The U.S. and Michigan Outlook for 2016-2018 Consensus Revenue Estimating Conference Lansing, Michigan January 14, 2016 University of Michigan RSQE

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

RSQE: January 2016

The U.S. and Michigan Outlook for 2016-2018

Consensus Revenue Estimating ConferenceLansing, MichiganJanuary 14, 2016

University of MichiganRSQE

RSQE: January 2016

The Current State of the Economy

RSQE: January 2016

International Headwinds• Board-based declines in commodity prices

– The price of oil keeps sliding lower

– Many other key commodity prices are down sharply

– Domestic oil-related activity contracting

• Slowing growth in developing economies

• Sharp increase in the value of the dollar– Hurts domestic exports, industrial activity

RSQE: January 2016

30

40

50

60

70

80

90

100

110

120

130

140

2008 2009 2010 2011 2012 2013 2014 2015

Dollars per Barrel, Monthly

Price of Oil(West Texas Intermediate Crude)

RSQE: January 2016

International Headwinds• Board-based declines in commodity prices

– The price of oil keeps sliding lower

– Many other key commodity prices are down sharply

– Domestic oil-related activity contracting

• Slowing growth in developing economies

• Sharp increase in the value of the dollar– Hurts domestic exports, industrial activity

RSQE: January 2016

Trade-Weighted Value of the Dollar

90

100

110

120

130

2008 2009 2010 2011 2012 2013 2014 2015

Index, Jan 1997 = 100

RSQE: January 2016

Latest Data • 2015q3 real GDP growth at 2.0 percent

– 0.7pp drag from inventory correction

• Real GDP up 2.1 percent y-o-y in 2015q3– Net exports reduced y-o-y growth by 0.7pp

• Domestic Final Sales up 2.8 percent y-o-y• Labor Market keeps improving

– October-December payroll job gains averaged over 280,000

– Unemployment rate down to 5.0 percent

– Initial Unemployment Insurance claims very low

RSQE: January 2016

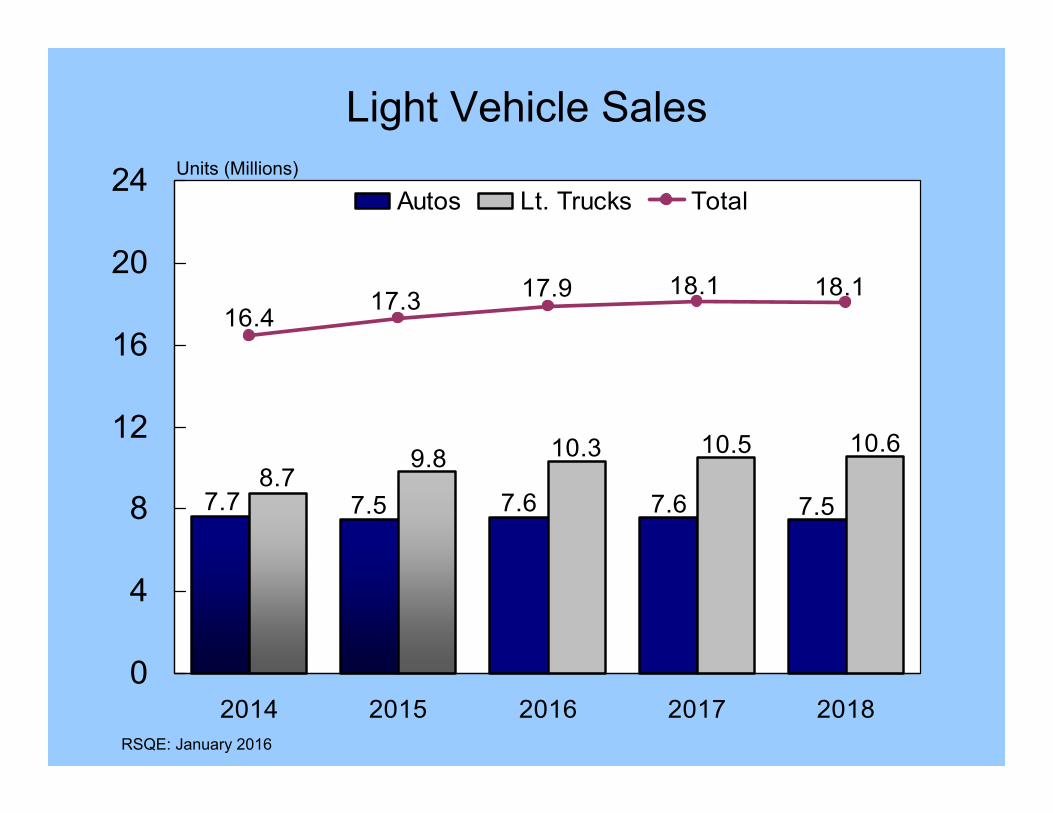

Latest Data • Light Vehicle Sales booming

– October-December averaged 17.8-million pace

– Annual sales averaged 17.3 million

– Just shy of a new record year

• Industrial Activity weak– Stronger dollar slowed manufacturing growth

– Mining-related activity down sharply, still falling

• Service Sector expanding at a solid pace

RSQE: January 2016

Light Vehicle Sales

8

9

10

11

12

13

14

15

16

17

18

19

20

2007 2008 2009 2010 2011 2012 2013 2014 2015

Units (Millions)

RSQE: January 2016

Latest Data • Light Vehicle Sales booming

– October-December averaged 17.8-million pace

– Annual sales averaged 17.3 million

– Just shy of a new record year

• Industrial Activity weak– Stronger dollar slowed manufacturing growth

– Mining-related activity down sharply, still falling

• Service Sector expanding at a solid pace

RSQE: January 2016

Key Inputs

RSQE: January 2016

Monetary Policy• New federal funds target range: 25-50bps

• Weak inflation did not delay the rate increase

– FOMC thinks temporary factors are to blame

• Pace of future tightening is data-dependent

– Most consistent with our outlook:

25bps increase every other FOMC meeting

– Largely reflecting slow inflation

RSQE: January 2016

Market Interest Rates

0.40.1 0.1 0.0 0.1

1.2

2.1

3.1

2.32.7 2.8

2.3 2.22.6

3.03.5

4.04.3 4.4

4.0 3.94.3

4.65.1

0

2

4

6

4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4

Actual Forecast

’13 2014 2015 2016 2017 2018

Percent

3-Month T-bill

10 Year T-Note

Conv. Mortgage

RSQE: January 2016

Fiscal Policy:• Bipartisan Budget Act of 2015

– Suspended debt ceiling through March 2017

– Sequestration partially fixed through FY 2017

– Increased Overseas Contingency Funding

• Fiscal 2016 spending bill– Several ACA-related taxes delayed

– Lifted oil export ban

• No tax reform on the horizon

RSQE: January 2016

Federal Budget, NIPA Basis(Billions of Dollars)

Forecast FY’14 FY’15 FY’16 FY’17 FY’18

Current receipts 3253.4 3392.0 3565.0 3755.4 3972.0% change 7.7 4.3 5.1 5.3 5.8

Current expenditures 3863.1 3988.2 4169.7 4341.0 4536.3% change 1.8 3.2 4.6 4.1 4.5Consumption 955.2 956.1 981.4 1016.4 1052.9% change -2.0 0.1 2.7 3.6 3.6

Transfer payments 2411.8 2537.0 2644.1 2751.8 2880.7% change 3.2 5.2 4.2 4.1 4.7

Surplus (+) or deficit (-) -609.7 -596.2 -604.7 -585.6 -564.3Percent of GDP -3.5 -3.3 -3.3 -3.0 -2.8

RSQE: January 2016

RSQE Forecast

RSQE: January 2016

2.4

2.8

2.4 2.5 2.5

0.0

1.0

2.0

3.0

4.0

2014 2015 2016 2017 2018

Real GDP GrowthPercent

RSQE: January 2016

Growth Rate of Real GDP

2.5

0.6

3.8

-0.9

4.64.3

2.1

3.9

2.0 1.9 2.32.9

-2

-1

0

1

2

3

4

5

6

4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4

Actual Forecast

’13 2014 2015 2016 2017 2018

2.5 2.5 2.1 2.8 2.7 2.3

4th Quarter to 4th Quarter Growth Rate of Real GDP (%)

Percent, AR

RSQE: January 2016

Nonfarm Payroll Employment Gainsand Unemployment Rate

253

126165

185

240203

284

219181

5.05.4

6.6

5.7

7.0

5.04.8

4.5 4.4

0

100

200

300

400

4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 44

5

6

7

8Actual Forecast

’13 2014 2015 2016 2017 2018

PercentThousands of Jobs per Month

Unemployment Rate

Avg. Monthly Job Gains*

* 1/3 the change in quarterly value

2.5 2.9 2.7 2.5 2.1 1.74th Quarter to 4th Quarter Job Change (Millions)

RSQE: January 2016

2.12.02.01.81.71.5

0.1

2.3 2.4

1.6

-1

0

1

2

3

4

2014 2015 2016 2017 2018

Core All ItemsPercent

Consumer Price Inflation(CPI-U)

RSQE: January 2016

Housing Market

1.101.04

0.650.71

0.89

0.440.440.410.400.35

1.531.47

1.001.11

1.30

0.0

0.5

1.0

1.5

2.0

2014 2015 2016 2017 2018

Singles Multis Total

5.115.084.904.64

4.33

0

2

4

6

2014 2015 2016 2017 2018

A. Housing StartsUnits (Millions) Units (Millions)

B. Existing Home Sales*

*Single-family homes

RSQE: January 2016

7.57.67.57.7 7.6

10.68.7

9.8 10.3 10.5

18.117.917.316.418.1

0

4

8

12

16

20

24

2014 2015 2016 2017 2018

Autos Lt. Trucks TotalUnits (Millions)

Light Vehicle Sales

RSQE: January 2016

Risks to the Outlook:

• World Economic Growth• Commodity prices• Financial market volatility• Monetary policy

– Policy over-reaction to noisy data– Our assessment of Fed’s policy stance

• Abnormal Weather

RSQE: January 2016

UNIVERSITY OF MICHIGAN

THE MICHIGAN ECONOMIC OUTLOOK

FOR 2016–2018

JANUARY 14, 2016

Motor Vehicle Industry Revisited

RSQE: January 2016

0

5

10

15

20

'90 '92 '94 '96 '98 '00 '02 '04 '06 '08 '10 '12 '14 '16 '18

With data

U.S. Light Vehicle Sales, 1990–2018Millions

17

18

'91 '93 '95 '97 '99 '01 '03 '05 '07 '09 '11 '13 '15 '17

RSQE: January 2016

With data

2014 20162015 2017 2018

U.S. Light Vehicle SalesTotal vs. Detroit Three, 2014–18

Total

Millionsof Units

Detroit Three

7.3 7.6 7.9 8.0 8.0

02468

101214161820

16.417.3 17.9 18.1 18.1

Annual % Detroit Threemarket share

44.3 44.144.544.4

43.6

RSQE: January 2016

Michigan Outlook

RSQE: January 2016

0

1

2

3

4

2.0 1.6 1.8 1.5 1.0

82.7 67.2 76.5 63.0 45.5

4th Quarter to 4th Quarter Growth Rate (%)

4th Quarter to 4th Quarter Change (Thousands)1.5

63.7

4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 42014 2015 2016’13 2017 2018

Annual Rate(%)

Michigan Job Growth

Actual Forecast

RSQE: January 2016

2.6

3.8

1.4

0.7

1.4 1.61.2

0.8

Change in Jobs by Industry Sector(Thousands of jobs)

2013q4to

2014q4

2014q4to

2015q4

2015q4to

2016q4

2016q4to

2017q4

2017q4to

2018q4

Total jobs

Government

Manufacturing

Private educ. &health svcs.

Prof. & bus. svcs.

Construction

Trade, trans., util.

67

-2

18

6

17

7

12

77

-7

21

18

15

9

5

63

1

7

6

15

9

11

64

0

4

4

17

12

12

46

1

-2

5

13

8

9

RSQE: January 2016

3,8003,9004,0004,1004,2004,3004,4004,5004,6004,7004,800

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18

With data

Michigan Wage and Salary EmploymentFirst Quarter of 2000 to Fourth Quarter of 2018

Thousands of jobs

ForecastPeak ’00q2

Loss: ’00q2–’9q3 = 858,400

Trough ’9q3

’18q4

’15q3

Gain:’9q3–’18q4 = 624,700(73% of jobs lost)

RSQE: January 2016

Michigan Unemployment Rate2014–18

0%1%2%3%4%5%6%7%8%9%

10%

7.1

5.44.9 4.6 4.5

2014 2015 2016 2017 2018

RSQE: January 2016

6.5 5.0 4.8 4.5 4.54th Quarter Unemployment Rate

Detroit CPI

2014 2015 2016 2017

Michigan Inflation and Income Growth

1.1

– 1.3

1.52.4

2018

2.4

RSQE: January 2016

0%1%2%3%4%5%6%

–1%–2%

Personal Income

4.1 4.3 4.3 4.4 4.5

0%1%2%3%4%5%6%

–1%–2%

Real Disposable Income

2.7 2.71.8

5.1

1.8

0%1%2%3%4%5%6%

–1%–2%

State Revenue Outlook

RSQE: January 2016

RSQE Forecast – State Revenues by Fiscal Year (Millions of dollars)

Actual2015P

Forecast2016 2017 2018

GFGP revenue

(% change)

9,928

(10.1)

10,035

(1.1)

10,345

(3.1)

10,837

(4.7)

RSQE: January 2016

PPreliminary

RSQE Forecast – State Revenues by Fiscal Year (Millions of dollars)

Actual2015P

Forecast2016 2017 2018

GFGP revenue

(% change)

9,928

(10.1)

10,035

(1.1)

10,345

(3.1)

10,837

(4.7)

RSQE: January 2016

PPreliminary

Earmarked stateSAF revenue(% change)

11,766

(2.1)

12,175

(3.5)

12,610

(3.6)

13,059

(3.6)

Michigan Outlook Summary

The job recovery enters its seventh year, and adds 172,200 jobs from yearend 2015 to yearend 2018.

The continuing recovery is consistent with an expandingU.S. economy, strong vehicle sales, and continued improve-ment in the housing sector.

RSQE: January 2016

Job gains average 57,400 per year over that time span,a bit slower than the pace in recent years.

The top three job producers over the forecast period arethe professional and business services sector, the trade-transportation-utilities sector, and construction.

Michigan Outlook Summary

A key challenge will be diversifying sources of jobs growthas the manufacturing expansion matures.

The 9-year recovery through 2018 replenishes 73 percentof the jobs lost from mid-2000 to summer 2009 . . .

returning the state to the same job level posted at thebeginning of 2003.

RSQE: January 2016

Unemployment continues to decline, but more slowly asslack in the labor market continues to dissipate.Local prices begin to increase again as energy prices stopfalling and national inflation rises.

UNIVERSITY OF MICHIGANUNIVERSITY OF MICHIGAN

www.rsqe.econ.lsa.umich.edu

Related Documents