THE IMPACT OF PARTICIPATION OF BUDGET SETTING ON THE JOB SATISFACTION OF EMPLOYEES AND THE PERFORMANCE OF LOCAL GOVERNMENT (Empirical Study at Daerah Istimewa Yogyakarta) POPI FAUZIATI Senior Lecturer [email protected] At Department of Accountancy University of Bung Hatta ABSTRACT Many accounting studies that examine relationships with satisfaction the participation and performance budgeting. The results indicated that participation has a positive relationship with satisfaction (French, Kay & Meyer, 1966; Chenhall, 1986; Frucot & Shearon, 1991). While relations with the participation of the performance can be divided into two opinions. First, the study suggested a positive relationship (Kenis, 1979; Merchant, 1981; Brownell, 1982; Brownell and McInnes, 1986). Second, research indicates a negative relationship (Milani, 1975, Bryan and Locke, 1967). To mediate the second opinion may be used is the intervening or moderating variable in the relationship. Kren (1992) found that participation has a relationship to job performance through relevant information (JRI). The purpose of this study was to test empirically the relationship with satisfaction the participation and performance using job relevant information (JRI) as an intervening variable. JRI is the information that facilitates decision-making. Data were collected through questionnaires and 149 questionnaires media that can be processed at the rate (53%) and processed using Analysis of Moment Structure (AMOS 4.01).The results indicate that the relationship of participation in job satisfaction has a strong relationship. While the job relevant information (JRI) cannot mediate the relationship of participation in the performance or

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

THE IMPACT OF PARTICIPATION OF BUDGET SETTING ON THE JOBSATISFACTION OF EMPLOYEES AND THE PERFORMANCE

OF LOCAL GOVERNMENT(Empirical Study at Daerah Istimewa Yogyakarta)

POPI FAUZIATISenior Lecturer

[email protected] At Department of AccountancyUniversity of Bung Hatta

ABSTRACT

Many accounting studies that examine relationships withsatisfaction the participation and performance budgeting. Theresults indicated that participation has a positive relationshipwith satisfaction (French, Kay & Meyer, 1966; Chenhall, 1986;Frucot & Shearon, 1991). While relations with the participation ofthe performance can be divided into two opinions. First, the studysuggested a positive relationship (Kenis, 1979; Merchant, 1981;Brownell, 1982; Brownell and McInnes, 1986). Second, researchindicates a negative relationship (Milani, 1975, Bryan and Locke,1967). To mediate the second opinion may be used is the interveningor moderating variable in the relationship. Kren (1992) found thatparticipation has a relationship to job performance throughrelevant information (JRI).

The purpose of this study was to test empirically therelationship with satisfaction the participation and performanceusing job relevant information (JRI) as an intervening variable.JRI is the information that facilitates decision-making. Data werecollected through questionnaires and 149 questionnaires media thatcan be processed at the rate (53%) and processed using Analysis ofMoment Structure (AMOS 4.01).The results indicate that therelationship of participation in job satisfaction has a strongrelationship. While the job relevant information (JRI) cannotmediate the relationship of participation in the performance or

results of the budget is in contrast with the results of Kren(1992).

Key Words: Participation, Job Relevant Information, LocalGovernment, Job Satisfaction, Performance.

INTRODUCTION

Background

The running autonomy recently is a part of the existing

reform on the national life by the central government,

accommodated in Regulation No. 22/1999 on district Government.

This district autonomy is formally carried out in early year of

2001. One of the consequences of the birth of the regulation is

the need of an arrangement of central and district government

financial relationship. District autonomy, which has more

“content”, has become a basic of hope of district government and

the society in the district for long time. Currently, with the

birth of Regulations No. 22 and No. 25/1999, this hope starts to

be real. Those regulations are the main part of the reform in

district financial side.

In running its daily duties, district government forms

District Official comprising of operator element and staff

element. Operator element comprises of: official giving basic

services, such as education and health, official giving service

arrangement of society’s economic development, official providing

and implementing instrument, and official seeking for fund.

While, staff element comprises of District Development Planning

Official (BAPPEDA), District Area Secretary (SEKWILDA), and

Inspectorate.Therefore, with wider responsibility of operator and

staff elements, the two elements have to be rigorous in

implementing their duties, which can be reflected from their

performance. The more rigorous they are in implementing their

duties, the better the performance is, and vice versa. While the

feeling of like and dislike to someone on his or her work in the

realization of someone’s working satisfaction.

The performance and the working satisfaction can be

reflected in the participation of someone on something valuable,

either in place at which he or she is involved everyday, or in

the organization as a whole. The participation can take a form of

its participation in determining vision, mission, organizational

objective, and the determination of organizational policies. One

of the reflections is the management instrument of tool in the

planning and controlling process.

With the existence of participation from subordinates in

budget setting, it can give an opportunity to include local

information. With this way, subordinates can communicate or

convey several personal informations, which likely to be included

in the standard or budget used as the base of performance

measurement. But, subordinates can also not convey or hide

several personal informations; so, it can affect their

performance. This budget setting in a period of organizational

activities gives several benefits: planning, organizing,

controlling, coordination, communication, and motivation. Another

benefit of budget is to communicate and to motivate. Similarly as

what has been explained above, the subordinates and superiors to

exchange information can use budget so that the decision made is

the result of together decision. The motivation benefit emerges

because the budget is used as a base for the superior in

implementing an action to reach the objectives of the department

he o she led. By seeing the number of benefit, which can be

given by the budget, therefore, the researcher is interested to

test on how is “The Impact of Participation In Budget Setting on

The Performance And The Working Satisfaction of Regencies and

Counties Government in DIY.” The writer wants to retest whether

by using the same theory, but different sample and location will

give the same result as the previous research.

The reason why the researcher do this is the similarity of

the process of budget setting in our country, which asking for

each official participation to give any program, which will be

implemented next year, and how much is the cost needed of the

program. With the participation of officer in budget setting,

thus, the researcher wants to examine how is the level of

satisfaction and performance of the officer involved in the

budget setting.

Basically, this research is a replication of the research

carried out by Kren (1992), entitled: “Budgetary Participation

and Managerial Performance: The Impact of Information and

Environmental Volatility”, taking sample manages in the

manufacture companies, which was pure private companies.

Problem Formulation

In profit organization, participation in budget setting

affects positively on the working satisfaction, but how if it is

tested in the non-profit organization (District Government). The

result of the pervious research shows inconsistent result on the

impact of participation in the budget setting on the performance.

Beside found the existence of positive relation, it is also found

negative relation. Because of the existence of inconsistency,

the result of the research, therefore, the researcher wants to

find out how is the impact of participation in budget setting on

the working satisfaction and the performance of regencies and

Counties Government, and wishes to test whether the job relevance

information variable can mediate the relation between the

participation in budget setting and the performance.

Research Objectives and Benefits

The objective of this research is to uncover empirically the

amount of the impact between the variable of participation in

budget setting and the working satisfaction and the performance

of Regencies and Counties government. In detail, the objective of

this research is to give empirical prove on the amount of the

relation between participation in budget setting on the working

satisfaction and the performance, and the role of job relevance

information variable in mediating the relation between the

participation in budget setting with the performance.

There are two benefits wanted to obtained from this

research, first, to give knowledge to the academic about the

impact of participation in budget setting on the working

satisfaction and performance, in which the relation between the

participation in budget setting and performance is mediated by

the job relevance information. Second, to give input for the

authority related to the district government to use and evaluate

the result of this research in reaching the working satisfaction

and performance, especially in increasing the effectiveness of

budget setting and performance.

THEORETICAL FRAMEWORK AND HYPOTHESIS DEVELOPMENT

A. Participation in Budget Setting

Participation is a process of cooperation in decision making

by two groups or more, affecting on the decision itself in the

future (Leung, 1990). The participation in budget setting is the

involvement, which comprises of giving opinion, consideration and

ideas from subordinates and leaders in preparing and revising the

budget.

The research on participation in budget setting is often

carried out by researchers in management accounting, probably

because of participation has big possibility to be developed in a

research, compared with other variables related to the budget.

Argyris (1952) concluded that the biggest contribution of the

budgeting activity will be happened if the subordinates are

allowed to participate in budget setting activity. Argyris (1955)

also said that the subordinate’s flow has to be given an

opportunity to participate in various decisions made by the

organization, in which the decision directly or indirectly

affects on them. Brownell (1982a) explained that the manager

participation in the budget setting process is the process in

which the managers are assessed on their performance and will get

a reward based the reached budget target, their involvement, and

their impact of on the setting of budget target. The level on

involvement and the impact of managers in the process of budget

setting are the condition differentiating the participative

budget and non-participative budget (Milani, 1975).

B. Working Satisfaction

Working satisfaction is an individual characteristic. Each

individual has different satisfaction appropriate with the system

and the value applied in him or her. Lawler (1991) characterized

four theoretical approaches discussing on the working

satisfaction, fulfillment theory, equity theory, discrepancy

theory, and two-factor theory.

Working satisfaction can have a very important position for

the organizational behavior (Luthans, 1995: 125). The important

factors for the working satisfaction can be seen from 3 sides.

First, working satisfaction is an emotional factor, abstract, but

can only be predicted. Second, if the result of the work has

fulfilled or exceeded what has been expected, of example if

someone feels that he or she has worked hard, but he or she

receives lower incentive, perhaps the person will react

negatively with the co-workers, superior and also his or her job.

On the contrary, if he or she is treated and paid well, his or

her character will be positive. Third, this third factors sees

the working satisfaction in many attitudes related with the job.

In this case, there are 5 dimensions of working characteristic,

which later, can affect behavior, they are:

1. His own job, meaning, whether the job interesting or not.

Also, there is an opportunity to learn, tempting enough.

2. Wage, in the form of the received amount, whether equals with

the others in the organization or not.

3. Promotion opportunity, by getting higher positions in the

organization.

4. Supervision, giving clue and technical assistance.

5. Co-workers, with co-workers, who technically adequate enough

and support cooperation.

The five working characteristics determine the working

satisfaction, but related to the thing related to the

participation is the fourth (supervision). In the case of

supervision, there are 2 dimensions of leadership. First, the

character of employee-centeredness; the amount of working

satisfaction depends on how far the superior pay attention to the

employees’ welfare. Second, participative leadership, that is

manager allows his subordinates to participate in the decision

making, related to their job. The second one is generally will

increase the working satisfaction. Although like that, other

characteristics are also important enough factors in the working

satisfaction. Similarly in the job itself, which can be seen in

the working group (friendly, helpful), working condition (clean,

interesting, not hot, not noisy).

Several researches results (French, Kay & Meyer, 1986;

Chenhall, 1986; Frucot & Shearon, 1991) show that participation

in budget setting has positive impact on the working

satisfaction. Based on the results of the research, thus, this

research uses working satisfaction as the dependent variable.

C. Performance

The proxy for the performance is rather difficult. As whole,

perhaps there is company’s profit or the achievement of budget

can be used as the measurement. But, it might be difficult for

the individual, although there is a measurement of wage

improvement (Frucot and Shearon, 1991). In the division in which

there is no revenue and only burden/expenditure, it is difficult

to hold a measurement of performance, has the expenditure under

the budget, which has been determined, showed good performance?

Not always, perhaps, with the stress on the expenditure will

emerge efficiency.

Sometimes, it is really difficult to determine that certain

expenditure will reach certain objective or benefit. It is

similar with part of research and development. Usually, the

performance is difficult to measure because the result will be

obtained several yeas later after the burden is released. It also

exists in the education, whether the burden released for the

media, such as a pretty expensive video can be measured with the

result of the related section. The result might be far from the

spent burden. In the non-profit organization, the measurement of

performance cannot be determined by using the same tools as in

common companies (profit oriented). It is not clear and not

logical. So, in this kind of organization, the balance point is

used as the measurement of reached performance (Anthony et al.,

1984: 644).

The measurement system of public-sector performance is a

system, which aimed to help the public managers to assess the

achievement of a strategy through financial and non-financial

measurement tools. This measurement is aimed to meet three

objectives. First, it is meant to be able to help to repair the

government performance. The measurement of performance is meant

to be able to help government to focus on the goal and objective

of working unit program. Finally, it will increase the efficiency

and the effectiveness of public-sector organization in serving

the public. Second, public-sector measurement is meant to

allocate sources and decision making. Third, the measurement of

public-sector is meant to implement public responsibility and

repair institutional communication. The performance of public

sector is multidimensional, so, there is no single indicator,

which can be used to show the performance comprehensively.

Different with private sector, because the character of output

resulted by public sector is more intangible output. Therefore,

the only financial measurement is not enough for public sector.

D. Job Relevance Information

Job relevance information is information, which can help

managers to choose the best action through better-informed effort

(Kren, 1992). For example, the information about inflation,

economic condition, and company’s financial condition. Kren

(1992) carried out a research entitled “Budgetary Participation

and Managerial Performance: The Impact of Information and

Environmental Volatility.” This research was carried out by

including volatility environmental condition. This is the change

or the variety of situation faced by an organization. The result

of the research showed that, as a whole (with the number of

sample of 80), JRI acted as intervening, which explains the

relation between the participation in budget setting on the

managerial performance with correlation of 0.214 at the

significance level of one percent (performance<0.001).

The result of Indriani (1993) research said that the job

relevance information gives better knowledge about the

alternative decisions and actions needed to reach the objectives

(Locke et al., 1967). The job relevance information is an

important variable in budgeting system because the information

can give a more precise prediction about the environment.

Therefore, it becomes the choice of opportunity to be effective

(Muslimah, 1998).

Based on the description above and previous researches, it

can be formulates a hypothesis as follow:

H1: The participation in budget setting affects positively onthe working satisfaction.

H2: The relation between the participation in budget settingand the performance will be explained by indirect impact inwhich the higher the participation, the more the usage ofjob relevance information, and job relevance informationrelates positively with the performance.

RESEARCH METHOD

Sample and Data Collecting Technique

The samples of this research are the staff and operator

elements participating in budgeting in 4 regencies, Sleman,

Bantul, Kulon Progo, Gunung Kidul, and and county, Yogyakarta.

Those samples comprise of Official element, Mayor, Financial

Section in Mayor’s office, and budgeting staff. The data

collection was carried out by using questionnaire. The number of

distributed questionnaire is of 300 questionnaires. The

researcher expects will receive returned questionnaires of 150.

To make it more effective, the distribution of the questionnaires

to the respondents was carried out by delivering the

questionnaires by the researcher. The reason is to make the

return level becomes high and the researcher can give direct

explanation about the fulfillment of the questionnaire. The step

taken to control the distributed questionnaires was by calling

the respondent via telephone to make sure that the questionnaire

has been fulfilled.

Variable Identification and Measurement

The data in this research comprises of primary data,

collected though questionnaire. And, the secondary data was

collected from the literature research, which is previous

research on the participation in budget setting and the

theoretical bases appropriate with the topic of this research.

The research is planned as an empirical research to test the

proposed hypothesis. The variables, wanted to examine are budget

participation, job relevance information, performance and

satisfaction. The instrument in this research was using the

instruments, which have been made by the researcher before and

have been modified.

Participation Variable and Performance Measurement

The measurement of participation and performance is carried

out by using the instrument from Kenis (1979), that has been

developed by Mardiasmo (2001) and has been suited with budgeting

system in Indonesia. This instrument will use Likert 5 scale,

starting from the statement of ‘extremely disagree’ until

extremely agree’.

The Measurement of Satisfaction Variable

For the working satisfaction, it is used the instrument from

the previous research, that is Weiss et al., (1967) in Minnesota

Satisfaction Questionnaire. The scale comprises of one until five

scales. Scale one says ‘extremely disagree’ and scale five says

‘extremely agree’. This instrument uses 20 questions, which was

the simple form of 100 existing questions. This instrument is

chosen because its validity has been tested, having enough

internal consistency.

Job Relevance Information Variable Measurement

Job relevance information is information to ease the

decision facilitating related with the job or position. This

variable is used to obtain the respondents’ perception on the

information availability for the decisions related with their

job. The measurement of this variable uses questionnaires

developed by O’Reilly (1980), which then used by Kren (1992) and

Muslimah (1998). This instrument uses Likert scale, starting from

one (extremely disagree) until five (extremely agree).

Analysis Instrument

Statistical analysis used to test the model and hypothesis

is Structural Equation Model (SEM) with using version 4.01 AMOS

program. This test is carried out in two parts. First, testing

whether the proposed model has been appropriate or not, and

second, testing the proposed hypothesis. In the test, there are

several steps to be passed:

1. Developing path diagram

2. Evaluating the SEM assumptions

3. Evaluating the criteria of Goodness of fit of the research

model

The second part of the testing step is the test of each

hypothesis proposed in this research model. This test is

identical with trust-test in the multiple regression, using

stepwise method. To determine whether the hypothesis is accepted

or rejected, it can be seen from the value of Critical Ratio (CR)

at the Regression Weight.

DATA ANALYSIS AND DISCUSSION

Respondents

The number of returned questionnaires is of 159 (53%)

from the total amount of 300 questionnaires. From the returned

questionnaires, 10 questionnaires are not fulfilled completely

so, they cannot be processed further. After the completion

analysis is carried out, the remain questionnaires are of 149.

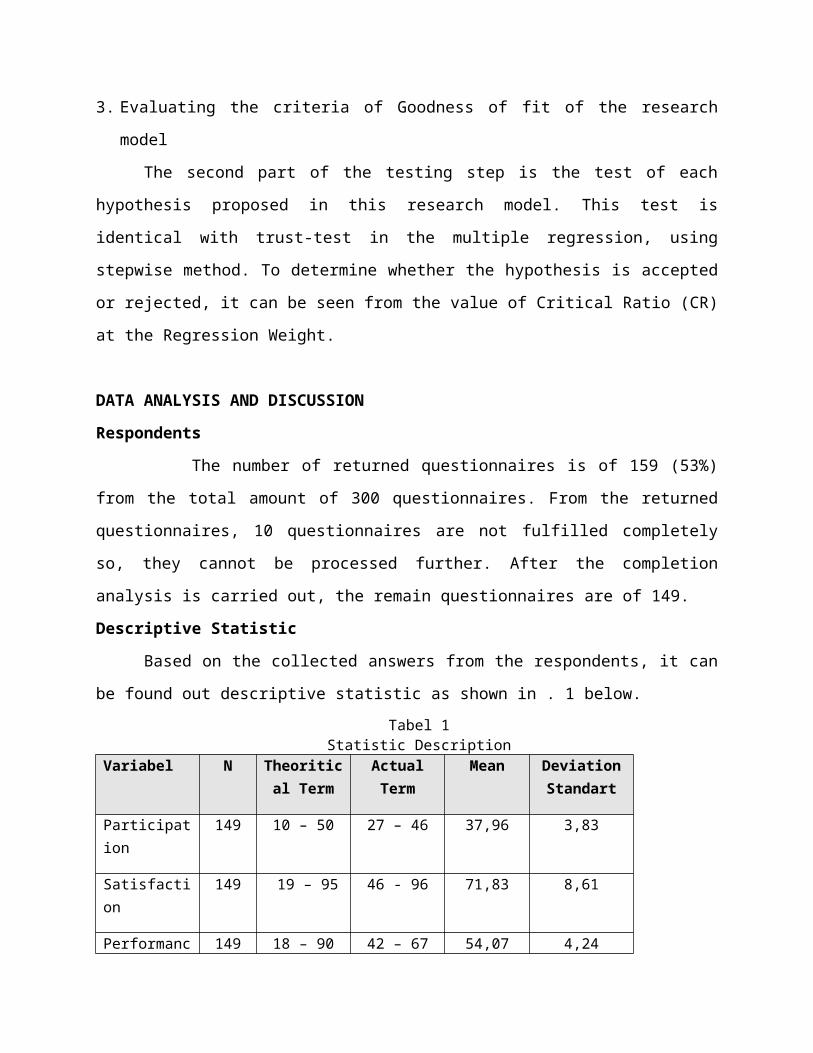

Descriptive Statistic

Based on the collected answers from the respondents, it can

be found out descriptive statistic as shown in . 1 below. Tabel 1

Statistic DescriptionVariabel N Theoritic

al TermActualTerm

Mean DeviationStandart

Participation

149 10 – 50 27 – 46 37,96 3,83

Satisfaction

149 19 – 95 46 - 96 71,83 8,61

Performanc 149 18 – 90 42 – 67 54,07 4,24

e

JRI 149 8 – 40 21 – 35 30,11 3,53

Instrument Test

Instrument test is carried out by factorizing-analyzed the

questions items using SPSS software. To see the reliability f

the instrument, therefore, it will be measured Cronbach Alpha of

each instrument. The instruments stated as reliable if the

instrument has bigger Cronbach alpha value than 0.6 (Nunnally

1978, as quoted by Flory et al., 1992). While, for validity

testing, it is carried out to find out how good an instrument in

measuring the concept, which has to be measured. And, to find out

whether the questions in the questionnaire are valid or not, it

is used factor analysis. The method used is varimax rotation, and

each variable is hoped to have factor loading more than 0.4

(Riyanto, 1997). Besides, the value of Kaiser’s MSA, which is

bigger than 0.5, can be said appropriate for factor analysis and

indicating construct validity from each instrument (Kaiser and

Rice, 1974). The result of reliability testing and instrument

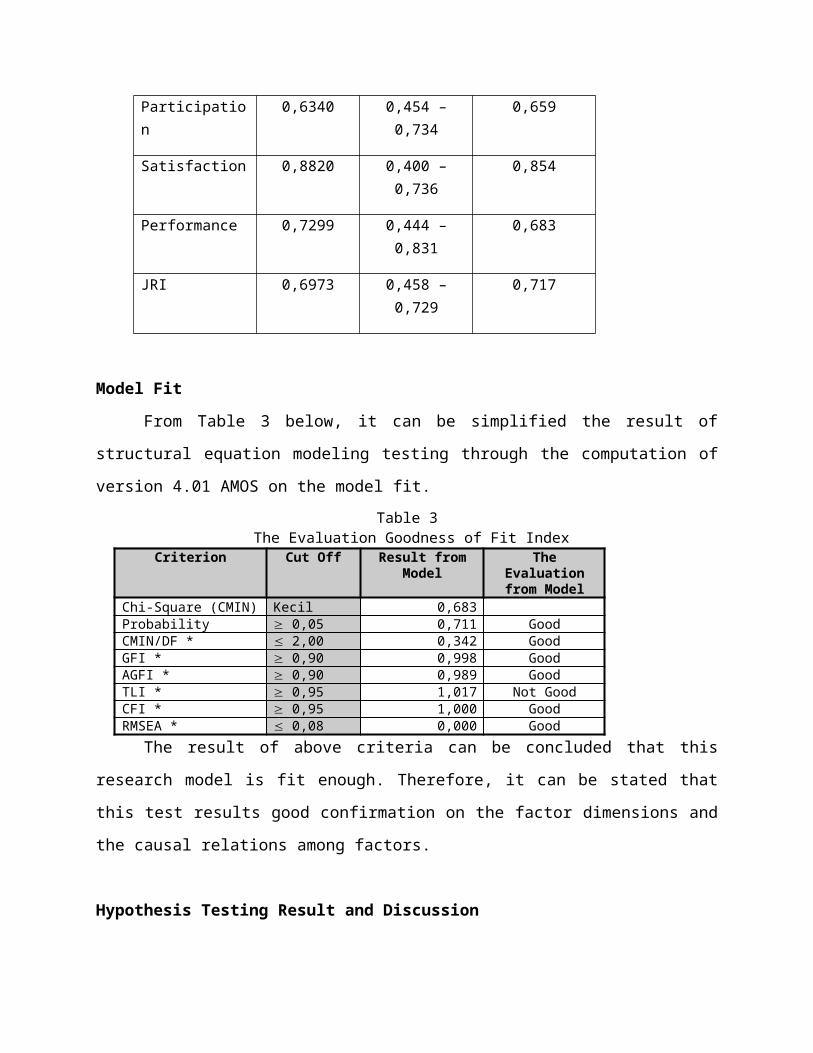

validity can be seen in Table. 2.Table. 2

The Summary of Realiability and Validity

Variable Cronbachalpha

Factor loading Kaiser’s MSA

Participation

0,6340 0,454 –0,734

0,659

Satisfaction 0,8820 0,400 –0,736

0,854

Performance 0,7299 0,444 –0,831

0,683

JRI 0,6973 0,458 –0,729

0,717

Model Fit

From Table 3 below, it can be simplified the result of

structural equation modeling testing through the computation of

version 4.01 AMOS on the model fit.Table 3

The Evaluation Goodness of Fit IndexCriterion Cut Off Result from

ModelThe

Evaluationfrom Model

Chi-Square (CMIN) Kecil 0,683Probability 0,05 0,711 GoodCMIN/DF * 2,00 0,342 GoodGFI * 0,90 0,998 GoodAGFI * 0,90 0,989 GoodTLI * 0,95 1,017 Not GoodCFI * 0,95 1,000 GoodRMSEA * 0,08 0,000 Good

The result of above criteria can be concluded that this

research model is fit enough. Therefore, it can be stated that

this test results good confirmation on the factor dimensions and

the causal relations among factors.

Hypothesis Testing Result and Discussion

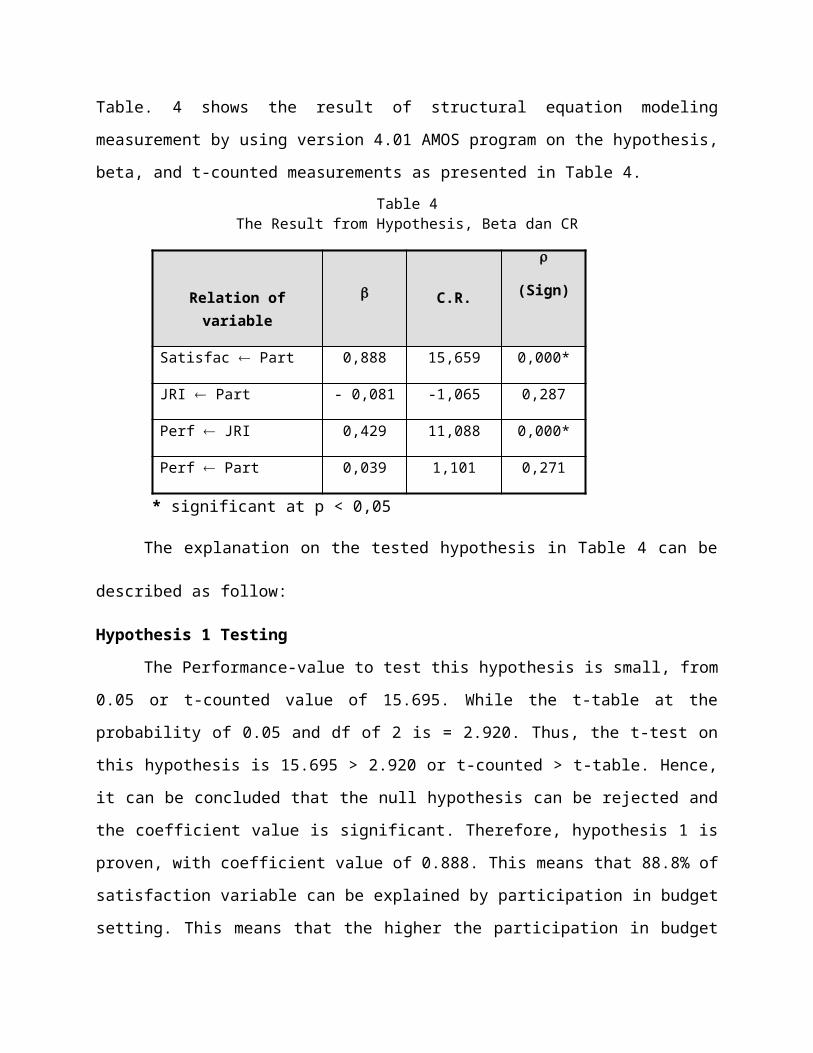

Table. 4 shows the result of structural equation modeling

measurement by using version 4.01 AMOS program on the hypothesis,

beta, and t-counted measurements as presented in Table 4.Table 4

The Result from Hypothesis, Beta dan CR

Relation ofvariable

C.R.

(Sign)

Satisfac Part 0,888 15,659 0,000*

JRI Part - 0,081 -1,065 0,287

Perf JRI 0,429 11,088 0,000*

Perf Part 0,039 1,101 0,271

* significant at p < 0,05

The explanation on the tested hypothesis in Table 4 can be

described as follow:

Hypothesis 1 Testing

The Performance-value to test this hypothesis is small, from

0.05 or t-counted value of 15.695. While the t-table at the

probability of 0.05 and df of 2 is = 2.920. Thus, the t-test on

this hypothesis is 15.695 > 2.920 or t-counted > t-table. Hence,

it can be concluded that the null hypothesis can be rejected and

the coefficient value is significant. Therefore, hypothesis 1 is

proven, with coefficient value of 0.888. This means that 88.8% of

satisfaction variable can be explained by participation in budget

setting. This means that the higher the participation in budget

setting the higher the working satisfaction. The result of this

research supports the Indrianto (1993) and Indriani (1993)

researches. Other research, which conveys that participation in

the participation in budget setting, affects the working

satisfaction. This is conveyed by French, Kay & Meyer (1986);

Chenhall (1986); and Frucot & Shearon (1991).

Hypothesis 2 Testing

The aim of this hypothesis is to see whether the variable of

job relevance information functions as intervening variable in

the relation between the participation in budget setting and

performance. The Performance-value to test the relation between

participation and the performance of this hypothesis is big from

0.05 or t-counted value of 1.101. While, t-table at the

probability of 0.05 and df of 2 is of 2.920 (t-counted < t-

table). Thus, the result is not significant. Similarly in the

relation between participation and the J –1.065 < 2.920. While,

the relation of job relevance information with performance, its

Performance-value is small 0.05 (0.000) or t-counted > t-table

(11.088< 2.920). It can be found out that the job relevance

information significantly affects on the performance. As a

result, based on the test result, it can be found out that the

participation in budget setting is not significantly affecting

the performance. It is similar with the participation in budget

setting, which is also not significantly affecting the job

relevance information.

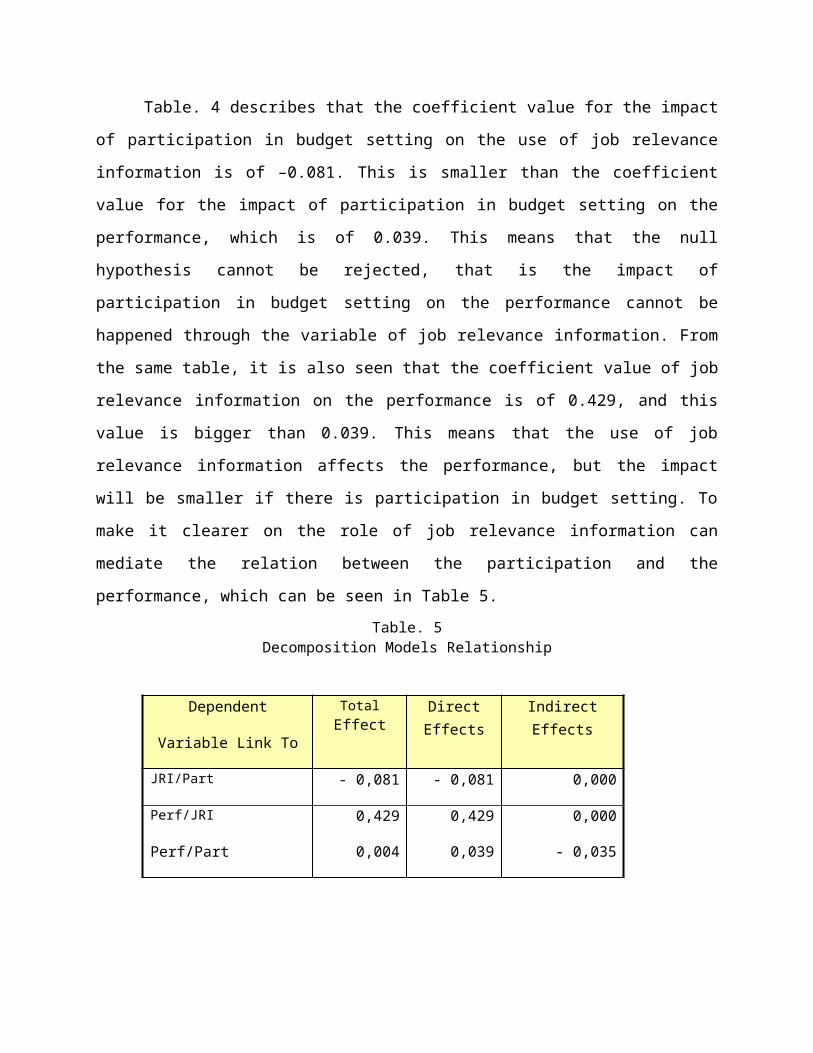

Table. 4 describes that the coefficient value for the impact

of participation in budget setting on the use of job relevance

information is of –0.081. This is smaller than the coefficient

value for the impact of participation in budget setting on the

performance, which is of 0.039. This means that the null

hypothesis cannot be rejected, that is the impact of

participation in budget setting on the performance cannot be

happened through the variable of job relevance information. From

the same table, it is also seen that the coefficient value of job

relevance information on the performance is of 0.429, and this

value is bigger than 0.039. This means that the use of job

relevance information affects the performance, but the impact

will be smaller if there is participation in budget setting. To

make it clearer on the role of job relevance information can

mediate the relation between the participation and the

performance, which can be seen in Table 5.Table. 5

Decomposition Models Relationship

Dependent

Variable Link To

TotalEffect

DirectEffects

IndirectEffects

JRI/Part - 0,081 - 0,081 0,000

Perf/JRI 0,429 0,429 0,000

Perf/Part 0,004 0,039 - 0,035

From the above Table, it can be seen that the direct

relation between the participation and the performance (0.039) is

bigger compared with the relation through job relevance

information (-0.035). This means that with the existence of job

relevance information as the intervening variable, it will reduce

the relation between the participation and the performance. The

result of this research is different with the result of Kren

(1992) research, in which the result of his research said that

the job relevance information could mediate the relation between

the budget participation and the performance.

Conclusion

Based on the result of the data analysis and the hypothesis

testing, thee are several problems proposed in this research will

be answered. The followings are the conclusions that become the

gist of the analysis and the hypothesis testing.

1. Empirically, hypothesis 1 is proven. This means that this

research can achieve to prove that the participation in the

budget setting affects the working satisfaction. The result of

data processing shows that the increase participation in

budget setting will increase working satisfaction, although

there are other factors affecting the relation of the two

variables. The result of this research supports the result of

Indriantoro (1993) research, which obtained the high level of

participation in budget setting supports the working

satisfaction in Indonesia. Generally, the previous researches,

finding positive relation between the participation in budget

setting and the working satisfaction, were carried out by

French Kay and Mayer (1996), Milani (1975) and Cherington and

Cherington (1973).

2. Empirically, hypothesis 2 is not proven. This means that the

relation between the participation in budget setting and the

performance cannot be mediated by job relevance information

variable. The result of data processing shows that the

participation is not affecting the use of job relevance

information. The higher participation, the lower the use of

job relevance information. The use of job relevance

information affects the performance. This means that the more

the use of job relevance information, the better the

performance is. This means that the result of this result

cannot reject the null hypothesis, that is the job relevance

information cannot mediate the relation between the

participation in budget setting with performance.

The result of this research is different with the result of

research carried out by Kren (1992), that concluded that the

JRI could act as the intervening variable among the variables

of participation and performance. This difference might be

because the respondents are the managers in manufacture

companies.

Implication and Limitation

It is better for this research to be widened, either from

the scope of population district of the variables, which want to

be tested. It is needed to be considered because the budget

participation is a part of the management participation, which is

very meaningful in profit organization or non-profit organization

in increasing working effectiveness and efficiency. Because JRI

cannot act as an intervening variable, then, JRI cannot be used

as the base of consideration in making decision. This thing is

likely caused by the difference in the observed organizational

structure, working environment, and the form of organization. The

researcher suggests for the further research to try to use other

variables that can be used as intervening variables, as

decentralization, motivation, and authority. Frocot and Shearon

(1991) categorized factors affecting the relation of

participation in budget setting that can affect the relation of

participation in the participation in budget setting with

performance. The working satisfaction is macro variable like

organizational structure and technology, working ethic, and

cultural difference. Besides, the micro-level variable, which

affects the relation, is the leadership style and individual

personality.

Although this research has been carried out well, but the

researcher is aware of the existence of several limitation that

cannot be avoided. The followings are the existing limitations:

1. The respondents in this research are only limited in the

governmental officers existing in Daerah Istimewa Yogyakarta.

This research maybe will show a difference result of it is

implemented in District Government in other districts.

2. The data resulted from the use of instrument, which based on

the perception of respondents’ answers, will emerge a problem

if the respondents perception is different with the real

condition. And, the conclusion drawn is only based on the data

collected through the use of written instrument.

3. The use of AMOS analysis is aimed to test the carried out

research. From the result of data processing, it can be seen

that the research model has met several criteria of goodness

of fit. So, the model can be said as a fit model. But, because

in this research, the researcher does not compare the model

with comparison model, hence, this research model cannot be

said as the most optimal model because there might be better

other models.

References

Arbuckle, J.L. (1997). Amos User’s Guide, Version 3.6: Chicago:SmallWaters Corporation.

Argyris, C. (1955). Organizational Leadership and ParticipationManagement. The Journal of Business. Vol. XXVII (January): 1-7.

Brownell, P. (1982a). Participation in the Budgeting Process:When It Works and When It Doesn’t. Journal of Accounting Literature.741 (Spring):124-153.

Brownell, P. (1982b). The Role of Accounting Data in PerformanceEvaluation, Budgetary Participation, and OrganizationalEffectiveness. Journal Accounting Research. 20 (Spring): 12-27.

Brownell, P., and M. McInnes. (1986). Budgetary Participation,Motivation, and Managerial Performance. The Accounting Rewiew.61 (October), 587-600.

Bryan and Locke. (1967). Goal Setting as a Means of IncreasingMotivation and Managerial Performance. Journal of AppliedPsychology. 52 (Juni): 274-277.

Chenhall, R.H., and D.Morris. (1986). The Impact of Structur,Enviromental and Interdependence on the Perceived Usefulnessof Management Accounting Systems. The Accounting Review(January): 16-35.

Chenhall, R.H., and P.Brownell. (1988). The Effect of

Participative Budgeting on Job Satisfaction and Performance:Role Ambiguity as an Intervening Variabel. Accounting,Organization and Society. Vol 13: 225-233.

Due, John F.(1975). Keuangan Negara. Jakarta. Yayasan PenerbitUniversitas Indonesia.

Ferdinand, Augusty (2000). Structural Equation Modelling dalam PenelitianManajemen. Badan Penerbit Universitas Dipenogoro.

Flory, S.M., T.J. Philips, Jr., R.E. Reidenbach, and Dp. Robin.

(1992). A Multidimensional Analysis of Selected EthicalIssues in Accounting. The Accounting Review Vol. 67, No.2: 284-302.

Frucot, Veronique and Shearon, Winston T. (1991). BudgetaryParticipation, Locus of Control and Mexican ManagerialPerformance and Job Satisfaction. The Accounting Review(January): 80-89.

Henley, D., Likierman, A., Perrin, J., Evans, M., Lapsley, I.,and Whiteoak, J. (1992). Public Sector Accounting and Financial Control,4th., London: Chapman & Hall.

Indriani. (1993). Pengaruh Partisipasi Terhadap Kinerja dan Kepuasan Kerja:

Studi pada Karyawan Pemerintah Daerah Tingkat I Daerah Istimewa Aceh. TesisS-2.

Indriantoro, N. (1993). The Effect of Participative Budgeting on JobPerformance and Job Satisfaction with Locus of Control and Cultural Dimentionsas Moderating Variables. Dissertation.

Kaiser, H.F. and J. Rice. (1974). Educational and PsychologicalMeasurement, Vol. 34, No.1.

Kren, L. (1992). Budgetary Participation and ManagerialPerformance: The Impact of Information and EnvironmentalVolatility. The Accounting Review (July): 511-526.

Lapsley, I. (1988). Research in Public Sector Accounting: AnAppraisal. Accounting, Auditing and Accountability. Vol 1. No. 1: 21-33.

Leung, M. (1990). The Effect of Managerial Role on Relationship betweenBudgetary Participation and Job Satisfaction. Tesis Monash University,Australia.

Mardiasmo. (2001). Budgetary Slack Resulted from the Effects ofLocal Government Financial Dependency on Central andProvincial Government in Planning and Preparing LocalGovernment Budget: The Case of Indonesia. Jurnal Riset Akuntansi,Manajemen, Ekonomi. Vol 1 No.1: 33-54.

Mardiasmo. (2002). Akuntansi Sektor Publik. Yogyakarta: Penerbit Andi.

Milani K. (1975). The Relationship of Participation in Budgeting-Setting to Industrial Supervisor Performance and Attitude: AField Study. The Accounting Review (April): 274-284.

Muslimah, S. (1998). Dampak Gaya Kepemimpinan, KetidakpastianLingkungan dan Informasi Job Relevan terhadap PerceivedUsefulness Sistem Penganggaran. Jurnal Riset Akuntansi Indonesia Vol.I. No.2 (Juli), 219-238.

Nunnally, J. (1978). Psychometric Methods. New York: Mc Graw-Hill.

Rosidi. (2000). Partisipasi dalam Penganggaran dan PrestasiManajer: Pengaruh Komitmen Organisasi dan Informasi JobRelevant. Jurnal Ekonomi dan Manajemen. Vol 1. No.1. (Juni): 1-15.

Weiss, D.J., R.V. Davis. G.W. England and L.H.Lofguist. (1967).Manual For Minesssota Satisfaction Questionnaire. Minessota Studies inVocational Rehabilitation.

Related Documents