THE ROLE OF ISLAMIC BANKING OPERATIONS ON FINANCING AND DEVELOPMENT OF SMALL ENTERPRISES IN LIBYA IBRAHIM KHALIFA MOHAMED ELGHWAIL Master in Islamic Banking and Finance Faculty of Finance & Admin. Science Al-Madinah International University 2016/1436H

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

THE ROLE OF ISLAMIC BANKING OPERATIONS ON

FINANCING AND DEVELOPMENT OF SMALL

ENTERPRISES IN LIBYA

IBRAHIM KHALIFA MOHAMED ELGHWAIL

Master in Islamic Banking and Finance

Faculty of Finance & Admin. Science

Al-Madinah International University

2016/1436H

i

1. TITLE PAGE

THE ROLE OF ISLAMIC BANKING

OPERATIONS ON FINANCING AND

DEVELOPMENT OF SMALL

ENTERPRISES IN LIBYA

IBRAHIM KHALIFA MOHAMED ELGHWAIL

MIB153BL374

Thesis submitted in fulfillment

of the requirements for the degree of Master in Islamic Banking and Finance)

Faculty of Finance & Admin. Science

Supervised by:

Prof. Dr. Sadun Naser Yassin Alheety

December 2016/ Rabie’ awal 1438

ii

CERTIFICATION OF DISSERTATION WORK PAGE

The thesis of student named: IBRAHIM KHALIFA MOHAMED ELGHWAIL

Under the title The Role of Islamic banking operations on Financing and

Development of Small Enterprises in Libya

Has been approved by the following:

SupervisorAcademic

……………………….. Name

……………………….. Signature

Supervisor of amendments

……………………….. Name

……………………….. Signature

Head of Department

……………………….. Name

……………………….. Signature

Dean, of the Faculty

……………………….. Name

……………………….. Signature

Deanship of Postgraduate Studies

……………………….. Name

……………………….. Signature

iii

DECLARATION

I declare that the work in this thesis is my original work; it has not submitted previously

or concurrently for any degree or qualification at any other institutions,And I hereby

confirm that there is no plagiarism or data falsification/ fabrication in the thesis, and

scholary integrity is upheld as according to the Alamdinah International University

(MEDIU).

Name: ………………………….

Signature: ………………………..

Date: ……………………………

iv

COPYRIGHT

Al-MADINAH INTERNATIONAL UNIVERSITY

DECLARATION OF COPYRIGHT AND AFFIRMATION

OF FAIR USE OF UNPUBLISHED RESEARCH

Copyright © 2016 by [IBRAHIM KHALIFA MOHAMED ELGHWAIL], All

rights reserved.

[THE ROLE OF ISLAMIC BANKING OPERATIONS ON FINANCING AND

DEVELOPMENT OF SMALL ENTERPRISES IN LIBYA (MEDIU)]

No part of this unpublished research may be reproduced, stored in a retrieval system,

Or transmitted, in any form or by any means, electronic, mechanical, photocopying,

recording or otherwise without the prior written permission of the copyright holder

except as provided below.

1. Any material contained in or derived from this unpublished research may only be

used by others in their writing with due acknowledgement.

2. MEDIU will have the right to make, store in a retrieval system and supply copies of

this unpublished research if requested by other Universities and research libraries

for instructional and academic purposes.

Name: ………………………...

Signature ……………………..

Date: ………………………….

v

ABSTRACT

This research highlights the possibility of Islamic banking operations in financing and

developing small and medium enterprises in Libya. The aim of this study is to identify

the relationship between Islamic banking operations of Mudarabah, Murabaha and

Musharkah, and financing and developing small and medium enterprises. The approach

taken in this study is analytical and inductive while the tool used is the questionnaire.

This study has shown that the relationship between Islamic banking operations

(Mudarabah, Murabaha, Musharkah) and financing and developing small and medium

enterprises is positive. Also, one of the key obstacles is the difficulty of how to obtain

financing.

ii

ACKNOWLEDGEMENT

Alhamdulillahi Rabbil ‘Ālamȋn,. All praise is due to Allah (swt) for giving me

wisdom, strength and determination to complete this thesis.

On this very special page of this thesis, I would like to acknowledge the people

who have been very special in this endeavor. I extend my extreme gratitude to my

supervisors for their guidance, valuable advices, constructive comments and

suggestions.

I am also indebted to my parents who motivated me to study and for being a

source of encouragement throughout my studies. I would also like to thank all the

faculties and administrative staff of MIU and my fellow colleagues in the Master of

Science in Islamic Banking program who contributed directly or indirectly in this

journey.

iii

TABLE OF CONTENTS

Declaration ............................................................................................................... v

Acknowledgements .................................................................................................. 1

Table of Contents ..................................................................................................... iii

List of Tables ........................................................................................................... vii

List of Figures .......................................................................................................... viii

Chapter One: Introduction .................................................................................. 1

1.1 Introduction............................................................................................. 1

1.2 Background To The Study ...................................................................... 4

1.3 Problem Statement .................................................................................. 6

1.4 Research Questions ................................................................................. 7

1.5 Research Objectives................................................................................ 7

1.6 Significance Of The Research ................................................................ 7

1.7 Definition Of Key Terms ........................................................................ 8

1.8 Structure Of The Chapters ...................................................................... 9

Chapter Two: Literature Review ........................................................................ 11

2.1 Introduction............................................................................................. 11

2.2 Criteria For Definition Of Smes ............................................................. 15

2.2.1 Quantitative Criteria ...................................................................... 15

2.2.2 Qualitative Criteria ........................................................................ 17

2.3 Definition Of Sme’s ................................................................................ 18

2.4 Constraints Faced By Smes In Libya...................................................... 18

2.4.1 Riba ............................................................................................... 20

2.4.2 Profit-And-Misfortune Sharing (Pls) ............................................ 21

2.4.3 Halal .............................................................................................. 22

2.4.4 Maysir And Gharar ....................................................................... 23

2.4.5 Zakat.............................................................................................. 23

2.4.6 Sharia Board .................................................................................. 24

2.5 The Differences Between Islamic And Conventional Banking .............. 24

2.6 Role Of Islamic Banking In The Economy ............................................ 26

2.6.1 Effects On Savings And Investment ............................................. 26

iv

2.6.2 Impact On The Rate And Pattern Of Growth ............................... 27

2.6.3 Impact On Allocative Efficiency .................................................. 27

2.6.4 Consequences For The Stability Of The Banking System ............ 28

2.7 Swot: Islamic Banking ............................................................................ 28

2.7.1 Strengths........................................................................................ 28

2.7.2 Weaknesses ................................................................................... 29

2.7.3 Opportunities ................................................................................. 30

2.7.4 Threats ........................................................................................... 31

2.8 Competitive Advantage Of Islamic Banking .......................................... 33

2.9 Competition In Islamic Banking Perspective ......................................... 36

2.10 Islamic Finance ..................................................................................... 43

2.11 Efficiency of Islamic Finance for Sme's ............................................... 46

2.12 Venture Capital And Islamic Finance for SME's ................................. 48

2.13 Prohibition of Interest and Profitability in Islamic Banks .................... 51

2.14 Islamic Finance Forms .......................................................................... 52

2.14.1 Musharaka (Diminishing Partnership) ........................................ 53

2.14.1.1 Practical steps for Musharaka: ........................................ 56

2.14.1.2 Few Concepts Related to Musharakah Muntahiyah ....... 57

2.14.1.3 Modern Musharakah Practices ....................................... 58

2.14.1.4 Stages in the implementation of Musharakah Mutanaqisah

...................................................................................................... 61

2.14.2 Mudaraba .................................................................................... 68

2.14.2.1 Categories of Mudaraba: ................................................ 68

2.14.3 Murabaha .................................................................................... 69

2.14.4 Istisna'a ........................................................................................ 70

2.14.4.1 Categories of istisna'a (Mumani, 2014) .......................... 71

2.14.5 Closed-End Leasing .................................................................... 72

2.15 SUMMARY .......................................................................................... 73

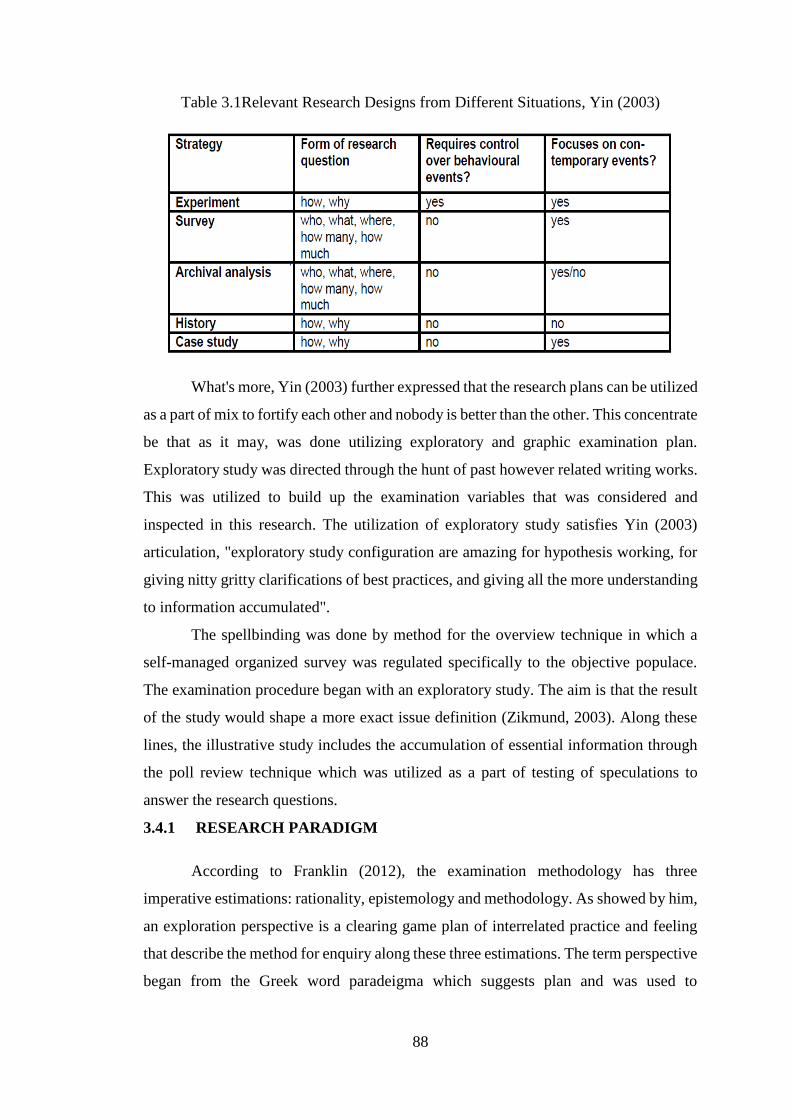

CHAPTER THREE ................................................................................................. 85

RESEARCH METHODOLOGY ............................................................................ 85

3.1 Introduction............................................................................................. 85

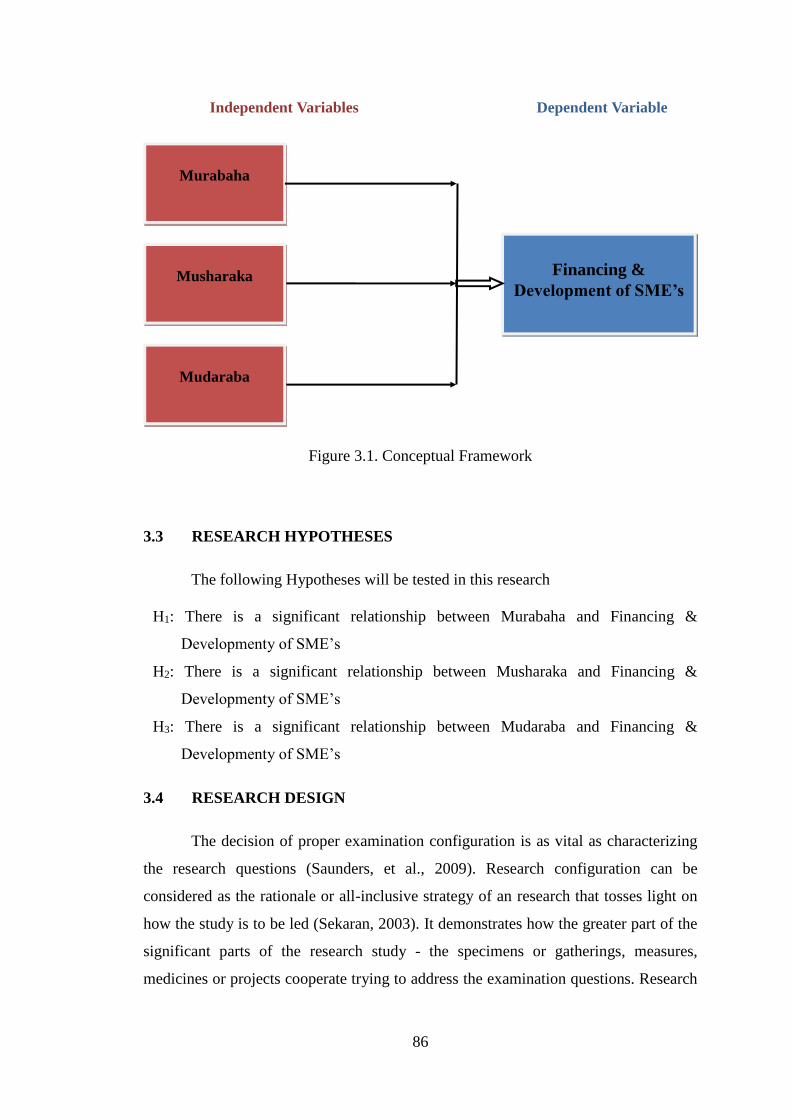

3.2 Conceptual Framework ........................................................................... 85

3.3 Research Hypotheses .............................................................................. 86

v

3.4 Research Design ..................................................................................... 86

3.5 Research Paradigm ................................................................................. 88

3.6 Research Approach ................................................................................. 91

3.7 Research Strategy ................................................................................... 92

3.8 Time Horizon .......................................................................................... 93

3.9 Data Collection Methods ........................................................................ 94

3.9.1 Primary Data Collection................................................................ 94

3.9.2 Secondary Data Collection............................................................ 95

3.10 Research Population, Sample Size And Sampling ............................... 96

3.11 Research Instrument ............................................................................. 98

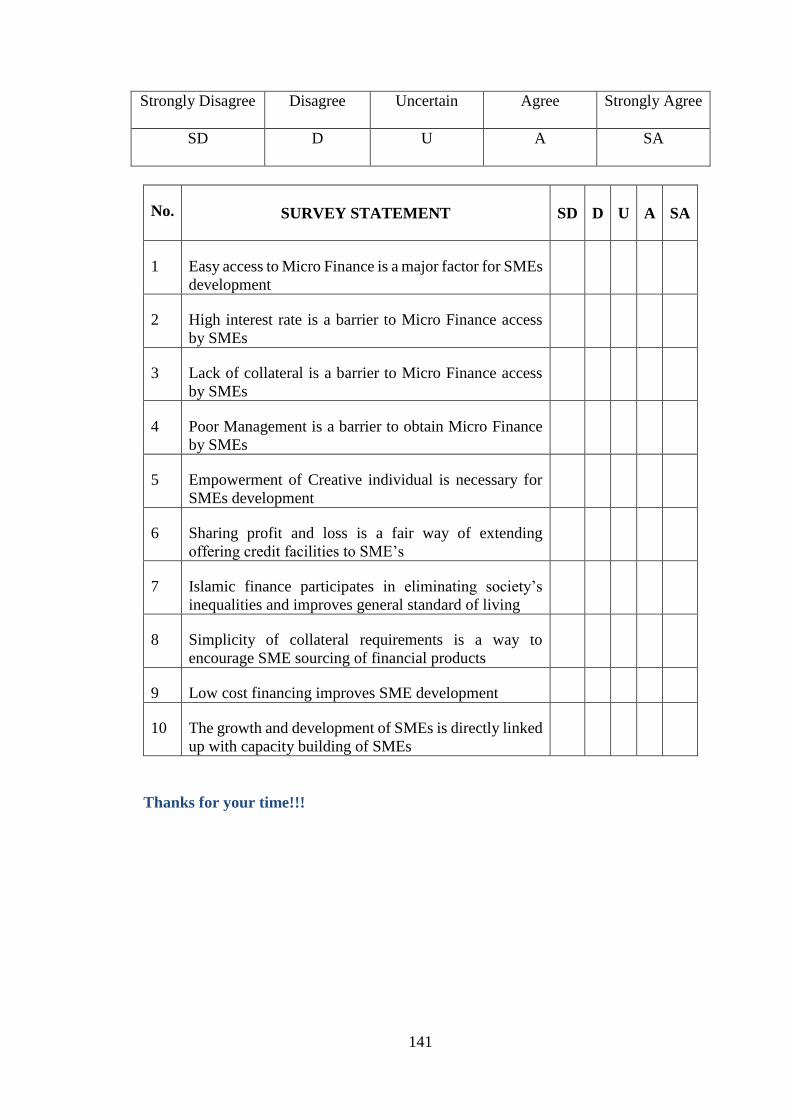

3.12 Questionnaire Design............................................................................ 98

3.13 Ethnical Considerations ........................................................................ 98

3.14 Data Analysis ........................................................................................ 99

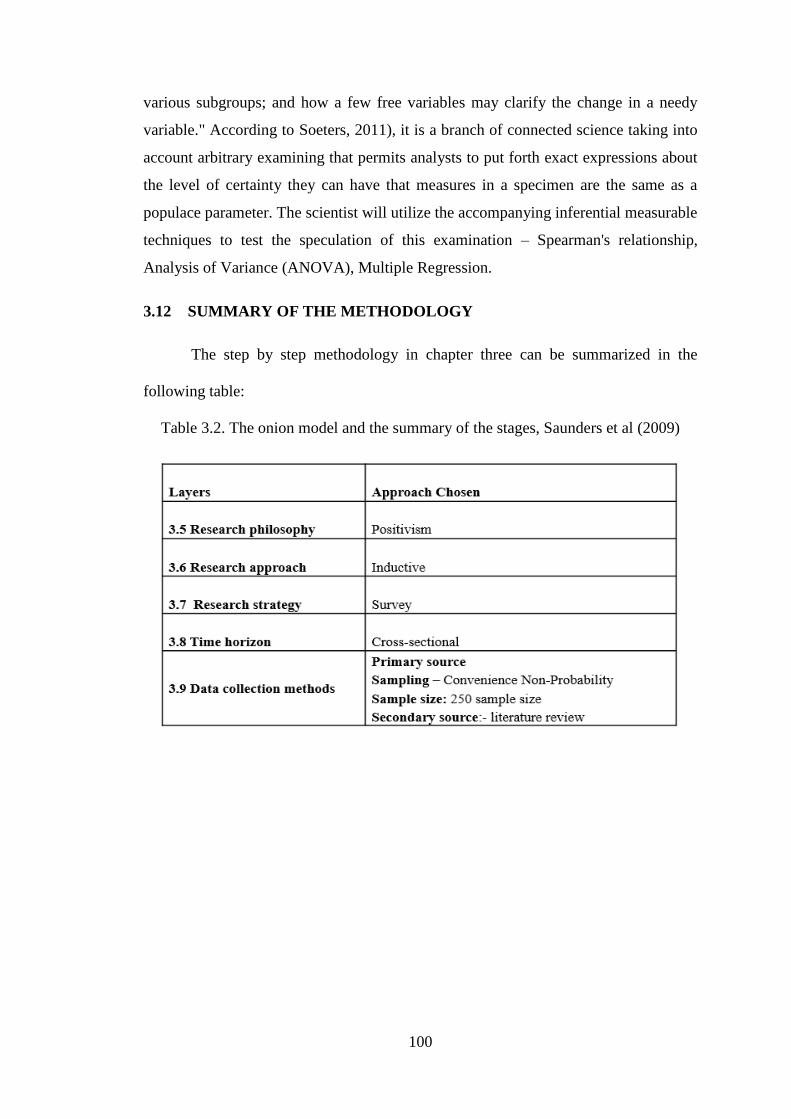

3.15 Summary of the Methodology .............................................................. 100

CHAPTER FOUR: DATA ANALYSIS AND RESULTS ................................. 101

4.1 Introduction............................................................................................. 101

4.2 Descriptive Statistics .............................................................................. 102

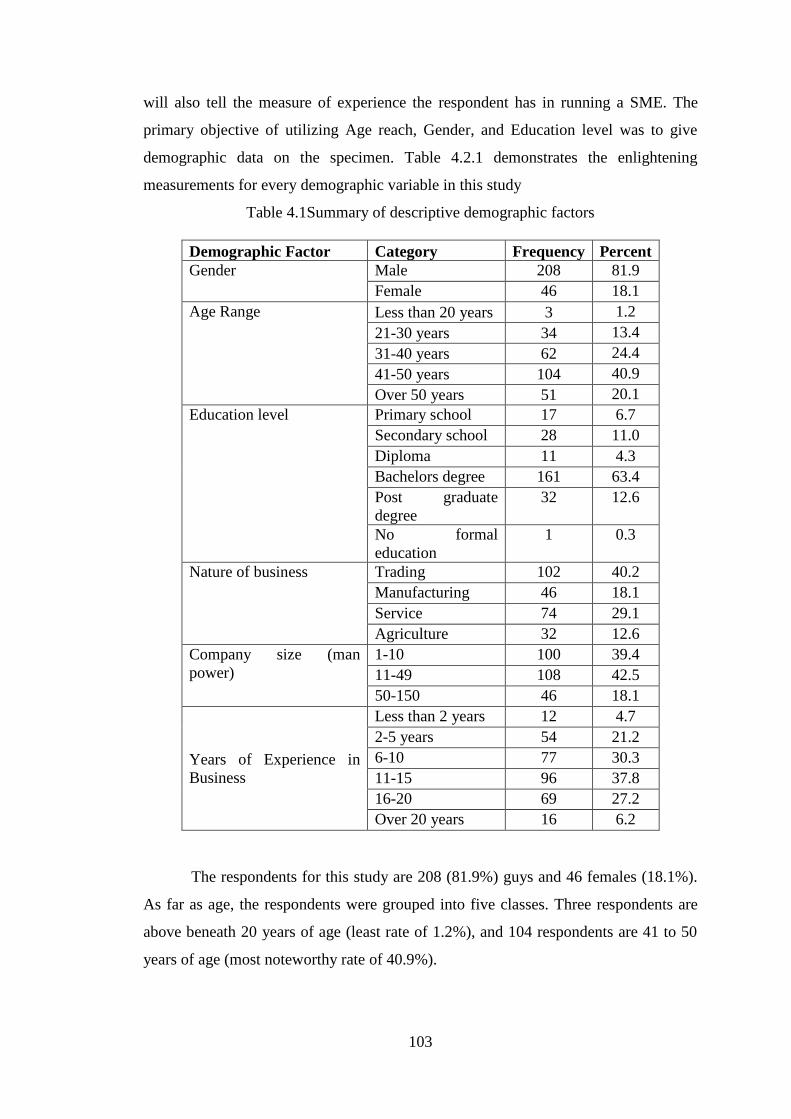

4.2.1 Demographic Information of the Sample ...................................... 102

4.2.2 Results: Descriptive Analysis of Research Constructs ................. 104

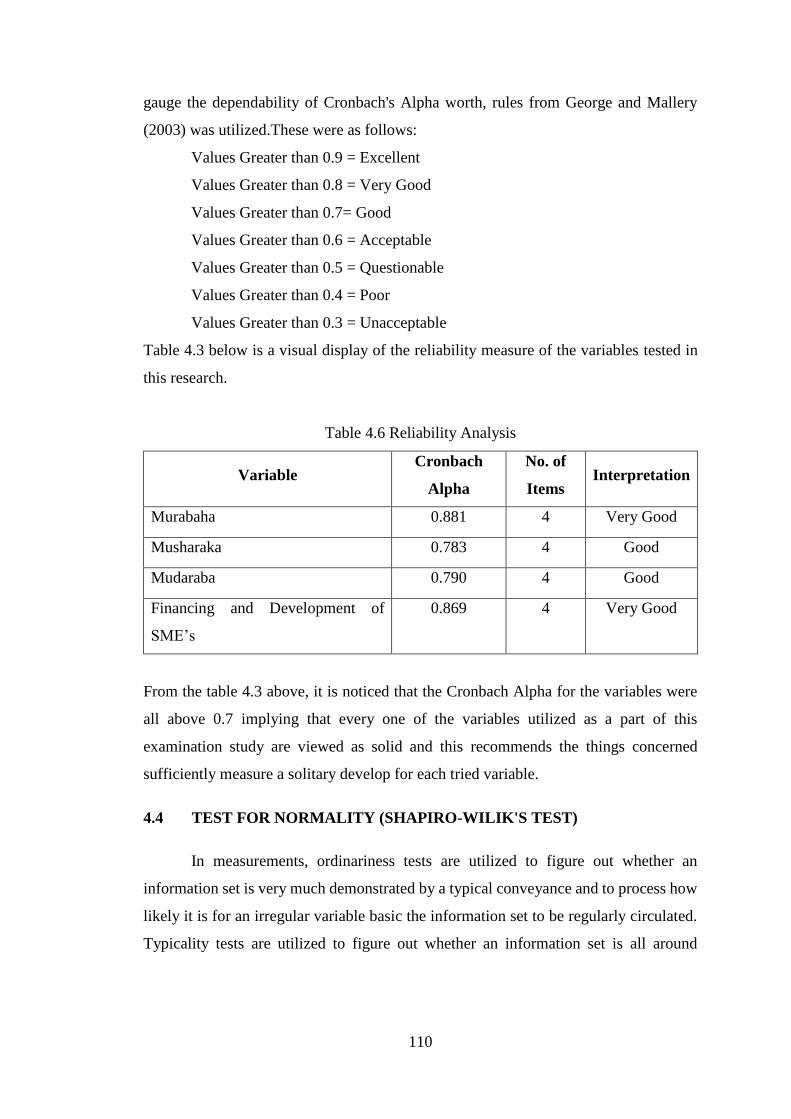

4.3 Reliability Analysis ................................................................................ 108

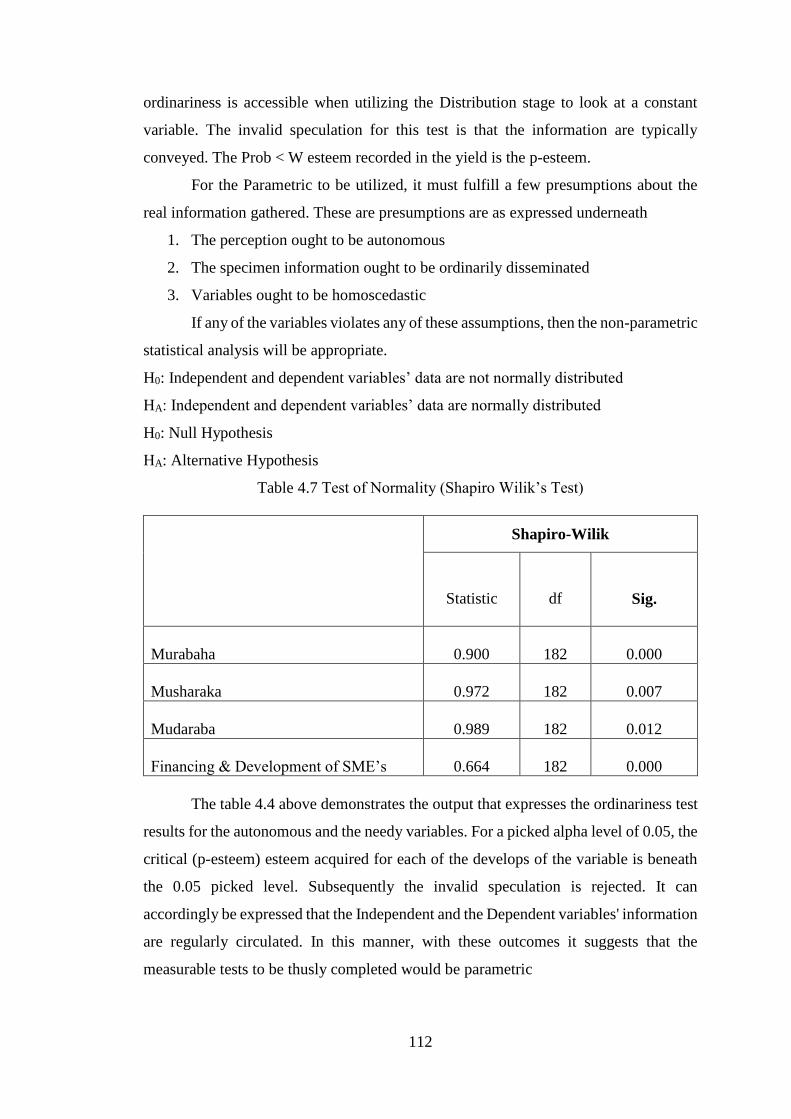

4.4 Test for Normality (Shapiro-Wilik's Test) .............................................. 110

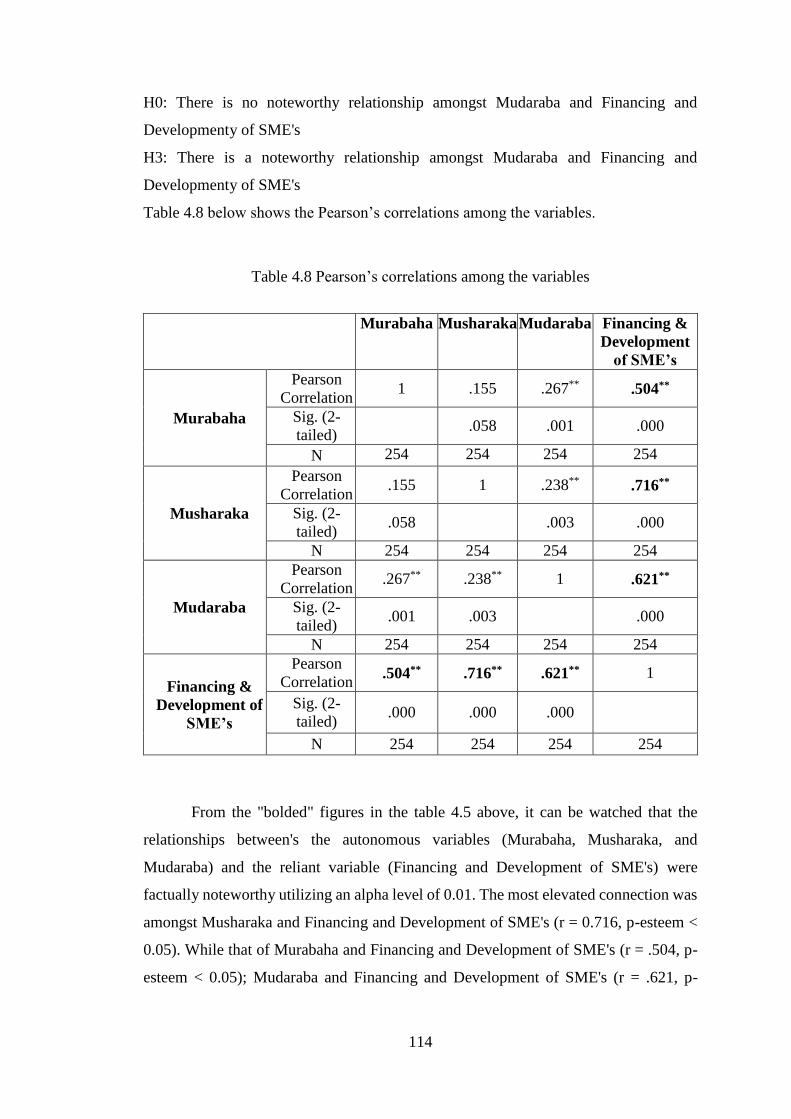

4.5 Bivariate Correlation Analysis Of Research Variables .......................... 113

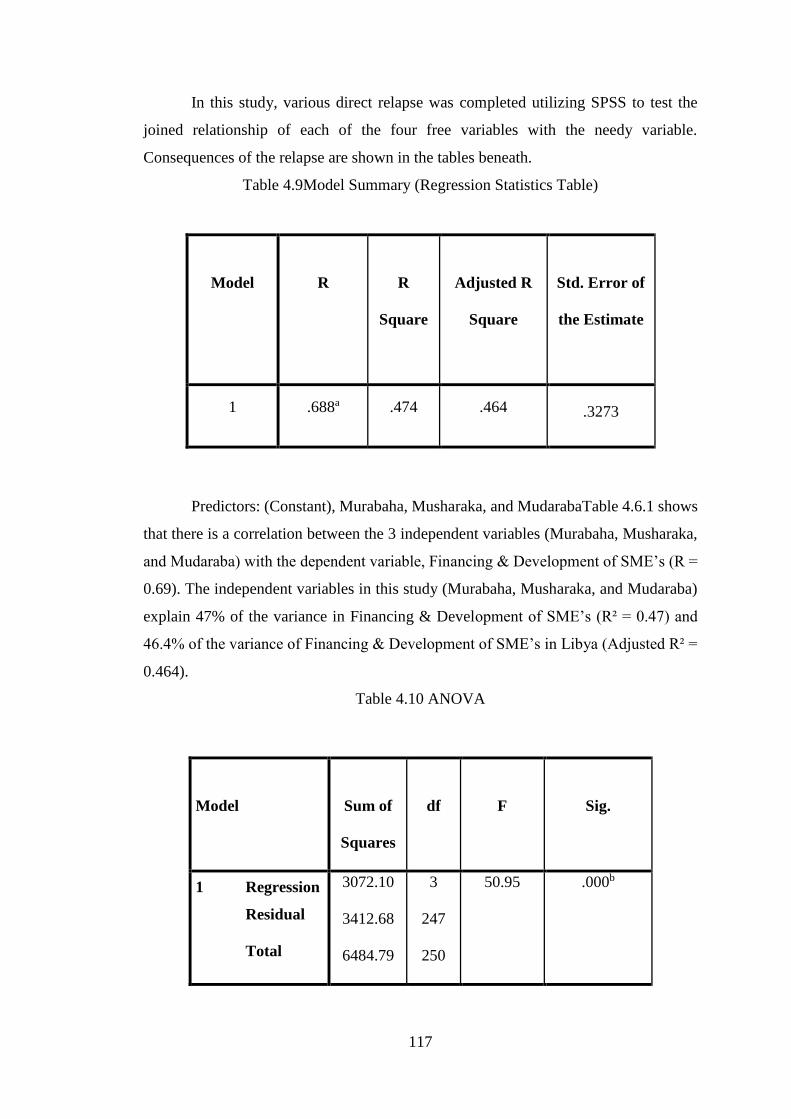

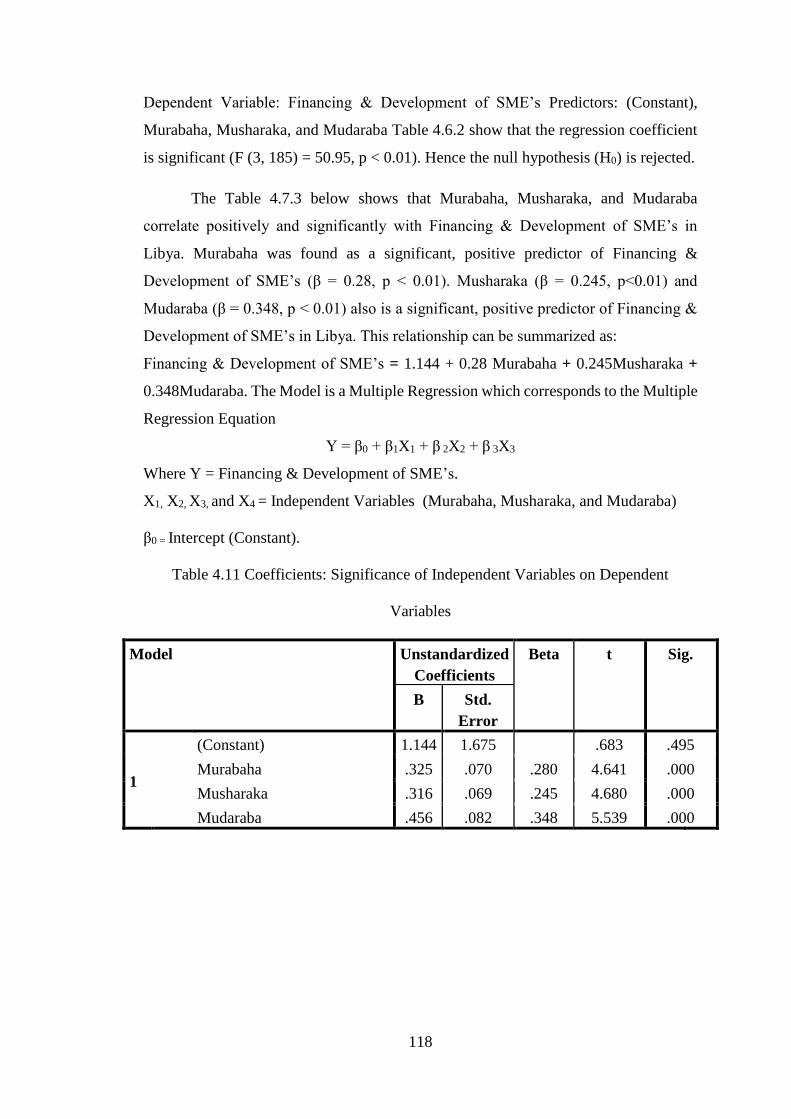

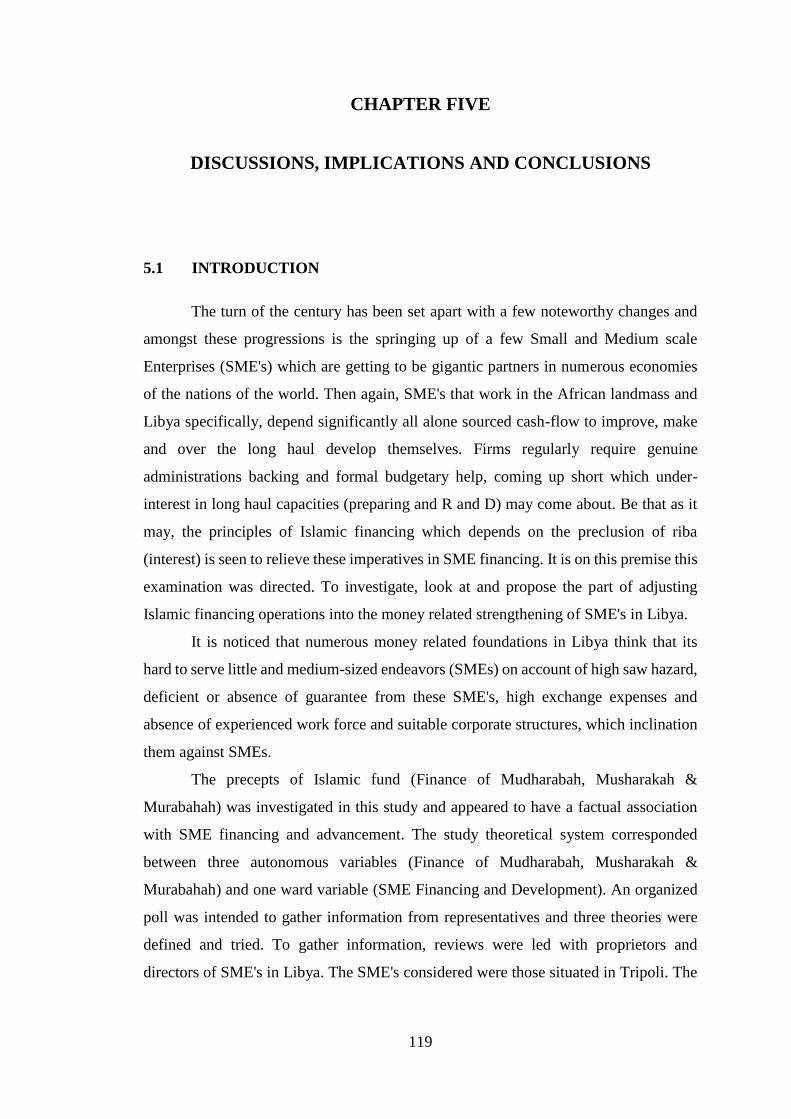

4.6 Multiple Regression Analysis ................................................................. 115

CHAPTER FIVE: DISCUSSIONS, IMPLICATIONS AND

CONCLUSIONS .................................................................................................... 119

5.1 Introduction............................................................................................. 119

5.2 Summary of the Findings ....................................................................... 121

5.2.2 Objective 1: To look at the relationship amongst Murabaha and

Financing and Development of SME's ......................................... 122

5.2.3 Objective 2: To inspect the relationship amongst Musharaka

and Financing and Development of SME's .................................. 122

vi

5.2.4 Objective 2: To examine the relationship between Mudarabah

and Financing & Development of SME’s ................................... 123

5.3 Research Contributions ........................................................................... 123

5.4 Experienced Gained ................................................................................ 124

5.5 Limitations Of The Research Study ....................................................... 124

5.6 Suggestions for Future research.............................................................. 125

REFERENCES ...................................................................................................... 127

APPENDIX ............................................................................................................ 137

vii

LIST OF TABLES

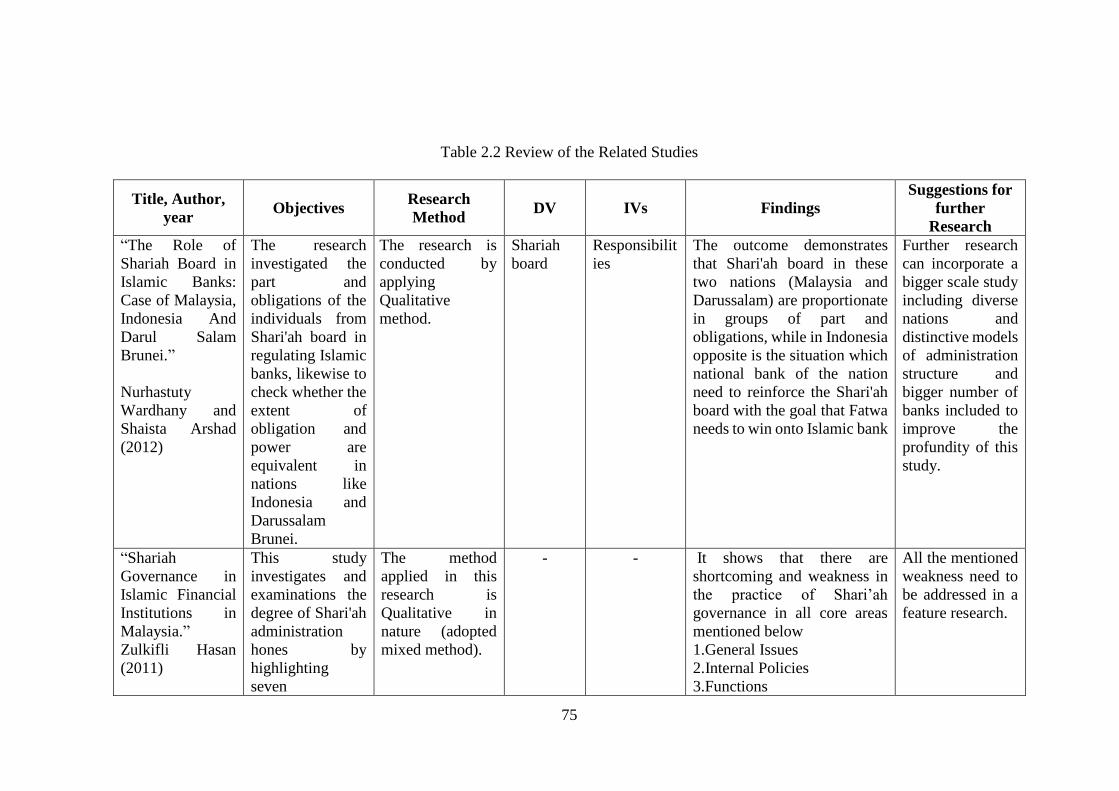

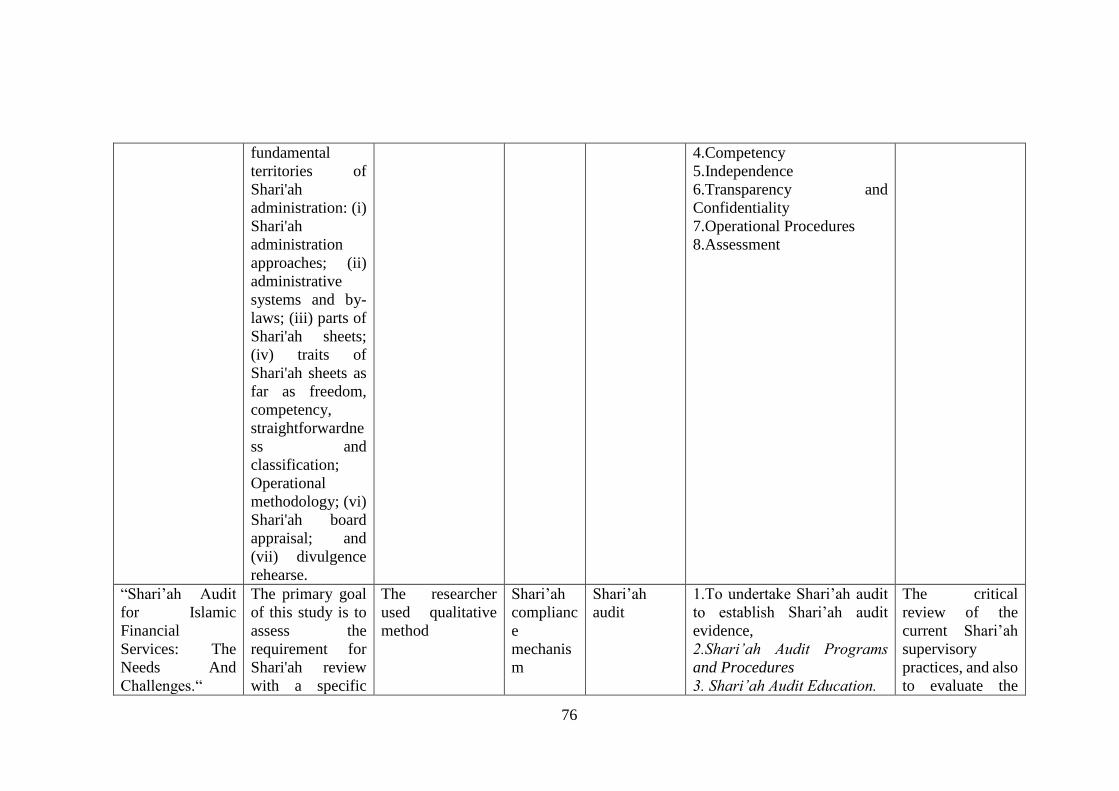

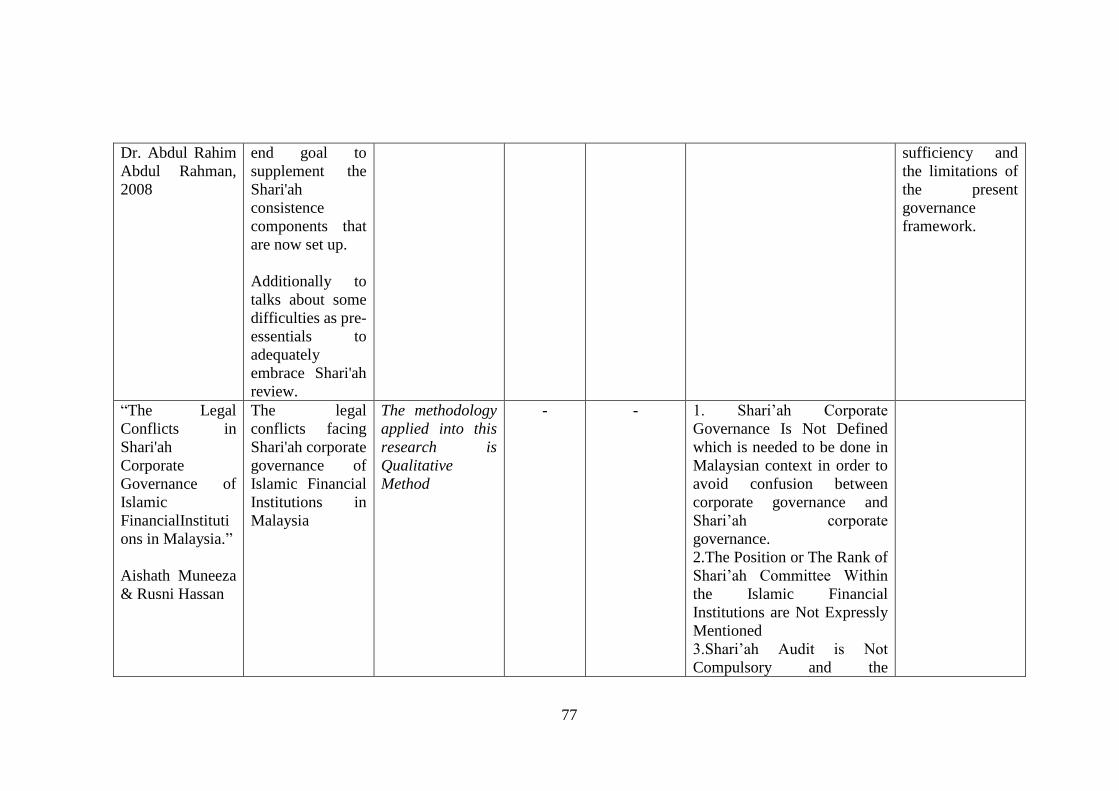

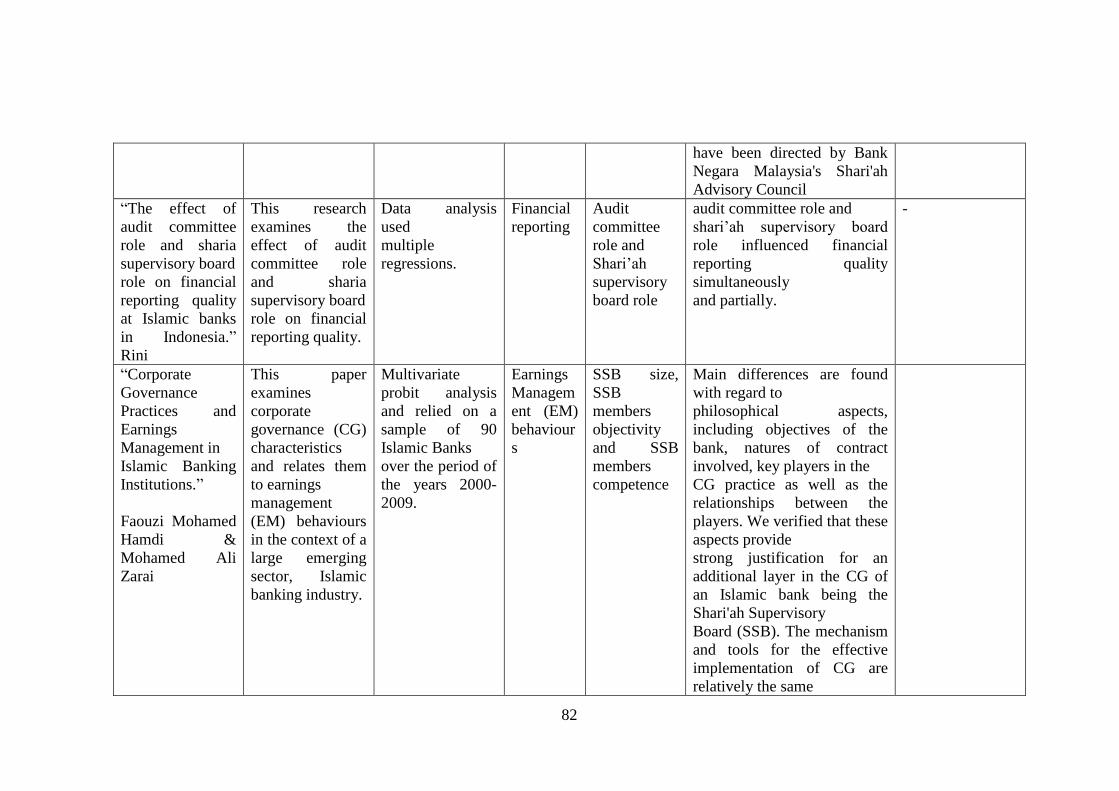

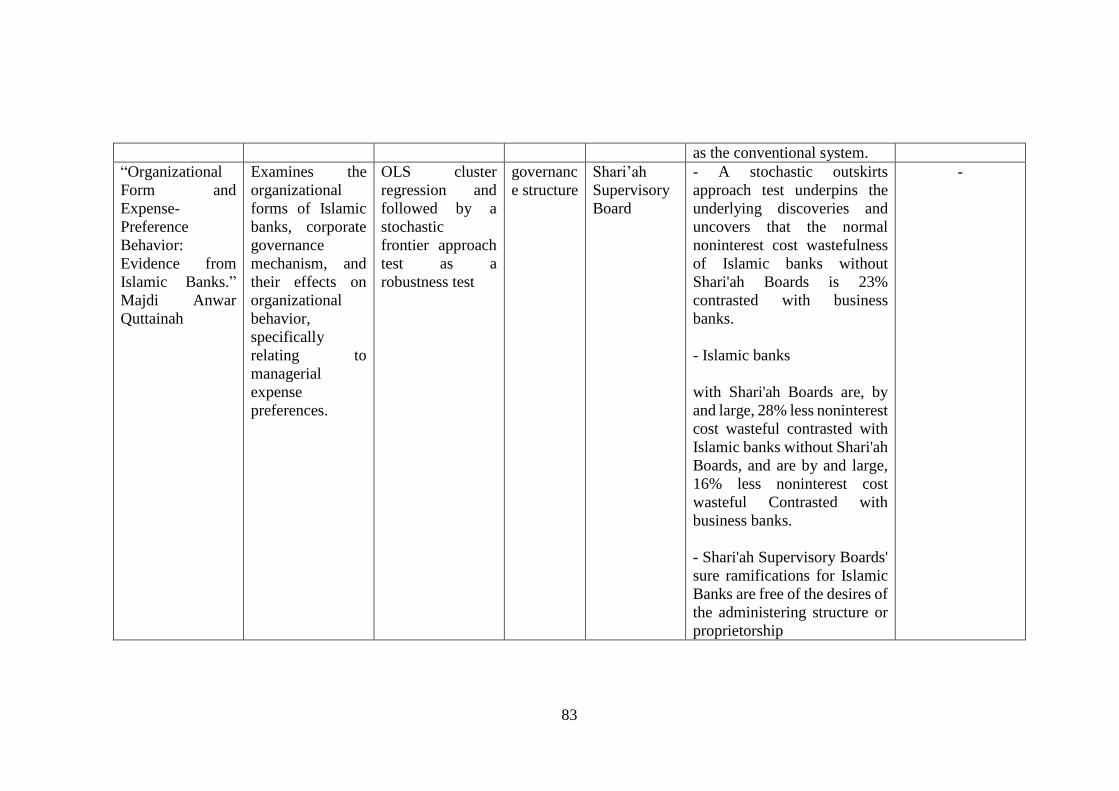

Table 2.1 Summary of the SWOT-analysis. 33 Table 2.2 Review of the Related Studies 75

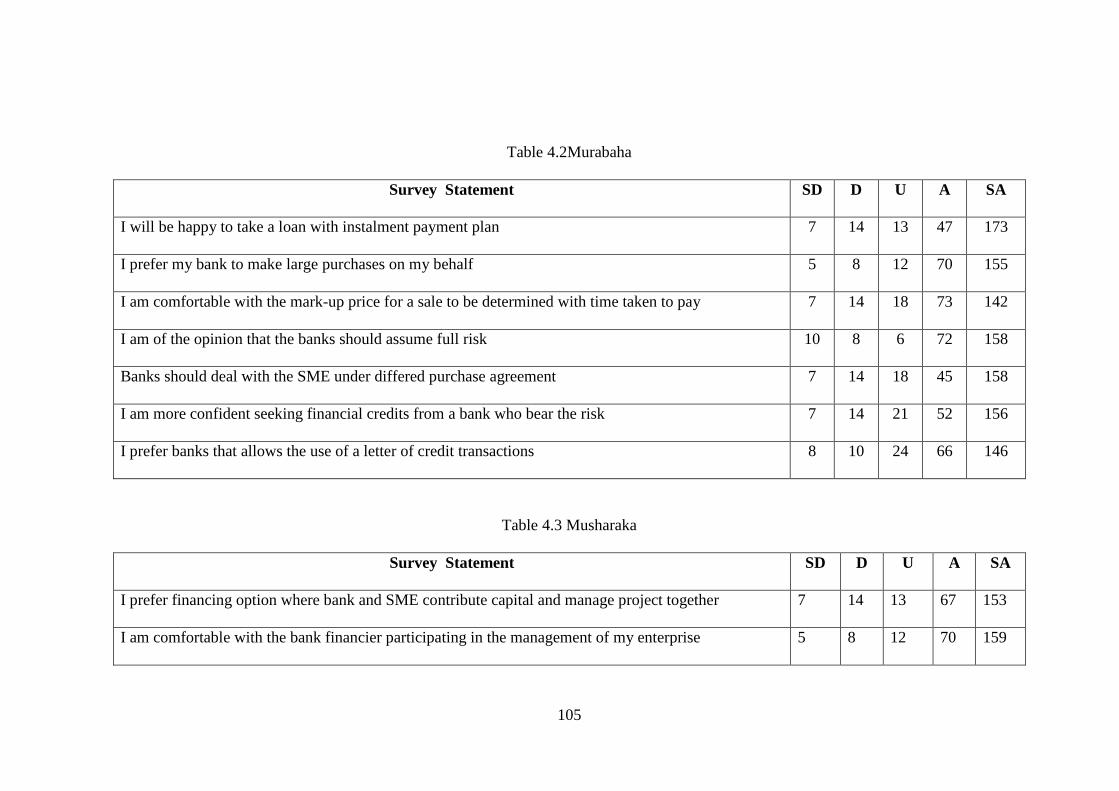

Table 3.1 Relevant Research Designs from Different Situations, Yin (2003) 88 Table 3.2. The onion model and the summary of the stages, Saunders et al (2009) 100 Table 4.1 Summary of descriptive demographic factors 103 Table 4.2 Murabaha 105 Table 4.3 Musharaka 105

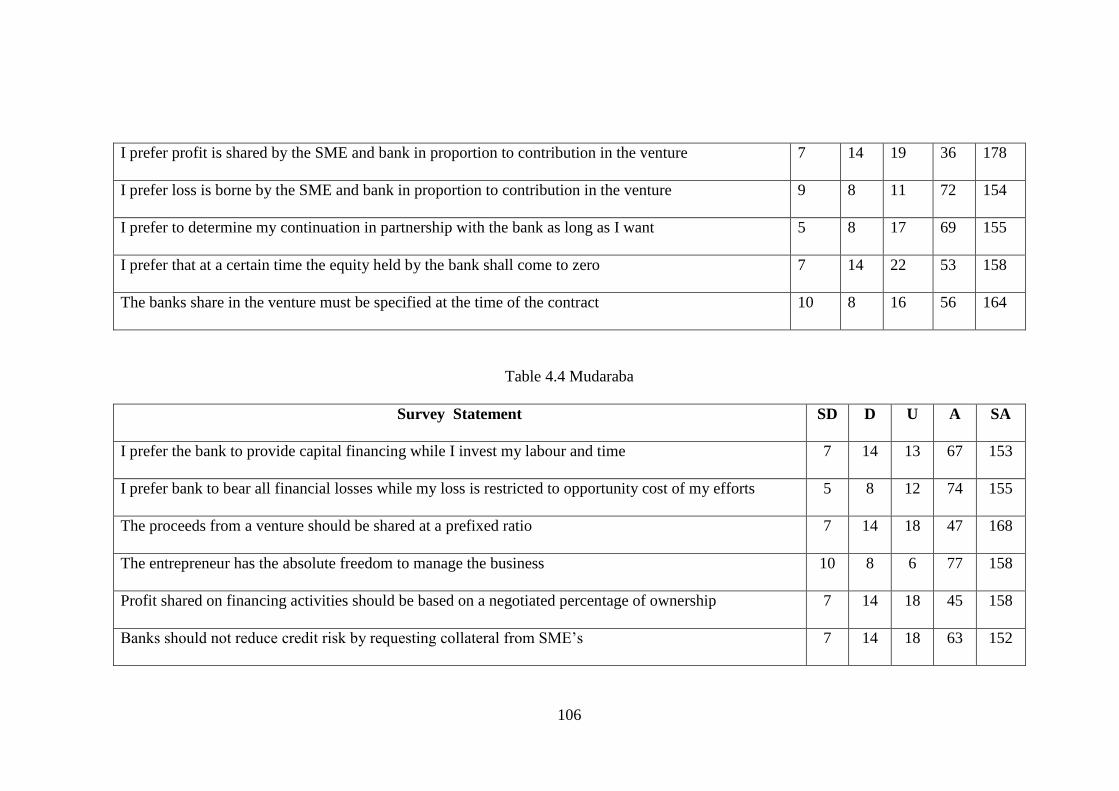

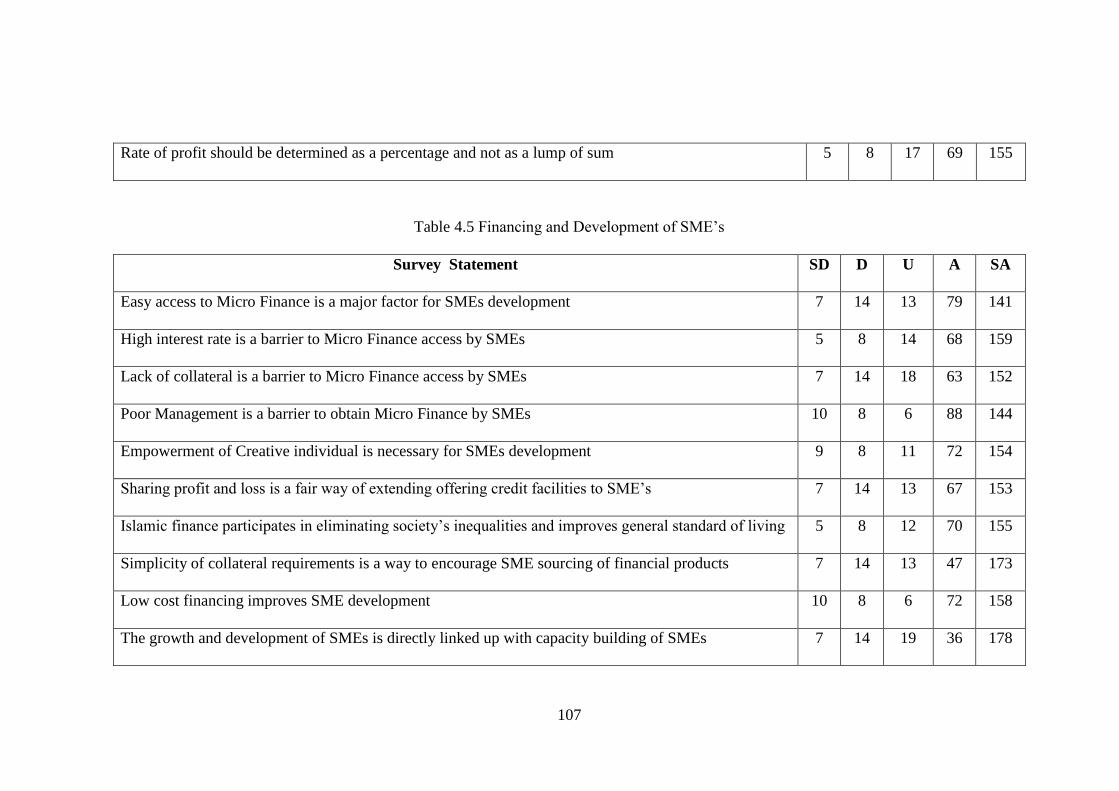

Table 4.4 Mudaraba 106 Table 4.5 Financing and Development of SME’s 107 Table 4.6 Reliability Analysis 110

Table 4.7 Test of Normality (Shapiro Wilik’s Test) 112 Table 4.8 Pearson’s correlations among the variables 114 Table 4.9 Model Summary (Regression Statistics Table) 117 Table 4.10 ANOVA 117 Table 4.11 Coefficients: Significance of Independent Variables on Dependent

Variables 118

viii

LIST OF FIGURES

Figure 3.1. Conceptual Framework 86

1

CHAPTER ONE

INTRODUCTION

1.1 INTRODUCTION

Many economists think that developing and encouraging the establishment of

small and medium enterprises are of most important resources for the process of

economic and social development in all countries in general and the developing

countries in particular. They are considered to be a fundamental factor for increasing

production potentiality and contributing to solving the problems of poverty and

unemployment. For that, many countries gave these enterprises more concern, and

offered them the help and assistance in different ways according to the available

possibilities.

Because of the significance of these enterprises, most of the developing

countries focused their efforts on them so they encourage establishing small and

medium enterprises, particularly after they proved they can efficiently and competently

solve main problems facing the different economies, better than the large industries.

This increasing concern about small and medium enterprises occurs in both the official

and private organizations because they require more manpower and investment in them

is less than the large enterprises. In addition, they are a field for developing

administrative, technical, productive and marketing skills, and open wide areas for

individual initiations and self-employment, which decrease the pressure of providing

job opportunities on the public sector.

These enterprises have enjoyed different ways of care and assistance in both

public and private sectors because they contribute a lot in the industry sector, for

example, the small and medium enterprises constitute approximately 90% of the world

establishments and employ 50%-60% of world manpower. This necessitates providing

support in different modes for these vital sectors.

It is known that Islam puts high attention to the fair distribution of revenues and

wealth and makes sure of optimal benefit of the citizens from the socio-economic gains.

If the majority of governments, administrative authorities, cooperatives and social

2

organizations support the financing of small and medium-sized enterprises programs,

these institutions' policies aim at reducing the rate of poverty and unemployment in the

least-developed societies in their countries of concern.

And small or medium ownership of the company takes several forms: sole

proprietorship, partnership, ended corporation, or limited liability company, but

regardless of the form, the owner managers control dramatically in the daily operations

of their projects and are considered key decision makers. (Hill and Wright, 2001).

Although small and medium-sized companies are considered useful in business

development, but several studies have proven that they often suffer from financial

constraints more than large companies (Ritjonan 0.2008). From this perspective, the

normal lending of banks often fails to meet the financial needs of small and medium-

sized businesses , this is because they fail in making correct assessment of the risks of

such companies, especially small ones (Jibekos and Van Hozil 0.2008).

It is very important to note that the perception of the Islamic finance and the

rules through which the Islamic banks depend on, are based on Islamic Sharia law,

which is called "the jurisprudence of transactions", which includes the Islamic

provisions governing the operations and business deals (Hassan, 2006). These rules and

applications are derived from the Quran, as well as the correct Sunnah as the second

source of Islamic law. And with time, Ijtihad grew up across the views of Muslim

scholars and studies that have contributed to the foundation of principles and provisions

governing the transactions and deals (Shudhor,2008).

The perspective which founded the Islamic Sharia law revolves on the

prohibition of all forms of opposite earns collected from granting loans, or accepting to

pay fees in the form of benefits known as "usury" or "Riba" in the Islamic reference

(Angelo, 2005). The term "haram" is used to describe the buying and selling of goods

or providing services that do not match the principles of Islamic law (Angelo, 2005).

In early times, the principles and regulations based on the assets of Islamic law,

were of great value as a basis for the prosperity of the economy at that time (Shudhor

0.2008). But unfortunately , Islamic banks were established only in the late twentieth

century to apply these principles to private enterprises or semi-private for the benefit of

the Muslim community, where it achieved success and attracted more attention not only

among Muslims but also non-Muslims who were impressed by the nature of the Islamic

banks and the effects it left even in the time of shrinking in global economy which

3

caused recession , crises and conflicts among economists and financial experts in the

world (Hassan,2006).

What distinguishes the Islamic banking products is that they include new

markets mechanisms such as micro-credit, and traditional banking industry have started

to realize that the perception of these small loans should be corrected and become

financially acceptable, which made it gradually gain the credibility among the major

financial industry, where many traditional financial institutions started to adopt projects

funded by small loans as one of the sources of growth (Shudhor ,2008). In the same

context, products targeting small and medium companies are considered another axis

for the development of banks, where specialized banks compete in the presentation of

a comprehensive and integrated financial products, as well as advisory services on the

implementation of business projects for small businesses in Libya. It is said that the

definition of small and medium-sized companies is not a standard and it is not unified

globally because it differs from one country to another. Several criteria are taken into

account in the selection and classification such as the number of workers , size of annual

assets and sales and the annual production and others.

This research defines small and medium enterprises according to the number of

workers employed in the project. The project is considered small if it holds five workers

or less, and medium if it employs between 6 to 20 workers, and a large one if the number

of employees exceeded 20 people. The purpose of the adoption of this criterion is due

to the ease of identifying the number of workers in a business, in addition to being more

reliable than the annual sales volume.

As mentioned above, the small and medium enterprises suffer from the lack of

funding, which is one of the biggest obstacles, in addition to problems in marketing and

administrative transactions, , the weakness of the overall accounting system, the lack of

qualification of manpower, and the many institutional and governmental legislation

constraints, and in this search I did not go through the Funder for lack of time. It is

important to draw attention to a significant matter that this study is on the Shariah-

compliant small and medium enterprises in Libya. Also, the questionnaire was confined

to small and medium enterprises only and did not include banks because time was too

limited.

4

1.2 BACKGROUND TO THE STUDY

SMEs serve as a decent means in the accomplishment of the grand destinations

of each financial project in nations of the world that are equipped towards producing

business and diminishing neediness to the barest least furthermore creating

entrepreneurial capacities and additionally nearby substance. Plus, a couple of various

focal points that can be attributed to SME's fuse that access to infrastructural workplaces

are made basic and reachable, there are moreover the assistance of money related

activities occasioned by the proximity of SME's, change of lifestyle of the laborers of

SMEs and their dependants furthermore the people who are direct or roundaboutly

associated with them. Supporting these facts, Ajose (2010) states that, SMEs are the

turn of money related improvement and first reason for contact for the business world.

Little and medium-sized attempts (SMEs) when in doubt work in various parts of the

economy of a nation and these fuses the zones, for instance, the organization, trade,

agri-business, and amassing divisions. They are also contained a couple firms and these

join for example; town craftsmanship makers, little machine shops, programming

associations which are had down to earth involvement in the arrangement, creation and

amassing of fragile items. SMEs generally work in the formal division of the economy

and use chiefly wage-securing workers. SMEs are consistently masterminded by the

amount of agents and/or by the estimation of their favorable circumstances. The size

request changes inside regions and transversely over countries in admiration to the

measure of the economy and its blessings. It is fundamental to note that there is a base

furthermore the best size for SMEs (Inegbenebor, 2006).

It is of note that subsidizing and back is of enormous significance to the survival

of the SME's. Money related foundations everywhere throughout the world were shaken

up by the Great Recession that began in 2007 and achieved a trough in 2009 preceding

recuperation started. The breakdown of Wall Street Investment Banking monster,

Lehman Brothers, in September of 2008 exasperated the retreat and prompted

shopper/speculator vulnerability (Wilson, 2012). There is motivation to trust that bank

disappointments and vast misfortunes in benefits because of either illiquidity or

indebtedness were a typical marvel which promotes contracted monetary movement.

Because of the focal part of the United States in the worldwide economy, different

nations additionally encountered a serious retreat. The money related administrations

industry was at the focal point of the emergency in nations everywhere throughout the

5

world, as the benefits of monetary foundations drooped from 2007 to 2009. It is

conceivable that the vast misfortunes banks endured were identified with the dangerous

practices they occupied with before and paving the way to the emergency. It gives the

idea that numerous banks were willing to take part in dangerous practices to augment

benefits, which gave them a motivator to unwind their norms for affirming contracts

and different advances to stay aggressive in the commercial center (El-Gamal, 2006).

Benefits for banks were driven by customizable rate credits (and home loans) which

implied that financing costs on advances differed with economic situations. Premium

has been the key driver for the benefit for banks and budgetary establishments alike; be

that as it may, a moderately new routine of fund—Islamic Finance—takes part in the

same exercises as ordinary saves money with one key distinction. Rather than charging

or paying a premium, Islamic Banks use different methods of money to make their

practice productive.

Islamic Finance began in the 1970s in the Middle East and North Africa locale

to basically give managing an account administrations to the Muslim populace (Bakar,

2010). The paying and/or procuring of premium (riba in Arabic) is restricted to the

religion of Islam, henceforth, prompting a keeping money framework that depends on

Islamic standards. Interest is disallowed in Islam since it is seen as a strategy for the

wealthy to misuse the monetarily distraught by troubling them with installments

notwithstanding the central sum that has been loaned out (Saeed 1999). Keeping in mind

the end goal to work on saving money without charging a premium, Islamic banks have

embraced Sharia-agreeable methods of fund permitting them to be beneficial and

consistent with Islamic Law. The principle methods of account utilized by Islamic banks

are Mudaraba, Musharaka, and Murabaha (Ahmed and Umar, 2004).

Mudaraba is like funding, as it is the act of loaning out cash to somebody who

is accepted to be dexterous in a specific field keeping in mind the end goal to understand

a benefit. There is no opportunity to act on the grounds that the subtle elements of how

the mudaraba assets are to be overseen are set in the agreement (Saeed, 1999). This

permits the bank to guarantee that it will recuperate its capital and an arrival in the

capital by deciding the result. Musharaka is an aggregate business wander contract

where the bank loans out to a borrower and shares the benefits/misfortunes (Saeed,

1999). It doesn't permit the borrower to have much opportunity to act on the grounds

that the subtle elements of the agreement are laid out; thus, similar to the mudaraba, it

permits the bank to get an arrival on capital without much instability. Murabaha is the

6

most broadly utilized mode by Islamic keeps money with around 75% of all exchanges.

It is utilized as a part of advancing cash for merchandise and depends on the time

estimation of cash (Saeed, 1999). Rather than charging enthusiasm, there is a pre-

decided expense charged for crediting the assets in view of the extent of the advance.

Whether Mudaraba or Musharaka would alleviate hazard for Islamic banks and possibly

make them more beneficial is questionable. In any case, Murabaha would likely

moderate danger because of the settled charge paying little mind to the hazard of the

credit. Since 75% of all exchanges in Islamic account are Murabaha, it is sensible to

trust that Islamic banks' danger levels are lower than that of customary banks.

Research shows that the surveyed yearly improvement rate for Islamic Banks

was up to 15% going before the Great Recession (Ahmed and Moghul 2003-2004). This

development has backed off all through the budgetary emergency because of more

stringent corporate administration and exhaustive screening forms (Bakar, 2010). The

development of Islamic account the world over is halfway credited to the developing

populace of Muslims in the West, which has prompted the spread of Islamic fund in

nations like the United States and the United Kingdom. Albeit Islamic account has been

becoming quickly, the benefits of Islamic banks may have diverse patterns. The

motivation behind this study is to survey whether Islamic banks fared superior to

anything routine banks all through the crest to trough years (2007-2009) of the Great

Recession.

It is sensible to guess that they may have performed superior to anything

ordinary banks since they don't charge a premium. Premium was the fundamental driver

for benefits for routine banks and incentivized them to make hazardous credits with

high financing costs. Islamic banks' methods of fund permit them to create income in a

way that is separated from the inspiration to search out hazardous advances, henceforth

making Islamic banks more hazard opposed and conceivably more gainful.

1.3 PROBLEM STATEMENT

Small and medium enterprises played and still playing important roles in the

growth and development and the conversion of many of the economies of countries

across the world to the manufacturing stage. But in Libya, the situation is different

where it did not register its positive presence, and this is due to many problems it faces,

and on top of them, the changing of government policies, and the dilemma of funding

7

and finding resources, in addition to management problems and surroundings. (African

Journal, 2012).

Since the establishment of banks and other financial institutions in Libya, the

first goal was to provide support for the development of large companies, as well as the

development of small and medium-sized enterprises. Unfortunately, the first efforts that

have been made did not give any positive results for the benefit of small and medium-

sized enterprises, and the basic dilemma was the lack of funding and finding the

necessary financial resources. This is due to the risk of the continuity of the company's

activity, information asymmetry, poor preparation of project proposals, inadequate

collateral, and the difficulty of verifying previous credits that were obtained, in addition

to the lack of sufficient historical records of the concerned companies, which result in

the reluctance of formal financial institutions for providing funding and the granting of

credit facilities for the small and medium enterprises (Alavi and Broujen ,2010).

1.4 RESEARCH QUESTIONS

1. To what extent does Murabahah effect financing and developing SMEs?

2. What is the effect of Musharakah on financing and developing SMEs?

3. To what extent does Mudharabah effect financing and developing SMEs?

1.5 RESEARCH OBJECTIVES

The broad target of this dissertation is to analyze the effect of Islamic keeping

money operations on Financing and Development of SME's. In the wake of considering

the important parameters and the announcement of issues and reason, the accompanying

particular destinations would be investigated.

1. To investigate the relationship between Murabahah and financing and

developing SMEs.

2. To investigate the relationship between Musharakah and financing and

developing SMEs.

3. To investigate the relationship between Mudharabah and financing and

developing SMEs.

8

1.6 SIGNIFICANCE OF THE RESEARCH

SME's that work in the African mainland and Libya specifically, depend on

significantly all alone sourced cash-flow to develop, make and over the long haul

develop themselves. Firms regularly require genuine administrations backing and

formal monetary help, coming up short which under-interest in long haul capacities

(preparing and R and D) may come about, (Oyelaran-Oyeyinka, 2003).

Libyan Government now tries to set up and create Islamic Banks in Libya

surprisingly. So Libya will begin the improvement of new Islamic Banking operations

to build up the business division in the nation. In this way, the discoveries of this

research on Islamic managing an account financing will be imperative for the

improvement of little and medium scale ventures in the nation.

This examination is one of its kind and subject, as well as it is trusted that the

discoveries will enhance understanding the truth of Islamic financing as a profitable

wellspring of backing for a change of the SME segment and the strengthening of

business people in creating nations. In financial hypothesis, we realize that if the

expense of Investment is high, the poor will stay in reverse, and the necessities will be

more noteworthy for nothing premium banks to put resources into these zones. The

discoveries of this research will uncover reasonable ramifications for the way that,

Islamic financing helps and engages the poor to begin their endeavors in a minimal

effort of speculation contrasted and other ordinary premium based managing an account

and financing models.

Besides, the discoveries from this examination would contribute its own

standard to national improvement and help the legislature of Libya structure procedures

to bolster and inspire the Implementation of new managing an account approaches to

goad the development of Islamic keeping money. Moreover, the discoveries from this

research will give the genuine importance of financial improvement from Islamic point

of view. The discoveries of this research will likewise include to the writing Islamic

managing an account and financing. This would be exceptionally important to future

specialists in the field of SME financing and Islamic speculation and financing models

1.7 DEFINITION OF KEY TERMS

Banks: An organization enabled to manage money, local and remote, and to get

the stores of cash and to credit those monies to outsiders.

9

Hadith: An adage or custom of the Prophet Muhammad (S.A.W.).

Hadith-Qudsi: An adage of Allah Ta'ala described by Prophet Muhammad (S.A.W.)

which is not from the Noble Qur’an.

Halal : passable, legitimate

Murabaha: A sort of "expense in addition to" exchange in which the bank

purchases the advantage then promptly offers it to the client at a pre-concurred higher

value payable by portions. This office is frequently utilized as a part of the way that

standard keeping money clients may look for a home loan when purchasing property.

Musharakah: This is an organization, typically of restricted span, framed to do

a particular venture.Interest for a Musharakah can either be in another endeavor, or by

giving additional backings to a present one. Advantages are apportioned on a pre-chosen

premise, and any incidents shared in degree to the capital duty.

Mudarabah: A type of speculation organization between a bank and a business

that shares the danger and misfortunes/benefits between both sides at pre-concurred

levels. A mudaraba exchange, bringing a portion of the advantages of a business credit

to shariah-agreeable business clients, successfully requires the bank to take a stake in

the business, with customers putting their time and skill in running the undertaking.

1.8 STRUCTURE OF THE CHAPTERS

This research dissertation will be composed of the accompanying sections:

Chapter 1: This section covers the review of the research, the examination

foundation, the issue articulation, research goals, essentialness and impediments of the

research. This section will give the peruser an expansive outline of the examination.

Chapter 2: This section will assess important optional information from an

assortment of auxiliary sources. It will talk about and survey related research and

articles that fringe about the topic.

Chapter 3: This section will introduce an expansive depiction of the research

procedure. It will investigate the strategies of information gathering and examination.

The research instrument and the sorts of information gathered will be talked about in

this part.

Chapter 4: This part will concentrate on the presentation of the gathered and

broke down information utilizing Statistical Package for Social Science (SPSS)

programming.

10

Chapter 5: This part finishes up the discoveries from this study. This is

analyzed against discoveries by different creators. Proposals would be proffered in this

section in light of the discoveries. Additionally in light of the confinements and extent

of this examination; proposals to future analysts will be expressed in this section.

11

CHAPTER TWO

LITERATURE REVIEW

2.1 INTRODUCTION

The Previous Studies We will tackle the previous studies so that we get to know

the importance and role of the small enterprises in achieving the economic development.

Through consecution and search in books and internet articles to find closely related

studies about this study, the following studies were discovered.

Maysaa Habeeb Salman’s study titled “The Funded Developmental Impact of

the SMEs in light of Strategic Development” is an applied study on the enterprises

funded by the Authority of Operating and Developing Enterprises in the Arab Republic

of Syria. The researcher evaluated the developmental impact of small enterprises which

are operated in a supportive developmental strategy. Those enterprises were established

by the support of the government according to a strategic plan of developmental

enterprises. The researcher also evaluated the extent of success these enterprises in

performing their roles in the developmental, social and economic process. The results

showed that the small enterprises are surly capable to provide permanent job

opportunities, seasonal job opportunities, improvement of income level, and decrease

of poverty. In addition, the small enterprises contributed in empowering women

economically in Syria.

Appropriate Economic Strategies and Policies for Promoting and Developing

Small Enterprises: A Case Study in Cairo City (12th Annual Conference: Investment

Crisis Management in the light of the World Economic Blocs). This study tries to

identify the suitable economic strategies and policies which are adopted by the

government for the sake of developing and promoting the small enterprises so that the

problems of poverty and unemployment can be solved, achieving the economic

development and promoting the level of living. It aims at recognizing the development

and importance of small enterprises and discovering the impact of the new global trends

such as globalization, partnership and foreign investment on the small industries. Also,

it aims to identify the role of large industries in developing and supporting the small

12

industries, the features of the small industries and the challenges facing them. Finally,

this study endeavours to give strategic plans for developing the small industries in the

future.

Idrees mohammed Saleh’s study (2009) is entitled “Small and Medium

Enterprises in Libya and Their Role in the Development Process”. It aimed to describe

the role of small enterprises and their importance for achieving the social, economic

development, and to recognize the most significant obstacles that impede these

enterprises and prevent them from fulfilling their role in the development process, and

to suggest the comprehensive solutions for initiating small and medium enterprises and

participating in achieving the social and economic security. This study has concluded

these results:

In Libya, there is no permanent classification based on which we can know

whether an enterprise is small or medium. The problem, according to the entrepreneurs,

is not the lack of administrative and technical experiences and skills but it lies in the

personal funds and the inability to meet the work needs. The difficulty of bank

financing, on the other side, constitutes one of the main obstacles faced by these

enterprises. A big number of small and medium entrepreneurs find it difficult to apply

for financial support from the banks.

Sami Zaidan’s Study (2005) is under the title, “Activating the Role of Small and

Medium Industries in the Process of Social and Economic Development in Syria”. This

study was applied on the small and medium enterprises registered in the private sector

in Syria between 1970 and 2001. It focused on the importance of activating the role of

these industries in the process of social and economic development in Syria. It

concluded many results the most significant of which are that the economic surplus

gained from the small and medium constitutes the most proportion of the surplus

achieved in the private industrial sector, although this surplus was below the desired

level. Also, these small and medium enterprises contributed in attracting new

entrepreneurs to the market but it still below the desired level. Finally, it was discovered

that the economic competency of the small and medium industries was not appropriate

for the Syrian economy and they surpassed the big enterprises. In addition, many small

enterprises suffer from the strong competition, and that some of them are under the

threat of collapsing in the light of globalization and market economy. However, that

does not inhibit many small enterprises to continue in the local market and then the

international market.

13

Stoner’s study (1983) confirmed the importance of strategic planning for the

small enterprises. It was conducted on 451 samll industrial institution in the United

States of America. It aimed to link between the strategic planning processes and the

environmental factors represented by the industry/technology, manpower and economic

factors. That affected the continuity of these institutions. The researcher found that there

are relations between environment conditions and factors, and the strategic planning

processes of these institutions.

Decarlo and Lyons’s study (1980) was implemented on a group of small

industrial enterprises in Britain. It demonstrated that there is a percentage of failure in

the small enterprises because they basically lack the strategic planning in general. The

success of these enterprises depends on their ability to do environmental analysis and

strategy building, objectives and plans which contribute in achieving bigger

opportunities for their growth and continuity in the world of enterprises. That can be

achieved by maintenance of harmony between competitive factors, providers (or

importers), consumers, technological change and the decisions of the strategic

management of these enterprises.

The Role of the SMEs in the Socio-economic Stability in Karachi by Jarid

Quzaishi and Ghobend Mohammed Hairani.

Islamic saving money likewise alluded to as member managing an account in

some speech, is keeping cash or sparing cash development that is solid with the gauges

of Islamic law (Sharia) and it is sensible application through the change of Islamic

monetary angles (Memon, 2007). Sharia blocks the portion or affirmation of specific

premium or charges (known as Riba or usury) for advances of money. Making

Investments in associations that give stock or organizations considered contrary to

Islamic norms is moreover Haraam (illicit). While these norms were used as the reason

for a flourishing economy in earlier times, it is just in the late twentieth century that

different Islamic banks were molded to apply these principles to private or semi-private

business establishments inside the Muslim social order (Memon, 2007).

In the midst of the Islamic Golden Age, early sorts of proto-private venture and

free markets were accessible in the Caliphate, where an early market economy and an

early kind of mercantilism were made between the eighth-twelfth several years, which

some suggest as "Islamic private undertaking". The budgetary economy of the period

relied on upon the by and large streamed cash the dinar, and it weaved territories that

were at that point fiscally self-governing.

14

Different monetary thoughts and methods were associated in early Islamic

keeping cash, including bills of exchange, affiliation (mufawada, for instance, limited

associations (mudaraba), and sorts of capital(al-mal), capital conglomeration (nama al-

mal), checks, promissory notes, trusts, esteem based records, crediting, records and

assignments. Progressive endeavors self-governing from the state moreover existed in

the medieval Islamic world, while the workplace association was also exhibited in the

midst of that time. An extensive part of these early industrialist thoughts was grasped

and further advanced in medieval Europe from the thirteenth century onwards.The parts

and chances of Small and Medium-scale Enterprises (SMEs) in National Growth and

Development in all Economies are very much archived. The motivation behind this

study was to inspect the part of Islamic saving money and Operations on the financing

and advancement of the Small and Medium scale Enterprises area in Libya (Miskam

and Ehsan, 2011).

Dissimilar to the traditional saving money framework, Islamic managing an

account standards set by Islamic law (Shariah) are gone for liberating the human soul

from dishonest practices and corrupt practices. Thusly, premium free saving money is

a restricted idea signifying various saving money instruments or operations which stay

away from premium (Hasan, 2011). Islamic fund for the SMEs portrays the money

related administrations for low pay populaces in which the administrations gave a match

to Islamic standards. In like manner, Islamic money is basically moral fund as its

adjusting the necessities of mankind. As per Baker (2010), Islamic money is a thriving

business sector. Notwithstanding the monetary emergency which has irritated the

economies of industrialized and making countries, the Islamic record has been

successful and has thoroughly enjoyed a 29 percent improvement in assets in 2009 and

a 8.85% advancement rate in 2010. These points of interest are immediately worth $895

billion. Likewise, the Global Head Islamic Finance of Thomson Reuters predicts that

Islamic cash industry will create to $2 trillion volume in the accompanying 5 years

(Miskam and Ehsan, 2011). Since Islam confines the tolerant or paying a premium

which is the base of most standard overseeing an accounting framework, numerous

Muslims feel faltered to utilize their items and administrations (Hasan, 2011).

This section extensively surveys the aggregate writing pertinent to Islamic

managing an account operations and its precepts in the financing and improvement of

little organizations. The point of directing a writing audit is to guarantee that no

imperative variable from past works that has been discovered over and again to have

15

affected the issue is overlooked. As indicated by Sekaran (2003) writing audit or writing

overview is the documentation of a complete survey of both distributed and unpublished

works assembled from sources known as the auxiliary information source.

The general method utilized in this writing survey comprised of giving

understanding from recorded and current points of view. This helps the analyst to

delineate the basic development and foundational hugeness of the topic. Moreover, the

data and points of interest were acquired by analyzing and looking pertinent

examination expositions and articles, insightful compositions, books written in the same

field. Furthermore, Information was accumulated from Emerald research database,

ProQuest research database, and other Internet sources. In completing writing audit, a

deductive methodology is most appropriate for this kind of research that uses the writing

survey to distinguish hypotheses and thoughts and variables which will be tried utilizing

the accumulated information. This deductive methodology builds up a hypothetical or

calculated structure which is along these lines tried (Saunders et al., 2009).

2.2 CRITERIA FOR DEFINITION OF SMES

SMEs assume a vital part in the financial and social improvement of nations.

SMEs are imperative to practically every nation on the planet, however particularly to

creating nations, particularly the individuals who have significant work and wage

circulation challenges. To pick a particular definition for SMEs is something

troublesome and jumbled. In any case, there are a couple of criteria that can be

considered. These criteria could be quantitative criteria like the amount of business and

volume of capital. There are in like manner subjective criteria like regulatory and

particular ones, so it can be assumed that the significance of SMEs changes from

country to country (Hamzeh, 2014). Keeping in mind the end goal to comprehend the

meaning of SMEs we need to know the way of these criteria in more points of interest.

2.2.1 Quantitative Criteria

Occupation: This rule is utilized to recognize SMEs and extensive undertakings

and is viewed as one of the fundamental criteria and the most generally utilized

(Hamzeh, 2014). As indicated by US International Trade Commission, SMEs are

associations with up to 500 specialists. In the EU, SMEs have between 11 to 200

laborers and arrangements under $40 billion). In Japan, SMEs in the business have up

to 300 specialists however those in wholesale and retail have up to 150 and 50 delegates,

16

independently. Making countries use the World Bank benchmark of 11 to 150 delegates

and offers of under US $5 billion (Levine, 2006). In Taiwan, little associations are up

to 20 specialists and medium associations are underneath 200 agents (Hamzeh, 2014).

In Ireland, the SMEs use 50 delegates where in Yemen the little associations unite under

4 specialists. Medium it is considered when the amount of specialists is between 5-9

delegates (Hamzeh, 2014). The SMEs definition differs from nation to nation as

indicated by the level of financial improvement. As per the Statistics Department of

Libya, organizations are ordered little on the off chance that they have between 1-4

representatives and medium in the event that they have between 5-19 workers (Statistic

Department of Libya, 2008). As needs be it appears that this standard fluctuates starting

with one nation then onto the next, contingent upon the extent of the populace in every

nation. For example, China is very surprising from nations, for example, Bahrain or

Jordan (Spencer, 1998).

Capital: Capital is one of the essential generally utilized measures to decide the

extent of the business, since it speaks to an imperative component in deciding the

creation limit of the Business. Likewise, it varies from nation to nation and starting with

one part then onto the next (Hamzeh, 2014). For instance, in Indonesia and India , the

SMEs are the ones who have under $250,000 as a capital where in Saudi Arabia, the

little associations are who have a capital of 5 million riyals which is indistinguishable

to $1.332 million and 25 million riyals for medium associations which is relative to

$6.665million . In Libya, when the capital is not precisely $ 35,000 is considered as a

little business and medium when the capital is $140,000 (Hamzeh, 2014).

Appropriately, nations vary in the extent of the capital arranged for the SMEs on the

premise of the monetary improvement starting with one nation then onto the next, for

occurrence, a nation like "Burkina Faso" can't be like a created nation, for example,

Switzerland or Germany, the financial advancement assumes a critical part in deciding

capital of SMEs (Saudi, 1998).

Deals Volume: Business volume is another model for gathering of associations;

it is an accurate measure of the activity level of the business and its forcefulness

(Sengupta, 2007). This premise is as regularly as could reasonably be expected used as

a part of the United States and Europe, where little associations are named with their

turnover around 1 million dollars a year or less, while in Arab world it is less

fundamental to use and some consider it more invaluable for business associations

rather than present day business.

17

Quantity and Value of Production: According to Rahman (2008) some gives

more hugeness to the value and the measure of the yield, and to the level of the quality

to perceive minimal, medium and significant associations. As demonstrated by this

standard, SMEs are described as those associations that are little and they relate to

minimal size markets of low-pay clients,then again, vast organizations are described by

a boundless generation that goes past their business sectors to the neighborhood and

local markets.

Creation Capacity: This standard is viable in the examination between

organizations where the way of the item like in assembling, sugar and bond, however

in a few organizations where the item structures are various, for example, materials, the

vitality sort of hardware is not an exact measure of the business size (Hamzeh, 2014).

It can be said that each standard of quantitative criteria that have been specified contrasts

starting with one nation then onto the next relying upon the level of monetary,

profitable, and populace variables and what applies to a nation may not be right in

another nation (Saqr et al, 2004).

2.2.2 Qualitative Criteria

Overseeing and Organizing: It is expected that the SMEs have been

recognized by extensive size organizations, as far as the association and administration

(Hamzeh, 2014). SMEs are portrayed by effortlessness, and they frequently absence of

specialized to association aptitudes. Regarding administration, SMEs are frequently

controlled by their proprietor. The proprietors of SMEs are responsible for showcasing,

fund and specialized perspectives; consequently, the accomplishment of these

organizations depends vigorously on the experience and skill of the proprietor

(Asalmeye and Ali, 2002).

Specialized Standard: SMEs, for the most part, utilize the straightforward strategies

for creation with low capital-escalated and high work serious techniques, hence,

innovative techniques are utilized as a part of the extensive business underway, and as

indicated by this foundation organizations are arranged to little, medium and huge in

view of the degree motorization. It is uncommon to discover SMEs using the same

innovation utilized by huge firms (Tanch, 2003).

18

2.3 DEFINITION OF SME’S

As per the International Labor Organization, SMEs are the generation and

craftsmanship offices which are not depicted by specialization in supervision and they

are regulated by the proprietor with up to 250 laborers (Saad, J., et al 2004). This

definition suggests the quantitative standard criteria related to the amount of agents and

it has all the earmarks of being near what was taken by the European Union. The

importance of the United Nations Industrial Development Organization (UNIDO) All

little era units, which joins rural, careful work, and craftsmanship organizations despite

present day small assembling plants, whether as generation lines or those that don't

(Hamzeh, 2014). The importance of the Economic and Social Commission for Western

Asia (ESCWA) SMEs are any business that uses between 50-250 delegates (Hamzeh,

2014). The making countries use the World Bank benchmark of 11-150 specialists and

offers of under US $5 billion and under 500 delegates in made countries where this

definition alters the condition of the making countries and what they have with the made

countries and what it is suited them (Ayyagari et al., 2005). The business is viewed as

little in the event that it utilizes 5 laborers or less, and medium-surveyed endeavors that

utilize to 20, and the business is dealt with as expansive on the off chance that it utilizes

more than 20 workers. As needs be, this grouping relates to the positioning of the Royal

Scientific Society (Hamzeh, 2014).

2.4 CONSTRAINTS FACED BY SMES IN LIBYA

An Islamic Bank is made plans to dispose of uniqueness and make the value in

the economy, trade, business, and industry; develop money related establishment and

make openings for work. Then again, having recognized Islamic keeping money simply

like a game plan for managing an account that is solid with the guidelines of Islamic

law, it should be noticed that the critical hypothesis behind such banks is the limitation

of usury (Riba) yet it doesn't restrict all increments on capital. It is only the

augmentation stipulated or searched for over the key of a credit or commitment that is

denied. Islamic norms basically oblige that execution of capital should similarly be

considered while compensating the capital. The disallowance of a danger-free return

and authorization of exchanging, as love in the Quran section 2 Verse 275:

"Allah has allowed exchanging and taboo Riba"

19

The favored Quran makes the money related activities in an Islamic set-up bona fide

asset maintained with the ability to bring about 'regard extension'. The critical

refinement amidst Islamic and traditional managing an accounting framework structure

is the way to go of riba and advantage. Precisely when the unbelievers of Mecca

struggled that exchange resemble riba the consecrated Qur'an tended to that exchange

and riba are parallel and have nothing in like way and that Allah has allowed the

exchange and forbidden riba. Consequently, so as to make this point clear together with

the likelihood of Islamic keeping cash we have to clarify and disconnect between these

two terms to be particular riba or premium and advantage (Memon, 2007).

In spite of that SMEs are extremely huge for financial advancement; despite

everything they experience the ill effects of numerous issues. As talked about in the

segments over, the significant issue confronting them is the absence of financing

(Memon, 2007), and this issue is deteriorating in the underdeveloped nations, including

Libya. It has been watched that the proprietors of SMEs in Libya depend on own reserve

funds or sell advantages for asset their organizations. These subsidizing sources are

deficient for SMEs in this manner; they need to look for option financing sources. In

such way, we find that SMEs obtain either from the usury surplus units or from Islamic

banks surplus units for the substantive thought and considered honest to goodness also.

As SMEs decrease neediness through the procedure of employment creation and turned

into the subsectors most element fare. Particularly, being not so much capital but rather

more workers requesting, SMEs, from a social point of view, are more proficient in the

allotment of assets contrasted with huge organizations. As the development of SMEs

area is key significance to create and advance of any economy, the style of Islamic

money is the most appropriate and more commendable other option to back SMEs (Anis

and Rosliza, 2011).

To comprehend this issue, we need foundation concerning the nuts and bolts of

Islamic managing an account. Islamic Banking will be managing an accounting

framework in view of Islamic law (Sharia). It takes after Sharia, or Fiqh Almuamalat

(Islamic guidelines on exchanges). Principles and practices of Fiqh Almuamalat are

extricated from the Qur'an (Islamic Holy Book) and the Sunnah, and other auxiliary

wellsprings of Islamic law, for example, ijma‟an (aggregate assertions conclusion

among the researchers of Shariah) and ijtihad (singular thinking) (Rahman, 2008).

Fundamentally, the Islamic keeping money framework is characterized as a managing

an account exchange that is steady with Islamic law, and the primary guideline is to

20

disallow premium or Riba (usurious), in light of the fact that the Islamic Banking

framework is without premium saving money. Islamic banks, as being restricted from

getting or paying premium, don't give out credits; rather, they utilize different structures

like "Murabaha, Musharkh, Modharbh, Istisnaa and Leasing" to make benefit (Besar et

al, 2009). In an outline, so what is Islamic managing an account? It is characterized as

those money related organizations that are situated in their destinations and operations,

on the Islamic law, the sharia. Sharia as a lawful framework depends on the code of

conduct got from the Qur‟an, the Holy Book of Islam, and the Tradition of the Holy

Prophet, the Hadith. For banks to have the capacity to fit in with Islamic tenets and

standards, five religious elements must be followed as far as speculation conduct (Elgar,

2007):

Riba is precluded in all exchanges.

Business and speculation depend on halal exercises.

Maysir (betting) is prohibited and exchanges ought to be free from gharar

(theory or instability).

Zakat (almsgiving) must be paid by the bank to advantage society.

All exercises ought to be in accordance with Islamic standards, and there ought

to be a unique sharia board that regulates and instructs the bank on the property

regarding exchanges (Elgar 2007).

2.4.1 Riba

Riba truly implies „increase‟ or „excess‟ however is in the Qur‟an alluded to as

any extra installments on whatever is advanced, which means interest. As one of the

meeting respondents clarified it: interest comes from various perspectives, Allah calls

it riba (Interview 2). Riba is equivalent, to usury, as well as to all interest and is seen as

uncalled for, exploitative and useless. It is along these lines denied in Islam and Muslims

ought to avoid it for their welfare (Warde 2000). It is additionally expressed in the

Qur‟an that the individuals who overlook the restriction of interest are at war with God

and His Prophet Muhammad. Moreover, Allah expresses that "whoever eats of usury

turns into the fragile living creature and blood implied just for the damnation fire". By

disallowing riba, Islam wishes to build up a general public that is established on decency

and equity (Elgar 2007).

21

This, in any case, does not imply that capital is costless since it is just the

foreordained estimating of capital that is taboo. What it means is that proprietors of

capital in the Islamic request don't have the privilege to request an altered return rate

and can't request any extra installment without sharing the dangers included. Islam lean

towards that the danger of misfortune is similarly shared somewhere around two and

moneylenders ought to be qualified for offering any benefits from an endeavor that they

have financed (Warde 2000).

Along these lines, the sharing of benefits is adequate and has been the

establishment for the advancement and usage of Islamic managing an account. What

varies benefit sharing from interest, and in this manner makes it true blue, is the way

that it is just the benefit sharing proportion that is foreordained and not the rate of return

2.4.2 Profit-and-misfortune sharing (PLS)

The idea of benefit and-misfortune sharing is based upon the possibility that all

benefits and misfortunes got from a physical speculation ought to be shared between

the bank and the borrower, and ought to be founded on the parties‟ separate level of

support. This is the thing that the Muslim world puts stock in. In Islamic saving money,

return-bearing contracts are utilized rather than enthusiasm bearing, which implies that

the bank sets up an association with the borrower.

Two sorts of associations exist: mudarada, which is a commendable

organization or a fund trusteeship, and musharak, which is a more extended term value

like a plan. As indicated by Hickson &Turner (2005), Commenda is restricted

association. In both sorts of organizations, the bank obtains an authoritative offer of the

benefits created from business wanders. What contrasts benefit sharing from interest,

and along these lines makes it real, is the way that it is just the benefit sharing proportion

that is foreordained and not the rate of return (Warde 2000). The rule of PLS implies

that Islamic banks turn out to be specifically concerned with respect to the gainfulness

of the physical venture, pretty much as ordinary banks are worried about the benefit of

the undertaking, because of the danger of potential default on the advance. In any case,

customary banks underline the accepting of premium installments, settled upon by the

borrower, and the productivity of an ordinary bank is not straightforwardly influenced

by the speculation venture's rate of return the length of the premium is being paid. The

productivity of Islamic banks, then again, is straightforwardly associated with the

22

genuine rate of return and the banks should accordingly concentrate on the arrival of

the physical venture (Elgar, 2007). What additionally contrasts the benefit and-

misfortune sharing contracts from the premium based contracts utilized as a part of

ordinary keeping money is the predominant properties for danger administration, as the

installment that the borrower makes to the bank is balanced after the customer's

monetary circumstance.

Islamic banks consistently assemble data about the circumstance of their

customers, with a specific end goal to compute their offer of benefits. Because of this,

agreements based on the PLS guideline are said to give more noteworthy soundness in

the money related markets and urges banks to recognize the significance of long haul

associations with their customers (Elgar, 2007). This is affirmed in the meetings made,

where Islamic keeping money is expressed to be a more secure choice for the borrower,

as a bank can't request installments if the customer is unequipped for paying (e.g. a

business gone bankrupt), in spite of the fact that this is not the case if carelessness,

bungle or misrepresentation can be demonstrated.

The purpose for this is Islamic banks are thought to be financial specialists, in

contrast with moneylenders, and along these lines has a stake in the more extended term

achievement of the customer. Therefore, the customer can concentrate on a long haul

attempt that thusly could create social and financial advantages to the general public as

opposed to being worried about obligation overhauling (Warde, 2000). The fixation on

long run connections in the benefit and-misfortune sharing theory may, in any case,

result in higher expenses inside the Islamic keeping money framework, due to the

requirement for administering the borrower's exhibitions, and frequently implies that

the banks must put more in administrative aptitudes and skill with a specific end goal

to dissect venture ventures (Elgar, 2007).

2.4.3 Halal

Islamic budgetary exercises must take after a strict code of „ethical

investments‟, implying that Islamic banks can't put resources into business or

merchandise that are haram (prohibited) in Islam. Haram is for instance, pork, drugs

including liquor, prostitution and betting. This is the reason theory inside money is not

permitted as it is seen as betting. Rather, Islamic banks must take part in exercises that

are allowed, halal, as indicated by the sharia law. In Islamic keeping money everything

23

must be unadulterated and a man won't have the capacity to get a record in an Islamic

bank on the off chance that he or she is not immaculate

Moreover, Islamic banks are urged to organize the creation of key products that

fulfill the necessities of most of the group, subsequent to the satisfaction of material

needs is considered to guarantee religious opportunity. Furthermore, it is seen as

unsuitable for Islamic banks to put resources into organizations that take an interest in

the creation and advertising of extravagance wares because of the absence of crucial

merchandise and administrations, for example, nourishment, apparel, haven, wellbeing

and instruction that social orders experience the ill effects of (Elgar 2007).

2.4.4 Maysir and Gharar

The Quran prohibits a wide range of betting, maysir, as it permits the speculator

to wind up rich without exertion. Betting, by being a session of immaculate chance, is

considered as dishonest by the shari‟a law as it adds to the unjustified enhancement of

society. Nearby betting, the Islamic law additionally precludes business exercises which

are occupied with or contains any component of betting, bringing about that no Islamic

banks are permitted to have these sorts of organizations as their customers (Elgar, 2007).

In Islam, money related exchanges that include hypothesis, gharar, is another banned

component.

The meaning of gharar is peril, yet is ready to go terms communicated as theory

without sufficient information or as a to a great degree unsafe exchange. Theoretical

business, for example, purchasing products or shares at low cost keeping in mind the

end goal to offer them at a higher cost later on, is thought to be gharar and in this way

illicit. Gharar is likewise pertinent to speculations that incorporate exchanging fates on

money markets, and is what's more seen to exist in every future deal, because of the

instability after some time. This judgment of instability and gharar has prompted the

dismissal of protection, since it contains an obscure danger, and thus there has been an

advancement of Islamic protection, called takaful protection (Elgar 2007).

2.4.5 Zakat

As per the religion of Islam, social equity is of awesome significance and is

refined through arranging society on Islamic social and legitimate standards. Thusly,

equity and uniformity can be gotten, implying that all individuals will have parallel open

24

doors in life. Islamic banks must be occupied with philanthropy since the confidence in

Islam is that no sibling inside the Muslim people group ought to be poor. To ensure

each Muslim a reasonable way of life, Islam has an understood instrument that

empowers a redistribution of salary and riches.

Almsgiving, zakat, is the most key instrument so as to redistribute pay from the

well off to poor people and is an obligatory duty inside the Muslim people group.

Islamic banks and budgetary foundations, which work in those nations where zakat is

not gathered by the state, must all alone make a zakat reserve. This religious tax

collection ought to be gathered from the underlying capital of the bank, on the stores

and on the benefits, and ought to be conveyed by the banks straightforwardly to poor

people or by implication through a religious organization (Elgar, 2007).

2.4.6 Sharia Board

All banks occupied with Islamic saving money must build up a sharia board,

which is a council of religious guides that will guarantee that the exercises and

instruments of the banks are in consistence with the morals of Islam. At the point when

required the board additionally controls the accumulation and dispersion of zakat. The

sharia board constitutes an extra layer of administration, making Islamic banks contrast

from ordinary (Warde, 2000).

2.5 THE DIFFERENCES BETWEEN ISLAMIC AND CONVENTIONAL

BANKING

Today, Islam is the main religion that in any case keeps up the preclusion of

usury, in spite of the fact that this has not generally been the situation. The two other

Abrahamic religions, and in addition Hinduism, have prior prohibited usury (Elgar,

2007). Every single huge religion was already against loan fees as this is expressed out

of the heavenly books. In Christianity, there were disallowances or strict confinements

upon usury for over 1400 years, implying that the taking of a wide range of interest was

admissible. In any case, this has step by step changed inside these religions through the

improvement of laws to abrogate just over the top interest, and this intemperate kind of

interest is still thought to be usurious (Elgar, 2007).

Both Islamic and ordinary banks go about as delegates and trustees for their

customers‟ resources. What varies Islamic keeping money from the routine framework

25

is the way it imparts its misfortunes and benefits to its customers, implying that a

component of commonality is made and that the investors are offered sure proprietor

ship rights (Dar and Presley, 2000). The danger sharing logic of Islamic keeping money

depends on the conviction that the bank must share the borrower's danger. At the point

when utilizing foreordained financing costs, as in ordinary keeping money, an arrival

to the moneylender is ensured and strikes the borrower lopsidedly, which in the religion

of Islam is seen as practical waste and unseemly in a social connection.

Hence, benefit and-misfortune sharing (PLS) is favored in Islamic keeping

money, contrasted with ordinary saving money where the premium based rule is

utilized. By utilizing the PLS rule, Islamic banks can make a relationship between the

borrower, loan specialist and delegate that is based on money related trust and

organization (Yudistira, 2003). Another key component in Islamic saving money is the

requirement for social and monetary improvement finished through business hones that

are in accordance with the Islamic standards and through zakat. Both Islamic and

traditional banks are administratively directed, also Islamic banks must have a sharia

board to control that they are taking after the religious rules of Islam, as said prior. In

contrast with a traditional bank, which fundamentally can be seen as a borrower and

moneylender of assets, an Islamic bank is thought to be an accomplice with its investors,