INTERNATIONAL ACCOUNTING AND BUSINESS CONFERENCE 2011 PROCEEDINGS IABC2011 Page 1 THE MARKET VALUATION OF R&D: EMPIRICAL EVIDENCE FROM MALAYSIAN FIRMS SUNARTI BINTI HALID AMIZAHANUM BINTI ADAM NUR ADURA BINTI AHMAD NORUDDIN MASETAH BINTI AHMAD TARMIZI Faculty of Accountancy Universiti Teknologi MARA Seri Iskandar Campus 32610 Bandar Baru Seri Iskandar Perak Malaysia [email protected] Abstract Purpose - The major objective of this study is to understand and recognize the value relevance of research and development (R&D) in market valuation. The firms selected for this study is from Malaysia from the period 2000-2007. This study have examined whether the market perceived R&D information as an important variable in determining the value of a company. Specifically, this study empirically investigated the association between R&D information in determining and explaining the market value. The study also described a relationship between R&D with all other assets. Furthermore, we examined the relationship between the R&D and the sign of earnings items. Design/methodology/approach - An equity valuation model based on the modified balance sheet identity was used to permit R&D and other assets to have separate empirical coefficient values. Findings - This study found weak empirical support at best for the value relevance of R&D at the firm level. However, market was taken into consideration BVNA in determining the firm‟s equity value as compared to R&D. Also, the results showed that the market‟s valuation of R&D is not priced differently from other assets. In addition, our results provided evidence that there is no significant relationship between R&D information and the sign of earnings items. Originality/value - This study employs an approach using the equity valuation model to measure the value relevance of R&D in market valuation. Keywords - Research and Development, Market Valuation, Equity Valuation Model Paper type - Research Paper

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

INTERNATIONAL ACCOUNTING AND BUSINESS CONFERENCE

2011

PROCEEDINGS IABC2011 Page 1

THE MARKET VALUATION OF R&D:

EMPIRICAL EVIDENCE FROM MALAYSIAN FIRMS

SUNARTI BINTI HALID

AMIZAHANUM BINTI ADAM

NUR ADURA BINTI AHMAD NORUDDIN

MASETAH BINTI AHMAD TARMIZI

Faculty of Accountancy

Universiti Teknologi MARA

Seri Iskandar Campus

32610 Bandar Baru Seri Iskandar

Perak Malaysia

Abstract

Purpose - The major objective of this study is to understand and recognize the value relevance

of research and development (R&D) in market valuation. The firms selected for this study is

from Malaysia from the period 2000-2007. This study have examined whether the market

perceived R&D information as an important variable in determining the value of a company.

Specifically, this study empirically investigated the association between R&D information in

determining and explaining the market value. The study also described a relationship between

R&D with all other assets. Furthermore, we examined the relationship between the R&D and the

sign of earnings items.

Design/methodology/approach - An equity valuation model based on the modified balance

sheet identity was used to permit R&D and other assets to have separate empirical coefficient

values.

Findings - This study found weak empirical support at best for the value relevance of R&D at

the firm level. However, market was taken into consideration BVNA in determining the firm‟s

equity value as compared to R&D. Also, the results showed that the market‟s valuation of R&D

is not priced differently from other assets. In addition, our results provided evidence that there is

no significant relationship between R&D information and the sign of earnings items.

Originality/value - This study employs an approach using the equity valuation model to

measure the value relevance of R&D in market valuation.

Keywords - Research and Development, Market Valuation, Equity Valuation Model

Paper type - Research Paper

INTERNATIONAL ACCOUNTING AND BUSINESS CONFERENCE

2011

PROCEEDINGS IABC2011 Page 2

Introduction

Research and development (R&D) is perceived part of the innovation process which involve the

translation of knowledge into tangible output. However, according to Dato‟ Shaziman bin Abu

Mansor, Minister of Works, in Construction Industry Research Achievement International

Conference (2009), „‟the translating R&D into something tangible in the market is challenge”.

He added it is normal to expect less than five percent R&D results to reach the market in

Malaysia.

To promote the R&D in Malaysia, Multimedia Super Corridor (MSC) Malaysia had allocated

RM85 million for the MSC Malaysia Research and Development Grant Scheme (MGS) which

help the company to develop its ICT/Multimedia products to its full commercial potential. Other

than that, Malaysian Industrial Development Authority (MIDA) had introduced various

incentives for R&D, which among others include give pioneer status with income tax exemption

of 100% of the statutory income for five years and Investment Tax Allowance (ITA) of 100% on

the qualifying capital expenditure incurred within 10 years; to a contract R&D company i.e. a

company that provides R&D services in Malaysia to a company other than its related company.

R&D is an expensive activity where it requires an investment of certain amount of capital with

the belief that they would result in some increased benefits in the future periods. The evidence

from previous study seems to indicate that the company that will received benefit from the R&D

activities basically those in the high-technology industries. Chamberlain‟s (1999) study on share

price reaction to R&D spending announcements for a sample of Canadian companies revealed

that investors react differently to R&D announcements by high and low technology firms and

that the market's assessment of R&D spending plans may be influenced by other factors, such as

insider trading activity. It is collaborate with findings discovered by Chan et al. (1990) which

found that investors reacted positively to the announcement of R&D expenditures especially

firms in the high-technology sector.

In Malaysia, with various governments‟ incentives, the R&D activity was still considered

relatively low. European Commission in Comparative Analysis of R&D Developments in

Malaysia (1992) reported that the R&D activities in Malaysia mainly in high technology by

foreign multinational companies (MNCs) but were conducted outside Malaysia and often in their

home countries. While, manufacturing by local enterprise were mainly in the low technology

sector which requires minimal R&D activities. Alfan (2003) reported that the amount spend on

R&D was very much less compared to other countries such as the United States, Japan and

Germany. Alfan found that from a survey by the Malaysia Science and Technology Information

Centre (MASTIC) revealed that the major factors contribute to the lack of R&D activities was

due to the lack of R&D strategy and shortage of expert R&D personnel.

INTERNATIONAL ACCOUNTING AND BUSINESS CONFERENCE

2011

PROCEEDINGS IABC2011 Page 3

Most current studies produce results that accounting number of R&D has value-relevance or in

other words has future economic benefit. Many researchers have conjectured that benefits from

the research and development are plausible. According to Nobelius (2004), R&D has been

studied for a long time within different contexts, economies and environmental demands

throughout the years. Nevertheless, whether information on intangible assets reported under

current financial reporting requirements conveys information that is value relevant to market

participants‟ valuation of firms‟ equity has long been a question of interest to accounting

policymakers and researchers.

Basically, the primary purpose for conducting the tests of value relevance is to extend our

knowledge regarding the relevance and reliability of accounting numbers as reflected in equity

values. The value relevance research assesses how well accounting numbers reflect information

used by equity investors. Besides, the findings of this research should be important for those

involved in the setting and monitoring of standards, as relevance and reliability are the two

primary criteria in accounting conceptual framework.

However, one could pose the question as to whether the controversy surrounding R&D is really

important or whether it is just making „noise‟ in the security market. Apart from that, one of the

possibilities is to examine whether the market perceives the amount of R&D as an important

variable in the determination of the value of a company. As a complement, the empirical aims of

this study are to investigate the relationship between R&D disclosures in accounts and market

values and the relationship between R&D with other assets. Apart from that, this paper uses an

equity market value as the valuation benchmark for a sample firms from Malaysian over a period

of seven years from 2000 to 2007. Further, we examined the relationship between R&D and the

sign of earnings items. Earnings items are used as a proxy throughout the study period.

Literature Review

Value Relevance of Accounting Numbers

Accounting information is considered as the most important mechanism for the investors to

evaluate the performance of the company. It is an important way for companies to communicate

with the market participants. Meanwhile, value relevance is the ability of accounting numbers to

confine information relevant to equity valuation. In other words, accounting numbers is defined

as value relevant if it has a predicted association with equity market values. Basically, value

relevance most commonly measured by the r-squared in a regression of market price on

accounting information. The greater the variables of the explanatory power of specific financial

statement, the greater would be the value relevance.

Many of the researches have shown that financial statements and other accounting information

play a vital role in the capital markets since they provide essential information about the value of

INTERNATIONAL ACCOUNTING AND BUSINESS CONFERENCE

2011

PROCEEDINGS IABC2011 Page 4

firms. The distribution of value-relevant accounting information helps to reduce the information

asymmetry among the investors. Furthermore, Jenkins (2002) stated that value relevance in the

accounting literature refers to the strength of the relationship between accounting information

and stock market valuation. Besides, value relevance means measuring the degree to which

markets responds to reported accounting information or, in other words, the degree to which

accounting information is able to drive equity prices.

Francis and Schipper (1999) operationalize value relevance in two ways. The first measure of

relevance focuses on the market-adjusted returns, which could be earned, based on

foreknowledge of financial statement information. Meanwhile, second measure is based on the

explanatory power of accounting information for measurers of market value. The first relation

investigates the ability of earnings to explain annual market-adjusted returns (earnings relation);

the second examines the ability of assets and liabilities to explain market value of equity

(balance sheet relation); and the third examines the ability of book values and earnings to explain

market equity values (book value and earnings relation).

As mentioned by Barth et al. (2001), value relevance studies use various valuation models to

tests of specific null and alternative hypotheses regarding relevance and reliability. Moreover,

numerous papers use equity market value as the valuation benchmark to assess how well

particular accounting numbers reflect information used by investors. The tests often focus on the

coefficient on the accounting numbers in the estimation equation. Holthausen and Watts (2001)

classify the value relevance study into three categories. According to them, the first category is

the relative association studies that compare the association between stock market values and

alternative bottom lines measurers. The accounting number with the greater r-squared is

described as being more value relevant. Meanwhile, the second category is the incremental

association studies that determine whether the accounting number of interest is helpful in

explaining value given other specified variables. Thus, the accounting number is typically

deemed to be value relevant if its estimated regression coefficient is significantly different from

zero. Holthausen and Watts also noted the third category is marginal information content studies

that investigate whether a particular accounting number adds to the information set available to

investors. This type of research typically uses event studies to determine if the release of an

accounting number is associated with value changes. Price reactions are considered evidence of

value relevance.

A study done by Landsman (1986), which shows the relationship between market values and

accounting numbers, is to look at empirical evidence of the relationship between pension funds

assets and liabilities and the market value of shareholder equity. The data used in his study was

taken from United States companies over three annual accounting periods, from 1979 to 1981.

Landsman employed an equity valuation model based on the balance sheet identity, which

permitted pension and non-pension assets and liabilities to have separate empirical coefficient

values. His model was based on the fundamental accounting identity, which holds that

shareholders‟ equity is the residual of corporate assets less corporate liabilities. By using this

INTERNATIONAL ACCOUNTING AND BUSINESS CONFERENCE

2011

PROCEEDINGS IABC2011 Page 5

equation, Landsman was able to compare the coefficient values of non-pension assets and

liabilities to their pension counterparts. The empirical findings of this study show the market

prices the assets and liabilities of pension funds as part of the corporate assets and liabilities.

Landsman (1986) lists four econometric problems associated with estimation of the model. One

of the major econometric problems when estimating the cross-sectional valuation model is the

problem of heteroscedasticity disturbance. This problem arises from the fact that large or small

firms tend to produce large or small disturbance. The independent variable that was used in

Landsman‟s study is the total sales value of the firm. Landsman (1986) also discusses the

problem of multicollinearity due to the existence of a linear relationship among the explanatory

variables of regression model. The presence of a severe multicollinearity problem could result in

misleading inferences being drawn from sample t-statistics. In particular, in a case where the

sample t-statistics are unbiased, if there are no other econometric problems, it is difficult to

determine whether the sampling variances are large because of multicollinearity, or whether the

variance of the true population is large. In order to reduce this problem, Landsman estimated his

model using the net asset form; using net non-pension assets and net pension assets.

Besides, Gopalakrishnan and Sugrue (1993) extended the work of Landsman (1986) in pension

fund property rights. The main findings of their study indicated that investors perceive pension

assets and liabilities as part of corporate assets and liabilities. Furthermore, it shows that pension

assets and liabilities have significant information content beyond what is conveyed by non-

pension assets and liabilities. On the other side, Dhaliwal (1986) examined empirically whether

capital market participants view unfunded vested pension obligations as debt liabilities in

assessing the market risk of the firm. A test was conducted in their study in order to examine the

effect of the inclusion of unfunded vested pension obligations in the measurement of financial

leverage on the explanatory power of the model. Dhaliwal reported that the market views these

pension liabilities as a form of a debt and the market is capable of using the footnote disclosure

regarding unfounded vested liabilities in its assessment of market risk. Therefore, there is no

reason to incorporate this information into the balance sheet.

Kane and Unal (1990) reported on their empirical investigation of structural and temporal

variation in the market‟s valuation of banking firms. The authors developed a model to capture

the hidden reserves in United States banking firms. According to them, hidden capital exists

whenever the accounting measure of a firm‟s net worth diverges from its economic value. Such

unbooked capital has on-balance-sheet and off-balance-sheet sources. Kane and Unal developed

a model to estimate both forms of hidden capital and to test hypotheses about their determinants.

Therefore, the model makes direct use of accounting information on the bookable position of a

firm and separate bookable from unbookable sources of value. Kane and Unal (1990) used

regression analysis to partition the market value of a firm‟s stock into two components. The two

components namely recorded capital reserves and unrecorded (or hidden) net worth. In their

study, hidden capital is, in turn, allocated between values that are either unbooked or bookable

through asset turnover or write-downs on a historical-cost balance sheet under General Accepted

INTERNATIONAL ACCOUNTING AND BUSINESS CONFERENCE

2011

PROCEEDINGS IABC2011 Page 6

Accounting Practices (GAAP) or values, which GAAP currently designated as an unbookable off

balance-sheet item.

Francis and Schipper (1999) argued that financial statements have lost a significant portion of

their relevance to investors, specifically over the period of 1952 until 1994. This finding and its

implications raise concerns among financial accountants, standard-setters, educators and

auditors, and have given rise to a number of research and policy initiatives whose common goal

is to improve financial reporting by altering the current financial reporting model. The

interpretation of value relevance as given by Francis and Schipper is based on value relevance as

indicated by a statistical association between financial information and prices or returns. The

statistical association measures whether investors actually use the information in question in

setting prices, hence, value relevance would be measured by the ability of information in

financial statements to change the total mix of information in the marketplace. Moreover, they

noted a decline in the value relevance of earnings and an increase in the value relevance of book

value over time for the United States firms. These studies also found no evidence that the value

relevance of the combined earnings and book values has declined over time.

Francis and Schipper (1999) also compared the value relevance of accounting information

between high and low technology firms. The results indicated that high technology firms have

not experienced a greater decline in the value relevance of accounting information (earnings and

book value) compared to low technology firms. Meanwhile, according to Barth et al. (2001), a

primary focus of financial statements is equity investment. As well, the primary purpose for

conducting tests of value relevance is to extent our knowledge regarding the relevance and

reliability of accounting amounts as reflected in equity values. It is supported by Ball and Brown

(1968), where the financial information is relevant if it summarizes or captures the factors that

affect security prices. Furthermore, value relevance in the accounting literature refers to the

strength of the relationship between accounting information and stock market valuation (Jenkins,

2002). Indeed, value relevance is measuring the degree to which the market responds to reported

accounting information in the financial statement. Similarly, another study by Chen et al. (2001)

reported that accounting information is value-relevant in the Chinese market according to both

the pooled cross-section and time series regressions or the year-by-year regression.

Arce and Mora (2002) studied the differences in the value relevance of earnings and book value

across eight European countries that represent the most important capital markets in Europe.

Their findings revealed a significant difference in the value relevance of earnings and book value

in all countries under study except Belgium and Italy. Earnings are more value relevant than

book value in the United Kingdom, the Netherlands and France. Meanwhile, book value is more

relevant than earnings in Germany, Switzerland and Spain. Apart from that, Black and White

INTERNATIONAL ACCOUNTING AND BUSINESS CONFERENCE

2011

PROCEEDINGS IABC2011 Page 7

(2003) has examined the effect of earnings sign, firm size and macroeconomics events on the

value relevance of earnings and book value in three countries. The samples of countries selected

for their study were Germany, Japan and the United States. In their study, they compared the

value relevance of earnings relative to book value of equity. Their study hypothesizes that book

values are more value relevant than earnings in Germany and Japan while earnings are more

value relevant in the United States, because capital providers in Germany and Japan are more

concerned with balance sheet measurers such as liquidity. The results show that Germany are

robust, as book value is more value relevant for both positive and negative earnings, in all years

with sufficient sample sizes, and for all size quartiles. However, their findings suggested that

earning sign, firm size and macroeconomic events affect the value relevance of earnings and

book value in Japan and the United States.

Value Relevance of Intangibles

There is an extensive body of literature review providing empirical evidence on the relevance of

intangibles for equity valuation and, therefore, pointing out the need to take intangibles into

account in investment, credit and management decision-making. McCarthy and Schneider (1995)

analyzed the market perception of goodwill as an asset in the determination of a firm‟s valuation

in the United States market. They also examined how the market perceives goodwill in relation

to all other assets. Their findings show that investors perceive goodwill as an asset when valuing

a firm and suggest that the market include goodwill when valuing a company. Besides, another

finding is that, relative to book value, goodwill is valued by the market at least as much as other

assets.

Jennings et al. (1996) also studied the relationship between purchased goodwill and market

value. The authors examined the relation between equity values and accounting goodwill

numbers in the United States during the period 1982-1988. The study indicates a strong cross-

sectional relation between equity values and accounting assets and liabilities. Besides, the

estimated coefficients for recorded net goodwill are positive and highly significant in each of the

seven years. Furthermore, the results also suggest that investors may view purchased goodwill as

an economic resource that does not decline in value for some firms.

Meanwhile, in the second part of their study, Jennings et al. (1996) examined whether purchased

goodwill was reflected in equity values as a wasting resources. Actually, their motivation was

the fact that all United States firms are required to amortize goodwill over periods not exceeding

40 years. Besides, this requirement is based on the argument that purchased goodwill declines in

value over time because the underlying stream of cash flows is likely to be of limited duration.

The authors estimated a cross-sectional regression based on income statement issues that involve

regressing equity values on components of expected future earnings, including expected

goodwill amortization.

Their results indicate a strong positive cross-sectional association between equity values and

recorded goodwill assets amounts after controlling for other components of net assets. In

addition, Jennings at al. (1996) finds evidence of a negative association between equity values

and goodwill amortization after controlling for other components‟ expected earnings. In the

INTERNATIONAL ACCOUNTING AND BUSINESS CONFERENCE

2011

PROCEEDINGS IABC2011 Page 8

meantime, Ibrahim et al. (2001) conducted a study concerning accounting for goodwill in

Malaysian context. Their study attempts to investigate the association between purchased

goodwill and market value and to describe the relationship between purchased goodwill and

other assets. Ibrahim et al. findings stated that the market incorporates the information on

purchased goodwill in the valuation of a firm and the results also show that the market seems to

perceive purchased goodwill to have at least a value equal to other asset.

As mentioned by Barth et al. (2001), the fair value accounting value relevance literature also

addresses questions relating to non-financial intangible assets costs related to goodwill. The

findings show that available estimates of intangible asset values reliably reflect the values of the

assets as assessed by investors. Besides, the estimates have a significantly positive relation with

share price. In fact, there was a review of the literature indicates the diverse paradigms that have

encompassed R&D. The transition from early days‟ booming markets and economic growth in

the 1950s to today‟s highly competitive and global marketplace is reflected in the way R&D has

been managed (Nobelius, 2004).

Moreover, in an efficient capital market, relevant information about firms will be reflected in

security prices regardless of whether the information is reported on the balance sheet or in the

footnotes (Dyckman & Morse, 1986). Besides, Nobelius (2004) noted that early success stories

such as the industrial research laboratories Bell Labs, Xerox Parc and Lockheed Martin

Skunkwords have been replaced by companies like the more market-focused 3M, the rapid

introductions of new product ranges from Japanese manufacturers like Toyota and Sony, and

R&D collaborations like Ericsson‟s network of companies around the “Bluetooth” technology

and standard.

In addition, R&D constitutes a fundamental factor for the successful introduction of new, more

efficient and clean supply and end-use technologies and the achievement of economic, safety,

environmental and other goals (Barreto and Kypreos, 2004). Hence, do investors really look at

R&D information in determining company‟s market value or value of companies? These

questions raise another issue taken up by this study, which is to examine whether the commotion

surrounding the subject of R&D is really important to the investors due to corporate growth, or is

just to create „noise‟ in the security market. Thus, the study will try to uncover if R&D reported

in the financial statement is being taken into consideration by investors when valuing a company.

Therefore, prior research had been conducted to examine the value relevance of R&D. Other

than that, numerous articles that consist of various models and framework also had been

developed.

Many studies have tested whether stock prices or returns of firms that invest in R&D increase

according to the level of R&D intangibles. Chan et al. (1990) acknowledged a positive effect on

stock prices for two days surrounding R&D announcements. Meanwhile, there is evidence that

previous level of firm‟s involvement in R&D affect the firm‟s market value. Other prior research

INTERNATIONAL ACCOUNTING AND BUSINESS CONFERENCE

2011

PROCEEDINGS IABC2011 Page 9

that related was Shevlin (1991). Shevlin investigated whether capital market investors, in

assessing the market values of R&D firms‟ equity, view R&D Limited Partnership (LP) as

increasing both the assets and liabilities of the R&D firms. The results are consistent with market

participants capitalizing in-house R&D expenditures, viewing the call option feature of the

limited partnership as relevant information in assessing the market value of the R&D firm.

Shevlin (1991) also estimated the LP variables from information provided in footnote disclosure

items by R&D firms.

Several implications arise from Shevlin‟s study. The empirical results are consistent with the

argument that footnote disclosures allow investors to make some estimate of the value of the LP

to the firm. The results also indicate that in addition to the reported assets and debt on the face of

the balance sheet, investors use information in the footnotes to help assess the market value of

firms. Finally, Shevlin‟s results add further support to the empirical usefulness of the balance

sheet identity approach as used by Landsman (1986) to develop a cross-sectional valuation

model to address off-balance sheet issues.

Past research has generally attested to the information advantage of a general accounting rule

that would capitalize R&D (e.g. Lev and Sougiannis, 1996). Lev and Sougiannis (1996) address

the issues of reliability, objectivity, and value-relevance of R&D capitalization. For this reason,

Lev and Sougiannis documented a significant inter-temporal association between firms‟ R&D

capital and subsequent stock returns, suggesting a systematic mispricing of the shares of R&D

intensive companies, or a compensation for an extra market risk factor associated with R&D.

They attempt to establish an empirical connection between R&D spending and subsequent

earnings. Indeed, they examined this issue empirically for the United States in a cross-sectional

framework and estimate R&D amortization rates based on the relation between earnings and

lagged R&D expenditures. Finally, the findings suggest that R&D capitalization yields

statistically reliable and economically relevant information to investors. In other words, they find

that the capitalized R&D amount is value relevant.

Even though, Aboody and Lev (1998) examined the value-relevance of information on the

capitalization of software development costs, which was promulgated in 1985 by Financial

Accounting Standards Board No. 86 (SFAS 86), they concluded that capitalized software

development costs are impounded in prices and that large distortions in the firm‟s financial

position arise from expensing rather than capitalizing R&D spending. They identify four

variables that are significantly associated with the capitalization decision using data from 163

software companies over 1987-1995.1 Based on the results, the authors argue that the coefficient

of the software asset is only slightly lower than the coefficient of equity, indicating that

investor‟s value, on average, the capitalized software asset slightly less than a firm‟s tangible

assets. The results find no evidence that somewhat subjective software capitalization values are

irrelevant to investors‟ decisions. Nevertheless, Lev and Sougiannis (1996) found the asset to be

1 Aboody and Lev’s results are based on regression of the annual capitalized development cost (as a percent of

market value of equity) on market value of equity, profitability, development intensity, leverage and systematic risk.

INTERNATIONAL ACCOUNTING AND BUSINESS CONFERENCE

2011

PROCEEDINGS IABC2011 Page 10

value-relevant using a synthesized R&D asset and research on value-relevance shows that the

market is capable of valuing intangible assets, especially R&D. They estimate the R&D capital

of a large sample of public companies using Almon lag technology. In addition, Lev and

Sougiannis (1996) found that the stock price as well as stock returns reflects the market‟s view

on intangibles.

Choi et al. (2000) reported empirical evidence on the relationship between the reported value of

intangible asset, the associated amortization expense, and firms‟ equity market values. According

to them, there is a positive relation between the book value of intangible assets and the market

value of common equity. Moreover, consistent with the uncertainty hypothesis, the market‟s

valuation of a dollar of intangible assets is lower than its valuation of other reported balance

sheet items (Choi et al., 2000). With regards to the income statement hypotheses, the regression

analyses show that amortization expense is not significantly related to annual stock returns. Choi

et al. (2000) suggest that either the market does not view intangible assets as wasting assets or

that recorded amortization expense reflects the decline in value of the intangible asset with

considerable error.

Furthermore, a study done by Boone and Raman (2001), represent that off-balance sheet

(unrecorded) R&D benefits could generate ex ante inequity in the capital markets in the form of

an information gap (asymmetry) between informed investors and other investors. Here, the

results suggest that the market makers adverse selection costs are higher for R&D-intensive

firms rather than non-R&D-intensive firms. For R&D-intensive firms, there is a negative

association between market liquidity and the magnitude of off-balance sheet R&D assets. In

other words, these studies suggest that market liquidity will improve if there is more disclosure

about these firms‟ R&D projects. Meanwhile, Chan et al. (2001) summarized that R&D activity

represents a significant and growing portion of firm resources. They found that high R&D plays

a distinctive role arises from stocks with high R&D relative to the market value of equity.

Besides, their evidence does not support a direct link between R&D spending and future stock

returns. In other words, the association between R&D intensity measured relative to sales and

future returns is not strong for firms engaged in R&D.

Xu and Zhang (2004) examined the role of R&D in explaining the cross-section of stock returns

in Japanese market for the period from 1985 to 2000. R&D activities are characterized by

potential high reward and great uncertainty in future cash flows. According to them, Japan also

had the second largest stock market in the world in terms of market capitalization. Xu and Zhang

(2004) concluded that the average stock return is positively related to R&D expenditure in that

period. Besides, Han and Manry (2004) examined the value relevance of R&D disclosures and

advertising expenditures reported by firms listed on the Korean Stock Exchange from 1988 to

1998, using a regression model based on the Ohlson equity-valuation framework. From that

research, R&D expenditures are positively associated with stock price, suggesting that

capitalizing R&D expenditures is appropriate. However, these findings suggest that investors

believe the economic benefits of advertising expenditures expire in the current period, similar to

other expenses.

INTERNATIONAL ACCOUNTING AND BUSINESS CONFERENCE

2011

PROCEEDINGS IABC2011 Page 11

Zainol et al. (2008) in the study using the PROBIT model, conclude that R&D activities initiated

by a firm are an important signal for a firm‟s potential future value-creation. According to this

study which was conducted based on 230 public- listed companies from the main board of Bursa

Malaysia, companies in the consumer sector have a higher probability of reporting R&D as

intangible assets than the companies in industrial sector. By treating R&D as intangible assets,

the consumer sector companies manage to increase the possible inflow of foreign direct

investment and enhance the market value of the firm. The study also finds that companies with

high total assets tend to have a greater probability of reporting R&D cost as intangible assets.

The study also reveals companies which report the R&D as intangible assets are eligible for tax

credit, tax deduction and special depreciation allowance including tax exemption under

Malaysian Income Tax Act, 1967. According to Mani (2002), in South Korea, companies are

permitted to apply for 50 percent tax credit for the expenditure over and above the average

expenditure in the past two years. The tax credits in South Korea include the cost of R&D

personnel, patents registration, maintenance fees and the cost of leasing of fixed and current

assets for companies undertaking R&D activities. Wang and Tsai (1998) discover that small and

medium sized enterprises in Taiwan are motivated to spend for R&D when tax credits are

provided to them. However, due to uncertain nature of outcomes of R&D, many companies

report R&D as an expense and immediately write-off from the balance sheet. Even though this

practice is found to be common in many corporations, nevertheless this has under-estimate the

accumulation of intellectual capital and does not accurately capture a company‟s equity strength

(Zainol et al. (2008).

R&D cost is believed to create value for science and technology development even though the

cost for R&D is usually high. According to Tishler (2008), the cost of executing R&D program

is a function of the expected outcomes of the R&D program. Based to his study, when the

expected outcomes of the R&D programs are identical, the expected profit maximizing firm

should always choose the highest-risk R&D program as on average, when the high-risk R&D

programs are successful, the markets will expand overtime. In relation to this issue, Ella

Syafputri report in Science and Development Network (dated 24 September 2007), Malaysia has

allocated RM12 billion in its 2008 budget to R&D and commercialization of science and

technology in universities. The four universities which received at least RM400 million for their

research programmes include Universiti Sains Malaysia, Universiti Kebangsaan Malaysia,

Universiti Malaya and Universiti Putra Malaysia (research university status are granted for these

four universities). The money allocation may help to improve infrastructure and develop a better

system for commercialization.

One of the possible reasons which may contribute to the increase in the allocation of R&D cost is

due to the increase number of research scientists and engineers in year 1998. Other than that, the

RM12 billion allocation may be said to improve weak and non-existent linkages between the

private sector and institute of higher learning and government research institution that results

much of Malaysia‟s R&D activities at institutional level have not been able to pass through the

INTERNATIONAL ACCOUNTING AND BUSINESS CONFERENCE

2011

PROCEEDINGS IABC2011 Page 12

commercial stage of development (White Paper - Comparative Analysis of R&D Developments

in Malaysia, 2002). Callen and Morel (2005) in their study incorporating the Ohlson model agree

that cross-sectional and panel data studies of R&D investments consistently show that R&D

expenditures are value relevant and impounded in security prices. However, results of their

studies reported that a very weak empirical support exists for the value-relevance of R&D

expenditures (only 25 percent R&D investment significantly affects firm‟s valuation).

For pragmatic reasons, most research on intangibles focuses on those intangibles generated by

R&D expenditures. Meanwhile, data on R&D spending are widely available because R&D

expenditures must be disclosed separately under SFAS No.2, Accounting for Research and

Development Costs. Overall, research suggests that investors use disclosures on intangibles

expenditures and those intangibles expenditures have future benefits, but that these benefits are

more uncertain than those associated with conventionally recognised assets (Maines et al., 2003).

In addition, a study by Laincz (2005), presents the partial equilibrium for a single industry

demonstrating how growth-promoting R&D subsidies alter the endogenously determined market

structure. The results indicated about optimal R&D policies in existing endogenous growth

models rely on strong assumptions regarding market structure.

Development of the Theoretical Framework

Theoretical Model

The accounting identity model, also called the balance sheet model is based on the theory that

the market value of the firm‟s equity is the market value of its assets minus the market value of

its liabilities where investors assign values to the firm by taking the difference between the

market value of total assets and the market value of total liabilities. Balance sheet model has

been widely used by many researchers in their study.

The balance sheet model includes only the balance sheet variables in the regression equation, as

in Landsman (1986). In his study, Landsman empirically examined whether pension fund assets

and liabilities associated with corporate-sponsored defined benefit pension plans are valued by

the securities market as corporate assets and liabilities, a recent study which used an equity

valuation based on balance sheet model. This model permits pension and nonpension assets and

liabilities to have separate empirical coefficient values. Essentially, the model was actually based

on basis accounting equation, which holds that shareholders equity is the residual of corporate

assets less corporate liabilities. Therefore, the shareholders‟ equity can be written as:

Shareholders‟ equity (Net assets) = Total assets - Total liabilities

The use of this equation enables Landsman to compare coefficient values of assets and liabilities

to their counterparts. By removing earning, which is one of the explanatory variables; there is no

longer a weighted average between the income variable and the balance sheet variable. The

model is as follows: -

INTERNATIONAL ACCOUNTING AND BUSINESS CONFERENCE

2011

PROCEEDINGS IABC2011 Page 13

MVEjt = a0 + a1BVNAjt + a2R/Djt + ejt…(Model 3.1)

Where

MVEjt = Market value of shareholders‟ equity of firm j in year t

BVNAjt = Book value of the net assets minus R&D of firm j in

year t

R/Djt = Research and development of firm j in year t

ejt = Error term

Meanwhile, Barth et al. (2001) noted that value relevance studies use various valuation models to

tests for specific null and alternative hypotheses regarding relevance and reliability. Numerous

papers use equity market value as the valuation benchmark to assess how well particular

accounting numbers reflect information used by investors. Besides, the tests often focus on the

coefficient of the accounting numbers in the estimation equation. Similar to Barth et al. (2001),

we examine whether the estimated coefficient on the accounting numbers is significantly

different from zero with the predicted sign. Rejecting the null of no significance or unpredicted

sign is interpreted as evidence that the accounting amount is relevant and not totally unreliable.

This study also examines how the market perceives the accounting numbers in relation to all

other amounts recognized in financial statements. Thus, rejecting the null that the coefficients are

the same is interpreted as evidence that the accounting numbers being studied have relevance and

reliability that differ from recognized amounts. Therefore, the multiple regression analysis is

used to test the model and analyzed the relationship. The market valuation model is estimated for

each of the years from 2000 to 2007. Thus, the model tested in this study is as follows: -

MVEjt = a0 + a1BVNAjt + a2EARNjt + a3R/Djt + ejt…(Model 3.2)

Where

MVEjt = Market value of shareholders‟ equity of firm j in year t

BVNAjt = Book value of the net assets minus R&D of firm j in

year t

EARNjt = Net profit of firm j in year t

R/Djt = Research and development of firm j in year t

ejt = Error term

We estimated yearly cross-sectional regressions over a seven-year period from 2000 to 2007 and

use r-squared as one of the method to measure value-relevance. Apart from that, there is another

extension model that can be tested empirically to discover the relationship between R&D

information and the sign of earnings items throughout the study period. Besides, a new variable

was added to the original model used in this study. The basic model had been extended to

INTERNATIONAL ACCOUNTING AND BUSINESS CONFERENCE

2011

PROCEEDINGS IABC2011 Page 14

include a dummy variable. This dummy variable stood for the direction of earnings items, which

were divided into positive (profit) and negative (loss). If the reported earnings items were

positive, the value for this dummy variable was 1. On the other hand, if the reported earnings

items were negative, the value for this dummy variable was 0. The new extended model is

established as follows: -

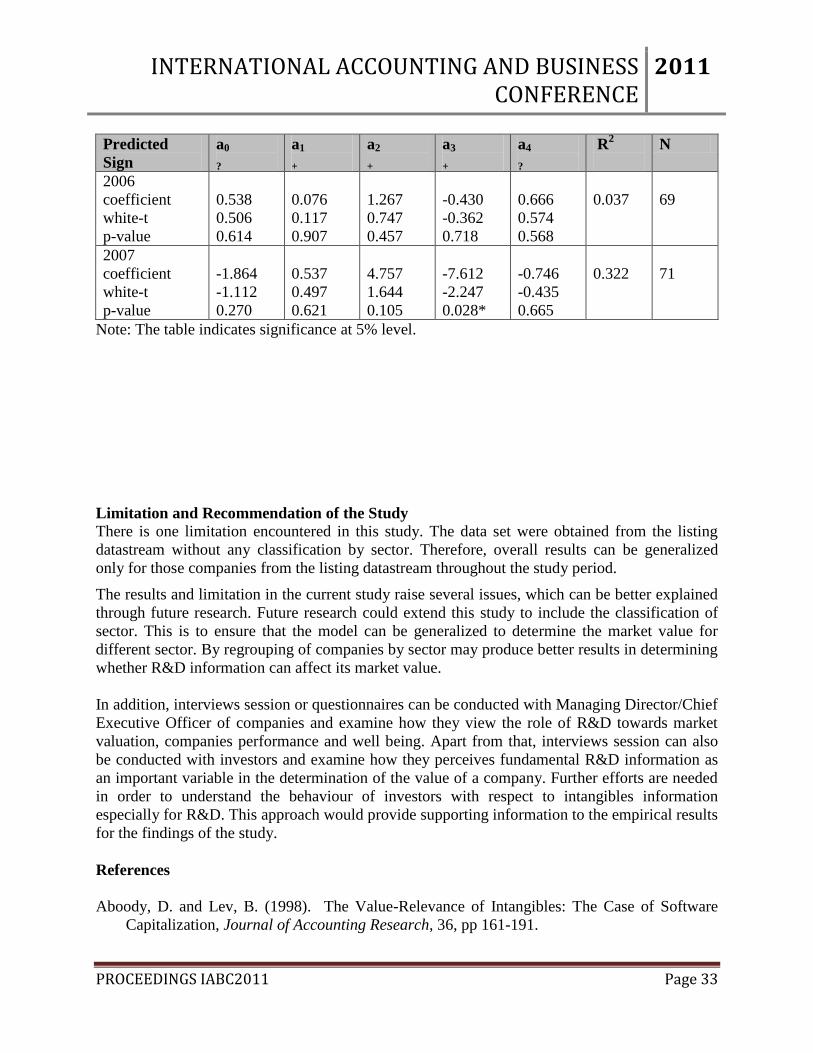

R/Djt = a0 + a1MVEjt + a2 BVNAjt + a3EARNjt + a4DEARNjt +

ejt… (Model 3.3)

Where

R/Djt = Research and development of firm j in year t

MVEjt = Market value of shareholders‟ equity of firm j in year t

BVNAjt = Book value of the net assets minus R&D of firm j in

year t

EARNjt = Net profit of firm j in year t

DEARNjt = Dummy variable taking the value of 1 for positive

earnings and 0 otherwise

ejt = Error term

From the above models discussed, error terms are independent, identically normally distributed

with mean 0 and a constant variance, σ2.

Research Hypotheses

Three hypotheses have been developed and will be tested in this study. In fact, the analysis that

is going to be performed will be based on these three hypotheses. The first hypothesis to be

addressed in this study is whether R&D should be considered as an important element when

determining a firm‟s market value. In order to achieve this objective, a3 is the coefficient of main

interest (as in Model 3.2). If the market places value on R&D of a firm, then R&D should be

significant and positively correlated with the firm‟s market value. In order to check for this

relationship the following null hypothesis is tested based on the Model 3.2:

H1: a3 = 0

If the R&D information is significant variable, then further examination should test how the

market perceives R&D in relation to all other assets. In other words, is it priced differently from

other assets? In order to check for this relationship, the following null hypothesis is established

based on the Model 3.2:

H2: a1 = a3

Meanwhile, the third hypothesis examine whether there is any relationship between R&D and the

sign of earnings items throughout the study period. In order to check for this relationship, the

following null hypothesis is tested based on the Model 3.3:

INTERNATIONAL ACCOUNTING AND BUSINESS CONFERENCE

2011

PROCEEDINGS IABC2011 Page 15

H3: There is no relationship between R&D information and the sign of earnings items.

Description of Data Collection

As stated earlier, the main objectives of the study is to investigate empirically the association

between R&D information in determining and explaining the market value and to establish a

relationship between R&D information with all other assets specifically over the period of 2000

until 2007 based on Malaysian firms. Literally, assets are rights accruing to the entity meanwhile

equities represent sources of the assets and consists of liabilities and the stockholders equity.

Thus, income earned is the property of the entity until it is distributed as dividends to the

shareholders. Hence, the firm‟s book value of net assets (excluding R&D), earning and R&D

will be the independent variables in the framework. Consequently, the theoretical model is

presents in Figure 3.1.

Figure 3.1: The Framework for the Relationship between Independent and Dependent

Variables

Sample Selection

It is now possible to see how both sampling design and sample size are important to establish the

representativeness of the sample for generalizability (Sekaran, 2000). According to the Sekaran,

if the appropriate sampling design is not used, a large sample size will not, in itself, allow the

Independent Variables

Book Value of Net Assets (Excluding R&D)

R&D

Earnings

Dependent Variable

Market Value of Equity

(Share price x ordinary

shares outstanding)

INTERNATIONAL ACCOUNTING AND BUSINESS CONFERENCE

2011

PROCEEDINGS IABC2011 Page 16

findings to be generalized to the population. Similarly, unless the sample size is adequate for the

desired level of precision and confidence, no sampling design, however sophisticated, can be

useful to the researcher in meeting the objectives of the study (Sekaran, 2000). Thus, sampling

decisions should consider both the sampling design and the sample size.

Black and White (2003) have listed several criteria in choosing sample for their research. These

criteria, as set by Black and White, are used in selecting sample for this research. Thus, the study

population consists of Malaysian firms. The coverage of the study is seven years, starting with

year 2000 until 2007 fiscal year from the listing datastream. Indeed, the data of this study are

extracted from the Balance Sheet and Profit and Loss Statement of the respective firms. Data for

this study were collected from the Thompson One Banker over seven-year period from 2000 to

2007.

A firm-year is included as observation if all such variables (market value of shareholders‟ equity,

book value of net assets, earnings and R&D) are presented for a given fiscal year. Firm-year

from the selected companies with any missing variables is excluded. As a result, the final

sample consists of various sample sizes during the period under study. Table 3.1 summarizes the

sample selection and size used for the study. After excluding the missing observations of

variables market value of equity, book value of net assets, earning and R&D, the final sample for

this study is 387 firm-year observations.

Table 3.1: Sample Selection and Size

Sample Selection

Firm-years

Thompson One Banker 2000-2007

9872

Missing observations of market value of equity

(MVE), book value of net assets (BVNA),

earnings (EARN) and capitalized R&D (R/D)

(9485)

Sample Size

387

Table 3.2: Sample Classified by Years

Year Original

Datastream

Clean Data

(Record R&D)

Non-record

R&D

2000 1234 19 1215

2001 1234 31 1203

INTERNATIONAL ACCOUNTING AND BUSINESS CONFERENCE

2011

PROCEEDINGS IABC2011 Page 17

2002 1234 35 1199

2003 1234 46 1188

2004 1234 53 1181

2005 1234 63 1171

2006 1234 69 1165

2007 1234 71 1163

Variable Definitions

The accounting variables included in the regression model are market value of equity, book

value of net assets, earnings and research and development. A summary of the variables of

interest is presented in Table 3.3. The market value of shareholders‟ equity (MVE) is defined as

the share price multiplied by the number of shares outstanding at the end of the accounting year.

The book value of total assets, research and development (R&D), total liabilities and the earning

figure (EARN) are also taken directly from the Thompson One Banker without any modification,

but with variables combined in some cases as shown. However, the book value of net assets

(BVNA) is derived by deducting the total assets (excluding R&D) with total liabilities.

Table 3.3: Variables Required for Regression from Thompson One Banker

Name variables required for

regression Variables Symbol

Market value of equity

Ordinary share outstanding x share price

MVE

Book value of total assets

Total assets

Book value of total liabilities

Total liabilities

Total sales

Turnover

Earnings

Profit attributable to Shareholders

EARN

INTERNATIONAL ACCOUNTING AND BUSINESS CONFERENCE

2011

PROCEEDINGS IABC2011 Page 18

Name variables required for

regression Variables Symbol

Net assets

Book value of total assets - Book value of total

liabilities - Research and development

BVNA

Research and Development

R&D to sales

R&D

Measurement

Measurement procedures

For purposes of empirical analysis, this study uses descriptive statistics and regressions analysis

as the underlying statistical tests. A descriptive statistics of the data obtained will be conducted

to obtain sample characteristics. In other words, descriptive statistics are used to describe and

summarize the dependent and independent variables. Apart from that, correlation is a statistical

method used to answer questions about relations between variables.

The correlation coefficient is a number that measurers the strength of the relation variables.

Values of the correlation coefficient can range from +1.00 for perfectly positively correlated

variables to -1.00 for perfectly negatively correlated variables. A correlation coefficient of -1.00

and +1.00 indicates perfect correlation. If there is absolutely no relationship between the two

variables, the correlation coefficient will be zero. A coefficient correlation that is close to zero

shows that the relationship is quite weak.

Past studies have used Ordinary Least Square (OLS) regression of market values on accounting

measurers to examine value relevance. Thus, OLS regression test is performed on the dependent

variable (MVE), to check the relationship between the R&D accounting numbers for the firms

operating in selected countries. OLS is based on a number of assumptions about the variables

and the error term that must be satisfied in order to ensure the interpretations of the regression

estimates are valid. According to Gujarati (1995), under these assumptions, the OLS estimators

of the regression coefficients are the best linear unbiased estimator.

Basically, r-squared measures the movement or changes in a variable that can be explained by

movements in another variable.2 A variable with greater r-squared indicates explanatory power

of that variable in explaining market value of equity. If the r-squared is lower, then the

explanatory variable is less relevant. A 5% significance level was used in this study. This test is

performed using the MICROFIT 4.0 software package. Besides, the analysis of the data is based

on cross-sectional regression. This study also discusses two major statistical problems associated

with the estimation of the models. The two major problems are heteroscedasticity disturbances

2 Literally, r-squared is the proportion of the variance of Y that has been explained by X. For technical reasons (the

total squared error can be decomposed into two squared components: explained and unexplained), the variance (the squared standard deviation) has traditionally been used.

INTERNATIONAL ACCOUNTING AND BUSINESS CONFERENCE

2011

PROCEEDINGS IABC2011 Page 19

and multicollinearity. Heteroscedasticity is the most common statistical problem to be

encountered when estimating a cross-sectional valuation model.

According to Ibrahim et al. (2003a), one of the major econometric problems when estimating

cross-sectional valuation models is heteroscedastic disturbances that appear from the fact that

large (small) firms tend to produce large (small) disturbances. If heteroscedasticity is present,

then the usual OLS estimators, although unbiased, no longer exhibit minimum variance among

all linear unbiased estimators (Gujarati, 1995). In short, they are no longer the best linear

unbiased estimator. Meanwhile, in the case of the two-variable linear model, one common

deflation technique involves transforming the variables by deflating the independent variable

(Landsman, 1986). This procedure implies that the true error variance is proportional to the

square of the independent. Landsman (1986) addressed the heteroscedasticity problem by

estimating the model in deflated form. In this respect, all variables are deflated by total sales.

Besides, the multicollinearity problem will be discussed in depth in Chapter 4.

Finally, the Wald Test is computed in Model 3.2 to measure whether the information provided

by one variable is significantly different from that provided by another. The Wald Test is

performed using the MICROFIT 4.0 software package. In this study, the Wald Test is computed

in order to check how the market perceives R&D in relation to all other assets.

Deflation Technique

Potential statistical problems associated with the estimation of the model were also noted in the

models that are relevant to the present study; as in the examples in Landsman (1986). The major

problem is heteroscedasticity disturbances. In addressing this issue, entire variables are

transformed by deflating them with the independent variable, which in this study is earnings/total

sales, to produce a constant (but still unknown) variance. Through this „deflation technique‟ the

heteroscedasticity problems can be minimized. The „deflation technique‟ has been widely used

by previous researchers, for example Landsman (1986), Shevlin (1991), McCarthy and

Schneider (1995) and Jennings et al. (1996). In these studies, (except for Shevlin, 1991) all data

in the basic models are deflated by total sales in order to reduce the heteroscedasticity problems

as well as to increase efficiency.

Findings & Conclusion

Descriptive Statistics

Estimates of Correlation on the Independent and Dependent Variables

A summary of the estimates of correlation between independent and dependent variables is

reported in Table 4.1. Table 4.1 presents the correlation of market value of equity (MVE) and

independent variables which include the book value of net assets (BVNA), earnings of the firm

(EARN) and research and development (R&D) in Malaysian firms during the period 2000-2007.

From the table, we can see that the correlation between MVE and R&D are considerably

INTERNATIONAL ACCOUNTING AND BUSINESS CONFERENCE

2011

PROCEEDINGS IABC2011 Page 20

moderate (Year 2000 = 0.379; Year 2001 = 0.438; Year 2002 = 0.544; and Year 2003 = 0.198;

Year 2004 = 0.057; Year 2005 = 0.122; Year 2006 = 0.118; and Year 2007 = 0.240) and a

significant positive. In other words, higher correlation between independent and dependent

variables can predict the regression of market value. Apart from that, based on the estimated

coefficients of correlation between other assets in valuing the market shareholder‟s equity in

Malaysian firms for 2000 until 2007 shows a significant positive correlation. Besides, the value

for correlation between BVNA and MVE is somewhat higher than the correlation between R&D

with MVE.

Table 4.1: Estimated Correlation Matrix of Variables for Malaysian Firms

Variables

BVNA

EARN

RD

2000

MVE

BVNA

EARN

0.654

-0.110

-0.600

0.379

0.018

0.133

2001

MVE

BVNA

EARN

0.670

-0.323

-0.460

0.438

0.111

-0.191

2002

MVE

BVNA

EARN

0.483

0.388

-0.033

0.544

0.255

0.254

2003

MVE

BVNA

EARN

0.359

0.342

0.285

0.198

0.405

-0.017

2004

MVE

BVNA

EARN

0.329

0.190

0.419

0.057

0.580

0.033

2005

MVE

BVNA

EARN

0.362

0.581

0.539

0.122

0.300

0.077

2006

MVE

BVNA

EARN

0.552

0.543

0.574

0.118

0.192

0.118

2007

MVE

BVNA

EARN

0.626

0.304

0.233

0.240

0.399

-0.292

Descriptive Statistics on the Independent and Dependent Variables

In general, descriptive statistics summarizes and describes the observation of the data used in this

study. As mentioned in the Chapter 3, one potential econometric problem when estimating cross-

sectional valuation models is the problem of heteroscedastic disturbances, which arise from the

fact that large or small companies tend to produce large or small disturbances. Thus, to address

this issue, the whole variables are transformed by deflating all variables with the total

INTERNATIONAL ACCOUNTING AND BUSINESS CONFERENCE

2011

PROCEEDINGS IABC2011 Page 21

sales/earnings in order to produce a constant variance but still unknown. Besides, this „deflation

technique‟ is hoped to eliminate the heteroscedasticity problem. A summary of the overall

descriptive statistics obtained from the sample size is presented in Table 4.2. The table provides

the mean, standard deviation and coefficient of variation for selected variables: market value of

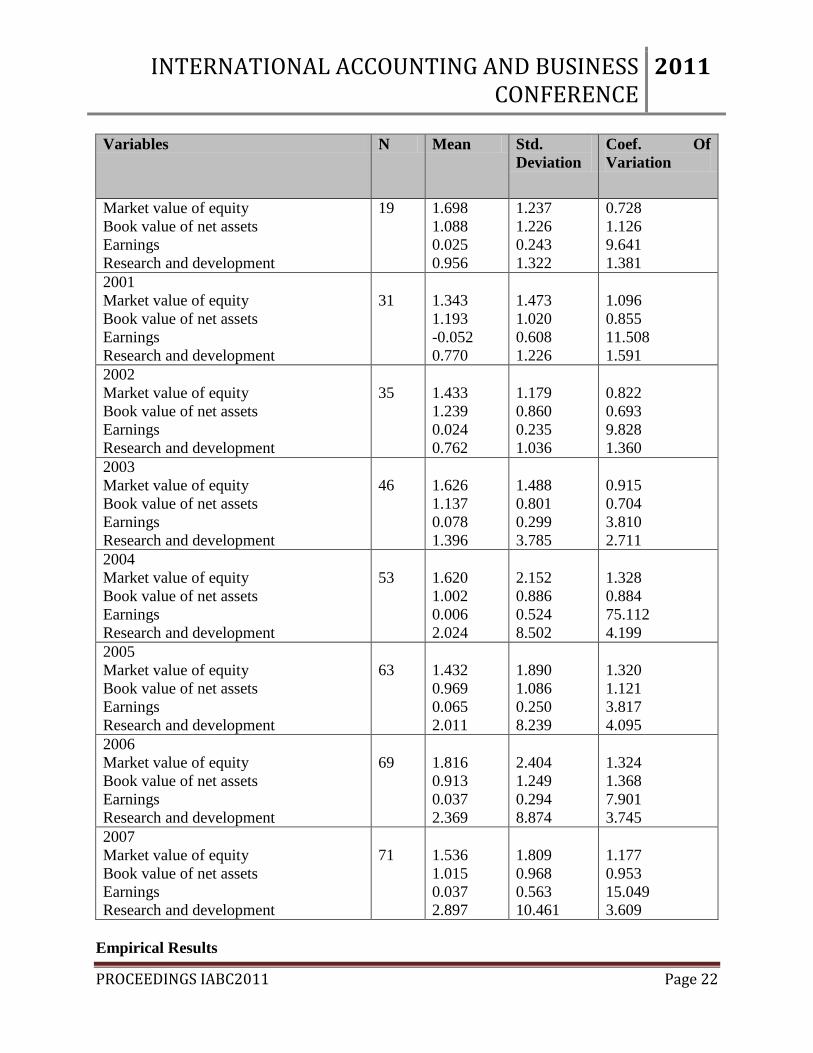

equity, book value of net assets, earnings and R&D, during the period 2000-2007.

Table 4.2 presents the mean, standard deviation and coefficient of variation for selected variables

in Malaysian firms during the period 2000-2007. Besides, all the variables were deflated by the

total sales. From the table, the results show that the values vary significantly throughout the

study period. The mean values of R&D in Malaysian companies are considerably moderate

throughout the study period (Year 2000 = 0.956; Year 2001 = 0.770; Year 2002 = 0.762; Year

2003 = 1.396; Year 2004 = 2.024; Year 2005; 2.011; Year 2006 = 2.369; and Year 2007 =

2.897). It concludes that R&D is a significant activity from the sample of Malaysian firms.

Apart from that, the mean values of variable MVE in Malaysian companies are also considerably

moderate (Year 2000 = 1.698; Year 2001 = 1.343; Year 2002 = 1.433; Year 2003 = 1.626; Year

2004 = 1.620; Year 2005 = 1.432 ;Year 2006 = 1.816; and Year 2007 = 1.536). Meanwhile, in

2001, the mean value of earnings was negative, which constitute of -0.052 (as reported in Table

4.2). The negative value shows that a few firms in Malaysia are suffering from losses in Year

2001. Standard deviation is a measure of the spread of data in relation to the mean. The standard

deviation is the traditional choice and is the most widely used. It summarizes how far an

observation typically is from the average. It is the most common measure of the variability of a

set of data. If the standard deviation is smaller, it means the probability of distribution is tighter.

From Table 4.2 it can be seen that standard deviation values for R&D is somewhat higher than

other selected variables during the period 2000-2007 (Year 2000 = 1.322; Year 2001 = 1.226;

Year 2002 = 1.036; Year 2003 = 3.785; Year 2004 = 8.502; Year 2005 = 8.239; Year 2006 =

8.874; and Year 2007 = 10.461). Meanwhile, the coefficient of variation is defined as the

standard deviation divided by the average and is a relative measure of variability as a percentage

or proportion of the average. The result also shows that the coefficient of variation for earnings

(Year 2000 = 9.641; Year 2001 = 11.508; Year 2002 = 9.828; Year 2003 = 3.810; Year 2004 =

75.112; Year 2005 = 3.817; Year 2006 = 7.901 and Year 2007 = 15.049) is higher than

coefficient of variation for R&D (Year 2000 = 1.381; Year 2001 = 1.591; Year 2002 = 1.360;

Year 2003 = 2.711; Year 2004 = 4.199; Year 2005 = 4.095; Year 2006 = 3.745 and Year 2007 =

3.609). This measure (coefficient of variation values for earnings) which is the ratio of standard

deviation of earnings to mean earnings capture the volatility for earnings for a given mean dollar

amount of earnings. In other words the earnings are more volatile than R&D in Malaysian firms

throughout the study period.

Table 4.2: Descriptive Statistics for Malaysian Firms (Deflated Form - Total Sales as

Deflator)

Variables N Mean Std.

Deviation

Coef. Of

Variation

2000

INTERNATIONAL ACCOUNTING AND BUSINESS CONFERENCE

2011

PROCEEDINGS IABC2011 Page 22

Variables N Mean Std.

Deviation

Coef. Of

Variation

Market value of equity

Book value of net assets

Earnings

Research and development

19 1.698

1.088

0.025

0.956

1.237

1.226

0.243

1.322

0.728

1.126

9.641

1.381

2001

Market value of equity

Book value of net assets

Earnings

Research and development

31

1.343

1.193

-0.052

0.770

1.473

1.020

0.608

1.226

1.096

0.855

11.508

1.591

2002

Market value of equity

Book value of net assets

Earnings

Research and development

35

1.433

1.239

0.024

0.762

1.179

0.860

0.235

1.036

0.822

0.693

9.828

1.360

2003

Market value of equity

Book value of net assets

Earnings

Research and development

46

1.626

1.137

0.078

1.396

1.488

0.801

0.299

3.785

0.915

0.704

3.810

2.711

2004

Market value of equity

Book value of net assets

Earnings

Research and development

53

1.620

1.002

0.006

2.024

2.152

0.886

0.524

8.502

1.328

0.884

75.112

4.199

2005

Market value of equity

Book value of net assets

Earnings

Research and development

63

1.432

0.969

0.065

2.011

1.890

1.086

0.250

8.239

1.320

1.121

3.817

4.095

2006

Market value of equity

Book value of net assets

Earnings

Research and development

69

1.816

0.913

0.037

2.369

2.404

1.249

0.294

8.874

1.324

1.368

7.901

3.745

2007

Market value of equity

Book value of net assets

Earnings

Research and development

71

1.536

1.015

0.037

2.897

1.809

0.968

0.563

10.461

1.177

0.953

15.049

3.609

Empirical Results

INTERNATIONAL ACCOUNTING AND BUSINESS CONFERENCE

2011

PROCEEDINGS IABC2011 Page 23

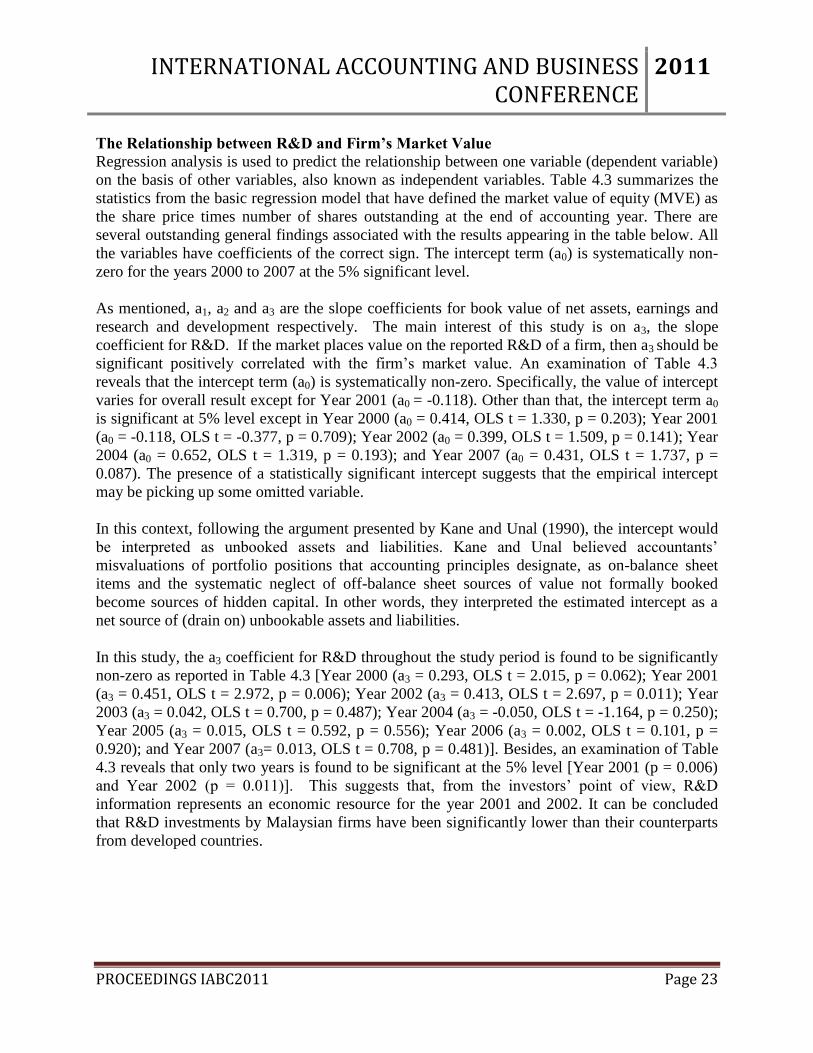

The Relationship between R&D and Firm’s Market Value

Regression analysis is used to predict the relationship between one variable (dependent variable)

on the basis of other variables, also known as independent variables. Table 4.3 summarizes the

statistics from the basic regression model that have defined the market value of equity (MVE) as

the share price times number of shares outstanding at the end of accounting year. There are

several outstanding general findings associated with the results appearing in the table below. All

the variables have coefficients of the correct sign. The intercept term (a0) is systematically non-

zero for the years 2000 to 2007 at the 5% significant level.

As mentioned, a1, a2 and a3 are the slope coefficients for book value of net assets, earnings and

research and development respectively. The main interest of this study is on a3, the slope

coefficient for R&D. If the market places value on the reported R&D of a firm, then a3 should be

significant positively correlated with the firm‟s market value. An examination of Table 4.3

reveals that the intercept term (a0) is systematically non-zero. Specifically, the value of intercept

varies for overall result except for Year 2001 (a0 = -0.118). Other than that, the intercept term a0

is significant at 5% level except in Year 2000 (a0 = 0.414, OLS t = 1.330, p = 0.203); Year 2001

(a0 = -0.118, OLS t = -0.377, p = 0.709); Year 2002 (a0 = 0.399, OLS t = 1.509, p = 0.141); Year

2004 (a0 = 0.652, OLS t = 1.319, p = 0.193); and Year 2007 (a0 = 0.431, OLS t = 1.737, p =

0.087). The presence of a statistically significant intercept suggests that the empirical intercept

may be picking up some omitted variable.

In this context, following the argument presented by Kane and Unal (1990), the intercept would

be interpreted as unbooked assets and liabilities. Kane and Unal believed accountants‟

misvaluations of portfolio positions that accounting principles designate, as on-balance sheet

items and the systematic neglect of off-balance sheet sources of value not formally booked

become sources of hidden capital. In other words, they interpreted the estimated intercept as a

net source of (drain on) unbookable assets and liabilities.

In this study, the a3 coefficient for R&D throughout the study period is found to be significantly

non-zero as reported in Table 4.3 [Year 2000 (a3 = 0.293, OLS t = 2.015, p = 0.062); Year 2001

(a3 = 0.451, OLS t = 2.972, p = 0.006); Year 2002 (a3 = 0.413, OLS t = 2.697, p = 0.011); Year

2003 (a3 = 0.042, OLS t = 0.700, p = 0.487); Year 2004 (a3 = -0.050, OLS t = -1.164, p = 0.250);

Year 2005 (a3 = 0.015, OLS t = 0.592, p = 0.556); Year 2006 (a3 = 0.002, OLS t = 0.101, p =

0.920); and Year 2007 (a3= 0.013, OLS t = 0.708, p = 0.481)]. Besides, an examination of Table

4.3 reveals that only two years is found to be significant at the 5% level [Year 2001 (p = 0.006)

and Year 2002 (p = 0.011)]. This suggests that, from the investors‟ point of view, R&D

information represents an economic resource for the year 2001 and 2002. It can be concluded

that R&D investments by Malaysian firms have been significantly lower than their counterparts

from developed countries.

INTERNATIONAL ACCOUNTING AND BUSINESS CONFERENCE

2011

PROCEEDINGS IABC2011 Page 24

Apart from that, Malaysia‟s R&D intensity still indicates that it is still below that of other

developing countries such as South Africa, Pakistan, India, China, Brazil and Venezuela. A

major reason for Malaysia‟s low R&D intensity is that many Malaysian enterprises are oriented

towards the domestic market and thereafter remain less pressure to be innovative, through R&D,

to be competitive in the international markets (White Paper - Comparative Analysis of R&D

Developments in Malaysia, 2002). In fact, annual surveys carried out by the United Kingdom

Department of Trade & Industry, none of Malaysian companies ranked in the top 500

international companies that undertook R&D investment in the year 2000 and 2001. This shows

that firms in Malaysia do not spent as much on R&D as compared to other firms in developed

countries. Apart from that, R&D activities among firms in Malaysia were very limited.

Compared to firms in other countries such as the United States, Japan and Germany, the amount

spent on R&D by Malaysian firms was very much less (Alfan, 2003).

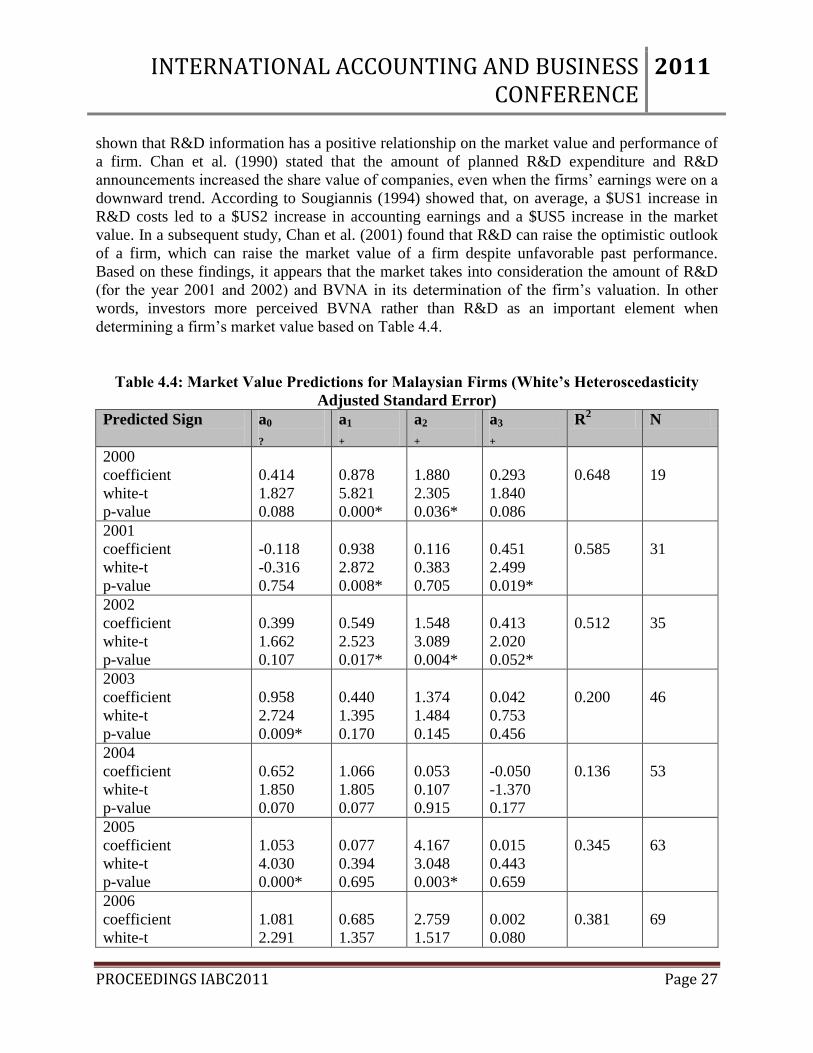

Apart from that, investors more perceive on BVNA in market valuation. The result (as reported

in Table 4.3) is as follows: [Year 2000 (a1 = 0.878, OLS t = 4.512, p = 0.000); Year 2001 (a1 =

0.938, OLS t = 4.654, p = 0.000); Year 2002 (a1 = 0.549, OLS t = 3.074, p = 0.004); Year 2003

(a1 = 0.440, OLS t = 1.488, p = 0.144); Year 2004 (a1 = 1.066, OLS t = 2.346, p = 0.023); Year

2005 (a1 = 0.077, OLS t = 0.337, p = 0.737); Year 2006 (a1 = 0.685, OLS t = 2.952, p = 0.004);

and Year 2007 (a1= 1.025, OLS t = 4.972, p = 0.000)]. Consequently, these findings confirm the

belief that the market was taking into consideration BVNA in determining the firm‟s equity

value as compared to R&D.

As explained in Chapter 3, r-squared measures the movement or changes in a variable that can be

explained by movements in another variable. A variable with greater r-squared indicates

explanatory power of that variable in explaining market value of equity. In general, the higher

the r-squared value, the better the model fits the data. However, if r-squared is lower, then the

explanatory variable is less relevant. Table 4.3 reports the result of r-squared value for Malaysian

companies across the year 2000-2007 (Year 2000 = 0.648; Year 2001 = 0.585; Year 2002 =

0.512; Year 2003 = 0.200; Year 2004 = 0.136; Year 2005 = 0.345; Year 2006 = 0.381; and Year

2007 = 0.423). On top, we can conclude that the Model 3.2 has its explanatory power due to a

higher value of r-squared for year 2000, 2001, 2002 and 2007. Therefore, there is an evidence to

infer that a linear relationship exists between the dependent and independent variables for whole

year of study.

INTERNATIONAL ACCOUNTING AND BUSINESS CONFERENCE

2011

PROCEEDINGS IABC2011 Page 25

Table 4.3: Market Value Predictions for Malaysian Firms (Basic Model)

Predicted Sign

a0

?

a1

+

a2

+

a3

+

R2 N

2000

coefficient

OLS-t

p-value

0.414

1.330

0.203

0.878

4.512

0.000*

1.880

1.901

0.077

0.293

2.015

0.062

0.648

19

2001

coefficient

OLS-t

p-value

-0.118

-0.377

0.709

0.938

4.654

0.000*

0.116

0.338

0.737

0.451

2.972

0.006*

0.585

31

2002

coefficient

OLS-t

p-value

0.399

1.509

0.141

0.549

3.074

0.004*

1.548

2.376

0.024*

0.413

2.697

0.011*

0.512

35

2003

coefficient

OLS-t

p-value

0.958

2.660

0.011*

0.440

1.488

0.144

1.374

1.895

0.065

0.042

0.700

0.487

0.200

46

2004

coefficient

OLS-t

p-value

0.652

1.319

0.193

1.066

2.346

0.023*

0.053

0.085

0.932

-0.050

-1.164

0.250

0.136

53

2005

coefficient

OLS-t

p-value

1.053

3.889

0.000*

0.077

0.337

0.737

4.167

4.396

0.000*

0.015

0.592

0.556

0.345

63

2006

coefficient

OLS-t

p-value

1.081

3.569

0.001*

0.685

2.952

0.004*

2.759

2.832

0.006*

0.002

0.101

0.920

0.381

69

2007

coefficient

OLS-t

p-value

0.431

1.737

0.087

1.025

4.972

0.000*

0.641

1.889

0.063

0.013

0.708

0.481

0.423

71

Note: The table indicates significance at 5% (*).

Model (Basic): MVEjt = a0 + a1BVNAjt + a2EARNjt + a3R/Djt + ejt…(Model 3.2)

INTERNATIONAL ACCOUNTING AND BUSINESS CONFERENCE

2011

PROCEEDINGS IABC2011 Page 26

The Relationship Between R&D and Firm’s Market Value after taking into Consideration

Heteroscedasticity Problem

The first common econometric problem to be encountered when estimating cross-sectional

valuation models is heteroscedasticity. This problem arises due to the fact that small companies

tend to produce small disturbance whereas large firms produce large disturbance. If

heteroscedasticity is present, then the standard errors are understated, resulting in overstated t-

statistics. In order to address these issues, the entire variables are transformed by deflating them

with the independent variable, which in this case is earnings/total sales, to produce a constant

(but still unknown) variance. As discussed in Chapter Three, „deflation technique‟ hopefully