THE REPORT Turkey 2012 ECONOMY ENERGY COUNTRY PROFILE BANKING TOURISM CAPITAL MARKETS INSURANCE REAL ESTATE CONSTRUCTION INDUSTRY TELECOMS & IT INTERVIEWS 9 781907 065590

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

THE REPORTTurkey 2012

ECONOMY ENERGY COUNTRY PROFILEBANKING TOURISM CAPITAL MARKETSINSURANCE REAL ESTATE CONSTRUCTIONINDUSTRY TELECOMS & IT INTERVIEWS 9 7 8 1 9 0 7 0 6 5 5 9 0

CONTENTS TURKEY 2012

New realitiesPage 12

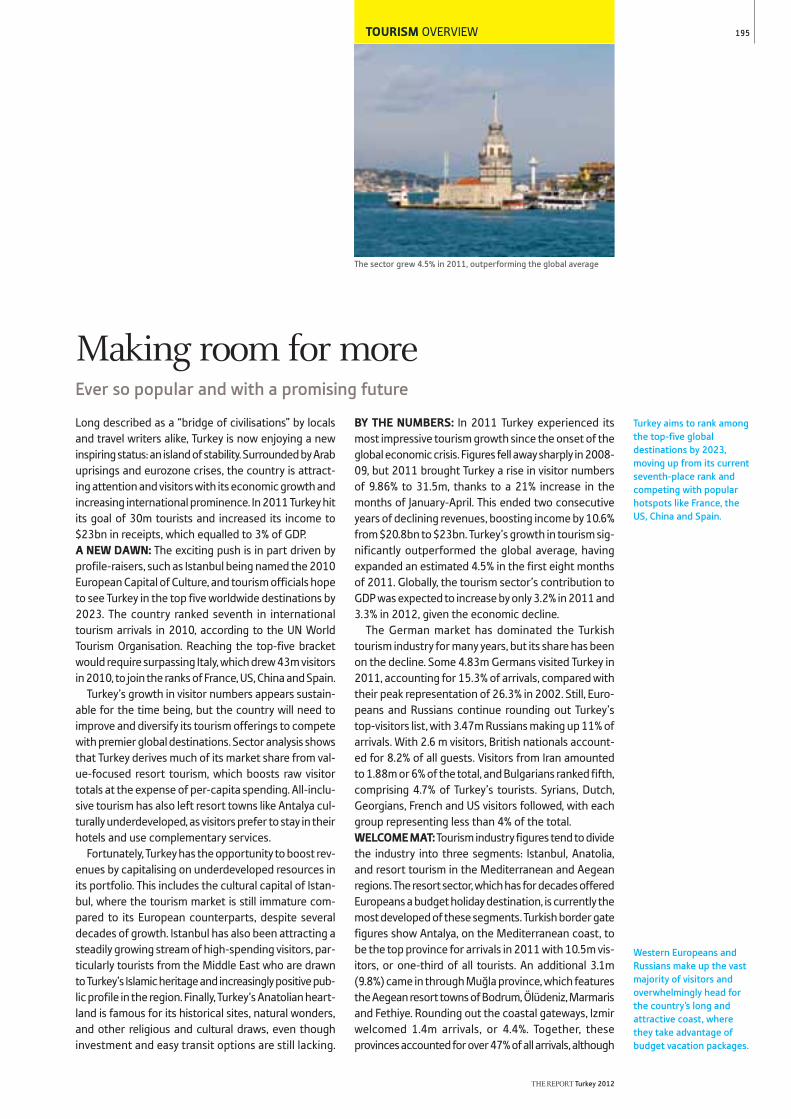

As it moves forward with its third term in office,the Justice and Development Party has over-seen several significant developments. Thecountry has come to be regarded as a region-al leader, and an ongoing legal case againstformer members of the military (though notwithout its critics) is a sign of a new opennessabout formerly taboo subjects. A number of con-stitutional reforms are also under discussion.

A country transformedPage 25

After a year of remarkable growth in2011, which saw the country’s GDPexpand by an estimated 7.8% year-on-year, analysts are predicting a slowerpace for 2012, with the governmentforecasting 4%. The country has beena magnet for foreign direct investmentin recent years, while privatisationefforts continue in earnest. Challengesremain, including a large currentaccount deficit and the risk of inflation.

9

12

15

1618

20

21

22

25

33

3437

3940

COUNTRY PROFILEGrowing influence: The country is a political andeconomic link between the West and the Middle East

POLITICSNew realities: Recent years have brought aremarkable political transformationSetting an example: Regional peace is high onthe agenda as the country seeks to strengthenits role model statusViewpoint: Prime Minister Recep Tayyip Erdo!anInterview: Ahmet Davuto!lu, Minister of ForeignAffairsInterview: Rifat Hisarcıklıo!lu, President, Foreign Economic Relations BoardThe only show in town: High-profile investigations and court cases are dominatingthe headlinesViewpoint: Joe Biden, US Vice-President

ECONOMYA country transformed: Growth is expected tocontinue at a measured paceFacilitating business: While the country is moving up in the rankings, there is still plenty ofroom for improvementInterview: Ali Babacan, Deputy Prime Minister Raising revenue: Fresh bidding rounds are underway for privatisation of state assetsInterview: Mustafa Koç, Chairman, Koç HoldingInterview: Hüsnü Özye!in, Chairman, FIBA Holding

41

4344

46

5354

55

5660

62

66

74

75

76

77

78

798081828384

A win-win relationship: Recent years have seena jump in trade with Gulf statesTowards 100: Setting the long-term sights highViewpoint: Jim O’Neill, Chairman, GoldmanSachs Asset Management

BANKINGStrong strategies, good growth: As banksexpand financial practices, the sector benefitsInterview: Mehmet "im#ek, Minister of FinanceViewpoint: Erdem Ba#çı, Governor, Central Bankof the Republic of TurkeyAlternatively growing: Online and mobile banking cast a wide net for new customersBig lenders: Critical changes and growth signsRoundtable: Martin Spurling, CEO, HSBC Turkey;Adnan Bali, CEO, $# Bankası; and Hüseyin Aydın,General Manager, Ziraat BankasıAs the market swings: The sector’s response toa rapidly shifting monetary policy

CAPITAL MARKETSOn the rebound: The prospects are bright aftera tough year in 2011The next big thing: Legal changes have pavedthe way for the growth of Islamic bondsInterview: Vedat Akgiray, Chairman, Capital Markets BoardInterview: $brahim Turhan, Chairman and CEO,$MKB Borsa IstanbulTaking the middle ground: Significant opportunities open to private equity investorsViewpoint: $lhami Koç, General Manager, $#Investment

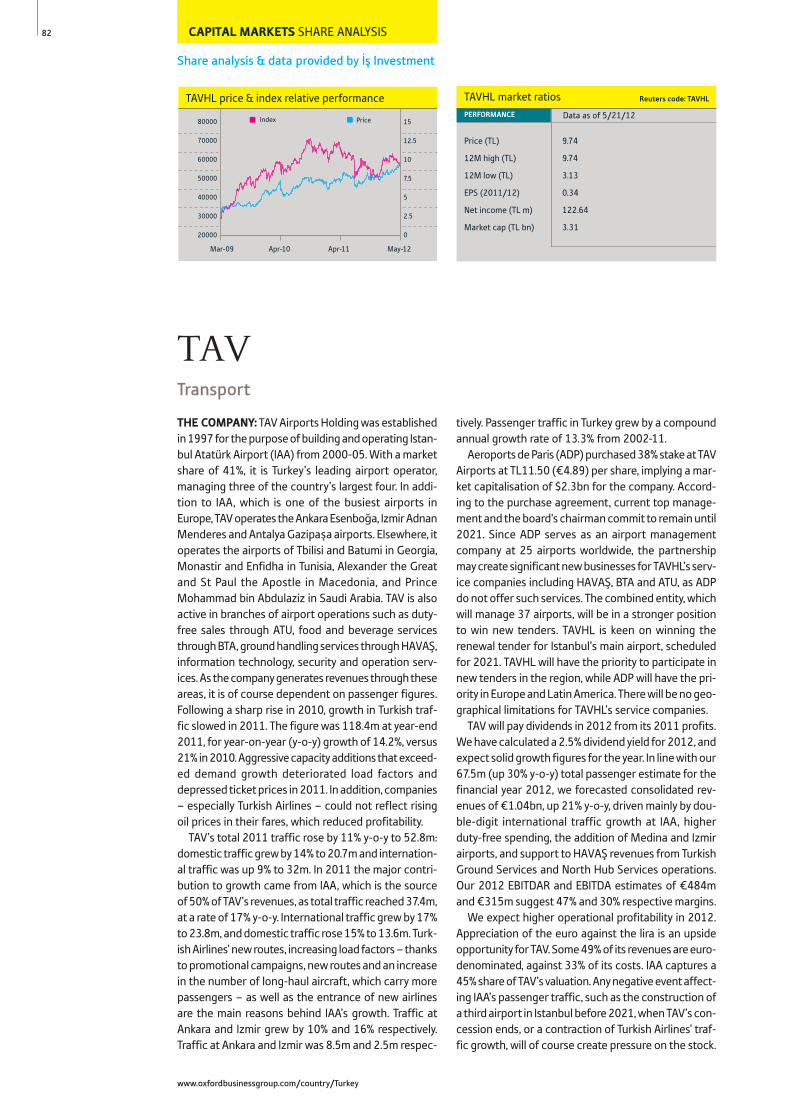

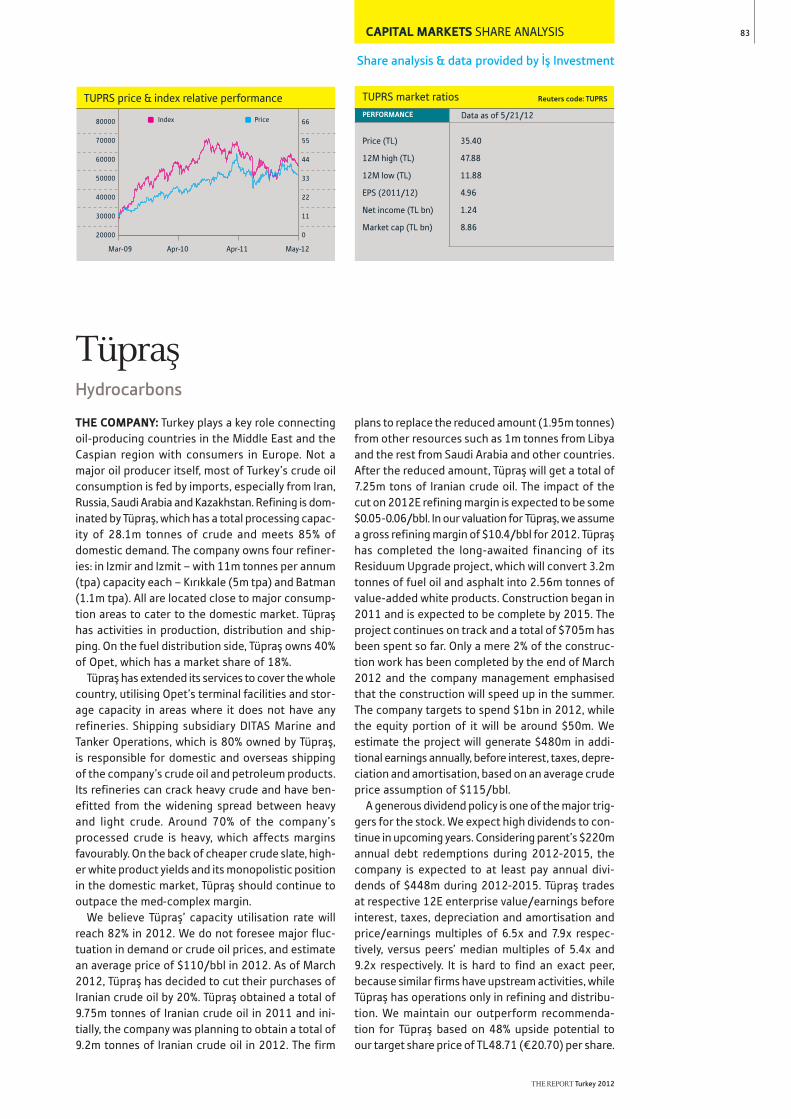

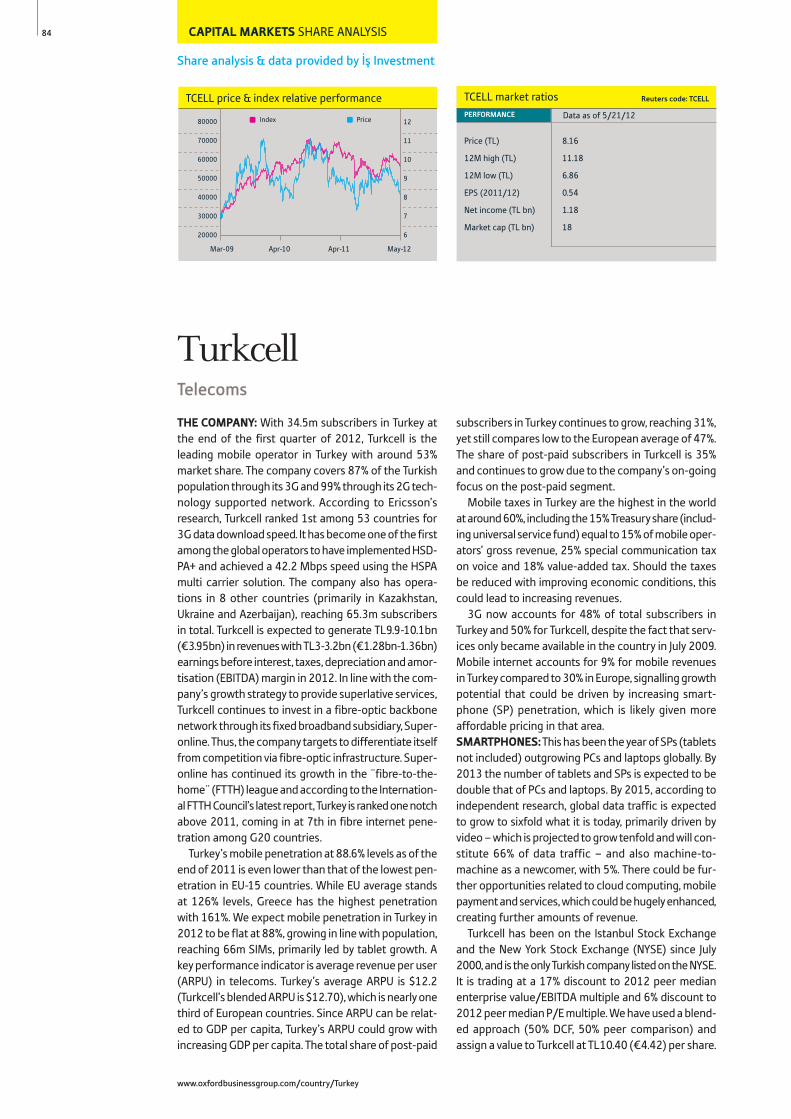

Stocks & Bonds: Share analysis & data provided by !" InvestmentTürk Traktör: Agricultural equipmentArçelik: White goodsHalkbank: BankingTAV: TransportTüpra#: HydrocarbonsTurkcell: Telecoms

ISBN 978-1-907065-59-0

Editor-in-Chief: Andrew JeffreysEditorial Director: Peter Grimsditch

Regional Editor: Paulius KuncinasEditorial Manager: Sean Cox

Chief Sub-editor: Alistair TaylorDeputy Chief Sub-editor: JenniePattersonWeb Editor: Barbara IsenbergSub-editors: Danya Chudacoff, ElyseFranko-Filipasic, Sam Inglis, Elise Laker,William ZemanContributing Sub-editor: MiiaBogdanoff

Analysts: Owen Barron, MatthewGhazarian, Jon Gorvett, Esther Parker,Ayla-Jean Yackley

Senior Editorial Researcher: SusanMano!luEditorial Researchers: Thomas Bacon,Souhir Mzali, Adeline Oka

Art Director: Yonca ErginDeputy Art Director: Cemre StrugoArt Editor: Meltem MuzmuzIllustrations: Shi-Ji LiangPhotographer: Mark Hammami

Production Manager: Selin Bolu

Operations Manager: Yasemin DiriceLogistics & Distribution Coordinator:Esen BarinOperations Assistant: Öznur Usta

OBG would like to thank its localpartners for their assistance andsupport in the research of this project.

CONTENTS TURKEY 2012

www.oxfordbusinessgroup.com/country/Turkey

4

Power playsPage 94

Located between the Middle East andEurasian regions and Western markets,Turkey is a key player in energy trade. Withso many projects in the pipeline and the gov-ernment pledging full liberalisation of thesector, plenty of opportunities await bothinvestors and contractors. Reducing the ener-gy import bill is a key government priority.

86

90

94

100

101

102

103

105107

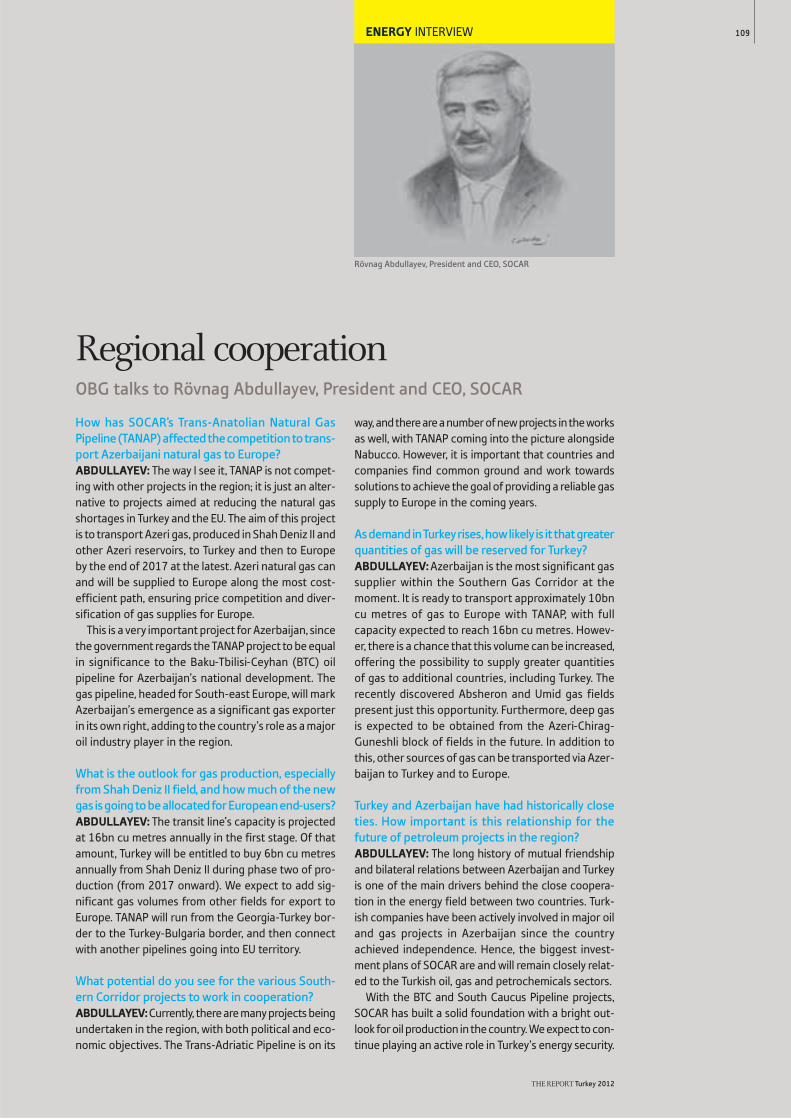

109

111

116

121

INSURANCECleared for take-off: Strong growth potentialcontinues to attract the attention of foreignprovidersOpening the door: Government-drivenchanges are set to make pensions more attractive

ENERGYPower plays: Transit, pipeline and renewableprojects are all in the worksSo crazy it just might work: A massive canalmay one day reshape IstanbulInterview: Taner Yıldız, Minister of Energy andNatural ResourcesInterview: Alexander Medvedev, Director-General, Gazprom ExportIt’s in the pipeline: Investments in the oil andgas infrastructure continueInterview: Tony Hayward, CEO, Genel EnergyWater world: Hydroelectric power plants are amajor renewable energy sourceInterview: Rövnag Abdullayev, President andCEO, SOCARPush for renewables: Turning to wind, sun andwater to boost energy security and protect theenvironment

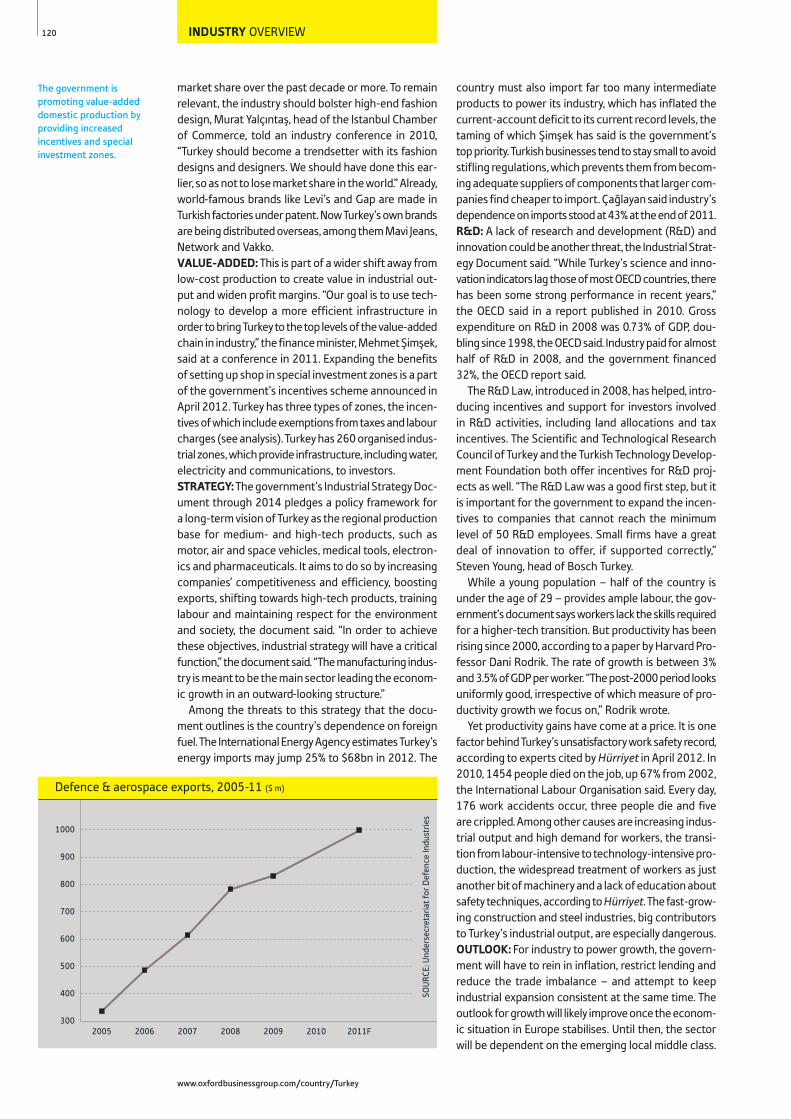

INDUSTRYGaining ground: Building a global reputationfor exporting high-quality productsInterview: Hüseyin Özdilek, President, ÖzdilekHolding

122123125

126

130

132

137

138139140

146

147

148

150

156

157

158

160

163164

166

170

171172

Interview: Tuncay Özilhan, CEO, Anadolu GroupSteel resolve: Production of steel remains strong Interview: Muharrem Dörtka#lı, President andCEO, Turkish Aerospace IndustriesA driving force: Automobile production hasbeen increasing steadilyIn the zone: Industrial parks provide incentivesfor both local and foreign investors

CONSTRUCTION & REAL ESTATEPlanned development: Urban renewal programmes and infrastructure projects Interview: Ahmet Haluk Karabel, President,Housing Development AdministrationInterview: Avni Çelik, Chairman, SINPA"Further afield: Contractors working abroad Rising star: Increased demands in both the residential and commercial marketsBuyers from abroad: A proposed law will makeit easier for foreigners to purchase propertyInterview: Erman Ilıcak, Chairman, RönesansHoldingViewpoint: Anthony Khoi, President and CEO,Aerium Turkey

TRANSPORTMore ways than one: Multiple projects areunder way for continued economic growthIn stops and starts: The privatisation portfolioincludes a number of big-ticket itemsInterview: Binali Yıldırım, Minister of Transport,Communications and Maritime AffairsInterview: Temel Kotil, CEO, Turkish Airlines

AGRICULTURENew pastures: A varied climate and fertile soilmake the country a breadbasket for the regionInterview: Recep Konuk, Chairman, Konya "ekerOut in the country: Gulf states look to acquirefarmland to meet growing demand at home

TELECOMS & ITStaying in touch: The growth of the mobilesector and internet is driving competition andinnovation among providers Come together: Sector players seek to expand their reach into different segments Interview: K. Gökhan Bozkurt, CEO, Türk TelekomInterview: Süreyya Ciliv, General Manager, Turkcell

Chairman: Michael Benson-Colpi

Director of Field Operations: ElizabethBoissevain

Regional Director: Karine LoehmanCountry Director: Meike Neitz

Field Operations Executive: MeltemOkurField Operations Coordinator: ZeynepAkdamar

Project Coordinator: Ba#ak Uluköse

For all editorial and advertisingenquiries please contact us at:[email protected] order a copy of this publication or to enquire about your subscriptionplease contact us at: [email protected].

All rights reserved. No part of thispublication may be reproduced, storedin a retrieval system or transmitted inany form by any means, without theprior written permission of OxfordBusiness Group.

Whilst every effort has been made toensure the accuracy of the informa-tion contained in this book, theauthors and publisher accept noresponsibility for any errors it maycontain, or for any loss, financial orotherwise, sustained by any personusing this publication.

Updates for theinformation provided in thisvolume can be found in OxfordBusiness Group's 'Economic Updates'service available via email or atwww.oxfordbusinessgroup.com

CONTENTS TURKEY 2012 5

THE REPORT Turkey 2012

Gaining groundPage 116

Rising domestic demand and growingexports are keeping the industrial sectorbusy, with production up 9% in 2011. Carsand chemicals lead the pack in terms ofexports, with textiles and steel also keysectors. As many raw materials are import-ed, reining in the trade deficit is increas-ingly important, and adding value andincentivising investors are key to growth.

A growing dynamismPage 180

The government currently funds 90% offormal education activities, but with thepassage of a new education law that intro-duces a number of changes, private insti-tutions are likely to play an increasing role,helping to reduce pressure on the sector.The health care system is also undergoingmajor reforms that are aimed at boostingthe quality and the accessibility of provision.

More ways than onePage 150

Strengthening infrastructure to relievebottlenecks caused by a growing popu-lation and rising trade volumes remainsa key priority. Some $180bn is due to bespent in the sector over the next decade,including large-scale plans across allmodes of transport. PPPs and BOT con-tracts are expected to play a signifi-cant role in expansion and upgrade work.

Put it to printPage 206

With an attentive audience across mul-tiple platforms, the sector is working tomake use of several new connections.A new media law introduced in 2011aims to increase foreign investmentand resolve allocation disputes. As con-tent moves online, advertisers are hop-ing to benefit from its monetisation.

173

178

180

185

186187

191192

195201203

206209

210

211

214

217

218

219224

226

227

232

234

236237

238242244

Technological upgrade: A growing populationof web users is driving demand Need for speed: Investments by operators areleading to faster internet connections

EDUCATION & HEALTHA growing dynamism: Increasing state investment and an expanding private role Interview: Zekeriya Yıldırım, Chairman,Darü##afaka FoundationInvesting in the future: Competition is growing Comprehensive growth: A rising economy iscreating opportunities for expansion Interview: Recep Akda!, Minister of HealthGrowth spurt: A wave of private investment

TOURISMMaking room for more: A promising futureInterview: Kadir Topba#, Mayor of IstanbulNeighbourhood guests: Closer regional ties arehelping to boost the number of visitors

MEDIA & ADVERTISINGPut it to print: Legal reforms create opportunitiesRefreshing the page: Providing content in newand innovative waysInterview: Hanzade Do!an Boyner, Chairwoman, Do!an OnlineGoing digital: Social media and online advertising are taking hold Connected to the market: Popular internetplatforms are the targets for sector growth

TAXDeloitte TurkeyNew principles: The updated commercial codewill boost transparency and auditing standardsA business-friendly package: Incentives andother recent tax developmentsLegal liabilities: Ins and outs of Turkish tax lawViewpoint: Anthony Wilson, Partner in Charge,Deloitte Turkey

LEGAL FRAMEWORKHergüner Bilgen ÖzekeModernising corporate law: An up-to-datelegal code will make for a healthier economy Change for the better: An overview of the current legal landscapeViewpoint: Ümit Hergüner, Managing Partner,Hergüner Bilgen Özeke

THE GUIDEArt boom: Greater importance is being placedon arts and cultureSoap power: The success of Turkish television Rewriting pre-history: Excavations at GöbekliTepe have unearthed some spectacular findsFinding a place to stay: HotelsListings: Important numbers Facts for visitors: Useful information

7

Country ProfilePer capita GDP has tripled over the past decadeGreater spending power among the youth populationIncreased post-secondary school attendanceRising technological entrepreneurship and internet useGeographical location is advantageous for trade

COUNTRY PROFILE

Per capita GDP rose from $2900 in 2001 to over $10,500 in 2011

Over the past decade, Turkey has experienced a num-ber of important transitions that have led to demograph-ic, economic and cultural transformation. These changeshave made contemporary Turkey a regional focal pointthat many Turks regard as an extension of its influencein Ottoman times.

Following the onset of a devastating banking crisisand severe economic recession in 2001, the Justiceand Development Party (AKP) won a landslide victoryin national elections and set about reforming the coun-try’s regulatory environment. A decade of stable AKPleadership has been largely responsible for the coun-try’s economic success, though the political transfor-mation of the country has been source of concernamong Turkey’s traditional elites.

Per capita GDP, which was $2905 in 2001, reached$10,576 in 2011. The young population is increasing-ly mobile and consumption-oriented, which has helpedexpand the nation's service industries while also caus-ing the current account deficit to triple.

While the Turkey of today is vastly more affluent thanthat of a decade ago, the country's conservative andfamily-oriented culture has seen few changes. Manyunmarried men and women still live with their families,even in urban areas, and as a result the availability ofresources among the under-30 demographic is quitehigh, fuelling consumption in everything from textilesto automobiles and cultivating the emergence of aninvestment culture. This demographic strength is amongthe most frequently cited reasons international busi-nesses have given for entering the Turkish market.FOREIGN POLITICS: The EU accession process hasseen waning support from the population over the pastsix years. The relevance of Europe to Turkish experiencehas declined with both the economic recession andstronger political ties with non-European countries. Asa result, the Turkish government is committed to bal-ancing its regional and international interests with softpower and trade, while reducing the role of the Westand NATO in setting policy. This has alarmed many

observers, who have accused the country of "turningEast". Rather, Turkey has risen in prominence as a polit-ical and trade liaison for Western countries, many ofwhich are isolated from the Middle East and NorthAfrica as a result of their history of colonisation andimperialism. Thus, as Turkey’s ties with its Middle East-ern neighbours have grown stronger, its importance inWestern politics has increased in kind.POPULATION: As of December 2011 the populationwas estimated at 74.7m, with nearly 77% of Turkey'scitizens residing in urban areas. Istanbul, the country'slargest city, is home to an estimated 18.2% of the pop-ulation, or 13.6m people, and is the second-largest cityin Europe. Ankara, the capital, has 4.8m residents andthe Aegean city of Izmir has 3.9m.

The country is young compared to other regionalcounterparts – 50% are under the age of 30. The 15-64 age group makes up 67% of the total population,indicating that the youth segment’s dominance of thecountry will continue for some time.

The populace is has a slightly disproportionate num-ber of males, who comprise 50.2% compared to 49.8%females. Women account for 43% of university gradu-ates and are well-represented in white collar positions,particularly in banking and academia. However, femaleworkplace participation has declined overall, from 34.1%in 1990 to 21.6% in 2010.EDUCATION: The country has 166 universities offer-ing two- and four-year degrees, and the expandingyouth population has seen the proliferation of privatetraining institutes providing post-secondary vocation-al training. Despite improvements in the educationalsystem, Turkey still lags in gender equality. Females areunder-represented at all levels of education betweenmiddle school and post-graduate. Additionally, while theliteracy rate was over 94%, illiteracy was four timesmore common among females.INFRASTRUCTURE & TECHNOLOGY: Turkey has invest-ed significant resources in the expansion of air and roadinfrastructure over the past decade and continues to

9

THE REPORT Turkey 2012

Growing influenceA political and economic link between the West and the Middle East

COUNTRY PROFILE

expand and upgrade both commuter and inter-city railoptions. Public transportation is readily available inmost of the major cities and is steadily expanding,though the long history of habitation in Istanbul andAnatolia mean projects that require significant diggingcan be challenging given the likelihood of coming acrosshistorical artefacts.

The recent increase in per-capita income and easedaccess to credit have resulted in a rise in automobileownership. Particularly in Istanbul, this has caused con-gestion, often leading to gridlock during peak com-muting hours. However, less populated cities have beenbetter able to cope with the increased traffic.

Turks are a technology-savvy people; around 25mhouseholds are served by the internet and over 33mTurks are Facebook users. While this penetration rateis only approximately 40%, usage rate are comparableto the UK, as users are engaged at home, in the office,in internet cafes and on their mobile devices.LANGUAGE & ETHNICITY: The country is home to avast number of ethnically distinct groups, though thesedistinctions are often subtle and are not officially quan-tified by the state. Most statistics estimate the ethnicTurkish population at 70-75%, with Kurds comprisingroughly 18% and other minorities 7-12%.

Turkish is the official language of the state and thefirst language of more than 90% of the population.Kurdish, having been officially banned for decades, isbecoming steadily more accepted and is even taughtin some schools; however, societal challenges remainfor Kurdish speakers and the language is not often spo-ken in public outside of the south-east. Arabic is alsocommonly used by about 1.6% of the population, par-ticularly in the south-east of the country.CULTURAL SENSITIVITY: Turkish people are general-ly fairly conservative and expect foreign visitors torespect national and personal values. It is wise to dressconservatively for business, and while in day-to-day lifemeeting times are less important, punctuality is a mustin the business world. Turks are generally patriotic and

proud of their nation, particularly given its economicgrowth and success over the past decade, and they aremore comfortable with foreigners who demonstratesome knowledge – or at least curiosity – about the his-tory and language of their country. In general, business-people and politicians regard Turkey as an importantdestination and do not feel that this is a “fly-in, fly-out”market. It is important to maintain eye contact, partic-ularly in the business world, as this is seen as an indi-cation of one's honesty.GEOGRAPHY & NATURAL RESOURCES: Turkey is bor-dered by eight countries and surrounded by four sig-nificant bodies of water. The Bosphorus Strait flows fromthe Black Sea into the Marmara Sea, dividing the cityof Istanbul into two parts. The European portion of thecountry, comprising 3% of the country’s land mass, issevered again from Anatolia by the Dardanelles, whichflows between the Marmara and the Aegean Sea. Thecountry is also bordered by the Mediterranean to thesouth. In total, Turkey has 7200 km of coastline – near-ly triple the length of its 2600 km of land borders.

The country is in a somewhat precarious political sit-uation given the diversity and varying dispositions ofbordering nations, but it has for the past decade main-tained a "good neighbour" policy that has seen fairlypositive bilateral relations with surrounding countries:Greece and Bulgaria in the west and north, Georgia andArmenia to the north-east, Azerbaijan and Iran to theeast, and Iraq and Syria to the south-east.ECONOMY & CONTRIBUTING SECTORS: While thereare some hydrocarbons resources, the country is stillheavily dependent on imports for electricity genera-tion and motorised vehicles. Energy spending accountsfor more than 50% of the nation’s current deficit.Increasingly, the government is exploring opportuni-ties in on- and offshore exploration, particularly in theeast, and in the Black and Mediterranean Seas.

Despite the dearth of accessible hydrocarbonsreserves, Turkey is a major producer of a number of valu-able minerals. It has more than 70% of the world’sboron reserves and is also home to significant reservesof coal, copper, gold, iron ore, limestone and marble.

Approximately 30% of the country’s land is arable andagriculture accounts for roughly 10% of total GDP. Theagriculture sector also accounts for 30% of employment;however, the scale of the sector’s contribution to GDPhas been reduced by the expansion of both the ener-gy generation and manufacturing industries. The coun-try is a net importer of energy and finished goods, buthas a thriving manufacturing sector, the output ofwhich is predominantly directed to exports.

Europe is the nation's primary trade partner, with theEU importing 52% of Turkey's output. This has exposedthe economy to very real risks of a slowdown. As of end-2011, however, the Turkish economy has still record-ed unexpected growth due to high demand for thecountry's exports following the devaluation of the lira.The country suffers from a current account deficit ofroughly 10%, given the deflated value of the lira, whichhit a low of !.39 in December 2011. This decrease can be partly attributed to oil and natural gas imports.

10

With a population of 13.6m, Istanbul is the biggest city in the country and the second largest in Europe

www.oxfordbusinessgroup.com/country/Turkey

11

PoliticsJustice and Development Party consolidates its positionEU accession process at a standstill for the time beingDebate on constitutional reform on the agenda in 2012Regional upheaval brings challenges and opportunitiesErgenekon investigations and court cases continue

POLITICS OVERVIEW

The Justice and Development Party is in its third term in office

Reforms to bring the country more into line with EUstandards, driven by a widespread desire to makeTurkey a more democratic and free-market-basedeconomy, have gone hand-in-hand with increasedgovernment popularity, stability and economicgrowth. Indeed, there is a great new confidence inTurkish politics and society. This has also led to agreater assertiveness in the international field, wheremany now see the country as a positive role modelfor development throughout the Muslim world.

The country still faces some long-standing chal-lenges, however. The Kurdish issue continues tohaunt political life, stunting development of thesouth-east in particular. The tension between a moresocially conservative and a more secular outlookalso provides the framework for much debate inpublic and private life. Various human rights issuesare also a concern, as is the treatment of journalistsand the perceived state censorship of criticism (seeMedia & Advertising chapter). Meanwhile, the ArabSpring presents challenges for Turkey’s relationswith its neighbours – in particular with Syria. Effortsto end long-standing disputes with Armenia and theArmenian diaspora have made slow progress. EU: Progress toward EU accession has also faltered.Turkey’s application for membership was filed in1987. It joined the Customs Union in 1995, yet didnot begin full membership negotiations until 2005.These involve Turkey completing the 35 chapters ofEU law, known as aquis. As of December 2011, nego-tiations had been opened on 13 chapters, one ofwhich had been provisionally closed. Eight chapterscould not be opened, as they are related to Turkey’srelations with the Republic of Cyprus, an EU mem-ber that Turkey does not recognise. The deadlock,combined with growing hostility from some Europeangovernments toward Turkish membership, continuesto stymie progress on EU accession (see analysis).

Nonetheless, as it moves forward with its thirdterm in power, the Justice and Development Party

(AKP) of Prime Minister Recep Tayyip Erdo!an canlook back on a series of significant achievements.RULING BODIES: Turkey is a democratic republic,with a president as head of state and a governmentled by a prime minister. It has a single-chamber par-liament, the Grand National Assembly of Turkey(TBMM), with a multiparty system in operation.

The political system is governed by the constitu-tion, the current version of which was originallydrawn up under military rule, in 1982. Since then,the constitution has been extensively amended, witha new version also now under debate.

The current president, Abdullah Gül, was electedto the office by parliament in 2007. At that time, thiswas the method for electing the head of state, asoutlined in the 1982 constitution. Yet an amendmentthat same year then introduced direct nationwideelections for the office. Under the old constitution,presidents were elected for a single, seven-year term,with this changed to a maximum of two five-yearterms by the 2007 amendment. This constitutionalchange threw a question mark over Abdullah Gül’srights to re-election, with the possibility that 2012might see the first direct presidential vote – fiveyears after Gül took office. Instead, in January 2012parliament voted to allow the incumbent his full,seven-year term, with the first direct elections nowscheduled for 2014 – subject to a legal challengeto this decision made by the opposition.

The president’s powers are not purely ceremoni-al. As commander-in-chief, he or she can appoint thechief of the general staff and presides over meet-ings of the National Security Council – the key bodybringing together politicians and military leaders. Thepresident also has the power of appointment in keyinstitutions inside the judiciary, the Higher Educa-tion Council, the State Supervisory Council and theuniversities. These areas have all traditionally beenareas of political controversy. While the president maynot initiate legislation, the office holder does hold

Turkey’s currentconstitution was drawn upin 1982 but has since beenextensively amended, and anew version is now underdebate.

12

New realitiesRecent years have brought a remarkable political transformation

www.oxfordbusinessgroup.com/country/Turkey

POLITICS OVERVIEW

veto powers over bills passed by the TBMM, whichif exercised, returns them for further debate. If thebill is then passed again without any changes, thepresident is obliged to pass it, though he or she mayalso refer it to the Constitutional Court or put it toreferendum, if still opposing the bill.GRAND NATIONAL ASSEMBLY: The TBMM is thusthe supreme legislature, with its single chambercomprising 550 deputies elected for four-year termsvia a system of proportional representation, knownas the D’Hondt method. For this, the country is divid-ed into 85 electoral districts. There is also a nation-al party threshold of 10%, meaning votes cast for par-ties receiving less than 10% of the national votehave their ballots re-cast for the next preference.

This has tended to work against minority andregionally based parties. There have been repeatedcalls from the EU and electoral reformers in Turkeyfor the threshold to be lowered in any future con-stitutional amendments. However, the rules alsoallow for independent candidates to be elected, pro-vided they garner more than 10% of the vote in theirprovince. This enabled the supporters of minority par-ties, such as the largely Kurdish Peace and Democ-racy Party (BDP), to run as independents in 2011 andreform as a party group once elected to office. It isat the TBMM that the future prime minister must wina vote of confidence to form a government. He orshe is then appointed by the president.

In the past, when parliament was deeply dividedamong many parties, this usually meant a coalitionwould have to be formed before an administrationcould take office. Since the AKP victory in 2002,however, the prime minister has been able to counton a clear majority in the TBMM from his own par-ty alone. The president appoints the Council of Min-isters, or cabinet, the members of which do not haveto be deputies, but usually are. The 61st cabinet,appointed in July 2011, consisted of the prime min-ister, four deputy prime ministers and 21 ministers.

The government initiates legislation in the formof bills that go before a number of committees – therewere 17 specialised committees in 2011 – and thenbefore the TBMM for voting. Bills go to the presi-dent for final ratification. Deputies and oppositionparties may also attempt to bring their own billsbefore committee and the TBMM.ELECTION RESULTS: The three last general elec-tions for the TBMM, in 2002, 2007 and 2011, sawvictories for the AKP in each. The party won 363seats, with 34.28% of the vote in 2002, 341 seatsand 46.66% of the votes in 2007, and 327 seats with49.83% of the votes in 2011 – illustrating growingpopular support, yet also showing the vagaries ofthe proportional electoral system.

In 2002 the only other party to win representa-tion was the Republican People’s Party (CHP), Turkey’soldest party. Formed in 1923 by the Republic’sfounder, Mustafa Kemal Atatürk, this won 178 seatsin 2002, with 19.38% of the votes. The 2002 elec-tion was a watershed, in that it saw the demise of a

string of parties that had dominated Turkish politicsin the 1990s – the True Path Party, the MotherlandParty and the Democratic Left Party. These all failedto gain a single seat and have yet to recover fromthis defeat, failing again to win any in 2007 or 2011.

After the 2007 election the CHP was joined inopposition by the Nationalist Action Party (MHP),which won 71 seats with 14.29% of the vote. The CHPitself won 112 seats with 20.85% of the vote, whilethe “independents” won 26 seats, 22 of which lat-er became the Kurdish Democratic Society Party(DTP). This was banned in 2009, after the courtsfound links between it and the outlawed KurdishWorkers’ Party (PKK) – an armed group branded “ter-rorist” by Turkey, the US and EU.

In 2011 the CHP won 135 seats with 25.98% ofthe votes, the MHP 53 seats with 13.01% of the votesand the independents 35 seats, all of which becamethe ethnic-Kurdish BDP’s representation.

Thus a pattern appears in which parliament – andthe country as a whole – divides roughly half behindthe government and half against, with the opposi-tion split between left-leaning nationalists in theCHP, right-leaning nationalists in the MHP and minor-ity independents like those comprising the BDP, orits previous incarnations. The CHP, led by KemalK›l›çdaro!lu, and MHP, led by Devlet Bahçeli, have alsooften found themselves cast in the role of defend-ers of an older, more statist Turkey, in the face of thepro-free-market policies of the AKP.

The divide has also often been characterised assecular versus religious, given the Islamist back-ground of the AKP, with both Erdo!an and Gül hav-ing been members of the ill-fated 1995-97 WelfareParty government, which was ousted by the militaryand its allies in what became known as the soft coup,or the February 28 process (see analysis).

Yet many of the AKP leaders are anxious to describetheir party as a conservative democratic group, akinto the Christian Democrats in Germany. Clearly the

13

THE REPORT Turkey 2012

Victories in the last three general elections have demonstrated the AKP’s growing popular support

The government initiateslegislation in the form ofbills that go before severalcommittees and the TBMM.Bills go to the president forfinal ratification.

POLITICS OVERVIEW

AKP is a broad movement, encompassing both lib-eral and more pious opinion, with this also a sourceof speculation over disputes within the ranks.Nonetheless, in early 2012, the party seemed uni-fied behind its current leadership, with little to chal-lenge it within the walls of the TBMM.JUDICIAL POWERS: The Turkish penal code is basedon those of Switzerland and Italy, with separate judi-cial, military and administrative courts. Each has itsown courts of first instance and appellate courts,with the court of jurisdictional disputes chargedwith resolving any disagreement over which systemshould try a case. The supreme courts of the judi-cial system are the Constitutional Court and theCourt of Appeals. The former can be called in by thepresident, or 20% of the TBMM’s deputies, to decideif a new law is constitutional.

Since the constitutional referendum of Septem-ber 2010, the court has had 17 members, ratherthan the previous 11. Parliament was given theauthority to appoint three of these new judges, withother nominating bodies also brought into theprocess. The Court of Appeals (or Court of Cassa-tion) reviews the decisions of the civil and criminallower courts. There is no jury system, with decisionstaken by a panel of three judges in serious cases, whilesingle judges deal with trials at the lower levels.

In the administrative system, the highest cham-ber is the Council of State. This reviews decisions ofthe lower administrative courts and can also give itsopinions on new legislation to the government. Inthe military system, the highest court is the SupremeMilitary Court of Appeals. The military courts underit have jurisdiction in cases involving military per-sonnel acting against other military personnel, or overcrimes committed on military property or during theexercise of military duty. They also have jurisdictionin areas under martial law, or emergency rule.

In 2009 civilian courts were vested with the pow-er to try military personnel accused of threatening

national security or being involved in organisedcrime. This opened the door to prosecution of anumber of military commanders accused of involve-ment in conspiracies to overthrow the government– the “Ergenekon” case (see analysis).

This also further aligned the Turkish judiciary withEU accession requirements, such as full civilian over-sight of the military. Turkey is also a signatory to anumber of European conventions with legal ramifi-cations, such as the European Convention on HumanRights. Crimes against the security of the state werepreviously tried by state security courts (DGMs), withthree judges, one of whom was military. This systemwas changed in 2005 after constitutional reforms,with DGMs replaced by heavy penal courts. Theseremain controversial, as debate on the nature ofcrimes against the security of the state continues.

The promotion and appointment of judges, abo-lition or establishment of courts and review of objec-tions is carried out by the High Council of Judges andPublic Prosecutors, which is overseen by the minis-ter of justice. This was also expanded by the 2010referendum changes, from seven to 22 members, withseveral new bodies receiving the right to nominate.

Currently, there is major debate on further con-stitutional reforms, with 2012 set as a year in whichthe government is due to launch its proposals, witha further referendum likely. Advocates say a newpackage will complete the shift away from the mil-itary-written constitution of 1982, aligning Turkey’spolitics with European states and placing the soldiersfirmly under civilian, political authority. Others, mean-while, fear that such a move may undermine the bal-ance between secular and religious forces in thecountry, paving the way for a more radical, IslamistTurkey; the military has long been seen by many CHPand MHP supporters as a guarantor of secularism.Given this polarity, finding cross-party agreement ona new charter has not been easy, with the processwidely seen likely to take most of 2012 to complete. OUTLOOK: The year ahead, then, is likely to see con-tinued debate on constitutional reform. It shouldalso see Turkey taking an important role in regionalconflicts, such as that in Syria, while its role as a mod-el for the wider Muslim world will also continue tobe debated. The EU accession process is unlikely tosee much progress, meanwhile, with EU domestic pol-itics and the deadlocked Cyprus dispute set to con-tinue to jam the wheels. Greek Cyprus also becomesEU term president in July 2012, and Turkey does notrecognise the Greek Cypriot state.

Domestically, the AKP looks well positioned to con-solidate its hold on the levers of power, with theparty’s different wings seeking to maintain theirauthority, while preserving overall balance. For theopposition, these will continue to be difficult times,as they seek to convince Turks that they have a moreforward-looking vision for the country’s youthfulpopulation. Meanwhile, the old Turkey continues to retreat, with its institutions increasingly com-ing under the influence of the new political realities.

14

President Abdullah Gül was elected by parliament in 2007, though the system has since been changed

There is ongoing debateover constitutionalreforms. The government isexpected to launch itsproposals in 2012, with areferendum likely.

www.oxfordbusinessgroup.com/country/Turkey

POLITICS ANALYSIS

Turkey has pursued a “zero problems with the neighbours” policy

With its thriving economy, democratic system and mod-erately Islamist leadership, in recent years, Turkey hasbeen frequently put forward as a role model for othernations in the Islamic world. This has been helped bygrowing soft power, evident in everything from thepopularity of Turkish soap operas in Egypt to the ubiq-uity of Turkish goods in Iraq. Turkey appears to com-bine successfully both Western and Muslim worlds;indeed, what was once seen by many to be an identi-ty crisis is now widely seen as a valuable flexibility – andunparalleled ability to bridge global divides.

Turkey’s foreign relations have benefitted consider-ably from this widely prevalent view, particularly underthe guidance of the current foreign minister, AhmetDavuto!lu. Taking office in May 2009, he reaffirmed hiscommitment to the “zero problems with the neigh-bours” policy, a stated commitment to address therange of long-standing disputes Turkey has had withmany of the countries immediately surrounding it. Threeyears on, this policy may have fallen foul of events inmany areas, yet as an example of a new spirit of engage-ment – and confidence – it has much to commend it. GEOSTRATEGIES: Turkey shares land borders withGreece, Bulgaria, Syria, Iraq, Iran, Armenia and Georgia,all of which have been hostile neighbours at some pointin recent decades. In 1998 Syria and Turkey came closeto war, over Syrian support of the Kurdish Workers Par-ty (PKK) terrorist group, while relations with Iraq andIran have gone through major ups and downs over theyears. Relations with Greece have frequently also beenpoor, particularly over the Cyprus issue.

Turkey’s land frontiers had been largely frozen overby the NATO/Soviet divide, but after 1990 they beganto open up again. The end of the Cold War also changedbalances in the Middle East, beginning a period of on-the-ground Western, and particularly US, involvementin Iraq. In the Caucasus the collapse of Soviet powerand the eruption of armed conflict between Armeniaand Azerbaijan led to the Nagorno-Karabakh dispute,which still dominates relations between these two

Germany and France haveargued in favour of“privileged partnership” asan alternative to Turkish EUmembership, an idea thecountry rejects.

15

THE REPORT Turkey 2012

Setting an exampleRegional peace high on the agenda as the country seeks to strengthenits role model status

countries and Turkey. Georgia’s fragmentation andRussian support for breakaway Abkhazia and SouthOssetia also demonstrates the fragility of this region.In the Balkans, relations have dramatically improved withGreece and Bulgaria, although the treatment of eth-nic Turks in both countries remains a concern. Turkeyhas also extended its influence in former Ottoman ter-ritories with Muslim populations, such as Kosovo andBosnia. With Syria, hostility remained, with Turkey alsoforging an alliance with Israel during the 1990s. EU NEGOTIATIONS: The EU path has been a tortuousone, however. The political leaderships in France andGermany have both been opposed to Turkish member-ship. Berlin and Paris have argued in favour of an ill-defined “privileged partnership” as an alternative, astatus Turkey rejects. Therefore, while negotiations maycontinue – and the government is keen that they shoulddo – progress is likely to be extremely slow. In the cur-rent climate of eurozone crisis, too, the issue is nothigh on the agenda in Brussels or Ankara.

Concurrent with this cooling in relations, under theJustice and Development Party (AKP) Turkey initiated amultilateral foreign policy, in particular turning greaterattention toward the Arab world. Prime Minister RecepTayyip Erdo!an began a process of breaking with Israelat the Davos summit in 2009, verbally attacking Israelipolitician Shimon Peres. Relations then reached an all-time low after the Mavi Marmara incident, on whicheight Turks and an American of Turkish origin werekilled by Israeli commandos in May 2010. Turkey stillawaits an apology from Israel for the event and has inthe meantime suspended all military cooperation.Turkey’s stance against Israel was immediately popu-lar in the Arab world and beyond. Relations with Syria,Lebanon, Jordan, Egypt and Libya improved greatly, withcommentators suggesting a period of “neo-Ottoman-ism” had begun. Davuto!lu instead sees Turkish policyas being aimed at creating a new framework for region-al peace. With the region going through enormouschanges, the need for this has perhaps been reinforced.

POLITICS VIEWPOINT

Prime Minister Recep Tayyip Erdo!an

Turkey is in a unique economic position and is sig-nificantly more prosperous than it was a decadeago. This is due, in large part, to our party’s effortsto create a reliable, stable and predictable polit-ical and economic environment.

Since late 2002 – except during the peak of therecent global financial crisis in 2009 – the Turk-ish economy has been in constant development,and today, investors can look forward with trustthat the government is paving the way for busi-ness with safe steps.

Among the government’s actions that haveenabled this development is the implementationof a series of incentive schemes. During our gov-ernments we have implemented three incentiveprogrammes – in 2003, 2006 and in 2009 – andwe announced the fourth one in April 2012. Theseschemes have resulted in a radical transforma-tion of the Turkish economy.

Turkey’s GDP was around $230bn when theJustice and Development Party (AKP) came topower in 2002, and over a nine-year period ithas more than tripled, reaching $772bn by theend of 2011. Similarly, the value of exports hasclimbed from $36bn to $135bn, and the reservesheld by the Central Bank of the Republic of Turkeyhave grown from around $27bn to $91bn between2002 and 2011. Over the same period, the lev-els of chronic inflation, unemployment and inter-est rates have all declined, and the ratio of grosspublic debt stock to GDP has fallen from about74% to 39% as well.

In the current economic environment, invest-ments carry a larger share in the growth of theeconomy than ever before. The total value ofinvestments in 2002 was $59bn, while at the endof 2011 this figure stood at $283bn.

Of this, private sector investments accountedfor $235bn of the total in 2011, up from around$43bn in 2002. This surge in investment is the

result of the confidence and stability prevailingin contemporary Turkey.

The schemes put into action during the pastnine years have played an important role in soar-ing investment. Each programme has been adapt-ed to trends in the global economy, as well asrecent changes in the domestic market. The incen-tive scheme that we announced in April has beenprepared and improved according to the newconditions, trends and requirements of domes-tic and global conditions. The latest programmewas prepared for an economy growing at a recordrate of 8.5%, with declining unemployment,increasing exports and a high level of resilienceto the shocks experienced by other economiesduring this time of global uncertainty.

The previous incentive programmes have con-siderably increased investment in Turkey. Forexample, the 2009 incentive programme result-ed in $157bn of investments and created morethan 375,000 jobs, just as it was intended to do.Compared to the 2006 programme, the 2009 pro-gramme saw investments increase by 73%.

What is more, in regards to the previous incen-tive programme in 2009, of the total amount offixed investment, 72% of the investment proj-ects granted incentives were greenfield projectswhose contribution to the economy has a signif-icant multiplier effect. The previous incentivesystem has proved successful, and we are nowupgrading and updating it in accordance withthe changing economic conditions as well as theneeds of investors.

The main objectives of the new incentivescheme are to reduce the current account deficitand boost production and investment for high-import-dependent intermediate goods. Thismeans increasing investment support in the least-developed regions of the country, improving effi-ciency in industry and logistics, and investing in

16

Supporting developmentPrime Minister Recep Tayyip Erdo!an on the government’s new investment incentives programme

www.oxfordbusinessgroup.com/country/Turkey

POLITICS VIEWPOINT

mid- and high-technology products to achieve atechnological transformation.

The new system comprises four differentschemes: general incentives, regional incentives,incentives for large-scale investments and incen-tives for strategic investments. More specifical-ly, we are offering investors value-added tax (VAT)exemptions and corporate tax reductions, as wellas support for insurance premiums, interest pay-ments and land provisions.

This new system will contribute to a structur-al transformation of Turkey’s industries, partic-ularly through strategic investments, by encour-aging domestic production of commonly importedgoods. With the new system, we have redefinedthe regions, decreased the minimum fixed invest-ment amount for large-scale investments andintroduced a new instrument, namely incentivesfor strategic investments that are intended toreduce the country’s current account deficit.

Under the new system, we intend to balancethe levels of local development nationwide, par-ticularly focusing on raising investment in theleast-developed areas. To maximise the impact ofthe programme as a balancing mechanism, wehave categorised the regions according to theirlevels of development. In preparation for thisregion-based approach, we have conducted thor-ough research to update information on eachprovince’s socio-economical ranking and groupedthem into six categories. This ranking system isalso flexible and will be constantly updated as dif-ferent areas reach new levels of development.

With this new incentive scheme, our main pur-pose is to focus on the least-developed regions,therefore incentives for investors in these areaswill benefit from more support. We have alreadyachieved great success in increasing investmentin the least-developed regions; under the incen-tive system launched in 2009, more than half of

incentive certificates were granted to investmentprojects in the least-developed regions.

The new incentive system gives also priority toseveral specific sectors, such as defence, auto-motives, aerospace and aviation, rail and seatransportation, pharmaceuticals, education,tourism and mining. Investments in these sectorswill be supported across Turkey as if they weremade in the fifth incentive region, which coversunderdeveloped areas in the east and south-east.

As for the incentives for strategic investments,the main goal is to promote and support invest-ments in sectors in which we have a considerabletrade deficit. By reducing the trade deficit in keyindustries, we are aiming to reduce our currentaccount deficit. It is important to highlight thatstrategic investments will be strongly supportedin all regions with the same incentives.

I believe that both domestic and foreigninvestors will utilise these incentives in the bestpossible way. In addition to introducing incentiveprogrammes, we are also actively supporting localand foreign investors through public institutions.To this end, we have established the InvestmentSupport and Promotion Agency of Turkey, whichis attached to the Prime Ministry and reportsdirectly to me. The agency assists investors before,during and after their investments.

The government is committed to attracting for-eign direct investment (FDI), and therefore it hasbeen doing its best to create an attractive invest-ment climate in Turkey. That is why, as a result ofour efforts, Turkey has attracted $110bn in FDIover the past nine years, whereas it had attract-ed only $15bn in the preceding eight decadesbefore 2002. I do believe that with the new incen-tive system, we will see more FDI flowing in. Wewill closely follow the implementation of the new incentive programme and work to supportinvestors at every stage of their investments.

17

THE REPORT Turkey 2012

POLITICS INTERVIEW

Ahmet Davuto!lu, Minister of Foreign Affairs

How does Turkey hope to influence and be influ-enced by its foreign partnerships? DAVUTO!LU: Thanks to the economic, political andsocial progress that Turkey achieved in the past decade,we were entrusted with more responsibility and haveconcurrently acquired more tools for engaging theregion and beyond. We began pursuing a more pro-active foreign policy fashioned around the vision ofaverting crisis, reaping opportunities of the post-Sovi-et age and contributing to global efforts to make theworld secure and stable. We are aware that foreignpolicy and economic success go hand in hand.

Economic relations between countries often createa favourable atmosphere to solve political problems,enhancing peace and security. We have thus adopteda multi-dimensional foreign policy based on maximumeconomic cooperation, integration and interdepend-ence with the international community.

To what extent can Turkey leverage its status as arole model for emerging Muslim democracies ineconomic and political terms?DAVUTO!LU: With the political transformation takingplace in the Middle East and North Africa (MENA) region,it is natural that Turkey follows developments closely,especially given that it shares a common history andculture with these countries. We hope that the legiti-mate expectations of the people will be addressed ina peaceful and democratic way.

Currently, Turkey is the 16th-largest economy in theworld and sixth-biggest in Europe, in terms of purchas-ing power parity, and we have raised democratic stan-dards as well. As a result, our soft power has increasedthroughout our neighbourhood and beyond. Turkey isoften described as a model for those countries in theMENA region that are currently undergoing a politicalshift towards a democracy. However, I do not com-pletely agree with this description. In modern interna-tional relations there is no “one size fits all” concept.Each country has its own dynamics and characteristics.

Turkey’s increased soft power is partly the result ofthe comparatively democratic approach taken by thegovernment, so people in neighbouring countries appre-ciate our progress and continue to further expresstheir desires for similar developments in their owncountries. This is why surveys of people throughout theMENA region show a very high favourability rates in atti-tudes toward Turkey. This is not to say that we are amodel for them, but it is apparent that Turkey providesa source of inspiration for peoples of the region.

The challenge for us is to respond in the most effec-tive way possible to this heightened interest in Turkey.We are by no means willing to impose our own rightsor preach to others as to what they should do. Our rela-tionships will first and foremost be guided by the desiresand needs of the countries in question. There is nodoubt that Turkey is strongly committed to the com-mon quest to upholding individual freedoms, humanrights, political liberty and rule of law, as well as to theconsolidation of reforms in this region.

What are the long-term plans for relations withIran, the rest of the MENA region and Central Asia? DAVUTO!LU: Iran is our neighbour and an importantregional actor at the confluence of the Middle East,South Asia and the Caucasus. Last year 2m Iranians vis-ited Turkey and bilateral trade volumes reached $16bn.I believe our efforts to bring lasting solutions to ten-sions in the region are welcomed by the internationalcommunity, and in the long term we intend to increaseour dialogue and cooperation to these ends.

The preservation of peace and stability in the regionis one of the main priorities of Turkey’s foreign policy.At a time when the MENA region is experiencing amoment of awakening, Turkey supports the peacefuland successful conclusion of political transformationon the basis of the legitimate demands of the people.Turkey attaches great importance to close dialogueand cooperation with Arab states in the MENA region,and we have taken important steps in the past few

18

Multi-dimensional policyOBG talks to Ahmet Davuto!lu, Minister of Foreign Affairs

www.oxfordbusinessgroup.com/country/Turkey

POLITICS INTERVIEW

years to develop and diversify relations with the Arabworld – both bilaterally and multilaterally. A number ofhigh-level bilateral strategic mechanisms have beenestablished between Turkey and some Arab countries,in addition to the Turkish-Arab Cooperation Forum, cre-ated in 2007 between Turkey and the Arab League.

Turkey aims to maximise the benefits of the existingbilateral and multilateral cooperation structures withits Arab partners and spares no effort to supportingthe processes of change in the MENA region. In the longterm, Turkey hopes to see the MENA region as a beltof stability, security and prosperity, where the will ofthe people reigns and universal values such as humanrights, rule of law and good governance thrive.

Turkey was the first country to recognise the inde-pendence of the Central Asian countries after the fallof the Soviet Union. Since 1991, our desire for a sta-ble, democratic and prosperous Central Asia has guid-ed our policy priorities in the region. In the last 20 yearswe have sought to increase engagement with thisregion. Some of our long-term objectives towards thesecountries include promoting political and economicreform processes; advancing stability and prosperity;and contributing to the emergence of an environmentconducive to regional cooperation. We foster an envi-ronment of cooperation through bilateral strategicpartnership agreements via the mechanisms of theHigh-Level Strategic Cooperation Council, in additionto multilateral approaches via the Cooperation Coun-cil of Turkic Speaking States.

In what ways can new diplomatic partners, specif-ically in Africa, help diversify Turkey’s foreign trade? DAVUTO!LU: In 2003 Turkey started to implement anew trade development strategy with African Countries,and in the following five years our trade volume withAfrica jumped three-fold to $17bn. Under this strate-gy, we plan to increase Turkey’s share in African nation-s’ total trade to 3% in the coming three years, and like-wise the share of African countries in our own total trade

volume to 10% – double the end-2010 figure of 5.2%.We hope to help develop cooperation with Africancountries in construction, contracting and consultan-cy, engineering and energy, and to enhance Turkey’scompetitiveness in African market.

Turkish businesses have worked hard to limit theadverse effects of the global economic fluctuations ontheir exports, and in 2011 Turkey's total exportsincreased to $134.6bn – a record in the history of coun-try. In 2010 and 2011, Turkey’s exports saw a record-breaking rise destined to more than 60 countries inSouth America, Africa and Asia thanks to its ability toreorient some of its export capacity from traditionalmarkets to new geographies offering untapped poten-tial. I must add that we do not see our policy with Africaas purely economic; we believe we can develop strate-gic partnerships on a regional and global level.

How can the heightened tension with Cyprus overincreased drilling in the Mediterranean be solved? DAVUTO!LU: I foresee two possible options for dif-fusing the current tension due to the Greek Cypriots’unilateral off-shore activities. First, by settling the Cyprusissue by July 1, 2012, and second, by establishing anad-hoc committee between the Turkish and Greek Cypri-ots – under the auspices of the UN – that will enableboth sides to determine the future course of off-shoreactivities in and around Cyprus. The island’s naturalresources, on the shore or at sea, belong to all Cypri-ots and they have equal inherent rights over them.

If our goal is to unite the island, it will not be fair forone side to take unilateral steps without consent of theother. Greek Cypriots should wait for a comprehensivesettlement or immediately launch bilateral talks withTurkish Cypriots. If our aims were beyond reunifying theisland, we would encourage each side to explore forhydrocarbon off their respective territories, but this isnot what Turkey or Turkish Cypriots want. It is very muchat the hands of Greek Cypriots to relieve the currenttension and to turn it into an opportunity to benefit all.

19

THE REPORT Turkey 2012

POLITICS INTERVIEW

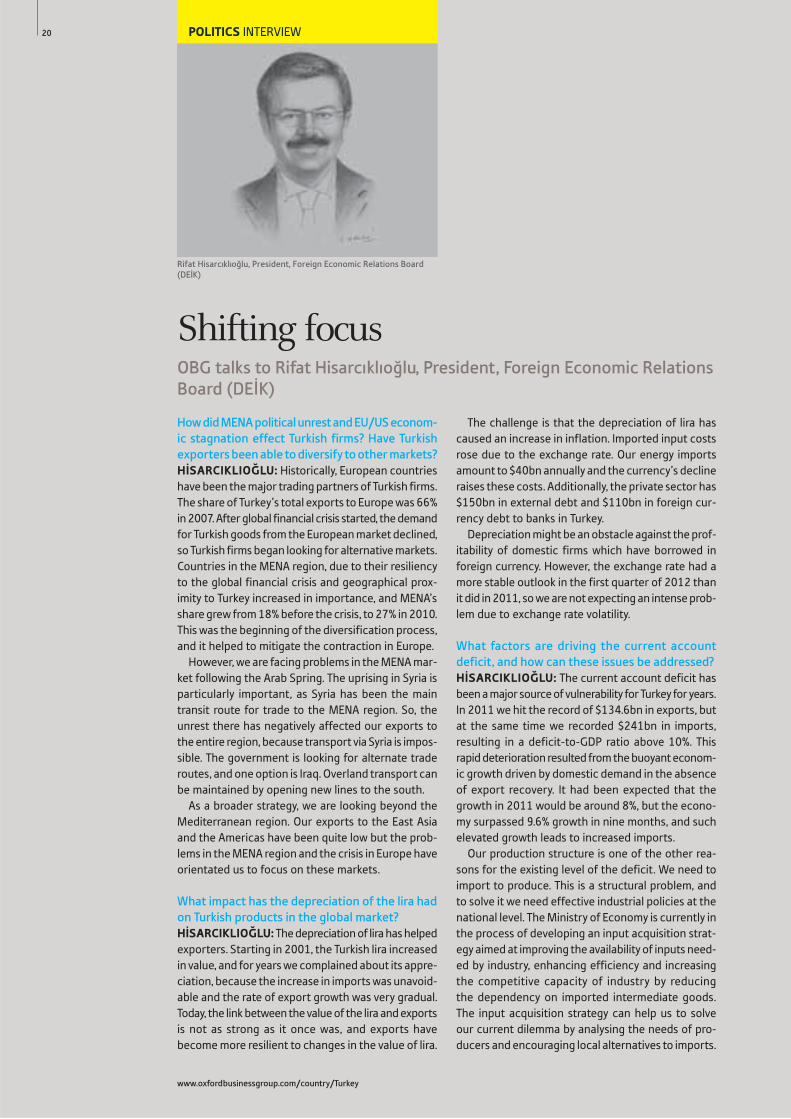

Rifat Hisarcıklıo!lu, President, Foreign Economic Relations Board(DE"K)

How did MENA political unrest and EU/US econom-ic stagnation effect Turkish firms? Have Turkishexporters been able to diversify to other markets? H"SARCIKLIO!LU: Historically, European countrieshave been the major trading partners of Turkish firms.The share of Turkey’s total exports to Europe was 66%in 2007. After global financial crisis started, the demandfor Turkish goods from the European market declined,so Turkish firms began looking for alternative markets.Countries in the MENA region, due to their resiliencyto the global financial crisis and geographical prox-imity to Turkey increased in importance, and MENA’sshare grew from 18% before the crisis, to 27% in 2010.This was the beginning of the diversification process,and it helped to mitigate the contraction in Europe.

However, we are facing problems in the MENA mar-ket following the Arab Spring. The uprising in Syria isparticularly important, as Syria has been the maintransit route for trade to the MENA region. So, theunrest there has negatively affected our exports tothe entire region, because transport via Syria is impos-sible. The government is looking for alternate traderoutes, and one option is Iraq. Overland transport canbe maintained by opening new lines to the south.

As a broader strategy, we are looking beyond theMediterranean region. Our exports to the East Asiaand the Americas have been quite low but the prob-lems in the MENA region and the crisis in Europe haveorientated us to focus on these markets.

What impact has the depreciation of the lira hadon Turkish products in the global market? H"SARCIKLIO!LU: The depreciation of lira has helpedexporters. Starting in 2001, the Turkish lira increasedin value, and for years we complained about its appre-ciation, because the increase in imports was unavoid-able and the rate of export growth was very gradual.Today, the link between the value of the lira and exportsis not as strong as it once was, and exports havebecome more resilient to changes in the value of lira.

The challenge is that the depreciation of lira hascaused an increase in inflation. Imported input costsrose due to the exchange rate. Our energy importsamount to $40bn annually and the currency’s declineraises these costs. Additionally, the private sector has$150bn in external debt and $110bn in foreign cur-rency debt to banks in Turkey.

Depreciation might be an obstacle against the prof-itability of domestic firms which have borrowed inforeign currency. However, the exchange rate had amore stable outlook in the first quarter of 2012 thanit did in 2011, so we are not expecting an intense prob-lem due to exchange rate volatility.

What factors are driving the current accountdeficit, and how can these issues be addressed?H"SARCIKLIO!LU: The current account deficit hasbeen a major source of vulnerability for Turkey for years.In 2011 we hit the record of $134.6bn in exports, butat the same time we recorded $241bn in imports,resulting in a deficit-to-GDP ratio above 10%. Thisrapid deterioration resulted from the buoyant econom-ic growth driven by domestic demand in the absenceof export recovery. It had been expected that thegrowth in 2011 would be around 8%, but the econo-my surpassed 9.6% growth in nine months, and suchelevated growth leads to increased imports.

Our production structure is one of the other rea-sons for the existing level of the deficit. We need toimport to produce. This is a structural problem, andto solve it we need effective industrial policies at thenational level. The Ministry of Economy is currently inthe process of developing an input acquisition strat-egy aimed at improving the availability of inputs need-ed by industry, enhancing efficiency and increasingthe competitive capacity of industry by reducing the dependency on imported intermediate goods.The input acquisition strategy can help us to solve our current dilemma by analysing the needs of pro-ducers and encouraging local alternatives to imports.

20

Shifting focusOBG talks to Rifat Hisarcıklıo!lu, President, Foreign Economic RelationsBoard (DE!K)

www.oxfordbusinessgroup.com/country/Turkey

POLITICS ANALYSIS

The military has had a powerful hold on Turkish politics in the past

Perhaps nothing has been more symbolic of the trans-formation in Turkish society over the past few years thanthe string of indictments the country’s courts haverecently been issuing against senior military figures. Thecountry is in the thick of a major, public reassessmentand reform of the relationship between its soldiers andcivilians – and thus between its past and present. Thisprovokes a deal of controversy both inside and outsideTurkey, and is part of a complex process.

It has seen both a new openness in discussion of pre-viously taboo subjects, such as past military coups,while also leading to allegations of a curtailment of freespeech in the prosecution of several anti-governmentand often pro-military figures. This controversy is like-ly to continue, with the year ahead seeing some majorcourt appearances by senior military leaders.SHIRTS OF STEEL: The Turkish Armed Forces is thesecond-largest military in NATO after the US, and hasplayed a key role in the country’s politics since thefoundation of the modern republic in 1923. Seeingitself as principle guardian of the secular nature of thatrepublic, and responsible for ensuring Turkey’s progresstowards the goals set by the republic’s founder, MustafaKemal Atatürk, the military has not hesitated to inter-vene if it saw this progress threatened.

In 1980 the September 12 coup was launched. Themilitary undoubtedly restored order in a country thatwas, at the time, beset by violent confrontation betweenleft and right. The military then wrote the 1982 con-stitution under which Turkey is still governed – albeitin amended form – and withdrew from outright rule.

However, the generals maintained a powerful holdon politics over the years that followed, predominant-ly through the National Security Council, on which thetop generals met with the leading politicians. For manyyears, the General Staff and its decisions were seen asbeing more important than those of the government,both inside and outside Turkey.

In 1997 the pro-Islamist Welfare Party (RP) was elect-ed to government, however. The military, seeing the RP

Recent events havebrought a new openness inthe discussion of previouslytaboo subjects, while alsoleading to allegations of acurtailment of free speechin the prosecution of anti-government figures.

21

THE REPORT Turkey 2012

The Ergenekon andSledgehammer cases haveinvolved the prosecution ofa number of journalists,academics and politicalactivists accused of linkswith the conspiracies.

The only show in townHigh-profile investigations and court cases are dominating the headlines

as a threat to the Kemalist state they had sworn to pro-tect, organised a “soft coup” – known as the February28 process – that saw the government obliged to resign,this time without overt military action.

The leaders of the current Justice and DevelopmentParty (AKP) government were all important figures inthat RP administration. Therefore, when the AKP wonthe general election of 2002, some in the military andothers were, allegedly, very concerned. What happenednext is highly controversial and has been the subjectof a lengthy series of court cases. ERGENEKON: Known as the “Ergenekon” conspiracy,after an alleged group that sought to trigger anothercoup and oust the AKP, this has since widened to includethe “Sledgehammer” case – which includes allegationsof sinister plots to create instability and overthrow thegovernment, hatched from within the military. This inturn has led to a major investigation of the military itself.Most spectacularly, in March 2012 the former chief ofthe general staff General Ya"ar Büyükanıt was obligedto give testimony in court on the Sledgehammer case.Then in April 2012 the trial of the leader of the 1980military coup, General Kenan Evren, began. At issue ishis role in the alleged torture and disappearance of manyTurks following the takeover. Both these events wouldhave been unthinkable even a few years ago. They indi-cate just how diminished the role of the military is inTurkish politics and how open the discussion now is oversome of the darkest hours in the country’s recent past.

These moves have not been without their critics.Also prosecuted in the Ergenekon and Sledgehammercase have been a number of journalists, academicsand political activists accused of links with the conspir-acy, with this sounding alarm bells for many inside andoutside Turkey. There are also concerns over the capac-ity of the judicial system to deal fairly and efficientlywith such momentous cases. Yet the period ahead islikely to see much re-examination of the recent past.This will likely increase civilian oversight of the mili-tary, while shedding welcome light on recent darkness.

POLITICS VIEWPOINT

Joe Biden, US Vice-President

The US and Turkey have been NATO allies since 1952,and our economic and military relationships are flour-ishing. Trade between the two countries grew by 45%in 2011 alone, to the benefit of both the American andthe Turkish people. In June of 2009 President BarackObama announced our intent to deepen ties betweenAmerican entrepreneurs and their counterparts fromcountries around the world that have significant Mus-lim populations. Nearly a year later, the first GlobalEntrepreneurship Summit brought innovators from 50nations to meet in Washington, DC.

At the summit, President Obama said, ”We’ve cometogether today because of what we share, a belief thatwe are all bound together by certain common aspira-tions – to live in dignity, to get an education, to livehealthy lives and maybe start a business without hav-ing to pay tribute or a bribe to anyone, to speak freelyand have a say in how we are governed, to live in peaceand security and to give our children a better future.”So we might ask the question: what does entrepreneur-ship have to do with those larger aspirations?

Entrepreneurship must be built on solid foundations.This includes a political system that guarantees basicliberties, including the freedom of speech and the free-dom of religion; an educational system that trains itsstudents to challenge established orthodoxy, and aneconomic system that encourages fair competition andrewards those who excel. These foundations haveenabled generations of Americans and others to givelife to world-changing ideas.

It is no coincidence that the most prosperous coun-tries in the world are also the most entrepreneurial coun-tries in the world. This is the group Turkey aspires tojoin. A remarkable economic success story is unfold-ing in Turkey – the economy has tripled in size over thepast decade, exports have quadrupled and per capitaincome has grown dramatically – allowing families tobuild better lives for themselves and for their children.

Turkey is cultivating its own brand of homegrown tal-ents, but it will need a collective effort by society. Estab-

lished entrepreneurs and chambers of commerce mustmentor the next generation, sharing the wisdom gainedby their successes and their failures. Universities andcorporations must work together through researchand internships to nurture and develop the entrepre-neurial skills of students. Investors must occasionallybe willing to take a chance on an unknown talent andan unproven dream. And governments must unlock thecommercial marketplace by facilitating access to cap-ital, removing cumbersome regulations and endingcorrupt practices that stifle competition.

In eight countries and territories, including Turkey,we have launched a programme called Partnership fora New Beginning, which brings together government,private sector and civil society leaders to build anddeepen engagement in areas of economic opportuni-ty, science and technology, and education. The US isparticularly focused on encouraging women entrepre-neurs, because societies that deny women basic rightsare squandering half of their intellectual capital. Studyafter study has shown that those nations that refuseto empower women’s participation in economic affairsare being left behind. Already, in the developing world,almost half of new businesses are women-owned.

We’re also fulfilling a pledge President Obama madein Cairo to build networks of entrepreneurs and expandexchanges in education and to foster cooperation inscience and technology. We have led delegations of busi-nesspeople and investors to Lebanon, Turkey, Egypt, Jor-dan, Tunisia, Indonesia, Morocco and Algeria. We alsounderstand that in these exchanges the US stands tolearn something, because the seeds of innovation andchange do not rest in the US alone.

The objective is to see nations grow in a secure fash-ion. We as a country benefit when democracies flour-ish. I am optimistic about the future because I see thata new generation of entrepreneurs has a chance, likeno other generation before it, to set the course ofdirection for the world, to steer it, to bend the curve in the direction of progress, openness, and humanity.

22

The direction of progressJoe Biden, US Vice-President, on the importance of entrepreneurship

www.oxfordbusinessgroup.com/country/Turkey

23

EconomyPer capita income levels rising at a steady paceAn increasingly simple regulatory system for businessesPrivatisation remains a chief government objectiveTrade with Gulf states is on the riseA series of ambitious long-term development plans

ECONOMY OVERVIEW

The republic now ranks as the world’s 15th-largest economy

Undergoing a major transformation over the pastdecade, the Turkish economy is now the world’s 15thlargest and the sixth largest in Europe, according to 2011World Bank figures for GDP at purchasing power par-ity (PPP). The country has an estimated population of74.7m, giving it the second-largest internal market inEurope, after Germany. Bordering that continent, as wellas the Middle East and the Caucasus, and with a coast-line on both the Mediterranean and Black Seas, Turkeyalso has a unique position in international trade. Thisgives it direct access to a variety of markets, while alsomaking it a major transit route for many more.

A decade ago the economy had just been hit by amajor financial crisis, which had seen the currencyhalve in value overnight, a string of high-street bankscollapse and inflation reach around 100%. Back then,a series of unstable coalition governments presided overan economy that was still heavily state dominated; atthe same time, despite its central economic role, thestate also faced the problem of limited revenues, giv-en the size of the unregistered or “grey” economy. Percapita income in 2001, when the crisis hit, was just $2905at current prices, according to IMF figures – less thanhalf that of Mexico. A decade later, things are very dif-ferent. In 2011, Turkey’s per capita GDP stood at $10,576,a three-fold increase (and higher than that of Mexico). FAST-PACED EXPANSION: In recent years, the statehas withdrawn from many areas of the economy, whileregulation and taxation have been strengthened. Thecurrent government of Prime Minister Recep TayyipErdo!an’s Justice and Development Party (AKP) haswon three general elections in a row, all by a large mar-gin. Inflation has been largely in single digits until recent-ly, while the banking system emerged stronger than everfrom 2001 and was able to withstand the global finan-cial crisis far better than its European peers.

Indeed, in the first quarter of 2011, Turkey outpacedeven China in terms of economic growth, recording ablistering 11.9% GDP expansion year-on-year (y-o-y) atcurrent prices. This was the highest GDP growth in the

world for a quarter where the Organisation for Econom-ic Cooperation and Development’s average was 0.5%.

Yet despite this performance, there are some caus-es for concern, both in terms of its own structures andin external factors. The continued eurozone crisis andsluggish recovery elsewhere will likely have an impact,as Turkey is reliant on external sources for growth.Nonetheless, the economy is expected to continue itsexpansion in 2012 – albeit at a more measured pace.KEY PLAYERS: Turkey’s macroeconomic policy hasbeen determined by the ruling AKP government since2002, with the key institutions at the political levelincluding the Office of the Prime Minister, with Erdo!anthe current prime minister, Ali Babacan the deputyprime minister responsible for the economy and $brahimHalil Çanakçı undersecretary of the treasury; the Min-istry of Finance, with Mehmet "im#ek the current min-ister; and the Ministry of Economy, headed politicallyby Zafer Ça!layan. There are also ministries dedicatedto development; energy and natural resources; food,agriculture and animal husbandry; science, industryand technology; and others all with important roles inpolicy-making and implementation. The Central Bankof the Republic of Turkey (CBRT), meanwhile, is inde-pendent of the government, with its primary objectivemaintaining price stability. Since 2005, its Monetary Pol-icy Committee has held regular, scheduled meetings toannounce policy decisions. For the banking sector,meanwhile, the Banking Regulation and SupervisionAgency acts as its name suggests, while the Capital Mar-kets Board oversees capital markets.

Turkey is also home to a number of economic asso-ciations, from chambers of commerce to trade unions.Some of the well-known and influential today includethe Turkish Business and Industry Association, the Unionof Chambers and Commodity Exchanges of Turkey, theIndependent Industrialists’ and Businessmen’s Associ-ation, and finally the Turkish Exporters Assembly. INDICATORS: While the double-digit growth of first-quarter 2011 grabbed headlines, Turkey’s economy

In 2011 per capita GDPstood at $10,576, a three-fold increase over figuresseen during the country’seconomic crisis in 2001.

25

THE REPORT Turkey 2012

Macroeconomic policy isdetermined by thegovernment, with inputfrom key institutions suchas the Office of the PrimeMinister, the Ministry ofFinance and the Ministry ofEconomy.

A country transformedGrowth is expected to continue at a measured pace

ECONOMY OVERVIEW

had begun picking up speed some time before. Indeed,2010 saw a major recovery under way, after the effectsof the global downturn sent the economy into a divein 2009. Using the expenditure approach to calculation,in that year, GDP at constant prices shrank by 4.7%year-on-year (y-o-y), according to figures from thenational statistical office, TurkStat. Yet by the thirdquarter of 2009, the economy had moved back intogrowth, expanding 6% after three quarters of succes-sive shrinkage. Thus, as 2010 began, the economy wasin recovery. GDP growth at constant prices was 9.2%over the year, with the first two quarters showing 12.6%and 10.4% expansion. Most analysts saw the main fac-tor behind this as a series of major interest rate cuts.The CBRT knocked 10.25 percentage points off therate between October 2008 and November 2009, withthe overnight borrowing rate reaching 6.5% by the lat-ter month. This stoked consumer and business spend-ing, accelerating Turkey out of the downturn.

At constant prices, GDP for 2010 thus ended 8.9%up on 2009, with the final quarter seeing 9.2% growth.The headline first-quarter 2011 figure of 11% repre-sented a continuation of an increasing trend. The sec-ond and third quarters of 2011 recorded 9.1% and 8.4%growth, respectively, with some analysts pointing tofrontloading of projects during the first half of 2011due to the June general elections as a further factorbehind growth. Figures released at the beginning of April2012 put growth at 5.2% for the fourth quarter of