The Lease Accounting Rules are Changing FASB/IASB put Lease Project on their Agenda Bill Bosco - Leasing 101 914-522-3233 2006 AFLA Annual Meeting & Conference September 13-15, 2006 Rancho Mirage, CA

The Lease Accounting Rules are Changing FASB/IASB put Lease Project on their Agenda Bill Bosco - Leasing 101 914-522-3233 2006 AFLA Annual Meeting & Conference.

Dec 29, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

The Lease Accounting Rules are Changing

FASB/IASB put Lease Projecton their Agenda

Bill Bosco - Leasing 101

914-522-3233

2006 AFLA Annual Meeting & Conference

September 13-15, 2006

Rancho Mirage, CA

Agenda• What is changing?• Why the change? • What is the time table?• What are the alternative accounting methods?• What are the likely outcomes?• What is the industry doing about the changes?• How may my business change?• What does future hold?• Q&A

What is changing?• The FASB is changing FAS 13

• The focus is on lessee accounting

• The objectives of the changes are:

– To eliminate operating lease accounting

– To capitalize all material leases

What is behind the changes?• Change in conceptual framework

• Re-thinking the lease accounting model– Leased asset either capitalized by lessee or

off-balance sheet– Rules based with bright-line tests– Allows for financial engineering

• Global harmonization of accounting rules

• Off-balance sheet scandals

What is the timetable?• Research phase – remainder of 2006

• Board deliberation – 2007

• Preliminary views document – 2008

• Issuing final rule – 2009

Alternative LeaseAccounting Methods

The Assets and Liabilities approach

The Whole Asset approach

The Risk and Rewards approach

The Executory Contract approach

The Variable Interest approach

Capitalizes all leases at value of the lessee’s rights and obligations under the lease -typically the PV of minimum lease payments

Capitalizes the FMV of the leased asset with offsetting credits: a liability to return the asset and the PV of the minimum lease payments

The economic significance of the lessor’s residual interest would determine the nature of the transaction

The nature of the contract under commercial law and a substantive analysis of economic performance would determine the nature of the transaction

The concepts of control and risk of loss determines who records the asset

Possible Outcomes?

The Assets and Liabilities approach

The Whole Asset approach

The Risk and Rewards approach

The Executory Contract approach

The Variable Interest approach

Best Bet* Possible No Chance! Logical but Unlikely

Unlikely

*Important Variables:

• Materiality carve out = some operating leases• Usage based ($ per mile) contingent rents off-balance sheet =

lower capitalization• TRAC valued at FMV = zero value• TRAC amount included in minimum lease payments = full

capitalization of asset

What is Industry Doing?• Leasing trade organizations interacting with

the FASB• Providing industry input & expertise• Taking the “High Ground”• Help the FASB “get it right”• Influence the process to avoid burdensome

compliance for customers

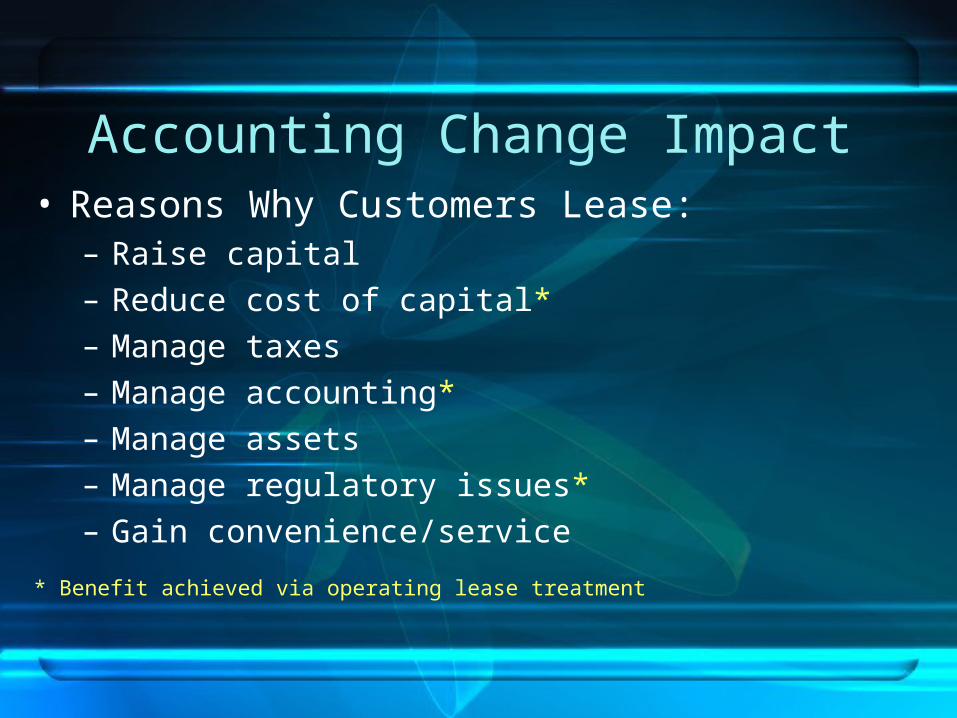

Accounting Change Impact• Reasons Why Customers Lease:

– Raise capital– Reduce cost of capital* – Manage taxes – Manage accounting* – Manage assets – Manage regulatory issues* – Gain convenience/service

* Benefit achieved via operating lease treatment

Future Changes to Lessee Accounting

• What are our concerns?– Operating lease classification is a major reason for

leasing & it may be lost– The complexities & cost to implement may

cause customers to borrow rather than lease

• The benefits!– Tax benefits lower cost of financing– Vehicle residual values are strong so minimum lease

payments can be reduced– Customers value services and convenience

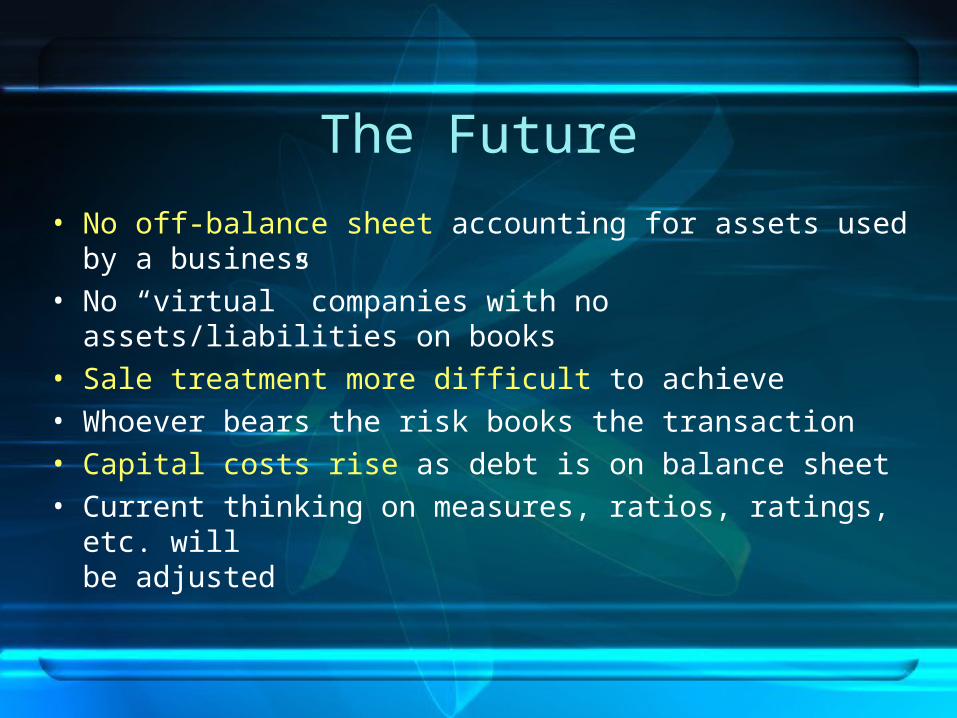

The Future

• No off-balance sheet accounting for assets usedby a business

• No “virtual” companies with no assets/liabilities on books• Sale treatment more difficult to achieve• Whoever bears the risk books the transaction• Capital costs rise as debt is on balance sheet• Current thinking on measures, ratios, ratings, etc. will

be adjusted

The Future

• Despite the pressure on off balance sheet accounting, leasing will continue to provide multiple benefits

• The value added lessor will:– Have a strong balance sheet– Provide low cost capital– Provide service/convenience and be relationship minded – Take credit & equipment risk– Price tax benefits into the lease rate– Provide customer focused creative solutions

Related Documents