THE NEED FOR BUSINESS MANAGEMENT SYSTEMS THE BIG 5 NATIONAL GRANTS MANAGEMENT ASSOCIATION (NGMA) Luncheon Series – Washington, D.C. March 21, 2012 Richard Solloway Solloway & Associates 301-320-5611 [email protected] sollowayassociates.com

THE NEED FOR BUSINESS MANAGEMENT SYSTEMS THE BIG 5 NATIONAL GRANTS MANAGEMENT ASSOCIATION (NGMA) Luncheon Series – Washington, D.C. March 21, 2012 Richard.

Dec 27, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

THE NEED FOR

BUSINESS MANAGEMENT SYSTEMS

THE BIG 5NATIONAL GRANTS MANAGEMENT ASSOCIATION (NGMA)

Luncheon Series – Washington, D.C. March 21, 2012

Richard Solloway Solloway & Associates

301-320-5611 [email protected]

sollowayassociates.com

Solloway&Associates(c) March 21, 2012 2

Solloway&Associates(c) March 21, 2012 3

THE BIG 5 – OPERATING SYSTEMS

• FINANCIAL • TRAVEL • PROPERTY MANAGEMENT• PERSONNEL• PROCUREMENT

Solloway&Associates(c) March 21, 2012 4

KEY CHARACTERISTICS

ESTABLISHED WRITTEN POLICIES

ADHERE TO FEDERAL STANDARDS

POLICIES CONSISTENTLY APPLIED

REASONABLENESS OF POLICIES

Solloway&Associates(c) March 21, 2012 5

FEDERAL REFERENCES NONPROFITS

2 CFR PART 230 – COST PRINCIPLES 2 CFR PART 215 – ADMINISTRATIVE REQUIREMENTS

UNIVERSITIES 2 CFR PART 220 – COST PRINCIPLES 2 CFR PART 215 – ADMINISTRATIVE REQUIREMENTS

STATE, LOCAL & INDIAN TRIBAL GOV’TS 2 CFR PART 225 – COST PRINCIPLES OMB CIRCULAR A-102 and COMMON RULE –

ADMINISTRATIVE REQUIREMENTS

Solloway&Associates(c) March 21, 2012 6

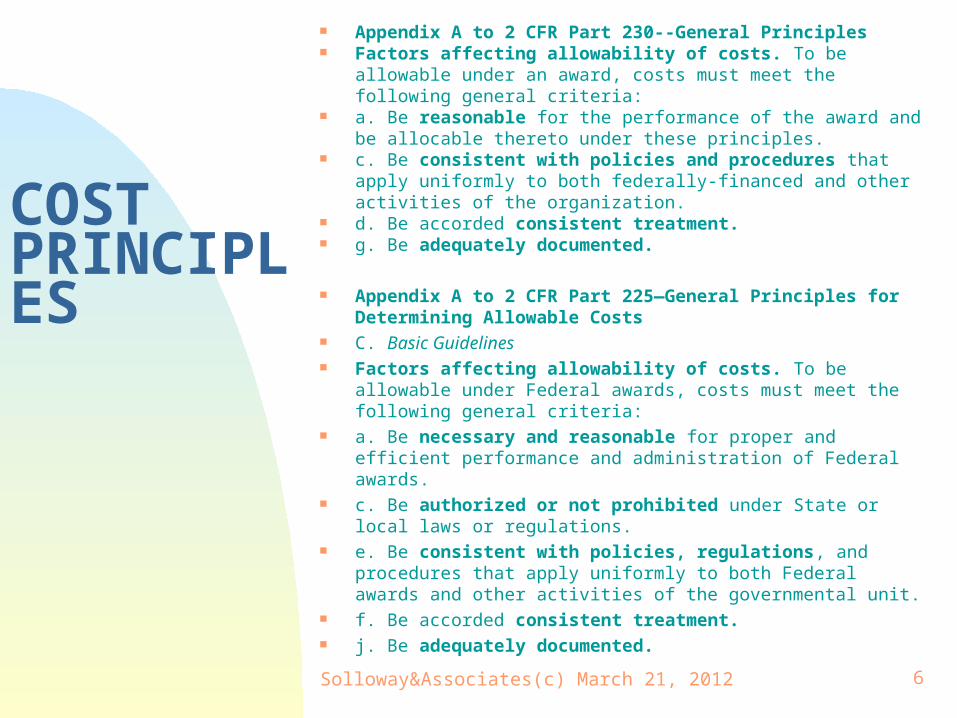

COSTPRINCIPLES

Appendix A to 2 CFR Part 230--General Principles Factors affecting allowability of costs. To be allowable under an

award, costs must meet the following general criteria: a. Be reasonable for the performance of the award and be allocable

thereto under these principles. c. Be consistent with policies and procedures that apply

uniformly to both federally-financed and other activities of the organization.

d. Be accorded consistent treatment. g. Be adequately documented.

Appendix A to 2 CFR Part 225—General Principles for Determining Allowable Costs

C. Basic Guidelines Factors affecting allowability of costs. To be allowable under

Federal awards, costs must meet the following general criteria: a. Be necessary and reasonable for proper and efficient

performance and administration of Federal awards. c. Be authorized or not prohibited under State or local laws or

regulations. e. Be consistent with policies, regulations, and procedures that

apply uniformly to both Federal awards and other activities of the governmental unit.

f. Be accorded consistent treatment. j. Be adequately documented.

Solloway&Associates(c) March 21, 2012 7

FINANCIAL

Solloway&Associates(c) March 21, 2012 8

STANDARDS FOR FINANCIAL MANAGEMENT SYSTEMS

NONPROFITS and UNIVERSITIES 2 CFR Part 215.21

STATE, LOCAL & INDIAN TRIBAL GOV’TS OMB Circular A-102 and Common Rule §_.20

Solloway&Associates(c) March 21, 2012 9

KEY FINANCIAL STANDARDSNONPROFITS and UNIVERSITIES

2 CFR Part 215.21 (b) Recipients' financial management systems shall provide for the following.

(1) Accurate, current and complete disclosure of the financial results of each federally-sponsored project or program in accordance with the reporting requirements set forth in §215.52. If a Federal awarding agency requires reporting on an accrual basis from a recipient that maintains its records on other than an accrual basis, the recipient shall not be required to establish an accrual accounting system. These recipients may develop such accrual data for its reports on the basis of an analysis of the documentation on hand.

(2) Records that identify adequately the source and application of funds for federally-sponsored activities. These records shall contain information pertaining to Federal awards, authorizations, obligations, unobligated balances, assets, outlays, income and interest.

(3) Effective control over and accountability for all funds, property and other assets. Recipients shall adequately safeguard all such assets and assure they are used solely for authorized purposes.

Solloway&Associates(c) March 21, 2012 10

KEY FINANCIAL STANDARDSNONPROFITS and UNIVERSITIES

2 CFR Part 215.21 (4) Comparison of outlays with budget amounts for each award.

Whenever appropriate, financial information should be related to performance and unit cost data.

(5) Written procedures to minimize the time elapsing between the transfer of funds to the recipient from the U.S. Treasury and the issuance or redemption of checks, warrants or payments by other means for program purposes by the recipient. ….

(6) Written procedures for determining the reasonableness, allocability and allowability of costs in accordance with the provisions of the applicable Federal cost principles and the terms and conditions of the award.

(7) Accounting records including cost accounting records that are supported by source documentation.

Solloway&Associates(c) March 21, 2012 11

KEY FINANCIAL STANDARDSSTATE, LOCAL & INDIAN TRIBAL GOV’TS

OMB Circular A-102 and Common Rule §_.20

a) A State must expand and account for grant funds in accordance with State laws and procedures for expending and accounting for its own funds. Fiscal control and accounting procedures of the State, as well as its subgrantees and cost-type contractors, must:

(1) Permit preparation of reports required by this part and the statutes authorizing the grant,

(2) Permit the tracing of funds to a level of expenditures adequate to establish that such funds have not been used in violation of the restrictions and prohibitions of applicable statutes.

(b) The financial management systems of other grantees and subgrantees must meet the following standards:

(1) Financial reporting. Accurate, current, and complete disclosure of the financial results of financially assisted activities must be made in accordance with the financial reporting requirements of the grant or subgrant.

(2) Accounting records. Grantees and subgrantees must maintain records which adequately identify the source and application of funds provided for financially-assisted activities. These records must contain information pertaining to grant or subgrant awards and authorizations, obligations, unobligated balances, assets, liabilities, outlays or expenditures, and income.

Solloway&Associates(c) March 21, 2012 12

KEY FINANCIAL STANDARDSSTATE, LOCAL & INDIAN TRIBAL GOV’TS

OMB Circular A-102 and Common Rule §_.20 (3) Internal control. Effective control and accountability must be

maintained for all grant and subgrant cash, real and personal property, and other assets. Grantees and subgrantees must adequately safeguard all such property and must assure that it is used solely for authorized purposes.

(4) Budget control. Actual expenditures or outlays must be compared with budgeted amounts for each grant or subgrant. Financial information must be related to performance or productivity data, including the development of unit cost information whenever appropriate or specifically required in the grant or subgrant agreement. If unit cost data are required, estimates based on available documentation will be accepted whenever possible.

(5) Allowable cost. Applicable OMB cost principles, agency program regulations, and the terms of grant and subgrant agreements will be followed in determining the reasonableness, allowability, and allocability of costs.

Solloway&Associates(c) March 21, 2012 13

KEY FINANCIAL STANDARDSSTATE, LOCAL & INDIAN TRIBAL GOV’TS

OMB Circular A-102 and Common Rule §_.20

(6) Source documentation. Accounting records must be supported by such source documentation as cancelled checks, paid bills, payrolls, time and attendance records, contract and subgrant award documents, etc.

(7) Cash management. Procedures for minimizing the time elapsing between the transfer of funds from the U.S. Treasury and disbursement by grantees and subgrantees must be followed whenever advance payment procedures are used. Grantees must establish reasonable procedures to ensure the receipt of reports on subgrantees' cash balances and cash disbursements in sufficient time to enable them to prepare complete and accurate cash transactions reports to the awarding agency. When advances are made by letter-of-credit or electronic transfer of funds methods, the grantee must make drawdowns as close as possible to the time of making disbursements. Grantees must monitor cash drawdowns by their subgrantees to assure that they conform substantially to the same standards of timing and amount as apply to advances to the grantees.

Solloway&Associates(c) March 21, 2012 14

STATE, LOCAL & INDIAN TRIBAL GOV’TS OMB Circular A-102

2. Post-Award Policies. j. Conditional exemptions. (1). OMB authorizes conditional exemption from OMB administrative requirements and cost principles for certain Federal programs. … A Federal agency shall consult with OMB during its consideration of whether to grant such an exemption. (2). To promote efficiency in State and local program administration, …. where most of the State agency's resources come from non-Federal sources, Federal agencies may exempt these covered State-administered, non-entitlement grant programs from certain OMB grants management requirements. (3). When a Federal agency provides this flexibility, as a prerequisite to a State's exercising this option, a State must adopt its own written fiscal and administrative requirements for expending and accounting for all funds, which are consistent with the provisions of 2 CFR part 225 (OMB Circular A-87), …

Solloway&Associates(c) March 21, 2012 15

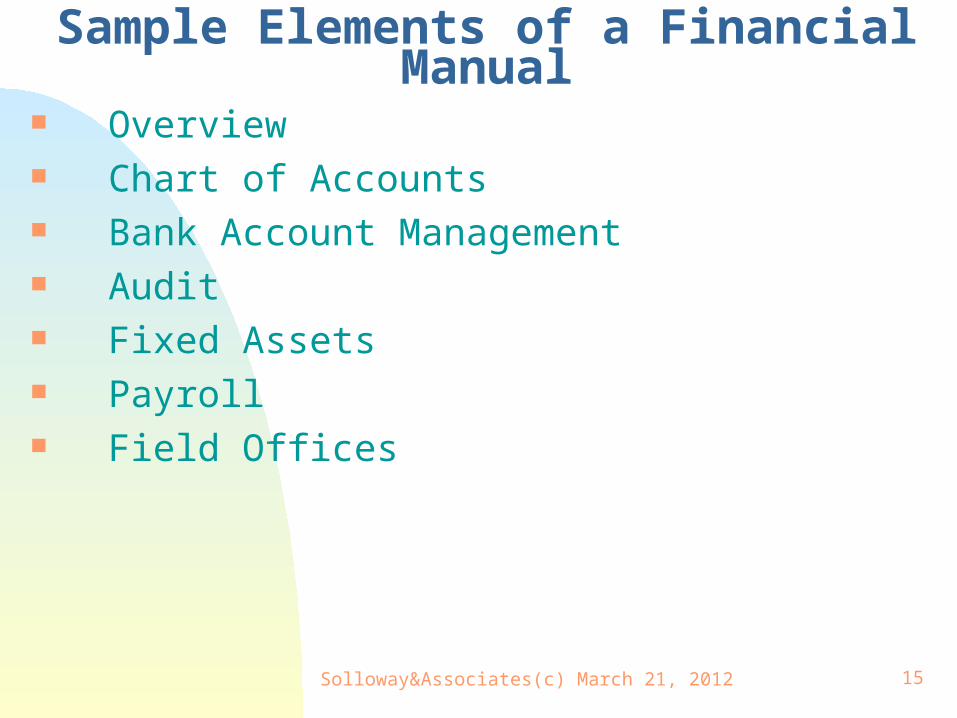

Sample Elements of a Financial Manual Overview Chart of Accounts Bank Account Management Audit Fixed Assets Payroll Field Offices

Solloway&Associates(c) March 21, 2012 16

TRAVEL

Solloway&Associates(c) March 21, 2012 17

TRAVEL REGULATIONS 2CFRPart220.53. Travel costs.

b. Lodging and subsistence. Costs incurred by employees and officers for travel, including costs of lodging, other subsistence, and incidental expenses, shall be considered reasonable and allowable only to the extent such costs do not exceed charges normally allowed by the institution in its regular operations as the result of the institution's written travel policy.

2CFRPart225.43. Travel costs. b. Lodging and subsistence. Costs incurred by employees and officers for travel,

including costs of lodging, other subsistence, and incidental expenses, shall be considered reasonable and allowable only to the extent such costs do not exceed charges normally allowed by the governmental unit in its regular operations as the result of the governmental unit's written travel policy.

e. Foreign travel. Direct charges for foreign travel costs are allowable only when the travel has received prior approval of the awarding agency.

2CFRPart230. 51. Travel costs. b. Lodging and subsistence. Costs incurred by employees and officers for travel,

including costs of lodging, other subsistence, and incidental expenses, shall be considered reasonable and allowable only to the extent such costs do not exceed charges normally allowed by the non-profit organization in its regular operations as the result of the non-profit organization's written travel policy.

e. Foreign travel. Direct charges for foreign travel costs are allowable only when the travel has received prior approval of the awarding agency.

Solloway&Associates(c) March 21, 2012 18

Sample Sections of a Travel Manual

General Policy Travel Procedures Travel Expense Policies Travel Advances Reporting Requirements

Solloway&Associates(c) March 21, 2012 19

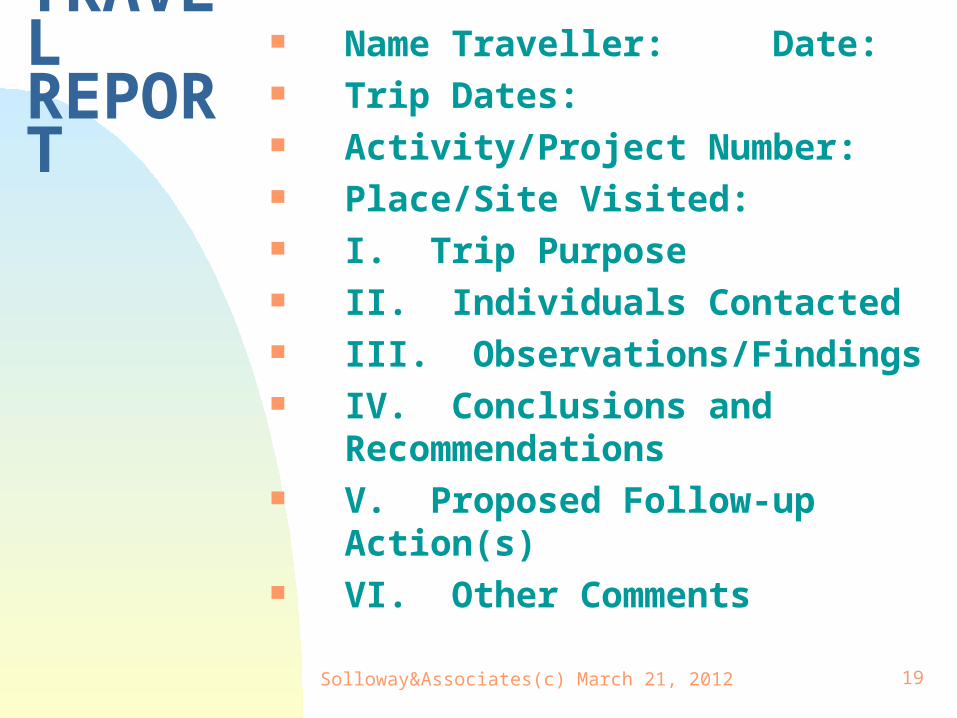

TRAVEL

REPORT

Name Traveller: Date: Trip Dates: Activity/Project Number: Place/Site Visited: I. Trip Purpose II. Individuals Contacted III. Observations/Findings IV. Conclusions and

Recommendations V. Proposed Follow-up Action(s) VI. Other Comments

Solloway&Associates(c) March 21, 2012 20

PROPERTY MANAGEMENT

Solloway&Associates(c) March 21, 2012 21

DEFINITIONS Equipment means tangible nonexpendable

personal property including exempt property charged directly to the award having a useful life of more than one year and an acquisition cost of $5,000 or more per unit. However, consistent with recipient policy, lower limits may be established.

2 CFR Part 215.2(l) Definitions Supplies means all personal property excluding

equipment, intangible property, and debt instruments as defined in this section, …

2 CFR Part 215.2(hh) Definitions

Solloway&Associates(c) March 21, 2012 22

KEY PROPERTY STANDARDSNONPROFITS and UNIVERSITIES

2 CFR Part 215.30 - .37 Purpose of property standards. Set forth uniform standards governing management and

disposition of property furnished by the Federal Government whose cost was charged to a Federal award. The recipient may use its own property management standards and procedures provided it observes the provisions of §215.31 through §215.37.§_.30

Insurance coverage. Recipients shall, at a minimum, provide the equivalent insurance coverage for real property and equipment acquired with Federal funds. §_.31

Real property. Each Federal awarding agency shall prescribe requirements for recipients concerning the use and disposition of real property acquired in whole or in part under awards. §_.32

Federally-owned and exempt property. Title to federally-owned property remains vested in the Federal Government. Recipients shall submit annually an inventory listing of federally-owned property in their custody to the Federal awarding agency §_.33(a)(1)

Solloway&Associates(c) March 21, 2012 23

KEY PROPERTY STANDARDSNONPROFITS and UNIVERSITIES

2 CFR Part 215.30 - .37 Equipment. Title to equipment acquired by a recipient with Federal funds

shall vest in the recipient, subject to conditions of this section. §_.34(a)

The recipient's property management standards for equipment acquired with Federal funds and federally-owned equipment shall include all of the following …..§_.34(f)

Equipment records shall be maintained accurately and shall include the following information. …..§_.34(f)(1)

Recipients shall, at a minimum, provide the equivalent insurance coverage for real property and equipment acquired with Federal funds. §_.34(f)(2)

A physical inventory of equipment shall be taken and the results reconciled with the equipment records at least once every two years. §_.34(f)(3)

Solloway&Associates(c) March 21, 2012 24

KEY PROPERTY STANDARDSNONPROFITS and UNIVERSITIES

2 CFR Part 215.30 - .37 A control system shall be in effect to insure adequate safeguards to

prevent loss, damage, or theft of the equipment. §_.34(f)(4)

Adequate maintenance procedures shall be implemented to keep the equipment in good condition. §_.34(f)(5)

Where the recipient is authorized or required to sell the equipment, proper sales procedures shall be established which provide for competition to the extent practicable and result in the highest possible return. §_.34(f)(6)

Supplies and other expendable property. Title to supplies and other expendable property shall vest in the recipient upon acquisition. §_.35(a)

Solloway&Associates(c) March 21, 2012 25

KEY PROPERTY STANDARDS STATE, LOCAL & INDIAN TRIBAL GOV’TS

OMB Circular A-102 and Common Rule §_.32

Equipment. Title. Subject to the obligations and conditions set forth in this section, title to equipment acquired under a grant or subgrant will vest upon acquisition in the grantee or subgrantee respectively. §_.32(a)

States. A State will use, manage, and dispose of equipment acquired under a grant by the State in accordance with State laws and procedures. §_.32(b)

d) Management requirements. Procedures for managing equipment, whether acquired in whole or in part with grant funds, until disposition takes place will, as a minimum, meet the following requirements: §_.32(d)

Property records must be maintained that: include a description of the property, a serial number or other identification number, the source of property, who holds title, the acquisition date, and cost of the property, percentage of Federal participation in the cost of the property, the location, use and condition of the property, and any ultimate disposition data including the date of disposal and sale price of the property. §_.32(d)(1)

Solloway&Associates(c) March 21, 2012 26

KEY PROPERTY STANDARDS STATE, LOCAL & INDIAN TRIBAL GOV’TS

OMB Circular A-102 and Common Rule §_.32

A physical inventory of the property must be taken and the results reconciled with the property records at least once every two years. §_.32(d)(2)

A control system must be developed to ensure adequate safeguards to prevent loss, damage, or theft of the property. Any loss, damage, or theft shall be investigated. _.32(d)(3)

Adequate maintenance procedures must be developed to keep the property in good condition. §_.32(d)(4)

If the grantee or subgrantee is authorized or required to sell the property, proper sales procedures must be established to ensure the highest possible return. §_.32(d)(5)

Solloway&Associates(c) March 21, 2012 27

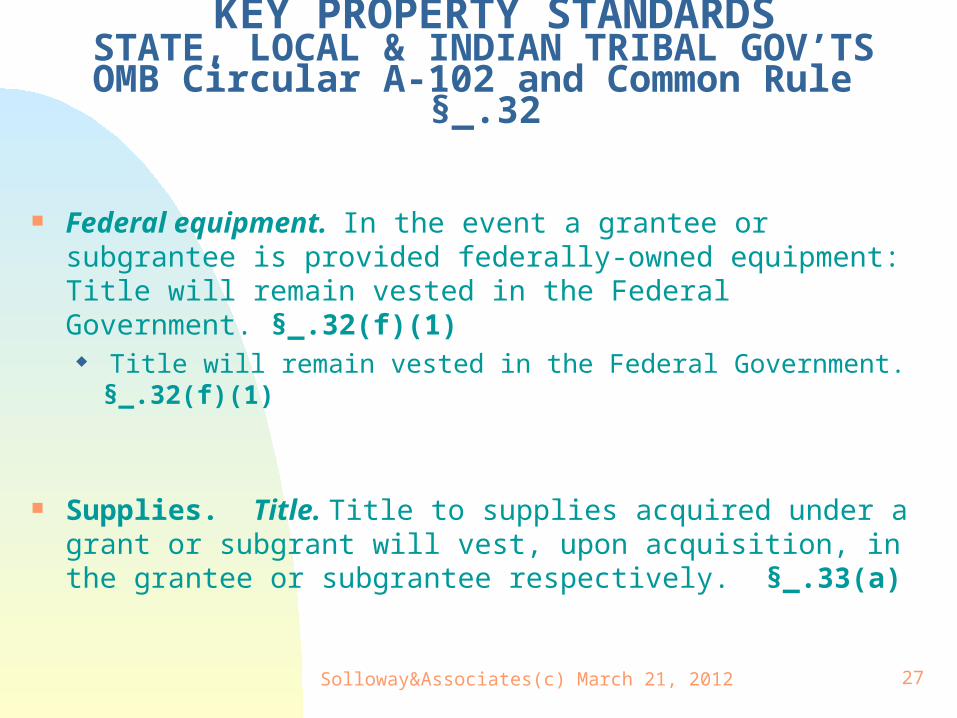

KEY PROPERTY STANDARDS STATE, LOCAL & INDIAN TRIBAL GOV’TS

OMB Circular A-102 and Common Rule §_.32

Federal equipment. In the event a grantee or subgrantee is provided federally-owned equipment: Title will remain vested in the Federal Government. §_.32(f)(1) Title will remain vested in the Federal Government. §_.32(f)

(1)

Supplies. Title. Title to supplies acquired under a grant or subgrant will vest, upon acquisition, in the grantee or subgrantee respectively. §_.33(a)

Solloway&Associates(c) March 21, 2012 28

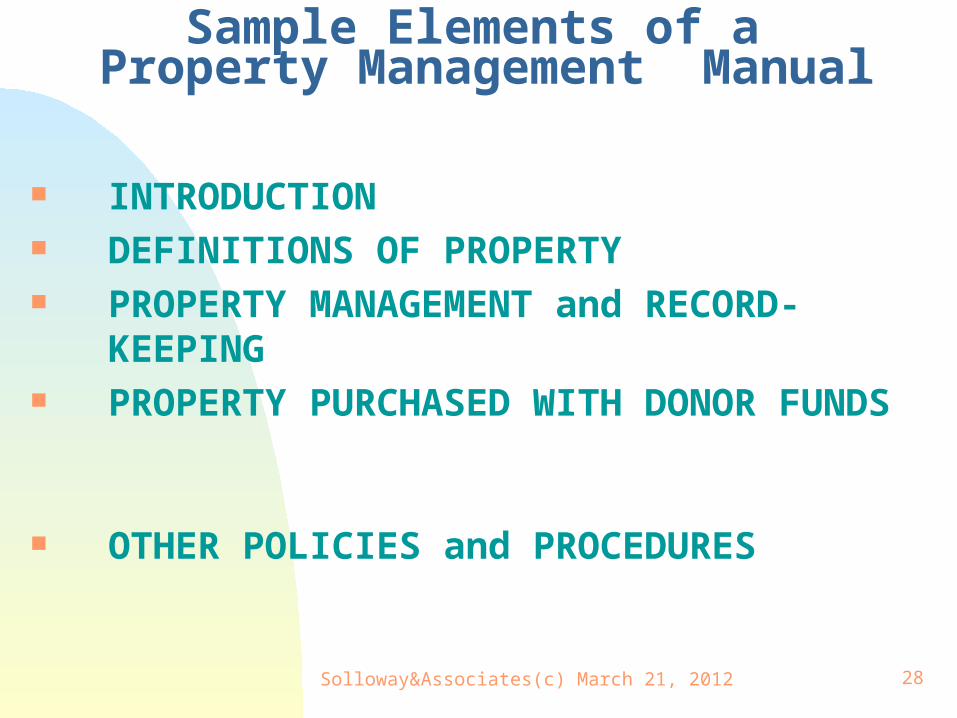

Sample Elements of a Property Management Manual

INTRODUCTION DEFINITIONS OF PROPERTY PROPERTY MANAGEMENT and RECORD-

KEEPING PROPERTY PURCHASED WITH DONOR

FUNDS OTHER POLICIES and PROCEDURES

Solloway&Associates(c) March 21, 2012 29

PERSONNEL

Solloway&Associates(c) March 21, 2012 30

PERSONNEL

2 CFR Part 230 – COST PRINCIPLES FOR NONPROFITS

2 CFR Part 225 - COST PRINCIPLES FOR STATE, LOCAL & TRIBAL GOV’TS

2 CFR Part 220 - COST PRINCIPLES FOR UNIVERSITIES

Solloway&Associates(c) March 21, 2012 31

PERSONNEL – COST PRINCIPLES NONPROFITS 2 CFR Part 230

Compensation for personal services. Allowability. Except as otherwise specifically provided in this paragraph, the costs of such compensation are allowable to the extent that: (1) Total compensation to individual employees is reasonable for the services rendered and conforms to the established policy of the organization consistently applied to both Federal and non-Federal activities (2CFR Part 230. 8.b.(2))

Compensation for personal services. Fringe benefits. Fringe benefits in the form of employer contributions or expenses for social security, employee insurance, workmen's compensation insurance, pension plan costs (see subparagraph 8.h of this appendix), and the like, are allowable, provided such benefits are granted in accordance with established written organizational policies. (2CFR Part 230. 8.g.(2))

Pension plan costs. Costs of the organization's pension plan which are incurred in accordance with the established policies of the organization are allowable, provided: (a) Such policies meet the test of reasonableness; (b) The methods of cost allocation are not discriminatory; (2CFR Part 230. 8.i.(1))

Severance pay. Severance pay, also commonly referred to as dismissal wages, is a payment in addition to regular salaries and wages, by organizations to workers whose employment is being terminated. Costs of severance pay are allowable only to the extent that in each case, it is required by:(a) Law (b) Employer-employee agreement (c) Established policy that constitutes, in effect, an implied agreement on the organization's part, or (d) Circumstances of the particular employment. (2CFR Part 230. 8.k.(1))

Solloway&Associates(c) March 21, 2012 32

PERSONNEL – 2 CFR Part 230 Employee morale, health, and welfare costs. The costs of employee …

services, and any other expenses incurred in accordance with the non-profit organization's established practice or custom for the improvement of working conditions, employer-employee relations, employee morale, and employee performance are allowable. (2CFR Part 230. 13.a.)

Housing and personal living expenses. These costs are allowable as direct costs to sponsored award when necessary for the performance of the sponsored award and approved by awarding agencies. (2CFR Part 230. 20.a.)

Labor relations costs. Costs incurred in maintaining satisfactory relations between the organization and its employees are allowable. (2CFR Part 230. 24)

Relocation costs. Relocation costs are allowable, subject to the limitation described in subparagraphs 42.b, c, and d of this appendix, provided that: (1) The move is for the benefit of the employer. (2) Reimbursement to the employee is in accordance with an established written policy consistently followed by the employer. (2CFR Part 230. 42.a.(1),(2))

Solloway&Associates(c) March 21, 2012 33

PERSONNEL – 2 CFR Part 225 Basic Guidelines. Factors affecting allowability of costs. Be consistent with policies,

regulations, and procedures that apply uniformly to both Federal awards and other activities of the governmental unit. (2CFR Part 225. C.1.e.)

Compensation for Personal Services. Is reasonable for the services rendered and conforms to the established policy of the governmental unit consistently applied to both Federal and non-Federal activities; (2CFR Part 225. 8.a.(1))

Fringe Benefits. The cost of fringe benefits in the form of regular compensation paid to employees during periods of authorized absences from the job, such as for annual leave, sick leave, holidays, court leave, military leave, and other similar benefits, are allowable if: They are provided under established written leave policies; (2CFR Part 225. 8.d.(2))

Pension plan costs. Pension plan costs may be computed using a pay-as-you-go method or an acceptable actuarial cost method in accordance with established written policies of the governmental unit. (2CFR Part 225. 8.e.)

Post-retirement health benefits. PRHB costs may be computed using a pay-as-you-go method or an acceptable actuarial cost method in accordance with established written polices of the governmental unit. (2CFR Part 225. 8.f.)

Severance pay. Payments in addition to regular salaries and wages made to workers whose employment is being terminated are allowable to the extent that, in each case, they are required by law, employer-employee agreement, or established written policy. (2CFR Part 225. 8.g.(1))

Solloway&Associates(c) March 21, 2012 34

PERSONNEL – 2 CFR Part 225 Basic Guidelines. Factors affecting allowability of costs. Be consistent with policies,

regulations, and procedures that apply uniformly to both Federal awards and other activities of the governmental unit. (2CFR Part 225. C.1.e.)

Compensation for Personal Services. Is reasonable for the services rendered and conforms to the established policy of the governmental unit consistently applied to both Federal and non-Federal activities; (2CFR Part 225. 8.a.(1))

Fringe Benefits. The cost of fringe benefits in the form of regular compensation paid to employees during periods of authorized absences from the job, such as for annual leave, sick leave, holidays, court leave, military leave, and other similar benefits, are allowable if: They are provided under established written leave policies; (2CFR Part 225. 8.d.(2))

Pension plan costs. Pension plan costs may be computed using a pay-as-you-go method or an acceptable actuarial cost method in accordance with established written policies of the governmental unit. (2CFR Part 225. 8.e.)

Post-retirement health benefits. PRHB costs may be computed using a pay-as-you-go method or an acceptable actuarial cost method in accordance with established written polices of the governmental unit. (2CFR Part 225. 8.f.)

Severance pay. Payments in addition to regular salaries and wages made to workers whose employment is being terminated are allowable to the extent that, in each case, they are required by law, employer-employee agreement, or established written policy. (2CFR Part 225. 8.g.(1))

Solloway&Associates(c) March 21, 2012 35

PERSONNEL – 2 CFR Part 220 Basic Considerations. Reasonable costs. A cost may be considered reasonable if … the extent to which

the actions taken with respect to the incurrence of the cost are consistent with established institutional policies and practices applicable to the work of the institution generally, including sponsored agreements. (2CFR Part 220. C.3.)

Compensation for personal services. Are allowable to the extent that the total compensation to individual employees conforms to the established policies of the institution, consistently applied .. (2CFR220. 10.a.)

Noninstitutional professional activities. Unless an arrangement is specifically authorized by a Federal sponsoring agency, an institution must follow its institution-wide policies and practices concerning the permissible extent of professional services that can be provided outside the institution for noninstitutional compensation. (2CFR Part 220. 10.e.)

Fringe benefits. Fringe benefits in the form of employer contributions or expenses for social security, employee insurance, workmen's compensation insurance, tuition or remission of tuition for individual employees are allowable, provided such benefits are granted in accordance with established educational institutional policies … (2CFR Part 220. 10.f.(2))

Rules for pension plan costs are as follows: Costs of the institution's pension plan which are incurred in accordance with the established policies of the institution are allowable, provided such policies meet the test of reasonableness … (2CFR Part 220. 10.f.(3)(a))

Rules for sabbatical leave are as follows: Costs of leave of absence by employees for performance of graduate work or sabbatical study, travel, or research are allowable provided the institution has a uniform policy … (2CFR Part 220. 10.f.(4)(a))

Solloway&Associates(c) March 21, 2012 36

PERSONNEL – 2 CFR Part 220 Severance pay. Severance pay is compensation in addition to regular salary and wages which

is paid by an institution to employees whose services are being terminated. Costs of severance pay are allowable only to the extent that such payments are required by law, by employer-employee agreement, by established policy that constitutes in effect an implied agreement on the institution's part, or by circumstances of the particular employment. … (2CFR Part 220. 10.h.(1))

Employee morale, health, and welfare costs and costs. The costs of employee expenses incurred in accordance with the institution's established practice or custom for the improvement of working conditions, employer-employee relations, employee morale, and employee performance are allowable. (2CFR220. 16.)

Labor relations costs. Costs incurred in maintaining satisfactory relations between the institution and its employees are allowable.(2CFR Part 220. 27.)

Recruiting costs. Subject to subsections J.42.b, c, and d of this Appendix … costs are allowable to the extent that such costs are incurred pursuant to a well-managed recruitment program. … (2CFR Part 220. 42.a.)

Recruiting costs. Costs … incurred to attract professional personnel from other institutions that do not meet the test of reasonableness or do not conform with the established practices of the institution, are unallowable. (2CFR Part 220. 42.c.)

Solloway&Associates(c) March 21, 2012 37

Sample Sections of a Personnel Manual ABOUT (YOUR ORGANIZATION’S NAME) INTRODUCTION GENERAL EMPLOYMENT INFORMATION COMPENSATION BENEFITS EMPLOYEE RESPONSIBILITIES STANDARDS of CONDUCT

Solloway&Associates(c) March 21, 2012 38

PROCUREMENT

Solloway&Associates(c) March 21, 2012 39

PROCUREMENT STANDARDS

NONPROFITS and UNIVERSITIES 2 CFR Part 215.40 - .48

STATE, LOCAL & INDIAN TRIBAL GOV’TS OMB Circular A-102 and Common Rule §_.36

Solloway&Associates(c) March 21, 2012 40

KEY PROCUREMENT STANDARDSNONPROFITS and UNIVERSITIES

2 CFR Part 215.40 - .48 Standards are furnished to ensure materials and services are obtained in an

effective manner and in compliance with the provisions of applicable Federal statutes and executive orders. No additional procurement standards or requirements shall be imposed by the Federal awarding agencies upon recipients, unless specifically required by Federal statute or executive order or approved by OMB. §_.40

The standards contained in this section do not relieve the recipient of the contractual responsibilities arising under its contract(s). §_.41

The recipient shall maintain written standards of conduct governing the performance of its employees engaged in the award and administration of contracts. §_.42

All procurement transactions shall be conducted in a manner to provide, to the maximum extent practical, open and free competition. §_.43

Solloway&Associates(c) March 21, 2012 41

KEY PROCUREMENT STANDARDSNONPROFITS and UNIVERSITIES

2 CFR Part 215.40 - .48 All recipients shall establish written procurement procedures. §_.44(a)

Where appropriate, an analysis is made of lease and purchase alternatives to determine which would be the most economical and practical procurement for the Federal Government. §_.44(a)(2)

Positive efforts shall be made by recipients to utilize small businesses, minority-owned firms, and women's business enterprises, whenever possible. §_.44(b)

The type of procuring instruments used ( e.g., fixed price contracts, cost reimbursable contracts, purchase orders, and incentive contracts) shall be determined by the recipient. The “cost-plus-a-percentage-of-cost” or “percentage

… of construction cost” methods of contracting shall not be used. . §_.44(c)

Solloway&Associates(c) March 21, 2012 42

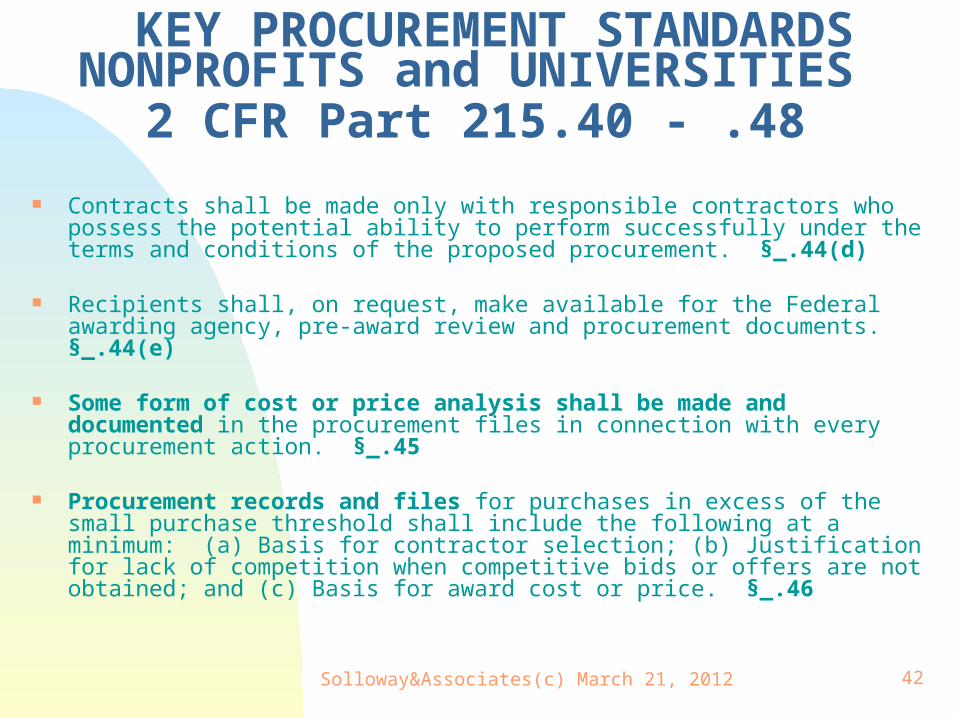

KEY PROCUREMENT STANDARDSNONPROFITS and UNIVERSITIES

2 CFR Part 215.40 - .48 Contracts shall be made only with responsible contractors who possess the

potential ability to perform successfully under the terms and conditions of the proposed procurement. §_.44(d)

Recipients shall, on request, make available for the Federal awarding agency, pre-award review and procurement documents. §_.44(e)

Some form of cost or price analysis shall be made and documented in the procurement files in connection with every procurement action. §_.45

Procurement records and files for purchases in excess of the small purchase threshold shall include the following at a minimum: (a) Basis for contractor selection; (b) Justification for lack of competition when competitive bids or offers are not obtained; and (c) Basis for award cost or price. §_.46

Solloway&Associates(c) March 21, 2012 43

KEY PROCUREMENT STANDARDSNONPROFITS and UNIVERSITIES

2 CFR Part 215.40 - .48

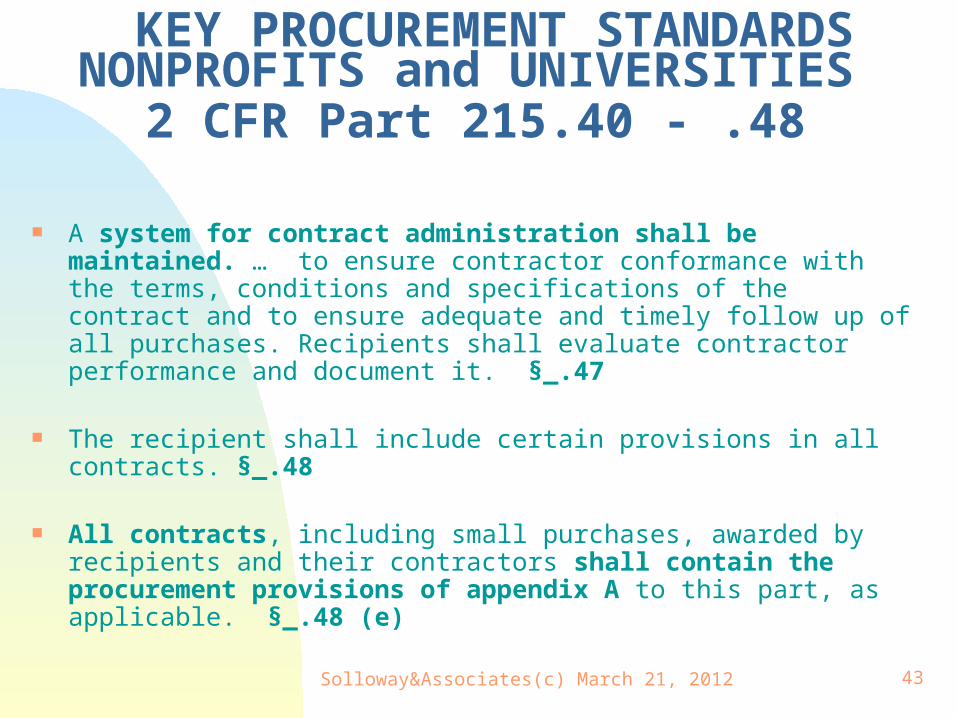

A system for contract administration shall be maintained. … to ensure contractor conformance with the terms, conditions and specifications of the contract and to ensure adequate and timely follow up of all purchases. Recipients shall evaluate contractor performance and document it. §_.47

The recipient shall include certain provisions in all contracts. §_.48

All contracts, including small purchases, awarded by recipients and their contractors shall contain the procurement provisions of appendix A to this part, as applicable. §_.48 (e)

Solloway&Associates(c) March 21, 2012 44

KEY PROCUREMENT STANDARDS STATE, LOCAL & INDIAN TRIBAL GOV’TS

OMB Circular A-102 and Common Rule §_.36

States. When procuring property and services under a grant, a State will follow the same policies and procedures it uses for procurements from its non-Federal funds. The State will ensure that every purchase order or other contract includes any clauses required by Federal statutes and executive orders and their implementing regulations. § 135.36(a)

Procurement standards. Grantees and subgrantees will use their own procurement procedures which reflect applicable State and local laws and regulations, provided that the procurements conform to applicable Federal law and the standards identified in this section. §_.36(b)(1)

Grantees and subgrantees will maintain a written code of standards of conduct governing the performance of their employees engaged in the award and administration of contracts. The recipient shall include certain provisions in all contracts. §_.36(b)(3)

Grantee and subgrantee procedures will provide for a review of proposed procurements to avoid purchase of unnecessary or duplicative items. §_.36(b)(4)

Grantees and subgrantees will maintain records sufficient to detail the significant history of a procurement. §_.36(b)(9)

Solloway&Associates(c) March 21, 2012 45

KEY PROCUREMENT STANDARDS STATE, LOCAL & INDIAN TRIBAL GOV’TS

OMB Circular A-102 and Common Rule §_.36

Grantees and subgrantees will have protest procedures to handle and resolve disputes relating to their procurements and shall in all instances disclose information regarding the protest to the awarding agency. §_.36(b)(12)

Competition. All procurement transactions will be conducted in a manner providing full and open competition consistent with the standards of §_.36. §_.36(c)(1)

Grantees will have written selection procedures for procurement transactions. §_.36(c)(3)

Methods of procurement to be followed— Procurement by small purchase procedures. §_.36(d)(1) Procurement by sealed bids. §_.36(d)(2) Procurement by competitive proposals. §_.36(d)(3) Procurement by noncompetitive proposals. §_.36(d)(4)

Solloway&Associates(c) March 21, 2012 46

KEY PROCUREMENT STANDARDS STATE, LOCAL & INDIAN TRIBAL GOV’TS

OMB Circular A-102 and Common Rule §_.36

Contracting with small and minority firms, women's business enterprise and labor surplus area firms. The grantee and subgrantee will take all necessary affirmative steps to assure that minority firms, women's business enterprises, and labor surplus area firms are used when possible.§_.36(e)(1)

Contract cost and price. Grantees and subgrantees must perform a cost or price analysis in connection with every procurement action including contract modifications. §_.36(f)(1)

Awarding agency review. Grantees and subgrantees must make available, upon request of the awarding agency, technical specifications on proposed procurements where the awarding agency believes such review is needed to ensure that the item and/or service specified is the one being proposed for purchase. §_.36(g)(1)

Bonding requirements. For construction or facility improvement contracts or subcontracts … §_.36(h)

Contract provisions. A grantee's and subgrantee's contracts must contain provisions in paragraph (i) of this section. .§_.36(i)

Solloway&Associates(c) March 21, 2012 47

Sample Sections of a Procurement Manual

INTRODUCTION GENERAL PROCUREMENT POLICIES PROCUREMENT POLICIES FILES AND RECORDS PROCUREMENT CYCLE and PROCEDURES PROCUREMENT INSTRUMENTS

Solloway&Associates(c) March 21, 2012 48

Issue Manuals, Don’t Keep Them in Draft Remember, Manuals Can Always Be Updated Each Manual Should Be Issued Separately Keep Them Simple, So They’ll Be Read Train Staff on Your Manuals/Operations Be Sure to Follow Your Policies

SOME THOUGHTS TO KEEP IN MIND

Solloway&Associates(c) March 21, 2012 49

Thank You and Questions?

49

Related Documents