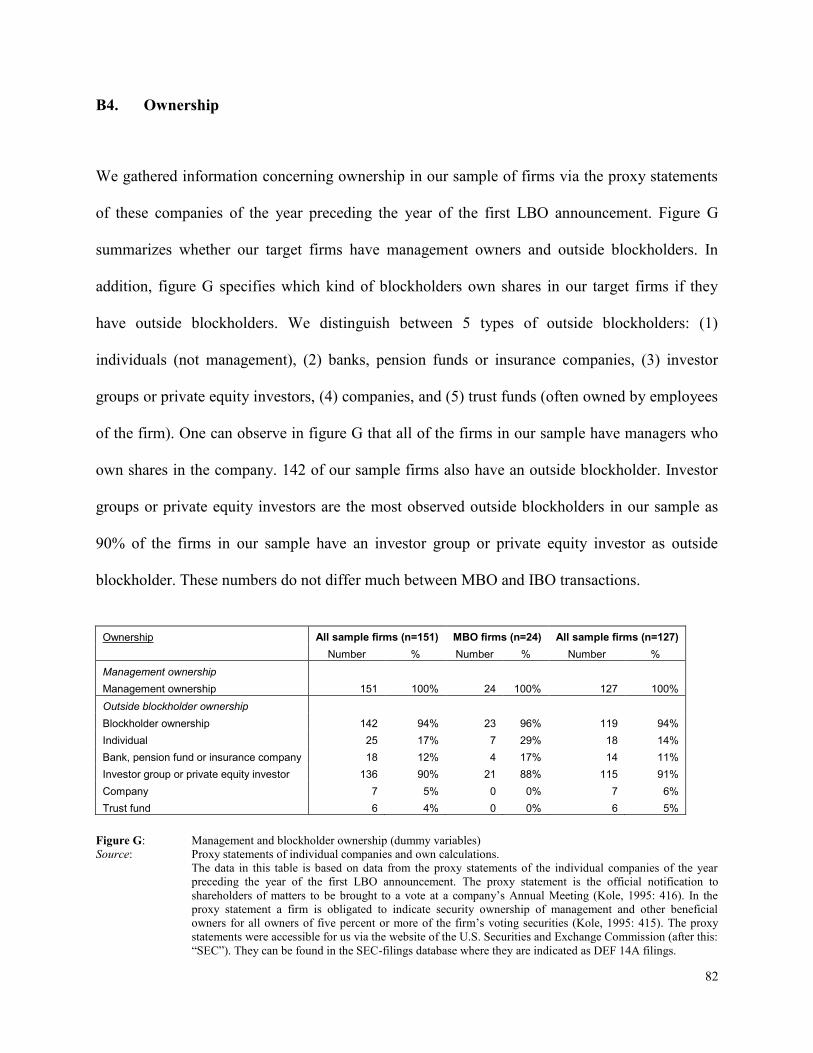

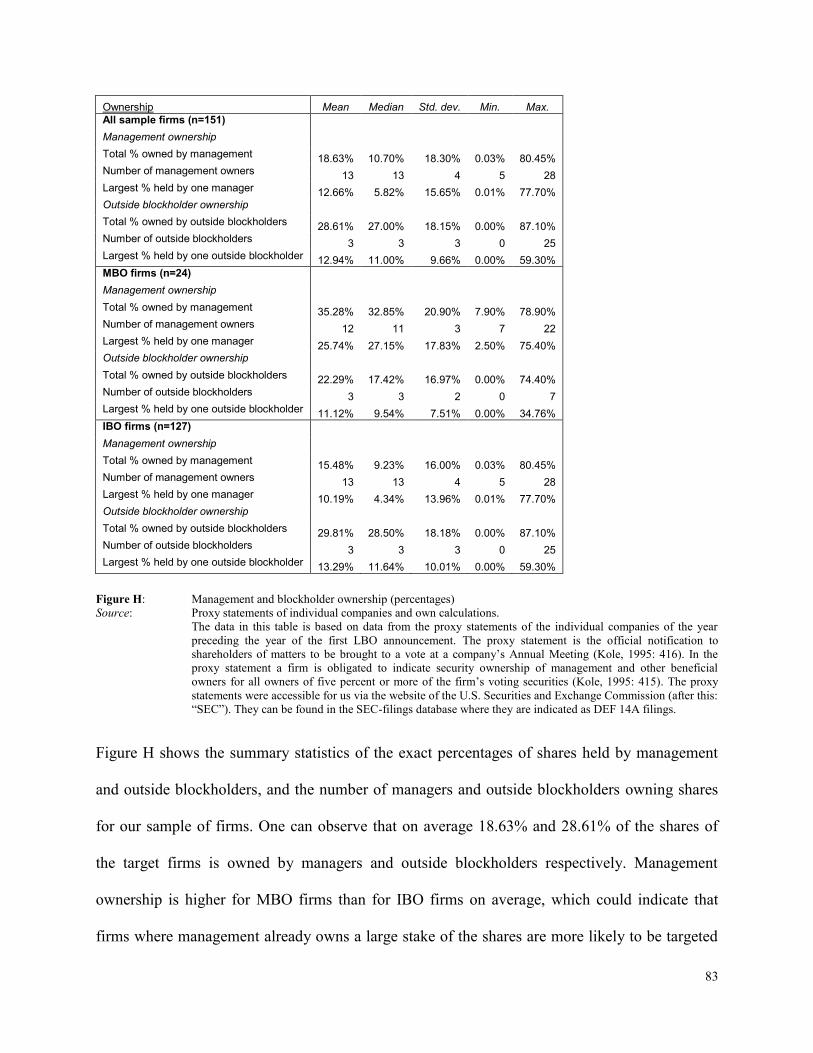

1 The relationship between financial flexibility and firm value: Examined via an event study methodology considering LBO announcements Master Thesis Financial Management Ron de Vaan MSc. University of Tilburg

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

The relationship between financial

flexibility and firm value:

Examined via an event study methodology considering LBO

announcements

Master Thesis Financial Management

Ron de Vaan MSc.

University of Tilburg

2

Title: The relationship between financial flexibility and firm value

Subtitle: Examined via an event study methodology considering LBO announcements

Date of graduation: 2011, February 22

Name of graduation department: Department of Finance

Faculty name: Faculty of Economics and Business administration

Student: Ron de Vaan MSc.

Student number: s374591

Supervisor: Dr. M.R.R. van Bremen

Number of words: 15.645 (excluding figures and appendices)

3

To Lambert and Ad

4

Table of contents (Paper)

Acknowledgements ....................................................................................................................... 6

Abstract ............................................................................................................................ 8

Introduction ............................................................................................................................ 9

Chapter 1 Theory .............................................................................................................. 16

§1.1 The relationship between financial flexibility and firm value ............................... 16

§1.2 The relationship between financial distress costs and firm value .......................... 17

§1.3 The opportunity costs of financial distress .............................................................. 20

Chapter 2 Methodology .................................................................................................... 23

§2.1 Research design .......................................................................................................... 23

§2.2 Hypotheses .................................................................................................................. 28

§2.2.1 The investment opportunity magnitude hypothesis ...................................................... 28

§2.2.2 The cash flow volatility hypothesis .............................................................................. 31

§2.3 Data ............................................................................................................................. 33

§2.3.1 Sample selection and data sources .............................................................................. 33

§2.3.2 Descriptive statistics .................................................................................................... 37

§2.4 Empirical techniques ................................................................................................. 41

§2.4.1 Event study ................................................................................................................... 41

§2.4.2 Cross-sectional regression analysis ............................................................................. 43

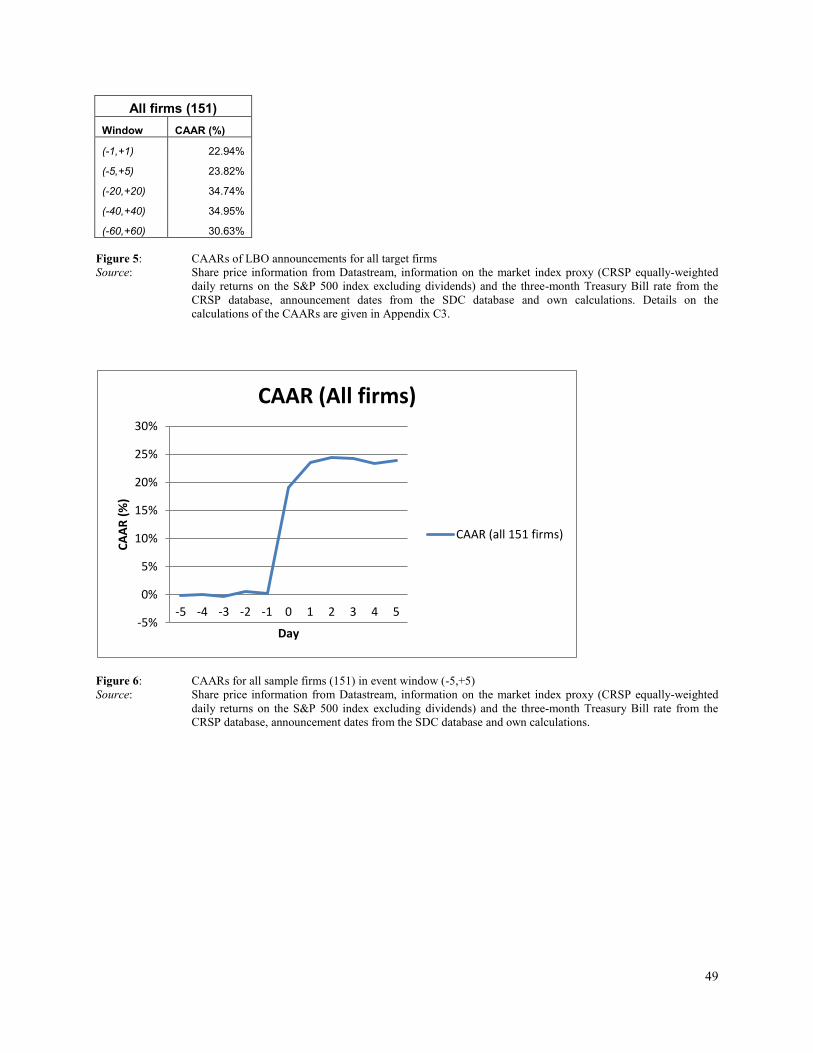

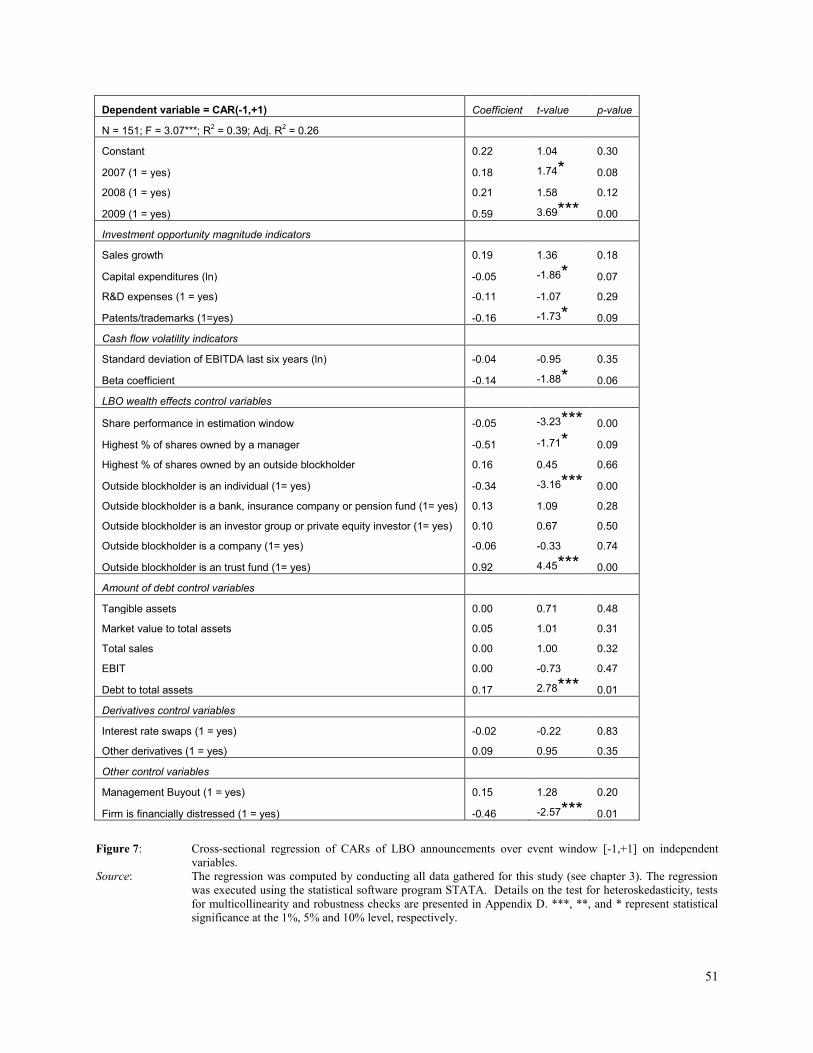

Chapter 3 Results .............................................................................................................. 48

§3.1 Event study ................................................................................................................. 48

§3.2 Cross-sectional regression analysis........................................................................... 50

Chapter 4 Discussion ........................................................................................................ 54

§4.1 The investment opportunity magnitude hypothesis ................................................ 55

§4.2 The cash flow volatility hypothesis ........................................................................... 58

§4.3 Other interesting results ............................................................................................ 60

Chapter 5 Conclusion ....................................................................................................... 62

References .......................................................................................................................... 64

5

Table of contents (Appendices)

Appendix A Theoretical background ................................................................................. 69

A1. The different sources of funds to finance investments ............................................ 69

A2. Perfectly competitive and efficient markets ............................................................ 70

A3. Factors explaining leverage ....................................................................................... 71

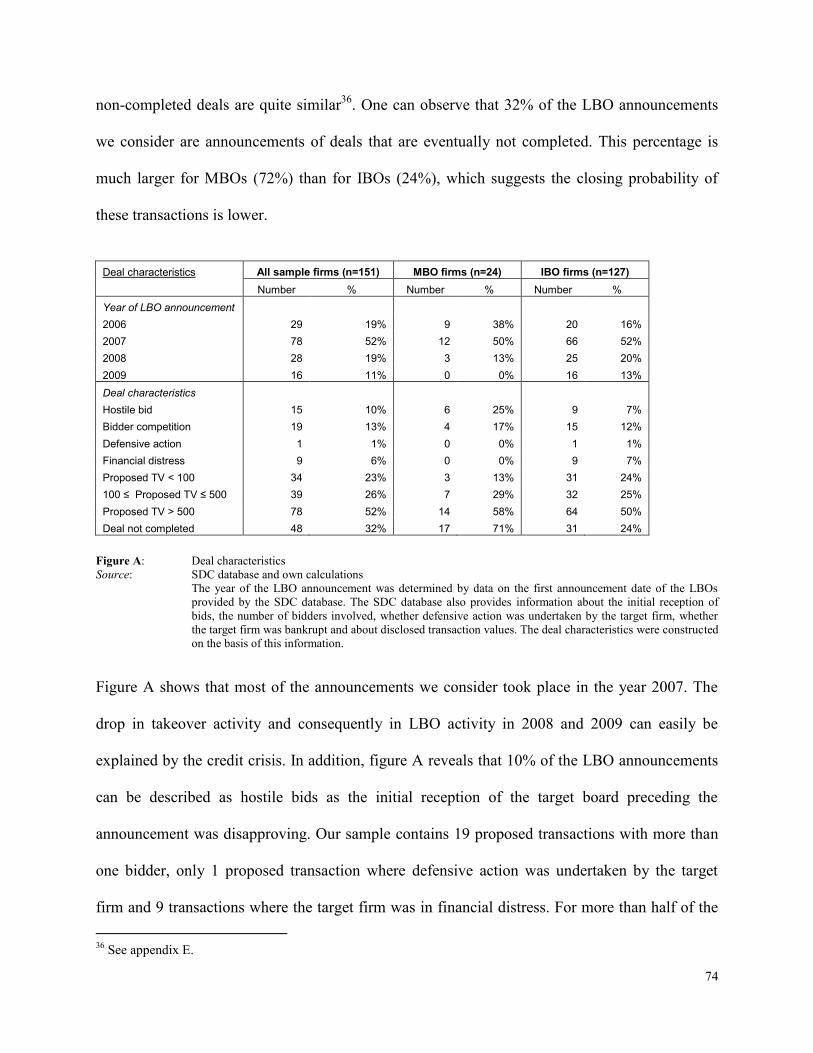

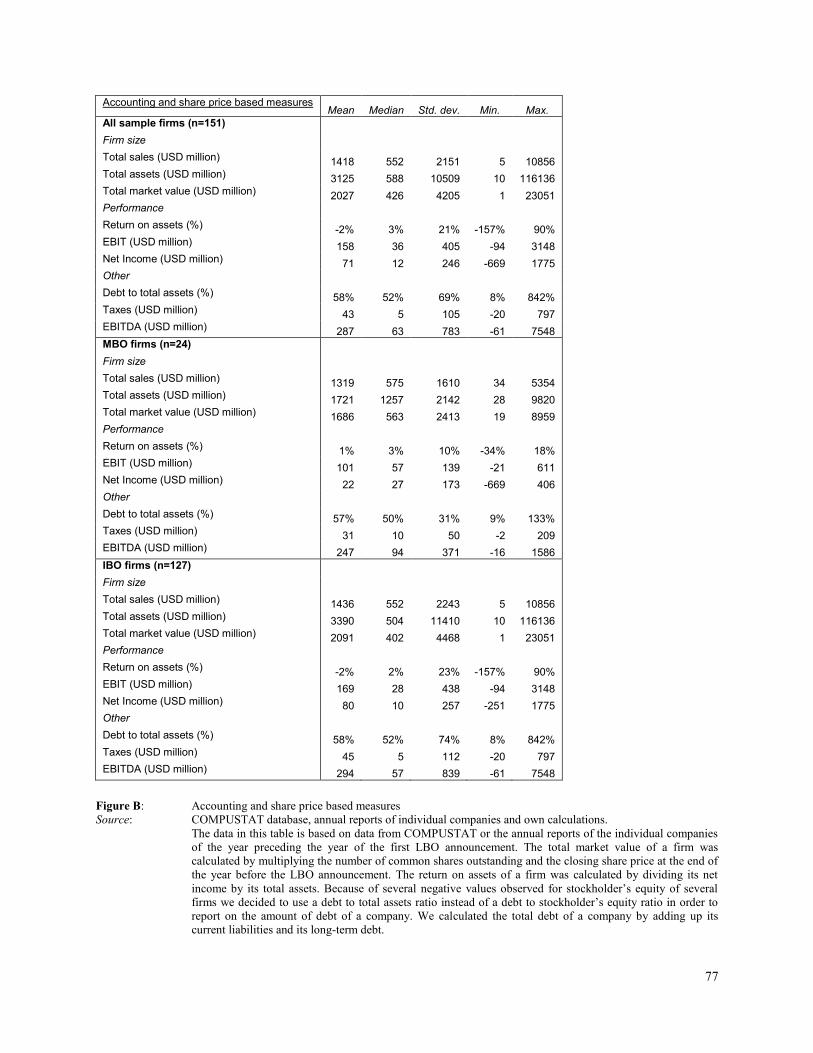

Appendix B Elaborate descriptive statistics ...................................................................... 73

B1. Deal characteristics .................................................................................................... 73

B2. Accounting and share price based measures ........................................................... 76

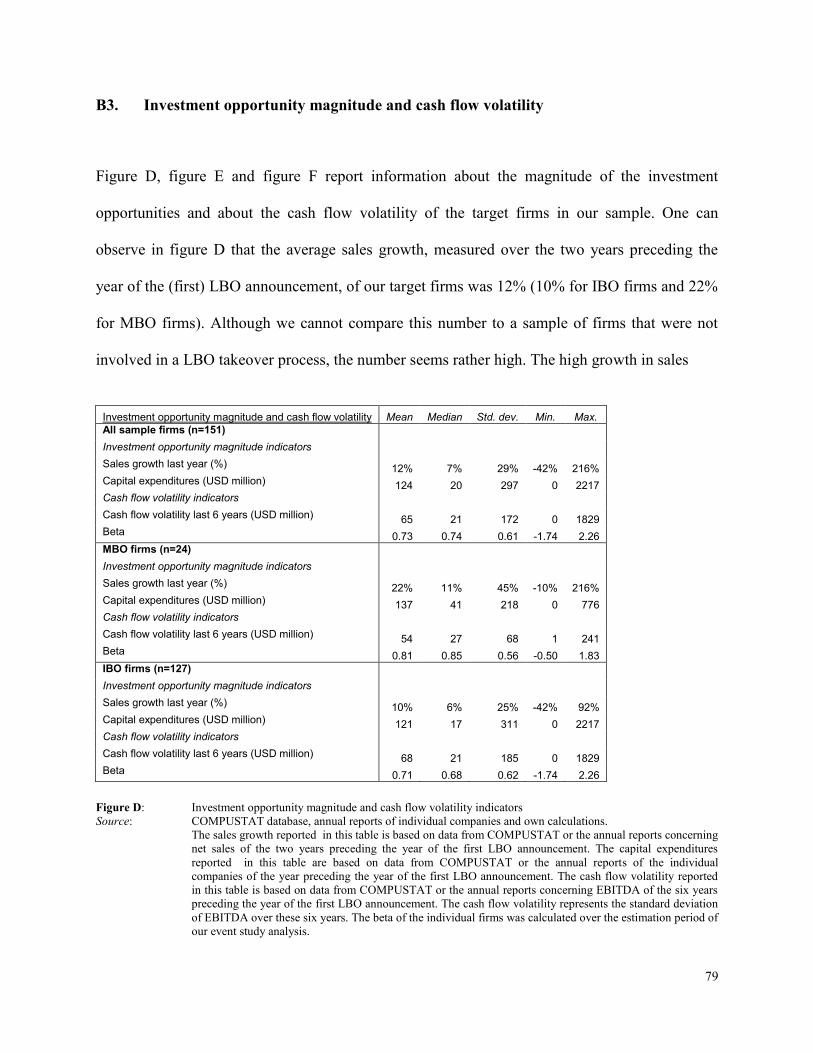

B3. Investment opportunity magnitude and cash flow volatility .................................. 79

B4. Ownership ................................................................................................................... 82

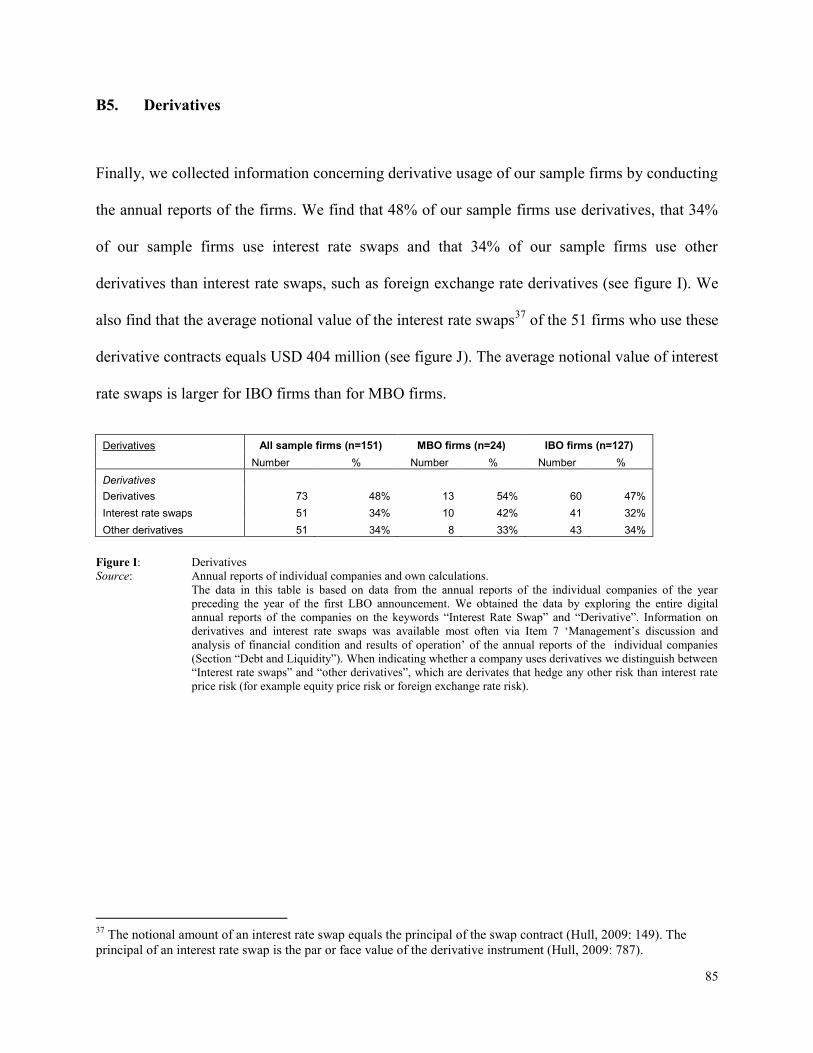

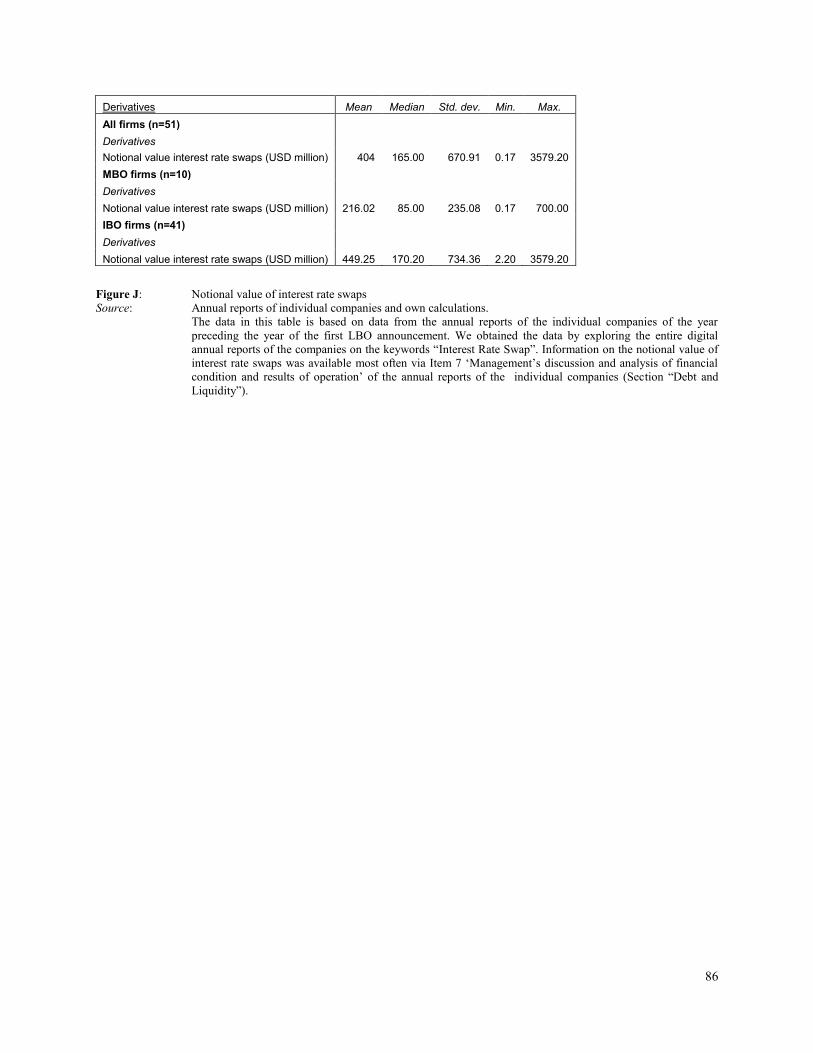

B5. Derivatives .................................................................................................................. 85

B6. Summary ..................................................................................................................... 87

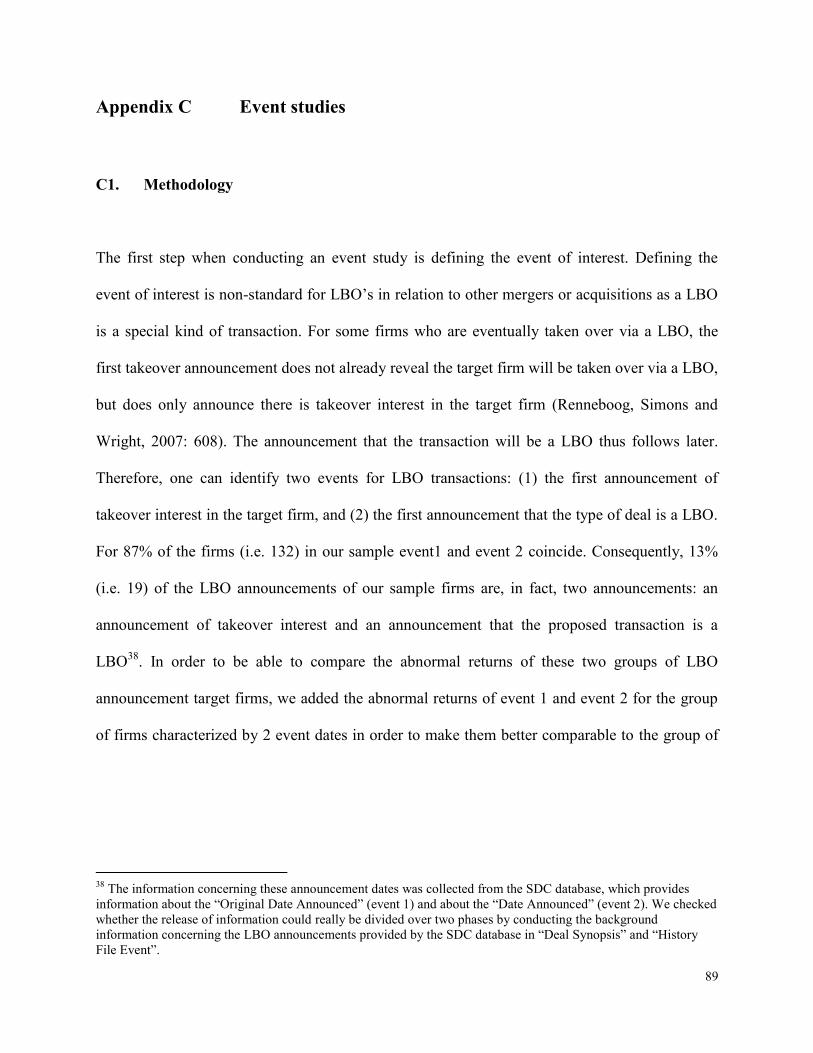

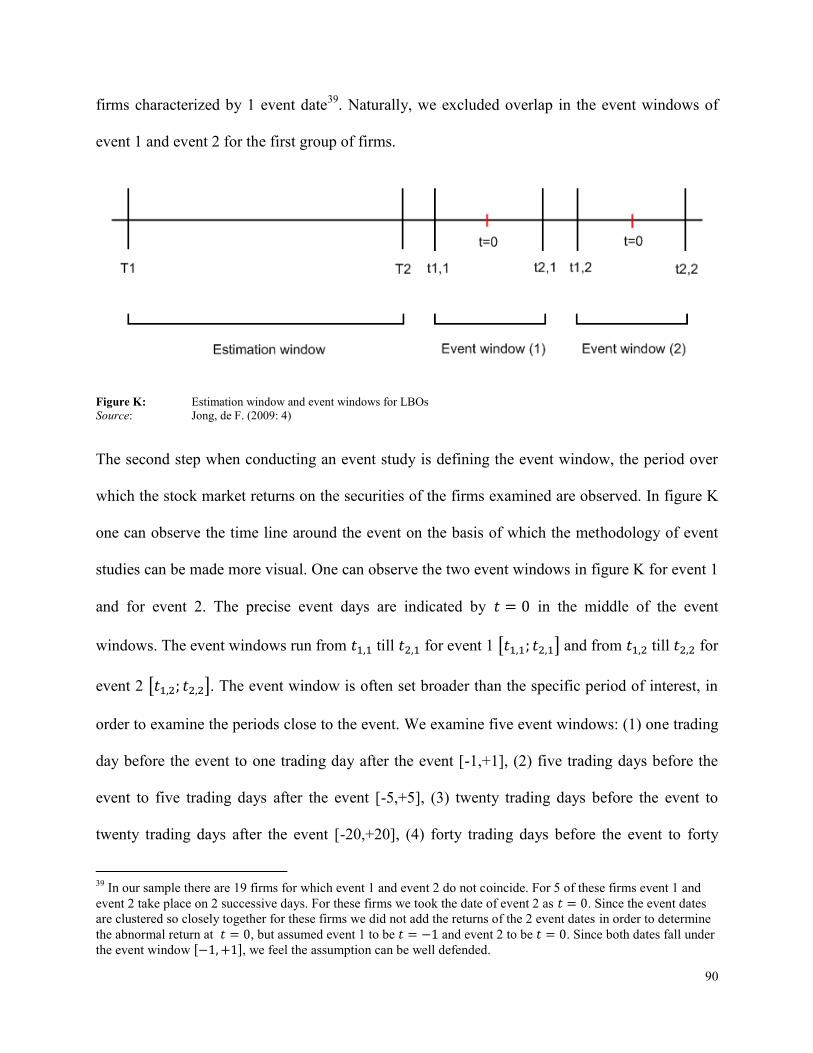

Appendix C Event studies ................................................................................................... 89

C1. Methodology ............................................................................................................... 89

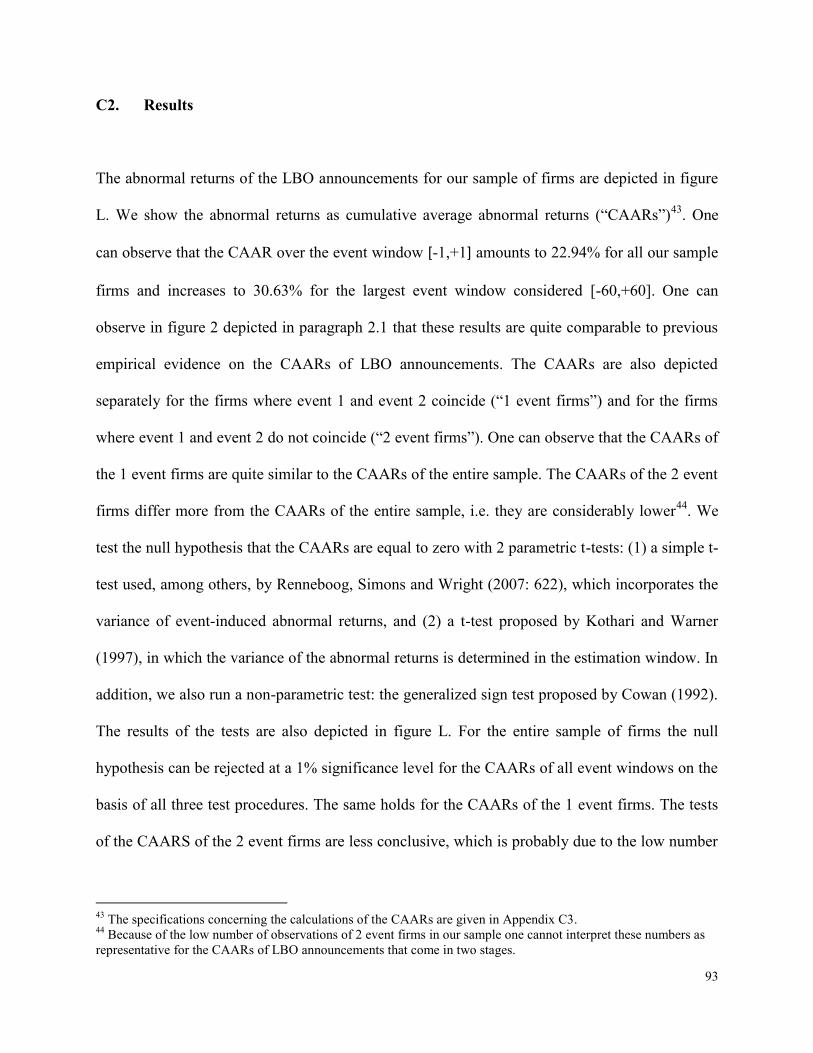

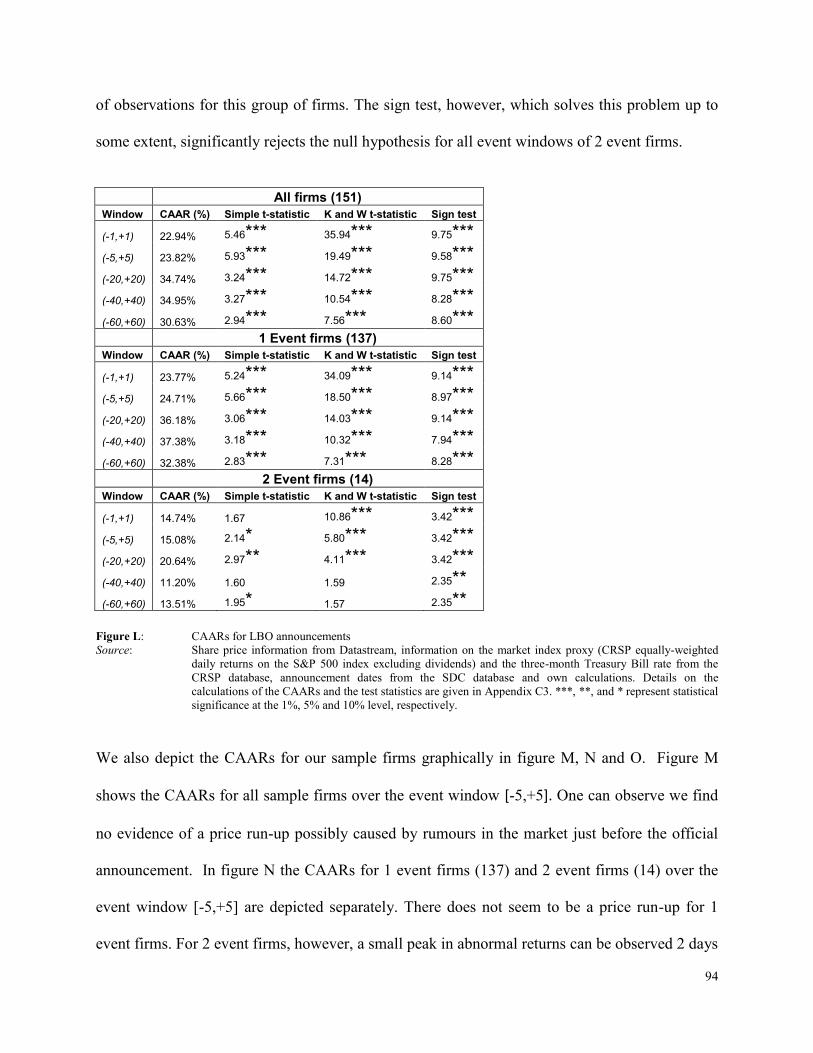

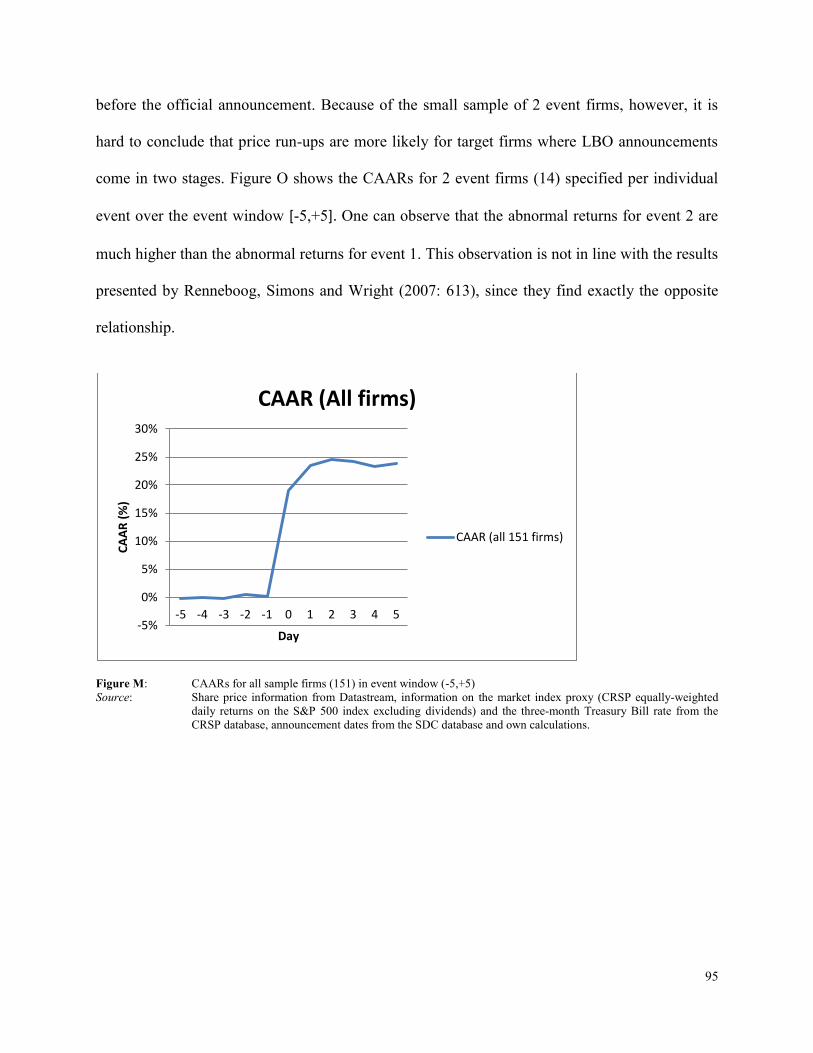

C2. Results ......................................................................................................................... 93

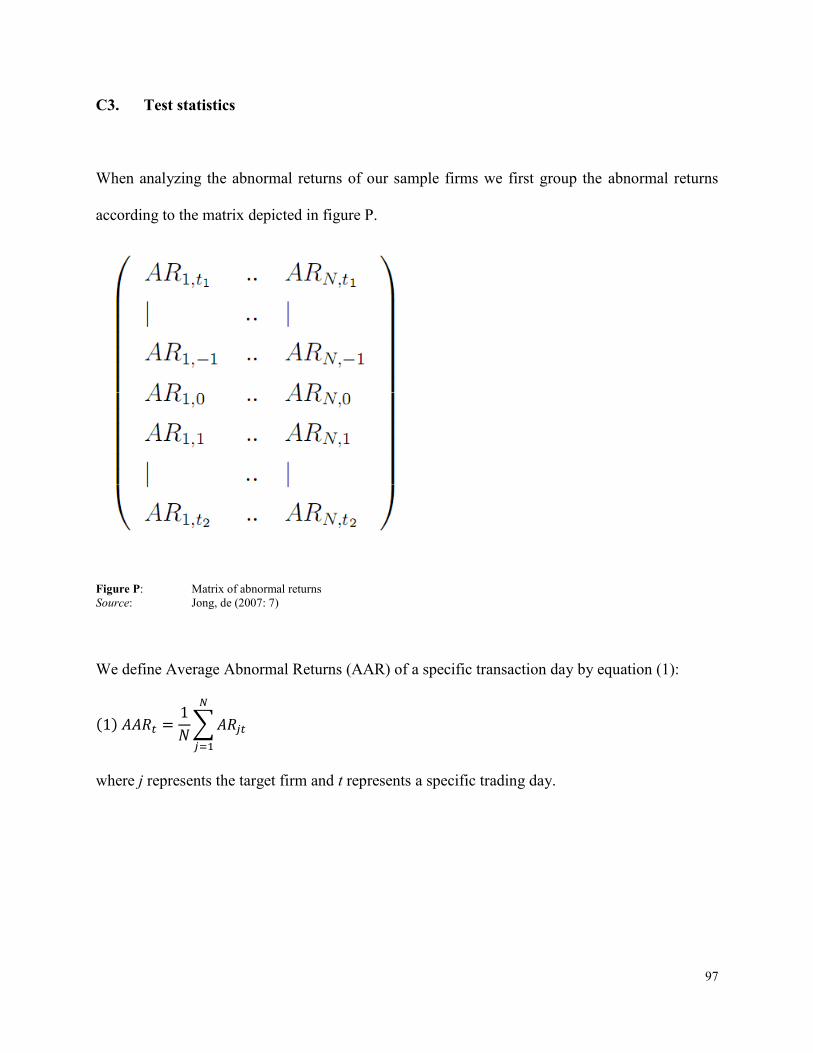

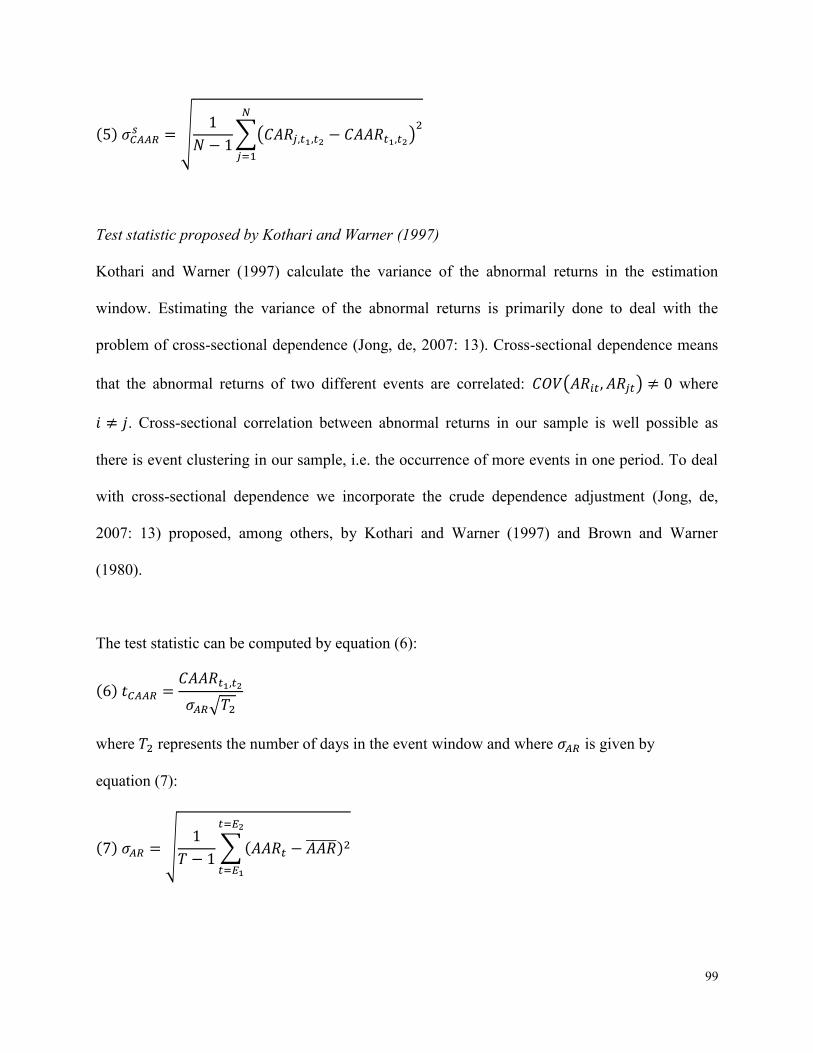

C3. Test statistics............................................................................................................... 97

Appendix D Regression analysis ....................................................................................... 102

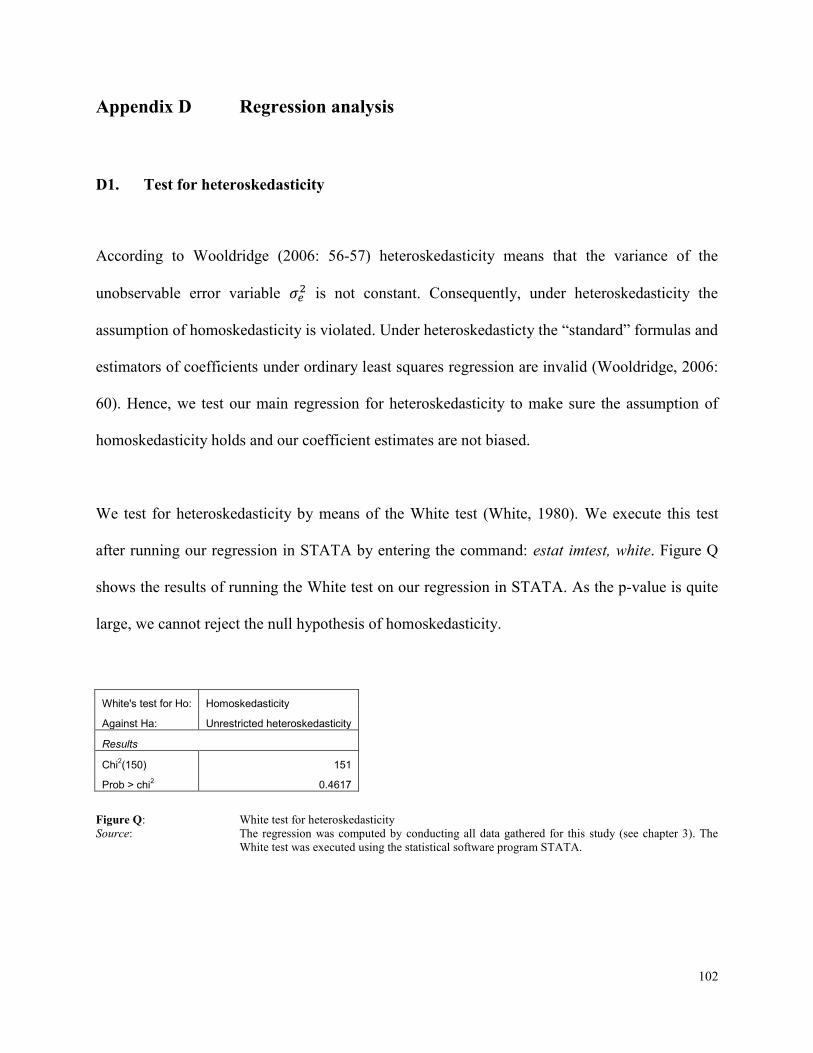

D1. Test for heteroskedasticity ...................................................................................... 102

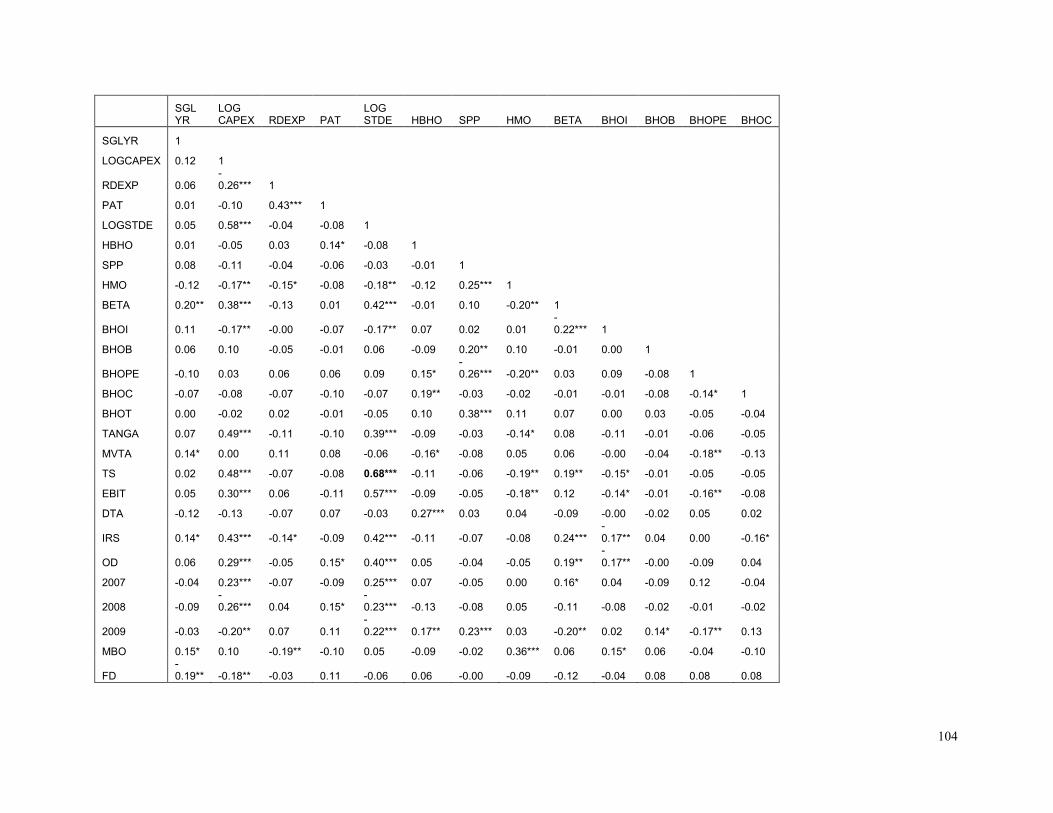

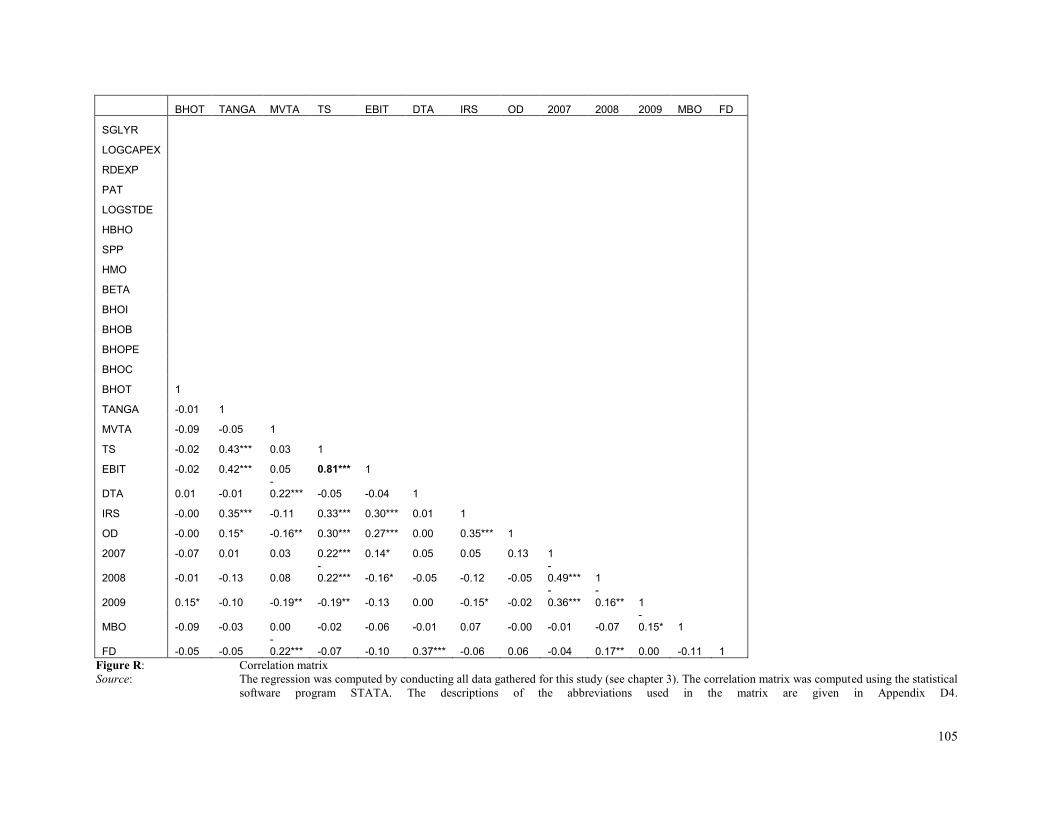

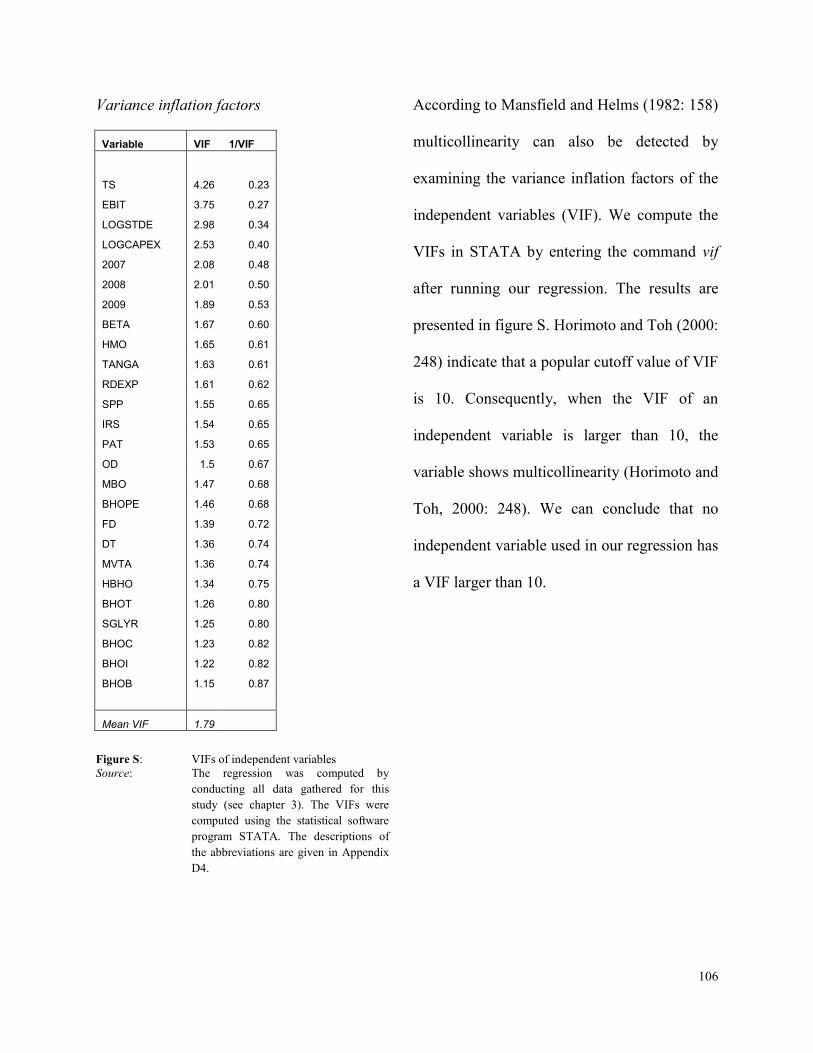

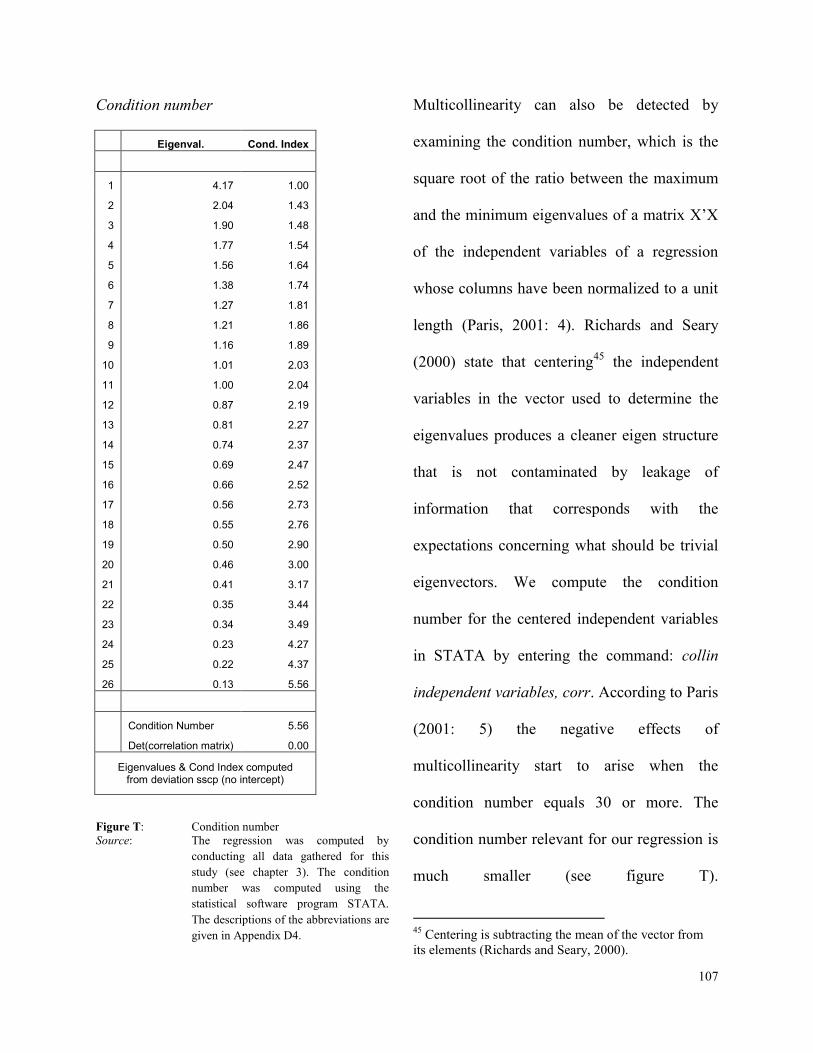

D2. Tests for multicollinearity ....................................................................................... 103

D3. Robustness checks .................................................................................................... 108

D4. Description of independent variables ..................................................................... 111

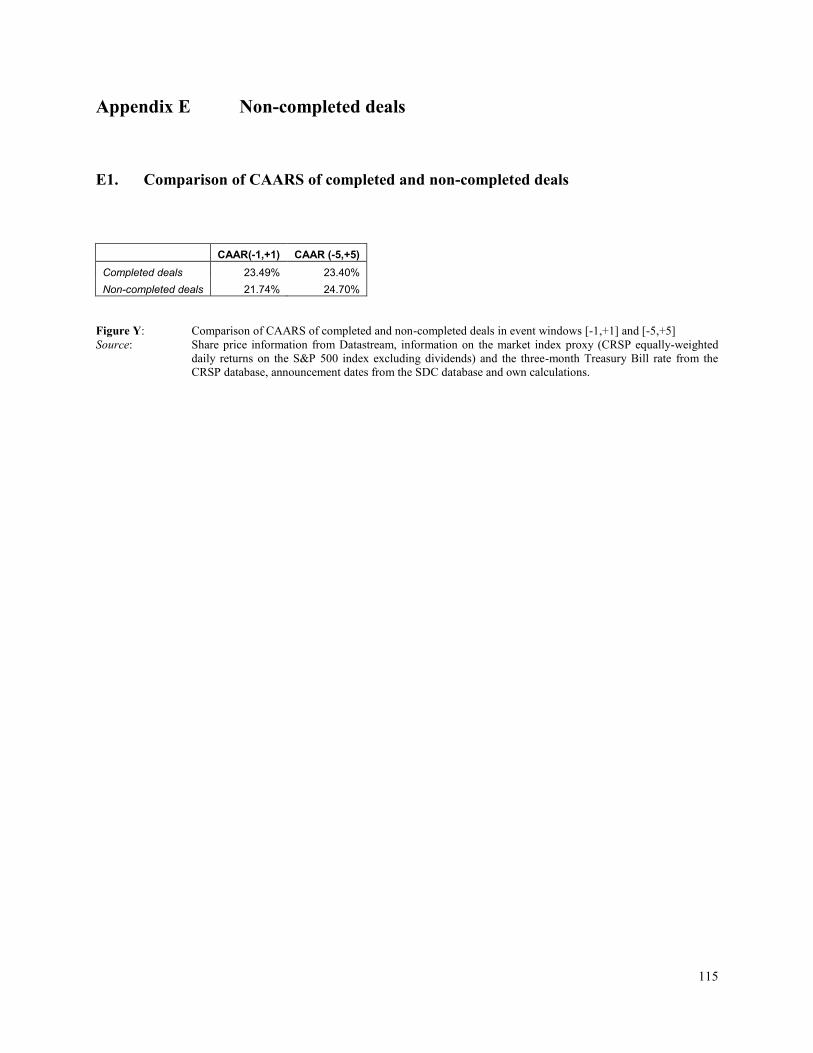

Appendix E Non-completed deals .................................................................................... 115

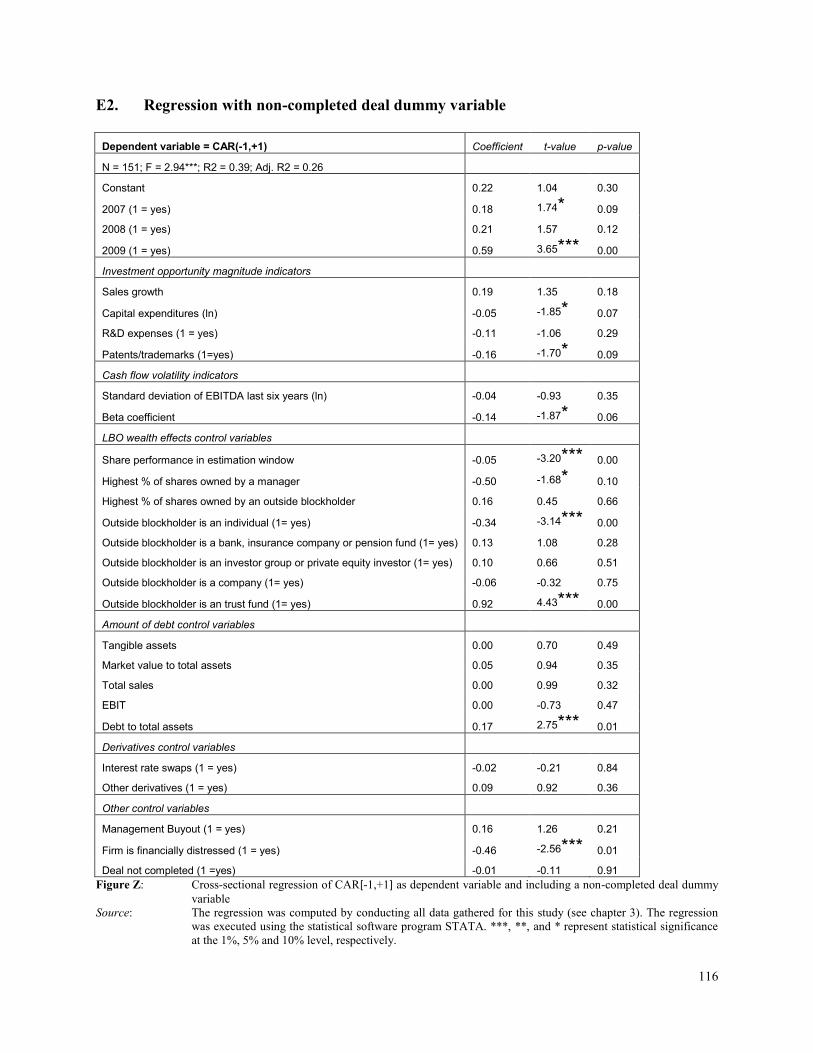

E1. Comparison of CAARS of completed and non-completed deals ......................... 115

E2. Regression with non-completed deal dummy variable ......................................... 116

6

Acknowledgements

Writing this thesis was more challenging for me than the thesis I wrote for my Master in

Economics at Tilburg University 2 years ago. Although the subjects of both theses were equally

challenging, the circumstances I faced when writing this thesis were less favorable. When I

wrote my previous thesis I still lived with my parents and I had all the time in the world to write

it. For this thesis much less time was available to me, especially because of the internship at

Rembrandt Fusies & Overnames, which later became a job, I did simultaneously. In addition,

there were some bumps in the road during the last year that kept me from working on the thesis:

a compulsory moving of house due to neglect of our lessor and the death of two very close

friends. All in all, I am very glad I found the energy to finish the thesis, which means my life as a

student at Tilburg University will come to an end and my working life will begin.

I would like to thank several persons who have contributed directly and indirectly to this thesis.

First of all, I would like to thank my girlfriend Iris for her unconditional support. Although I was

considerably stressed and moody because of the high workload of the thesis and my job, she

understood my situation and was there to cheer me up when I most needed it. In addition, I am

very grateful to my parents Ad en Marian for their moral and financial support. I have also

benefited from the friendships with my best friends and close family-members as these

relationships brought relaxation and distraction while writing the thesis. For this I thank them.

I am also very grateful to my colleagues at Rembrandt Fusies & Overnames who gave me the

chance to do an internship and combine the theory and practice of Finance. Because of the

7

internship I know that I made the right educational choices in my life. In addition, I was able to

obtain working experience because of the internship, which is a very valuable matter that many

economical programs at Dutch Universities unfortunately still lack.

In particular, I would like to thank my supervisor Dr. Michel van Bremen for his good and well-

meant advice. I am especially grateful to him for understanding my busy life of combining an

internship / job with writing a master thesis.

Ron de Vaan.

8

Abstract

There are two strategies that lead firms to financial flexibility: (1) adopting a conservative capital

structure, and (2) reducing cash flow volatility. While there is strong empirical evidence

confirming the value of reducing cash flow volatility for firms, there is less convincing empirical

evidence confirming the value of the other strategy to achieve financial flexibility. In this paper

we explore whether financial flexibility, achieved by adopting a conservative capital structure,

creates value for firms. We use the special character of leveraged buyout transactions as a tool to

examine the value of financial flexibility. Leveraged buyouts (LBOs), namely, lead to a

deterioration in the financial flexibility of target firms since they often result in the adoption of a

more non-conservative capital structure by target firms in relation to the capital structure of these

firms before such transactions. By performing an event study and a cross-sectional regression

analysis considering 151 LBO announcements for US target firms in the period 2006 – 2009, we

find that the abnormal returns on a target firm‟s stock during the period surrounding a LBO

announcement are negatively related to the magnitude of a firm‟s investment opportunities and

to a firm‟s cash flow volatility. Both the magnitude of a firm‟s investment opportunities and a

firm‟s cash flow volatility are larger for firms that have a higher need for financial flexibility. As

a result, we conclude that the strategy of adopting a conservative capital structure to achieve

financial flexibility is valuable for firms, especially for those firms who have a higher need for

financial flexibility.

9

Introduction

The recent credit crisis, which broke out in summer 2007 (Brunnermeier, 2009: 77), has once

again invigorated the discussion on the value of financial flexibility for firms. Too heavily

financed and therefore financially inflexible companies, for example the originators of subprime

mortgages, went bankrupt (FT, May 6, 2009). On the other hand, the crisis has provided

investment opportunities for companies who were financially healthier. In the oil and gas

industry, for example, there has been a wave of consolidation as weaker firms were taken over

by their stronger counterparts at much lower prices than would have been paid before the credit

crisis (FT, October 20, 2008). In addition, it is very likely that companies in highly innovative

industries that were able to invest in product development, because of their financial flexibility,

were able to create a technological gap with those firms that were not able to invest during the

crisis.

According to Gamba and Triantis (2008: 2) financial flexibility represents the firm‟s ability to

access and restructure it‟s financing at low cost, by means of which firms become able to avoid

the costs of financial distress and to fund investment when profitable opportunities arise. There

are numerous examples of financially distressed companies that had to sell value-creating

businesses to manage liquidity constraints. According to Léautier (2007: 30) US independent

power producers were forced to sell power generation assets under fair value to meet debt

obligations in the period 2002 – 2003 following the crisis that hit the US power industry. Culp

and Miller (1999) discuss how Metallgesellschaft had to liquidate its „value-creating‟ oil

derivatives portfolio to manage a liquidity constraint. In addition, there are many examples of

10

financially vulnerable or inflexible firms who were not able to finance profitable investment

opportunities. Minton and Schrand (1999), for example, show by examining 1300 non-financial

companies that firms in the top quartile in cash flow volatility in their industry are characterized

by 19% less capital expenditures than the average firm operating in the industry. Doherty (2000:

213) reports that every 1 US dollar reduction in a firm‟s capital reduces the firm‟s investment

budget by approximately 35%. Léautier (2007: 31) also mentions the non-pursuance of value-

creating acquisition opportunities of firms, because of the adverse impact of such acquisitions on

the financial situation of a firm, as a clear negative effect of financial inflexibility or

vulnerability.

The value of financial flexibility seems to be well recognized in the field. In a survey study of

392 CFOs of US firms Graham and Harvey (2001: 210) find that the main motivation of firms to

choose a certain capital structure is financial flexibility. Brounen et al. (2001: 1) confirm this

finding in a survey of 313 CFOs of European firms. Bancel and Mittoo (2004: 1) also support the

finding of Graham and Harvey (2001) examining managers of European firms. In addition, there

is theoretical justification for the value of financial flexibility. In a theoretical model Tirole

(2006), for example, describes how misaligned incentives between equity holders (owners), bond

holders (creditors) and managers in relation with information asymmetries between managers

(insiders) and equity and debt holders (outsiders) can lead to credit rationing. In his model

providers of capital simply refuse to lend to firms, independent of the rate offered by managers

or equity holders, thereby reducing the probability that value-creating investment opportunities

will be financed significantly. Reducing the need for external financing of firms would increase

11

this probability. While the value of financial flexibility is recognized in the field and is supported

theoretically, its value is less well documented in the empirical literature.

According to Léautier (2007: 38-39) there are two paths that lead firms to financial flexibility:

(1) adopting a conservative capital structure, and (2) reducing cash flow volatility. By „adopting

a conservative capital structure‟ we mean „not attracting too much debt, but relying on internal

funds and equity too in order to finance investments‟1. Firms should finance some or even a large

share of their investments with equity as adopting a non-conservative capital structure or

financing many investments with debt comes with certain risks. The main risks firms face after

passing a certain threshold level of debt is the incurrence of financial distress costs and the

inability to finance promising investment opportunities. By not attracting too much debt firms

can prevent the incurrence of financial distress costs and maintain the ability to finance

promising investment opportunities. Adopting a conservative capital structure leads to financial

flexibility for three reasons: (1) the availability of internal funds makes it easier to fund

investments and withstand adverse cash flow shocks, (2) equity protects firms from the downside

as there are no obligated payments to providers of equity capital such as is the case with

providers of debt capital, and (3) a conservative capital structure makes it easier and less

expensive for firms to attract external funds which provides flexibility to finance operations and

investments even when facing adverse cash flow shocks2. Although adopting a conservative

1 In Appendix A1 we treat the different sources a firm has to finance investments more elaborately.

2 A firm‟s capital structure is reflected in the cost of capital providers of external funds charge to firms. Firms with

more debt are generally perceived as more risky by investors, which is consequently reflected in a higher rate of

return demanded on the funds they provide to firms and in the willingness of investors to provide funds to firms as

investors incorporate the risk of bankruptcy in their investment decision. As a result, it is, in general, more

expensive and more difficult for firms with more debt to obtain external funds. This statement can be supported by

showing what happens to a firm‟s credit ratings when its debt ratio deteriorates. Firms with higher debt ratios,

namely, in general receive lower credit ratings than firms with lower debt ratios. Credit ratings serve as a guideline

for the riskiness of a firm to many investors. As a result, obtaining funds to finance investments becomes more

12

capital structure can be rewarding for firms, financing investments with retained earnings or

equity is an expensive manner of financing investments3. Therefore, firms also try to become

more financially flexible by reducing their cash flow volatility, for example, via risk transfer. By

„reducing cash flow volatility‟ we mean adopting strategies that smooth a firm‟s income pattern.

By adopting such strategies firms can lower the probability of being confronted with financial

distress costs and lower the probability of not being able to finance investments when facing

adverse cash flow shocks at a lower cost than issuing equity (Léautier, 2007: 39).

One can demonstrate the value of financial flexibility for firms when showing that one of these

two strategies is positively related to firm value. Especially on the relationship between

(reducing) cash flow volatility and firm value there is convincing evidence on such a positive

relation. First of all, Shin and Stulz (2000: 20-21), and Allayannis and Weston (2003: 23-24) find

a negative relationship between cash flow volatility and shareholder value, measured among

others by price-to-book ratio. In addition, Smithson and Simkins (2005: 13) sum up several

studies that associate the usage of derivatives contracts, which are instruments that reduce cash

flow volatility, with higher firm values. Allayannis and Weston (2001: 273-274), for example,

find a positive relationship between the use of foreign exchange derivatives and firm value,

measured by Tobin‟s Q, by investigating 720 large nonfinancial firms. There is, however, less

empirical evidence on the proposed positive relation between „adopting a conservative capital

structure‟ and firm value in the light of financial flexibility. Of course, there are other studies that

difficult and more expensive when credit ratings deteriorate. Some examples of the difficulties that accompany a

decrease in credit ratings are the inability to access capital markets for very short-term lending and the need to

collateralize all lending (Léautier, 2007: 34). 3 A firm that holds liquid internal funds, such as cash or liquid short-term assets, cannot invest these funds and earn

a positive return on the funds. Forgoing this positive return can be interpreted as an opportunity cost of holding

liquid internal funds. Equity financing is, among others, more expensive than debt financing because of an adverse

selection problem inherent to this source of financing. In Appendix A1 the adverse selection problem of equity is

treated more extensively.

13

theoretically support the assumption of Léautier (2007: 38-39) that adopting a conservative

capital structure is value-creating for firms in the light of financial flexibility (Gamba and

Triantis, 2008; Nash et al., 2003). Direct empirical evidence on this relationship, however, is

rare. Consequently, we have to rely on more indirect evidence that supports the assumed positive

relation. Since financial flexibility actually helps firms to avoid the costs of financial distress, we

could interpret empirical evidence on a negative relationship between financial distress costs and

firm value as such indirect evidence. According to Andrade and Kaplan (1998: 1444) financial

economists have indicated the measurement of financial distress costs to be difficult. The reason

is that economists find it hard to distinguish whether financial distress or the factors that pushed

a firm into financial distress are the cause of bad performance of a firm. Altman (1984: 1067-

1089), for example, finds the indirect costs of financial distress to be substantial. Altman,

however, cannot separate the costs of financial distress from negative shocks in operating

income. Asquith, Gertner, and Scharfstein (1994: 625-658), Gilson (1997: 161-197), Hotchkiss

(1995: 3-22), and LoPucki and Whitford (1993: 597-618) provide indirect evidence on the notion

that financial distress is costly. Because the firms used in the samples of these papers are

economically distressed, in addition to financially distressed, however, it is hard to conclude

whether the costs of financial distress, the costs of economic distress or an interaction of these

costs is measured in these papers. Andrade and Kaplan (1998: 1445) estimate financial distress

costs to be 10 percent to 20 percent of firm value by studying thirty-one highly leveraged

transactions that become financially and not economically distressed4. In addition, Andrade and

Kaplan (1998: 1445) find that the primary cause of financial distress is high leverage. Hence,

4 All firms in the sample of Andrade and Kaplan have positive operating margins which exceed the industry margin.

Consequently, the firms considered by Andrade and Kaplan are healthy in relation to their industry comparatives

irrespective of their leverage ratio.

14

Andrade and Kaplan provide evidence on the negative relationship between financial distress

costs, caused by adopting a non-conservative capital structure, and firm value.

While there is strong empirical evidence on a positive relationship between reducing a firm‟s

cash flow volatility and firm value, there is less convincing empirical evidence on a positive

relationship between the adoption of a conservative capital structure and firm value in the light

of financial flexibility. The aim of this thesis is to provide empirical support for this proposed

positive relationship. Consequently, our main research question is: does financial flexibility,

achieved by adopting a conservative capital structure, create value for firms? We use the special

character of leveraged buyout transactions as a tool to examine the value of financial flexibility.

We actually measure the effect of financial flexibility on firm value by analyzing the abnormal

returns of target firms during the announcement of a leveraged buyout transaction. Leveraged

buyout announcements, namely, reveal a target firm‟s financial flexibility is very likely going to

deteriorate in the near future. We hypothesize that this deterioration will have the largest

negative impact on those firms that value financial flexibility the most.

The structure of this paper is as follows. In chapter 1 we examine more elaborately what

financial flexibility exactly is. In addition, we explore the relationship between financial

flexibility and firm value according to economic theory more extensively. In chapter 2 we

discuss the methodology we use to answer our main research question. First of all, we explain

the research design of the study and we formulate our hypotheses. Then, we describe the data

and the empirical techniques we used to test these hypotheses. In chapter 3 we present the results

15

of this study. Chapter 4 discusses the meaning and the implications of the results. Finally, we

draw conclusions in chapter 5.

16

Chapter 1 Theory

In the Introduction we have framed our main research question and we have embedded the topic

of this thesis in the literature. Although we have already defined financial flexibility in short and

although we have given a comprehensive description of the relationship between financial

flexibility and firm value in the Introduction, we treat both subjects more extensively in this

chapter. First of all, we describe financial flexibility and its relationship with firm value more

elaborately. Then, we discuss how financial distress costs are related to firm value as this

relationship is closely connected to the relationship between financial flexibility and firm value.

§1.1 The relationship between financial flexibility and firm value

Financial flexibility is the firm‟s ability to finance its operations or investments even when

facing adverse cash flow shocks (Léautier, 2007: 29). The goal of achieving financial flexibility

often is part of a broader risk management strategy of firms. Financial flexibility creates value

for firms in two manners: (1) by helping firms to avoid the direct and indirect costs of financial

distress, and (2) by providing firms with the ability to always have the resources available to

invest. The second source of value creation of financial flexibility can, in fact, also be interpreted

as helping firms to avoid the opportunity cost of financial distress, namely not having the

resources available to invest. We define a firm as in financial distress when a firm experiences

difficulties in meeting its debt obligations (Berk and DeMarzo, 2007: 491). The direct costs of

financial distress are the costs corresponding to the most extreme situation of financial distress,

namely bankruptcy. When a firm becomes financially distressed and files for bankruptcy, outside

17

professionals, such as legal and accounting experts, consultants, appraisers, and auctioneers, are

generally hired (Berk and DeMarzo, 2007: 495). Hiring such professionals leads to high costs.

The indirect costs of financial distress are harder to measure, but are commonly much larger than

the direct costs. Indirect costs of financial distress exist of, among others, the loss of customers,

the loss of suppliers, the loss of employees, the loss of receivables and the forced sale of valuable

assets in order to meet financial obligations. The third category of financial distress costs are the

opportunity costs of financial distress, which are probably even harder to measure than the

indirect costs of financial distress. We define these opportunity costs as the inability of firms to

invest in promising investment opportunities. Financial flexibility provides firms with the ability

to avoid all of these costs. Consequently, it helps firms to prevent value destruction and it

provides firms with the ability to exploit promising investment opportunities. Both

characteristics of financial flexibility create value for firms.

§1.2 The relationship between financial distress costs and firm value

The relationship between financial distress costs and firm value is already well-documented in

the economic literature. Financial distress costs, namely, are an important ingredient in the

theories discussing the relationship between capital structure and cost of capital (a u-shaped

curve) and the relationship between capital structure and firm value (an inverted u-shaped curve).

According to Modigliani and Miller (1958: 268) in a perfect capital market5 a firm‟s financing

choice or capital structure choice does not affect a firm‟s weighted average cost of capital (after

5 According to Modigliani and Miller a capital market is perfect if it meets the following 3 conditions: (1) Investors

and firms can trade the same set of securities at competitive market prices equal to the present value of their future

cash flows, (2) there are no taxes, transaction costs or issuance costs associated with security trading, and (3) a

firm‟s financing decisions do not change the cash flows generated by its investments, nor do they reveal new

information about them (Berk and DeMarzo, 2007: 432).

18

this: “WACC”) or a firm‟s value6. Not many capital markets, however, are perfect. In most

capital markets, namely, there is taxation and there are considerable transaction costs.

The effects of taxation and financial distress costs on the WACC, or risk profile, of a firm and on

firm value can be well illustrated by considering what happens to both variables when a firm

attracts more debt and consequently adopts a less conservative capital structure. Taxation

positively affects a firm‟s WACC (i.e. the WACC becomes lower) when attracting more debt

because of the tax deductibility of interest payments. Transaction costs, which are primarily

financial distress costs, however, affect a firm‟s WACC negatively when attracting more debt.

Leverage, namely, increases the risk for firms of incurring financial distress costs, which

effectively reduce the cash flows available to investors. The tradeoff theory weights the benefits

of debt that result from shielding cash flows from taxes against the costs of financial distress

associated with leverage (Berk and DeMarzo, 2007: 501). The tradeoff theory, discussed

extensively among others by Stewart Myers (1983: 575-592), states that the total value of a

levered firm equals the value of the firm without leverage plus the present value of the tax

savings from debt, less the present value of financial distress costs. The tradeoff theory indicates

that companies have an incentive to take on more debt to take advantage of the tax benefits of

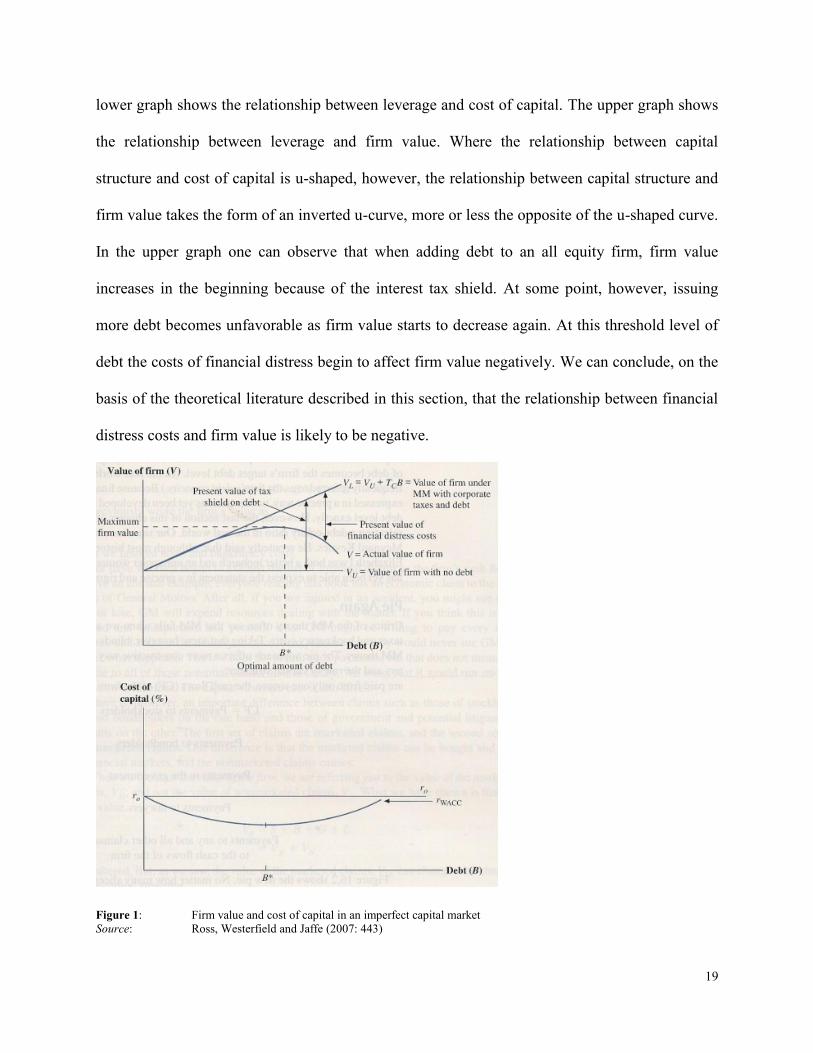

debt, but that taking on too much debt leads to value decreasing financial distress costs. Figure 1

illustrates the effects of taxation and transaction costs on a firm‟s WACC and on firm value. The

6 Modigliani and Miller argue that when a firm attracts more debt it‟s cost of equity rises since the firm becomes

more risky to invest in for equity holders. More debt holders in a firm, namely, means more investors who receive

their money earlier than equity holders, the residual claimants of a firm, when the firm goes bankrupt. The cost of

debt, however, rises very slowly and the fraction of firm value financed with debt increases when a firm attracts

more debt holders. Because more emphasis is put on the relatively low cost of debt, a firm‟s WACC does not change

when a firm increases its usage of debt as a source of funding. Since the WACC does not change when altering the

capital structure of a firm, in a perfect capital market, firm value is also unaffected by a change in capital structure.

The cash flows a firm will earn in the future do not change and neither does the discount rate at which these cash

flows are transformed to present value.

19

lower graph shows the relationship between leverage and cost of capital. The upper graph shows

the relationship between leverage and firm value. Where the relationship between capital

structure and cost of capital is u-shaped, however, the relationship between capital structure and

firm value takes the form of an inverted u-curve, more or less the opposite of the u-shaped curve.

In the upper graph one can observe that when adding debt to an all equity firm, firm value

increases in the beginning because of the interest tax shield. At some point, however, issuing

more debt becomes unfavorable as firm value starts to decrease again. At this threshold level of

debt the costs of financial distress begin to affect firm value negatively. We can conclude, on the

basis of the theoretical literature described in this section, that the relationship between financial

distress costs and firm value is likely to be negative.

Figure 1: Firm value and cost of capital in an imperfect capital market

Source: Ross, Westerfield and Jaffe (2007: 443)

20

§1.3 The opportunity costs of financial distress

In perfectly competitive markets or efficient markets firms cannot make a profit nor are they able

to create value7. Fortunately for firms there are not many markets that approach the definitions of

a perfectly competitive or efficient market. The market descriptions of these markets are mere

extreme exhibits of the direction in which markets tend to move. Nevertheless, it is important to

recognize that not all industries offer equal opportunities for sustained profitability (Porter, 1985:

1). According to Porter (1985: 4) the rules of competition are embodied in five competitive

forces: (1) the entry of new competitors, (2) the threat of substitutes, (3) the bargaining power of

buyers, (4) the bargaining power of suppliers, and (5) the rivalry among the existing competitors.

The collective strength of these five competitive forces will determine the ability of firms to

make a profit or to create value in a market. As the strength of each of these five forces will be

different from market to market, the inherent profitability of markets will also differ from market

to market. Consequently, firms will be able to create more value in markets where the five

competitive forces are favorable than in markets where they are unfavorable. The competitive

forces, however, are dynamical and subject to change. Consequently, when defining competitive

strategy firms should not only focus on being in the right market as to some extent one could also

consider the market a firm operates in as a natural endowment. In contrast, irrespective of the

market a firm operates in, a firm should focus even more on how it can change the competitive

forces in a market to its own favor when defining competitive strategy. In order to be able to

make a profit or to create value a firm should focus on its relative position in the market. Firms

can realize a favorable relative position in a market by creating a sustained competitive

advantage.

7 In Appendix A2 perfectly competitive markets and efficient markets are shortly described.

21

A sustained competitive advantage is a value creating strategy not simultaneously being

implemented by any current or potential competitors who are, above all, unable to duplicate the

benefits of this strategy (Barney, 1991: 206). The indication that a competitive advantage is

sustained does not mean that the specific competitive advantage has eternal life. It does imply

that it will not disappear because of duplication efforts of other firms. Porter (1985: 11) defines

two basic types of competitive advantage a firm can possess: (1) low cost, and (2) differentiation.

Combined with the scope of activities for which firms seek to achieve a competitive advantage

these two types of competitive advantage lead to three generic strategies for achieving a

favorable relative position in a market: (1) cost leadership, (2) differentiation, and (3) focus

(Porter, 1985: 11). Firms use the cost leadership and differentiation strategy to realize a

competitive advantage in many segments of a market, while they use the focus strategy to

acquire cost leadership or differentiation in a more narrow market segment or niche market. In

all strategies firms are effectively trying to influence the five competitive forces in a market to

change them to their favor. In a cost leadership strategy firms try to create barriers to entry by

realizing innovative cost efficient production techniques or by taking over competitors to create

economies of scale. In a differentiation strategy firms try to create barriers to entry by being

unique. Firms may realize the creation of such barriers by producing highly innovative products,

by creating a very strong brand name or by taking over firms that operate in different segments

in the same market in order to be able to offer a unique package of products and services to

buyers. The common characteristic that these strategies share is that the achievement of a

competitive advantage via any strategy requires investments. The ability to invest in investment

opportunities that correspond to a firm‟s strategy is instrumental for a firm wanting to achieve a

competitive advantage. When a firm is in financial distress it does not have the resources

22

available to invest in promising investment opportunities that support the strategy which leads to

a firm‟s ultimate goal: achieving a competitive advantage. The disability to invest can be

interpreted as the opportunity cost of financial distress. Financial flexibility provides firms with

the ability to always have the resources available to invest and, consequently, helps firms to

avoid the opportunity costs of financial distress. Since firms can better execute the actions which

lead to the achievement of a competitive advantage when financially flexible, financial flexibility

is value-creating for firms.

23

Chapter 2 Methodology

At this point, we understand what financial flexibility is and how it theoretically creates value for

firms. In the Introduction we have already defined the two strategies firms can adopt in order to

become financially flexible. We showed that there is strong empirical evidence on a positive

relationship between ‘reducing cash flow volatility’ and firm value. Additionally, we indicated

there is less empirical evidence on the proposed positive relationship between ‘adopting a

conservative capital structure’ and firm value. Consequently, we aim to provide empirical

support on this relationship in this paper. In chapter 2 we describe the methodology we use to

investigate this relationship. First of all, we explain the research design we employed to examine

our main research question. Second, we formulate our main hypotheses. Finally, we define the

data and empirical techniques we make use of in this paper to test our main hypotheses.

§2.1 Research design

We believe we can measure the effect of financial flexibility on firm value by analyzing the

abnormal stock returns of target firms surrounding the period of a leveraged buyout (LBO)

announcement. According to Sudarsanam (2003: 268) a LBO is an acquisition of a corporation

financed mostly with cash, the cash being raised with a preponderance of debt. Almost all LBOs

are transactions where a listed company is acquired and subsequently delisted. Consequently,

they are referred to as public-to-private or going-private transactions (Renneboog and Simons,

2005: 2). According to Renneboog and Simons (2005: 2) virtually all these transactions are

financed by borrowing substantially above the industry average. In general, there are three types

24

of public to private transactions or LBOs: (1) the management buyout (MBO), (2) the

management buyin (MBI), and (3) the institutional buyout (IBO). In a MBO the incumbent

management takes the initiative to take the company private. The funding of the deal is provided

by the management team itself and by private equity investors. In a MBI the company is taken

over by an outside team of managers. Again the funding is provided by the management team

and private equity investors. A LBO is indicated to be an IBO when the new owners of the

delisted firm are solely institutional investors or private equity firms (Renneboog and Simons,

2005: 592).

The market considers LBO‟s as value creating. Substantial premiums are paid for target firms by

acquirers and substantial abnormal returns are observed during the takeover period. Renneboog,

Simons and Wright (2007: 610), for example, find the premiums offered in all UK public-to-

private transactions in the period 1997-2003 to be approximately 41%. The UK evidence is quite

similar to US evidence as Harlow and Howe (1993: 109-118)8 and Travlos and Cornett (1993: 1-

25)9 find the premiums to be 44.9% and 41.9% respectively. In addition, Renneboog, Simons

and Wright (2007: 610) find that the cumulative average abnormal returns (CAARs) surrounding

the announcement of a public-to-private transaction amount to approximately 26% over the event

window [-5,+5] and amount to approximately 29% over the event window [-40,+40] for their

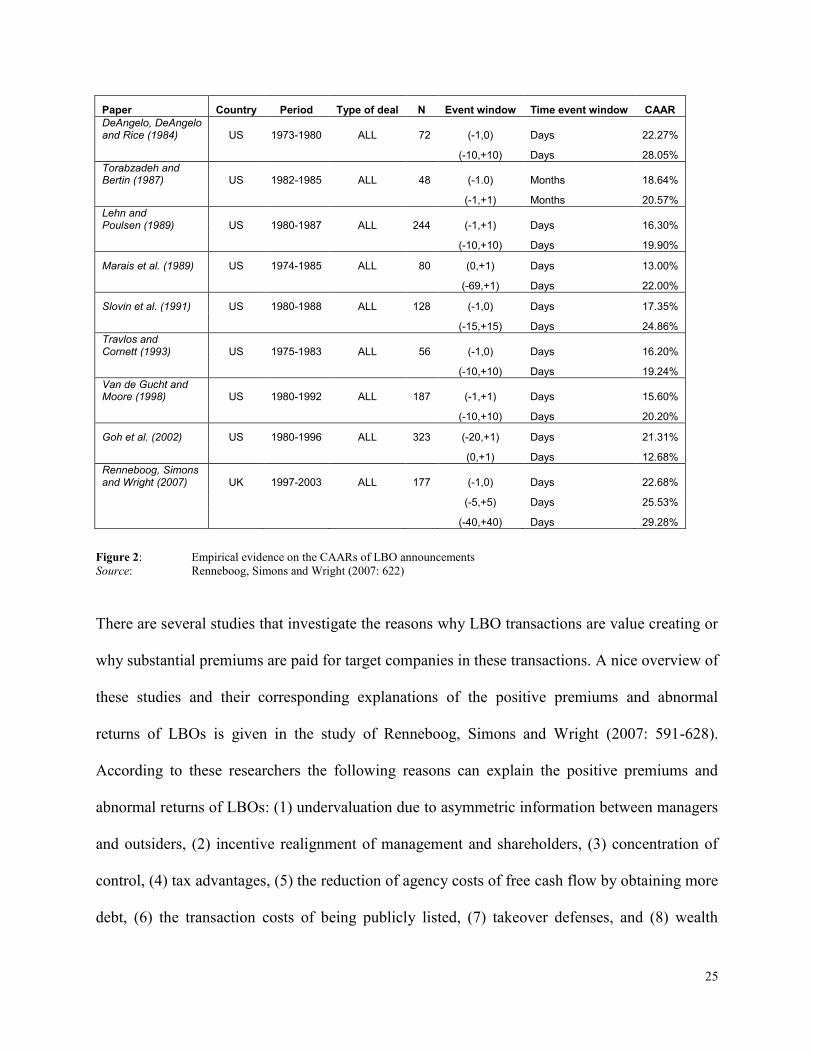

sample of firms. Again there are several studies that obtain similar results for US transactions

(see figure 2).

8 Harlow and Howe (1993: 109-118) examine LBO transactions in the period 1980-1989.

9 Travlos and Cornett (1993: 1-25) examine LBO transactions in the period 1975-1983.

25

Paper Country Period Type of deal N Event window Time event window CAAR

DeAngelo, DeAngelo and Rice (1984) US 1973-1980 ALL 72 (-1,0) Days 22.27%

(-10,+10) Days 28.05%

Torabzadeh and Bertin (1987) US 1982-1985 ALL 48 (-1.0) Months 18.64%

(-1,+1) Months 20.57%

Lehn and Poulsen (1989) US 1980-1987 ALL 244 (-1,+1) Days 16.30%

(-10,+10) Days 19.90%

Marais et al. (1989) US 1974-1985 ALL 80 (0,+1) Days 13.00%

(-69,+1) Days 22.00%

Slovin et al. (1991) US 1980-1988 ALL 128 (-1,0) Days 17.35%

(-15,+15) Days 24.86%

Travlos and Cornett (1993) US 1975-1983 ALL 56 (-1,0) Days 16.20%

(-10,+10) Days 19.24%

Van de Gucht and Moore (1998) US 1980-1992 ALL 187 (-1,+1) Days 15.60%

(-10,+10) Days 20.20%

Goh et al. (2002) US 1980-1996 ALL 323 (-20,+1) Days 21.31%

(0,+1) Days 12.68%

Renneboog, Simons and Wright (2007) UK 1997-2003 ALL 177 (-1,0) Days 22.68%

(-5,+5) Days 25.53%

(-40,+40) Days 29.28%

Figure 2: Empirical evidence on the CAARs of LBO announcements

Source: Renneboog, Simons and Wright (2007: 622)

There are several studies that investigate the reasons why LBO transactions are value creating or

why substantial premiums are paid for target companies in these transactions. A nice overview of

these studies and their corresponding explanations of the positive premiums and abnormal

returns of LBOs is given in the study of Renneboog, Simons and Wright (2007: 591-628).

According to these researchers the following reasons can explain the positive premiums and

abnormal returns of LBOs: (1) undervaluation due to asymmetric information between managers

and outsiders, (2) incentive realignment of management and shareholders, (3) concentration of

control, (4) tax advantages, (5) the reduction of agency costs of free cash flow by obtaining more

debt, (6) the transaction costs of being publicly listed, (7) takeover defenses, and (8) wealth

26

transfers from stakeholders to shareholders. Renneboog, Simons and Wright (2007: 610-619)

conclude that only three of the reasons summed up above can significantly explain the gains

from going private: undervaluation, incentive realignment of management and shareholders and

concentration of control.

In this study we do not intend to explain the gains of LBOs or public-to-private transactions. We

do, however, want to explain why the gains of LBO transactions are larger for some firms than

for other firms. In fact, we use the special character of LBO transactions as a tool to measure the

value of financial flexibility. Since virtually all LBOs are financed with a lot of debt, one may

expect the leverage ratio of the target firm to be much higher and the capital structure of the

target firm to be much less conservative after the transaction. According to Marais et al. (1989:

155) the proportion of debt in the capital structure of the target firm more than triples on average

following a successful buyout. Lehn and Poulsen (1988) present similar results. In addition,

Marais et al. (1989: 155) indicate that most rated debt securities of LBO targets experience

serious downgradings. Warga and Welch (1993: 961) also state that bond ratings of firms

involved in LBOs are usually significantly downgraded. Undergoing a LBO can actually be

interpreted as the opposite of the strategy to achieve financial flexibility we are interested in,

namely adopting a conservative capital structure, as it leads the target firm to adopt a more non-

conservative capital structure. Consequently, the announcement of a leveraged buyout

transaction reveals a target firm‟s financial flexibility is very likely going to deteriorate in the

near future. This deterioration in financial flexibility will have the largest negative impact on

those firms that value financial flexibility the most.

27

The value of financial flexibility for firms heavily depends on a firm‟s need for financial

flexibility. In general, there are two crucial factors that determine a firm‟s need for financial

flexibility: (1) the characteristics of a firm‟s investment opportunities, and (2) a firm‟s cash flow

volatility (Léautier, 2007: 6). The two main characteristics of investment opportunities are timing

and magnitude (Léautier, 2007: 31). Firms that are more regularly confronted with investment

opportunities whose timing is more unpredictable have a higher need for financial flexibility,

since these firms often do not exactly know when they need money to invest in promising

projects, which makes it harder for these firms to match income and expenses. Firms whose

investment opportunities are of a larger magnitude also have a higher need for financial

flexibility, since financing larger investments obviously is more difficult. Consequently, we can

conclude that these firms have a higher need for financial flexibility. The value of financial

flexibility is also larger for these firms as the need for financial flexibility is positively related to

the value of financial flexibility. The cash flow volatility of a firm is the other, next to a firm‟s

investment opportunity characteristics, crucial factor determining a firm‟s need for financial

flexibility. The probability of being confronted with direct and indirect financial distress costs

and the probability of not being able to finance investments when facing adverse cash flow

shocks is higher for firms characterized by a higher cash flow volatility. As a result, the need for

financial flexibility and the value of financial flexibility is also higher for these firms.

Hence, we expect a deterioration in financial flexibility to have the largest negative impact on

those firms characterized by investment opportunities that arise more quickly after one another,

that arise on a more unpredictable pattern and whose magnitude is larger than those of other

firms and on those firms characterized by a higher cash flow volatility. Consequently, we expect

28

the abnormal stock returns of target firms surrounding the period of a leveraged buyout

announcement to be lower for these type of firms.

§2.2 Hypotheses

On the basis of the research design we have just described we are able to formulate our main

hypothesis. In total, we formulate two main hypotheses. In this section we define our hypotheses

accurately and we embed them in the literature.

§2.2.1 The investment opportunity magnitude hypothesis

In the previous section we concluded that firms characterized by investment opportunities that

arise more quickly after one another, that arise on a more unpredictable pattern and whose

magnitude is larger than those of other firms, value financial flexibility more. While this

relationship is a clear one , it is harder to indicate how one should measure the characteristics of

the investment opportunities of firms in order to be able to test whether the relationship

empirically holds. Especially the rate at which a firm gets confronted with investment

opportunities and the unpredictability of investment opportunities seem very hard to measure.

Consequently, we focus on measuring the magnitude of the investment opportunities of firms in

order to be able to test whether the proposed relationship empirically holds. We measure the

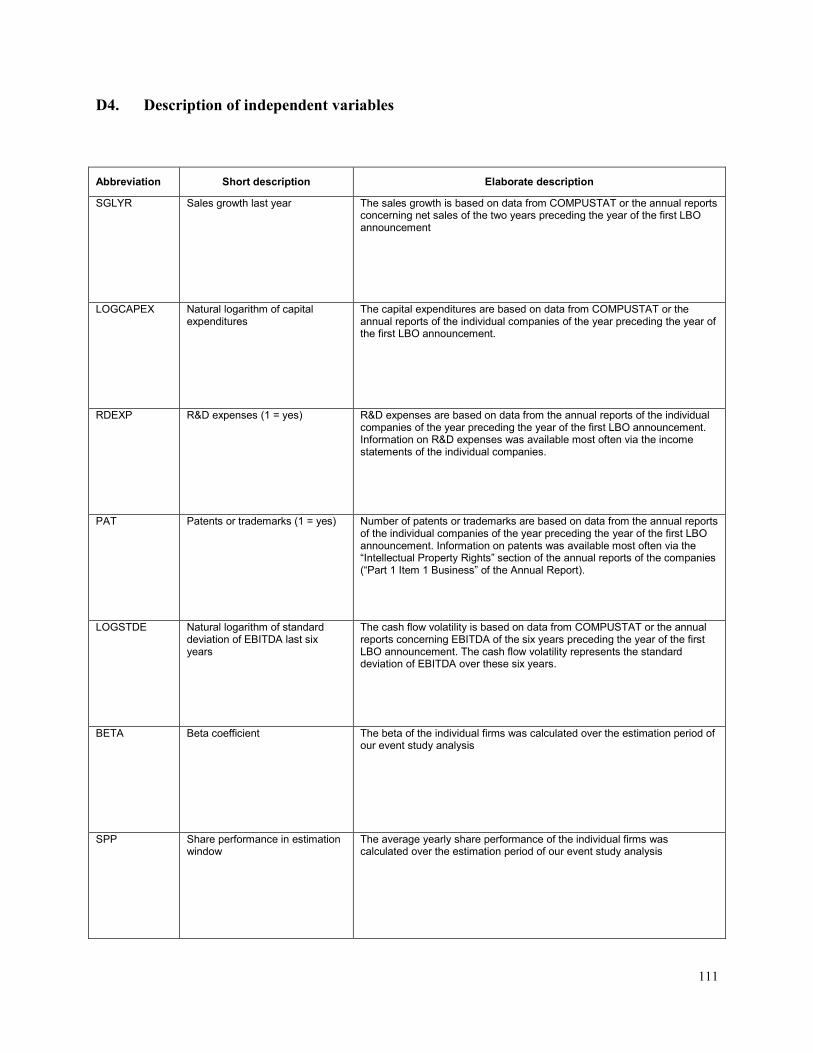

magnitude of a firm‟s investment opportunities by four variables: (1) sales growth, (2) capital

expenditures, (3) research and development expenses, and (4) the number of patents or

trademarks a firm possesses. We build upon the real options literature where investments today

are perceived as opportunities to generate returns tomorrow (Luehrman, 1998; Copeland and

29

Antikarov, 2003) to support our methodology of measuring investment opportunities by the

investments firms made in the recent past. First of all, we believe that historical sales growth can

measure the magnitude of a firm‟s investment opportunities as (sales) growth often is a result of

investments made in the past. Pindado and Rodrigues (2005: 348), for example, anticipate that

the investment opportunities of a firm will influence a firm‟s future sales growth. Nash et al.

(2003: 211) find that high investment opportunity firms are characterized by a significantly

higher sales growth than firms with less investment opportunities in a study of the costs and

benefits of restrictive covenants. Del Monte and Papagni (2003: 1003-1014) find the sales

growth rate of firms with R&D expenditures to be higher than that of firms without R&D

expenditures. Second, we believe that the amount of capital expenditures of a firm is a good

measure of the magnitude of a firm‟s investment opportunities. According to John and Mishra

(1989, 837), namely, capital expenditures represent levels of current investment. Additionally,

capital expenditures are purchases of new property, plant and equipment of firms and are

depicted as cash required for investment activities on a firm‟s cash flow statement (Berk and

DeMarzo, 2007: 33). The expenditures can be qualified as investment opportunities since their

goal is to generate positive future cash flows or, in other words, to create value in the future.

Finally, we believe the R&D expenditures of firms and the number of patents or trademarks that

firms possess to be a valid measure of the magnitude of a firm‟s investment opportunities. Nash

et al. (2003: 211), for example, find that high investment opportunity firms are characterized by

significantly higher R&D expenditures than firms with less investment opportunities. In addition,

Gaver and Gaver (1993), Chung and Charoenwong (1991), Gilson (1997) and Skinner (1993)

also measure investment opportunities with R&D expenses. A patent confers firms perfect

appropriability or a monopoly position for a self-developed product for a limited amount of time

30

(Levin et al., 1987: 783). Consequently, because of a patent firms are able to reap the benefits of

R&D activities. As a result, acquiring a patent can be interpreted as an investment of firms to

generate positive returns in the future. According to Landes and Posner (1987: 268) a trademark

is a word, symbol, or other signifier used to distinguish a good or service produced by one firm

from the goods or services of other firms. Consequently, a trademark protects the name a

company has invested in for probably several years on the basis of which it is often able to sell

more of its products than competitors or to sell products at a premium in relation to competitors.

As a result, acquiring a trademark can be interpreted as an investment of firms to generate

positive returns in the future too.

Hypothesis 1: The abnormal returns on a target firm‟s stock during the period surrounding a

LBO announcement are negatively related to the magnitude of a firm‟s investment opportunities,

measured either by sales growth, capital expenditures, research and development expenses, or

the number of patents or trademarks a firm possesses.

The exact hypothesis formulated above has never been tested directly before. There is, however,

some theoretical and indirect evidence. We interpret empirical evidence on the notion that

financial distress costs differ across firms and on the notion that firms incurring the highest

financial distress costs are the least likely to adopt non-conservative capital structures as such

indirect evidence. In a theoretical study Gamba and Triantis (2008: 2263) show that the value of

financial flexibility depends positively on a firm‟s growth potential, which we belief to measure

up to a certain extent by a firm‟s historical sales growth. Bartram et al. (2009: 17), show that

firms who use derivatives are characterized with lower capital expenditures. Since derivative

31

users are likely to have a higher need for financial flexibility, this finding indicates that firms

with a higher need for financial flexibility employ less investment activities measured by a firm‟s

capital expenditures. The finding suggests that firms who have a higher need for financial

flexibility are slowed down in their investment activity by financial inflexibility, which

obviously will affect firm value negatively. Opler and Titman (1994: 1015) find that highly

leveraged firms lose substantial market share to their more conservatively financed competitors

in industry downturns. In addition, Opler and Titman (1994: 1037) show that these indirect

financial distress costs are more pronounced for firms with high R&D expenditures and for firms

operating in more concentrated and more competitive industries. Consequently, Opler and

Titman provide indirect evidence that the value of financial flexibility differs across firms. In

addition, Opler and Titman (1993: 1985) find that firms with high expected costs of financial

distress, i.e. firms characterized by high R&D expenditures, are less likely to undertake

leveraged buyouts. Since a LBO leads to a severe deterioration in a firm‟s capital structure, i.e. a

firm‟s capital structure becomes less conservative because of a LBO, one can interpret the

findings of Opler and Titman as indirect evidence on the notion that certain firms, namely those

firms with high R&D expenditures, are less willing to adopt a non-conservative capital structure

since these firms are characterized by high expected costs of financial distress.

§2.2.2 The cash flow volatility hypothesis

In paragraph 2.1 we concluded that firms characterized by a higher cash flow volatility than

other firms value financial flexibility more. We believe the cash flow volatility of firms can be

measured by the following two variables: (1) the standard deviation of a firm‟s EBITDA over a

recent time period, and (2) the beta coefficient of a firm‟s security. First of all, we believe the

32

standard deviation of a firm‟s EBITDA over a recent time period to be a good measure of a

firm‟s cash flow volatility as EBITDA can be interpreted as a rude measure of a firm‟s cash flow

since it reflects the cash a firm has earned from its operations (Berk and DeMarzo, 2007: 30). In

addition, EBITDA is used in many other empirical studies as estimator variable of a firm‟s true

cash flow (see for example Stein et al., 2001: 100-109, and Kaplan and Zingales, 1997: 169-

215). Second, we believe we can measure a firm‟s cash flow volatility by the beta coefficient of

a firm‟s security. According to Berk and DeMarzo (2007: 308) the beta of a security is the

sensitivity of the security‟s return to the return of the overall market. The beta actually measures

how much of the variability of the return on a firm‟s stock is due to systematic, market-wide

risks (Berk and DeMarzo, 2007: 308). The beta coefficient thus is not an exact measure of a

firm‟s cash flow volatility. However, since the price of a firm‟s security reflects the present value

of the cash flows a firm is expected to generate in the future (Berk and DeMarzo, 2007: 245)

there certainly is a positive relationship between a firm‟s beta coefficient and its cash flow

volatility. The beta coefficient, however, should be interpreted more as the risk on fluctuations

in a firm‟s cash flow due to fluctuations in the business cycle.

Hypothesis 2: The abnormal returns on a target firm‟s stock during the period surrounding a

LBO announcement are negatively related to the cash flow volatility of a firm, measured either

by the standard deviation of a firm‟s EBITDA over a recent time period, or the beta coefficient

of a firm‟s security.

There is no direct empirical evidence that the value of financial flexibility is larger for more

cash-flow volatile firms. In addition, there neither is indirect empirical evidence on this

33

proposed relationship which shows a positive relation between financial distress costs and cash

flow volatility. Shin and Stulz (2000: 20-21), and Allayannis and Weston (2003: 23-24),

however, report a negative relationship between cash flow volatility and shareholder value,

measured among others by price-to-book ratio. In addition, Smithson and Simkins (2005: 13)

report several studies that associate the usage of derivatives contracts, which are instruments that

reduce cash flow volatility, with higher firm values. We belief that the negative relationship

between cash flow volatility and firm value can be explained to a large extent by the positive

relationship between cash flow volatility and financial distress costs. There are theoretical

studies that confirm the positive relation between financial distress costs and cash flow volatility.

Stein et al. (2001: 102), for example, indicate the most important determinant of distress to be

the variability of cash flows. Consequently, we believe the value of financial flexibility to be

higher for firms characterized by a higher cash flow volatility.

§2.3 Data

Now we have formulated our main hypotheses we can start with explaining the method we use to

test our hypotheses. We begin by describing the dataset we gathered on the basis of which we are

able to test the hypotheses. First of all, we will discuss the sample selection procedure. Then, we

will shortly describe the most important descriptive statistics of our dataset.

§2.3.1 Sample selection and data sources

We retrieved all 160 officially disclosed LBO announcements in the United States from October

2006 until September 2009 from the SDC Platinum Worldwide M&A database ( “SDC”), which

provides detailed information on mergers & acquisitions. We focus on the US market solely

34

because of data availability motives. We focus on the time period October 2006 – September

2009 primarily in order to capture the effects of the financial market turmoil or financial credit

crisis which had its most severe impact on the US stock market between October 2007 and

October 2008 (Brunnermeier, 2009: 77). We do realize that data selection out of this specific

time period may bias our results, as financial flexibility is of more worth to firms in financially

unstable times. However, since the goal of this study is examining the value of financial

flexibility to firms, we see no harm in examining it in a period when firms are expected to need it

the most. In addition, although there is evidence of increased takeover activity since mid 2003

(Martynova and Renneboog, 2008: 2152) until summer 2007, the beginning of the credit crisis,

few economists officially, i.e. in published articles, speak of this period as the sixth merger wave.

As the focus of this study is on examining the value of financial flexibility we do not recognize

the added value of examining this value by studying the period of the „sixth merger wave‟ and

thereby adding to the literature on the wealth effects of LBOs. We chose the end date of the time

period we examine, September 2009, because the market index proxy (CRSP equally-weighted

daily returns on the S&P 500 index) we use to conduct our event studies was only available until

December 31, 2009 at the time we conducted the analysis. Since the maximum event window we

use stretches from 60 transaction days before the announcement date to 60 transaction days after

the announcement date, the end date was set 3 months before December 31, 2009. The starting

date of the time period we examine was set exactly 3 years before the end date.

In relation to other mergers and acquisitions a LBO is a special kind of transaction. For some

firms who are eventually taken over via a LBO, the first takeover announcement does not already

reveal the target firm will be taken over via a LBO, but does only reveal there is takeover interest

35

in the target firm. The announcement that the transaction will be a LBO thus follows later. The

SDC database provides information on both announcements and their corresponding dates. In

addition, the SDC database provides a lot of other information about the proposed transaction:

the transaction value, a deal synopsis, information concerning deal characteristics such as

whether the transaction is a MBO or an IBO, whether the bid was perceived as a hostile bid,

whether there was talk of bidder competition, whether the target firm undertook defensive action,

whether the offer was a tender offer and whether the target firm was in financial distress at the

time of the announcement. The SDC database also provides information on the target firm such

as firm activities and accounting information. Since the accounting data available on the target

firms via the SDC database dispose of many missing variables, we gathered most of the

accounting data of the target firms from the COMPUSTAT database which was accessible for us

via Wharton Research Data Services (“WRDS”). We consulted the annual reports of the target

companies when the COMPUSTAT database contained missing variables for specific firms. The

annual reports were accessible for us via the website of the U.S. Securities and Exchange

Commission (“SEC”). The annual reports can be found in the SEC-filings database where they

are indicated as 10-K filings.

We supplemented the data by also gathering share price data of the target firms, information

concerning the ownership structure of the target firms, information concerning R&D

expenditures of the target firms, information on patents and trademarks possessed by the target

firms and the usage of derivatives by the target firms. We gathered the unadjusted share prices of

our target firms from DataStream via the Ticker Codes reported for the target firms in the SDC

database. We downloaded our market index proxy (CRSP equally-weighted daily returns on the

36

S&P 500 index excluding dividends) and the three-month Treasury Bill rate from the CRSP

database which was accessible for us via WRDS. Data on beneficial ownership by management

or by outside shareholders was collected from the target firm‟s last proxy statement prior to the

LBO announcement. The proxy statement is the official notification to shareholders of matters to

be brought to a vote at a company‟s Annual Meeting (Kole, 1995: 416). In the proxy statement a

firm is obligated to indicate security ownership of management and other beneficial owners for

all owners of five percent or more of the firm‟s voting securities (Kole, 1995: 415). The proxy

statements were also accessible for us via the website of the U.S. Securities and Exchange

Commission (after this: “SEC”). They can be found in the SEC-filings database where they are

indicated as DEF 14A filings. Finally, we retrieved information concerning R&D expenditures of

the target firms, the number of patents possessed by the target firms and the usage of derivatives

(interest rate swaps and other derivatives) by the target firms from the annual reports of these

firms. Especially the data we gathered via the annual reports and the proxy statements of the

target firms make our dataset a unique one as these data are not available in any electronic

database. Unfortunately, we had to exclude 9 firms from our sample of 160 firms, because of

divergent reasons. Hence, we retain a sample of 151 firms. First of all, we had to exclude 5

firms10

from our sample due to data unavailability of their stock prices in the time period

surrounding the LBO announcement. Second, we had to remove 4 firms11

from our sample

because of data unavailability of the SEC filings of these firms.

10

The specific firms are RailAmerica Inc., Brand Energy & Infrastructure Services Inc., Sum Total Systems Inc.,

Exotacar Inc. and MSC Software Corp. 11

The specific firms are North Country Hospitality Inc., Maxim Crane Works Holdings Inc., Loring Ward

International Ltd. and Mercari Communications Group Ltd.

37

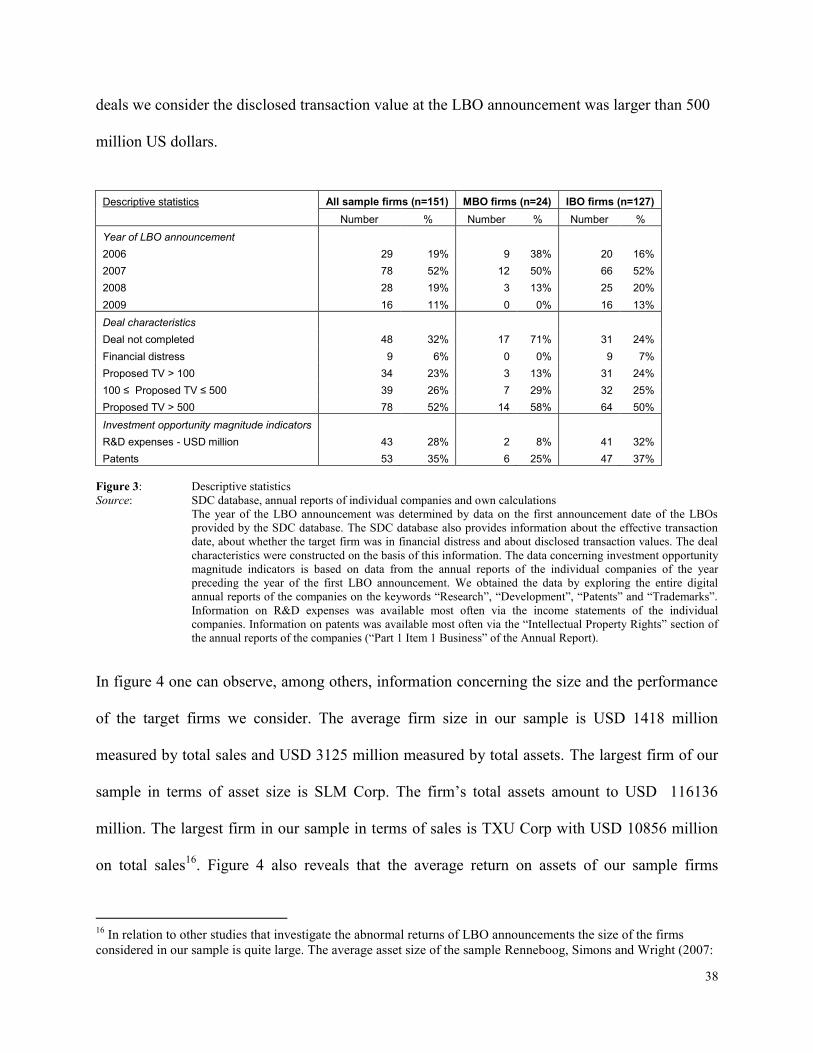

§2.3.2 Descriptive statistics

Figure 3 and 4 display instructive descriptive statistics of the proposed LBO transactions we

consider. The goal of showing these statistics is to provide some background information on the

dataset we use on the basis of which we draw important conclusions12

. In figure 3 one can

observe we were only able to distinguish between MBO transactions and IBO transactions on the

basis of the information provided in the deal synopsis of the SDC database13

. In total, our dataset

contains 127 IBOs and 24 MBOs. Additionally, one can observe in the last row of figure 3 that

we do not only consider the announcements of completed LBO deals, but also the

announcements of LBO deals that were not completed14

. Since we focus on explaining the value

of financial flexibility in this study and not on explaining the wealth effects of completed LBO

transactions, we believe that considering the announcements of not completed deals in addition

to the announcements of completed deals does not create bias in our data sample15

. Figure 3 also

shows that most of the announcements we consider took place in the year 2007. The drop in

takeover activity and consequently in LBO activity in 2008 and 2009 can easily be explained by

the credit crisis. Furthermore, one can observe that our sample contains 9 transactions where the

target firm was in financial distress at the time of the announcement. For more than half of the

12

In Appendix B more elaborate descriptive statistics of the dataset we use are depicted. 13

Consequently, we are not able to indicate whether some of the proposed IBO transactions in our sample are

actually MBIs. 14

We can distinguish the not completed deals from the completed deals, since no effective transaction dates are

given for these deals by the SDC database. In the deal synopsis provided by the SDC database this observation is

confirmed as the synopsis reveals a LBO takeover agreement was officially disclosed, but also that it was later

withdrawn. The announcement dates given by the SDC database for these transactions reflect the announcements of

the LBO takeover agreements and not the announcements of the withdrawals. 15

One could argue that not completed deals could be associated with lower abnormal returns as shareholders could

somehow be able to determine the uncertain character of these announced deals. Nevertheless, we test this

relationship in our regression analysis and we are not able to find a significant negative or positive relationship

between the abnormal returns of the LBO announcements we consider and a dummy variable for not completed

deals. In addition, the cumulative abnormal returns for target firms of completed and non-completed deals are quite

similar. In Appendix E the test and the comparison we just described are depicted.

38

deals we consider the disclosed transaction value at the LBO announcement was larger than 500

million US dollars.

Descriptive statistics All sample firms (n=151) MBO firms (n=24) IBO firms (n=127)

Number % Number % Number %

Year of LBO announcement

2006 29 19% 9 38% 20 16%

2007 78 52% 12 50% 66 52%

2008 28 19% 3 13% 25 20%

2009 16 11% 0 0% 16 13%

Deal characteristics

Deal not completed 48 32% 17 71% 31 24%

Financial distress 9 6% 0 0% 9 7%

Proposed TV > 100 34 23% 3 13% 31 24%

100 ≤ Proposed TV ≤ 500 39 26% 7 29% 32 25%

Proposed TV > 500 78 52% 14 58% 64 50%

Investment opportunity magnitude indicators

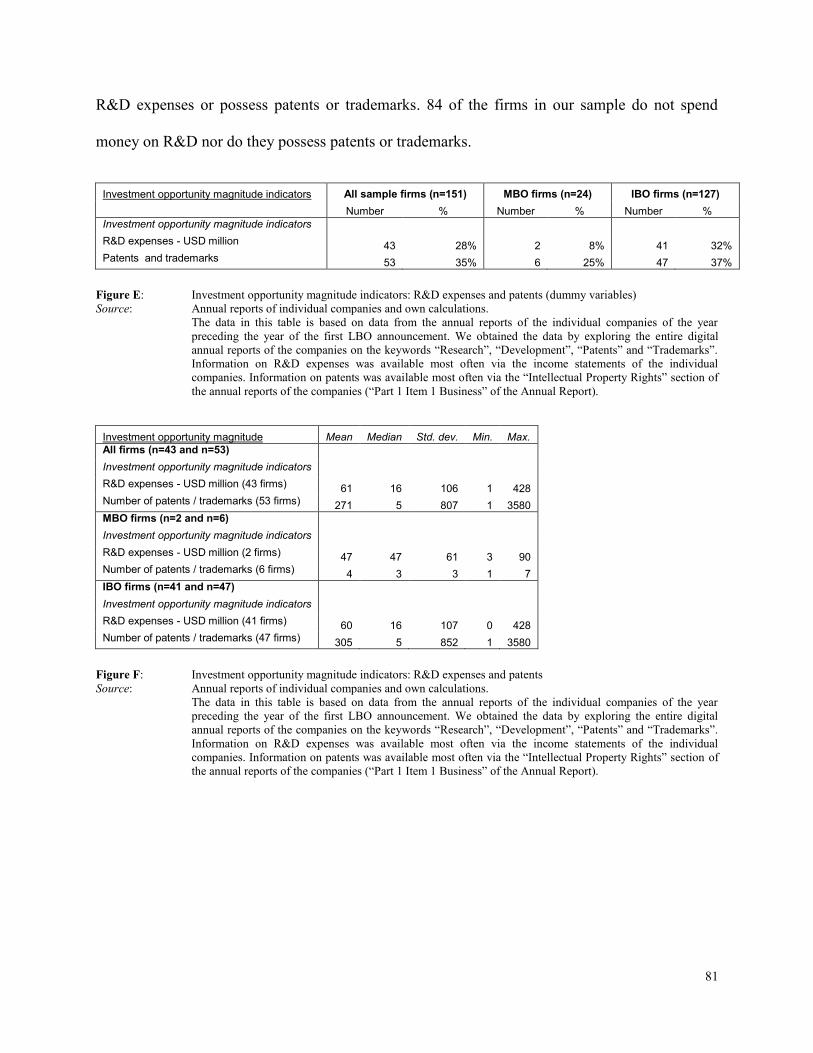

R&D expenses - USD million 43 28% 2 8% 41 32%

Patents 53 35% 6 25% 47 37%

Figure 3: Descriptive statistics

Source: SDC database, annual reports of individual companies and own calculations

The year of the LBO announcement was determined by data on the first announcement date of the LBOs

provided by the SDC database. The SDC database also provides information about the effective transaction

date, about whether the target firm was in financial distress and about disclosed transaction values. The deal

characteristics were constructed on the basis of this information. The data concerning investment opportunity

magnitude indicators is based on data from the annual reports of the individual companies of the year

preceding the year of the first LBO announcement. We obtained the data by exploring the entire digital

annual reports of the companies on the keywords “Research”, “Development”, “Patents” and “Trademarks”.

Information on R&D expenses was available most often via the income statements of the individual

companies. Information on patents was available most often via the “Intellectual Property Rights” section of

the annual reports of the companies (“Part 1 Item 1 Business” of the Annual Report).

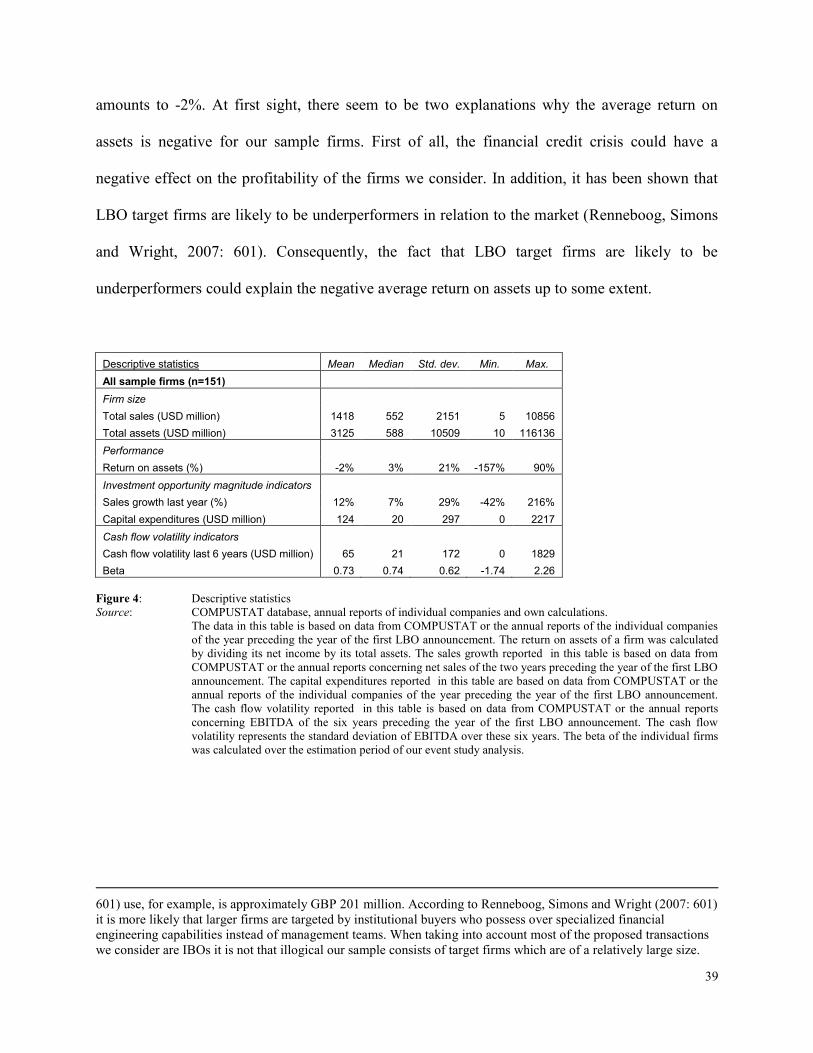

In figure 4 one can observe, among others, information concerning the size and the performance

of the target firms we consider. The average firm size in our sample is USD 1418 million

measured by total sales and USD 3125 million measured by total assets. The largest firm of our

sample in terms of asset size is SLM Corp. The firm‟s total assets amount to USD 116136

million. The largest firm in our sample in terms of sales is TXU Corp with USD 10856 million

on total sales16

. Figure 4 also reveals that the average return on assets of our sample firms

16

In relation to other studies that investigate the abnormal returns of LBO announcements the size of the firms

considered in our sample is quite large. The average asset size of the sample Renneboog, Simons and Wright (2007:

39

amounts to -2%. At first sight, there seem to be two explanations why the average return on

assets is negative for our sample firms. First of all, the financial credit crisis could have a

negative effect on the profitability of the firms we consider. In addition, it has been shown that

LBO target firms are likely to be underperformers in relation to the market (Renneboog, Simons

and Wright, 2007: 601). Consequently, the fact that LBO target firms are likely to be

underperformers could explain the negative average return on assets up to some extent.

Descriptive statistics Mean Median Std. dev. Min. Max.

All sample firms (n=151)

Firm size

Total sales (USD million) 1418 552 2151 5 10856

Total assets (USD million) 3125 588 10509 10 116136

Performance

Return on assets (%) -2% 3% 21% -157% 90%

Investment opportunity magnitude indicators

Sales growth last year (%) 12% 7% 29% -42% 216%

Capital expenditures (USD million) 124 20 297 0 2217

Cash flow volatility indicators

Cash flow volatility last 6 years (USD million) 65 21 172 0 1829

Beta 0.73 0.74 0.62 -1.74 2.26

Figure 4: Descriptive statistics

Source: COMPUSTAT database, annual reports of individual companies and own calculations.

The data in this table is based on data from COMPUSTAT or the annual reports of the individual companies

of the year preceding the year of the first LBO announcement. The return on assets of a firm was calculated

by dividing its net income by its total assets. The sales growth reported in this table is based on data from

COMPUSTAT or the annual reports concerning net sales of the two years preceding the year of the first LBO

announcement. The capital expenditures reported in this table are based on data from COMPUSTAT or the

annual reports of the individual companies of the year preceding the year of the first LBO announcement.

The cash flow volatility reported in this table is based on data from COMPUSTAT or the annual reports

concerning EBITDA of the six years preceding the year of the first LBO announcement. The cash flow

volatility represents the standard deviation of EBITDA over these six years. The beta of the individual firms

was calculated over the estimation period of our event study analysis.

601) use, for example, is approximately GBP 201 million. According to Renneboog, Simons and Wright (2007: 601)

it is more likely that larger firms are targeted by institutional buyers who possess over specialized financial

engineering capabilities instead of management teams. When taking into account most of the proposed transactions

we consider are IBOs it is not that illogical our sample consists of target firms which are of a relatively large size.

40

Finally, figure 3 and 4 report information about the magnitude of the investment opportunities

and about the cash flow volatility of the target firms in our sample, which are, in fact, the most

important variables in our analysis as it are key inputs for testing our hypotheses. One can

observe in figure 4 that the average sales growth, measured over the two years preceding the year

of the (first) LBO announcement, of our target firms was 12%. Although we cannot compare this

number to firms that were not involved in a LBO takeover process, the number seems rather

high. The high growth in sales observed among the firms in our sample suggests high growth

firms are more likely targets for LBOs. In addition, figure 4 indicates average capital

expenditures to be USD 124 million, average cash flow volatility over the 6 years preceding the

year of the (first) LBO announcement to be USD 65 million and an average beta coefficient of

0.73 for our sample firms. The average beta coefficient observed is lower than one, which

indicates the stock returns of our sample firms are less prone to swings in the business cycle than

the average firm. Figure 3 shows how many firms in our sample spend money on research and

development and how many firms possess patents or trademarks. One can observe that 43 firms

in our sample have positive R&D expenses and 53 firms in our sample possess patents or

trademarks. The firms that have positive R&D expenses often do also possess patents or

trademarks, which is not surprising as patents and trademarks are only filed for when serious

research and development activity has taken place already. In total, 67 of the firms in our sample

have positive R&D expenses or possess patents or trademarks. 84 of the firms in our sample do

not spend money on R&D nor do they possess patents or trademarks.

41

§2.4 Empirical techniques

In the previous section we described the data selection procedure, we described the different data

sources we have used in order to gather our data and we provided some informative descriptive

statistics of our dataset. In this section we describe the empirical techniques we used to analyze

the data we gathered in order to test whether the hypotheses we formulated in section 2.2

empirically hold. We employed two empirical techniques for our data analysis: (1) event studies,