THANKS FOR WRITING IN CHARTING THE COURSE Why the Next Big Move in Interest Rates Might Not Be Up FINDING YOUR PATH Reflections on the Empty Nest GUEST FEATURE Zen and the Art of Being a Landlord ZEITGEIST: NEWS HIGHLIGHTS TRAILBLAZING The Anna, Redmond, WA NOTABLES AND QUOTABLES Contrarian Investing 2 2 5 7 9 11 12 IN THIS ISSUE THE PATHFINDER REPORT September 2014

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

THE PATHFINDER REPORT: SEPTEMBER 2014 1

Thanks for WriTing in

CharTing The Course Why the Next Big Move in Interest Rates Might Not Be Up

finDing Your PaThReflections on the Empty Nest

guesT feaTureZen and the Art of Being a Landlord

ZeiTgeisT: neWs highlighTs

TrailblaZing The Anna, Redmond, WA

noTables anD QuoTablesContrarian Investing

2

2

5

7

9

11

12

IN THIS ISSUE

The PaThfinder

RepoRtSeptember 2014

THE PATHFINDER REPORT: SEPTEMBER 2014 2

THANKS FOR WRITING INThanks for writing in. Please keep those cards and letters coming.

If you have expertise in an area that could be of interest to our readers, please email us at [email protected] with information about your proposed subject matter. We will be happy to consider it for a future edition.

CHARTING THE COURSEWhy the Next Big Move in Interest Rates Might Not Be UpBy Mitch Siegler, Senior Managing Director

We tend to believe what we want to believe and to see what we want to see. As Ned Davis of the eponymous equity and fixed income research firm Ned Davis Research, Inc. noted in The Triumph of Contrarian Investing, “what feels right, easy and obvious in your gut is quite often wrong.” (Or, as we like to say, what feels safe may

be risky and what feels risky may be safe.)

This maxim was true for investors after markets collapsed in 2008 – stock prices had been beaten down providing investors with a substantial margin of safety. Now that we are able to look through the rearview mirror, it’s apparent that in the aftermath of the Great Recession there was far more upside than downside. The converse may be true nowadays with the Dow at 17,000 and the 10-year Treasury rate at a 14-month low of 2.42%, well below its 2014 peak of 3.01% on January 3rd.

Of course, the economic beacons signaling an expanding economy are plain as day to us, too. There are cranes in the air and new construction as far as the eye can see. Road repairs, new highway on/off-ramps and downtown residential skyscrapers dot the landscape. Companies are hiring and building and expanding factories. Last month, Amazon announced a 700,000 square foot distribution center bringing 2,500 jobs to San Bernadino – it’s the company’s fifth California distribution facility! Banks seem to be overcoming any remaining skittishness and

we’re observing a substantial increase in commercial and industrial loans. These data points signal an economy on the mend, which generally goes hand in glove with rising interest rates.

Now, don’t get us wrong: Like just about everyone else we know, we expect the 10-year Treasury to rise. It’s really not a question of “if ” but “when”. And, we’re putting our money where our mouth is, largely borrowing on a fixed rate basis (while it’s more costly than taking variable-rate loans, we’re able to sleep well at night).

We all know about mean reversion and it seems like rates have been below the mean for a number of years. But, if you look back a bit in time, today’s low rates aren’t really such outliers. According to A History of Interest Rates, Fourth Edition, the average rates in the 1930s, 1940s and 1950s were 2.98%, 2.54% and 2.99%, respectively. Kind of surprising to see numbers like that, huh?

Notwithstanding all of the hullabaloo about a rebounding economy, we see considerable headwinds keeping rates from rising meaningfully in the near-term. First, the Fed is nervous about repeating its big mistake from 1937 – raising rates too early – many historians believe this triggered “Depression, The Sequel.” Recent Fed policy statements, including remarks by Fed Chairman Janet Yellen, suggest that the Fed still sees plenty of slack in the labor markets and is reluctant to tap on the brakes until these folks return to work. The Fed’s go-to inflation measure, the Commerce Department’s Personal Consumption Expenditures Price Index, was up 1.6% in June from the prior year, its 26th straight month below the Fed’s 2.0% target.

Of perhaps greater significance, we’re in a global economy and U.S. interest rates are determined, in part, by the

THE PATHFINDER REPORT: SEPTEMBER 2014 3

world’s other major central banks. As you’ll see from the chart below, U.S. rates – super-low in an historical context, are substantially above those of many major developed nations.

Spreads Between U.S. 10-Year/30-Year Bond Yields and Those of Other Countries

Of course, Europe has serious challenges, as evidenced by the free-fall in government bond yields and the 10% decline this summer in Germany’s DAX stock market index. Germany’s ZEW Index of Economic Expectations – a survey of investors and analysts to gauge sentiment – declined to 8.6 in August from 27.1 in July, its lowest reading since December 2012. The European Union Gross Domestic Product (GDP) data, released in mid-August, showed a paltry (0.1%) increase with Germany registering a 0.1% decline. Last month, we learned that Germany’s GDP shrank during the second quarter by 0.6% – the first decline since 2012. The German bund is now yielding a record-low .93%.

Finland’s bond yield is a tad higher at 1.11% and the French yield is 1.31%. Weak sisters Italy and Spain have rates rivaling the “gold-standard” U.S. bond rate at about 2.45% and 2.27%, respectively –that doesn’t make much sense. These über-low yields may be the canary in the coal mine for a triple-dip Euro recession – suggesting low Euro rates for the foreseeable future.

And it’s not just Europe: Japan’s second quarter GDP fell the most since 2011, following the Fukushima nuclear incident. In China, government policies are causing banks to tone down their lending, a move likely to further crimp economic growth. Unlike in Vegas, what happens abroad doesn’t stay there; it impacts the U.S. and world economies. Viewed through this prism, maybe our rates aren’t so low after all.

In retrospect, it appears that the Fed’s zero interest rate policy (ZIRP) weakened the U.S. dollar, which stimulated exports and boosted economic growth. Because the Fed isn’t operating in a vacuum, virtually all other developed countries’ central banks piggybacked on the Fed, adopting similar interest rate strategies. Today, the tailwind from ZIRP has effectively evaporated because everyone else has copied the Fed. A reverse move – raising interest rates – will likely have an opposite effect on U.S. exports and economic growth so the Fed will likely delay meaningful increases in rates as long as possible – certainly until it believes other countries will follow.

Interest rates are one of the most important finance drivers. They determine companies’ borrowing costs and cost of capital and establish investors’ return expectations. Myriad stories abound of real estate investors being crushed when lenders foreclose on their properties after interest rates move higher and property cash flows don’t keep pace with rising debt service costs. On the flip side, those with the right instincts of where rates are going can make a fortune.

Historically, increasing interest rates are consistent with economic expansions – there is more demand for borrowing amid economic growth. As noted above, the 10-year Treasury rate, an important indicator of interest rate trends, is now under 2.4% as compared with its long-term average above 5%. You’ll recall the average 10-year rates during the decades of the ‘30s, ‘40s and ‘50s – 2.54% to 2.99%. On the other end of the spectrum, we recall the interest rate environment when we borrowed on our first property in 1983 – the mortgage rate then was about 13% and the 10-year was north of 10%. So, perspective is awfully important.

Like we said, along with most investor friends, we expect rates to rise a bunch at some point – again, it’s a question of “when”, not “if ”. But, when everyone is absolutely convinced that the next big move in rates is up, that can set the stage for surprises – and one surprise might be

THE PATHFINDER REPORT: SEPTEMBER 2014 4

another year or two of a low, low 10-year rate. Imagine the implications for your investment strategies and for real estate transaction value and pricing.

An even greater surprise would be a major downward move in the 10-year Treasury over several years. Unthinkable, right? Well, Van Hoisington, president of $4 billion fixed income investor Hoisington Investment Management expects “that over the next several years, U.S. 30-year yields could decline into the range of 1.7-

2.3%, which is where 30-year yields in the Japanese and German economies, respectively, currently stand.” Food for thought.

Mitch Siegler is Senior Managing Director of Pathfinder Partners, LLC. Prior to co-founding Pathfinder in 2006, Mitch founded and served as CEO of several companies and was a partner with an investment banking and venture capital firm. Reach him at [email protected].

THE PATHFINDER REPORT: SEPTEMBER 2014 5

By the time this article is published, our family home of the last 18 years will be a little quieter as our youngest heads off to the University of Michigan for (hopefully) a four year stint. Okay, a lot quieter. No more sleeping with one eye open waiting for the midnight entrance, and no more fear of the neighbors ringing the doorbell because

the party (“I’m just going to have a few friends over”) is just a little too loud.

The pending departure has left me reflective on a number of fronts; foremost, as a parent, of course, hoping that at least a small percentage of those many life lessons have sunken in to the point that we are sending off to the world a young adult who will be inquisitive and intelligent, passionate and playful, and whose smart decisions will outnumber his dumb ones, hopefully by a healthy margin.

As parents and as real estate investors, Mrs. Pathfinder and I have thought about what this will mean for our home and for us. We have kids who are at the tail end of the Millennial generation (defined as children born from about 1980 to 1995), and the one certainty this time is uncertainty. Will the kids finish college in four years? Will they move back to San Diego for the summers? Will they return after they graduate? If they do come back, will they find jobs? And finally, will they move back into the family home? It used to be a little easier to answer these questions. Your kids finished up their college adventures in four years, and were then able to land a job (and their own housing) or headed off to graduate school. In either case, the nest remained empty. Not so much anymore.

The discussion begins with job prospects. While unemployment rates for the 18-34 year-old group have receded by almost 40% over the 2010 high water mark,

the rate is still significantly higher than it was during the boom years of the early 2000s. And, an undergraduate degree isn’t what it used to be. At the same time, the cost of housing has essentially rebounded to pre-Recession levels. So faced with the triple whammy of (i) mediocre job prospects, (ii) high housing costs and (iii) significant student loans (see below), the decision to move back in with the folks may have just become a little easier.

I’ve written before about the extraordinary increase in the cost of a college education over the last couple of decades. Not surprisingly, the outstanding balance of student loans in this country matches the pace of those increases. According to a recent piece in Forbes, that debt is now in excess of $1.2 trillion, over $1 trillion of which is federal student loans, up from $240 billion in 2003. The Institute for College Access and Success says the average student now graduates with over $26,000 in debt. But that’s just the principal balance. Given that interest continues to accrue and compound during the college years, the debt grows to over $38,000 or over $320/month based on a 10-year payback. In part as a result of these factors, many millennials aren’t self-supporting and have decided to postpone the Big Three key life decisions: marriage, buying their first home and having children. And they’ve moved back home in record numbers.

Like many people in San Diego and other urban areas, our home is a mix of urban and suburban. We’re relatively close to the primary urban centers, yet in enough of an enclave where the kids could attend public schools and their safety was never a major concern. Our home was the perfect size for our family of four (not counting the two dogs); four bedrooms and three bathrooms, where we could accommodate an occasional visitor and had plenty of room for entertaining friends and family.

With all of that, I’ve been wrestling with the idea of keeping or selling the family home. It’s not an easy or immediate decision. Certainly no one has a gun to my head. And I am influenced, in a not so subtle way, by a few comments on the subject recently made to me by Mrs. Pathfinder, who will never be described by anyone who knows her

FINDING YOUR PATHReflections on the Empty NestBy Lorne Polger, Senior Managing Director

THE PATHFINDER REPORT: SEPTEMBER 2014 6

as a shrinking violet: “I’ll agree to move when you take my cold, dead body out the front door.” Like many men, I’m not always entirely perceptive, but I’m thinking that she hasn’t quite warmed up to the idea.

At least three primary factors are influencing my thoughts on the home issue. Size, finances and location. I suspect these factors have become a common thread in many spousal discussions.

First of all, if the kids don’t come back, do we really need a four-bedroom house? Sure, it’s great for the four days a year when enough visitors come to take advantage of it, but the reality is that two people need a lot less room than four. As we get older (my wife and I are in our 50s), do we need the same space in the same configuration? Is a back yard necessary at this point, other than to let the dogs outside? And if this next home will be our last, should we be thinking about a single story residence? How big a carbon footprint do we need to leave? If we decide to move, these various elements point me to a smaller home. On the other hand, do we adopt a wait-and-see approach? The two-bedroom townhome in the city is probably not going to work out so great if the kids do come back. Maybe we wait a few years.

Second, from a financial perspective, values are back, which is great on the sell side, but not so great on the buy side. At this stage of life, should we take on debt to buy a nicer home? Is now the time to do that, given that interest rates remain near their historic lows and they’ll likely rise in the future? If we wait, will we get priced out of the market if rates and prices continue to rise? Maybe we buy now.

Finally, there is the location issue, which, in part, ties in to the middle age freeness of having a home without the kids. Should we be a little more urban? Wouldn’t it be nice to have an ocean view? How great would it be to be able to walk from our home to local restaurants or shops, or just take an evening stroll with the dogs down to the water? What price would we be willing to pay for that convenience?

Lots of unanswered questions. It’s interesting that I find it relatively easy to make sound investment decisions, yet the question of selling the family home challenges me.

Maybe I’ll figure this out next year. Or maybe not.

Lorne Polger is Senior Managing Director of Pathfinder Partners, LLC. Prior to co-founding Pathfinder in 2006, Lorne was a partner with a leading San Diego law firm, where he headed the Real Estate, Land Use and Environmental Law group. Reach him at [email protected].

THE PATHFINDER REPORT: SEPTEMBER 2014 7

A successful landlord is part leader, part diplomat and part mediator. The success of a real estate project often hinges on the management, personal style and cohesion of the people involved. During the course of some of Pathfinder’s investments, we’ve worked with individuals whose personalities have ranged from temperate to turbulent. We’re all different, of course,

and different professions tend to attract different types of people. When you interface with brokers, contractors, architects, property managers, leasing managers, home owners association (HOA) managers, HOA board members, maintenance supervisors, neighbors and 92-year old Mrs. Smith in Unit #101 whose dog hates the new building colors, it’s important to adapt. Implementing a property’s business plan while effectively managing and getting along with all of the parties involves a delicate balance of control, compromise, calm and often a touch of Zen Buddhism.

Pathfinder has managed 75 investments during the past several years – including 3,000 apartments, 500,000 square feet of commercial space, 300 single-family homes and condos, a hotel and even a 100-year-old-church-converted-to-townhomes – and we’ve learned a thing or two about what works and what doesn’t. The following are a few lessons learned:

Aspire to Communicate Openly and Transparently

“Better than a thousand hollow words, is one word that brings peace.” - Buddha

If you’re going to update, renovate, rename, repair or materially alter a property, it is essential to communicate properly with the residents. We thought we were communicating well but learned this lesson the hard way.

During one of our more substantial renovations – a $2.5 million interior and exterior overhaul of a twelve-story apartment project – some long-term residents rose-up against their new landlord and provided us with a list of demands to satisfy before they contacted the local version of 60 Minutes to trash our reputation. Realizing that perhaps we had been overly zealous in the implementation of our renovations, we held a town-hall style forum with the residents to hear their complaints. The residents talked, we listened, and vice versa – no punches were thrown and empathy was the order of the day. (And while it’s not true that the Pathfinder principals who attended the meeting wore Kevlar® undergarments, the Godiva® chocolates we brought along sure didn’t hurt.) By the end of the meeting, we had achieved a better understanding of the tenants’ issues and we were able to implement meaningful changes to help alleviate their concerns (i.e., no hammering before 10:00 a.m. on weekends). The residents appreciated the opportunity to voice their concerns and the discussion led to a new level of mutual respect on both sides.

Seek Trustworthy, Local Partners

“A good friend who points out mistakes and imperfections and rebukes evil is to be respected as if he reveals a secret of hidden treasure.” - Buddha

Because we’re in the business of buying opportunistic and value-add real estate, Pathfinder’s properties tend to come with their own unique challenges. Some properties have a little “hair” while others resemble Chewbacca from Star Wars. Providing a haircut and preparing the property for eventual resale always involves

diligent oversight and can sometimes require heavy lifting. But the implementation and quality control of the property improvements can prove difficult for properties a plane ride away. One strategy to offset this

GUEST FEATUREZen and the Art of Being a LandlordBy Matt Quinn, Director of Asset Management

THE PATHFINDER REPORT: SEPTEMBER 2014 8

challenge is to team with local, best-in-class property managers and to maintain these relationships through trust, good communication and alignment of incentives.

This methodology proved particularly helpful during one of Pathfinder’s more technical (and costly) renovations of a Seattle-area apartment project that we discovered was slowly sliding down a hillside. We assembled a team of local, trusted experts (a geotechnical consultant, structural engineer, general contractor and project manager) to help us assess the problem and develop a solution. Our ultimate solution, which by no means was a quick or inexpensive fix, involved securing the building to the underlying soil through a pin-pile system and jacking the building, via hydraulic lifts, back to level before pouring new concrete footings. Two months, 20 steel rods, seven inches of building-lift and a dozen broken windows later, our team managed to secure the building and reverse the sloping. In difficult and unfamiliar situations, we have learned to trust our experienced advisors – despite our elevated blood pressure

Go With Your Gut

“The mind is everything. What you think you become.”- Buddha

Pathfinder currently has more than 40 active investments in half-a-dozen western states. Given the number of active assets and a range of property types and geographies, we find ourselves making numerous decisions on a daily basis. While we study and analyze extensively, we’ve learned that in property-related decisions, our initial gut instinct is often on target. When a contractor’s bid seems expensive – it often is. When a contractor seems suspect – he often is. When the returns on a potential investment appear too attractive – they often are. Recently, when we sold a large apartment project, our instincts told us that the three broker opinions of value

we received were too conservative. Our math may not have made sense but our gut told us that we had a marquee, one-of-a-kind property for which the standard investment valuation metrics may not apply. In an effort to convey our belief that the property could sell above the brokers’ expectations, we marketed the property unpriced in the hope that we might be pleasantly surprised. We sold the property for more than $1,000,000 above the average broker opinion of value. The investment was a big success and another good lesson on the importance of trusting your instincts.

You Don’t Know What You Don’t Know (a.k.a. Remain Humble)

“Before enlightenment, I chopped wood and carried water. After enlightenment, I chopped wood and carried water.” - Buddha

While we enjoy singing of our successes, we also remain mindful of our failures and the lessons we learn from them. And we know that the

Buddha prizes humility above all. So we’re resolved to keep our heads down, continue to learn from our past experiences and stay Zen.

Matt Quinn is a Director at Pathfinder Partners, LLC focusing on asset management activities. Prior to joining Pathfinder in 2009, Matt worked with a San Diego-based firm which consulted on mergers and acquisitions and with the Wealth Management division of a California regional bank. Reach him at [email protected].

THE PATHFINDER REPORT: SEPTEMBER 2014 9

Phoenix, Bellwether for U.S. Housing Softens

Phoenix, among the hardest-hit U.S. housing markets during the 2006-2010 real estate downturn, bounced back hard and fast during the past several years. Home prices, down 56% from the peak, sprung back by about one-third. Homes in some stage of foreclosure, more than 50,000 in 2010, are an estimated 4,300 now. Today, sales activity is slowing and prices are plateauing. Inventories of homes for sale have reached their highest level since 2011 while year-over-year sales fell 12% in June.

And Phoenix is not alone. Listings in Sacramento rose 44% in July as sales fell 11%. It’s a similar story in Sin City: sales in Las Vegas dipped 10% with listings skyrocketing 53% from July 2013 to July 2014. Nationally, sales are down 5% in July over the same month last year. In a mid-August report, Fannie Mae reduced its national housing forecasts for 2014 and 2015. Fannie now forecasts 431,000 new-home sales this year, a paltry gain of 0.6% over 2013.

As the blowback from high foreclosures (which led to massive purchases of homes by investors) fades, the market is increasingly reliant on traditional drivers – job growth, consumer purchasing power, mortgage availability and interest rates. Rising prices (they’re up 46%) have caused investors to scale back their purchases while homeowners test the market. The upshot is falling demand and rising supply. Don’t look for further price declines as plenty of investors are waiting in the wings, combing markets for any remaining deals (they’re scarce) and standing ready to prop up local housing markets.

Source: The Wall Street Journal

What Renters Really Want

Houston-based multifamily research firm, J Turner Research, recently released some tidbits from its largest-ever apartment resident survey. The survey featured over 27,600 participants and focused on resident lifestyle preferences. Much of the feedback was to be expected. Millennials (33 and younger) made up the largest portion of respondents. Gyms and walkability are must-haves. Quiet space is essential. But, a few of the findings were surprising:

• 84% of rentersspend their weekday evenings inside their homes and almost 75% of the respondents never or rarely visit nightclubs.

• 42% of renters cookevery day and 73% rank a grocery as the most important store to have near their apartment.

• 67%ofrentersdonothaveapetand81%donotrent storage units – the need for pet amenities and storage units may be more hype than reality.

• Energy-efficientappliancesrankedasthetop-choiceamong green apartment features and 17% of renters want to buy an electric car in the next five years.

The survey’s results can be interpreted in numerous ways but there are a few easy lessons for apartment developers and renovators:

• Renters spend a lot of time at home and like to cook – comfortable unit interiors and functional kitchens are crucial.

• All else being equal, communities near grocery stores have an edge on the competition.

• Today’s renter is eco-conscience and communities need to cater to this evolving, green minded demographic (this trend is most likely going to become more pronounced over time).

Source: Multifamily Executive

ZEITGEIST –SIGN OF THE TIMES

THE PATHFINDER REPORT: SEPTEMBER 2014 10

Deciphering the Zillow/Trulia Merger

Zillow and Trulia were both founded in 2005 with the goal of revolutionizing the retail home buying process. Nine years later, the combined companies account for 48% of home listing web traffic. Last month, Zillow announced its plan to acquire Trulia for $3.5 billion, creating what industry insiders have dubbed “Godzulia”. So what does this mean for consumers and investors? Ideally, consumers would expect more accurate and up-to-date data through the merger with the two companies now able to combine their respective home listing sources (MLS, individual brokers and third-party service providers). Zillow’s

“Zestimate” – the proprietary algorithm that calculates how much a property is worth – may also become more precise through

the combined platform. Interestingly, Zillow doesn’t list increased accuracy as an expected benefit of the merger and analysts believe the deal is simply a market-share grab. If this is the case, the consumer may be disadvantaged by the proposed merger as less competition can result in decreased innovation and poor customer service.

Investors in the two companies saw excellent initial results from news of the merger with stock prices for Zillow and Trulia spiking 15% and 25%, respectively, following the initial announcement in late July. Stocks of both companies have subsequently declined from their post-announcement highs by nearly 15%, possibly because the companies have yet to prove they can profitably grow their advertising revenue and web traffic. Additionally, the National Association of Realtors (“NAR”) is reportedly requesting that federal antitrust regulators block the merger on the grounds that the real estate internet search industry is already too consolidated.

Source: The Wall Street Journal

THE PATHFINDER REPORT: SEPTEMBER 2014 11

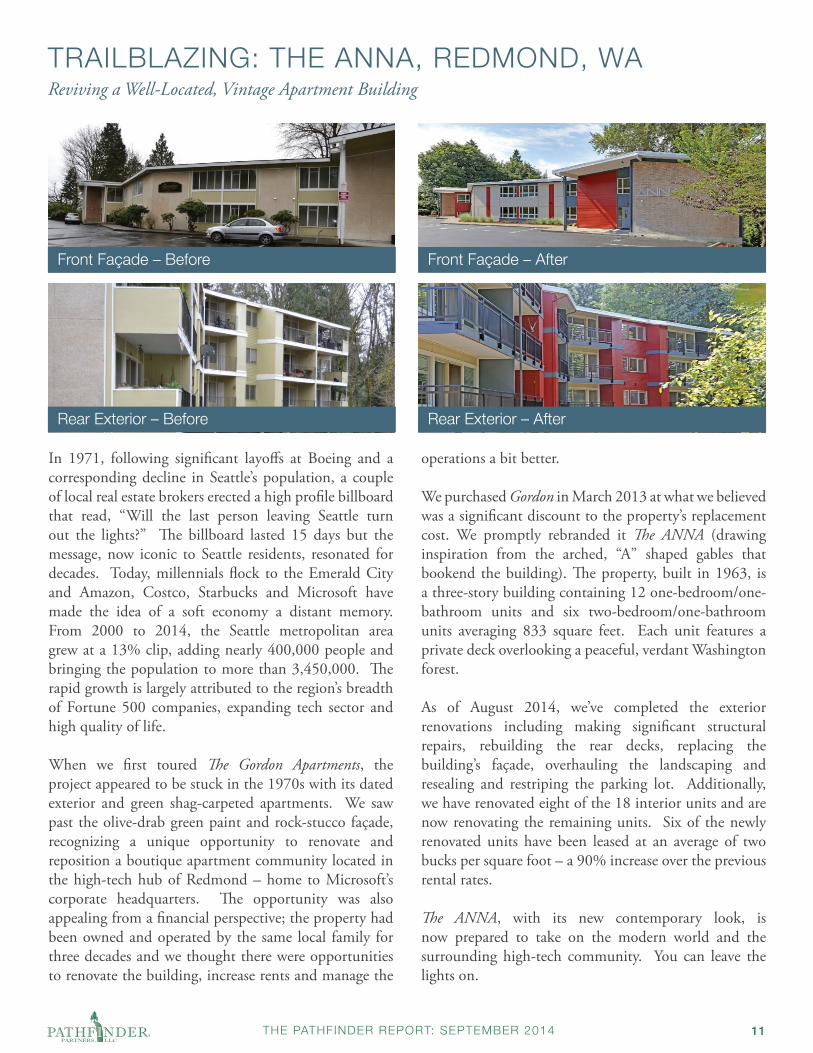

TRAILBLAZING: THE ANNA, REDMOND, WAReviving a Well-Located, Vintage Apartment Building

In 1971, following significant layoffs at Boeing and a corresponding decline in Seattle’s population, a couple of local real estate brokers erected a high profile billboard that read, “Will the last person leaving Seattle turn out the lights?” The billboard lasted 15 days but the message, now iconic to Seattle residents, resonated for decades. Today, millennials flock to the Emerald City and Amazon, Costco, Starbucks and Microsoft have made the idea of a soft economy a distant memory. From 2000 to 2014, the Seattle metropolitan area grew at a 13% clip, adding nearly 400,000 people and bringing the population to more than 3,450,000. The rapid growth is largely attributed to the region’s breadth of Fortune 500 companies, expanding tech sector and high quality of life.

When we first toured The Gordon Apartments, the project appeared to be stuck in the 1970s with its dated exterior and green shag-carpeted apartments. We saw past the olive-drab green paint and rock-stucco façade, recognizing a unique opportunity to renovate and reposition a boutique apartment community located in the high-tech hub of Redmond – home to Microsoft’s corporate headquarters. The opportunity was also appealing from a financial perspective; the property had been owned and operated by the same local family for three decades and we thought there were opportunities to renovate the building, increase rents and manage the

operations a bit better.

We purchased Gordon in March 2013 at what we believed was a significant discount to the property’s replacement cost. We promptly rebranded it The ANNA (drawing inspiration from the arched, “A” shaped gables that bookend the building). The property, built in 1963, is a three-story building containing 12 one-bedroom/one-bathroom units and six two-bedroom/one-bathroom units averaging 833 square feet. Each unit features a private deck overlooking a peaceful, verdant Washington forest.

As of August 2014, we’ve completed the exterior renovations including making significant structural repairs, rebuilding the rear decks, replacing the building’s façade, overhauling the landscaping and resealing and restriping the parking lot. Additionally, we have renovated eight of the 18 interior units and are now renovating the remaining units. Six of the newly renovated units have been leased at an average of two bucks per square foot – a 90% increase over the previous rental rates.

The ANNA, with its new contemporary look, is now prepared to take on the modern world and the surrounding high-tech community. You can leave the lights on.

Front Façade – Before Front Façade – After

Rear Exterior – Before Rear Exterior – After

THE PATHFINDER REPORT: SEPTEMBER 2014 12

“

“Value investing is at its core the marriage of contrarian streak and a calculator.”

- Seth Klarman,Founder of Baupost Group

“It is impossible to produce superior performance unless you do something different from the majority.”

- John Templeton,Founder Templeton Global Funds

“I will tell you how to become rich. Close the doors. Be fearful when others are greedy. Be greedy when others are fearful.”

- Warren Buffet

“Doing what everyone else is doing at the moment, and therefore what you have an almost irresistible urge to do, is often the wrong thing to do at all.”

- Phil Fisher,American investor and author of

“Common Stocks and Uncommon Profits”“NOTABLES AND QUOTABLES

Contrarian Investing

“Mimicking the herd invites regression to the mean.”

- Charles Munger,Vice-Chairman, Berkshire Hathaway

“If everyone is thinking alike, then no one is thinking.”

- Benjamin Franklin

THE PATHFINDER REPORT: SEPTEMBER 2014 13

IMPORTANT DISCLOSURES

Copyright 2014, Pathfinder Partners, LLC (“Pathfinder”). All rights reserved. This report is prepared for the use of Pathfinder’s clients and business partners and subscribers to this report and may not be redistributed, retransmitted or disclosed, in whole or in part, or in any form or manner, without our written consent.

The information contained within this newsletter is not a solicitation or offer, or recommendation to acquire or dispose of any investment or to engage in any other transaction. Pathfinder Partners LLC does not render or offer to render personal investment advice through our newsletter. Information contained herein is opinion-based reflecting the judgments and observations of Pathfinder personnel and guest authors. Our opinions should be taken in context and not considered the sole or primary source of information.

Materials prepared by Pathfinder research personnel are based on public information. The information herein was obtained from various sources. Pathfinder does not guarantee the accuracy of the information.

All opinions, projections and estimates constitute the judgment of the authors as of the date of the report and are subject to change without notice.

This newsletter is not intended and should not be construed as personalized investment advice. Neither Pathfinder nor any of its directors, officers, employees or consultants accepts any liability whatsoever for any direct, indirect or consequential damages or losses arising from any use of this report or its contents.

Do not assume that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended or undertaken by Pathfinder Partners LLC) made reference to directly or indirectly by Pathfinder Partners LLC in this newsletter, or indirectly via a link to an unaffiliated third party web site, will be profitable or equal past performance level(s).

Investing involves risk of loss and you should be prepared to bear investment loss, including loss of original investment. Real estate investments are subject to the risks generally inherent to the ownership of real property and loans, including: uncertainty of cash flow to meet fixed and other obligations; uncertainty in capital markets as it relates to both procurements of equity and debt; adverse changes in local market conditions, population trends, neighborhood values, community conditions, general economic conditions, local employment conditions, interest rates, and real estate tax rates; changes in fiscal policies; changes in applicable laws and regulations (including tax laws); uninsured losses; delays in foreclosure; borrower bankruptcy and related legal expenses; and other risks that are beyond the control of the General Partner. There can be no assurance of profitable operations because the cost of owning the properties may exceed the income produced, particularly since certain expenses related to real estate and its ownership, such as property taxes, utility costs, maintenance costs and insurance, tend to increase over time and are largely beyond the control of the owner. Moreover, although insurance is expected to be obtained to cover most casualty losses and general liability arising from the properties, no insurance will be available to cover cash deficits from ongoing operations.

Please add [email protected] to your address book to ensure you keep receiving our notifications.

Related Documents

![PlAne-hoPPer s K Andboo - The Trove [multi]/1st Edition...Legends, Pathfinder Map Pack, Pathfinder Module, Pathfinder Pawns, Pathfinder Player Companion, Pathfinder Roleplaying Game,](https://static.cupdf.com/doc/110x72/60c09751c0e51316cd1dc344/plane-hopper-s-k-andboo-the-trove-multi1st-edition-legends-pathfinder-map.jpg)