The Impact of FRS on Taxation Tan Hooi Beng 11 August 2009

The Impact of FRS on Taxation Tan Hooi Beng 11 August 2009.

Dec 26, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

The Impact of FRS on Taxation

Tan Hooi Beng11 August 2009

© 2008 Deloitte Touche Tohmatsu2

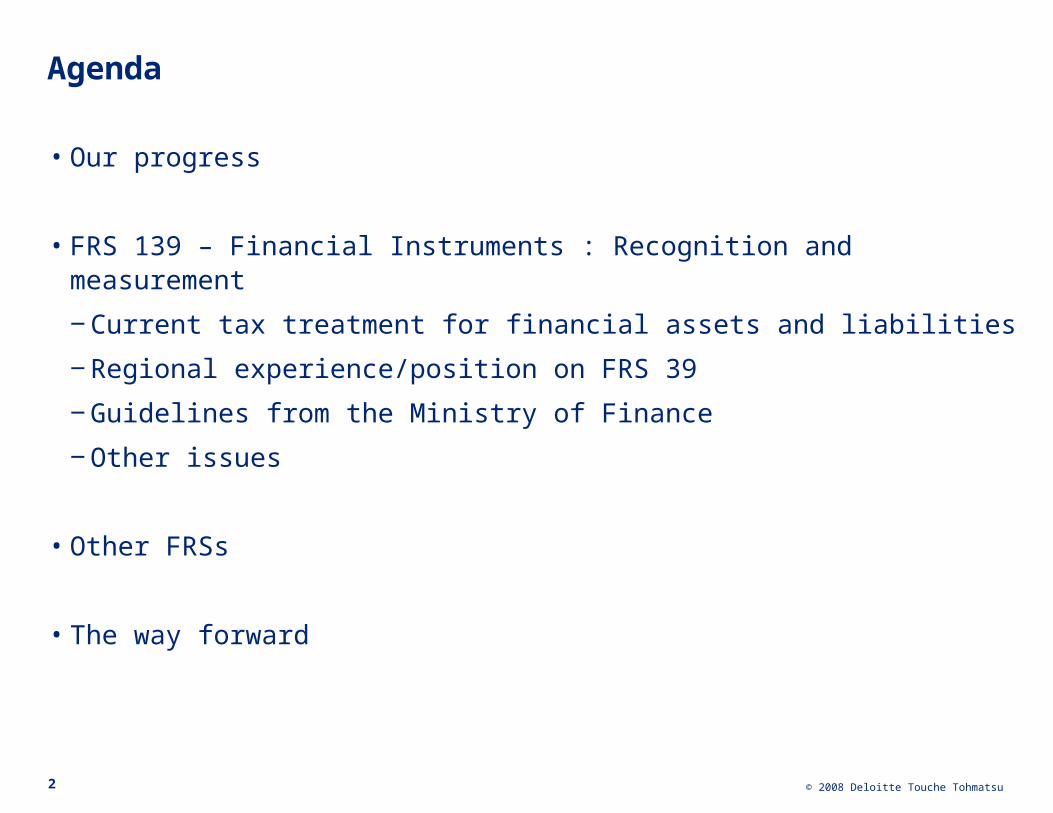

Agenda

• Our progress

• FRS 139 – Financial Instruments : Recognition and measurement

‒ Current tax treatment for financial assets and liabilities

‒ Regional experience/position on FRS 39

‒ Guidelines from the Ministry of Finance

‒ Other issues

• Other FRSs

• The way forward

© 2008 Deloitte Touche Tohmatsu3

Our Progress

Our Progress

• 1978 - First adoption of few international accounting standards, IAS

• 1997 - Parliamentary Act established MASB, conferring MASB standards a legal standing for all companies

• 2005 - Renaming of MASB standards to Financial Reporting Standards (FRS) in line with International Financial Reporting Standards (IFRS)

• 2006 - Introduction of two-tier financial reporting for private and non-private entities

• 2007 - FRS made identical to IFRS

• 1 April 2008 – MOF issued "Guidelines On Income Tax Treatment From Adopting FRS 139" which are applicable to FIs

• 1 August 2008 - Announcement of convergence plan with IFRS by 1 January 2012 by MASB and FRF

• 22 Apr 2009 - Establishment of Joint Tax Working Group on Financial Reporting Standards (JTWG-FRS)

© 2008 Deloitte Touche Tohmatsu5

FRS 139 - Financial Instruments : Recognition and measurement

Current Tax Treatment for Financial Assets and Liabilities

• Capital vs revenue

• Disposal of financial assets (revenue account):- Realized gain – taxable

- Realized loss – deductible

• If financial assets (revenue account) are carried at lower of cost or MV and such assets has been written down to MV, the difference write down or diminution in value will be allowed as deduction

• Capital account (e.g. investment in subsidiary)- Gain – not taxable- Loss – not deductible

• Diminution in value – not deductible

• Interest on financial liabilities- Deductible if tax deductions rules are met

Current Tax Treatment for Financial Assets and Liabilities

(Cont’d)

© 2008 Deloitte Touche Tohmatsu8

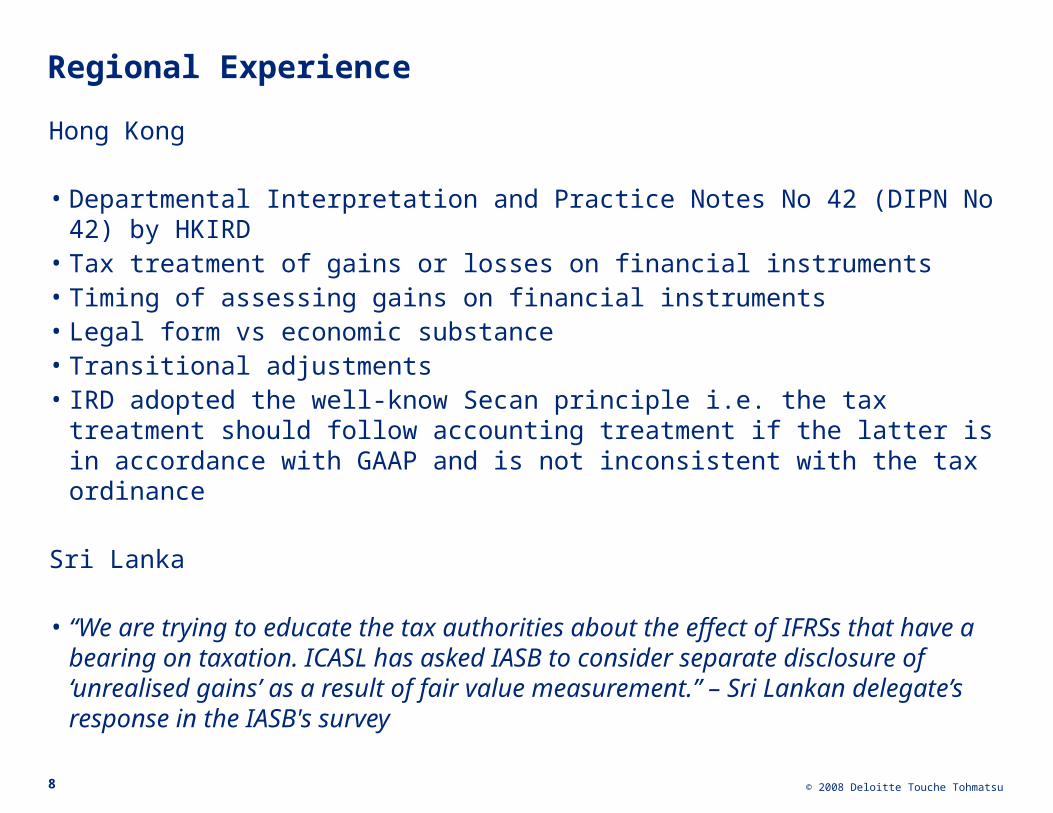

Regional Experience

Hong Kong

• Departmental Interpretation and Practice Notes No 42 (DIPN No 42) by HKIRD• Tax treatment of gains or losses on financial instruments• Timing of assessing gains on financial instruments• Legal form vs economic substance• Transitional adjustments• IRD adopted the well-know Secan principle i.e. the tax treatment should follow

accounting treatment if the latter is in accordance with GAAP and is not inconsistent with the tax ordinance

Sri Lanka

• “We are trying to educate the tax authorities about the effect of IFRSs that have a bearing on taxation. ICASL has asked IASB to consider separate disclosure of ‘unrealised gains’ as a result of fair value measurement.” – Sri Lankan delegate’s response in the IASB's survey

© 2008 Deloitte Touche Tohmatsu9

Regional Experience (Cont’d)Singapore

• FRS 39 - financial period begining on or after 1 January 2005• IRAS Circular dated 30 December 2005• Similar to Malaysian MOF's position• What were the Pre-FRS 139 tax treatments?

‒ Realised vs. unrealised‒ Capital account vs. revenue account‒ For banks, generally, accounting treatment for financial derivatives were accepted

• What are the FRS 139 tax treatments?‒ Alignment between accounting treatment and tax treatment‒ Minimize tax adjustment‒ For non-banks

• Revenue vs capital

• If revenue, taxable/deductible even unrealised

‒ For banks• Mainly on revenue account

‒ Transitional tax rules

© 2008 Deloitte Touche Tohmatsu

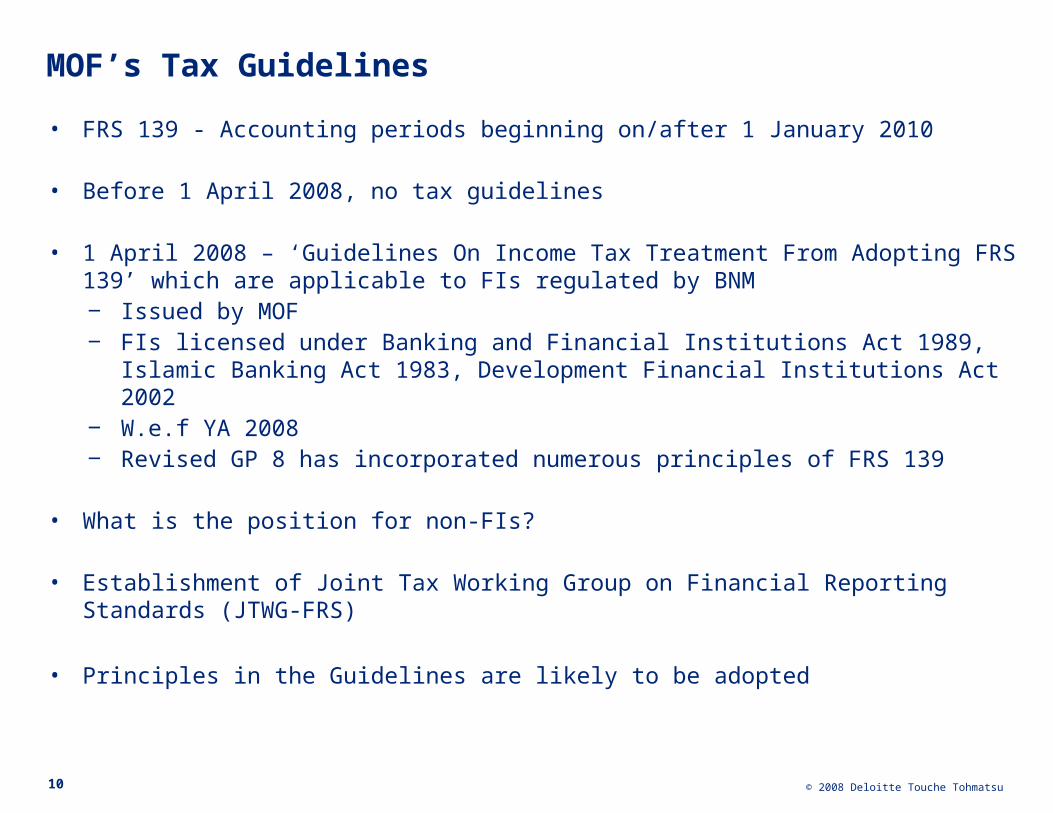

MOF’s Tax Guidelines • FRS 139 - Accounting periods beginning on/after 1 January 2010

• Before 1 April 2008, no tax guidelines

• 1 April 2008 – ‘Guidelines On Income Tax Treatment From Adopting FRS 139’ which are applicable to FIs regulated by BNM‒ Issued by MOF‒ FIs licensed under Banking and Financial Institutions Act 1989, Islamic Banking

Act 1983, Development Financial Institutions Act 2002 ‒ W.e.f YA 2008‒ Revised GP 8 has incorporated numerous principles of FRS 139

• What is the position for non-FIs?

• Establishment of Joint Tax Working Group on Financial Reporting Standards (JTWG-FRS)

• Principles in the Guidelines are likely to be adopted

10

© 2008 Deloitte Touche Tohmatsu

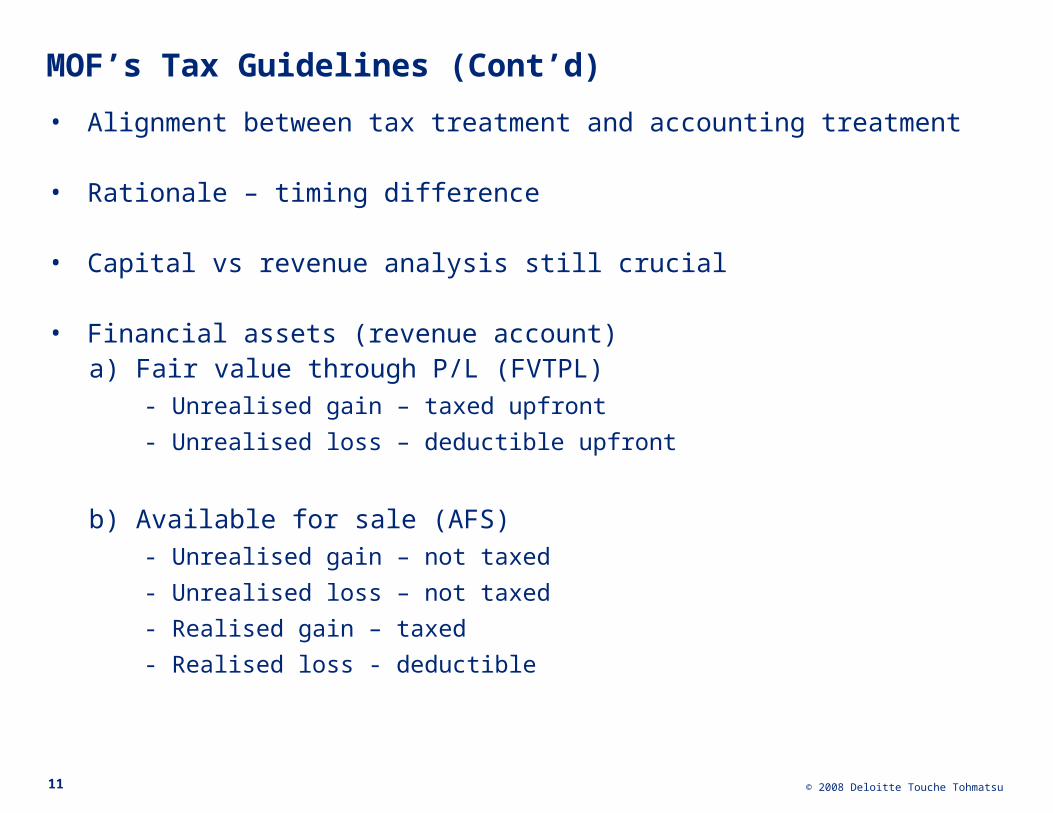

MOF’s Tax Guidelines (Cont’d) • Alignment between tax treatment and accounting treatment

• Rationale – timing difference

• Capital vs revenue analysis still crucial

• Financial assets (revenue account)a) Fair value through P/L (FVTPL)

- Unrealised gain – taxed upfront

- Unrealised loss – deductible upfront

b) Available for sale (AFS)

- Unrealised gain – not taxed

- Unrealised loss – not taxed

- Realised gain – taxed

- Realised loss - deductible

11

© 2008 Deloitte Touche Tohmatsu

MOF’s Tax Guidelines (Cont’d) • Financial assets (revenue account)

• Interest calculated by EIR method taxed (HTM and LAR)

• Impairment losses – deductible

• Financial assets (capital account)• IRB to ascertain what is capital and what is not

• Traditional rules apply‒ Gain – not taxed, even realised!

‒ Loss – not deductible, even realised!

‒ Impairment losses – not deductible

12

© 2008 Deloitte Touche Tohmatsu

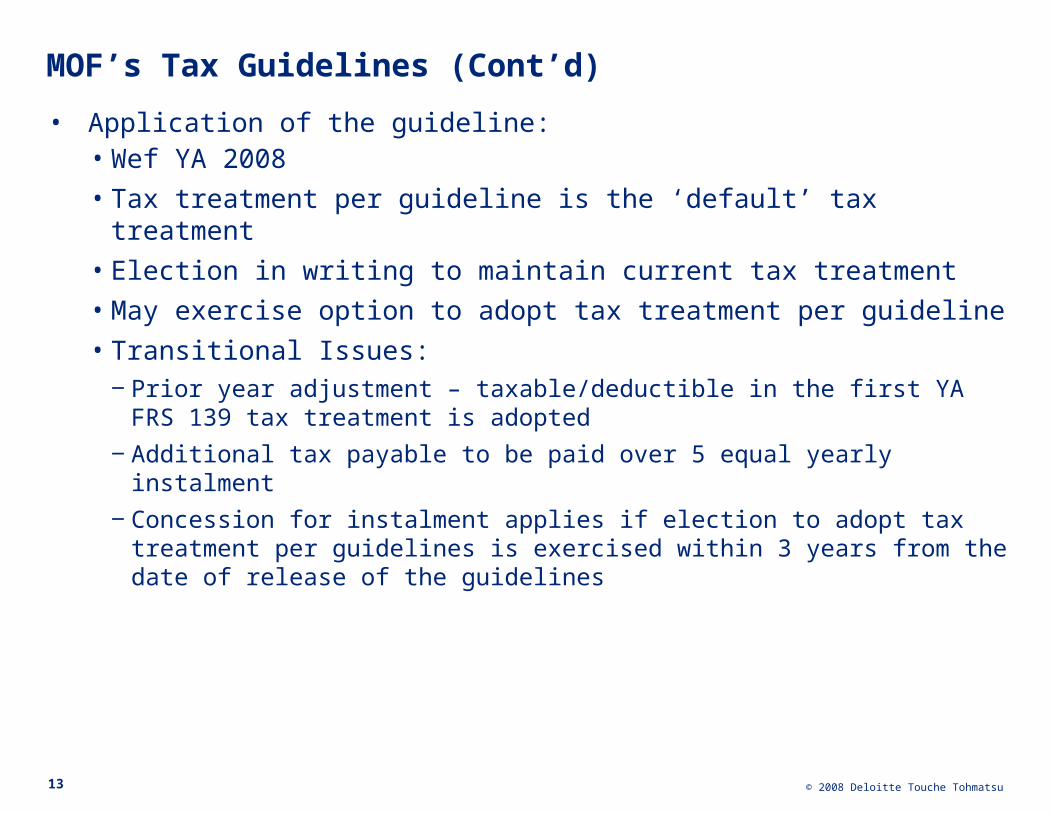

MOF’s Tax Guidelines (Cont’d) • Application of the guideline:

• Wef YA 2008

• Tax treatment per guideline is the ‘default’ tax treatment

• Election in writing to maintain current tax treatment

• May exercise option to adopt tax treatment per guideline

• Transitional Issues:‒ Prior year adjustment – taxable/deductible in the first YA FRS 139 tax treatment is

adopted

‒ Additional tax payable to be paid over 5 equal yearly instalment

‒ Concession for instalment applies if election to adopt tax treatment per guidelines is exercised within 3 years from the date of release of the guidelines

13

© 2008 Deloitte Touche Tohmatsu

Other Issues • Receivables & impairment• Inter-co loan

• Treatment of interest income and interest expense

• Investment/loan balance for tax purposes e.g. Sec 33(2) interest restriction calculation

• Inter-co loan (with no written terms)• Debt vs equity

• Impairment for bad debts – deductible?

14

© 2008 Deloitte Touche Tohmatsu15

Other FRSs – A Quick Tour

© 2008 Deloitte Touche Tohmatsu16

FRS 2 – Share based payment

© 2008 Deloitte Touche Tohmatsu17

Food for thought

“If stock options aren’t a form of compensation, what are they? If compensation isn’t an expense, what is it? And, if expenses shouldn’t go into the calculation of earnings, where in the world do they go?” – Warren Buffett, CEO, Berkshire Hathaway

© 2008 Deloitte Touche Tohmatsu

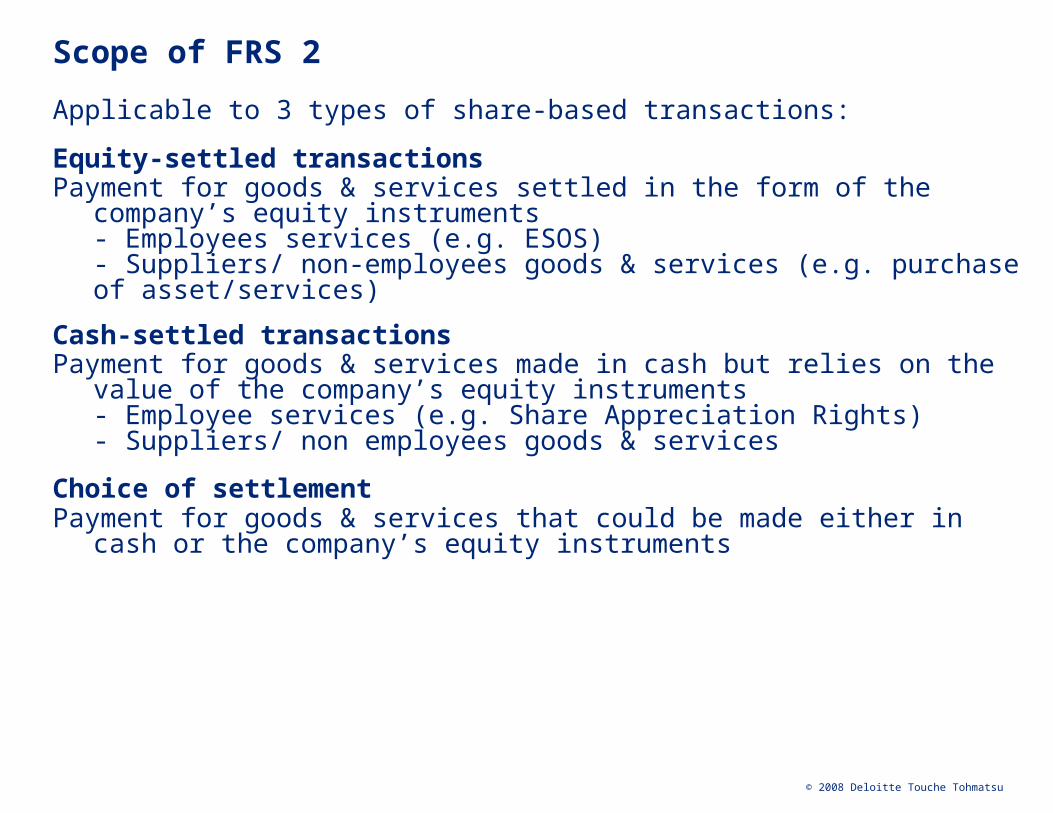

Scope of FRS 2

Applicable to 3 types of share-based transactions:

Equity-settled transactions Payment for goods & services settled in the form of the company’s equity

instruments - Employees services (e.g. ESOS)- Suppliers/ non-employees goods & services (e.g. purchase of asset/services)

Cash-settled transactions Payment for goods & services made in cash but relies on the value of the

company’s equity instruments- Employee services (e.g. Share Appreciation Rights)- Suppliers/ non employees goods & services

Choice of settlementPayment for goods & services that could be made either in cash or the company’s

equity instruments

© 2008 Deloitte Touche Tohmatsu19

Accounting Treatment

Journal entriesJournal entries ValueValue TimingTiming

Equity-settled - Employee services

Dr Staff cost xxx Cr Equity xxx

Fair value of equity instrument granted

Grant date

Tax Issues

1. Is “staff cost” deductible?

2. If affirmative, what is the value?

3. If affirmative, when to claim?

© 2008 Deloitte Touche Tohmatsu20

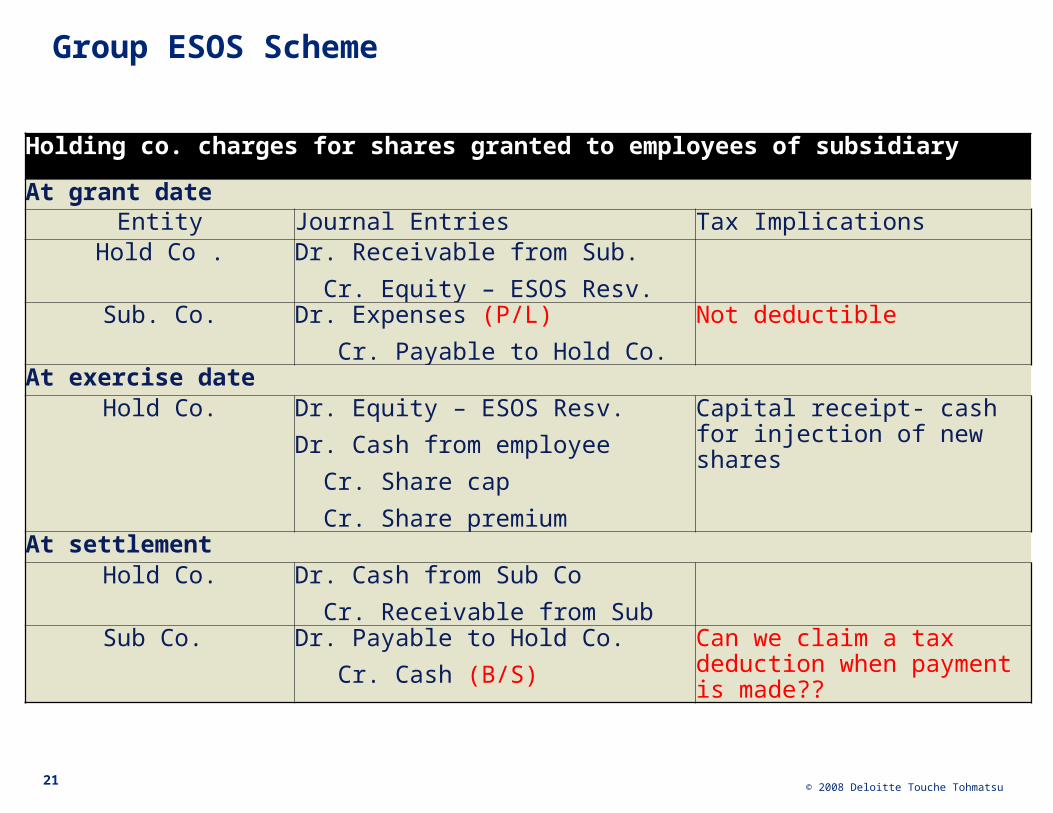

Group ESOS Scheme

With an inter-company charges by Parent Co

A’s Employees

Subsidiary A

US Parent

Share option

Services

© 2008 Deloitte Touche Tohmatsu21

Group ESOS Scheme

Holding co. charges for shares granted to employees of subsidiary

At grant dateEntity Journal Entries Tax Implications

Hold Co . Dr. Receivable from Sub.

Cr. Equity – ESOS Resv.Sub. Co. Dr. Expenses (P/L)

Cr. Payable to Hold Co.

Not deductible

At exercise dateHold Co. Dr. Equity – ESOS Resv.

Dr. Cash from employee

Cr. Share cap

Cr. Share premium

Capital receipt- cash for injection of new shares

At settlementHold Co. Dr. Cash from Sub Co

Cr. Receivable from SubSub Co. Dr. Payable to Hold Co.

Cr. Cash (B/S)

Can we claim a tax deduction when payment is made??

© 2008 Deloitte Touche Tohmatsu22

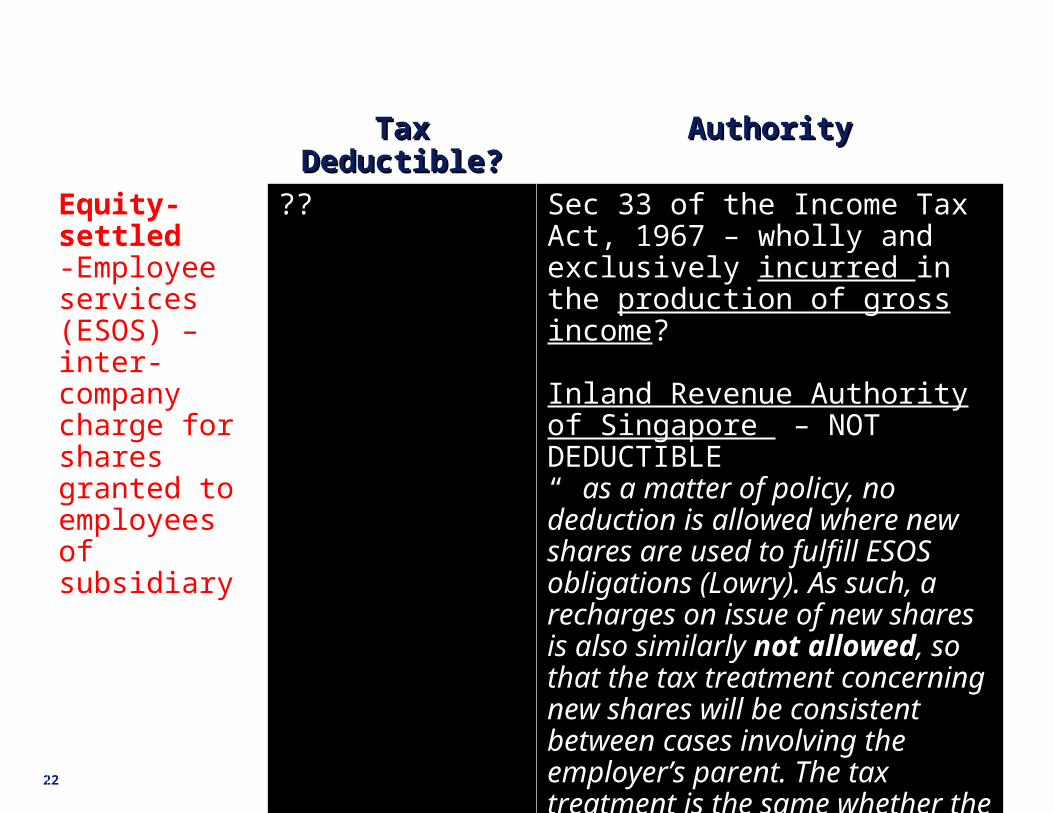

Tax Treatment

Tax Deductible?Tax Deductible? AuthorityAuthority

Equity-settled -Employee services(ESOS) – inter-company charge for shares granted to employees of subsidiary

?? Sec 33 of the Income Tax Act, 1967 – wholly and exclusively incurred in the production of gross income?

Inland Revenue Authority of Singapore – NOT DEDUCTIBLE“ as a matter of policy, no deduction is allowed where new shares are used to fulfill ESOS obligations (Lowry). As such, a recharges on issue of new shares is also similarly not allowed, so that the tax treatment concerning new shares will be consistent between cases involving the employer’s parent. The tax treatment is the same whether the parent is a foreign or Singapore company”

© 2008 Deloitte Touche Tohmatsu23

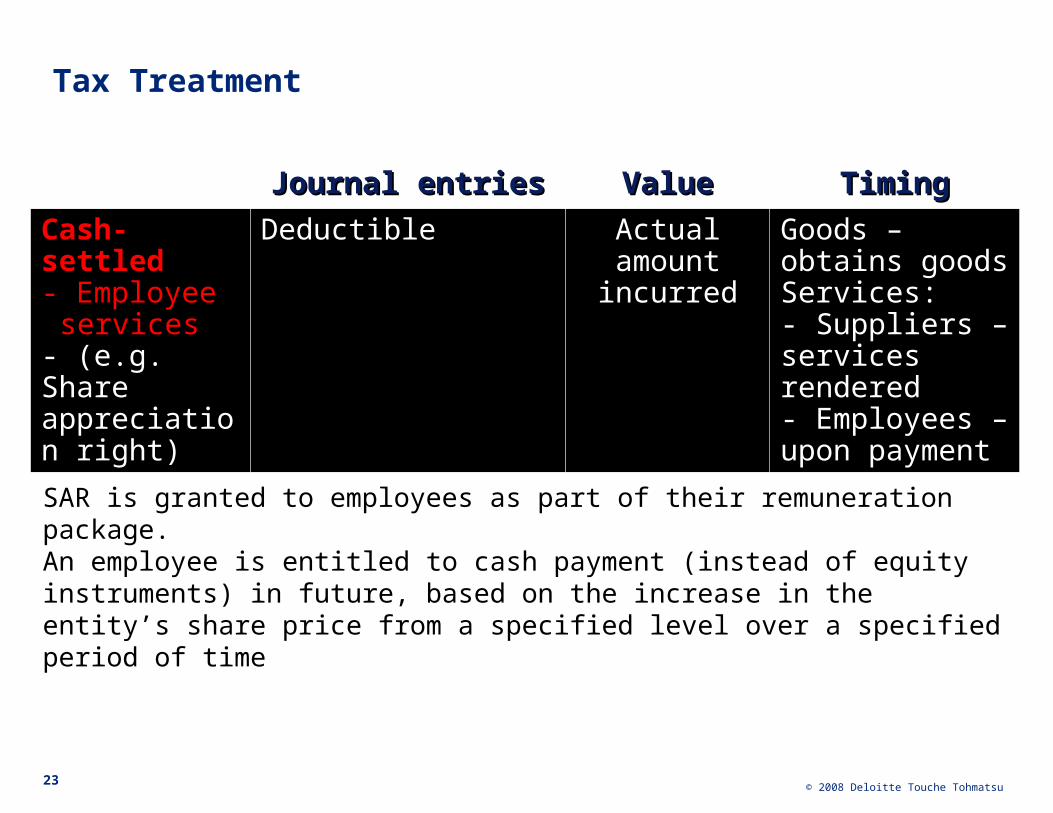

Tax Treatment

Journal entriesJournal entries ValueValue TimingTiming

Cash-settled- Employee services- (e.g. Share appreciation right)

Deductible Actual amount incurred

Goods – obtains goodsServices:- Suppliers – services rendered- Employees – upon payment

SAR is granted to employees as part of their remuneration package.An employee is entitled to cash payment (instead of equity instruments) in future, based on the increase in the entity’s share price from a specified level over a specified period of time

© 2008 Deloitte Touche Tohmatsu

Implications of recognising ESOS costs

• Cost of ESOS recognised as expense in P &L – impacts accounting profits

• However cost of ESOS not tax deductible

• Effective tax rate increases

• Impacts earnings-per-share (EPS)

• Comparability of EPS distorted

• ESOS cost is a real economic cost – contractual and in recognition of the employees contribution

• Singapore: deduction only available for treasury shares, purchase price of the treasury shares LESS grant price)

© 2008 Deloitte Touche Tohmatsu25

Summary of potential tax treatments

• Equity settled share based payments to suppliers for goods and services is deductible

• Cash settled share based payments (suppliers & employees) is deductible upon actual cash settlement

• Equity share based payments to employees (ESOS), not tax deductible save for a situation where there actual cost is incurred in acquiring the options (e.g. treasury shares in Singapore and parent issued options to subsidiary employees for a consideration).

• Recharges from parent may not be tax deductible if Singapore’s treatment is followed

• Keep adequate documents to substantiate tax deduction claim, primarily to prove the value

• Keep proper schedules in the tax computation to monitor movement

© 2008 Deloitte Touche Tohmatsu26

FRS 5 - Non-current assets held for sale and discontinued operations

© 2008 Deloitte Touche Tohmatsu27

• Non-current asset whose carrying amount will be recovered principally through a sale transaction rather than through continuing use

• Non-current asset to be classified as HFS if:- Available for immediate sale in its present condition

• Its sale must be highly probable – Management commitment to sell– Active programme to locate a buyer (advertisement)– Sale to be completed within 1 year

• It must be genuinely sold, not abandoned

• To be classified as HFS, above conditions must be met at balance sheet date

FRS 5 – Non-current asset held for sale (HFS)

© 2008 Deloitte Touche Tohmatsu28

Held for Sale – Presentation & Disclosure

Balance Sheet (extract) 20x6 20x5ASSETSNon-current assets XX XXCurrent assetsTrade receivable xx xxNon-current assets classified as HFS xx xxTotal assets XX XXEQUITY & LIABILITIESEquity attributable to equity holders of parentShare capital xx xxAmounts recognised directly in equity relatingto non-current assets held for saleTotal equity XX XXNon-current liabilities XX XXCurrent liabilitiesLiabilities directly associated with non-current assets classified as held for sale xx xxTotal liabilities XX XX

© 2008 Deloitte Touche Tohmatsu29

FRS 5 Non-current assets held for sale

Tax ImplicationsFRS 5 Tax Implication

Non-current assets classified as HFS Deemed disposal? Compute BA/BC? ITA definition of disposal (Para 61*)

Asset continued to be used, temporary disuse No deemed disposal – continue to claim CA ?**

Disposal value Para 62: Market Value?***

* Para 61, Schedule 3 – “Any plant or machinery which is used for the purposes of a business and in respect of which qualifying expenditure has been incurred is disposed of within the meaning of this Schedule if it is sold, discarded or destroyed or if it ceases to be used for the purposes of that business”

** Para 56, Schedule 3 – “For the purposes of this Schedule, an asset which is temporarily disused in relation to a business of a person shall be deemed to be in use for the purposes of the business if it was in use for the purposes of the business immediately before becoming disused and if during the period of disuse it is constantly maintained in readiness to be brought back into use for those purposes”

*** Para 61, Schedule – “Subject to subparagraph (2), for the purposes of this Schedule, where an asset is disposed of by a person, its disposal value shall be taken to be an amount equal to its market value at the date of its disposal or, in the case of its disposal by way of sale, transfer or assignment..”

What is the tax treatment if asset HFS is reclassified as non-current asset (in use)?

© 2008 Deloitte Touche Tohmatsu30

Other FRSs

© 2008 Deloitte Touche Tohmatsu31

• FRS 121 – The Effects of Changes in Foreign Exchange Rates- Foreign currency, functional currency and presentation currency

• FRS 108 – Accounting Policies, Changes in Accounting Estimates & Errors

• FRS 116 – Property, Plant and Equipment

• Etc

Other FRSs

© 2008 Deloitte Touche Tohmatsu32

• Adoption of FRS has tax implications

• Joint Tax Working Group on Financial Reporting Standards (JTWG-FRS) to expedite effort

• Tax authorities to be lenient in the earlier years

• Overall objective: Alignment between accounting treatment and tax treatment

The Way Forward

© 2008 Deloitte Touche Tohmatsu33

Related Documents