1 The relationship between Financial Participation Plans and Company Financial Performance Evidence from a Dutch Longitudinal Panel Paper for the Mid Year Fellows Conference, SMLR, Rutgers University NJ, 25 February 2011 DRAFT, Please do not quote Any comments highly appreciated ! 16 February 2011 Geert BRAAM and Erik POUTSMA Institute for Management Research, Nijmegen School of Management Radboud University, PO Box 9108 HK Nijmegen, Netherlands Tel. +31 24 3611608 / Fax. +31 24 3611933 Correspondence: [email protected] Abstract This study investigates the relationship between several forms of financial participation (profit sharing, stock options and shares) and company financial performance for the period of 1992 – 2009 comprising 2216 observations. Using a unique dataset of a panel of companies listed on the Euronext Amsterdam Stock Exchange, we are not only able to distinguish between forms of participation but also to what extend these plans are narrow- based, directed to top management and executives only, or broad-based, targeted to all employees. The panel data allows us also to take into account time lag effects, as profit sharing is usually said to have short term effects while stock options and share plans are more targeted to longer term impact. We used accounting and market-based indicators for company financial performance such as ROE, ROA, earnings per share and dividend yield. The results of the econometric panel analysis using STATA 10 show that when firm size, period and fixed firm effects, or industry and random firm effects are controlled for, in comparison with companies with no plan, broad-based profit sharing and share plans and combinations of these plans show systematically significant higher positive relationships with many performance indicators than narrow-based plans. We discuss the findings in light of future directions of research, in particular also by adding more employment, qualitative and social performance data.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

The relationship between Financial Participation Plans and Company Financial Performance Evidence from a Dutch Longitudinal Panel

Paper for the Mid Year Fellows Conference,

SMLR, Rutgers University NJ, 25 February 2011

DRAFT, Please do not quote

Any comments highly appreciated!

16 February 2011

Geert BRAAM and Erik POUTSMA Institute for Management Research, Nijmegen School of Management

Radboud University, PO Box 9108 HK Nijmegen, Netherlands Tel. +31 24 3611608 / Fax. +31 24 3611933

Correspondence: [email protected]

Abstract

This study investigates the relationship between several forms of financial participation

(profit sharing, stock options and shares) and company financial performance for the period

of 1992 – 2009 comprising 2216 observations. Using a unique dataset of a panel of

companies listed on the Euronext Amsterdam Stock Exchange, we are not only able to

distinguish between forms of participation but also to what extend these plans are narrow-

based, directed to top management and executives only, or broad-based, targeted to all

employees. The panel data allows us also to take into account time lag effects, as profit

sharing is usually said to have short term effects while stock options and share plans are

more targeted to longer term impact. We used accounting and market-based indicators for

company financial performance such as ROE, ROA, earnings per share and dividend yield.

The results of the econometric panel analysis using STATA 10 show that when firm size,

period and fixed firm effects, or industry and random firm effects are controlled for, in

comparison with companies with no plan, broad-based profit sharing and share plans and

combinations of these plans show systematically significant higher positive relationships

with many performance indicators than narrow-based plans. We discuss the findings in light

of future directions of research, in particular also by adding more employment, qualitative

and social performance data.

2

The Influence of Financial Participation on Company Performance.

Evidence from a Dutch Longitudinal Panel

1. Introduction

The growing body of research on the relationship between financial participation and

firm performance indicates that the adoption of schemes which allow for employee

participation in profits and/or share ownership and options plans is often associated with

higher levels of productivity or other outcomes. However, most studies focus on specific

forms of financial participation and do not compare the impact of different forms of financial

participation in one study simultaneously. A second shortcoming of most studies is that they

often use dummies for the existence of a scheme while not specifying the spread and

coverage in the firm. Finally, studies are mainly cross sectional with problems addressing

causality. In this paper we are able to overcome these shortcomings in using a longitudinal

panel of companies with three forms of narrow and broad-based financial participation plans

(profit sharing, share plans and option plans) where we are able to approach the causal

relationship with performance.

The results show that when firm, period, size and industry effects are controlled for,

in comparison with companies with no plan, broad-based profit sharing and share plans

show systematically significant higher positive relationships with many performance

indicators than narrow-based plans. In addition, both the option plans for top management

and the broad-based option plans are negatively related with firm performance in

comparison with companies with no plan. However, broad-based option plans in

combination with broad-based profit sharing plans have the opposite effect on firm

performance, suggesting synergic impacts since one type of plan may compensate for

disadvantages of the other plan.

This study contributes to the literature in several ways …

The remainder of the article is structured as follows. First, we review related

literature and develop hypotheses regarding the relationship between several forms of

financial participation and company financial performance. Next the research method is

3

described, and the results are presented and discussed. Finally, we draw conclusions, discuss

limitations of our study, and point out directions for further research.

2. Literature and hypotheses

Since the 1970s a growing number of studies focused on the relationship between financial

participation and changes in attitudes and behaviour of employees as well as firm

performance. Much of this research originates from experiences in the USA and UK, while

limited amount of research is found in continental Europe and other parts of the world.

Most of the studies focus on one type of financial participation, i.e. profit sharing or

employee share ownership or stock options. In addition, the research is divided in a branch

focussing on schemes for executives separated from the branch of research on so-called

broad-based employee share ownership. Similar theoretical arguments are used for the

impact of narrow and broad-based schemes, such as the agency and incentives approach,

but there are also important differences. We follow Klein (1987) who argues that there are

three main arguments for the impact of financial participation schemes on attitude and

behaviour of employees.

(1) The ownership impact, also called the intrinsic motivating effect; this implies that simply

through the fact of receiving a share of the company employees develop the feeling of co-

ownership and act accordingly. Pierce et al. (1991, 2001, 2003) emphasize the importance of

psychological ownership. The argument is that ownership changes the mindset in such a way

that psychological ownership is developed, which causes changes in attitudes and behaviour.

Several empirical studies support this view (Kaarsemaker, 2006; Pendleton, 2001; Pendleton

et al., 1998; Wagner et al., 2003). This is expressed in extra effort to keep the sustain the

company and the ownership and to protect the company from external threats.

(2) The motivation impact, also called the extrinsic effect; employees deliver extra effort

because they expect to receive an extra reward in the end.

(3) The commitment impact, also called the instrumental effect; through financial

participation and alignment of interests, both employees and employer act upon the

4

common interest. This is expressed by a focus on profit and profitability of the firm, a

willingness to participate in strategic decision making and a focus on cost effective working.

The subsequent literature more or less supports these effects, while other literature

tries to find moderators and intervening variables to clarify the hypothesized effects.

Usually, the behavioural impacts under study are extra effort, cooperation and citizenship

behaviour, turnover and commitment.

Most studies focus on specific forms of financial participation such as employee share

ownership plans (ESOPs), profit sharing (deferred or cash) or stock options. However, there

are important differences between these schemes in nature and in its incentive effects,

especially the difference between shares related schemes and profit sharing arrangements.

The last one is typically directed to the short term (in case of cash) and is an expression of

past performance, while the others are much more directed to the long term and focused on

future performance with some risk included. A profit share is also easier to allocate in cash

which makes the incentive effective more direct and stronger. In addition, there are more

studies on broad-based share plans and broad-based profit share plans than on broad-based

options, partly due to availability of data. Many studies focused on narrow-based option

plans. We now proceed with a short summary of research results.

Since the 1970s a large number of studies looked into the relationship between share

plans and attitudes and behaviour of employees. Most studies were performed in the UK

and USA. Of the more than 50 studies, two third noted a positive relationship with attitudes

and behaviour while the others did not show clear results (Kaarsemaker, 2006). Also the

relationship between share plans and performance is frequently investigated. Since the

1970s, we note more than 70 studies where the research focused on profit, productivity and

ROE. In part the research also used more subjective evaluations of relative performance. A

number of studies deliver overviews of the results (Conte and Svejnar 1990; Dougouliagos

1995; Kruse and Blasi 1997; Pérotin and Robinson 2003). In summary, most studies conclude

a small positive effect of share plans on productivity. This relationship is stronger in case of

broader coverage and spread of shares among employees. However, most studies are cross

sectional which makes drawing conclusions on causal inferences difficult. The few studies

5

that use longitudinal panel data show positive effects *of … on …+ on the longer term (Kruse,

1992, 1993; Fakhfakh & Pérotin, 2000; Jones & Kato, 1995).

The relationship between profit sharing and performance is also investigated many

times. The general outcome is that the relationship is positive. The review and metastudies

of Doucouliagos (1995) and Kruse en Blasi (1997) show in general and for the countries

where the studies are performed, positive significant effect of profit sharing plans on

productivity, while share plans show neutral or weak positive relationships.

The objectives of stock option plans are to attract, motivate and bind executives and

employees. The aim is to attract and commit less risk averse employees who accept that part

of their remuneration lies in the future and is risky (Hall en Murphy, 2002). Because most

employees and top management are risk averse the incentive effect of option plans might

not be substantial. Important is also to what extent options are part of salary or mainly

developed as a perk, an extra bonus. In case of executives and management options may be

a substantial part of salary, while in case of broad-based plans this is usually not the case.

Not much incentive effect is expected from broad-based plans. In addition, like in most

collective rewards, the free rider effect in large groups will lower the performance effect

(Lazear 2002). Another critic on stock option plans is that it might be a very costly type of

remuneration. Since options are risky a risk premium is expected and needed. In case of top

managers this might boost the number of options to cover the risk. If then options should

appear on the profit and loss account, this remuneration might be less cost effective.

Compared with share plans, option plans may be less risky but at the same time it

generates less ownership feelings. Ownership might occur at the point of exercise but in

practice in most cases the shares are sold immediately. Commitment effect of options may

develop as long as the vesting period which is comparable with deferred profit sharing

schemes (in the Netherlands usually 4 years in order to benefit from tax exemption).

Critics suggest that options are not very effective since management may have

possibilities for earnings management where options are part of strategies to extract the

most personal benefits, the ‘rent extraction perspective’ (Bartov and Mohanram, 2004).

Besides, management may use put option to lower the risk of lower benefits. Finally, the

6

move to accounting standards where options are more and more expensed makes option

plans an unfavorable form of remuneration.

Most research on stock options focuses on options for executives and managers and

show mixed results on performance. There are only a few studies that focus on broad-based

plans. In a UK study a positive relation was found between broad option plans and

performance, but due to the nature of the study – cross sectional - the causal order could

not be decided (Conyon en Freeman 2000). A more in depth study is performed by the

Rutgers University (Blasi et al. 2000, Sesil et al. 2001). In this study of USA companies

positive relationships were found between broad-based option plans and a serie of

performance indicators in comparison with companies that have no broad-based plan.

However, the study included many companies from biotechnology en computer industry

where substantial option plans are common; this is not the case in the Netherlands.

Important is to note is that studies do not or cannot make a distinction between

different types of plans. That is, studies cannot conclude if the effect is attributed to the plan

under study while there may be also other plans in place. Moreover, the existence of a

combination of plans may have synergic impacts on performance because one type of plan

may compensate for disadvantages of the other plan. For instance, the short term effect of

profit sharing combined with the longer term effect of share plans; or ownership effects

combined with motivation effects. There are hardly any studies that investigated the

interaction of different plans. Aan exemption might be Robinson & Wilson (2006), who, in

the passing, found that the combination of profit sharing and share plans is positively related

to higher efficiency compared with companies with no plans.

Hypotheses:

Following Klein’s model and the studies discussed, we formulate the following hypotheses.

Share plans have a long term impact due to ownership and commitment. This is dependent

on the amount of shares; in case of top management, the effect may be stronger than in

case of broad-based plans.

H1 Share plans for top management (1a) and broad-based share plans (1b) have a longer

term positive relationship with firm performance.

7

According to the model of Klein profit sharing may have a direct short term motivation

effect. In case of broad-based profit sharing plans the free rider effect may limit the effect.

H2 Profit sharing plans for top management (2a) and broad-based profit sharing plans

(2b) have a short term positive relationship with firm performance.

According to Klein’s model option plans have no clear direction of the impact. These plans

do not develop ownership. Motivation and commitment might be boosted only for the

period before exercise. Due to the larger substance of these plans for top management than

broad-based plans, the effects may only appear with top management plans. However, since

earnings management may manipulate the use of options, the impact on sustained

performance may be limited.

H3 Option plans for top management (3a) and broad-based option plans (3b) have

neutral impact on firm performance on the longer term.

Finally, we can formulate complementarity hypotheses.

H4a Profit sharing plans in combination with share plans are positively associated with firm

performance on the short and longer term.

H4b Profit sharing plans in combination with option plans are positive associated with firm

performance on the short and longer term.

3. Research method

3.1 Sample

In order to test the hypotheses, we used a sample of 2216 observations over an eighteen-

year period for 195 non-financial companies that were publicly listed on the Euronext

Amsterdam Stock Exchange for the period of 1992 – 2009 [accounting years). We excluded

the financial firms because the performance information of financial firms may bias the

results as a consequence of the unique nature of performance measurement in this sector.

8

Our sample is composed of publicly traded firms operating in a variety of different

industries, including 34 different two-digit standard industrial classification (SIC) codes.

To collect the data, we used different sources. First, data on general firm information

and information about firm performance were collected from Amadeus and REACH. The

Amadeus database contains financial information on over 11 million public and private

companies in 41 European countries. REACH (Review and Analysis of Companies in Holland)

a comprehensive database of approximately the 5.000 most important Dutch companies

including financial, historical and marketing data.

Second, data on several forms of financial participation reports were collected from

Company.info. Company.info is a database that contains comprehensive information about

more than 2 million public Dutch firms. Two independent raters with a background in

business administration and economics used content analysis to code the information

disclosed per firm per year in predefined coding categories. For each company they assessed

per year whether the company used the narrow or broad-based financial share plans, profit

sharing and/or option plans. Finally, the data on general firm information and firm

performance and firms’ use of the different types of financial participation plans was merged

yielding a complete data set.

Table 1 presents descriptive statistics. Panel A shows the distribution of sample firms

across industry and size, while Panel B presents that distribution across year and industry. In

Panel A and B we clustered the sample firms in 5 maind industry groups (SIC codes):

Manufacturing (20-39), Trade (50-59), Services excluding ICT ( 40-49, 70-79 excl. 72-73), ICT

(72-73) and Mining (10-17).1 Among these industry groups manufacturing is well

represented with 1025 observations (55%), trade with 335 observations (18%) and services

with 298 observations (16%). ICT has 197 observations (11%), while mining represents two

companies (1%).

[Insert Table 1]

3.2 Variable measurement

3.2.1 Dependent variables

1 Our sample is composed of publicly traded firms operating in a variety of different industries, including 34

different two-digit standard industrial classification (SIC) codes,. However, because for 5 industries we had less than ten observations, we reclassified our sample in these five main groups.

9

To measure firm financial performance we used six different measures of performance that

we classified in three groups: accounting-based, accounting and market-based, and market-

based measures. The accounting-based performance measures Return on equity (ROE) and

Return on assets (ROA) were based on the information disclosed in a company’s (annual)

financial report. The accounting and market-based performance indicators Earnings per

share (Eps) and Shareholders’equity per share (Seps) were calculated using information

disclosed in a company’s financial statements and information on the number of outstanding

shares. Finally, the market-based performance indicators Dividend Yield and Exchange rate

per AEX point reflected a firm’s performance on the stock market. The dividend yield

indicates how high the dividend per share price is, while the exchange rate per AEX-point

indicates the outperformance of the share compared to the AEX index. Please note that

these performance indictors measured different aspects of firm performance. For example,

dividend payments are usually because relatively stable, while share price fluctuate more.

An increase in a firm’s stock exchange price leads to an increase in the exchange rate per

AEX point, but to decreases of the dividend yield, ceteris paribus. Table 2 provides an

overview of the performance indicators.

3.2.1 Independent variables

To assess companies’ use of the different forms of financial participation plans we used

dummy variables. Two independent raters with a background in business administration and

economics used content analysis to code the information disclosed per firm per year. Using

data from Company.info, the raters read the entire contents of the corporate annual reports

to assess whether a company used share plans, profits sharing plans and/or stock option

plans for each year that the company was stock exchange listed. In addition, they assessed

whether these financial plans were narrow-based (top management only) or broad-based

(financial participation plans for management and employees). During these content

analyses some judgment was exercised. To control for subjectivity, in the event of

differences in judgment between the raters, the best interpretation was discussed in a

meeting of the raters and the authors of this paper.

10

Table 1, Panel C presents the distribution of the sample firms across industry and use

of share plans, profit sharing plans and/or stock option plans. As far as the data were

available, 17%, 14% and 65% of the sample firms used respectively share, profit sharing and

option plans. In addition, Panel C shows whether these financial participation plans used

were narrow- or broad-based. Respectively 8%, 2% and 45% of the firms used narrow-based

share, profit sharing and option plans, while respectively 9%, 12% and 21% of the firms used

broad-based share, profit sharing and option plans.

Data on share plans were collected with a one-year lag effect because share plans

have a longer term effect on firm performance relatively to profit sharing plans. As a

consequence of institutional constraints (tax regulation), options plans have the relatively

longest term impact on firm performance. Data on option plans were collected with a four-

year lag effect. For robustness reasons we also examined the relationships between firm

performance and profit share plans with a one-year lag, share plans with a two-year lag, and

option plans with a three-year and five-year lag. Additional analysis showed that the results

were qualitatively similar when using different time lags for the different forms of financial

participation. We reports the results with profit-sharing plans with no time lag, share plans

with one-year lag and option plans with a four-year lag.

3.2.1 Control variables

We included company size and year dummies, and firm fixed effects as control

variables. The natural logarithm of total assets was included to proxy for the size of the

company. The year dummies were included to control for omitted variables that vary over

time but are constant between the firms. Finally the fixed firm effects were included to

control for omitted variables that differ between the firms but are constant over time. When

the results the Hausman test showed that we could use random effects estimators, we also

included a time-invariant vector of industry dummies to control for industry effects on

company performance.

3.3 Analysis

11

Our hypotheses were tested using panel data regression techniques with Stata 10. Panel

data regression techniques have the advantage to incorporate both the cross-sectional

information reflected in the differences between the firms, and information in the time-

series or within-subject information reflected in the changes within the firms over time

(Wooldridge, 2002). As a consequence, panel data analysis makes it possible to control for

some types of omitted variables, i.e. firm fixed and year effects.

To test our hypotheses, we estimated the following general panel data model:

PERFi,j,t = β0 + β2 STMi,t + β3 SBBi,t + β4 PSTMi,t + β5 PSBBi,t + β6 OTMi,t + β7 OBBi,t

+ β81 STMi,t * PSTMi,t + β82 PSTMi,t * OTMi,t + β83 STMi,t * OTMi,t + β84 STMi,t * PSTMi,t * OTMi,t

+ β91 SBBi,t * PSBBi,t + β92 PSBBi,t * OBBi,t + β93 SBBi,t * OBBi,t + β94 SBBi,t * PSBBi,t * OBBi,t

+ β10 LNTAi,t + β11 FFEi + β12 YEARt + εt

where,

PERFi,j,t = performance of firm i in year t measured by performance indictor j;

with j = Return on equity (ROE); Return on assets (ROA); Earnings per share (Eps); Shareholders’equity per share (Seps); Dividend Yield (DY); Exchange rate per AEX point (EXPAEX).

STMi,t = dummy variable coded as 1 if firm i has narrow-based (top management only) share plans in year t and 0 otherwise;

SBBi,t = dummy variable coded as 1 if firm i has broad-based share plans in year t and 0 otherwise;

PSTMi,t = dummy variable coded as 1 if firm i has narrow-based (top management only) profit sharing plans in year t and 0 otherwise;

PSBBi,t = dummy variable coded as 1 if firm i has broad-based profit sharing plans in year t and 0 otherwise;

OTMi,t = dummy variable coded as 1 if firm i has narrow-based (top management only) option plans in year t and 0 otherwise;

OBBi,t = dummy variable coded as 1 if firm i has broad-based option plans in year t and 0 otherwise;

LNTAi,t = company size measured by its natural logarithm of total assets of firm i in year t;

FFEi = fixed effect of firm i.

YEAR = a vector of year dummies.

12

We applied a Hausman test to test whether the random effects estimators were

unbiased. The results of this test showed that when using our dependent variables EPS, SEPS

and Expaex we had to use fixed effect estimators, while random effects estimators could be

used for ROE, ROA and DY. If random effects are present, then the random effects estimator

is preferred for its greater precision. In addition, the random effects estimator permits to

estimate the effects of time-invariant variables. For this reason, we included a vector

industry dummies when using random effects estimators.

13

4. Results

Table 2 reports the results of the regression analyses for the hypothesized

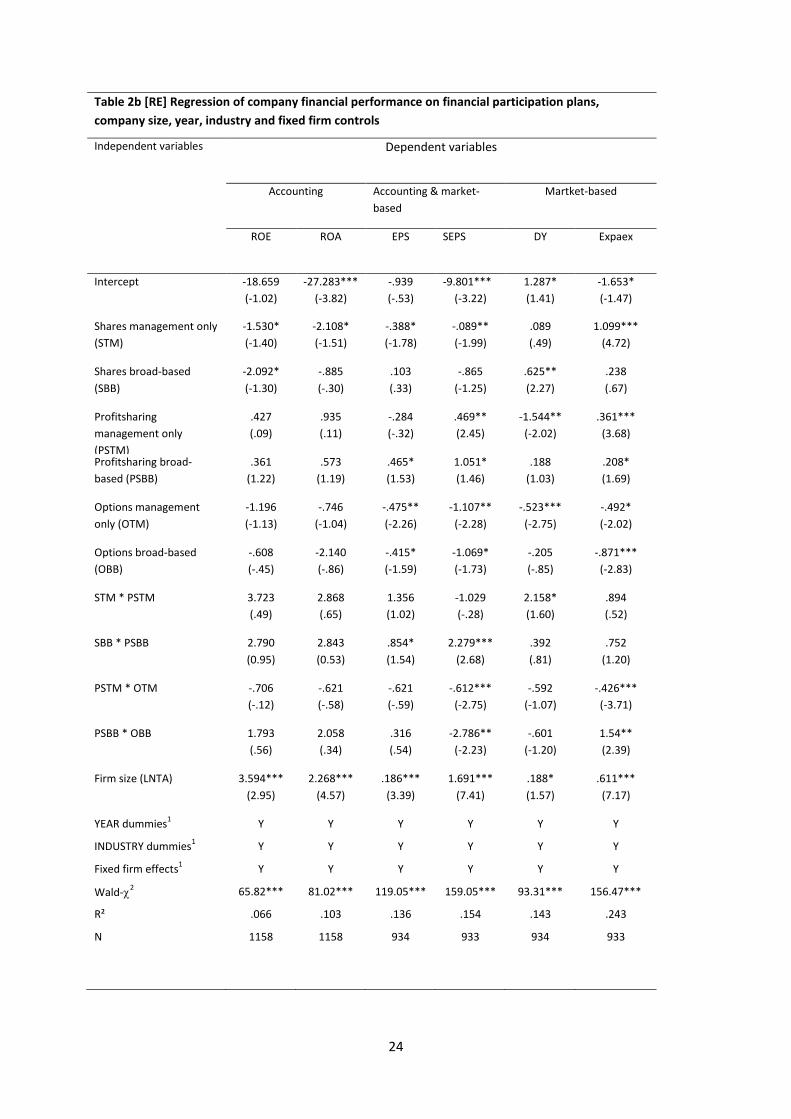

relationships between share, profit sharing and option plans, the combinations of profit

sharing plans and share or option plans, and firm performance.

[Insert Table 2]

H1 predicts a positive longer term relationship between share plans for top

management (1a) and broad-based share plans (1b) and firm performance. Table 2 showed

that the relationships between share plans for top management and company performance

were mixed. The results showed a positive association between narrow-based share plans

and firm performance when the performance was measured with market-based measures

Dividend yield and Exchange rate per AEX point. The coefficients which estimated the

difference between expected performance for firms with and without share plans for top

management once variation in performance related to profit sharing and option plans, firm

size, period and fixed firm effects, or industry and random firm effects had been partialed

out showed that share plans for top management were positively and significantly

associated with Exchange rate per AEX point (β = 1.06, p.<0.01), while its association with

Dividend yield was also positive but not significant. These finding suggest that firms with

narrow-based share plans perform on average significantly better on the stock market than

firms without narrow-based share plans, controlling for all other factors specified in the

model. However, contrary to the expectation, share plans for top management were

significantly negatively related to Shareholders’ equity per share (β = .05, p.<0.10), whereas

its associations with ROE, ROA and Earnings per share were also negative but not significant.

In addition, broad-based share plans were positively related to firm performance

when the performance was measured using the measures Earnings per share, Dividend yield

and Exchange rate per AEX point. The positive association with Dividend yield was significant

(β = 0.62, p.<0.05), while the positive relationships between broad-based employee share

plans and Earnings per share and Exchange rate per AEX point were not significant. Contrary

to the expectations, broad-based share plans were marginally significantly negatively related

to ROE (β = -2.09, p.<0.10), while its association with ROA and Shareholders’ equity per

share were also negative but not significant. Together these results show partial support for

14

H1 suggesting a positive longer term relationship between narrow- and broad-based share

plans and market-based firm performance.

H2 predicts a short term positive relationship between profit sharing plans for top

management (2a) and broad-based profit sharing plans (2b) and firm performance. The

results showed that profit sharing plans for top management were significantly positively

related to Shareholders’ equity per share (β = .55, p.<0.01) and Exchange rate per AEX point

(β = .42, p.<0.01), while its association with ROE and ROA were also positive but not

significant. However, contrary to the expectation, these narrow-based financial participation

plans were negatively related to Earnings per share and Dividend Yield, whereas its

association with Dividend Yield was also significant (β = -1.54, p.<0.05). These findings lead

to rejection of H2a.

Broad-based profit sharing plans were consistently positively related to firm

performance. The associations with Earnings per share (β = .85, p.<0.05), Shareholders’

equity per share (β = .98, p.<0.10) and Exchange rate per AEX point (β = .10,p.<0.01) were

significant, while the relationships with ROE, ROA and Dividend Yield were also positive but

not significant. These findings suggest that, when the other independent variables in the

equations are controlled for, firms with broad-based profit sharing plans on average have a

better short-term performance than firms that do not have these profit sharing plans. It

provides support for H2b suggesting that broad-based profit sharing plans positively

influence company performance.

H3 predicts a neutral impact of option plans for top management (3a) and broad-

based option plans (3b) on firm performance on the longer term. In spite of the fact that we

expected neutral relationships between narrow- and broad-based options plans and firm

performance, our findings consistently showed negative associations between narrow- and

broad-based options plans and the accounting- and market-based firm measures of firm

performance. Option plans for top management were significantly negatively related to

Earnings per share (β = -.38, p.<0.10), Shareholders’ equity per share (β = -.70, p.<0.10) and

Dividend Yield (β = -.53, p.<0.01), while the negative relationship between these narrow-

based participation plans and ROE, ROA and Exchange rate per AEX point were not

significant. Broad-based option plans were significantly negatively associated with Earnings

per share (β = -.70, p.<0.05), Shareholders’ equity per share (β = -.85, p.<0.10) and Exchange

rate per AEX point (β = -.99, p.<0.01). The relationships between broad-based option plans

15

and ROE, ROA and Dividend yield were also negative but not significant. Contrary to our

expectations, these findings thus consistently show negative associations suggesting that

both the option plans for top management and the broad-based option plans have a

negative impact on firm performance on the longer term. As a consequence, we have to

reject H3a and H3b.

Finally, to test whether the existence of these combinations of plans may have

synergic impacts on performance since one type of plan may compensate for disadvantages

of the other plan, H4 predicts that profit sharing plans in combination with narrow- and

broad-based share plans (4a) or option plans (4b) are positively associated with firm

performance on the short and longer term. Table 2 shows the results to test whether the

existence of these combinations of plans may have synergic impacts on performance since

one type of plan may compensate for disadvantages of the other plan. The findings in Table

2 show that profit sharing plans in combination with share plans for top management were

significantly positively associated with Dividend yield (β = 2.158, p.<0.10). At the same time,

the interaction effects of these combinations of narrow-based participation plans are

positively but not significantly related to ROE, ROA, Earnings per share and Exchange rate

per AEX point. However, the interaction effect of profit sharing and share plans for top

management on Shareholders’ equity per share was negatively but relatively small and not

significant. In addition, the results consistently show positive relationships between broad-

based profit sharing plans in combination with share plans and firm performance. The

positive association with Earnings per share (β = 1.03, p.<0.10) and Exchange rate per AEX

point (β = 2.86, p.<0.05) were also significant. These findings suggest that the subset of firm

having both broad-based profit sharing and share plans on average perform better than

firms that do not have these plans, while controlling for all other factors specified in the

model. Together these results provide support for H4a. It suggests that the combinations of

narrow- and broad-based profit sharing and share plans have a positive short and longer

term effect on firm performance.

Finally, table 2 shows the results to test hypothesis H4b, which predicts a positive

association between profit sharing plans in combination with option plans and firm

performance on the short and longer term. Contrary to the expectations, the interaction

effects of the narrow-based combinations of profit sharing and option plans on firm

16

performance were consistently negative. The negative associations between the

combinations of profit sharing and option plans for top management and Shareholders’

equity per share (β = -63, p.<0.05) and Exchange rate per AEX point (β = -.49, p.<0.01) were

also significant.

The relationships between broad-based combinations of profit sharing and option

plans and firm performance were inconsistent. The interaction effect of the combination of

broad-based profit sharing and option plans on Exchange rate per AEX point was positive

and significant (β = 1.83, p.<0.01). However, the interaction effect of the combination of

broad-based profit sharing and option plans on shareholders’ equity per share was

significant but negative (β = -2.47, p.<0.05). The relationships between the combination of

broad-based profit sharing and option plans and ROA, ROA, Earnings per share and Dividend

Yield were not significant.

These findings suggest that narrow-based combinations of profit sharing and option

plans have a negative impact on firm performance on the short and longer term relative to

firms that do not have profit sharing and option plans for top management, while the broad-

based combinations of profit sharing and option plans do not have differential effects on

firm performance. Together these findings lead to the rejection of H4b.

In sum, the results support H2b and H4a and provide partial support for H1. These

findings suggest that broad-based profit sharing and share plans and combinations of these

plans positively affect firm performance relative to firms that do not have these financial

participation plans. Narrow-based share plans and combinations of profit sharing and share

plans for top management positively affect market-based firm performance relative to firms

that do not have these financial participation plans.

5. Conclusion and discussion

This paper assessed the relationship between financial participation and firm

performance using a longitudinal panel of companies with narrow and broad-based financial

participation plans (profit sharing, share plans and option plans). The results show that when

firm, period, size and industry effects are controlled for, in comparison with companies with

no plan, broad-based profit sharing and share plans show systematically significant higher

17

positive relationships with many performance indicators than narrow-based plans. In

addition, both the option plans for top management and the broad-based option plans are

negatively related with firm performance in comparison with companies with no plan.

However, broad-based option plans in combination with broad-based profit sharing plans

have the opposite effect on firm performance, suggesting synergic impacts since one type of

plan may compensate for disadvantages of the other plan.

References

GB: include Bartov and Mohanram, 2004 Blair, M.(1995). Ownership and Control: Rethinking corporate governance for the twenty-first century,

Washington DC: Brookings Institution. Blasi, Joseph and Douglas L. Kruse, 1996, “Employee stock ownership and corporate performance

among public companies”, Industrial & Labor Relations Review, 50, 1; pp. 60-80. Blasi, Joseph, Douglas Kruse, James Sesil, Maya Kroumova, and Ed Carberry. 2000. Stock Options,

Corporate Performance and Organizational Change. Oakland, Ca.: National Center for Employee Ownership. (www.nceo.org/library/optionreport.html )

Conte, M. and Svenjar 1990. ‘The performance effects of employee ownership plans’ In Blinder, A. Paying for Productivity: a Look at the Evidence. Washington DC: Brookings Institution.

Conyon Martin J. and Richard B. Freeman, 2001, “Shared modes of compensation and firm performance: UK evidence”, NBER working paper series.

Doucouliagos, C., 1995, “Worker participation and productivity in labor-managed and participatory capitalist firms: A meta-analysis”, Industrial and Labor Relations Review, 49, 1, pp 58-78.

Estrin, Saul, Paul Grout and Sushil Wadhwani, 1987, “Profit sharing and employee share ownership”, Economic Policy, April, pp.13-62.

Estrin, Saul and Derek C. Jones, 1995, “Worker participation, employee ownership, and productivity: Results from French producer co-operatives”, Advances in the Economic Analysis of Participatory and Labor-Managed Firms, vol 5, pp 3-24.

Estrin, Saul, Derek C. Jones and Jan Svejnar, 1987, “The productivity effects of worker participation: Producer cooperatives in Western Economies,” Journal of Comparative Economics, 11(1), March, pp. 40-61.

Fakhfakh Fathi, 1998, “Sharing schemes and productivity: An empirical analysis based on large French firms using production functions and frontiers”, Advances in the Economic Analysis of Participatory and Labor-Managed Firms, vol 6, pp115-134.

Fakhfakh Fathi and Virginie Pérotin, 2000, “The effects of profit-sharing schemes on enterprise performance in France”, Economic Analysis, 3, 2, pp 93 - 111.

Hall, Brian and Kevin. Murphy, 2002, Stock options for undiversified executives,Journal of Accounting and Economics,

Jones, Derek C. and Takao Kato, 1995, “The productivity effects of employee stock ownership plans and bonuses: Evidence from Japanese panel data”, American Economic Review, 85, 3, pp. 391-414.

18

Jones, Derek C. and Takao Kato, 1993, “On the scope, nature and effects of employee ownership in Japan”, Industrial and Labor Relations Review, 46, pp. 352-367.

Kaarsemaker, E. (2006). Employee Ownership and Human resource Management. A Theoretical and Empirical Treatise with a Digression on the Dutch Context. Doctoral Dissertation, Radboud University: Nijmegen

Kaarsemaker, E., and Poutsma, E. (2006) ‘The Fit of Employee Ownership With Other Human Resource Management Practices: Theoretical and Empirical Suggestions Regarding the Existence of an Ownership High-Performance Work System, or Theory O’. Economic and Industrial Democracy. 27(2) 669-685.

Klein, K. (1987). ‘Employee stock ownership and employee attitudes: a test of three models.’ Journal of Applied Psychology, 72(2), 319-332.

Kruse, 1991 “Profit sharing and employment variability: Microeconomic evidence on the Weitzman theory”, Industrial and Labor Relations Review, 44, pp 437-453.

Kruse, Douglas L, 1992, “Profit sharing and productivity: Microeconomic evidence from the United States”, Economic Journal, 102, 410, pp 24-36.

Kruse, Douglas L., 1993, Profit Sharing - Does It Make a Difference ? Kalamazoo (Mich, US): W.E. Upjohn Institute for Employment Research.

Kruse, Douglas L. and Joseph Blasi, 1997, “Employee ownership, employee attitudes, and firm performance: A review of the evidence”, in David Lewin, Daniel J.B. Mitchell, and Mahmood A. Zaidi (eds.), The Human Resource Management Handbook, Part 1, JAI Press (Greenwich, CT, US).

Kruse, Douglas L., Richard B. Freeman, and Joseph R. Blasi (Eds) (2010) Shared Capitalism at Work Employee Ownership, Profit and Gain Sharing, and Broad-Based Stock Options. Chicago: University of Chicago Press, 2010

Kruse, Douglas L.,1999, “Economic democracy or just another risk for workers? Reviewing the evidence on employee ownership and profit sharing”, paper presented at the Conference on Democracy, Participation and Economic Development, Columbia University, April.

Kruse, Douglas L., 2002, “Research evidence on prevalence and effects of employee ownership”, paper presented in testimony before the Subcommittee on Employer-Employee Relations, Committee on Education and the Workforce, US House of Representatives, 13 Feb. , http://www.nceo.org/library/kruse_testimony.html.

Lazear, Edward P, 1995, Personnel Economics. Cambridge (MA, US): MIT Press. Lazear, Edward, 2002, Output-based pay: incentives, retention or sorting, Unpublished paper, Hoover

Institution and Graduate School of Business, Stanford University Meihuizen, Hanne E., 2000, “Productivity effects of employee stock ownership and employee stock

option plans in firms listed on the Amsterdam stock exchange: An empirical analysis”, paper presented at the 10th congress of the International Association for the Economics of Participation, Trento (Italy).

OECD, 1995, “Profit Sharing in OECD Countries”, Chapter Four, Employment Outlook, pp. 139 – 169. Pendleton, A. (2001). Employee ownership, participation and governance: a study of ESOPs in the UK.

London and New York: Routledge. Pendleton, A. (2005). ‘Employee share ownership, employment relationships, and corporate

governance’ in Harley, B., Hyman, J. and Thompson, P. (eds.) Participation and Democracy at Work: Essays in Honour of Harvie Ramsay. London: Palgrave.

Pendleton, A. (2006). ‘Incentives, Monitoring, and Employee Stock Ownership Plans: New Evidence and Interpretations.’ Industrial Relations, 45(4): 753–777.

Pendleton, A (2009) ‘Employee participation in employee share ownership: an evaluation of the factors associated with participation and contributions in Save As You Earn plans’, British Journal of Management, forthcoming

Pendleton, Andrew, Erik Poutsma, Chris Brewster and Jos van Ommeren, 2001,Employee Share Ownership and Profit Sharing in the European Union. Dublin:European Foundation for the Improvement of Living and Working Conditions.

19

Pendleton, A., Wilson, N. and Wright, M. (1998). ‘The perception and effects of share ownership: empirical evidence from employee buy-outs.’ British Journal of Industrial Relations, 36(1), 99-123.

Pérotin, V. and Robinson, A. (2003). 'Employee participation in profit and ownership: a review of the issues and evidence'. Luxembourg: European Parliament.

Pierce, Jon L., Stephen A. Rubenfeld, and Susan Morgan. Employee ownership: A conceptual model of process and effects. Academy of Management Review, 1991, 16, 121-144.

Pierce, Jon L., Tatiana Kostova, and Kurt T. Dirks. Toward a theory of psychological ownership in organizations. Academy of Management Review, 2001, 26, 298-310.

Pierce, Jon L., Tatiana Kostova, and Kurt T. Dirks. The state of psychological ownership: Integrating and extending a century of research. Review of General Psychology, 2003, 7, 1, 84-107.

Poole, M. (1989). The origins of economic democracy: profit-sharing and employee-shareholding schemes. London: Routledge.

Poutsma, Erik, 2001, Recent Trends in Employee Financial Particiaption in the European Union. Luxembourg: Office for the Official Publications of the European Communities.

Robinson, A., and Wilson, N. (2006). ‘Employee financial participation and productivity: an empirical reappraisal.’ British Journal of Industrial Relations, 44(1), 31-50.

Sesil, James, Maya Kroumova, Joseph Blasi, and Douglas Kruse, 2002, Broad-based employee stock options in US 'new economy' firms, British Journal of Industrial Relations, 40: 273-294.

Uvalic, Milica. 1991. The PEPPER Report: Promotion of Employee Participation in Profits and Enterprise Results, Supplement 3/91, Social Europe. Luxembourg: Office for Official Publications of the European Communities

Vaughan Whitehead, D. (1995) Workers’ Financial Participation: East-West Experiences. Geneva: International Labour Office.

Wagner, S., Parker, C. and Christiansen, N. (2003). ‘Employees that think and act like owners: effects of ownership beliefs and behaviors on organizational effectiveness.’ Personnel Psychology, 56(4), 847-871.

Wooldridge, J.M. (2002). Econometric analysis of cross section and panel data. The MIT Press, Cambridge, Massachusetts.

20

Table 1 Summary statistics of sample firms (1992-2009)

Panel A: Firm characteristics

Industry

(US SIC codes)

Number of

firms

Company size

No of employees Total assets per employee

n % Mean Std. dev. Mean Std. dev.

Manufacturing (20-39) 1195 53.9 14433 3719 2992514 723544

Trade (50-59) 370 16.7 13852 3681 1913183 471730

Services excluding ICT

(40-49, 70-79 excl. 72-73)

379 17.1 28400 6466 2207348 607616

ICT (72-73) 231 10.4 2878 6268 255568 65429

Mining (10-17) 41 1.9 36059 14478 12583961 7047160

Total 2216 100

Panel B Firms across year and industry

Year

Industry Total

Manufactu

ring

Trade Services

excluding ICT

ICT Mining

1992 75 25 17 6 1 124

1993 75 25 17 6 1 124

1994 75 25 17 6 1 124

1995 75 25 17 6 1 124

1996 75 25 17 6 1 124

1997 94 30 25 17 2 168

1998 89 27 26 16 2 160

1999 60 19 22 15 2 118

2000 61 19 22 15 3 120

2001 61 19 23 15 3 121

2002 61 19 24 16 3 123

2003 60 19 24 16 3 122

2004 60 19 24 16 3 122

2005 62 19 25 16 3 125

2006 59 18 24 16 3 120

2007 52 14 20 15 3 104

2008 51 13 18 14 3 99

2009 50 10 17 14 3 94

Total 1195 370 379 231 41 2216

21

Panel C: Panel C Use of shares, profit sharing and/or stock options across industry

Industry

Financial participation plans

Shares Profit sharing Options Total

0 1 2 0 1 2 0 1 2

Manufacturing 892 175 118 997 21 167 492 492 201 1185

Trade 299 43 26 324 4 40 157 184 27 368

Services excluding ICT 284 54 34 344 10 18 114 205 53 372

ICT 199 16 15 218 0 12 47 53 130 230

Mining 19 4 18 21 10 10 10 19 12 41

Total 1693 292 211 1904 45 247 820 953 423 2196

Explanation 0 = absence of type of financial participation plan. 1= narrow-based financial participation plans (directed to top management and executives only). 2 = broad-based financial participation plan (targeted to all employees).

22

Table 2 Regression of company financial performance on financial participation plans, company size,

year, industry and fixed firm controls

Independent variables Dependent variables

Accounting Accounting & market-

based

Martket-based

ROE ROA EPS SEPS DY Expaex

Intercept -18.659

(-1.02)

-27.283***

(-3.82)

.853

(.40)

-20.834***

(-5.24)

1.287*

(1.41)

-.992

(-.47)

Shares management only

(STM)

-1.530*

(-1.40)

-2.108*

(-1.51)

-.144

(-.60)

-.058*

(-1.30)

.089

(.49)

1.068***

(4.41)

Shares broad-based

(SBB)

-2.092*

(-1.30)

-.885

(-.30)

.234

(.63)

-.760

(-1.08)

.625**

(2.27)

.093

(.25)

Profitsharing

management only

(PSTM)

.427

(.09)

.935

(.11)

-.261

(-.25)

.515**

(2.66)

-1.544**

(-2.02)

.422***

(4.06)

Profitsharing broad-

based (PSBB)

.361

(1.22)

.573

(1.19)

.857**

(2.20)

.938*

(1.29)

.188

(1.03)

.102***

(2.59)

Options management

only (OTM)

-1.196

(-1.13)

-.746

(-1.04)

-.388*

(-1.48)

-.701*

(-1.41)

-.523***

(-2.75)

-.296

(-1.12)

Options broad-based

(OBB)

-.608

(-.45)

-2.140

(-.86)

-.707**

(-2.11)

-.856*

(-1.35)

-.205

(-.85)

-.993***

(-2.93)

STM * PSTM 3.723

(.49)

2.843

(.65)

1.754

(.85)

-.156

(-.04)

2.158*

(1.60)

.303

(.14)

SBB * PSBB 2.790

(0.95)

2.843

(0.53)

1.036*

(1.58)

2.864**

(2.31)

.392

(.81)

.271

(.41)

PSTM * OTM -.706

(-.12)

-.621

(-.58)

-1.210

(-1.02)

-.638**

(-2.85)

-.592

(-1.07)

-.496**

(-4.13)

PSBB * OBB 1.793

(.56)

2.058

(.34)

.214

(.32)

-2.471**

(-1.96)

-.601

(-1.20)

1.83***

(2.71)

Firm size (LNTA) 3.594***

(2.95)

2.268***

(4.57)

.198

(1.13)

2.406***

(8.16)

.188*

(1.57)

.498***

(3.16)

YEAR dummies

1 Y Y Y Y Y Y

INDUSTRY dummies

1 Y Y N N Y N

Fixed firm effects1 Y Y Y Y Y Y

F-statistic 4.22*** 6.81*** 9.73***

Wald-

2 65.82*** 81.02*** 93.31***

R² .066 .103 .104 .157 .143 .187

N 1158 1158 934 933 934 933

23

Table 2a [FE] Regression of company financial performance on financial participation plans,

company size, year and fixed firm controls

Independent variables Dependent variables

Accounting Accounting & market-

based

Martket-based

ROE ROA EPS SEPS DY Expaex

Intercept 10.306

(.10)

-29.577**

(-4.26)

.853

(.40)

-20.834***

(-5.24)

2.486*

(1.51)

-.992

(-.47)

Shares management

only (STM)

-1.365

(-1.14)

-.813

(-.35)

-.144

(-.60)

-.058*

(-1.30)

.121

(.65)

1.068***

(4.41)

Shares broad-based

(SBB)

-2.867*

(-1.53)

-1.414

(-.39)

.234

(.63)

-.760

(-1.08)

.476*

(1.64)

.093

(.25)

Profitsharing

management only

(PSTM)

.219

(.15)

1.086

(.09)

-.261

(-.25)

.515**

(2.66)

-

1.491**

(-1.86)

.422***

(4.06)

Profitsharing broad-

based (PSBB)

.333

(1.15)

1.501

(.04)

.857**

(2.20)

.938*

(1.29)

.095

(.29)

.102***

(2.59)

Options management

only (OTM)

-1.206

(-.95)

-1.095

(-.44)

-.388*

(-1.48)

-.701*

(-1.41)

-

.429***

(-2.10)

-.296

(-1.12)

Options broad-based

(OBB)

-1.555

(-.92)

-3.573

(-1.09)

-.707**

(-2.11)

-.856*

(-1.35)

-.256

(-.98)

-.993***

(-2.93)

STM * PSTM 4.004

(.34)

3.859

(.17)

1.754

(.85)

-.156

(-.04)

2.220*

(1.37)

.303

(.14)

SBB * PSBB 3.369

(0.98)

2.624

(0.39)

1.036*

(1.58)

2.864**

(2.31)

.350

(.68)

.271

(.41)

PSTM * OTM -.210

(-.12)

-2.259

(-.17)

-1.210

(-1.02)

-.638**

(-2.85)

-.249

(-.27)

-.496**

(-4.13)

PSBB * OBB 4.059

(1.12)

3.097

(1.01)

.214

(.32)

-2.471**

(-1.96)

-.273

(-.52)

1.83***

(2.71)

Firm size (LNTA) 1.565

(1.09)

2.809***

(4.45)

.198

(1.13)

2.406***

(8.16)

.106

(.87)

.498***

(3.16)

YEAR dummies

1 Y Y Y Y Y Y

Fixed firm effects1 Y Y Y Y Y Y

F-statistic 2.45*** 3.03*** 4.22*** 6.81*** 2.94*** 9.73***

R² .068 .067 .104 .157 .106 .187

N 1158 1158 934 933 934 933

24

Table 2b [RE] Regression of company financial performance on financial participation plans,

company size, year, industry and fixed firm controls

Independent variables Dependent variables

Accounting Accounting & market-

based

Martket-based

ROE ROA EPS SEPS DY Expaex

Intercept -18.659

(-1.02)

-27.283***

(-3.82)

-.939

(-.53)

-9.801***

(-3.22)

1.287*

(1.41)

-1.653*

(-1.47)

Shares management only

(STM)

-1.530*

(-1.40)

-2.108*

(-1.51)

-.388*

(-1.78)

-.089**

(-1.99)

.089

(.49)

1.099***

(4.72)

Shares broad-based

(SBB)

-2.092*

(-1.30)

-.885

(-.30)

.103

(.33)

-.865

(-1.25)

.625**

(2.27)

.238

(.67)

Profitsharing

management only

(PSTM)

.427

(.09)

.935

(.11)

-.284

(-.32)

.469**

(2.45)

-1.544**

(-2.02)

.361***

(3.68)

Profitsharing broad-

based (PSBB)

.361

(1.22)

.573

(1.19)

.465*

(1.53)

1.051*

(1.46)

.188

(1.03)

.208*

(1.69)

Options management

only (OTM)

-1.196

(-1.13)

-.746

(-1.04)

-.475**

(-2.26)

-1.107**

(-2.28)

-.523***

(-2.75)

-.492*

(-2.02)

Options broad-based

(OBB)

-.608

(-.45)

-2.140

(-.86)

-.415*

(-1.59)

-1.069*

(-1.73)

-.205

(-.85)

-.871***

(-2.83)

STM * PSTM 3.723

(.49)

2.868

(.65)

1.356

(1.02)

-1.029

(-.28)

2.158*

(1.60)

.894

(.52)

SBB * PSBB 2.790

(0.95)

2.843

(0.53)

.854*

(1.54)

2.279***

(2.68)

.392

(.81)

.752

(1.20)

PSTM * OTM -.706

(-.12)

-.621

(-.58)

-.621

(-.59)

-.612***

(-2.75)

-.592

(-1.07)

-.426***

(-3.71)

PSBB * OBB 1.793

(.56)

2.058

(.34)

.316

(.54)

-2.786**

(-2.23)

-.601

(-1.20)

1.54**

(2.39)

Firm size (LNTA) 3.594***

(2.95)

2.268***

(4.57)

.186***

(3.39)

1.691***

(7.41)

.188*

(1.57)

.611***

(7.17)

YEAR dummies

1 Y Y Y Y Y Y

INDUSTRY dummies1 Y Y Y Y Y Y

Fixed firm effects1 Y Y Y Y Y Y

256.47*** Wald-

2 65.82*** 81.02*** 119.05*** 159.05*** 93.31*** 156.47***

R² .066 .103 .136 .154 .143 .243

N 1158 1158 934 933 934 933

25

***, ** and * indicate statistical significance at the 1 percent, 5 percent, and 10 percent levels respectively (t-

values in parentheses). H1 and H2 are tested one-tailed; H3 and H4 are tested two-tailed.

Explanation of the variables

Dependent variables: ROE = Return on equity; ROA = return on total assets; Eps= earnings per share; Seps =

Shareholders’equity per share; Dy = dividend yield; Expaex = exchange rate per AEX point.

Independent variables: STM = dummy variable coded as 1 if firm has narrow-based (top management only)

share plans and 0 otherwise; SBB = dummy variable coded as 1 if firm has broad-based share plans and 0

otherwise; PSTM = dummy variable coded as 1 if firm has narrow-based (top management only) profit sharing

plans and 0 otherwise; PSBB = dummy variable coded as 1 if firm has broad-based profit sharing plans and 0

otherwise; OTM = dummy variable coded as 1 if firm has narrow-based (top management only) option plans and

0 otherwise; OBB = dummy variable coded as 1 if firm has broad-based option plans and 0 otherwise; LNTA =

company size measured by firm’s natural logarithm of total assets; YEAR = a vector of year dummies.

INDUSTRY = a vector of industry dummies based on the Standard Industrial Classification System two-digit

code for industry sector; FFE = firm fixed effect.

1 Results on the year dummies, two-digit industry dummies and fixed firm effects are not reported for

parsimony.

Related Documents