The Nature of Management Accounting

The Nature of Management Accounting. 2 Management vs. Financial Accounting (1 of 6) Necessity Financial Accounting (FA): SEC (or banks or suppliers)

Dec 22, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

The Nature of Management Accounting

2

Management vs. Financial Accounting (1 of 6)

Necessity Financial Accounting (FA): SEC (or banks or

suppliers) requires publicly traded companies to publish financial statements according to GAAP.

Management accounting (MA) is optional. Purpose.

FA: Produce financial statements for outside users.

MA: Help managers plan, implement and control.

3

Management vs. Financial Accounting (2 of 6)

Users. FA: faceless group, external users, present

or potential shareholders. MA: Known managers who influence what

information is needed. Underlying structure.

FA: built around: Assets = Liabilities + Stockholders’ Equity.

MA: 3 purposes each with its own set of concepts and constructs (addressed later).

4

Management vs. Financial Accounting (3 of 6) Source of principles.

FA: GAAP. MA: whatever managers believe is useful.

Time orientation. FA: historical, tell it like it was. MA: future/decision oriented, tell it like it will

be. (However, the past is often a good predictor of the future.)

5

Management vs. Financial Accounting (4 of 6) Information content.

FA: financial statements are the end product and include primarily financial info.

MA: non-monetary as well as monetary info. Information precision.

FA: Uses approximations but as a generalization is more precise than MA.

MA: Management needs info rapidly to be useful in decision making and therefore precision is sometimes sacrificed.

6

Management vs. Financial Accounting (5 of 6) Report frequency:

FA: Publicly traded, SEC: quarterly, with more detailed info annually.

MA: Up to management.

Report timeliness. FA: Usually, several weeks to months after

fiscal close of accounting period. MA: Quickly to be useful for decision making.

7

Management vs. Financial Accounting (6 of 6)

Report entity. FA: Organization as a whole. MA: Relatively small parts

(responsibilities centers such as departments, product lines, divisions, subsidiaries as well as organization as a whole.)

8

Uses of Management Accounting

1. Measurement of revenues, costs, and assets.

2. Control.3. To aid in choosing among

alternative courses of action.

9

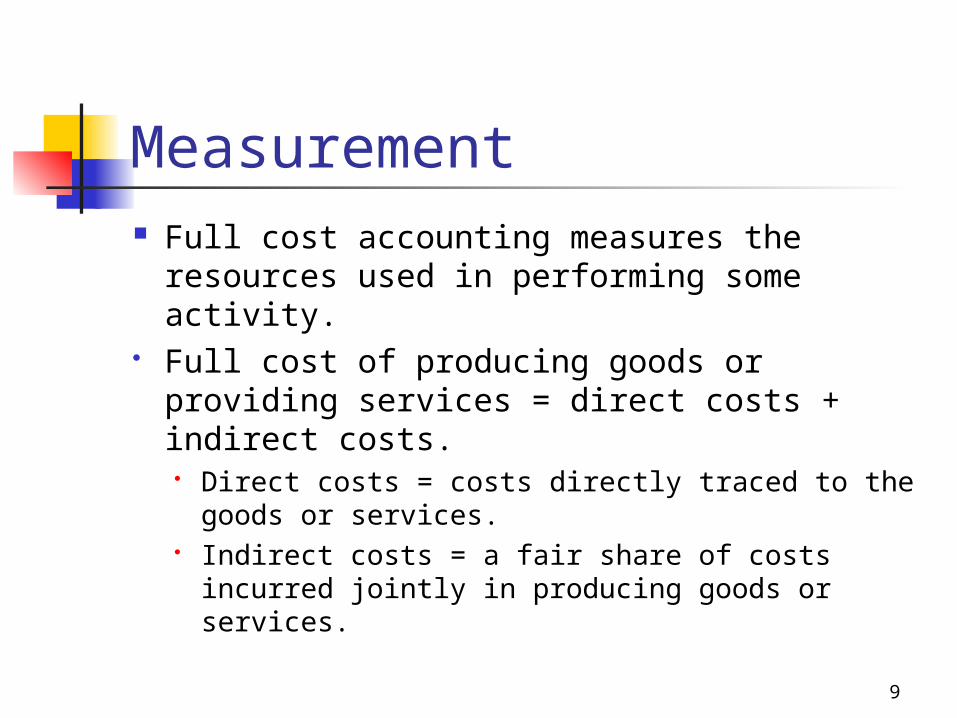

Measurement Full cost accounting measures the

resources used in performing some activity.

Full cost of producing goods or providing services = direct costs + indirect costs. Direct costs = costs directly traced to the

goods or services. Indirect costs = a fair share of costs incurred

jointly in producing goods or services.

10

Measurement example Be careful of how you allocate that

overhead. How expensive is that ashtray?

11

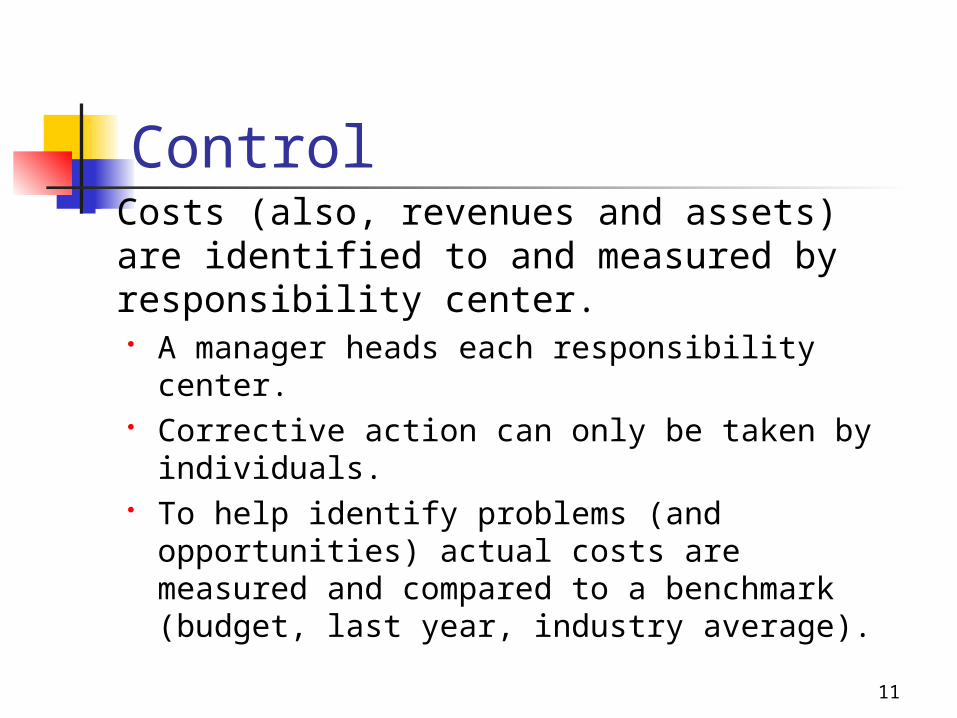

Control Costs (also, revenues and assets) are

identified to and measured by responsibility center. A manager heads each responsibility center. Corrective action can only be taken by

individuals. To help identify problems (and

opportunities) actual costs are measured and compared to a benchmark (budget, last year, industry average).

12

Alternative Choice Decisions Differential costs of alternative

possible actions are developed.

13

General Observations on MA

Different numbers for different purposes. Many different types of costs: historical,

standard, overhead, variable, fixed, differential, marginal, opportunity, direct, estimated, full, etc.

Clarify which type you are talking about. Accounting numbers are approximations. Best that we can with incomplete data. Accounting evidence is only partial evidence

other factors help make decisions. People not numbers get things done. How you

use the numbers is as important as how the numbers are produced.

14

The Behavior of Costs and Decision-Making

15

What will be covered A general overview of how costs

“behave.” Several applications of how this

knowledge can help you make better, informed, decisions.

Some examples of what we will be able to solve:

16

Breakeven analysis You are considering offering a new

service (such as delivery of take-out) and you wish to determine what volume you will need to generate to cover your costs.

17

Close a location decision You are responsible for several

locations. One location consistently shows a “loss” on its income statement. Should it be closed? If so, will your region be better off?

18

Special orders decisions You have been offered a one-time

special order. You need to determine if you should accept the order given the price is lower than the normal charge for comparable meals you serve.

19

Behavior of Costs Cost-volume relationships.

Fixed and variable costs. Step-function costs.

20

Relation of Costs to Volume

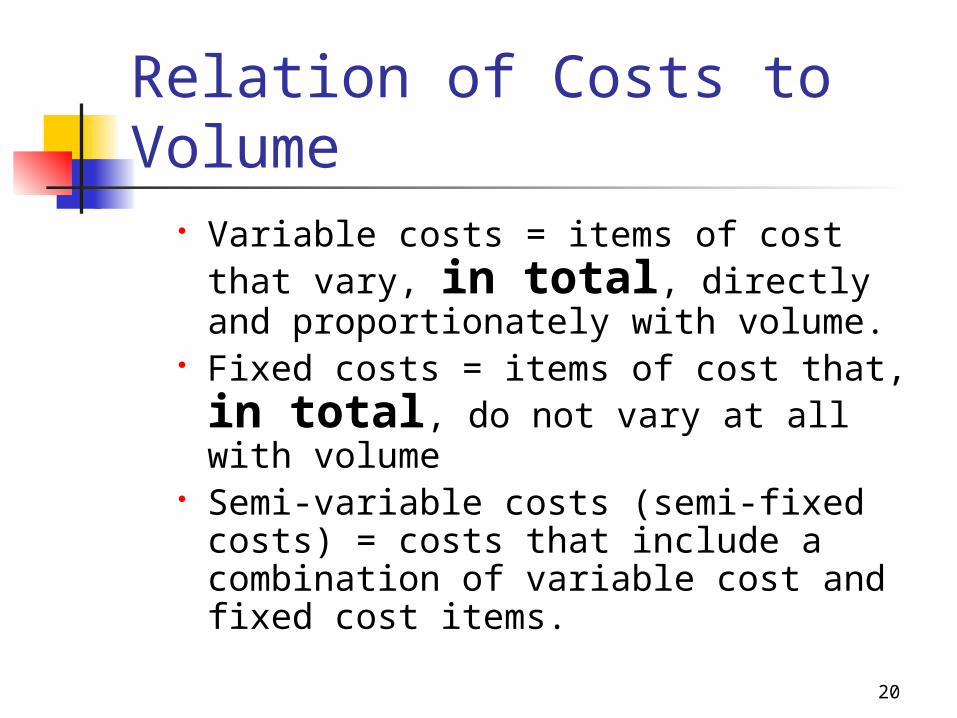

Variable costs = items of cost that vary, in total, directly and proportionately with volume.

Fixed costs = items of cost that, in total, do not vary at all with volume

Semi-variable costs (semi-fixed costs) = costs that include a combination of variable cost and fixed cost items.

21

Variable Costs Items of cost that vary, in total,

directly and proportionately with volume. Volume refers to activity level. Examples:

Material costs varies with units sold. Electricity costs varies with production hours. Stationery and postage costs varies with

number of letters written.

22

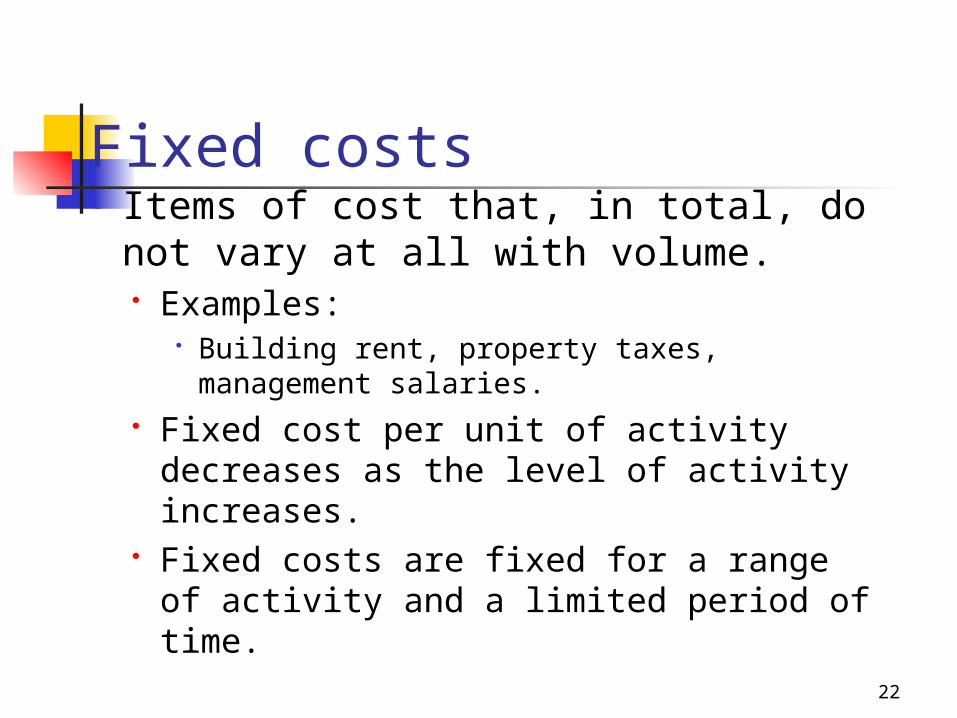

Fixed costs Items of cost that, in total, do not

vary at all with volume. Examples:

Building rent, property taxes, management salaries.

Fixed cost per unit of activity decreases as the level of activity increases.

Fixed costs are fixed for a range of activity and a limited period of time.

23

Beware of how cost behave! Fixed costs should not be treated

as variable in decision making. Senate gym example.

24

Cost-volume (C-V) diagram

Y or vertical axis reflects total cost. X or horizontal axis reflects volume. y = mx + b.

y is the cost at a volume of x; m is the rate of cost change per unit of

volume change, or the slope (variable costs).

b is the vertical intercept, which represents the fixed cost component.

25

Profit-graph Add revenue line to C-V diagram. Assumes constant selling price. UR = unit revenue TR = total revenue

26

TC = TFC +(UVC*X)

TC = total cost; TFC = total fixed cost (per time

period), UVC = Unit variable cost (per unit

of volume), X = volume.

27

Cost Relations

Average costs = total cost/volume. Average cost behaves differently

than total cost. As volume goes up

Total fixed cost remains constant, total variable costs goes up, per unit variable costs stays the same, per unit fixed cost goes down, per unit total cost goes down.

28

Step-function costs

Incurred when costs are added in discrete chunks, e.g., a manager for every 10 workers.

Adding the “chunk” of costs increases capacity.

Height of a stair step (riser) indicates the cost of adding incremental capacity.

Step width (tread) shows how much additional volume of that activity can be serviced by this additional increment of capacity.

29

Contribution Unit contribution margin = marginal

income = unit selling price - variable cost per unit = UR - UVC.

What is contribution: First it is the contribution to cover fixed

costs. Then it is the contribution toward profit.

30

Breakeven Volume TR = UR*X TC = TFC + (UVC*X) Breakeven: TR = TC Substituting: UR*X = TFC +

(UVC*X) X = TFC/(UR - UVC)

31

Break-even Volume In units = Fixed costs/unit

contribution In revenue dollars just compute

break-even in units and multiply by the selling price.

32

A simple example You run a restaurant that serves

one type of meal that sells for $5. The variable costs (ingredients,

container, etc.) total $3. Monthly fixed costs (rent, salary,

etc.) total $4,000. What is the breakeven amount in

volume and in sales dollars?

33

Target Profit Add to breakeven analysis to show

units or dollar of sales to achieve a target (T) level of profit:

UR*X = TFC + (UVC*X) + T

X = (TFC+T)/(UR - UVC)

34

A simple example - continued Instead of just breaking even, you

would like to make a profit of $2,500.

What volume of meals will you need to serve?

35

Now your turn.

Take-out problem.

36

Up the ante Some slightly harder problems

Grizzly Express

Store 201 example

37

Limitations of C-V Relations A straight line approximates cost

behavior only within a certain range of volume, the relevant range. When volume approaches zero,

management takes steps to reduce fixed costs.

When volume exceeds relevant range, fixed costs increase.

38

Limitations (continued)

Amount of variable costs depends on the time period over which behavior is estimated (the relevant time period). If the time period is one day, few

costs are variable. Over an extremely long time period,

no costs are fixed.

39

Linear Assumption C-V relationship is often not linear.

Some cost functions are curved (curvilinear).

Segments of the curve can be approximated by a straight line, each with its own relevant range.

40

Short-Run Alternative Choice Decisions

41

Highlights

Alternative choice decisions: manager seeks to choose best of several alternative courses of action.

Introduces construct of differential costs and revenues for several types of problems, each having a relatively short time horizon.

42

Differential Costs and Revenues

Costs that are different under one set of conditions than they would be under another.

Revenues that are different under one set of conditions than they would be under another.

43

Nature of Full and Differential Costs

Full cost of a product or other cost object = sum of direct cost + fair share of applicable indirect costs.

Differential costs include only those cost elements of cost that are different under a certain set of conditions.

44

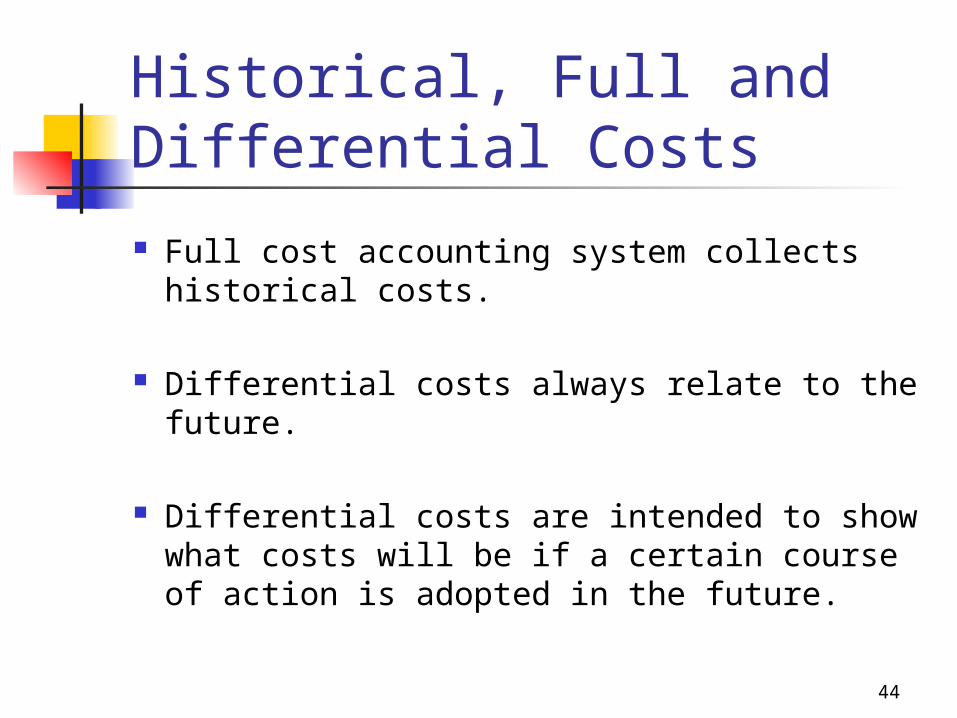

Historical, Full and Differential Costs

Full cost accounting system collects historical costs.

Differential costs always relate to the future.

Differential costs are intended to show what costs will be if a certain course of action is adopted in the future.

45

Steps in the Analysis

Define the problem. Select possible alternative solutions. (Status

quo may be the benchmark against which other alternatives are measured.)

For each alternative, measure and evaluate consequences that can be expressed in quantitative terms.

Identify those consequences that cannot be expressed in quantitative terms and evaluate them against each other and against the measured consequences.

Reach a decision.

46

Opportunity costs

A measure of the value that is lost or sacrificed when the choice of one course of action requires giving up an alternative course of action.

Not measured in accounting records.

47

Sunk Cost A cost that has already been incurred

and therefore cannot be changed by any decision currently being considered.

Not a differential cost.

48

Importance of Time Span

The longer the time span the more items of cost that are differential.

In the very long run full costs are differential costs.

49

Sensitivity Analysis

Considers how sensitive the quantitative measurements of the alternatives are to changes in assumptions.

50

Just One Fallacy

Each additional unit of production adds just variable costs.

If many units are added, then step function costs (i.e., fixed costs) are added.

Therefore, step function costs are averaged out over the additional units of volume.

51

Sell Now or Process Further Assume that the product being

offered can either be sold currently as is for a certain sum or processed further, with additional costs, at which time it can be sold for a greater amount than now.

52

Sell Now or Process Further

Cost per unit to date

Cost per unit to

complete

Material $300 $200

Labor 200 100

Var. OH 100 100

Fixed OH 200

Total $800 $400

53

Sell Now or Process Further The product is being discontinued and

its price has fallen. If the product is processed to completion it can be sold for only $1,000 (less than cost incurred of $1,200 = $800 + $400)

If sold now they will bring in $500. What should we do? Should we incur $400 more cost

knowing we will end up losing money overall? Is this throwing good money at bad?

54

Differential costs

Sell Now

Process

Further

Difference

Revenue $500 $1,000 $500

Current costs

800 800 0

New costs

0 400 <400>

Total costs

800 1,200 <400>

Profit <300>

<200> 100

55

Sunk Costs Cost that have already been

incurred and cannot be changed. Not relevant to any decision Cost of $800 already incurred in

the previous example are sunk and should be ignored. They do not change the situation in any way.

56

Variation on a theme Restaurant 314

57

Make or Buy Often a company will purchase an

ingredient externally that is part of what they are making.

They could make this ingredient internally if it is to their benefit to do so.

These decisions usually only involve costs, not revenues.

Qualitative factors must be considered.

58

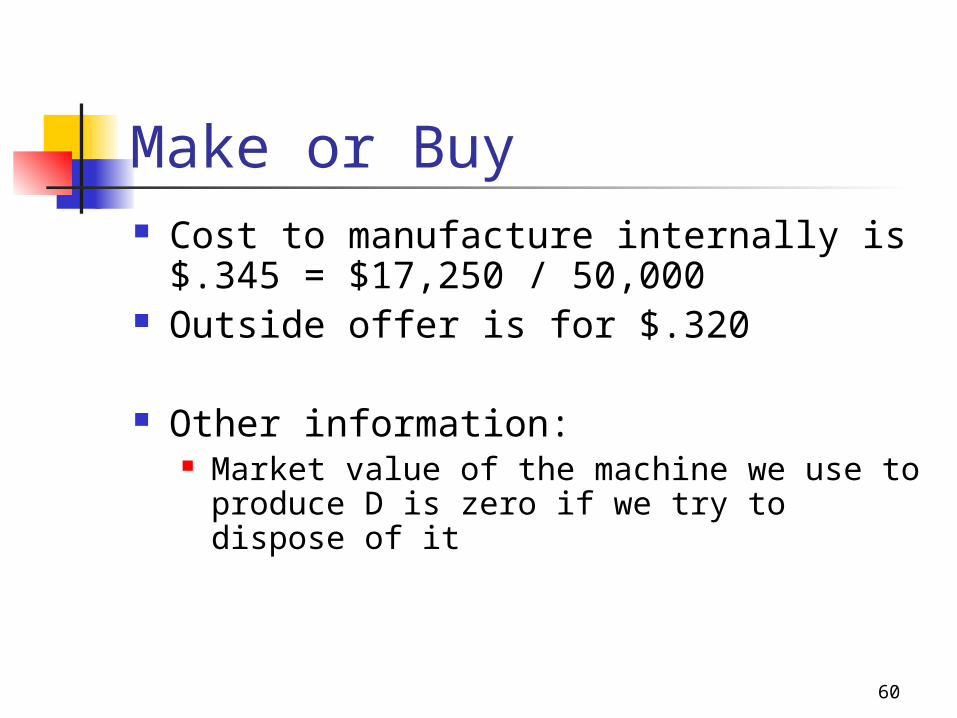

Make or Buy XYZ Co. is considering an offer to

supply 50,000 units of ingredient D at a cost of $.32 per unit.

The company is currently producing ingredient D internally with the following costs:

59

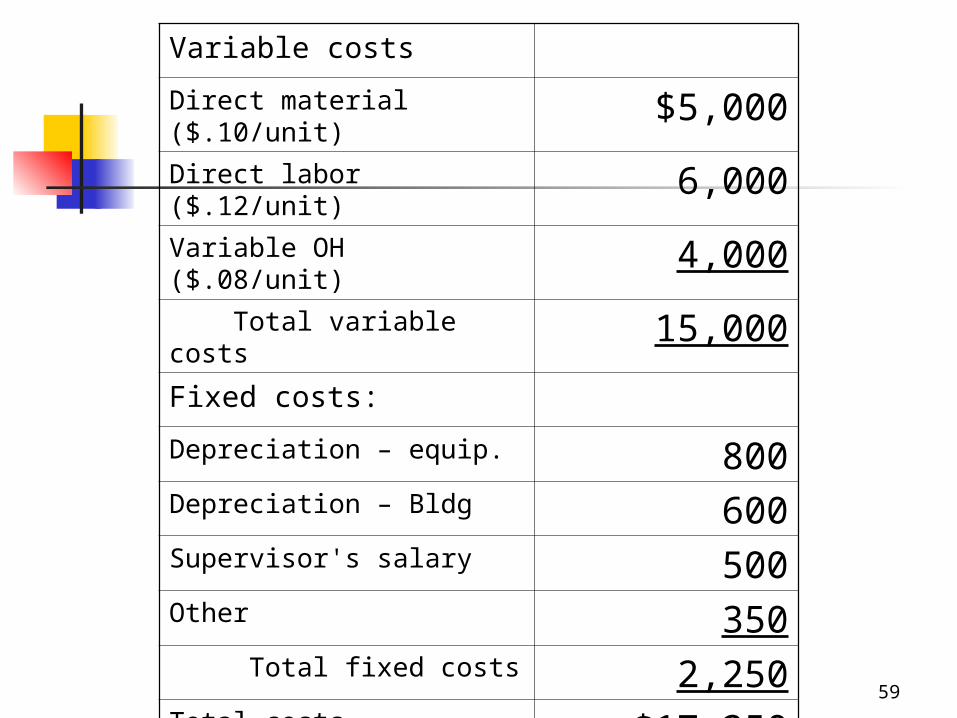

Variable costs

Direct material ($.10/unit) $5,000Direct labor ($.12/unit) 6,000Variable OH ($.08/unit) 4,000 Total variable costs 15,000Fixed costs:

Depreciation – equip. 800Depreciation – Bldg 600Supervisor's salary 500Other 350 Total fixed costs 2,250Total costs $17,250

60

Make or Buy Cost to manufacture internally is $.345

= $17,250 / 50,000 Outside offer is for $.320

Other information: Market value of the machine we use to

produce D is zero if we try to dispose of it

61

Internal Costs

External Costs

Difference

Variable costs

Direct material ($.10/unit)

$5,000 $0 $5,000

Direct labor ($.12/unit) 6,000 0 6,000

Variable OH ($.08/unit)

4,000 0 4,000

Total variable costs 15,000 0 15,000

Fixed costs:

Depreciation – equip. 800 800 0

Depreciation – Bldg 600 600 0

Supervisor's salary 500 500

Other 350 350 0

Total fixed costs 2,250 1,750 500

Cost of buying outside 0 16,000 (16,000)

Total costs $17,250 $17,750 ($500)

62

Avoidable Costs Not all fixed costs are irrelevant sunk costs Some fixed costs are avoidable (i.e., they

can be avoided under one alternative) In the previous example we can terminate

the supervisors, hence this fixed costs is avoidable and therefore relevant and differential.

Since avoidable costs of $15,500 is less than the cost of the external part, we should reject the offer based on financial grounds.

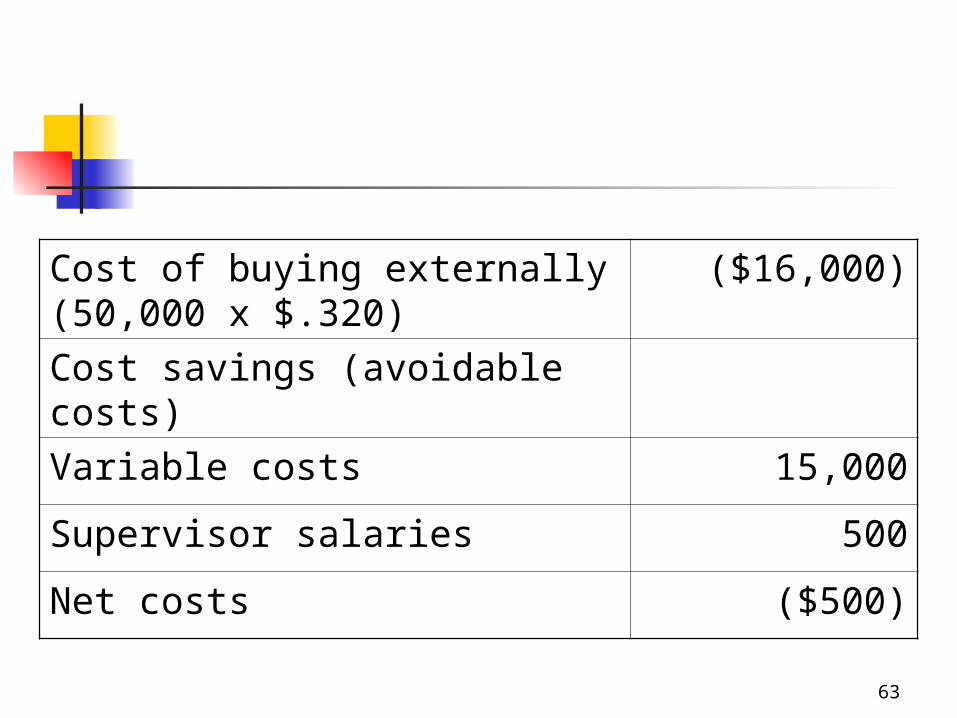

63

Cost of buying externally (50,000 x $.320)

($16,000)

Cost savings (avoidable costs)

Variable costs 15,000

Supervisor salaries 500

Net costs ($500)

64

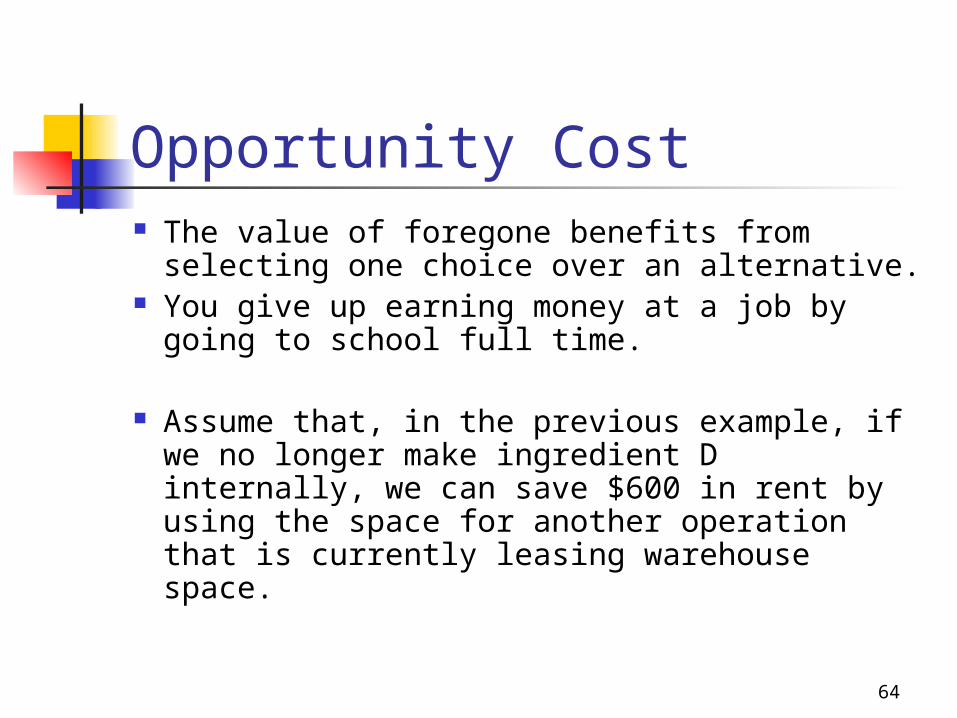

Opportunity Cost The value of foregone benefits from

selecting one choice over an alternative. You give up earning money at a job by

going to school full time.

Assume that, in the previous example, if we no longer make ingredient D internally, we can save $600 in rent by using the space for another operation that is currently leasing warehouse space.

65

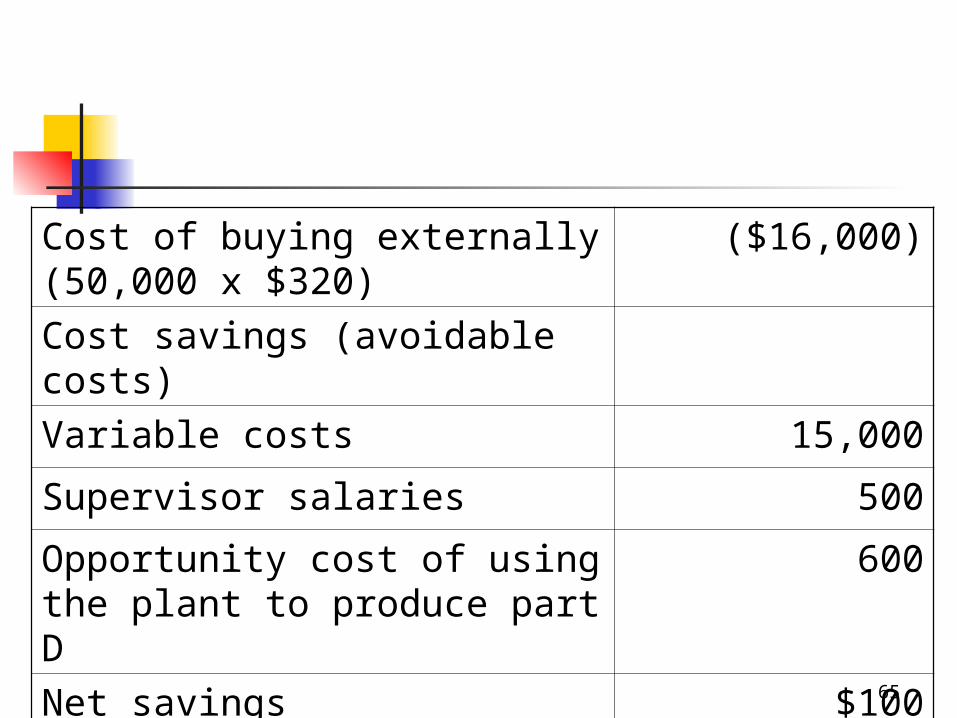

Cost of buying externally (50,000 x $320)

($16,000)

Cost savings (avoidable costs)

Variable costs 15,000

Supervisor salaries 500

Opportunity cost of using the plant to produce part D

600

Net savings $100

66

Your turn

Sauce It Up

67

Dropping a Product Need to calculate the change in

profit if the product is dropped versus retained.

Both differential costs and revenues are considered.

Procedure differs if there is excess capacity versus at capacity

If at capacity need to consider opportunity costs.

68

Dropping a Store Region 5 is considering dropping Store

#2. Direct fixed costs are items directly

traceable to the division Example – salary of a worker who spends all

his time in this restaurant Allocated fixed costs are fixed costs that

are shared between divisions Example – Salary of the regional manager

69

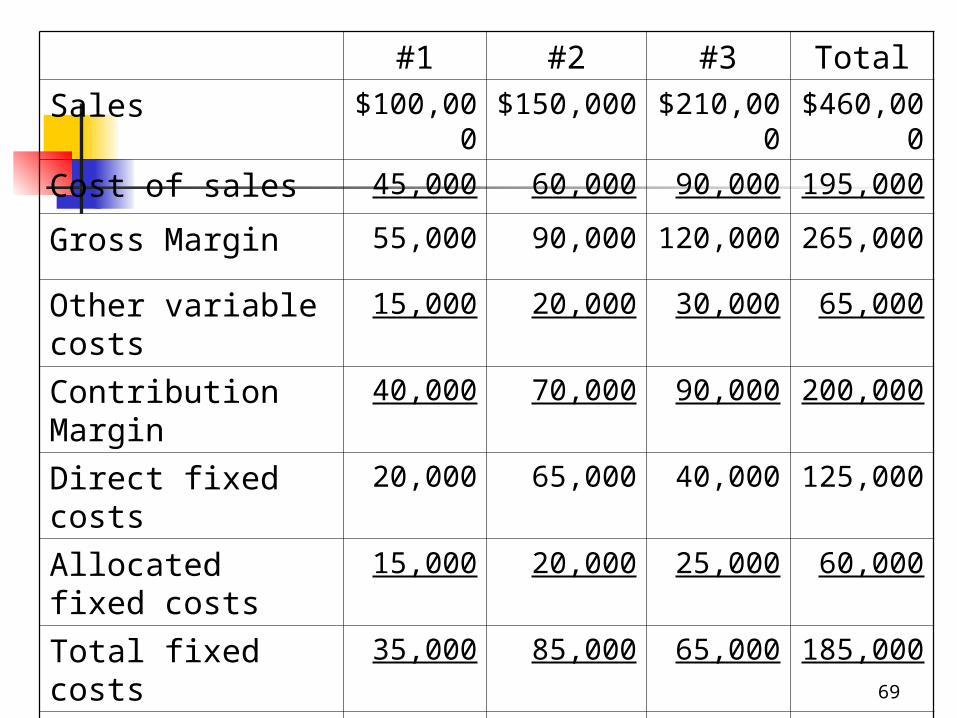

#1 #2 #3 Total

Sales $100,000

$150,000 $210,000

$460,000

Cost of sales 45,000 60,000 90,000 195,000

Gross Margin 55,000 90,000 120,000 265,000

Other variable costs

15,000 20,000 30,000 65,000

Contribution Margin

40,000 70,000 90,000 200,000

Direct fixed costs 20,000 65,000 40,000 125,000

Allocated fixed costs

15,000 20,000 25,000 60,000

Total fixed costs 35,000 85,000 65,000 185,000

Net Income $5,000 $(15,000)

$25,000

$15,000

70

Dropping a Product Should #2 be dropped?

It is showing a loss of ($15,000)! What would happen to the division’s total net

income if the store was dropped?

Assume the direct fixed costs are building rent that can be avoided.

Allocated fixed costs are the regional manager’s salary and some corporate costs.

If Store #2 were dropped, there would not be any impact on the other store’s volume.

71

Lost revenue $(150,000)

Cost savings

COGS 60,000

Other variable costs 20,000

Direct fixed costs 65,000

Total cost savings 145,000

Net loss from dropping division

$(5,000)

72

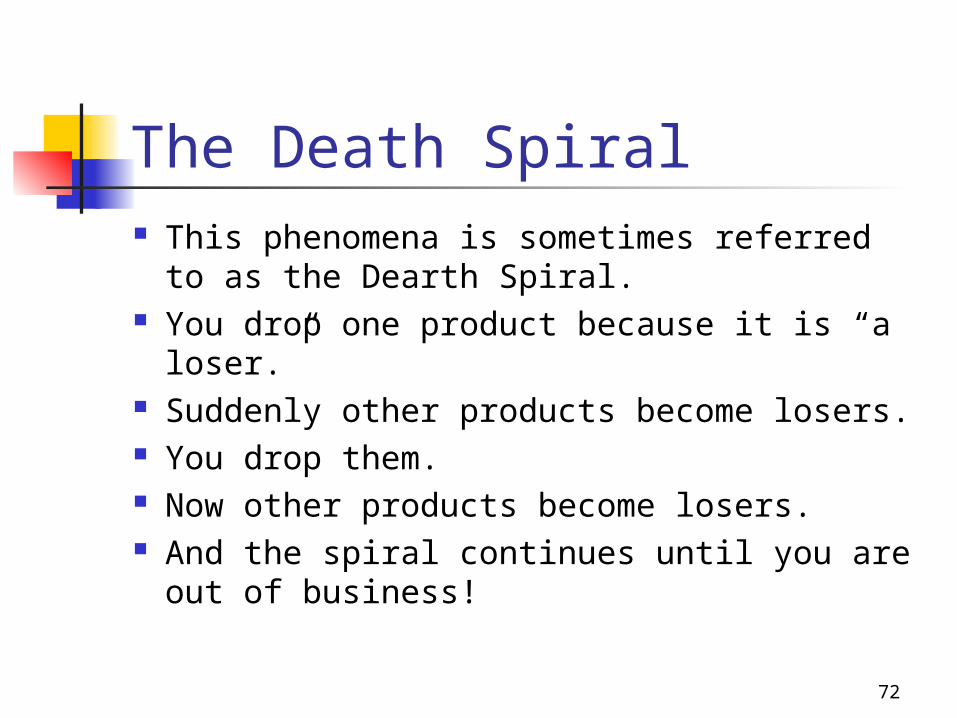

The Death Spiral This phenomena is sometimes referred to

as the Dearth Spiral. You drop one product because it is “a

loser.” Suddenly other products become losers. You drop them. Now other products become losers. And the spiral continues until you are out

of business!

73

Your turn.

Drop store 103 example.

74

Variation on a theme Try your hand at a special order

problem.

Girl Scouts example

How Special

75

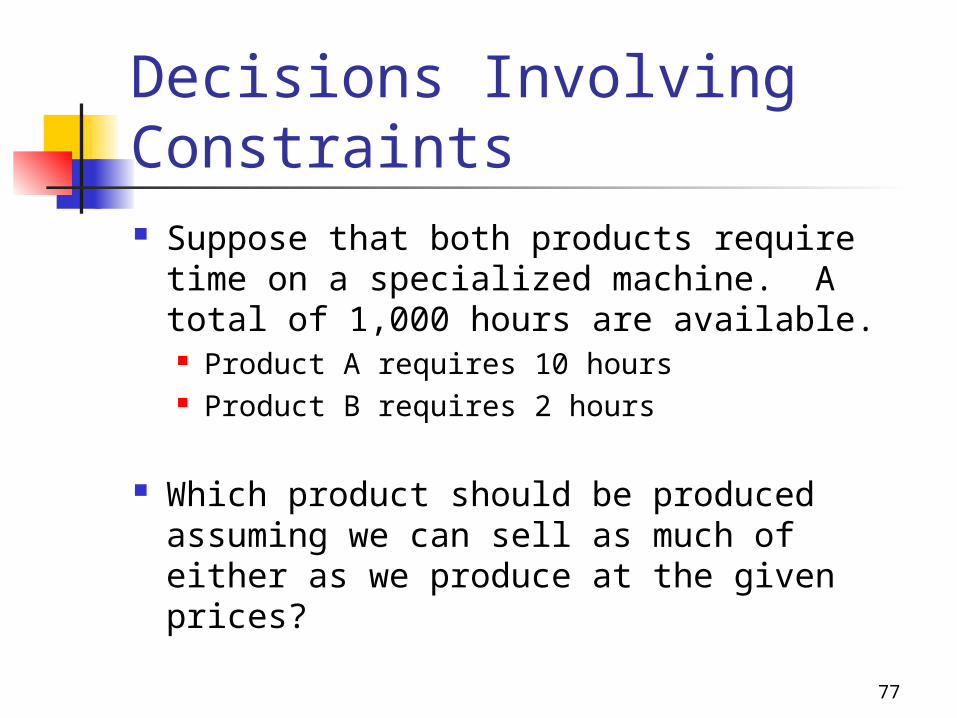

Decisions Involving Constraints Basic decision is to keep any

product/store with a positive contribution margin as long as you can keep selling it.

That changes if making one product affects another product.

An example is when there is a constraint such as a limited amount of skilled labor or machine time

76

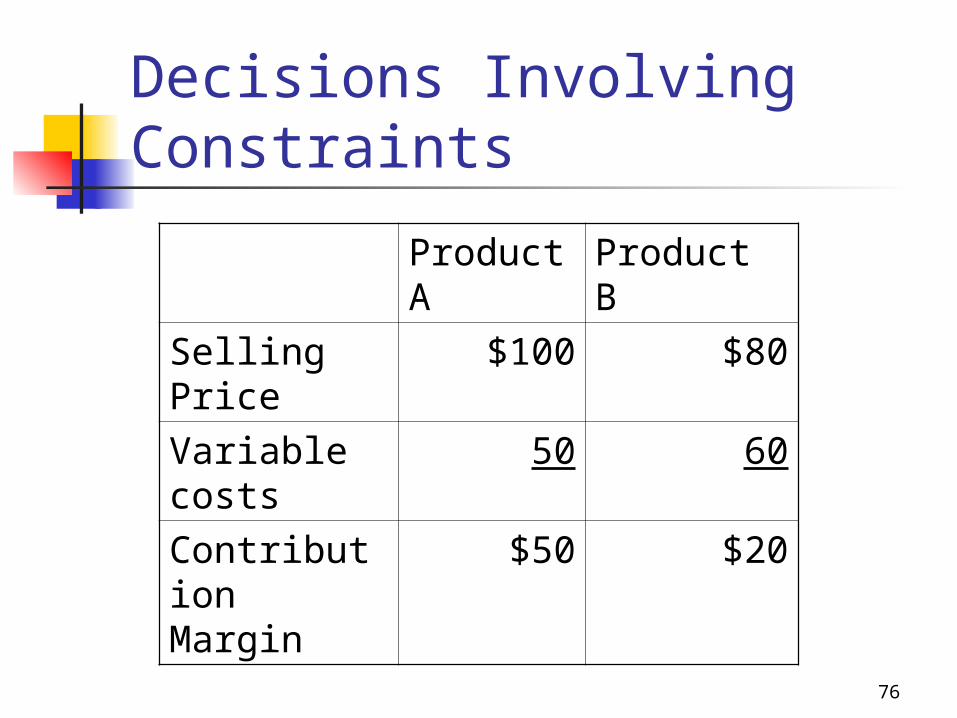

Decisions Involving Constraints

Product A

Product B

Selling Price

$100 $80

Variable costs

50 60

Contribution Margin

$50 $20

77

Decisions Involving Constraints Suppose that both products require

time on a specialized machine. A total of 1,000 hours are available. Product A requires 10 hours Product B requires 2 hours

Which product should be produced assuming we can sell as much of either as we produce at the given prices?

78

Decisions Involving Constraints Product A has the highest CM, we

make $50 for every one sold versus only $20 for each B.

But what about those machine hours?

79

Decisions Involving Constraints Since A requires 10 hours and we have

1,000 total, we can produce 100 A. At $50 each = $5,000 CM

Since B requires only 2 hours we can produce 500 total. At $20 each = $10,000

Company is better off producing all Product B.

80

Decisions Involving Constraints Decision rule:

Under conditions of a constraint, produce the product with the highest contribution margin per unit of the constraint.

A has $50/10 hours or $5 per machine hour.

B has $20/2 hours or $10 per machine hour.

81

A Few More Examples To Try Drew

Walter’s

Wasted Away

Related Documents