THE PATIENT PROTECTION AND AFFORDABLE CARE ACT Ag Employer’s Guide to Health Care Reform Matt Bigham Sales Manager Western Growers Assurance Trust Copyright © 2013Western Growers Reproduction permission requests should be directed to 1-877-942-4529. The information in this webinar and related material should not be construed as legal advice or legal opinion on specific facts and should not be considered representative of the views of its authors, its sponsors, and/or Western Growers. This webinar and material is not intended as a definitive statement on the subject addressed. Rather, it is intended to serve as a tool providing practical advice and references.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

THE PATIENT PROTECTION AND AFFORDABLE CARE ACT

Ag Employer’s Guide to Health Care Reform

Matt BighamSales Manager

Western Growers Assurance Trust

Copyright © 2013Western Growers

Reproduction permission requests should be directed to 1-877-942-4529. The information in this webinar and related material should not be construed as legal advice or legal opinion on specific facts and should not be considered representative of the views of its authors, its sponsors, and/or Western Growers. This webinar and material is not intended as a definitive statement on the subject addressed. Rather, it is intended to

serve as a tool providing practical advice and references.

Health Care Reform’s Vision

Patient Protection & Affordable Care Act (“ACA”) Promise of Robust, Universal Coverage

Requiring most Individuals have health insurance or pay penalty; Expand availability of coverage

Creating Health Insurance Exchanges Encouraging employers to provide coverage to full-time employees Removing barriers to coverage: Guaranteed Issue/No Pre-existing Conditions

Exclusions

2

Our Roadmap3

Delayed: Employer Mandate Penalty & Reporting Requirements Employer Plan Changes that have Already Occurred Individual Mandate Large Group Highlights Small Group Highlights All Employers

Employer Requirements, Considerations & Decisions

Planning for 2014, 2015 & After

Delayed: Employer Mandate Penalty

4

Delayed: Employer Mandate & Reporting Requirements Employer mandate penalty and reporting requirements delayed until

January 1, 2015 No Infrastructure for reporting info re: coverage from Insurers,

Group Health Plans, Government Agencies to Federal Gov. W/O Info: Exchanges/Marketplace Cannot Verify Employer

Sponsored Coverage Cannot impose Pay-or-Play Penalties (hence the delay)

Remainder of law in effect • Health insurance market reforms• Individual mandate• Health Insurance Exchanges

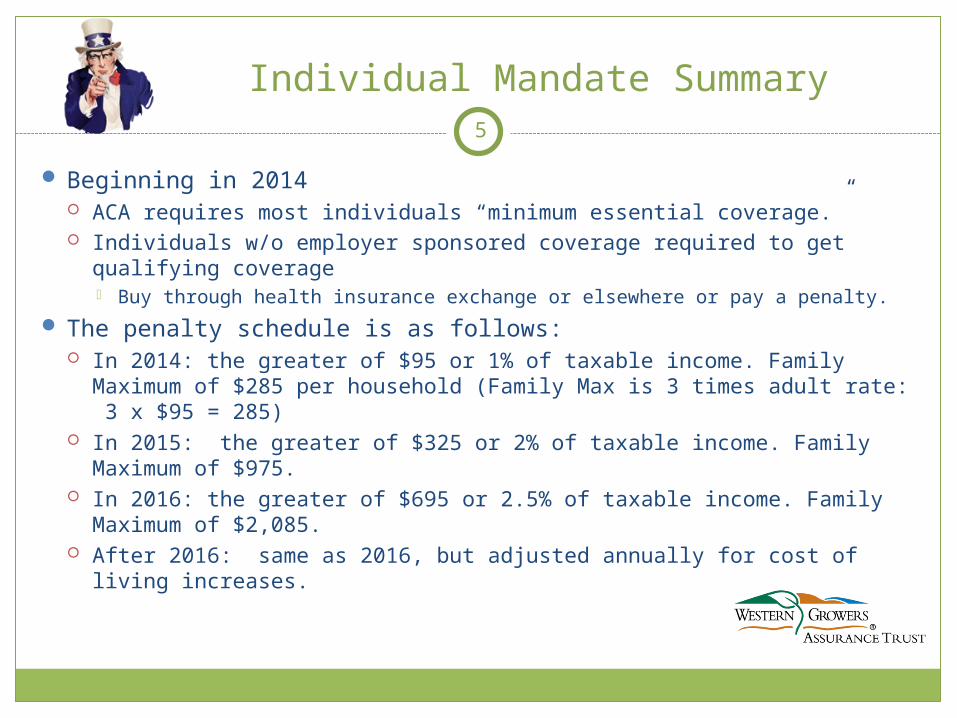

Individual Mandate Summary

Beginning in 2014 ACA requires most individuals “minimum essential coverage.” Individuals w/o employer sponsored coverage required to get qualifying

coverage Buy through health insurance exchange or elsewhere or pay a penalty.

The penalty schedule is as follows: In 2014: the greater of $95 or 1% of taxable income. Family Maximum of

$285 per household (Family Max is 3 times adult rate: 3 x $95 = 285) In 2015: the greater of $325 or 2% of taxable income. Family Maximum of

$975. In 2016: the greater of $695 or 2.5% of taxable income. Family Maximum of

$2,085. After 2016: same as 2016, but adjusted annually for cost of living increases.

5

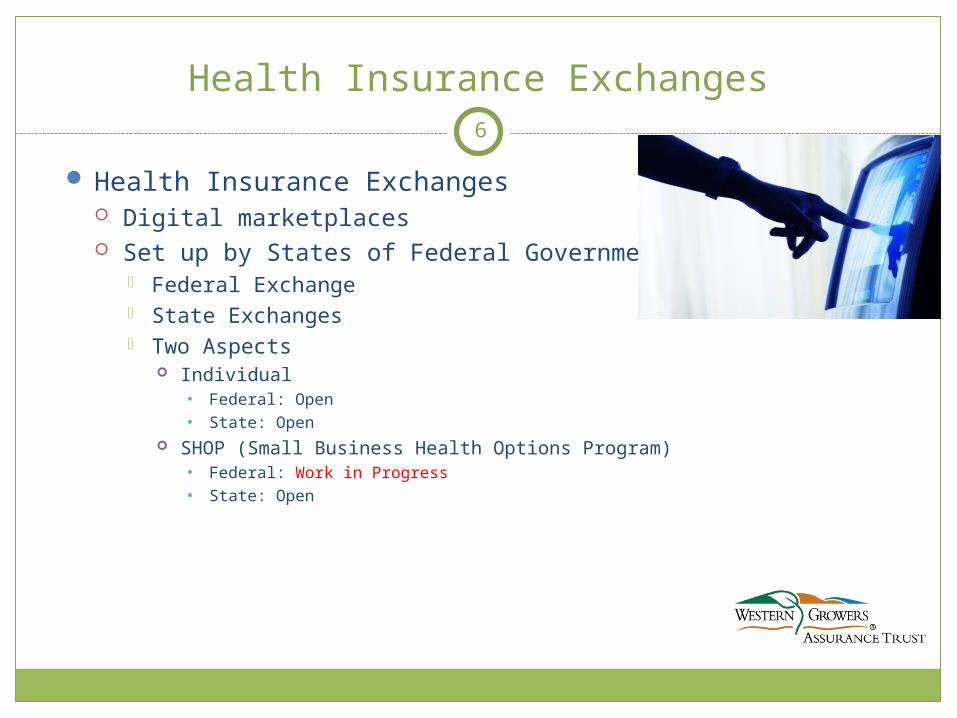

Health Insurance Exchanges

Health Insurance Exchanges Digital marketplaces Set up by States of Federal Government

Federal Exchange State Exchanges Two Aspects

Individual• Federal: Open• State: Open

SHOP (Small Business Health Options Program)• Federal: Work in Progress• State: Open

6

Employer Play or Pay MandateShared Responsibility

7

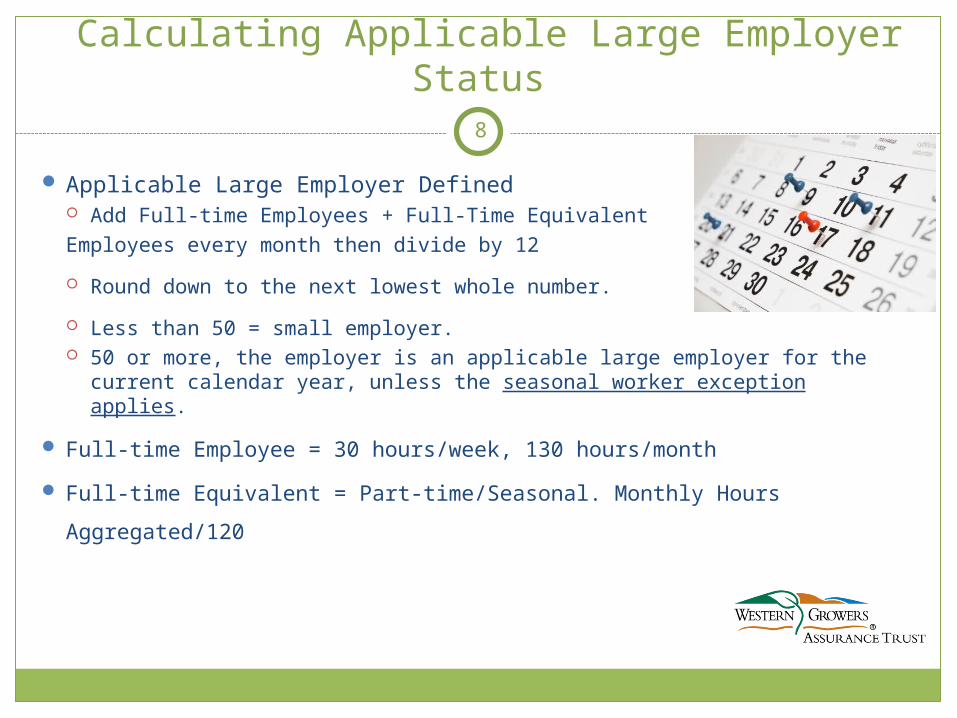

Calculating Applicable Large Employer Status

Applicable Large Employer Defined Add Full-time Employees + Full-Time Equivalent

Employees every month then divide by 12

Round down to the next lowest whole number.

Less than 50 = small employer. 50 or more, the employer is an applicable large employer for the current

calendar year, unless the seasonal worker exception applies.

Full-time Employee = 30 hours/week, 130 hours/month

Full-time Equivalent = Part-time/Seasonal. Monthly Hours Aggregated/120

8

Aggregating Employees of Controlled Groups

Employees that work for a “controlled group of corporations” or “affiliated service group” must be aggregated to determine whether they work for a large employer. All entities treated as single employer under Section 414 (b), (c), (m) or (o) are treated as single employer for

purposes of Pay or Play Rules & Penalties

Large employer status determined based on number of full-time employees and full-time equivalent employees employed by the controlled group.

Penalties assessed and paid at large employer member level not controlled group level.

9

What if an Applicable Large Employer Doesn’t offer Coverage?

If an applicable large employer fails to offer coverage to substantially all full-time employees, may be subject to penalty. Penalty must be triggered.

Triggered if a full-time employee (30 hours/week) goes to an Exchange and receives a tax subsidy to offset cost of his health benefits coverage purchased through exchange.

IRS comes knocking: Penalty is $2,000 multiplied by all full-time employees minus the first 30. Calculated monthly.

10

What if an Applicable Large Employer Offers Coverage but the Coverage Does Not Meet the Law’s Requirements?

If an applicable large employer Offers Coverage, but

The coverage is unaffordable (meaning the employee contributions for self-only coverage exceed 9.5% w-2 income, rate of pay, or federal poverty level

Regulatory Safe Harbors – Impossible calculate Household Income

Fails to provide minimum value (Plan's share of the total allowed costs of benefits is less than 60% of actuarial value)

Employer pays $3,000 per employee receiving a subsidy (or $2,000 x all Employees minus first 30 whichever is less).

11

What if an Employer offers coverage and employees opt-out to go to the Exchange for a subsidy?

Assume employer offers full-time employees the opportunity to enroll in coverage that meets the law’s standards: affordable, minimum value, and correct benefits (minimum essential coverage)

Affordability = Employees contribution for self-only coverage does not exceed 9.5% of safe harbor calculation (w-2 income, rate of pay, or federal poverty level) for self only coverage

Minimum Value = plan pays for 60% of the benefits covered (calculator derived,

insurer determines)

Minimum Essential Coverage: Not defined succintly, but essentially major

medical coverage Employees may opt-out and go to an Exchange

No penalty to employer. Employee’s purchase through Exchange is with after-tax dollars.

12

Small Employer Options

Small Employers Less than 50 full time employees (and full time equivalents) Not required to offer coverage: may do so. The type of coverage offered to small employers by carriers will change

Qualified Health Plans Essential Health Benefits Packages (Non-grandfathered plans)

Insurance options available in the Exchange and outside the Exchange In the Exchange: Metal tier plans known as Qualified Health Plans

Bronze, Silver, Gold, Platinum & Catastrophic

13

Small Employer Options

Small Employers Are not out of the woods…

Discrimination Rule Not very clear and subject to change Self-funded plans Fully-funded plans

Carrier Underwriting Guidelines Will Vary from carrier to carrier Contribution Participation

14

Small Employer Tax Credit

Small Employer Tax Credit Eligibility Businesses with 25 or fewer full-time equivalent employees Employee average annual salary of less than $50,000. Employer must also contribute at least 50 percent toward the employee’s premium cost. This contribution requirement also applies to add-on coverage including vision, dental and other

limited-scope coverage. Employers w/10 or less full-time equivalent employees making an average of $25,000 or less qualify for the

maximum credit. Nonprofit or tax-exempt employers held to same criteria as other small businesses and their tax credit is less.

Calculating the credit Tax credits are available in the tax year 2013 for employers with 25 or fewer full-time equivalent employees Tax credits greater in 2014. Tax credits available for two consecutive years (i.e. until 2016).

15

Tax Year Maximum Tax Credit as % of Ins. Premium Expenses

Phase One 2010-2013 35%Phase Two 2014-2016 50%

Employer Considerations

Important Considerations Employers should consider:

The many reasons you currently offer coverage Offering coverage, but modifying your plans to meet Minimum Value

To evaluate the total cost of dropping coverage you should consider: What your competitors are doing - will they offer health benefits to attract workers

and will this put you at a disadvantage in the marketplace? Will your employees insist on additional compensation to offset the loss of

coverage? What is the true impact of the penalty and how does it compare in light of the tax

benefit you receive from offering coverage? Exchange Notice Requirement:

October 1, 2013. Employers must notify existing & new employees (w/14 days of hire date) informing the employee of the existence of Exchanges.

16

2014 & Beyond

In 2014 Offer qualifying coverage to full-time employees & dependents 90 day waiting period Coordinate with the Exchange New Market Reforms: No Pre-ex, Dollar Limits on Essential Benefits

Prohibited, Out-of-pocket maximums To Prepare for 2015 Pay-or-Play Mandate Penalty:

Employers should calculate the number of Full-Time Employees and Full-Time Equivalents

Consider implementing Safe Harbor Provisions Perform cost benefits analysis: Offering coverage vs. Paying Penalty

In 2015: Employer Mandate & Reporting Reqs Effective In 2018, the Cadillac Tax goes into effect.

17

Questions?

Matt BighamSales ManagerWestern Growers Insurance [email protected]/health-care-reform

18

Immigration Reform & Ag Workers

Immigration Reform Without it no real health care reform

Senate Bill Provides legal status – pathway to

citizenship Ag Employees fall into this category Not eligible for subsides at federal or state exchange

Full-time Employees Treated as any other worker under ACA Obligation and potential penalties remain

19

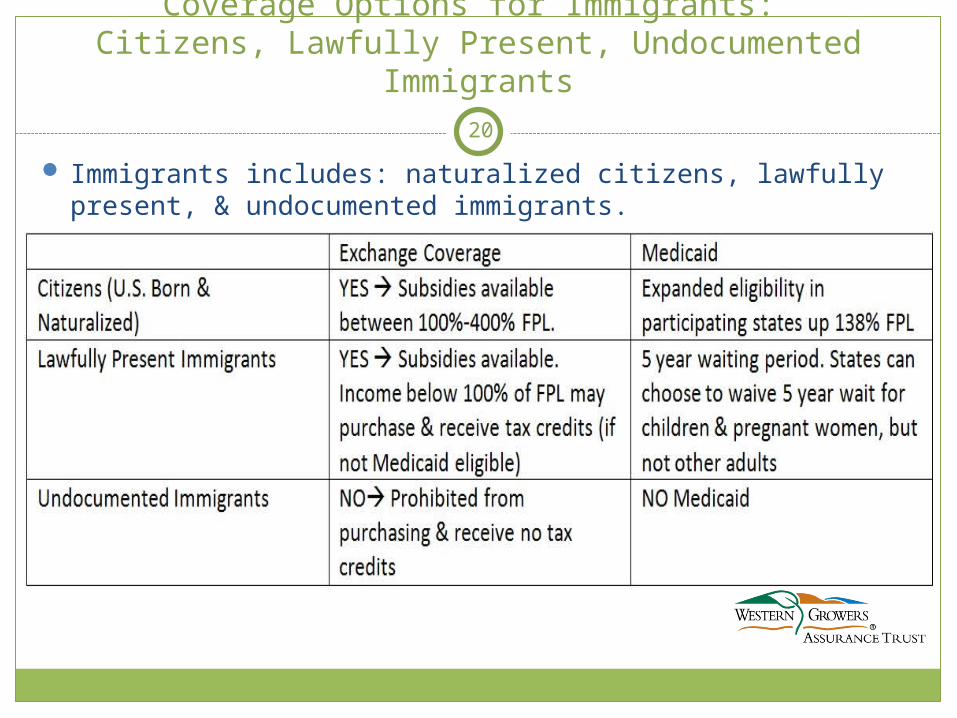

Coverage Options for Immigrants: Citizens, Lawfully Present, Undocumented Immigrants

Immigrants includes: naturalized citizens, lawfully present, & undocumented immigrants.

20

Immigration Reform & Ag Workers

General Rule: Lawfully Present – Play Ball Individual Mandate

H-2A workers subject to if Resident Aliens Employer Mandate

If Full-Time Employees, employer owes obligation Large Employer Status

Seasonal Workers: 120 day or fewer not counted If more than 120 days, counted

21

Speaking of Reporting Part 8

Section 6056 Applicable large employer report to the IRS, and to

furnish certain related employee statements to its full-time employees. Controlled Group and Affiliated Service Group Rules apply

For penalties, however, under the employer shared responsibility rules, each “applicable large employer member” (i.e., each member of the controlled group) is treated separately.

6056 regulations don’t require reporting of (1) the length of any waiting period, (2) the employer’s share of the total allowed costs of benefits provided under the plan, (3) the monthly premium for the lowest-cost option in each of the enrollment categories

(such as self-only coverage or family coverage) under the plan, and (4) the reporting of the months, if any, during which any of the employee’s dependents were

covered under the plan.

22

Speaking of Reporting Part 9

Section 6056: info reported to IRS The name, address, and EIN of the applicable large employer member; The name and telephone number of the applicable large employer’s contact person; The calendar year for which the information is reported; A certification as to whether the applicable large employer member offered to its

full-time employees (and their dependents) the opportunity to enroll in minimum essential coverage under an eligible employer-sponsored plan, by calendar month;

The months during the calendar year for which coverage under the plan was available;

Each full-time employee’s share of the lowest cost monthly premium (self-only) for coverage providing minimum value offered to that full-time employee under an eligible employer-sponsored plan, by calendar month;

The number of full-time employees for each month during the calendar year; The name, address, and TIN of each full-time employee during the calendar year

and the months, if any, during which the employee was covered under the plan; and Such other information as the Secretary may prescribe or as may be required by a

tax form or instructions.

23

Speaking of Reporting Part 10

IRC Section 6056 returns: Filed on or before February 28 (March 31 if filed electronically) of the year

succeeding the calendar year to which it relates. Similar to 6055, the first return (for 2015) will be filed in early 2016. Electronic filing is generally required of section 6056 information returns

except that an applicable large employer member filing fewer than 250 returns during the calendar year may file on paper. For purposes of applying the 250-return threshold, section 6056 returns and W-2

forms are aggregated. Thus, for example, an applicable large employer member required to file 150 section 6056 returns and 200 Forms W-2 must file electronically.

The statements required to be furnished to full-time employees must include the name, address and EIN of the applicable large employer member, and the information required to be shown on the section 6056 return described above. Statements will be on yet-to-be-issued Form 1095-C, or a substitute that includes the information required to be shown on Form 1095-C. A statement must be furnished to a full-time employee on or before January 31 of the year succeeding that calendar year.

24

Related Documents