The Importance of the COBIT Framework IT Processes For Effective Internal Control over the Reliability of Financial Reporting: An International Survey UWCISA Symposium, October 11-13, 2007, Toronto, Canada Uday Murthy University of South Florida David S. Kerr University of North Carolina at Charlotte

The Importance of the COBIT Framework IT Processes For Effective Internal Control over the Reliability of Financial Reporting: An International Survey.

Dec 18, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

The Importance of the COBIT Framework IT Processes For Effective Internal Control over the Reliability of

Financial Reporting: An International Survey

UWCISA Symposium,

October 11-13, 2007, Toronto,

Canada

Uday MurthyUniversity of South Florida

David S. KerrUniversity of North Carolina at Charlotte

2

Introduction and Background

Publicly held companies must have a system of internal controls, per regulatory requirements

Internal controls are heavily “IT-dependent” Need for strong IT governance COBIT – a framework for IT governance

Specifies “best practices” for IT processes Conformance to COBIT IT processes should

result in better internal control

3

Motivation

To understand the extent to which the COBIT IT processes contribute to effective internal control over the reliability of financial reporting Given limited resources, are there certain “key”

processes that organizations should focus on from the viewpoint of reliability of financial reporting?

To determine whether demographic variations in IT auditors explain differences in perceptions regarding the value of COBIT

4

COBIT

Control OBjectives for Information and related Technology

Focus of COBIT is on the management and control of IT Comprises 34 IT processes organized into 4 domains

Plan and Organize (plan) Acquire and Implement (build) Deliver and Support (run) Monitor and Evaluate (monitor)

5

Figure 1: COBIT Framework

6

Prior Work

COBIT usage survey by Guldentops and De Haes (2002) Profile of COBIT adopters (n=182)

Almost half of the respondents were from the Americas Most over 1,000 employees with 1/3rd > 10,000 employees 90% of responding organizations used COBIT Uses: audit planning and audit program development, validate current

IT controls, to evaluate IT risks, to reduce IT risks, and as a framework for improving IT

~ 40% of respondents indicated that their control framework and audit process was partly COBIT-based; less than 5% of respondents indicated that COBIT had been formally adopted and was enforced as corporate policy

7

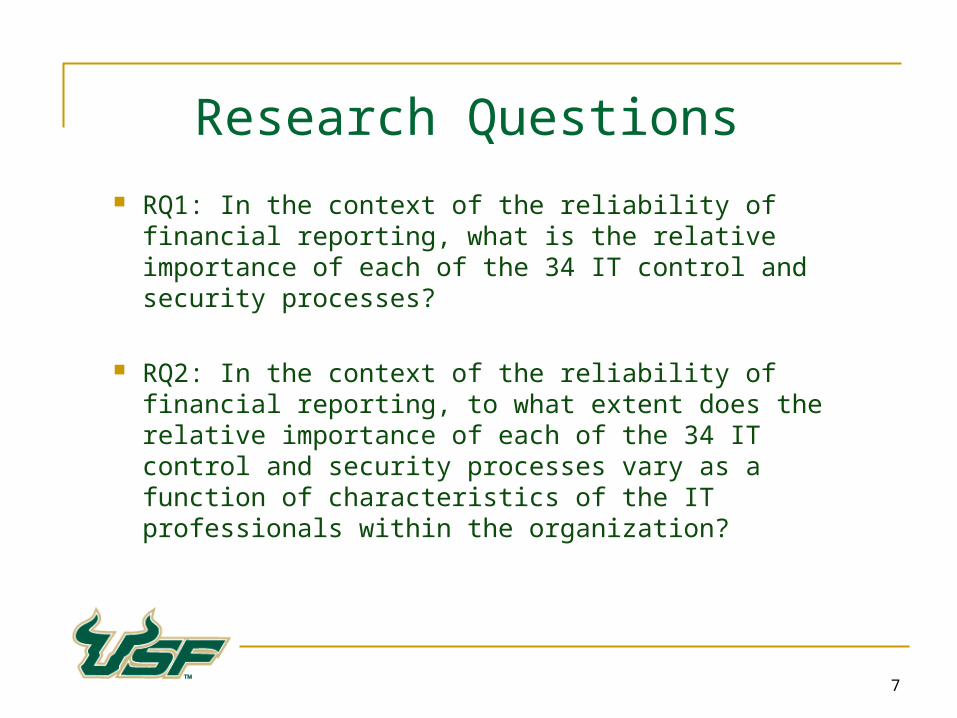

Research Questions

RQ1: In the context of the reliability of financial reporting, what is the relative importance of each of the 34 IT control and security processes?

RQ2: In the context of the reliability of financial reporting, to what extent does the relative importance of each of the 34 IT control and security processes vary as a function of characteristics of the IT professionals within the organization?

8

Method

Web survey of IT professionals ISACA members targeted through local chapters Sections of survey instrument

Demographics Background information COBIT familiarity Importance rating for each process, top 10 processes

9

Respondents 189 respondents from 21 countries Average age: 40.1 years Gender: 71% were male. Working in…

industry: 66% public accounting: 18% government: 16%

Average time with current employer: 5.8 years Degrees: 38% masters; 57% bachelors Certifications: 58% CISAs

10

Selected Demographics

TIME SPENT REVIEWING IT

CONTROLS Frequency Percent

Less than 10% 18 9.5 10% - 25% 39 20.6 26% - 50% 34 18.0 51% - 75% 33 17.5

Greater than 75% 65 34.4

Familiarity with COBIT*

Frequency Percent

1 2 1.1 2 11 5.8 3 60 31.7 4 55 29.1 5 61 32.3

* 1 = Not at all familiar; 3 = Somewhat familiar; 5 = Very familiar

11

Table 2COBIT Processes Sorted by Mean Importance Ratings

COBIT

Process* Description of process

Mean importance rating

DS5 Ensure System Security 4.661

AI6 Manage Changes 4.487

PO9 Assess Risk 4.413

DS11 Manage Data 4.333

M2 Assess Internal Control Adequacy 4.328

PO8 Ensure Compliance with External Requirements 4.222

DS10 Manage Problems and Incidents 4.101

AI4 Develop and Maintain Procedures 4.085

M1 Monitor the Process 4.079

PO11 Manage Quality 4.074

DS4 Ensure Continuous Service 4.048

M4 Provide for Independent Audit 4.021

DS7 Educate and Train Users 4.005

PO10 Manage Projects 3.952

M3 Obtain Independent Assurance 3.947

DS9 Manage the Configuration 3.931

PO2 Define the Information Architecture 3.884

12

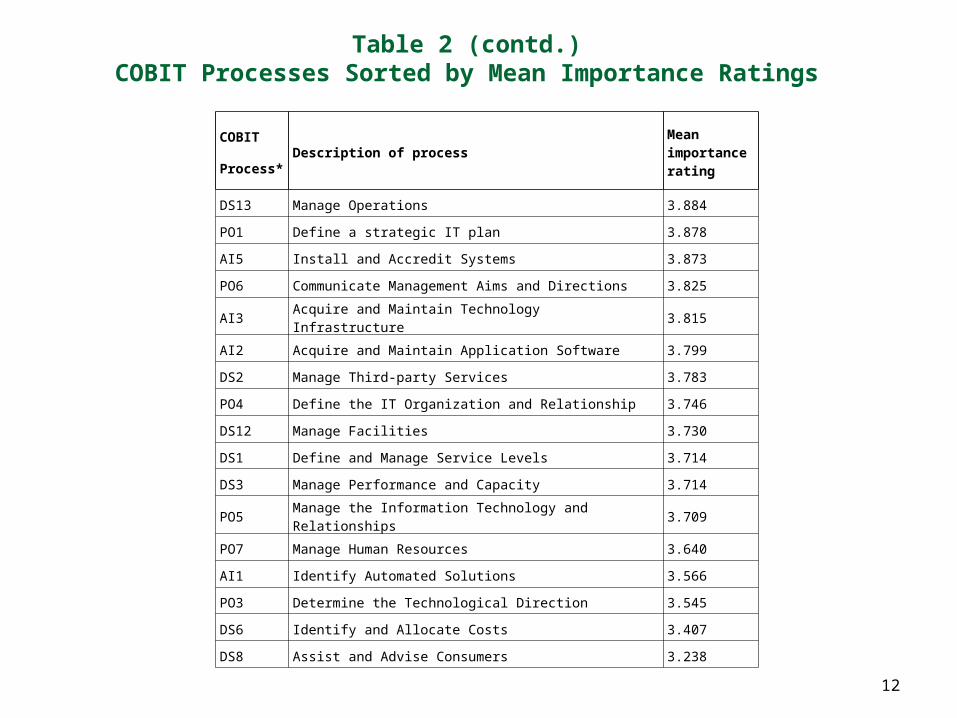

Table 2 (contd.)COBIT Processes Sorted by Mean Importance Ratings

COBIT

Process* Description of process

Mean importance rating

DS13 Manage Operations 3.884

PO1 Define a strategic IT plan 3.878

AI5 Install and Accredit Systems 3.873

PO6 Communicate Management Aims and Directions 3.825

AI3 Acquire and Maintain Technology Infrastructure 3.815

AI2 Acquire and Maintain Application Software 3.799

DS2 Manage Third-party Services 3.783

PO4 Define the IT Organization and Relationship 3.746

DS12 Manage Facilities 3.730

DS1 Define and Manage Service Levels 3.714

DS3 Manage Performance and Capacity 3.714

PO5 Manage the Information Technology and Relationships 3.709

PO7 Manage Human Resources 3.640

AI1 Identify Automated Solutions 3.566

PO3 Determine the Technological Direction 3.545

DS6 Identify and Allocate Costs 3.407

DS8 Assist and Advise Consumers 3.238

13

Table 3Number of times each IT process was selected as a “Top 10” process

COBIT process Description of process Top 10 count

DS5 Ensure System Security 147

AI6 Manage Changes 133

PO9 Assess Risk 122

M2 Assess Internal Control Adequacy 98

DS11 Manage Data 97

PO1 Define a strategic IT plan 91

M1 Monitor the Process 81

AI4 Develop and Maintain Procedures 74

DS10 Manage Problems and Incidents 70

DS7 Educate and Train Users 66

PO8 Ensure Compliance with External Requirements 64

M4 Provide for Independent Audit 58

M3 Obtain Independent Assurance 55

DS4 Ensure Continuous Service 51

DS9 Manage the Configuration 50

PO10 Manage Projects 49

PO2 Define the Information Architecture 48

14

Table 3 (contd.)Number of times each IT process was selected as a “Top 10” process

COBIT process Description of process Top 10 count

AI2 Acquire and Maintain Application Software 46

PO11 Manage Quality 45

PO6 Communicate Management Aims and Directions 44

AI3 Acquire and Maintain Technology Infrastructure 39

PO4 Define the IT Organization and Relationship 38

DS1 Define and Manage Service Levels 38

DS13 Manage Operations 36

PO5 Manage the Information Technology and Relationships 35

AI5 Install and Accredit Systems 35

PO7 Manage Human Resources 34

DS2 Manage Third-party Services 31

DS3 Manage Performance and Capacity 29

PO3 Determine the Technological Direction 24

DS6 Identify and Allocate Costs 20

AI1 Identify Automated Solutions 19

DS12 Manage Facilities 17

DS8 Assist and Advise Consumers 6

15

Table 4Factor Analysis Results: Rotated Component Matrix

COBIT process

Factor 1 Factor 2 Factor 3 Factor 4 Factor 5 Factor 6

Key processes: General & application

controlsPlanning and IT mgmt processes

Organization and relationships

processesTechnology processes

Operations and facilities processes

Independent audit processes

AI6: Manage Changes .787 .121 .104 .120 .117 .098

DS5: Ensure System Security.755 .196 .145 .175 .130 .114

DS11: Manage Data .734 .197 -.050 .153 .294 .033

M2: Assess Internal Control Adequacy .673 .067 .239 -.011 .056 .390

AI4: Develop and Maintain Procedures .643 .041 .176 .348 .050 .143

PO9: Assess Risk .624 .092 .417 .093 .138 .221

DS10: Manage Problems and Incidents .584 .431 .166 .000 .354 .074

M1: Monitor the Process .551 .254 .244 -.056 .245 .318

DS7: Educate and Train Users.533 .326 .171 .274 .102 .081

AI5: Install and Accredit Systems.497 .083 .057 .458 .262 .165

DS4: Ensure Continuous Service.280 .764 -.002 .149 .178 -.023

DS3: Manage Performance and Capacity .186 .711 .249 .132 .269 .131

DS1: Define and Manage Service Levels .202 .693 .242 .066 .235 .197

PO3: Determine the Technological Direction -.011 .649 .511 .251 -.011 -.004

PO1: Define a strategic IT plan.158 .648 .428 -.011 .036 .040

DS8: Assist and Advise Consumers-.010 .616 .210 .177 .343 .263

DS6: Identify and Allocate Costs-.015 .590 .252 .148 .217 .478

PO10: Manage Projects .282 .543 .181 .300 .019 .039

PO11: Manage Quality .484 .485 .164 .159 -.064 .063

16

Table 4 (continued)Factor Analysis Results: Rotated Component Matrix

Factor 1 Factor 2 Factor 3 Factor 4 Factor 5 Factor 6

COBIT process

Key processes: General & application

controlsPlanning and IT mgmt processes

Organization and relationships

processesTechnology processes

Operations and facilities processes

Independent audit processes

PO4: Define the IT Organization and Relationship

.138 .285 .759 .063 .147 .131

PO5: Manage the Information Technology and Relationships

.148 .209 .711 .091 .171 .180

PO6: Communicate Management Aims and Directions

.133 .510 .587 .071 .083 .086

PO7: Manage Human Resources.167 .280 .572 .165 .245 .134

PO2: Define the Information Architecture .266 .454 .566 .148 -.095 -.067

PO8: Ensure Compliance with External Requirements .388 .032 .520 .179 .263 -.002

AI2: Acquire and Maintain Application Software .283 .126 .188 .800 .131 -.023

AI3: Acquire and Maintain Technology Infrastructure .140 .242 .256 .707 .306 -.012

AI1: Identify Automated Solutions.160 .408 -.008 .656 -.085 .285

DS13: Manage Operations.444 .185 .272 .185 .606 .252

DS2: Manage Third-party Services.247 .351 .223 .084 .577 -.043

DS12: Manage Facilities .293 .338 .109 .167 .570 .315

DS9: Manage the Configuration.409 .042 .393 .277 .546 .075

M3: Obtain Independent Assurance.441 .109 .158 .086 .048 .765

M4: Provide for Independent Audit.458 .156 .086 .086 .163 .672

17

Table 5Ratings of Technology Processes by Employment Type

Employment type Mean* Std. Deviation NPublic accounting 4.0505 .67762 33

Industry 3.6640 .83671 124

Government 3.6022 .65783 31

Total 3.7216 .79507 188

Panel A: Descriptive Statistics* 1=Not at all important; 5=Very important.

Source

Type III Sum of Squares df Mean Square F Sig.

Corrected Model 4.424(a) 2 2.212 3.596 .029

Intercept 1813.311 1 1813.311 2948.191 .000

Employment 4.424 2 2.212 3.596 .029

Error 113.786 185 .615

Total 2722.111 188

Corrected Total 118.210 187

Panel B: Tests of Between-Subjects Effects

a R Squared = .037 (Adjusted R Squared = .027)

18

Table 6Ratings of Technology Processes: North America vs. Rest of the World

Panel A: Descriptive Statistics* 1=Not at all important; 5=Very important.

Panel B: Tests of Between-Subjects Effects

a R Squared = .017 (Adjusted R Squared = .011)

Country Mean* Std. Deviation NUSA or Canada 3.8197 .80259 98

All other countries3.6148 .77719 90

Total 3.7216 .79507 188

Source

Type III Sum of Squares df Mean Square F Sig.

Corrected Model 1.970(a) 1 1.970 3.152 .077

Intercept 2593.100 1 2593.100 4149.321 .000

Country 1.970 1 1.970 3.152 .077

Error 116.240 186 .625

Total 2722.111 188

Corrected Total 118.210 187

19

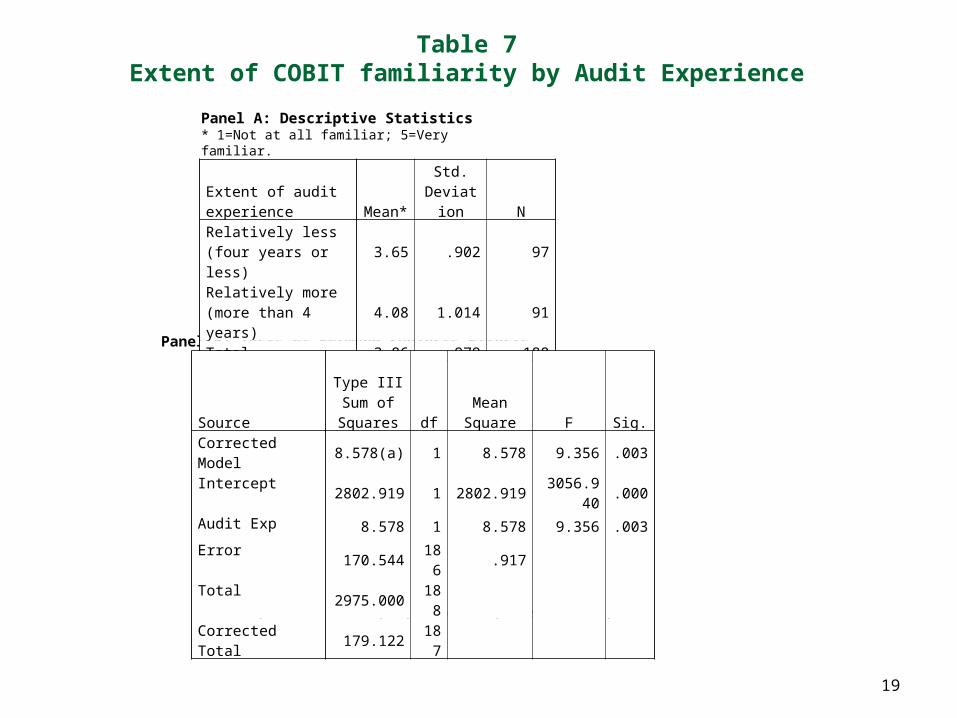

Table 7Extent of COBIT familiarity by Audit Experience

Panel A: Descriptive Statistics* 1=Not at all familiar; 5=Very familiar.

Panel B: Tests of Between-Subjects Effects

a R Squared = .048 (Adjusted R Squared = .043)

Extent of audit experience Mean*

Std. Deviation N

Relatively less (four years or less)

3.65 .902 97

Relatively more (more than 4 years)

4.08 1.014 91

Total 3.86 .979 188

Source

Type III Sum of Squares df

Mean Square F Sig.

Corrected Model 8.578(a) 1 8.578 9.356 .003

Intercept 2802.919 1 2802.919 3056.940 .000

Audit Exp 8.578 1 8.578 9.356 .003

Error 170.544 186 .917

Total 2975.000 188

Corrected Total 179.122 187

20

Table 8Extent of work relating to task of reviewing/evaluating IT controls:

North America vs. Rest of the World

Panel A: Descriptive Statistics+Scale 1 = less than 10%; 2 = 10% - 25%; 3 = 26% - 50%; 4 = 51% - 75%; 5 = greater than 75%.

Panel B: Tests of Between-Subjects Effects

a R Squared = .028 (Adjusted R Squared = .022)

Country Mean+

Std. Deviation N

USA or Canada 3.69 1.380 98

All other countries 3.23 1.366 90

Total 3.47 1.389 188

SourceType III Sum

of Squares df Mean Square F Sig.Corrected Model 9.951(a) 1 9.951 5.274 .023

Intercept 2251.270 1 2251.270 1193.265 .000

Country 9.951 1 9.951 5.274 .023

Error 350.916 186 1.887

Total 2629.000 188

Corrected Total 360.867 187

21

Table 9Extent of Work Relating to Task of Reviewing/Evaluating IT Controls

by Employment Type

Panel A: Descriptive Statistics+Scale 1 = less than 10%; 2 = 10% - 25%; 3 = 26% - 50%; 4 = 51% - 75%; 5 = greater than 75%.

Panel B: Crosstabulation

Employment type Mean+

Std. Deviation N

Public accounting 3.94 1.345 33

Industry 3.46 1.428 124

Government 3.03 1.140 31

Total 3.47 1.390 188

Percentage of work relating to task of

reviewing/evaluating IT controls

Employment type

Less than 10%

10% - 25%

26% - 50%

51% - 75%

Greater than 75% Total

Public accounting Count 2 4 6 3 18 33

Expected Count 3.2 6.7 6.0 5.8 11.4 33.0

Industry Count 14 26 15 27 42 124

Expected Count 11.9 25.1 22.4 21.8 42.9 124.0

Government Count 2 8 13 3 5 31

Expected Count 3.0 6.3 5.6 5.4 10.7 31.0

Total Count 18 38 34 33 65 188 Expected Count 18.0 38.0 34.0 33.0 65.0 188.0

22

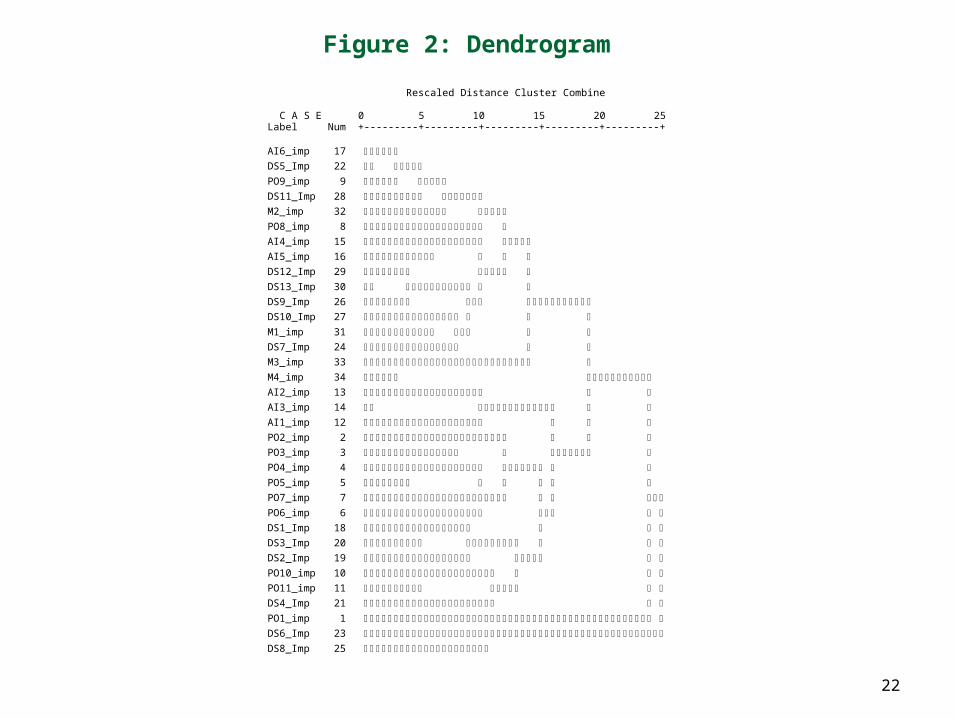

Figure 2: Dendrogram

Rescaled Distance Cluster Combine C A S E 0 5 10 15 20 25 Label Num +---------+---------+---------+---------+---------+ AI6_imp 17 DS5_Imp 22 PO9_imp 9 DS11_Imp 28 M2_imp 32 PO8_imp 8 AI4_imp 15 AI5_imp 16 DS12_Imp 29 DS13_Imp 30 DS9_Imp 26 DS10_Imp 27 M1_imp 31 DS7_Imp 24 M3_imp 33 M4_imp 34 AI2_imp 13 AI3_imp 14 AI1_imp 12 PO2_imp 2 PO3_imp 3 PO4_imp 4 PO5_imp 5 PO7_imp 7 PO6_imp 6 DS1_Imp 18 DS3_Imp 20 DS2_Imp 19 PO10_imp 10 PO11_imp 11 DS4_Imp 21 PO1_imp 1 DS6_Imp 23 DS8_Imp 25

23

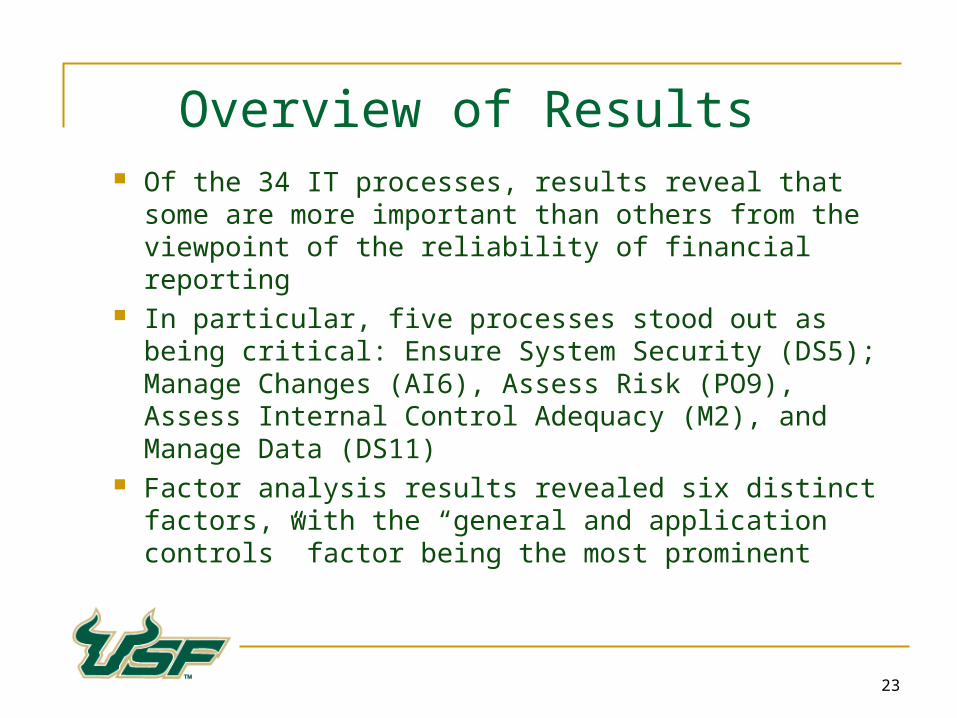

Overview of Results Of the 34 IT processes, results reveal that some are more

important than others from the viewpoint of the reliability of financial reporting

In particular, five processes stood out as being critical: Ensure System Security (DS5); Manage Changes (AI6), Assess Risk (PO9), Assess Internal Control Adequacy (M2), and Manage Data (DS11)

Factor analysis results revealed six distinct factors, with the “general and application controls” factor being the most prominent

24

Limitations

True response rate and hence extent of non-response bias is unknown

Extent to which importance ratings were affected by the length of the instrument is unknown (the “fatigue factor”)

Order of 34 processes was not randomized Despite instructions, it is possible that respondents were not

attuned to the focus on the effect of the COBIT IT processes on the reliability of financial reporting

Lack of a “reference point” or context for assessing importance of IT processes

25

Conclusion and Future Research

Some COBIT IT processes are deemed more critical than others from the standpoint of the reliability of financial reporting

Internal and external auditors can focus their attention on the “Top 10” most critical COBIT processes

Future research could focus on the why question – why some IT processes are deemed more critical than others

Also worth investigating the extent to which COBIT processes contribute to other organizational objectives

Related Documents