Electron Commer Res (2012) 12:151–175 DOI 10.1007/s10660-012-9090-z The mediating role of the dimensions of the perceived risk in the effect of customers’ awareness on the adoption of Internet banking in Iran Payam Hanafizadeh · Hamid Reza Khedmatgozar Published online: 24 March 2012 © Springer Science+Business Media, LLC 2012 Abstract One of the major issues banks are faced with in providing Internet Bank- ing (IB) services is the adoption of these services by the customers. This study seeks answer to the question that whether bank customers’ awareness of the services and advantages of IB is effective in reducing the negative effect of customers’ perceived risk on their intention of IB adoption. To this end, the two constructs of the dimen- sions of the perceived risk and IB awareness are simultaneously considered. Besides, in the research model, the effect of IB awareness on each dimension of the perceived risk and the effect of these dimensions on intention of IB adoption by the customers are investigated. The results indicate that IB awareness acts as a factor reducing all dimensions of the perceived risk (including time, financial, performance, social, se- curity, and privacy). In addition, it was found out that except for social risk, other dimensions of the perceived risk have significantly negative effect on the intention of IB adoption. Finally, proving the direct and positive effect of IB awareness on adoption intention, it was concluded that the dimensions of customers’ perceived risk plays a mediating role in the positive effect of IB awareness on IB adoption intention. In this respect, management approaches centered on the concept of IB awareness are offered for reducing the dimensions of customers’ perceived risk. Keywords Internet banking · Adoption · Dimensions of the perceived risk · Awareness P. Hanafizadeh ( ) School of Management and Accounting, Allameh Tabataba’i University, Nezami Ganjavi Street, Tavanneer, Valy Asr Avenue, P.O. Box 14155-6476, Tehran, Iran e-mail: hanafi[email protected] H.R. Khedmatgozar Department of Financial Engineering, University of Science and Culture, Tehran, Iran e-mail: [email protected]

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Electron Commer Res (2012) 12:151–175DOI 10.1007/s10660-012-9090-z

The mediating role of the dimensions of the perceivedrisk in the effect of customers’ awarenesson the adoption of Internet banking in Iran

Payam Hanafizadeh · Hamid Reza Khedmatgozar

Published online: 24 March 2012© Springer Science+Business Media, LLC 2012

Abstract One of the major issues banks are faced with in providing Internet Bank-ing (IB) services is the adoption of these services by the customers. This study seeksanswer to the question that whether bank customers’ awareness of the services andadvantages of IB is effective in reducing the negative effect of customers’ perceivedrisk on their intention of IB adoption. To this end, the two constructs of the dimen-sions of the perceived risk and IB awareness are simultaneously considered. Besides,in the research model, the effect of IB awareness on each dimension of the perceivedrisk and the effect of these dimensions on intention of IB adoption by the customersare investigated. The results indicate that IB awareness acts as a factor reducing alldimensions of the perceived risk (including time, financial, performance, social, se-curity, and privacy). In addition, it was found out that except for social risk, otherdimensions of the perceived risk have significantly negative effect on the intentionof IB adoption. Finally, proving the direct and positive effect of IB awareness onadoption intention, it was concluded that the dimensions of customers’ perceived riskplays a mediating role in the positive effect of IB awareness on IB adoption intention.In this respect, management approaches centered on the concept of IB awareness areoffered for reducing the dimensions of customers’ perceived risk.

Keywords Internet banking · Adoption · Dimensions of the perceived risk ·Awareness

P. Hanafizadeh (�)School of Management and Accounting, Allameh Tabataba’i University, Nezami Ganjavi Street,Tavanneer, Valy Asr Avenue, P.O. Box 14155-6476, Tehran, Irane-mail: [email protected]

H.R. KhedmatgozarDepartment of Financial Engineering, University of Science and Culture, Tehran, Irane-mail: [email protected]

152 P. Hanafizadeh, H.R. Khedmatgozar

1 Introduction

Development of information technology and emergence of various forms of Internetbanking in recent years have substantially changed the ways banks communicate withtheir customers [28, 71].

Internet Banking (IB) is one of the branches of electronic banking in which thecustomers have the opportunity of using a broad range of services such as cash trans-fer, paying the bills, getting information on deposits, investment and cheque servicesthrough Internet and the website designed by the banks [64].

IB offers many advantages to both banks and their customers. Regarding the ad-vantages of IB for the banks, one can point to release from temporal and spatiallimitations, reducing operational and administrative expenses, awareness from theactivities of customers, and creating the potential for expanding the range of services[7, 83]. In addition, IB provides the customers with the possibility of more rapidlyconducting a broad range of financial transactions electronically, through the bankwebsite, at any time and place and with less handling fees in comparison to otherbank methods [7, 48].

However, despite the increasing number of Internet users and all IB advancements,the number of IB users has not yet increased as expected [82].

One of the factors affecting the adoption of online shopping among customers isthe concept of the perceived risk [80]. Researchers of customer behavior have oftendefined perceived risk as the customers’ perception about lack of trust and the poten-tial adverse effects of purchasing a good or service [55]. Many studies have revealedthat customers perceive different dimensions of the risk. The predictive value of eachdimension in the total risk and its reductive behavior greatly depend upon the class ofthe good or service [32]. If online shopping is considered as a short-term relationshipbetween the buyer and seller, the dimensions of the perceived risk in IB, which is along-term relationship, will be observed in a more complicated form requiring moreaccurate investigation.

When studying the concept of customers’ perceived risk in various fields, it shouldbe noted that different forms of risk may be perceived independently from each otherand their impact may be different, because each of them can be caused by differentsources and in a different condition [56]. Although the concept of the perceived risk,as a barrier of IB adoption, has been investigated in relatively many studies; moststudies, except for a limited number (e.g. [52, 55]), provide two main forms. First,the concept of the perceived risk has been considered as a single construct ratherthan a collection of dimensions (e.g. [83, 84]). Second, in most of these studies, theconcept of the perceived risk has been regarded as equivalent to one or more specificdimensions from among the dimensions of the perceived risk, such as security andprivacy [20, 60]. In this respect, the first aim of this study is to investigate the effectsof each dimension of the perceived risk on IB adoption, separately.

Littler and Melanthiou [55] argue that research on the concept of the perceivedrisk is conducted based on the assumption that customers can have rational evalua-tions from the effects and probabilities of these events. To put it more simply, it isassumed that customers have the necessary awareness of the various angles of a goodor service and obtain ensuring information. However, if the perceived risk is viewed

The mediating role of the dimensions of the perceived risk 153

as a collection of dimensions rather than a single construct, the question arises thathow much does the concept of awareness affect each dimension of the perceived riskin IB adoption? Finding answer to this question is the second goal of this study.

The third and the main objective of the present study is finding the answer to thequestion that regarding the results obtained from the first and second objectives, isit possible to consider a mediating role for each dimension of the perceived risk inthe relationship between IB awareness and IB adoption. The answer to this questionbasically specifies two very important concepts that can be regarded as the main con-tribution of the present study. First, considering the concept of the perceived risk asa set of dimensions, it becomes clear that by mediating which dimension of the per-ceived risk, IB awareness increases IB adoption. Second, it is determined that whichdimension of the perceived risk, plays a higher mediating role in the positive effect ofIB awareness on IB adoption intention. Accordingly, the answer to this question cangreatly help bank managers and planners in developing marketing strategies using therole of awareness and information on IB. In other words, they will find out that theycan increase IB adoption by their customers through focusing more on which aspectsof the products, facilities and their advantages.

With respect to the knowledge acquired from the literature on IB adoption, it canbe claimed that simultaneously investigating the two concepts of the dimensions ofthe perceived risk and IB awareness and their relationship in this study is unique.

Findings of Gholami et al. [34] indicated that the changes caused by informationand communication technology in less-developed countries have stronger impactsupon human development index scores in comparison to more developed countries.Al-Somali et al. [5] argued that despite the conduction of many studies on IB adop-tion in various countries of world, few studies can be found that investigate this issuein developing countries of the Middle East. The present article investigates the re-search model in Iran in order to achieve its objectives. Iran is a developing countryin the Middle East. The population of this country in 2009 is about 66.5 million peo-ple and the number of Internet users is estimated to be 32.2 million people in thiscountry [43]. According to the report of Iran central Bank [19], the number of IBservices users at the end of the first quarter of 2009 was around 5.8 million people(i.e. 8.7 % of the population) who receive these services from 11 governmental and 6private banks. Comparison of this statistics with the statistics in a developed countrylike England can be interesting. England with a population of 61.5 million people in2009 had 48.75 million Internet users [42] and according to the report of Associationof Payment Clearing [8], the number of IB users in the first half of 2009 was over22 million people (i.e. 35.8 % of the population). Comparison of these two statis-tics clearly indicates that Iran is back-warded with respect to the application of IB.The problem of IB adoption by the customers in Iran is the main problem banks facein expanding these services. Therefore, the findings of this study, besides its theo-retical contributions, can help managers of Iranian banks to develop their marketingstrategies for more rapidly expanding IB adoption by customers.

This paper is organized as following: Sect. 2 introduces the theoretical backgroundof the study including studies on Internet banking, hypotheses, and research model.Section 3 describes research methodology and Sect. 4 presents data analysis and re-sults of hypotheses testing. Section 5 investigates research findings and offers their

154 P. Hanafizadeh, H.R. Khedmatgozar

theoretical and managerial implications. Finally, Sect. 6 presents the conclusion andoffers suggestions for further research in future.

2 Theoretical background

The theoretical framework of this paper consists of four parts. The first part reviewsthe related literature on IB and models employed by the studies on IB adoption. In thesecond part, the dimensions of the perceived risk in IB adoption is investigated on thebasis of the perceived risk theory (PRT) and the related hypotheses are presented. Thethird part explains the concept of IB awareness and the related hypotheses. Finally,in the fourth part, the research model is proposed on the basis of the hypothesespresented in parts 2 and 3.

2.1 Studies on Internet banking

Since the mid 1990s, a radical change has been witnessed in the service channelsof the banks introduced by new technologies like Internet banking [64]. This funda-mental change led to a new literature in research in the field of banking technology.Akinci et al. [2] point out that four interrelated fields can be identified by reviewingthis literature:

• Retail banking services• Structure of bank distribution channels• Banks, bank managers, and their attitudes, perceptions, orientation and strategies

toward new technologies like IB• Customer characteristics including demographical characteristics, attitudes, inten-

tions, adoption, and satisfaction

The field considered in this study is part of the fourth filed, i.e., IB adoption by thecustomers.

Hernandez and Mazzon [38] categorized IB adoption studies into two categories:

• Descriptive studies: the aim of which is to identify characteristics, attitudes, re-actions, adoption barriers, and features making IB adoption seem attractive to thecustomers (e.g. [2, 33, 47]).

• Relational studies: whose aim is to determine variables affecting IB adoption usingone of the models for the adoption of new technologies or a combination of them.

In this study, it is tried to look into the issue of IB adoption on the basis of the secondapproach.

The basic theoretical approaches and models used in the relational studies con-ducted in the field of adoption of new technologies like IB can be summarized asfollows:

1. Theory of Reasoned Action (TRA) [30]2. Diffusion of Innovation (DOI) [67]3. Theory of Planned Behavior (TPB) [1]4. Social Cognitive Theory (SCT) [10]

The mediating role of the dimensions of the perceived risk 155

5. Technology Acceptance Model (TAM) [25]6. Commitment-Trust Theory (CTT) [58]7. Perceived Risk Theory (PRT) [45, 49, 69]

Many researchers have also tried to use, develop, and combine these models andtheories in order to investigate the issue of adoption of new technologies like IB(DTPB: Taylor and Todd [77]; TAM2: Venkatesh and Davis [78]; UTAUT: Venkateshet al. [79]; Pikkarainen et al. [64]; Chan and Lu [20]; Lai et al. [51]; Ndubisi [61];Yiu et al. [83]; Zolait and Ainin [86]; Al-Somali et al. [5]; Lee [52]; Polasik andWisniewski [65]).

The theory used as the basic concept of this study is the perceived risk theory(PRT). The main feature of this theory distinguishing it from other theories and mod-els is the fact that, unlike other theories or models which concentrate on the positivefactors influencing customers’ adoption of IB, this theory specifically focuses on thenegative factors (risks) which prevent customers from IB adoption. In the next sec-tion, this theory is introduced in the field of IB.

2.2 The perceived risk and its dimensions

As it was mentioned earlier, the perceived risk can be defined as the customer’s per-ception of lack of trust and the potential adverse effects of purchasing a good orservice [55]. The perceived risk is considered as an important factor which influencescustomer behavior [63].

Researchers in the field of as perceived risk theory (PRT) [29] identified perceivedrisk as the combination of several dimensions [45, 49, 69]. These dimensions includeperformance, financial, social, psychological, security, privacy, and physical risks.These dimensions have been used and even developed by many researchers (for moreinformation refer to Lim [54]).

Gemünden [32] argued that the predictive value of each dimension in the total riskand its reductive behavior greatly depend upon the class of the good or service. Sincethe first objective of this study is to investigate the effects of the dimensions of theperceived risk on IB adoption, the literature in this area is reviewed below.

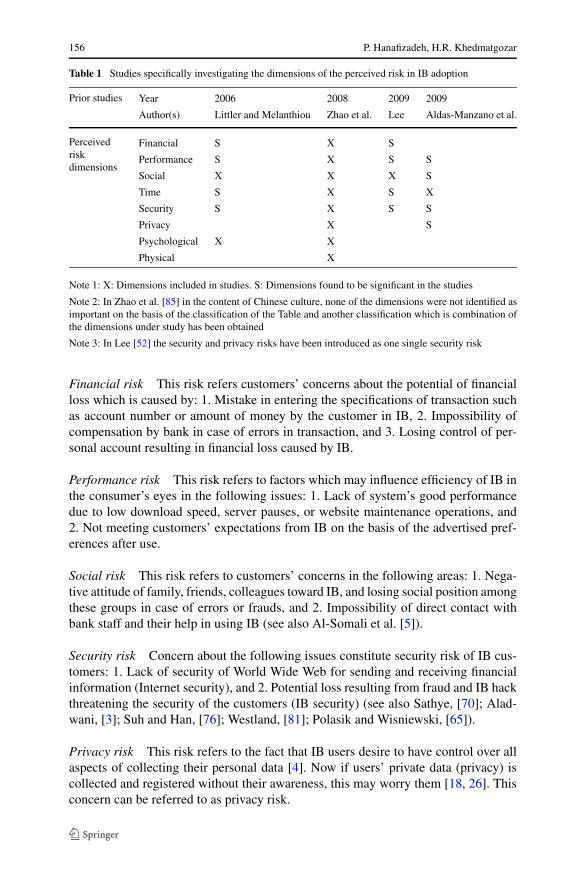

Studies which, based on PRT, have investigated the dimensions of the perceivedrisk specifically in IB adoption are limited to four studies the details of which arepresented in Table 1.

It can be inferred from Table 1 that some concepts of these studies overlap eachother. According to the results of these studies and by summarizing the concepts ofthe dimensions of the perceived risk in them, the dimensions of the perceived risk canbe categorized into six groups: time, financial, performance, social, security, and pri-vacy. Considering the general definition of each dimension, provided by Feathermanand Pavlou [29] and Lee [52], in the following, each of these dimensions is definedin terms of IB.

Time risk This risk refers to customers’ concerns about following issues: 1. Toomuch time spent for learning how to use IB; 2. Too much time devoted for solvingproblems caused by using IB (such as proving transaction errors), and 3. Too muchtime which must be spent doing and completing transactions in IB.

156 P. Hanafizadeh, H.R. Khedmatgozar

Table 1 Studies specifically investigating the dimensions of the perceived risk in IB adoption

Prior studies Year 2006 2008 2009 2009

Author(s) Littler and Melanthiou Zhao et al. Lee Aldas-Manzano et al.

Perceivedriskdimensions

Financial S X S

Performance S X S S

Social X X X S

Time S X S X

Security S X S S

Privacy X S

Psychological X X

Physical X

Note 1: X: Dimensions included in studies. S: Dimensions found to be significant in the studies

Note 2: In Zhao et al. [85] in the content of Chinese culture, none of the dimensions were not identified asimportant on the basis of the classification of the Table and another classification which is combination ofthe dimensions under study has been obtained

Note 3: In Lee [52] the security and privacy risks have been introduced as one single security risk

Financial risk This risk refers customers’ concerns about the potential of financialloss which is caused by: 1. Mistake in entering the specifications of transaction suchas account number or amount of money by the customer in IB, 2. Impossibility ofcompensation by bank in case of errors in transaction, and 3. Losing control of per-sonal account resulting in financial loss caused by IB.

Performance risk This risk refers to factors which may influence efficiency of IB inthe consumer’s eyes in the following issues: 1. Lack of system’s good performancedue to low download speed, server pauses, or website maintenance operations, and2. Not meeting customers’ expectations from IB on the basis of the advertised pref-erences after use.

Social risk This risk refers to customers’ concerns in the following areas: 1. Nega-tive attitude of family, friends, colleagues toward IB, and losing social position amongthese groups in case of errors or frauds, and 2. Impossibility of direct contact withbank staff and their help in using IB (see also Al-Somali et al. [5]).

Security risk Concern about the following issues constitute security risk of IB cus-tomers: 1. Lack of security of World Wide Web for sending and receiving financialinformation (Internet security), and 2. Potential loss resulting from fraud and IB hackthreatening the security of the customers (IB security) (see also Sathye, [70]; Alad-wani, [3]; Suh and Han, [76]; Westland, [81]; Polasik and Wisniewski, [65]).

Privacy risk This risk refers to the fact that IB users desire to have control over allaspects of collecting their personal data [4]. Now if users’ private data (privacy) iscollected and registered without their awareness, this may worry them [18, 26]. Thisconcern can be referred to as privacy risk.

The mediating role of the dimensions of the perceived risk 157

Lee’s [52] reasoning that IB creates no threat to human life, has excluded physicalrisk from the dimensions of the perceived risk in IB adoption. In this respect andconsidering the studies of Littler and Melanthiou [55] and Zhao et al. [85] which havenot identified psychological risk as one dimension of the risk affecting IB adoption,physical and psychological risk have been excluded from the list of dimensions of theperceived risk in IB adoption.

Beliefs about the results of behavior, including the perceived risk, are among themain components and bases of the attitude toward behavior [46]. Regarding adoptionof technologies like IB, Venkatesh et al. [79] argue that since technology adoption isoptional, attitude and intention are positively related to each other. Therefore, dimen-sions of the perceived risk in IB adoption can influence customers’ perception aboutIB adoption and negatively affect their intention of adopting such technology [83].Considering these discussions, the following hypotheses can be put forward:

H1: customers’ perceived risk of IB (1—Time, 2—Financial, 3—Performance, 4—Social, 5—Security, and 6—Privacy) negatively influences their intention of IBadoption.

In the above hypothesis, time risk is considered as H1-1, financial risk as H1-2,performance risk as H1-3, social risk as H1-4, security risk as H1-5, and privacy riskas H1-6.

2.3 Awareness from Internet banking

Howcroft et al. [40] concluded in their studies that one of the most important rea-sons of customers’ reluctance for adopting IB is their unawareness of its servicesand advantages. Moreover, Sathye [70] notes that low degree of awareness of Inter-net banking is a critical factor in causing customers not to adopt Internet banking.Azouzi [9] concluded in his study that awareness of its advantages and services has asignificant positive effect on adopting and using Internet banking.

This issue has also been confirmed by Gerrard et al. [33]; Al-Somali et al. [5].Pikkarainen et al. [64] also comment that the volume of information customers re-ceive about IB is recognized as the main influential factor in adopting this service.Information of customers about service, facilities, advantages, and way of using IB,can be regarded as IB awareness. In this regard, the following hypothesis can be pre-sented:

H2: IB awareness positively influences bank customers’ intention of IB adoption.

Rogers and Shoemaker’s [68] theory states that before customers become ready toadopt a product or service, they pass through the process of knowledge, persuasion,decision, and confirmation. In other words, they argue that acceptance or rejectionof an innovation commences when the customers become aware of the product andits advantages and disadvantages. Thus, customer awareness of the product, its fa-cilities, advantages, and disadvantages is among the initial and important stages indetermining innovation of the individual. On the other hand, Aldas Manzano andNavarre [4] found out that customer innovation negatively affects IB risk perception.Besides, Cooper [24] considers risk level as an important factor of innovation adop-tion by the customer. In this respect, it can be concluded that customer awareness of

158 P. Hanafizadeh, H.R. Khedmatgozar

IB, as an important factor of innovation, can exert a negative effect on customers’risk regarding IB. Littler and Melanthiou [55], confirming this issue, argue that oneof the mediating factors which affect risk perception of the customers is insufficientinformation about the products and its advantages and disadvantages. Lichtensteinand Williamson [53], also, point to the significance of knowledge and support in in-forming customers for reducing the risk and increasing their willingness for receivingIB services.

With respect to the previous hypotheses in which the negative effect of the di-mensions of the perceived risk and the positive effect of IB awareness on IB adoptionintention are considered, it seems logical to consider a negative direction for the effectof IB awareness on the dimensions of the perceived risk. Consequently, the followinghypotheses are put forward:

H3: IB awareness negatively influences the dimensions of the perceived risk for IBadoption (including 1—Time, 2—Financial, 3—Performance, 4—Social, 5—Security, 6—Privacy).

In the above hypothesis, the effect of awareness on time risk is considered as H3-1,financial risk as H3-2, performance risk as H3-3, social risk as H3-4, security risk asH3-5, and privacy risk as H3-6.

2.4 Research model

The research model of present study which is designed on the basis of the hypothesespresented in the previous section is depicted in Fig. 1.

Fig. 1 The proposed research model

The mediating role of the dimensions of the perceived risk 159

3 Research methodology

3.1 Survey administration

The survey method was used for collecting data in order to test the hypotheses.Considering the objectives mentioned in previous sections, the statistical popula-tion of the study is composed of Iranian bank customers who do not activelyuse IB. Three points must be mentioned about the selection of statistical popu-lation. First, considering the model and research objectives, the aim is to inves-tigate the dimensions of the perceived risk in IB adoption intention and the ef-fect of IB awareness on the dimensions of the perceived risk before IB adoption.Second, those who actively use IB cannot have a true conception of their percep-tions before IB adoption. The reason is the changes of the content of the dimen-sions of the perceived risk and degree of IB awareness after adoption. Third, asit was mentioned, the statistical population consists of the customers who do notactively use IB. Hence, those who have IB account but do not use it due to vari-ous reasons part of which being the dimensions of the perceived risk, are consid-ered in the population. Regarding the defined statistical population, the statisticalsample was also selected from among Iranian bank customers who do not activelyuse IB.

Two methods of self-administered survey and Internet survey were utilized fordata collection. This was done in order to reduce the amount of possible bias. Inthis method, first, five regions in the northern, southern, central, eastern, and west-ern parts of Iran were selected and random sampling was conducted in them. Thissampling was done in places like trains (with the permission of Iranian railway or-ganization), commercial centers, governmental organizations, private companies, in-dustrial factories, and universities, and lasted for one month in December 2009. Insum, 462 questionnaires were collected and after removing uncompleted question-naires 414 completed questionnaires were obtained. In the second method, Internetsurvey, an online questionnaire was developed, first. In the next stage, the addresslink of this questionnaire was placed on the home page of two well-known websitesabout management and banking (www.betsa.ir, www.banki.ir). Also, in order to in-crease the reply rate, the questionnaire was advertised in three forums. Finally, usingthis method and during one month, 140 replies were obtained. Thus, a sample of 554was achieved.

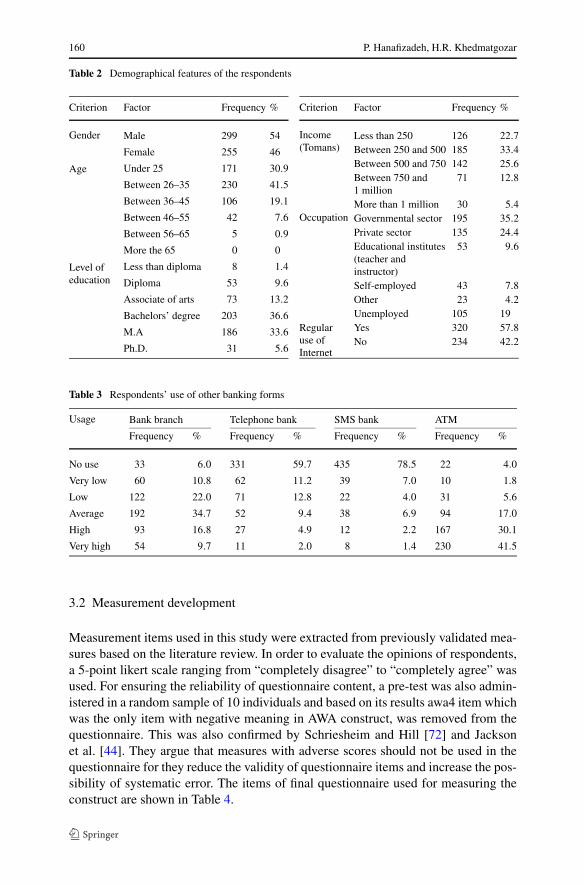

Table 2 presents the demographical features of the respondents. 54 % of therespondents were male and the highest ratio (41.5 %) with respect to age be-longed to (26–35) group. Most of the respondents, that is, 36.6 % had bachelor’sdegree. 57.8 % of the respondents regularly used Internet and the highest ratio(33.4 %) regarding income belonged to the income group of 250000 to 500000Tomans. In addition, Table 3 presents the amount of respondents’ use of otherforms of banking services in which the average to high usage of bank branchesand ATMs, and not using Telephone bank, as well as SMS banking is observ-able.

160 P. Hanafizadeh, H.R. Khedmatgozar

Table 2 Demographical features of the respondents

Criterion Factor Frequency %

Gender Male 299 54

Female 255 46

Age Under 25 171 30.9

Between 26–35 230 41.5

Between 36–45 106 19.1

Between 46–55 42 7.6

Between 56–65 5 0.9

More the 65 0 0

Level ofeducation

Less than diploma 8 1.4

Diploma 53 9.6

Associate of arts 73 13.2

Bachelors’ degree 203 36.6

M.A 186 33.6

Ph.D. 31 5.6

Criterion Factor Frequency %

Income(Tomans)

Less than 250 126 22.7Between 250 and 500 185 33.4Between 500 and 750 142 25.6Between 750 and1 million

71 12.8

More than 1 million 30 5.4Occupation Governmental sector 195 35.2

Private sector 135 24.4Educational institutes(teacher andinstructor)

53 9.6

Self-employed 43 7.8Other 23 4.2Unemployed 105 19

Regularuse ofInternet

Yes 320 57.8No 234 42.2

Table 3 Respondents’ use of other banking forms

Usage Bank branch Telephone bank SMS bank ATM

Frequency % Frequency % Frequency % Frequency %

No use 33 6.0 331 59.7 435 78.5 22 4.0

Very low 60 10.8 62 11.2 39 7.0 10 1.8

Low 122 22.0 71 12.8 22 4.0 31 5.6

Average 192 34.7 52 9.4 38 6.9 94 17.0

High 93 16.8 27 4.9 12 2.2 167 30.1

Very high 54 9.7 11 2.0 8 1.4 230 41.5

3.2 Measurement development

Measurement items used in this study were extracted from previously validated mea-sures based on the literature review. In order to evaluate the opinions of respondents,a 5-point likert scale ranging from “completely disagree” to “completely agree” wasused. For ensuring the reliability of questionnaire content, a pre-test was also admin-istered in a random sample of 10 individuals and based on its results awa4 item whichwas the only item with negative meaning in AWA construct, was removed from thequestionnaire. This was also confirmed by Schriesheim and Hill [72] and Jacksonet al. [44]. They argue that measures with adverse scores should not be used in thequestionnaire for they reduce the validity of questionnaire items and increase the pos-sibility of systematic error. The items of final questionnaire used for measuring theconstruct are shown in Table 4.

The mediating role of the dimensions of the perceived risk 161

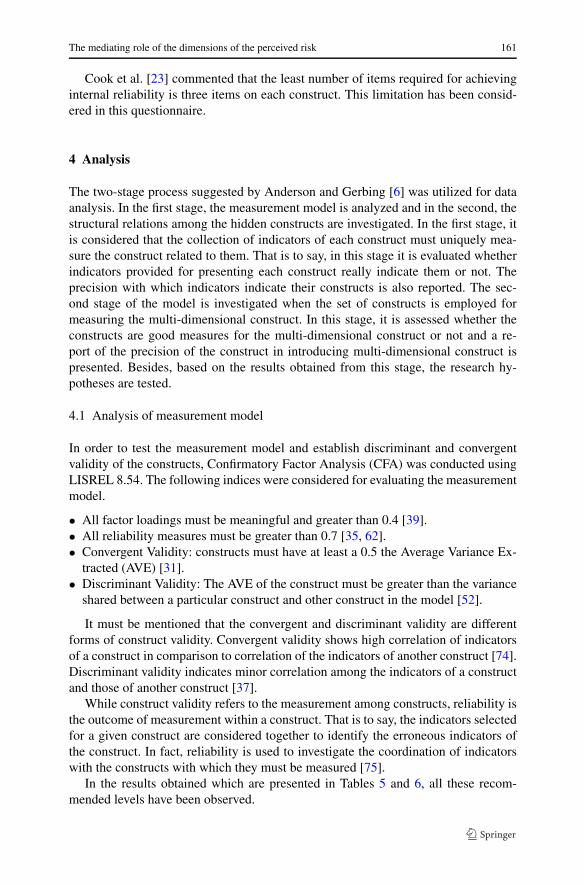

Cook et al. [23] commented that the least number of items required for achievinginternal reliability is three items on each construct. This limitation has been consid-ered in this questionnaire.

4 Analysis

The two-stage process suggested by Anderson and Gerbing [6] was utilized for dataanalysis. In the first stage, the measurement model is analyzed and in the second, thestructural relations among the hidden constructs are investigated. In the first stage, itis considered that the collection of indicators of each construct must uniquely mea-sure the construct related to them. That is to say, in this stage it is evaluated whetherindicators provided for presenting each construct really indicate them or not. Theprecision with which indicators indicate their constructs is also reported. The sec-ond stage of the model is investigated when the set of constructs is employed formeasuring the multi-dimensional construct. In this stage, it is assessed whether theconstructs are good measures for the multi-dimensional construct or not and a re-port of the precision of the construct in introducing multi-dimensional construct ispresented. Besides, based on the results obtained from this stage, the research hy-potheses are tested.

4.1 Analysis of measurement model

In order to test the measurement model and establish discriminant and convergentvalidity of the constructs, Confirmatory Factor Analysis (CFA) was conducted usingLISREL 8.54. The following indices were considered for evaluating the measurementmodel.

• All factor loadings must be meaningful and greater than 0.4 [39].• All reliability measures must be greater than 0.7 [35, 62].• Convergent Validity: constructs must have at least a 0.5 the Average Variance Ex-

tracted (AVE) [31].• Discriminant Validity: The AVE of the construct must be greater than the variance

shared between a particular construct and other construct in the model [52].

It must be mentioned that the convergent and discriminant validity are differentforms of construct validity. Convergent validity shows high correlation of indicatorsof a construct in comparison to correlation of the indicators of another construct [74].Discriminant validity indicates minor correlation among the indicators of a constructand those of another construct [37].

While construct validity refers to the measurement among constructs, reliability isthe outcome of measurement within a construct. That is to say, the indicators selectedfor a given construct are considered together to identify the erroneous indicators ofthe construct. In fact, reliability is used to investigate the coordination of indicatorswith the constructs with which they must be measured [75].

In the results obtained which are presented in Tables 5 and 6, all these recom-mended levels have been observed.

162 P. Hanafizadeh, H.R. Khedmatgozar

Tabl

e4

Item

sus

edin

the

ques

tionn

aire

Con

stru

ctIt

ems

Ref

eren

ces

Tim

eR

isk

(TIM

)tim

1In

my

opin

ion,

lear

ning

how

tous

eIn

tern

etba

nkin

gse

rvic

esta

kes

alo

tof

time

[4,5

2,55

,85]

tim2

Alo

tof

time

mus

tbe

spen

tfor

tran

sact

ions

inIB

serv

ices

for

bank

ing

tran

sact

ions

tim3

Ith

ink

Ish

ould

spen

da

lot

oftim

eso

lvin

gth

epr

oble

ms

aris

ing

from

IBsy

stem

s(s

uch

aspr

ovin

gth

epa

ymen

terr

ors)

Fina

ncia

lRis

k(F

IN)

fin1

Iam

afra

idof

losi

ngm

ym

oney

whe

ntr

ansf

erri

ngm

oney

onth

eIn

tern

etdu

eto

care

less

ness

orm

ista

kes

like

erro

neou

sen

try

ofac

coun

tnum

ber

orth

eam

ount

ofm

oney

[52,

85]

fin2

Iam

afra

idth

atI

will

notb

eab

leto

getc

ompe

nsat

ion

from

bank

inca

seof

erro

rs

fin3

Iam

afra

idof

losi

ngco

ntro

lof

my

acco

untb

yus

ing

IBsy

stem

s

Perf

orm

ance

Ris

k(P

ER

)pe

r1In

my

opin

ion

IBsy

stem

sm

ayno

twor

kpr

oper

lydu

eto

low

dow

nloa

dsp

eed

orm

aint

enan

ceop

erat

ions

orth

eym

ayfa

cese

rver

paus

es[4

,52,

55]

per2

IBse

rver

sm

ayno

twor

kpr

oper

lyan

dth

epr

oces

sof

paym

entm

aybe

wro

ng

per3

Iam

afra

idth

atIB

mig

htno

tpro

vide

the

adva

ntag

esad

vert

ised

Soci

alR

isk

(SO

C)

soc1

Iam

sure

that

ifI

deci

deto

use

IBan

dm

ista

keor

frau

dha

ppen

inm

yIn

tern

etba

nkin

gtr

ansa

ctio

ns,I

will

lose

my

good

posi

tion

amon

gm

yfr

iend

s,fa

mily

,and

colle

ague

s[5

5,85

]

soc2

Ith

ink

ifI

use

IBsy

stem

s,pe

ople

will

nota

dmir

em

efo

rus

ing

it

soc3

Usi

ngIB

syst

ems,

Iwill

notb

eab

leto

have

dire

ctre

latio

nsw

ithba

nkst

affa

ndus

eth

eirh

elps

and

this

give

sm

ean

unpl

easa

ntfe

elin

g

Secu

rity

Ris

k(S

EC

)se

c1I

feel

unse

cure

dab

outs

endi

ngan

dre

ceiv

ing

my

finan

cial

info

rmat

ion

onIB

syst

ems

[4,5

2,55

,85]

sec2

Ith

ink

IBsy

stem

sca

nea

sily

beac

cess

edby

unau

thor

ized

peop

lelik

eha

cker

s

sec3

Inm

yop

inio

n,W

orld

Wid

eW

ebis

nota

safe

and

appr

opri

ate

plac

efo

rfin

anci

altr

ansa

ctio

ns

Priv

acy

Ris

k(P

RI)

pri1

Use

ofIn

tern

etfo

rfin

anci

altr

ansa

ctio

nsin

crea

ses

the

poss

ibili

tyof

unw

ante

dem

ails

[4,8

5]

pri2

Ith

ink

ifI

use

IBsy

stem

s,it

mig

htbe

poss

ible

for

bank

tom

ake

my

pers

onal

info

rmat

ion

acce

ssib

lefo

rot

her

orga

niza

tions

orco

mpa

nies

with

outm

yco

nsen

t

pri3

Ith

ink

ifI

use

IBsy

stem

s,m

ypr

ivac

yis

thre

aten

eddu

eto

illeg

alus

eof

my

pers

onal

info

rmat

ion

The mediating role of the dimensions of the perceived risk 163

Tabl

e4

(Con

tinu

ed)

Con

stru

ctIt

ems

Ref

eren

ces

Aw

aren

ess

(AW

A)

awa1

Ith

ink

Ige

teno

ugh

info

rmat

ion

abou

tthe

serv

ices

ofIB

syst

ems

[5,6

4]aw

a2I

thin

kI

gete

noug

hin

form

atio

nab

outt

head

vant

ages

ofIB

syst

ems

awa3

Ith

ink

Ige

teno

ugh

info

rmat

ion

abou

tthe

way

sof

open

ing

acco

unta

ndus

ing

IBsy

stem

s

awa5

Inge

nera

l,I

have

enou

ghin

form

atio

nab

outI

B

Inte

ntio

nto

use

(IN

T)

int1

Iin

tend

tous

eIB

regu

larl

yin

futu

re[5

,52,

66,8

3]in

t2I

inte

ndto

use

IBfo

rqu

ick

and

easy

acce

ssto

my

bank

info

rmat

ion

infu

ture

int3

Iam

goin

gto

use

IBfo

rm

yba

nktr

ansa

ctio

nsin

futu

re

int4

Ith

ink

that

Iw

illus

eIB

mor

eth

anba

nkbr

anch

esin

futu

re

Not

e:It

emaw

a4ha

sbe

enre

mov

edfr

omth

equ

estio

nnai

re

164 P. Hanafizadeh, H.R. Khedmatgozar

Table 5 Validation of the final measurement model, reliability and convergent validity

Construct Item Factor Loading T-Value CA CR AVE

Time Risk (TIM) tim1 0.64 14.06 0.74 0.75 0.51

tim2 0.84 17.69

tim3 0.64 14.08

Financial Risk (FIN) fin1 0.85 24.24 0.91 0.91 0.78

fin2 0.90 26.27

fin3 0.90 26.64

Performance Risk (PER) per1 0.81 21.45 0.86 0.86 0.67

per2 0.89 24.24

per3 0.74 19.17

Social Risk (SOC) soc1 0.72 15.98 0.75 0.76 0.52

soc2 0.82 17.85

soc3 0.61 13.70

Security Risk (SEC) sec1 0.78 21.14 0.89 0.90 0.74

sec2 0.86 24.34

sec3 0.94 27.52

Privacy Risk (PRI) pri1 0.91 26.77 0.92 0.92 0.79

pri2 0.90 26.37

pri3 0.85 24.41

Awareness (AWA) awa1 0.92 27.31 0.90 0.90 0.70

awa2 0.88 25.38

awa3 0.82 23.09

awa5 0.71 18.80

Intention to use (INT) int1 0.87 12.57 0.93 0.93 0.77

int2 0.86 12.95

int3 0.89 11.71

int4 0.89 11.87

Recommendation 0.70 0.70 0.50

Notes: CA = Cronbach’s Alpha; CR = Composite Reliability; AVE = Average Variance Extracted; ∗p <

0.001

4.2 Analysis of the structural model

In order to analyze the structural model proposed, structural equation modeling(SEM) was utilized and its fitness was evaluated through Chi-Square test. When thesample size is between 75 and 200, the Chi-Square value of a rational index shows thefitness. However, for models with larger n, the value of Chi-Square is always statisti-cally significant. (Of course this is not totally agreed upon by the researchers and itsrejection or acceptance is debated. For more information please refer to Barrett [12].In addition, Chi-Square is influenced by the amount of correlations in the model.The higher these correlations, the weaker the fitness will be [16, 50]. In this regard,

The mediating role of the dimensions of the perceived risk 165

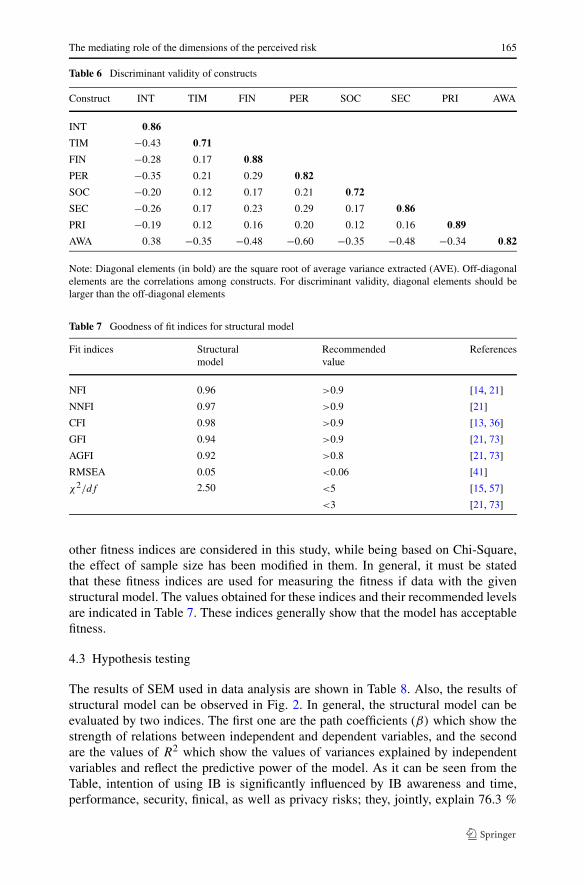

Table 6 Discriminant validity of constructs

Construct INT TIM FIN PER SOC SEC PRI AWA

INT 0.86

TIM −0.43 0.71

FIN −0.28 0.17 0.88

PER −0.35 0.21 0.29 0.82

SOC −0.20 0.12 0.17 0.21 0.72

SEC −0.26 0.17 0.23 0.29 0.17 0.86

PRI −0.19 0.12 0.16 0.20 0.12 0.16 0.89

AWA 0.38 −0.35 −0.48 −0.60 −0.35 −0.48 −0.34 0.82

Note: Diagonal elements (in bold) are the square root of average variance extracted (AVE). Off-diagonalelements are the correlations among constructs. For discriminant validity, diagonal elements should belarger than the off-diagonal elements

Table 7 Goodness of fit indices for structural model

Fit indices Structuralmodel

Recommendedvalue

References

NFI 0.96 >0.9 [14, 21]

NNFI 0.97 >0.9 [21]

CFI 0.98 >0.9 [13, 36]

GFI 0.94 >0.9 [21, 73]

AGFI 0.92 >0.8 [21, 73]

RMSEA 0.05 <0.06 [41]

χ2/df 2.50 <5 [15, 57]

<3 [21, 73]

other fitness indices are considered in this study, while being based on Chi-Square,the effect of sample size has been modified in them. In general, it must be statedthat these fitness indices are used for measuring the fitness if data with the givenstructural model. The values obtained for these indices and their recommended levelsare indicated in Table 7. These indices generally show that the model has acceptablefitness.

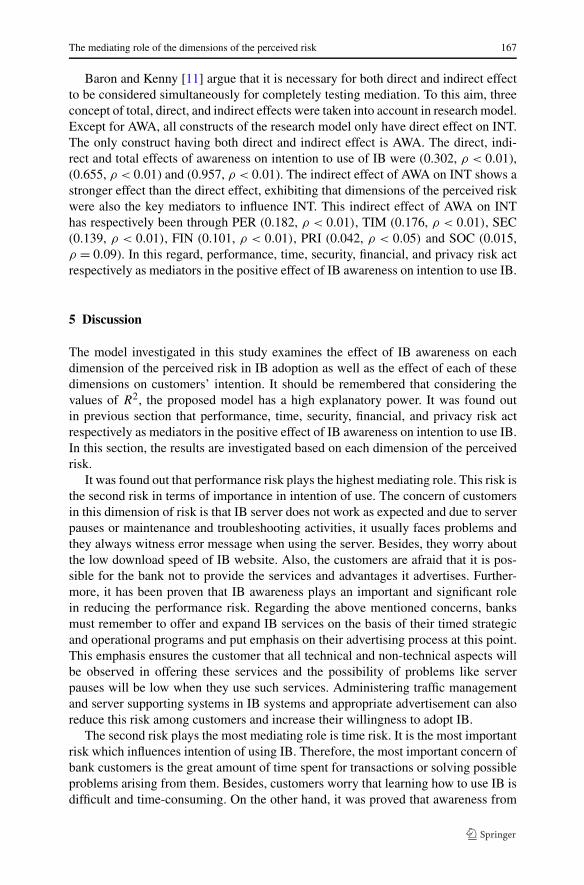

4.3 Hypothesis testing

The results of SEM used in data analysis are shown in Table 8. Also, the results ofstructural model can be observed in Fig. 2. In general, the structural model can beevaluated by two indices. The first one are the path coefficients (β) which show thestrength of relations between independent and dependent variables, and the secondare the values of R2 which show the values of variances explained by independentvariables and reflect the predictive power of the model. As it can be seen from theTable, intention of using IB is significantly influenced by IB awareness and time,performance, security, finical, as well as privacy risks; they, jointly, explain 76.3 %

166 P. Hanafizadeh, H.R. Khedmatgozar

Table 8 Assessment of the structural model

No. From To β R2 t-value p-value Supported?

H1-1 TIM INT −0.54 0.76 −13.54 0.000** Yes

H1-2 FIN −0.21 −4.19 0.000** Yes

H1-3 PER −0.31 −6.39 0.000** Yes

H1-4 SOC −0.05 −1.59 0.11 No

H1-5 SEC −0.29 −6.14 0.000** Yes

H1-6 PRI −0.13 −2.16 0.03* Yes

H2 AWA 0.30 4.43 0.000** Yes

H3-1 AWA TIM −0.33 0.51 −6.19 0.000** Yes

H3-2 FIN −0.47 0.62 −10.41 0.000** Yes

H3-3 PER −0.59 0.75 −12.66 0.000** Yes

H3-4 SOC −0.34 0.52 −6.52 0.000** Yes

H3-5 SEC −0.48 0.63 −10.28 0.000** Yes

H3-6 PRI −0.33 0.61 −7.35 0.000** Yes

Note: **Significance at p < 0.001, *Significance at p < 0.05

Fig. 2 Results of structural modeling analysis

of the total variance in intention. On the one hand, social risk does not significantlyinfluence intention of using IB. Thus, all H1 and H2 hypotheses expect for H1-4 aresupported. On the other hand, IB awareness has significant negative influence on alldimensions of the perceived risk. The values of variance percentage explained byawareness in all these aspects are high. Consequently, all hypotheses from H3-1 toH3-6 are supported.

The mediating role of the dimensions of the perceived risk 167

Baron and Kenny [11] argue that it is necessary for both direct and indirect effectto be considered simultaneously for completely testing mediation. To this aim, threeconcept of total, direct, and indirect effects were taken into account in research model.Except for AWA, all constructs of the research model only have direct effect on INT.The only construct having both direct and indirect effect is AWA. The direct, indi-rect and total effects of awareness on intention to use of IB were (0.302, ρ < 0.01),(0.655, ρ < 0.01) and (0.957, ρ < 0.01). The indirect effect of AWA on INT shows astronger effect than the direct effect, exhibiting that dimensions of the perceived riskwere also the key mediators to influence INT. This indirect effect of AWA on INThas respectively been through PER (0.182, ρ < 0.01), TIM (0.176, ρ < 0.01), SEC(0.139, ρ < 0.01), FIN (0.101, ρ < 0.01), PRI (0.042, ρ < 0.05) and SOC (0.015,ρ = 0.09). In this regard, performance, time, security, financial, and privacy risk actrespectively as mediators in the positive effect of IB awareness on intention to use IB.

5 Discussion

The model investigated in this study examines the effect of IB awareness on eachdimension of the perceived risk in IB adoption as well as the effect of each of thesedimensions on customers’ intention. It should be remembered that considering thevalues of R2, the proposed model has a high explanatory power. It was found outin previous section that performance, time, security, financial, and privacy risk actrespectively as mediators in the positive effect of IB awareness on intention to use IB.In this section, the results are investigated based on each dimension of the perceivedrisk.

It was found out that performance risk plays the highest mediating role. This risk isthe second risk in terms of importance in intention of use. The concern of customersin this dimension of risk is that IB server does not work as expected and due to serverpauses or maintenance and troubleshooting activities, it usually faces problems andthey always witness error message when using the server. Besides, they worry aboutthe low download speed of IB website. Also, the customers are afraid that it is pos-sible for the bank not to provide the services and advantages it advertises. Further-more, it has been proven that IB awareness plays an important and significant rolein reducing the performance risk. Regarding the above mentioned concerns, banksmust remember to offer and expand IB services on the basis of their timed strategicand operational programs and put emphasis on their advertising process at this point.This emphasis ensures the customer that all technical and non-technical aspects willbe observed in offering these services and the possibility of problems like serverpauses will be low when they use such services. Administering traffic managementand server supporting systems in IB systems and appropriate advertisement can alsoreduce this risk among customers and increase their willingness to adopt IB.

The second risk plays the most mediating role is time risk. It is the most importantrisk which influences intention of using IB. Therefore, the most important concern ofbank customers is the great amount of time spent for transactions or solving possibleproblems arising from them. Besides, customers worry that learning how to use IB isdifficult and time-consuming. On the other hand, it was proved that awareness from

168 P. Hanafizadeh, H.R. Khedmatgozar

the advantages, services, and ways of using IB plays a significant role in reducingtime risk. Therefore, banks must take technical actions to reduce the possibility ofdelay in payments and transaction times and inform the customers of these activities.Also, necessary guides and instructions about the possible problems arising at thetime of use must be prepared and provided to the customers to ensure them thatthey will not spend much time solving these problems. Establishing and expandingtelephone guide centers can also be useful in this regard. As Yiu et al. [83] argue,designing demonstrations and advertisements for their use among bank customerscan ensure them that they can easily learn how to use IB.

The security risk is the third risk playing a mediating role. It is the third risk bankcustomers are faced with in adopting IB. This risk is the customers’ concerns regard-ing Internet security and security of IB website. Also, it was proved that awarenesshas a significant role in reducing this risk. Banks are now using various solutions suchas firewalls, filtering routers, callback modems, encryption biometrics, smart cards,digital certificates [59], and two-factor authentication systems [65] for creating secu-rity in IB systems. But these concepts are not understandable for many customers.Giving information about these issues both in technical and non-technical terms en-sures customers that bank is trying to provide the security of IB system in the bestway possible. Another strategy regarding awareness that, through creating sense ofsecurity, can encourage customers for adopting IB is giving information about vari-ous frauds in the area of IB such as phishing [17] and providing the customers withguidelines for protection against these frauds. These cases and third-party trust certi-fication bodies [4, 84] can increase customers’ awareness of security issues and, byreducing this risk in their minds, increase their willingness to adopt IB.

The fourth risk, among the dimensions of the perceived risk, in which IB aware-ness plays a part, is financial risk. This is the fourth risk negatively affecting inten-tion to use IB. Customers’ concern about impossibility of getting compensation frombank in the case of mistake, possibility of erroneous transactional data entry, andfear of losing control over personal account using IB are among the main concernsof customers in this risk. Also, it was proved that awareness plays a significant partin reducing financial risk. Solutions proposed that can reduce this risk and encour-age customers for adopting IB include: 1. Developing and offering guidelines andinstructions which explain customer rights and banks responsibilities in the field ofIB; 2. Giving information about the articles of electronic commerce law that referto the validity of electronic documents resulting from IB transactions; 3. Planning,administering, and advertising about consumer reassurance programs such as aftersale redress policy; 4. Giving information about the features of possibility of con-firming transaction at the same time it is going on which minimizes error possibility;and 5. Expanding IB services which increase user’s authority in managing personalaccount (such as continuous payment planning and giving appropriate informationabout it).

The fifth risk which plays mediating role in the relationship between IB awarenessand intention of IB adoption is privacy risk. It is the fifth and the last risk influencingintention of IB adoption. Banks’ illegal use of customers’ private information and itsresults such as receiving unwanted emails or endangering privacy constitute the mainconcerns of customers in this risk. The role of awareness in reducing this risk was

The mediating role of the dimensions of the perceived risk 169

also proved. Bestavros [15] offered recommendations for reducing this risk whichwere also emphasized by Aldas-Manzano et al. [4]. Considering these recommen-dations and emphasizing the role of awareness in reducing this risk, the followingsolutions are offered: 1. Giving information about articles of electronic commercelaw that places responsibility of disclosing IB customers’ private information uponbank; 2. Placing the issue of protecting customers’, particularly IB customers, privacyin the quality policy of banks and giving information about it; 3. Giving informationand creating trust regarding protection of customers’ privacy at the time of openingaccount; and 4. Designing and launching IB system in a way which does not requiresending email to customers.

On the basis of the results obtained, it became clear that social risk has minor effecton customers’ intention of using IB. This means that customers are not afraid of thenegative attitude of their family, friends, or colleagues, as well as loosing physicalcontact with bank staff. This finding is in line with the findings of Lee [52] regardingthis risk. On the other hand, the role of IB awareness in reducing social risk is proved.These results can be justified in two ways. The first is that sufficient IB awareness ofrespondents’ relatives caused them to have positive view toward IB which made themregard this risk as minor in their responses. Another justification is that according tothe findings of Venkatesh and Davis [78] and Lee [52], social norms, in spite ofsignificant effect on services having obligatory application, have less influence uponthe intention of using services having optional usage like IB.

In most solutions suggested in this section for reducing the dimensions of the per-ceived risk, especial attention has been paid to the concept of advertising. Pikkarainenet al. [64] argued that:

“Banks should now concentrate in their advertising more on informative issuesrather than on building only brands with less informative advertisements”.

As it was mentioned before, the concept of IB awareness was emphasized in thefindings and focusing on customers’ awareness from each dimension of risk, the ef-fect of awareness on intention of IB adoption was explained. This awareness whichcan be explained as giving information rather than merely advertising can be createdthrough various channels like TV, radio, magazines, brochures, shows in ATMs, bankwebsite, weblogs, E-mails, short messages, or public training courses.

6 Conclusion and suggestions

This study followed three aims. The first aim was to investigate the effect of eachdimension of the perceived risk on bank customers’ intention of using IB based on theperceived risk theory. The results showed that except for social risk, other dimensionsof risk including time, performance, security, financial, and privacy has significantnegative effects on IB use.

The second aim was to examine the effect of the concept of IB awareness on eachdimension of the perceived risk in IB adoption. The findings indicated that IB aware-ness reduces all aspects of the perceived risk (respectively, performance, security,financial, social, privacy, and time).

The third aim of this study was to determine if it was possible on the basis ofthe results to consider a mediating role for each dimension of the perceived risk in

170 P. Hanafizadeh, H.R. Khedmatgozar

Fig. 3 The mediating role ofdimensions of the perceived riskin the relationship betweenconcept of awareness and IBadoption

the relationship between the concept of awareness and IB adoption. According to theresults, it was found out that IB awareness has a significant role in increasing theintention of using IB. Considering this finding and the results of the first and secondaims, it can be concluded that IB awareness, regarding its direct positive effect onthe intention, by reducing the dimensions of the perceived risk, indirectly reducestheir negative effect on the intention and thus results in the increase in customers’willingness to adopt IB. According to these results, it was found out that Customers’IB awareness affects intention to use IB through the mediation of performance, time,security, financial, and privacy risks, respectively. (Of course, it must be mentionedthat considering the results of the first aim, this effect is not true in the case of socialrisk.) Figure 3 clearly shows this mediating effect.

Finally, regarding these results, solutions based on the concept of IB awarenesswere offered applying which within the framework of marketing strategies like pulland push [27] and customer targeting [22] banks can reduce the perceived risk oftheir customers for adopting IB.

With respect to the limitations of this study, suggestions can be proposed for de-veloping the model under investigation both from a theoretical and survey point ofview.

As it was mentioned in Sect. 4.3, 23.7 % of the variance of intention of researchwas not explained by the dimensions of the perceived risk and IB awareness. Thiscan be attributed to not entering other factors influencing the intention to use IB inresearch model. In this respect and in order to reduce this value, one suggestion forfuture research can be made as simultaneous investigation of the dimensions of theperceived risk and other variables affecting intention to use IB according to modelsand theories proposed in the area of IB adoption.

In this study, the research model is investigated cross-sectionally. This means thatthe research model is investigated according to views expressed by the respondents atone point of time. This approach, as one of the common approaches, was selected dueto theoretical and survey limitations. Another approach to be utilized is longitudinalapproach. The method used by this approach is to collect the views of respondentsthrough a survey. Then, by dividing the respondents into two test and control groupsduring a time period, comprehensive information on IB is provided to test groupsand at the end of this period, the views of respondents are measured again. Throughthis method and by comparing the results obtained from two groups, the effect of

The mediating role of the dimensions of the perceived risk 171

IB awareness on the dimensions of the perceived risk and intention to use IB can beinvestigated.

As it was mentioned in Sect. 3.1, the statistical population of the research is com-posed of bank customers who do not actively use IB. The sampling was also con-ducted from this population. According to the reasons pointed out in this section, itis argued that excluding customer actively using IB does not cause bias in the resultsobtained; rather, it leads to better explanation of the results. However, this issue canbe considered as one limitation of the present study. For an in depth analysis, It issuggested that future studies embark on comparing the results obtained from thesetwo statistical population.

This study was conducted in Iran with its unique geographical, cultural, and eco-nomic features. Considering previous studies on similar models and theories, it seemsthat changes in the mentioned features would result in change in the type and powerof the relations within the model. Thus, another suggestion for future research is toinvestigate cultural, national, geographical, and economic restrictions of populationregarding the concepts of awareness, dimensions of the perceived risk, and the rela-tionship among them. In other words, interpretation of the results of research modelby focusing upon cultural, national, and economic features of the countries can pavethe way for expanding an area of IB adoption studies, called comparative studies onIB adoption based on target community.

References

1. Ajzen, I. (1985). From intentions to actions: a theory of planned behavior. In J. Kuhl & J. Beckmann(Eds.), Action control: from cognition to behavior (pp. 11–39). Heidelberg: Springer.

2. Akinci, S., Aksoy, S., & Atilgan, E. (2004). Adoption of Internet banking among sophisticated con-sumer segments in an advanced developing country. International Journal of Bank Marketing, 22(3),212–232.

3. Aladwani, A. M. (2001). Online banking: a field study of drivers, development challenges and expec-tations. International Journal of Information Management, 21(3), 213–225.

4. Aldas-Manzano, J., Lassala-Navarre, C., Ruiz-Mafe, C., & Sanz-Blas, S. (2009). The role of consumerinnovativeness and perceived risk in online banking usage. International Journal of Bank Marketing,27(1), 53–75.

5. Al-Somali, S. A., Gholami, R., & Clegg, B. (2009). An investigation into the acceptance of onlinebanking in Saudi Arabia. Technovation, 29(2), 130–141.

6. Anderson, J. C., & Gerbing, D. W. (1988). Structural equation modeling in practice: a review andrecommended two-step approach. Psychological Bulletin, 103(3), 411–423.

7. Angelakopoulos, G., & Mihiotis, A. (2011). E-banking: challenges and opportunities in the Greekbanking sector. Electronic Commerce Research, 11(3), 297–319.

8. Association of Payment Clearing Services (Apacs). http://www.ukpayments.org.uk/media_centre/press_releases/-/page/871/. Last accessed on 2010-10-24.

9. Azouzi, D. (2009). The adoption of electronic banking in Tunisia: An exploratory study. Journal ofInternet Banking and Commerce, 14(3), 1–11.

10. Bandura, A. (1986). Social foundations of thought and action: A social cognitive theory. EnglewoodCliffs: Prentice-Hall.

11. Baron, R., & Kenny, D. (1986). The moderator-mediator variable distinction in social psychologi-cal research: Conceptual, strategic and statistical considerations. Journal of Personality and SocialPsychology. Monograph Supplement, 51(6), 1173–1182.

12. Barrett, P. (2007). Structural equation modeling: Adjudging model fit. Personality and IndividualDifferences, 42(5), 815–824.

13. Bentler, P. M. (1990). Comparative fit indexes in structural models. Psychological Bulletin, 107(2),238–246.

172 P. Hanafizadeh, H.R. Khedmatgozar

14. Bentler, P. M., & Bonett, D. G. (1980). Significance tests and goodness of fit in the analysis of covari-ance structures. Psychological Bulletin, 88(3), 588–606.

15. Bestavros, A. (2000). Banking industry walks ‘tightrope’ in personalization of web services. BankSystems + Technology, 37(1), 54–56.

16. Bollen, B., & Long, B. C. (1993). Testing structural equation models. Newbury Park: Sage.17. Butler, R. A. (2007). Framework of anti-phishing measures aimed at protecting the online consumer’s

identity. Electronic Library, 25(5), 517–533.18. Castañeda, J. A., & Montoro, F. J. (2007). The effect of Internet general privacy concern on customer

behavior. Electronic Commerce Research, 7(2), 117–141.19. Central Bank of I.R. Iran. http://www.cbi.ir/simplelist/2546.aspx. Last accessed on 2010-10-24.20. Chan, S., & Lu, M. (2004). Understanding Internet banking adoption and use behavior: a Hong Kong

perspective. Journal of Global Information Management, 12(3), 21–43.21. Chau, P. Y. K. (1997). Re examining a model for evaluating information center success using a struc-

tural equation modeling approach. Decision Sciences, 28(2), 309–334.22. Chiang, M. H., & Teng, C. I. (2003). Installed base collapsing strategies with network externalities.

Journal of Management, 20(5), 829–857.23. Cook, J. D., Hepworth, S. J., Wall, T. D., & Warr, P. B. (1981). The experience of work. San Diego:

Academic Press.24. Cooper, R. G. (1997). Examining some myths about new product winners. In R. Katz (Ed.), The

human side of managing technological innovation (pp. 550–560). London: Oxford University Press.25. Davis, F. D. (1989). Perceived usefulness, perceived ease of use, and user acceptance of computer

technology. Management Information Systems Quarterly, 13(3), 319–340.26. DePallo, M. (2000). National survey on consumer preparedness and e-commerce: A survey of com-

puter users age 45 and older. Washington: AARP.27. Dowling, G. R. (2004). The art and science of marketing. Oxford: Oxford University Press.28. Eriksson, K., Kerem, K., & Nilsson, D. (2008). The adoption of commercial innovations in the former

Central and Eastern European markets: The case of Internet banking in Estonia. International Journalof Bank Marketing, 26(3), 154–169.

29. Featherman, M. S., & Pavlou, P. A. (2003). Predicting e-services adoption: a perceived risk facetsperspective. International Journal of Human-Computer Studies, 59(4), 451–474.

30. Fishbein, M., & Ajzen, I. (1975). Belief, attitude, intention, and behavior: an introduction to theoryand research. Reading: Addison Wesley.

31. Fornell, C., & Larcker, D. F. (1981). Evaluating structural equation models with unobservable vari-ables and measurement error. Journal of Marketing Research, 18(1), 39–50.

32. Gemünden, H. G. (1985). Perceived risk and information search: a systematic meta-analysis of theempirical evidence. International Journal of Research in Marketing, 2(2), 79–100.

33. Gerrard, P., Cunningham, J. B., & Devlin, J. F. (2006). Why consumers are not using Internet banking:a qualitative study. The Journal of Services Marketing, 20(3), 160–168.

34. Gholami, R., Dolores Anon Higon, M., Hanafizadeh, P., & Emrouznejad, A. (2010). Is ICT the key todevelopment? Journal of Global Information Management, 18(1), 66–83.

35. Hair, J. F., Anderson, R. E., Tatham, R. L., & Black, W. C. (1995). Multi-variate data analysis withreadings. Englewood Cliffs: Prentice-Hall International.

36. Hatcher, L. (1994). A step-by-step approach to using the SAS(R) system for factor analysis and struc-tural equation modeling. Cary: SAS Institute.

37. Heeler, R. M., & Ray, M. L. (1972). Measure validation in marketing. Journal of Marketing Research,9(4), 361–370.

38. Hernandez, J. M. C., & Mazzon, J. A. (2007). Adoption of Internet banking: proposition and imple-mentation of an integrated methodology approach. International Journal of Bank Marketing, 25(2),72–88.

39. Hinkin, T. R. (1995). A review of scale development practices in the study of organizations. Journalof Management, 21(5), 967–988.

40. Howcroft, B., Hamilton, R., & Hewer, P. (2002). Consumer attitude and the usage and adoption ofhome-based banking in the United Kingdom. International Journal of Bank Marketing, 20(2), 111–121.

41. Hu, L. T., & Bentler, P. M. (1998). Fit indices in covariance structure modeling: Sensitivity to underparameterized model misspecification. Psychological Methods, 3(4), 424–453.

42. Internet Word State (UK). http://www.Internetworldstats.com/eu/uk.htm. Last accessed on 2010-10-24.

The mediating role of the dimensions of the perceived risk 173

43. Internet Word State (IRI). http://www.Internetworldstats.com/me/ir.htm. Last accessed on 2010-10-24.

44. Jackson, P. R., Wall, T. D., Martin, R., & Davids, K. (1993). New measures of job control, cognitivedemand, and production responsibility. Journal of Applied Psychology, 78(5), 753–762.

45. Jacoby, J., & Kaplan, L. B. (1972). The components of perceived risk. Paper presented at the 3rdAnnual Convention of the Association for Consumer Research, Chicago, Illinois, 2–6 November.

46. Jarvenpaa, S. L., & Todd, P. A. (1997). Consumer reactions to electronic shopping on the World WideWeb. Journal of Electronic Commerce Research, 1(2), 59–88.

47. Jun, M., & Cai, S. (2001). The key determinants of Internet banking service quality: A content analy-sis. International Journal of Bank Marketing, 19(7), 276–291.

48. Kalakota, R., & Whinston, A. (1997). Electronic commerce: a manager’s guide. Reading: AddisonWesley.

49. Kaplan, L. B., Szybillo, G. J., & Jacoby, J. (1974). Components of perceived risk in product purchase:a cross validation. Journal of Applied Psychology, 59(3), 278–291.

50. Kenny, D. A. (2001). Measuring model fit. New York: Wiley.51. Lai, V. S., & Li, H. (2005). Technology acceptance model for Internet banking: an invariance analysis.

Information & Management, 42(2), 373–386.52. Lee, M. C. (2009). Factors influencing the adoption of Internet banking: An integration of TAM and

TPB with perceived risk and perceived benefit. Electronic Commerce Research and Applications, 8(3),130–141.

53. Lichtenstein, S., & Williamson, K. (2006). Understanding consumer adoption of Internet banking: aninterpretive study in the Australian context. Journal of Electronic Commerce Research, 7(2), 50–66.

54. Lim, N. (2003). Consumers’ perceived risk: sources versus consequences. Electronic Commerce Re-search and Applications, 2(3), 216–228.

55. Littler, D., & Melanthiou, D. (2003). Consumer perceptions of risk and uncertainty and the implica-tions for behavior towards innovative retail services: the case of Internet banking. Journal of Retailingand Consumer Services, 13(6), 431–443.

56. Mandrik, C. A., & Bao, Y. (2005). Exploring the concept and measurement of general risk aversion.Advances in Consumer Research, 32, 531–539.

57. Marsh, H. W., & Hocevar, D. (1985). Application of confirmatory factor analysis to the study ofself-concept: First- and higher order factor models and their invariance across groups. PsychologicalBulletin, 97(3), 562–582.

58. Morgan, R. M., & Hunt, S. D. (1994). The commitment-trust theory of relationship marketing. Journalof Marketing, 58(1), 20–38.

59. Mukherjee, A., & Nath, P. (2003). A model of trust in online relationship banking. InternationalJournal of Bank Marketing, 21(1), 5–15.

60. Narayanasamy, K., Rasiah, D., & Tan, T. M. (2011). The adoption and concerns of e-finance inMalaysia. Electronic Commerce Research, 11(4), 383–400.

61. Ndubisi, N. O. (2007). Customers’ perceptions and intention to adopt Internet banking: the moderationeffect of computer self-efficacy. Journal of Knowledge, Culture and Communication (AI & SOCIETY),21(3), 315–327.

62. Nunnally, J. C. (1978). Psychometric theory (Vol. 2). New York: McGraw-Hill.63. Pavlou, P. A. (2003). Consumer acceptance of electronic commerce: integrating trust and risk with

the technology acceptance model. International Journal of Electronic Commerce, 7(3), 101–134.64. Pikkarainen, T., Pikkarainen, K., Karjaluoto, H., & Pahnila, S. (2004). Consumer acceptance of online

banking: an extension of the technology acceptance model. Internet Research, 14(3), 224–235.65. Polasik, M., & Wisniewski, T. P. (2009). Empirical analysis of Internet banking adoption in Poland.

International Journal of Bank Marketing, 27(1), 32–52.66. Prompattanapakdee, S. (2009). The adoption and use of personal Internet banking services in Thai-

land. The Electronic Journal on Information Systems in Developing Countries, 37(6), 1–31.67. Rogers, E. M. (1983). Diffusion of innovations. New York: Free Press.68. Rogers, E. M., & Shoemaker, F. (1971). Communications in innovation. New York: Free Press.69. Roselius, T. (1971). Consumer rankings of risk reduction methods. Journal of Marketing, 35(1), 56–

61.70. Sathye, M. (1999). Adoption of Internet banking by Australian consumers: an empirical investigation.

International Journal of Bank Marketing, 17(7), 324–334.71. Sayar, C., & Wolfe, S. (2007). Internet banking market performance: Turkey versus the UK. Interna-

tional Journal of Bank Marketing, 25(3), 122–141.

174 P. Hanafizadeh, H.R. Khedmatgozar

72. Schriesheim, C. A., & Hill, K. (1981). Controlling acquiescence response bias by item reversal: Theeffect on questionnaire validity. Educational and Psychological Measurement, 41(4), 1101–1114.

73. Segars, A. H., & Grover, V. (1993). Re-examining perceived ease of use and usefulness: a confirma-tory factor analysis. Management Information Systems Quarterly, 17(4), 517–525.

74. Spector, P. E. (1992). Summated rating scale construction: An introduction. Sage University paperseries on quantitative applications in the social sciences. Newbury Park: Sage.

75. Straub, D., Boudreau, M. C., & Gefen, D. (2004). Validation guidelines for IS positivist research.Communications of the Association for Information Systems, 13, 380–427.

76. Suh, B., & Han, I. (2002). Effect of trust on customer acceptance of Internet banking. ElectronicCommerce Research and Applications, 1(3), 247–263.

77. Taylor, S., & Todd, P. A. (1995). Understanding information technology usage: a test of competingmodels. Information Systems Research, 6(2), 144–176.

78. Venkatesh, V., & Davis, F. D. (2000). A theoretical extension of the technology acceptance model:four longitudinal field studies. Management Science, 45(2), 186–204.

79. Venkatesh, V., Morris, M. G., Davis, G. B., & Davis, F. D. (2003). User acceptance of informationtechnology: toward a unified view. Management Information Systems Quarterly, 27(2), 425–478.

80. Vrechopoulos, A. P., Siomkos, G. J., & Doukidis, G. I. (2001). Internet shopping adoption by Greekconsumers. European Journal of Innovation Management, 4(3), 142–153.

81. Westland, J. C. (2002). Transaction risk in electronic commerce. Decision Support Systems, 33(1),87–103.

82. White, H., & Nteli, F. (2004). Internet banking in the UK: why are there not more customers? Journalof Financial Services Marketing, 9(1), 49–56.

83. Yiu, C. S., Grant, Y. K., & Edgar, D. (2007). Factors affecting the adoption of Internet banking inHong Kong: implications for the banking sector. International Journal of Information Management,27(5), 336–351.

84. Yousafzai, S. Y., Pallister, J. G., & Foxall, G. R. (2003). A proposed model of e-trust for electronicbanking. Technovation, 23(11), 847–860.

85. Zhao, A. L., Hanmer-Lloyd, S., Ward, P., & Goode, M. M. H. (2008). Perceived risk and Chineseconsumers’ Internet banking services adoption. International Journal of Bank Marketing, 26(7), 505–525.

86. Zolait, A. H. S., & Ainin, S. (2008). Incorporating the innovation attributes introduced by Rogers’ the-ory into theory of reasoned action: An examination of Internet banking adoption in Yemen. Computerand Information Science, 1(1), 36–51.

Payam Hanafizadeh is an Assistant Professor at the School of Man-agement and Accounting (formerly Tehran Business School) at Al-lameh Tabataba’i University in Tehran, Iran and a member of the De-sign Optimization under Uncertainty Group at the University of Water-loo, Canada. He was a visiting research fellow at the Faculty of Busi-ness and Government, University of Canberra, Australia in 2010 and avisiting scholar at the Department of Systems Design Engineering, Uni-versity of Waterloo, Canada in 2004. He received his M.Sc. and Ph.D.in Industrial Engineering from Tehran Polytechnic University and pur-sues his research in Information Systems and Decision-making underUncertainty. He is the co-author of Online Advertising and Promotion:Modern Technologies for Marketing, published 2012 by IGI Global,USA. He has published more than 50 articles in reputable journals suchas the Information Society, Journal of Global Information Management,Telecommunications Policy, Systemic Practice and Action Research,

Electronic Commerce Research, Energy Policy, Management Decision, Journal of Information Technol-ogy Research, Higher Education Policy, Mathematical and Computer Modeling, Expert Systems with Ap-plications, International Journal of Information Management, among others. Dr. Hanafizadeh has also beenserving on the Editorial Review Board for the International Journal of Information Technologies and Sys-tems Approach, the International Journal of Enterprise Information Systems, the Journal of InformationTechnology Research, the Journal of Electronic Commerce in Organizations, and the International Journalof Decision Support System Technology.

The mediating role of the dimensions of the perceived risk 175

Hamid Reza Khedmatgozar holds a B.Sc. in Industrial Engineeringfrom Yazd University, Yazd, Iran, and a Master’s degree in FinancialEngineering from University of Science and Culture, Tehran, Iran. Hisrecent research appears in Electronic Commerce Research. Currently,he is a Ph.D. Student of Information Technology (IT) Management atIranian Research Institute for Information Science and Technology-IRANDOC, Tehran, Iran. His research interests revolve around ITAdoption in Financial Markets and Risk Management.

Related Documents