The New Economy: USA and FRG Phillip J. Bryson Duisburg, Summer, 2001

The New Economy: USA and FRG Phillip J. Bryson Duisburg, Summer, 2001.

Dec 20, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

The New Economy: USA and FRG

Phillip J. Bryson

Duisburg,

Summer, 2001

US German Roles in a New Era

Is the United States leading the world into a new economic era?

Is there a ”New Economy.” The information-age service economy seems to be based upon new rules.

Is that New Economy developing in Germany? With the international spread of technologies, they should tend toward a common level.

Two Main Propositions

the economy has changed in terms of its fundamental structure and, of less significance

changes have produced a boom • The boom has recently been approaching

either a new phase or an end. So, have fundamental changes

permanently altered the nature of and prospects for growth and change?

I. Current Productivity and Economic Performance

Did the U.S. boom of the 1990s, together with its effects and causes, warrant the designation ”New Economy”?

In Germany, a period of fiscal trial following reunification is now giving way to economic reinvigoration. Europeans are encouraged by economic integration and the arrival of the Euro.

I. Current Productivity and Economic Performance

The American Decade Stagnation in the early 90s. Apparent

triumph of the Asian Statist Model. Porter (1990) wrote that a government’s

role in generating international competitiveness was a vital ”if not the most important, influence” in national economic performance. The policies of the Japanese and Korean governments were ”associated with the success these nations’ firms have enjoyed”

The Boom that Followed The boom of the 1990s was fundamentally

different from preceding ones. The long expansions of the 1960s and 1980s had been flawed by • inflationary tendencies when employment levels

were high, or • had high levels of both inflation and

unemployment.• 1980s boom had huge federal budget deficits

(expan- sionary fiscal policy) • tight monetary policy response to the inflationary

seventies.

The Boom of the Nineties fiscal policy restrictive, monetary

policy accommodative. The longest period of economic

expansion in U.S. history, • declining unemployment • wage and price stability, • rising productivity, and • strong economic growth. • Productivity growth in the U.S., reports

Krugman has accelerated, perhaps from 1 percent per annum to 2 percent or more.”

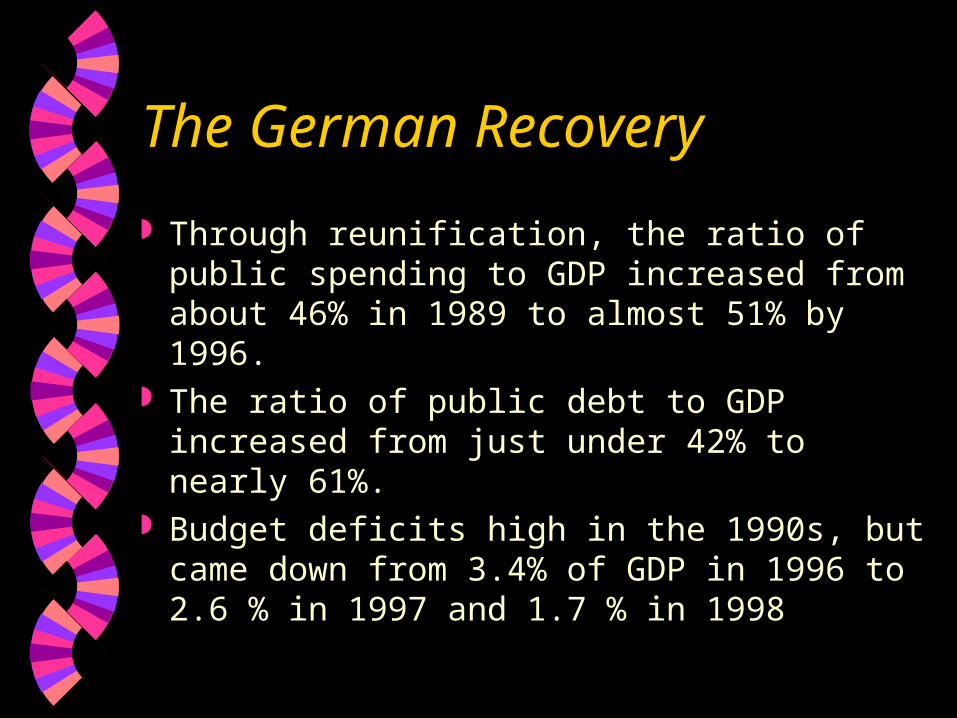

The German Recovery

Through reunification, the ratio of public spending to GDP increased from about 46% in 1989 to almost 51% by 1996.

The ratio of public debt to GDP increased from just under 42% to nearly 61%.

Budget deficits high in the 1990s, but came down from 3.4% of GDP in 1996 to 2.6 % in 1997 and 1.7 % in 1998

The German Recovery

High interest rates offset high reunification outlays for reconstruction.

The structural unemployment problem was worsened by the tight- money situation. West German unemployment has exceeded eleven per cent; in the east, the real rate has been close to 20 % recently

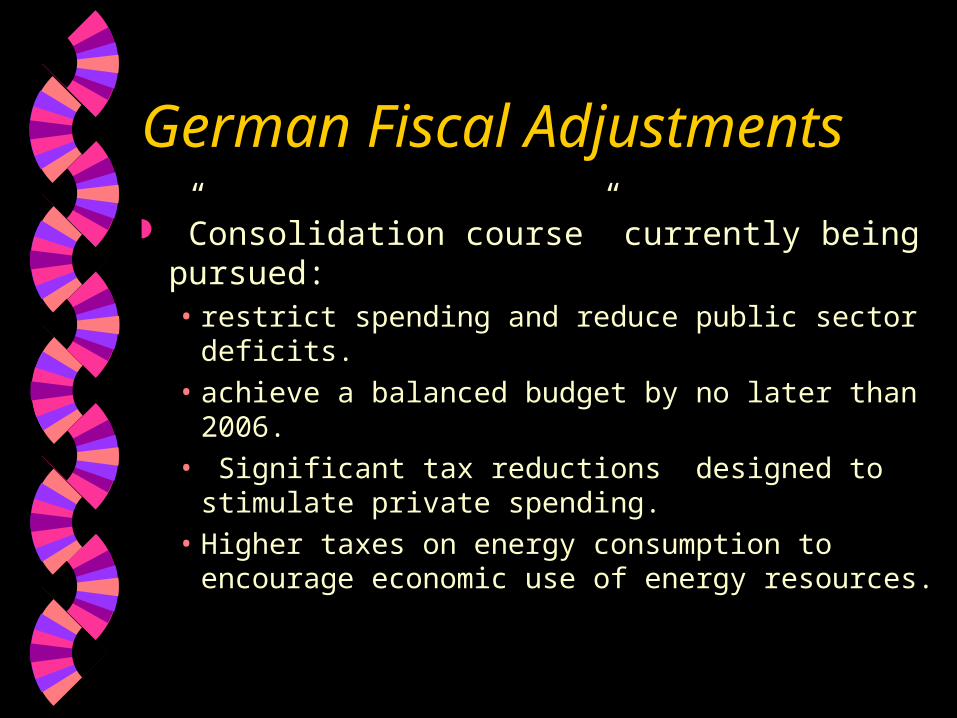

German Fiscal Adjustments

”Consolidation course” currently being pursued:• restrict spending and reduce public sector

deficits. • achieve a balanced budget by no later than

2006.• Significant tax reductions designed to

stimulate private spending. • Higher taxes on energy consumption to

encourage economic use of energy resources.

BRD Corporate Governance Change?

German corporate governance, traditionally based on finance through the banking system, may be changing . The development of the German stock market, the Dax, as a means inter alia of generating venture capital for high tech and information industries, began to support the development of a nascent, New Economy.

Foundations of Economic Reorganization: Strategic Investments in the U.S Excess capacity generation into the 1970s,

Stock prices depressed with underutilization of the capital stock, was underutilized;

little demand for products of obsolete technologies.

Nevertheless, managers refused to downsize, continued to invest. The result was

Share prices remained low and unproductive assets accumulated.

Growing Need for Restructuring

In the 1960s, large conglomerates formed. Separate and disparate businesses under

single management, but information dispersed in separate corporate divisions.

Competitive managerial outsiders noted low ratio of share prices to corporate assets in excessively large and unmanageable firms

With prices low and assets large, they could leverage takeovers, produce greater profits and higher share prices.

1980s Mergers and Acquisitions This was not merely an expression of corporate

greed, but a preparatory period of industrial restructuring.

Many inefficiently managed firms forced to exit the industrial scene. The effect?• The value of public equity more than doubled

(from $1.4 to $3 trillion in a decade), • a decline in productivity was reversed, • real income was increased over the period by

about a third, • record levels established for R&D

1980s Investments and 1990s Boom

In 1970, total private gross fixed investment below 15% of GDP.

It increased to 16.4% in 1974, to 18.8% in 1979, then stayed around 17 or 18% until the mid-1980s.

By 1989 it was back down to 15.3 and by 1994 to 14.6% of GDP. So these expenditures were substantial from about the mid-1970s into the 1990s.

U.S. Private Investment in IT, 1960-99• Year PFI* IPE* IPE/PFI IE* IE/PFI

• (Private (Information (IPE as (Industrial (IE as % Fixed Processing % PFI)

Equipment) of PFI)

• Investment) Equipment

– and Software

• 1960 75.7 4.9 6.47 9.3 12.3

• 1970 150.4 16.7 11.10 20.2 13.4

• 1975 236.5 28.2 11.92 31.1 13.2

• 1980 484.2 69.6 14.37 60.4 12.5

• 1982 531.0 88.9 16.74 62.3 11.7

• 1984 670.1 121.7 18.16 67.6 10.1

• 1986 740.7 137.6 18.58 74.8 10.1

• 1988 802.7 155.9 19.42 83.5 10.4

• 1990 847.2 176.1 20.79 91.5 10.8

• 1994 1034.6 233.7 22.59 113.3 11.0

• 1998 1460.0 356.9 24.45 150.2 10.3

• 1999 1577.4 407.2 25.81 151.4 9.6

• Source: Table B-16, Economic Report of the President, 2000, p. 326 and own calculations.

German Restructuring in the EU

Economic integration, developing since the ECSC established in 1950 and still evolving, creates and diverts international trade

Expanding trade promotes structural adjustments in industry, cost savings and greater competitiveness as producers incur economies of scale and scope.

Advocates of integration believe dynamic effects great.

Germany and the New Economy

If there is something really new in the New Economy it will prove susceptible to transplantation.

Characteristics of the U.S. economy of the 1990s will be subject to replication in technical fields and in relevant industries in Europe and Asia at an early date.

The New Economy in the US Development of the internet economy the most

important feature of the 1990s boom. The service sector provides the largest number

of jobs and generates nearly two-thirds of GDP in the United States.

Knowledge-based industries, e.g., finance, insurance, business, legal and other professional services have led the growth of the services sector.

High tech industries have been the leading growth sector recently.

Capital Market and IT. In the first half of 1999, the venture

capital industry raised $25 billion at an annual rate.• Over $16 billion, went to the IT sector, • $12 billion went into Internet companies. In

terms of market capitalization. • the IT hardware sector now accounts for

about 14 percent of the US total. (A decade ago only six percent.)

• Software component c. 9 percent was only two percent in 1989. Of total value of U.S. stocks, internet sector stocks represent about 4 percent.

Computers and Technical Change

Diffusion of computer-based technologies due to rapid decline in computer prices.

Jorgenson and Stiroh: this resulted not in economy-wide technical change (creating greater output from the same inputs), but in massive substitution of computers for labor and other inputs in home and business sector use.

Computers and Technical Change Since 1990, computers responsible for c. one

sixth of annual 2.4 percent output growth. Computers represent c. 20 percent of the

capital inputs contribution to growth, They represent 14 percent of the services

contribution of consumer durables. Computer-related gains are fundamentally

changing the economy• not by producing general growth spillover effects• but returns to IT investments are captured by

computer users themselves as they substitute equipment for other inputs.

Trade´s Role in the 1990s Boom The US economy increasingly open

• The ratio of exported and imported goods and services to the GDP, the US reached 29.3% in 1998 (Japan’s at 18.1%). Heilemann et al (p. 38) indicate the openness ratio of the Euro-Zone, calculated exclusive of intra-EU trade, would not be much higher.

• U.S. trade with the developing countries (40% of the total) significantly larger than Germany’s (16%);

• American trade with transition countries only about one percent, Germany’s about 10 percent.

Trade´s Role in the 1990s Boom

U.S. exports in recent years a prime driver of economic growth, but exports have not increased as rapidly as imports.

Huge, long-standing balance of trade deficits due to • Dollar appreciation on foreign

currency markets,• modest prices of petroleum imports

before 1999 OPEC rejuvenation, and • more than robust consumer demand.

Stock Prices, „Wealth Effect“ and Savings

The ”wealth effect” comes from increasing share prices. It encourages consumption by providing an alternative form of wealth accumulation. Why would one need normal savings when the value of one‘s stock holdings increases continually. Thus, private savings in the U.S. even became negative towards the end of the boom.

Stock Prices, „Wealth Effect“ and Savings

•Wie gerechnet wird, PI – C = S. (Wenn PI<C, S< 0.) Aber diese Rechnung achtet nicht auf capital gains (Kapital Gewinne). PI + CG - C = S, oder

• PI + CG < C, S < 0.•Mit Verlust dieser Kapital Gewinne, S < 0, so

daß wir erwarten müßen, daß AD sich verkleinert und daß das Wachstum sich mindert. Wir kommen dadurch zu einer Rezession.

• Bginning in 1990, U.S. households’ real net worth increased by c. $15 trillion, or by more than 50 percent. Of total wealth creation in the 1990s, more than 60 percent came from rising stock values

Are Business Cycles History? Zarnowitz (1999) evaluates whether

certain factors promoting productivity growth also promote greater economic stability.• Downsizing and rationalization stabilize the

economy. But through cost-cutting and more effective production, effective downsizing leads to growth and, ultimately, to subsequent opportunities for ”upsizing.” Inflationary pressure may also return with recovery, with upward wage adjustments and associated inflationary pressure following.

Do factors promoting growth also promote stability?

Breakthroughs in information technologies are thought to stabilize the economy. They induce increased investments and increase business profits.

But these productivity-enhancing effects have yet to be documented quantitatively, any specific link between information technologies and the stability of economic growth remains unclear.

Do factors promoting growth also promote stability?

Improved inventory control, especially through just-in-time management techniques, helps to stabilize the economy.

But Zarnowitz finds that constant dollar inventory investments in the 1990s remained about as ”volatile and as cyclical” as in the past.

Do factors promoting growth also promote stability?

The growth of the service economy adds stability, since the more volatile manufacturing and construction sectors have declined in significance.

This is probably true, but with growing international competition in services, they are also becoming more cyclical.

Do factors promoting growth also promote stability?

Deregulation of financial and other industries is believed to have added stability. More competition in airlines, trucking, banking, etc., has enhanced productivity growth

But it is unlikely that further deregulation will promote further stability.

Do factors promoting growth also promote stability?

Discretionary macro policies could also be the source of greater cyclical stability. Macro-economic control through interest-rate adjustments has been quite effective in recent years as compared to the earlier effort to manage money growth.

But policy agents cannot always anticipate and avert business recessions or financial crises, and policies can still be ”wrong, mistimed, or bungled”

Do factors promoting growth also promote stability? Finally, globalization has reduced

instability• Importing many resources and products

reduces domestic inflationary pressure. Foreign markets reduce dependence on domestic demand for prosperity.

• Globalized capital markets are broader and more liquid, reducing the risk of bubbles and crashes.

At the same time, added stock market volatility and the economy’s vulnerability to financial and currency market instability is greater (Asian crisis).

Weaknesses,Potential Problems

Savings Rates low due to wealth effect High consumption, high imports and

high levels of personal indebtedness. When will expectations change.

Increasing energy prices spill over and drive up the prices of numerous other products

Increasing tightness in labor markets prompted interest rate increases by the Fed after mid-1999

Again, what is a “new economy” The use of the expression ”New

Economy,” when limited to a few, glamorous high-tech sectors, is misleading.

We have in fact only one economy. If the new sectors of the economy do not interact with and change economic processes in the old sectors, creating a whole new economic structure, we should not talk of a New Economy.

What is its future? Even if the New Economy is not recession

proof, it will not disappear in a slowdown. The internet economy and its companion, the relentless process of globalization, are here to stay. They will be the basis of recovery, of expansion, and of future well-being.

The benefits of the service and internet economy will continue to spread, affecting partners and competitors of the US globally.

What is its future? New technologies and the ratio of IT and

high- tech products to the BIP is lower in the EU than in the US, and the contribution of these new sectors to EU national growth is also smaller.

But internal European market growth, with continuing liberalization and deregulation, will increase competitiveness and dynamism. • Note the European Commission’s initiative

”eEurope 2002" to use the internet as a more integral part of education and ecommerce.

A parallel development is the Euro

Related Documents