George Alogoskoufis, Interna’onal Macroeconomics, 2016 The Monetary Approach to Interna8onal Macroeconomics Professor George Alogoskoufis Athens University of Economics and Business 1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

TheMonetaryApproachtoInterna8onal

MacroeconomicsProfessorGeorgeAlogoskoufis

AthensUniversityofEconomicsandBusiness

1

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

TheMonetaryApproach• The monetary approach is one of the central pillars of international

macroeconomics. Its point of departure is the so called monetary model, which identifies the factors affecting long-term nominal exchange rates. The monetary model was originally used as a framework of analysis of the balance of payments in a fixed exchange rate regime (Frenkel and Johnson 1976), and then as a framework for analysis of the determination of nominal exchange rates in a flexible exchange rate regime (Frenkel and Johnson 1978).

• The basic monetary approach assumes that there is full flexibility in prices and focuses on the equilibrium conditions in the money market and the international foreign exchange markets. Although this is basically an ad hoc model, like the Mundell-Fleming model, many of its theoretical properties are confirmed by inter-temporal optimization models in monetary economies (see Lucas 1982).

2

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

PurchasingPowerParity• A key component of the monetary approach is the concept of

purchasing power parity. The idea originated from the early 19th century, and one can find it in the writings of Ricardo. The idea was revived in the early 20th century by Cassel (1921).

• The approach of Cassel starts with the observation that the exchange rate is the relative price of two currencies. Since the purchasing power of the domestic currency is 1/P, where P is the domestic price level and the purchasing power of the foreign currency is 1/P*, where P* is the foreign price level, the relative price of two currencies should reflect their relative purchasing power. In this case, it should follow that,

3

S = P / P* s = p − p*

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

PurchasingPowerParityandtheISCurve

ThetheoryofpurchasingpowerparitycanbederivedfromtheIScurveofanopeneconomy,whentheelas8cityofaggregatedemandwithrespecttotherealexchangeratetendstoinfinity.

Asδtendstoinfinity,aggregatedemandwillbefiniteonlyifthelogarithmoftherealexchangerates+p*-ptendstozero,thatisifpurchasingpowerparityissa8sfied.

Iftheelas8cityofaggregatedemandwithrespecttotherealexchangerateisveryhigh,thentherecannotbelargedevia8onsbetweendomes8candinterna8onalprices,expressedinacommoncurrency,asevensmalldevia8onswouldproducelargechangesinaggregatedemand.Effec8vely,thetheoryofpurchasingpowerparityassertsthatdomes8candforeigngoodsareperfectsubs8tutes.

4

y = δ (s + p*− p)+ γ y −σ i + g

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

ThePurchasingPowerParityApproach

• Thepurchasingpowertheoryapproachessen8allyrequiresthattherealexchangerateshouldbeconstant.However,thispredic8onisgenerallyrejectedbyempiricalevidence.Realexchangeratesarenotconstant,butdisplayconsiderablefluctua8ons.Moreover,thereseemstobeastrongposi8vecorrela8onbetweennominalandrealexchangerates,whichisnotconsistentwithpurchasingpowerparity.

• Avariantofthisapproach,whichwewillexaminebelow,allowsfluctua8onsintherealexchangerateandtreatspurchasingpowerparityasatheorydeterminingthelong-termrealexchangerate.

• Inanycase,forthemonetarymodelwithfullyflexibleprices,theassump8onofpurchasingpowerparityiscentral.

5

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

TheMonetaryApproachtotheBalanceofPayments

• Themonetaryapproachtothebalanceofpayments(FrenkelandJohnson1976),usesthemonetarymodeltoexplainthebehaviorofthebalanceofpayments,underaregimeoffixedexchangerates.

• Considerasmallopeneconomythatmaintainsaconstantexchangeratethroughinterven8onsofitscentralbankintheforeignexchangemarket.

• Themoneysupplyisdeterminedby,

6

M = µB = µ(Bf + Bd )

• whereΜdenotesthemoneysupply,Bthemonetarybase(highpoweredmoney),μthemul8plierofthemonetarybase,Bfnetforeignexchangereservesofthecentralbank,andBdnetdomes8ccreditofthecentralbanktothepublicandthebankingsystem.

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

EquilibriumintheMoneyMarketunderFixedExchangeRates

7

m = θbf + (1−θ )bd

m − p = φy − λi

i = i*

s_= p − p*

m = s_+ p*+φy − λi*

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

MainPredic8onsoftheMonetaryApproachtotheBalanceofPayments

• Adevalua8on(increaseins),ariseintheinterna8onalpricelevel,anincreaseindomes8coutputandincomeandareduc8onininterna8onalnominalinterestrates,increasethedemandformoney,and,forgivendomes8ccredit,causeincreasesinforeignreserves.Theincreaseinforeignexchangereserveswilloccurthroughsurplusesinthebalanceofpayments.

• Ontheotherhand,ifthereisanexpansionindomes8ccreditexpansion,theonlyresultwillbealossofnetforeignexchangereserves,asthedemandformoneywillnotchange.Thus,adomes8ccreditexpansionwillcauseadeficitinthebalanceofpayments.

8

bf =1θ

s_+ p*+φy − λi*−(1−θ )bd

⎡⎣⎢

⎤⎦⎥

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

TheConceptoftheBalanceofPaymentsRelevantfortheMonetaryApproach

• Themonetaryapproachtothebalanceofpaymentsisnotconcernedwiththedetermina8onofthecurrentaccount,buttheso-calledofficialbalance.

• Officialbalanceisnoneotherthanthesumofthecurrentaccountandthecapitalaccount,withouttakingaccountofchangesinthenetforeignexchangereservesofthecentralbank.

• Onecouldcallthemonetaryapproachasthemonetaryapproachtothechangeinforeignexchangereservesofthecentralbank.

9

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

TheMonetaryApproachtoFlexibleExchangeRates

10

i = i*+ se•

m − p = φy − λi

s = p − p*

se•

= 1λs −m +φy − λi*+ p*( )

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

MainPredic8onsoftheMonetaryApproachtotheExchangeRate

• Increasesindomes8cmoneysupplyandinterna8onalinterestratescauseadeprecia8onofthenominalexchangerate

• Increasesindomes8cincomeandtheinterna8onalpricelevelcauseanapprecia8onofthenominalexchangerate.

• Inanequilibriumwithout"bubbles"therecanbenoexpecta8onsoffuturechangesintheexchangerate.Theexchangerate,asanon-predefinedvariable,immediatelyadjuststothesteadystateequilibrium

11

s = m −φy + λi*− p*

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

TheMonetaryApproachandRealExchangeRates

• Itrequiresthattherealexchangerateisconstant,andthataslongasdomes8cinfla8ondiffersfrominterna8onalinfla8ontherewillbeacon8nuousadjustmentoftheexchangerate,inordertosa8sfythepurchasingpowerparitycondi8on.

• However,empirically,purchasingpowerparitydoesnotappeartobevalid.

• Realexchangeratesfluctuate,andtheirfluctua8onsarecloselyrelatedtofluctua8onsinnominalexchangerates.

• Avariantofthemonetarymodel,combinesitwiththeassump8onofthegradualadjustmentofthepricelevelinordertoachievepurchasingpowerparityinthesteadystate.Thus,theassump8onofpurchasingpowerparityisonlyassumedtoholdinthesteadystateandnotintheshortrun.

12

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

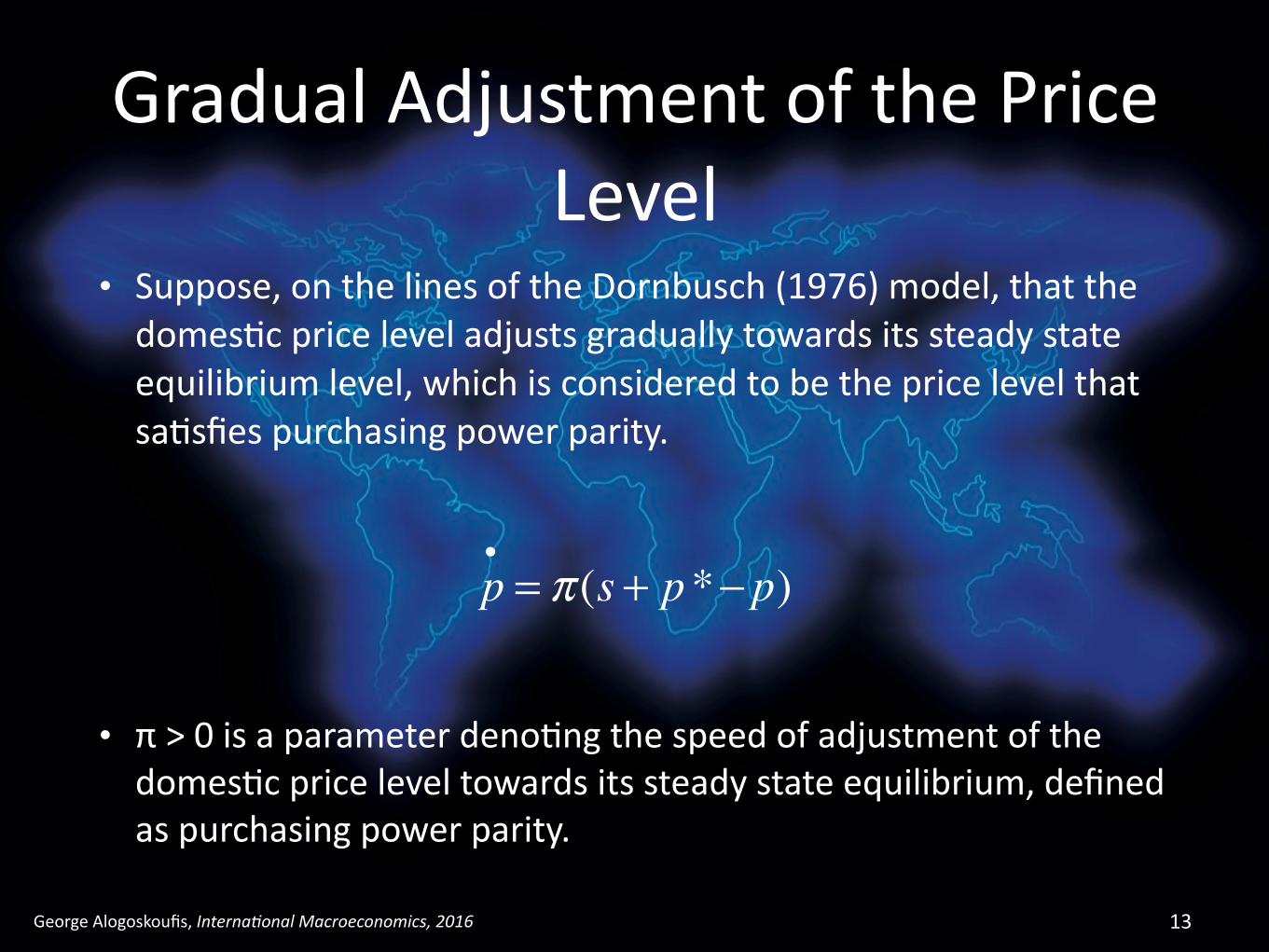

GradualAdjustmentofthePriceLevel

• Suppose,onthelinesoftheDornbusch(1976)model,thatthedomes8cpriceleveladjustsgraduallytowardsitssteadystateequilibriumlevel,whichisconsideredtobethepricelevelthatsa8sfiespurchasingpowerparity.

13

p•= π (s + p*− p)

• π>0isaparameterdeno8ngthespeedofadjustmentofthedomes8cpriceleveltowardsitssteadystateequilibrium,definedaspurchasingpowerparity.

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

TheMonetaryModelwithGradualPriceAdjustment

Asthedomes8cpricelevelisapredeterminedvariable,andcannotadjustintheshortruntoequilibratethedomes8cmoneymarket,thisrolemustbeplayedbythedomes8cnominalinterestrate.Sincethedomes8cnominalinterestratecanonlydifferfromtheinterna8onalnominalinterestratetotheextentthatthereareexpecta8onsoffuturechangesintheexchangerate,theexpectedandactualchangeintheexchangeratemustbesuchastomaintainequilibriuminthedomes8cmoneymarket.

14

p•= π (s + p*− p)

s•= se

•

= 1λ

p −m +φy − λi*( )

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

TheMonetaryApproachwithGradualAdjustmentofthePriceLevel

15

p

s

s=0 p=0

E

45ºp* pE

sE

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

APermanentIncreaseintheDomes8cMoneySupply

16

p

s

s=0 p=0

E

45ºp*

E'

E0

pE pE'

sE

s0

sE'

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

TheDynamicPathoftheNominalExchangeRate,thePriceLevelandtheDomes8cNominal

InterestRate

17

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

TheDynamicPathoftheNominalandtheRealExchangeRate

18

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

APermanentIncreaseinDomes8cOutput

19

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

APermanentIncreaseintheInterna8onalPriceLevel

20

p

s

s=0 p=0

E

45ºp*

E'

pE

sE

sE'

p*'

p*

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

TheMonetaryApproachtotheExchangeRateinDiscreteTime

Themonetarymodelcaneasilybyadaptedtoaaccommodatediscrete8meandstochas8cshocks.Astochas8cversionofthemonetarymodeltakesthefollowingform,

21

mt − pt = φyt − λit

it = it* + Etst+1 − st

pt = st + pt*

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

TheDetermina8onoftheNominalExchangeRate

Usingthemodeltoeliminatetheothertwoendogenousvariables,iandp,theexchangerateisdeterminedby,

22

st =λ1+ λ

Etst+1 +1

1+ λ(mt −φyt + λit

* − pt*)

Thecurrentnominalexchangerateisaweightedaverageoftheexpectedfuturenominalexchangerate,andthesocalledfundamentalsf,whichinthecaseofthemonetarymodelaretheexogenousvariablesthataffectthedomes8cmoneymarket.Thesearethedomes8cmoneysupplym,fullemploymentoutputy,theinterna8onalnominalinterestratei*andtheinterna8onalpricelevelp*.

ft = mt −φyt + λit* − pt

*

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

TheRa8onalExpecta8onsSolu8onfortheNominalExchangeRate

Throughsuccessivesubs8tu8ons,wegetthatthera8onalexpecta8onssolu8onfortheexchangeratemustsa8sfy,

23

st =1

1+ λλ1+ λ

⎛⎝⎜

⎞⎠⎟i=0

k∑i

Et mt+i −φyt+i + λit+i* − pt+i

*( )+ λ1+ λ

⎛⎝⎜

⎞⎠⎟k+1

Etst+k+1

Ifexpecta8onsaboutthefutureevolu8onoftheexchangerategrowataratewhichdoesnotexceed1/λ,then,itfollowsthat,

limk→∞

λ1+ λ

⎛⎝⎜

⎞⎠⎟k+1

Etst+k+1 = 0

Thiscondi8oniscalledatransversalitycondi'on,andessen8allyprecludesexplosiveexpecta8onsaboutthefutureevolu8onoftheexchangerate.

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

TheFundamentalSolu8onfortheExchangeRate

Takingthelimitofthesolu8on,asktendstoinfinity,andusingthetransversalitycondi8on,thera'onalexpecta'onsequilibriumsolu'onfortheexchangeratecanbewrigenas,

24

st =1

1+ λEt

λ1+ λ

⎛⎝⎜

⎞⎠⎟i=0

∞∑i

mt+i −φyt+i + λit+i* − pt+i

*( ) = 11+ λ

λ1+ λ

⎛⎝⎜

⎞⎠⎟i=0

∞∑i

Et ft+i

Thisisthesocalledfundamentalsolu'onfortheexchangerate,asitdependsonlyontheexpectedfutureevolu8onofthefundamentalsofthedomes8cmoneymarket.

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

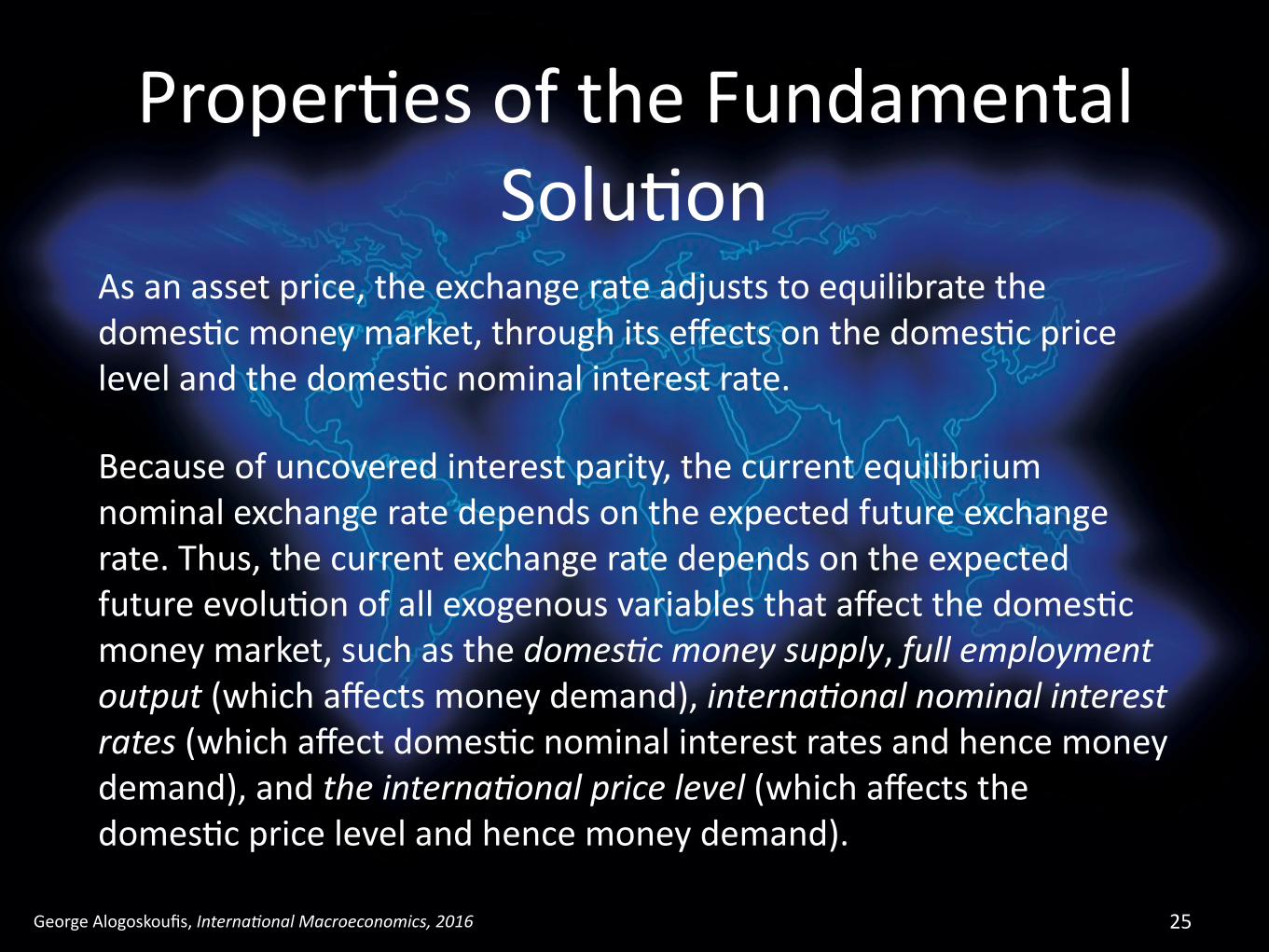

Proper8esoftheFundamentalSolu8on

Asanassetprice,theexchangerateadjuststoequilibratethedomes8cmoneymarket,throughitseffectsonthedomes8cpricelevelandthedomes8cnominalinterestrate.

Becauseofuncoveredinterestparity,thecurrentequilibriumnominalexchangeratedependsontheexpectedfutureexchangerate.Thus,thecurrentexchangeratedependsontheexpectedfutureevolu8onofallexogenousvariablesthataffectthedomes8cmoneymarket,suchasthedomes'cmoneysupply,fullemploymentoutput(whichaffectsmoneydemand),interna'onalnominalinterestrates(whichaffectdomes8cnominalinterestratesandhencemoneydemand),andtheinterna'onalpricelevel(whichaffectsthedomes8cpricelevelandhencemoneydemand).

25

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

Expecta8onsand“Bubbles”fortheExchangeRate

Thefundamentalsolu8onisnottheonlysolu8on.Amoregeneralsolu8onwouldtaketheform,

26

st =1

1+ λλ1+ λ

⎛⎝⎜

⎞⎠⎟i=0

∞∑i

Et ft+i + zt

wherezisanextraneousvariable,followingastochas8cprocessdefinedby,

zt =1+ λλ

zt−1 + ε tz

whereεzisawhitenoiseprocess,withzeromeanandconstantvariance.zis

anexplosivestochas8cprocess,andisojenreferredtoasabubble.Iftheexchangeratedependsonabubble,thenthebubblewilleventuallydominateitsbehavior,andthepathoftheexchangeratewillbeexplosive.

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

ClosedFormSolu8onsfortheExchangeRate:FundamentalsfollowaSta8onaryAR(1)Process

Inordertosaymoreaboutexchangeratedetermina8oninthemonetarymodel,weneedtomakeassump8onsabouttheexogenousprocessesdrivingthefundamentals.

Letusini8allyassumethethefundamentalsfollowasta8onaryAR(1)process,aroundaconstantmean.Thus,thefundamentalsareassumedtofollow,

27

ft = (1− ρ) f0 + ρ ft−1 + ε tf

Thekperiodaheadpredictor,i.ethera8onalexpecta8onabouttheirvaluekperiodsahead,dependsonlyonthecurrentfundamentals,accordingto,

Et ft+i = (1− ρ i ) f0 + ρ i ft

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

TheMeanandVarianceoftheExchangeRate

Subs8tu8nginthefundamentalsolu8on,theclosedformsolu8ontakestheform,

28

st = f0 +1

1+ λ(1− ρ)ft − f0( )

Themeanoftheexchangerateisequaltothemeanofthefundamentals,andthecurrentexchangeratedependsonthedevia8onofthecurrentfundamentalsfromtheirmean.Theresponseofthenominalexchangeratetodevia8onsofthecurrentfundamentalsfromtheirmeanislessthanonetoone,sinceλisposi8ve.Thus,thevarianceofthenominalexchangeratewillbelowerthanthevarianceofthefundamentals.

Var(st ) =1

1+ λ(1− ρ)⎛⎝⎜

⎞⎠⎟

2

Var( ft ) <Var( ft )

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

TheFundamentalsFollowaNon-Sta8onaryProcess

Letusalterna8velyassumethatthefundamentalsfollowanintegratedAR(1)process,i.ethatthechangeinthefundamentalsfollowsanAR(1)process.Thisprocesstakestheform,

29

Δft = ρΔft−1 + ε tf

Undersuchaprocess,thekperiodaheadpredictorofthefundamentalsandtheclosedformsolu8onfortheexchangeratetaketheform,

Et ft+k = ft + ρ iΔft = ft +1− ρ k

1− ρ⎛⎝⎜

⎞⎠⎟i=1

k∑ ρΔft

st = ft +λρ

1+ λ(1− ρ)Δft

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

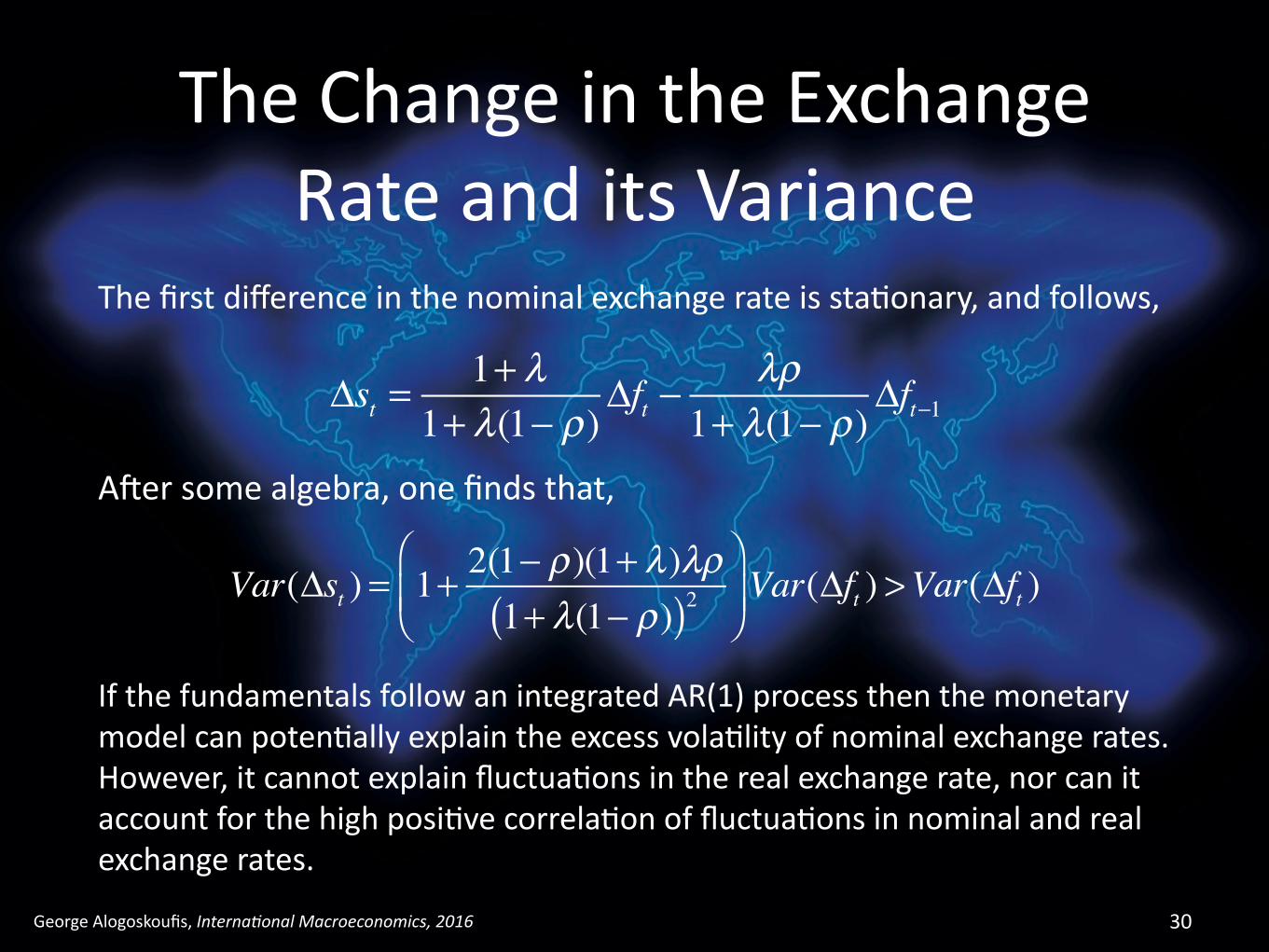

TheChangeintheExchangeRateanditsVariance

Thefirstdifferenceinthenominalexchangerateissta8onary,andfollows,

30

Δst =1+ λ

1+ λ(1− ρ)Δft −

λρ1+ λ(1− ρ)

Δft−1

Ajersomealgebra,onefindsthat,

Var(Δst ) = 1+ 2(1− ρ)(1+ λ)λρ1+ λ(1− ρ)( )2

⎛

⎝⎜⎞

⎠⎟Var(Δft ) >Var(Δft )

IfthefundamentalsfollowanintegratedAR(1)processthenthemonetarymodelcanpoten8allyexplaintheexcessvola8lityofnominalexchangerates.However,itcannotexplainfluctua8onsintherealexchangerate,norcanitaccountforthehighposi8vecorrela8onoffluctua8onsinnominalandrealexchangerates.

Related Documents