The use of Stalking Horse proceedings to maximize value in insolvency workouts in United States of America and Canada By: Allan Nackan CA▪CIRP March 2012 stalk-ing-horse Pronunciation: 'sto-ki[ng]-"hors Function: noun Date: 1519 1 : a horse or a figure like a horse behind which a hunter stalks game 2 : something used to mask a purpose

The use of Stalking Horse proceedings to maximize value in insolvency workouts in USA and Canada by Allan Nackan CPA, CIRP_March 2012

Dec 29, 2015

This is a paper that I prepared in March 2012 as part of the INSOL Global Insolvency Program and in obtaining my accreditation as a Fellow of INSOL International. It focuses on the use of Stalking Horse proceedings as a tool for maximizing value in bankruptcy sales.

Allan Nackan

[email protected]

416-496-3732

Allan Nackan

[email protected]

416-496-3732

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

The use of Stalking Horse proceedings to

maximize value in insolvency workouts in

United States of America and Canada

By: Allan Nackan CA▪CIRP March 2012

stalk-ing-horse Pronunciation: 'sto-ki[ng]-"hors Function: noun Date: 1519

1 : a horse or a figure like a horse behind which a hunter stalks game

2 : something used to mask a purpose

Table of Contents

Introduction ....................................................................................................................................... 1

Evolution and use of Stalking Horse procedure to sell distressed businesses ........................................ 2

Elements of a stalking horse sale process ............................................................................................ 3

Stalking horse bidder .......................................................................................................................... 5

Court involvement in the process ....................................................................................................... 6

Vesting title and finality of sale ........................................................................................................... 9

Credit bidding .................................................................................................................................. 11

Value creation .................................................................................................................................. 12

Advantages and disadvantages of a stalking horse sale process ......................................................... 14

Conclusions ...................................................................................................................................... 15

Bibliography ..................................................................................................................................... 16

Page 1

The use of stalking horse proceedings to maximize

value in insolvency workouts in United States of

America and Canada

Introduction

Stalk-ing-horse - Etymology: after the former practice of bird hunters of hiding behind a horse (or a

decoy) until he had reached within close range of prey.

The use of this term in insolvency proceedings is a bit of a misnomer. Unlike its hunting origins, there is

generally no concealed purpose of the stalking horse in insolvency workouts. On the contrary insolvency

sales happen in a “fishbowl”1. The stalking horse offer is the “floor bid” against which all other offers

must compete. The purchaser is publically identified and the terms of its offer are put on display for all

to see. The purchaser’s identity and terms of its offer become known to all other bidders, creditors and

other stakeholders and are this information is publically exposed through the Court process. This might

discourage certain bidders but, for the not-so-faint- hearted, bankruptcy sales present an excellent

opportunity to acquire a business at bargain prices and free and clear of pre-existing liabilities. From

the perspective of the seller, the stalking horse process has proved itself to be a very effective method

for maximizing value of the enterprise, which is after all a prime objective in all insolvency workouts.

This paper will cover the following areas:

Discuss the evolution and use of this technique to sell distressed businesses in insolvency

proceedings in USA and Canada

Explore elements of a stalking horse sale process

Explain why this can be such an effective value creation tool, citing recent real life examples and

comparing and contrasting this methodology to other sale processes

Review some of the case law that has evolved in both jurisdictions

Discuss some of the complexities, including the issue of the credit bidding by secured lenders

1 As noted by David Powlen in his article “Bargains Await Buyers Skilled at Navigating Section 363 Minefields”, July

1, 2007

Page 2

Evolution and use of Stalking Horse procedure to sell distressed

businesses

In Canada, bankruptcy sales have traditionally been conducted by way of blind bidding or sealed tender,

whereby participants are asked to put forward their best offers by a specified bid deadline. An

insolvency practitioner would most often accept the most promising bid and then proceed to negotiate

the terms of that offer. Traditionally, there was no auction and no second chance to increase or amend

a bid once submitted. The sales process was administered by an insolvency practitioner, with very little

transparency into this process until a sale was concluded. Sales processes were traditionally set up this

way to create a competitive bidding environment and an efficient process for attracting the best offer.

Equally important was the desire to ensure the “integrity of the sale process” in that all buyers are

afforded a level playing field and there should be no opportunity for the shopping of bids. The simplicity

and certainty of process also leads to less legal challenges by a “bitter bidder” or other stakeholder. The

process does rely heavily on the integrity and sound professional judgement of the insolvency

practitioner who is administering the sale.

By contrast, sale proceedings under Chapter 11 of the US Bankruptcy Code have always been much

more spirited. As mild-mannered Canadians we were intrigued to watch the much more heavily-

contested US proceedings from a distance, in which competitive auctions, greater transparency and

deals struck on the steps of the courthouse were the order of the day. The Stalking Horse auction

process is a refinement that is a regular feature in the US sales.

With the marked increase in cross-border proceedings between Canada & US2, trends and concepts

emanating from the USA inevitably spill north – CCAA and BIA amendments heavily modelled on

Chapter 11-style proceedings, creditor committees, critical supplier provisions, etc., to name but a few.

In my view, the stalking horse auction process is one of our better imports from the US – because it

often directly leads to value maximization.

When dealing with corporate groups that have international scope, it is relatively common for an

insolvent group to sell its global business in its entirety (e.g. Nortel Networks, Abitibi Bowater, TerreStar

Networks). This calls for a combined or at least consistent approach to the sale of its global assets. It is

2 Recent examples include of Canadian-US cross border proceedings where staking horse process was effectively used include: Nortel, Indalex, Eddie Bauer, Brainhunter, TerreStar

Page 3

not uncommon for the sale to be led by investment bankers in New York, touting all of the global assets

by way of s. 363 sales, including a stalking horse feature. For example, in Nortel Networks, which

operated as a truly global enterprise in more than 70 countries around the world and with 3 main

concurrent insolvency proceedings (namely, Chapter 11 in US, CCAA in Canada, and Administration in

UK and EMEA), the only feasible way to sell Nortel’s business units and intellectual property was on a

co-operative basis which included assets in multiple jurisdictions. All major sales were co-ordinated out

of the US and sold in staking horse auctions that yielded unprecedented recoveries and at very healthy

multiples of the initial stalking horse bids (see CHART B on page 13). It would have been impossible to

carve up Nortel’s assets and sell them in separate assets sales across the globe and the equivalent value

would never have been attained.

Even in standalone Canadian proceedings, stalking horse sales are much more commonplace (e.g.

Timminco3, Komtech4, Canwest5). Not only has this enhanced recoveries but familiarity and consistency

of process is comforting for prospective US purchasers, who previously voiced frustration about the

closed Canadian-style process, where they did not get a second chance to improve their bid.

Elements of a stalking horse sale process

In the United States, an insolvent debtor wishing to restructure its affairs will usually file for protection

under Chapter 11 of the US Bankruptcy Code. In Canada, a similar type of relief will be sought by

commencing a proceeding under the Companies' Creditor Arrangement Act (“CCAA”) or under Division I

of the Bankruptcy & Insolvency Act (“BIA”). The above types of proceedings allow for the debtor to

remain in possession of the business and have protection of a stay of proceedings while it attempts to

restructure its affairs, with the ultimate aim of presenting a plan to their creditors. In recent years, due

largely to the difficulties in raising interim financing (otherwise called debtor-in-possession financing or

“DIP”) and the prohibitive costs of Chapter 11 and CCAA proceedings, many debtors have opted to sell

all or part of their businesses as a going concern in an abridged insolvency proceeding pursuant to s. 363

3 Re Timminco Limited (2012) ONSC 506 (Ont. Commercial List) and (2012) ONSC 948 (Ont.

Commercial List) 4 Komtech Inc. (Re.) 2011 ONSC 3230 5 Re Canwest Publishing Inc./Publications Canwest Inc., 2010 ONSC 2870, 2010 CarswellOnt 3509 (Ont.S.C.J.

[Commercial List])

Page 4

of the US Bankruptcy Code or s. 36 of CCAA6. While on its face it may seem that some of the controls of

a creditor vote are lost, these sales are still on notice to creditors who can still voice their objections.

The majority of these sale proceedings have come to include a stalking horse auction process which in

broad strokes can be described as follows:

The company identifies and then enters into an Agreement of Purchase and Sale with a bidder

which becomes known as the “stalking horse”. The stalking horse may be identified by a

competitive process (resulting in a two-stage process) but, in some instances, a single party

comes forward or is selected by the Company to fulfil that role.

The stalking horse provides a “floor bid” against which any other expressions of interest will be

evaluated in a court-authorized sale process.

Company applies to Court to approve the stalking horse offer and a sale/auction process.

The company then exposes its assets to the market, casting its net as wide as possible to attract

as many purchasers as possible, including strategic and financial buyers. Most often, they will be

assisted in this endeavor by financial advisors, investment bankers (and in Canada, the court-

appointed Monitor).

If no better qualifying bids are received by the bid deadline, then the stalking horse will acquire

the assets pursuant to the terms of their agreement.

If higher qualifying bids are received, then an auction process will follow, pursuant to auction

rules that were are approved by the Court. At the conclusion of that auction process, the

company will be authorized to enter into an agreement of sale with the highest bidder.

The stalking horse will earn a pre-determined break-up fee and expense reimbursement if it is

not the successful acquiror. This is to compensate them for time and expense incurred in

performing due diligence, negotiating the stalking horse sale agreement, and further provides a

financial reward for agreeing to guarantee the floor price.

The court will then approves the winning transaction and grants a vesting order, conveying the

assets to the purchaser free and clear of all liens and encumbrances.

6 Equivalent section of BIA is s. 65.13 which provides for quick sales of assets where certain criteria are met. For

the balance of this paper I have only focussed on CCAA provisions but the same effect can be achieved under BIA.

Page 5

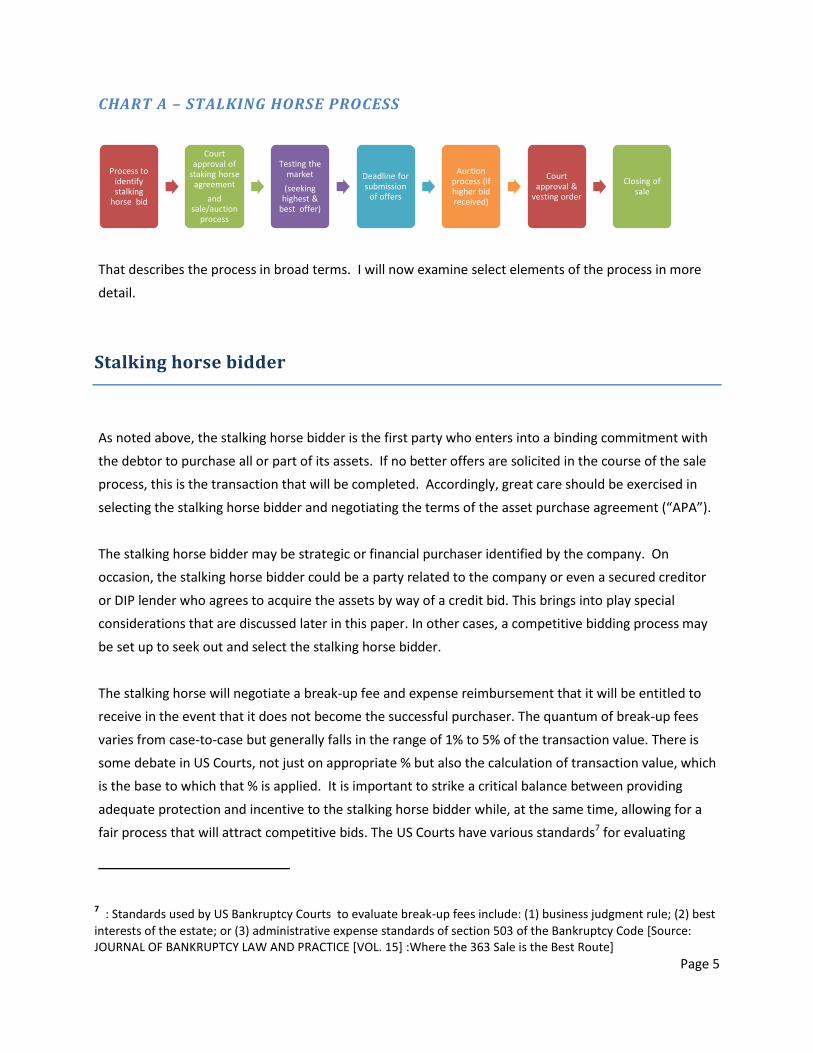

CHART A – STALKING HORSE PROCESS

That describes the process in broad terms. I will now examine select elements of the process in more

detail.

Stalking horse bidder

As noted above, the stalking horse bidder is the first party who enters into a binding commitment with

the debtor to purchase all or part of its assets. If no better offers are solicited in the course of the sale

process, this is the transaction that will be completed. Accordingly, great care should be exercised in

selecting the stalking horse bidder and negotiating the terms of the asset purchase agreement (“APA”).

The stalking horse bidder may be strategic or financial purchaser identified by the company. On

occasion, the stalking horse bidder could be a party related to the company or even a secured creditor

or DIP lender who agrees to acquire the assets by way of a credit bid. This brings into play special

considerations that are discussed later in this paper. In other cases, a competitive bidding process may

be set up to seek out and select the stalking horse bidder.

The stalking horse will negotiate a break-up fee and expense reimbursement that it will be entitled to

receive in the event that it does not become the successful purchaser. The quantum of break-up fees

varies from case-to-case but generally falls in the range of 1% to 5% of the transaction value. There is

some debate in US Courts, not just on appropriate % but also the calculation of transaction value, which

is the base to which that % is applied. It is important to strike a critical balance between providing

adequate protection and incentive to the stalking horse bidder while, at the same time, allowing for a

fair process that will attract competitive bids. The US Courts have various standards7 for evaluating

7 : Standards used by US Bankruptcy Courts to evaluate break-up fees include: (1) business judgment rule; (2) best

interests of the estate; or (3) administrative expense standards of section 503 of the Bankruptcy Code [Source: JOURNAL OF BANKRUPTCY LAW AND PRACTICE [VOL. 15] :Where the 363 Sale is the Best Route]

Process to identify stalking

horse bid

Court approval of

staking horse agreement

and sale/auction

process

Testing the market

(seeking highest &

best offer)

Deadline for submission

of offers

Auction process (if higher bid received)

Court approval &

vesting order

Closing of sale

Page 6

break-up fees as outlined in cases such as Re Hupp Industries8. The Canadian courts have also weighed

in on the appropriateness of break-up fees. It is the general consensus in both jurisdictions that break-

up fees are not appropriate in the case of the sale to a non-arm’s length party.

The stalking horse bidder has a strategic advantage in that they get to dictate the terms of the APA by

which others must abide, they have the advantage of more time and greater access to company’s

management for due diligence, and they might also have input into formulating the bidding and auction

procedures (including input on qualification of bidders, timelines, minimum bid increments, ability to

view other bids, and good faith deposits). The break-up fees and bidding increments set for the auction

may provide a further advantage over other bidders who must start the bidding at an amount which

exceeds stalking horse bid price plus break-up fee plus initial bidding increment. This can have a

“chilling” effect on the bidding of others.

Court involvement in the process

In both Canada and the US, the courts have an active involvement in approving and supervising various

aspects of the stalking horse sales process, including: approval of stalking horse offer; approval of the

bidding and auction procedures, final sale approval and vesting of title, and dealing with any objections.

The jurisprudence in both jurisdictions is rich in precedents endorsing this means of selling an insolvent

business as a going concern, resulting in a favourable outcome for employees, customers, suppliers etc.

The objective of a filing under Chapter 11 or CCAA is for the business to successfully emerge, having

filed a plan of reorganization that is approved by the requisite majority of its creditors. In the current

economic climate since the downturn in 2008, this has been increasingly difficult to achieve due to the

constrained capital markets. Thus, Court-approved sales of the business or assets of an insolvent entity

outside of the ordinary course have become more prevalent, implemented under s. 363 of the US

Bankruptcy Code or s. 36 of CCAA. In fact, practice has sometimes evolved such that a stalking horse

deal is pre-packaged prior to a filing and then the process implemented in an abridged Chapter 11 or

CCAA filing. The Chrysler case is an extreme example of where the sale of its assets was concluded

within 40 days of the Bankruptcy filing. While this does result in a quick transition of the business into

new hands, often preserving value, a number of complicated back-end issues remain to be dealt with in

the Company.

8 Re. Hupp Industries, 140 B.R. 191 Bank. ND. Ohio 1992

Page 7

IN USA 9

In Chapter 11 proceedings, section 363(b) of the Bankruptcy Code authorizes the debtor-in-possession to

sell its property outside the ordinary course of business, after notice and a hearing. Historically, there

was reluctance to authorize sales outside of the protection of a plan, except in narrow circumstances

(e.g. fast depreciating assets). However, practice has evolved such that the majority of US courts will

authorize sales under section 363(b) as long as there is appropriate justification for the sale.

The leading case dealing with the business justification standards for granting such approval is In Re.

Lionel Corp.10 In that case, the U.S. Court of Appeals (Second Circuit) referred to the following as factors

for a court to consider in approving a section 363(b) sale:

a) Proportionate value of the asset being sold to the estate as a whole

b) Time elapsed time since filing of the petition

c) Likelihood that a reorganization plan will be proposed in the near future

d) The effect of the sale on a future plan of reorganization

e) The proceeds of sale vis-à-vis any appraisals

f) Whether the asset is increasing or decreasing in value

In considering whether to approve a section 363 sale, courts will require that the purchase price is “fair

and reasonable”. Practically, the fact that the purchase price often consists of a combination of cash,

credit bids and assumed liabilities makes it more complicated to evaluate fair value. In Abbott's

Dairies11, the court seemed to settle on the fact that a competitive auction process might generally be

sufficient to establish fair value. I concur that the market test of a public auction is a more effective way

to establish “real” value than relying on theoretical appraisals.

In November 2009, the Fifth Circuit's decision in In re Gulf Coast Oil Corp. 12was a sobering reminder that

there are limits to what some courts will permit in section 363 sales. Judge Steen identified a list of

9 Reference source: What’s driving Section 363 Sales after Chrysler and General Motors? By Robert M. Fishman &

Gordon E. Gouveia appearing in Norton Journal of Bankruptcy Law and Practice [Vol. 19 #4] 10 Comm. of Equity Security Holders v. Lionel Corp. (In re Lionel Corp.), 722 F.2d 1063 (2d Cir. 1983

11 In re Abbotts Dairies of Penn., Inc., 788 F.2d 143 (3d Cir. 1986) 12 In Re: Gulf Coast Oil Corporation and Century Resources, Inc. and New Century Energy Corp.

New Century Energy Corp Case No: 08-50213

Page 8

factors that could be considered in determining whether to approve a section 363 sale prior to plan

confirmation. Some of the factors identified were inter alia: the need for an immediate sale; business

justification for the sale and sale process being separate from the plan; satisfaction of due process; APA

designed to facilitate competitive bidding; existence of active and aggressive marketing efforts; whether

the sale generally benefits the estate or just select creditors; all the assets (including crown jewels)

being sold or just smaller portion of assets; are extraordinary protections being sought by purchaser

(which would usually be sought at plan confirmation).

It is interesting to note that these factors bear some similarity to the factors that a Canadian court will

consider in approving a sale – see Nortel and Soundair decisions referenced below. In my view, this

reinforces the overriding caveat that, while stalking horse procedures can be a very effective tool for

maximizing value, due process and careful supervision are essential components to be observed to

achieve a fair outcome and guard against abuses.

IN CANADA

In Canadian CCAA proceedings, the debtor company may not sell or otherwise dispose of assets outside

of the ordinary course of business unless authorized to do so by a court13. In deciding whether to grant

such authorization, the court will consider, among other things14: (a) whether the process leading to the

sale was reasonable; (b) whether the Monitor approved process; (c) whether the Monitor filed the

report stating that in their opinion the proposed sale would be more beneficial to creditors than a sale

under a bankruptcy; (d) extent to which creditors were consulted; (e) effects of the proposed sale on

creditors and other interested parties; (f) whether consideration received is reasonable and fair taking

into account their market value.

In re Nortel Networks Corp15, Justice Morawetz concluded that:

“the CCAA is intended to be flexible and must be given a broad and liberal interpretation to

achieve its objectives and a sale by the debtor which preserves its business as a going concern is,

in my view, consistent with those objectives”.

13 S. 36(1) of CCAA 14 S. 36 (3) of CCAA 15 Re Nortel Networks Corp. (2009) 55 C.B.R. (5th), 229 (ONT) S.C.J. at para 47

Page 9

Justice Morawetz recognized that continuation of business as a going concern was a key consideration

albeit under new ownership as opposed to stewardship of the debtor16. He identified the factors which

the Court should consider in determining whether to approve a sale under CCAA in absence of a plan,

namely:

a) is a sale transaction warranted at this time?

b) will the sale benefit the whole "economic community"?

c) do any of the debtors' creditors have a bona fide reason to object to a sale of the business?

d) is there a better viable alternative?

The desire to maximize realizations by conducting an auction process and ensuring fair process, a

hallmark of the Canadian system, was further balanced by requiring that Nortel would return to court to

seek approval of the most favourable transaction to emerge from the auction process and will have to

satisfy the elements established by the court for approval as set out in Soundair17 , namely: sufficient

effort to attract best price, efficacy, integrity and fairness of the process.

The “Nortel test” (above) has been adopted by the Canadian courts in approving numerous other

stalking horse sale processes, including: Brainhunter18, CanWest19, and Clothing for Modern Times20.

Vesting title and finality of sale

One of the attractive features of purchasing assets of an insolvent company by the methods described

in this paper is that the buyer gets a vesting order of the court conveying the assets free and clear of

existing liens and encumbrances and benefits from the finality of a court-approved process. This is

particularly desirable in an insolvency situation where numerous liabilities have been incurred by the

selling entity, some known and some unknown, and the purchaser only wishes to expose itself to the

liabilities specifically assumed as part of the transaction.

16 Re Nortel Networks Corp. (2009) 55 C.B.R. (5th), 229 (ONT) S.C.J. at para 40 17 Royal Bank v. Soundair (1991), 7 C.B.R.(3rd) 1 (Ont. C.A.) at para. 16. 18 Re Brainhunter Inc. (2009), 62 C.B.R. (5th) 41 (Ont. S.C.J.). 19 Re. CanWest Publishing Inc. [2010] O.J.. 2190 20 Re. Clothing for Modern Times Ltd., 2012 ONSC 1200

Page 10

IN CANADA

The scope of the vesting orders is rather broad. The model form of Approval and Vesting Order in use in

Ontario21 provides that the property:

“shall vest absolutely in the Purchaser, free and clear of and from any and all security interests

(whether contractual, statutory, or otherwise), hypothecs, mortgages, trusts or deemed trusts

(whether contractual, statutory, or otherwise), liens, executions, levies, charges, or other

financial or monetary claims, whether or not they have attached or been perfected, registered or

filed and whether secured, unsecured or otherwise (collectively, the "Claims")”.

The motion seeking a vesting order should be served on all persons having an economic interest in the

purchased assets, unless circumstances warrant a different approach. The property will be conveyed free

and clear of all of these claims. Where ownership of the property being sold is in dispute, that will not

stand in the way of the sale but the claimant could still have a claim against the proceeds of sale.

IN USA22

The Bankruptcy Code permits the transfer of the debtor's property free and clear of any interest in the

property if specific conditions in section 363(f) are satisfied23. In addition, section 363(m) effectively

moots appeals of the sale, thus providing finality. As a general rule, the application of this sections

effectively transfers free and clear title to the purchaser. That said, there are a limited number of

bankruptcy cases where the finality of sale and ability to convey assets free & clear was challenged, for

example:

In Clear Channel24, the Ninth Circuit questioned whether or a sale can be free and clear of junior

liens and that these claims might still attach to the assets.

In Lehman Brothers, the debtor attempted to reconsider a transaction that had already closed

on the basis that the purchaser received an unexpected windfall (assumed liabilities were

21 Model Approval and Vesting Order as developed by Commercial List Users Committee in Ontario – see

http://www.ontariocourts.ca/scj/en/commerciallist/ 22 Research sources include the following articles: Pathology of 363 Sales by Goodwin Procter LLP and Section 363:

A useful tool for asset sales in bankruptcy DLA Piper. 23 Conditions are set out in Sec 363(f) of US Bankruptcy Code 24 Clear Channel Outdoor, Inc. v. Knupfer (In re PW,LLC), 391 B.R. 25, 40–41 (B.A.P. 9th Cir. 2008)

Page 11

significantly overstated or in accurate, with the result that the buyer may have paid significantly

less than anticipated).

The majority of US courts have taken a broad view that all 3rd party interests can be extinguished on

sale. However, there are other cases when they have taken a narrower view that employment

discrimination claims under ERISA; environmental remediation claims; and future claims for product

liability cannot be fully extinguished.

Credit bidding

It is not uncommon in the context of bankruptcy sales for a secured lender to submit a credit bid for the

assets. There are several reasons why they would want to do this, including:

Exchanging the assets for its debt in hope of monetizing at a later date, when conditions are

more favourable and the business improves etc.

Desire to set a floor price in an auction in an effort to coax out other offers. If no better offers

are received, they will come to own the assets as stalking horse bidder.

In some circumstances a credit bid may be used aggressively as a part of a “loan to own”

strategy. This would involve purchasing the debt, usually at a discount, and then submitting an

offer as stalking horse for the assets. The advantage that this presents is that it may give them a

tactical advantage to acquire the assets at a favorable price considering that they paid less than

face value for the debt but are still able to submit a credit bid at the full face value of debt.

There are special considerations to bear in mind when dealing with credit bids submitted by parties

related to the debtor or bids that are submitted by a secured lender/DIP lender. These “insiders” are

privy to information that other bidders may not have. It may be perceived that management is not as

forthcoming and cooperative in due diligence with other bidders or that they have their own self-serving

agenda. In those circumstances, it is helpful to interpose an intermediary (such as the Monitor in

Canadian CCAA proceedings) to ensure that all parties are treated in an even-handed manner.

Another complexity of credit bidding occurs with a syndicated loan25. There might be divergent interests

within the syndicate (some parties wanting to submit a credit bid and others just looking to cash out).

25

Davies : Anticipated Credit Bidding in Syndicated Loan Documentation, April 6, 2011

Page 12

The syndicated loan documents should attempt to address these issues and anyone acquiring the loan

should be mindful of what rights they are acquiring.

In US, section 363(k) expressly allows for credit bidding by secured creditors and there are an abundance

of cases in which this has occurred. There have been conflicting decisions26 as to whether secured

lenders have the right to credit bid in a sale under a plan. That issue should be clarified in 2012 when

heard by the US Supreme Court27. However, that debate seems to be limited the right to credit bid in a

plan involving a sale, whereas it is clear that credit bids are permissible under a section 363 sale. This

sets up an interesting conflict where a sale under section 363 could lead to a different result than sale

under a plan.

In Canada, there is no statutory authority for credit bidding but the case law clearly indicates that this is

permissible28 and it occurs with some frequency.

Value creation

This paper opens with the proposition that a stalking horse auction is an effective tool for maximizing

realizations to stakeholders. It is therefore appropriate to reflect on why this is the case:

An implicit feature of these types of sales is the “certainty” that a buyer for the assets will

emerge and that the transaction will be closed within a defined timeline - either with the

stalking horse or winning bidder. This “certainty” of outcome provides comfort to employees

and all other stakeholders as to the continuity of business and facilitates an orderly going

concern sale. Absent this fact, the business might deteriorate rapidly in value as employees seek

alternate jobs and customers and suppliers pursue contingencies.

The dynamics of a public auction sets up a competitive environment which is conducive to

maximizing value. Examples can be cited of cases where fierce bidding has yielded excellent

26 Right to credit bid was denied in In re Philadelphia Newspapers, 599 F.3d 298 (3rd Cir. 2010) and In re Pacific

Lumber Co., 584 F.3d 229 (5th Cir. 2009). In River Road Hotel Partners, 651 F.3d 642 (7th Cir. 2011), the 7th circuit

upheld the right to credit bid even if part of a plan. 27 Radlax Gateway Hotel v. Amalgamated Bank, 181 L. Ed 2d 547 (December 12, 2011) 28 Recent cases in Canada where credit bidding was permitted include: In Re White Birch Paper Holding Company

[2010] Q.J. No.10469 at paragraph 34 and 35; and also: Re CanWest Publishing Inc [2010] O.J. No 2190]

Page 13

results. Certain parties are not just motivated by wanting to acquire the assets for themselves

but equally wanting to ensure that their competitors do not or are forced to pay a premium

prices. For example, when the Nortel sold its intellectual property in 2011, including thousands

of patents relating to internet, communication, and networking, a pitched battle ensued

between Google who acted as the stalking horse bidder and the consortium comprising

Microsoft, Apple, EMC, Research In Motion, Ericsson and Sony, which ultimately succeeded in

winning the auction. After a four-day auction, the end result was a final purchase price of $4.5B

which was 5 times the stalking horse bid submitted by Google of $900m. The creditors of Nortel

were the big winners and such result could never have been achieved without the auction

dynamic.

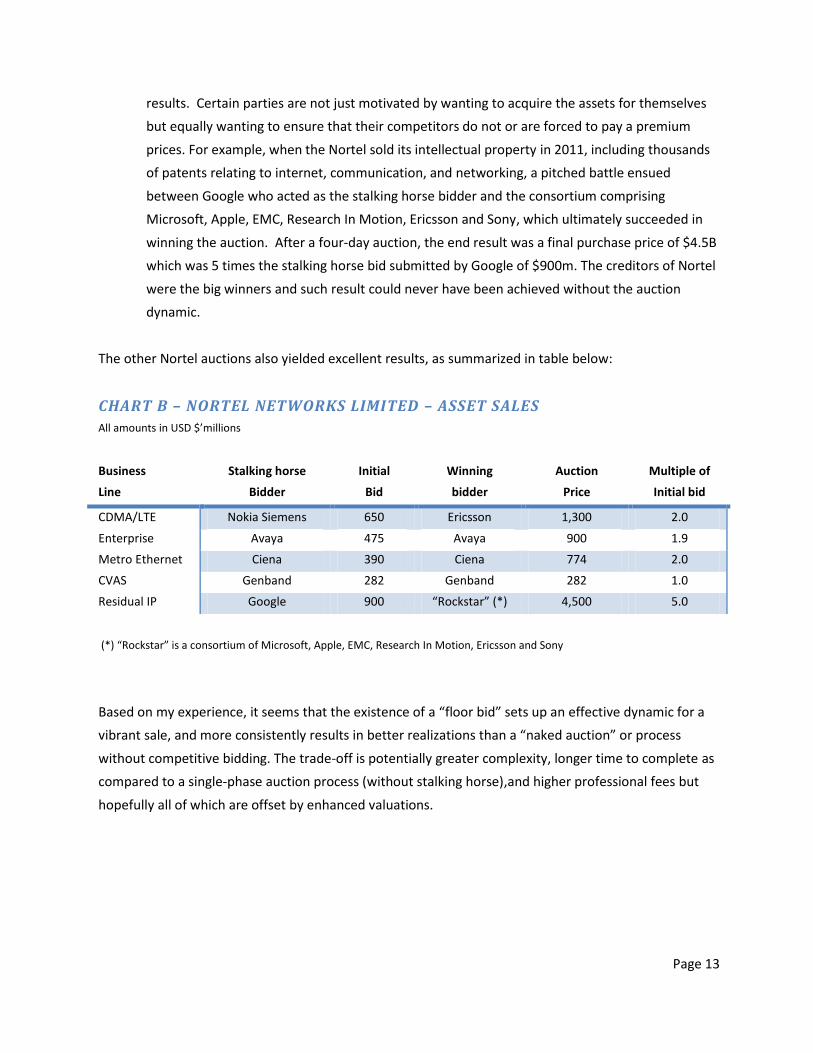

The other Nortel auctions also yielded excellent results, as summarized in table below:

CHART B – NORTEL NETWORKS LIMITED – ASSET SALES

All amounts in USD $’millions

Business

Line

Stalking horse

Bidder

Initial

Bid

Winning

bidder

Auction

Price

Multiple of

Initial bid

CDMA/LTE Nokia Siemens 650 Ericsson 1,300 2.0

Enterprise Avaya 475 Avaya 900 1.9

Metro Ethernet Ciena 390 Ciena 774 2.0

CVAS Genband 282 Genband 282 1.0

Residual IP Google 900 “Rockstar” (*) 4,500 5.0

(*) “Rockstar” is a consortium of Microsoft, Apple, EMC, Research In Motion, Ericsson and Sony

Based on my experience, it seems that the existence of a “floor bid” sets up an effective dynamic for a

vibrant sale, and more consistently results in better realizations than a “naked auction” or process

without competitive bidding. The trade-off is potentially greater complexity, longer time to complete as

compared to a single-phase auction process (without stalking horse),and higher professional fees but

hopefully all of which are offset by enhanced valuations.

Page 14

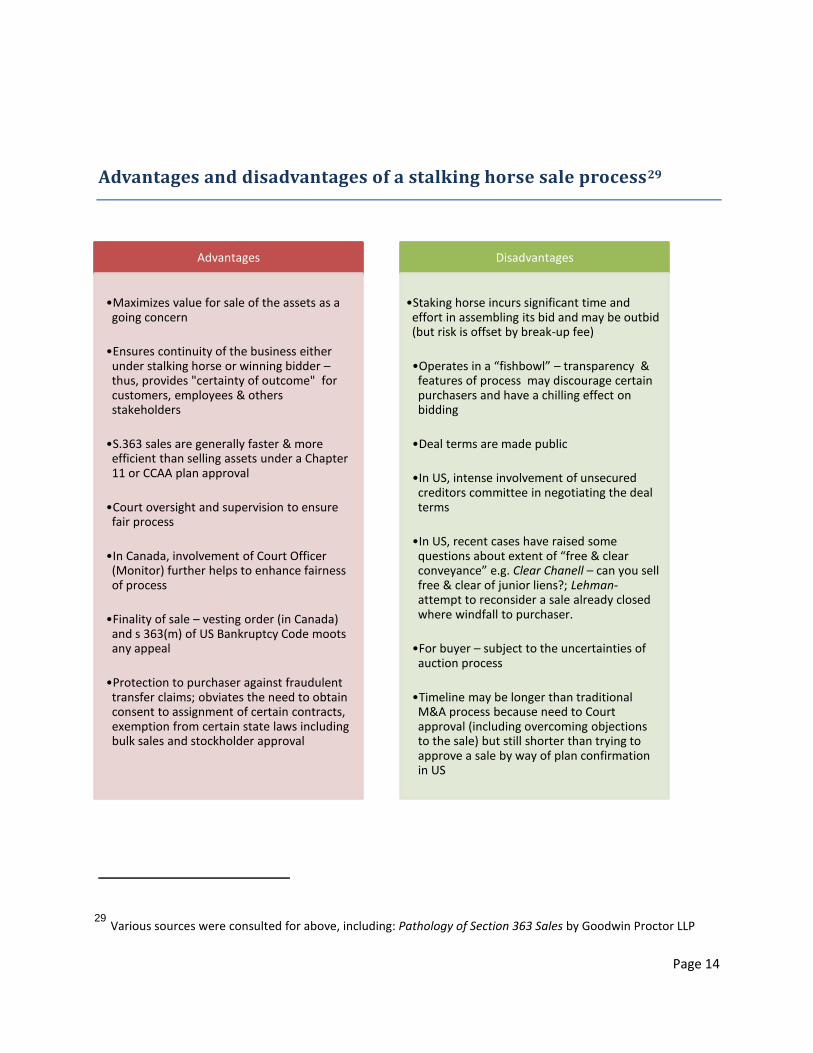

Advantages and disadvantages of a stalking horse sale process29

29 Various sources were consulted for above, including: Pathology of Section 363 Sales by Goodwin Proctor LLP

Advantages

•Maximizes value for sale of the assets as a going concern

•Ensures continuity of the business either under stalking horse or winning bidder – thus, provides "certainty of outcome" for customers, employees & others stakeholders

•S.363 sales are generally faster & more efficient than selling assets under a Chapter 11 or CCAA plan approval

•Court oversight and supervision to ensure fair process

•In Canada, involvement of Court Officer (Monitor) further helps to enhance fairness of process

•Finality of sale – vesting order (in Canada) and s 363(m) of US Bankruptcy Code moots any appeal

•Protection to purchaser against fraudulent transfer claims; obviates the need to obtain consent to assignment of certain contracts, exemption from certain state laws including bulk sales and stockholder approval

Disadvantages

•Staking horse incurs significant time and effort in assembling its bid and may be outbid (but risk is offset by break-up fee)

•Operates in a “fishbowl” – transparency & features of process may discourage certain purchasers and have a chilling effect on bidding

•Deal terms are made public

•In US, intense involvement of unsecured creditors committee in negotiating the deal terms

•In US, recent cases have raised some questions about extent of “free & clear conveyance” e.g. Clear Chanell – can you sell free & clear of junior liens?; Lehman- attempt to reconsider a sale already closed where windfall to purchaser.

•For buyer – subject to the uncertainties of auction process

•Timeline may be longer than traditional M&A process because need to Court approval (including overcoming objections to the sale) but still shorter than trying to approve a sale by way of plan confirmation in US

Page 15

Conclusions

At the date of writing this paper, this curiously named process is now firmly entrenched in the lexicon

and practice of bankruptcy & restructuring in both Canada and USA. There is now a rich history of

cases on both sides of the border where stalking horse procedures have been used very effectively to

maximize the values of an insolvent business, resulting in favourable outcomes for employees,

customers, suppliers etc.

From a Canadian perspective, the stalking horse process is one of the more successful imports to come

out of the cross-pollination that inevitably occurs in cross-border proceedings. As demonstrated in this

paper, Canada has embraced the benefits of stalking horse process (its value maximization potential)

and married this with the requirement for fairness and due process.

Insolvency practitioners (legal and financial advisors) have displayed ingenuity in the way they have

used this process to maximize values and engineer the continuity of insolvent businesses, albeit under

new ownership. Purchasers seeking to acquire distressed assets/businesses have also found ways to use

stalking horse process as a creative tool for achieving their objectives.

Due to the pivotal role that the stalking horse bidder plays in shaping the sale process, there is potential

for abuse. We have witnessed cases where parties have clearly tried to push the envelope and abuse

this leverage in the sales/restructuring process. As a result, certain checks and balances are necessary

to ensure fair process, particularly in cases when an insider or the secured/DIP lender acts is the stalking

horse bidder. The supervisory role played by the courts (and Monitor in Canada) is critical to

maintaining a healthy balance between desire to obtain the highest and best price while still ensuring a

fair process.

Page 16

Bibliography

Barnes, T. (n.d.). Acknowledging his valuable insights and clarification on points of US Law.

Cademartori, Malani J.- SheppardMullin. (2010, March 31). One's Crisis is Another's Opportunity: Section

363 Sales. Retrieved March 2012, from SheppardMullin Bankruptcy Blog:

http://www.bankruptcylawblog.com/cat-asset-sales-and-acquisitions.html

Collins, S.F., Gage, J.D., McElcheran K.P., Vauclair, S.A. - McCarthys. (2008, February 28). M&A — CCAA:

Has the Stalking Horse Left the Barn? Retrieved March 2012, from McCarthy Tetrault:

http://www.mccarthy.ca/article_detail.aspx?id=3923

Cover Image (Stalking Horse). (n.d.). Retrieved March 2012, from The Independent:

http://blogs.independent.co.uk/wp-content/uploads/2012/01/stalking-horse-21.jpg

Davies: Jay A. Swartz et al at;. (2011, April 6). Flash: Anticipating Credit Bidding in Syndicated Loan

Documentation and Trust Indentures. Retrieved March 2012, from Davies Ward Phillips &

Vineberg: http://www.dwpv.com/en

Feder, B. D. (2009, February). Acquiring Distressed Businesses in Chapter 11 Cases - Riding A "Stalking

Horse" Bid to Victory. Retrieved March 2012, from Financier Worldwide:

http://www.financierworldwide.com/article.php?id=3337&page=1

Fishman, R. M. (2010). What’s Driving Section 363 Sales after Chrysler and General Motors? Norton

Journal of Bankruptcy Law and Practice [Vol.19 #4], 351-359.

Goodwin Procter LLP. (2004, October 27). Pathology of Section 363 Sales (Not as Simple as They Look).

Retrieved March 2012, from Findlaw: http://library.findlaw.com/2004/Oct/27/133620.html

Jones Day. (2003, November). Bankruptcy Sales: The Stalking Horse. Retrieved March 2012, from Jones

Day: http://www.jonesday.com/newsknowledge/publicationdetail.aspx?publication=2177

Lawrence Mittman and John D. Penn - Haynes and Boone LLP. (2012, February 1). Retrieved March 2012,

from Lexology: Can secured creditors credit bid in Chapter 11 plans? Supreme Court to decide

MacFarlane, A. a.-F. (2010). Show Me the Money! Stalking Horse Auctions in Cross-Border Insolvencies:

Value Maximization and Increase in Transparency. National Insolvency Review, 70-75.

Maerov, A. a. (2010, March 19). Courts Approve Stalking Horse Bids. Retrieved March 2012, from

Canadian Lawyer.ca: http://www.lawyersweekly.ca/index.php?section=article&articleid=1124

Montgomery, Alan and Perkins, Mark - Herbert Smith. (2010, March). The stalking horse disposals.

Retrieved March 2012, from Herber Smith:

http://www.herbertsmith.com/NR/rdonlyres/F507BFFE-BFE9-4782-A1E9-

56A47C65E7B5/16140/TheNortelRetructuringTheStalkingHorseIFLRMarch2010.PDF

Nadia Khattak - PCL US. (2009, April 28). Section 363 Sales: New Stalking Horse Strategies. Retrieved

March 2012, from Practical Law Company: http://us.practicallaw.com/6-385-9854

Page 17

Powlen, D. (2007, July 1). Bargains Await Buyers Skilled at Navigating Section 363 Minefields. Retrieved

March 2012, from Turnaround Management Association:

http://www.turnaround.org/Publications/Articles.aspx?ObjectId=7792&Mode=

Robinson, D. (2009). The Changing Face of Insolvency. Retrieved march 2012, from The Chambers

Magazine [Issue # 29]: http://www.chambersmagazine.co.uk/Article/THE-CHANGING-FACE-OF-

INSOLVENCY

Sarra, D. J. (2010). Stalking Horses, Rogue White Knights and Circling Vultures: Financing Insolvency.

Stevens, Turney - Harperth Capital. (2004, April). Section 363 Offers Big Advantages. Retrieved March

2012, from Nashville Medical News:

http://www.harpethcapital.com/articles/Section363_April04.pdf

Tonti, Amy M.and Sizemore, Luke A. - Reed Smith LLP. (2012, March 15). Successor liability – does it

survive a Section 363(f) sale? Retrieved March 15, 2012, from Lexology:

http://www.lexology.com/library/detail.aspx?g=378a7778-b6df-439f-b916-3a06b06bd313

Walsh, Timothy W. and Roldan, Vincent J. - DLA Piper. (2009, August 24). Section 363: A useful tool for

asset sales in bankruptcy. Retrieved March 2012, from DLA Piper:

http://www.dlapiper.com/section-363:a-useful-tool-for-asset-sales-in-bankruptcy/

Related Documents