The Most Taxing The Most Taxing Questions Questions © 2001 Dr. B. C. Paul © 2001 Dr. B. C. Paul

The Most Taxing Questions © 2001 Dr. B. C. Paul. Taxes and Project Analysis Showed you how to get cash flows and compute returns but do you really get.

Dec 28, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

The Most Taxing The Most Taxing QuestionsQuestions© 2001 Dr. B. C. Paul© 2001 Dr. B. C. Paul

Taxes and Project AnalysisTaxes and Project Analysis Showed you how to get cash flows and compute Showed you how to get cash flows and compute

returns but do you really get the money?returns but do you really get the money? Income taxes of 32% - 36%Income taxes of 32% - 36% Sales taxes of 7%Sales taxes of 7% Property taxes of several percent of asset valuesProperty taxes of several percent of asset values An Average American usually works a little over 4 An Average American usually works a little over 4

months/year just to pay taxesmonths/year just to pay taxes We often talk of “Before” and “After” Tax AnalysisWe often talk of “Before” and “After” Tax Analysis

Rates of ReturnRates of Return

Real and NominalReal and Nominal Before tax and After taxBefore tax and After tax And of course combinations Nominal – And of course combinations Nominal –

After Tax Rate of ReturnAfter Tax Rate of Return Need to Make Sure You Are ConsistentNeed to Make Sure You Are Consistent

Doing A Cash Flow With Doing A Cash Flow With TaxesTaxes

Cash flows for Engineering Economic Analysis Cash flows for Engineering Economic Analysis are simply lists of money received and money are simply lists of money received and money spent on a time line showing when the event spent on a time line showing when the event occursoccurs

Adding Taxes to Your Cash FlowAdding Taxes to Your Cash Flow Taxes are an expense – put them on the time-line Taxes are an expense – put them on the time-line

where they occurwhere they occur

Implicit in putting Tax on the time line is that Implicit in putting Tax on the time line is that you know what the amount isyou know what the amount is

Several Types of TaxesSeveral Types of Taxes

Sales TaxesSales Taxes Charged to End User of ProductCharged to End User of Product Normally not charged on raw material inputs Normally not charged on raw material inputs

to a processto a process If make aluminum out of bauxite, bauxite is If make aluminum out of bauxite, bauxite is

normally not taxednormally not taxed Tax occurs whether or not business or Tax occurs whether or not business or

individual is making a “profit”individual is making a “profit” Ie they can make your initial negative cash flows Ie they can make your initial negative cash flows

larger, not just your later positive flows smallerlarger, not just your later positive flows smaller

Types of TaxesTypes of Taxes

Property TaxesProperty Taxes Levied on value of assets (saw some Levied on value of assets (saw some

examples with Herby and Hanna Housing)examples with Herby and Hanna Housing) Also levied whether or not business has a Also levied whether or not business has a

profitprofit Inventory TaxesInventory Taxes

Normally target retailers to get them to move Normally target retailers to get them to move goods not just sit on themgoods not just sit on them

Again levied whether or not business has a Again levied whether or not business has a profitprofit

Income TaxIncome Tax

Normally the single largest biteNormally the single largest bite Bush has tried to cut rate but can still be Bush has tried to cut rate but can still be

36%36% Historically and in some places income tax Historically and in some places income tax

can be 90%can be 90%

Extent to Which a Business pays income Extent to Which a Business pays income taxes varies with how business is set uptaxes varies with how business is set up

Common Business Common Business Arrangements Arrangements (Liability and Tax Issues)(Liability and Tax Issues)

Sole ProprietorshipSole Proprietorship This is your own business (sometimes a jointly This is your own business (sometimes a jointly

owned business with a spouse)owned business with a spouse) Husband-Wife teams may become one entity for tax Husband-Wife teams may become one entity for tax

purposespurposes

Business is handled as part of your personal tax Business is handled as part of your personal tax returnreturn Generally use a series of schedules with a 1040 long Generally use a series of schedules with a 1040 long

formform Profits and losses become part of your personal incomeProfits and losses become part of your personal income

The Sole ProprietorshipThe Sole Proprietorship

Liability IssuesLiability Issues The actions and liabilities of the business The actions and liabilities of the business

are your actions and liabilitiesare your actions and liabilities In Civil action your personal assets may be In Civil action your personal assets may be

seized to satisfy business problemsseized to satisfy business problems

Risk issuesRisk issues You must capitalize the business and You must capitalize the business and

assume all the riskassume all the risk

The PartnershipThe Partnership

Risk MitigationRisk Mitigation The capitalization and skills aspects of the The capitalization and skills aspects of the

business are split between multiple individualsbusiness are split between multiple individuals

For Tax Purposes the earnings and losses For Tax Purposes the earnings and losses of the business split to each individuals of the business split to each individuals taxes - just like a sole proprietorship only taxes - just like a sole proprietorship only earnings or losses are ratios of ownershipearnings or losses are ratios of ownership

The Partnership PerilThe Partnership Peril

Partnership is seldom used todayPartnership is seldom used today Liability problemLiability problem

The actions of any partner or the business The actions of any partner or the business become your actionsbecome your actions Including the personal debts and actions of your Including the personal debts and actions of your

partnerpartner

The CorporationThe Corporation

Incorporation causes the business to Incorporation causes the business to become a separate entity - legally and for become a separate entity - legally and for tax purposestax purposes You have no liability for the actions and You have no liability for the actions and

finances of the business (unless there was finances of the business (unless there was knowing illegal action - pierce the corporate knowing illegal action - pierce the corporate veil)veil)

Board of Directors generally are not liable Board of Directors generally are not liable and company often buys insurance for themand company often buys insurance for them

IncorporatingIncorporating

Incorporating is relatively inexpensiveIncorporating is relatively inexpensive About $50 to fileAbout $50 to file There is a lot of paperwork both to create There is a lot of paperwork both to create

and maintainand maintain Have to decide where to incorporate - Have to decide where to incorporate -

Incorporation is a State legal actionIncorporation is a State legal action have to have some sort of business presence in have to have some sort of business presence in

your state of incorporationyour state of incorporation

Taxing CorporationsTaxing Corporations A corporation fills out its own tax returns A corporation fills out its own tax returns

and pays its own taxesand pays its own taxes Only distributions of earnings are a taxable Only distributions of earnings are a taxable

event for individual owners of corporationsevent for individual owners of corporations Sale of your interest in a corporation will Sale of your interest in a corporation will

usually create a “Capital Gains” event.usually create a “Capital Gains” event.

The Double Tax ProblemThe Double Tax Problem The company pays tax on its profitsThe company pays tax on its profits Then you pay taxes when the distribute them Then you pay taxes when the distribute them

to youto you

Fighting Double TaxationFighting Double Taxation Individuals who incorporate their freelance Individuals who incorporate their freelance

work use Corporation for protectionwork use Corporation for protection Paper work transfers earnings to individual as Paper work transfers earnings to individual as

wages or bonuses so corporation makes little or wages or bonuses so corporation makes little or no moneyno money

Subchapter S Corporations / TrustsSubchapter S Corporations / Trusts Corporations distribute their tax events directly Corporations distribute their tax events directly

to the share-holdersto the share-holders Share holders deal with on their own income taxShare holders deal with on their own income tax

S Type CorporationsS Type Corporations

Attempt to give people what use to be Attempt to give people what use to be possible with partnershipspossible with partnerships

Paper-work is rather restrictivePaper-work is rather restrictive Can make for nightmarish individual tax Can make for nightmarish individual tax

returnsreturns There are limits on what S Type can doThere are limits on what S Type can do

Corporate Veil may not be quite as Corporate Veil may not be quite as effectiveeffective

Income TaxIncome Tax

For most businesses and individuals the For most businesses and individuals the single largest bitesingle largest bite

As in cash flowsAs in cash flows Income is Gross Revenue taken inIncome is Gross Revenue taken in minus expenses necessary to obtain itminus expenses necessary to obtain it

Result is Net Income as seen in many Result is Net Income as seen in many cash flowscash flows Why not just have government take its cut?Why not just have government take its cut?

Is Net Income Really Is Net Income Really IncomeIncome

Business Earnings - Operating ExpensesBusiness Earnings - Operating Expenses But do real businesses just pop in out of But do real businesses just pop in out of

nowhere and then run?nowhere and then run? Our cash flows show that there are really Our cash flows show that there are really

necessary investments to make incomenecessary investments to make income

Tax code recognized the need to distinguish Tax code recognized the need to distinguish between real growth of wealth available for between real growth of wealth available for consumption and defraying prior investments consumption and defraying prior investments in making the moneyin making the money

Deducting the Cost of Deducting the Cost of InvestmentInvestment DepreciationDepreciation

Equipment and real buildings are worn out by Equipment and real buildings are worn out by productionproduction

Depreciation allows the “wear out” factor on Depreciation allows the “wear out” factor on an asset to be deducted from the income (if its an asset to be deducted from the income (if its not replaced what will happen to production)not replaced what will happen to production)

AmortizationAmortization Non physical assets also have a useful lifeNon physical assets also have a useful life Example a patent on a new medicineExample a patent on a new medicine

(patents expire after a number of years)(patents expire after a number of years)

Deducting the Deducting the InvestmentInvestment

DepletionDepletion Some assets are a natural resource that Some assets are a natural resource that

costs money to isolate and put into a costs money to isolate and put into a recoverable form but is neither a machine recoverable form but is neither a machine nor an intangible rightnor an intangible right

ExamplesExamples An oil fieldAn oil field A mineral depositA mineral deposit

True Usable DollarsTrue Usable Dollars

Gross RevenueGross Revenue Minus Operating ExpensesMinus Operating Expenses Minus DepreciationMinus Depreciation Minus AmortizationMinus Amortization Minus DepletionMinus Depletion Equals true usable dollars - Now the Equals true usable dollars - Now the

Government takes its cutGovernment takes its cut

Taxes as a means of Taxes as a means of Shaping Social PolicyShaping Social Policy

Government also uses special tax treatment Government also uses special tax treatment as a way to encourage people to do things as a way to encourage people to do things considered to be for the good of societyconsidered to be for the good of society Tax credits for educationTax credits for education Tax credits for health insurance or pension plans for Tax credits for health insurance or pension plans for

employeesemployees Investment tax credits for people who invest in Investment tax credits for people who invest in

technologies believed to benefit the countrytechnologies believed to benefit the country Tax free bonds for public works projects (interest is not Tax free bonds for public works projects (interest is not

taxed as income)taxed as income)

Non special credit Non special credit approachesapproaches

Generally keeping money moving and Generally keeping money moving and equipment and infrastructure current is equipment and infrastructure current is considered goodconsidered good Government allows certain long term investments to be Government allows certain long term investments to be

treated as an expense even though they last for years treated as an expense even though they last for years (computers and office equipment)(computers and office equipment)

Government allows for faster depreciation/AmortizationGovernment allows for faster depreciation/Amortization Done by fudging asset lives downDone by fudging asset lives down Done by allowing more depreciation early - less lateDone by allowing more depreciation early - less late

More Incentive More Incentive ApproachesApproaches

DepletionDepletion Allowing depletion to be based on a Allowing depletion to be based on a

percentage of the asset value sold rather percentage of the asset value sold rather than what was actually invested in the findthan what was actually invested in the find More key or riskier the natural resource is to find More key or riskier the natural resource is to find

or develop (or the more key it is to national or develop (or the more key it is to national interest) the greater the percentageinterest) the greater the percentage

Fear of Giving Away the Fear of Giving Away the StoreStore

One hand says that Government should One hand says that Government should stimulate private investmentstimulate private investment

The other hand says that these are all just The other hand says that these are all just breaks for the wealthy (even though they breaks for the wealthy (even though they may be the only ones who can make the big may be the only ones who can make the big investments)investments)

Result is a series of anti-tax breaks designed Result is a series of anti-tax breaks designed to take back what government may have to take back what government may have given.given.

Breaks Against the RichBreaks Against the Rich

Progressive Income TaxProgressive Income Tax More you make the higher your tax rateMore you make the higher your tax rate

Around 75% of the income to reach the Poverty Line Around 75% of the income to reach the Poverty Line are not taxed at allare not taxed at all

Brackets (just got rearranged)Brackets (just got rearranged) Basic living only about 10-12%Basic living only about 10-12% Middle Income around 20%Middle Income around 20% Wealthy levels 28-32%Wealthy levels 28-32%

Businesses are usually synthetic individualsBusinesses are usually synthetic individuals Most firms doing big engineering are mostly in Most firms doing big engineering are mostly in

“Wealthy” tax bracket“Wealthy” tax bracket

More Anti-BreaksMore Anti-Breaks RecaptureRecapture

Many special tax credits have to be deducted Many special tax credits have to be deducted from future deductionsfrom future deductions

Property that got a special benefit have to add Property that got a special benefit have to add back into or reduce deductions if convertedback into or reduce deductions if converted

ExampleExample Mining Companies can deduct tunnels to develop a Mining Companies can deduct tunnels to develop a

mineral deposit as an expense even though they mineral deposit as an expense even though they last for yearslast for years

If they do that the money they deducted will be taken If they do that the money they deducted will be taken away from future depletion allowanceaway from future depletion allowance

You Can’t Duck Your You Can’t Duck Your TaxesTaxes Alternative Minimum TaxAlternative Minimum Tax

Have to do your taxes twice - once with your Have to do your taxes twice - once with your deductions and breaksdeductions and breaks

Then do them a second time with only very real Then do them a second time with only very real conservatively interpreted deductionsconservatively interpreted deductions

Get two Taxable IncomesGet two Taxable Incomes Use the regular tax brackets on regular income tax to Use the regular tax brackets on regular income tax to

see how much you owesee how much you owe Use a special low tax rate on your alternative Use a special low tax rate on your alternative

minimum tax incomeminimum tax income

Pay the larger of the two tax billsPay the larger of the two tax bills

Building Our Tax Building Our Tax StructureStructure

The tax structure measures income The tax structure measures income “somewhat accurately” and taxes it“somewhat accurately” and taxes it It allows operating expenses to be deducted It allows operating expenses to be deducted

from gross revenuefrom gross revenue It allows our capital investments to be It allows our capital investments to be

deducted over time through Depreciation/ deducted over time through Depreciation/ Amortization and DepletionAmortization and Depletion

The Tax StructureThe Tax Structure Our Tax Code attempts to promote good Our Tax Code attempts to promote good

Social PolicySocial Policy Provides advantages to encourage people to Provides advantages to encourage people to

invest in the economyinvest in the economy special credits and accelerated special credits and accelerated

Depreciation/Amortization/DepletionDepreciation/Amortization/Depletion

Requires those who have more to “give” moreRequires those who have more to “give” more Progressive taxProgressive tax Recapture of benefitsRecapture of benefits Alternative Minimum Tax (hard to deduct away all Alternative Minimum Tax (hard to deduct away all

your income)your income)

The Problem of Inflation The Problem of Inflation and Long Term and Long Term InvestmentInvestment If I buy something for $47,000 and sell it for If I buy something for $47,000 and sell it for

$54,000 did I make money?$54,000 did I make money? The arithmetic clearly shows I saw a profit which The arithmetic clearly shows I saw a profit which

should be taxableshould be taxable

What if the sale was 10 years after the What if the sale was 10 years after the purchase and it now takes $56,000 to have purchase and it now takes $56,000 to have the same buying power as $47,000 10 years the same buying power as $47,000 10 years agoago In long term investments numeric profit and new In long term investments numeric profit and new

income are two different thingsincome are two different things

The Long Term Investment The Long Term Investment DilemmaDilemma

Obvious way around problem is indexing to Obvious way around problem is indexing to inflationinflation Until Bush’s latest “tax-cut” not got inflation Until Bush’s latest “tax-cut” not got inflation

indexing into tax codeindexing into tax code Alternative method is what is called “Capital Alternative method is what is called “Capital

Gains”Gains” Money coming from redemption of long held Money coming from redemption of long held

investments is taxed at a lower rate than income from investments is taxed at a lower rate than income from a short fast return activitya short fast return activity

Also promotes long term investment with what might Also promotes long term investment with what might be a tax break (might also be getting shafted)be a tax break (might also be getting shafted)

Who Gets Taxed?Who Gets Taxed?

Anyone and anything the IRS can get its Anyone and anything the IRS can get its fangs intofangs into

Individuals pay income taxIndividuals pay income tax Businesses also pay income taxBusinesses also pay income tax

How business income tax is handled varies How business income tax is handled varies with the way the company is set-upwith the way the company is set-up

Doing Rudimentary After Doing Rudimentary After Tax AnalysisTax Analysis

Add up the Gross Revenue coming into the Add up the Gross Revenue coming into the company as a result of the project.company as a result of the project.

Add up the cost of producing the goodsAdd up the cost of producing the goods Common dilemma - how do you account for Common dilemma - how do you account for

expenses, inventory, earningsexpenses, inventory, earnings Leads to several different accounting methodsLeads to several different accounting methods

Simplest is cash - money coming in is an earning - money Simplest is cash - money coming in is an earning - money going out is an expense (money in inventory is a black hole)going out is an expense (money in inventory is a black hole)

People get whole degrees in how to account for and track People get whole degrees in how to account for and track events - not going to go into detail hereevents - not going to go into detail here

Income and ExpenseIncome and Expense

Another problem is assets that last for a Another problem is assets that last for a period of timeperiod of time A true expense is actually consumed in A true expense is actually consumed in

producing the goodsproducing the goods Machines, computers, office furniture, race Machines, computers, office furniture, race

horses are worn by production, but not horses are worn by production, but not consumed in the yearconsumed in the year These goods must generally be “capitalized”These goods must generally be “capitalized” Means even though the money goes out now the Means even though the money goes out now the

reduction in taxable income is not immediatereduction in taxable income is not immediate

The Cook BooksThe Cook Books

Accounting decisions will determine how you handle Accounting decisions will determine how you handle goods in inventorygoods in inventory There are rules about switching or what you must do when There are rules about switching or what you must do when

you elect an accounting methodyou elect an accounting method

Tax laws and SEC rules tell what types of Tax laws and SEC rules tell what types of expenditures must be “capitalized” and what can be expenditures must be “capitalized” and what can be expensedexpensed For taxes generally expense everything you canFor taxes generally expense everything you can Produce the most glowing now profit for share holder Produce the most glowing now profit for share holder

reports - capitalize all you canreports - capitalize all you can

Result is many sets of booksResult is many sets of books

Doing the TaxesDoing the Taxes

Regular TaxesRegular Taxes IncomeIncome Minus expensesMinus expenses Minus expensing of Minus expensing of

Capital Investments Capital Investments (Preference Item)(Preference Item)

Alternative Minimum Alternative Minimum TaxTax IncomeIncome Minus expensesMinus expenses

The Step as an IndividualThe Step as an Individual

IncomeIncome Wages, Salaries, tipsWages, Salaries, tips InterestInterest

list Tax exempt interest separatelylist Tax exempt interest separately

Alimony/ Unemployment / SS / PensionAlimony/ Unemployment / SS / Pension (State income taxes may allow exclusion of State (State income taxes may allow exclusion of State

Public service pensions)Public service pensions)

Capital Gains / LossesCapital Gains / Losses Business Gains / LossesBusiness Gains / Losses

Sched C Business / Sched E Rental-Partnership-Sched S / Sched F Sched C Business / Sched E Rental-Partnership-Sched S / Sched F FarmingFarming

The Capitalization The Capitalization QuestionQuestion

Business Purchases that serve over Business Purchases that serve over time- rather than being consumed by time- rather than being consumed by immediate use or sale are “Capitalized”immediate use or sale are “Capitalized” They are taken off income over timeThey are taken off income over time

IRS dictates what must be capitalized IRS dictates what must be capitalized and over how longand over how long

Generally most desirable to expense Generally most desirable to expense things - this is done under Section 179things - this is done under Section 179

Section 179Section 179 Need some definitionsNeed some definitions

Tangible means can be touched - exists in Tangible means can be touched - exists in physical formphysical form

Real Property means permanently attached Real Property means permanently attached and located (buildings etc)and located (buildings etc)

Personal Property means not permanently Personal Property means not permanently attached (machines etc)attached (machines etc)

Mostly important to small businessMostly important to small business Can expense up to $20,000 of personal Can expense up to $20,000 of personal

propertyproperty

179 Deductions179 Deductions

Office equipmentOffice equipment Equipment used in manufactureEquipment used in manufacture Storage tanks for oilStorage tanks for oil LivestockLivestock Animal Sheds and GreenhousesAnimal Sheds and Greenhouses Research FacilitiesResearch Facilities

Limiting 179 DeductionsLimiting 179 Deductions

Dollar limit on deductionDollar limit on deduction Also cannot exceed Taxable Income from Also cannot exceed Taxable Income from

the business (ie can’t use to generate the business (ie can’t use to generate loss on your business)loss on your business) Respond by either splitting equipment between Depreciation Respond by either splitting equipment between Depreciation

and Expensingand Expensing Or can carry over as a 179 loss next yearOr can carry over as a 179 loss next year

if you don’t make money you can’t undo the electionif you don’t make money you can’t undo the election If sell or switch to less 50% business use have to add previous If sell or switch to less 50% business use have to add previous

179 back to your income179 back to your income (Recapture provisions) (Recapture provisions)

Depreciation + Depreciation + AmortizationAmortization

If the item cannot expense goes into If the item cannot expense goes into depreciation/amortizationdepreciation/amortization

IRS Life ClassesIRS Life Classes 3 Year Property3 Year Property

Tractor Trailers/ Rent to Own Property/ Race HorsesTractor Trailers/ Rent to Own Property/ Race Horses 5 Year Property5 Year Property

Auto’s busses and trucks (if you take mileage deduction you Auto’s busses and trucks (if you take mileage deduction you cannot depreciate your business car)cannot depreciate your business car)

Research equipmentResearch equipment Office Equipment, and computersOffice Equipment, and computers CattleCattle

Depreciation LivesDepreciation Lives

7 year property7 year property FurnitureFurniture Rugs in rental propertyRugs in rental property AppliancesAppliances Railroad trackRailroad track Anything else not specified elsewhereAnything else not specified elsewhere

10 year property10 year property Barges and tugsBarges and tugs Greenhouses and Animal ShedsGreenhouses and Animal Sheds Vineyards and Fruit treesVineyards and Fruit trees

Depreciation LivesDepreciation Lives

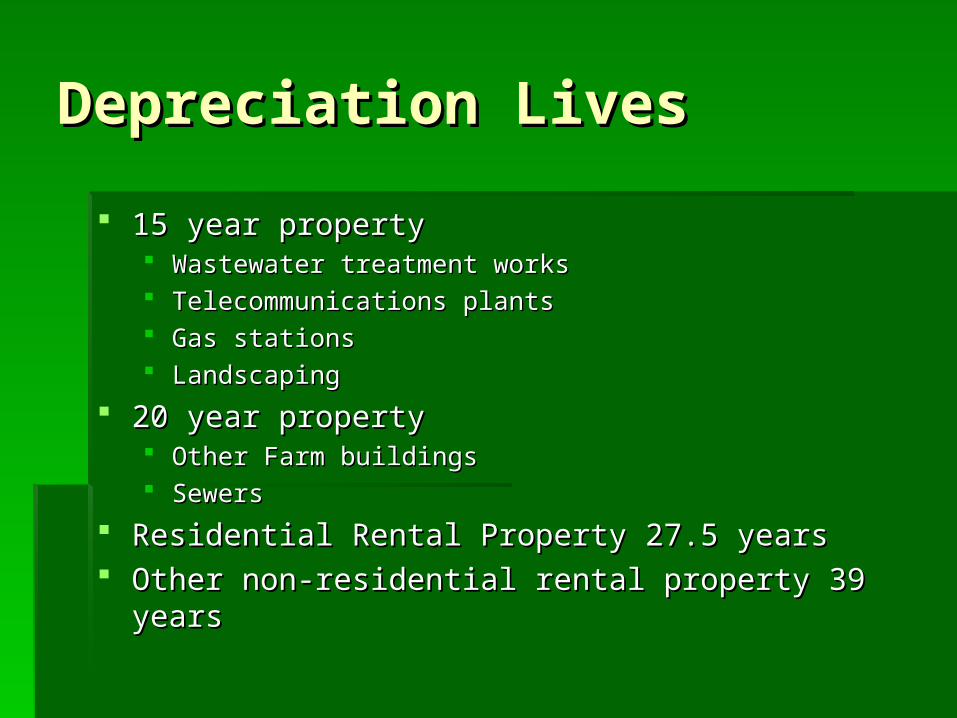

15 year property15 year property Wastewater treatment worksWastewater treatment works Telecommunications plantsTelecommunications plants Gas stationsGas stations LandscapingLandscaping

20 year property20 year property Other Farm buildingsOther Farm buildings SewersSewers

Residential Rental Property 27.5 yearsResidential Rental Property 27.5 years Other non-residential rental property 39 yearsOther non-residential rental property 39 years

DepreciationDepreciation Depreciation subtracts a portion of the Depreciation subtracts a portion of the

cost of a “capitalized” item from income cost of a “capitalized” item from income each year over the life of the itemeach year over the life of the item The value of the item to be depreciated is The value of the item to be depreciated is

called the “Cost Basis”called the “Cost Basis” Example - Example - Civilized Engineers Incorporated plans to Civilized Engineers Incorporated plans to

build two 110 story residential rental buildings equipped build two 110 story residential rental buildings equipped with anti-aircraft guns fire proof parachutes and dust with anti-aircraft guns fire proof parachutes and dust masks. The high class apartments will bring in 301 masks. The high class apartments will bring in 301 million dollars a year. 161 mi1lion will be spent on debt million dollars a year. 161 mi1lion will be spent on debt service, and 40 million on maintenance and security.service, and 40 million on maintenance and security.

DepreciationDepreciation

Calculating Civilized Engineers Gross RevenueCalculating Civilized Engineers Gross Revenue Gross Revenue $301,000,000Gross Revenue $301,000,000 Minus interest expenseMinus interest expense $140,000,000 (interest at 7% first year $140,000,000 (interest at 7% first year

on a 2 billion dollar loan)on a 2 billion dollar loan) Minus security and maintenance $40,000,000 (ignore that some Minus security and maintenance $40,000,000 (ignore that some

of the maintenance supplies are really depreciable)of the maintenance supplies are really depreciable) Net Income is $121,000,000Net Income is $121,000,000

What is the Depreciation Life of a Residential What is the Depreciation Life of a Residential Rental Building?Rental Building?

27.5 Years27.5 Years (WTC 1973-2001)(WTC 1973-2001)

Calculating DepreciationCalculating Depreciation

Simplest Method of Depreciation is Straight Simplest Method of Depreciation is Straight LineLine FormulaFormula Basis*(1/n) = DepreciationBasis*(1/n) = Depreciation

Suppose Basis is 2.5 billion dollarsSuppose Basis is 2.5 billion dollars $2,500,000,000*(1/27.5) = $90,910,000$2,500,000,000*(1/27.5) = $90,910,000

Net income $120,000,000Net income $120,000,000 Minus Depreciation $90,910,000Minus Depreciation $90,910,000

Taxable Income = $29,090,000Taxable Income = $29,090,000

Common Alternate Common Alternate Depreciation MethodsDepreciation Methods

Declining Balance MethodDeclining Balance Method FormulaFormula Initial Depreciation = Basis * Declining Initial Depreciation = Basis * Declining

Balance Rate/nBalance Rate/n Adjusted Basis = Basis - Previous Adjusted Basis = Basis - Previous

DepreciationDepreciation Subsequent Depreciation - Adjusted Basis * Subsequent Depreciation - Adjusted Basis *

Declining Balance Rate/nDeclining Balance Rate/n

Terms in the Declining Terms in the Declining Balance MethodBalance Method

Declining Balance Rate says how fast it Declining Balance Rate says how fast it depreciatesdepreciates Common rates Common rates

Double Declining Balance is 200% or 2 for rate in Double Declining Balance is 200% or 2 for rate in the formulathe formula

150% or 1.5 is also common150% or 1.5 is also common

ApplyApply $2,500,000*(1.5/27.5) = $136,363,636$2,500,000*(1.5/27.5) = $136,363,636 Adjusted Basis = $2,500,000,000-$136,363,636Adjusted Basis = $2,500,000,000-$136,363,636

$2,363,636,364$2,363,636,364

Next Years DepreciationNext Years Depreciation

Work with adjusted basisWork with adjusted basis Year 2 depreciation $2,363,636,364*(1.5/27.5)= Year 2 depreciation $2,363,636,364*(1.5/27.5)=

$128,925,620$128,925,620 New Adjusted basisNew Adjusted basis

$2,363,636,364 - $128,925,620 = $2,234,710,744$2,363,636,364 - $128,925,620 = $2,234,710,744

Formula repeats in Future YearsFormula repeats in Future Years Minor problem - the building never Minor problem - the building never

depreciates all the way because basis keeps depreciates all the way because basis keeps changingchanging

Solving the ProblemSolving the Problem

Problem is solved by switching methodsProblem is solved by switching methods Calculate straight line depreciation on the Calculate straight line depreciation on the

adjusted basisadjusted basis over the over the remaining remaining depreciation lifedepreciation life

When Straight Line does better than the When Straight Line does better than the declining balance method switchdeclining balance method switch

The result is an asset that will depreciate in The result is an asset that will depreciate in the allotted time.the allotted time.

Illustrating the SwitchIllustrating the SwitchLife 27.5 Rate 1.5Year Basis Declining Balance Straight Line

1 2500000000 136363636.4 90909090.912 2363636364 128925619.8 89193825.043 2234710744 121893313.3 87635715.444 2112817431 115244587.1 86237446.145 1997572843 108958518.7 85003099.726 1888614325 103015326.8 83938414.437 1785598998 97396308.97 83051116.188 1688202689 92083783.03 82351350.689 1596118906 87061031.23 81852251.58

10 1509057875 82312247.71 81570695.9311 1426745627 77822488.74 81528321.5412 1345217305 73375489.38 81528321.5413 1263688984 68928490.03 81528321.5414 1182160662 64481490.67 81528321.5415 1100632341 60034491.31 81528321.5416 1019104019 55587491.96 81528321.5417 937575698 51140492.6 81528321.5418 856047376 46693493.24 81528321.54

Units of Production Units of Production DepreciationDepreciation

Walley’s Widget Factory has purchased a Walley’s Widget Factory has purchased a Thingamabob machine to align widgets. Thingamabob machine to align widgets. The machine cost $100,000 and will align The machine cost $100,000 and will align 1,000,000 widgets over its life-time. This 1,000,000 widgets over its life-time. This year the Widget Factory produced year the Widget Factory produced 200,000 widgets. What is Walley’s 200,000 widgets. What is Walley’s depreciationdepreciation

$100,000 * 200,000/1,000,000 = $20,000$100,000 * 200,000/1,000,000 = $20,000

ACRS and MACRSACRS and MACRS

Accelerated Cost Recovery System / Accelerated Cost Recovery System / Modified Accelerated Cost Recovery Modified Accelerated Cost Recovery SystemSystem IRS specified rate and lifeIRS specified rate and life Turns out to be Declining Balance Switching Turns out to be Declining Balance Switching

to Straight Lineto Straight Line Which tax law went in under and property class Which tax law went in under and property class

determines what the declining balance rate isdetermines what the declining balance rate is

Declining Balances and Declining Balances and MACRSMACRS

Things that use 200% Declining Balance switching Things that use 200% Declining Balance switching to Straight Lineto Straight Line 3, 5, 7, and 10 year property not used on a farm3, 5, 7, and 10 year property not used on a farm Provides most aggressive early tax deductions - usually Provides most aggressive early tax deductions - usually

choice where boosting IRR is an objective or of interestchoice where boosting IRR is an objective or of interest

Things that use 150% Declining Balance Things that use 150% Declining Balance Switching to Straight LineSwitching to Straight Line 15 and 20 year property15 and 20 year property All personal property used on farmsAll personal property used on farms Any 3, 5, 7, 10 year year property where you elect to Any 3, 5, 7, 10 year year property where you elect to

use a less aggressive depreciationuse a less aggressive depreciation

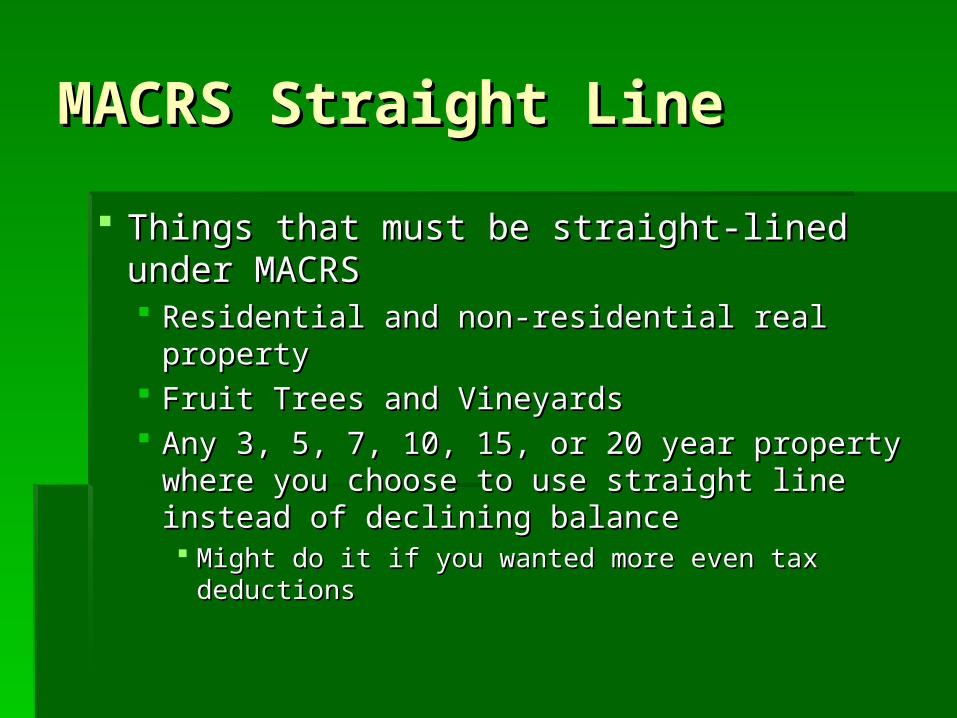

MACRS Straight LineMACRS Straight Line

Things that must be straight-lined under Things that must be straight-lined under MACRSMACRS Residential and non-residential real propertyResidential and non-residential real property Fruit Trees and VineyardsFruit Trees and Vineyards Any 3, 5, 7, 10, 15, or 20 year property Any 3, 5, 7, 10, 15, or 20 year property

where you choose to use straight line where you choose to use straight line instead of declining balanceinstead of declining balance Might do it if you wanted more even tax Might do it if you wanted more even tax

deductionsdeductions

Mid Time Line ProblemsMid Time Line Problems

Taxes are settled on an annual basisTaxes are settled on an annual basis Property can go into service anytime in yearProperty can go into service anytime in year Where do I put the cash - had that problem Where do I put the cash - had that problem

with cash flowswith cash flows Silent convention is costs at beginning earning Silent convention is costs at beginning earning

at endat end

IRS lets choose a Mid Year, Mid Quarter, IRS lets choose a Mid Year, Mid Quarter, Mid Month depending on type of propertyMid Month depending on type of property

Impact of Mid Something Impact of Mid Something ConventionConvention

Property went into service at the middle of Property went into service at the middle of somethingsomething if went in in Marchif went in in March

Middle of third monthMiddle of third month Won’t get first years full depreciation - get a Won’t get first years full depreciation - get a

fraction according to how much of the time you fraction according to how much of the time you spent.spent.

Could also use Mid Quarter - Middle First QuarterCould also use Mid Quarter - Middle First Quarter Could use Mid Year Convention Middle of first yearCould use Mid Year Convention Middle of first year

Mid Something Mid Something Convention in ActionConvention in Action

Say we used Mid Year Convention on Say we used Mid Year Convention on our 110 Story Apartment Buildingour 110 Story Apartment Building

First Year We calculated $136,363,636First Year We calculated $136,363,636 But now we only get half of thatBut now we only get half of that

$68,181,818 for first year$68,181,818 for first year This will effect adjusted basis in remaining This will effect adjusted basis in remaining

yearsyears

Applying Depreciation for Applying Depreciation for Tax LiabilityTax Liability

Doing Civilized Doing Civilized Engineers Inc.Engineers Inc. Gross Revenue Gross Revenue

$301,000,000$301,000,000 Minus Interest Minus Interest

$140,000,000$140,000,000 Minus Security and Maint Minus Security and Maint

$40,000,000$40,000,000 27.5 SL depreciation27.5 SL depreciation

$90,910,000$90,910,000

Taxable Income Taxable Income $30,090,000$30,090,000

Cash ResultCash Result Gross Revenue Gross Revenue

$301,000,000$301,000,000 Minus Payments Minus Payments

$161,000,000$161,000,000 Minus Security and Minus Security and

Maint $40,000,000Maint $40,000,000 Cash flow Cash flow

$100,000,000$100,000,000

Alternative Minimum TaxAlternative Minimum Tax

Have to calculate taxable income without Have to calculate taxable income without “preference items”“preference items” Special deductions such as the 179 Special deductions such as the 179

expensing of capital propertyexpensing of capital property Declining Balance and shorter depreciation Declining Balance and shorter depreciation

lives are also a preference itemlives are also a preference item We need to Check Alternative Minimum Tax for We need to Check Alternative Minimum Tax for

Civilized Engineers Inc.Civilized Engineers Inc.

Depreciation Calculations Depreciation Calculations for ADS on Alternative for ADS on Alternative Minimum TaxMinimum Tax

All depreciation is straight lineAll depreciation is straight line Lives are longerLives are longer

Rent to own property 4 years (was 3)Rent to own property 4 years (was 3) Computer/ Communications / Medical Computer/ Communications / Medical

Equipment 5 years (was 5)Equipment 5 years (was 5) Personal Property not specified elsewhere Personal Property not specified elsewhere

12 years (was 5, 7, little 10)12 years (was 5, 7, little 10)

Doing ADS DepreciationDoing ADS Depreciation

Returning to our Rental Sky ScraperReturning to our Rental Sky Scraper $2,500,000,000 * (1/40) = $62,500,000 $2,500,000,000 * (1/40) = $62,500,000

under ADSunder ADS Under the GDS (standard) portion of Under the GDS (standard) portion of

MACRSMACRS $2,500,000,000 * (1/27.5) = $90,910,000$2,500,000,000 * (1/27.5) = $90,910,000

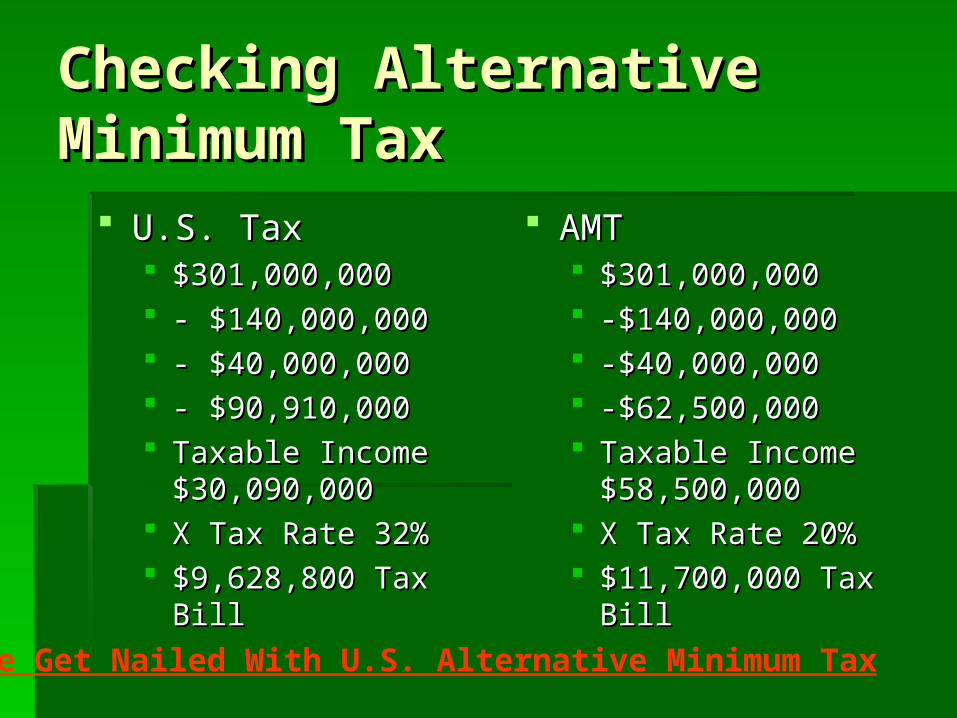

Checking Alternative Checking Alternative Minimum TaxMinimum Tax

U.S. TaxU.S. Tax $301,000,000$301,000,000 - $140,000,000- $140,000,000 - $40,000,000- $40,000,000 - $90,910,000- $90,910,000 Taxable Income Taxable Income

$30,090,000$30,090,000 X Tax Rate 32%X Tax Rate 32% $9,628,800 Tax Bill$9,628,800 Tax Bill

AMTAMT $301,000,000$301,000,000 -$140,000,000-$140,000,000 -$40,000,000-$40,000,000 -$62,500,000-$62,500,000 Taxable Income Taxable Income

$58,500,000$58,500,000 X Tax Rate 20%X Tax Rate 20% $11,700,000 Tax Bill$11,700,000 Tax Bill

We Get Nailed With U.S. Alternative Minimum Tax

The Tax Loss ProblemThe Tax Loss Problem Suppose our Business had been such that Suppose our Business had been such that

we had really been depreciating with 150% we had really been depreciating with 150% Declining Balance instead of straight lineDeclining Balance instead of straight line $301,000,000$301,000,000 -$140,000,000 interest-$140,000,000 interest -$40,000,000 expenses-$40,000,000 expenses -$136,364,000 depreciation-$136,364,000 depreciation Taxable Income -$15,364,000Taxable Income -$15,364,000

Company may have a positive cash flow Company may have a positive cash flow but a tax lossbut a tax loss No - There is no EIC for corporationsNo - There is no EIC for corporations

The Corporate Structure The Corporate Structure ProblemProblem

Large corporations can take tax losses in Large corporations can take tax losses in one division into over-all booksone division into over-all books Provided company as whole is tax profitable, Provided company as whole is tax profitable,

a division may provide an instant reduction a division may provide an instant reduction in tax liabilityin tax liability

If parent company cannot take deduction If parent company cannot take deduction now then loss must be “carried forward”now then loss must be “carried forward”

Tax Loss Carried ForwardTax Loss Carried Forward Next YearNext Year

Gross Income $301,000,000Gross Income $301,000,000 - Interest -$137,000,000- Interest -$137,000,000 - Expenses -$ 40,000,000- Expenses -$ 40,000,000 - Depreciation -$128,926,000- Depreciation -$128,926,000 - Tax Loss CF -$ 15,364,000- Tax Loss CF -$ 15,364,000 Taxable Income - $19,993,000Taxable Income - $19,993,000

(of course there is also the AMT problem (of course there is also the AMT problem where company may be carrying losses where company may be carrying losses forward and paying tax both) forward and paying tax both)

Tax Loss Carried ForwardTax Loss Carried Forward Companies may develop fairly substantial Companies may develop fairly substantial

tax loss on new project start uptax loss on new project start up being able to cash into the larger corporate kitty being able to cash into the larger corporate kitty

can strengthen project economicscan strengthen project economics

Building large tax losses can be dangerousBuilding large tax losses can be dangerous may make you a bargain “take-over” target for may make you a bargain “take-over” target for

someonesomeone Could also be someones corporate strategy (build Could also be someones corporate strategy (build

and sell out)and sell out)

Corporate Central IssuesCorporate Central Issues

Linking Divisions of Companies so they Linking Divisions of Companies so they can deduct each others tax losses often can deduct each others tax losses often creates liability issuescreates liability issues

Companies may try to create separate Companies may try to create separate divisions as “firewalls”divisions as “firewalls” Lawsuit or other liability often cannot pass Lawsuit or other liability often cannot pass

from one company to anotherfrom one company to another GM and SaturnGM and Saturn

Seeing some use it to avoid pension liabilitySeeing some use it to avoid pension liability

AmortizationAmortization Depreciation for intangible stuffDepreciation for intangible stuff

Patents and CopyrightsPatents and Copyrights Designs and PatternsDesigns and Patterns Customer and Contact ListsCustomer and Contact Lists FranchisesFranchises Non-Competition AgreementsNon-Competition Agreements Specialized Computer SoftwareSpecialized Computer Software

(Over the counter Software Depreciates in 3 years)(Over the counter Software Depreciates in 3 years)

Straight Line over 15 yearsStraight Line over 15 years

Things with No Things with No DepreciationDepreciation

Land does not depreciateLand does not depreciate Business “Goodwill” not considered a Business “Goodwill” not considered a

depreciable or amortizable assetdepreciable or amortizable asset Consumer Assets for Individual taxpayersConsumer Assets for Individual taxpayers

Your car (can depreciate a portion if used for Your car (can depreciate a portion if used for business and personal)business and personal)

Your house (if rented could depreciate)Your house (if rented could depreciate) hitch - you get tax free capital gains on your homehitch - you get tax free capital gains on your home

Related Documents