The FAST-REFERENCE PROBLEM SOLVER for EXECUTIVES and ACCOUNTANTS Steven M. Bragg Includes: ■ Capital budgeting techniques ■ Foreign exchange risk management ■ Essential GAAP ■ Working capital management techniques ■ Stock registration alternatives ■ Key performance metrics THE VEST POCKET Controller VEST POCKET Controller

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

The all-new fast-reference problem solver

Accounting

T he Vest Pocket Controller is the handy pocket pr oblem solver that gives today’s busy executives and accountants the helpful

information they need in a quick-r eference format.

Whether in public practice or priv ate industr y, professionals will always have this reliable reference tool at their fingertips because it easily goes anywhere—to a client ’s office, on a business trip , or to an important lunch meeting.

Providing concise answ ers to the questions y ou ar e most likely to encounter during a typical business day , The V est Pocket Controller covers:

• The most heavily used GAAP accounting standar ds• The management areas a controller is likely to encounter• A variety of financial analysis topics with a par ticular focus on bottleneck analysis

• Metrics a controller is most likely to need, along with helpful examples

• The primary control systems you need to ensure your transactions are as error-free as possible

• How to analyze capital budgeting proposals so that only truly necessary assets are acquired

Packed with practical techniques and rules of thumb for analyzing, evaluating, and solving the day-to-day pr oblems ev ery contr oller faces, The Vest Pocket Controller helps y ou quickly pinpoint what to look for, what to watch out for , what to do, and ho w to do it. Its easy-to-use Q & A format offers hundr eds of explanations sup-ported by a multitude of examples, tables, char ts, and ratios.

Convenient and compr ehensive, The Vest P ocket Contr oller is a powerful companion for the ever-changing world of the controller.

STEVEN M. BRA GG, CPA, has been the chief financial officer or controller of four companies, as w ell as a consulting manager at E rnst & Young and auditor at D eloitte. H e is the author of over thir ty books primarily targeted to ward controllers and their needs. B ragg r eceived a master ’s degr ee in finance fr om Bentley College, an MBA from Babson College, and a bachelor ’s degree in economics from the University of Maine.

The FAST-REFERENCE PROBLEM SOLVER for EXECUTIVES and ACCOUNTANTS

Steven M. Bragg

Includes:■ Capital budgeting techniques■ Foreign exchange risk management■ Essential GAAP■ Working capital management techniques■ Stock registration alternatives■ Key performance metrics

THEVESTPOCKET

Controller

PMS 279 PMS 2623 GLOSSY

THE VEST POCKET Controller

Bragg

$29.95 USA/$35.95 CAN

E1BINDEX 03/10/2010 Page 418

E1FFIRS 03/04/2010 Page 1

Additional Praise for The Vest Pocket Controller

``The Vest Pocket Controller presents the accounting com-munity with a fantastic resource that provides relevantand concise guidance. The question-and-answer formatallows the reader the opportunity to find the answer andreview the accounting treatment with some additionalinsight and commentary. The Vest Pocket Controller is anindispensable guide for all accountants.''

—Josh Nowack, CPA, MBA, Nowack StrategicBusiness Advisory & CPA

``The Vest Pocket Controller provides important informa-tion in an easy-to-use format. This book should be re-quired reading for anyone in an accounting or financerole as it is a resource that will be referenced time andagain. Since reading the book for the first time, I find my-self referring to its content on a regular basis. Not onlywill you find The Vest Pocket Controller in my vest pocket,but I will also be giving it to everyone in my accountingdepartment.

—Steven Randall, Managing Partner, Vonya Global LLC

``This book is a quick reference guide for a controller. Itprovides clear and concise answers with explanations tothe various questions a controller may have in his day-to-day operations, with plenty of examples. A valuable addi-tion to any controller’s library.''

—Priya K Srinvasan, Owner, Priya K Srinivasan CPA

``The Vest Pocket Controller is a comprehensive, incrediblywell-organized reference for controllers and accountingprofessionals alike complete with real-world scenariosand easy-to-follow journal entries. Once again, StevenBragg has put together a must-have accounting ‘cheatsheet’ for CPAs, accountants, and all level of financeprofessionals.''

—Adrienne Gonzalez, Founding Editor,JrDeputyAccountant.com

``Steve provides a clear and effective guide for readersfrom accountants to financial managers. This book coverskey topics concisely and clearly and earns a place as a keyreference book.''

—Paul Apodaca, Principal at Apodaca Consultingand Finance Manager, WONIK Quartz International

E1FFIRS 03/04/2010 Page 2

E1FFIRS 03/04/2010 Page 3

TheVestPocketController

E1FFIRS 03/04/2010 Page 4

E1FFIRS 03/04/2010 Page 5

THEVESTPOCKETCONTROLLER

Steven M. Bragg

John Wiley & Sons, Inc.

E1FFIRS 03/04/2010 Page 6

Copyright# 2010 by John Wiley & Sons, Inc. All rights reserved.

Published by John Wiley & Sons, Inc., Hoboken, New Jersey.

Published simultaneously in Canada.

No part of this publication may be reproduced, stored in a retrievalsystem, or transmitted in any form or by any means, electronic,mechanical, photocopying, recording, scanning, or otherwise, except aspermitted under Section 107 or 108 of the 1976 United States CopyrightAct, without either the prior written permission of the Publisher, orauthorization through payment of the appropriate per-copy fee to theCopyright Clearance Center, Inc., 222 Rosewood Drive, Danvers, MA01923, (978) 750-8400, fax (978) 646-8600, or on the web at www.copyright.com. Requests to the Publisher for permission should be addressed to thePermissions Department, John Wiley & Sons, Inc., 111 River Street,Hoboken, NJ 07030, (201) 748-6011, fax (201) 748-6008, or online at www.wiley.com/go/permissions.

Limit of Liability/Disclaimer of Warranty: While the publisher and authorhave used their best efforts in preparing this book, they make norepresentations or warranties with respect to the accuracy or completenessof the contents of this book and specifically disclaim any impliedwarranties of merchantability or fitness for a particular purpose. Nowarranty may be created or extended by sales representatives or writtensales materials. The advice and strategies contained herein may not besuitable for your situation. You should consult with a professional whereappropriate. Neither the publisher nor author shall be liable for any loss ofprofit or any other commercial damages, including but not limited tospecial, incidental, consequential, or other damages.

For general information on our other products and services or for technicalsupport, please contact our Customer Care Department within the UnitedStates at (800) 762-2974, outside the United States at (317) 572-3993 or fax(317) 572-4002.

Wiley also publishes its books in a variety of electronic formats. Somecontent that appears in print may not be available in electronic books. Formore information about Wiley products, visit our web site atwww.wiley.com.

Library of Congress Cataloging-in-Publication DataBragg, Steven M.

The vest pocket controller/Steven M. Bragg.p. cm.

Includes index.ISBN 978-0-470-59373-8 (pbk.)

1. Managerial accounting. 2. Corporations–Accounting.3. Accounting. I. Title.HF5657.4.B723 2010658.15'11–dc22

2009051056

Printed in the United States of America

10 9 8 7 6 5 4 3 2 1

E1FTOC 03/10/2010 Page 7

CONTENTS

Preface xxv

About the Author xxvii

PART I ACCOUNTING STANDARDS 1

One Revenue Recognition 3

When Can I Report Revenue atGross Instead of Net? � 3

How Does the InstallmentMethod Work? � 4

Can I Recognize Revenue WhenThere Is a Right of Return? � 5

When Can I Record Bill-and-HoldSales? � 5

How Does the Percentage-of-Completion Method Work? � 6

How Does the Completed-ContractMethod Work? � 6

What Types of PricingArrangements Are Usedin Contracts? � 7

How Do I Account for ContractLosses? � 10

How Do I Account for AdditionalClaims under a Contract? � 11

How Does the DepositMethod Work? � 11

How Do I Account forInstallation Fees? � 13

What Recognition MethodsCan I Use for ServiceBillings? � 15

How Do I Record Revenue forFranchise Sales? � 17

vii

E1FTOC 03/10/2010 Page 8

Two Investment Accounting 19

Which Securities Are Designatedas Marketable EquitySecurities? � 19

What Is the Accounting forMarketable Equity Securities? � 19

What Is the Accounting for Transfersbetween Available-for-Sale andTrading Investments? � 22

What Is the Accounting forInvestments in Debt Securities? � 24

What Is the Accounting for DebtSecurities among Portfolios? � 25

How Are Deferred Tax EffectsRecognized for Changes inInvestment Valuation? � 26

What Is the Accounting for SignificantEquity Investments? � 26

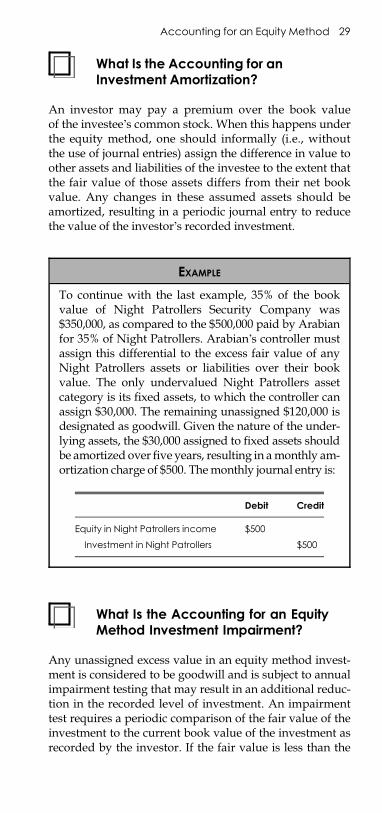

What Is the Accounting for anInvestment Amortization? � 29

What Is the Accounting for anEquity Method InvestmentImpairment? � 29

When Is the Equity MethodNo Longer Used? � 30

What Are the Key Decisions forRecording Gains or Losseson Securities? � 30

Three Inventory Accounting 33

How Do I Account for Goodsin Transit? � 33

How Does Inventory OwnershipVary under Different DeliverySituations? � 33

How Do I Account for ConsignedInventory? � 34

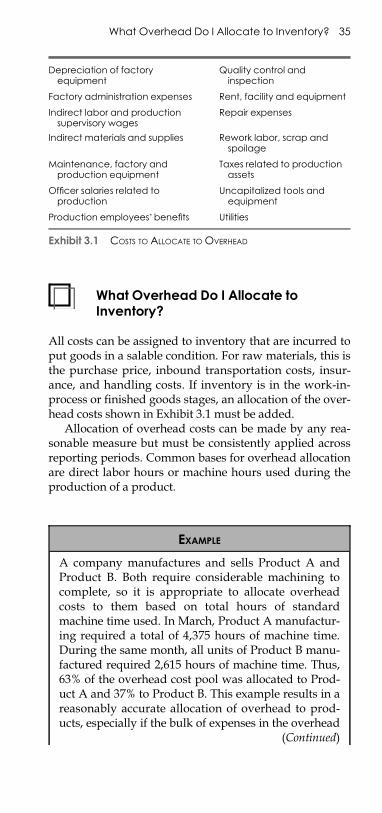

What Overhead Do I Allocateto Inventory? � 35

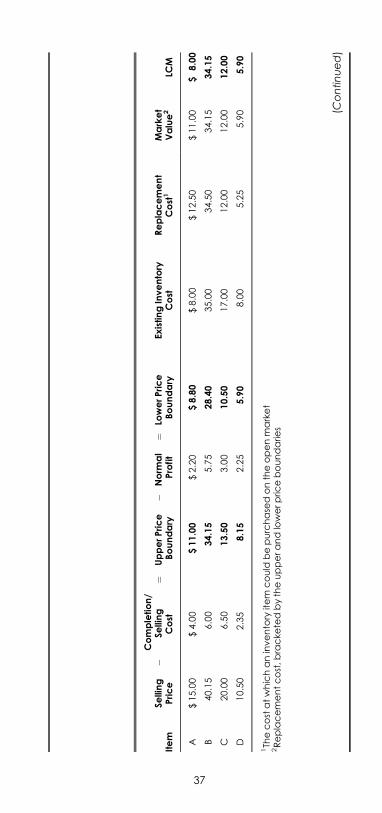

How Do I Account for the Lowerof Cost or Market Rule? � 36

How Does the First-in, First-outValuation Method Work? � 38

viii Contents

E1FTOC 03/10/2010 Page 9

What Are the Advantagesand Disadvantages of FIFOValuation? � 40

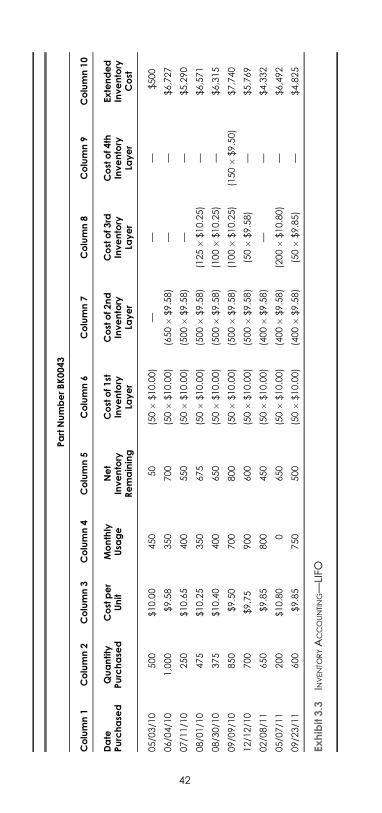

How Does the Last-in, First-outValuation Method Work? � 41

What Are the Advantages andDisadvantages of LIFOValuation? � 43

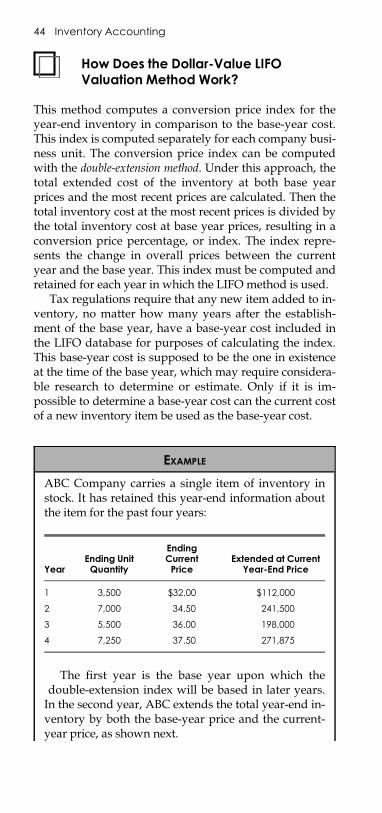

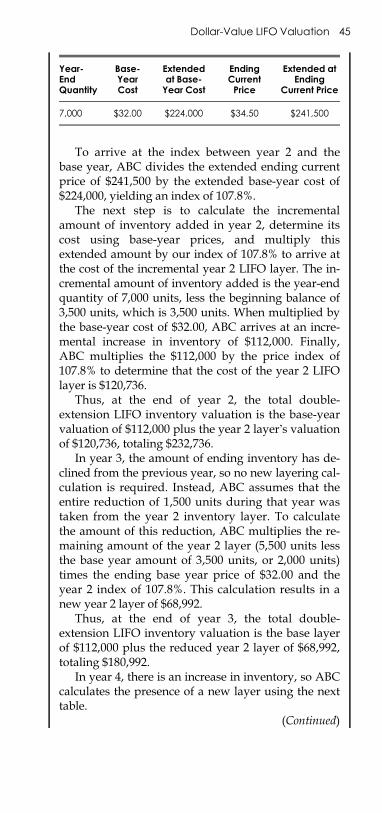

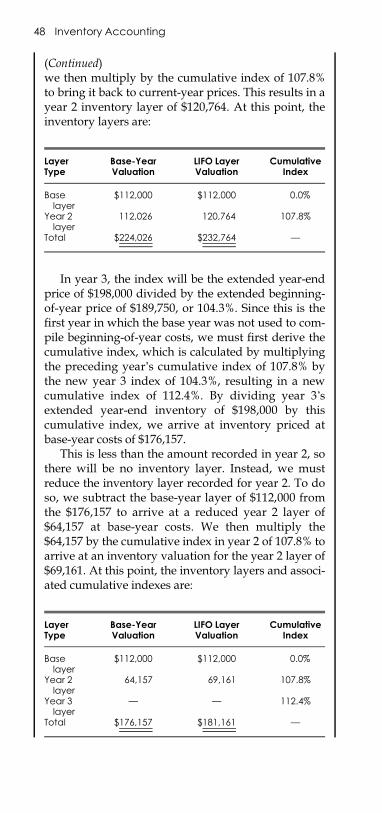

How Does the Dollar-Value LIFOValuation Method Work? � 44

How Does the Link-ChainValuation Method Work? � 46

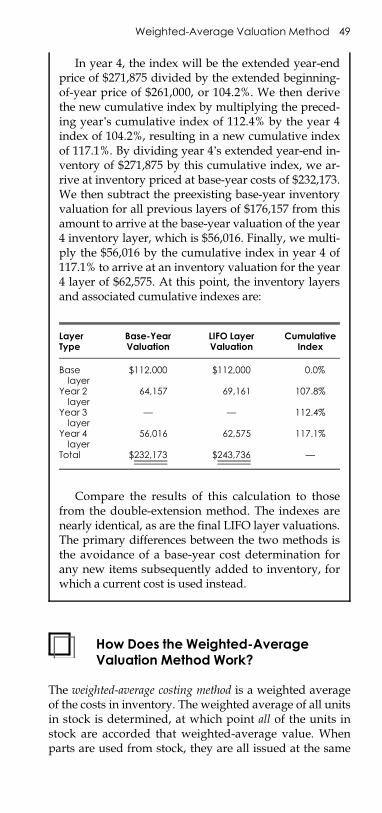

How Does the Weighted-AverageValuation Method Work? � 49

Four Fixed Asset Accounting 53

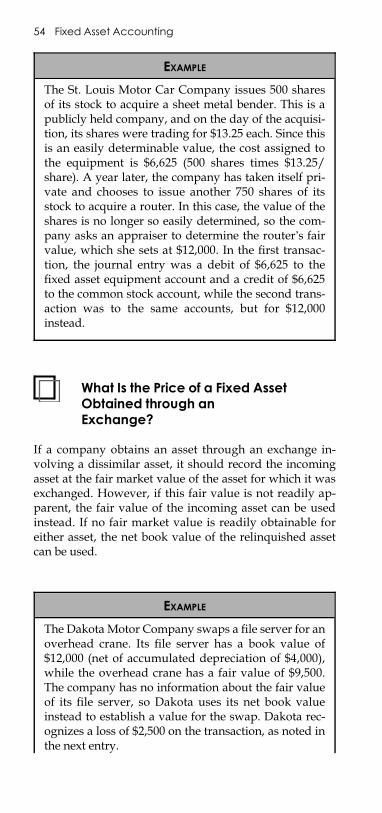

What Is Included in the CapitalizedCost of a Fixed Asset? � 53

What Is the Price of a PurchasedFixed Asset? � 53

What Is the Price of a FixedAsset Obtained through anExchange? � 54

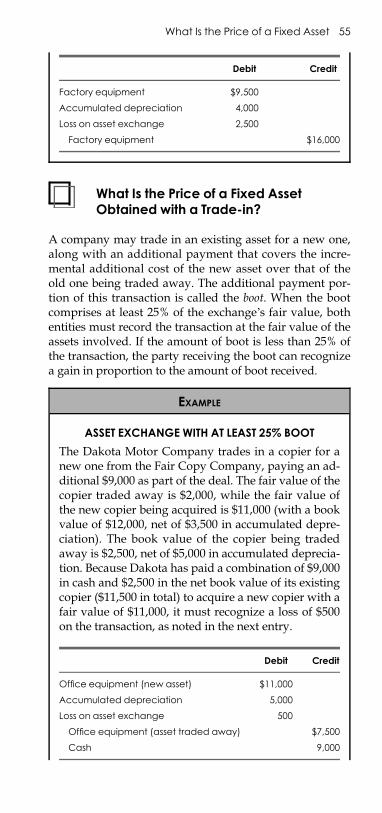

What Is the Price of a Fixed AssetObtained with a Trade-in? � 55

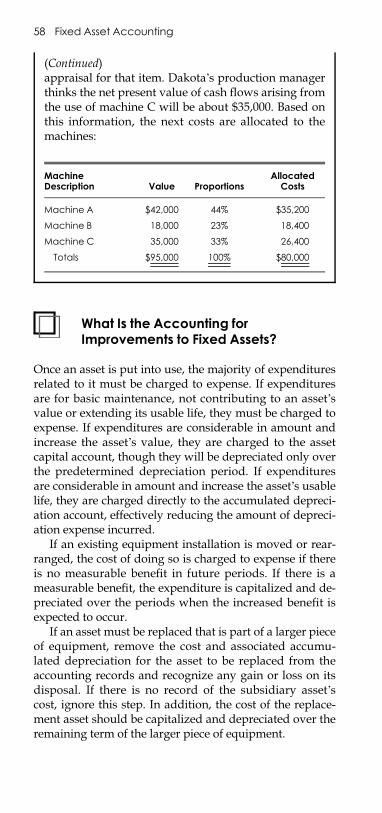

What Is the Price of a Group ofFixed Assets? � 57

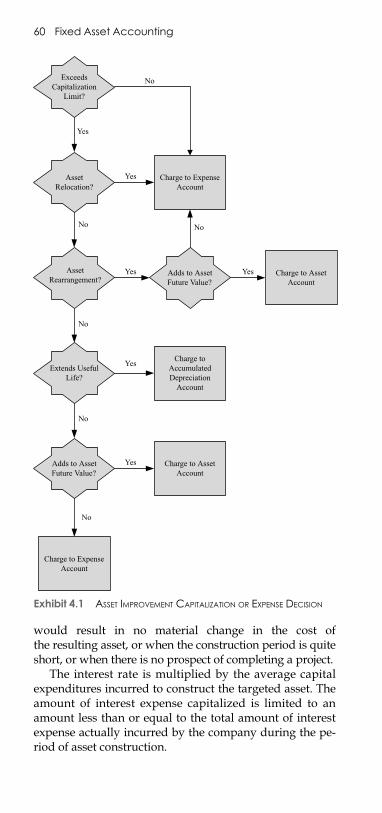

What Is the Accounting forImprovements to FixedAssets? � 58

How Is Interest Associated witha Fixed Asset Capitalized? � 59

What Is the Accounting for a FixedAsset Disposition? � 61

What Is the Accounting for an AssetRetirement Obligation? � 62

What Is the Accounting forDonated Assets? � 64

What Is the Accounting forConstruction in Progress? � 65

What Is the Accounting for Land? � 66What Is the Accounting for Leasehold

Improvements? � 66

Contents ix

E1FTOC 03/10/2010 Page 10

How Is an Asset’s Depreciation BasisCalculated? � 66

What Are the General DepreciationConcepts? � 67

How Is Straight-Line DepreciationCalculated? � 68

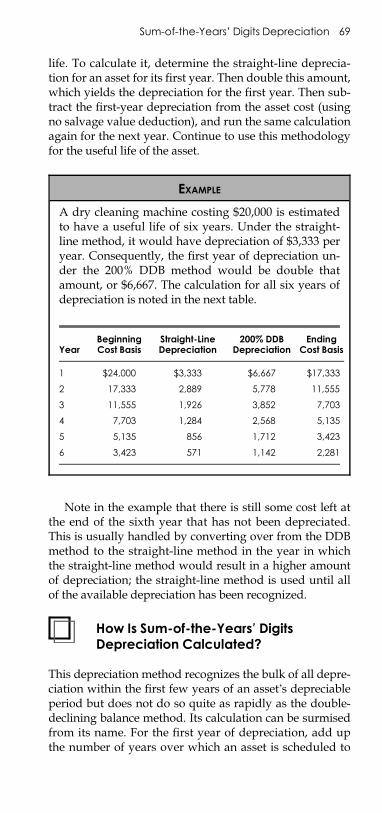

How Is Double-Declining BalanceDepreciation Calculated? � 68

How Is Sum-of-the-Years’ DigitsDepreciation Calculated? � 69

How Is Units-of-ProductionDepreciation Calculated? � 70

What Is the Accounting forAsset Impairment? � 71

What Is the Accounting forIntangible Assets? � 72

Five Debt Accounting 75

When Is Debt Categorized asShort-Term or Long-Term? � 75

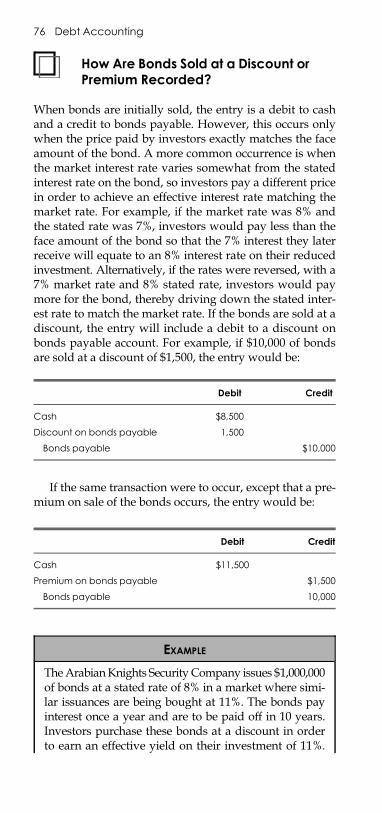

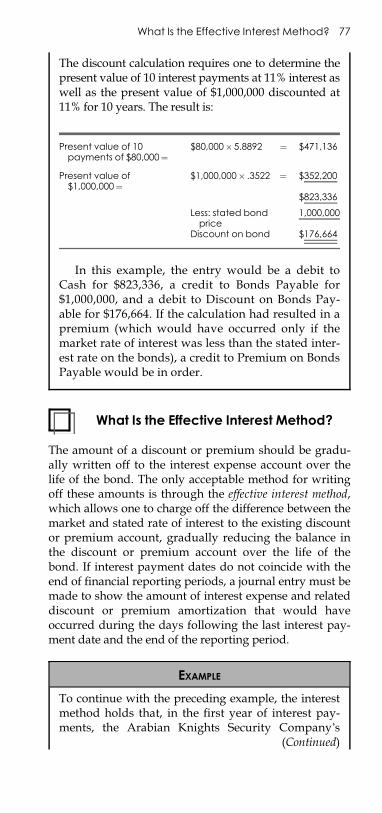

How Are Bonds Sold at a Discountor Premiu1m Recorded? � 76

What Is the EffectiveInterest Method? � 77

How Is Debt Issued with No StatedInterest Rate Recorded? � 79

How Are Debt Issuance CostsRecorded? � 79

How Is a Debt Issuance withAttached Rights Recorded? � 80

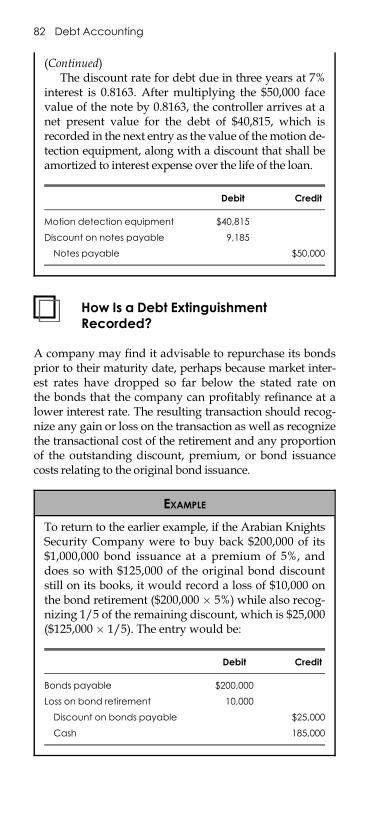

How Is a Debt Issuance forProperty Recorded? � 81

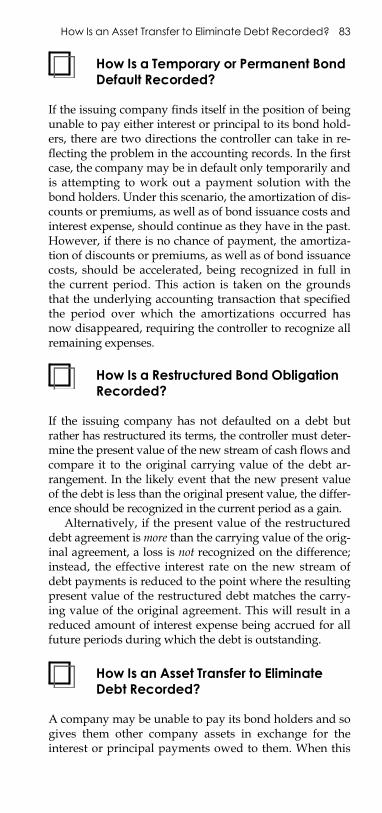

How Is a Debt ExtinguishmentRecorded? � 82

How Is a Temporary or PermanentBond Default Recorded? � 83

How Is a Restructured BondObligation Recorded? � 83

How Is an Asset Transfer to EliminateDebt Recorded? � 83

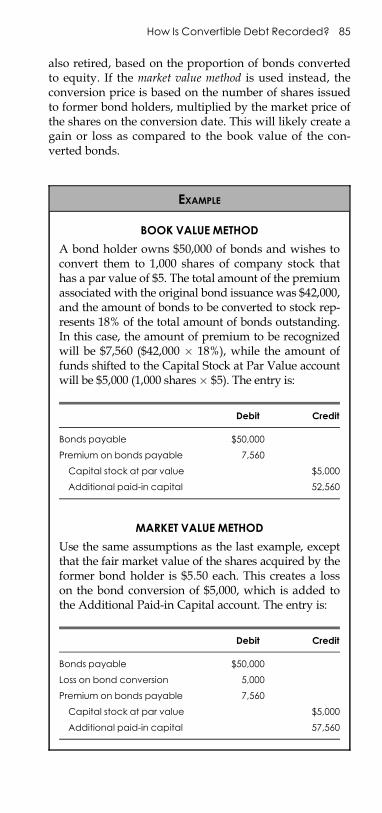

How Is Convertible DebtRecorded? � 84

x Contents

E1FTOC 03/10/2010 Page 11

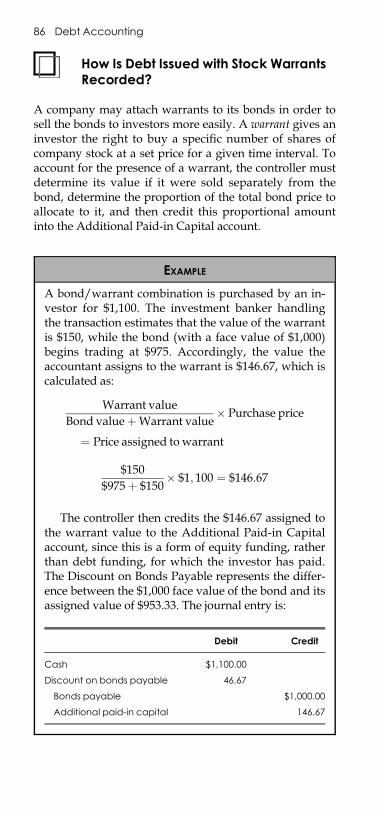

How Is Debt Issued with StockWarrants Recorded? � 86

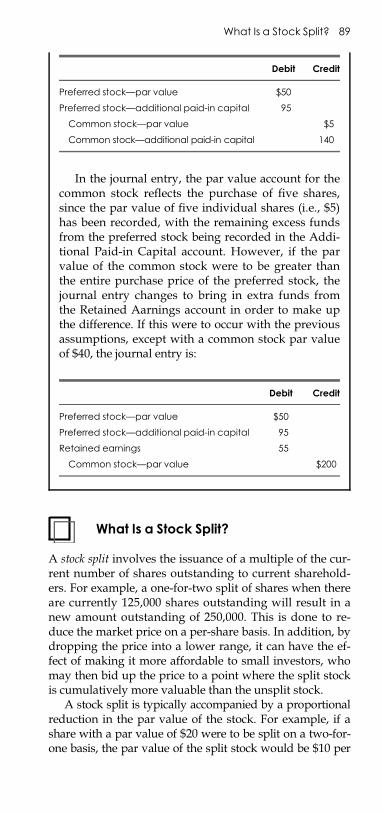

Six Stockholders' Equity 87

What Is Par Value? � 87How Is Stock Valued that Is Issued

for Property or Services? � 87What Are the Characteristics of

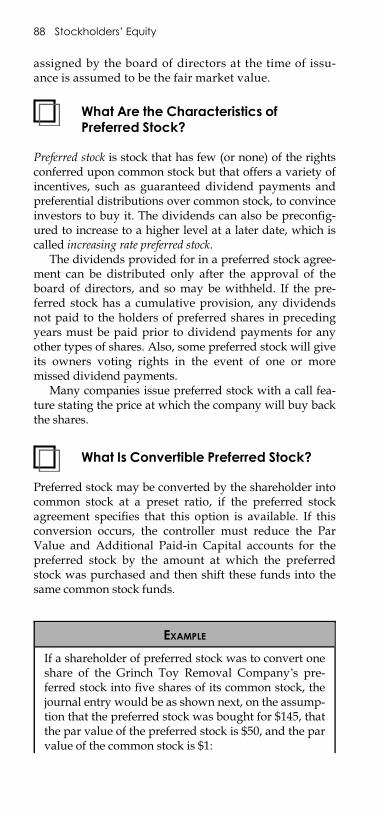

Preferred Stock? � 88What Is Convertible Preferred

Stock? � 88What Is a Stock Split? � 89What Is a Stock Subscription? � 90What Is Retained Earnings? � 91What Is a Stock Warrant? � 92What Are the Key Dates

Associated with Dividends? � 93What Is a Property Dividend? � 93What Is a Stock Dividend? � 94What Is a Liquidating

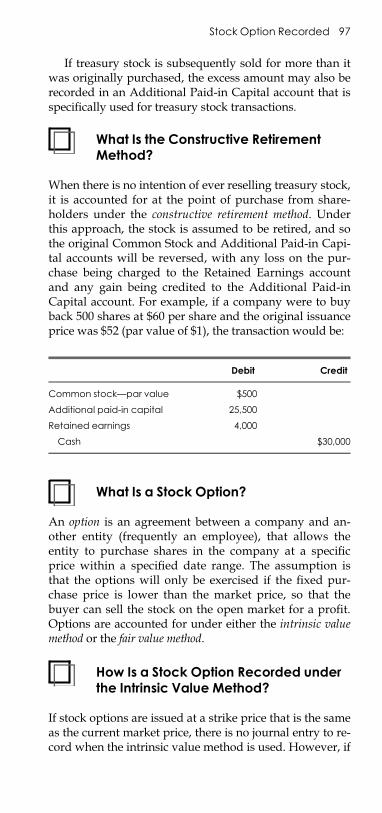

Dividend? � 95What Is Treasury Stock? � 96What Is the Constructive

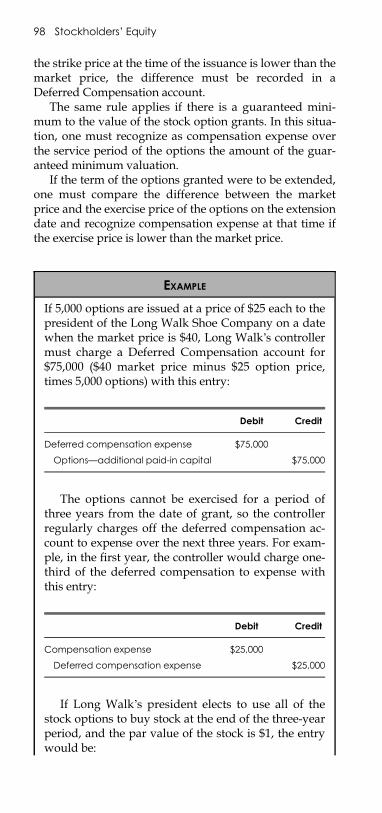

Retirement Method? � 97What Is a Stock Option? � 97How Is a Stock Option Recorded

under the Intrinsic ValueMethod? � 97

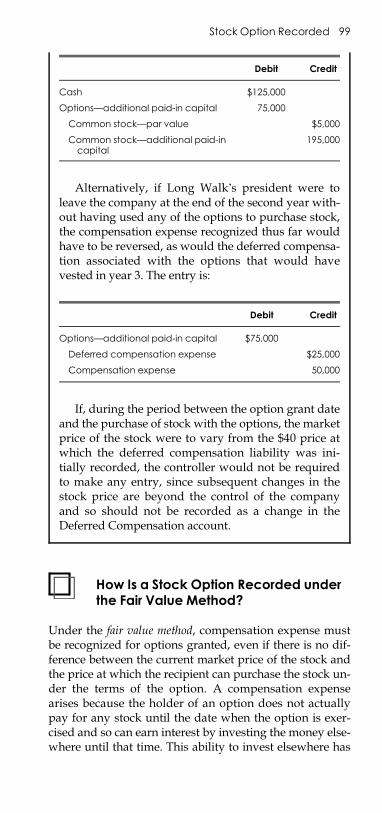

How Is a Stock Option Recordedunder the Fair Value Method? � 99

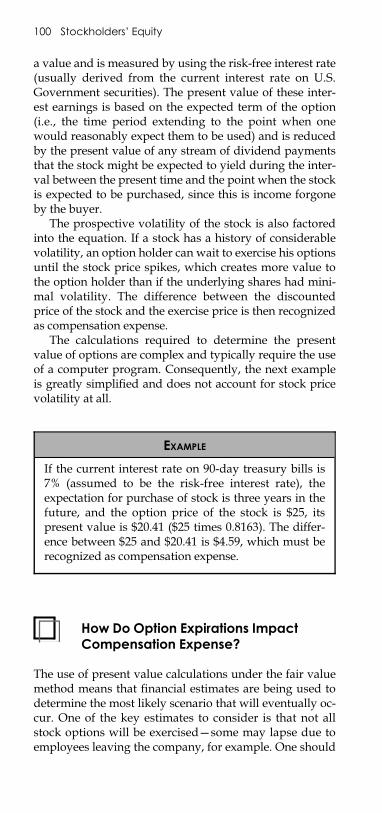

How Do Option Expirations ImpactCompensation Expense? � 100

What Happens When an OptionExpires? � 101

What Happens if the CompanyBuys Options from the OptionHolder? � 101

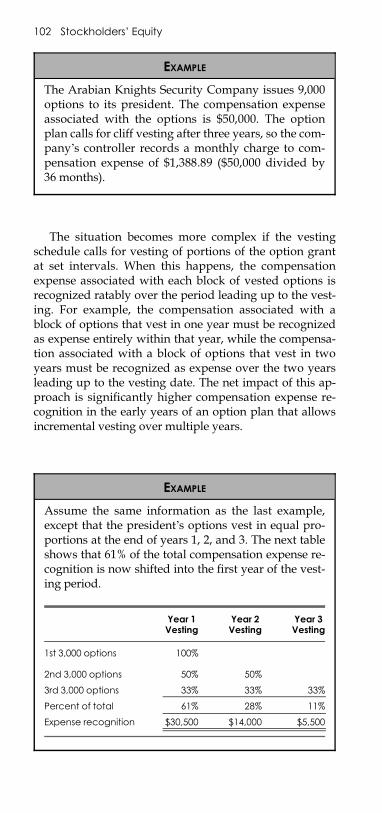

How Is the Option Vesting PeriodRecognized? � 101

What Are Stock AppreciationRights? � 103

Contents xi

E1FTOC 03/10/2010 Page 12

How Do I Account for StockAppreciation Rights? � 103

How Does an Employee StockOwnership Plan Work? � 104

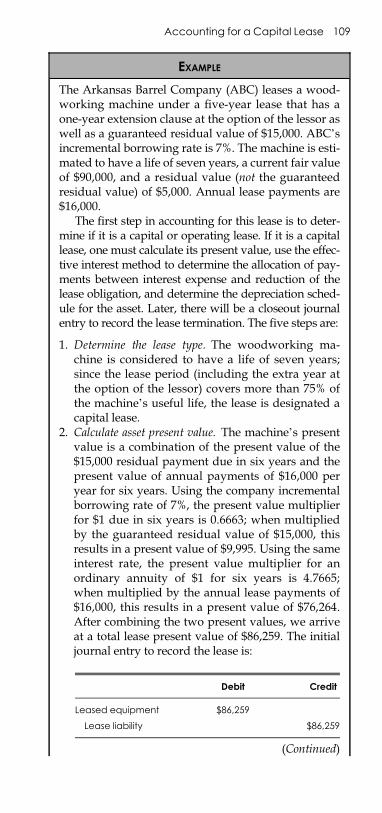

Seven Lease Accounting 107

What Is the Accounting foran Operating Lease by theLessee? � 107

What Is the Accounting for aCapital Lease by theLessee? � 108

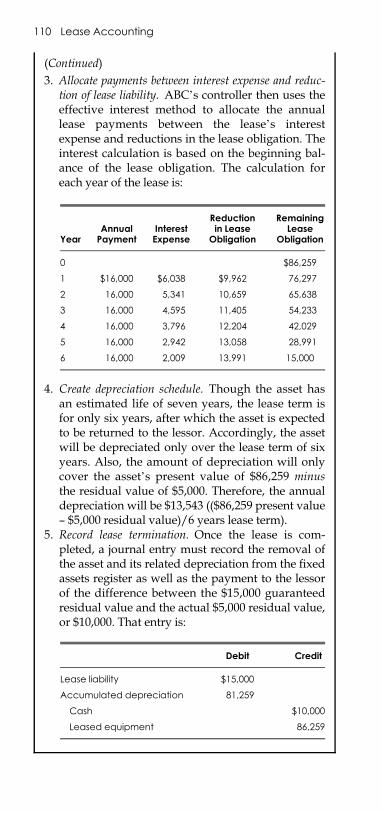

How Does the Lessor Accountfor an Operating Lease? � 111

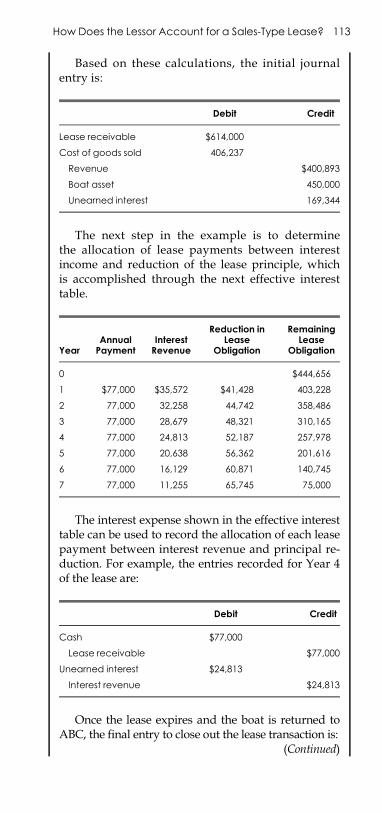

How Does the Lessor Accountfor a Sales-Type Lease? � 111

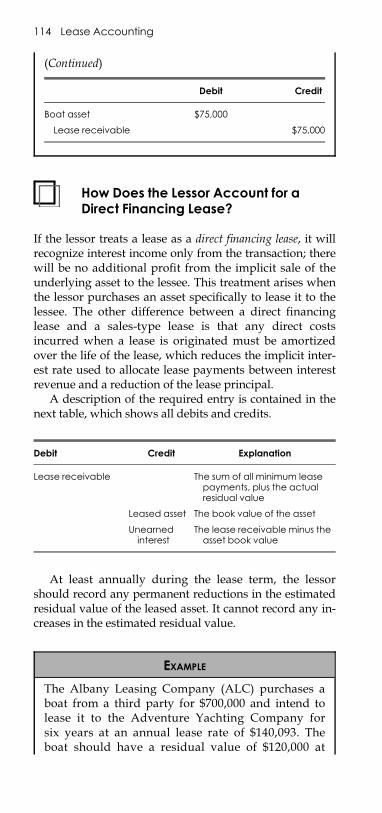

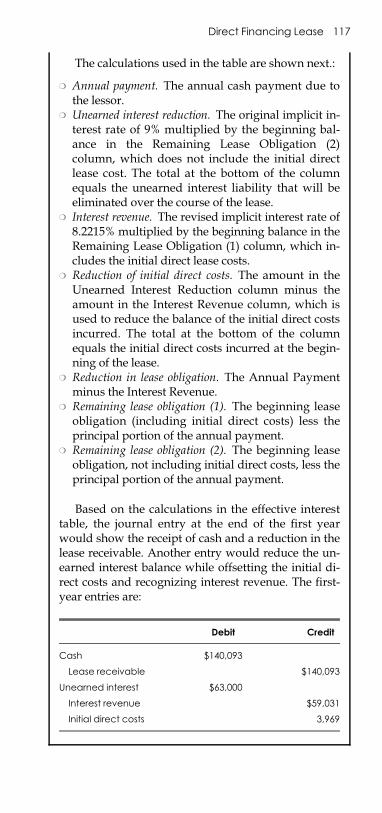

How Does the Lessor Account fora Direct Financing Lease? � 114

What Is the Accounting for aLease Termination? � 118

What Is the Accounting for a LeaseExtension by the Lessee? � 118

What Is the Accounting for a LeaseExtension by the Lessor? � 119

What Is the Accounting for aSublease? � 119

What Is the Accounting for a Sale-Leaseback Transaction? � 119

Eight Foreign Currency Accounting 121

What Is the Goal of ForeignCurrency Accounting? � 121

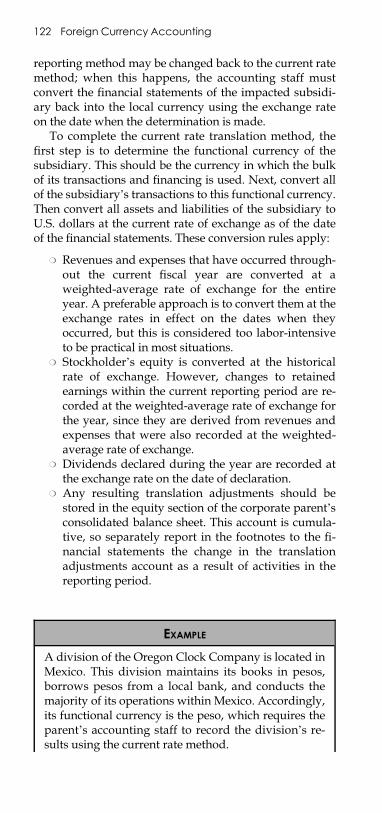

How Does the Current RateMethod Convert ForeignCurrency Transactions intoU.S. Dollars? � 121

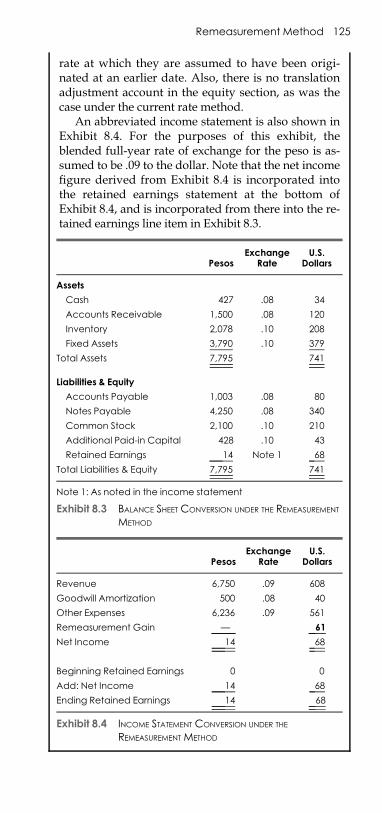

How Does the RemeasurementMethod Convert ForeignCurrency Transactions intoU.S. Dollars? � 124

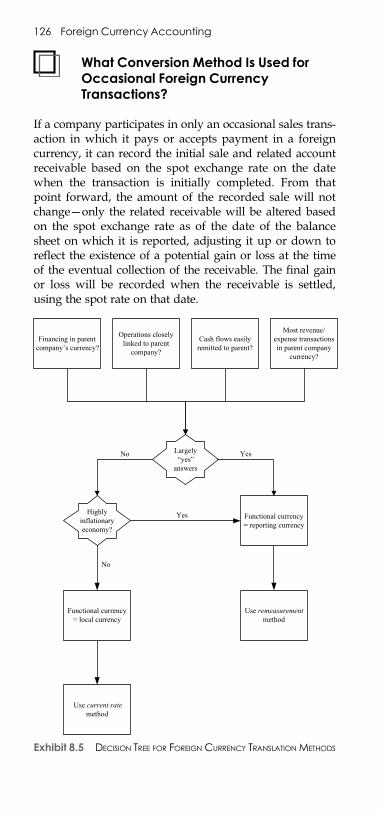

What Conversion Method Is Usedfor Occasional ForeignCurrency Transactions? � 126

xii Contents

E1FTOC 03/10/2010 Page 13

How Do I Decide Which ConversionMethod to Use? � 127

What Is the Accounting for ForeignCurrency TranslationAdjustments? � 127

What Exchange Rates Are Usedfor Conversion Calculations? � 128

How Is Foreign ExchangeHandled in IntercompanyTransactions? � 129

PART II ACCOUNTINGMANAGEMENT 131

Nine Closing the Books 133

What Types of Closes Are There? � 133What Problems Contribute to a

Delayed Close? � 133How Does Activity Acceleration

Improve the Close? � 134How Do Reporting Changes

Improve the Close? � 135How Can Journal Entry

Optimization Improve theClose? � 136

How Can I Improve theInventory Close? � 136

How Can I Improve thePayroll Close? � 137

How Can I Improve thePayables Close? � 137

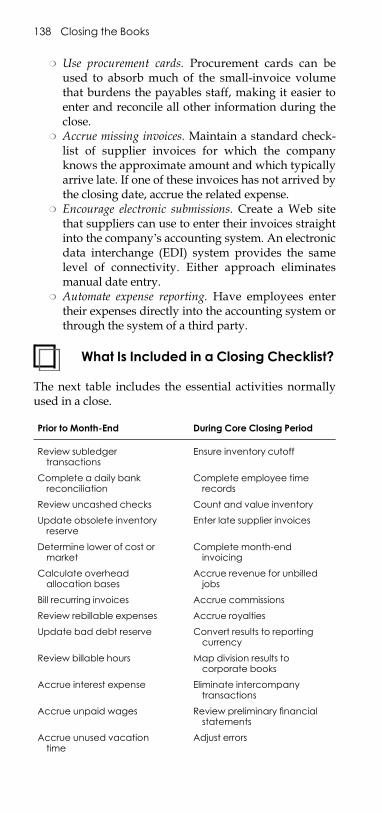

What is Included in a ClosingChecklist? � 138

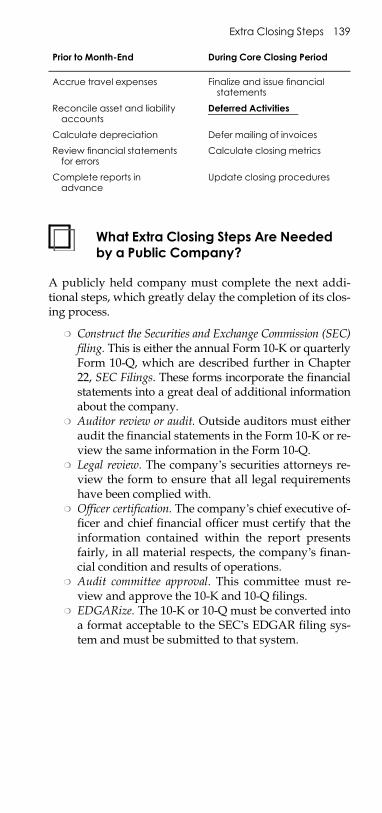

What Extra Closing StepsAre Needed by a PublicCompany? � 139

Ten Cash Management 141

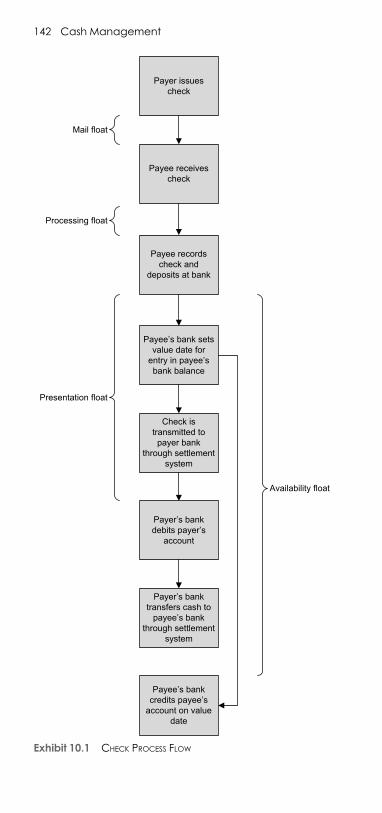

What Types of Float Are Associatedwith a Check Payment? � 141

What Is Value Dating? � 143What Is a Lockbox? � 143What Is Remote Deposit

Capture? � 143

Contents xiii

E1FTOC 03/10/2010 Page 14

Why Is Cash ConcentrationUseful? � 144

What Strategies Are Availablefor Cash Concentration? � 144

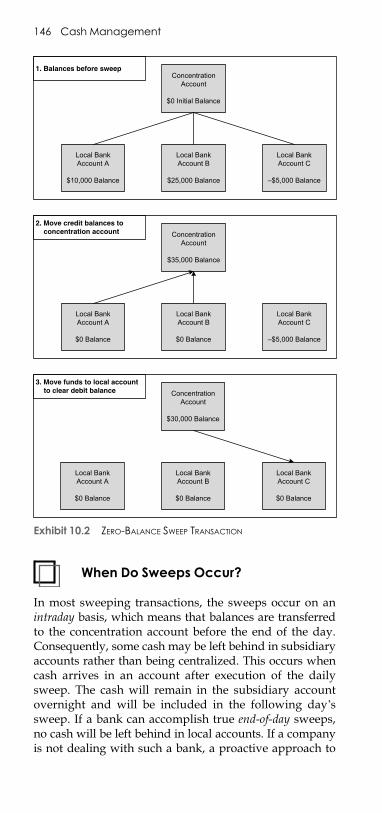

What Is Physical Sweeping? � 145When Do Sweeps Occur? � 146When Are Intercompany Loans

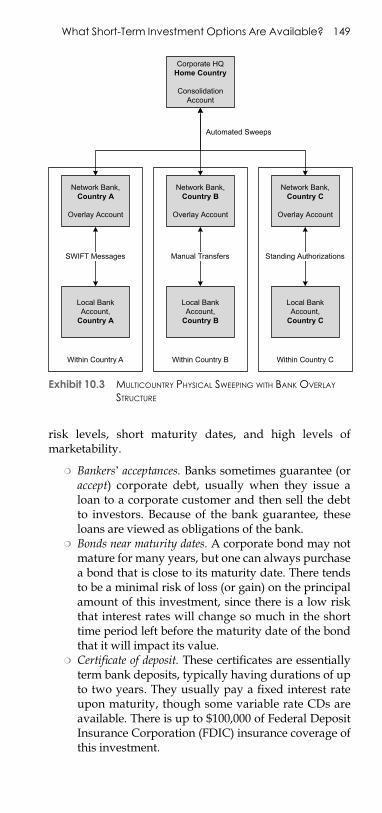

Linked to Cash Sweeps? � 147What Is Notional Pooling? � 147What Is a Bank Overlay

Structure? � 148What Short-Term Investment

Options Are Available? � 148What Investment Strategies

Are Used for Short-TermInvestments? � 150

Eleven Receivables Management 153

How Do I Create and Maintaina Credit Policy? � 153

How Do I Obtain FinancialInformation AboutCustomers? � 154

How Does a Credit-GrantingSystemWork? � 155

What Payment Terms ShouldI Offer to Customers? � 156

When Should I Review CustomerCredit Levels? � 157

How Can I Adjust the InvoiceContent and Layout toImprove Collections? � 157

How Can I Adjust Billing Deliveryto Improve Collections? � 158

Should I Offer Early PaymentDiscounts? � 159

How Do I Optimize CustomerContacts? � 159

How Do I Manage CollectionInformation? � 160

How Do I Handle PaymentDeductions? � 161

xiv Contents

E1FTOC 03/10/2010 Page 15

How Do I Collect OverduePayments? � 162

When Should I Take Legal Action toCollect from a Customer? � 164

Twelve Inventory Management 165

How Do I Increase the Accuracyof Inventory Records? � 165

How Do I Reduce the Number ofStock-Keeping Units inInventory? � 168

How Do I Reduce InventoryPurchases? � 169

How Do I Compress InventoryStorage Space? � 170

How Do I Avoid Inventory Losses onShort Shelf Life Items? � 171

How Do I Improve PickingEfficiency? � 171

How Do I Store Inventory toReduce Picking Travel? � 173

How Do I Reduce InventoryScrap? � 173

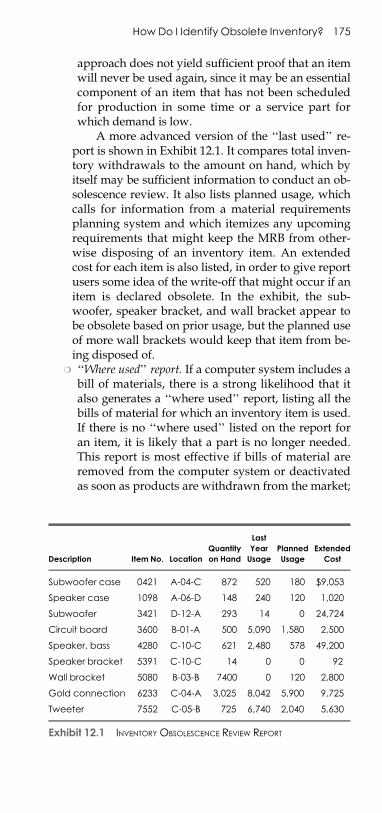

How Do I Identify ObsoleteInventory? � 174

How Do I Sell ObsoleteInventory? � 176

Thirteen Debt Management 177

What Is Commercial Paper? � 177What Is Factoring? � 177What Is Accounts Receivable

Financing? � 178What Is Field Warehouse

Financing? � 178What Is Floor Planning? � 179What Is an Operating Lease? � 179What Is a Capital Lease? � 180What Is a Line of Credit? � 180What Is a Bond? � 180What Types of Bonds Can

Be Issued? � 181

Contents xv

E1FTOC 03/10/2010 Page 16

What Is a Bridge Loan? � 182What Is Receivables

Securitization? � 182What Is a Sale and Leaseback

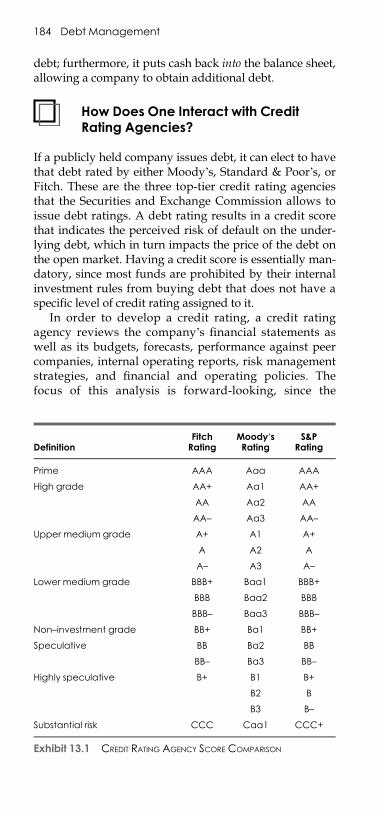

Arrangement? � 183How Does One Interact with Credit

Rating Agencies? � 184How Do the Credit Rating

Agency Scores Compareto Each Other? � 185

Forteen Equity Registration 187

What Methods Are Used toRegister Stock for Sale? � 187

What Are the Contents of aForm S-1? � 187

When Is a Form S-3 Used? � 189When Is a Form S-8 Used? � 190What Is a Shelf Registration? � 191Why Must a Registration Statement

Be Declared Effective? � 192When Can the Regulation

A Exemption Be Used? � 192What Are the Advantages of Using

a Regulation A Exemption? � 193What Is the Process for Using the

Regulation A Exemption? � 193What Are the Restrictions on

Using the RegulationD Exemption? � 194

When Can Rule 144 be Usedto Register Stock? � 195

PART III FINANCIAL ANALYSIS 197

Fifteen Financial Analysis 199

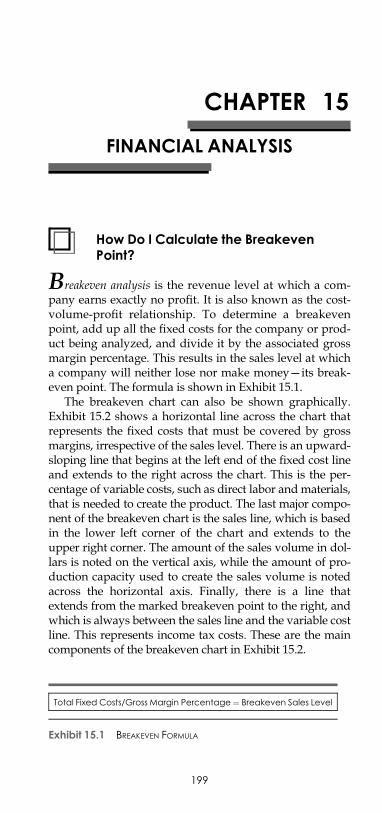

How Do I Calculate theBreakeven Point? � 199

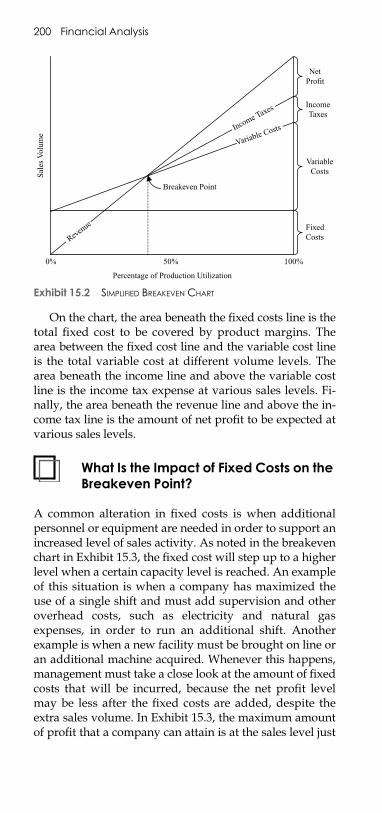

What Is the Impact of Fixed Costson the Breakeven Point? � 200

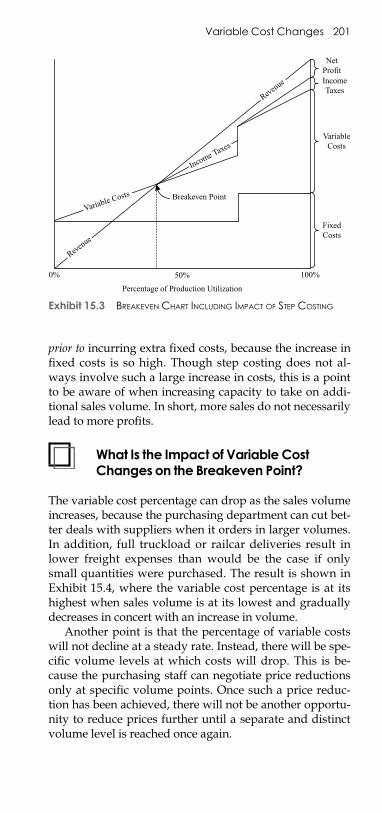

What Is the Impact of VariableCost Changes on the BreakevenPoint? � 201

xvi Contents

E1FTOC 03/10/2010 Page 17

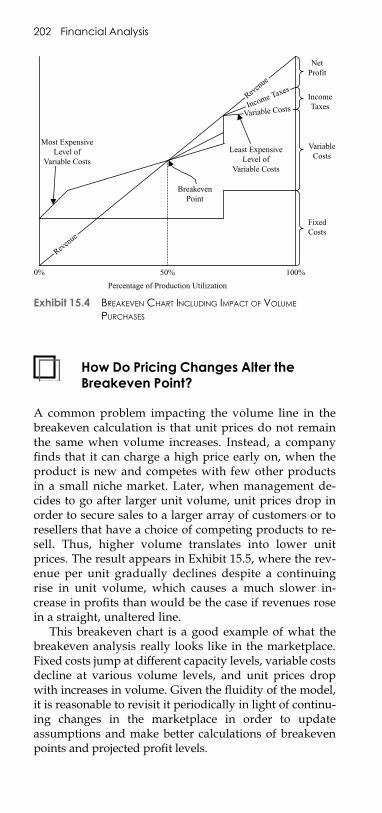

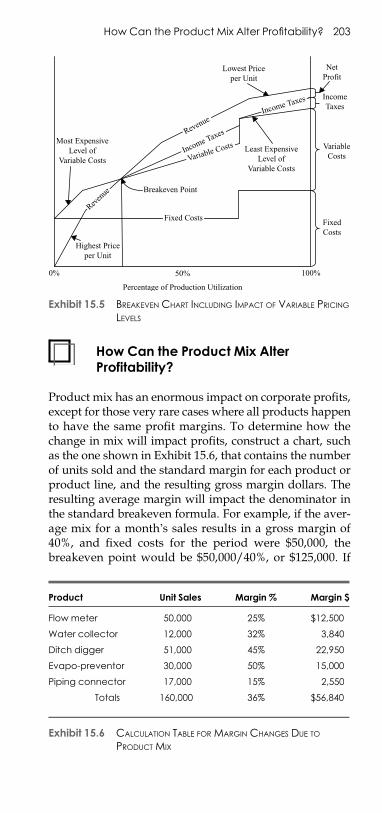

How Do Pricing Changes Alterthe Breakeven Point? � 202

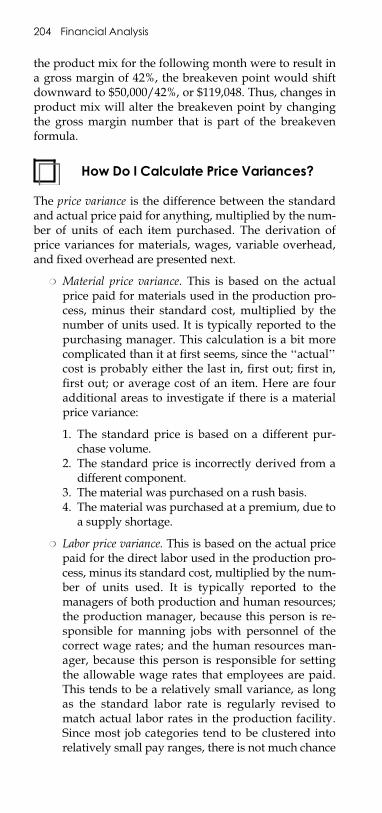

How Can the Product Mix AlterProfitability? � 203

How Do I Calculate PriceVariances? � 204

How Do I Calculate EfficiencyVariances? � 206

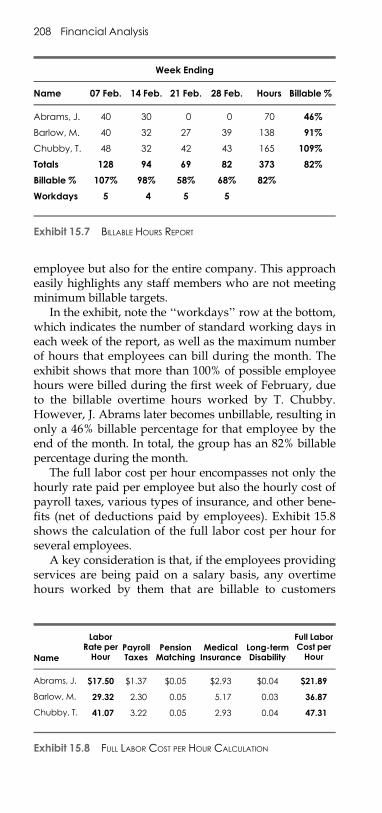

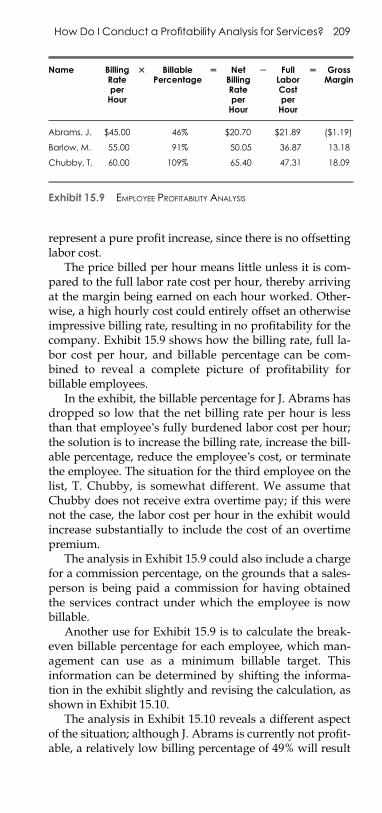

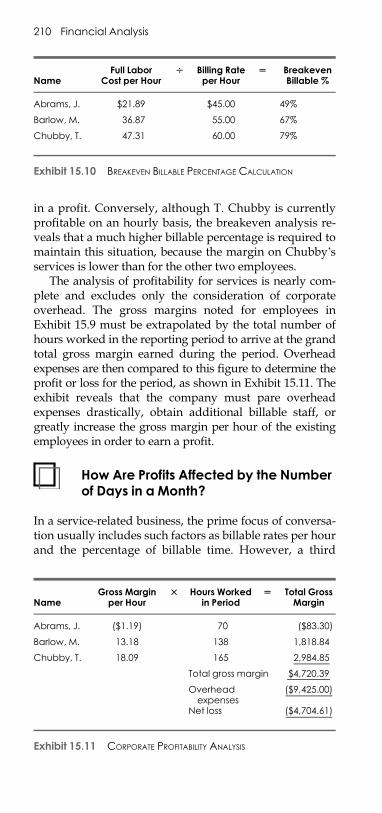

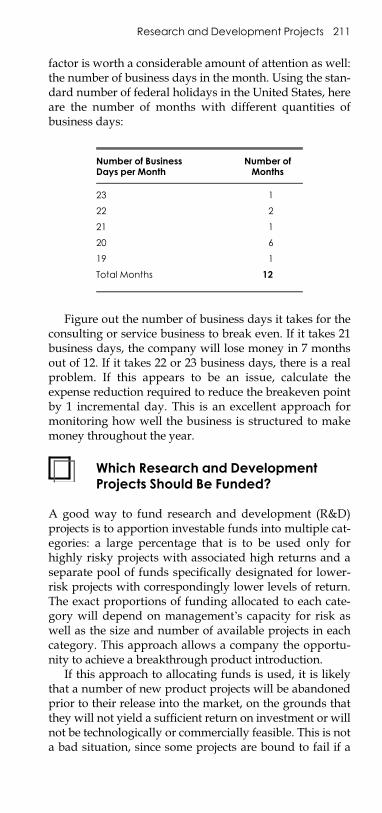

How Do I Conduct a ProfitabilityAnalysis for Services? � 207

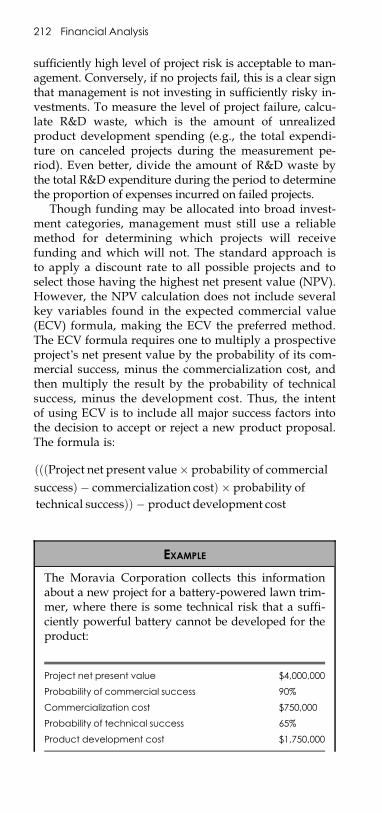

How Are Profits Affected by theNumber of Days in a Month? � 210

Which Research and DevelopmentProjects Should be Funded? � 211

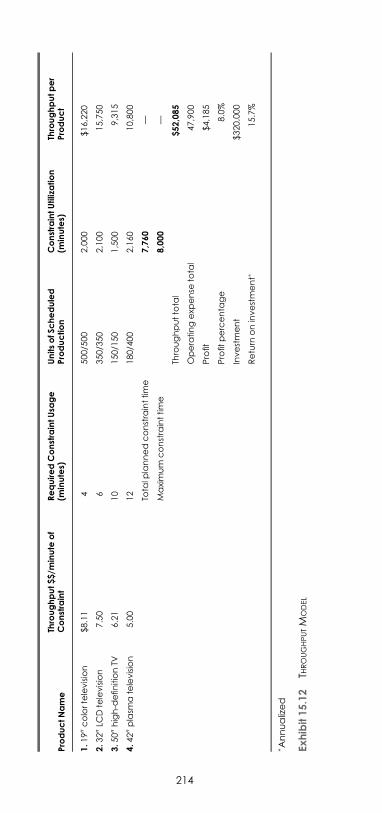

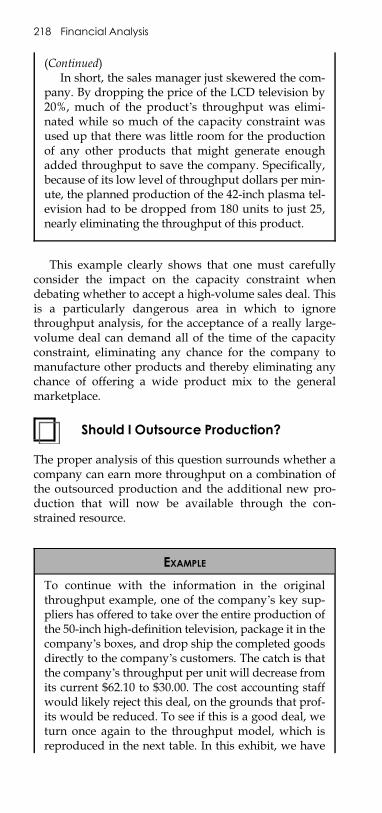

How Do I Create a ThroughputAnalysis Model? � 213

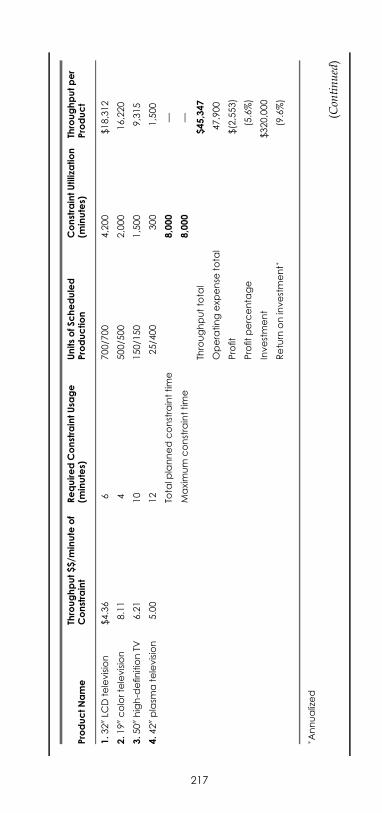

How Do I Determine if MoreVolume at a Lower PriceCreates More Profit? � 216

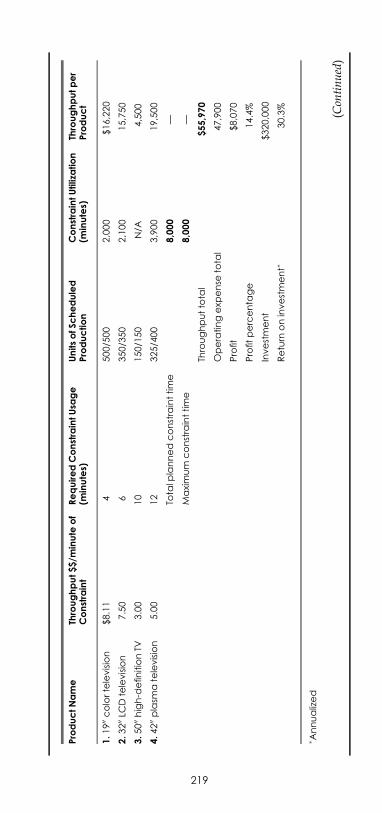

Should I Outsource Production? � 218Should I Add Staff to the Bottleneck

Operation? � 220Should I Produce a New Product? � 222

Sixteen Pricing Analysis 227

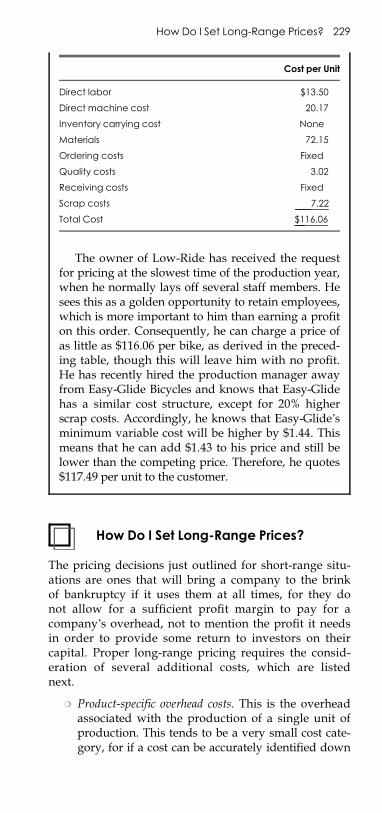

What Is the Lowest Price that IShould Accept? � 227

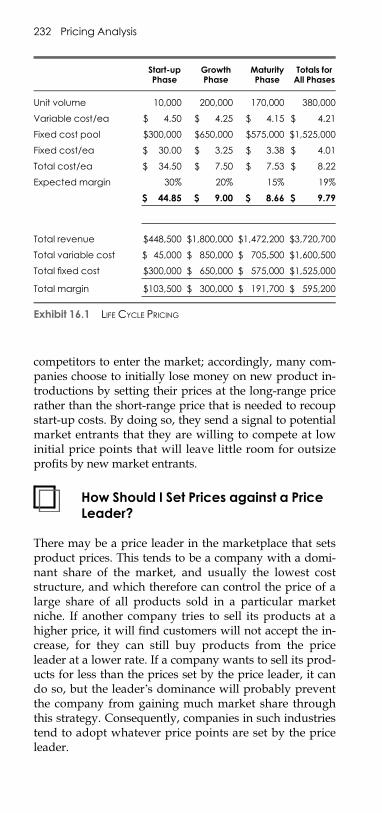

How Do I Set Long-Range Prices? � 229How Should I Set Prices over the

Life of a Product? � 231How Should I Set Prices against

a Price Leader? � 232How Do I Handle a Price War? � 233How Do I Handle Dumping by

a Foreign Competitor? � 234When Is Transfer Pricing

Important? � 235How Do Transfer Prices Alter

Corporate Decision Making? � 235How Does the External Market

Price Work as a Transfer PricingMethod? � 236

Contents xvii

E1FTOC 03/10/2010 Page 18

How Does Adjusted Market PricingWork as a Transfer PricingMethod? � 237

How Do Negotiated Transfer PricesWork as a Transfer PricingMethod? � 238

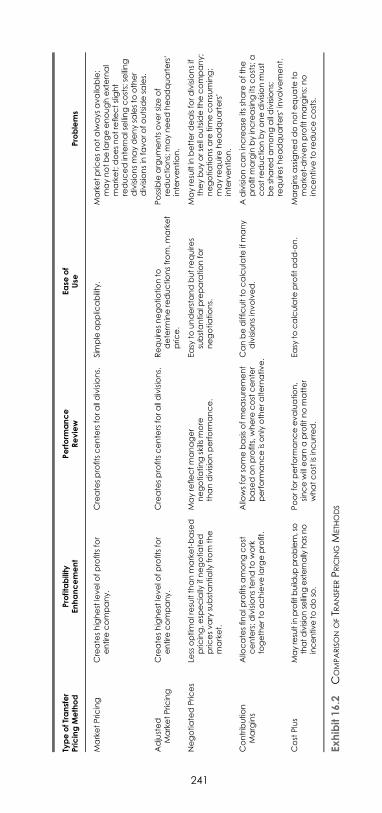

How Does the Contribution MarginWork as a Transfer PricingMethod? � 239

How Does the Cost-Plus MethodWork as a Transfer PricingMethod? � 240

How Do the Transfer PricingMethods Compare toEach Other? � 242

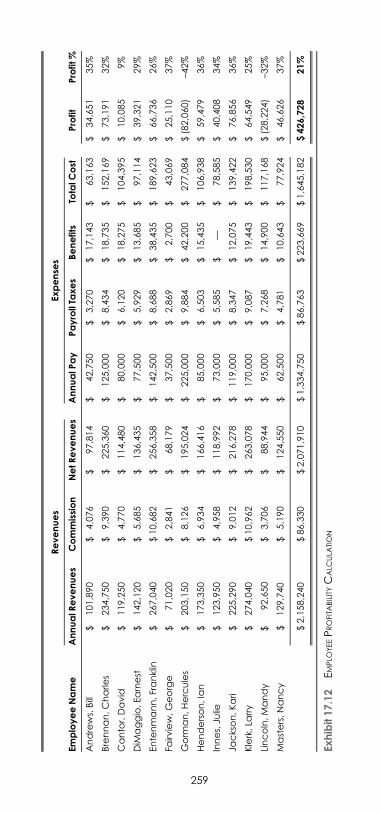

Seventeen Cost Reduction Analysis 243

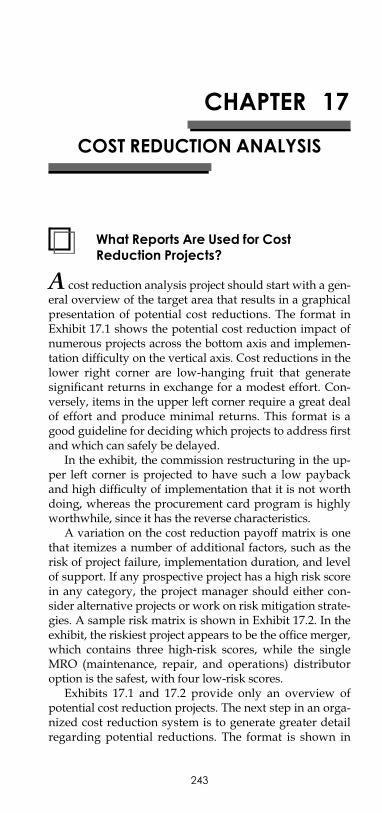

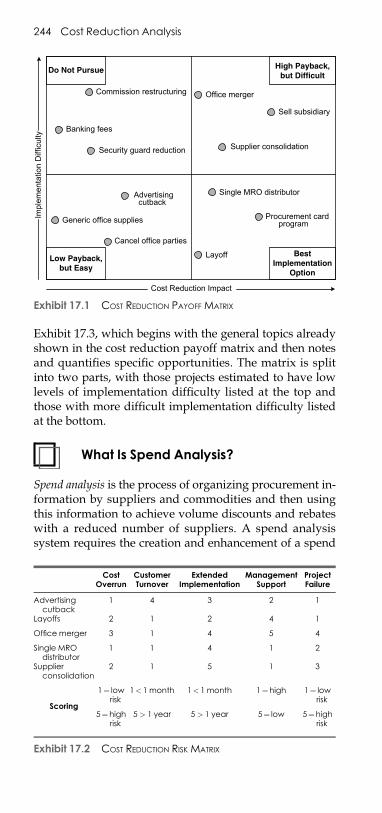

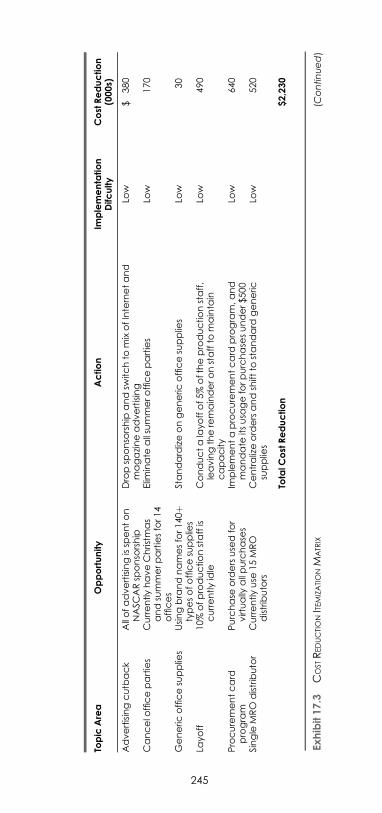

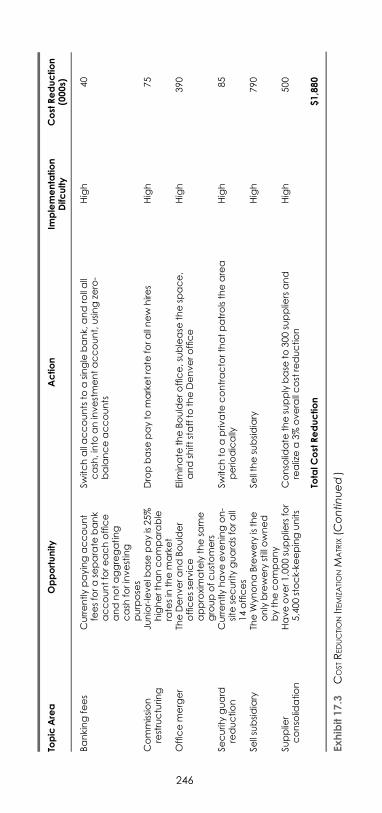

What Reports Are Used for CostReduction Projects? � 243

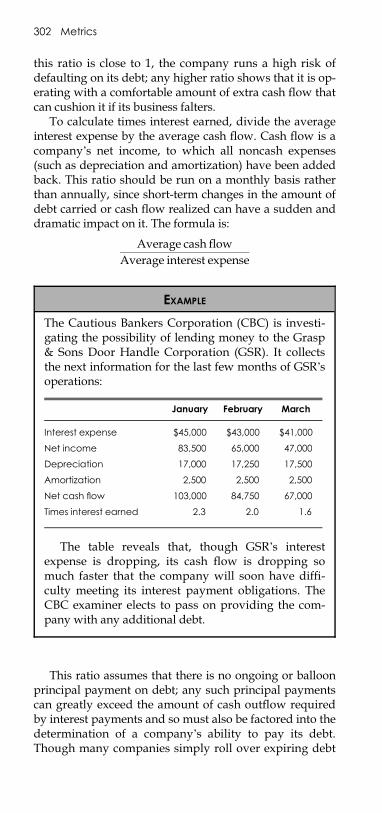

What Is Spend Analysis? � 244How Is the Spend Database

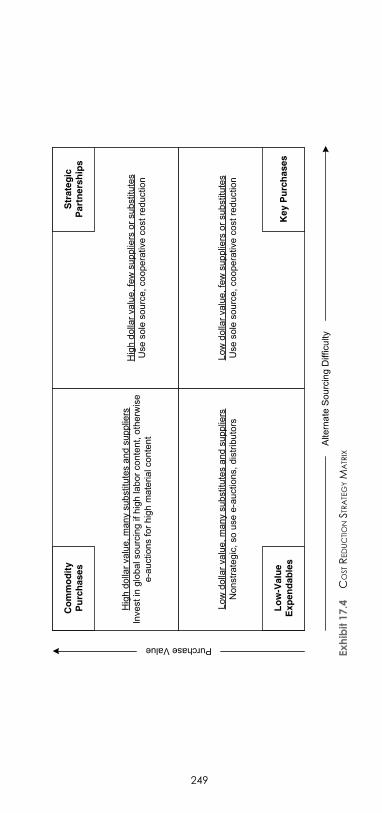

Constructed? � 247How Does Supplier Consolidation

Work? � 248How Does Parts Consolidation

Work? � 250Can Spend Analysis Work for

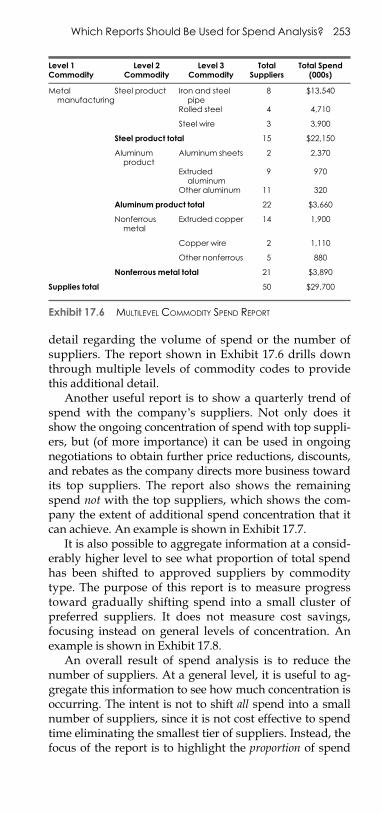

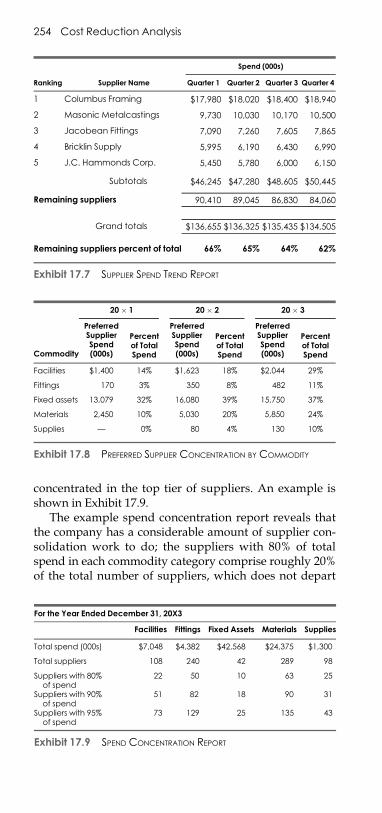

MRO Items? � 250What Is Spend Compliance? � 251Which Reports Should Be Used

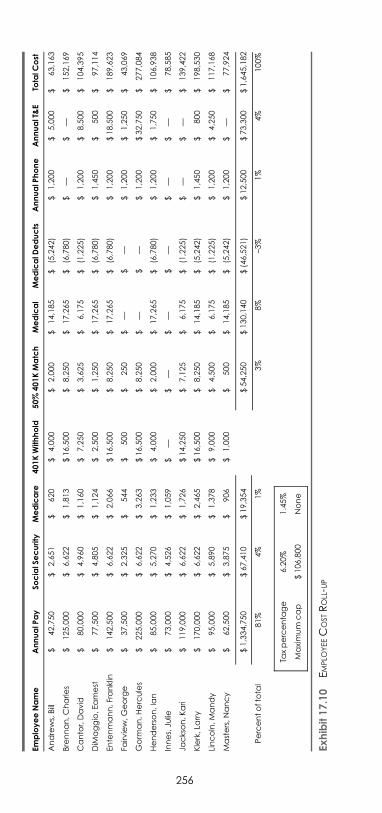

for Spend Analysis? � 252What Is the Analysis for a

Workforce Reduction? � 255What Is the Cost of a Workforce

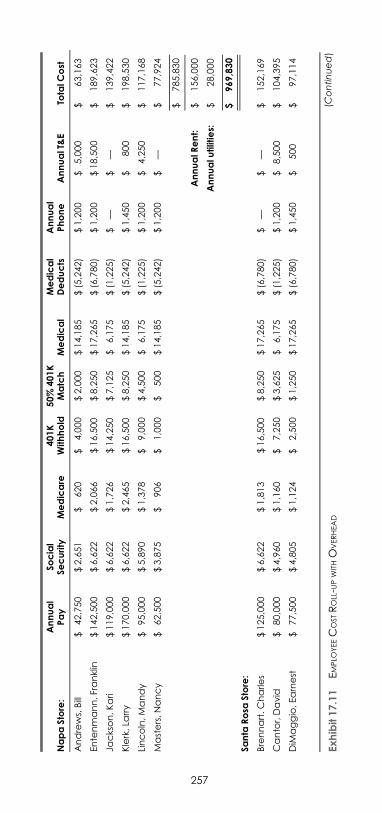

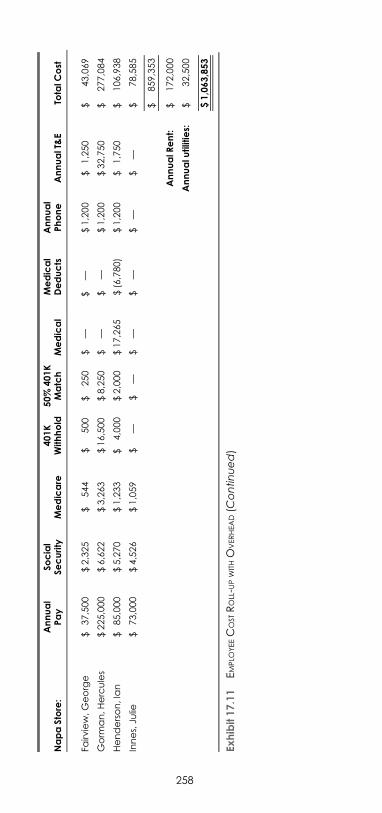

Reduction? � 260What Are the Alternatives to a

Workforce Reduction? � 261How Does 5S Analysis Reduce

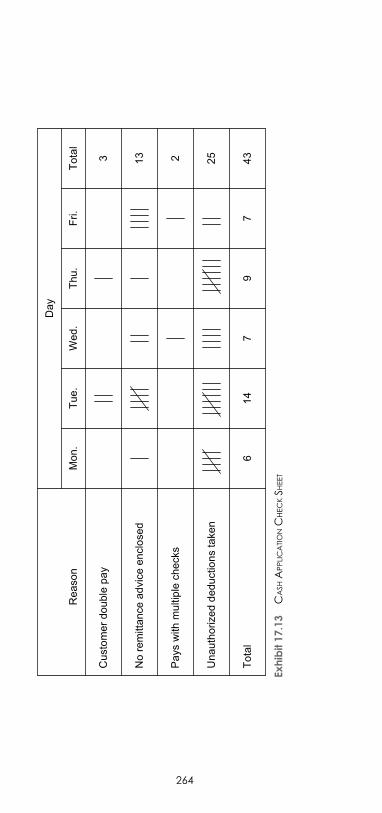

Costs? � 262How Are Check Sheets Used? � 263How Is Error Quantification

Used? � 265

xviii Contents

E1FTOC 03/10/2010 Page 19

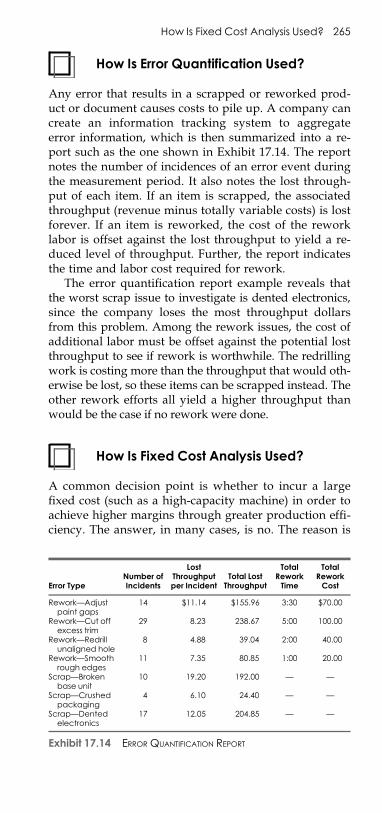

How Is Fixed Cost AnalysisUsed? � 265

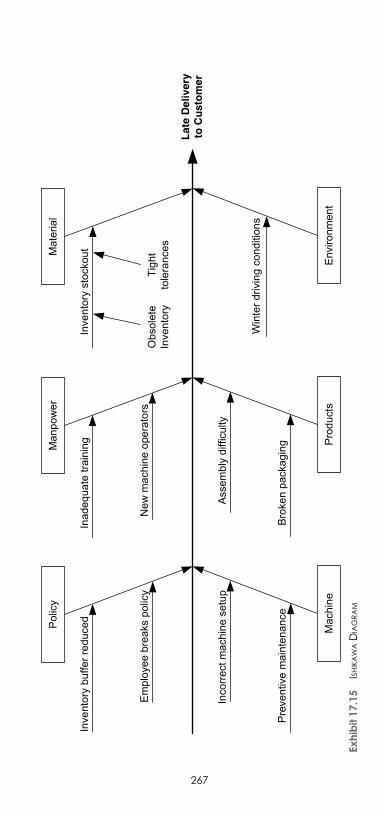

How Are Ishikawa DiagramsUsed? � 266

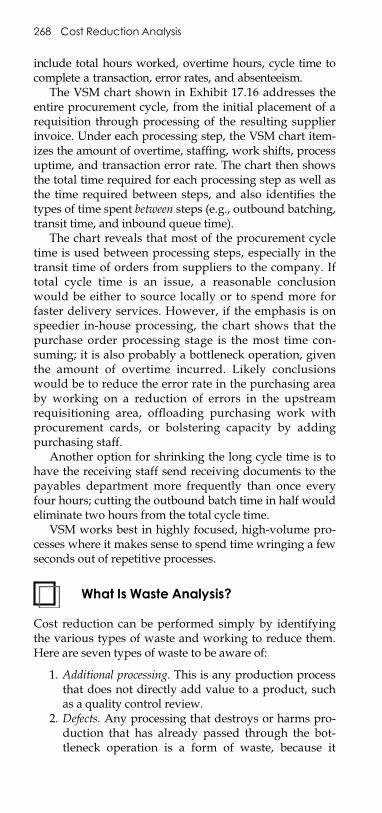

How Is Value StreamMappingUsed? � 266

What Is Waste Analysis? � 268

Eighteen Metrics 271

How Do I Calculate AccountsPayable Turnover? � 271

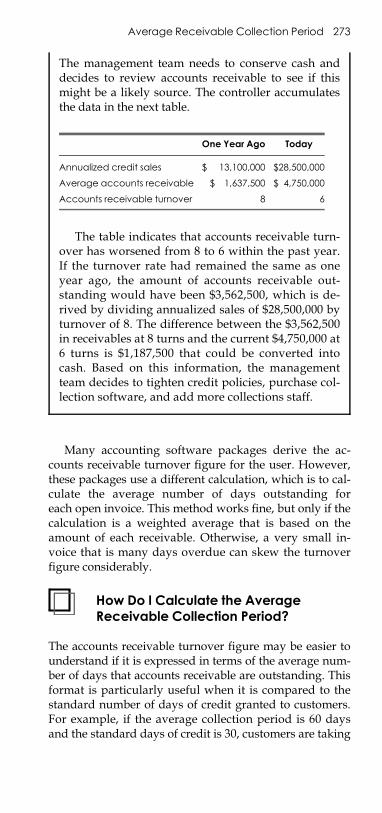

How Do I Calculate AccountsReceivable Turnover? � 272

How Do I Calculate theAverage ReceivableCollection Period? � 273

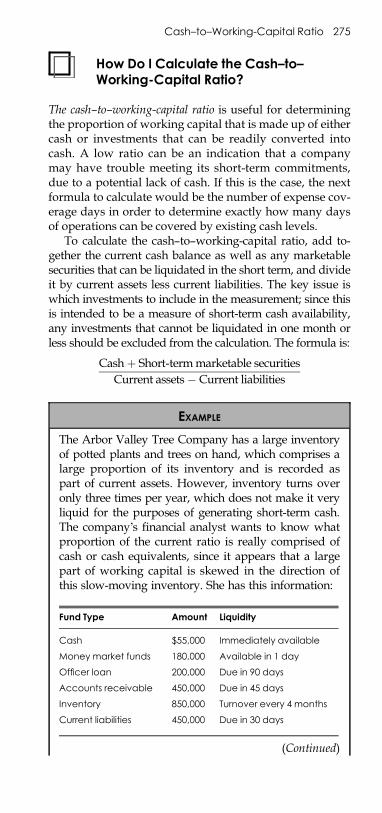

How Do I Calculate the Cash-to-Working-Capital Ratio? � 275

How Do I Calculate the CoreGrowth Rate? � 276

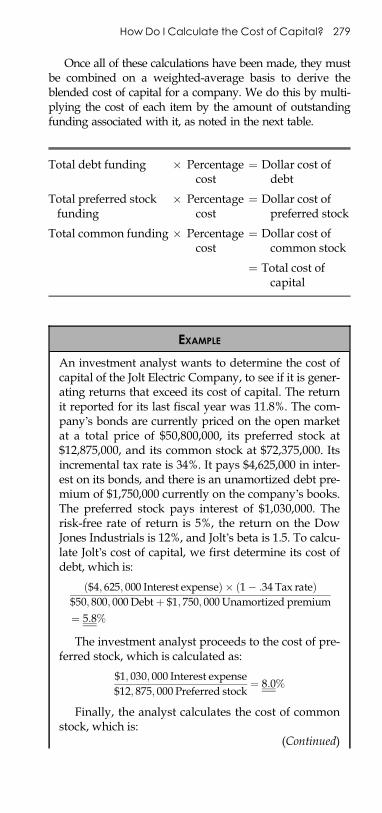

How Do I Calculate the Cost ofCapital? � 277

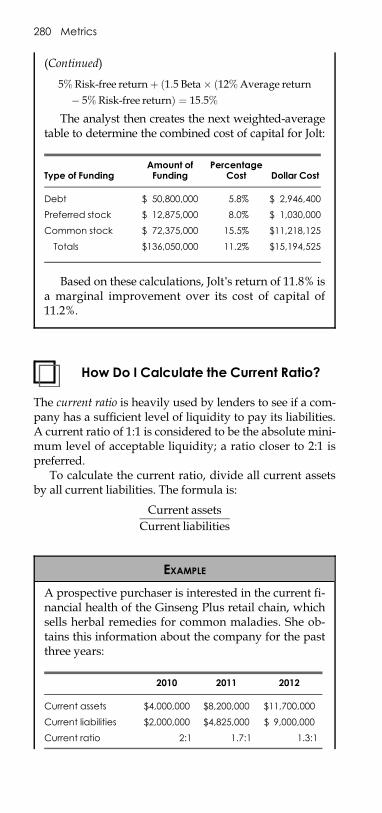

How Do I Calculate the CurrentRatio? � 280

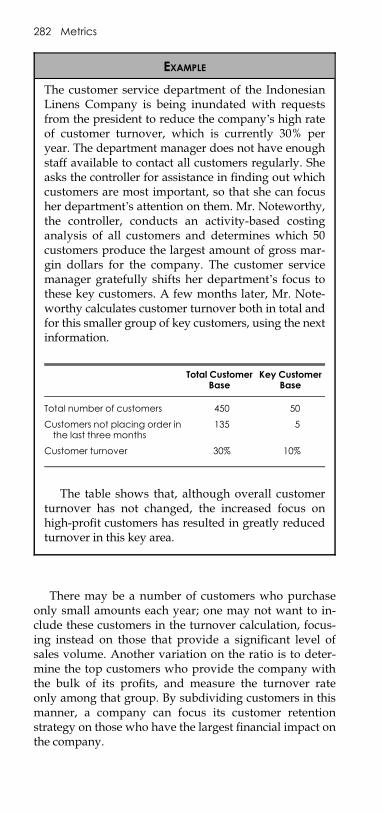

How Do I Calculate CustomerTurnover? � 281

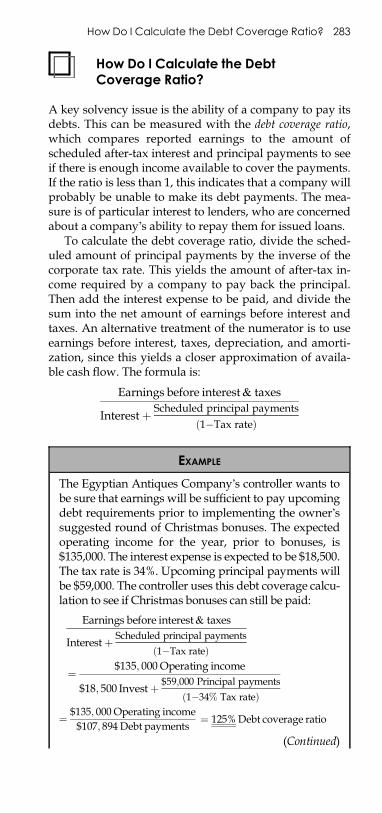

How Do I Calculate the DebtCoverage Ratio? � 283

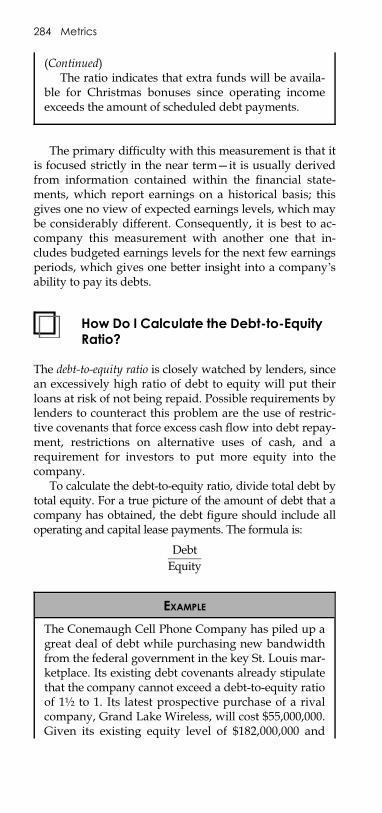

How Do I Calculate the Debt-to-Equity Ratio? � 284

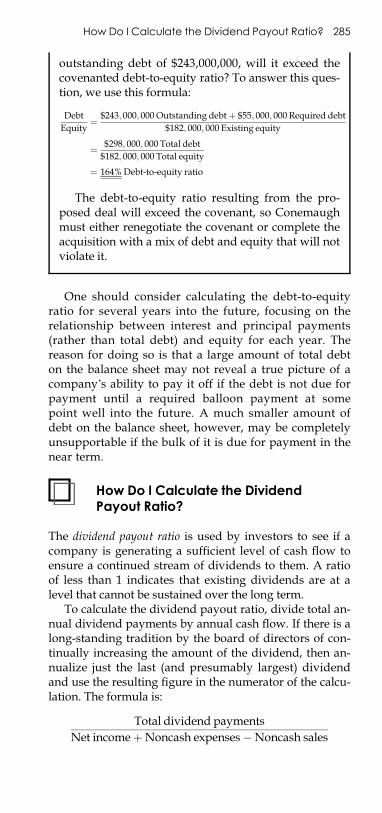

How Do I Calculate the DividendPayout Ratio? � 285

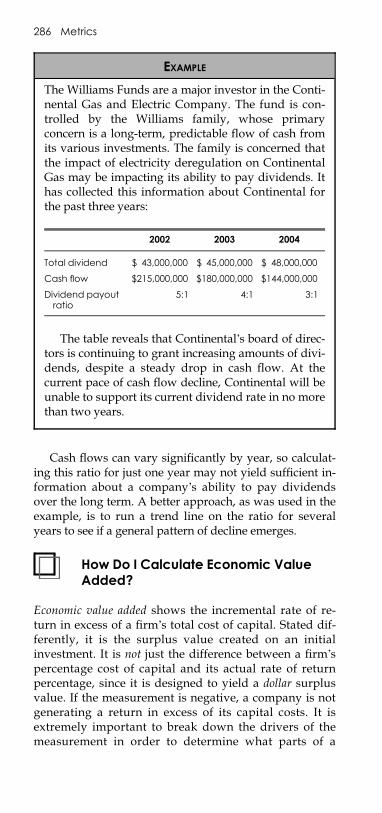

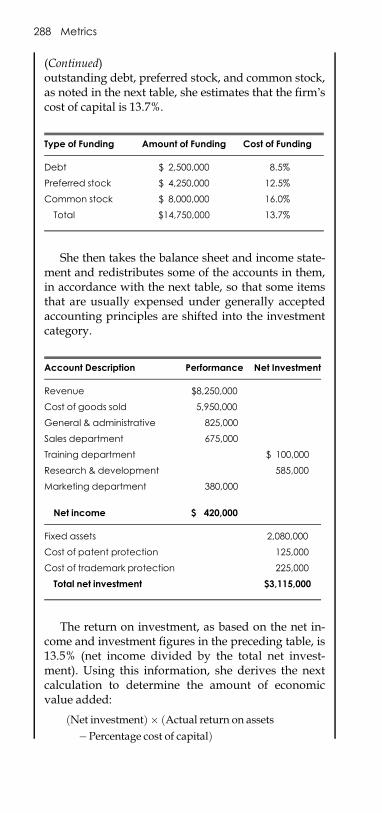

How Do I Calculate EconomicValue Added? � 286

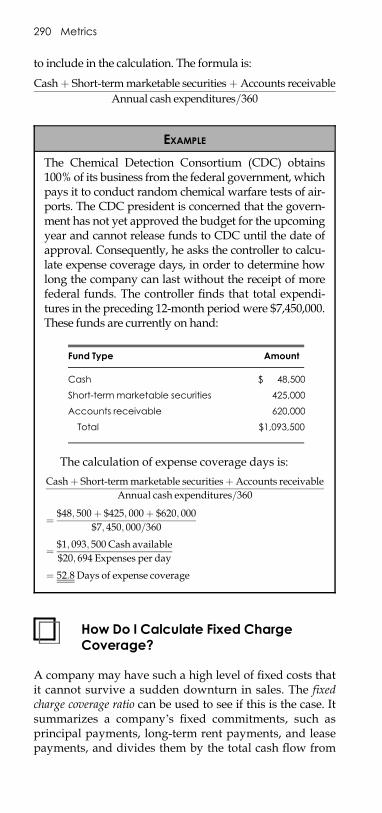

How Do I Calculate ExpenseCoverage Days? � 289

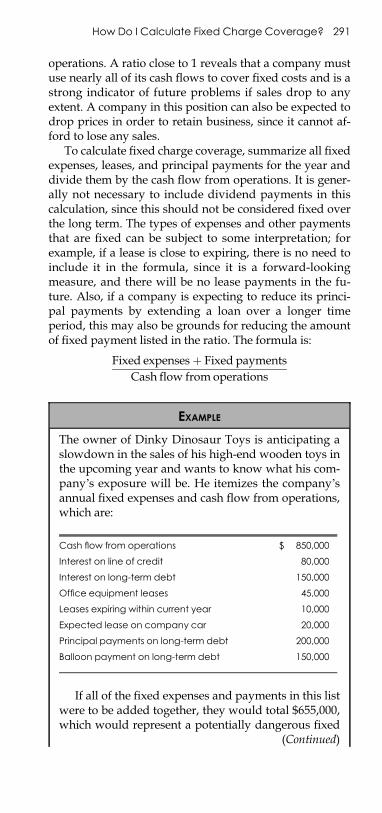

How Do I Calculate Fixed ChargeCoverage? � 290

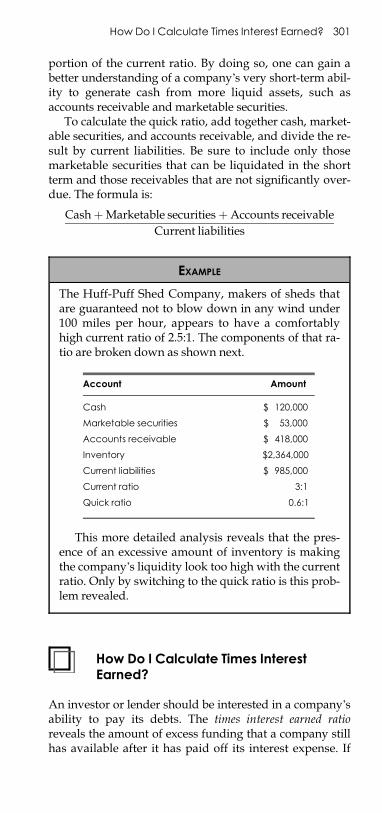

How Do I Calculate InventoryAccuracy? � 292

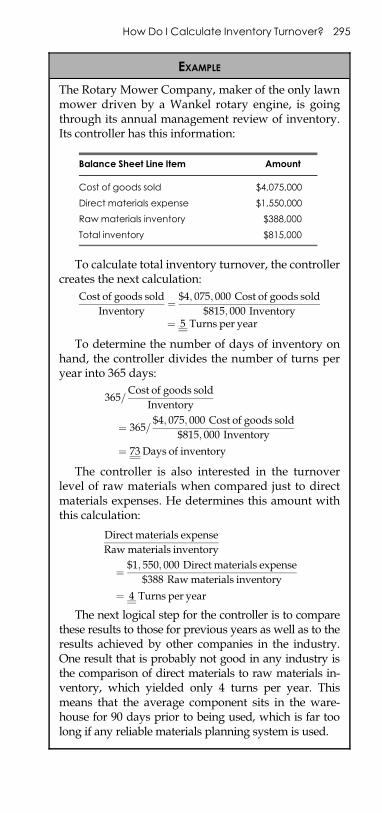

How Do I Calculate InventoryTurnover? � 294

Contents xix

E1FTOC 03/10/2010 Page 20

How Do I Calculate the Marginof Safety? � 296

How Do I Calculate Net Worth? � 297How Do I Calculate the Price/

Earnings Ratio? � 299How Do I Calculate the

Quick Ratio? � 300How Do I Calculate Times

Interest Earned? � 301How Do I Calculate Working

Capital Productivity? � 303

PART IV CONTROL SYSTEMS 305

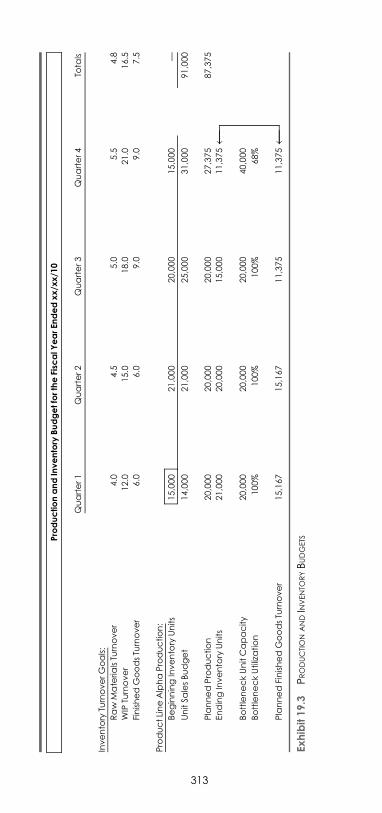

Nineteen Budgeting 307

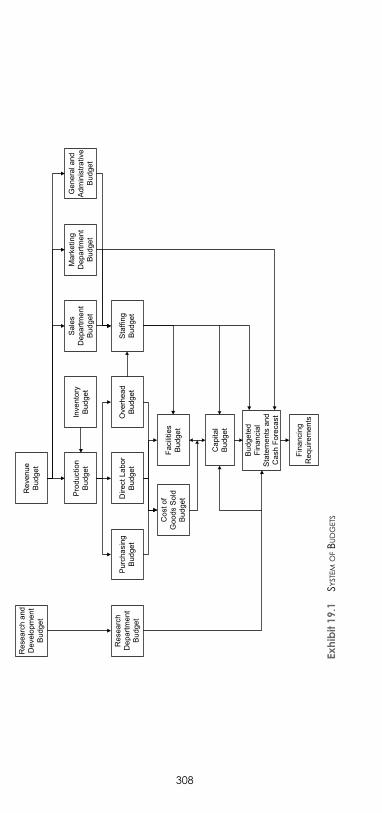

Why Is Budgeting Important? � 307How Do the Various Budgets

Fit Together? � 307How Is the Revenue Budget

Constructed? � 310How Are the Production

and Inventory BudgetsConstructed? � 312

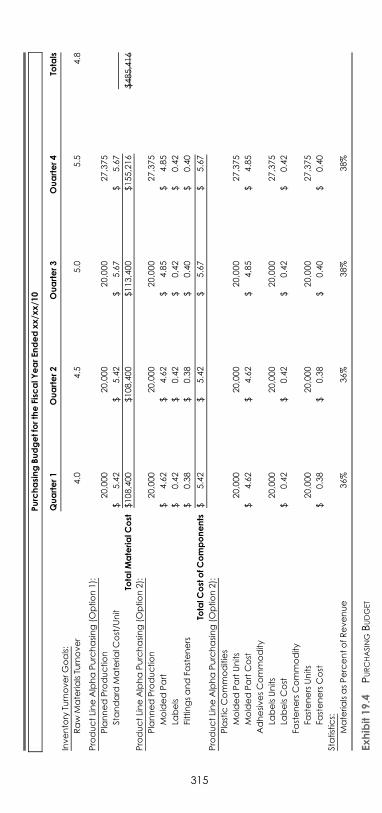

How Is the Purchasing BudgetConstructed? � 314

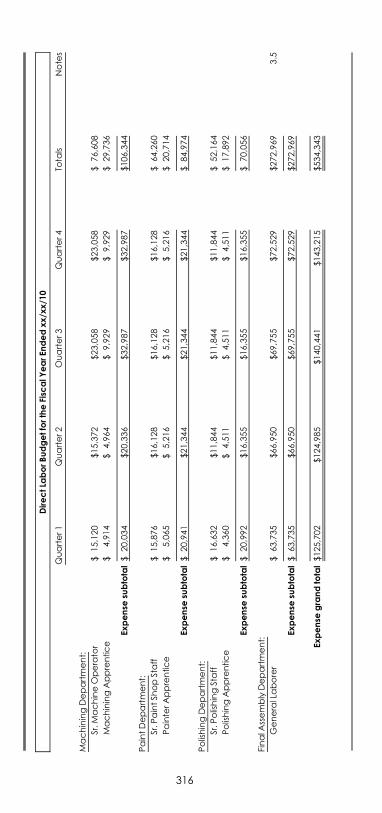

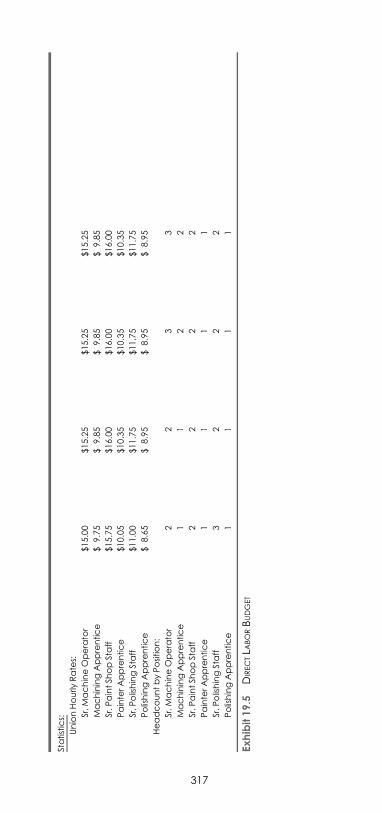

How Is the Direct Labor BudgetConstructed? � 314

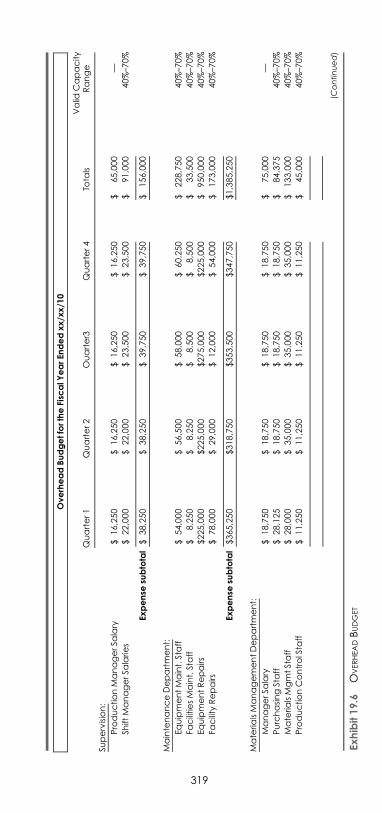

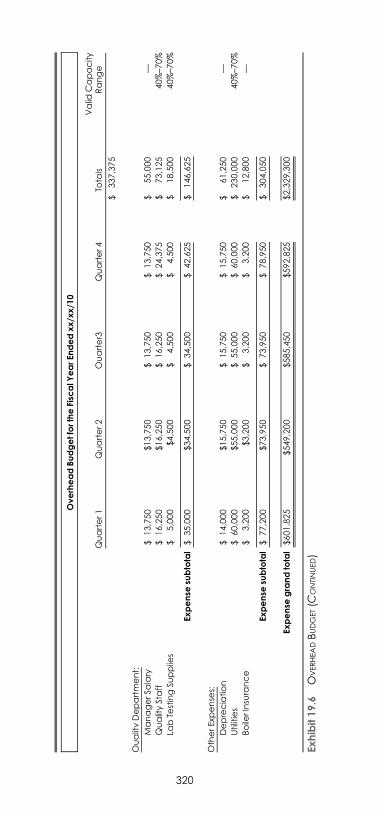

How Is the Overhead BudgetConstructed? � 318

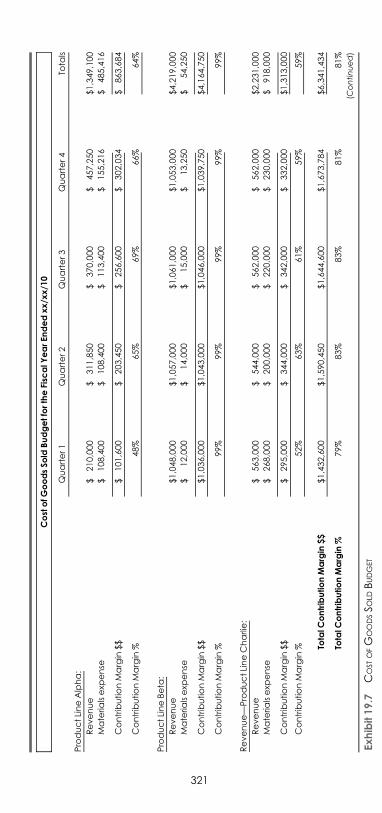

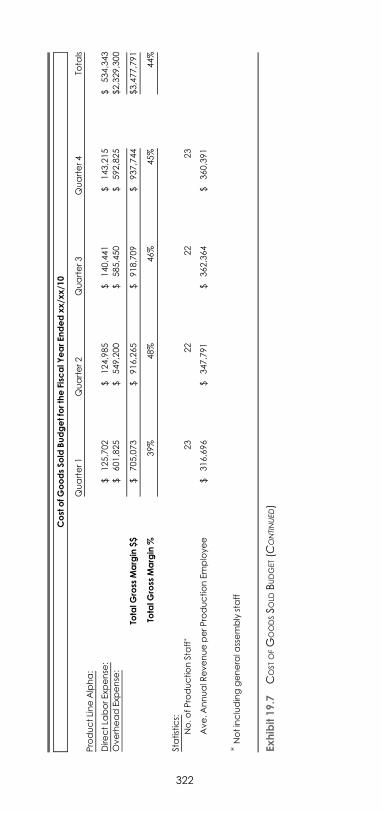

How Is the Cost of Goods SoldBudget Constructed? � 318

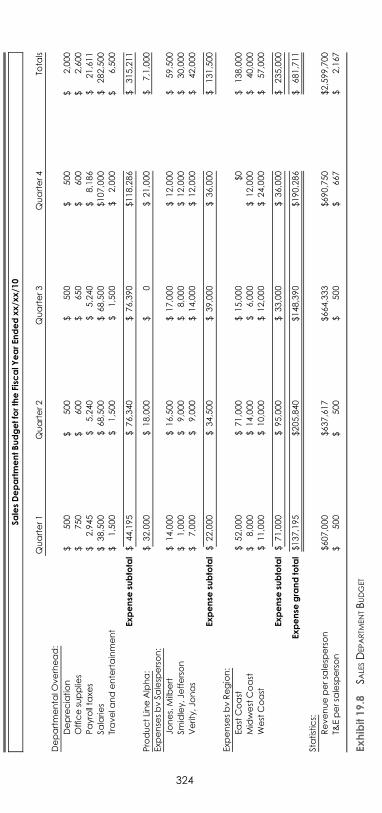

How Is the Sales DepartmentBudget Constructed? � 323

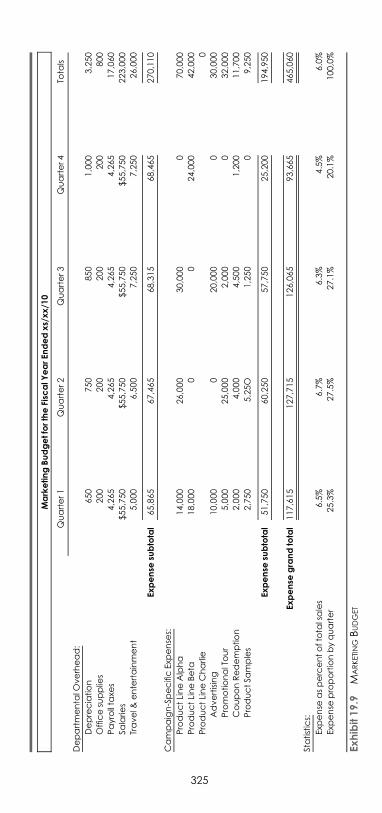

How Is the Marketing BudgetConstructed? � 323

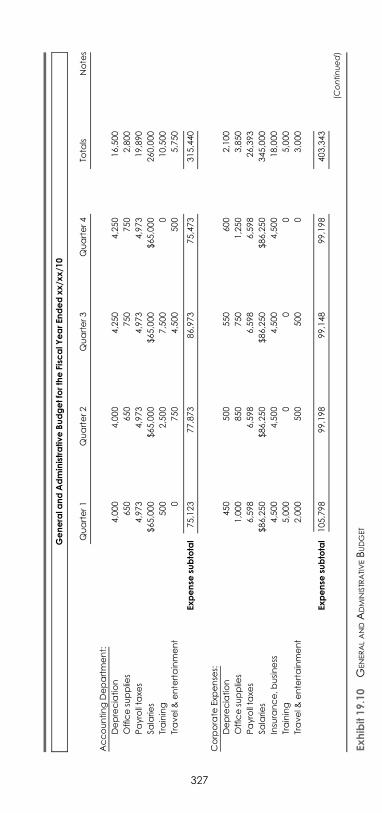

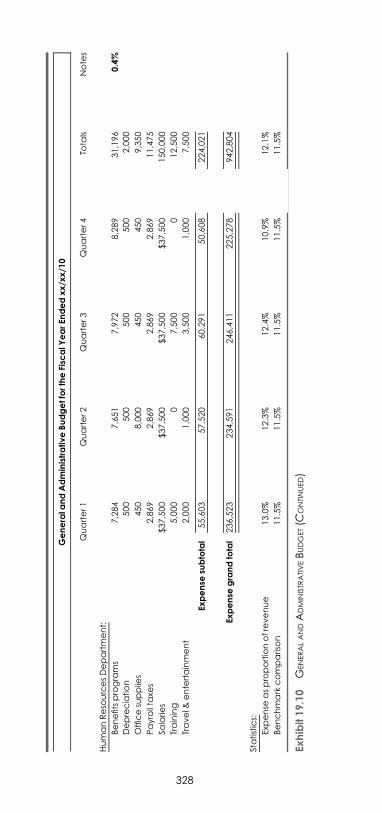

How Is the General andAdministrative BudgetConstructed? � 326

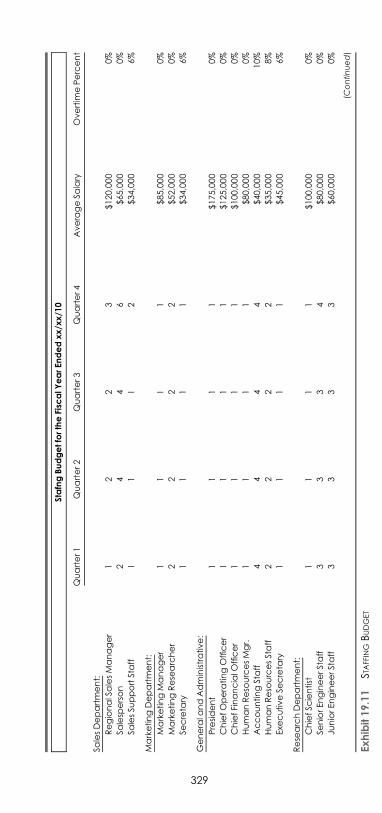

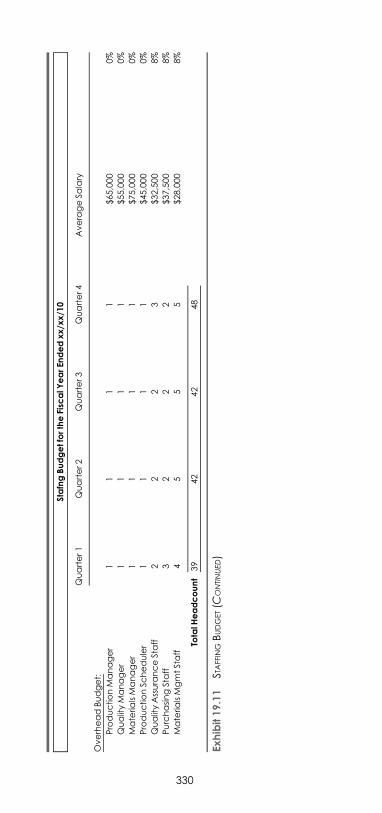

How Is the Staffing BudgetConstructed? � 326

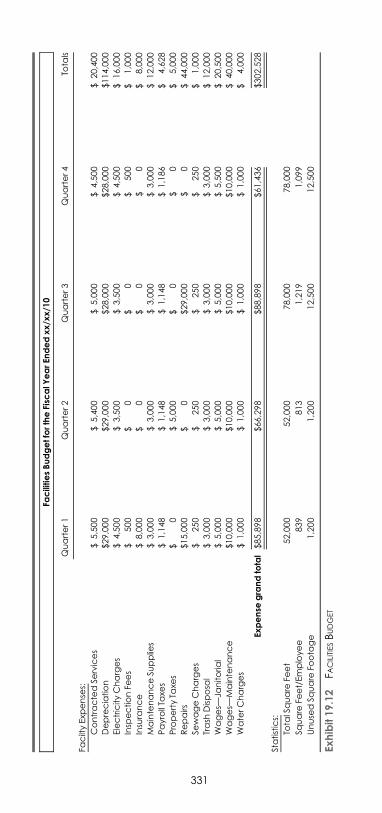

How Is the Facilities BudgetConstructed? � 326

xx Contents

E1FTOC 03/10/2010 Page 21

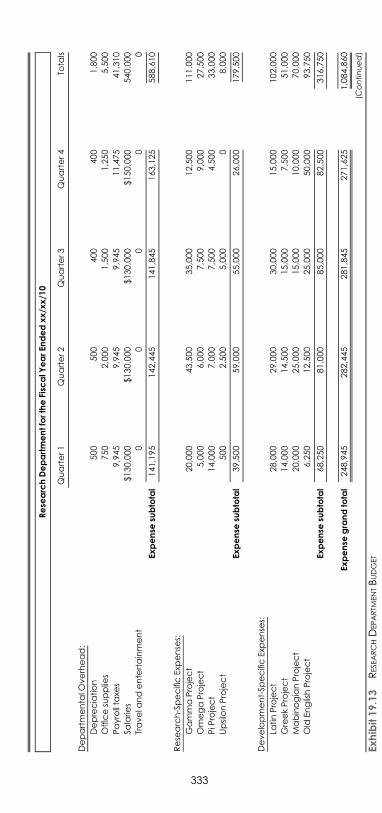

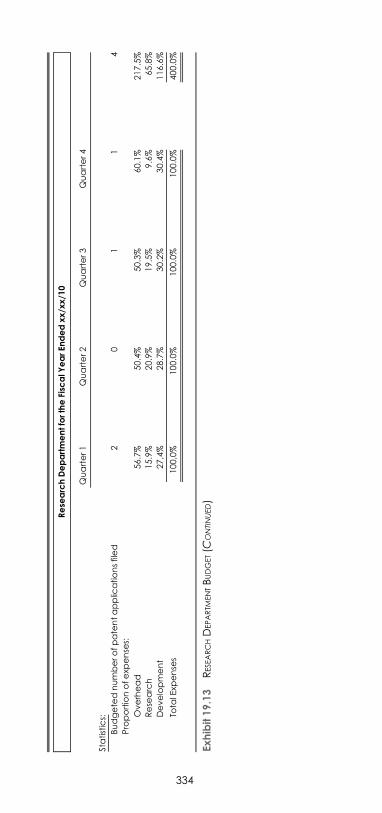

How Is the Research DepartmentBudget Constructed? � 332

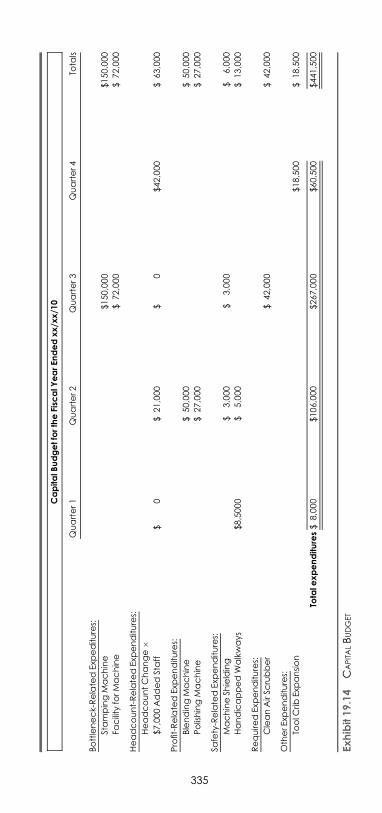

How Is the Capital BudgetConstructed? � 332

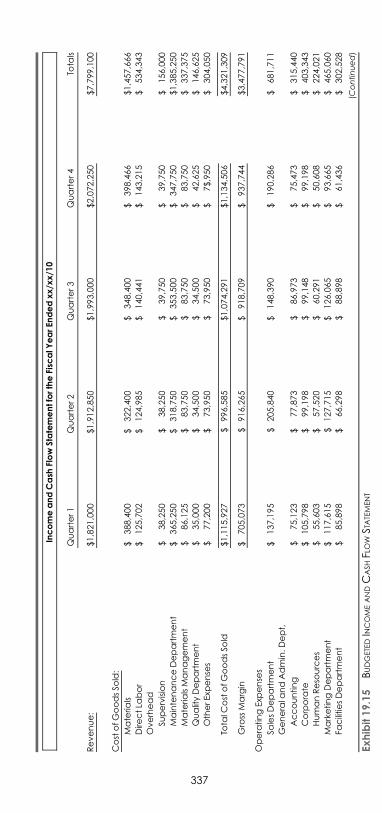

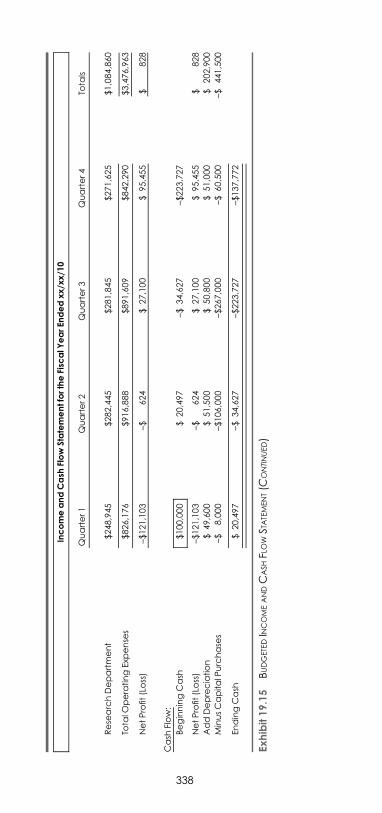

How Are the Budgeted FinancialStatements Constructed? � 336

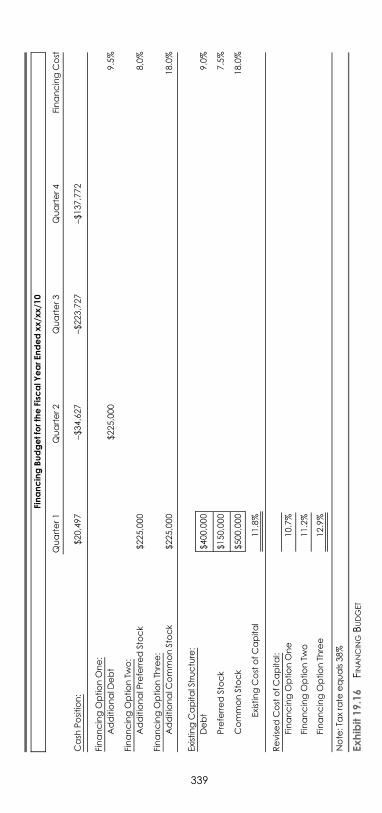

How Is the Financing BudgetConstructed? � 336

What Is a Flex Budget? � 340

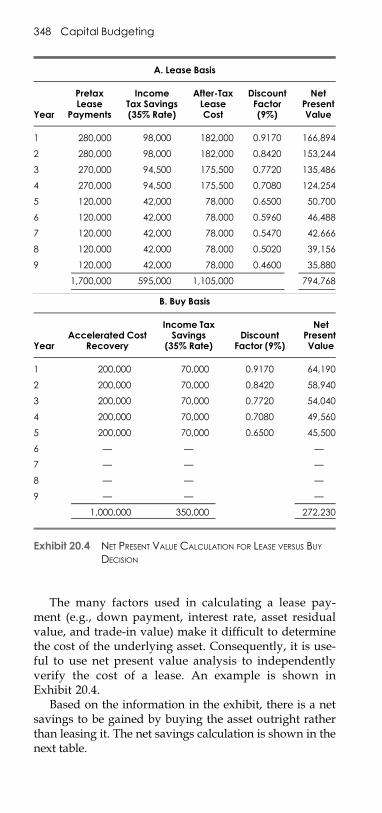

Twenty Capital Budgeting 341

What Is Capital Budgeting? � 341What Are the Problems with Capital

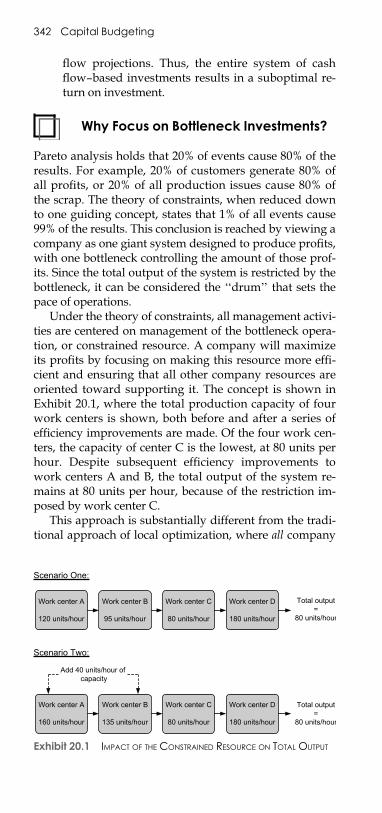

Budgeting Analysis? � 341Why Focus on Bottleneck

Investments? � 342When Should I Invest in a

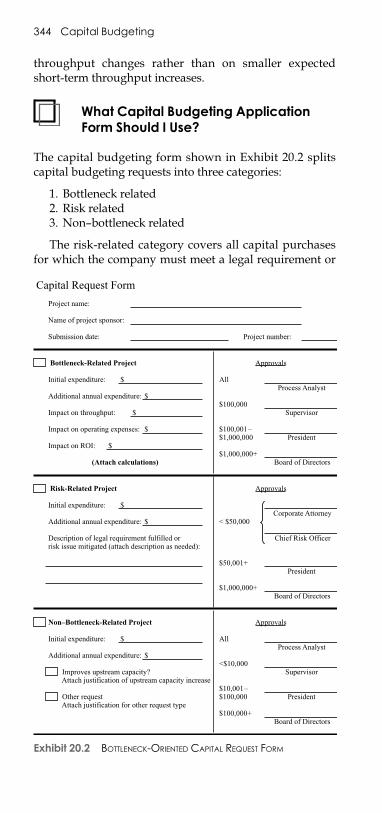

Bottleneck Operation? � 343What Capital Budgeting Application

Form Should I Use? � 344Should I Invest in Upstream

Workstations? � 345Should I Invest in Downstream

Workstations? � 346Should I Lease an Asset or

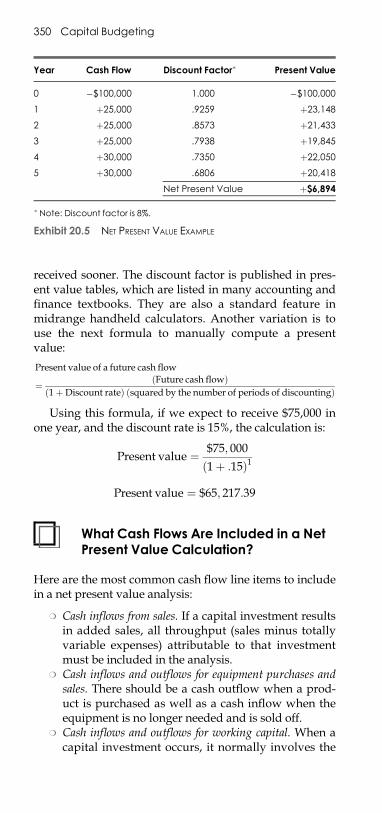

Buy It? � 347What Is Net Present Value? � 349What Cash Flows Are Included

in a Net Present ValueCalculation? � 350

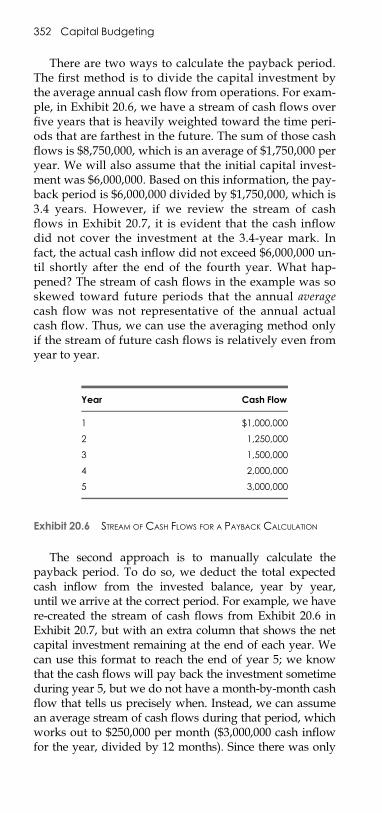

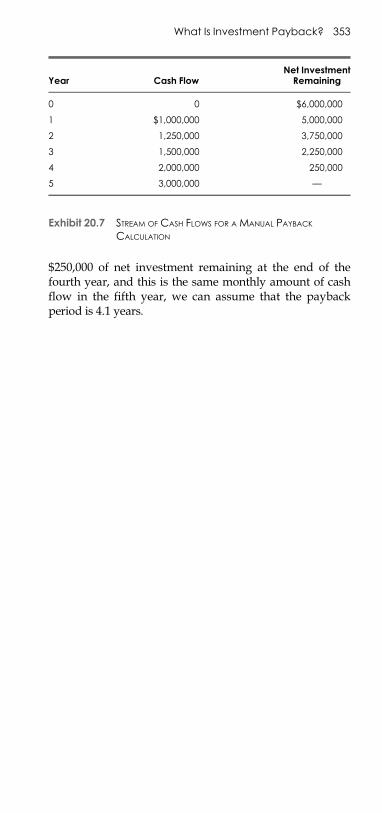

What Is Investment Payback? � 351

Twenty-One Control Systems 355

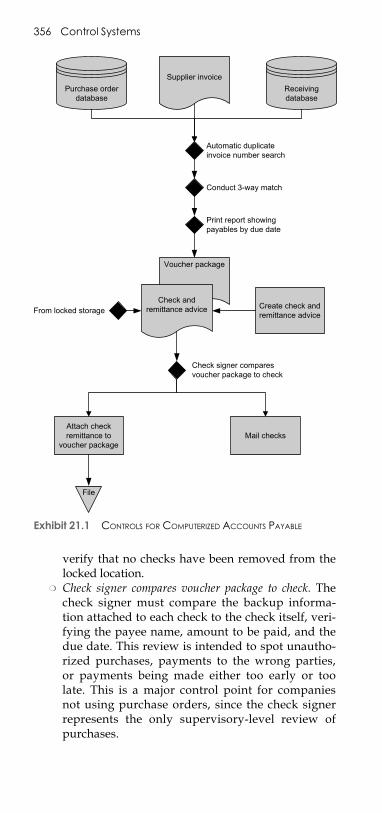

What Are the Controls for aComputerized AccountsPayable System? � 355

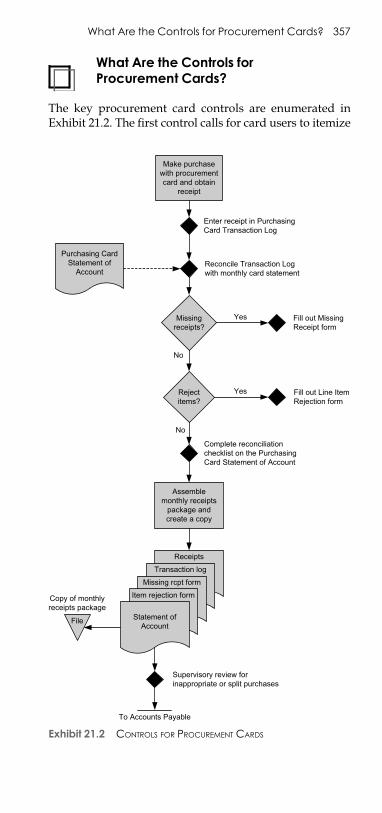

What Are the Controls forProcurement Cards? � 357

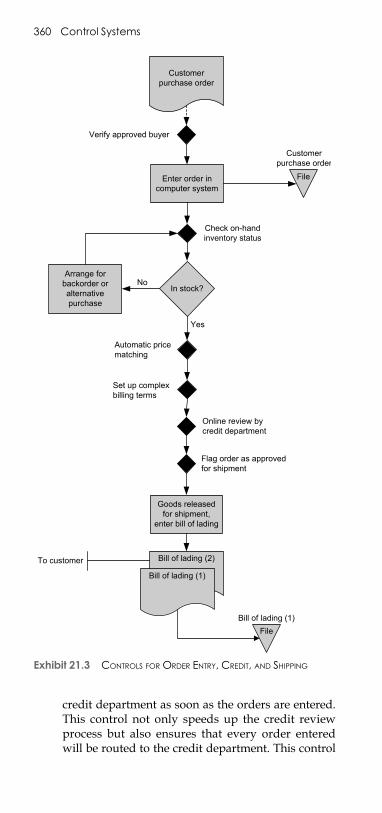

What Are the Controls for OrderEntry, Credit, and Shipping? � 359

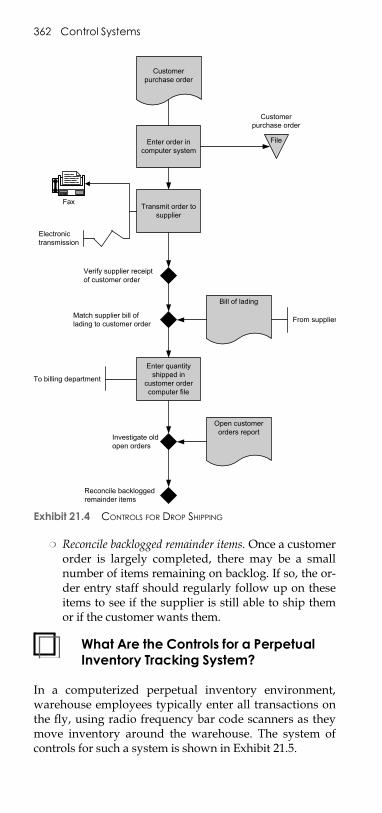

What Are the Controls for Drop-Shipped Orders? � 361

Contents xxi

E1FTOC 03/10/2010 Page 22

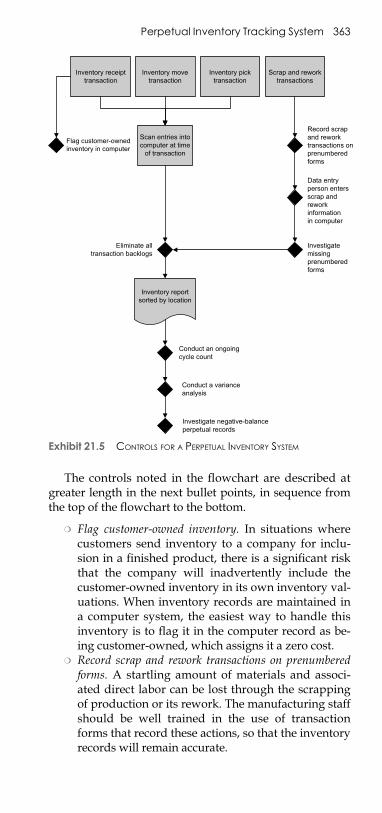

What Are the Controls for aPerpetual InventoryTracking System? � 362

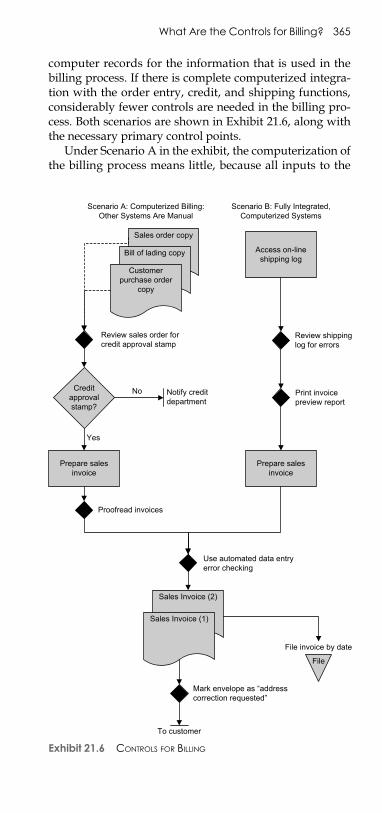

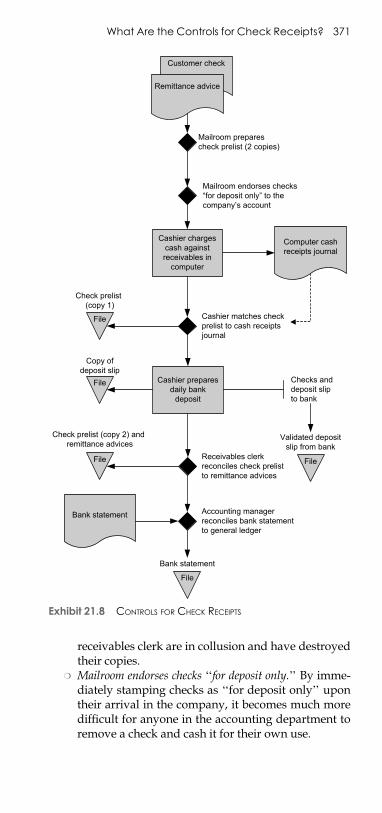

What Are the Controls for Billing? � 364What Are the Controls for

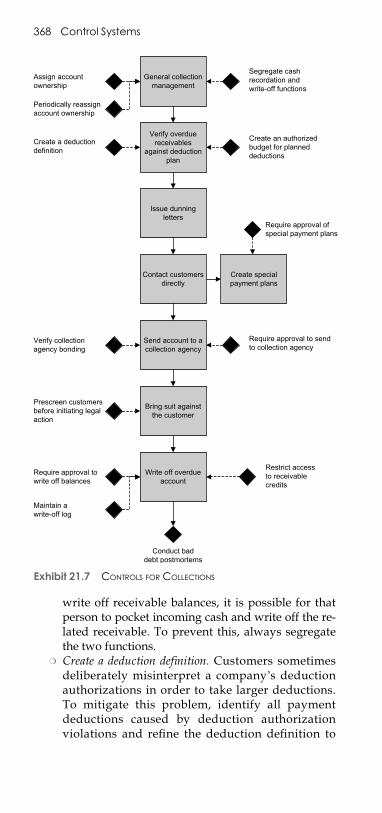

Collections? � 367What Are the Controls for

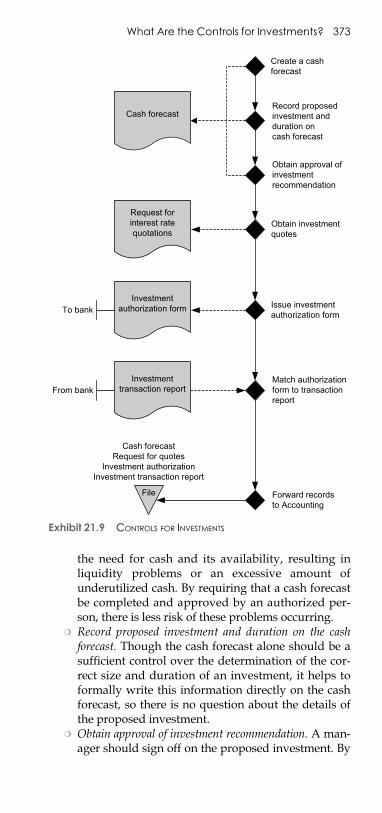

Check Receipts? � 370What Are the Controls for

Investments? � 372What Are the Controls for

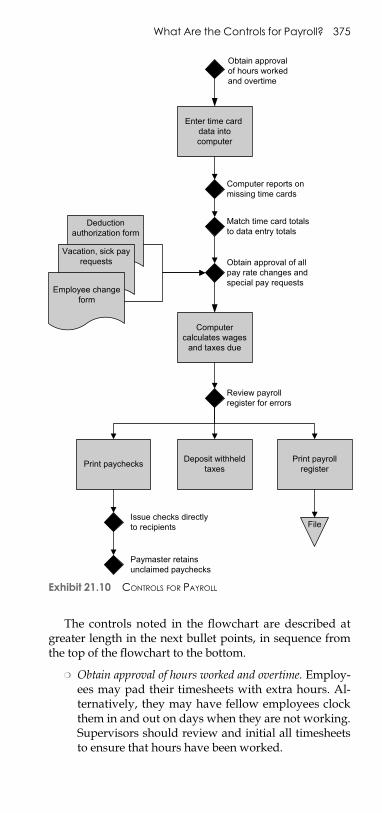

Payroll? � 374

PART V PUBLIC COMPANYACCOUNTING 379

Twenty-Two SEC Filings 381

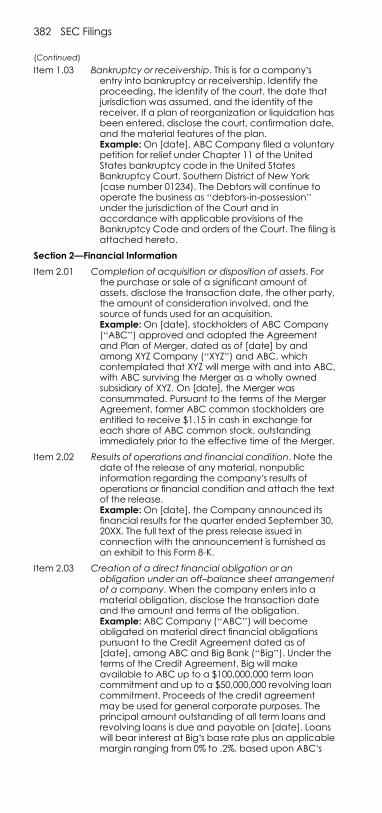

What Is the Form 8-K? � 381What Information Is

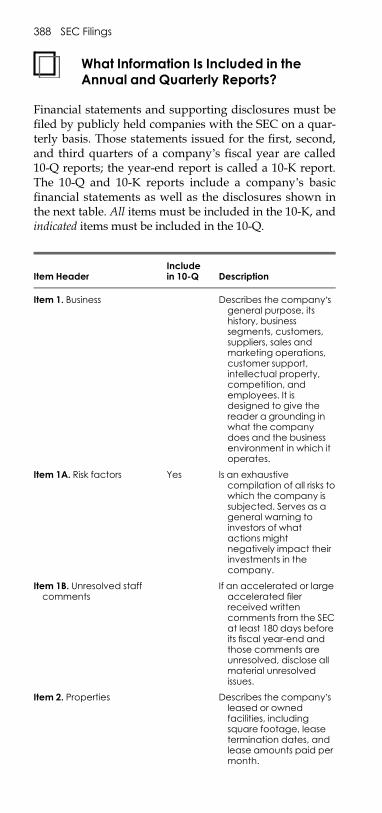

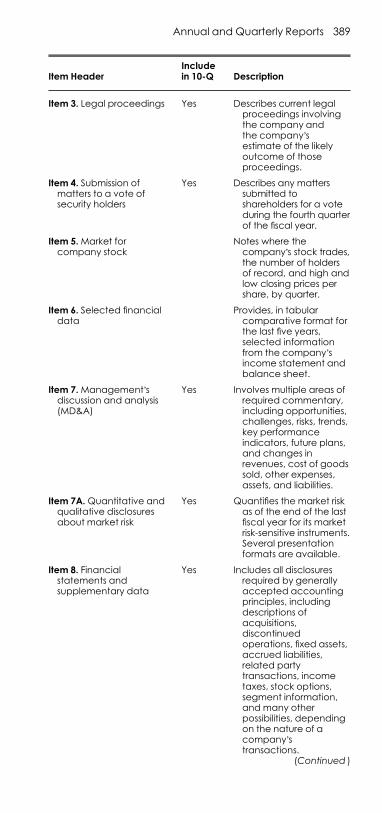

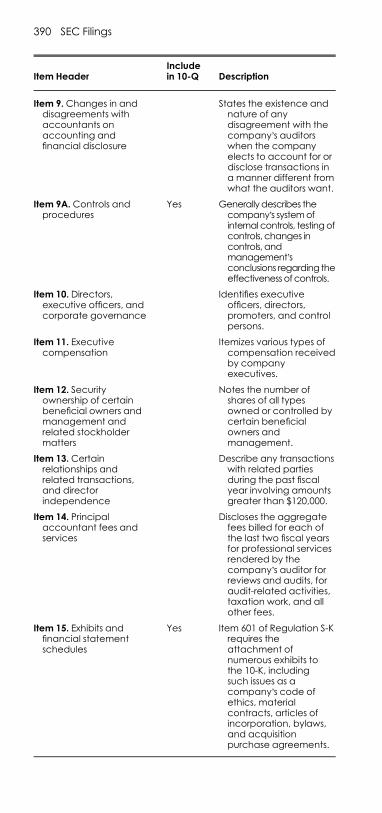

Included in the Annual andQuarterly Reports? � 388

When Must Annual and QuarterlyReports be Filed? � 391

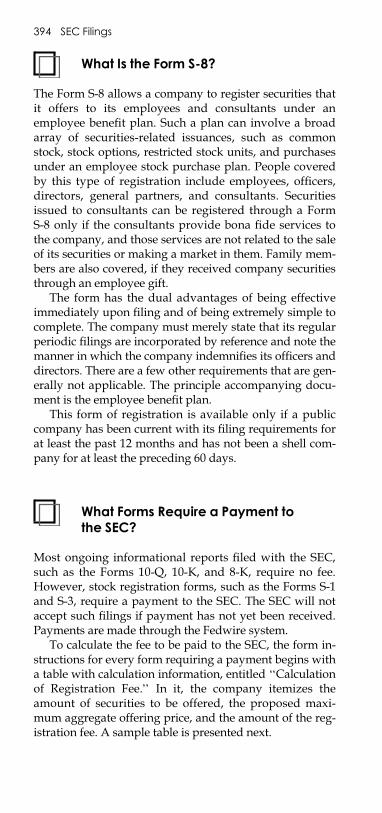

What Is the Form S-1? � 391What Is the Form S-3? � 393What Is the Form S-8? � 394What Forms Require a Payment

to the SEC? � 394How Do I Make a Fedwire

Payment? � 395

Twenty-Three Public Company Accounting Topics 397

When Is Interim ReportingRequired? � 397

What Is the Integral View ofInterim Reporting? � 397

What Is the Discrete View ofInterim Reporting? � 398

How Are Changes in AccountingPrinciple and EstimateAccounted for in InterimPeriods? � 398

xxii Contents

E1FTOC 03/10/2010 Page 23

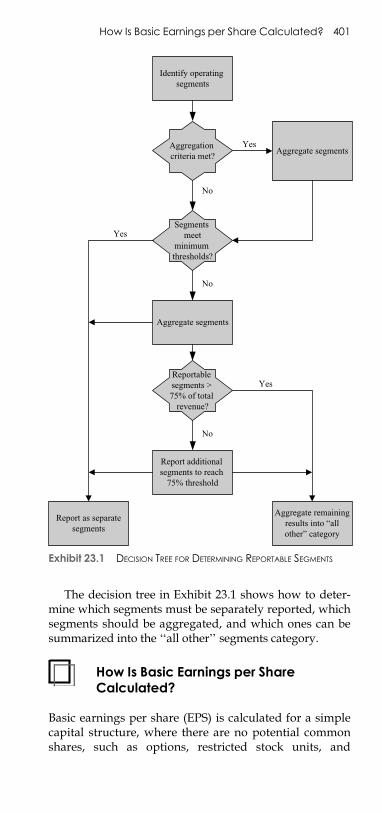

When Is Segment InformationRequired? � 398

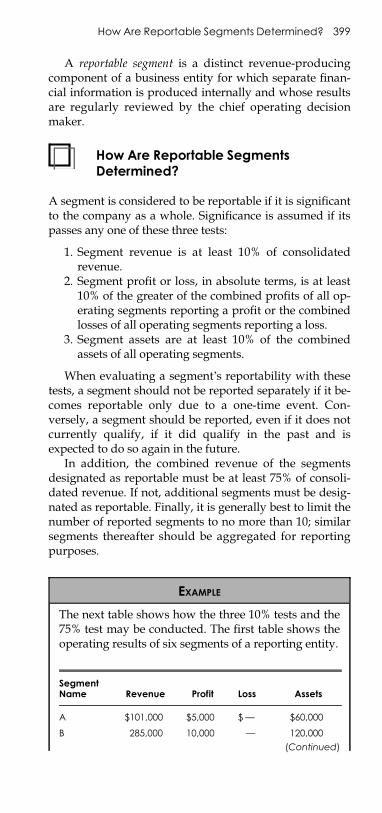

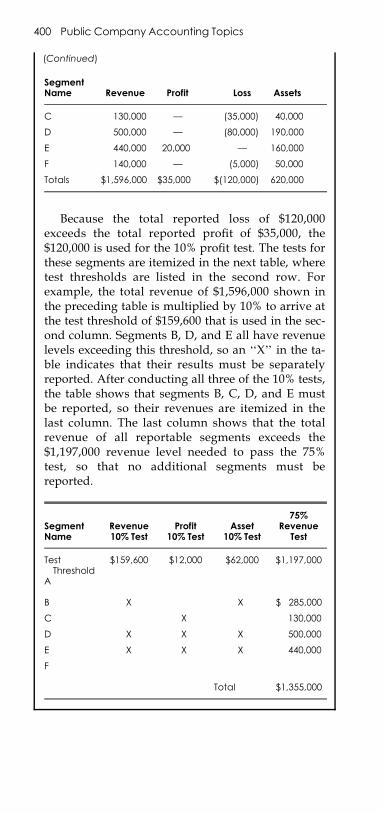

How Are Reportable SegmentsDetermined? � 399

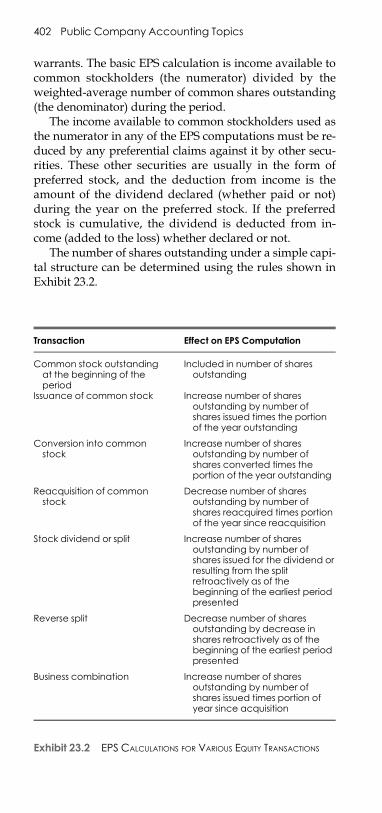

How Is Basic Earnings per ShareCalculated? � 401

How Is Diluted Earnings per ShareCalculated? � 403

What Methods Are Used forCalculating Diluted Earningsper Share? � 403

How Should Non-GAAPInformation Be Disclosed? � 404

Index 405

Contents xxiii

E1FTOC 03/10/2010 Page 24

E1FPREF 03/04/2010 Page 25

PREFACE

This is a handy pocket problem solver for the controller.It covers the multitude of areas that a controller may ad-dress during the working day—accounting standards,management issues, financial analysis, controls, and evenhow to handle a variety of public company issues. It doesso with hundreds of concise explanations that are sup-ported by a multitude of examples, tables, charts, and ra-tios. The layout is designed for quick comprehension ofsuch questions as:

m Should I report revenue at gross or net?m What are the different types of marketable securities,

and how do I account for them?m How do I use the FIFO and LIFO inventory valua-

tion methods?m How do I account for bond discounts and premiums?m How do I record a treasury stock transaction?m When is a lease a capital lease?m How do I convert foreign currency transactions into

the home currency?m How do I achieve a fast close?m How do I set up cash sweeping or notional pooling?m How do I create a perpetual inventory system?m What exemptions are available for stock registrations?m How do I create a throughput analysis model?m How do I set long-range prices?m How do I create a spend analysis system?m Should I lease an asset or buy it?m What controls should I implement for the core

accounting systems?

Part I (Chapters 1–8) covers the most heavily usedGAAP accounting standards. These standards are segre-gated into the topics of revenue recognition, investments,inventory, fixed assets, debt, stockholders’ equity, leases,and foreign currency accounting. Numerous explanatoryexamples are intermingled with the text.

Part II (Chapters 9–14) addresses a number of manage-ment areas that a controller is likely to encounter. Theseinclude a discussion of the steps needed to close the

xxv

E1FPREF 03/04/2010 Page 26

books, the banking structures needed to marshal cash intothe proper investments, how to accelerate the collection ofreceivables, what can be done to minimize the investmentin inventory, what types of debt are available, and how toregister equity for sale.

Part III (Chapters 15–18) delves into a variety of finan-cial analysis topics, with a particular focus on bottleneckanalysis, how to set prices correctly, and how to reducecosts. Chapter 18 contains a number of the metrics that acontroller is most likely to need, along with helpfulexamples.

Part IV (Chapters 19–21) describes the primary controlsystems that a controller needs to ensure that transactionsare as error-free as possible. It also describes a comprehen-sive budgeting system and how to analyze capital budget-ing proposals so that only truly necessary assets areacquired.

Part V (Chapters 22–23) covers a number of the morecommon reports that must be filed periodically with theSEC as well as the accounting issues that are specific tothe public company: earnings per share, interim reporting,and segment reporting.

Throughout, The Vest Pocket Controller has been struc-tured to provide concise answers to the questions that acontroller is most likely to encounter during a typicalbusiness day. Keep it handy for easy reference and dailyuse.

xxvi Preface

E1FLAST 03/04/2010 Page 27

ABOUT THE AUTHOR

Steven Bragg, CPA, has been the chief financial officer orcontroller of four companies as well as a consulting man-ager at Ernst & Young and auditor at Deloitte & Touche.He received a master’s degree in finance from BentleyCollege, an MBA from Babson College, and a bachelor’sdegree in economics from the University of Maine. He hasbeen the two-time president of the Colorado MountainClub and is an avid alpine skier, mountain biker, and cer-tified master diver. Mr. Bragg resides in Centennial, Colo-rado. He has written the following books through JohnWiley & Sons except where indicated:

Accounting and Finance for Your Small BusinessAccounting Best PracticesAccounting Control Best PracticesAccounting Policies and Procedures ManualAdvanced Accounting Systems (Institute of Internal Auditors)Billing and Collections Best PracticesBusiness Ratios and FormulasThe Controller’s FunctionController’s Guide to CostingController’s Guide to Planning and Controlling OperationsController’s Guide: Roles and Responsibilities for the New

ControllerControllershipCost AccountingCost Reduction AnalysisEssentials of PayrollFast CloseFinancial AnalysisGAAP GuideGAAP Policies and Procedures ManualGAAS GuideInventory AccountingInventory Best PracticesInvestor RelationsJust-in-Time AccountingManagement Accounting Best PracticesManaging Explosive Corporate GrowthMergers and Acquisitions

xxvii

E1FLAST 03/04/2010 Page 28

The New CFO Financial Leadership ManualOutsourcingPayroll AccountingPayroll Best PracticesRevenue RecognitionRun the Rockies (CMC Press)Running a Public CompanySales and Operations for Your Small BusinessThe Ultimate Accountants’ReferenceThe Vest Pocket ControllerThroughput AccountingTreasury Management

xxviii About the Author

E1FLAST 03/04/2010 Page 29

FREE ONLINERESOURCESBY STEVE BRAGG

Mr. Bragg Steve issues a free accounting best practicespodcast. You can sign up for it at www.accountingtools.com, or access it through iTunes.

xxix

E1FLAST 03/04/2010 Page 30

E1C01 03/04/2010 Page 1

PART I

ACCOUNTINGSTANDARDS

E1C01 03/04/2010 Page 2

E1C01 03/04/2010 Page 3

CHAPTER 1

REVENUE RECOGNITION

When Can I Report Revenue at GrossInstead of Net?

Reporting on a ‘‘gross’’ basis is appropriate when theentity takes ownership of the goods being sold to its cus-tomers, with the risks and rewards of ownership accruingto it. For example, if the entity runs the risk of obsolescenceor spoilage during the period it holds the merchandise,gross reporting would normally be appropriate. However,if the entity merely acts as an agent for the buyer or sellerfrom which it earns a commission, ‘‘net’’ reporting wouldbe more appropriate. These factors are indicators that reve-nue should be recorded at its gross amount:

m The company that is the primary obligor in the ar-rangement is the company responsible for the fulfill-ment of the order, including the acceptability of theproduct or service to the customer.

m The company has general inventory risk. This existsif a company takes title to a product before the prod-uct is ordered by a customer or will take title to theproduct if the customer returns it.

m The company has physical loss inventory risk. Thisexists if the title to the product is transferred to thecompany at the shipping point and then transferredto the customer upon delivery.

m The company establishes the selling price.m The company changes the product or performs part

of the service.m The company has multiple suppliers for the product

or service ordered by the customer.m The company is involved in determining the nature,

type, characteristics, or specifications of the productor service by the customer.

m The company has credit risk for the amount billed tothe customer. This exists if the company must pay

3

E1C01 03/04/2010 Page 4

the supplier irrespective of whether the customerhas paid.

A company should record revenue at its net value if apreponderance of the preceding bullet points were not thecase, and especially if it is being paid what is in essence acommission.

How Does the Installment Method Work?

Under the installment method, revenue recognition isdeferred until the period of cash collection. The seller rec-ognizes both revenues and cost of sales at the time of thesale; however, the related gross profit is deferred to thoseperiods in which cash is collected. The installment methodcan be used in most sales transactions for which paymentis to be made through periodic installments over anextended period of time and the collectibility of the salesprice cannot be reasonably estimated. This method is ap-plicable to the sales of real estate, heavy equipment, homefurnishings, and other merchandise sold on an installmentbasis. The six to use in accounting for sales under the in-stallment method are presented next.

1. During the current year, record sales and cost ofsales in the regular manner. Record installment salestransactions separately from other sales. Set up in-stallment accounts receivable identified by the yearof sale (e.g., Installment Accounts Receivable—2010).

2. Record cash collections from installment accountsreceivable. Cash receipts must be properly identifiedas to the year in which the receivable arose.

3. At the end of the current year, transfer installmentsales revenue and installment cost of sales todeferred gross profit properly identified by the yearof sale. Compute the current year’s gross profit rateon installment sales as follows:

Gross profit rate ¼ 1� Cost of installment salesInstallment sales revenue

� �

Alternatively, the gross profit rate can be com-puted as follows:

Gross profit rate ¼Installment sales revenue� Cost of installment sales

Installment sales revenue

4. Apply the current year’s gross profit rate to the cashcollections from the current year’s installment sales

4 Revenue Recognition

E1C01 03/04/2010 Page 5

to compute the realized gross profit from the currentyear’s installment sales.

Realized gross profit ¼Cash collections from current year’s installmentsales� Current year’s gross profit rate

5. Separately apply each of the previous years’ grossprofit rates to cash collections from those years’ in-stallment sales to compute the realized gross profitfrom each of the previous years’ installment sales.

Realized gross profit ¼Cash collections from previous years’ installmentsales� Previous years’ gross profit rate

6. Defer the current year’s unrealized gross profit tofuture years. The deferred gross profit to carry for-ward to future years is computed as follows:

Deferred gross profit ð2010Þ ¼Ending balance installment account receivableð2010Þ �Gross profit rate ð2010Þ

Can I Recognize Revenue When ThereIs a Right of Return?

A company can record revenue from a sales transaction atthe time of the sale if all of the next conditions are met,and the company must accrue any estimated losses (suchas warranty or sales returns) at the same time:

m The sale price is fixed on the sale date.m The buyer is obligated to pay the seller.m The buyer’s payment obligation would not be

changed if the product is subsequently damaged ordestroyed.

m The seller does not have significant future perform-ance obligations connected to the sale.

m The amount of future returns can be reasonablyestimated.

When Can I Record Bill-and-Hold Sales?

In a bill-and-hold situation, a company bills its customerbut stores the sold goods on behalf of the customer. Thisscenario presents a high risk for fraud, since customersmay not agree to or be aware of the sales. Accordingly, all

When Can I Record Bill-and-Hold Sales? 5

E1C01 03/04/2010 Page 6

of the next factors must be present before a bill-and-holdtransaction can be recorded as revenue:

m The customer requests this arrangement.m The customer has a substantial business purpose for

doing so.m There is a fixed delivery schedule to the customer.m The goods are both segregated and ready for shipment.

How Does the Percentage-of-Completion Method Work?

The principal method for recognizing revenue under along-term construction contract is the percentage-of-comple-tion method. It recognizes income as work on a contract (orgroup of closely related contracts) progresses. The re-cognition of revenues and profits is related to costsincurred in providing the services required under thecontract.

Under this method, work in progress (WIP) is accumu-lated in the accounting records. If the cumulative billingsto date under the contract exceed the amount of the WIPplus the portion of the contract’s estimated gross profit at-tributable to that WIP, the contractor recognizes a currentliability captioned ‘‘billings in excess of costs and esti-mated earnings.’’ This liability recognizes the remainingobligation of the contractor to complete additional workprior to recognizing the excess billing as revenue.

If the reverse is true—that is, the accumulated WIP andgross profit earned exceed billings to date—the contractorrecognizes a current asset captioned ‘‘costs and estimatedearnings in excess of billings.’’ This asset represents theportion of the contractor’s revenues under the contractthat have been earned but not yet billed under the con-tract provisions. Where more than one contract exists,these assets and liabilities are determined on a project-by-project basis, with the accumulated assets and liabilitiesbeing separately stated on the balance sheet. Assets andliabilities are not offset unless a right of offset exists. Thus,the net debit balances for certain contracts are not ordinar-ily offset against net credit balances for other contracts.

How Does the Completed-ContractMethod Work?

The completed-contract method recognizes income onlywhen a construction contract is complete or substantially

6 Revenue Recognition

E1C01 03/04/2010 Page 7

complete. It is most commonly used for shorter-durationcontracts or when it is not possible to use the percentage-of-completion method.

Under this method, contract costs and related billingsare accumulated in the accounting records and reportedas deferred items on the balance sheet until the project iscomplete or substantially complete. A contract is regardedas substantially complete if remaining costs of completionare immaterial. When the accumulated costs (WIP) exceedthe related billings, the excess is presented as a current as-set (inventory account). If billings exceed related costs, thedifference is presented as a current liability. This determi-nation is also made on a project-by-project basis with theaccumulated assets and liabilities being stated separatelyon the balance sheet. An excess of accumulated costs overrelated billings is presented as a current asset, and in mostcases an excess of accumulated billings over related costsis presented as a current liability.

What Types of Pricing ArrangementsAre Used in Contracts?

There are four types of contracts based on their pricingarrangements.

1. Fixed-price contracts. Contracts for which the price isnot usually subject to adjustment because of costsincurred by the contractor. The contractor bears therisks of cost overruns.

2. Time-and-materials contracts. Contracts that providefor payments to the contractor based on direct laborhours at fixed rates and the contractor’s cost ofmaterials.

3. Cost-type contracts. Contracts that provide for reim-bursement of allowable or otherwise defined costsincurred plus a fee representing profits.

4. Unit-price contracts. Contracts under which the con-tractor is paid a specified amount for every unit ofwork performed.

EXAMPLE

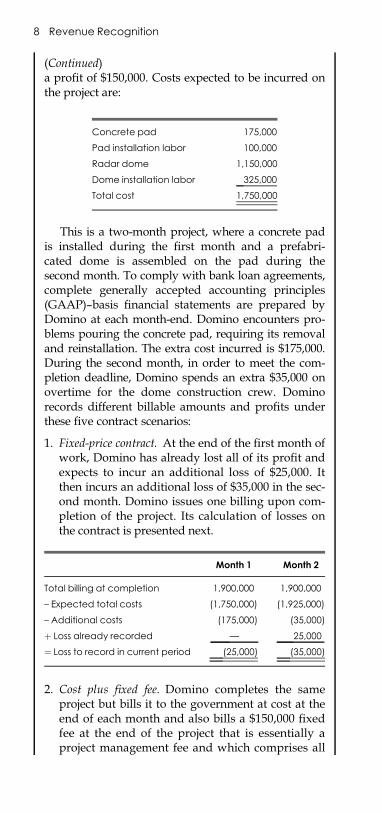

Domino Construction Inc. enters into a governmentcontract to construct an early warning radar dome.The contract amount is for $1,900,000, on whichDomino expects to incur costs of $1,750,000 and earn

(Continued)

Types of Pricing 7

E1C01 03/04/2010 Page 8

(Continued)a profit of $150,000. Costs expected to be incurred onthe project are:

Concrete pad 175,000

Pad installation labor 100,000

Radar dome 1,150,000

Dome installation labor 325,000

Total cost 1,750,000

This is a two-month project, where a concrete padis installed during the first month and a prefabri-cated dome is assembled on the pad during thesecond month. To comply with bank loan agreements,complete generally accepted accounting principles(GAAP)–basis financial statements are prepared byDomino at each month-end. Domino encounters pro-blems pouring the concrete pad, requiring its removaland reinstallation. The extra cost incurred is $175,000.During the second month, in order to meet the com-pletion deadline, Domino spends an extra $35,000 onovertime for the dome construction crew. Dominorecords different billable amounts and profits underthese five contract scenarios:

1. Fixed-price contract. At the end of the first month ofwork, Domino has already lost all of its profit andexpects to incur an additional loss of $25,000. Itthen incurs an additional loss of $35,000 in the sec-ond month. Domino issues one billing upon com-pletion of the project. Its calculation of losses onthe contract is presented next.

Month 1 Month 2

Total billing at completion 1,900,000 1,900,000

– Expected total costs (1,750,000) (1,925,000)

– Additional costs (175,000) (35,000)

þ Loss already recorded — 25,000

¼ Loss to record in current period (25,000) (35,000)

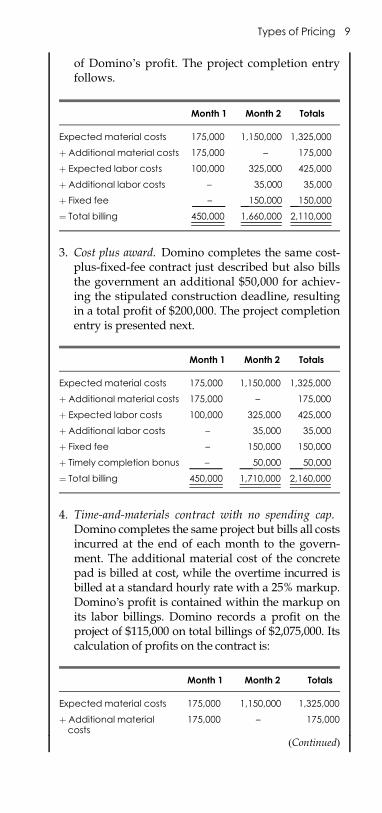

2. Cost plus fixed fee. Domino completes the sameproject but bills it to the government at cost at theend of each month and also bills a $150,000 fixedfee at the end of the project that is essentially aproject management fee and which comprises all

8 Revenue Recognition

E1C01 03/04/2010 Page 9

of Domino’s profit. The project completion entryfollows.

Month 1 Month 2 Totals

Expected material costs 175,000 1,150,000 1,325,000

þ Additional material costs 175,000 – 175,000

þ Expected labor costs 100,000 325,000 425,000

þ Additional labor costs – 35,000 35,000

þ Fixed fee 100–0 150,000 150,000

¼ Total billing 450,000 1,660,000 2,110,000

3. Cost plus award. Domino completes the same cost-plus-fixed-fee contract just described but also billsthe government an additional $50,000 for achiev-ing the stipulated construction deadline, resultingin a total profit of $200,000. The project completionentry is presented next.

Month 1 Month 2 Totals

Expected material costs 175,000 1,150,000 1,325,000

þ Additional material costs 175,000 – 175,000

þ Expected labor costs 100,000 325,000 425,000

þ Additional labor costs – 35,000 35,000

þ Fixed fee – 150,000 150,000

þ Timely completion bonus 100–0 50,000 50,000

¼ Total billing 450,000 1,710,000 2,160,000

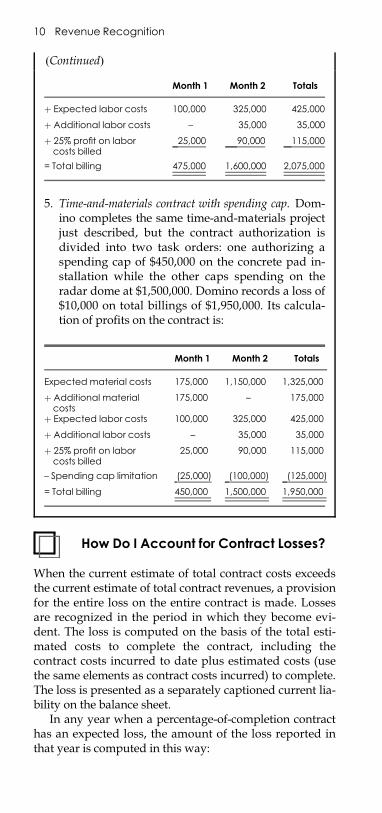

4. Time-and-materials contract with no spending cap.Domino completes the same project but bills all costsincurred at the end of each month to the govern-ment. The additional material cost of the concretepad is billed at cost, while the overtime incurred isbilled at a standard hourly rate with a 25% markup.Domino’s profit is contained within the markup onits labor billings. Domino records a profit on theproject of $115,000 on total billings of $2,075,000. Itscalculation of profits on the contract is:

Month 1 Month 2 Totals

Expected material costs 175,000 1,150,000 1,325,000

þ Additional materialcosts

175,000 – 175,000

(Continued)

Types of Pricing 9

E1C01 03/04/2010 Page 10

How Do I Account for Contract Losses?

When the current estimate of total contract costs exceedsthe current estimate of total contract revenues, a provisionfor the entire loss on the entire contract is made. Lossesare recognized in the period in which they become evi-dent. The loss is computed on the basis of the total esti-mated costs to complete the contract, including thecontract costs incurred to date plus estimated costs (usethe same elements as contract costs incurred) to complete.The loss is presented as a separately captioned current lia-bility on the balance sheet.

In any year when a percentage-of-completion contracthas an expected loss, the amount of the loss reported inthat year is computed in this way:

Month 1 Month 2 Totals

þ Expected labor costs 100,000 325,000 425,000

þ Additional labor costs – 35,000 35,000

þ 25% profit on laborcosts billed

25,000 90,000 115,000

= Total billing 475,000 1,600,000 2,075,000

5. Time-and-materials contract with spending cap. Dom-ino completes the same time-and-materials projectjust described, but the contract authorization isdivided into two task orders: one authorizing aspending cap of $450,000 on the concrete pad in-stallation while the other caps spending on theradar dome at $1,500,000. Domino records a loss of$10,000 on total billings of $1,950,000. Its calcula-tion of profits on the contract is:

Month 1 Month 2 Totals

Expected material costs 175,000 1,150,000 1,325,000

þ Additional materialcosts

175,000 – 175,000

þ Expected labor costs 100,000 325,000 425,000

þ Additional labor costs – 35,000 35,000

þ 25% profit on laborcosts billed

25,000 90,000 115,000

– Spending cap limitation (25,000) (100,000) (125,000)

= Total billing 450,000 1,500,000 1,950,000

(Continued)

10 Revenue Recognition

E1C01 03/04/2010 Page 11

Reported loss ¼Total expected lossþAll profit previously recognized

How Do I Account for Additional Claimsunder a Contract?

Claims represent amounts in excess of the agreed-on con-tract price that a contractor seeks to collect from custom-ers for unanticipated additional costs. The recognition ofadditional contract revenue relating to claims is appro-priate if it is probable that the claim will result in addi-tional revenue and if the amount can be estimatedreliably. All of the next four conditions must exist inorder for the probable and estimable requirements tobe satisfied.

1. The contract or other evidence provides a legal basisfor the claim.

2. Additional costs are not the result of deficiencies inthe contractor’s performance.

3. Additional costs are identifiable and reasonable.4. The evidence supporting the claim is objective and

verifiable, not based on management’s ‘‘feel’’ for thesituation or on unsupported representations.

How Does the Deposit Method Work?

The deposit method is used in a real estate sale where thesale is, in substance, the sale of an option and not realestate. The seller does not recognize any profit and doesnot record a receivable. Cash received from the buyer(initial and continuing investments) is reported as a de-posit on the contract. However, some cash may be re-ceived that is not subject to refund, such as interest onthe unrecorded principal. These amounts are used to off-set any carrying charges on the property. If the interestcollected on the unrecorded receivable is refundable, theseller records this interest as a deposit before the sale iscompleted and then includes it as a part of the initial in-vestment once the sale is consummated. If deposits onretail land sales eventually are recognized as sales, theinterest portion of the deposit is recognized separatelyas interest income. For contracts that are canceled, thenonrefundable amounts are recognized as income andthe refundable amounts are returned to the depositor atthe time of cancellation.

How Does the Deposit MethodWork? 11

E1C01 03/04/2010 Page 12

EXAMPLE

Elbrus Investments enters into two separate propertyacquisition transactions with the Buena Vista LandCompany.

1. Elbrus pays a $50,000 deposit and promises to payan additional $800,000 to buy land and a buildingin an area not yet properly zoned for the facilityElbrus intends to construct. Final acquisition of theproperty is contingent upon these zoning changes.Buena Vista does not record the receivable, and re-cords the deposit with the following entry:

Cash 50,000

Customer deposits 50,000

Part of the purchase agreement stipulates thatBuena Vista will retain all interest earned on the de-posit and that 10% of the deposit is nonrefundable.Buena Vista earns 5% interest on Elbrus’s depositover a period of four months, resulting in $208 ofinterest income that is offset against the propertytax expenses of the property with the next entry:

Cash 208

Property tax expense 208

Immediately thereafter, the required zoningchanges are turned down, and Elbrus cancels thesales contract. Buena Vista returns the refundableportion of the deposit to Elbrus and records thenonrefundable portion as income with this entry:

Customer deposits 50,000

Income from contract cancellation 10,000

Cash 40,000

2. Elbrus pays a $40,000 deposit on land owned andbeing improved by Buena Vista. Elbrus immedi-ately begins paying $5,000/month under a four-year, 7% loan agreement totaling $212,000 of prin-cipal payments and agrees to pay an additional$350,000 at closing, subject to the land being ap-proved for residential construction. After two

12 Revenue Recognition

E1C01 03/04/2010 Page 13

How Do I Account for Installation Fees?

A fee may be charged to install equipment. If customersnormally cannot purchase the equipment in a separatetransaction, the installation fee is considered an advancecharge for future services. The fee is recognized as reve-nue over the estimated service period. The costs of instal-lation and the installed equipment are amortized over theperiod the equipment is expected to generate revenue. Ifcustomers normally can purchase the equipment in a sep-arate transaction, the installation fee is part of a producttransaction that is accounted for separately as such.

months, Buena Vista has earned $167 of refundableinterest income on Elbrus’s deposit and has beenpaid $7,689 of refundable principal and $2,311 ofrefundable interest on the debt. Buena Vista re-cords these events with the next entry.

Cash 10,167

Customer deposits 10,167

The land is approved for residential construc-tion, triggering sale of the property. Buena Vista’sbasis in the property is $520,000. Buena Vista usesthe next entry to describe completion of the sale.

Cash 350,000

Note receivable 204,311

Customer deposits 50,167

Gain on asset sale 84,478

Land 520,000

EXAMPLE

Vintner Corporation has invented a nitrogen injectiondevice for resealing opened wine bottles, which itcalls NitroSeal. The device is especially useful for res-taurants, which can seal wine bottles opened for cus-tomers who want to take home unfinished wine.Because the NitroSeal device is massive, Vintner pays

(Continued)

How Do I Account for Installation Fees? 13

E1C01 03/04/2010 Page 14

(Continued)a third party to install each unit for a fixed fee of $200,charging restaurants a $300 nonrefundable installa-tion fee plus a monthly fee for a 20-month cancelablecontract. The initial entries to record an installationcharge from a supplier and related installation billingto a customer are:

Installation asset 200

Accounts payable 200

Accounts receivable 300

Unearned installation fees (liability) 300

Vintner recognizes the installation revenue and as-sociated installation expense for each installation in1/20 increments to match the contract length, eachwith this entry:

Unearned installation fees 15

Installation revenue 15

Installation expense 10

Installation asset 10

A customer cancels its contract with Vintner after5 months. As a result, Vintner accelerates all remain-ing amortization on the installation asset and recog-nizes all remaining unearned installation fees at once,using the next entries.

Unearned installation fees 225

Installation revenue 225

Installation expense 150

Installation asset 150

If the service contract had included a clause for arefundable installation fee, then cancelation after fivemonths would still have resulted in immediate accel-eration of amortization on the installation asset. How-ever, the unearned installation revenue could not berecognized. Instead, this entry would have recordedthe return of the installation fee:

Unearned installation fees 225

Cash 225

14 Revenue Recognition

E1C01 03/04/2010 Page 15

What Recognition Methods Can I Usefor Service Billings?

Once a transaction is determined to be a service transac-tion, one of four methods is used to recognize revenue.The method chosen is to be based on the nature and extentof the service(s) to be performed.

1. Specific performance method. This method is usedwhen performance consists of the execution of a sin-gle act. Revenue is recognized at the time the acttakes place. For example, a stockbroker records salescommissions as revenue upon the sale of a client’sinvestment.

2. Proportional performance method. This method is usedwhen performance consists of a number of identicalor similar acts.

a. If the service transaction involves a specified num-ber of identical or similar acts, an equal amount ofrevenue is recorded for each act performed.

b. If the service transaction involves a specifiednumber of defined but not identical or similaracts, the revenue recognized for each act is basedon this formula:

Direct cost of individual actTotal estimated direct costs of the transaction

� Total revenues from complete transaction

c. If the service transaction involves an unspecifiednumber of acts over a fixed time period for per-formance, revenue is recognized over the periodduring which the acts will be performed by usingthe straight-line method unless a better method ofrelating revenue and performance is appropriate.

EXAMPLE

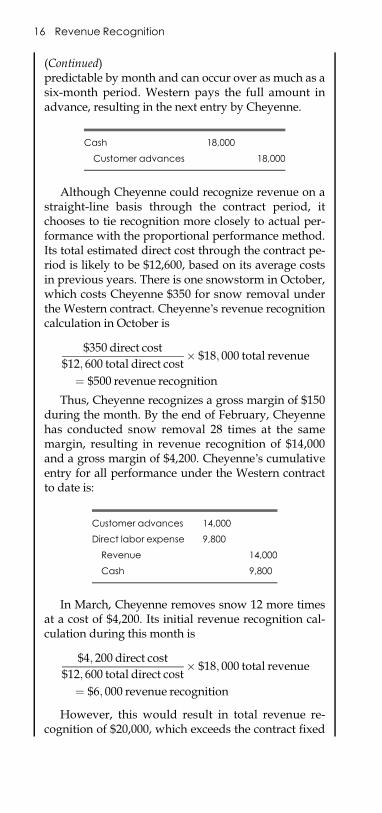

The Cheyenne Snow Removal Company enters into acontract with the Western Office Tower to plow itsparking lot. The contract states that Cheyenne will re-ceive a fixed payment of $500 to clear Western’s centralparking lot whenever snowfall exceeds two inches.Following an unusually snowy winter, Western electsto cap its snow removal costs by tying Cheyenne intoan annual $18,000 fixed price for snow removal, nomatter how many snowstorms occur. Snowfall is not

(Continued)

Recognition Methods 15

E1C01 03/04/2010 Page 16

(Continued)predictable by month and can occur over as much as asix-month period. Western pays the full amount inadvance, resulting in the next entry by Cheyenne.

Cash 18,000

Customer advances 18,000

Although Cheyenne could recognize revenue on astraight-line basis through the contract period, itchooses to tie recognition more closely to actual per-formance with the proportional performance method.Its total estimated direct cost through the contract pe-riod is likely to be $12,600, based on its average costsin previous years. There is one snowstorm in October,which costs Cheyenne $350 for snow removal underthe Western contract. Cheyenne’s revenue recognitioncalculation in October is

$350 direct cost$12; 600 total direct cost

� $18; 000 total revenue

¼ $500 revenue recognition

Thus, Cheyenne recognizes a gross margin of $150during the month. By the end of February, Cheyennehas conducted snow removal 28 times at the samemargin, resulting in revenue recognition of $14,000and a gross margin of $4,200. Cheyenne’s cumulativeentry for all performance under the Western contractto date is:

Customer advances 14,000

Direct labor expense 9,800

Revenue 14,000

Cash 9,800

In March, Cheyenne removes snow 12 more timesat a cost of $4,200. Its initial revenue recognition cal-culation during this month is

$4; 200 direct cost$12; 600 total direct cost

� $18; 000 total revenue

¼ $6; 000 revenue recognition

However, this would result in total revenue re-cognition of $20,000, which exceeds the contract fixed

16 Revenue Recognition

E1C01 03/04/2010 Page 17

3. Completed performance method. This method is usedwhen more than one act must be performed andwhen the final act is so significant to the entire trans-action taken as a whole that performance cannot beconsidered to have taken place until the perform-ance of that final act occurs.

4. Collection method. This method is used in circum-stances when there is a significant degree of uncer-tainty surrounding the collection of service revenue.Under this method, revenue is not recognized untilthe cash is collected.

How Do I Record Revenue forFranchise Sales?

Revenue is recognized, with a provision for bad debts,when the franchisor has substantially performed all mate-rial services or conditions. Only when revenue is collectedover an extended period of time and collectibility cannotbe predicted in advance would the use of the installmentmethod of revenue recognition be appropriate. Substan-tial performance means:

m The franchisor has no remaining obligation to eitherrefund cash or forgive any unpaid balance due.

m Substantially all initial services required by theagreement have been performed.

m No material obligations or conditions remain.

If initial franchise fees are large compared to servicesrendered and continuing franchise fees are small com-pared to services to be rendered, a portion of the initial feeis deferred in an amount sufficient to cover the costs offuture services plus a reasonable profit, after consideringthe impact of the continuing franchise fee.

fee by $2,000. Accordingly, Cheyenne only recognizessufficient revenue to maximize the contract cap, re-sulting in a loss of $200 for the month.

Customer advances 4,000

Direct labor expense 4,200

Revenue 4,000

Cash 4,200

How Do I Record Revenue for Franchise Sales? 17

E1C01 03/04/2010 Page 18

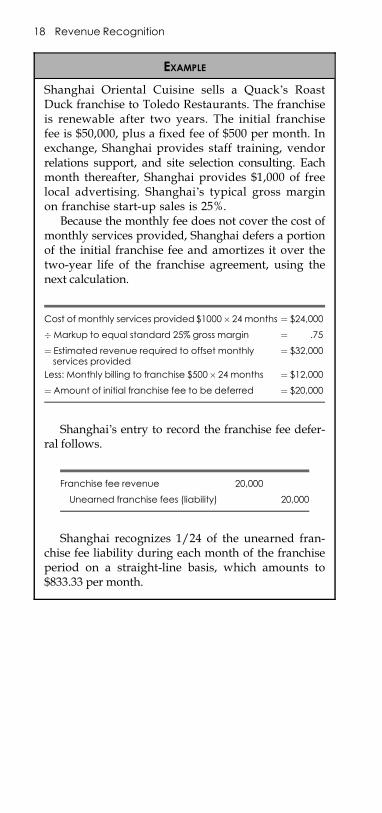

EXAMPLE

Shanghai Oriental Cuisine sells a Quack’s RoastDuck franchise to Toledo Restaurants. The franchiseis renewable after two years. The initial franchisefee is $50,000, plus a fixed fee of $500 per month. Inexchange, Shanghai provides staff training, vendorrelations support, and site selection consulting. Eachmonth thereafter, Shanghai provides $1,000 of freelocal advertising. Shanghai’s typical gross marginon franchise start-up sales is 25%.

Because the monthly fee does not cover the cost ofmonthly services provided, Shanghai defers a portionof the initial franchise fee and amortizes it over thetwo-year life of the franchise agreement, using thenext calculation.

Cost of monthly services provided$1000� 24 months ¼ $24,000

�Markup to equal standard 25% gross margin ¼ .75

¼ Estimated revenue required to offset monthlyservices provided

¼ $32,000

Less: Monthly billing to franchise $500� 24 months ¼ $12,000

¼ Amount of initial franchise fee to be deferred ¼ $20,000

Shanghai’s entry to record the franchise fee defer-ral follows.

Franchise fee revenue 20,000

Unearned franchise fees (liability) 20,000

Shanghai recognizes 1/24 of the unearned fran-chise fee liability during each month of the franchiseperiod on a straight-line basis, which amounts to$833.33 per month.

18 Revenue Recognition

E1C02 03/04/2010 Page 19

CHAPTER 2

INVESTMENT ACCOUNTING

Which Securities Are Designated asMarketable Equity Securities?

Marketable securities are investments that can be easilyliquidated through an organized exchange, such as theNew York Stock Exchange. If a company also holds secu-rities that are intended for the control of another entity,these securities should be segregated as a long-term in-vestment. Marketable securities must be grouped into oneof three categories at the time of purchase and reevaluatedperiodically to see if they still belong in the designatedcategories:

1. Available for sale. This category includes both debtand equity securities. It contains those securities thatdo not readily fall into either of the next two catego-ries. It can include investments in other companiesthat comprise less than 20% of total ownership.

2. Held to maturity. This category includes only debt se-curities for which the company has both the intentand the ability to hold them until their time ofmaturity.

3. Trading securities. This category includes both debtand equity securities that the company intends tosell in the short term for a profit. It can include in-vestments in other companies comprising less than20% of total ownership.

What Is the Accounting for MarketableEquity Securities?

Available-for-sale securities are reported on the balancesheet at their fair value, while unrealized gains and lossesare charged to an equity account and reported in othercomprehensive income in the current period. The balancein the equity account is eliminated only upon sale of the

19

E1C02 03/04/2010 Page 20

underlying securities. If a permanent reduction in thevalue of an individual security occurs, the unrealized lossis charged against earnings, resulting in a new and lowercost basis in the remaining investment. Any subsequentincrease in the value of such an investment above the newcost basis cannot be formally recognized in earnings untilthe related security is sold, and so the interim gains will betemporarily parked in the unrealized gains account in theequity section of the balance sheet.

All interest, realized gains or losses, and debt amorti-zation for available-for-sale securities are recognizedwithin the continuing operations section of the incomestatement. The listing of these securities on the balancesheet under either current or long-term assets is depen-dent on their ability to be liquidated in the short term andto be available for disposition within that time frame, un-encumbered by any obligations.

The amortized cost of held-to-maturity securities is re-corded on the balance sheet. These securities are likely tobe listed on the balance sheet as long-term assets. If mar-ketable securities are shifted into the held-to-maturity cate-gory from debt securities in the available-for-sale category,their unrealized holding gain or loss should continue to bestored in the equity section while being gradually amor-tized down to zero over the remaining life of each security.

Trading securities are recorded on the balance sheet attheir fair value. This type of security is always positionedin the balance sheet as a current asset.

EXAMPLE

AVAILABLE-FOR-SALE TRANSACTIONS

The Arabian Knights Security Company has pur-chased $100,000 of equity securities, which it does notintend to sell in the short term for profit, and thereforedesignates as available for sale. Its initial entry to re-cord the transaction is:

Debit Credit

Investments—available for sale $100,000

Cash $100,000

After a month, the fair market value of the securi-ties drops by $15,000, but management considers the

20 Investment Accounting

E1C02 03/04/2010 Page 21

loss to be a temporary decline, and so does not recorda loss in current earnings. However, it must still alterthe value of the investment on the balance sheet toshow its fair value, and report the loss in Other Com-prehensive Income, which requires this entry:

Debit Credit

Unrealized loss on security investment(reported in Other ComprehensiveIncome)

$15,000

Investments—available for sale $15,000

Management then obtains additional informationindicating that the loss is likely to be a permanentone, so it then recognizes the loss with this entry:

Debit Credit

Loss on equity securities $15,000

Unrealized loss on security investment(reported in Other ComprehensiveIncome)

$15,000

Another month passes by and the fair value of theinvestment rises by $3,500. Since this gain exceeds thevalue of the newly written-down investment, man-agement cannot recognize it, even though the newvalue of the investment would still be less than itsoriginal amount. Instead, this entry is used to adjustthe investment value on the balance sheet:

Debit Credit

Investments—available for sale $3,500

Unrealized gain on security investment(recorded in Other ComprehensiveIncome)

$3,500

EXAMPLE

TRADING TRANSACTIONS

The Arabian Knights Security Company purchases$50,000 of equity securities that it intends to trade fora profit in the short term. Given its intentions, these

(Continued)

Accounting for Marketable Equity 21

E1C02 03/04/2010 Page 22

What Is the Accounting for Transfersbetween Available-for-Sale andTrading Investments?

An investment designated as a trading security can beshifted into the available for sale portfolio of investmentswith no recognition of a gain or loss on the value of theinvestment, since this type of investment should havebeen adjusted to its fair value in each reporting period al-ready. If a gain or loss has arisen since the last adjustmentto fair value, this amount should be recognized at the timeof the designation change.

If an investment designated as an available-for-sale se-curity is shifted into the trading portfolio of investments,any gain or loss required to immediately adjust its valueto fair value should be made at once. This entry should

(Continued)securities are added to the corporate portfolio of trad-ing securities with this entry:

Debit Credit

Investments—held for trading $50,000

Cash $50,000

After two months, the fair value of these tradingsecurities declines by $3,500. The company recognizesthe change in current earnings with this entry:

Debit Credit

Loss on security investment $3,500

Investments—held for trading $3,500

Later in the year, the fair value of the securitiesexperiences a sudden surge, resulting in a value in-crease of $5,750. The company records the changewith this entry:

Debit Credit

Investments—held for trading $5,750

Gain on security investments $5,750

22 Investment Accounting

E1C02 03/04/2010 Page 23

include an adjustment from any prior write-down invalue that may have occurred when securities were classi-fied as available for sale.

EXAMPLE

TRANSFER FROM THE TRADING PORTFOLIO TO THE

AVAILABLE-FOR-SALE PORTFOLIO

The Arabian Knights Security Company owns $17,500of equity securities that it had originally intended tosell for a profit in the short term and so had classifiedthe investment in its trading portfolio. Its intent hasnow changed, and it wishes to hold the securitiesfor a considerably longer period, so it must shift thesecurities into the available-for-sale account. It hadmarked the securities to market one month previ-ously, but now the securities have lost $350 of value.The company records the next entry to reclassify thesecurity and recognize the additional loss:

Debit Credit

Investments—available for sale $17,150

Loss on equity securities 350

Investments—held for trading $17,500

EXAMPLE

TRANSFER FROM THE AVAILABLE-FOR-SALE

PORTFOLIO TO THE TRADING PORTFOLIO

The Arabian Knights Security Company finds that itmust liquidate $250,000 of its available-for-sale port-folio in the short term. This investment had previ-ously been marked down to $250,000 from an initialinvestment value of $275,000, and its value has sincerisen by $12,000. The incremental gain must now berecognized in current income. The entry is:

Debit Credit

Investments—held for trading $262,000

Investments—available for sale $250,000

Gain on security investments 12,000

Accounting for Transfers 23

E1C02 03/04/2010 Page 24

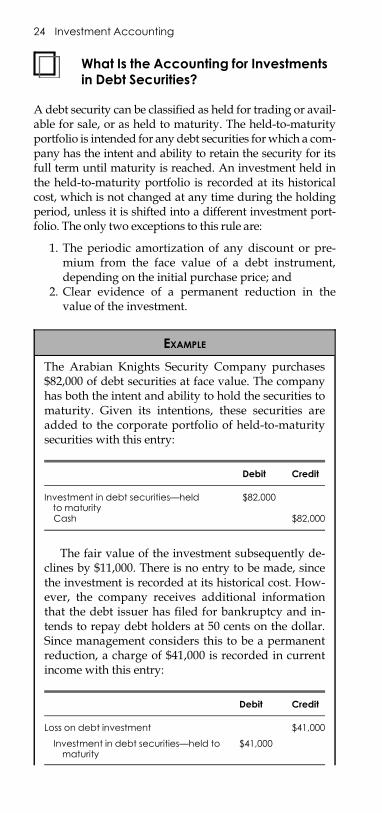

What Is the Accounting for Investmentsin Debt Securities?

A debt security can be classified as held for trading or avail-able for sale, or as held to maturity. The held-to-maturityportfolio is intended for any debt securities forwhich a com-pany has the intent and ability to retain the security for itsfull term until maturity is reached. An investment held inthe held-to-maturity portfolio is recorded at its historicalcost, which is not changed at any time during the holdingperiod, unless it is shifted into a different investment port-folio. The only two exceptions to this rule are:

1. The periodic amortization of any discount or pre-mium from the face value of a debt instrument,depending on the initial purchase price; and

2. Clear evidence of a permanent reduction in thevalue of the investment.

EXAMPLE

The Arabian Knights Security Company purchases$82,000 of debt securities at face value. The companyhas both the intent and ability to hold the securities tomaturity. Given its intentions, these securities areadded to the corporate portfolio of held-to-maturitysecurities with this entry:

Debit Credit

Investment in debt securities—heldto maturity

$82,000

Cash $82,000

The fair value of the investment subsequently de-clines by $11,000. There is no entry to be made, sincethe investment is recorded at its historical cost. How-ever, the company receives additional informationthat the debt issuer has filed for bankruptcy and in-tends to repay debt holders at 50 cents on the dollar.Since management considers this to be a permanentreduction, a charge of $41,000 is recorded in currentincome with this entry:

Debit Credit

Loss on debt investment $41,000

Investment in debt securities—held tomaturity

$41,000

24 Investment Accounting

E1C02 03/04/2010 Page 25

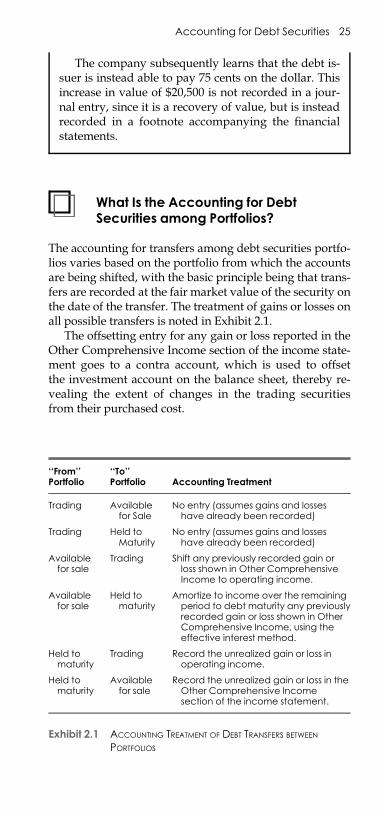

What Is the Accounting for DebtSecurities among Portfolios?

The accounting for transfers among debt securities portfo-lios varies based on the portfolio from which the accountsare being shifted, with the basic principle being that trans-fers are recorded at the fair market value of the security onthe date of the transfer. The treatment of gains or losses onall possible transfers is noted in Exhibit 2.1.

The offsetting entry for any gain or loss reported in theOther Comprehensive Income section of the income state-ment goes to a contra account, which is used to offsetthe investment account on the balance sheet, thereby re-vealing the extent of changes in the trading securitiesfrom their purchased cost.

The company subsequently learns that the debt is-suer is instead able to pay 75 cents on the dollar. Thisincrease in value of $20,500 is not recorded in a jour-nal entry, since it is a recovery of value, but is insteadrecorded in a footnote accompanying the financialstatements.

‘‘From’’Portfolio

‘‘To’’Portfolio Accounting Treatment

Trading Availablefor Sale

No entry (assumes gains and losseshave already been recorded)

Trading Held toMaturity

No entry (assumes gains and losseshave already been recorded)

Availablefor sale

Trading Shift any previously recorded gain orloss shown in Other ComprehensiveIncome to operating income.

Availablefor sale

Held tomaturity

Amortize to income over the remainingperiod to debt maturity any previouslyrecorded gain or loss shown in OtherComprehensive Income, using theeffective interest method.

Held tomaturity

Trading Record the unrealized gain or loss inoperating income.

Held tomaturity

Availablefor sale

Record the unrealized gain or loss in theOther Comprehensive Incomesection of the income statement.

Exhibit 2.1 ACCOUNTING TREATMENT OF DEBT TRANSFERS BETWEEN

PORTFOLIOS

Accounting for Debt Securities 25

E1C02 03/04/2010 Page 26

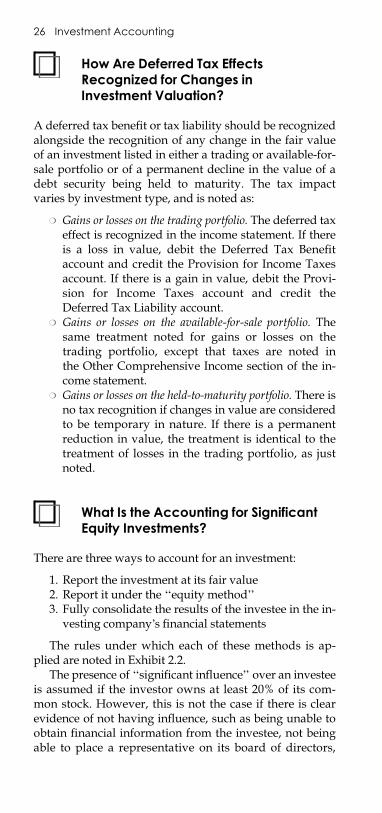

How Are Deferred Tax EffectsRecognized for Changes inInvestment Valuation?

A deferred tax benefit or tax liability should be recognizedalongside the recognition of any change in the fair valueof an investment listed in either a trading or available-for-sale portfolio or of a permanent decline in the value of adebt security being held to maturity. The tax impactvaries by investment type, and is noted as:

m Gains or losses on the trading portfolio. The deferred taxeffect is recognized in the income statement. If thereis a loss in value, debit the Deferred Tax Benefitaccount and credit the Provision for Income Taxesaccount. If there is a gain in value, debit the Provi-sion for Income Taxes account and credit theDeferred Tax Liability account.

m Gains or losses on the available-for-sale portfolio. Thesame treatment noted for gains or losses on thetrading portfolio, except that taxes are noted inthe Other Comprehensive Income section of the in-come statement.

m Gains or losses on the held-to-maturity portfolio. There isno tax recognition if changes in value are consideredto be temporary in nature. If there is a permanentreduction in value, the treatment is identical to thetreatment of losses in the trading portfolio, as justnoted.

What Is the Accounting for SignificantEquity Investments?

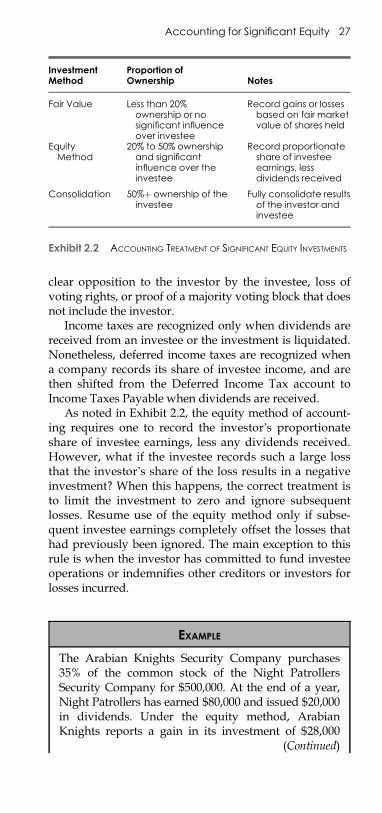

There are three ways to account for an investment:

1. Report the investment at its fair value2. Report it under the ‘‘equity method’’3. Fully consolidate the results of the investee in the in-

vesting company’s financial statements

The rules under which each of these methods is ap-plied are noted in Exhibit 2.2.

The presence of ‘‘significant influence’’ over an investeeis assumed if the investor owns at least 20% of its com-mon stock. However, this is not the case if there is clearevidence of not having influence, such as being unable toobtain financial information from the investee, not beingable to place a representative on its board of directors,

26 Investment Accounting

E1C02 03/04/2010 Page 27

clear opposition to the investor by the investee, loss ofvoting rights, or proof of a majority voting block that doesnot include the investor.

Income taxes are recognized only when dividends arereceived from an investee or the investment is liquidated.Nonetheless, deferred income taxes are recognized whena company records its share of investee income, and arethen shifted from the Deferred Income Tax account toIncome Taxes Payable when dividends are received.

As noted in Exhibit 2.2, the equity method of account-ing requires one to record the investor’s proportionateshare of investee earnings, less any dividends received.However, what if the investee records such a large lossthat the investor’s share of the loss results in a negativeinvestment? When this happens, the correct treatment isto limit the investment to zero and ignore subsequentlosses. Resume use of the equity method only if subse-quent investee earnings completely offset the losses thathad previously been ignored. The main exception to thisrule is when the investor has committed to fund investeeoperations or indemnifies other creditors or investors forlosses incurred.

InvestmentMethod

Proportion ofOwnership Notes

Fair Value Less than 20%ownership or nosignificant influenceover investee

Record gains or lossesbased on fair marketvalue of shares held

EquityMethod

20% to 50% ownershipand significantinfluence over theinvestee

Record proportionateshare of investeeearnings, lessdividends received

Consolidation 50%þ ownership of theinvestee

Fully consolidate resultsof the investor andinvestee

Exhibit 2.2 ACCOUNTING TREATMENT OF SIGNIFICANT EQUITY INVESTMENTS

EXAMPLE

The Arabian Knights Security Company purchases35% of the common stock of the Night PatrollersSecurity Company for $500,000. At the end of a year,Night Patrollers has earned $80,000 and issued $20,000in dividends. Under the equity method, ArabianKnights reports a gain in its investment of $28,000

(Continued)

Accounting for Significant Equity 27

E1C02 03/04/2010 Page 28

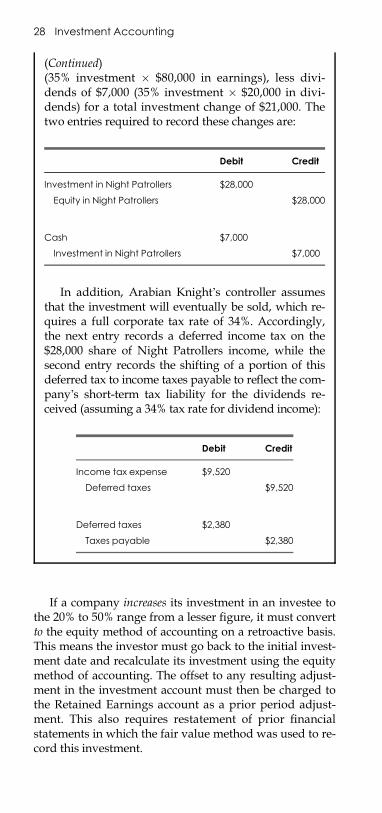

If a company increases its investment in an investee tothe 20% to 50% range from a lesser figure, it must convertto the equity method of accounting on a retroactive basis.This means the investor must go back to the initial invest-ment date and recalculate its investment using the equitymethod of accounting. The offset to any resulting adjust-ment in the investment account must then be charged tothe Retained Earnings account as a prior period adjust-ment. This also requires restatement of prior financialstatements in which the fair value method was used to re-cord this investment.

(Continued)(35% investment � $80,000 in earnings), less divi-dends of $7,000 (35% investment � $20,000 in divi-dends) for a total investment change of $21,000. Thetwo entries required to record these changes are:

Debit Credit