The Super Circular – Will It Be A Game Changer? April 14, 2015 Beth A. Wood, CPA, State Auditor 1 NASACT Middle Management Conference

The Super Circular – Will It Be A Game Changer? April 14, 2015 Beth A. Wood, CPA, State Auditor 1 NASACT Middle Management Conference.

Dec 19, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

The Super Circular – Will It Be A Game Changer?

April 14, 2015

Beth A. Wood, CPA, State Auditor1

NASACT Middle Management Conference

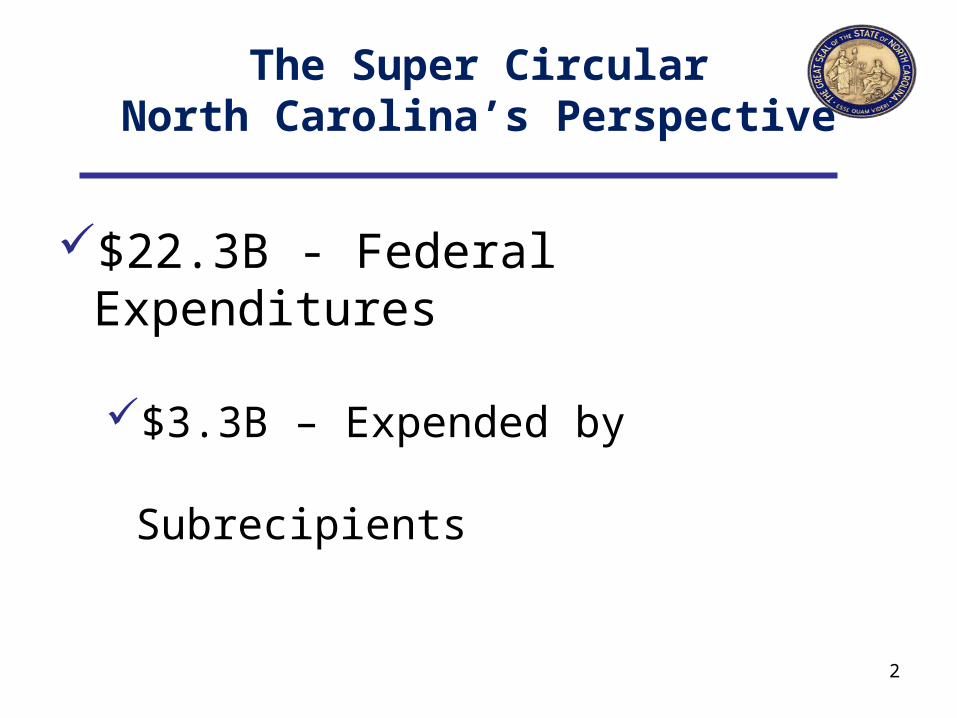

The Super CircularNorth Carolina’s Perspective

$22.3B - Federal Expenditures

$3.3B – Expended by Subrecipients

2

The Super CircularNorth Carolina’s Perspective

State Agencies – 26+

Universities - 17

Community Colleges – 58

Clerks of Courts - 100

3

The Super CircularNorth Carolina’s Perspective

County Governments – 100

Cities/Towns – 552

Local School Boards - 115

Authorities – Water/Sewer/ - 500+

4

The Super CircularWhy?

Objective:Strengthen Oversight and Focus

Audits Where There is The Greatest Risk of Waste, Fraud and Abuse of Taxpayer Dollars…..

5

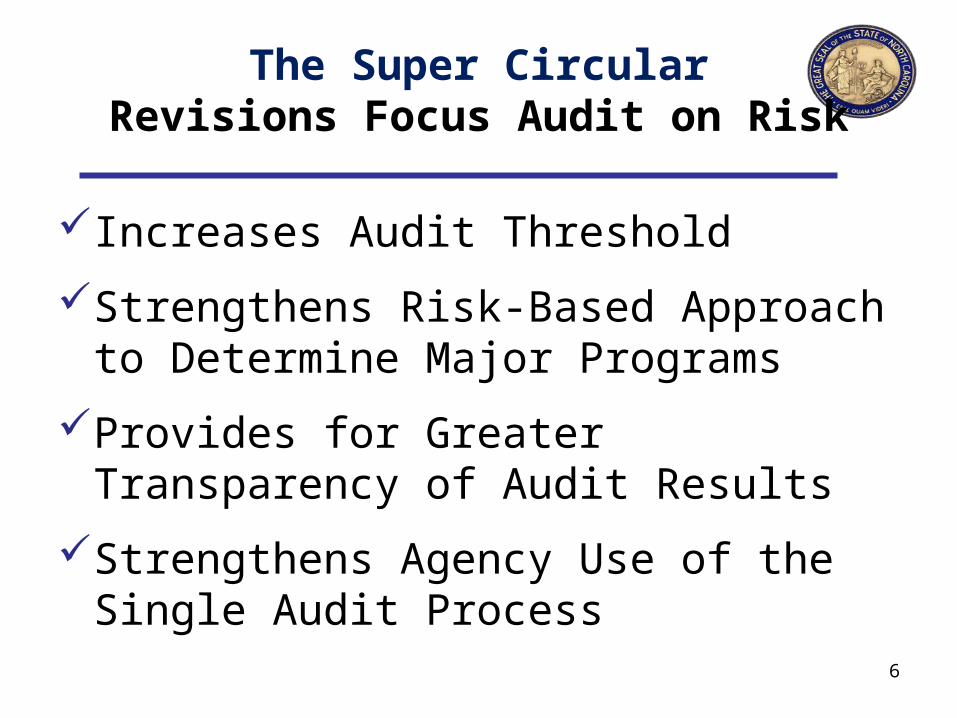

The Super CircularRevisions Focus Audit on Risk

Increases Audit Threshold

Strengthens Risk-Based Approach to Determine Major Programs

Provides for Greater Transparency of Audit Results

Strengthens Agency Use of the Single Audit Process

6

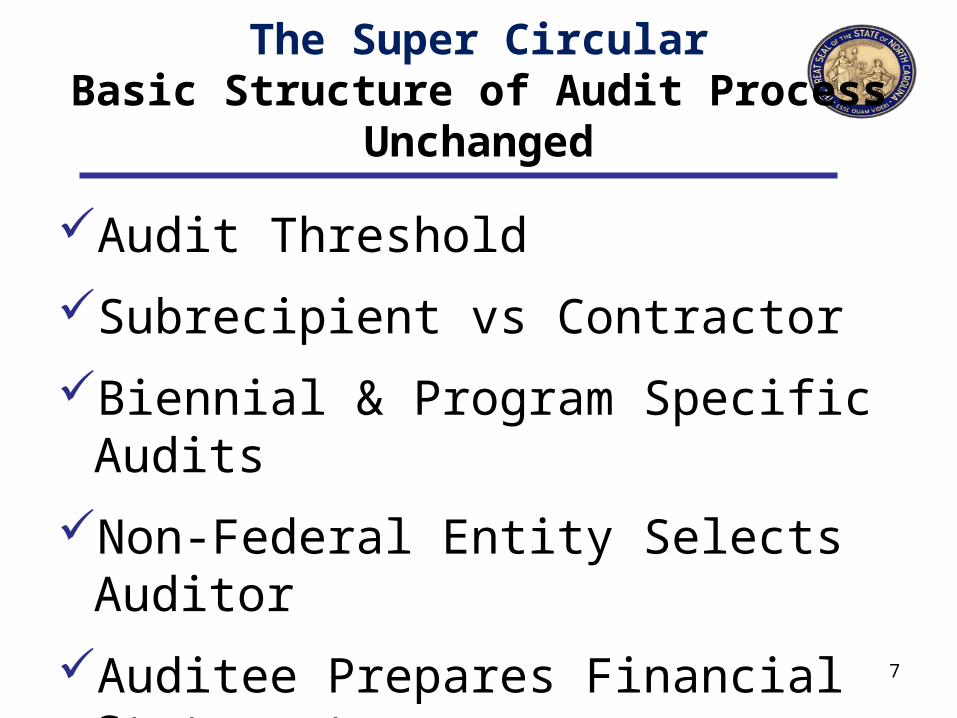

The Super CircularBasic Structure of Audit Process

Unchanged

Audit Threshold

Subrecipient vs Contractor

Biennial & Program Specific Audits

Non-Federal Entity Selects Auditor

Auditee Prepares Financial Statements

7

The Super CircularBasic Structure of Audit Process

Unchanged

Audit Follow-up & Corrective Action9 Month Due DateReporting to Federal Audit

ClearinghouseMajor programs determined based on

riskCompliance Supplement overall

format 8

The Super CircularAudit Threshold

Allows Federal Agencies to Focus Audit Resolution

Depending on:

Pre-Award Review of Risks,

Standards for Program Management

Subrecipient Monitoring

Remedies for Noncompliance 9

The Super CircularAudit Threshold

Increases Audit Threshold from

$500,000 to $750,000

Depending on:

Pre-Award Review of Risks,

Standards for Program Management

Subrecipient Monitoring

Remedies for Noncompliance 10

The Super CircularMajor Program Determination

Focuses Audits on the areas with internal control deficiencies that have been identified as material weaknesses

11

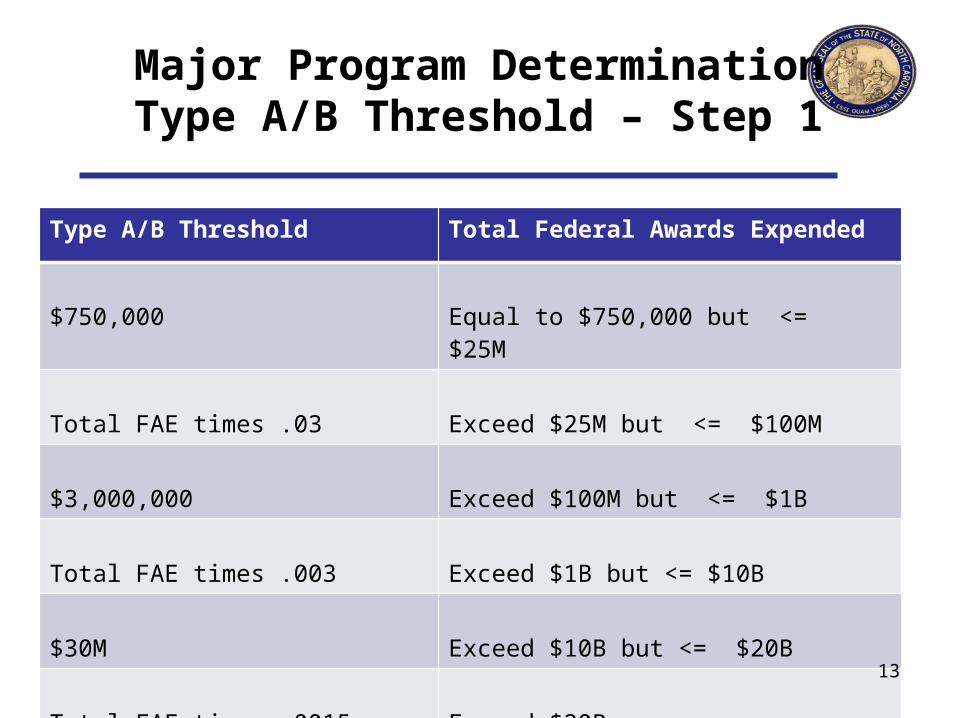

Major Program DeterminationType A/B Threshold – Step 1

Programs are grouped based on dollars

Type A programs are those at/above the threshold

Type B are those below the threshold

Type A/B threshold is sliding scaleMinimum increases from $300,000 to $750,000

12

Major Program DeterminationType A/B Threshold – Step 1

Type A/B Threshold Total Federal Awards Expended

$750,000 Equal to $750,000 but <= $25M

Total FAE times .03 Exceed $25M but <= $100M

$3,000,000 Exceed $100M but <= $1B

Total FAE times .003 Exceed $1B but <= $10B

$30M Exceed $10B but <= $20B

Total FAE times .0015 Exceed $20B13

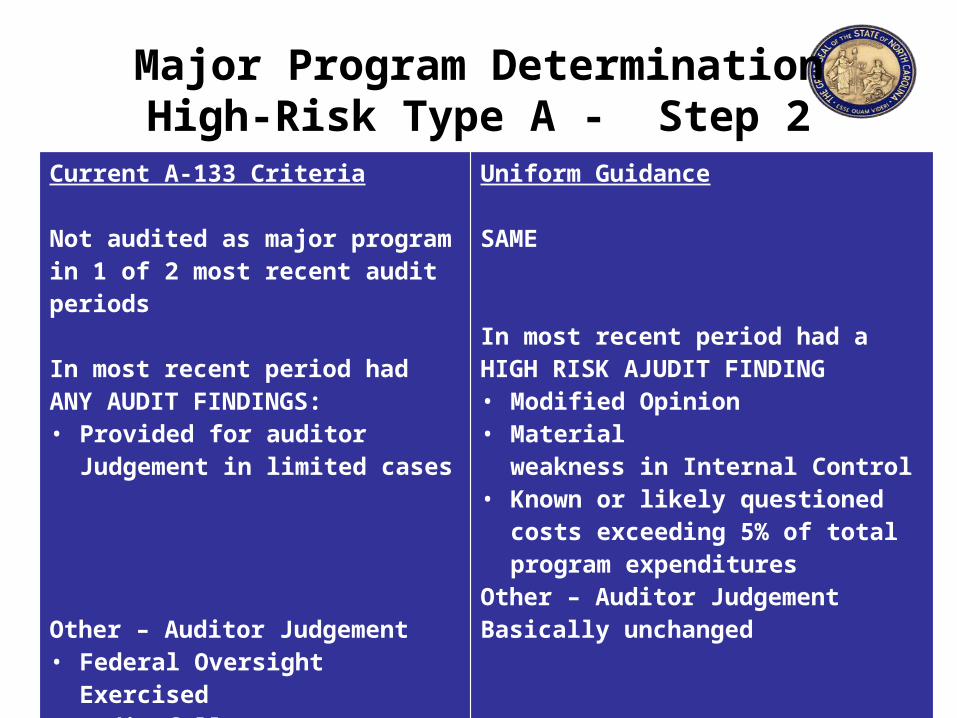

Major Program DeterminationHigh-Risk Type A - Step 2

Programs are grouped based on dollars

Type A programs are those above the threshold

Type B are those below the threshold

Type A/B threshold is sliding scaleMinimum increases from $300,000 to $750,000

14

Current A-133 Criteria

Not audited as major program in 1 of 2 most recent audit periods

In most recent period had ANY AUDIT FINDINGS:• Provided for auditor Judgement

in limited cases

Other – Auditor Judgement• Federal Oversight Exercised• Audit follow-up• Personnel changes which

increased risk

Uniform Guidance

SAME

In most recent period had a HIGH RISK AJUDIT FINDING• Modified Opinion• Material

weakness in Internal Control• Known or likely questioned costs

exceeding 5% of total program expenditures

Other – Auditor Judgement Basically unchanged

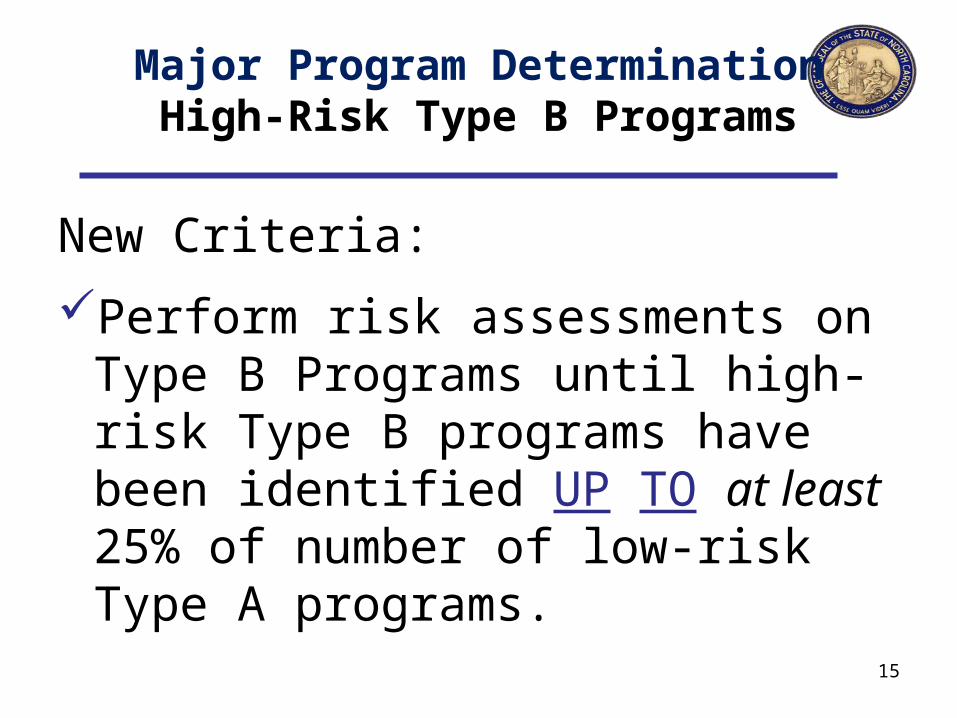

Major Program DeterminationHigh-Risk Type B Programs

New Criteria:

Perform risk assessments on Type B Programs until high-risk Type B programs have been identified UP TO at least 25% of number of low-risk Type A programs.

15

Major Program DeterminationPercentage of Coverage Rule

16

Type of Auditee Current New

Not low-risk 50% 40%

Low-risk 25% 20%

The Super CircularLow-Risk Auditee

17

Current (2 prior years) New (2 prior years)

• Annual Single Audits• Unmodified opinion on financial

statements in accordance with GAAP

• Unmodified SEFA in relation to opinion

• No GAGAS material weaknesses• In either of proceeding 2 years,

none of Type a Programs had: Materials Weakness Material noncompliance QC that exceed 5%• Timely filing with FAC• Auditor reporting going concern not

preclude low-risk• Waivers

SAMEUnmodified opinions on statements in accordance with GAAP or basis of accounting required by state law

SAME

SAMESAME

SAMENO Audit reporting of going concern

NO Waivers

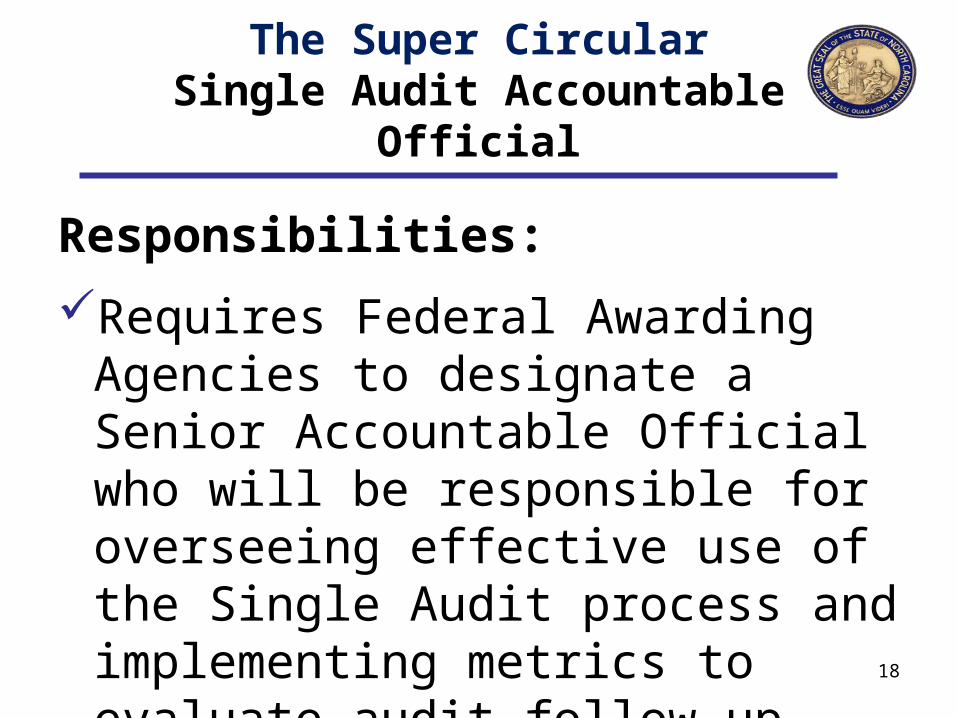

The Super CircularSingle Audit Accountable Official

Responsibilities:

Requires Federal Awarding Agencies to designate a Senior Accountable Official who will be responsible for overseeing effective use of the Single Audit process and implementing metrics to evaluate audit follow-up.

18

The Super CircularSingle Audit Accountable Official

• Ensure agency effectively uses the single audit process,

• Develop a baseline, metrics, and targets to track, over time, the effectiveness of:– Agency’s process to follow up on audit findings

• Single audits in:– Improving non-Federal entity accountability for

Federal Awards– Use by the agency in making award decisions

• Designate the agency’s Key Management Single Audit Liaison 19

The Super CircularAudit Findings

• Increases the Threshold for reporting known/likely questioned costs from $10,000 to $25,000

• Requires Questioned Costs by Identified by CFDA number and applicable award

• Requires Identification of Findings as repeat from the immediately prior audit and the finding number from prior audit

• Prescribes audit finding numbers in the format prescribed by data collection form 20

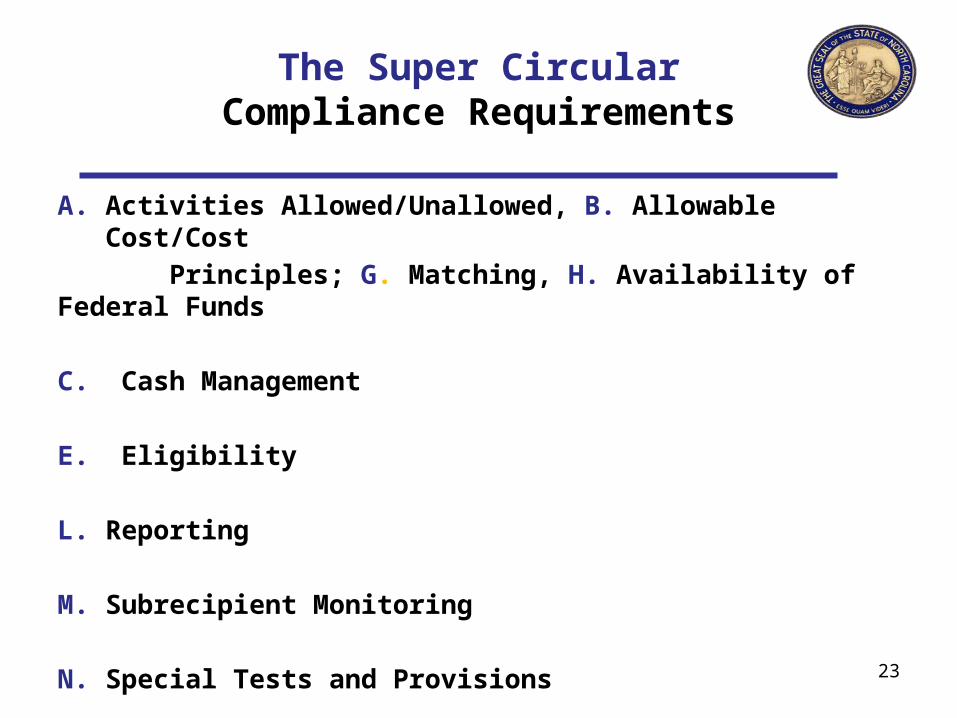

State Auditor’s UpdateAffects of Super Circular

On the Horizon:Going From 14 Compliance Requirements to

6 Compliance Requirements

21

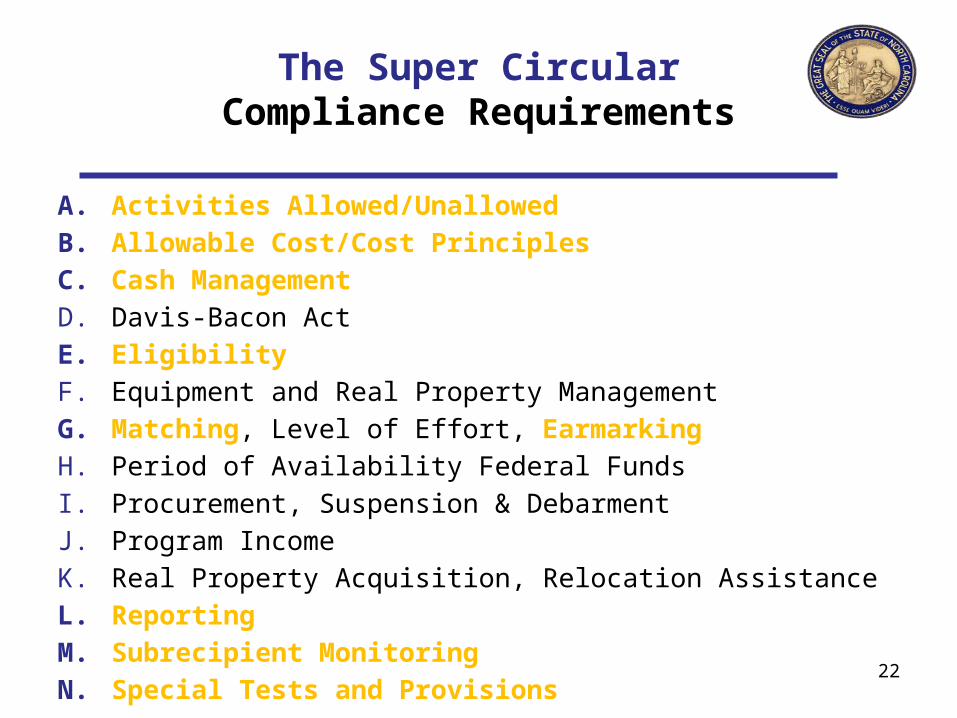

The Super CircularCompliance Requirements

A. Activities Allowed/Unallowed

B. Allowable Cost/Cost Principles

C. Cash Management

D. Davis-Bacon Act

E. Eligibility

F. Equipment and Real Property Management

G. Matching, Level of Effort, Earmarking

H. Period of Availability Federal Funds

I. Procurement, Suspension & Debarment

J. Program Income

K. Real Property Acquisition, Relocation Assistance

L. Reporting

M. Subrecipient Monitoring

N. Special Tests and Provisions22

The Super CircularCompliance Requirements

A. Activities Allowed/Unallowed, B. Allowable Cost/Cost

Principles; G. Matching, H. Availability of Federal Funds

C. Cash Management

E. Eligibility

L. Reporting

M. Subrecipient Monitoring

N. Special Tests and Provisions

23

The Super CircularNASACT Middle Management Conference

Questions?

24

Related Documents