The Importance of Manufacturing Southern New England Economic Summit and Outlook May 30, 2003

The Importance of Manufacturing Southern New England Economic Summit and Outlook May 30, 2003.

Dec 27, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

The Importance of Manufacturing

Southern New England

Economic Summit and Outlook

May 30, 2003

The Importance of Manufacturing OVERVIEW

Manufacturing Outlook

Campaign for Growth and Manufacturing Renewal

GDP Forecast

Gross domestic product

0

0.5

1

1.5

2

2.5

3

3.5

4

2003.1 2003.2 2003.3 2003.4 2002 2003 2004

Per

cen

t C

han

ge

(saa

r)

Quarters Annual

Personal Consumption Forecast

Personal consumption expenditures

0

0.5

1

1.5

2

2.5

3

3.5

2003.1 2003.2 2003.3 2003.4 2002 2003 2004

Pe

rce

nt

Ch

an

ge

(sa

ar)

Quarters Annual

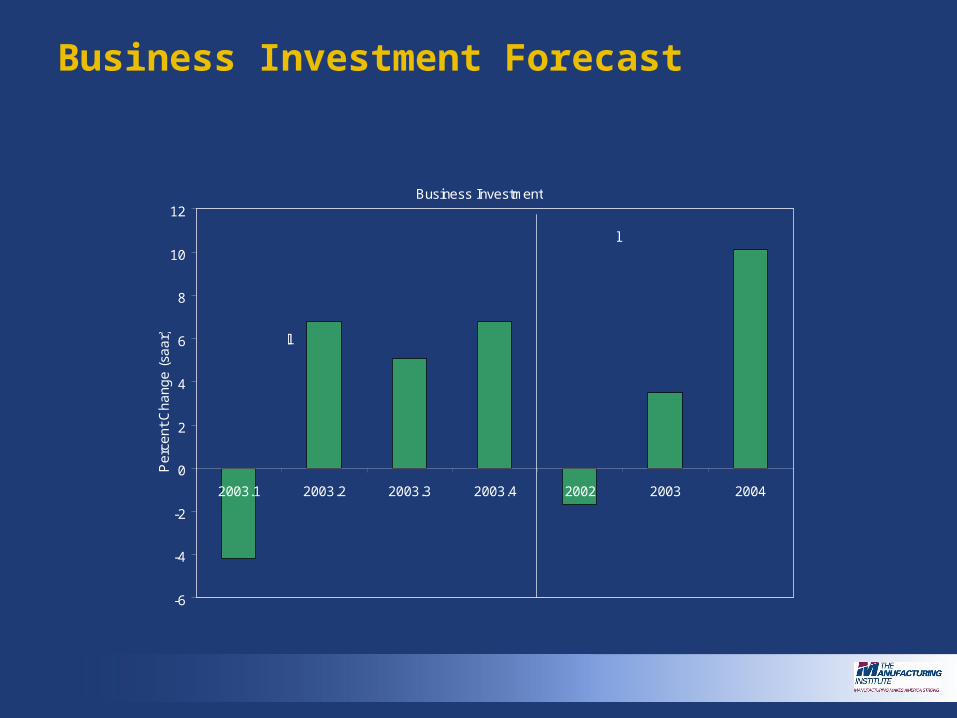

Business Investment Forecast

Business Investment

-6

-4

-2

0

2

4

6

8

10

12

2003.1 2003.2 2003.3 2003.4 2002 2003 2004

Pe

rce

nt

Ch

an

ge

(sa

ar) Overall

Quarters Annual

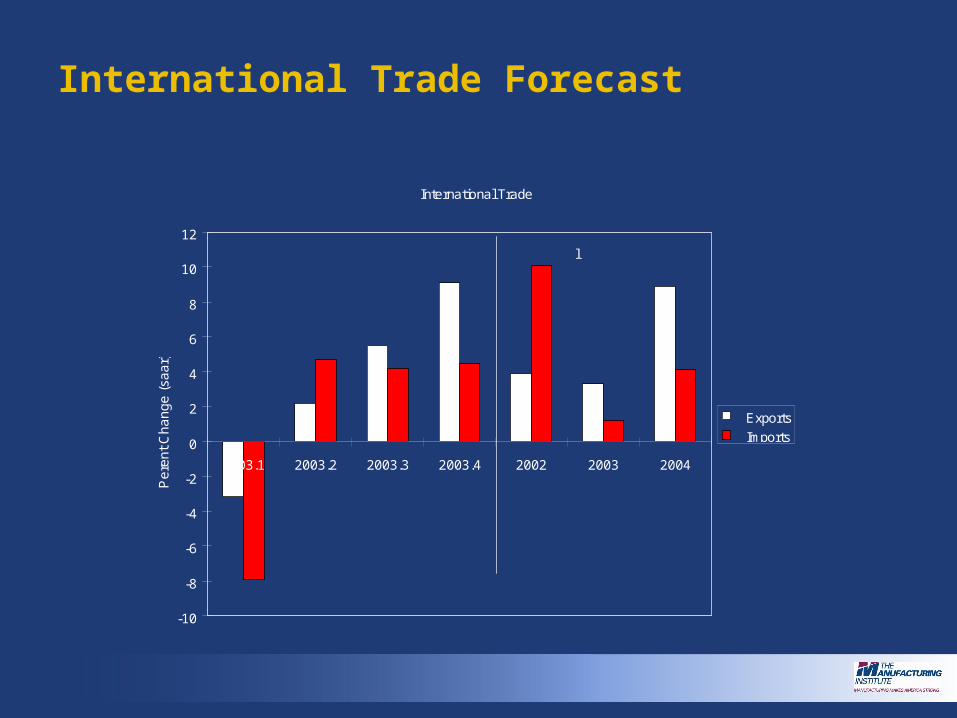

International Trade Forecast

International Trade

-10

-8

-6

-4

-2

0

2

4

6

8

10

12

2003.1 2003.2 2003.3 2003.4 2002 2003 2004

Pe

ren

t C

ha

ng

e (

saa

r)

Exports

Imports

Quarters Annual

Changing Face of Manufacturing – Largest Sectors in 1950

0%

2%

4%

6%

8%

10%

12%

14%

Food PrimaryMetals

MotorVehicles

Share of Manufacturing

GDP

1950

2001

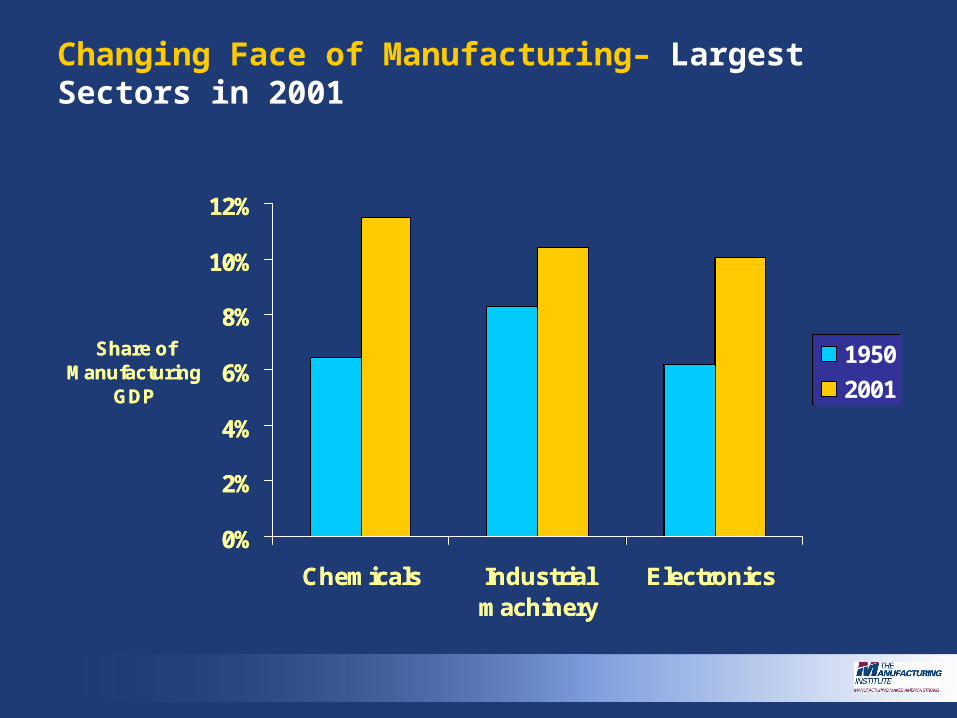

Changing Face of Manufacturing– Largest Sectors in 2001

0%

2%

4%

6%

8%

10%

12%

Chemicals Industrialmachinery

Electronics

Share of Manufacturing

GDP

1950

2001

0%

2%

4%

6%

8%

10%

12%

Chemicals Industrialmachinery

Electronics

Share of Manufacturing

GDP

1950

2001

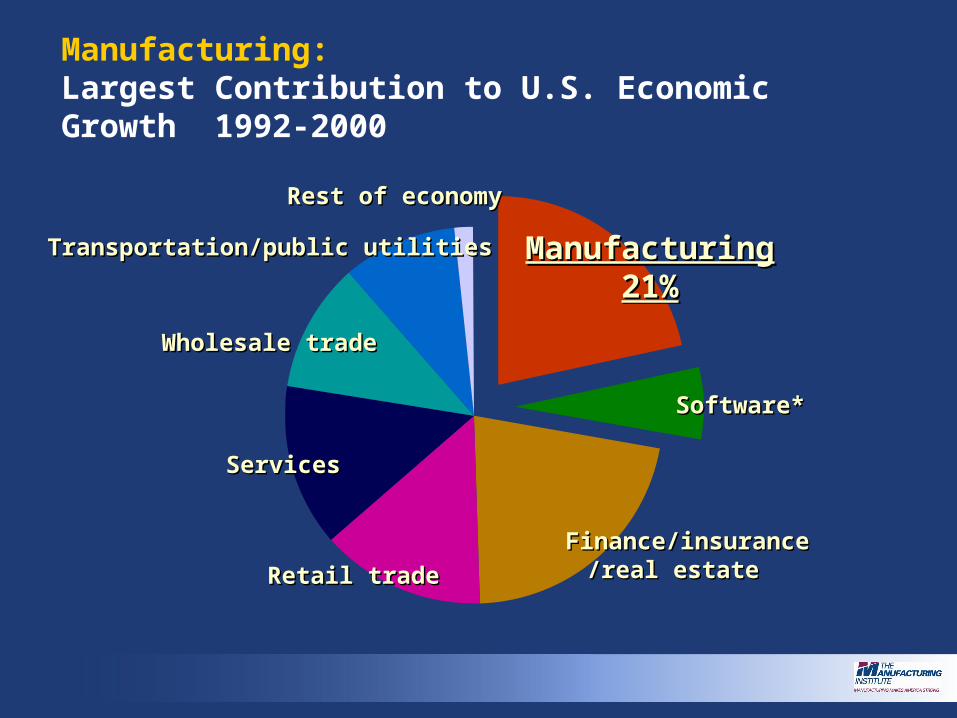

Manufacturing’s Contributions are Huge:

»GDP growth»Productivity»Wages»R&D»International Trade

Manufacturing: Largest Contribution to U.S. Economic Growth 1992-2000

ManufacturingManufacturing21%21%

Software*Software*

Finance/insuranceFinance/insurance/real estate/real estate Retail tradeRetail trade

ServicesServices

Wholesale tradeWholesale trade

Transportation/public utilities Transportation/public utilities

Rest of economyRest of economy

Productivity Growth: Higher and Faster

Manufacturing Productivity Has Grown 50 Percent Faster Than Overall Productivity Growth

Manufacturing Share of Real GDP & EmploymentGDP Has Remained ConstantWhile Share of Employment Has Declined

Manufacturing Pays More: 22 Percent Higher Wages

$10,000$10,000

$20,000$20,000

$30,000$30,000

$40,000$40,000

$50,000$50,000

$60,000$60,000

ManufacturingManufacturing Rest of WorkforceRest of Workforce

Ave

rage

An

nu

al C

omp

ensa

tion

Ave

rage

An

nu

al C

omp

ensa

tion

Wages

Benefits

Wholesale/retail

Services

Agriculture

Trans, finance, minerals, Trans, finance, minerals, construction, etc.. construction, etc..

Manufacturing Multiplier: Supports 9 Million Jobs in Other Sectors

00

22

44

66

88

1010

1212

1414

1616

Manufacturing JobsManufacturing Jobs Other Sectors’Other Sectors’

Jobs

(in

mil

lion

s)Jo

bs (

in m

illi

ons)

Manufacturing R&DAmerican Manufacturers Contribute More to R&D

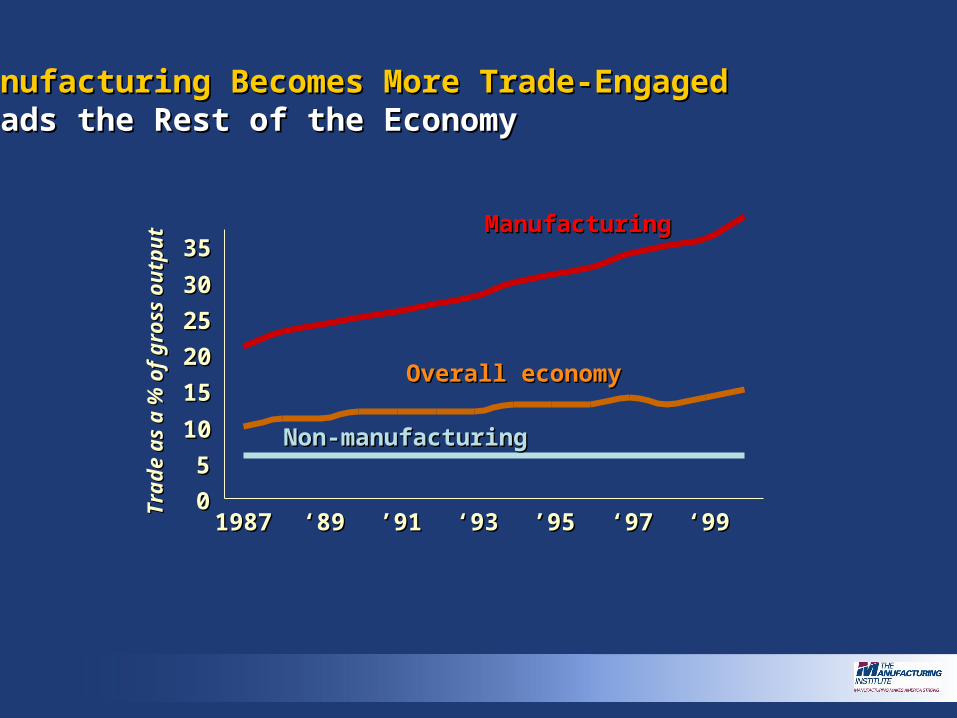

Manufacturing Becomes More Trade-EngagedManufacturing Becomes More Trade-Engaged LeadsLeads the Rest of the Economythe Rest of the Economy

00

55

1010

1515

2020

2525

3030

3535

19871987 ‘‘8989 ’’9191 ‘‘9393 ’’9595 ‘‘9797 ‘‘9999

ManufacturingManufacturing

Overall economyOverall economy

Non-manufacturingNon-manufacturing

Tra

de a

s a

% o

f gr

oss

outp

ut

Tra

de a

s a

% o

f gr

oss

outp

ut

Short Term Challenges: 2001 was a Manufacturing Recession

-7%

-6%

-5%

-4%

-3%

-2%

-1%

0%

1%

2%

Manufacturing Overall GDP Non-manufacturing

Percent Change in GDP,

2001

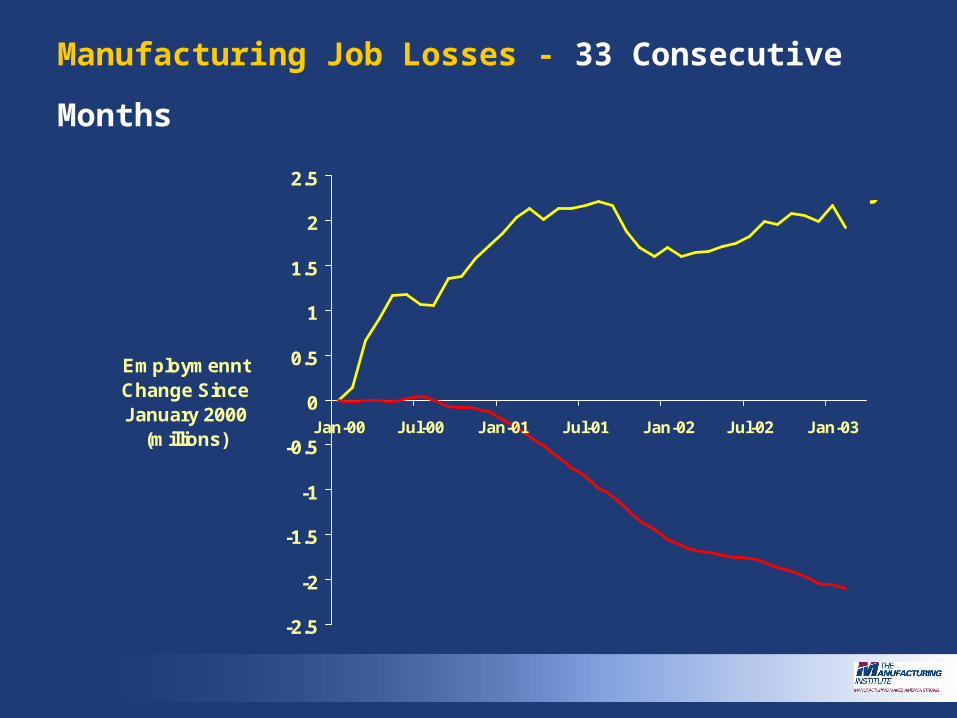

Manufacturing Job Losses – 33 Consecutive

Months

-2.5

-2

-1.5

-1

-0.5

0

0.5

1

1.5

2

2.5

Jan-00 Jul-00 Jan-01 Jul-01 Jan-02 Jul-02 Jan-03

Employmennt Change Since January 2000

(millions)

Rest of Economy

Manufacturing Job Losses - 33 Consecutive

Months

-2.5

-2

-1.5

-1

-0.5

0

0.5

1

1.5

2

2.5

Jan-00 Jul-00 Jan-01 Jul-01 Jan-02 Jul-02 Jan-03

Employmennt Change Since January 2000

(millions)

Manufacturing

Rest of Economy

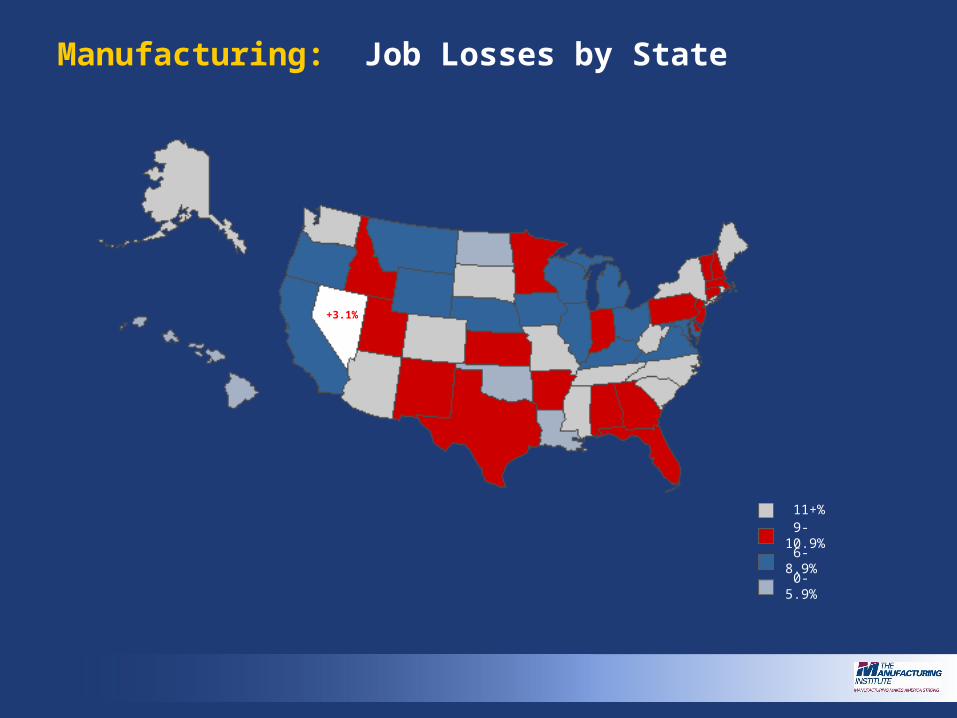

Manufacturing: Job Losses by State

+3.1%

0-5.9%

6-8.9%

9-10.9%

11+%

Manufacturing Jobs Lost Since 2000

# 19 Connecticut 27,800 jobs 10.5% of all manufacturing jobs

# 21 Massachusetts 45,200 jobs 10.3% of all manufacturing jobs

# 7 Rhode Island 9,300 jobs 12.2% of all manufacturing jobs

~ ~ ~

#1 Washington State 55,700 jobs 15.7% of all manufacturing jobs

#2 Maine 12,600 jobs 14.6% of all manufacturing jobs

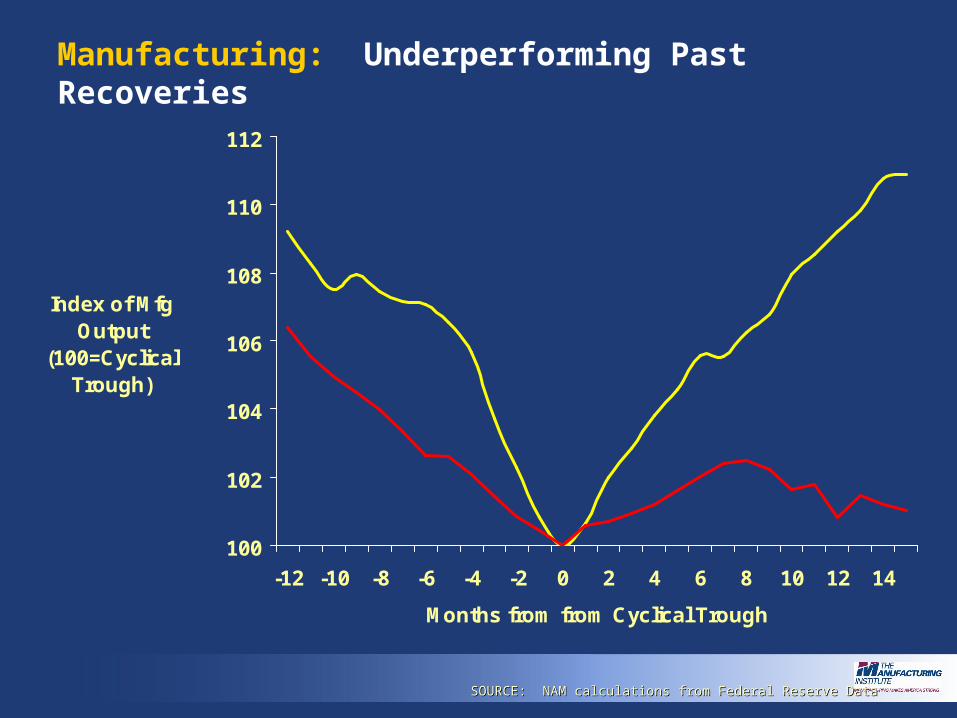

Manufacturing: Underperforming Past Recoveries

100

101

102

103

104

105

106

107

108

109

110

-12 -10 -8 -6 -4 -2 0 2 4 6 8 10 12

Months from from Cyclical Trough

Index of Mfg Output

(100=Cyclical Trough)

Previous Six Mfg Recoveries

Manufacturing: Underperforming Past Recoveries

SOURCE: NAM calculations from Federal Reserve DataSOURCE: NAM calculations from Federal Reserve Data

100

102

104

106

108

110

112

-12 -10 -8 -6 -4 -2 0 2 4 6 8 10 12 14

Months from from Cyclical Trough

Index of Mfg Output

(100=Cyclical Trough)

Previous Six Mfg Recoveries

2002

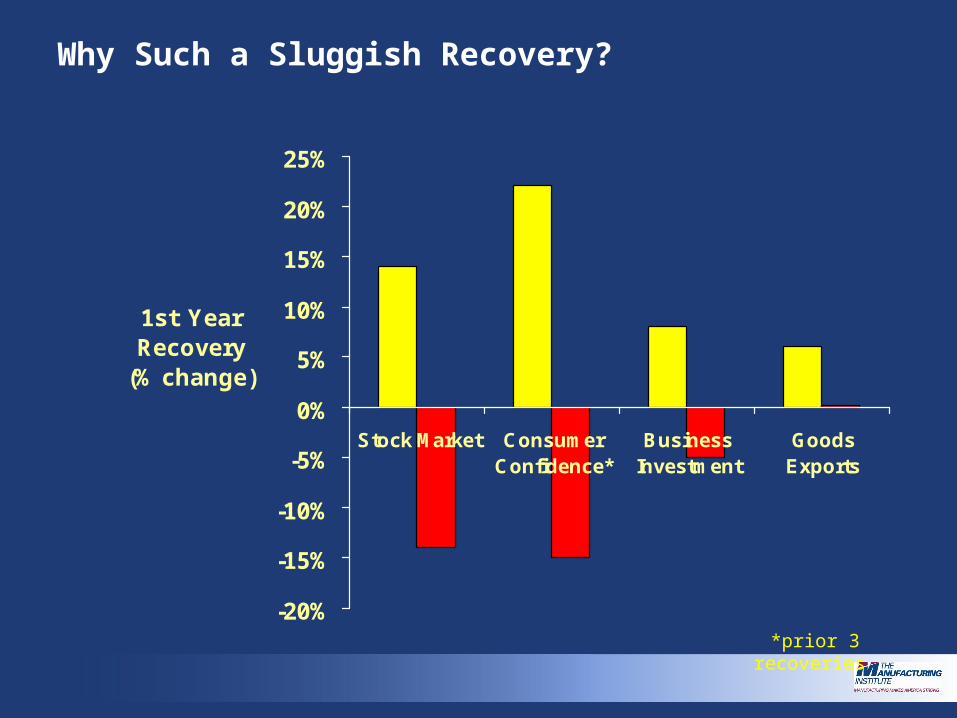

Why Such a Sluggish Recovery?

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

Stock Market ConsumerConfidence*

BusinessInvestment

GoodsExports

1st Year Recovery

(% change)

Previous 6 Recoveries

2002

*prior 3 recoveries

What We Need:

NAM’s Strategy for Growth and Manufacturing

Renewal:

“ a plan of action for the federal government to complement private sector actions to effectively sustain U.S. manufacturing leadership at the top of global competitiveness.”

Legislative Issues for Manufacturing: NAM Pro-growth Priorities

• Reduce Tax Burden

• Expand International Trade

• Curb Health Care Mandates

• Stabilize Energy Pricing

»Raise Awareness about manufacturing’s strengths

»Draw Attention to Challenges»Identify New Solutions for

Structural Problems »Enact Solutions

www.nam.org/renewal

Workforce Objective– Make manufacturing preferred career

choice by 2010

The Bad News…Manufacturing Faces a Crisis

• Little understanding of our importance

• Negative images repels desirable candidates

• Education and training systems are not tuned in to our needs

• WE ARE BEHIND THE CURVE

Manufacturing’s Image Is Bad

• “Dark, dirty, dangerous, dead-end, demeaning”

• Assembly Line “Torturous and tedious”

“Ant in an ant colony”

• Low pay, lay-offs, polluters and scandal

• Old Economy,” declining, unimportant, gone off-shore

The Good News…We can have a major impact

We can increase the number and quality of recruits if manufacturers…

• Implement a sustained campaign to improve our image

• Fill the career information void

• Make high schools, community colleges and universities focus on our needs and skill sets

First Report of the Manufacturing

Campaign President: announce that manufacturingis a high priority and pursue the right policies

Congress: establish National ManufacturingDay and enact the right policies

Educators: Take students to modern plantsand provide accurate career information

Manufacturers: open doors to students and teachers

June 10--Second Report

Securing America's Future:

The Case for a Strong Manufacturing Base

• Innovation process powering the economy

• Formula for higher standard of living

• Troublesome signs

October: Third report

The high cost of doing business in the US:

»Regulatory costs»Taxes»Health care and pensions»Legal system»Energy

U.S. Department of Commerce: Field Hearings on Manufacturing Competitiveness• Over 20 field hearings around the country

• New Hampshire on May 29 on IT and telecomm

• Future hearing in Conn. on aerospace and machinery

• Interim report in July

• Final report in September

The Importance of Manufacturing

Southern New England Economic Summit and

OutlookMay 30, 2003

Related Documents