1 The Market Microstructure Approach to Foreign Exchange: Looking Back and Looking Forward This draft: 14 October 2012 Michael R. King, Carol Osler and Dagfinn Rime*** Abstract Research on foreign exchange (FX) market microstructure stresses the importance of order flow, heterogeneity among agents, and private information as crucial determinants of short-run exchange rate dynamics. Microstructure researchers have produced empirically-driven models that fit the data surprisingly well. But currency markets are evolving rapidly in response to new electronic trading technologies. Transparency has risen, trading costs have tumbled, and transaction speed has accelerated as new players have entered the market and existing players have modified their behavior. These changes will have profound effects on exchange rate dynamics. Looking forward, we highlight fundamental yet unanswered questions on the nature of private information, the impact on market liquidity, and the changing process of price discovery. We also outline potential microstructure explanations for long-standing exchange rate puzzles. JEL Classification: F31, G12, G15, C42, C82. Keywords: exchange rates, market microstructure, information, liquidity, electronic trading. ***Michael King is at University of Western Ontario, Carol Osler is at Brandeis University and Dagfinn Rime is at the Norges Bank. The authors would like to thank Michael Melvin, {names} for helpful comments and suggestions. The views expressed in this paper are those of the authors and do not necessarily represent those of the Norges Bank. Please address all correspondence to Michael R King, Richard Ivey School of Business, UWO, [email protected], tel: 519-661-3084.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

TheMarketMicrostructureApproachtoForeignExchange:

LookingBackandLookingForward

This draft: 14 October 2012

Michael R. King, Carol Osler and Dagfinn Rime***

Abstract

Research on foreign exchange (FX) market microstructure stresses the importance of order flow,

heterogeneity among agents, and private information as crucial determinants of short-run

exchange rate dynamics. Microstructure researchers have produced empirically-driven models

that fit the data surprisingly well. But currency markets are evolving rapidly in response to new

electronic trading technologies. Transparency has risen, trading costs have tumbled, and

transaction speed has accelerated as new players have entered the market and existing players

have modified their behavior. These changes will have profound effects on exchange rate

dynamics. Looking forward, we highlight fundamental yet unanswered questions on the nature of

private information, the impact on market liquidity, and the changing process of price discovery.

We also outline potential microstructure explanations for long-standing exchange rate puzzles.

JEL Classification: F31, G12, G15, C42, C82.

Keywords: exchange rates, market microstructure, information, liquidity, electronic trading.

***Michael King is at University of Western Ontario, Carol Osler is at Brandeis University and Dagfinn Rime is at

the Norges Bank. The authors would like to thank Michael Melvin, {names} for helpful comments and suggestions.

The views expressed in this paper are those of the authors and do not necessarily represent those of the Norges

Bank. Please address all correspondence to Michael R King, Richard Ivey School of Business, UWO,

[email protected], tel: 519-661-3084.

2

The ancient and honorable field of international finance has grown furiously of

late in activity, in content, and in scope.

Michael R. Darby

These opening words, written by the editor to introduce the inaugural issue of the Journal

of International Money and Finance (JIMF) in 1982, could well have been written about the field

of foreign exchange (FX) research today. Over the past thirty years, research on exchange rates

has continued to grow in response to the puzzles and controversies that naturally arose following

the move to floating rates after the breakdown of Bretton Woods.

This paper focuses on one facet of this research, FX market microstructure. Researchers

in this field take a microeconomic approach to understanding the determination of exchange

rates, which are, after all, just prices. Microstructure research in general analyzes the agents that

trade in financial markets, the incentives and constraints that emerge from the institutional

structure of trading, and the nature of equilibrium. FX microstructure builds on this general

approach, but with models and empirical tests tailored to the study of currency markets.

This survey looks back at the key findings from the FX microstructure literature over the

past 30 years, highlighting along the way the many important contributions published by JIMF.1

We interpret the impact of microstructure research on the exchange rate literature using insights

from Karl Popper, who stressed the interplay between empirical analysis and the development of

theory. Most of the major findings in microstructure are empirical. This emphasis reflects the

access of microstructure researchers to high-quality data and the focus on the decision-making of

individual FX market participants. The growing availability of rich datasets has permitted

1 For other FX microstructure surveys, see: Evans and Rime (2012), Frankel, Galli, and Giovannini (1996), Lyons (2001),

Osler (2006, 2008), Sarno and Taylor (2001), and Vitale (2008). For surveys of FX intervention, see: Sarno and Taylor (2001), King (2005), Neely (2008), and Menkhoff (2010).

3

powerful tests of exchange-rate theories, allowing quick ‘falsification’ and providing strong

pointers for how they might be improved. The survey also highlights ways in which

microstructure research has contributed to powerful new explanations for long-standing puzzles,

such as the forward bias puzzle, the profitability of technical analysis, and the greater

explanatory power of purchasing power parity (PPP) over the long run.

Having highlighted stylized facts from the FX microstructure literature, this article draws

attention to structural changes in the currency markets over the past decades, which have

important implications for this field of study. Finally this article looks forward and highlights

those research areas and questions that remain contentious or unanswered, which may provide

fruitful areas for future research.

The JIMF, always receptive to the ‘facts first’ approach favored by microstructure

researchers, has been the leading outlet for this field (see Appendix A). A review of the literature

shows that the JIMF has published twice as many FX microstructure papers as the next leading

outlet. The JIMF has published key microstructure papers even if they adopted methodologies

not widely accepted in economics (e.g., surveys), even if they reached conclusions at odds with

the rest of international economics (e.g., Evans and Lyons 2002a); and even if they dealt with

microstructural nonlinearities orthogonal to standard models (e.g., Osler 2005). The JIMF has

thus played an important role in establishing this line of inquiry as a respected part of

international economics.

This paper has five sections. Section 1 looks back to the origins of FX microstructure.

Section 2 reviews the most powerful finding from microstructure, namely the impact of order

flow on exchange rate movements. Section 3 discusses liquidity provision and price discovery,

and outlines the implications for exchange rate models. Section 4 raises open questions prompted

4

by the FX market’s rapid, on-going evolution. Section 5 outlines potential microstructure

explanations for long-standing exchange rate puzzles. Section 6 concludes.

Section1:TheemergenceofFXmicrostructure

A focus on the microstructure of FX markets was a natural development in the scientific

analysis of floating exchange rates. This view is best appreciated in terms of Karl Popper’s

depiction of the progress of science. For Popper, science is an evolutionary process in which

theories are proposed, falsified by evidence, and then improved in light of the evidence. Such

criticism is an essential activity and represents the only route through which science can achieve

progress. FX microstructure research is primarily empirical, and can be characterized as adopting

this falsification approach to knowledge.

When fixed exchange rates were abandoned in the early 1970s there was almost no

evidence available to guide the development of exchange-rate models. Few countries had

experimented with floating exchange rates and those few experiments were brief. In the absence

of other evidence theorists postulated that PPP holds continuously – a theory that was falsified in

the short run and, in some tests, in the long run (Rogoff 1996). The emerging evidence

highlighted a specific shortcoming of continuous PPP, namely the exclusion of investor behavior

(Kouri, 1976). Since international investing was discouraged under Bretton Woods, evidence on

investor behavior was limited. Constrained by the lack of data, economists proceeded inductively

and developed elegant money supply and portfolio balance models to explain the determination

and behavior of exchange rates. Underpinning these parsimonious models was the assumption

that uncovered interest rate parity (UIP) held continuously.

5

As more data became available, these next-generation exchange rate models were

falsified, as all models inevitably are. The empirical challenges to these models were broad-

based. UIP failed to hold at short horizons. Rather than depreciating as UIP predicted, high

interest currencies were found to generally appreciate (Hodrick 1987; Engel, 1996; Bacchetta et

al, 2009). Even covered interest rate parity (CIP) did not hold during turbulent periods (Taylor

1989). More broadly, these models were shown to forecast short-run exchange rate movements

less well than the random-walk hypothesis (Meese and Rogoff 1983; Faust et al. 2003). With no

consensus on how to address this failure of UIP, one strategy was to modify existing models by

introducing an exogenous, time-varying risk premium. As noted by Burnside et al. (2007), this

approach was ‘fraught with danger’ because it introduced an important source of model

misspecification. Scientific progress, according to Popper, mandated the development of a third

round of exchange-rate models.

Given the discouraging track record of the inductive approach, microstructure researchers

adopted a deductive ‘facts first’ approach and began speaking directly to currency traders and

other FX market participants (Taylor and Allen, 1992; Cheung and Chinn 2001, 2004; Gehrig

and Menkhoff, 2004; Lui and Mole, 1998; MacDonald and Marsh, 1996; Menkhoff, 1998, 2001;

Menkhoff and Gehrig, 2006). Researchers quickly established that the standard macroeconomic

theories did not reflect the actual process through which dealers set exchange rates. Goodhart

(1988) forcefully makes the case for this pragmatic approach: “economists cannot just rely on

assumption and hypotheses about how speculators and other market agents may operate in

theory, but should examine how they work in practice, by first-hand study of such markets.”

This strategy paralleled the approach taken by researchers of equity market microstructure.

6

StylizedfactsonFXmarkets

Any visitor to a currency dealing room in the 1980s saw dealers on multiple telephones

noisily trading with other dealers. Similar activity could be observed in almost any city

worldwide, since the FX markets are geographically decentralized. Then, as now, London

captured about one-third of global FX trading, New York captured about one-fifth and trading in

Asia was divided among Hong Kong, Tokyo, and Singapore.2 In the most liquid currencies the

trading day is 24 hours long and trading floors are busiest when both London and New York are

open. A currency’s liquidity tends to be deepest during local trading hours and there is a brief

“overnight” lull in all FX trading activity between about 19:00 and 22:00 GMT (Lyons, 2001;

Rime 2003; Osler, 2009). By 2010 the U.S. dollar (USD) was involved on one side of roughly

three-quarters of all spot transactions, followed by the euro (EUR) at 46 percent, the Japanese

yen (JPY) at 20 percent and the UK pound (GBP) at 14 percent.

[Enter Table 1 and Figure 1: Average daily interdealer trading activity by the hour]

Currency dealers are employed by the major commercial and investment banks. They

intermediate trades between end-customers, and manage inventories or trade speculatively with

other dealers in an interdealer market. The major end-customer groups include corporations

engaged in international trade; asset managers such as hedge funds, mutual funds, endowment

and pension funds, and insurance firms; smaller banks and central banks; and governments. Until

the mid-1980s, trading by financial and corporate agents both represented roughly 20% percent

of the market (with interdealer trading accounting for the rest). While the share of corporate

trading has held steady over the years, the share of financial agents has risen dramatically. In

2 Details on the composition of FX trading across currency pairs, countries, and instruments can be found in the 2010 Triennial

Central Bank Survey of FX market activity (BIS, 2010; King and Mallo, 2010).

7

2010, trading by financial institutions represented over 50 percent of daily average turnover

(King and Rime, 2010). Currency markets are lightly regulated, if at all, with low transparency,

little monitoring, and no official reporting requirements.

[Enter Figure 2: FX spot market turnover by counterparty type]

Any microeconomic investigation of a market begins by identifying the key agents’

objectives and constraints. Some FX market agents resemble the actors in standard exchange rate

models. Hedge funds, for example, correspond well to the rational investors. They use currencies

as a store of value and are motivated by profits, given the standard compensation scheme of 2

percent of assets under management and 20 percent of any profits. Like their modeling

counterparts, hedge funds condition their trades on exchange-rate forecasts which they base on

information gathered with costly effort. Their trading is limited by personal risk aversion, as in

the models, but also by firm-based risk considerations and funding constraints.

Exporters and importers also have identifiable counterparts in standard exchange rate

models. Such firms use foreign currency as a medium of exchange and therefore purchase more

(less) of a currency once it has depreciated (appreciated). Most such firms do not permit

speculative trading (Osler 2009) and do not condition their trades on exchange rate forecasts

(Goodhart 1988, Bodnar et al. 1998). This choice is rational given the high costs of risk control

and monitoring in firms where speculative trading is permitted (Osler 2009).

Other agents in currency markets do not have recognizable counterparts in standard

models. Most international asset managers do not condition their trades on forecasts of future

exchange rates (Taylor and Farstrup 2006), a choice that may be rational in light of the close

correspondence between exchange-rate dynamics and a random walk. These asset managers also

appear to be somewhat indifferent to execution costs, though those costs tend to be high (Osler et

8

al. 2012). Retail traders do condition their trades on exchange rate forecasts, but those forecasts

appear uninformative because as a group they lose money (Heimer and Simon 2011).

Dealers are entirely absent from the standard macroeconomic models. They earn bonuses

based on trading profits earned from liquidity provision and speculative position taking. Dealers

are constrained in their risk-taking by position and loss limits. Given the volatility of exchange

rates and the low costs of trading, dealers generally maintain inventories close to zero, especially

at the end of the day. Inventory half-lives in currency markets are measured in minutes, even at

the smaller banks (Lyons, 1998; Bjønnes and Rime 2005; Osler et al. 2011), whereas in equity

and bond markets they are measured in days (Madhavan and Smidt 1993; Hansch et al. 1998).

The dealers themselves trade actively with each other with interdealer trading accounting

for over 60 percent of spot FX trades during the 1980s and early 1990s (BIS, 2010). Interdealer

trading is carried out either directly or indirectly via limit-order markets run by the electronic

brokers EBS and Thomson Reuters (Lyons, 1995). In the interdealer limit-order markets, prices

are ‘firm’ and brokers’ best bid and ask quotes provide a reliable signal of ‘the market. No agents

are specifically tasked with providing liquidity. Every agent can either supply (‘make’) liquidity

by placing a limit order, or demand (‘take’) liquidity by entering a market order.

Researchers have noted two key features of the market that constrain equilibrium prices.

First, when quoting prices to end-customers dealers always begin with the prevailing interdealer

quotes and adjust from there. Customer quotes are therefore tied to interdealer quotes. Second,

interdealer quotes are constrained in turn by dealers’ preference for holding zero inventories

overnight. This preference, which is rational given the volatility of exchange rates, implies that

whatever inventory is accumulated by dealers though market making during a given day must,

9

by the end of that same day, be sold to other customers. And it is the exchange rate that moves

to induce the necessary trading by customers.

[Figure 3: A typical FX dealer’s inventory]

Researchers visiting trading floors naturally sought to gain access to transactions and

quote data, only to discover that such information was not yet captured electronically. The first

high-frequency databases were thus assembled by hand. Goodhart and Figliuoli (1991), for

example, analyze the behavior of the interdealer market as a whole using minute-by-minute

exchange-rate quotes. Their pioneering work documented key stylized facts, such as the

tendency for bid-ask spreads to cluster at just a few price levels and for exchange rate returns to

be negatively autocorrelated.

Lyons (1995, 1998) studies the daily positions of a single active FX dealer during 1992.

He documents that the dealer averaged $100 000 in profits per day on volume of $1 billion per

day (or one basis point) and his positions had a half-life of only 10 minutes. By decomposing the

dealer’s profits, Lyons (1998) finds that intermediation was more important than speculation,

consistent with that dealer’s approach, known as ‘jobbing’, which focused almost exclusively on

providing liquidity to other dealers. Jobbing was unusual even in 1992, and seems to be extinct

as a strategy today. In a more recent study of four dealers at a major Scandinavian bank, Bjønnes

and Rime (2005) identify a greater role for speculation with dealers actively trading across the

two electronic broker platforms, EBS and Thomson Reuters. Mende and Menkhoff (2006) find

that intermediation was the dominant source of profits for the dealing room of a small German

bank. These studies highlight important differences between small and large dealing banks, and

confirm the market-held view that large banks extract a substantial information advantage from

observing more extensive trading flows.

10

Insightsfromthemarket

Many FX market insights were first documented through surveys of dealers, many – if

not most – of which were published in JIMF: Taylor and Allen (1992), Lui and Mole (1998),

Cheung and Chinn (2001, 2004), Gehrig and Menkhoff (2004), Menkhoff (1998, 2001) and

Menkhoff and Gehrig (2006). Despite being a standard tool in most social science disciplines,

surveys have not been widely used in economics. By publishing these surveys, the JIMF

demonstrated intellectual independence and made a valuable contribution to the profession.

Such surveys help explain otherwise puzzling results uncovered through empirical

research. For example, the clustering of bid-ask spreads documented by Goodhart and Figliuoli

(1991) was explained by dealer reports that informal ‘market conventions’ was a strong

determinant when quoting spreads (Cheung and Chinn, 2001). Since the market is intensely

competitive, deviating from the competitive equilibrium is costly. These surveys also showed

that market participants were heterogeneous in their trading styles, their views about other

market participants, and their beliefs about the determinants of exchange rates.

A key market insight, documented by Menkhoff and Gehrig (2006), is the shared belief

among FX dealers that exchange rates respond to currency-market flows. The importance of

flows follows logically from dealers’ preference for zero overnight inventory holdings. Traders

generally view the importance of trading flows to be self-evident; indeed, dealers base their

trading strategies on this perspective (Osler 2006). This belief, however is profoundly

inconsistent with the first and second generation exchange-rate theories with their inductively-

derived focus on stock holdings of assets to the exclusion of asset flows. The view in these

models that FX stocks could simply be first-differenced to create flows proved incorrect, as not

all cross-border FX flows take place within currency markets, as discussed later. Similarly the

11

assumption that UIP and PPP hold continuously implies that flows have no role in maintaining

these equilibrium relations. Likewise the assumption that all information is public and

interpreted identically by all agents is inconsistent with traders’ views of price discovery, with

private insights about exchange rates incorporated in prices through trading.

Section2:Orderflowandexchangeratereturns

The shared belief among traders that currency flows are a critical driver of exchange rates

could not be rigorously tested until researchers gained access to high-frequency transaction data.

Such data was initially scarce during the 1980s when FX trades were predominantly executed

over the telephone with back-office settlement relying on paper tickets and facsimiles. Pioneers

such as Charles Goodhart, Rich Lyons, and Richard Olsen painstakingly assembled detailed

datasets from printed records generously provided by dealer banks and FX brokers including

EBS, OANDA, and Thomson Reuters.

InterdealerorderflowinfluencesFXreturns

Lyons (1995) provides the first estimates of how order flow influences exchange rates.

Lyons’ data comprise the complete trading record of a specific dealer during one week in 1992.

Lyons found that this dealer would raise his quotes by 0.0001 DEM for incoming orders worth

$10 million. As he recognized, however, one cannot extrapolate from a single dealer to the

overall market.

Subsequent empirical work using comprehensive transactions data strongly confirmed the

importance of interdealer trading flows for explaining exchange-rate dynamics. To arrive at this

insight, however, researchers had to sort out a few methodological issues. One currency had to

12

be identified as the asset being traded and one as the medium of exchange. Market convention

dictates that the traded asset is the base currency (or denominator) in the standard exchange rate

quote. In EUR-USD, for example, a standard quote is 1.25 USD per EUR, so the base currency is

the euro. To establish whether a currency was in net demand or net supply, it was also necessary

to assign a direction to trades (either buys or sells), which was challenging as every FX trade

involves both a demander and a supplier of liquidity. This ambiguity was resolved by

recognizing that the product provided by a dealer is liquidity, namely the ability to trade a given

quantity of FX quickly and inexpensively.

By viewing liquidity as the product, it became straightforward to assign trade direction:

the aggressor in the trade is the agent purchasing (or taking) liquidity. For standard trades, the

customer is the aggressor so the customer’s trade determines the trade direction. When the

customer buys the base currency, the trade is categorized as a purchase. When dealers trade with

each other, the dealer initiating the transaction is the liquidity demander. If the dealer demanding

liquidity is purchasing the base currency, the trade is categorized as a purchase. In the

microstructure literature, trading flows are thus calculated as the difference between buyer-

initiated trades and seller-initiated trades, a measure called “order flow”. In other asset markets,

this measure is called the “order imbalance”. Order flow corresponds to net liquidity demand for

the base currency, with positive order flow associated with the base currency appreciating.

Evans and Lyons (2002b) first provided estimates of the exchange-rate’s response to

interdealer order flow using transactions in USD-Deutschemark (DEM) and USD-JPY during

four months of 1996. They regress the base currency’s daily return, rt, on order flow, xt, and

fundamentals, Ft:

rt = + xt + Ft + t (1)

13

where the fundamental variables are interest differentials, either lagged or in first difference.

Subsequent researchers have sometimes included lagged exchange-rate returns. Consistent with

the belief of traders, the estimated coefficient on order flow is positive and economically

significant, indicating that net demand for the base currency raises its value in terms of the other

currency. Specifically, an extra $1 billion in daily interdealer order flow was associated with a

0.5% appreciation of the USD vis-à-vis the DEM, with explanatory power on the order of 60

percent. Evans and Lyons (2002a) show that the explanatory power is higher, exceeding 70

percent, when returns are allowed to respond to order flow across additional currencies. When

returns are regressed only on the interest differential or its first difference, the explanatory power

is consistently below 1 percent.

Traders applauded this research as a sign that academics were getting better attuned to

reality, with dealing banks creating teams to analyze their own order flow. Microstructure

researchers noted that the Evans and Lyons’ (2002a,b) findings matched similar order flow

evidence in equity and bond markets (Holthausen et al. 1990; Chordia, Roll, and Subrahmanyam

2002; Simon 1991, 1994; Brandt and Kavajecz 2005; Pasquariello and Vega 2007). While some

economists saw the new results as highlighting a new direction for research, others remained

skeptical and called for more evidence, particularly as the data were proprietary and not available

to other researchers. This key finding has now been replicated with longer datasets, datasets that

cover more currencies, datasets that are more recent, datasets from both large and small dealing

banks, and datasets including brokered rather than direct interdealer trades.3 Table 2 presents

new evidence on this result for a broader set of currencies, and for longer samples, than ever

before.

3 For studies linking order flow to exchange rates, see: Berger et al. (2006b), Bjønnes et al. (2011), Evans (2002a), Hau,

Killeen, and Moore (2002), Killeen, Lyons and Moore (2006), King et al. (2010), Payne (2003) and Rime et al. (2010).

14

[Enter Table 2: Price Impact of Order Flow on Exchange Rates]

Explainingtheinfluenceofinterdealerorderflow

The evidence that order flow influences exchange rates, though striking, could not be

fully credible without a rigorous explanation. An early criticism was that order flow was not a

determinant of exchange rate at all, but rather reflected reverse causality with exchange rate

returns causing interdealer order flow. Empirical support for the causal influence from order flow

to returns was provided by Evans and Lyons (2005), Killeen et al (2006) and Daniélsson and

Love (2006). The study by Daniélsson and Love (2006) reveals that the estimated influence from

interdealer order flow to FX returns is stronger when one controls for feedback trading at the

level of the individual transaction. The intuition is that there is nothing additional to learn from

feedback trading than from prices.

The analysis of macroeconomic news events provided a further challenge to the idea,

standard in inductively-derived models, that public information instantly affects exchange rates

with no role for trading in this process. Econometric analysis of transactions data revealed that

the impact of news operates primarily through order flow (Love and Payne 2003, Evans and

Lyons 2002c, 2008; Rime et al. 2010). As ever, the JIMF published key results, including Evans

and Lyons’ (2005) finding that these order-flow effects do not happen instantaneously, but

persist for days. Similarly, Cai, Lee and Melvin (2001) identify an independent role for customer

order flow that is distinct from the impact of macroeconomic announcements and central bank

intervention in their study of the dramatic volatility of the Japanese yen in 1998.

Having established a separate role for order flow, researchers were able to explain its

effect by drawing on three mutually consistent theories already well-established in the broader

15

microstructure literature. The first theory focuses on dealers’ inventory and operating costs, the

second postulates a finite price elasticity of asset demand, and the third focuses on information

asymmetry. All were originally derived in optimizing models with fully rational agents.

Inventoryeffects

Dealers are compensated for the costs of operations and the risk of holding inventories by

charging a bid-ask spread. Order flow will naturally cause quotes to move between the bid and

ask, consistent with Evans and Lyons (2002b). Buyer-initiated trades will move the quotes

upwards, while seller-initiated trades move the quotes downwards. Inventory effects and the bid-

ask bounce documented in many asset markets are not entirely consistent with the empirical

findings, however, because inventory effects should only persist for a few minutes, given the

market’s liquidity, whereas the effect of order flow on exchange rates persists much longer.

Berger et al. (2008), for example, show that the price impact of interdealer order flow declines

gradually over time but remains statistically and economically significant even at three months.

Finiteelasticityofdemand

A lasting effect of order flow on exchange rates emerges when the price elasticity of

supply and demand are finite (Shleifer 1986). Evans and Lyons (2002b) outline a model of

currency trading in which finite elasticity is center stage. Every trading day in the model includes

three rounds of trading. In Round 1, dealers begin the day with zero inventory and are contacted

by random customers to trade. Dealers quote prices, trade with end-customers, and accumulate

inventory. In Round 2, the dealers trade with each other, effectively redistributing the aggregate

inventory among themselves. In Round 3, dealers want to return to their preferred zero overnight

inventory position so they set the quotes at a level such that a second set of customers willingly

16

purchase dealers’ aggregate inventory. This model captures so many important aspects of

currency markets that it has become the intellectual workhorse of the microstructure field.

The first set of customers can be viewed as demanding instantaneous liquidity from

dealers in response to exogenous shocks to their desired currency holdings. Since these

customers permanently change their currency holdings, they effectively demand overnight

liquidity from the market as a whole. Dealers willingly provide instantaneous liquidity, but are

reluctant to provide overnight liquidity so move prices sufficiently that other customers are

willing to do so. The theory is not specific on which end-customers demand liquidity in Round 1

and which provide overnight liquidity in Round 3. Round-1 customers might include

corporations that face exogenous shocks to currency demand due a competitor raising prices,

technology changes, or changes in barriers to trade. Or they may be financial customers whose

demand is influenced by private information, noise trading mistaken for information (Black

1986), portfolio rebalancing by customers, or other random liquidity shocks. Corporate demand

in Round 3 might arise as exchange rate movements change relative product prices. Similarly

financial institutions may respond endogenously due to risk aversion, since a weaker currency

promises a higher risk premium, other things equal. The heavy reliance of traders on technical

analysis, documented by Taylor and Allen (1992), among others, also creates endogeneity in

financial demand because technical analysis involves momentum and contrarian trading.

Since theory is agnostic on the respective roles of corporate and financial customers in

the Evans and Lyons (2002a,b) framework, researchers have viewed the question as empirical.

Round 1 customers can be distinguished from Round 3 customers according to the correlation

between their order flow and returns. Round-1 customer order flow should be positively

correlated with contemporaneous exchange rate returns, while Round-3 order flow is negatively

17

correlated. Researchers have also used the intertemporal properties of order flow to identify

Round-1 from Round-3 customers. Round-3 trading should lag Round-1 trading, but not vice

versa. Round-1 customer order flow should not respond to lagged FX returns while Round-3

customer order flow should.

Based on this identification strategy, studies using different time horizons and data

sources consistently find that financial customers demand liquidity in Round 1 while corporate

customers provide overnight liquidity in Round 3. Bjønnes, Rime, and Solheim (2005) use

comprehensive data on trading in Swedish krona to identify financial institutions as Round-1

customers and corporations as Round-3 customers. Marsh and O’Rourke (2005) use daily

customer order flow from Royal Bank of Scotland and find that financial order flow does not

respond to lagged returns while corporate order flow responds negatively. King et al. (2010) use

eleven years of daily data collected for the Canadian dollar by the central bank to show that

corporate order flow is negatively correlated with exchange rate returns, while financial order

flow is positively related. This relationship is present in the response of order flow to

macroeconomic surprises, to changes in macroeconomic expectations, and to changes in prices

of commodity futures that influence the Canadian dollar.

The Evans and Lyons (2002a,b) 3-round dealer model has a number of implications for

modeling exchange rates. First, it highlights the crucial role of corporate customers in

determining exchange rates. Second, it highlights the relevance of finitely elastic currency

demand, which contrasts with the assumption of infinite price elasticity under continuous UIP

and PPP theories. Third, it shows that exchange rate models need not explicitly include dealers.

Dealers may be involved in virtually every currency transaction, but because they prefer to hold

zero inventory overnight they do not provide overnight liquidity and are thus of limited relevance

18

beyond the intraday horizon.4 This statement does not imply that one cannot learn low-frequency

dynamics from studying interdealer order flow. Since they primarily intermediate end-customers,

interdealer order flow can potentially mirror the customer market. One cannot, however, capture

the heterogeneity of end-customers with interdealer trading since the interdealer flow is the sum

of orders across different end-customer types.

Privateinformation

Information provides a third reason why interdealer order flow could have a persistent

impact on exchange rates. This possibility emerges directly from classic microstructure studies

such as Glosten and Milgrom (1985) and Kyle (1985) that model the process through which

private information influences prices via the order flow of informed agents. In the equity markets

that inspired these models, the existence of private information about individual firms is not

questioned. The existence of private information in currency markets is more controversial

because most exchange rate fundamentals are publicly announced, such as interest rates and

general price levels. But such public announcements are necessarily delayed relative to the

realization of the fundamental variable itself, which provides time for agents to gather private

information. This timing gap is also present in the disconnect puzzle between macro

fundamentals and exchange rate variability, suggesting there is scope for disagreement around

public information. Many hedge funds and other active traders devote extensive resources to

gathering market intelligence, which would not be rational if there was no pay off to this activity.

It is likewise noteworthy that dealers consistently stress the importance of private information in

surveys. For example, Cheung and Chinn (2001) report that dealers view larger banks as having

an informational advantage due to their larger customer base and market network.

4 Proprietary traders employed by commercial and investment banks are classified as financial customers, not dealers.

19

The microstructure evidence supports the market participants’ belief in private

information relevant for future exchange rates. Evans and Lyons (2005) and Bjønnes, Osler, and

Rime (2011) show that customer and interdealer order flow, respectively, have predictive power

for future exchange rates. King et al. (2008) find that customer order flow has explanatory power

over and above macroeconomic fundamentals and commodity prices when predicting

movements in the Canadian dollar. Evans and Lyons (2009) and Evans (2010) provide evidence

that Citibank customer order flow can be used to predict future GDP and inflation rates. Finally,

Rime, Sarno, and Sojli (2010) show that interdealer order flow has predictive power for

upcoming macro statistical releases.

If private information explains part of the influence of order flow on exchange rates, then

agents must have access to different information sets or hold heterogeneous beliefs about public

information. A predictable hypothesis would be that the contribution of different agents’ trades

to FX returns will depend on the extent to which they are informed. Microstructure research

suggests that some of this heterogeneity reflects imperfect rationality. Osler and Oberlechner

(2011) show that currency dealers, as a group, tend to be overconfident and this tendency does

not diminish over time. Myriad studies show that professional exchange rate forecasts are biased,

inefficient, and inconsistent across time horizons (MacDonald 2000). This microstructure view

of information is strikingly different from the inductively-derived perspective of standard

exchange-rate models which assume all agents are homogenous and perfectly rational, all

information is immediately announced to the public, and prices respond instantaneously to news.

There is abundant evidence supporting the heterogeneity of beliefs about exchange rates

and the role of trading for revealing private information. MacDonald and Marsh (1996), for

example, find that FX forecasters hold significant differences of opinion due to their

20

idiosyncratic interpretation of widely-available information. This heterogeneity translates into

economically meaningful differences in forecast accuracy, with the extent of these disagreements

determining market trading volume. Evans and Lyons (2005) and Carlson and Lo (2006) show

that the information contained in macro news announcements takes days to become impounded

in prices through the trades of dealers and end-customers. Bauwens, Omrane and Giot (2005)

find that both scheduled and unscheduled macro news announcements have a significant impact

on FX markets, with volatility increasing prior to these announcements reflecting increased

uncertainty among market participants. Dominguez and Panthaki (2006) argue that the standard

definition of news in macro models should be broadened to incorporate both non-fundamental

news and order-flow. Dunne, Hau and Moore (2010) identify a strong influence from FX order

flow to equity markets, suggesting that FX order flow captures changes in heterogeneous beliefs

about fundamentals relevant to different asset classes.

Currency markets also display informational heterogeneity across customer locations and

customer types. Menkhoff and Schmeling (2008) find that agents located in centers of political

and financial decision-making are better informed than others. Among customer types, studies

consistently conclude that financial customers are better informed than non-financial customers

(Bjønnes et al. 2011; Carpenter and Wang 2003; Frömmel, Mende and Menkhoff 2008; Osler

and Vandrovych 2009). Trades by corporate customers in liquid currencies appear to carry zero

information, consistent with their role as liquidity providers. The empirical evidence indicates

that the trades of retail investors carry no information; instead retail traders generally lose

money, which suggests they (unintentionally) serve as overnight liquidity providers rather than

rational speculators (Heimer and Simon 2011; Nolte and Nolte 2011). Finally, research indicates

21

that larger dealers themselves bring their own independent private information to the FX market

(Bjønnes et al., 2011; Menkhoff and Schmeling, 2010; Moore and Payne, 2010).

Bacchetta and van Wincoop (2006), Evans (2011), Evans and Lyons (2005c, 2006),

Frankel et al. (1996), Lyons (2001), and Sarno and Taylor (2001) have developed FX

microstructure models that attribute the influence of order flow on exchange rates to private,

heterogeneous information.

Section3:Liquidityandpricediscoveryincurrencymarkets

Liquidity provision and price discovery are perhaps the two most important functions of

financial markets. FX microstructure research has naturally focused on these topics, with

implications for the modeling of exchange rates. Given that much of the existing microstructure

research focuses on equity markets, it is important for exchange rate modelers to recognize that

the conclusions of equity microstructure research “cannot be taken over in to and applied to the

FX market because the nature of the markets differ” (Booth 1994, p. 210).

Liquidityprovision

Classic theories of liquidity provision indicate that bid-ask spreads should rise – and

liquidity decline – with dealers’ risk aversion, volatility, the expected time between trades, and

trade size, and information asymmetry (Ho and Stoll 1981; Glosten and Milgrom 1985). While

bid-ask spreads in the interdealer FX market appear to conform to these predictions, recent FX

research shows they do not hold in the customer markets.

In the interdealer market, Glassman (1987) confirms that the variation in interdealer bid-

ask spreads reflect greater uncertainty, with market makers judging the probability of exchange

22

rate changes based on recent and long-term volatility. Hartmann (1998) and De Jong, Mahieu

and Schotman (1998) confirm the importance of trading volumes and volatility for explaining

bid-ask spreads. Focusing on a specific time period, Kaul and Sapp (2006) document that FX

dealers widened bid-ask spreads from December 1999 to January 2000 as Y2K concerns led to

increased safe-haven flows and rising dealer inventories in an environment of greater uncertainty

and lower liquidity. Similarly, Mende (2006) studies FX interdealer spreads around September

11, 2001, and confirms they widened dramatically on the day of the 9/11 attacks then reverted to

normal the next day, reflecting the spike in risk aversion and volatility from the event.

Hau, Killeen and Moore (2002) study one setting where the behavior of interdealer bid-

ask spreads did not conform to standard theory. They find that bid-ask spreads on the newly

created EUR were wider, not narrower, than the prior DEM spreads, despite the greater

transaction volumes in the new currency. The authors argue this widening was paradoxically due

to the higher transparency of order flow in the interdealer market. With only one currency in

which to trade vis-à-vis the USD, dealers had fewer options for managing inventories without

risking detection by other dealers.

The behavior of interdealer bid-ask spreads also conforms to the theoretical predictions

from research on limit-order markets. Using minute-by-minute quotes from Reuters, Goodhart

and Figliuoli (1991) and Goodhart and Payne (1996) confirm that trades are a major factor in

spread determination and the frequency of quote revisions. Since these data were indicative

quotes, like much of the high frequency data available in the 1990s, there was concern that they

might not accurately represent firm prices or transaction prices. Daníelsson and Payne (2002)

compare indicative and firm quotes and find that indicative prices lagged when the market

moved quickly, but indicative bid-ask quotes were generally quite close to firm quotes when

23

sampled at horizons of 5 minutes or longer. Lo and Sapp (2008) show that FX dealers’ decision

whether to submit limit or market orders in interdealer limit order books is conditional on the

previous type of order submitted as well as the recent volatility of the market, consistent with the

theoretical predictions from Parlour (1998) and Foucault (1999). More market orders are used

early in the trading day when information flows into the market, consistent with Bloomfield et al.

(2005). Finally, Menkhoff et al. (2011) confirm that liquidity in the interdealer market responds

to changes in volatility, bid-ask spreads, and other market conditions similarly to other markets,

driven by informed traders.

The end-customer segment of the FX market does not behave consistently with classic

microstructure theories regarding liquidity provision. Classical theories predict, for example, that

dealers will “shade their prices”, which means they shift prices down when their inventory is

excessive and vice versa (Ho and Stoll 1981). Such price shading has been documented in equity

markets (Madhavan and Smidt 1993) and bond markets (Dunne et al. 2007). But studies of

individual currency dealers provide no evidence of price shading (Bjønnes and Rime 2005; Osler

et al. 2011), with the lone exception of Lyons’ FX jobber (Lyons, 1995). Dealers explain that

quote shading would reveal information about their inventory position that could make them

vulnerable. They prefer to unload inventory quickly in the liquid interdealer market.

The empirical facts on the bid-ask spreads quoted by dealers to their customers is equally

at variance with classical microstructure theories. The orthodox view is that dealers widen

spreads to protect themselves from adverse selection when trading against informed customers

(Glosten and Milgrom 1985; Glosten 1989; Madhavan and Smidt 1993). However, Osler et al.

(2011) show that FX bid-ask spreads for more informed customers – such as financial customers

or customers making bigger trades – are narrower, not wider. This finding has been confirmed by

24

Ding (2009) for trade size and Rietz, Schmidt, and Taylor (2009) for customer type. This

discrimination in favor of larger trades could reflect the lower per-unit operating costs, or the

stronger bargaining power of financial customers (Green, et al. 2007; Rietz et al. 2009).

Financial customers are also generally better informed and dealers may quote strategically to see

their order flow, which may provide them with an information advantage when trading with

other dealers (Bjønnes et al. 2011). Dealers thus have an incentive to maximize their trading with

informed customers rather than to avoid such trading (Naik et al., 1999).

The contrasting findings for bid-ask spreads between the segments of the FX market

highlights the importance of market structure in pricing behavior. Market makers lose when

trading against better informed customers in any market. In the NYSE, which has just one tier,

market makers (or specialists) have no one else with whom to trade after observing an informed

customer trade. In consequence, they must offset those losses by charging wider spreads to

informed customers. The FX market is a two-tier market, so dealers who trade with informed

customers can turn around and exploit the information when trading with other dealers. They can

quote narrower spreads to informed customers and make up the difference through more

informed interdealer trading.

Marketstructureandpricediscovery

Market structure influences the price discovery process. Classical microstructure theories

assume a one-tier market in which adverse selection is the dominant concern. While some

exchange rate models have attempted incorporating these theories, the discussion in the previous

section highlights two reasons why the classic theories cannot be directly applied in the FX

context: (i) no influence from adverse selection to customer bid-ask spreads has been detectable

25

in currency markets; (ii) the currency market’s two-tier structure provides a rigorous, rational

basis for the observed pattern of those bid-ask spreads.

Osler et al. (2011) propose a three-stage price discovery process relevant to the two-tier

structure of FX markets. Following the literature, they assume that information originates with

end-customers. In Stage 1, an informed customer trades with a dealer who receives a signal

about the customer’s private information. This information, however, does not become

embedded in prices at this stage because the informed customer pays a narrower spread than

uninformed customers. In Stage 2 the dealer trades on customer’s private information in the

interdealer market, leading other dealers to adjust their quotes in line with the customer’s

original trade. The price continues moving in the direction implied by the customer information

even after the first dealer has traded. In Stage 3, other customers contact dealers and the quotes

they receive reflect this new information, completing the price discovery process. There is now

substantial evidence consistent with this price discovery process for exchange rates.

A first key feature of Stage 2 is the dealers’ decision to mimic the trades of their

informed customers. Using a probit analysis, Osler et al. (2011) confirm that dealers are more

likely to trade aggressively after larger customer trades and trades with financial customers.

Bjønnes et al. (2011) show that larger dealers (who are viewed as more informed) also tend to

trade more aggressively. More persuasively, these authors show that a dealer’s tendency to trade

aggressively rises with the volume of their business with informed and/or financial customers but

is unaffected by the volume of business with corporate customers and governments.

A second key feature of Stage 2 is the reaction of other dealers to an interdealer trade.

Goodhart and Payne (1996) and Menkhoff and Schmeling (2010) provide evidence that other

dealers adjust their quotes in the direction of the most recent trade, thereby contributing to the

26

impact of any embedded information. After observing an aggressive interdealer purchase, for

example, other dealers raise their quotes. Less informed dealers will also reverse the direction of

their trades so that it matches the direction of dealers who are viewed as better informed.

Thenatureandsourcesofprivateinformation

Microstructure research certainly provides extensive evidence that interdealer and

financial order flows carry information about upcoming returns. The exact nature of that

information remains the subject of some debate. Is the information fundamental or transitory?

The predictive power of customer and interdealer order flow for exchange-rate fundamentals,

reviewed above, certainly suggests that the information may be linked to fundamentals.

Dealers are considered among the best-informed agents in FX markets. Not only does

dealer order flow anticipate returns (Rime, Sarno, and Sojli, 2010; Bjønnes et al., 2011), it does

so better than the trades of any individual group including leveraged investors (Osler and

Vandrovych, 2009). But dealers typically hold positions for only a handful of minutes (Bjønnes

and Rime 2005; Lyons 1995). This time horizon seems inconsistent with the notion that the

information behind their trades is related to fundamentals. In surveys, dealers express the view

that exchange rate fundamentals either do not exist or, if they do exist, do not matter (Menkhoff

1998). Instead dealers focus on customer order flow as one source of information on which to

take speculative positions. There is no necessary inconsistency here, however, as dealers could

focus on order flow and yet the information it contains may still be related to fundamentals.

If dealers are extracting fundamental information from customer order flow, what

fundamental information does it reveal. And which end-customer segment has this information?

It has already been noted that certain categories of hedge funds devote substantial resources to

27

macroeconomic analysis in an effort to anticipate macro statistical releases. Dealers could

certainly acquire this information by observing the hedge fund trades. Dealers might also gather

relevant information embedded in the trades of other agents but unknown to those agents

themselves (Evans, 2010). Corporate traders, for example might reflect fundamental information

about the state of domestic output, even though the corporations themselves do not trade on

exchange rate forecasts (Goodhart 1988; Bodnar 1998). By observing sufficient corporate trades,

dealers may detect a pattern that is dispersed and not known to individual corporate traders

(Lyons 2001). Likewise, the trades of real money institutional investors such as mutual funds and

pension funds might unwittingly reveal fundamental information on investor risk aversion or

portfolio rebalancing (Breedon and Vitale, 2010; Killeen, Lyons and Moore, 2006). Finally,

recent research suggests that dealers bring their own independent information to the market

(Bjønnes, Osler, and Rime, 2011; Moore and Payne, 2011). The source and nature of private

information revealed by customer and dealer order flow remains an open question.

Section4:Electronictradingandexchangeratedynamics

Electronic trading has brought huge structural changes to FX markets over the past

decade. In this section we briefly describe the most important institutional changes and highlight

their importance for exchange rate dynamics. Greater detail on these changes is available in King

and Rime (2010) and King et al. (2011).

TradingamongdealersandtraditionalFXcustomers

When introduced on FX trading floors in the late 1980s, Thomson Reuters Dealing

replaced the telephone with an electronic system for dealers to exchange messages, allowing for

speedier and more efficient interdealer trading. The more important change occurred in the early

28

1990s when Reuters introduced the first electronic limit-order market for FX, now known as

Thomson Reuters Matching, while a consortium of dealers launched a competing platform,

Electronic Broking Service (EBS). These systems revolutionized the interdealer segment, but

remained inaccessible to end-customers. The landscape changed dramatically in the late-1990s,

however, when a number of multibank trading platforms were launched that targeted end-

customers directly.5 These systems enhanced transparency, improved operating efficiency, and

reduced trading costs at the expense of greater concentration among the top dealers who

streamed quotes to these platforms. Over the next decade, massive investments in the IT

infrastructure by dealers and market participants opened the door to algorithmic trading, with

hedge funds and high-frequency traders gaining direct access to interdealer markets from 2005

onwards (King and Rime 2010). Starting in the early 2000s, the top banks launched proprietary

single-bank trading platforms for their customers, allowing them to create pools of liquidity that

are not visible to the market.6

Individual dealing banks now stream executable prices to their FX customers across an

array of public and proprietary trading platforms. As electronic brokers and dealers have

segmented the market, different platforms have been launched targeting small corporate

customers, sophisticated corporate customers, institutional asset managers, and leveraged

investors such as hedge funds. These platforms are expensive to design, develop, and maintain,

which means there are now substantial barriers to entry and economies of scale in FX dealing.

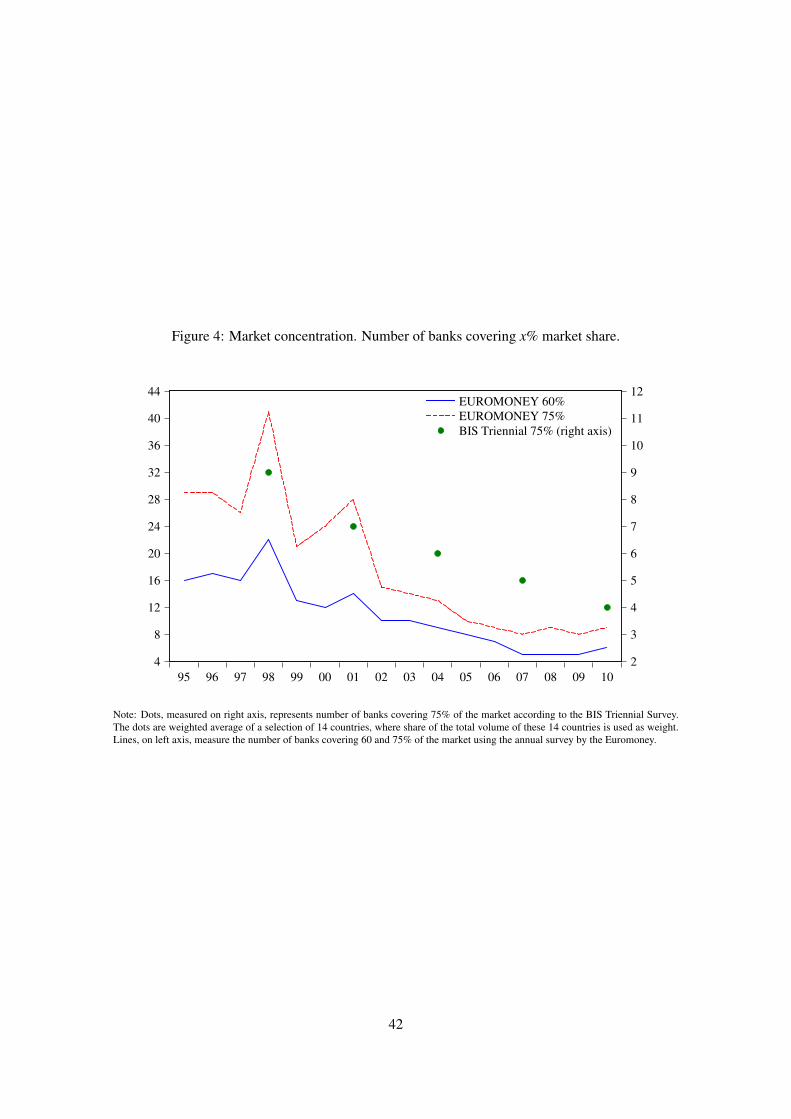

Market making has, therefore, become a far more concentrated business with Euromoney

reporting that the share of wholesale FX trading at the top three banks reached 40% in 2010, up

from only 19% in 1998.

5 FX Connect was launched in 1996, Currenex in 1999, Hotspot FXi in 2000, and FXall and Lava in 2001. 6 UBS launched FX Trader in 2000, followed by Barclays’ BARX in 2001 and Deutsche Bank’s Autobahn in 2002.

29

[Enter Figure 4: Market concentration]

The high volume of customer transactions passing through the largest dealing rooms has,

in turn, changed the economics of inventory management. It was always more profitable to lay

inventory off on other customers, but dealers generally chose the interdealer market because it

was faster. Now that advantage has been severely eroded, so dealers generally hold or

“warehouse” inventory accumulated in customer trades. The change in the paradigm of inventory

management has been extremely rapid. Less than one quarter of trades were crossed internally in

2007, but by 2010 that fraction reached a reported 80 percent at the largest dealers. Anecdotal

reports suggest that liquidity provision and flow-based customer businesses have become the

biggest source of FX revenues at the largest dealing banks following the 2007-2009 crisis.

The increased volume of customer business captured by the largest dealers has

consolidated their information advantage relative to smaller banks, many of whom have chosen

to curtail market making in the most liquid currencies. Small banks still have a comparative

advantage in trading their local currency, so they choose to focus primarily on that niche

business as well as relationship management and credit provision. Large banks, meanwhile, have

aggressively developed new approaches to extracting information from customer flows. Dealers

are most comfortable internalizing the trades of uninformed customers (“non-directional” flows).

Dealers still actively court the trades of informed customers, however, they tend not to

internalize such trades, consistent with our earlier economic analysis of dealer incentives. Instead

they aggressively trade in interdealer markets to unwind any associated inventory position and

possibly to take outright speculative positions. To optimize this effort, dealers have developed

systems to screen out “predatory” flows, meaning trades in which a customer profits at the

dealer’s expense due time latency between trade instruction and execution on the dealer’s own

30

platforms. Dealers prefer to exclude such customers from their platforms. The warehousing of

dealer trades in this new environment has not yet been the focus of research.

The reduction in interdealer trading associated with the single-bank platforms has tended

to reduce market transparency, but another development in the dealer-customer trading has had

the opposite effect. On request-for-quote (RFQ) platforms customers looking for the best

available price can now request quotes from several dealing banks simultaneously. By

eliminating the need to search across banks sequentially, this system greatly improved

customers’ negotiating power. Bid-ask spreads for customers that previously had low bargaining

power, most notably corporate customers, tumbled accordingly (Goodhart et al., 2002; Bjønnes

and Rime, 2005). There are as yet no studies of RFQ platforms in currency markets.

RetailFXtrading

Electronic trading has enabled individuals of modest wealth, previously shut out of the

market, to trade speculatively for their own account. This trading generally takes place over a

new type of electronic trading platform known as the retail aggregator. By bundling many small

retail trades into trades that meet the minimum $1 million size for interdealer trades, retail

aggregators can provide narrow spreads on even tiny trades. Retail trading has grown rapidly and

was estimated to have reached $125–150 billion per day by 2010, or 8 to 10 percent of the

market (King and Rime 2010). Since retail customer order flow is generally uninformed (Heimer

and Simon 2011), these customers are a profitable group to serve. Currently there is fierce

competition for such business among the large banks, since they can effectively use these traders

to provide liquidity for more informed customers. Evidence on retail trading remains quite

limited, and represents a potentially fruitful area for future research.

31

Algorithmictradersandliquidity

As electronic trading systems progressed, it became possible for order-submission

strategies to be programmed and executed entirely by computers (Chaboud et al. 2009). In some

cases, computers simply automated the process of splitting larger trade into smaller transactions

to reduce price impact. In other cases, computers provide a competitive advantage to traders

whose strategies rely on speed such as triangular or covered-interest rate arbitrage.

Traders soon realized they could use the high execution speeds to take advantage of tiny

discrepancies in the prices or timing of different trading platforms. These “high-frequency

traders” typically provide substantial liquidity to the market via the hundreds or even thousands

of tiny limit orders they submit each day. This strategy was initially profitable and spread rapidly

in consequence, but it has compromised the profitability of traditional strategies and major banks

have consequently pulled back from supplying on multibank platforms. The flash crash of 2010

raises important questions about the reliability of liquidity provision from high-frequency

traders. Due to the need for liquidity, high-frequency trading is concentrated in the spot FX

markets for the major currency pairs. While this segment remained relatively liquid in the

turbulent period following Lehman Brothers’ collapse (Baba and Packer, 2009; Melvin and

Taylor, 2009), there is no rigorous evidence on whether high-frequency traders provide true

liquidity.

An important question facing FX markets is whether high-frequency traders are really

increasing the liquidity of FX markets or merely creating a liquidity mirage that dries up when it

is needed most. Future research could investigate whether high-frequency traders contribute to

market liquidity primarily by submitting limit orders or by linking liquid pools across different

trading platforms, thereby reducing market fragmentation.

32

Liquidityaggregators

With many electronic platforms competing to attract customers, there could conceivably

be a fragmentation in market liquidity that could compromise market efficiency. A similar

fragmentation has been observed in equity markets, where the introduction of Alternative

Trading Systems (ATS) has eroded the market shares of the established exchanges. In FX

markets the tendency towards fragmentation has been offset by the development of electronic

tools that collect streaming price quotes from many competing platforms. By providing

information on best prices these so-called “liquidity aggregators” perform a function similar to

the National Best Bid and Offer (NBBO) system in the US, which also distributes information on

the best bid and offer prices across all equity exchanges. The liquidity aggregators of currency

markets, however, also allow customers to trade at the best prices, which is one reason they have

proven especially popular with hedge funds. Despite the perceive threat to liquidity from the

proliferation of exchanges, the evidence to date from equity markets is reassuring (O’Hara and

Ye 2011; Degryse et al. 2011). FX liquidity aggregators, and their influence on liquidity and

market dynamics, have yet to be studied.

TheglobalintegrationofFXmarkets

Only a few researchers have studied how electronic trading may contribute to the

transmission of information as well as shocks across global FX markets. Evans and Lyons

(2002b) and Cai, Howorka and Wongswan (2008) document how electronic trading in the major

currencies affects the returns and volatility of currencies in other regions. While most researchers

view order flow as a mechanism for aggregating dispersed private information, Evans and Lyons

(2002c) also conjecture that it is a proxy for liquidity as it affects the price impact of trades.

33

Banti et al. (2012) adopt this liquidity view and use order flow from real money investors across

twenty currencies to construct a measure of global liquidity risk. Similar to the Pastor–

Stambaugh liquidity measure for the US stock market, Banti et al. (2012) show that liquidity

risk is priced in the cross-section of FX returns. Mancini et al. (forthcoming) confirm this finding

using data for 12 currencies using high-frequency data from the EBS platform. They construct a

wide range of liquidity measures and show that there are strong commonalities in liquidity across

global FX markets. They also show that low interest rate currencies used to fund carry trades

offer insurance against exposure to liquidity risk. Their data cover only the global financial crisis

from 2007-2009, so it remains to be seen if their strong results also hold in calmer periods.

Greater financial integration can have adverse effects as highlighted by the dislocation in

global FX markets during the 2007-2009 financial crisis. Despite originating in the US sub-prime

mortgage markets, Melvin and Taylor (2009) document how the crisis spread globally across

asset markets in 2007 and 2008, making it difficult to trade FX anywhere in any substantial size.

FX volatility spiked to unseen levels, liquidity disappeared, and the cost of trading currencies

skyrocketed. Thus greater integration of FX markets through electronic trading may prove to be

a double-edged sword that increases liquidity and lowers transaction costs in good times, but

transmits shocks in bad times. Again, more research on this possibility is warranted.

Section5:Microstructureandexchangeratepuzzles

The earlier discussion of order flow stressed its importance for exchange rate

determination. In this section, we explore whether order flow can contributed to resolving some

of the long-standing puzzles in FX markets, namely the forward bias puzzle, the profitability of

technical analysis, and the greater power of PPP at longer time horizons.

34

Orderflowandtheforwardbiaspuzzle

The importance of order flow for exchange rate determination provides the foundation for

recent breakthroughs in our understanding of the failure of UIP and the associated profitability of

the carry trade. The failure of UIP is so well known in international economics that we state it

here only briefly. Under UIP, equilibrium expected exchange rate returns should compensate

investors for the interest rate differential and risk premium:

E{st+1 – st} = (it* – it) + rpt (2)

where st is the (log) price of the home currency in terms of the foreign currency, it* and it are

domestic and foreign interest rates, and rpt is a time-varying risk premium.

While UIP typically implies that high interest rate currencies should depreciate relative to

low interest rate currencies, hundreds of studies find the opposite (Hodrick 1987; Engel 1996).

Many investors exploit this regularity by borrowing in currencies with low interest rates and

investing the proceeds in currencies with high interest rate, a strategy known as the “carry trade”

(Burnside 2012). Figures 5 depicts a popular carry trade during the early 2000s. Investors funded

in Japanese yen where interest rates were low and invested in the Australian dollar where the

interest rates were high, earning positive returns as the Australian dollar generally appreciated.

Economists have sought to explain this puzzle by introducing a risk premium. While earlier

studies focused on the variance of FX returns, recent evidence points to the skewness of returns

(Rafferty 2011; Brunnermeier et al. 2009). High interest rate currencies tend to exhibit

negatively-skewed returns, implying that they appreciate slowly over long periods but then crash

abruptly, as illustrated for the JPY/AUD in Figure 5.

35

Figure 5: Australian-Japanese carry trade

Current widely-respected explanations for the failure of UIP rely on the influence of

order flow on FX returns. Plantin and Shin (2011) assume that (i) the exchange rate always faces

an exogenous probability of returning to its fundamental value and (ii) order flow has a positive,

linear influence on exchange rates. The latter assumption implies that the order flow associated

with carry trades will itself cause the high-interest rate currency to appreciate. When combined

with the assumptions of (iii) ‘slow moving’ investment capital (Mitchell et al. 2007), (iv)

positive feedback from carry-trade returns to funds invested in this strategy, and (v) a non-zero

interest differential, the model produces negatively skewed returns to carry trades (Breedon et al,

2011). This model fits an extensive array of microstructure findings beyond the influence of

order flow on returns, as outlined in Osler (2012).

Abreu and Brunnermeier (2003) develop a generic model of bubbles that relies on the

response of prices to order flow. They show that coordination problems can arise under

asymmetric information. Traders will rationally choose not to sell until everyone else is selling,

but under asymmetric information they have difficultly identifying when others will sell. Traders

therefore wait longer before selling, which allows bubbles to emerge and prices to rise above

36

fundamentals. A crash inevitably occurs, though it is delayed. The information asymmetries and

coordination problems highlighted in this model can certainly be found in currency markets.

The JIMF has once again contributed to this line of research. Osler (2005) examines how

price-contingent trading, specifically stop-loss orders, create currency crashes when order flow

influences returns. A stop-loss buy order instructs a dealer to buy a specific quantity of a

currency if and when the currency’s value rises to a pre-specified level. A stop-loss sell order is

triggered when the currency’s value falls. These orders are common in currency markets.

Customers can place them free of charge and every dealer monitors a book of them. Such orders

generate order flow that tends to push FX prices further, automatically triggering yet more stop-

loss orders and associated order flow, leading to a price cascade.

The violent losses that disrupt otherwise positive carry-trade returns are typically

concentrated on just a small number of days, pointing to the importance of stop-loss orders.

Stop-loss induced price cascades are familiar to all currency traders, who describe the associated

currency moves as extremely rapid, with the rate jumping over key price levels without trading.7

Stop-loss orders can thus account for the exceptional swiftness of carry-trade unwinds.

Orderflowandtheprofitabilityoftechnicalanalysis

Many technical trading strategies are profitable in FX markets (Menkhoff and Taylor

2007). This empirical finding can be explained using order flow models. The documented

profitability of trend-following technical strategies, including those based on moving averages

and filter rules, is consistent with the same theories that explain the profitability of the carry

trade. Technical analysts predict that exchange rate down-trends (up-trends) will tend to be

7 Stop-loss orders contribute to extreme returns in other markets, such as the May 2010 flash crash in US equity markets

(CFTC-SEC 2010).

37

interrupted at specific support (or resistance) levels. If these levels are crossed, the existing trend

will intensify. These predictions have been substantiated for support and resistance levels

distributed to customers by major market players (Osler 2000). As outlined in Osler (2003), this

highly non-linear behavior follows logically when one combines the influence of order flow on

returns with the asymmetric clustering of stop-loss and take-profit orders near round numbers.

OrderflowandthePPPpuzzle

It is by now well-established that PPP holds in the long run for most currency pairs

(Rogoff, 1996). The short-run failure of continuous PPP highlights a potentially important area

in which the standard models could be improved. The short-run irrelevance and long-run

relevance of PPP emerges naturally in Black (1985), Driskill (1981), and Osler (1995), all of

whom independently develop and test models based on the insight that exchange rates are

influenced by trading flows in currency markets.8 More recently, Fan and Lyons (2003) observe

that financial order flow appears to be informative only at short horizons, while corporate order

flow is informative at long horizons. Thus order flow from different end-customers may drive

exchange rates away from PPP in the short-run but towards PPP over a longer horizon.

To understand this intuition, recall that exogenously-driven financial flows have a

stronger influence on short run exchange-rate movements than exogenously-driven corporate

flows. Over the longer horizon, however, the influence of financial flows should be

approximately zero. A financial agent who opens a position today, buying currency and creating

positive order flow, will eventually liquidate that position, selling currency and creating

offsetting negative order flow. Over a longer horizon, the net impact should be minimal. Froot

8 Dahl et al. (2008) discuss the consistency between these models and the stylized facts of currency microstructure.

38

and Ramadorai’s (2005) study of State Street’s investor flows provide support for this hypothesis

as they find that the positive influence of financial order flow disappears after about one year.

In contrast, corporate trades do not net to zero because their FX order flow represents

only one side of a round-trip corporate transaction. Consider a US firm paying for imports from a

European exporter. The US importer first buys euros through a currency dealer to pay for the