I n September of 1999, Viacom announced its merger with CBS. 1 The huge deal combined CBS’s television network, its 15 TV stations, more than 160 radio stations, and several Internet sites with Viacom’s well- known cable channels (e.g., MTV, Nickelodeon, Showtime, TNN), 19 television stations, movie and television production (Paramount Pictures, UPN), publishing (Simon & Schuster), theme parks, and more. The $38 billion merger was bigger than any previous deal between two media com- panies. In fact, it was almost double the size of the previous record. The 1995 record-setting deal in which Disney acquired Capital Cities/ABC had been worth $19 billion [$21.2 billion]. While the size of the Viacom/CBS deal was unprecedented, the basic dynamic underlying the merger was not. Since the mid-1980s, major media companies had been engaged in a feeding frenzy, swallowing up other media firms to form ever-larger conglomerates. Including the Viacom/CBS merger, the 1990s alone saw well over $300 billion in major media deals. So rather than being unique, the Viacom/CBS announcement was just ◆ 21 2 ◆ David Croteau and William Hoynes THE NEW MEDIA GIANTS Changing Industry Structure NOTE: From The Business of Media: Corporate Media and the Public Interest (pp. 71-107), by David Croteau and William Hoynes, 2001, Thousand Oaks, CA: Pine Forge. Copyright 2001. Reprinted by permission of Sage Publications, Inc.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

In September of 1999, Viacom announced its merger with CBS.1

The huge deal combined CBS’s television network, its 15 TV stations,more than 160 radio stations, and several Internet sites with Viacom’s well-known cable channels (e.g., MTV, Nickelodeon, Showtime, TNN),19 television stations, movie and television production (Paramount Pictures,UPN), publishing (Simon & Schuster), theme parks, and more. The $38billion merger was bigger than any previous deal between two media com-panies. In fact, it was almost double the size of the previous record. The1995 record-setting deal in which Disney acquired Capital Cities/ABC hadbeen worth $19 billion [$21.2 billion].

While the size of the Viacom/CBS deal was unprecedented, the basicdynamic underlying the merger was not. Since the mid-1980s, major mediacompanies had been engaged in a feeding frenzy, swallowing up othermedia firms to form ever-larger conglomerates. Including the Viacom/CBSmerger, the 1990s alone saw well over $300 billion in major media deals.So rather than being unique, the Viacom/CBS announcement was just

◆ 21

2

◆ David Croteau and William Hoynes

THE NEW MEDIA GIANTSChanging Industry Structure

NOTE: From The Business of Media: Corporate Media and the Public Interest(pp. 71-107), by David Croteau and William Hoynes, 2001, Thousand Oaks, CA:Pine Forge. Copyright 2001. Reprinted by permission of Sage Publications, Inc.

Dines02.qxd 7/26/02 2:33 PM Page 21

another example—and certainly not thelast—of the mergers that transformed theindustry toward the end of the 20th century.

These deals not only changed the mediaindustry playing field but also sometimesmade it difficult to figure out who, exactly,were the players. While media mergers andacquisitions had been mostly betweenmedia companies, there were also non-media companies who ventured into thelucrative media market. In 1985, manu-facturing giant General Electric boughtRCA—owners of the NBC broadcast net-work. Westinghouse—producer of every-thing from household appliances tocomponents for nuclear reactors—boughtCBS in 1995. Three years later, the com-bined company dropped the Westinghousename in favor of CBS Corporation and thenproceeded to sell off the manufacturingparts of the conglomerate—in essence split-ting back into two companies. Seagram’s,best known for its alcoholic drinks andTropicana orange juice, became a majormedia company, buying MCA in 1995(now Universal Studios), Polygram recordsin 1998, and others. Microsoft, the soft-ware behemoth, also began investing in tra-ditional media companies such as the cablecompany Comcast, as well as Internet sites,and entering into a vast number of othermedia deals. Most important, traditionaltelecommunications firms also became cen-tral media players. In fact, at the time of theViacom/CBS merger, the only media dealsthat had been larger were the ones in whichphone company giant AT&T acquired twocable companies, TCI (for $48 billion in1998) and MediaOne (for $54 billion in1999); a sign of the coming integration oftelephony, cable television, and Internetaccess.

◆ Making Sense of Mergers

At various points in history antimonopolyconcerns have resulted in the dismantling ofmedia conglomerates. In more recent years,

facilitated by an increasingly lax regulatoryenvironment, major media companies havebeen buying and merging with other com-panies to create ever-larger media conglom-erates, all of which are now global in theiractivities. A decade and a half of such merg-ers have rapidly transformed the organiza-tional structure and ownership pattern ofthe media industry. In the process, thedilemmas associated with the market andpublic sphere models of media have beendramatically highlighted.

From a market perspective, industrychanges such as the Viacom/CBS deal canbe understood as the rational actions ofmedia corporations attempting to maxi-mize sales, create efficiencies in production,and position themselves strategically to facepotential competitors. Despite the growthin media conglomerates, many observersbelieve the profusion of media outlets madepossible by recent technological develop-ments—especially cable and the Internet—makes the threat of monopolisticmisbehavior by these media giants highlyunlikely. How can we talk about monopo-lies, they ask, when we have moved from asystem of three television networks to onethat will soon boast 500+ channels? Howcan a handful of companies monopolize thedecentralized Internet? The media industryas a whole has grown, they also note, andthe larger media companies simply reflectthe expansion of this field.

But the public sphere perspective directsus to a different set of concerns. Growth inthe number of media outlets, for example,does not necessarily ensure content thatserves the public interest. Centralized cor-porate ownership of vast media holdingsraises the possibility of stifling diverseexpression and raises important questionsabout the powerful role of media in ademocratic society. Even with new mediaoutlets, it is still a handful of media giantswho dominate what we see, hear, and read.The expansion of new media technologieshas only strengthened, not undermined,the power and influence of new mediaconglomerates. . . .

22 ◆ A Cultural Studies Approach

Dines02.qxd 7/26/02 2:33 PM Page 22

The New Media Giants ◆ 23

◆ Structural Trends in theMedia Industry

The basic structural trends in the mediaindustry have been characterized in recentyears by four broad developments.

1. Growth. Mergers and buyouts havemade media corporations bigger thanever.

2. Integration. The new media giantshave integrated either horizontally bymoving into multiple forms of mediasuch as film, publishing, radio, and soon, or vertically by owning differentstages of production and distribution,or both.

3. Globalization. To varying degrees, themajor media conglomerates havebecome global entities, marketing theirwares worldwide.

4. Concentration of ownership. As majorplayers acquire more media holdings,the ownership of mainstream mediahas become increasingly concentrated.

Some of these phenomena are overlap-ping or interrelated developments.However, to describe the specifics of thesedevelopments, we examine each separately.

GROWTH

The last decades of the 20th century willbe remembered as ones of expansive mediagrowth. Not only was the number of mediaoutlets available to the public via cable,satellite, and the Internet greater than ever,but the media companies themselves weregrowing at an unprecedented pace. In 1983,the largest media merger to date had beenwhen the Gannett newspaper chain boughtCombined Communications corporation—owner of billboards, newspapers, andbroadcast stations—for $340 million [$581million]. Even when the value of that deal is

adjusted for inflation, 1999’s $38 billionViacom-CBS deal was more than 65 timesas big.

This enormous growth in conglomera-tion was largely fueled by a belief in the var-ious benefits to be had from being big.Larger size meant more available capital tofinance increasingly expensive media pro-jects and size was also associated with effi-ciencies of scale. But most important,integrated media conglomerates can exploitthe “synergy” created by having many out-lets in multiple media. Synergy refers to thedynamic where components of a companywork together to produce benefits thatwould be impossible for a single, separatelyoperated unit of the company. In the cor-porate dreams of media giants, synergyoccurs when, for example, a magazinewrites about an author, whose book is con-verted into a movie (whose CD soundtrackis played on radio stations), which becomesthe basis of a television series, which has itsown Web site and computer games.Packaging a single idea across all these var-ious media allows corporations to generatemultiple revenue streams from a single con-cept. To do this, however, media companieshad to expand to unprecedented size.

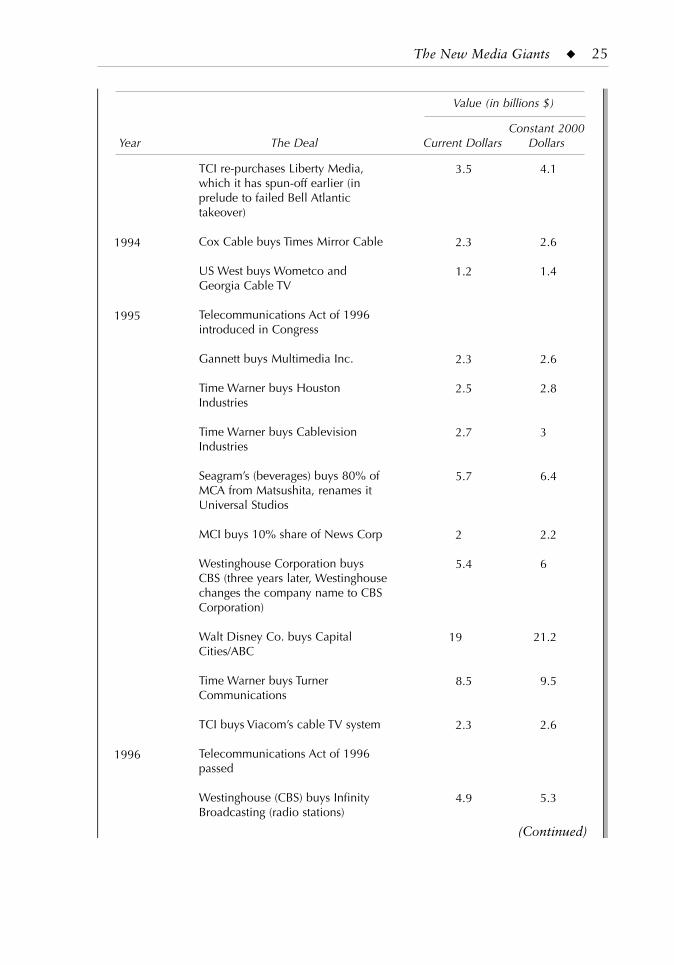

Ironically, as the scale of corporategrowth increased, concern with regulatingpotential media monopolies virtually dis-appeared from mainstream political dis-course. As a result, the big mediaplayers have—with sometimes stunningfrequency—been merging with or buyingout other big media players. (See Exhibit2.1.) To better understand these mergersand acquisitions, it is informative to take acloser look at one example, the Viacom/CBS deal mentioned earlier.

The Viacom/CBS Merger

CBS was created in 1928 and has longbeen a major broadcaster with a strongradio and television presence. Throughmuch of its history, it was popularly associ-ated with its news programming, especiallywith Edward R. Murrow and WalterCronkite, who were among the preeminent

(Text continues on page 28)

Dines02.qxd 7/26/02 2:33 PM Page 23

24 ◆ A Cultural Studies Approach

1985

1986

1987

1989

1990

1993

Rupert Murdoch’s News Corp.(newspapers, television in Australia,Britain, U.S.) buys Metromedia (sixtelevision stations) as the launchingpad for his new Fox network

Turner Broadcasting buysMGM/United Artists (keepingMGM’s library of 3,000 films butselling off the rest for $.8 billion)

General Electric buys RCA (ownersof NBC network)

Capital Cities (backed by investorWarren Buffett) buys the muchlarger ABC television network

National Amusements (movietheaters) buys Viacom

Sony buys CBS Records

Time Inc. merges with WarnerCommunications

Sony acquires control of ColumbiaPictures and TriStar movie studios

Matsushita Electric Industrial Co.buys MCA (Universal Studios,Geffen Records, Motown)

US West buys a quarter share ofTime Warner

Viacom buys ParamountCommunications (Universal Studios,Geffen Records, New York Knicks,publishing)

Viacom buys Blockbuster

$1.6

1.5

6.4

3.5

3.4

2

14.1

4.8

6.6

2.5

8.3

4.9

$2.5

2.4

10.1

5.5

5.3

3

19.4

6.6

8.6

2.9

9.8

5.8

Exhibit 2.1 Select Media Mergers and Acquisitions of $1 Billion (current) or More(1984-2000)

Value (in billions $)

Constant 2000Year The Deal Current Dollars Dollars

Dines02.qxd 7/26/02 2:33 PM Page 24

The New Media Giants ◆ 25

1994

1995

1996

TCI re-purchases Liberty Media,which it has spun-off earlier (inprelude to failed Bell Atlantictakeover)

Cox Cable buys Times Mirror Cable

US West buys Wometco andGeorgia Cable TV

Telecommunications Act of 1996introduced in Congress

Gannett buys Multimedia Inc.

Time Warner buys HoustonIndustries

Time Warner buys CablevisionIndustries

Seagram’s (beverages) buys 80% ofMCA from Matsushita, renames itUniversal Studios

MCI buys 10% share of News Corp

Westinghouse Corporation buysCBS (three years later, Westinghousechanges the company name to CBSCorporation)

Walt Disney Co. buys CapitalCities/ABC

Time Warner buys TurnerCommunications

TCI buys Viacom’s cable TV system

Telecommunications Act of 1996passed

Westinghouse (CBS) buys InfinityBroadcasting (radio stations)

3.5

2.3

1.2

2.3

2.5

2.7

5.7

2

5.4

19

8.5

2.3

4.9

4.1

2.6

1.4

2.6

2.8

3

6.4

2.2

6

21.2

9.5

2.6

5.3

(Continued)

Value (in billions $)

Constant 2000Year The Deal Current Dollars Dollars

Dines02.qxd 7/26/02 2:33 PM Page 25

26 ◆ A Cultural Studies Approach

Exhibit 2.1 continued

Value (in billions $)

Constant 2000Year The Deal Current Dollars Dollars

1997

1998

News Corp. buys New WorldCommunications Group, Inc.

US West buys controlling interest inContinental Cablevision

A. H. Belo Corporation buysProvidence Journal Company (16TV stations plus major newspapers)

Tribune Company buys RenaissanceCommunications (TV stations)

Microsoft buys an 11.5% stake inComcast Corp

Reed Elsevier and Wolters Kluwermerge (print/electronicpublishing/databases; Lexis/Nexis)

News Corp buys internationalFamily Entertainment (FamilyChannel and MTM EntertainmentTV production)

TCI buys one-third of CablevisionSystems

Westinghouse-CBS buys AmericanRadio Systems

Westinghouse-CBS acquiresGaylord, owners of Country MusicTV and The Nashville Network

AT&T buys TCI(Tele-Communications, Inc)

Bertelsmann buys RandomHouse/Alfred a. Knopf/CrownPublishing

AOL (America Online) buysNetscape (Internet browser)

Seagram buys Polygram (music)

3.6

10.8

1.5

1.1

1

7.8

1.9

1.1

2.6

1.6

53.6

1.3

4.2

15.1

3.9

11.7

1.6

1.2

1.1

8.3

2

1.2

2.8

1.7

56

1.4

4.4

15.8

Dines02.qxd 7/26/02 2:33 PM Page 26

The New Media Giants ◆ 27

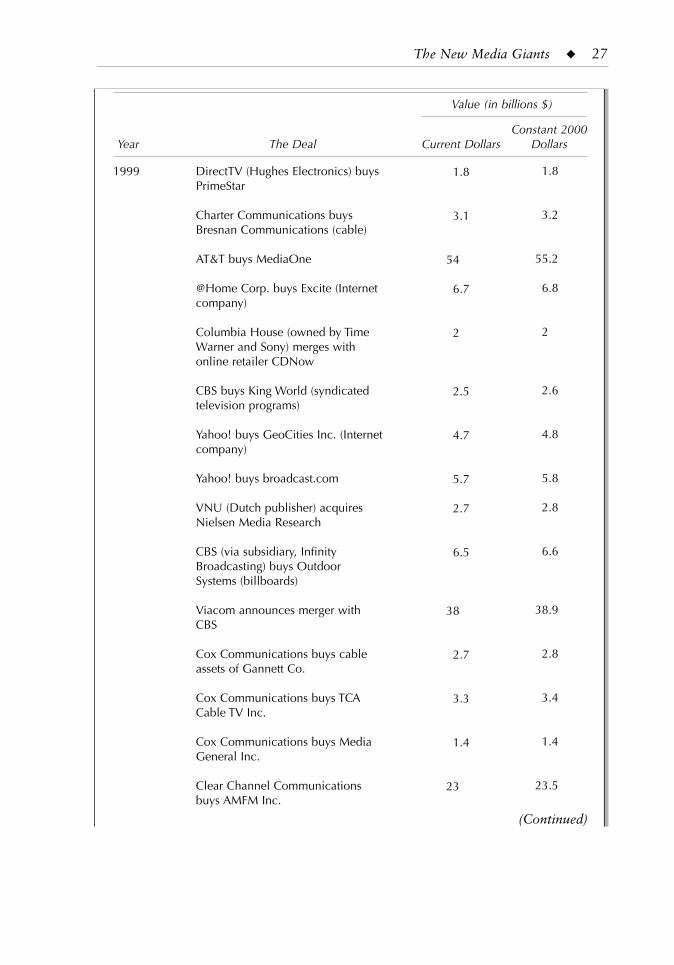

1999 DirectTV (Hughes Electronics) buysPrimeStar

Charter Communications buysBresnan Communications (cable)

AT&T buys MediaOne

@Home Corp. buys Excite (Internetcompany)

Columbia House (owned by TimeWarner and Sony) merges withonline retailer CDNow

CBS buys King World (syndicatedtelevision programs)

Yahoo! buys GeoCities Inc. (Internetcompany)

Yahoo! buys broadcast.com

VNU (Dutch publisher) acquiresNielsen Media Research

CBS (via subsidiary, InfinityBroadcasting) buys OutdoorSystems (billboards)

Viacom announces merger withCBS

Cox Communications buys cableassets of Gannett Co.

Cox Communications buys TCACable TV Inc.

Cox Communications buys MediaGeneral Inc.

Clear Channel Communicationsbuys AMFM Inc.

1.8

3.1

54

6.7

2

2.5

4.7

5.7

2.7

6.5

38

2.7

3.3

1.4

23

1.8

3.2

55.2

6.8

2

2.6

4.8

5.8

2.8

6.6

38.9

2.8

3.4

1.4

23.5

(Continued)

Value (in billions $)

Constant 2000Year The Deal Current Dollars Dollars

Dines02.qxd 7/26/02 2:33 PM Page 27

28 ◆ A Cultural Studies Approach

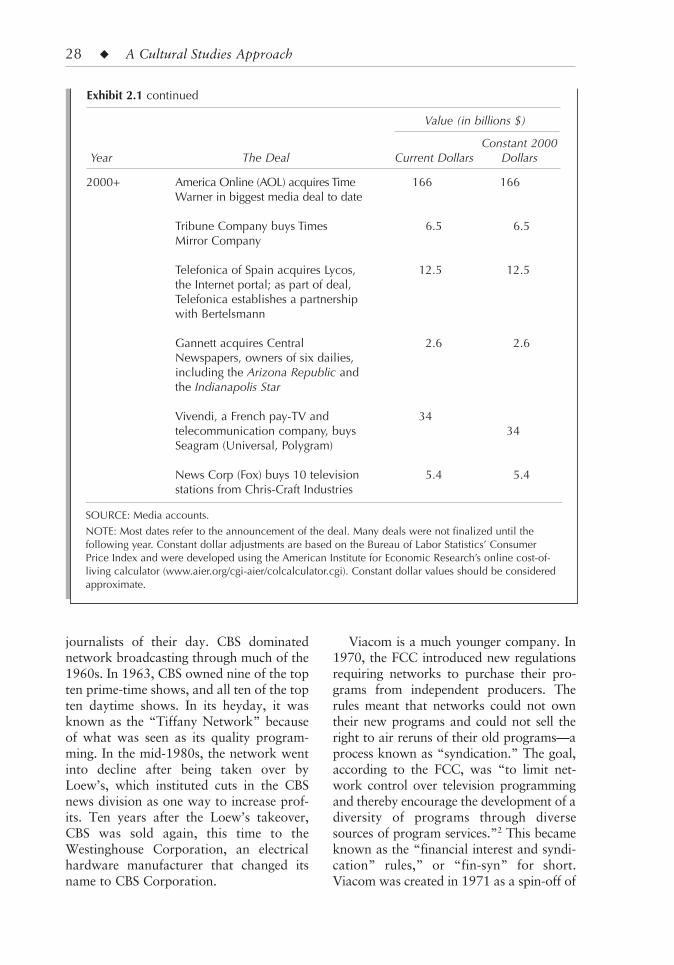

journalists of their day. CBS dominatednetwork broadcasting through much of the1960s. In 1963, CBS owned nine of the topten prime-time shows, and all ten of the topten daytime shows. In its heyday, it wasknown as the “Tiffany Network” becauseof what was seen as its quality program-ming. In the mid-1980s, the network wentinto decline after being taken over byLoew’s, which instituted cuts in the CBSnews division as one way to increase prof-its. Ten years after the Loew’s takeover,CBS was sold again, this time to theWestinghouse Corporation, an electricalhardware manufacturer that changed itsname to CBS Corporation.

Viacom is a much younger company. In1970, the FCC introduced new regulationsrequiring networks to purchase their pro-grams from independent producers. Therules meant that networks could not owntheir new programs and could not sell theright to air reruns of their old programs—aprocess known as “syndication.” The goal,according to the FCC, was “to limit net-work control over television programmingand thereby encourage the development of adiversity of programs through diversesources of program services.”2 This becameknown as the “financial interest and syndi-cation” rules,” or “fin-syn” for short.Viacom was created in 1971 as a spin-off of

SOURCE: Media accounts.

NOTE: Most dates refer to the announcement of the deal. Many deals were not finalized until thefollowing year. Constant dollar adjustments are based on the Bureau of Labor Statistics’ ConsumerPrice Index and were developed using the American Institute for Economic Research’s online cost-of-living calculator (www.aier.org/cgi-aier/colcalculator.cgi). Constant dollar values should be consideredapproximate.

2000+ America Online (AOL) acquires TimeWarner in biggest media deal to date

Tribune Company buys TimesMirror Company

Telefonica of Spain acquires Lycos,the Internet portal; as part of deal,Telefonica establishes a partnershipwith Bertelsmann

Gannett acquires CentralNewspapers, owners of six dailies,including the Arizona Republic andthe Indianapolis Star

Vivendi, a French pay-TV andtelecommunication company, buys Seagram (Universal, Polygram)

News Corp (Fox) buys 10 televisionstations from Chris-Craft Industries

166

6.5

12.5

2.6

34

5.4

166

6.5

12.5

2.6

34

5.4

Exhibit 2.1 continued

Value (in billions $)

Constant 2000Year The Deal Current Dollars Dollars

Dines02.qxd 7/27/02 2:49 PM Page 28

The New Media Giants ◆ 29

CBS to comply with these new FCC regula-tions. In order to sell the syndication rightsto its old programs, such as I Love Lucy andThe Andy Griffith Show, CBS was requiredto create a new corporate entity, separatefrom the network. Thus, Viacom was born.

In 1986, National Amusements, a movietheater chain headed by Sumner Redstone,purchased Viacom for $3.4 billion [$5.3billion], keeping the name for the new com-pany. Viacom grew quickly, purchasingother media enterprises. Most notably, in1993, it bought Paramount for $8.3 billion[$9.8 billion] and Blockbuster Video for$4.9 billion [$5.8 billion]. From a stepchildof CBS, Viacom had become a media giantin its own right. In 1999, the circle wascompleted as Viacom returned to purchaseits former parent, CBS, for $38 billion,creating a new Viacom that was estimatedto be worth over $70 billion.

So what happened? Why was a muchsmaller media company being broken up in1971 under the fear of monopoly, while amuch larger company was allowed to keepgrowing in 1999? The equation was some-thing like this: technology + politics = dereg-ulation. It was the combination of changingcommunications technology, coupled with aconservative shift in national politics, thatled to major deregulation of the mediaindustry. This deregulation, in turn, allowedmedia corporations to expand rapidly.

Changing Technology

New technology is one key element facil-itating industry changes. When CBS wasforced to spin off Viacom in 1971, tele-vision viewer options were usually limitedto three national broadcast networks (ABC,CBS, and NBC), public television, and per-haps one or two local independent stations.By the end of the century, there were sixnational broadcast networks of varying size(including Fox, WB, UPN), a virtuallycountless number of cable channels, and“direct TV” satellite options. Media corpo-rations argued that many ownership regu-lations were no longer needed in this worldof proliferating media outlets.

If television offered abundant choices,critics of regulation contended, then theInternet was virtually limitless in its offer-ings. In its early days, especially, theInternet was seen even by many critics ofmainstream media as an antidote to bigmedia. Because of the apparently low costof entry and virtually no-cost distribution,it was thought to be a way to level the play-ing field between large media conglomer-ates and smaller independent producers.This, too, was a part of the argumentagainst regulation of big media.

But while technology has undoubtedlychanged the face of mass media, some ofthe changes amount to less than they firstappear. For example, while changes in tele-vision technology are ushering in the eraof the 500-channel universe, these newoptions—unlike traditional broadcast tele-vision—are expensive alternatives thatmany Americans cannot afford. At the endof the century, nearly a third of Americanhouseholds had no cable service at all andanother third had only basic cable.Expensive premium channels, pay-per-viewselections, and other options remain unaf-fordable to most families.

Also, more channels have not necessarilymeant more diversity. Instead, many of thecable options simply air either reruns ofbroadcast programs or provide a certaintype of previously existing programming(sports, music videos, etc.) 24 hours a day.More content does not necessarily meandifferent content.

The Internet, too, has shown signs ofbecoming dominated by major mediagiants. For a short period of time, manymajor media companies were not heavilyinvolved in Internet ventures. As a result,there was a brief window of opportunity fornew companies to get established. However,as this first stage of the industry passed, asecond stage of consolidation took place.

Two major types of players were drivingthis consolidation stage. First, as successfulnew Internet companies saw the value oftheir stock rise, they often tried to solidifythat value by buying something tangiblewith the money—often other media firms.

Dines02.qxd 7/26/02 2:33 PM Page 29

30 ◆ A Cultural Studies Approach

That way, when stock prices on overvaluedInternet companies fell—as they inevitablydid—these companies still had valuable, ifmore traditional, media assets. Second,after small ventures began showing how theInternet might be used for commerce, majormedia players stepped in either buying upsmaller companies or forcing them to mergein order to stay alive. Thus, establishedcompanies used their resources to buy theirway into the expanding Internet market.In the first half of 1999 alone, there wereover 650 Internet mergers and acquisitionsvalued at over $37 billion.3 This was morethan three times the number of deals madein the first six months of 1998.

The large-scale companies make it diffi-cult for new companies to compete inde-pendently. The once relatively low startupcosts of running a significant World WideWeb site—once touted as a central reasonfor the Internet’s revolutionary character—now routinely exceeds $1 million.4 As aresult, media companies with major capitalto invest now dominate the most popularsites on the World Wide Web.5

The Politics of Deregulation

If technology provided the tracks uponwhich deregulation was able to ride, thenconservative pro-business politics was theengine that propelled it along. The relax-ation of key regulations was absolutely cen-tral to the rapid expansion of mediaconglomerates. . . .

In 1993, a U.S. District Court ruled thatbroadcast networks should no longer besubject to many of the fin-syn regulations.Previously, television networks acquiredprogramming from outside producers whocontinued to own the programs. However,with the elimination of “fin-syn” rules, net-works were now free to air their own pro-gramming. Increased vertical integration ofproduction and exhibition resulted. Forexample, in the summer of 1999, Disneyformalized its vertical integration in tele-vision by merging its television productionstudios with its ABC network operations.The shift was aimed at controlling costs by

encouraging the in-house development andproduction of programs by Disney/ABC forbroadcast on the ABC network.6 Such inte-gration would have been impossible with-out the change in fin-syn regulations. . . .

The anti-regulatory sentiment in govern-ment that had escalated with the RepublicanReagan and Bush administrations continuedinto Democrat Bill Clinton’s administra-tion. Nowhere was this more clear than inthe passage of the wide-ranging 1996 Tele-communications Act. The act had beenheavily promoted by the media and telecom-munications industries, leading even theNew York Times to editorialize, “Forty mil-lion dollars’ worth of lobbying boughttelecommunications companies a piece ofSenate legislation they could relish. But con-sumers have less to celebrate.” The Timeswent on to argue that the bill’s “anti-regula-tory zeal goes too far, endangering the verycompetition the bill is supposed to create.”7

But antiregulation ruled the day andamong the many provisions of the act werethose that relaxed the regulations on thenumber of media outlets a single companymay own. (See Exhibit 2.2.) While theTelecommunications Act was promotedusing a market approach that emphasizedmore competition, the changes actuallyhelped to fuel a new wave of media mergersand acquisitions.

Patricia Aufderheide notes that “in themonths following the act, mergers and buy-outs multiplied. In 1997 alone, $154 billion[$163 billion] in media and telecommuni-cation deals was recorded in the followingcategories, according to Paul KaganAssociates research, telephone, $90[b]illion; radio, $8.3 billion; TV stationdeals, $9.3 billion; and entertainment andmedia networks, $22 billion.”8

One of the act’s provisions called for areview of certain ownership restrictionsand, as a result, the FCC announcedanother round of deregulation in the sum-mer of 1999. This time the FCC easedrestrictions on the number of local radioand television stations a single companycan own. The FCC eliminated regulations

Dines02.qxd 7/26/02 2:33 PM Page 30

The New Media Giants ◆ 31

restricting companies to one local TVstation in a market. Now companies areallowed to own two stations, as long as atleast eight other competitors are in thesame market and one of the company’s

two stations is not among the market’s topfour. Other conditions too, such as a fail-ing station, can be used to justify multiplestation ownership. In a reflection of theconvergence of media forms, another

Exhibit 2.2 Select Ownership Rules Changes in the 1996 Telecommunications Act

The 1996 Telecommunications Act eased restrictions on media ownership, leading tolarger media companies and more concentration of ownership.

Previous Rules New Rule Changes

National television

A single entity:Can own up to 12 stations No limit on number of stations

nationwide or Station reach increased to 35% of Can own stations reaching up to U.S. TV households

25% of U.S. TV households

Local television

A single entity:Can own only one station in a market Telecom Act called for review

In 1999, FCC announced it wouldallow multiple station ownership ina single market under certaincircumstances

National radio

A single entity:Can own up to 20 FM and No limit on station ownership

20 AM stations

Local radio

A single entity: Ownership adjusted by market size:Cannot own, operate, or control more In markets with 45+ stations, a single

than 2 AM and 2 FM stations entity cannot own more than in a market 8 stations total and no more than 5 in

Audience share of co-owned the same service (AM or FM)stations cannot exceed 25% . . . with 30-44 stations; 7 total,

5 same service. . . with 15-29 stations; 6 total,

3 same service (but no more than50% of the stations in the market)

. . . with 14 or fewer; 5 total, 3 sameservice (but no more than 50% ofthe stations in the market)

Limits may be waived if the FCC rulesit will increase the total number ofstations in operation.

Dines02.qxd 7/26/02 2:33 PM Page 31

32 ◆ A Cultural Studies Approach

regulatory change now allows for a singlecompany to own two TV stations and sixradio stations in a market as long as thereare at least 20 competitors among allmedia—cable, newspapers, and otherbroadcast stations.9

Consumer advocates bemoaned thechanges, arguing that they once againwould lead to more media outlets in fewerhands. But media executives once again hadsomething to cheer about. Lowell “Bud”Paxon, owner of PAX TV, greeted thechanges by saying, “I can’t wait to have aglass of champagne and toast the FCC!”Barry Diller, chairman and CEO of USANetworks, observed, “This is a real signifi-cant step. . . . This is going to changethings.”10

He was right. Less than a month afterthese new FCC regulatory changes, Viacomand CBS announced their plans to merge—adeal that would have been impossiblebefore the relaxation of FCC regulations.Even with the new rules, the new Viacomwould violate existing regulations. Forexample, its television stations could reachinto 41% of American households, but theFCC cap was 35%. In addition, it ownedboth the CBS network and had a 50% stakein the UPN network, but FCC regulationsprevent a network owner from having anownership interest in another network.Finally, Viacom’s ownership of numerousradio and television stations violated own-ership limitation rules in a half dozen mar-kets. Upon approval of the deal, the FCCgave Viacom time to comply with suchregulations.11 Some observers, though,believed that the FCC might change someof these limits by the time the complianceperiod expired.

So the growth in media conglomerateshas been fueled, in part, by the changingregulatory environment. In the years whenpublic interest concerns about monopolieswere preeminent, media companies wereconstrained in their ability to growunchecked. However, with the rise of moremedia outlets via new technology, the con-servative shift toward business deregulation

since the Reagan era, and the growth inthe media industry’s lobbying clout, mediacorporations have been relatively unencum-bered in their desire to grow.

Thus, as the 20th century came to aclose, a loose regulatory environmentallowed Viacom and CBS to create a newmedia giant. As announced, the 1999merger created a Viacom that

◆ was the nation’s largest owner of TVstations,

◆ was the nation’s largest owner of radiostations,

◆ controlled the nation’s largest cable net-work group,

◆ controlled the nation’s largest billboardcompany,

◆ was the world’s largest seller of advertis-ing with estimated sales of $11 billion—nearly twice that of second-placeNews Corp ($5.8 billion), and morethan double its next two competitors(Disney’s $5.1 billion and TimeWarner’s $3.8 billion).

In an earlier era, such concentrated mar-ket power would likely have been met byregulatory roadblocks. In this new era ofderegulation, it is likely that the deal will befollowed in the coming years by furtherindustry consolidation and even largerdeals. . . .

INTEGRATION

Horizontal Integration

A media corporation that is horizontallyintegrated owns many different types ofmedia products. Viacom is clearly a hori-zontally integrated conglomerate because itowns, among other things, properties inbroadcast and cable television, film, radio,and the Internet—all different types ofmedia. . . .

With the transformation of text, audio,and visual media into digital data, the

Dines02.qxd 7/26/02 2:33 PM Page 32

The New Media Giants ◆ 33

technological platforms that underliedifferent media forms have begun to con-verge, blurring the lines between once-dis-tinct media.

One visible symbol of convergence is thecompact disk. This single digital data stor-age device can be used for text, audio,video, or all three simultaneously. Its intro-duction—along with other types of digitaldata storage devices—has changed thenature of media. The personal computer isanother symbol of change. It can be used tocreate and read text documents; show staticand animated graphics; listen to audio CDsor digital music files; play CD computergames that combine audio, video, and text;watch digital videos; access and print pho-tos taken with a digital camera; and surf theInternet, among other things. All this is pos-sible because of the common digital foun-dation for various media.

But the significance of digital dataextends way beyond CDs and computers.Now, the digital platform encompasses allforms of media. Television and radiobroadcast signals are being digitized andanalog signals phased out. Newspapersexist in digital form on the Internet, andtheir paper versions are often printed inplants that download the paper’s content indigital form from satellites. This allows forsimultaneous publication in many cities ofnational papers such as USA Today.Filmless digital movie theaters are begin-ning to appear, where movies, that weredigitally downloaded via the Internet, areshown with a sophisticated computerizedprojector.

The convergence of media products hasmeant that media businesses have also con-verged. The common digital foundation tocontemporary media has made it easier forcompanies to create products in differentmedia. For example, it was a relativelysmall step for newspapers—with contentalready produced on computers in digitalform—to developed online World WideWeb sites and upload newspaper articlesto it. Thus, newspaper publishers have

become Internet companies. In fact, manymedia have embraced the Internet as a closedigital cousin of what they already do. Themusic industry, to use another example, hasresponded to the proliferation of boot-legged digital music files (MP3, Napster,etc.) by developing its own systems todeliver music via the Web to consumers—for a fee, of course.

Furthermore, convergence has erodedthe walls between what used to be threedistinct industries: media, telecommunica-tions, and computers. Recently, majorcable TV companies began entering thephone service business and offeringcabled-based Internet access. “Baby Bells”and long-distance phone companies are gettinginvolved in video delivery and Internet access.Computer software firms are teaming up withcable companies to create various “smart boxes”that facilitate delivery of cable-based mediaand communications services. Integration,therefore, involves even companies outsideof the traditional media industry, making itmore difficult than ever to mark clearboundaries.

Vertical Integration

While horizontal integration involvesowning and offering different types ofmedia products, vertical integrationinvolves owning assets that are involved inthe different steps in the production, distri-bution, exhibition, and sale of a single typeof media product. In the media industry,vertical integration tends to be more limitedthan horizontal integration, but it can stillplay a significant role. For some time, therehas been a widespread belief that “contentis king.” That is, the rise of the Internet andcable television in particular has led to anexplosion in outlets available to delivermedia products. Consequently, owning themedia content that is to be distributed viathese channels is widely believed to bemore valuable than owning the channelsthemselves. However, with the eliminationof most fin-syn rules, interest in vertical

Dines02.qxd 7/26/02 2:33 PM Page 33

34 ◆ A Cultural Studies Approach

integration has resurfaced, enablingbroadcast networks to once again produceand exhibit their own programs.

Viacom’s vertical integration can beseen, for example, in the fact that it ownsfilm production and distribution companies(e.g., Paramount Pictures) and multiplevenues to exhibit these films. These venuesinclude theater chains to show first-runfilms (e.g., Famous Players and UnitedCinemas International theater chains) anda video store chain to distribute the movieonce it is available on videotape for rental(Blockbuster Video). Viacom also ownspremium cable channels (e.g., Showtime,The Movie Channel), basic cable channels(e.g., Comedy Central), and a broadcastnetwork (CBS), all to air a film after itsrental life is over. Thus, when Viacomproduces a movie, it is assured of multiplevenues for exhibition.

. . . The numerous mergers that have leftan industry dominated by larger companieshave also produced an industry where themajor players are highly integrated.

At first glance, the average person maybe unaware of these trends that havereshaped the media industry. It is usuallydifficult to discern that apparently diversemedia products are, in fact, all owned by asingle company. Take television, for exam-ple. If you surf the television universe, youmight come across a local CBS affiliate,MTV, Comedy Central, Nickelodeon,Showtime, a UPN affiliate, VH-1, TheMovie Channel, The Nashville Network,and your local team on Home TeamSports. It is virtually impossible for thecasual viewer to realize that all of these areactually owned—all or in part—byViacom. It is even less likely that they willconnect the owners of all these stationswith the owner of their local theme park,movie theater, and radio stations. Butagain, one company could own them all:Viacom. However, Viacom is not unique inthis regard. The same phenomenon is trueof other collections of disparate media out-lets that are owned by the other mediagiants.

GLOBALIZATION

Growth in the size and integration ofcompanies has been accompanied byanother development: the globalization ofmedia conglomerates. More and more,major media players are targeting the globalmarketplace for the sale of their products.

There are three basic reasons for this strat-egy. First, domestic markets are saturated withmedia products so many media companies seeinternational markets as the key to futuregrowth. Media corporations want to be wellpositioned to tap these developing markets.

Second, media giants are often in a posi-tion to effectively compete with—and evendominate—the local media in other coun-tries. These corporations can draw on theirenormous capital resources to produceexpensive media products, such asHollywood blockbuster movies, that arebeyond the capability of local media. Mediagiants can also adapt already successfulproducts for new markets, again reaping therewards of expanding markets in these areas.

Third, by distributing existing mediaproducts to foreign markets, media compa-nies are able to tap a lucrative source ofrevenue at virtually no additional cost. Forexample, a movie shown in just one coun-try costs the same to make as a moviedistributed globally. Once the tens of millionsof dollars involved in producing a majormotion picture are spent, successful foreigndistribution of the resulting film can spell thedifference between profit and loss. Asa result, current decision making as towhether a script becomes a major film rou-tinely includes considerations of its poten-tial for success in foreign markets. Actionand adventure films translate well, forexample, because they have limited dia-logue, simple plots, and rely heavily on spe-cial effects and action sequences. Sexy stars,explosions, and violence travel easily toother cultures. Comedies, however, areoften risky because humor does not alwaystranslate well across cultural boundaries.

We can see examples of globalizationstrategies in the case of Viacom. . . . For

Dines02.qxd 7/26/02 2:33 PM Page 34

The New Media Giants ◆ 35

example, MTV is a popular Viacom cablechannel reaching over 70 million U.S. house-holds.12 It originated as a venue for recordcompanies to show music videos to advertisetheir artists’ latest releases. Over time, MTVhas added a stable of regular series (e.g., TheReal World, Road Rules, Beavis andButthead), specials (e.g., MTV’s House ofStyle), and events (e.g., MTV Video MusicAwards, MTV’s Spring Break), all aimed atthe lucrative teen and young adult market.

MTV describes itself in publicitymaterial as having an environment that is“unpredictable and irreverent, reflecting thecutting edge spirit of rock n’ roll that is theheart of its programming.” In reality, MTVis a well-developed commercial formulathat Viacom has exported globally, by mak-ing small adjustments to account for localtastes. In fact, MTV is really a global col-lection of MTV’s. Together, these MTV chan-nels are available in over 300 millionhouseholds in 82 territories that, Viacomsays, makes MTV the most widely distributednetwork in the world. Over three-quartersof households that receive MTV are outsideof the United States.

Viacom’s global ventures do not endwith MTV. Virtually every aspect of itsmedia business has a global component.Examples include the following specifics.

◆ Major motion pictures are routinelydistributed internationally and many,such as Paramount’s Forrest Gump andMission Impossible, earn more moneyfor Viacom internationally than they doin the United States.

◆ Famous Players Theatres Canada oper-ates more than 660 screens in more than100 locations. United CinemasInternational—a joint venture withUniversal—operates more than 90 the-aters in Asia, Europe, and South America.

◆ Paramount International Television dis-tributes more than 2,600 series andmovies internationally.

◆ Blockbuster Video operates 6,000 storesin 27 different countries.

◆ Publisher Simon & Schuster hasinternational operations in both theUnited Kingdom and Australia and sellsbooks in dozens of countries.

◆ Nickelodeon distributes its children’sprogramming in more than 100 coun-tries and, much like MTV, operates itsown cable channels across the globe.These include Nickelodeon LatinAmerica, Nickelodeon in the NordicRegion, Nickelodeon Turkey, Nick-elodeon U.K., Nickelodeon Australia,and the Nickelodeon Global Network.Nickelodeon even has theme parks inAustralia and other locations.

◆ Viacom’s production companies licenseand coproduce programs based on U.S.hits to be sold in international markets.These include Entertainment Tonight/China, a 50-minute Mandarin-languageseries produced in cooperation with theChinese government, and other nationalversions of the Entertainment Tonightseries that appear in the United Kingdom,Germany, and other countries.

International revenues are making up anincreasingly large percentage of the incomeof such companies as Viacom, Disney,Time Warner, and News Corp. As a result,all major media conglomerates are nowglobal players, representing a major shift inindustry structure.

CONCENTRATION OF OWNERSHIP

While individual media companies grow,integrate, and pursue global strategies,ownership in the media industry as a wholebecomes more concentrated in the hands ofthese new media giants. There is consider-able debate about the significance of thistrend but the trend itself has been clear. . . .

Ben Bagdikian is a researcher whosework on the ownership of media hasrevealed increased concentration. In thevarious editions of his The Media Mono-poly, Bagdikian has tracked the number offirms that control the majority of all media

Dines02.qxd 7/26/02 2:33 PM Page 35

36 ◆ A Cultural Studies Approach

products. This number has been decliningdramatically in the last 15 years. He notesthat in recent years, “a small number of thecountry’s largest industrial corporationshas acquired more public communicationspower—including ownership of the news—than any private businesses have everbefore possessed in world history.” 13 In thefifth edition of his book, he reports that in1996, just 10 media companies dominatedthe entire mass communication industry.With recent high-profile mergers, this figurecontinues to decline.

Within each sector of the industry, afew large companies dominate smallercompetitors.

◆ Two companies—Borders/Walden andBarnes & Noble—make a third of allU.S. retail book sales.14

◆ Five movie companies—Disney’s BuenaVista, News Corporation’s Fox, TimeWarner’s Warner Bros., Viacom’sParamount, and Sony—dominate thatindustry, accounting for more than 75%of the domestic box office in the summerof 1998.15

◆ Five companies—Seagram’s Universal,Sony, Time Warner, Bertelsmann, andEMI—distribute 95% of all music car-ried by record stores in the United States.

◆ Television continues to be dominated byfour major networks—Disney’s ABC,Viacom’s CBS, News Corporation’sFox, and General Electric’s NBC. Severalnew fledgling networks have entered thefield but are not yet major competitors—WB (Time Warner), UPN (Viacom),USA, and PAX. . . .

◆ InterpretingStructural Changes

The media industry, then, has been under-going significant changes in recent decadesas companies have grown, integrated, andbecome global players. There is little debate

about these basic trends. However, thesignificance of these trends is a subject ofintense debate. Market advocates see thesestructural changes as the normal evolutionof a growing and maturing industry. Butthe public sphere framework reminds usthat media cannot be treated simply asany other industry. Furthermore, it raisesserious questions about what thesestructural changes mean for diversity andindependence in content and for the powerof newly emerging media corporations.

THE MARKET PERSPECTIVE

From the perspective of the marketmodel, the media industry is one that hasenjoyed enormous growth in recent years.With that growth has come a repositioningof major players, the introduction of somesignificant new players, and an evolutionin the basic terrain of the industry. Thisperspective tends to see the growth of largermedia companies as the logical outcome ofan industry that has become more inte-grated across media and more global inscope. To operate effectively in such a newenvironment, media corporations mustdevelop new business strategies and drawon the larger capital resources availableonly to major global corporations. Thestructural changes of growth, integration,and globalization are merely the signs ofcompanies positioning themselves to oper-ate in this new media world. The concen-tration of media ownership, on the otherhand, is the natural by-product of a matur-ing industry, as young start-ups and older,underperforming firms are consolidatedinto the business plans of mature but inno-vative companies.

The rapid growth in media outlets, theconstant shifts in consumer tastes, and theever-changing terrain of the industry itselfmake any apparent domination of the indus-try by a few companies an illusion. No onecan control such a vast and constantly evolv-ing industry. Companies such as AmericaOnline (AOL), who have become majorplayers in the industry, did not exist a fewyears ago, while old media standards, such

Dines02.qxd 7/26/02 2:33 PM Page 36

The New Media Giants ◆ 37

as ABC, were long ago incorporated intonewly consolidated media companies.Change is built into the market and no com-pany can really dominate the marketplace.

Market advocates note that we should notbe nostalgic about the media era gone by. Inreality, as recently as the mid-1970s, themedia landscape was much more sparselypopulated than it is today and consumers hadfar fewer choices, on the whole. Comparedwith this earlier period, market advocatespoint out, we have a cornucopia of mediaoutlets and products available to us.

It is true that more communities hadcompeting daily newspapers than there aretoday, but often the quality of those smallerlocal papers was mediocre at best. In con-trast, today’s papers may be local monopo-lies and part of larger chains, but bydrawing on the resources of their owners,they are able to produce a higher-qualityproduct. Also, consumers have many moreoptions for news—especially cable televi-sion and the Internet—than they ever did inthe days of more competing daily papers,making local newspaper monopolies lesssignificant.

In the 1970s, many communities hadonly small local bookstores with very lim-ited inventory and choice. Today, more andmore communities have “superstore”booksellers with thousands of diverse selec-tions of books and magazines. Rather thankilling the old print medium, the Internethas been a shot in the arm for book sales asonline retailers such as Amazon.com offerhundreds of thousands of titles for sale atthe click of a mouse. This has made booksand other media products more widelyavailable than ever.

In the 1970s, local movie theaters werebeginning to feature more multiscreenofferings, but these were limited comparedto what is available today. Video rentalswere not readily available because VCRswere still primitive in those days. Today,more multiplex theaters bring moreoptions to moviegoers, while VCRs are in85% of homes and a wide array of videosis readily available for low-cost renting.

DVDs, too, have entered the medialandscape.

Radio was admittedly more diverse interms of regional preferences, but it is notclear whether a broader range of music wasreadily available to listeners. Today, radiohas become largely a chain-owned affairwith new standards of professionalism andhigh production values. In addition, onlinestreaming offers the potential of greatermusical variety to listeners.

Most striking, 90% of the prime-timetelevision audience in the mid-1970s waswatching just three television networks.Cable television was not really an alterna-tive because it was still largely used totransmit the “big three” broadcast networksto homes where reception was difficult.Satellite television, of course, was unheardof. Today, three new broadcast networkshave joined the older “big three.” Nearlythree-quarters of U.S. homes have cable,delivering an average of almost 60 chan-nels. Satellite television, with hundreds ofchannels, is expanding and by 2000, was inmore than 10% of homes.

Finally, the vast universe of the Internetis becoming available to more and morepeople at work and home, opening upunprecedented avenues for news, entertain-ment, and commerce via the printed wordor streaming audio-video.

In light of these rapid changes, as wehave seen, market advocates have called formore deregulation of the industry in orderto spur increased competition. Because ofdigitization, companies in fields that werepreviously separate can now compete witheach other if regulations are lifted. On thedelivery side, telephone companies, forexample, can now offer Internet access aswell, while cable companies can enter thetelephone and Internet business. On thecontent side, companies that had tradition-ally been focused in one medium can nowbranch out to work in films, television,print, Internet, and other media. All of this,market advocates contended, means morechoices and better media for the consumer;a regulatory system created in a far

Dines02.qxd 7/26/02 2:33 PM Page 37

38 ◆ A Cultural Studies Approach

different era is obsolete in this new dynamicmedia environment.

QUESTIONING THE MARKET:REVISITING THEPUBLIC SPHERE APPROACH

Although the market approach maycelebrate the new media environment, thereare questions that this focus on markets andprofits effectively obscures. The public sphereperspective suggests that the technologicalchange and growth in the number of mediaoutlets should not be accepted as anunequivocal benefit, especially if these out-lets are linked to a growing concentrationin media ownership.

The introduction of new media has neverensured quality content. History has shownthat the great potential of new media formshas often been subverted for purely commer-cial purposes. Both radio and television, atvarious points, were touted as having pro-found educational and civic potential. Thatpotential was never reached. Cable televisionhas, in many ways, simply reproduced theformats and formulas of broadcast television.Because it is not covered by the same contentrules that regulate broadcast television, cablehas had more leeway to air raunchy, violent,and sensationalistic entertainment. This typeof entertainment could be seen in everythingfrom adult-oriented cable movies to thefunny, but foul-mouthed, animated pre-pubescent offerings of South Park. Cable’svast wasteland was perhaps epitomized by itsmost highly rated programs in the late 1990s:professional wrestling. The popularity ofsuch cable programming pressured broadcasttelevision to seek increasingly wild andaggressive programs, leading many parents todespair about the lack of appropriate enter-tainment and educational television for theirchildren.

More wasted potential seems to haveplagued the growth of the Internet. Earlydiscussion of the “information superhigh-way” was quickly supplanted by a focuson e-commerce. Here, too, adult-oriented

sites proved to be very popular. While theremay be more media outlets, we need toexamine what these channels are delivering.

A concern for the health of the publicsphere leads us to argue that media outletsare only truly beneficial if they serve thepublic interest by delivering content that isgenuinely diverse and substantive. Early indi-cations were that, to the contrary, much ofcable television was delivering more of thesame commercial fare that characterizedbroadcast television. Why couldn’t some ofthese many channels be used to deliver inno-vative, diverse, and inclusive public affairsprogramming? Or alternative visions fromindependent filmmakers and other artists? Orprogramming that specifically spoke to thecommon challenges we face as a society?Instead, the fragmentary nature of the cabletelevision world might even be exacerbatingcultural divisions in the society, as segregatedprogramming targeted separate demographicgroups based on age, gender, class, and race.The Internet, too, has been used by majormedia companies primarily to sell productsto consumers and to promote other mediaventures, little of which added significantly toa vibrant public sphere.

Finally, the blurring of boundariesbetween media coupled with calls for deregu-lation raise the specter of fully integrated,multinational media giants that can simulta-neously dominate multiple media. Oldmonopoly criteria seem incapable of dealingwith this new market reality. Despite the factthat it was promoted as a means of increas-ing competition, the 1996 Telecommuni-cations Act has resulted in renewedconsolidation in the media industry. Despitethis continuing consolidation, market advo-cates continue to talk about the new “com-petition,” and policymakers seem unwillingto examine the significance of an emergingmedia monopoly by a few giant firms. . . .

On the content side, market theorypromised diversity from an unregulated mar-ket, but the reality seems to be quite different,as the same old media content is being sold innew packaging and underserved communi-ties continue to be marginalized. Little that is

Dines02.qxd 7/26/02 2:33 PM Page 38

The New Media Giants ◆ 39

fresh or independent seems to come from thenew media giants. This, coupled with thegrowth in the sheer size of these corporations,raises the disturbing specter of concentratedcorporate power capable of stifling diverseexpression and exerting significant politicalpower. . . .

◆ Notes

1. Details of the Viacom/CBS deal usedthroughout this chapter were obtained fromcompany press releases and media accounts,including the following: Paul Farhi, “Viacom toBuy CBS, Uniting Multimedia Heavyweights,“ Washington Post (September 8, 1999): A1;Sallie Hofmeister, “Viacom, CBS to Merge inRecord $37-Billion Deal,” Los Angeles Times(September 8, 1999), online at: www.latimes.com, accessed September 9, 1999; Brian Lowry;“What Effect? Only Prime Time Will Tell,” LosAngeles Times (September 8, 1999), online at:www.latimes.com, accessed September 9, 1999;Lawrie Mifflin, “Viacom Set to Acquire CBS inBiggest Media Merger Ever,” New York Times(September 8, 1999), online at: www.nytimes.com, accessed September 9, 1999; Lisa deMoraes, “Can Fledgling UPN Fly to NewViacom Nest?,” Washington Post (September 8,1999): C1; Judy Sarasohn, “Special Interests: ASilence That May Not Be Golden,” WashingtonPost (September 9, 1999): A19; John Schwartzand Paul Farhi, “Mel Karmazin’s SignalAchievement,” Washington Post (September 8,1999): E1.

2. Federal Communications Commission.“Comments Sought on November 1995 Expira-tion of Fin-Syn Rules,” New Report No. DC95-54, April 5, 1995, online at: www.fcc.gov,accessed October 12, 1999.

3. Noelle Knox, “Internet Mergers UpSharply,” Richmond Times Dispatch (July 17,1999): C1.

4. Maryann Jones Thompson, “Got aMillion Bucks? Get a Web Site,” The Industry

Standard, online at: www.thestandard.com/metrics/display/0,1283,899,00.html, accessedJune 16, 1999; www.thestandard.com/research/display/0,2799,9845,00.html, accessed August29, 2000.

5. See, for example, the latest list of popu-lar sites at: www.100hot.com. This particularservice tracks a sample of more than 100,000user to develop its listing. Other services, usingdifferent methodologies, will have slightly differ-ent results. See, for example, the “Top Rank-ings” list at: www.mediametrix.com/home.jsp?language=us, or the top sites listed by PC DataOnline at: www.pcdataonline.com/reports/tmSitesSingleFree.asp.

6. Kyle Pope, “Disney to Merge TelevisionStudio With ABC Network,” Wall StreetJournal (July 9, 1999): B4.

7. “A Flawed Communications Bill,”New York Times (June 20, 1995): A14.

8. Patricia Aufderheide, CommunicationsPolicy and the Public Interest (New York:Guilford Press, 1999), p. 89.

9. Bill Carter, “FCC Will Permit OwningStations in Big TV Markets,” New York Times(August 6, 1999): A1.

10. John Schwartz, “FCC Opens Up Big TVMarkets,” Washington Post (August 6, 1999):E3.

11. Federal Communications Commission,“FCC Approves Transfer of CBS to Viacom;Gives Combined Company Time to ComplyWith Ownership Rules” (May 3, 2000 pressrelease), online at: www.fcc.gov, accessed May8, 2000.

12. MTV descriptive information is fromthe Web sites of Viacom (www.viacom.com)and MTV (www.mtv.com), and from Viacom’s“1998 Annual Report.”

13. Ben Bagdikian, The Media Monopoly,5th ed. (Boston: Beacon, 1997), p. ix.

14. Ben Bagdikian, The Media Monopoly,5th ed. (Boston: Beacon, 1997), p. xxix.

15. “Summer Market Share,” Variety(September 14, 1998).

Dines02.qxd 7/26/02 2:33 PM Page 39

Related Documents