The New Growth Path: Provincial Implications Input to NCOP Select Committee February 15, 2011

The New Growth Path: Provincial Implications Input to NCOP Select Committee February 15, 2011.

Jan 02, 2016

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

The New Growth Path: Provincial Implications

Input to NCOP Select Committee

February 15, 2011

Overview

• The New Growth Path: A brief overview

• The spatial challenge

• Implications for provinces

• Implications for municipalities

SONA 11 February 2011

• “We have declared 2011 a year of job creation through meaningful economic transformation and inclusive growth.

• “We have introduced a New Growth Path that will guide our work in achieving these goals, working within the premise that the creation of decent work is at the centre of our economic policies.” …

• “All government departments will align their programmes with the job creation imperative. The provincial and local spheres have been requested to do the same.

• “The programmes of the State Owned Enterprises and development finance institutions should also be more strongly aligned to the job creation agenda.”

The jobs challenge

Labour absorption (Percentage of people aged 15-64 who are employed) (ILO)

South Africa 41,3%

Egypt 43,2%

India 55,6%

Argentina 56,5%

South Korea 58,1%

Malaysia 60,5%

Brazil 63,9%

China 71,0%

4Confidential

8

12

16

20

24

28

32

1980 1985 1990 1995 2000 2005

Mil

lio

ns

Working age population growth (1980-2009) =

Labour Force growth (1980-2009) = 1.9%

gap = unemployed + not participating

New global context• The rise of new economic

powers– China, India, Brazil– Scramble for Africa’s

resources• Economic fragility

– Imbalances and systemic weakness remain

– Slow recovery in global North– Policy space

• Climate change – and new massive green industrialisation wave

• Technological innovation – jobs for the future

5Confidential

0

10

20

30

40

50

60

70

80

1980

1983

1986

1989

1992

1995

1998

2001

2004

2007

2010

2013

% o

f glo

bal G

DP China

India

South Africa

Brazil

Japan

United States

Western Europe

world GDP and national shares calculated using PPP dollars (IMF WEO)

estimatedactual

China – an example

What we sell: Top 10 Exports1.Iron ore2.Ferro-Alloys3.Chromium ores4.Manganese ores5.Platinum

6.Flat-rolled steel

7.Wool (raw)

8.Copper waste and scrap

9.Zirconium and vanadium ores

10.Nickel plates, sheets and foil

What we buy: Top 10 Imports1.Cell-phones and phones2.Computers3.Printing machines4.Plastic and rubber boots5.Televisions and monitors6.Kettles, microwave ovens and toasters7.Dresses and women’s jackets8.Suitcases and bags9.Sports shoes10.Computer and cash register parts and accessories

6Confidential

Rail lines in Africa

The New Growth Path

• Addresses– Deep-seated structural

problems that lead to high joblessness and inequality

– Specifically have to turn around major job losses in recent crisis

– Take advantage of opportunities in regional economy and changing global conditions

• The process– Builds on mandate to prioritise

employment creation

– Approved by Cabinet in October 2010

– Cabinet lekgotla identified priorities for 2011/12, reflected in SoNA

• Requires alignment by all spheres and agencies of the state, with regular reporting on what they are doing to support employment creation and growth

Employment intensity and growth

• To achieve jobs target requires growth AND greater employment intensity of growth (employment increase relative to GDP growth)

• Employment intensity of 0,2% would require a growth rate of over 15%; employment intensity of 0,8 would require a growth rate of 4%

• Debates about historic intensity of growth: 0.8 from 1996 (Census data) to the second quarter of 2010 (QLFS data); 0.5 from 2001 (LFS data) to the second quarter of 2010 (QLFS data); and .67 from 2002 (LFS data) to the second quarter of 2009 (QLFS data).

5 million new jobs by 2020

Identify key jobs drivers where employment is

possible

Identify what is needed to achieve

the jobs and investment

New opportunities in changing

regional & global environment

Private sector: how to align outcomes

with jobs goals

Key steps by the state: directly and

in facilitating broader growth

The approach:

10

Look for employment opportunities in “jobs drivers” and implement policies

to take advantage of them

InfrastructureEnergy, transport, communications,

water,housing.

Spatial opportunities:

Rural development

African regional development

Main economic sectors:

Agriculture & agroprocessing

Mining and beneficiationManufacturing (IPAP2)Tourism/other services

Social capital:The social economy

The public sector

New economies:Green economy

Knowledge economy

Jobs drivers

11

Policy drivers

• Macro-economic strategy: counter-cyclical/support a competitive rand– More relaxed

monetary policy

– Address inflationary pressures through fiscal policy and targeted micro-economic strategies

1. Address cost drivers and inflationary pressures across the economy

2. Active industrial policy based on increasing competitiveness and targeting sectors that can create employment directly and indirectly

3. Comprehensive rural development

4. Stronger competition policy

5. Stepping up education and skills development

6. Enterprise development

7. Reform of Broad-Based BEE

8. Reform labour policies to support productivity and improve protection for vulnerable workers

9. Technology policies geared to improving innovation in ways that support employment creation and small- and micro-enterprise

10.Developmental trade policies with a strong orientation to new growth centres

11. Investment to support African development

Training at centre of new growth path

Key skills targets Engineers: 30 000Artisans: 50 000 by

2014/15 Broad-based workplace training:

10% of workforce or 1,2m workers on

training

Increase FET college intake to

1 million students

Computer skills at all schools, training for all

public servants

Sufficient resources for

training

Easier recruitment of foreign skills

coupled with skills transfer plans

SOEs to target artisans.Review of

SETA performance.

Confidential 13

Policy driver: Development

policy package

Looser monetary policy stance to support a more competitive (and stable)

exchange rate and reduce cost of investment Additional measures

to depreciate and then stabilise the rand, as required

Measures to address inflation

focussing on volatile prices

More restrained fiscal policy reflected in

around 2% real growth in expenditure

Address main cost drivers to

enhance competitiveness

Support higher savings including

through retirement-fund reform and

reduce the cost of industrial finance

Pact with organised labour and business on wages and

prices, protect the social wage and support job creation

Eliminate waste and

ensure rigorous reprioritisation

of budgets

Confidential 14

Resource driversResource drivers:• state budgets (national,

provincial and local)• the resources of SOEs

and DFIs• Universities and science

council resources• retirement funds• the domestic private

sector • international investment• donor funding• community-owned

financial institutions such as stokvels and co-ops.

15

• SoNA:– R9 billion in the Jobs Fund

over the next 3 years – public employment schemes plus subsidies to private employers

– R10 bn from the IDC in next 5 years for job-creating projects

– R20 billion in investment subsidies

– Comprehensive support for SMEs

Institutional driversThe developmental state• Agile, responsive,

learning• Profound shift in

culture – from compliance/process to delivery/outcomes

• Alignment around growth path – review budgets, programmes and procurement policies

1. The DFIs (IDC, DBSA, Land Bank, Khula, SAMAF, NEF)

2. The GEPF and the PIC, as crucial investment drivers

3. The SARB, within its Constitutional mandate

4. The infrastructure SOEs (Transnet and Eskom)

5. ITAC and Customs & Excise

6. The Competition Commission/Tribunal and other regulatory, standard-setting and accreditation bodies

7. The science councils, universities and Mintek

16

SOCIAL DIALOGUE• Time-consuming – but crucial• Deepen dialogue at sector and workplace• Strengthen institutions from constituencies to NEDLAC• Mobilise South Africans behind a vision

Institutional drivers outside the state

BUSINESS• Business and markets vital –

jobs, investment, entrepreneurship, technology

• Large companies linked to national-base

• Developmental state not simply hostage to market forces and vested interests: through careful alliances, clear purpose and leveraging its resource and regulatory capacity, can align market outcomes more clearly with development needs

LABOUR• Resources include skills commitments,

productivity-agreements, retirement funds, union investment vehicles, wage agreements, public service delivery

• Without a common vision and strategic unity, not possible to make real progress and the society will simply exhaust itself on policy polarisation, while the extent of the developmental crisis grows

17

In other words…

…a comprehensive response to the structural crises of poverty,

unemployment and inequality…

…based on solidarity across society

A dual challenge around geography• Apartheid space

was designed to enforce marginalisation and disempowerment– The Bantustans

as labour reserves

– Townships far from jobs, adding to the cost and difficulty of employment

– New administrations at municipal and provincial level

– Limited coherence on economic policy with national sphere

– Institutions and systems in some areas weak and under-funded

– Particularly in former Bantustans where revenues are low and it’s hard to attract skills

19

20

Bantustans

Provinces

Settlement patterns

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

Northern Cape

Free State

North W

est

Limpopo

Mpum

alanga

Eastern Cape

Western Cape

KwaZulu-N

atal

Gauteng

Mill

ions

of

rand

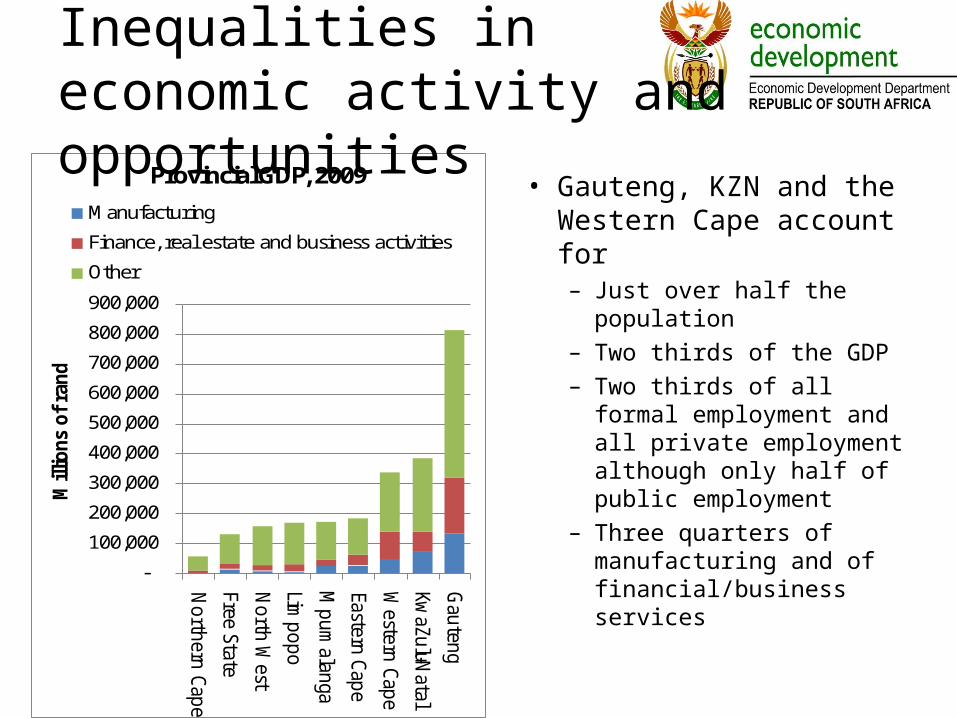

Provincial GDP, 2009

Manufacturing

Finance, real estate and business activities

Other

Inequalities in economic activity and opportunities

• Gauteng, KZN and the Western Cape account for – Just over half the

population– Two thirds of the GDP– Two thirds of all formal

employment and all private employment although only half of public employment

– Three quarters of manufacturing and of financial/business services

The employment challenge

• The labour absorption rate – the share of the population with employment – is around 64% internationally, but only 41% in South Africa

• Much lower in former Bantustan regions than in the metros and secondary cities

• Reflected in provincial disparities, with the lowest labour absorption rates in Limpopo and the Eastern Cape

0%

10%

20%

30%

40%

50%

60%

Limpopo

Eastern Cape

North W

est

KwaZulu-N

atal

Northern Cape

Mpum

alanga

Free State

Gauteng

Western Cape

Employment ratio, 2010

Municipal differences

• Differences in economic opportunity translate into huge differences in incomes

• Incomes in the former Bantustans are around a tenth as high as in the metros and secondary cities

• Income inequalities mean that average incomes are much higher than medians in all cases -

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

Major urban centre Rural and small town former RSA

Mostly former Bantustan

average median (roughly)

The result: Huge differences in municipal revenue and capacity

-

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

100.0

Mostly in former Bantustans (R400 pc; 70% subsidies)

Rural and smaller towns in former

RSA (R2100 pc; 20% subsidy)

Major urban centres (R4300 pc;

20% subsidy)

Billion

s of ra

nd

Subsidies

Own income

Municipal revenue by source, 2009

0

5

10

15

20

25

30

Major urban areas (R1290 pc)

Rural and small town former RSA

(R710 pc)

Mostly in former Bantustans (R230

pc)

Billion

s of ra

nd

OtherDonationsOwn incomeLoansGrants

Funding of capex by source, 2009

The New Growth Path response• The economic strategy:

– Develop a realistic spatial perspective – what can we do to improve conditions in every region?

– Ensure support from SOEs and DFIs

– Drive rural development to create livelihoods in impoverished regions

– Make economic centres (metros and secondary cities) more efficient

• Governance:– Support improved

communication and alignment between spheres on economic strategies

– Tailor implementation of NGP to realities of different regions

– Clear and practical annual priorities

– Improve understanding of the employment impact of projects, programmes and regulations, with regular reports

25

In the coming year...• Improve alignment between settlement patterns and

economic activity in the long run• Better planning to secure outcomes (eg power station

with human settlements, water, industry)• Improve connections between economic policy

departments in provinces, municipalities and national government, based in – Strengthening the Economic Development MinMEC– Clear prioritisation amongst economic programmes and

projects

• Address regulatory inefficiencies in economic centres (metros and secondary cities)

26

Provinces – initial areasof joint action• Align provincial and national economic plans• Integrated green economy plan developed by IDC for

all provinces• Provincial impact of infrastructure• Small business agencies: coordinated, one-stop shop• Agro-processing: connect the opportunities in a

systematic way• Procurement: review of regulations that will provide

provinces with new opportunities• Jobs goals to be developed by each province.

27

The contribution of SOEs and DFIs

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

North W

est

Limpopo

Mpum

alanga

E Cape

Gauteng

Free State

N Cape

W Cape

KZN

Transnet - employment from mega projects, including suppliers

Rail Ports Pipelines

0%

5%

10%

15%

20%

25%

30%

35%

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

Free State

Mpum

alanga

North W

est

Western Cape

Limpopo

Eastern Cape

Northern Cape

KwaZulu-N

atal

Gauteng

Share of GD

P

Valu

e in

Rm

ns a

nd n

umbe

r of j

obs

IDC disbursements, 2006 to 2010

Value (millions of rand)

Estimated employment impact

Province's contribution to national GDP (2009)

Eskom

• Major plants located near coal reserves, with localised employment effects– Should create 2000 new jobs in the coming year

• Main employment impact from maintaining electricity supply across the country

• Also create jobs in all provinces through– Procurement from build programme– Electrification programme– Municipal electricity maintenance

Working with the DFIs and SOEs• NGP should drive a spatial vision that

increasingly shapes projects from DFIs and SOEs

• EDD is working with the IDC, Khula and SAMAF to align with requirements of employment creation and equity in spatial terms

• Improve communication flows between spheres to maximise impact

Conclusion

• 2011 is a year of job creation• Coordination of policy, regulation, planning and implementation

across government is critical• Involve communities• The public sector contributes directly and by creating conditions for

new private activities that can generate new opportunities on a mass scale

• Social partners - business, labour and civil society - have a crucial role to play

32

Related Documents