The State of FinTech in Australia Plus what’s in store for 2017 - 2018

The State of FinTech in Australiam - Danielle Szetho

Jan 21, 2018

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

The State of FinTech in Australia

Plus what’s in store for 2017 - 2018

About FinTech Australia - our Fintech Industry Association

FinTech Australia is all about our

Fintech Startup Community -

Fintech Startups, Hubs,

Accelerators and VCs.

We are a national, independent,

not-for-profit organisation, run for

the benefit of our members across

all corners of Australia.

Our vision is ambitious!

To make Australia one of the world’s leading markets

for Fintech Innovation and Investment

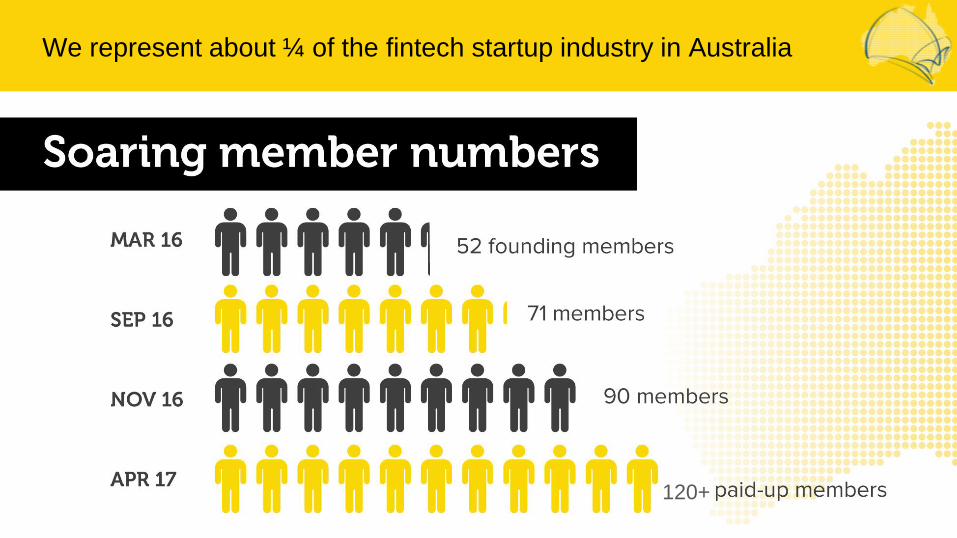

We represent about ¼ of the fintech startup industry in Australia

120+

We work across the Government and Regulatory community

Treasurer’s FinTech

Advisory Group

Open Financial Data

Policy

Transparent Business

Lending Practices

GST Treatment of Digital

Currencies

Equity Crowdfunding

Australian Payments

Council

New Payments Platform

Rollout

Open Data / Digital ID

Hackathons

Digital Australian Dollar

Interchange Fee

Regulation

Deregulation / Digital Bank

Licensing Consultation

Capital requirements for

Deposit-taking Institutions

Default Insurance settings

Default Pension Fund

settings

Digital Finance

Advisory Committee

ASIC Innovation Hub and

Regulatory Sandbox

Digital Advice Guidelines

and Standards

Open Financial Data

Access and Accreditation

P2P Regulation

RegTech and Reporting

AUSTRAC Fintel

Strategic Alliance

AUSTRAC Innovation Hub

and Regulatory Sandbox

Treatment of Digital

Currencies for AML/CTF

RegTech and Reporting

Australia’s case to be a

pretty hot fintech hub

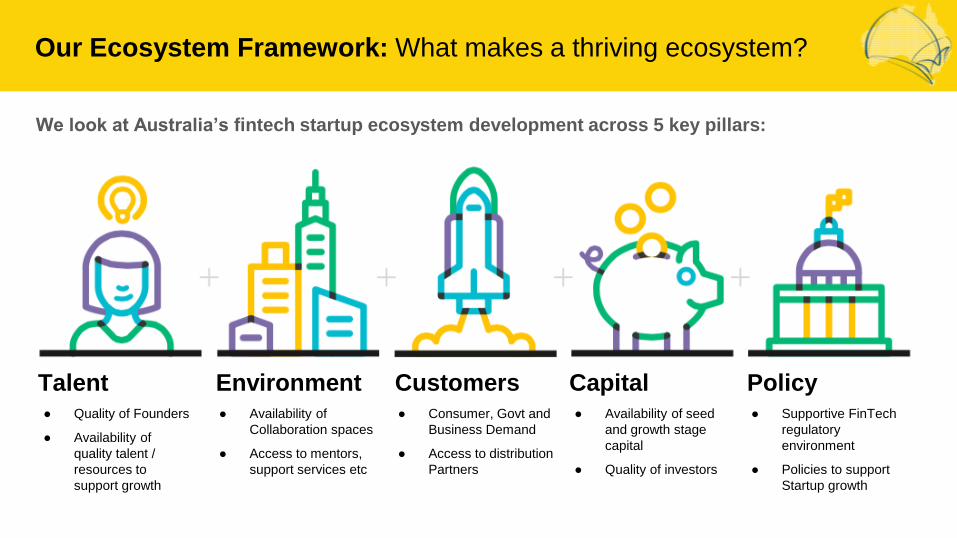

Our Ecosystem Framework: What makes a thriving ecosystem?

We look at Australia’s fintech startup ecosystem development across 5 key pillars:

Talent Environment Customers Capital Policy ● Quality of Founders

● Availability of

quality talent /

resources to

support growth

● Availability of

Collaboration spaces

● Access to mentors,

support services etc

● Consumer, Govt and

Business Demand

● Access to distribution

Partners

● Availability of seed

and growth stage

capital

● Quality of investors

● Supportive FinTech

regulatory

environment

● Policies to support

Startup growth

Substantial progress for Australian fintech policy development

Through 17 submissions to Government and

Regulators, we’ve made fintech policy headway:

● ASIC’s Regulatory Sandbox - test new

products for unlimited wholesale or up to 100

retail customers, without an AFSL/ACL

● Removed GST from the purchase of Digital

Currencies, recognising them under our tax

laws (and soon under our AML/CTF regime)

● Launch of Australia’s Equity Crowdfunding

Regime – initially for non-listed Public

companies

The recent Federal Budget also had more fintech wins

● Commitment to implement an Open Banking

Regime in 2018, and an inquiry in 2017 to

help guide implementation

● Consultation on formal response to

Productivity Commission inquiry on Data

Availability and Use more broadly

● Proposal to expand Equity Crowdfunding to

include Private companies

● Proposal for “Enhanced Regulatory Sandbox”

allowing a wider range of participants and

products to be tested for longer

● Reduced barriers for Challenger Banks to

obtain Bank licenses

Positioning Australia as:

The launchpad or gateway

between the East and West

Highly tech-savvy customer

base – the perfect test market

A Blockchain / DLT world

leader (breadth AND depth)

Gold standard regulations, but

still a progressive regulator

Exceptional quality talent; still

relatively low valuations

Challenges to overcome: The Bank/FinTech collaboration challenge

Impediments to Collaboration:

● Anecdotal average of 6-9 months from initial

meeting to Pilot (vs 2-3 months in Asia)

● Driven by over-zealous risk and security teams

forcing IBM-level compliance checks onto

innovative startups

● No commercial incentive to innovate from the

outside (i.e. do it ourselves mentality, even if it

costs more)

● Suspicion over Data sharing and leakage (but

Open Financial Data regime will overcome this)

Contact FinTech Australia

Danielle Szetho

CEO

http://fintechaustralia.org.au

@ausfintech

FinTech Australia on LinkedIn

Thank you

Related Documents