the volume has picked up significantly

this year. According to Fitch Ratings, there are several deals in the pipeline. "The

market in South Africa is almost exploding, from the point of view of comparing it to

some of the other markets that we work on in the emerging markets sector. It's very

busy in terms of the local participants in South Africa that are actively pursuing a

number of opportunities in their market. It's an increasing realisation by the local

participants that this is a form of funding that is available for them or in this case, an

opportunity for capital relief by the major banks." (Alex McKay, Fitch Ratings)

33

3 LEGAL,TAXATION AND ACCOUNTING FRAMEWORK

Securitisation has become an acceptable funding technique for well over a decade in the

United States and in Europe the technique has enjoyed increasing popularity since

inception and is becoming more complicated with the use of synthetic securitisations

and credit derivative arrangements. Synthetic securitisation transactions are in many

respects similar to traditional securitisation transactions without the necessity for

asset transfer through the use of credit derivatives. The capability to execute the

increasingly complex and diverse asset backed securitisation transactions require an in

depth understanding of the legal, accounting and taxation frameworks operating in

these jurisdictions. This chapter provides an outline of the necessary legal, accounting

and taxation frameworks in various nations, which facilitate the implementation of ABS

programs. Some details relating to common changes that have been implemented and

the difficulties encountered by the authorities are compared.

3.1 Legal and Taxation

From a legal perspective there are several common components which require

clarification and legal opinion prior to the execution of a securitisation transaction.

Treatment of these components which includes the method of transfer, true sale,

funding methodologies, solvency considerations, security, enforceability of securities

and documentation, as well as duties which differ between the various jurisdictions.

The main similarities and differences are discussed in turn below to highlight the

disparities between the developed and developing markets.

3.1.1 United Kingdom

3.1.1.1 Legal

The English legal system is known world over as common law. English common law

distinguishes between tangible and intangible property commonly expressed as choses in

possession and choses in action.

34

The latter are transferable only by a written conveyance. Hence, the Law of Property

Act 1925 required a written agreement to transfer actionable claims and a notice to

debtors was also required. However, traditional English law has always recognised

equitable transfers, that is, transfers that do not comply with the legal requirement of

law, but would be recognised as setting up a legal relationship between the transferor

and transferee. This means that the right of the assignee under an equitable transfer

is a right against the assignor, and not a independent right against any and all.

In almost all securitisations the legal mechanism for transferring assets varies with the

underlying asset classes and the most convenient method of achieving such transfer.

Such methods include assignment, novation, and declaration of trust, subrogation and

contractual participation. Inevitably the most appropriate method of achieving a valid

transfer will be detected by the terms of the underlying contracts which result in the

receivables being considered for securitisation. To ensure that the transfer of assets

is a valid transfer which is isolated from the credit risks of the originator it is normally

structured as a true sale which is not capable of being set aside by the insolvency

officer of the originator or by a court. In most cases a robust legal opinion, which

states that the risk is either non existence or negligible is sought.

Other legal requirements in the UK pertain to the funding method and the regulations,

which govern them. A range of funding mechanisms have been utilised which range from

bank market funding, or the use commercial paper and bond issuances including

Eurobonds. The various compliance regulations, which govern all the various funding

options, have to be complied with, to attain a structure with the least legal risk. In

addition the requirements of the regulator as discussed in Chapter 2 also need to be

legally complied with. And finally all the associated documentation and agreements

between the various parties in a securitisation transaction have to be valid and

enforceable under English law.

35

3.1.1.2 Taxation

Securitisation transactions in the UK attract stamp duty. A stamp duty of 3.5% to 4%

is payable on assignment of receivables. There is no stamp duty imposed on the sale of

mortgage receivables, but there is one on sale of non-mortgage receivables.

Generally parties to a securitisation get around this additional cost by executing

documents outside the jurisdiction, as the duty is payable at the place where the

agreement is executed. However, there is a common stamp law provision that if an

agreement executed outside the country but relating to property in the country comes

to the country after execution, it will be stampable then. Thus, execution of the

agreement outside the country defers the stamp duty implication till it is necessary to

bring the document into the country for the purpose of enforcement.

A transfer within the group can also obtain stamp duty relief, that is, by establishing

the SPV as a subsidiary of the originator. In UK practice, however, stamp duty is not

paid, as most securitization transactions are structured as equitable assignments and

not perfected legal transferes. When the transaction were to be perfected into a full

fledged sale of receivables, the document will attract stamp duty: therefore, the

originator is required to provide for full payment of duty. But this is usually regarded as

a theoretical tax - very rarely have circumstances arisen where the duty has actually

become payable.

As far as withholding tax on interest is concerned, the payer of interest is required to

withhold tax at the basic rate, unless the lender is a bank. Since securitisation SPVs are

not banks, transfer of loans to SPVs surely gives rise to the problem of withholding tax.

To get around these onerous withholding taxes a number of securitisation transactions

are structured as "participation" transfers, rather than true sales.

Value Added Tax is not applicable on sale of receivables in the UK.

36

There are no pre-defined income-tax rules on securitization in the UK but the tax

treatment is understood with reference to general tax law and practice. The basic

question to be decided for the originator is whether the disposition of the receivables

will be taken as a sale or financing. The question would, in most cases, be decided by

reference to the originator's accounting treatment. If the assets in question are

business assets, and they are being transferred, business profits/loss may arise. In

certain cases, the asset being transferred may be held as capital assets - for example,

in case of lease transactions. Ideally, in such cases, the physical asset and the

receivables therefrom should be split, and the receivables should only be transferred

rather than the physical asset. The other significant tax issue for the originator is the

deductibility of the initial fees of the issue. Incidental costs of raising finance may, if

properly structured, be deductible by the issuer under the FA 1996 rules. Accounting

Standard FRS4 will generally require issue costs, and thus the tax deductions, to be

amortised over the period of the notes.

An investor's UK tax position will be reasonably straightforward. Notes will generally

fall within the withholding tax exemption for quoted Eurobonds. In general, it is

believed that the accounting method employed by the investor for books will be adopted

for taxation too.

It is important that the SPV tax status is neutral. This can be achieved by matching

incomes and expenses. The payments made by the SPV will be principal and interest on

the bonds, of which interest will be tax deductible - principal will not be. Interest paid

by the SPV on a participating loan, that is, a loan with a right to participate in profits

(normally given by the originator as his contribution-credit enhancement) is not tax

deductible. Such interest is also not taxable in the hands of the originator.

37

3.1.2 The French Credit Foncier de France (“FCC”) The French legal process to facilitate the conduct of securitisations is the FCC. The

creation and operation of an FCC requires the participation of (i) investors (ii) a bank or

financial institution where the funds of the FCC will be deposited and (iii) a management

company to conduct the investment policy of the FCC. The FCC is a legal concept, not a

legal entity. With this system assets of FCC are regarded as the joint ownership of the

investors. Interest in an FCC, that is, the interest held by the investors, is itself a

transferable property. The activities of the FCC must consist exclusively of the co-

ownership of receivables and not of other types of securities such as shares. The

transfer mechanism provided for in the securitization law is inspired by the Loi Dailly

mechanism. Title to the receivables is transferred by the execution and dating of a

certain instrument, called bordereau.

3.1.3 Australia

As in other jurisdictions the law plays a vital role in the structure and regulation of

many securitisation programs that have been implemented in Australia. In the

Australian market both equity and debt securities are issued in lieu of asset backed

securitisations. However due to prohibitive stamp duty requirements on equities the

debt instruments are more popular. The main difference between the issuance of notes

in Australia compared to the rest of the world is that asset backed securities are

issued by the trustees as opposed to SPV’s. The trustee holds the securitised assets

on trust and the liabilities under the notes are limited to the proceeds from the

underlying assets that are available. The use of trusts to issue debt securities

introduces a series of unique trust issues, which include the roles of the trustees and

the indemnities, and liabilities that affect the trustees. Further the Australian

Corporations Law regulates all asset backed securities issued to the extent that they

are debentures, or an interest in a managed investment scheme.

38

It is an obligation of the Corporations Law to ensure that prospectus that are used to

canvass investments make a minimum set of positive disclosures and outlines the civil

liabilities associated with breach of these provisions.

Securitization SPVs will be taxed as per the general law applicable to taxation of

companies or trusts, whichever way the SPV is organised. If organized as trusts, the

trust can qualify for taxation a "flow through" vehicle, that is, as a pass through or tax

transparent entity provided all the unitholders are currently entitled to the entire

income of the trust. That is to say, if the trust is non-discretionary as to its income, it

will be a tax transparent entity. If the trustees have discretion as accumulation of the

income or reinvestment of cashflows, the trust will be liable to normal income tax

principles.

3.1.4 Hong Kong

Hong Kong is one of the most securitization-friendly jurisdictions in Asia. The legal

system is based in general terms on English Law. This makes it quite straightforward to

structure "true sale" transactions from a legal, regulatory and accounting perspective.

The legal framework, in particular bankruptcy law, is well developed, with a mixture of

legislation and case law. Most securitisation transactions in Hong Kong follow the

"equitable assignment" route, without giving a notice to the obligors. Registration of

equitable assignments is not insisted upon. However, transfer of mortgages would

require registration with the Land Registry offices.

Unlike other Asian countries in Hong Kong there is no withholding tax on interest

payments to a non-resident, making the securitization offshore of interest-bearing

receivables much simpler. Stamp duties, which are generally required in other

countries, are not applicable on equitable assignments. However, transfer of mortgages

would be treated as transfer of interests in land, and would attract duty of 2.75%.

Hong Kong does not have any Value-added tax.

39

3.1.5 Malaysia

The Malaysian legal system is partly based on Roman Dutch law and partly on English

common law. Sec. 4 (3) of Malaysian Civil Law Act, 1956 requires that the assignment of

a debt be notified to the debtor. This requirement generally acts as a hindrance to

execution of securitisation transactions and discourages originators from participating

since it is very onerous and usually not cost effective. An alternative based on the

British concept of equitable assignment has been introduced in Malaysia. (Assignment

of receivables, that is, transfer of a debt, can either be full fledged legal transfer or

can be a transfer not documented as a legal transfer but recognised by courts as an

effective transfer for purposes of enforcement. "Equity" means fairness, that is, to

meet the ends of justice. In English law, there were separate courts of Equity, which

would deal with equitable claims. In the Malaysian legal system, equity courts do not

exist: yet, courts do follow principles of equity to enforce claims, which are otherwise

not contractually enforceable.)

The Malaysian companies law contains provisions for avoiding a transfer made in

contemplation of bankruptcy. This, however, can be resolved by establishing that the

transfer took place at fair values. In case of an offshore SPV, numerous exchange

control issues will also arise - the Malaysian Exchange Control Act 1953 will be

applicable.

There was a stamp duty implication of 4% on transfer of receivables. In an attempt to

encourage securitisation transactions and to develop the corporate debt capital

markets Stamp duty has been abolished. For property transactions capital gains tax on

transfer of assets, has also been exempted in case of SPVs. To qualify for exemption

the SPV require exemption from the Securities Commission.

40

There are no specific provisions in the income-tax law on securitisation. Pass through

SPVs are expected to be tax exempt based on conduit rules, but other securitization

SPVs are likely to come for entity-level taxation. Malaysia currently does not have any

tax on capital gains. Hence, if the sale of receivables or assets by the originator can

qualify for a capital gains treatment, it can escape upfront taxation of profits on

securitization.

A withholding tax of 15% is applicable on interest payments to non-resident persons.

Normal practice for Malaysia is to incorporate the SPV in Labuan, an offshore financial

centre, in which case the withholding tax is not applicable.

3.1.6 South Africa

3.1.6.1 Legal

The legal system in South Africa is mainly based on Roman Dutch law with large

influences from the English common law. Aspects of the law that are generally taken

into consideration when concluding a transaction in South Africa include incorporation,

validity and enforceability of documentation, transfer and security, and restrictions..

It is essential to ensure that the SPV issuing asset backed securities is a company that

has been duly incorporated and validly existing under the laws of South Africa. And to

the extent that it is owned by a trust that such trust(s) are also legally incorporated.

The company and all other parties should also have the legal capacity and corporate

power to perform the functions required to execute its obligations under the

agreements.

41

There are no governmental or regulatory consents, approvals, authorisations or orders

required in the Republic of South Africa by the Issuer or registration, filing or similar

formalities in connection with the issue of asset backed securities to ensure the

legality, validity or enforceability with the exception of the following;

• the approval of the listing of the asset backed securities by the Bond

Exchange of South Africa ("BESA") for listed securities. BESA should also

make an application to the Financial Services Board ("FSB") for the Notes to

be declared a financial instrument by notice in the Government Gazette by

the FSB in terms of the definition of "financial instrument" in the Financial

Markets Control Act, 1989 ("FMCA"). The instruments should then be

included in the list of financial instruments, which may be dealt in on BESA.

• approval of the Offering Circular by the Central Depository Limited; and

• the lodging with the Registrar of Companies in terms of the Companies Act,

of the Subscription Agreement by the placement agents who are usually the

arranging banks.

Under South African law, in order to sell a personal right, the seller and the purchaser

must enter into an agreement of sale (the obligatory agreement) in terms of which the

identity of the parties, the personal right to be sold and the price at which it is to be

sold are agreed. In order for the seller to transfer ownership of the personal right to

the purchaser, the parties must have the intention to transfer ownership coupled with

delivery of the personal right. A personal right is delivered by way of cession and the

seller and the purchaser can thus give effect to the transfer of ownership by an

agreement of cession (the transfer agreement) between the transferor (the cedent)

and the transferee (cessionary). The consequence of a valid sale and cession by the

seller of the receivables is that such seller is divested of its right to payment (and all

other rights), which will vest in the purchaser (SPV). A creditor of the seller can no

longer attach the right and, the subsequent liquidation of the seller will not affect the

situation.

42

A creditor of the relevant seller would only be able successfully to challenge the sale

and cession if any of the following apply;

• where the person granting the security ("the debtor") (such as a surety,

insurance company, guarantor or mortgagor) and the creditor have agreed

that the latter may not cede or transfer the right then, if this agreement

forms an integral part of the agreement creating the right, South African

law may treat the right as inherently limited and incapable of transfer

without the express consent of the debtor;

• under common law restrictions a transfer will be unenforceable to the extent

that it weakens the debtor's position or renders it more onerous than it was

prior to the cession. For this reason, in general a transfer of a portion of a

debt is invalid except with the consent of the debtor;

• where a debtor and a creditor have agreed that a debt can be transferred

only if certain formalities are complied with, a transfer effected in defiance

of these agreed formalities will be legally ineffectual unless the formalities

are waived by the party in whose favour they are stipulated (usually the

debtor);

• where the contract creating the right is of an intensely personal nature (in

the sense that whether the transferor or, alternatively, the transferee

exercises the right makes a reasonable or substantial difference to the

debtor's position) the rights may not be transferred (for instance, an

employment or partnership contract);

• statutory restrictions prohibiting the transfer of incorporeal rights include

the Insolvency Act, 1936 ('the Insolvency Act") (for instance, an insolvent’s

rights to his earnings cannot be transferred), the Statutory Pensions

Protection Act, 1962 (a pensioner’s right to his pension may not be