The Recent Spike in Illicit Tobacco Trade in South Africa Dissertation submission to the Department of Economics of the University of Cape Town in partial fulfilment of the requirements for the Masters Specialising in Economic Development programme Student: Zeenat Ebrahim Student Number: EBRZEE005 Supervisor: Professor Corné van Walbeek Date: 7 February 2019 I gratefully acknowledge the funding received by the African Capacity Building Foundation, which is in turn is funded by the Bill & Melinda Gates Foundation. University of Cape Town

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

The Recent Spike in Illicit Tobacco Trade in South Africa

Dissertation submission to the Department of Economics of the University of Cape Town in

partial fulfilment of the requirements for the Masters Specialising in Economic Development

programme

Student: Zeenat Ebrahim

Student Number: EBRZEE005

Supervisor: Professor Corné van Walbeek

Date: 7 February 2019

I gratefully acknowledge the funding received by the African Capacity

Building Foundation, which is in turn is funded by the Bill & Melinda Gates Foundation.

Univers

ity of

Cap

e Tow

n

The copyright of this thesis vests in the author. No quotation from it or information derived from it is to be published without full acknowledgement of the source. The thesis is to be used for private study or non-commercial research purposes only.

Published by the University of Cape Town (UCT) in terms of the non-exclusive license granted to UCT by the author.

Univers

ity of

Cap

e Tow

n

ii

Table of Contents

Abstract ........................................................................................................................... 1

1 Introduction.............................................................................................................. 2

2 Literature Review...................................................................................................... 4

2.1 General motives behind the illicit supply of tobacco ..................................................... 5

2.2 Industry complicity in illicit tobacco supply................................................................... 8

2.3 Industry complicity: The South African context ........................................................... 12

3 Research Methods .................................................................................................. 14

3.1 Research design......................................................................................................... 14

3.1.1 Methodology: Semi-structured key informant interviews ........................................................... 14

3.2 Ethical considerations ................................................................................................ 20

4 Results .................................................................................................................... 21

4.1 Overview of the South African tobacco industry (1990 to 2009/10) ............................. 23

4.2 The disruption of the traditional tobacco market status quo (from 2009/10) ............... 27

4.2.1 Industry transformation and the role of informal markets .......................................................... 29

4.2.2 Methods to transform the tobacco industry: DTCs’ perspective.................................................. 33

4.3 Suspicions of industry complicity in illicit tobacco trade (from 2012 to 2014)............... 37

4.4 The unravelling of the multi-layered tobacco industry (from 2014).............................. 40

4.5 Under-declared production and its impact on excise revenue (from 2015)................... 42

4.5.1 DTCs: internal shifts in power dynamics....................................................................................... 44

4.6 MTCs recent tactics.................................................................................................... 47

4.6.1 Threats posed by government...................................................................................................... 47

4.6.2 Threats posed by competitors ...................................................................................................... 49

5 Discussion ............................................................................................................... 55

6 Conclusion .............................................................................................................. 59

7 References .............................................................................................................. 60

8 Appendices ............................................................................................................. 68

iii

Appendix A: Sample Interview Guide .............................................................................. 68

Appendix B: Information Sheet and Consent Form........................................................... 71

Appendix C: Ethics Approval ........................................................................................... 73

1

Abstract

Since 2015, the South African National Treasury has experienced declines in tax-paid cigarette

revenues. The declines have been attributed to upward spikes in the illicit tobacco trade. This

dissertation explores the upward spike in the illicit tobacco trade, in order to assess whether

or not a relationship exists between tobacco companies’ actions and the spike in illicit activity.

The study analyses information gathered from semi-structured key informant interviews in

order to derive expert insights into the spike. The results indicate that the tobacco industry

as a whole is using a variety of tactics to protect their interests. This thesis suggests that the

recent increase in the illicit tobacco trade is the result of an increase in under-declared

cigarette production by the tobacco industry, which exploits a weak enforcement of anti-

tobacco laws.

2

1 Introduction

A rising illicit tobacco trade undermines tobacco control policies, resulting in significant

negative consequences for public health and tax revenue (World Health Organization, 2013).

The World Health Organisation’s (WHO) concerns about these negative consequences led to

the expansion of Article 15 of the WHO’s Framework Convention on Tobacco Control (FCTC),

which focuses on combating illicit tobacco products. According to WHO FCTC, ‘The term illicit

tobacco trade is defined as a practice or a conduct prohibited by law which relates to

production, shipment, receipt, possession, distribution, sale or purchase of tobacco products,

including any practice or conduct intended to facilitate such activity.’ Article 15 gave rise to

the WHO FCTC’s first Protocol, the Protocol to Eliminate Illicit Trade in Tobacco Products

(World Health Organization, 2013).

Amongst other factors, the Protocol is aware of the need to control the tobacco supply chain,

owing to the global tobacco industry’s historical involvement in the illicit tobacco trade to

maximise profits (U.S. National Cancer Institute & World Health Organization, 2016, World

Health Organization, 2013). The global tobacco industry has also heavily opposed any threats

to their vested interests by lobbying the government against both tax-based and non-tax

tobacco control measures (Ross, 2015, Ross et al., 2016b, van Walbeek & Shai, 2015).

Since the early 1990s, the tobacco industry has opposed the South African government’s

attempts to use tobacco tax to strengthen tobacco control (van Walbeek, 2005). According to

the tobacco industry, the prime cause of the illicit tobacco trade is the high taxation of

tobacco products, which ultimately impedes the generation of tax revenue (Joossens & Raw,

2012, Kelton & Givel, 2008, van Walbeek & Shai, 2015). van Walbeek & Shai (2015) discuss

the South African tobacco industry’s opposition to rising tobacco taxes and the tactics they

have used to combat tobacco control measures. The South African tobacco industry and

private market research companies have, in the past, published inconsistent and sometimes

exaggerated size and growth estimations, raising questions as to the reliability, credibility,

and motives behind these estimations (Blecher, 2010, Blecher et al., 2015, IARC, 2011, van

Walbeek & Shai, 2015).

3

Despite the tobacco control measures in place in South Africa, from 2015/16 to 2017/18, the

National Treasury began to see a sharp decline in tax-paid cigarette consumption (ETCP,

2018). From 2016, the 20% decline in tax-paid cigarette consumption coincided with increases

in the illicit tobacco trade (Liedeman & Mackay, 2015, van der Zee, van Walbeek & Magadla,

forthcoming 2019).

The downward trend in tax-paid cigarette consumption and associated upward spikes in the

illicit tobacco trade since 2015 have raised questions about the tobacco industry’s possible

role in illicit tobacco activity. Historical evidence of exploitative illicit tobacco practices by the

tobacco industry makes it imperative that more research be conducted in order to understand

the extent and magnitude of the illicit tobacco trade in low-and middle-income countries,

including South Africa (World Health Organization, 2013).

This thesis explores the recent upward spike in the illicit tobacco trade in South Africa, in order

to assess whether or not a relationship exists between tobacco companies and the spike in

illicit activity. The study analyses information obtained from semi-structured key informant

interviews, which were used to derive expert insights regarding the motives behind the spike

in illicit tobacco trade. This study considers the context of the political economy of tobacco

trade, while remaining grounded in economic theory. The results could potentially contribute

to government decision-making on tobacco control policies, tax revenue, and law

enforcement.

This paper is structured as follows: Section Two discusses existing literature on industry

complicity in the supply of illicit tobacco at a global and domestic level. Section Three

describes the research design of the study, why it was chosen, and how it was applied. The

section also explains how the data was handled and analysed and the associated limitations.

Section Four discusses how the market entry of competitors, and the strengthening of

government legislation, threatened the interests of the established tobacco industry, and

how they responded. Section Five provides a discussion of the study’s findings followed by a

brief conclusion in Section Six.

4

2 Literature Review

Since the 1990s the South African government has been committed to reducing tobacco

consumption (van Walbeek, 2005). This was first done by using excise taxes1 as a tool to raise

the price of cigarettes (Chaloupka, Straif & Leon, 2011). Successful implementation of

effective tobacco control measures resulted in the country being regarded as a global leader

in tobacco control (Chelwa, van Walbeek & Blecher, 2016). The country’s commitment was

reaffirmed in 2005 when it signed the WHO FCTC (Roemer, Taylor & Lariviere, 2005).

According to the World Health Organization (2003), ‘The WHO FCTC is an evidence-based

treaty that reaffirms the right of all people to the highest standard of health. The WHO FCTC

represents a paradigm shift in developing a regulatory strategy to address addictive

substances; in contrast to previous drug control treaties, the WHO FCTC asserts the

importance of demand reduction strategies as well as supply issues.’ Supply issues were

divided into the licit and illicit supply of tobacco products.

The WHO FCTC recognises the important negative consequences of illicit tobacco supply on

public health and tobacco control measures and has therefore developed the Protocol to

Eliminate Illicit Trade in Tobacco Products (van Walbeek et al., 2013). The Protocol provides a

toolkit for controlling illicit trade, which includes the use of globally integrated monitoring

systems, measures to enhance international cooperation and collaboration, and law

enforcement (World Health Organization, 2013). However, despite the country’s previous

commitment to tobacco control, South Africa has yet to ratify the Protocol. The failure to

ratify sends signals to illicit tobacco suppliers that the government is less committed to the

fight against the illicit tobacco trade.

Since the increase in domestic tobacco companies in South Africa in 2009/10, tobacco

industry participants have accused each other of complicity in supplying illicit tobacco.

Ironically, all of the industry participants have been under suspicion and in some cases found

1 According to the U.S. National Cancer Institute & World Health Organization (2016), excise tax is defined as ‘atax or duty imposed on the sale or production of selected products, such as tobacco products.’

5

guilty, of improper business conduct (Pauw, 2017, van Loggerenberg, 2014, van

Loggerenberg, 2018, van Loggerenberg & Lackay, 2016). This chapter discusses previous

instances of industry complicity in illicit tobacco trade, providing a brief overview of the

general motives behind illicit tobacco supply, followed by global and domestic instances in

which the tobacco industry was found to be complicit in the supply of illicit tobacco.

2.1 General motives behind the illicit supply of tobacco

The illicit tobacco trade is essentially the failure to pay government-imposed tobacco taxes.

The IARC (2011), Ross (2015), U.S. National Cancer Institute & World Health Organization

(2016) describe how the circumvention of taxes can take the form of tax avoidance, which is

legal, and tax evasion, which is illegal. According to Ross (2015), ‘Tax Avoidance includes legal

activities and purchases in accordance with customs and tax regulations, most of which

include the payment of some tobacco taxes and are done mostly by individual tobacco users

(e.g., cross-border shopping, duty-free shopping, Internet and mail/phone purchases), but

tobacco companies also engage in it (e.g. changing some product features or its production

process in order to reduce tax liability).’ On the other hand, tax evasion, according Ross (2015),

is defined as ‘illegal activities intended to avoid paying some or all taxes. It includes smuggling

cigarettes across borders, selling genuine cigarettes that were manufactured illegally, selling

counterfeit or illicit white cigarettes, or selling or buying cigarettes via Internet, phone or mail

without paying the appropriate taxes.’

To date, the majority of scholarly research on the illicit tobacco trade, across several

disciplines, has focused on scope measurements of tax avoidance/evasion, which indirectly

serve as indicators for the measurement of the illicit tobacco trade. Various theoretical

models have been developed to measure the scope of such trade (IARC, 2011, Ross, 2015,

U.S. National Cancer Institute & World Health Organization, 2016). No matter which scope

measurement instruments is used, however, the primary motive for engaging in the illicit

tobacco trade is profit maximisation.

To maximise their profits, illicit tobacco traders often seek out and exploit weaknesses or

vulnerabilities in countries’ economic and political systems. Certain systems can provide the

conditions that make tax circumvention practices easier and thus create the economic

6

incentives for illicit tobacco activity. IARC (2011), Legresley et al. (2008), Nakkash & Lee

(2008), Ross (2015) and U.S. National Cancer Institute & World Health Organization (2016)

identify some of these conditions: tax/price differences and magnitudes, weak tax and

customs administration and control, weak governance, corruption, duty-free shops and trade

free zones, illicit trade routes, informal distribution networks, affordability of tobacco

products, political instability and tobacco industry involvement.

As demonstrated by Ross et al. (2016a), the tobacco industry has engaged in elaborate tax

avoidance strategies in order to circumvent tobacco control mechanisms, particularly high

tobacco taxes. Some of these strategies include:

Flooding the market with a product before a new tax is imposed, thus encouraging

stockpiling. The difference in tax levels provides a profit opportunity for the

manufacturer or importer.

Exploitation of complex non-uniform tax structures. This can lead to the tobacco

industry manipulating tax systems and circumventing the prescribed taxes by

adjusting products or production processes so that products can be re-classified to a

lower tax category. Non-uniform tax structures for products may prompt tobacco

manufacturers to adjust their pricing models, lowering prices on products aimed at

price-sensitive consumers while increasing prices on products aimed at less price-

sensitive consumers.

Lowering cigarette prices, which tends to drive tobacco volume sales, increasing

tobacco consumption as cigarettes become more affordable to a wider market.

Optimising on profits by raising the net-of-tax price on products in line with, or in

excess of, the increase in tax rate, and thereafter lobbying against further government

increases in taxes. By contrast, tobacco manufacturers may also reduce their profit

margins relative to the tax rate in order to increase sales volumes so as to preserve

their original profit margins; this is more likely to affect economy than premium

brands.

Reducing the quantity of product per pack, so as to maintain the price per pack, thus

preserving the perceived affordability of the pack.

7

Reducing tax liability and profit margins by lowering products’ prices so as to influence

ad valorem excise taxes, since excise taxes are calculated as a function of the retail

price.

South Africa provides a clear example of the tobacco industry’s influence on excise rates as a

result of multinational tobacco companies (MTCs) controlling retail prices. Van Walbeek

(2010) indicated how, historically, the South African government had been successful in

reducing cigarette consumption and raising tax revenues through the imposition of excise

taxes. In response to the rise in excise taxes, however, the tobacco industry, mainly through

its representative body, the Tobacco Institute of Southern Africa (TISA) 2, heavily lobbyied

against increases in the excise tax. They believe that a strong positive relationship existed

between excise taxes and the illicit tobacco trade (Rowell, Evans-Reeves & Gilmore, 2014, van

Walbeek & Shai, 2015).

2 According to their website, ‘The Tobacco Institute of Southern African (TISA) was established in 1991 and is anon-profit organisation representing the major tobacco manufacturers and tobacco farmers in South Africa.Main business: Representative of the non-commercial, common interest of manufacturers and marketers oftobacco products as well as the tobacco growers in South Africa.’ At the time of writing the members of TISAincluded British American Tobacco South Africa, Philip Morris South Africa, JT International South Africa, ClippaSales, OTP Distributors, Imperial Tobacco Southern Africa, Universal Leaf South Africa, Dimon South Africa,Tobacco Traders and LTP Tobacco.

8

2.2 Industry complicity in illicit tobacco supply

Historical MTC complicity in the illicit tobacco trade has been found in Africa, the Middle East,

Europe, Asia, and the Americas (Joossens & Raw, 2008, Joossens & Raw, 2012, Joossens et al.,

2016, Kelton & Givel, 2008, Lee & Collin, 2006, Legresley et al., 2008, Nakkash & Lee, 2008).

Kelton & Givel (2008) discuss how the ‘1998 legal settlement in the case of State of Minnesota,

et al., v. Philip Morris, Inc., et al. and the subsequent 1998 Master Settlement Agreement’,

resulted in the release of previously undisclosed tobacco-industry documents. These

documents exposed the intricate tax evasion practices of MTCs and the role of smuggling. The

nature of smuggling has changed over time, from large to small batches of illicit tobacco

moving across borders. What has remained consistent during this time, however, is MTCs

complicity in either supplying illicit tobacco or the failing to control their supply chains,

despite knowing that their products were destined for illicit markets (Joossens et al., 2016).

Large-scale smuggling by MTCs has, in some instances, led to MTCs’ own admission of

complicity (Joossens & Raw, 2008, Kelton & Givel, 2008). A letter sent by president and CEO

of Imperial Tobacco Ltd, Don Brown, to a senior executive of Imperial Tobacco Ltd in 1993 (as

cited by Kelton & Givel, 2008) states that: “As you are aware, smuggling cigarettes (due to

exorbitant tax levels) represents nearly 30% of total sales in Canada, and the level is growing.

Although we agreed to support the Federal government’s effort to reduce smuggling by

limiting our exports to the U.S.A., our competitors did not. Subsequently, we have decided to

remove the limits on our exports to regain our share of Canadian smokers. To do otherwise

would place the long-term welfare of our trademarks in the home market at great risk. Until

the smuggling issue is resolved, an increasing volume of our domestic sales in Canada will be

exported, then smuggled back here for sale.” According to the chairman of BAT in 2000 (as

cited by Joossens & Raw, 2008), ‘‘Where any government is unwilling to act or their efforts

are unsuccessful, we act, completely within the law, on the basis that our brands will be

available alongside those of our competitors in the smuggled as well as the legitimate

market.”

In many instances MTCs have not been held accountable or been sufficiently penalized for

questionable behaviour (Joossens & Raw, 2008, Joossens et al., 2016, Kelton & Givel, 2008).

9

In fact, Philip Morris International (PMI), Japan Tobacco International (JTI), British American

Tobacco (BAT), and Imperial Tobacco Limited (ITL), in an attempt to avoid litigation, signed

various agreements with the European Union (EU) to fight collaboratively against the illicit

tobacco trade. The agreements themselves contained loopholes, which protected MTCs from

the consequences of complicity in supplying illicit tobacco (Joossens et al., 2016).

Industry complicity in Canada remains one of the most notorious instances of tobacco

smuggling. Beginning in the 1980s, Canadian tobacco manufacturers exported tobacco

products to the United States (US) and thereafter illegally reimported the products via Native

American reservations and Canadian First Nation reserves. This was done in order to take

advantage of tax/price differentials between the two countries (Kelton & Givel, 2008). In the

1990s, local tobacco manufacturers in Canada actively participated in smuggling, exporting

cigarettes to the US and smuggling the cigarettes back into Canada without any leakage into

the US domestic market (Joossens & Raw, 2008, Joossens & Raw, 2012). According to Joossens

& Raw (2008) and the U.S. National Cancer Institute & World Health Organization (2016), in

2008, Canadian tobacco manufacturers, ITL, and Rothmans Benson and Hedges pleaded guilty

to illicit tobacco trading between 1989 and 1994. The companies were fined CA$1.5 billion

for illicit tobacco activity. In a similar case, according to Joossens & Raw (2008), significant

quantities of two ITL brands, Regal and Superkings, were exported from the UK to Latvia,

Kalingrad, Afghanistan, Moldova and Andorra, and a large proportion of the exports were

illegally smuggled back into the UK.

In the late 1990s and early 2000s, the European governments and European Community

suspected that American tobacco companies, specifically PMI and RJ Reynolds, were taking

advantage of tax/price differentials between countries by exporting American cigarette

brands to countries with lower tobacco taxes, and then illegally smuggling products back into

the US (Joossens & Raw, 2008, Joossens et al., 2016). According to Joossens et al. (2016),

the EU alleged in 2002 that RJ Reynolds were engaging ‘in organised crime, money laundering

and narcotics trafficking and in transactions that financed both the Iraqi regime under Saddam

Hussein and terrorist groups’. There have also been numerous instances of cigarettes which

have been produced in one country and consumed in another country, without the necessary

10

taxes been paid, such as illicit whites.3 According to Joossens & Raw (2012), illicit whites

dominated cigarette consumption in Libya and were produced in Luxembourg and Bulgaria.

Another example is the Jin Ling brand which was produced in Russia and consumed within

the EU (Joossens & Raw, 2012). In 2014, BAT was fined £650 000 by UK tax authorities for

over-supplying their brands to the Belgian market (Joossens et al., 2016).

Since the 1980s, the global tobacco giant, BAT, has engaged on numerous occasions in various

forms of illicit tobacco trade in pursuit of their strategic corporate objectives (Gilmore, AB &

McKee, M, 2004, Gilmore, AB. & McKee, M., 2004, Lee & Collin, 2006, Legresley et al., 2008).

Smuggling has been used as a strategy to gain entry into otherwise restricted markets and to

compete for market share. Such practices have been observed in Asia, the former Soviet

Union, the Middle East, and Africa, among others (Gilmore, AB & McKee, M, 2004, Gilmore,

AB. & McKee, M., 2004, Lee & Collin, 2006, Legresley et al., 2008). A number of studies

(Joossens et al. (2016), Kelton & Givel (2008), Legresley et al. (2008), Nakkash & Lee (2008),

Rowell, Evans-Reeves & Gilmore (2014) that have analysed newspaper articles, company

document depositories, tobacco company press releases, court judgements, and litigation

show how MTCs have either been complicit in the illicit tobacco trade or have used media

platforms to influence stakeholders’ understanding of the nature and magnitude of the illicit

tobacco trade.

Collin et al. (2004), whose study included the analysis of confidential documents from BAT’s

Guildford depository,4 argued that the evidence indicated that, in order to gain access to

restricted markets, BAT smuggled tobacco products into Burma, Vietnam, Thailand, and

Bangladesh. Nakkash & Lee (2008) show how BAT and PMI, in an attempt to gain access to -

and expand - market share, took advantage of weak governance and political unrest during

the Lebanese civil war. The war resulted in the eradication of local cigarette production and

led to the influx of contraband to the Lebanese market. Even after the civil war ended in the

3 Ross et al., (2016) define illicit/cheap whites as, ‘cigarettes manufactured by legitimate business enterprises,but a large share of the production is sold illegally outside the jurisdiction where they are produced.’4 The Guildford depository is a collection of documents which contain detailed activities of the tobacco industry;it is located in the United Kingdom and is run by BAT.

11

1990s, BAT continued to supply the Lebanese tobacco market with licit and illicit cigarettes.

BAT also exploited transition economies, such as the former Soviet Union (FSU), which it used

to gain entry into the Chinese market (Gilmore, AB. & McKee, M., 2004). In line with their

corporate objectives and in an attempt to penetrate the lucrative Chinese market, BAT used

a variety strategies to overcome barriers to entry, including restructuring their Asian business

divisions, so as to supply private traders and to control prices (Lee & Collin, 2006).

The African continent has not been free from illicit tobacco activities. Legresley et al. (2008),

in an analysis of BAT documents from the Guildford depository and the BAT Document

Archive, indicated that at least 40 of 54 African countries were exposed to smuggling and that

smuggling formed a key part of the company’s corporate strategy. They also show that BAT

took advantage of the opportunities available for illicit activity in Zaire (DRC), Togo, Ghana,

and Angola. A study of BAT’s Guildford depository, conducted by Wen et al. (2006) and Collin

et al. (2004), indicated that other leading global tobacco companies were also complicit in

illicit tobacco activity. BAT documents also revealed PMI’s proposed plans to engage in illicit

activity in Nigeria to support their arguments against government increases in taxes

(Legresley et al., 2008).

MTCs have, over decades, been complicit in the illicit tobacco trade despite collaborating with

governments and various agencies in the fight against it. These practices have cast doubt on

the credibility of their role in the fight against the illicit tobacco trade. Many scholars have

appealed to the WHO FCTC and governments to reject industry interference as part of their

commitment to eliminate the illicit tobacco trade (Legresley et al., 2008, Nakkash & Lee,

2008, Rowell, Evans-Reeves & Gilmore, 2014). It is also stressed in Article 5.3 of the FCTC

which requires “Parties to protect their tobacco control and public health policies from

commercial and other vested interests of the tobacco industry” (van Walbeek & Filby, 2018).

12

2.3 Industry complicity: The South African context

According to van Loggerenberg (2018) and van Loggerenberg & Lackay (2016), tobacco

smuggling has been a lucrative business in South Africa since 1994, and by 2013 ‘had reached

epidemic proportions’. Van Loggerenberg & Lackay (2016) indicated that, in 2008, South

African Revenue Services (SARS) confiscated 45 million illicit cigarettes from Masters

International Tobacco Manufacturing. The controversial owner of the business was linked to

the South African Arms deal (van Loggerenberg, 2018, van Loggerenberg & Lackay, 2016).

According to Corruption Watch (2018), ‘The Arms deal was not a single event, but rather a

series of corruption scandals and cover-ups’.

Escalating illicit activity within the country prompted a SARS investigative unit to probe into

the modus operandi of the illicit tobacco value chain (Project Honey Badger). Their findings

indicated the possibility of unlawful business practices by fifteen tobacco companies (Pauw,

2017, van Loggerenberg, 2018, van Loggerenberg & Lackay, 2016). Investigations also

exposed a complex and intricate network of money, which was sourced from smuggling

activities, and which was used to pay “influential businessmen, gangsters and politically

connected individuals” (Pauw, 2017). A domestic tobacco company, Carnilinx, was found

guilty of unpaid taxes. SARS seized ‘over R200 million worth of illicit tobacco’ and an affidavit

by Carnilinx indicated that ‘the company unlawfully and wrongfully smuggled two tonnes of

tobacco every week for 40 weeks to avoid paying excise duty’ (Pauw, 2017:193). They were

not the only participants in the underground illicit tobacco world: British American Tobacco

South Africa (BATSA) was exposed in the media for using spies to infiltrate government

agencies and report on their competitors’ businesses (Walter, 2015).

From 2015, South Africa’s tobacco economy was revealed to be multi-layered, in that it

involved corruption, tobacco industry state infiltration, and industry espionage. These had

significant negative consequences for the country both economically and politically. The

National Treasury’s Budget Review reveals that, since 2015, the country witnessed a sudden

decline in tax-paid cigarettes which could not be attributed to economic factors entirely and

indicated an increase in the trading of illicit tobacco (van Walbeek, 2014). Studies by van der

Zee, van Walbeek & Magadla (forthcoming 2019) show how the proliferation of low-

13

priced/illicit cigarettes penetrated all racial and socio-economic groups in South Africa. Case

studies by Liedeman & Mackay (2015) indicate the increased availability of illicit cigarettes in

Delft, Cape Town, between 2010/11 and 2015.

The change in conditions that allowed illicit tobacco to flourish from 2015 was linked to the

appointment of the new SARS commissioner, Tom Moyane, in 2014. Moyane’s leadership

decisions severely weakened SARS law enforcement capacity, resulting in conditions that

allowed undeclared cigarette production to thrive (Pauw, 2017). During his time as SARS

commissioner, the tax authority witnessed leadership purges and multiple state commissions

of inquiry into SARS, including SARS tax administration and governance.

The “epidemic proportions” of the illicit tobacco trade mentioned by van Loggerenberg &

Lackay (2016) in 2013 was dwarfed by subsequent developments. A 2018 Ipsos study,

commissioned by the Tobacco Institute of Southern Africa (TISA), showed that undeclared

cigarette production was spiralling out of control, with three out of four non-organised shops5

selling cigarettes below the amount of the combined excise tax and VAT (TISA, 2018b). The

cigarettes were deemed to be illicit, as the full tax could not have been paid on them. The

study also identified a domestic tobacco manufacturer, Gold Leaf Tobacco Company, as the

main perpetrator, claiming that they accounted for 75.1% of sales at a price below the cost of

the taxes. A follow up study conducted by Ipsos in the latter part of 2018 indicated that, within

three months, illicit trade in the informal market increased from 33% to 42% (TISA, 2018a).

Given the tobacco industry’s history of avoiding, and at times evading, the tobacco tax, this

thesis looks at the factors behind the recent upward spike in the illicit tobacco trade in South

Africa. The section that follows will specify the qualitative methods used.

5 According to the Ipsos study, non-organised shops included ‘independent small and medium businesses,including spazas, general dealers, corner cafes and hawkers”, excluding “mobile hawkers, taverns and shebeens”.

14

3 Research Methods

The aim of this study is to explore the recent upward spike in the illicit tobacco trade in South

Africa. A qualitative method, using data collection and analysis was deemed most appropriate

for this study. This took the form of semi-structured key informant interviews. This section

details the method used and is structured as follows: first a brief overview of the chosen

research design will be given, followed by a detailed description of the application of the

research design. The section will close with a discussion of ethical considerations.

3.1 Research design

One research design was applied to this study.

3.1.1 Methodology: Semi-structured key informant interviews

To explore and better understand the underlying motives behind the recent upward spike in

the illicit tobacco trade, semi-structured interviews with key informants6 were conducted so

as to gain insights into the local context of the illicit tobacco market. Given the highly complex

and sensitive nature of the illicit tobacco market, a flexible research instrument was

considered necessary to collect the primary data.

According to Ross (2015), U.S. National Cancer Institute & World Health Organization (2016)

and IARC (2011), interviewing key informants who have expert knowledge related to the

nuances of licit and illicit tobacco activity is a widely-used and recommended approach to

measure the scope of the illicit tobacco trade. This approach, however, has been less used in

the South African context, particularly because of the sensitive nature of the subject matter.

There are currently no South African academic studies that have used this approach (Ross,

2015).There are, however, private market research companies who have adopted this

approach to inform their assumptions and estimations regarding the market sizes and shares

of various industries. This information is thereafter sold for market research purposes.

6 The words key informant and research subjects will be used interchangeably throughout this paper.

15

Key informant interviews in this study are not used to determine which interviewee narratives

are correct, but merely to understand the socio-economic context that allows the illicit

tobacco trade to flourish in South Africa. The purpose is to delve into the social construction

of the illicit tobacco market in order to gain a deeper understanding of stakeholder

engagement in such activities, from a supply perspective. This information is expected to build

on the local knowledge base of the economics of tobacco control, so that a greater pool of

information is available for economic decision-making purposes.

Key informants, who work within - or who have expert knowledge of - the tobacco industry,

were interviewed in order to obtain primary data and gain expert insights into the tobacco

industry. Since these interviews were conducted on human subjects, ethics clearance was

required and obtained (see Appendix C).

The research design used in this study has been previously applied locally and internationally

in the field of tobacco control and public health. Tam & van Walbeek (2014) used semi-

structured interviews in a Namibian case study, ‘to illustrate challenges faced by low-income

countries working to forward tobacco control legislation’. Skafida et al. (2014) also applied

key informant interviews ‘to determine how transnational tobacco companies tried to

penetrate the Bulgarian cigarette market and influence tobacco excise tax policy after the fall

of communism and during Bulgaria’s accession to the European Union’. The next section will

explain in detail the application of the research design.

Research Instrument: Semi-structured key informant interviews - Primary data

Semi-structured interviews were selected as the appropriate research instrument for this

study since these allow for more digression than structured interviews. The fixed format of

structured interviews is restrictive as it does not allow for sufficient follow-up and probing of

interviewee responses. Probing for further clarification was imperative in this study because

it allowed the researcher to establish the interviewee’s comprehension of the question, and

how it was being interpreted in the answers, to direct questioning to what was said, to get

clarification of the decision/estimation process, and to extract complete narratives in the

responses (Qu & Dumay, 2011). Probing forms an essential part of investigating markets

where deep questioning is essential in order to arrive at reliable conclusions about specific

16

subjects. The aim of the semi-structured interviews of key informants who have expert

knowledge was to assess whether or not a relationship exists between tobacco companies’

actions and the recent upward spike in the illicit tobacco trade.

The research process involved the following steps:

1. Development of semi-structured interview questions (see Appendix A: Sample

Interview Guide).

2. Development of interviewing follow-ups and probes.

3. Development of a key informant sample list.

4. Contacting and securing interviews at a specific date and time.

5. Conducting semi-structured interviews.

6. Collating data.

7. Analysis of results.

As suggested by IARC (2011), Ross (2015) and U.S. National Cancer Institute & World Health

Organization (2016), research subjects were selected from role players across the tobacco

value chain, tobacco industry representatives, tobacco control and public health advocates,

appropriate government ministries, law enforcement agencies, private researchers,

independent consultants, customs and excise specialists, and officials within the government

and private sector. Further suggestions of individuals to contact were also obtained from

interviewees during the interview process. These was used to extend the key informant

sample list. The research subjects excluded any vulnerable groups and focused entirely on

experienced adults who have expert knowledge on the licit and illicit tobacco markets.

In order to protect the privacy of the research subjects, personal identifiers were removed to

ensure anonymity. Privacy was further maintained through pseudonymisation which ensured

that identifying fields were substituted with artificial identifiers.

Process of setting up interviews

After the key informant sample list had been developed, research subjects were contacted,

the researcher introduced herself and the study, and voluntary participation was specified

(see Appendix B: Information Sheet and Consent Form). Initial contact occurred by either

17

phone or email. Contact that occurred via phone was followed up by an email that re-

introduced the study to the research subject. The email included the Information Sheet and

Consent Form (see Appendix B). All further communication setting a date and time for

interviews was done via phone or email, whichever was preferred by the subject. The

interviews were conducted at the convenience of, and at a location specified by, the

interviewees, such as company premises or a public venue. The signed Information Sheet and

Consent Form was either emailed to the researcher or manually handed over to the

researcher before the interview.

In cases where the interview was conducted by phone, the researcher re-introduced the study

and read out the Information Sheet and Consent Form (see Appendix B). The Form specified

that interviewees who agreed to be interviewed by phone or Skype automatically provided

consent. In instances where the researcher had both a contact number and an email address

for the prospective interviewee but was unable to reach the individual by phone, she sent an

e-mail introducing herself and the study. Details regarding voluntary participation,

confidentiality, and the Information Sheet and Consent Form (see Appendix B) were also

provided. With the verbal consent of the subject, more than one interview may have occurred

in some instances. This allowed for follow-up questions based on first-round interviews.

Data

Key informant interviews are relatively simple to conduct (Ross, 2015). Information can be

obtained relatively quickly and can provide valuable background and corroborating

information on a specific subject. Despite the wide range of information gathered, the

researcher was aware that the selected technique also tends to be associated with

subjectivity and related bias, which are often shaped by individual experiences (Ross, 2015,

U.S. National Cancer Institute & World Health Organization, 2016). The information gathered

tended to be very broad in nature and not limited to discussions merely about the size of the

illicit tobacco market. Some of the issues discussed included legislation, the efficiency of

government agencies, industry interference in state and tobacco industry functioning, moral

viewpoints, and business strategies.

18

Given the sensitivity of the gathered information, it was necessary to protect interviewees

from any risks that might arise if their participation became known. For this reason, research

data obtained from key informant interviews was tape recorded and thereafter transcribed

onto a password-protected Microsoft Word document. The names of research subjects were

anonymized and pseudonymised during transcription. The tape-recorded research data was

deleted once transcribed. The Word document was stored on Google Document using Google

Document encryption to protect the data from third parties. Only the researcher has access

to the passwords. The research data was stored to support any queries that may arise from

potential thesis publication.

Because of work that the Economics of Tobacco Control Project (ETCP) does, the researcher

and supervisor are aware that the tobacco industry takes a special interest in the ETCP. They

therefore had to conduct the research with extraordinary care and ensure that the work was

done both ethically and thoroughly.

Analysis

Semi-structured key informant interviews included both face-to-face and phone interviews,

which took place from August to December 2018. Twenty individuals were interviewed,

including representatives of: domestic tobacco companies (6), multinational tobacco

companies (1), National Treasury (2), law enforcement agencies (2), the informal sector (1),

financial intelligence (1), tobacco control/public health advocates (3), independent

consultants (3), as well as one journalist. Research subjects were identified based on their

roles working within - or in relation to - the tobacco market and had specialist knowledge

regarding the nuances of the tobacco trade, including the illicit part of it. The list of

interviewees was compiled from names of individuals found on tobacco-related media

articles, books on the subject matter, referrals within the Economics of Tobacco Control

Project, referrals obtained during the interview process, and direct enquiry. Ex-employees of

tobacco companies, who had more than ten-years of experience within the tobacco industry,

were also included.

The term ’domestic and multinational tobacco companies’ includes each group’s industry

representative bodies. Multiple members of one of the industry representative bodies agreed

19

to participate in the study, but all industry members of the other industry representative body

refused to participate individually. They directed the researcher to contact their industry

representative body about study participation. Two of the 20 interviewees refused to be

recorded. They happened to form part of the same cohort, written notes were taken during

the interview process and more detailed notes were made immediately after the interview,

so as to reduce the likelihood of recall error.

Owing to the sensitive nature of the study’s subject matter, certain subjects who were

contacted refused to participate in the study. They believed that participation could

compromise national investigative efforts and their job security. Those who did agree to

participate did so in their professional capacities, and one interviewee gave permission for

the individual’s name to be disclosed even though this was not sought. One interviewee

requested that the tape-recording be paused on multiple occasions during the interview, so

as to disclose information off the record.

Questions for each interviewee were adapted as appropriate, and the following themes were

probed: 1) the reasons behind the recent upward spike in illicit tobacco trade, 2) the modus

operandi of illicit tobacco trade, 3) industry complicity in the illicit tobacco trade, 4) the role

of law enforcement with respect to the illicit tobacco trade, 5) opinions regarding reliable

sources of illicit tobacco market estimates. Interview data, which took the form of entangled

stories, was used to identify narratives which would aid the understanding of the social

construction of the South African illicit tobacco market. Key narratives were identified as

those most frequently mentioned or discussed in the greatest detail, or one that was

mentioned uniquely.

Limitations

The limitations of applying such a method and speaking to, in certain interviews, nervous or

uncertain interviewees meant that often the interviews included large amounts of irrelevant

material. Interviewees may have presented distorted responses which could be associated

with an attempt to promote a certain narrative, trying to compensate for being uncertain

about a specific question/topic, bias in recalling events and experiences, cautious limiting of

20

their responses in order not to be identified, or being influenced by emotional states, for

example, stress or fear of reprisal.

Because of the sensitive nature of the subject matter, it was very difficult to find interviewees

from government agencies who were willing to speak, even with all the safeguards and

precautions in place to preserve anonymity. This was anticipated by the researcher and was

a challenge. The researcher was also fully aware that certain cohorts, particularly members

of specific industry representative bodies, were pushing certain narratives. In such cases, the

responses of individuals or a group of individuals affiliated to a representative body were

designed to invoke a specific narrative and in certain instances the researcher asked the

question ‘why have you agreed to speak with me? What is the narrative that you are wanting

to convey?’. Some respondents had well-rehearsed answers, and this was evident throughout

the interview.

The researcher was aware that what was communicated by the interviewees during the

interview process might contain inaccuracies and have been driven by strategic commercial

objectives unique to each interviewee or group of interviewees. For this reason, great care

was taken to ensure that responses were not accepted uncritically but rather approached

with some skepticism. Given the nature of the research and complexity of the market, gaining

an understanding of the various narratives was the best that the researcher could do.

3.2 Ethical considerations

Since the collection of primary data for this study involved interviews with human subjects,

ethics clearance was required and granted (see Appendix C) by the University of Cape Town

(UCT) Commerce Faculty Ethics in Research Committee. Primary data collection only

commenced once ethics approval was granted by the Committee.

21

4 Results

Since the 1990s, the South African tobacco industry has been characterised by the presence

of only three MTCs, with British American Tobacco South Africa (BATSA) holding a near-

monopoly market position (van Walbeek, 2005). The two other tobacco companies included

Philip Morris South Africa (PMI) and Japan Tobacco International South Africa (JTI). The near-

monopoly market position of BATSA resulted in strong barriers to market entry, limiting

competition within the sector and securing the positions of the MTCs for decades. However,

gradual changes in government-imposed tax and non-tax tobacco-control measures, starting

with the Tobacco Products Control Act, 1993, impeded MTCs’ further exploitation of the

tobacco market. The Tobacco Products Control Act of 1993 was amended in 1999, 2007, and

2008. Some of the main provisions of the Act included: a complete ban on tobacco advertising

and sponsorship, smoke-free public areas and workplaces, restrictions on cigarettes sales to

minors, restrictions on smoking in cars where minors are present, and maximum-level

restrictions on tar and nicotine content.

In response to the tobacco control measures, MTCs persistently lobbied the government

against the tightening of tobacco legislation, increases in the excise tax, and the entry of new

competitors, all of which posed a threat to the interests of the established tobacco industry.

Rising competition (actual and potential) within the sector and government legislation

conflicted with MTCs’ interest in maintaining the status quo of the tobacco industry. MTCs

soon realised that they could not sustain the traditional power dynamics of the tobacco

market. As a result, they used a range of tactics to protect their interests. This section explores

the tactics adopted by MTCs to protect themselves from the rising threat of competition and

government legislation in the South African tobacco market.

The results presented below take the form of a narrative of the chronological development

of the tobacco trade since 1990, with a specific focus on the illicit trade narrative since 2009.

The story is framed around how the vested interest of an established industry came into

conflict with potential and actual competitors, and with the government. The narrative is

primarily shaped by information obtained from tobacco industry stakeholders during the

study’s interview process and from published literature.

22

The narrative will first provide an overview of the South African tobacco industry (1990 to

2009/10), which was followed by the disruption of the traditional tobacco market status quo

(from 2009/10). Thereafter the study explores suspicions of industry complicity in illicit

tobacco trade (from 2012 to 2014) and the unravelling of the multi-layered tobacco industry

(from 2014). This will be followed by an overview of under-declared production and its impact

on excise revenue (from 2015). Finally, the study explores multinational tobacco companies’

recent tactics to protect their interests.

23

4.1 Overview of the South African tobacco industry (1990 to 2009/10)

In 1999, British American Tobacco South Africa (BATSA) dominated the South African tobacco

industry, accounting for more that 90% of tobacco market share (van Walbeek, 2005). Their

position in the market was entrenched by BATSA’s advantage as first-mover into the country

and the merging of British American Tobacco plc (BAT) and Rothmans International, to form

BATSA in 1999 (van Walbeek, 2005). The strength of their market share allowed them to

establish strong and unrivalled pricing power within the sector. BATSA’s extensive cigarette

brand portfolios - including Peter Stuyvesant and Rothmans - retained their dedicated

followers in South Africa for decades.

Until 2010, BATSA had only two significant competitors, both of which were familiar rivals to

BAT at a global level: PMI and JTI (Gordon & Hedley, 2011). Market share rankings of the three

MTCs, led and dominated by BATSA, and followed by PMI and JTI in that order, allowed BATSA

to control the South African tobacco market. Although Philip Morris International historically

tended to be the dominant MTC in global market share rankings, in South Africa, they played

second fiddle to BATSA. According to an ex- PMI employee, PMI’s exit from - and re-entry to

- the South African tobacco market during periods of political instability did not aid their

competitive position and they persistently ranked second in terms of market share. PMI’s

Marlboro brand, however, helped to secure their market share. That, and their small brand

portfolio, relative to BATSA, played a significant role in sustaining their second-place market

share ranking.

Interviewees indicated that BATSA was, and still is, the only MTC in the South African tobacco

market that manufactures cigarettes locally, while both PMI and JTI import all their cigarettes.

Investment in local manufacturing and market share dominance resulted in BATSA, rather

than PMI and JTI, having a greater stake in the economic and political developments affecting

the South African tobacco industry. However, irrespective of whether cigarettes are

manufactured locally or imported, all three MTCs are represented by the same tobacco

industry representative body, the Tobacco Institute of Southern Africa (TISA). According to

TISA, they represent “major tobacco manufacturers and tobacco farmers in South Africa. Their

main business includes the representation of the non-commercial, common interest of

24

manufacturers and marketers of tobacco products as well as the tobacco growers in South

Africa.”

From its inception to the present, TISA’s chairperson, Francois van der Merwe, has been a

tobacco grower. For domestic cigarette manufacturing, TISA member tobacco growers have

supplied, and continue to supply, tobacco leaf predominantly to one cigarette manufacturer,

namely BATSA. Thus BATSA, given their market share dominance and strong tobacco leaf

purchasing power, is likely to have the greatest influence on TISA’s agenda. In fact, during the

interview process multiple stakeholders used the words TISA and BATSA interchangeably, and

two interviewees specifically mentioned that TISA and BATSA are synonymous: “TISA is

basically run by BATSA and Francois van der Merwe is in BATSA’s pocket”. Owing to the blurred

lines that separate TISA and BATSA, multiple interviewees indicated scepticism and caution

regarding the narratives presented by TISA to tobacco industry stakeholders and the public,

via the media.

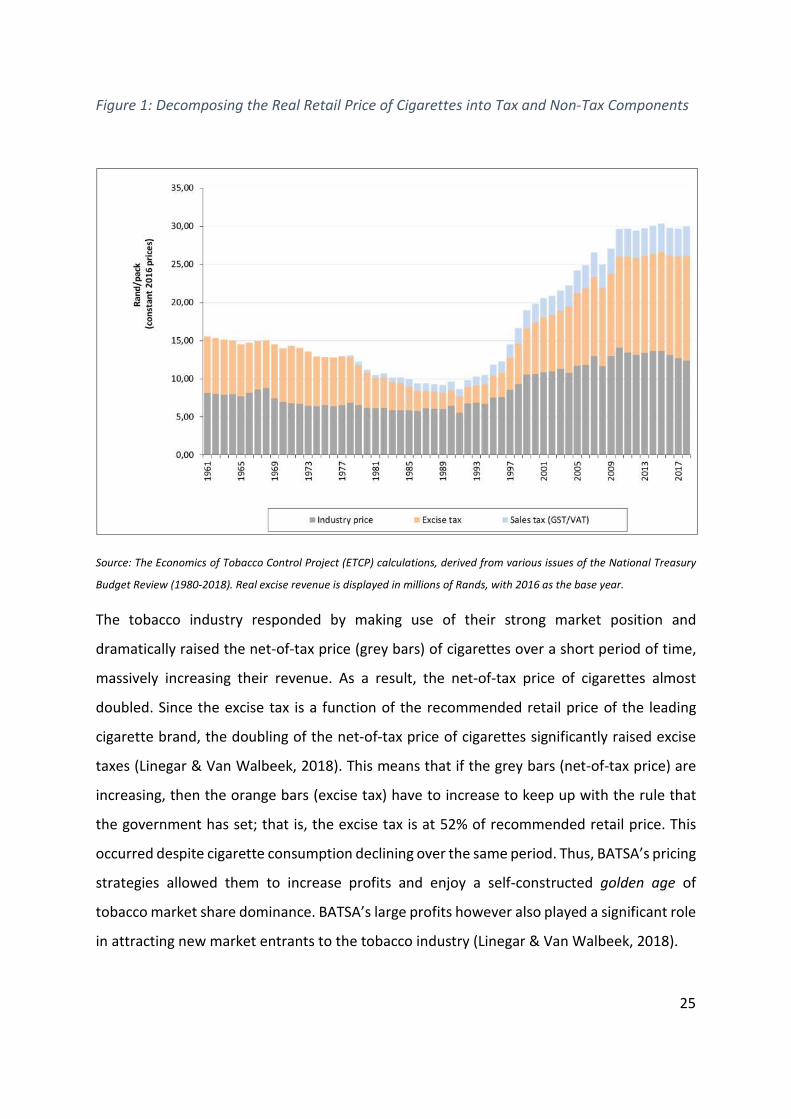

By decomposing the real retail price of cigarettes into tax and non-tax components (Figure 1)

we are able to assess how BATSA, between 1994 to 2010, leveraged their market power and

took advantage of margin opportunities (Linegar & Van Walbeek, 2018). The grey bars in

Figure 1 represent the industry price or the net-of tax-price while the orange bars represent

the excise tax and the blue bars represent sales tax (GST/VAT). With the release of Nelson

Mandela from prison and the abolition of apartheid in the early 1990s, the tobacco industry

became aware that significant political changes were approaching. From 1994, the

Department of Health publicly announced their commitment to protect public health. In 1994

the Minister of Finance announced that they would target a total tax burden of 50% of the

retail price of the most popular cigarette price category (Minister of Finance, 1999, Minister

of Finance, 2000). This was achieved in 1997. In 2004, the Treasury raised the tobacco tax

(excise tax plus VAT) benchmark to 52% of the recommended retail selling price of the most

popular brand of cigarettes (Minister of Finance, 2004). The most popular brand of cigarettes

was owned by BATSA.

25

Figure 1: Decomposing the Real Retail Price of Cigarettes into Tax and Non-Tax Components

Source: The Economics of Tobacco Control Project (ETCP) calculations, derived from various issues of the National Treasury

Budget Review (1980-2018). Real excise revenue is displayed in millions of Rands, with 2016 as the base year.

The tobacco industry responded by making use of their strong market position and

dramatically raised the net-of-tax price (grey bars) of cigarettes over a short period of time,

massively increasing their revenue. As a result, the net-of-tax price of cigarettes almost

doubled. Since the excise tax is a function of the recommended retail price of the leading

cigarette brand, the doubling of the net-of-tax price of cigarettes significantly raised excise

taxes (Linegar & Van Walbeek, 2018). This means that if the grey bars (net-of-tax price) are

increasing, then the orange bars (excise tax) have to increase to keep up with the rule that

the government has set; that is, the excise tax is at 52% of recommended retail price. This

occurred despite cigarette consumption declining over the same period. Thus, BATSA’s pricing

strategies allowed them to increase profits and enjoy a self-constructed golden age of

tobacco market share dominance. BATSA’s large profits however also played a significant role

in attracting new market entrants to the tobacco industry (Linegar & Van Walbeek, 2018).

26

Until 2010, despite government-imposed tax and non-tax tobacco-control measures, market

conditions enabled BATSA to earn impressive profits. Neither competition nor government

legislation at the time were in conflict with BATSA’s growth strategy, which centered heavily

on increasing the overall profitability of the company by increasing the profit per cigarette in

a decreasing market. BATSA’s objective was to maintain its stronghold on the tobacco market

and, as far as possible, limit competition and oppose the strengthening of tobacco legislation.

Up to 2009/10, the threat of competition from actual and potential competitors, and from

tobacco legislation, was more of a minor inconvenience than a major threat.

In 2009/10, however, changes the form of rising competition in the tobacco market started

to threaten BATSA’s market position. The change was driven mainly by the entry of domestic

tobacco companies (DTCs) and, to a lesser extent, changes in tobacco-control legislation. In

response to the threat, BATSA/TISA employed an assortment of tactics to protect their

interests and maintain BATSA’s dominance in the sector.

27

4.2 The disruption of the traditional tobacco market status quo (from 2009/10)

In the period leading up to 2009/10, non-MTC tobacco companies and prospective new

market entrants became increasingly aware of the margin opportunities that BATSA had

enjoyed for decades and they wanted a share of the lucrative tobacco market. In 2009/10,

DTCs began penetrating the tobacco market with relatively affordable cigarette brands,

increasing competition and thus threatening the market shares of more expensive and well-

established BATSA-owned cigarette brands. As a result, since 2010, the net-of-tax price of

cigarettes (Figure 1) began to decrease, reducing BATSA’s profit margins. The entry of DTCs

in 2010 also coincided with the upward spike in the illicit tobacco trade (van Walbeek, 2015).

The spike in the illicit tobacco trade implied either under- or non-payment of the relevant

tobacco taxes (van Loggerenberg & Lackay, 2016). Under- or non-payment of taxes meant

that illicit cigarette brands could be sold at much lower price points than BATSA-owned

cigarette brands. Cheaper licit cigarette brands could also be sold as lower price points than

BATSA-owned cigarette brands. Thus, cheaper illicit and licit cigarette brands were more

affordable options for price-sensitive smokers (Mukong & Tingum, 2018). Smokers responded

by shifting away from higher-priced to lower-priced cigarette brands. Consequently, the shift

towards cheaper cigarette brands negatively affected the profit margins of BATSA-owned

cigarette brands. BATSA’s profit margins, which had been increasing for almost two decades,

reached a tipping point.

Cigarette price volatility as a result of an upswing in the illicit tobacco trade and an increase

in DTCs since 2010 led to a decrease in the real net-of-tax price of cigarettes of MTC-owned

brands (Figure 1). This disrupted the traditional tobacco industry status quo and threatened

the established MTC power dynamics. As of 2009/10, BATSA could no longer sustain their

market dominance. The entry of new competitors was major threat to their market share and

profit margins.

Consistent with tactics previously adopted by MTCs globally in response to threats to their

interests, TISA, on behalf of BATSA, embarked on a number of national advertising campaigns

(van Walbeek & Shai, 2015). The campaign included billboards (as cited by van Walbeek &

Shai, 2015) with “an angry young man, peering through the sights of a gun, with the caption:

28

Warning: The money you spend on illegal cigarettes, he uses to buy guns”. The campaigns

promoted the narrative that the illicit tobacco trade, in 2010, was spiralling out of control and

leading to a proliferation of organised crime (van Walbeek & Shai, 2015). The aim of the

campaign presumably, was to dissuade the National Treasury from raising the excise tax on

cigarettes and to lobby the government to take action against organised crime. The claims,

however, were disputed by members of the public through the Advertising Standards

Authority (ASA); upon the ASA’s instruction, BATSA withdrew their campaign (van Walbeek &

Shai, 2015). This was not the first time, however, that TISA had used the media to promote a

similar narrative.

In 2006, despite the lack of evidence of an illicit tobacco trade, TISA, via the media, began to

present the same argument (Blecher, 2010, van Walbeek, 2014, van Walbeek & Shai, 2015).

TISA-driven illicit tobacco trade narratives, in 2010, thus represented a recycling of previously-

used media narratives, the difference being that in 2010 there was an actual increase in illicit

trade. This upward spike in illicit trade was subsequently confirmed by independent,

academic tobacco-control experts, from the University of Cape Town (van Walbeek & Shai,

2015).

It is likely that the threat of the entry of DTCs into the market in 2010, coupled with their

cheaper cigarette brands, severely threatened BATSA’s market share and the security of their

near monopoly status. In order to protect their market share, BATSA used the media to

promote the narrative that the illicit tobacco trade was associated with organised crime,

which threatened the safety of the country’s citizens. This scaremongering was used by

TISA/BATSA to lobby the government to take decisive steps against organized crime, but,

more importantly, to curb competition within the industry. van Walbeek & Shai (2015)

illustrate how between 2006 and 2011, TISA mispresented the size of the illicit tobacco

market by adjusting previous estimates downwards in order to create the impression that

illicit trade was spiralling out of control. This was all done on public platforms, including in the

media, which has thus become an important tool for the tobacco industry’s self-serving

promotion of their interests.

29

A former MTC employee indicated that BATSA had the economic resources to eradicate the

illicit tobacco trade had they wanted to, but that retaining barriers to market entry was more

important to their interests. Historically, BATSA made a strategic choice to condone moderate

levels of illicit tobacco trading as moderate levels helped BATSA to deter the entry of new

competitors. BATSA believed that prospective competitors were likely to sell their cigarette

brands at prices lower than BATSA-owned cigarette brands in order to gain traction in the

industry. New entrants would therefore have to compete against DTC-owned cheap cigarette

brands. However, within the cheap cigarette market, there was a large proportion of illicit

cigarette which were being sold far below the amount of the combined excise tax and VAT

and were therefore more affordable. Illicit cigarettes made it very difficult for licit cheap

cigarettes brands owned by new market entrants to compete. New market entrants would

not be able to compete effectively against cheap illicit cigarette brands and would therefore

be automatically kept out of the market. Thus, moderate levels of illicit tobacco trade aided

BATSA in deterring the entry of new competitors.

In 2009/10, however, the rise in illicit cigarettes exceeded the tolerated levels that BATSA had

previously condoned. Companies trading in illicit tobacco, which BATSA openly accused in the

media as being synonymous with DTCs, posed a severe threat to BATSA’s market share. The

illicit tobacco trade shifted from being regarded as a minor inconvenience, that indirectly

supported BATSA’s interests, to being a major threat, in direct conflict with BATSA’s interests.

4.2.1 Industry transformation and the role of informal markets

Interviews with DTCs offered an alternative perspective regarding the entry of new

participants to the South African tobacco market. All six DTC interviewees shared a narrative

that advocated the transformation of the South African tobacco industry to level the playing

field for market participants. Levelling the playing field alluded to equal opportunities being

granted to all market participants, by the abolition of the anticompetitive business practices

that had been imposed by BATSA. Anticompetitive business practices included deliberate

efforts at imposing and maintaining barriers to market entry and restricting DTCs’ entry to

formal retail channels.

30

The narrative revolved around the history of the tobacco industry, which interviewees

claimed is deeply embedded in apartheid-era ideals and which is dominated by white

monopoly capital. White monopoly capitalists, and BATSA in particular, are believed to have

imposed barriers to market entry in order to maintain exclusivity and impede the entry of

previously disadvantaged non-white market participants. They believe that white-owned

capitalist multinationals continue to control lucrative sectors of the economy, while forcing

DTCs to operate on the margins of tobacco trade.

Believing these things, DTCs use the theme of transformation as a slogan to justify forcefully

growing their positions- and demarginalizing themselves within the tobacco market. The word

transformation was often used as the politically correct term to express the sentiment that

‘we will take control, with or without consent’. The term is thus used as a form of rebellion

against the traditional South African tobacco industry status quo and the established power

dynamic. Further justification was found in the perception that pre- and post-apartheid

governments have consistently favoured MTCs for various reasons, despite incidences of

competitor spying and “state capture”, turning a blind eye to any doubtful business practices

(Pauw, 2017, van Loggerenberg, 2018, van Loggerenberg & Lackay, 2016).

All six interviewees indicated very little confidence in the ability of the government to support

DTCs in gaining a foothold in the tobacco market. This was captured in one of the comments

made by a DTC interviewee: “The tobacco industry, when it comes to multinationals, get full

support from the government, SARS (South African Revenue Services) and the police. This is

because they are all on the multinational’s payroll. The smaller players and FITA (Fair-Trade

Independent Association) on the other hand, get harassed by the police.” FITA is the industry

representative body for domestic tobacco companies. According to Fair-Trade Independent

Tobacco Association (2019), at the time of writing, their members included Afroberg Tobacco

Manufacturing, Amalgamated Tobacco Manufacturing, Carnilinx, Folha Manufacturers, Gold

Leaf Tobacco Corporation, Home of Cut Rag and Protobac. FITA’s website reflects their views

regarding the lack of government support for domestic tobacco companies: “FITA was

established in 2012 with a spirit to encourage smaller manufacturers in the tobacco industry

in Southern Africa to collaborate in respect of industry, regulatory and legislative matters

which are common to all and which, individually, there is little hope of making any significant

31

difference. Small manufacturers in Southern Africa are not afforded the same opportunities,

rights of appearance and opportunities to make industry representations as large industry

players” (Fair-Trade Independent Tobacco Association, 2019).

For these reasons, in their attempt to penetrate the tobacco market, and in the face of a

perceived lack of government support, DTCs embarked on a radical socio-economic

transformation of the tobacco industry. The transformation was governed by their own set of

rules, which permitted an ideological tax revolt leading to tobacco tax evasion and the sale of

illicit cigarettes (van Loggerenberg, 2018, van Loggerenberg & Lackay, 2016). Tobacco tax

evasion enabled DTCs to sell illicit cigarettes at relatively cheap price points, making cigarettes

more affordable to smokers and enabling their market share to grow (van der Zee, van

Walbeek & Magadla, forthcoming 2019). All of this was justified under the slogan of

transformation. According to one DTC interviewee: “The illicit tobacco market was a way for

new entrants to introduce their brands. A lot of the players were engaging in illicit trade. Some

are not as active now and some of them were previous employees of multinational companies,

engaging in rogue and lawful operations simultaneously.”

According to all six DTC interviewees, BATSA continues to capitalise on their history in the

South African tobacco market, which has allowed them to form, over decades, strong

relationships with formal retailers. Established relationships with retailers, coupled with their

strong portfolio of heritage cigarette brands, gave them a competitive advantage in the

market. They abused this advantage by persistently dictating retail shelf management

practices to formal retailers; that is, they dictated where their own brands and competitor

brands should be positioned on retail shelves.

DTCs argue that their brands, if allowed to be sold in formal retail channels at all, are often

placed under the shelf and out of the consumer’s line of sight, whereas BATSA brands are

placed on optimal shelf spaces, giving their brands an unfair competitive advantage. The

movement of DTC brands to below countertops significantly reduces the sales of such brands,

and therefore DTC brands could not compete effectively in formal retail channels. Since trade

in formal retail channels was not feasible, the only option was to trade through informal

markets.

32

Three of the DTC interviewees indicated that BATSA solidifies their shelf positions by

providing an assortment of incentives to retailers, particularly financial incentives with which

DTCs cannot compete. DTCs were not the only tobacco industry participants who criticised

BATSA’s anticompetitive business practices. According to the Competition Tribunal (2009), in

2009, the multinational tobacco company, JTI and the South African Competition Commission

complained to the Competition Tribunal alleging BATSA’s abuse of dominance and

anticompetitive business practices in formal retail stores. The case was, however, dismissed

by the Tribunal.

According to all six DTC interviewees, anticompetitive market entry practices, imposed by

BATSA, forced new entrants to penetrate the tobacco market through more novel channels,

such as South Africa’s abundant informal markets. The unregulated nature of the informal

markets created the conditions for illicit product sales to flourish. Weak law enforcement

capacities and resources in informal markets led to informal markets becoming places where

the illicit tobacco trade could thrive.

Two DTC interviewees indicated that prior to becoming cigarette manufacturers, they had

been traders of an assortment of other goods in the informal market; clothing was mentioned

specifically. Thus, over the years, they developed extensive business expertise trading within

the informal market. It was during this time that they became aware of the attractive margin

opportunities available in trading in illicit cigarettes. They therefore, amongst other things,

began selling smuggled cigarettes.

Their business prowess gave them a deep understanding of the functioning of informal

markets and how to exploit opportunities within the market, initially as traders and later as

manufacturers of cigarettes, in the latter case supplying both licit and illicit cigarettes to the

informal market. A deep knowledge of informal markets, rebellion against anticompetitive

business practices, weak law enforcement capacity in the informal markets, a tax revolt in the

name of transformation, and the desire to maximise profits in the shortest possible time, all

played a significant role in driving DTCs’ engagement in the illicit tobacco trade.

One DTC interviewee, while agreeing with the theme of transformation, also provided a moral

justification for engagement in the illicit tobacco trade. This revolved around the

33

interpretation of religious law in relation to “fairness” in terms of his obligation to pay excise

duties. According to the interviewee’s interpretation, religious law supersedes secular law

and in instances where a secular law is deemed unjust or unfair, it does not have to be

followed. He believed that tobacco excise taxes in South Africa were too high and unfairly

imposed on DTCs. Despite indicating that the excise tax was too high, the interviewee could