The Unique Alternative to the Big Four ® ESOP Features You May Not Have Considered Michigan Chapter of The ESOP Association Annual Conference September 25, 2014 Presented by: Pete Shuler - Crowe Horwath LLP ([email protected]) Justin Stemple – Warner Norcross & Judd ([email protected])

The Unique Alternative to the Big Four ® ESOP Features You May Not Have Considered Michigan Chapter of The ESOP Association Annual Conference September.

Dec 25, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

The Unique Alternative to the Big Four®

ESOP Features You May Not Have ConsideredMichigan Chapter of The ESOP Association

Annual Conference

September 25, 2014

Presented by: Pete Shuler - Crowe Horwath LLP ([email protected])

Justin Stemple – Warner Norcross & Judd ([email protected])

The Unique Alternative to the Big Four®

© 2013 Crowe Horwath LLP 2Audit | Tax | Advisory | Risk | Performance

Preface

Please fill out a session evaluation form and drop it off at the table outside of the main room Your feedback on topics and presenters is important and will be used to develop

subsequent programs

Take a moment to silence your cell phone

The Unique Alternative to the Big Four®

© 2013 Crowe Horwath LLP 3Audit | Tax | Advisory | Risk | Performance

Coordination with 401(k) Plan

Look for *Coordination with 401(k) Plan* noted throughout presentation

Must be the same HCE definition/assumptions Limitation Year definition

Top-heavy contribution coordination

The Unique Alternative to the Big Four®

© 2013 Crowe Horwath LLP 4Audit | Tax | Advisory | Risk | Performance

“Generous” Entry and Allocation Provisions

Maximum wait to enter: Service – 12 months (with 1,000 hours), then enter on the following semi-annual entry

date Age – 21

Maximum allocation provisions Work 1,000 hours during the plan year Be employed on the last day of the plan year

The Unique Alternative to the Big Four®

© 2013 Crowe Horwath LLP 5Audit | Tax | Advisory | Risk | Performance

“Generous” Entry and Allocation Provisions

Why would you want to be more generous? Can help resolve issues with maximum permissible contribution (25% of eligible payroll)

by increasing the eligible payroll Can help resolve issues with maximum annual allocation each participant can receive

by spreading the allocation across more participants Can get employees focused on the ESOP more quickly – they don’t have to wait up to

18 months to enter and up to three years before they get a statement

What is the downside? Current employees who had to wait a year to enter may not be happy Most turnover occurs early in employment and with younger employees Spreads the allocation a bit (less for each existing participant), but not as much as you

may think

The Unique Alternative to the Big Four®

© 2013 Crowe Horwath LLP 6Audit | Tax | Advisory | Risk | Performance

Dual Eligibility

Different contributions may have different eligibility rules Why would you want that?

Can allow new hires to starting contributing to the 401(k) quickly but require longer service to receive ESOP contributions

Different eligibility rules for “fixed” work schedules v. non-fixed/irregular work schedules Immediate for fixed; 1 year and age 21 for non-fixed Attempts to address part-time employees without delaying all employees

The Unique Alternative to the Big Four®

© 2013 Crowe Horwath LLP 7Audit | Tax | Advisory | Risk | Performance

Exclusions From Eligibility

Certain exclusions have no impact on nondiscrimination testing Collective bargaining group members Non-employees Nonresident aliens without any US earned income

Other nondiscriminatory categories may be excluded Division Facility Subsidiary Job classification Students/interns

No hours-based exclusions Part-time Temporary Seasonal

Non-benefitting employees

The Unique Alternative to the Big Four®

© 2013 Crowe Horwath LLP 8Audit | Tax | Advisory | Risk | Performance

Service-based Allocation

Two methods of allocation for employer contributions are approved without additional testing Compensation-based Per capita

Other methods are generally permissible as long as they don’t discriminate in favor of “highly compensated employees” Test must be performed annually to ensure that the allocation is “nondiscriminatory”

The Unique Alternative to the Big Four®

© 2013 Crowe Horwath LLP 9Audit | Tax | Advisory | Risk | Performance

Service-based Allocation

Example

ABC CompanyEmployee Stock Ownership Plan

Eligible Years ofParticipants Wages Service Wages Service Total Wages Points Wages Points

John Smith 50,000 10 50 100 150 15,873 20,134 16% 20%Joe Green 30,000 15 30 150 180 9,524 24,161 10% 24%Ed Brown 40,000 12 40 120 160 12,698 21,477 13% 21%Mary Johnson 120,000 1 120 10 130 38,095 17,450 38% 17%Edna Williams 75,000 5 75 50 125 23,810 16,779 24% 17%Total 315,000 43 315 430 745 100,000 100,000 100% 100%

Points Allocation ($100,000) Allocation %

The Unique Alternative to the Big Four®

© 2013 Crowe Horwath LLP 10Audit | Tax | Advisory | Risk | Performance

Service-based Allocation

Why would you want to use a service-based allocation? If the desire is to reward participants based at least partially on their service, service-

based allocation works Lot of flexibility in designing the formula, as long as the allocation is nondiscriminatory

What is the downside? Desire may be to reward employees based on current compensation, not service Could adversely impact recruiting Nondiscrimination testing must be passed

If highly compensated employees have the most service, test may not pass

Repurchase obligation impact Could put more shares into the accounts of participants who are closer to diversification and

retirement

The Unique Alternative to the Big Four®

© 2013 Crowe Horwath LLP 11Audit | Tax | Advisory | Risk | Performance

Compensation-based Allocation

Most common allocation method is pro rata by compensation Most common compensation definition is gross W-2 (includes pre-tax deferrals)

Withholding wages and Section 415 compensation are also pre-approved

Pre-approved exclusion of taxable fringes: “reimbursements or other expense allowances, cash and noncash fringe benefits, moving expenses, deferred compensation, and welfare benefits” – must be in the plan

Other exclusions permitted if non-discriminatory Bonuses Overtime Commissions Others?

The Unique Alternative to the Big Four®

© 2013 Crowe Horwath LLP 12Audit | Tax | Advisory | Risk | Performance

401(k) plan-based Allocation

Matching allocation Safe harbor allocation

Nonelective Matching QACA Eligibility rules/compensation definition Safe harbor notice(s) 401(k) must provide for safe harbor to be satisfied in the ESOP

*Coordination with 401(k) plan*

The Unique Alternative to the Big Four®

© 2013 Crowe Horwath LLP 13Audit | Tax | Advisory | Risk | Performance

Correction/Avoidance Options for Section 415 Excess

Section 415 Limits “annual additions” participants can receive under all company retirement plans to

lesser of their 100% of pay or $52,000 (adjusted for inflation annually) Annual additions are generally employee deferrals and Roth contributions, employer

contributions, and reallocated forfeitures Catch-up contributions (currently $5,500) are not counted for 415 purposes

Correction methods Return employee deferrals/Roth contributions to the individual Forfeit associated matching contributions Reallocate excess amounts to those who have not yet hit the 415 limit

*Coordination with 401(k) Plan*

The Unique Alternative to the Big Four®

© 2013 Crowe Horwath LLP 14Audit | Tax | Advisory | Risk | Performance

Correction/Avoidance Options for Section 415 Excess

Return employee contributions/forfeit associated match For participants at least age 50, deferrals that would have been returned can be

recategorized as catch-up contributions, if catch up contributions have not yet been fully utilized. This means they stay in the 401(k) plan.

Participant receives their own contributions back, less any taxes Positively impacts the average deferral percentage test if the participant is a highly

compensated employee Downside – Employees don’t like to get their deferrals back

Reallocating excess Generally the avoidance of a failure, not a correct Because the 415 limit is not hit, due to change in allocation, no deferrals are

recharacterized Any excess is reallocated to those who have not yet hit the limit, so more allocations for

lower paid people Downside – not financially beneficial for those who hit the limit

The Unique Alternative to the Big Four®

© 2013 Crowe Horwath LLP 15Audit | Tax | Advisory | Risk | Performance

Forfeitures

Timing Immediate upon distribution Five breaks in service

Use of forfeitures Expenses if cash forfeitures Reallocate Reduce next contribution

“Lost” participants http://www.dol.gov/ebsa/publications/2013ACreport3.html

No “Mr. Forfeiture”

The Unique Alternative to the Big Four®

© 2013 Crowe Horwath LLP 16Audit | Tax | Advisory | Risk | Performance

Paying ESOP Loan with Contributions v. Dividends

Sources of funds for the loan payment determines how the shares released by the loan payment are allocated

If employer contributions are used to fund the loan payment, the shares released are allocated based on compensation/points

If dividends/income distributions are used to fund the loan payment, at least a portion of the shares released are allocated based on stock account balance

Dividends earned on shares in participant accounts are always allocated on stock account balance

Dividends earned on suspense accounts shares can be allocated in different ways, but generally either on stock account balance or in the same manner as the contribution

The Unique Alternative to the Big Four®

© 2013 Crowe Horwath LLP 17Audit | Tax | Advisory | Risk | Performance

Paying ESOP Loan with Contributions v. Dividends

Not always a choice:

Limits on contributions can necessitate the need for dividends/income distributions to fund the loan payment Example - $2 million loan payment, but only $1.5 million can be contribution. $0.5 million

dividend can be used to fund the remainder 404 Limit is 25% of eligible compensation 415 Limit – dividends can be used to avoid a failure

If there are non-ESOP shareholders, and they receive dividends/income distributions, the ESOP must receive these as well Generally used to repay the loan

Similarly, some preferred stock (C-Corps only) requires a dividend Generally used to repay the loan

The Unique Alternative to the Big Four®

© 2013 Crowe Horwath LLP 18Audit | Tax | Advisory | Risk | Performance

Paying ESOP Loan with Contributions v. Dividends

But if there is a choice:

Use of dividends/income distributions will result in skewing the allocation towards participants with larger balances – longer-term participants If too much dividend is used, new participants may get little of the share release Can impact 409(p) testing (generally adversely) Can impact the repurchase obligation by putting more shares in the accounts of participants who

are closer to diversification and retirement

Keep in mind that FMV test must be passed

Additional deduction for C-Corps, not for S-Corps

The Unique Alternative to the Big Four®

© 2013 Crowe Horwath LLP 19Audit | Tax | Advisory | Risk | Performance

Pass-through Dividends

Dividends paid directly to participants based on their ESOP shares C-Corps only Can be paid directly from the company to the participant or through the ESOP no later

than 90 days after plan year end Can include allocated and suspense account dividends Not considered a distribution, so:

No notice and consent requirement No mandatory withholding Not eligible for rollover No early withdrawal penalty Reported on 1099-DIV not 1099R

Benefits Allows participants to get current income from the ESOP Can make the ESOP more meaningful, especially to younger participants

The Unique Alternative to the Big Four®

© 2013 Crowe Horwath LLP 20Audit | Tax | Advisory | Risk | Performance

Dividend Reinvestment Election

Very similar to pass-through dividends except that participants can elect to: Receive a pass-through dividend, or Have their dividend stay in the ESOP and be reinvested in employer stock

Can be based on vested shares only or on total shares, but all dividends on which participant is given an election are immediately 100% vested

May be offered to active participants or to all participants Reasonable opportunity to make election prior to dividend payment or distribution Opportunity to change election at least annually and when dividend

allocation/payment affected by plan document Default elections allowed

The Unique Alternative to the Big Four®

© 2013 Crowe Horwath LLP 21Audit | Tax | Advisory | Risk | Performance

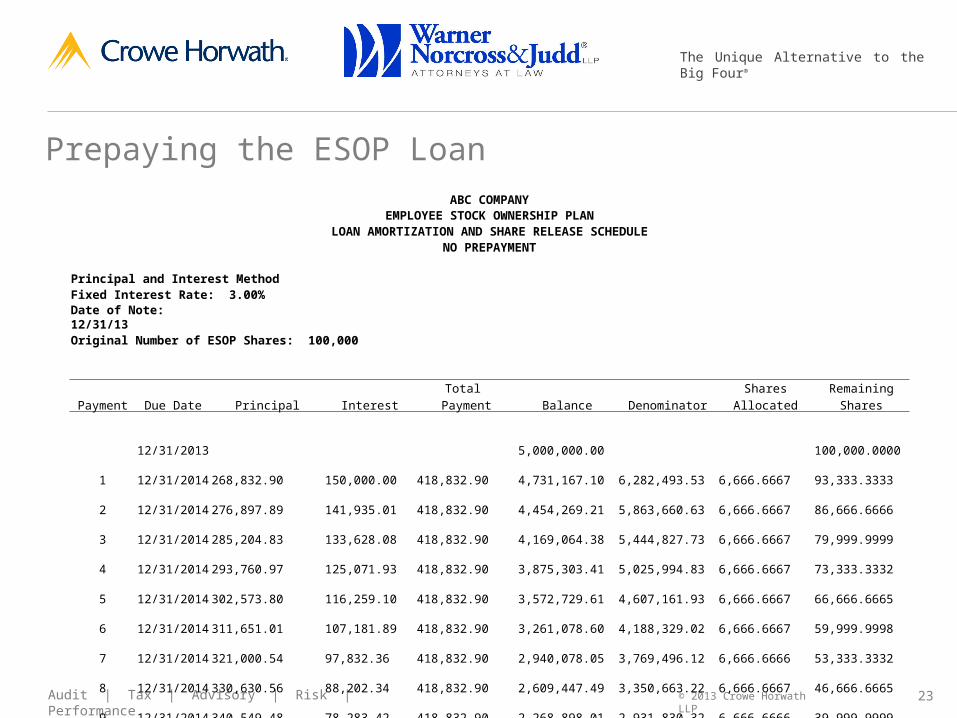

Prepaying the ESOP Loan

Share release for most ESOPs is calculated as follows:

Current year principal and interest (P&I) payments

÷

Current Year P&I + All Scheduled Future P&I

*

Suspense Account Shares at Beginning of the Year

The Unique Alternative to the Big Four®

© 2013 Crowe Horwath LLP 22Audit | Tax | Advisory | Risk | Performance

Prepaying the ESOP Loan

Prepaying the ESOP loan means making more than the scheduled payment in a year or years Results in shares being released and allocated faster to participants

Why would you want to prepay? Gets more shares into the accounts of participants in the ESOP at the time of the

prepayment

Why wouldn’t you want to prepay? Since shares are released faster, there are fewer shares for participants down the road Affects repurchase obligation by loading up accounts

The Unique Alternative to the Big Four®

© 2013 Crowe Horwath LLP 23Audit | Tax | Advisory | Risk | Performance

Prepaying the ESOP LoanABC COMPANY

EMPLOYEE STOCK OWNERSHIP PLANLOAN AMORTIZATION AND SHARE RELEASE SCHEDULE

NO PREPAYMENT

Principal and Interest MethodFixed Interest Rate: 3.00%Date of Note: 12/31/13Original Number of ESOP Shares: 100,000

Total Shares Remaining

Payment Due Date Principal Interest Payment Balance Denominator Allocated Shares

12/31/2013 5,000,000.00 100,000.0000 1 12/31/2014 268,832.90 150,000.00 418,832.90 4,731,167.10 6,282,493.53 6,666.6667 93,333.3333 2 12/31/2014 276,897.89 141,935.01 418,832.90 4,454,269.21 5,863,660.63 6,666.6667 86,666.6666 3 12/31/2014 285,204.83 133,628.08 418,832.90 4,169,064.38 5,444,827.73 6,666.6667 79,999.9999 4 12/31/2014 293,760.97 125,071.93 418,832.90 3,875,303.41 5,025,994.83 6,666.6667 73,333.3332 5 12/31/2014 302,573.80 116,259.10 418,832.90 3,572,729.61 4,607,161.93 6,666.6667 66,666.6665 6 12/31/2014 311,651.01 107,181.89 418,832.90 3,261,078.60 4,188,329.02 6,666.6667 59,999.9998 7 12/31/2014 321,000.54 97,832.36 418,832.90 2,940,078.05 3,769,496.12 6,666.6666 53,333.3332 8 12/31/2014 330,630.56 88,202.34 418,832.90 2,609,447.49 3,350,663.22 6,666.6667 46,666.6665 9 12/31/2014 340,549.48 78,283.42 418,832.90 2,268,898.01 2,931,830.32 6,666.6666 39,999.9999

10 12/31/2014 350,765.96 68,066.94 418,832.90 1,918,132.05 2,512,997.41 6,666.6667 33,333.3332 11 12/31/2014 361,288.94 57,543.96 418,832.90 1,556,843.11 2,094,164.51 6,666.6666 26,666.6666 12 12/31/2014 372,127.61 46,705.29 418,832.90 1,184,715.50 1,675,331.61 6,666.6667 19,999.9999 13 12/31/2014 383,291.44 35,541.47 418,832.90 801,424.07 1,256,498.71 6,666.6666 13,333.3333 14 12/31/2014 394,790.18 24,042.72 418,832.90 406,633.89 837,665.80 6,666.6667 6,666.6666 15 12/31/2014 406,633.89 12,199.02 418,832.90 - 418,832.90 6,666.6666 -

Totals 5,000,000.00 1,282,493.53 6,282,493.53 100,000.0000

The Unique Alternative to the Big Four®

© 2013 Crowe Horwath LLP 24Audit | Tax | Advisory | Risk | Performance

Prepaying the ESOP LoanABC COMPANY

EMPLOYEE STOCK OWNERSHIP PLANLOAN AMORTIZATION AND SHARE RELEASE SCHEDULE

PREPAYMENT

Principal and Interest MethodFixed Interest Rate: 3.00%Date of Note: 12/31/13Original Number of ESOP Shares: 100,000

Total Shares Remaining

Payment Due Date Principal Interest Payment Balance Denominator Allocated Shares

12/31/2013 5,000,000.00 100,000.0000 1 12/31/2014 468,832.90 150,000.00 618,832.90 4,531,167.10 6,179,975.59 10,013.5169 89,986.4831 2 12/31/2014 282,897.89 135,935.01 418,832.90 4,248,269.21 5,561,142.69 6,777.2582 83,209.2249 3 12/31/2014 291,384.83 127,448.08 418,832.90 3,956,884.38 5,142,309.79 6,777.2582 76,431.9667 4 12/31/2014 300,126.37 118,706.53 418,832.90 3,656,758.01 4,723,476.88 6,777.2582 69,654.7085 5 12/31/2014 309,130.16 109,702.74 418,832.90 3,347,627.85 4,304,643.98 6,777.2582 62,877.4503 6 12/31/2014 318,404.07 100,428.84 418,832.90 3,029,223.78 3,885,811.08 6,777.2582 56,100.1921 7 12/31/2014 327,956.19 90,876.71 418,832.90 2,701,267.59 3,466,978.18 6,777.2582 49,322.9339 8 12/31/2014 337,794.87 81,038.03 418,832.90 2,363,472.72 3,048,145.27 6,777.2582 42,545.6757 9 12/31/2014 347,928.72 70,904.18 418,832.90 2,015,544.00 2,629,312.37 6,777.2582 35,768.4175

10 12/31/2014 358,366.58 60,466.32 418,832.90 1,657,177.42 2,210,479.47 6,777.2582 28,991.1593 11 12/31/2014 369,117.58 49,715.32 418,832.90 1,288,059.84 1,791,646.57 6,777.2582 22,213.9011 12 12/31/2014 380,191.11 38,641.80 418,832.90 907,868.73 1,372,813.66 6,777.2582 15,436.6429 13 12/31/2014 391,596.84 27,236.06 418,832.90 516,271.89 953,980.76 6,777.2582 8,659.3847 14 12/31/2014 403,344.75 15,488.16 418,832.90 112,927.14 535,147.86 6,777.2582 1,882.1265 15 12/31/2014 112,927.14 3,387.81 116,314.96 - 116,314.96 1,882.1265 0.0000

Totals 5,000,000.00 1,179,975.59 6,179,975.59 100,000.0000

The Unique Alternative to the Big Four®

© 2013 Crowe Horwath LLP 25Audit | Tax | Advisory | Risk | Performance

Account Segregation/Conversion

Conversion of terminated participants’ accounts to cash prior to their distribution payment

Can occur in year of termination or any later year, whether or not the participant is eligible to receive a distribution

Generally done through recycling of shares, although could be done through redemption (with an updated valuation)

Best to convert all shares, not just the participants vested shares Segregation/conversion feature needs to be in the plan document

Cannot be discretionary, but the decision to put money into the ESOP to convert shares is up to the company each year

Need to have a provisions for partial conversion, if company does not want to put full amount in Generally pro-rata or based on termination date

The Unique Alternative to the Big Four®

© 2013 Crowe Horwath LLP 26Audit | Tax | Advisory | Risk | Performance

Account Segregation/Conversion

Why would you want to convert shares? Gets shares (and future appreciation of those shares) into the hands of your active

participants who can still affect the value of the company Gets risk of owning the shares out of the hands of terminated participants who no

longer have a stake in the company May not want terminated participants who now work for competitors to see your stock

price In a rising stock price environment, accelerates cash needed for the repurchase

obligation but reduces the amount paid to the participant overall

Why wouldn’t you want to convert shares? Accelerates cash flow needs Fiduciary obligation to invest the proceeds of the conversion

Can’t just stick it in cash *Coordination with 401(k) Plan* if proceeds to be transferred to the 401(k)

The Unique Alternative to the Big Four®

© 2013 Crowe Horwath LLP 27Audit | Tax | Advisory | Risk | Performance

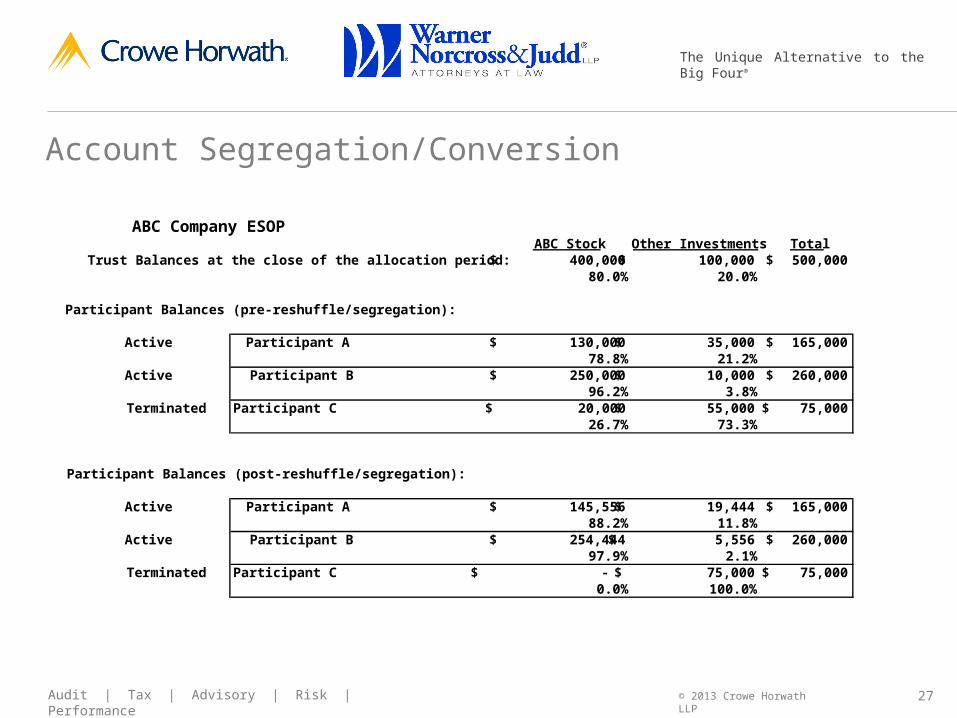

Account Segregation/Conversion

ABC Company ESOPABC Stock Other Investments Total

Trust Balances at the close of the allocation period: 400,000$ 100,000$ 500,000$ 80.0% 20.0%

Participant Balances (pre-reshuffle/segregation):

Active Participant A 130,000$ 35,000$ 165,000$ 78.8% 21.2%

Active Participant B 250,000$ 10,000$ 260,000$ 96.2% 3.8%

Terminated Participant C 20,000$ 55,000$ 75,000$ 26.7% 73.3%

Participant Balances (post-reshuffle/segregation):

Active Participant A 145,556$ 19,444$ 165,000$ 88.2% 11.8%

Active Participant B 254,444$ 5,556$ 260,000$ 97.9% 2.1%

Terminated Participant C -$ 75,000$ 75,000$ 0.0% 100.0%

The Unique Alternative to the Big Four®

© 2013 Crowe Horwath LLP 28Audit | Tax | Advisory | Risk | Performance

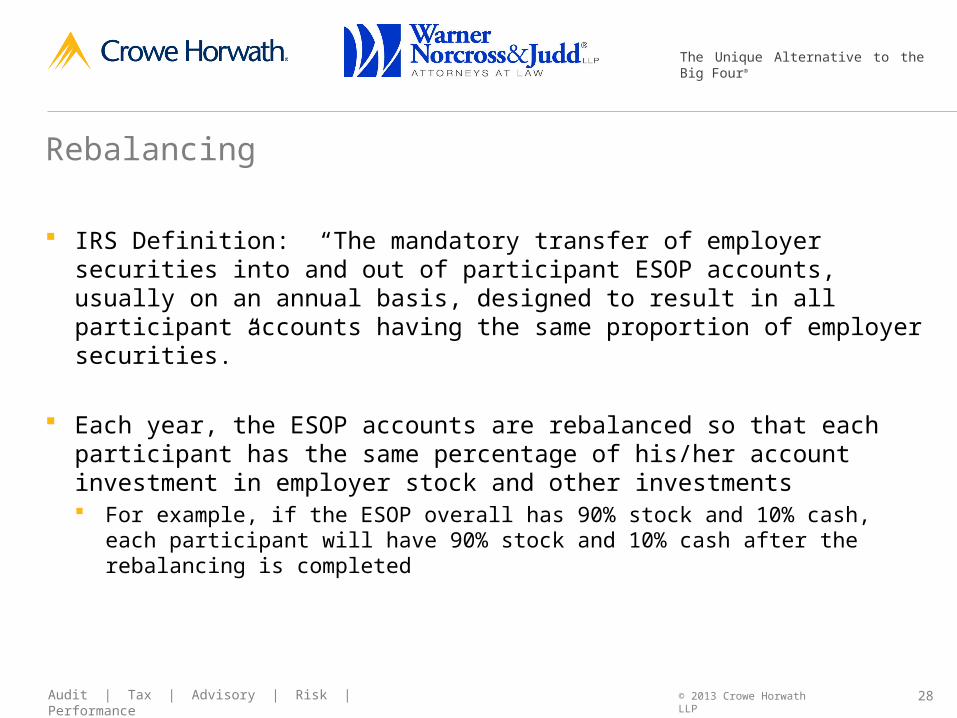

Rebalancing

IRS Definition: “The mandatory transfer of employer securities into and out of participant ESOP accounts, usually on an annual basis, designed to result in all participant accounts having the same proportion of employer securities.”

Each year, the ESOP accounts are rebalanced so that each participant has the same percentage of his/her account investment in employer stock and other investments For example, if the ESOP overall has 90% stock and 10% cash, each participant will

have 90% stock and 10% cash after the rebalancing is completed

The Unique Alternative to the Big Four®

© 2013 Crowe Horwath LLP 31Audit | Tax | Advisory | Risk | Performance

Diversification

Statutory Diversification

Enhanced diversification Longer period Higher percentage

Mandatory diversification

The Unique Alternative to the Big Four®

© 2013 Crowe Horwath LLP 33Audit | Tax | Advisory | Risk | Performance

Beneficiaries

Designation of Beneficiary Form

Default if no named beneficiary? Estate? Surviving Spouse? If no spouse, what next? Divorce? Disclaimers?

The Unique Alternative to the Big Four®

© 2013 Crowe Horwath LLP 34Audit | Tax | Advisory | Risk | Performance

QDROs

Qualified domestic relations order (“QDRO”) Alternate Payee

Spouse, former spouse, child, or other dependent

ESOP distributions v. Family Law/QDRO processor QDRO distribution provisions

When, how much, how paid

QDRO Procedures Sample QDRO

ESOP Other qualified retirement plans

The Unique Alternative to the Big Four®

© 2013 Crowe Horwath LLP 35Audit | Tax | Advisory | Risk | Performance

In-Service Distributions

When? Age 59 ½? Normal Retirement Age?

How much?

May accelerate repurchase obligation May reduce total amount paid Mitigates incentive to quit to gain access to ESOP account Acts as additional diversification tool

The Unique Alternative to the Big Four®

© 2013 Crowe Horwath LLP 36Audit | Tax | Advisory | Risk | Performance

Distributions

Form Lump sum of cash Installments of cash Lump sum of stock

Redeemed by the company Lump sum Installments – note / adequate security

Recycled by the ESOP Lump sum Installments – note / adequate security

The Unique Alternative to the Big Four®

© 2013 Crowe Horwath LLP 37Audit | Tax | Advisory | Risk | Performance

Distributions

Timing Immediate After plan year end Up to five year delay Financed securities delay

Mandatory cashouts $1,000 direct payment $1,000-$5,000 IRA rollover

Distribution Policy Distribution forms

The Unique Alternative to the Big Four®

© 2013 Crowe Horwath LLP 38Audit | Tax | Advisory | Risk | Performance

Questions?

Thank you!

The Unique Alternative to the Big Four®

© 2013 Crowe Horwath LLP 39Audit | Tax | Advisory | Risk | Performance

Postscript

Please fill out a session evaluation form and drop it off at the table outside of the main room Your feedback on topics and presenters is important and will be used to develop

subsequent TEA programs

Related Documents