Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

TAMARA BACKOVIĆ VULIĆ - BIBLIOGRAFIJA Rad objavljen u renomiranom međunarodnom časopisu:

1. Vesna Karadžić and Tamara Backović, “The Montenegrin Capital Market: Calendar Anomalies”, Economic Annals, Volume LVI, No. 191, 2011., ISSN: 0013 – 3264 »Časopis “Economic Annals” je akademski časopis koji se publikuje kvartalno. Izdavač je Ekonomski fakultet u Beogradu, Univerzitet u Beogradu. Radovi se objavljuju na engleskom jeziku. Časopis je rangiran u bazi podataka Elsevier Scopus® od strane SCImago Journal & Country Rank rangom Q3.

2. Tamara Backović Vulić, “Characteristics of Montenegrin capital market in terms of

efficiency”, odobren za štampanje u narednom broju časopisa Journal of Social and Business Studies, Volume 1, Issue 2, 2014. , ISSN print: 2303-6044, ISSN online: 2303-6176

»Časopis “Journal of Social and Business Studies” je međunarodni časopis koji se publikuje dvomjesečno. Izdavač je Social and Business Development Cenar u Sarajevu, neprofitna organizacija čiji je cilj poslovanja unapređenje obrazovanja, društva, kulture, poslovnog i tehnološkog razvoja kroz organizovanje seminara i konferencija, kao i objavljivanjem rezultata naučnih istraživanja. Radovi se objavljuju na engleskom jeziku. Časopis je indeksiran u sledećim međunarodnim bazama: Open Academic Journals Index (oaji.net), Google Scholar (scholar.google.com) i SHERPA/RoMEO (www.sherpa.ac.uk).

Ostali objavljeni radovi:

3. Tamara Backović, “Analiza vremenskih serija na primeru berzanskih indeksa u Crnoj Gori”, Preduzetnička ekonomija, Volume XIV, 2006., ISSN 1451-6659

4. Tamara Backović, “Proces donošenja odluke – intuicija ili primena formalnog modela odlučivanja”, Preduzetnička ekonomija, Volume IX, 2005., ISSN 1451-6659

5. Tamara Backović, “Uticaj preduzetništva na ekonomski rast i razvoj – teorijsko-empirijski pristup”, Entrepreneurial economy, Volume VII, 2004., ISSN 1451-6659

Radovi prezentovani na međunarodnim konferencijama:

6. Tamara Backović Vulić, “Testing the Efficient Market Hypothesis and its Citics - Application on the Montenegrin Stock Exchange”, IX Annual Conference “Global Imbalances, Financial Institutions, and Reforms in the Post-Crisis Era” organized by European Economics and Finance Society in Athens, Greece, 2010. published on website address: http://www.eefs.eu/conf/Athens/Papers/550.pdf

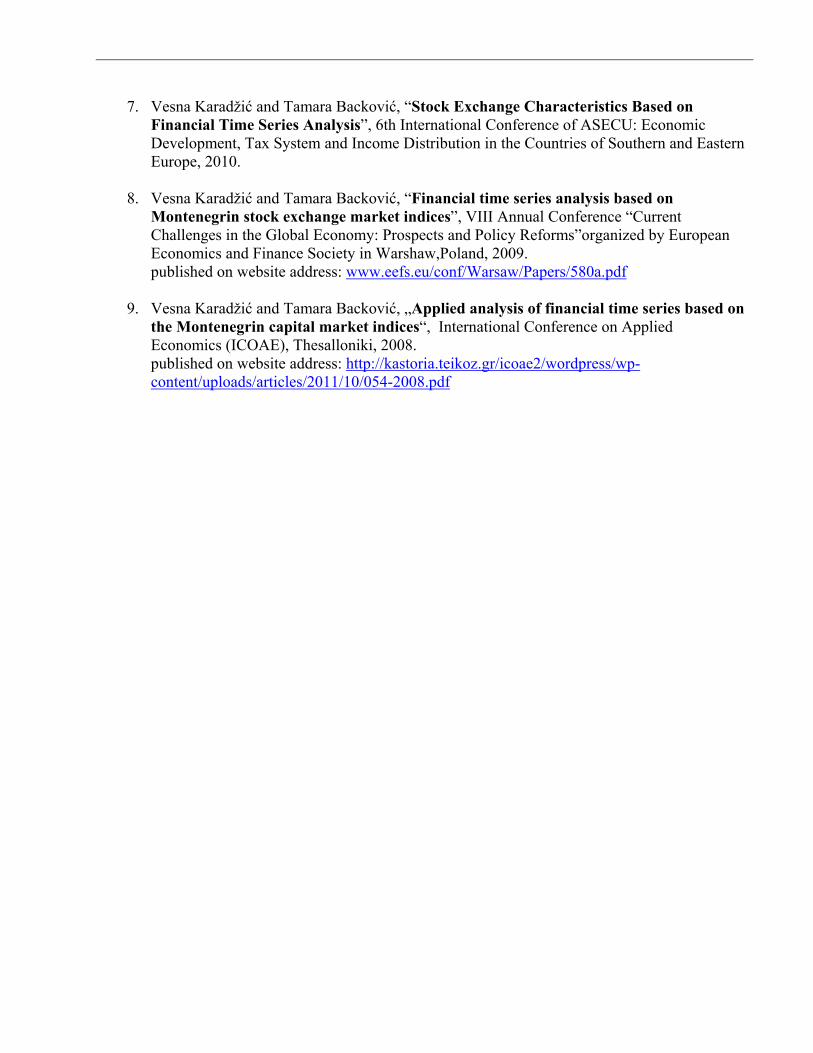

7. Vesna Karadžić and Tamara Backović, “Stock Exchange Characteristics Based on Financial Time Series Analysis”, 6th International Conference of ASECU: Economic Development, Tax System and Income Distribution in the Countries of Southern and Eastern Europe, 2010.

8. Vesna Karadžić and Tamara Backović, “Financial time series analysis based on Montenegrin stock exchange market indices”, VIII Annual Conference “Current Challenges in the Global Economy: Prospects and Policy Reforms”organized by European Economics and Finance Society in Warshaw,Poland, 2009. published on website address: www.eefs.eu/conf/Warsaw/Papers/580a.pdf

9. Vesna Karadžić and Tamara Backović, „Applied analysis of financial time series based on

the Montenegrin capital market indices“, International Conference on Applied Economics (ICOAE), Thesalloniki, 2008. published on website address: http://kastoria.teikoz.gr/icoae2/wordpress/wp-content/uploads/articles/2011/10/054-2008.pdf

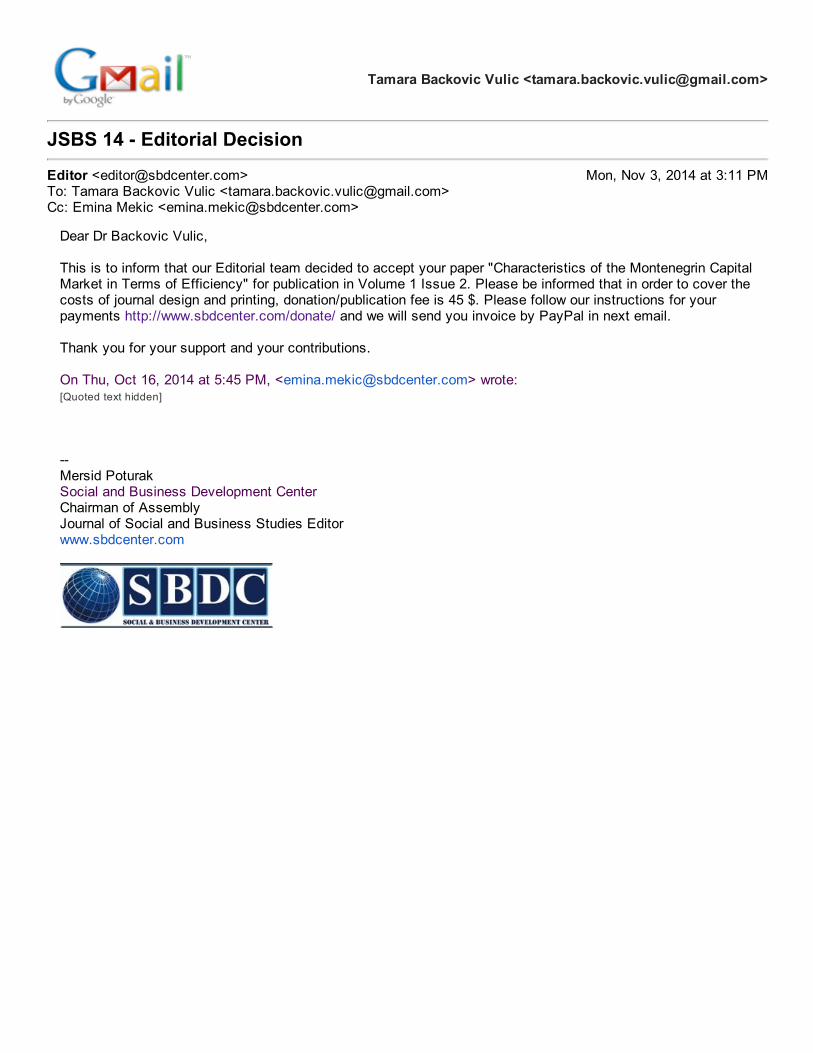

Tamara Backovic Vulic <[email protected]>

JSBS 14 - Editorial Decision

Editor <[email protected]> Mon, Nov 3, 2014 at 3:11 PMTo: Tamara Backovic Vulic <[email protected]>Cc: Emina Mekic <[email protected]>

Dear Dr Backovic Vulic,

This is to inform that our Editorial team decided to accept your paper "Characteristics of the Montenegrin CapitalMarket in Terms of Efficiency" for publication in Volume 1 Issue 2. Please be informed that in order to cover thecosts of journal design and printing, donation/publication fee is 45 $. Please follow our instructions for yourpayments http://www.sbdcenter.com/donate/ and we will send you invoice by PayPal in next email.

Thank you for your support and your contributions.

On Thu, Oct 16, 2014 at 5:45 PM, <[email protected]> wrote:[Quoted text hidden]

-- Mersid PoturakSocial and Business Development Center Chairman of AssemblyJournal of Social and Business Studies Editorwww.sbdcenter.com

ISSN: 2303-6044

Vol. 1 No. 1

JOURNAL OF SOCIAL

AND BUSINESS STUDIES

September, 2014

This page is intentionally left blank.

ISSN: 2303-6044

Vol. 1 No. 1

JOURNAL OF SOCIAL

AND BUSINESS STUDIES

September, 2014

PUBLISHER

Social and Business Development Center – SBDC

Adress: Ramiza Salčina 93, 71 000 Sarajevo

Bosnia and Herzegovina

Editor Mersid Poturak

Editorial Assistant Amela Poturak

ISSN 2303-6044

Phone: +38761 498 596

E-mail: [email protected]

Webpage http://www.sbdcenter.com/jsbs/

Frequency six issues per year

Current Volume 1/2014

Indexing and abstracting OAJI - Open Academic Journals Index

STATEMENT OF PURPOSE

Journal of Social and Business Studies (JSBS) is an international, interdisciplinary peer-reviewed journal,

published by Social and Business Development Center (SBDC), located in Bosnia and Herzegovina. This

journal aims to develop scientific knowledge that links current practice and theory in field of social and

business studies. The journal publishes refereed articles, research notes, case studies, book reviews or any other

type of research that might contribute to society and business in the areas that include, and are related to the

following fields: Business studies; Accounting, management, marketing, entrepreneurship; Business ethics,

business law, law and economics; Operations research, statistics, econometrics, experimental economics;

Business and economics education; Microeconomics: theory and applications; Government regulation,

industrial organization, game theory; International economics; International Business; Macroeconomics,

growth, government finance, monetary economics finance, investments; Sociology; Psychology; Anthropology;

Other – any business or social studies discipline. Submitted manuscripts should be in alignment with journal

guidelines and should not be under consideration elsewhere.

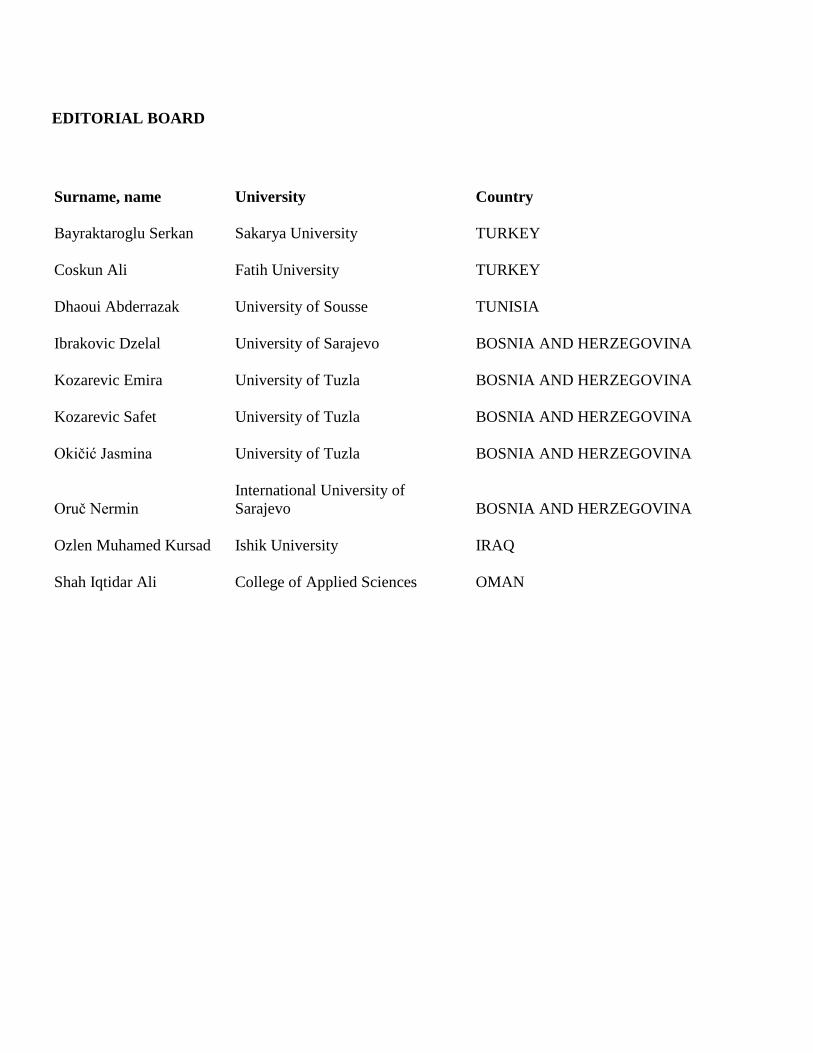

EDITORIAL BOARD

Surname, name

University

Country

Bayraktaroglu Serkan

Sakarya University

TURKEY

Coskun Ali

Fatih University

TURKEY

Dhaoui Abderrazak

University of Sousse

TUNISIA

Ibrakovic Dzelal

University of Sarajevo

BOSNIA AND HERZEGOVINA

Kozarevic Emira

University of Tuzla

BOSNIA AND HERZEGOVINA

Kozarevic Safet

University of Tuzla

BOSNIA AND HERZEGOVINA

Okičić Jasmina

University of Tuzla

BOSNIA AND HERZEGOVINA

Oruč Nermin

International University of

Sarajevo

BOSNIA AND HERZEGOVINA

Ozlen Muhamed Kursad

Ishik University

IRAQ

Shah Iqtidar Ali

College of Applied Sciences

OMAN

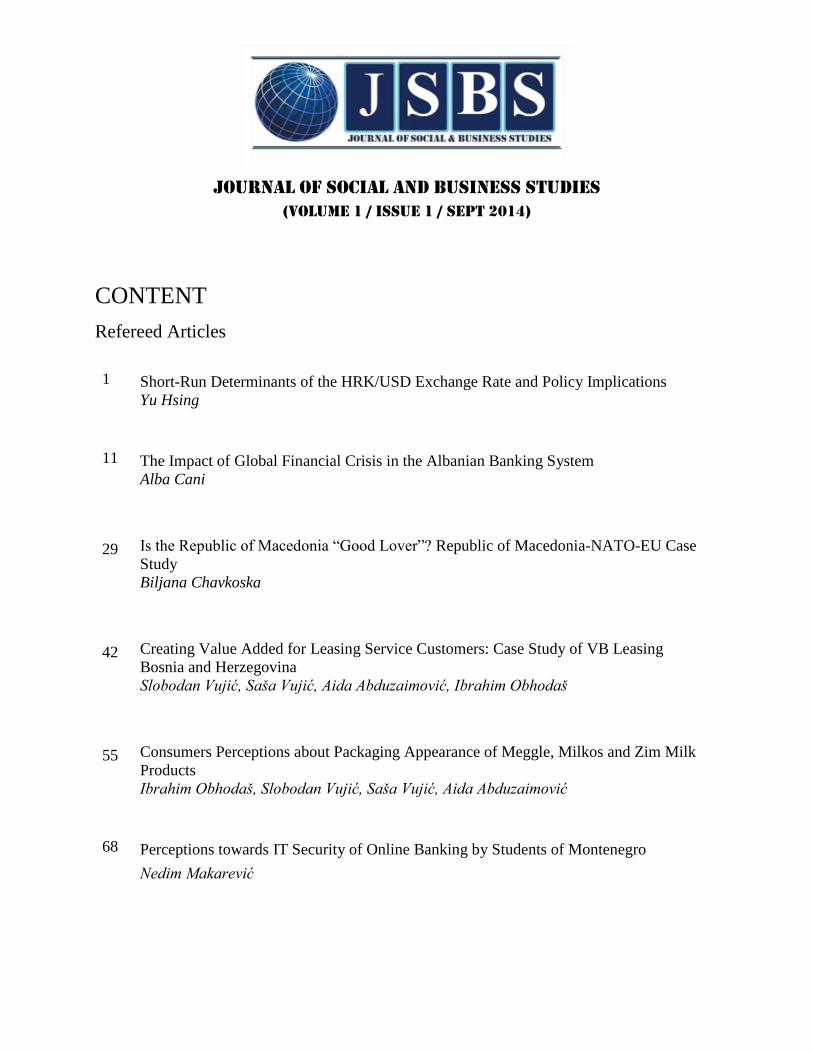

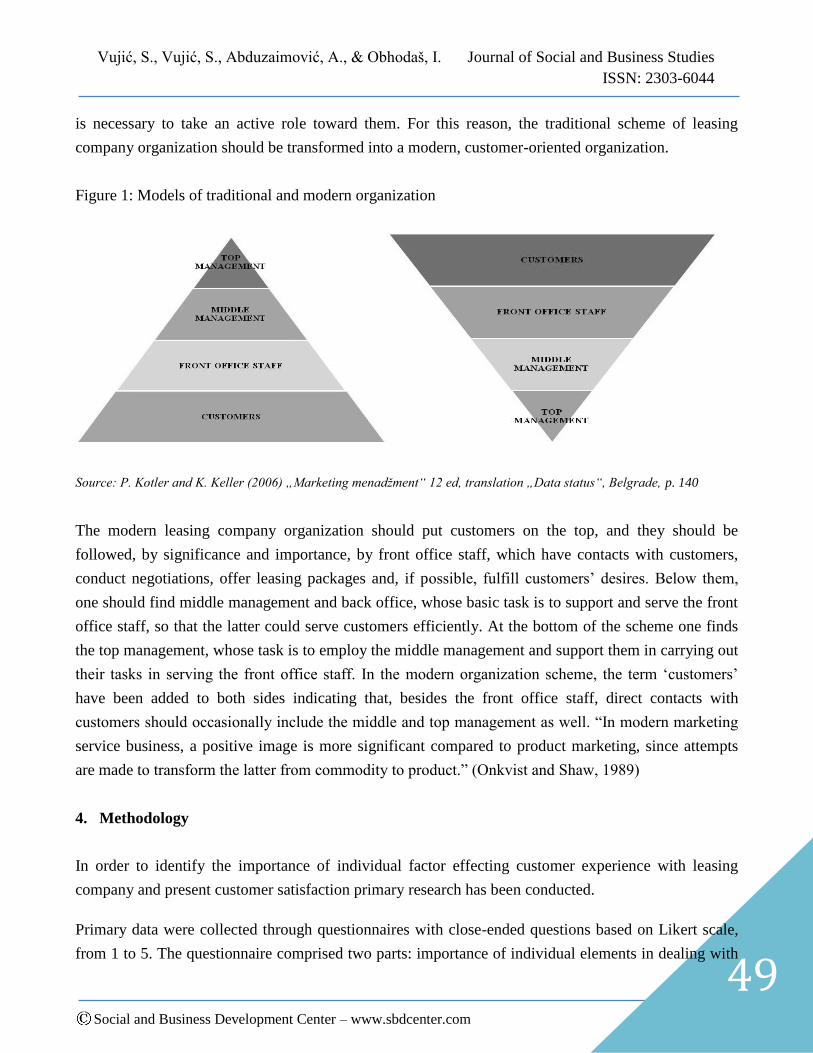

JOURNAL OF SOCIAL AND BUSINESS STUDIES

(Volume 1 / Issue 1 / Sept 2014)

CONTENT

Refereed Articles

1 Short-Run Determinants of the HRK/USD Exchange Rate and Policy Implications

Yu Hsing

11 The Impact of Global Financial Crisis in the Albanian Banking System

Alba Cani

29 Is the Republic of Macedonia “Good Lover”? Republic of Macedonia-NATO-EU Case

Study

Biljana Chavkoska

42 Creating Value Added for Leasing Service Customers: Case Study of VB Leasing

Bosnia and Herzegovina

Slobodan Vujić, Saša Vujić, Aida Abduzaimović, Ibrahim Obhodaš

55 Consumers Perceptions about Packaging Appearance of Meggle, Milkos and Zim Milk

Products

Ibrahim Obhodaš, Slobodan Vujić, Saša Vujić, Aida Abduzaimović

68 Perceptions towards IT Security of Online Banking by Students of Montenegro

Nedim Makarević

Journal of Social and Business Studies

ISSN: 2303-6044

Vol. 1(1) / pp. 1-10

Social and Business Development Center – www.sbdcenter.com

1

Short-Run Determinants of the HRK/USD Exchange Rate and Policy Implications

Yu Hsing

Southeastern Louisiana University

United States of America

Citation:

Hsing, Y. (2014). Short-Run Determinants of the HRK/USD Exchange Rate and Policy Implications. Journal of Social and

Business Studies, 1(1), 1-10

Article History

Submitted: 17 July 2014

Resubmitted: 31 July 2014

Accepted: 12 August 2014

Abstract

This paper examines short-run determinants of the Croatian kuna/U.S. dollar

(HRK/USD) exchange rate based on a simultaneous-equation model. Demand

and supply analysis is employed to examine the behavior of the HRK/USD

exchange rate. Comparative static analysis is used to determine the impact of a

change in an exogenous variable on the equilibrium exchange rate. The

EGARCH model is applied in empirical work. Major findings are that the

HRK/USD exchange rate is positively associated with the real 10-year U.S.

government bond yield, real GDP in Croatia, the real stock price in the U.S.

and expected exchange rate and is negatively influenced by real GDP in the

U.S. and the real stock price in Croatia.

Keywords: Exchange Rate Determination; Interest Rates; Output, Stock Prices;

EGARCH

JEL Classification: F31, F41

Yu Hsing Journal of Social and Business Studies

ISSN: 2303-6044

Social and Business Development Center – www.sbdcenter.com

2

1. Introduction

International trade has become more important in economic growth in Croatia. In 2013, the amount of

exports as a percent of GDP was 42.97%, and the amount of imports as a percent of GDP was 42.42%,

suggesting that Croatia had a relatively high trade openness index of 85.39%. To pursue a balanced

trade or to avoid a trade deficit, the exchange rate plays a pivotal role. Mainly due to the global

financial crisis, the Croatian kuna had depreciated 20.79% versus the U.S. dollar from 4.59398 in

2008.Q1 to 5.549 in 2013.Q4. While depreciation of the kuna would lead to more exports, it is

expected to have some negative effects such as higher costs of imports, import-led inflation,

international capital outflows, etc.

A volatile exchange rate is expected to hurt international trade and economic growth because importers

and exporters are uncertain about costs of exchange for foreign currencies and profits or losses that

trade may have. A substantially over-valued currency would be difficult to maintain as a government

needs to continue to sell foreign reserves to defend the domestic currency and may result in a potential

speculative attack. A substantially under-valued currency would help exports but may be subject to

external pressures to move it to the fundamental value.

This paper attempts to use demand and supply analysis to explain fluctuations of the HRK/USD

exchange rate in order to provide policymakers insights in conducting monetary policy and fiscal

policy to stabilize exchange rates and to pursue economic growth.

In the second section, literature will be surveyed. In the third section, the methodology will be

presented. In the fourth section, the data and empirical results will be reported and analyzed. A

conclusion will be made in the last section.

2. Literature Review

There have been several studies examining the determinants of exchange rates for Croatia or related

countries. Baharumshah and Borsic (2008) study purchasing power parity (PPP) for 13 Central and

Eastern European countries and find that PPP is valid for Croatia if either the U.S. dollar or the euro is

used. Tkalec and Vizek (2011) shows that absolute purchasing power parity holds for Croatia in the

long run, suggesting that the exchange rate is in accord with the fundamentals. They also report that

exchange rate pass-through to the domestic consumer price is not confirmed. Miteza (2012) examines

PPP for 6 Central and East European countries and finds that PPP is confirmed for four of six countries

and that the is very strong evidence of PPP for Slovakia, Poland and the Czech Republic. Kozul (2013)

Yu Hsing Journal of Social and Business Studies

ISSN: 2303-6044

Social and Business Development Center – www.sbdcenter.com

3

tests whether PPP applies to the Croatian kuna/euro exchange rate based on ADL and Engle-Granger

tests and finds that PPP does not hold for Croatia.

Funda and Lukinić (2008) indicate that the Balassa-Samuelson effect in Croatia is not confirmed and is

not expected to become an obstacle to satisfying the convergence criteria. Erjavec, Cota and Jakšić, S.

(2012) reveal that the main reason for the volatility of the Croatian kuna exchange rate comes from

demand shocks instead of supply shocks in the short run and long run. Hence, the exchange rate serves

as a shock absorber.

To the author‟s best knowledge, few of these studies have applied demand and supply analysis in

foreign exchange markets to determine the HRK/USD exchange rate in the short run. Monetary models

of exchange rates are based on the validity of purchasing power parity in the long run. In addition to

interest rates or stock prices, exchange rates may be affected by other variables. This paper attempts to

examine the HRK/USD exchange rate based on a simultaneous-equation model. The demand for and

the supply of the U.S. dollar versus the Croatian kuna are considered simultaneously in determining the

equilibrium HRK/USD exchange rate. A study of the determinants of the HRK/U.S. dollar exchange

rate would provide policymakers with more insights into the behavior of the kuna and other currencies.

3. Methodology

We can express the demand for and supply of the U.S. dollar versus the Croatian kuna in the foreign

exchange market as:

),,,,( eUSUSHRd ERYAUSD (1)

− + + + +

),,,( HRHRUSs ERYBUSD (2)

+ + + +

where

USDd = demand for the U.S. dollar,

USDs = supply of the U.S. dollar,

ε = the HRK/USD (Croatian kuna/U.S. dollar) exchange rate,

YHR

= real GDP or income in Croatia,

RUS

= the real interest rate in the U.S.,

EUS

= the real equity or stock price in the U.S.,

εe = the expected HRK/USD exchange rate,

YUS

= real GDP or income in the U.S.,

Yu Hsing Journal of Social and Business Studies

ISSN: 2303-6044

Social and Business Development Center – www.sbdcenter.com

4

RHR

= the real interest rate in Croatia,

EHR

= the real equity or stock price in Croatia.

We expect that the demand for the U.S. dollar has a negative relationship with the HRK/USD exchange

rate and a positive relationship with real GDP or income in Croatia, the real interest rate in the U.S., the

stock price in the U.S., and the expected HRK/USD exchange rate. The supply of the U.S. dollar is

expected to be positively associated with the HRK/USD exchange rate, real GDP or income in the U.S.,

the real interest rate in Croatia, and the stock price in Croatia. As real GDP or income in Croatia rises,

Croatians tend to import more goods and services from the U.S. and increase the demand for the U.S.

dollar. When real GDP or income in the U.S. rises, Americans tend to import more goods and services

from Croatia and increase the supply of the U.S. dollar in exchange for the Croatian kuna. A higher real

interest rate or stock price in the U.S. tends to attract Croatians to invest in these financial assets and to

increase the demand for the U.S. dollar. On the other hand, a higher real interest rate or stock price in

Croatia tends to attract American investors to buy these financial assets and increase the supply of the

U.S. dollar in exchange for the Croatian kuna.

Solving for the equilibrium values of the two endogenous variables simultaneously, we can express the

equilibrium exchange rate as a function of all the exogenous variables:

),,,,,,( eHRUSHRUSHRUS EEYYRRf (3)

Comparative static analysis shows that a change in any one of the exogenous variables is expected to

have an impact on the equilibrium HRK/USD exchange rate

0// JAR USR

US (4)

0// JBR HRR

HR (5)

0// JBY USY

US (6)

0// JAY HRY

HR (7)

0// JAE USE

US (8)

0// JBE HRE

HR (9)

0// JA e

e

(10)

Yu Hsing Journal of Social and Business Studies

ISSN: 2303-6044

Social and Business Development Center – www.sbdcenter.com

5

where )( BAJ is the Jacobian for the endogenous variables and has a negative value.

Note that in the monetary models based on the equilibrium condition in the money market, the sign of

the interest rate differential between Croatia and the U.S. may be positive or negative, depending upon

whether the Bilson (1978) model or the Dornbusch (1976) and Frankel (1979) models would apply.

Furthermore, the traditional view suggests that an increase in the interest rate would cause a currency to

appreciate whereas the revisionist view shows that a higher interest rate would cause a currency to

depreciate due to a higher default probability, a weaker financial position of firms that are debt

constrained, and a higher exchange rate risk premium (Huang, Hueng and Yau, 2010).

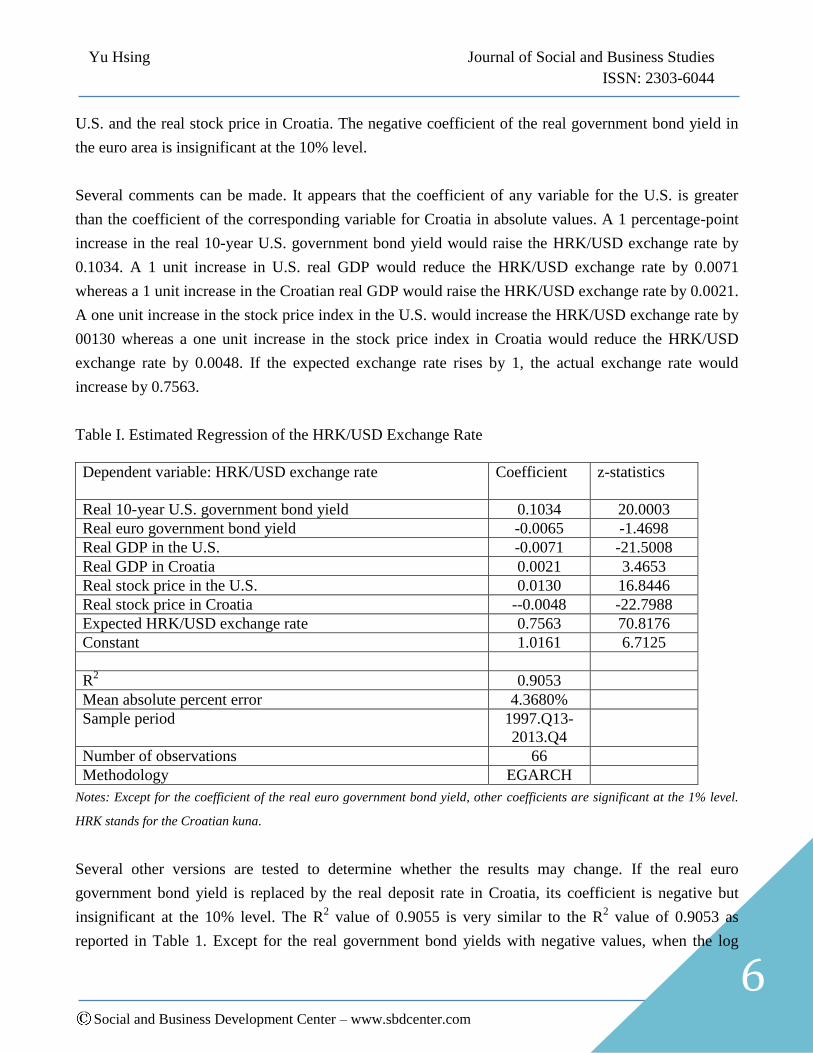

4. Empirical Results

The data were collected from the International Financial Statistics, which is published by the

International Monetary Fund. The HRK/USD exchange rate measures units of the kuna per U.S. dollar.

Hence, an increase means an appreciation of the U.S. dollar or a depreciation of the Croatian kuna. The

real interest rate in the U.S. is represented by the real 10-year government bond yield minus the

inflation rate in the U.S. Due to lack of data for the government bond yield, the real interest rate in

Croatia is represented by the government bond yield in the euro area minus the inflation rate in Croatia.

Real GDP in the U.S. or Croatia is an index number measured at the 2005 year. The expected exchange

rate is represented by the average HRK/USD exchange rate of past four quarters. The stock price in the

U.S. is represented by the share price in the U.S., and the stock value in Croatia is measured by the

share price in Croatia. The sample consists of quarterly data ranging from 1997.Q3 to 2013.Q4 and has

a total of 66 observations.

The ADF test on the regression residuals is employed to determine whether these time series variables

are cointgegrated. The value of the test statistic is estimated to be -3.3381, which is greater than the

critical value of -2.6016 in absolute values at the 1% level. Therefore, these variables have a long-term

stable relationship.

Table 1 presents estimated coefficients and other related statistics. The EGARCH method is applied in

empirical estimation in order to yield a positive conditional variance without restriction on the

parameters. As shown, 90.53% of the change in the equilibrium HRK/USD exchange rate can be

explained by the right-hand side variables. Except for the coefficient of the real government bond yield

in the euro area, other coefficients are significant at the 1% level. The equilibrium HRK/USD exchange

rate is positively associated with the real 10-year U.S. government bond yield, real GDP in Croatia, the

real stock price in the U.S., and the expected exchange rate. It is negatively affected by real GDP in the

Yu Hsing Journal of Social and Business Studies

ISSN: 2303-6044

Social and Business Development Center – www.sbdcenter.com

6

U.S. and the real stock price in Croatia. The negative coefficient of the real government bond yield in

the euro area is insignificant at the 10% level.

Several comments can be made. It appears that the coefficient of any variable for the U.S. is greater

than the coefficient of the corresponding variable for Croatia in absolute values. A 1 percentage-point

increase in the real 10-year U.S. government bond yield would raise the HRK/USD exchange rate by

0.1034. A 1 unit increase in U.S. real GDP would reduce the HRK/USD exchange rate by 0.0071

whereas a 1 unit increase in the Croatian real GDP would raise the HRK/USD exchange rate by 0.0021.

A one unit increase in the stock price index in the U.S. would increase the HRK/USD exchange rate by

00130 whereas a one unit increase in the stock price index in Croatia would reduce the HRK/USD

exchange rate by 0.0048. If the expected exchange rate rises by 1, the actual exchange rate would

increase by 0.7563.

Table I. Estimated Regression of the HRK/USD Exchange Rate

Dependent variable: HRK/USD exchange rate Coefficient z-statistics

Real 10-year U.S. government bond yield 0.1034 20.0003

Real euro government bond yield -0.0065 -1.4698

Real GDP in the U.S. -0.0071 -21.5008

Real GDP in Croatia 0.0021 3.4653

Real stock price in the U.S. 0.0130 16.8446

Real stock price in Croatia --0.0048 -22.7988

Expected HRK/USD exchange rate 0.7563 70.8176

Constant 1.0161 6.7125

R2 0.9053

Mean absolute percent error 4.3680%

Sample period 1997.Q13-

2013.Q4

Number of observations 66

Methodology EGARCH

Notes: Except for the coefficient of the real euro government bond yield, other coefficients are significant at the 1% level.

HRK stands for the Croatian kuna.

Several other versions are tested to determine whether the results may change. If the real euro

government bond yield is replaced by the real deposit rate in Croatia, its coefficient is negative but

insignificant at the 10% level. The R2 value of 0.9055 is very similar to the R

2 value of 0.9053 as

reported in Table 1. Except for the real government bond yields with negative values, when the log

Yu Hsing Journal of Social and Business Studies

ISSN: 2303-6044

Social and Business Development Center – www.sbdcenter.com

7

form is used, only the coefficients of the real U.S. government yield and the real stock price in Croatia

are significant whereas other coefficients are insignificant at the 10% level.

5. Summary and Conclusions

This paper has examined the determinants of the HRK/USD exchange rate in the short run based on a

simultaneous-equation model consisting of the demand for and supply of the U.S. dollar. A reduced-

form equation is estimated by the EGARCH method. The paper finds that a higher real U.S.

government bond yield, a higher real GDP in Croatia, a higher real stock price in the U.S., and a higher

expected exchange rate would raise the HRK/USD exchange rate whereas a higher U.S. real GDP and a

real higher stock price in Croatia would reduce the HRK/USD exchange rate.

There are several policy implications. It seems that demand and supply analysis of exchange rates in

the short run works reasonably well as it can explain approximately 90.53% of exchange rate

movements. The forecast error of 4.368% is relatively small. Interest rates, real GDP, stock prices and

the expected exchange rate in the U.S. and/or Croatia play important roles in exchange rate movements

in the short run. Recent higher real U.S. government bond yields or rising U.S. stock prices tend to

raise the HRK/USD exchange rate. Recent higher real government bond yields in the euro area or

higher U.S. real GDP would reduce the HRK/USD exchange rate. The current weaker economy in

Croatia is likely to put smaller downward pressure on the HRK/USD exchange rate. Relatively stable

stock prices in Croatia tend to stabilize the HRK/USD exchange rate.

6. References

Baharumshah, A. Z. & D. Borsic (2008). Purchasing Power Parity in Central & Eastern European

Pountries. Economics bulletin, 6, 1-8.

Bilson, J. F. O. (1978). Rational Expectations & the Exchange Rate in: J. Frenkel & H. Johnson, eds.

Economics of Exchange Rates (Addison-Wesley Press, Reading).

Broz, T. & T. Ridzak (2007). Exchange Rate Misalignment-A Case of Croatia. 4th International

Conference Global Challenges for Competitiveness: Business & Government Perspective

Chen, C. F., C. H. Shen, & C. A. A. Wang (2007). Does PPP Hold for Big Mac Price or Consumer

Price Index? Evidence from Panel Cointegration. Economics Bulletin, 6, 1-15.

Yu Hsing Journal of Social and Business Studies

ISSN: 2303-6044

Social and Business Development Center – www.sbdcenter.com

8

Chen, S. S. (2006). Revisiting the Interest Rate–Exchange Rate Nexus: A Markov-Switching

Approach. Journal of Development Economics, 79, 208-224.

Chen, S. W. (2009). Random Walks in Asian Foreign Exchange Markets: Evidence from New Multiple

Variance Ratio Tests. Economics Bulletin, 29, 1296-1307.

Cheung, Y.-W., M. D. Chinn, & A. G. Pascual (2005). Empirical Exchange Rate Models of the

Nineties: Are Any Fit to Survive? Journal of International Money & Finance, 24, 1150-1175.

Chinn, M. D. (1999). On the Won & Other East Asian Currencies. International Journal of Finance &

Economics, 4, 113-127.

Choudhry, T. (2005). Asian Currency Crisis & the Generalized PPP: Evidence from the Far East. Asian

economic journal, 19, 137-157.

Dornbusch, R. (1976). Expectations & Exchange Rate Dynamics. Journal of Political Economy, 84,

1161-1176.

Engel, C. (2010). Exchange Rate Policies. A Federal Reserve Bank of Dallas Staff Paper, DIANE

Publishing.

Erjavec, N., B. Cota, & S. Jakšić (2012). Sources of Exchange Rate Fluctuations: Empirical Evidence

from Croatia. Privredna kretanja i ekonomska politika, 22, 27-46.

Frankel, J. A. (1979). On the Mark: A Theory of Floating Exchange Rates based on Real Interest

differentials. American Economic Review, 69, 610-622.

Frenkel, J. A. (1976). A Monetary Approach to the Exchange Rate: Doctrinal Aspects & Empirical

Evidence. Scandinavian Journal of Economics, 78, 200-224.

Funda, J. & G. Lukinić (2008). Assessment of the Balassa-Samuelson Effect in Croatia. Financial

Theory & Practice, 31, 321-351.

Granger, C. W.J., B.-N.g Huang, & C.-W. Yang (2000). A Bivariate Causality between Stock Prices &

Exchange Rates: Evidence from Recent Asian Flu. The Quarterly Review of Economics & Finance, 40,

337-354.

Yu Hsing Journal of Social and Business Studies

ISSN: 2303-6044

Social and Business Development Center – www.sbdcenter.com

9

Hacker, R. S., H. K. Karlsson, & K. Månsson, (2014). An Investigation of the Causal Relations

between Exchange Rates & Interest Rate Differentials Using Wavelets. International Review of

Economics & Finance, 29, 321-329.

Ho, C. C., S. Y. Cheng, & H. Hou (2009). Purchasing Power Parity & Country Characteristics:

Evidence from Time Series Analysis. Economics Bulletin, 29, 444-456.

Kozul, I. (2013). Cointegration Analysis of Purchasing Power Parity in Republic Of Croatia. UTMS

Journal of Economics, 4, 253-268.

Miteza, I. (2012). The Law of One Price in Six Central & Eastern European Economies. Comparative

Economic Studies, 54, 581-596.

Park, D. (2011). Empirical Studies in Exchange Rates & Foreign Exchange Markets: A Survey. Asian

Journal of Financial Studies, 24, 851-908.

Saadaoui, J. (2011). Exchange Rate Dynamics & Fundamental Equilibrium Exchange

Rates. Economics Bulletin, 31, 1993-2005.

Schweigert, T. E. (2004). Croatian Exchange Rate Policy: Nominal Stability & Real Consequences.

Proceedings of Academy of Business & Administrative Sciences XI International Conference.

Seong, L. M. (2013). Reactions of Exchange Rates towards Malaysia Stock Market: Goods Market

Approach & Portfolio Balanced Approach. Interdisciplinary Journal of Contemporary Research in

Business, 5, 113-120.

Sorona, R. J. & J. Tica (2010). Purchasing Power Parity in CEE & Post-War Former Yugoslav

States. Czech Journal of Economics & Finance (Finance a uver), 60, 213-225.

Šošić, V. & E. Kraft (2006). Floating with a Large Life Jacket: Monetary & Exchange Rate Policies in

Croatia under Dollarization. Contemporary Economic Policy, 24, 492-506.

Tkalec, M. & M. Vizek (2010). Should the CNB Devaluate the Exchange Rate? Evidence from

Purchasing Power Parity. 16th Dubrovnik Economic Conference, Young Economists Seminar.

Yu Hsing Journal of Social and Business Studies

ISSN: 2303-6044

Social and Business Development Center – www.sbdcenter.com

10

Tkalec, M. & M. Vizek (2011). Purchasing Power Parity in a Transition Country: The Case of

Croatia. Comparative Economic Studies, 53, 223-238.

Journal of Social and Business Studies

ISSN: 2303-6044

Vol. 1(1) / pp.11-28

Social and Business Development Center – www.sbdcenter.com

11

The Impact of Global Financial Crisis in the Albanian Banking System

Alba Cani

Epoka University

Tirana, Albania

Citation: Cani, A. (2014). The Impact of Global Financial Crisis in the Albanian Banking System. Journal of Social and

Business Studies, 1(1), 11-28.

Article History

Submitted: 02 August 2014

Resubmitted: 15 August 2014

Accepted: 18 August 2014

Abstract

The banking system in Albania is represented as a consolidated and sustainable system.

Participation of powerful banking groups in the Albanian market could be seen as a

positive sign that provides security for the continuation of the growth and development

of this market. However, on the other hand, today's economy is severely affected by the

global financial crisis. The effects of this crisis we can also see in Albanian banking

system. Its impact was felt in every area of the Albanian economy, especially in the

financial intermediaries. The banking system, as one of the leading representatives of

financial intermediaries, is facing numerous difficulties as a result of the financial

crisis. The main purpose of this study is to examine the negative impacts of financial

crises in the Albanian banking sector. Therefore, this paper aims to investigate different

factors such as: injection of abundant liquidity, increased control over the banks of the

second level and pressure to increase transparency of banks and their influence on

current economic situation of the Albanian banking system. This study provides answer

on some research question such as: What are the possibilities for intervention to

prevent the negative effects of the crisis as well as to improve the situation? What are

these interventions and how should be implemented? Is there sufficient capacity for the

banking system to overpass the negative impact of this situation? This study concludes

with the result that the effec of financial crisis are felt in Albanian economy and

banking system but not with the same impact as in developed countries.

Keywords: Financial Crisis; Banking System; Sub-prime Mortgage Nonperforming

Loans EGARCH

JEL Classification: G010, G180, G210

Alba Cani Journal of Social and Business Studies

ISSN: 2303-6044

Social and Business Development Center – www.sbdcenter.com

12

1. Introduction

The economy is one of the areas where unexpected developments occur with high rates. Today the

global economy is facing problems and challenges that are unusual. The financial crisis has worried

almost all economists. Many questions and problems are solved unanimously, for other questions and

problems there are debates, while for some others no solutions are found. The question that arises is

whether should these crises happen; Are they normal for the global economy or they are artificially

created for geopolitical reasons?!

A popular expression says "the economy without crisis cannot be imagined in the same way as

Christianity cannot be perceived without hell." The arguments for the presence of crises are different

but we are interested to exit as soon as possible from this situation. Many countries have taken

measures to prevent negative effects on their economies or at least to minimize these effects. It is seen

that some countries have intervened in the right time with appropriate measures while some states have

delayed their decisions. Albania is a country which was not affected directly by the global financial

crisis because Albania is a country not well integrated into global financial markets. This negative side

of the Albanian finances made the effects of the crisis in Albania came indirectly and in a softer way

compared to developed countries. The reduction of remittances, lower consumer spending (more as a

result of panic), the problems of construction market, increased price of fuel and devaluation of the

Albanian Leke against foreign currencies, were some of the first effects of the crisis in the Albanian

economy. In the last quarter of year 2007 and first quarter of 2008 in Albania, economists started to

give their opinions and ideas about the crisis issue. Some solutions were taken ready by developed

countries and should only be implemented. Some other solutions were needed to be adapted to the

Albanian reality. So, from 2008 until now much focus is put to the measures to prevent the crisis

affecting Albanian economy. One of the fields that economists were cautious was the banking system.

The exposition of the Albanian banking system taking into consideration the effect of crisis is the main

issue of this research paper. The methodology used is a thorough study, based on a specialized

knowledge in Accounting and Financial Reporting courses obtained during a period of one year and the

Finance-Accounting courses and knowledge obtained during a three year period, as well as material

and theoretical studies important in the field of economy. The paper was prepared on the basis of

statistical data and uses a narrative approach, and comparative analysis regarding the problems and

effects of the crisis in the banking system.

The paper is organized as follows: the first section gives a thorough study for the global financial crisis

being followed by the financial crisis and central banking. The third part includes a study done for the

Alba Cani Journal of Social and Business Studies

ISSN: 2303-6044

Social and Business Development Center – www.sbdcenter.com

13

effects of this crisis in Albanian Banking sector. Finally, conclusions and recommendations are given

regarding the research papers‟ topic.

2. Literature Review

Globalization is viewed as the integration of the world in a single village where economic, political and

events that occur in one part of the world affect people in other parts of the world (Okeke, 2010).

According to Hausler (2002) globalization has to do with liberalization and integration of economies

including investment and trade, which has influenced financial and capital markets in the last decades.

In the findings of Balino (2000) the deregulation of banking activities was caused by the globalization

of finance.

Leyshon (1995) has found that liberalized financial markets are the source of increased financial assets

related with allocation of financial resources. Adei (2004) states that globalization has increased

chances for growth and development in some areas but there has been an increase in inequality

experienced especially by developed countries where Albania is part of this developing countries.

Based on different studies the financial crises is an immediate unexpected drop in the value of financial

assets owned by financial institutions.

Sanusi (2010) discovered that there are different factors that trigger the financial crisis such as:

negative investments ideology associated by fear or panic. This situation of fear and panic causes

further withdrawal of money from investors thus leading to increasing declines. Moreover, financial

networks and markets become unable to function and then collapse. According to Adamu (2010)

financial crisis shows its first signs when some financial institutions or assets lose a large part of their

value. Different scholars in the field of economics and finance have predicted the negative economic

effects before the current global financial crisis was spread in different parts of the world.

Minsky (1995) has cited that global financial integration is associated by the era of expansive

capitalism. Pettifor (2003) concluded that the credit expansion is fueled by the financial sector

expansion. This situation has initiated the creation of the “credit bubble” which has financed bubble in

assets, stocks, shares and property. According to Stiglitz (2010) the great recession of 2008 is

considered to be a complex issue and the causes of this crises were: underwriting standards for sub-

prime mortgages; flaws in credit rating agencies as well as risk management weaknesses at some large

U.S and European financial institutions.

Alba Cani Journal of Social and Business Studies

ISSN: 2303-6044

Social and Business Development Center – www.sbdcenter.com

14

3. The Global Financial Crisis

The term financial crisis is used to describe a wide range of situations in which some financial

institutions immediately lose a large part of their value. During a financial crisis, the unemployment

rate increases within a short period of time as many factories and production lines shut down

unexpectedly. Banks suspend many of these credits and loans resulted in nonperforming loans. Prices

fell everywhere, certainly influenced by the stock exchange market.

Many economists have offered their theories how the financial crises arise and evolve, what are their

causes and effects as well as ways to prevent them. However, researchers have not yet reached a

consensus on these issues and financial crises still represent a common phenomenon in the world

economy. The biggest financial crisis in history is considered the Great Depression in 1929 which

ended in 1945 based on statistical data.

Who were the causes of the crisis?

The financial crisis happened because of funding and acquisitions in the real estate, especially in the

housing sector. Actors of the crisis were individuals in the United States of America, who were

motivated by high prices of houses and got credit for buying them. The motivation for these purchases

of houses was based on the belief that over time, real estate prices would continue to rise, so a property

bought today would have a higher value a few months later, even if no investment was made on it.

Therefore, more and more buyers entered the market by raising the prices that were initially very high.

Another group of actors in this crisis were international financial institutions, which made capital

available in the form of credit for those individuals interested in real estate. The problem here is

doubled: primarily they attracted buyers with loans, the interest of which was initially very low, and

then went to another extreme of growth. The fact of increasing interest rate normally would have been

a problem for buyers, but their belief that they would be able to sell their properties for a higher price in

a very short period of time eliminated this concern from their minds. Secondly, banks gave credit not

only to qualified individuals based on their profile and revenues but also to those who clearly had a

higher risk profile, as they were unemployed or did not have a certain level of income to ensure paying

the loan. Naturally, it is surprising that how institutions like banks that have whole departments for

credit risk analysis, granted loans to these kinds of persons.

The explanation is as follows: Firstly, the mentality of increased prices was available even for the

banks, which believed that if individuals for one reason or another cannot make their payments, they

will be able to receive real estate and sell with higher prices, providing capital and principal and their

Alba Cani Journal of Social and Business Studies

ISSN: 2303-6044

Social and Business Development Center – www.sbdcenter.com

15

profits. Secondly, banks took an unusual step, by buying insurances regarding these loans, with the idea

that if the housing market demolished, they will get back the money that they had previously lent. This

brings us to the third group of actors of the financial crisis: the insurance company.

The concept of insurance companies works because even though insurance as a form of security were

purchased by many individuals or companies, only a few of them in fact need to use these insurance

plans. In this case, exactly the opposite happened. Housing prices which were grown without any basis

for the development of real estate burst like a bubble, engendering the financial crisis. The first

bankruptcy occurred to a mass of people, who may not be able to resell their homes, soon followed by

the failure of insurance companies, which were forced to pay according to contracts of banks.

The global financial crisis is not reflected in the same way in the whole economies of the countries

because of the different characteristics of the organization of the financial system and the economic one

of each country.

The financial crisis and central banking

Some years ago, in some countries central banking defined the appropriate level of short-term interest

rates in order to have a desired rate of inflation. Now everything is more complicated. The emergence

of the credit crisis has caused central banks to inject enormous amounts of liquidity in their banking

systems to support lending to the economy to limit recession. In different situations, they had to

cooperate with respective governments to recapitalize banks, which otherwise would have gone

bankrupt, causing a huge economic imbalance than that currently experienced. However, if the

assumptions are not completely wrong, it seems clear that the situation will not be as severe as during

the Great Depression, when the GDP in the United States fell by 25% during 1929-1932.

According to forecasts, in 2010 the world GDP marked the highest value that has been seen ever. There

is a clear movement of income from rich people to poor ones, and so far China has shown a very good

performance. The current recession has affected the private sector and particularly financial sector. The

main Cause include excessive optimism on the progress of ongoing economic growth which led to the

underestimation of credit risk by banks, other lenders and investors. In the United States, it seems clear

that the performance of subprime mortgage loans, which were expected to bring profits also enabling

the poorest people to possess a house, went out of control. However, there were other reasons, mainly

related to the management of banks and other financial institutions. The uncertainty on the extent of the

recession has been high, because it is caused by malfunction of the overall financial sector, which is

central to the economy and it is assumed that it provides access to the means of payment and allocation

of limited resources to the most productive uses.

Alba Cani Journal of Social and Business Studies

ISSN: 2303-6044

Social and Business Development Center – www.sbdcenter.com

16

If something is not progressing in this industry, it is likely that the consequences be much more severe

than in the case of problems in other sectors.

The primary objective of monetary policy has been to reduce the negative effects caused from the crisis

in the economy. Specifically:

Central banks have granted more loans to commercial banks, to reduce the pressure of the credit

contraction and to assist in the process of granting new loans. To achieve this, the central banks

have accepted a wider range of assets as collateral. As a result, the central bank balance sheets have

grown enormously.

Central banks introduced new institutional instruments to guarantee international liquidity, despite

weakness in the international networks of commercial banks.

Interest rates were reduced to minimum levels to encourage spending and in particular to reduce the

burden of debts.

In the case of commercial banks threatened by bankruptcy, the governments have provided new

loans aimed at continuance of activity. Experience of Lehman Brothers showed us that

consequences may lead to the bankruptcy of a large financial group.

Revenues from taxes have fallen everywhere and government spending primarily to support banks,

are increased. Consequently, budget deficits are expanded.

Since the beginning of the crisis, banks have received new capital more than 1 trillion dollars, this

figure roughly equal to the total decrease of the value of the assets in the balance sheet. IMF predicts

that the banks will need $ 875 billion to restore report of assets / capital in 25, or 1.7 trillion dollars to

decrease this report in 17. Therefore the process of recapitalizing the banking sector is a complicated

process and needs a long time to be completed.

It is not easy for commercial banks to collect new capital and this for several reasons:

Criteria for securing capital and liquidity will be stronger and tougher than in the past and it will

reduce the rate of return on capital used.

Many of accounting issues that caused uncertainty about the net value of banks are not solved yet.

Some sovereign wealthy funds have lost significant amounts of money by supplying banks with

new capital during the beginning of the crisis. If the economy continues to weaken, then the

government may need to inject more capital to ensure a sustainable economic activity. Despite the

progress of the future of the economy, it is likely that most of the additional capital will come from

retained earnings.

Consequently, this causes the following effects:

Differences between deposits‟ interest rates and bank loans‟ interest rates will be larger than in the

past.

Alba Cani Journal of Social and Business Studies

ISSN: 2303-6044

Social and Business Development Center – www.sbdcenter.com

17

Official interest rates will stay low for a long time, to maintain low cost of borrowing.

The opinion of lending banks will remain cautious for a long time.

Banking will be a less competitive form of financial intermediation than in the past and financing of

capital markets will be relatively more important.

International Development

The global economy continued to slow in 2012. Most of developed countries experienced continuous

contraction of GDP during this year, while emerging economies marked moderate growth rates. High

rates of unemployment, the weakness of aggregate demand, the need for fiscal consolidation and

reduction of borrowing of businesses and families have taken the form of a negative spiral for the

majority of developed economies. Financial markets have reflected this difficulty and are characterized

by risk premiums and higher yields. Developing countries have managed to maintain positive growth

values, although the above difficulties have affected the performance of exports and investment flows

to them. Global inflation pressures were generally restrained while remaining aligned to the emerging

economies rather than in industrialized countries.

The growth of the world economy during the second half of 2012, has been positive but at a slower

pace than in the first half of this year. Economic crunch was mostly seen in developed countries,

particularly in the Euro Zone, due to weakness in domestic consumption and investment, condition of

high unemployment, the collapse of the credit system and strong enforcement of strong fiscal reforms.

Emerging economies experienced economic growth in this period, although the pace of their

growth was driven by the decline of external demand and the implementation of restrictive policies

initiated from last year.

World Trade activity was weakened mainly due to the decline of demand for exports from

developed economies.

The performance of global financial markets has been generally positive in the last two quarters of

2012, reflecting the effects of policy initiatives mainly in the Euro Zone and the United States of

America (USA). Actions of the European Central Bank (ECB) as further facilitator of monetary policy,

commitment to purchase unlimited amount of publicly owned bonds in secondary markets,

restructuring of the banking sector in Spain, renovation of financial loan for Greece affected positively

the reliability of investors in financial markets. Rates of return required for state titles in the Euro Zone

declined and the marketing conditions, in almost all segments of the financial market, were improved.

Based on recent developments of macroeconomic indicators, global activity is expected to be recovered

gradually in late 2013 and strengthen this trend during the next year, supported by improved financial

conditions and monetary policies in most developed economies as well as in developing one.

Alba Cani Journal of Social and Business Studies

ISSN: 2303-6044

Social and Business Development Center – www.sbdcenter.com

18

However, there are a number of risks such as:

The slow implementation of structural reforms in the Euro Zone,

The further contraction of global trade

Geopolitical conflicts and macroeconomic instability in the developed countries continue to be

present.

These factors may adversely affect the financial markets thus delaying the process of global economic

recovery.

Table 1: Some important macroeconomic indicators

The change of

GDP

Unemployment

Rate Inflation Rate

Countries / Years 2011 2012 2012 2011 2012

USA 1.8 2.2 8.1 3.2 2.1

Eurozone 1.4 -0.5 11.3 2.7 2.5

Germany 3.0 0.7 5.9 2.3 2.0

France 1.7 0.0 10.2 2.1 2.0

UK 0.9 0.0 7.9 4.5 2.8

Japan -0.5 1.6 4.3 -0.3 0.0

Source: (EUROSTAT, 2013)

4. Methodology

The aim of this study is to give a comprehensive overview of the impact of global financial crisis in

Albania being focused in its banking system. The methodology used for measuring the impact was

based on macroeconomic indicators and all the available official data and statistics were taken from

central institutions in Albania. Reports and statistics were sourced from institutions such as: Bank of

Albania, IMF and Eurostat. In terms of global financial crisis, the study is based on the books of

Mishkin and Marone being the primary sources for research paper. The reports issued from Central

Bank were useful in providing qualitative and quantitative analysis based on reliable data. The

methodology is based mainly on qualitative technique where there is done an analysis and

interpretation of information taken from sources such as: books, Bank of Albania, magazines and IMF.

The paper was prepared on the basis of statistical data and uses a narrative approach, and comparative

analysis regarding the problems and effects of the crisis in the banking system.

Alba Cani Journal of Social and Business Studies

ISSN: 2303-6044

Social and Business Development Center – www.sbdcenter.com

19

5. Financial Crisis and Banking System

Current situation of the banking system

Nowadays several years after the financial crisis had started even the financial system in Albania has

begun to feel the adverse effects thus causing the banking activity to slow the pace of its development.

The current crisis felt by businesses and individuals has made the banking system in Albania to show

different problems. The increased level of nonperforming loans, lower interest rates of loans or lack of

liquidity are some of the main problems that the banking system has faced. In developing countries like

Albania the economic growth has been comparable to those of developed countries and it can be said

that there are still opportunities as well as economic potential for further development and growth. In

developing countries, as is also Albania, the inflation rate has been higher than in the developed

countries. This is because developing countries have also had a higher economic growth than

developed countries. On the other hand, it can be said that the global financial markets have not shown

stability. They have been highly volatile due to the problems triggered by the economies of Euro Zone

countries regarding to public debt.

The year 2012 has been a challenging year for the economy, for Albanian businesses, families as well

as for decision-making in microeconomic and macroeconomic level. Domestic and Foreign economic

and financial shocks have negatively affected the economic growth but they do not have infringed the

macroeconomic and financial stability of the country. Also, a negative impact in the financial markets

had the slow development of the economy of USA which in turn had influenced negatively the

financial markets of other countries. Albanian economy during 2012 was faced with favorable stroke,

coming from inside and outside environment. However, the economic developments of the year

generally remained within the parameters of economic stability, as in the real sector and the financial

sector. Output growth during the first nine months of the year was 1.6%, which was mainly affected by

increasing the level of services offered while shrinking the manufacturing sector. According to

INSTAT, employment in the economy grew by 0.33% on average; this increase was smaller than that

of 2.1% recorded the previous year.

The Albanian economy has recorded a positive growth of 1.6% in real terms during 2012. This

performance is influenced by the most comprehensive monetary stimulus and the improvement of

external economic and financial environment. Economic activity remains below the potential level

regardless of output growth. The latter is not associated with a general reduction of uncertainty,

affecting consumption and private investment, and consequently the supply and demand for loans.

Therefore, the demand for loans is estimated to be weak and dependent on the performance of slow rate

of economic activity, the uncertainty seen in the projections of the future, as well as on the cautious

Alba Cani Journal of Social and Business Studies

ISSN: 2303-6044

Social and Business Development Center – www.sbdcenter.com

20

behavior of the banking system in the lending direction. Developments in the financial sector have

reflected the dynamics of the real sector of the economy and credit growth in its historical minimum.

Influencing factors include the lack of healthy demand from business and individuals, and the high

sensitivity to the banking sector to the risk of credit default. The quality of the loan portfolio continued

to deteriorate, as shown by the increase in weight of loans in their total 18.8% versus 22.5% a year ago.

In accordance with the above developments the average inflation resulted in 2% staying within the

limit set by the Bank of Albania. Inflationary expectations remained near the target. Exchange rate

remained generally stable and mitigated the impact of fluctuations in foreign price inflation.

In these conditions, in support of medium-term target for inflation and aiming the reduction of the

negative output gap, the Bank of Albania lowered its interest rate three times during the year, going

down from 4.75% to 4%. By reducing the costs of financing the banking system, the monetary

authority aims to reduce the interest rate of loans and increased consumption and investment in the

economy. Banking system records sound and liquid balance and good capitalization position but it

continues to be characterized by a special care in financing investment. The volume of activity

expanded at lower rates due to slower growth of deposits and significant reduction in the lending rates.

For the banking sector, credit risk represents the most important challenge of the activity, while

exposure of the system to market risks and liquidity risk remains moderate.

Despite the difficult economic context taking into account the financial stability during 2012, some

important indicators of financial health are improved. The banking sector is relatively protected against

the risks of financial markets, exchange rate fluctuations and interest rate. On the other hand, risks

associated with the real sector's ability to repay debt are added. In support of its supervisory functions

the Bank of Albania has further strengthened regulatory framework towards enhancing transparency

and disclosure of information, the quality of bank management and the harmonization of legislation

with the national standards. An investment in the orientation of banks toward strategic plans is done

with focus the domestic economy as well as reducing the problems regarding NPL-s.

The performance of the financial system appears stable and the banking sector is well-capitalized,

liquid and with profit growth indicators. The annual growth in deposits and loans has fallen especially

for the loan case the growth has fallen to low historic levels. Non-bank financial institutions, savings

and credit societies, insurance companies, private supplementary pension companies and investment

fund, have further expanded their activity. Beside the positive developments in the financial system,

credit quality continues to present a major problem for the lending institutions that carries out these

activities in the country.

Alba Cani Journal of Social and Business Studies

ISSN: 2303-6044

Social and Business Development Center – www.sbdcenter.com

21

In Albania, the banking sector is the main financial intermediate. The level of financial intermediation

in Albania figured out as a ratio of assets of financial system to GDP is at 93.9% in the end of 2012.

The volume of assets of financial institutions rose by 2.9% compared with six months earlier and 7.3%

compared with a year ago. The banking sector remains a key segment of financial intermediation,

whose assets represent about 93.6% of the total assets of the financial system in general and about

87.9% of GDP.

Non-bank financial sector continues to reflect a lower total weight to total financial system. Total assets

of non-bank financial sector represent about 6.4% of the financial system, increasing the weight to 5.3

% for year 2011. This increase is due to the increased number of non-bank financial institutions. In late

2012, the share of non-bank financial sector activity to GDP was around 6%. So, it is clearly noted that

despite the fact that the global economic crisis has affected the Albanian financial system, there has

been an increase in its activity.

Financial crisis and its impact on banking system

Today in everyday people's lives, the word "crisis" has taken a certain sense from which derives any

negative phenomenon in the world economy and also in Albanian economy as well. Negative impacts

of the crisis in the Albanian economy have been and continue to be in different dimensions. This

financial crisis contaminated every country including developed countries or developing one. In this

section of this paper, the impact of the crisis on the Albania banking system is shown.

As mentioned above, this was one of the crises that gave her first signs late in 2007 and in early 2008.

During this period, the global stock markets and financial markets began to suffer reductions in their

values reaching minimum level. These made losses incurred by many companies and financial

institutions to reach stratospheric levels within a short period of time. These losses are estimated to

have been around $ 50000 milliard. Based on current studies and also in the statistical data it can be

said that the main reason for the start of this crisis were problems in the U.S. mortgage loans.

So, the high level of NPL-s caused a lack of liquidity in the banking system and this problem was

spread like the domino effect on financial markets around the world, also significantly reducing

confidence in these financial institutions. Among the main consequences of this crisis in the world

economy we can mention the devaluation of foreign currencies of the respective countries (especially

the dollar after Euro). It gave rise to budget deficits and growing unemployment.

Despite the increasing bank of Lehman Brothers and the consequences being spread in Europe,

withdrawals of bank deposits in the fourth quarter of 2008 in Albania were somewhat surprising.

Ultimately, the banking system was steadily increasing its assets, loans and deposits and with a

Alba Cani Journal of Social and Business Studies

ISSN: 2303-6044

Social and Business Development Center – www.sbdcenter.com

22

sensitive indicator of the return on assets above the level of 1%. The overall performance of the

economy was also good with a growth rate of over 6% and debt levels under control of the government.

Although Albania has modest financial institutions, this country is feeling the weight of this financial

crisis which has already taken the form of a global economic crisis. Disintegration of our country in

financial markets and the poor financial systems have served as barriers to be protected by strong initial

impact of "credit crisis”. Even though Albanians are under the effects of the crisis, but not in crisis, it

must be realized that they do not enjoy immunity and the consequences cannot be avoided. While the

banking sector is well capitalized and funded mainly by deposits of individuals. Our banking system is

characterized by a low level of lending to the economy.

Among other effects of the crisis we can mention:

Reduction of the volume of international trade.

Reduction in high rates of foreign direct investment (FDI)

Reduction of the level of lending by the banks of the second level and the reduction of remittances

from Albanian emigrants who are part of countries which are hit hard by the economic crisis.

These effects obviously influenced on banking activity:

By reducing their liquidity, then consequently lending. This led to less investment in Albania thus

creating economic crunch.

Another element of the banking crisis which influenced the banking system and finances as a whole

was "panic". People‟s fear of what is going to happen in the future was a concerning issue. So, they

postponed their spending and consumption thus reducing the liquidity of manufacturers making the

economy to enter in the recession period of business cycle.

Consumers were uncertain what is expected to happen in the days that followed. When it comes to their

savings, consumers were very sensitive. This situation stimulated panic in the Albanian market causing

withdrawals of deposits from the respective banks but relatively controlled by the banking system. So,

we can say that all the above problems negatively affected banking system by increasing suspicion in

this system. The majority of banks in Albania are with foreign capital, this capital coming from

countries worst affected by the crisis, such as Greece or Italy.

Alba Cani Journal of Social and Business Studies

ISSN: 2303-6044

Social and Business Development Center – www.sbdcenter.com

23

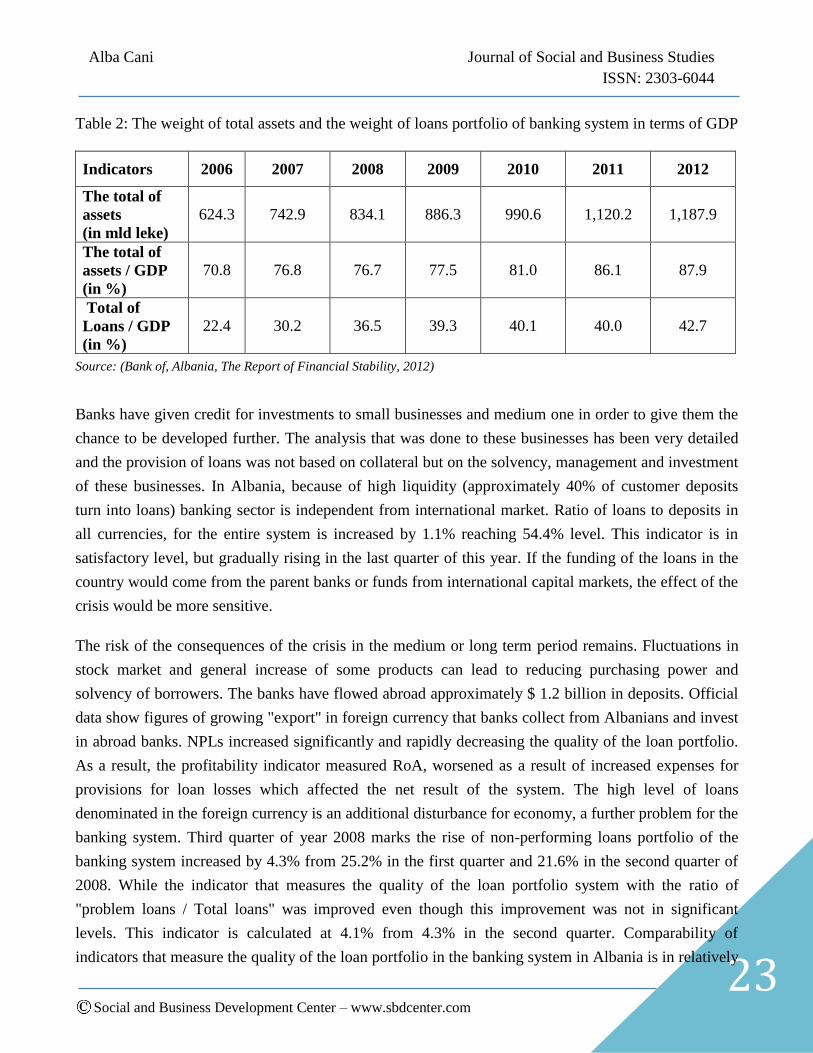

Table 2: The weight of total assets and the weight of loans portfolio of banking system in terms of GDP

Indicators 2006 2007 2008 2009 2010 2011 2012

The total of

assets

(in mld leke)

624.3 742.9 834.1 886.3 990.6 1,120.2 1,187.9

The total of

assets / GDP

(in %)

70.8 76.8 76.7 77.5 81.0 86.1 87.9

Total of

Loans / GDP

(in %)

22.4 30.2 36.5 39.3 40.1 40.0 42.7

Source: (Bank of, Albania, The Report of Financial Stability, 2012)

Banks have given credit for investments to small businesses and medium one in order to give them the

chance to be developed further. The analysis that was done to these businesses has been very detailed

and the provision of loans was not based on collateral but on the solvency, management and investment

of these businesses. In Albania, because of high liquidity (approximately 40% of customer deposits

turn into loans) banking sector is independent from international market. Ratio of loans to deposits in

all currencies, for the entire system is increased by 1.1% reaching 54.4% level. This indicator is in

satisfactory level, but gradually rising in the last quarter of this year. If the funding of the loans in the

country would come from the parent banks or funds from international capital markets, the effect of the

crisis would be more sensitive.

The risk of the consequences of the crisis in the medium or long term period remains. Fluctuations in

stock market and general increase of some products can lead to reducing purchasing power and

solvency of borrowers. The banks have flowed abroad approximately $ 1.2 billion in deposits. Official

data show figures of growing "export" in foreign currency that banks collect from Albanians and invest

in abroad banks. NPLs increased significantly and rapidly decreasing the quality of the loan portfolio.

As a result, the profitability indicator measured RoA, worsened as a result of increased expenses for

provisions for loan losses which affected the net result of the system. The high level of loans

denominated in the foreign currency is an additional disturbance for economy, a further problem for the

banking system. Third quarter of year 2008 marks the rise of non-performing loans portfolio of the

banking system increased by 4.3% from 25.2% in the first quarter and 21.6% in the second quarter of

2008. While the indicator that measures the quality of the loan portfolio system with the ratio of

"problem loans / Total loans" was improved even though this improvement was not in significant

levels. This indicator is calculated at 4.1% from 4.3% in the second quarter. Comparability of

indicators that measure the quality of the loan portfolio in the banking system in Albania is in relatively

Alba Cani Journal of Social and Business Studies

ISSN: 2303-6044

Social and Business Development Center – www.sbdcenter.com

24

good levels, compared with the general level of this indicator in the region. According to the Bank of

Albania, the NPLs result within acceptable standards. According to experts, the problem of loans will

increase because the number of loans granted during the last year has significantly increased. Banks

and banking system have been continuously privileged as a good part of their portfolio was invested in

government securities. The high interest rate of treasury bills and bonds often above deposit interest

rates with the same maturity time, did not only offer liquidity but also the best profits for banks and the

insurance company. This portfolio is 100% sure in terms of the security thus raising the level of

security of banks operating in Albania despite numerous shareholders and connections that these banks

have to European countries.

Although the level of credit in the economy has been growing from year to year, again we can say that

the level of lending remains low compared to western countries which were in the turbulence of the

recent crises. Less than 50% of deposits collected are given as loans for the economy being in this way

at a lower level compared with western countries where economies grant loans with more than 75% of

deposits collected. This low level of lending exhibits less Albanian banks to credit risk. It should be

noted that due to the low level of loans that Albanian banks have granted, they had the luxury of

selecting the best client.

Lack of liquidity is one of the negative effects of the crisis. Banking system was faced with this

phenomenon in late 2008, where as a result of the panic, the public began not only to reduce their level

of deposits but also to withdraw a portion of them. In 2008 there was a drastic decline in deposits. Lack

of liquidity poses not only risk for the banking system but also for the economy as a whole. This brings

less investment and consequently there will be a reduction in the overall level of economic

development of the country, low level of lending leading the economy to recession.

These effects mentioned above are the main ones which affected banking system because almost every

financial indicator (positive indicator of performance) of the banking system experienced significant

reduction.

There are generally two basic types of financial crises where we can mention:

Crisis of currency or exchange rates

The banking crisis and external debt crisis.

In this paper a lot of focus is given to the financial crisis which has several definitions, where the below

findings are mentioned: "Financial crisis is the situation in which the demand for money grows so fast"

or "Financial crisis refers to a situation in which financial institutions or financial assets lose their value

resulting in declining of financial institutions or non-financial institutions."

Alba Cani Journal of Social and Business Studies

ISSN: 2303-6044

Social and Business Development Center – www.sbdcenter.com

25

It can be said that the banking crisis occurs when the banking system suffers from liquidity problems as

well as when banks have a high level of nonperforming loans. This may lead the bank into bankruptcy.

A bank, in crisis situation necessarily requires the assistance of the state. Generally speaking the

banking crises generally pass in two stages: in the first stage at which banks create a large number of

NPL-s but tries not to report these loans based on reasons of trust, and the second stage which has to do

with the publication, deals with these problems and requires immediate solutions for them. These crises

have existed previously but problems transmitted in the economy probably have been different. During

the years 1980 - 1995 developed countries faced 65 crises with an estimated cost of $ 250 billion.

Finally, it is important to emphasize that financial crises (banking crises) have been inevitable and

economies of different countries coped with these negative phenomena. It is valuable to learn lessons

derived from these countries in order to face less negative consequences in the future. The behavior of

each person and of the banking system as a whole is an essential element for coping and dealing with

crises. "The majority of business failures do not result from the difficult times. The failures are

attributed to the wrong management and the way how difficult times just deteriorate the situation."

6. Banks Balance

2012 – The report of nonperforming loans to total loans resulted in 22.5% in the end of 2012, from

18.8% at the end of 2011.

2013 – In the first months of 2013, non-performing loans is 24%, with a tendency towards

deterioration.

Fund – There are 1 milliard euros of loans reported with problems, where approximately 300 million of

them are considered lost.

7. Conclusion

In conclusion we can say that the effects of the crisis in Albania are felt but it did not have the same

impact as in developed countries. This comes due to the fact that Albania is not well integrated into

global financial markets. But the fact that Albania is not strongly affected by the crisis does not mean

that it will not be affected by its consequences. Among the consequences of the financial crisis in

Albania we can mention the lowering upward rates of economy, increased unemployment, currency

devaluation against foreign currencies, reduction of production and consequently that of exports, the

decline in general business activity and reduced remittances. Those directly affected the performance of

the banking system influencing the increase of the number of loans with problems, the reduced growth

rates of deposits thus causing lack of liquidity in the market and as a result significantly lowering the

Alba Cani Journal of Social and Business Studies

ISSN: 2303-6044

Social and Business Development Center – www.sbdcenter.com

26

level of lending. Reduction of lending will lead to less investment in the economy, rising

unemployment and many other negative effects on our economy. Fortunately, some steps had been

undertaken which held banking system under control, but on the other hand attention should be shown

in interbank markets as well as for the economy as a whole in this period of crisis.

The particular attention should be paid to human capital. Recruitment for vacant positions in the

banking system should be made based on the ability of the worker and not on subjective factors. This

means that those who become part of the banking system must have appropriate qualifications and

experience. Control systems of the banking system continuously should not only perform periodic

controls but also 'surprise controls "(outside planning controls). So, in this moment the internal audit,

the external one as well as oversight of the Central Bank should be more cautious. If it is necessary, the

banking system must maintain liquidity and additional funding. The attention should be directed toward

immigrants, who are the main suppliers of income. The limit of security deposit should be increased, as

it has also happened in many other countries.

Finally, it should be emphasized that despite the effects of the crisis in the banking system and the

measures that have been taken or not, Albania has potential opportunities for development in this

sector. A better management of all assets and an inter-institutional functioning will make the

performance of the banking system to be constantly increasing.

8. References

Adammu, A. (2010). Social Science Reported Network. The Effects of Global Financial Crisis on

Nigerian Economy .

Adei, S. (2004). Impact of Globalization on Management: The African Perspective. Management in

Nigeria. EUROPEAN Journal of Business and Management, 39/40(21), 20-25.

Balino Tomas, U. A. (2000, June). The New World Banking Finance and Development. Finance and

Development, 41-44.

Bank of Albania. (2008). Financial System Stability in Albania for the second half of the year 2008.

Bank of Albania Statement.

Bank of Albania. (2009). The policies of monetary and financial stability - Lessons learned from the

crisis. The 8th International Conference of Bank of Albania.

Alba Cani Journal of Social and Business Studies

ISSN: 2303-6044

Social and Business Development Center – www.sbdcenter.com

27

Bank of Albania. (2012). Bank of Albania, The Report of financial stability.

Bank of Albania. (2012). The Report of Financial Stability. Tirana, Albania.

Bank of Albania. (2012). The Report on Financial Stability for the last quarter of 2012.

Bank of Albania. (2012). Bank of Albania, The Report of Financial Stability.

Bank of Albania. The Annual Report.

Bank of Albania. (2008-2012). The Annual Report of Supervision.

Bank of Albania. (2008-2012). The Annual Report of Banking Supervision. Albania

Dervishi, D. (2011). Monografi-Krizat Financiare dhe modeli stress indeks.

EUROSTAT. (2013). EUROSTAT. Retrieved from EUROSTAT.

Hausler, G. (2002). The Globalization of Finance. Journal of Finance and Development, Vol. 39, 10.

IMF. (2009). The implications of the global financial crisis for low income countries.

Kadareja, A. (2012). The Conservatorism of Banks: Zgjedhje e Qellimshme apo e Detyruar prej

ngjarjeve. Bankieri Magazine, No.3.

Kadareja, A., & Meka, E. (2012). The Banking in Albania and its path toward the future. Economicus

9.

Leyshon, A. (1995). Geographies of Money and Finance. Progress in Human Geography , Vol. 19 (1),

531.

Misnky, H. (1995, 29 March). Longer Waves in Financial Relations: Financial Factors in the More

Severe Depressions II. Journal of Economic Issues, 83 – 95.

Mishkin, F. Financial crises and aggregate economic activity. In F. Mishkin, Money Banking and