Original Article The imbalance of capitalisms in the Eurozone: Can the north and south of Europe converge? Aidan Regan Co-director Dublin European Institute, School of Politics and International Relations, University College Dublin (UCD), Ireland. E-mail: [email protected] Abstract The European response to the sovereign debt crisis has exposed a tension between the national and the supranational in a multilevel polity while opening up new political cleavages between the north and south of the Economic and Monetary Union (EMU). This dilemma has become particularly acute for programme countries that were either directly or indirectly in receipt of non-market financial fundingfrom the troika. Drawing upon a new international political economy approach to comparative political economy, this article argues that joining together two distinct macroeconomic growth regimes is the real source of the euro crisis: domestic demand-led models, which pre- dominate in southern Europe, and export-led models, which dominate the landscape of northern Europe. European policymakers assume that all member states can converge on an export-led model of growth. This vision of convergence is exacerbating rather than resolving the imbalance of capitalisms at the heart of the Eurozone. Comparative European Politics advance online publication, 2 March 2015; doi:10.1057/cep.2015.5 Keywords: comparative political economy; varieties of capitalism; Eurozone crisis Introduction The European response to a financial cum sovereign debt crisis in a currency union without a centralized fiscal treasury or political government is an experiment in crisis management. It has exposed a tension between the national and the supranational in a multilevel polity. No level of this multilevel governance system has the policy instruments to solve the crisis. Monetary policy remains supranational (that is, European) across 19 national governments with diverse fiscal, welfare state and labour market regimes (see Höpner and Schäfer, 2010; Scharpf, 2011). These countries have conflicting interests in terms of who should bear the burden of adjustment. For the sake of argument, we can identify this as a tension between © 2015 Macmillan Publishers Ltd. 1472-4790 Comparative European Politics 1–22 www.palgrave-journals.com/cep/

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Original Article

The imbalance of capitalisms in the Eurozone:Can the north and south of Europe converge?

Aidan ReganCo-director Dublin European Institute, School of Politics and International Relations, University CollegeDublin (UCD), Ireland.E-mail: [email protected]

Abstract The European response to the sovereign debt crisis has exposed a tensionbetween the national and the supranational in a multilevel polity while opening up newpolitical cleavages between the north and south of the Economic and Monetary Union(EMU). This dilemma has become particularly acute for programme countries that wereeither directly or indirectly in receipt of non-market financial fundingfrom the troika.Drawing upon a new international political economy approach to comparative politicaleconomy, this article argues that joining together two distinct macroeconomic growthregimes is the real source of the euro crisis: domestic demand-led models, which pre-dominate in southern Europe, and export-led models, which dominate the landscape ofnorthern Europe. European policymakers assume that all member states can converge onan export-led model of growth. This vision of convergence is exacerbating rather thanresolving the imbalance of capitalisms at the heart of the Eurozone.Comparative European Politics advance online publication, 2 March 2015;doi:10.1057/cep.2015.5

Keywords: comparative political economy; varieties of capitalism; Eurozone crisis

Introduction

The European response to a financial cum sovereign debt crisis in a currency unionwithout a centralized fiscal treasury or political government is an experiment in crisismanagement. It has exposed a tension between the national and the supranational in amultilevel polity. No level of this multilevel governance system has the policyinstruments to solve the crisis. Monetary policy remains supranational (that is,European) across 19 national governments with diverse fiscal, welfare state andlabour market regimes (see Höpner and Schäfer, 2010; Scharpf, 2011). Thesecountries have conflicting interests in terms of who should bear the burden ofadjustment. For the sake of argument, we can identify this as a tension between

© 2015 Macmillan Publishers Ltd. 1472-4790 Comparative European Politics 1–22www.palgrave-journals.com/cep/

creditor and debtor countries, or between the core and periphery of the Economic andMonetary Union (EMU) in Europe.

EMU member states currently have limited policy discretion to pursue anautonomous response to the crisis. In the absence of exchange rate or interest rateadjustment, the entire burden of adjustment must fall on domestic prices and wages.In effect, membership of the EMU means that national governments only have onepolicy instrument at their disposal: internal devaluation and structural reforms of thelabour market (Buti and Carnot, 2012; Armingeon and Baccaro, 2012a). From apolitical perspective, national governments must comply with the external mandatesof EMU membership by reducing their budget deficit to 3 per cent of GDP.The negative impact this has on employment is legitimated by the economic assum-ption that labour cost competitiveness and export-led recovery is the only way togenerate the conditions for economic growth. To achieve this, national governmentsare being encouraged to impose structural reforms in product and labour markets as ameans to enhance cost competitiveness. It is this assumption that supply-sidestructural reforms will lead to a convergence in export-led growth models acrossdifferent national models of capitalism that I challenge in this article.

To do this I draw upon and re-configure the core variables of the varieties ofcapitalism (VoC) theory in the study of comparative political economy, and proposea new framework based on macroeconomic growth regimes. I argue that thedomestic organization of different political economies in the north and south ofthe Eurozone has interacted with transnational European monetary policy to producedivergent economic and employment growth patterns since the establishment ofthe EMU. The causal source of the economic crisis was the attempt to join togethertwo distinct models of growth, domestic demand (south) and export led (north), intoa single currency while failing to account for the asymmetric effects this wouldproduce. The decline in competitiveness associated with current account imbalanceswas a logical consequence of Monetary Union. Northern European countries, I argue,are built around political coalitions and institutions that are conducive to an export-driven growth regime. Southern European countries, on the other hand, areinstitutionally conducive to growth models based around domestic consumption inthe non-tradable sectors of the economy (Johnston, 2012).

In this sense, the article critiques the narrow focus on cost competitiveness andmanufacturing in comparative political economy and proposes to analyse the ‘core’and ‘peripheral’ countries of the EMU as interconnected regions within a structurallyimbalanced currency union. It is an international case study on what happens whendiverse capitalist democracies with distinct growth models are integrated into, andsubsequently attempt to adjust in, a currency union without a centralized federalgovernment. In this regard, I push the VoC theory to its logical conclusion and arguethat if member states of the EMU operate according to their own distinct political andinstitutional logic (in my framework, conflicting macroeconomic growth regimes)then it is questionable whether some member states should remain in the Eurozone.

Regan

2 © 2015 Macmillan Publishers Ltd. 1472-4790 Comparative European Politics 1–22

The EMU needs a variegated response to the crisis that provides the flexibility formember states to carve out an autonomous economic and employment growthstrategy at the national level. If this is not forthcoming then it is perfectly rational forsome member states to consider leaving the euro, particularly those countries that arenot in a position to compete in international export markets. The remainder of thearticle is structured as follows. First, I outline a new VoC theoretical framework thatanalyses the EMU as a political economy with two interactive macroeconomicgrowth regimes that have become incompatible under monetary union: domesticdemand and export led. Second, using this framework, I trace the origins of theEurozone crisis to capital inflows that financed current account imbalances betweenthese growth regimes. Third, I detail the policy response of ‘internal devaluation’ indemand-led growth regimes in southern Europe, and the question as to whetherexternal competitiveness is the core problem facing these countries. Fourth, I analysethe political consequence of this one-sided adjustment for European integration.

The Diversity of Capitalist Democracies in the Eurozone

The central research finding in comparative political economy over the past 20 yearsis that what governments do is conditioned by the structure of the political economy.According to Hall and Soskice (2001), the organization of a country’s politicaleconomy includes the structure of corporate governance, industrial relations, finance,social protection, the labour market, education and training (Hassel, 2012). Therelations within these subsectors and their historical evolution over time producedifferent economic systems with distinct variants of comparative advantage. From apolitical science perspective, the underlying political coalitions of these institutionscondition the type of public policy choices that governments are likely to pursue intimes of economic crisis and growth (see Hay, 2004; Hall, 2012a).

In the Eurozone, one can argue that there are two variants of capitalism. NorthernEuropean countries, such as Germany, the Netherlands, Austria and Finland, are oftendescribed as coordinated market economies (CMEs). They have centralized unions andemployers with the capacity to autonomously coordinate collective bargaining andlabour market outcomes. In addition, they have embedded welfare state traditionscommitted to social protection and income security. They have traditionally reliedupon export-led economic growth as a mechanism to generate employment. Hence,their macroeconomic structure supports a preference for stable fiscal policies andsupply-side labour market reforms (Iverson and Soskice, 2013).

On the other hand, southern European countries in the Eurozone, Spain, Italy,Greece, Portugal and Cyprus, are often described as Mediterranean VoC (see Hayand Wincott, 2012 for a detailed analysis of welfare regimes). They have fragmentedtrade unions and employers with limited capacity to autonomously coordinatecollective bargaining and labour market outcomes. They have weak welfare states,

The imbalance of capitalisms in the Eurozone

3© 2015 Macmillan Publishers Ltd. 1472-4790 Comparative European Politics 1–22

and a significant amount of social security occurs through family relations.Traditionally, they have generated economic growth through domestic demand. Thisgives priority to wages, and consumer spending, over profit-generation in exportmarkets. Before the EMU, this organizational structure lent itself to an accommodat-ing monetary and fiscal policy, with governments regularly devaluing the currency tooffset a loss of competitiveness and the inflationary impact of a rapid increase indomestic prices. Wealth is often held in fixed assets such as property, and corporategovernance is dependent on close business relations among family-run firms.

This article hypothesizes that the attempt to join together these two distinctcapitalist growth regimes into a single currency is the real source of the Eurozonecrisis. Before monetary union these models of growth could co-exist without pro-ducing external imbalances between one another, but not afterwards (see Figure 1).The organization of the political economy in southern Europe is conducive to agrowth model based on domestic consumption and high inflation. In contrast, theorganization of the political economy in northern Europe is conducive to a growthmodel based on export market, and low inflation. Both of these regimes, however,became systematically connected through the single currency. That is, the strongexport base of northern Europe required high levels of domestic consumption in thesouth, which was largely funded through the capital account and external lending.In VoC theory, most research was focused on the supply-side coalitions that benefit

-10

-5

0

5

1980 1990 2000 2010 1980 1990 2000 2010

Current Account Net External Lending

North South (w/o Greece)South (w/ Greece)

Year

Cur

rent

Acc

ount

/Ext

erna

l Net

Len

ding

Bal

ance

(% o

f GD

P)

Figure 1: External balances between the EMU’s domestic demand and export-led economies (1980–2014).Note: Northern economies include Austria, Belgium, Finland, France, Germany and the Netherlands.Southern economies include Greece, Ireland, Italy, Portugal and Spain.Source: European Commission’s Directorate General for Economic and Financial Affairs (2014), adaptedfrom Alison Johnston and Aidan Regan (forthcoming).

Regan

4 © 2015 Macmillan Publishers Ltd. 1472-4790 Comparative European Politics 1–22

MNC firms in the export-oriented manufacturing sectors of northern Europe, nothow they affected domestic consumption or service expansion in the non-tradedsectors (Johnston and Regan, forthcoming).

These asymmetries (reflected in Figure 1) can only be observed by adopting aninternational political economy (IPE) perspective and examining member states ofthe EMU as integrated regions in a euro-financial market. The EMU is a semi-closedeconomy area with less than 10 per cent of trade leaving the Eurozone andpredominately going to other countries in the EU. The EMU was designed as anunaccommodating currency regime that provided unprecedented autonomy to theEuropean Central Bank (ECB). This primarily benefited the export-driven model ofnorthern Europe. But as will be shown in the empirical sections (‘The consequence:Creditor and debtor bargaining in Europe’ and ‘Discussion: Rethinking the politicaleconomy of European integration’) it also generated unprecedented outflows ofcapital from the core economies of the Eurozone, fuelling domestic consumption inthose regions that previously relied upon domestic demand to generate economic andemployment growth. The dominant causal explanation for the current accountimbalances is a loss of competitiveness measured in unit labour costs or the pricedeflator. What is not acknowledged is that the institutional factors that created theseimbalances were a consequence of monetary union. Hence, focusing on externalcompetitiveness and unit labour costs misdiagnoses the problem and cure.

To explain the disequilibria between northern and southern regions of theEurozone, I subsume fiscal, wage and monetary policies to create a two-dimensionaltypology of macroeconomic growth models (see Table 1). This leads to a distinctionbetween the domestic consumption and profit-export-oriented countries within theEMU, which directly corresponds to the previously ‘hard’ and ‘soft’ currencyregimes of Europe. Northern export-driven countries have long given up theinstruments of monetary policy to stabilize their currencies. This is not the case forsouthern Europe. Upon entry to the EMU it was assumed that these high-inflationcountries would converge on the stability-oriented macroeconomic policies ofnorthern Europe. It was assumed that convergence would take place through theinterest-rate price mechanism. As will be shown in the next section, the total oppositeoccurred. Their macroeconomic regimes diverged (buyers and sellers of money with

Table 1: Macroeconomic growth Regimes in the EMU

North South

Currency Hard – low inflation Soft – high inflationMonetary Stability-oriented Adjustable-orientedFiscal Counter-cyclical Pro-cyclicalLabour Corporatist Non-corporatistMacroeconomic Profit export Domestic demandEurozone Interdependence of financial banking institutions in both regimes

The imbalance of capitalisms in the Eurozone

5© 2015 Macmillan Publishers Ltd. 1472-4790 Comparative European Politics 1–22

a single interest rate) and trade imbalances widened. Internal demand, previously fedby wage increases, was now sustained by a decline in interest rates and debtaccumulation.

But who exactly is responding to the monetary impulses associated with the singlecurrency, and through what process do domestic institutions shape the strategy ofthese actors in reinforcing a growth regime based on either consumption or exports?In the traditional VoC framework it is the rational expectations of individual firms.In my framework it depends upon the producer group coalitions and the extent towhich these are anchored in the export or non-tradable sectors of the economy(see Schmidt, 2002, for a similar argument on the role of the state in shapingEuropean VoC). I consider the strategies that these political coalitions pursue anoutcome of the growth regime (Johnston and Regan, 2014).

I will now use this framework to empirically analyse the systemic origins of theEurozone crisis before analysing the impact and consequences for decision making inthe EMU. The article concludes with a discussion on the imbalance of capitalismswithin the Eurozone. Cases are selected on the basis of their growth regime. In thisarticle, I use the terms ‘core’, ‘Northern’ and ‘export-led models’ interchangeably todescribe the EMU economies that have emerged from the crisis unscathed (Austria,Belgium, Finland, Germany, the Netherlands and to a lesser degree France).Likewise, I use the terms ‘periphery’, ‘Southern’ and ‘domestic demand-drivenmodels’ to describe EMU countries that have come under crisis (Greece, Italy,Portugal, Spain and to a lesser extent Ireland).

The Origins: Cheap Money

The Eurozone is composed of 19 linguistically diverse countries and has acombined population of 317 million people. It has a GDP of €9.4 trillion andaccounts for 14.6 per cent of global trade (the second largest in the world). Beforethe crisis, only 10 per cent of this actually left the Eurozone, and predominatelywent to other EU countries. This means that the Eurozone, in effect, is a semi-closed trading economy (see De Grauwe and Ji, 2012). A gain in competitivenessfor one country, by definition, can only come at the expense of another country.The implication is that trade has become a zero-sum game among nineteennation-states sharing the same currency. Unless a country can gain in market shareoutside the euro area it will come at the expense of another EMU partner. This hasexposed a horizontal political tension between the member states of the EMU.Germany accounts for over 26.7 per cent of Eurozone GDP, and is by far thelargest exporter from the trading area. Given its economic resources, it is a rulemaker rather than a rule taker when designing the policies of the EMU. From amacroeconomic perspective, fiscal reflation in a closed economy will stimulate

Regan

6 © 2015 Macmillan Publishers Ltd. 1472-4790 Comparative European Politics 1–22

aggregate demand. But this Keynesian policy assumes that the closed economy isgoverned by a homogenous nation-state.

The core problem at the heart of the Eurozone crisis is a structural imbalancebetween export-led economies with current account surpluses (Germany, theNetherlands, Austria and Finland) and countries with current account deficits (Italy,Spain, Greece, Portugal and occasionally Ireland) that emerged directly after theestablishment of the EMU in 2000 (see Figure 1). These divergent trends are usuallytaken to illustrate the underperformance and loss of competitiveness by the ‘GIIPS’(Greece, Ireland, Italy, Portugal and Spain) countries in the Eurozone, and werecentral to the establishment of the new EU Commission ‘macroeconomic scorecard’in 2011, and subsequent economic reforms (see De la Porte and Heins, 2014).

The indicators in the new euro economic governance regime are firmly focused onhow to improve the balance of payments for debtor countries, through holding downunit labour costs. This, by definition, promotes competition in wages among memberstates as a strategy for economic development. Coordinated wage restraint bycentralized unions and employers, made possible by domestic institutions, iscertainly one of the core factors in explaining the export-oriented strategy of smallopen economies in Europe (Höpner and Lutter, 2014). Germany, despite its size, isperhaps the best example of this. But from the perspective of the EMU as a whole,what this approach to wage competition fails to appreciate is the negative impact ithas on the exporting capacity of other countries sharing the same currency. This is allthe more problematic if we accept that within the Eurozone there are two differentmacroeconomic growth models in the north and south: export profit and domesticconsumption. In this context, holding down wages in a semi-closed trading areanegatively affects all member states, but particularly those southern Europe countriesdependent on domestic demand.

The divergence in net international investment positions outlined in Figure 2 illustratesthat from 2000 to 2008 southern European countries imported more than they exported,thereby funding the current account imbalances highlighted in Figure 1. Capital flew outof countries where exports exceeded imports, such as Germany, to purchase assetslocated in countries with increased domestic demand (Greece, Ireland, Portugal andSpain), fuelling domestic prices through either private sector house price booms or publicsector spending. Since 2000, Germany’s current account surplus (€192.2 billion) hasbeen identical to the combined current account deficit of Greece, Italy, Portugal andSpain (DeGrauwe, 2013). This export of capital meant that these deficit countries becameindebted to surplus countries, with the implication that their economies become heavilyreliant on external credit to fuel domestic demand.

This change in the net international investment position was made possible by aone-size-fits-all monetary policy by the ECB and a single interest rate that madecheap credit widely available for rising domestic consumption. Hence, the currentaccount imbalances occurred because private banks in some member states (and thepublic sector in Greece) took advantage of negative interest rates, and the absence of

The imbalance of capitalisms in the Eurozone

7© 2015 Macmillan Publishers Ltd. 1472-4790 Comparative European Politics 1–22

exchange rate restrictions, and began borrowing excessively on the European moneymarkets for domestic consumption. VoC theorists failed to analyse this financialrelation because it was focused on the domestic exporting strategies of manufactur-ing firms, which predominately applied to northern CME countries. Therefore, theymissed the deep asymmetry of European monetary integration that was emerging.

The myth of market convergence

The increase in capital inflows from the core to the periphery is precisely what thepolitical leaders who signed up to the EMU wanted and got from the single currency(see Moravcsik, 1998, for a formal account). For Germany, it provided an anchor fora stable exchange rate that would benefit its export-driven model within Europe. Itremoved the volatility of exchange rate fluctuations and the ability of its tradingpartners to devalue their currencies relative to the Deutschmark. It provided anintegrated European finance market that was highly profitable for German banks.

-140

-120

-100

-80

-60

-40

-20

0

20

40

60

Germany Netherlands Portugal

Spain Greece

Figure 2: Net international investment as percentage of GDP.Source: European Commission’s Directorate General for Economic and Financial Affairs (2014).

Regan

8 © 2015 Macmillan Publishers Ltd. 1472-4790 Comparative European Politics 1–22

France, on the other hand, feared the economic might of German reunification, andsought a tool that would generate the conditions for a federal Europe that woulddecrease rather than increase the power of German money. For Ireland, Italy, Spain,Greece and Portugal, the EMU would reduce the cost of borrowing and facilitatecapital inflows for national investment. According to Moravcsik (2012), all thesecountries got what they wanted. This was less a case of economic calculation thandistributional politics. The critical mistake was that European policymakers assumedthat a convergence in ECB market interest rates, in addition to strict fiscal policies tobe embedded in the Growth and Stability Pact, would provide the conditions for aninstitutional convergence in business cycles across diverse capitalist democracies inthe Eurozone. This failed to account for the fact that sensitivity to interest rates variesaccording to domestic demand and the propensity to import in each member state.

The assumption of institutional convergence was not present in the negotiationsthat led to the European Monetary System in the late 1970s. During this period therewere competing perspectives between the ‘monetarists’ and the ‘economists’ (seeMourlon-Druol, 2012). Policymakers were deeply concerned about the real exchangerate and the inflation differentials that existed between northern and southern Europeancountries, as outlined in Table 2. Absent national central banks and the capacity toactively target the nominal exchange rate, monetary union would exacerbate thesedifferentials. It was for this reason that the German Chancellor, Helmut Schmidt,

Table 2: Nominal exchange rate changes and inflation averages for growth regimes in the EMU11

Average annual change in thenominal exchange rate

Average annual changein inflation

1980s (%) 1990–1998 (%) 1980s 1990–1998 (%)

Austria 2.41 1.40 3.84 2.61Belgium −0.56 1.33 4.90 2.26Finland 1.43 −1.27 7.32 2.24Germany 2.89 2.00 2.90 2.73The Netherlands 1.84 1.32 3.00 2.60Export-led average 1.60 0.96 4.39 2.49Greece −11.67 −4.83 19.50 12.05Italy −2.41 −1.45 11.20 4.38Portugal −8.83 −0.87 17.35 6.59Spain −2.34 −1.57 10.26 4.44Domestic demand-led average −6.31 −2.18 14.58 6.87France −1.69 1.92 7.38 2.06Ireland −1.33 0.50 9.34 2.39Oscillating demand/export economies average −1.51 1.21 8.36 2.23

Note: Data from Johnston and Regan (forthcoming) taken from EU KLEMS (2010) European Commis-sion’s Directorate General for Economic and Financial Affairs (2014).

The imbalance of capitalisms in the Eurozone

9© 2015 Macmillan Publishers Ltd. 1472-4790 Comparative European Politics 1–22

refused to accept a shared currency until there was real convergence in fiscal policyregimes and a commitment to coordinated wage restraint in the labour market.

The monetarists, who ultimately triumphed after Maastricht, argued that monetaryunion itself would lead to economic convergence and eventually a political union inEurope. It was assumed that a single interest rate in finance markets would lead tomarket convergence, but only if the ECB was constructed in the image of theBundesbank, and complemented with strict fiscal rules to be imposed on membercountries. A deeper analysis, reflecting much economic literature on rationalexpectations, argued that ‘supply side structural reforms’ in product and labourmarkets are what will really drive institutional convergence (see Hall, 2012a, b).Countries that implemented supply-side structural reforms aimed at liberalizing theirlabour markets would generate the conditions for wage flexibility, and thereforedevelop the capacity to adjust the price of their economies in the aftermath of anasymmetric shock. This is the economic idea that underpins the European response tothe crisis today (see Rosamond, 2002, for a more in-depth analysis on the discourseof competitiveness in European economic policymaking).

The problem with the assumption of rational expectations, however, is that it ignores thefact that most euro countries are demand-led. The structural adjustment programmes insouthern Europe are premised on the assumption that if governments reduce the welfarestate, decentralize collective bargaining and flexibilize the labour market they willeventually generate the conditions to compete with the German export model ininternational markets. It is certainly true that Germany introduced deeply contestedstructural reforms in the post-EMU era (usually captured under the ‘Hartz reforms’),which created significant political turmoil for both SPD- and CDU-led coalitions. In thisregard, Germany has the legitimacy to prescribe structural reforms as a panacea for theeconomic and employment crises in southern Europe. But it would be a mistake to assumethat these liberalizing reforms are the ultimate reason behind the competitive resilience ofthe German economy. CMEs have the strategic capacity to carve out an autonomousresponse and develop an export-led strategy to complement the monetary constraints of theEMU. Southern European countries do not have this institutional capacity for export-ledgrowth (see Storm and Naastepad, 2014 for a discussion on Eurozone trade).

Hence, while divergent current account imbalances within the EMU certainlyindicate the different long-term growth potential of southern and northern Europeaneconomies, and therefore their capacity to pay off debt and achieve lower interestrates on government bonds, they primarily reflect two different macroeconomicgrowth regimes (consumption and exports) that became systematically connectedthrough the European financial market. Deficit countries (in the private and publicsector) borrowed cheap money from surplus countries to feed domestic demand. Thismay or may not have crowded out their export sectors. But given that the Eurozone isa semi-closed trading economy, it would have been systematically impossible for allcountries to pursue a German export strategy. Each country, for a period, benefitedfrom the import–export exchange. This is precisely what the policymakers of the

Regan

10 © 2015 Macmillan Publishers Ltd. 1472-4790 Comparative European Politics 1–22

EMU had intended. However, they did not achieve their expected institutionalconvergence in the export organization of national political economies across eachmember state.

The Impact: Divergence and Debt

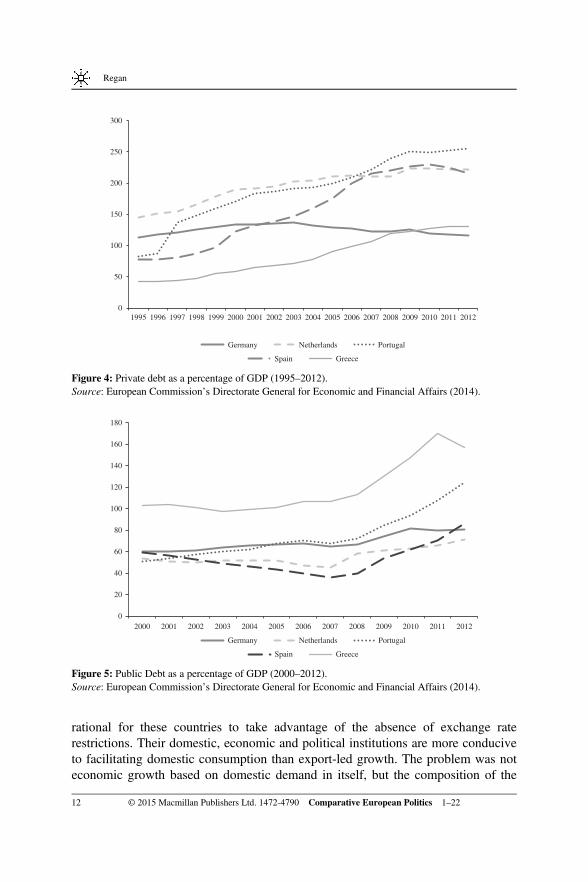

The outcome of joining together these qualitatively distinct growth regimes was thatpost-EMU demand-led European countries experienced a credit boom, fuellingdivergent and uncoordinated business cycles (see Figure 3 on credit flows). Investorsthrew their money at risky investments, leading to asset price bubbles andsubsequently private sector debt (see Figure 4). The euro currency as an isolatedvariable did not cause this, but it made some member states extremely vulnerable tofinancial markets and a sudden stop in capital inflows. This is precisely whathappened to Ireland and southern Europe from 2008 to 2012 (Lane, 2012). In theEurozone, countries experiencing a boom in domestic demand borrowed excessivelyfor either private or public spending. The outcome was strong economic andemployment growth in the domestic economy. This provided national governmentswith unprecedented fiscal resources to satisfy the political-distributional demands oftheir electorates. Hence, the real impact of the EMU was not macroeconomicconvergence but an explosion in cross-border capital flows, cheap credit and aninevitable rise in monetary debt cross the previous soft currency regimes (seeFigures 4 and 5). None of the peripheral countries had the policy tools to control theawesome power of cheap money. But from a VoC perspective it was perfectly

-10

-5

0

5

10

15

20

25

30

35

40

Germany Netherlands Portugal

Spain Greece

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Figure 3: Private credit flows as a percentege of GDP (1995–2012).Source: European Commission’s Directorate General for Economic and Financial Affairs (2014).

The imbalance of capitalisms in the Eurozone

11© 2015 Macmillan Publishers Ltd. 1472-4790 Comparative European Politics 1–22

rational for these countries to take advantage of the absence of exchange raterestrictions. Their domestic, economic and political institutions are more conduciveto facilitating domestic consumption than export-led growth. The problem was noteconomic growth based on domestic demand in itself, but the composition of the

0

50

100

150

200

250

300

Germany Netherlands Portugal

Spain Greece

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Figure 4: Private debt as a percentage of GDP (1995–2012).Source: European Commission’s Directorate General for Economic and Financial Affairs (2014).

0

20

40

60

80

100

120

140

160

180

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Germany Netherlands Portugal

Spain Greece

Figure 5: Public Debt as a percentage of GDP (2000–2012).Source: European Commission’s Directorate General for Economic and Financial Affairs (2014).

Regan

12 © 2015 Macmillan Publishers Ltd. 1472-4790 Comparative European Politics 1–22

investments that were made. In Ireland and Spain the banking sector invested cheapmoney in the commercial and housing mortgage markets, leading to an asset-priceboom (Dellepiane and Hardiman, 2012).

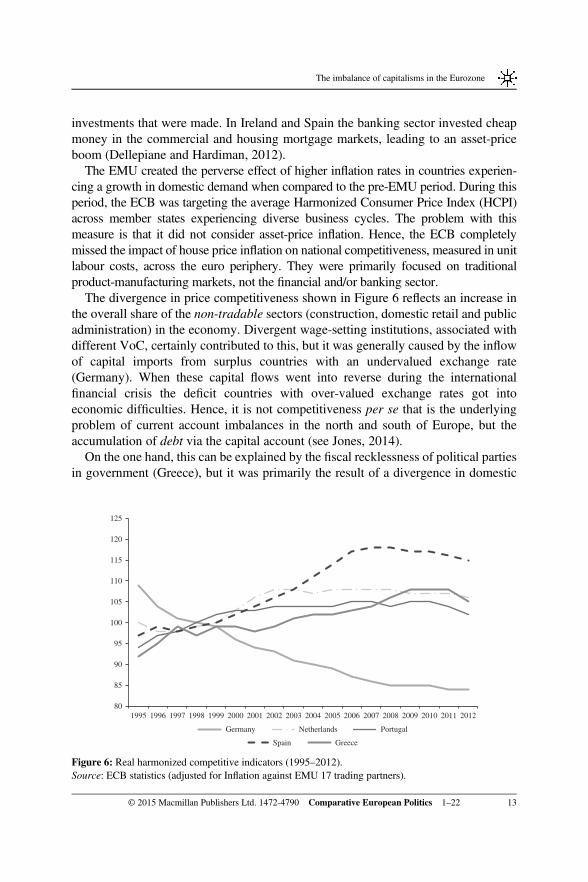

The EMU created the perverse effect of higher inflation rates in countries experien-cing a growth in domestic demand when compared to the pre-EMU period. During thisperiod, the ECB was targeting the average Harmonized Consumer Price Index (HCPI)across member states experiencing diverse business cycles. The problem with thismeasure is that it did not consider asset-price inflation. Hence, the ECB completelymissed the impact of house price inflation on national competitiveness, measured in unitlabour costs, across the euro periphery. They were primarily focused on traditionalproduct-manufacturing markets, not the financial and/or banking sector.

The divergence in price competitiveness shown in Figure 6 reflects an increase inthe overall share of the non-tradable sectors (construction, domestic retail and publicadministration) in the economy. Divergent wage-setting institutions, associated withdifferent VoC, certainly contributed to this, but it was generally caused by the inflowof capital imports from surplus countries with an undervalued exchange rate(Germany). When these capital flows went into reverse during the internationalfinancial crisis the deficit countries with over-valued exchange rates got intoeconomic difficulties. Hence, it is not competitiveness per se that is the underlyingproblem of current account imbalances in the north and south of Europe, but theaccumulation of debt via the capital account (see Jones, 2014).

On the one hand, this can be explained by the fiscal recklessness of political partiesin government (Greece), but it was primarily the result of a divergence in domestic

80

85

90

95

100

105

110

115

120

125

Germany Netherlands Portugal

Spain Greece

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Figure 6: Real harmonized competitive indicators (1995–2012).Source: ECB statistics (adjusted for Inflation against EMU 17 trading partners).

The imbalance of capitalisms in the Eurozone

13© 2015 Macmillan Publishers Ltd. 1472-4790 Comparative European Politics 1–22

consumption funded by private finance. This was made possible by an integrated andliberalized European money market that began with the abolition of capital controlsin the 1980s, followed by the harmonization of financial regulations in the 1990s, andculminated in the single currency: the EMU.

The political fallout within the EMU when these credit bubbles burst is now part ofEuropean history. In Ireland and southern Europe, the level of private and public debtaccumulated was quickly made visible to markets. Increased tax revenues madepossible by a period of full employment and high growth collapsed when domesticdemand contracted. Governments stepped in to guarantee the bad debts of theirfinancial sectors. Fiscal deficits increased and debt-GDP ratios soared (see Figure 5).In the absence of a central bank capable of acting as a lender of last resort,international investors panicked. Government bond yields rapidly diverged and thefragility of the Eurozone was exposed. Greece, Ireland and Portugal were catapultedout of international finance markets and had to resort to ECB-IMF-EU (troika) loansto avoid a sovereign default. In return for this ‘bailout’ these member states wererequired to implement an aggressive internal devaluation: public sector adjustmentand structural reforms, on the assumption that external competitiveness and labourmarket rigidities are the main obstacles to an export-led recovery (see Monastiriotiset al, 2013, and Hardiman and Regan 2013, for a detailed analysis on the impact).

The sovereign-debt crisis soon spread to Spain and Italy. While these countrieshave not been directly priced out of the international bond markets, they requiredemergency funding from the ECB to keep their banking systems and economiesliquid. In return for this they too must impose structural reforms and cuts in publicexpenditure. Hence, rather than confront the asymmetric implications of joiningtogether different macroeconomic growth regimes into a shared currency, andpropose a shared solution to what is fundamentally a Eurozone wide crisis, Europeanpolicymakers shifted the burden of adjustment on to the public sector of deficitcountries. The policy response of ‘internal devaluation’ is designed to stabilize thecommon euro currency and the best way to do this, it is argued, is for member statesto converge with the export-led growth model of Germany. But the outcome is tocollapse domestic consumption in countries traditionally reliant upon wage-led andsubsequently debt-led growth for employment. It is this collapse in imports and theincome effect of contracting domestic demand that explains the narrowing of externalimbalances since 2012, and rapidly rising unemployment. With the exception ofIreland, southern European countries continue to have a significantly overvalued realexchange rate and the price deflator remains constant (see Figure 6).

The Consequence: Creditor and Debtor Bargaining in Europe

There are four important political observations to be made about the European policyresponse to the Eurozone debt crisis. First, it is not supranational institutions such as

Regan

14 © 2015 Macmillan Publishers Ltd. 1472-4790 Comparative European Politics 1–22

the European parliament or the EU commission that have emerged to coordinate theadjustment, but the European Council. The new executive powers that have emergedfrom the EU Council have created a mode of governance that mirrors an executivefederalism with no formal-legislative legitimacy (Habermas, 2012). The outcome isan inter-governmental regime that gives ultimate priority to fiscal austerity andstructural reforms as the primary solution to the imbalance of capitalisms at the heartof the Eurozone project. In particular and reflecting the intergovernmental mode ofdecision making that has emerged, Germany and other export-led economies havesucceeded in getting all member states to pursue policies aimed at internalcompetitive devaluations, and to institutionalize this into a new Eurozone ‘fiscalcompact’. This has given the EU Council unprecedented procedures and capabilitiesto both monitor and sanction member states for violating the rules of austerity.It gives ultimate priority to national export competitiveness within the EMU, at theexpense of domestic consumption and employment.

Second, the asymmetric implication of pursuing supply-side reforms in the deficitcountries, with macroeconomic growth regimes based on consumption, is a collapsein domestic demand. This in turn has led to a divergence in levels of unemploymentacross the north and south of Europe. At the time of writing, the unemployment rateis 27 per cent in Greece, 26 per cent in Spain, 17 per cent in Portugal and almost12 per cent in Ireland. The cross-national youth unemployment rate in Spain, Italy,Portugal and Greece varies between 42 and 56 per cent (Gros, 2012). Most of this isthe outcome of a contraction in domestic consumption, not industrial output.To overcome the unemployment crisis these economies are being encouraged toadopt labour market supply-side reforms, as a complement to fiscal retrenchment, inorder to generate long-term economic growth. But there is limited empirical evidenceto suggest that these reforms can work in economies dependent upon domesticdemand (Baccaro and Rei, 2007). Empirically, it is widely accepted that structuralreforms only work as a long-term strategy in a period of strong economic growth, andwhen complemented by social security policies that ensure high levels of incomereplacement (Hemerijck, 2012). Since the onset of the crisis the policy response tolabour market problems has been dominated by labour market research in ECOFIN.This is narrowly aimed at structural reforms, and underestimates (or is indifferent to)the importance of government consumption and wage demand in sustainingemployment.

Third, the priority accorded to fiscal stability and structural reforms that hasemerged from the EU Council ignores the central problem facing policymakers in theEurozone: how to regain control over financial markets. The frustrated attempts toregulate the international financial system are being blockaded by political fragmen-tation among nation-states. This is particularly the case for CMEs such as Germany,who jealously guard their prerogatives to defend their domestic export sectors, andare therefore reluctant to build new supranational capacities for political action.Simultaneously, countries such as Ireland refuse to accept a coordinated financial

The imbalance of capitalisms in the Eurozone

15© 2015 Macmillan Publishers Ltd. 1472-4790 Comparative European Politics 1–22

transaction tax because of domestic financial interests. The EU policy response,therefore, ultimately, sets the seal on the intergovernmental mode of nationalregulation, which makes it possible for national governments to narrowly promotethe specific interests of their national variety of capitalism, thereby blocking off acoordinated response to rebalance the disequilibrium between the debtor and creditorcountries (Fabbrini, 2013).

Finally, and most importantly for the theoretical argument being developed in thisarticle, the northern European-inspired fiscal stability agenda promotes a one-size-fits-all solution that does not take into account the need for differential adjustmentprogrammes in the south of Europe. It rules out flexible interventions that are tailoredto the specific growth models, institutions and labour market problems of eachmember state. The underlying cognitive argument used to validate this strategy is thenotion of Ricardian equivalence or ‘expansionary fiscal contraction’. It is assumedthat a shrinking public sector will lead to increased competitiveness in the privatesector, which in turn will kick-start an economic recovery based on export-ledgrowth. The subsequent improvement in the current account, it is argued, will send asignal to international financial markets that the government has the capacity to payback its long-term borrowings. The problem with all of this, of course, is that it isbased on assumptions of rational expectations (see Blanchard and Leigh, 2013). It isbased on the same logical argument that was used to create the EMU in the first place:that a one-size-fits-all adjustment can lead to convergence in macroeconomic growthregimes. But there is not a complementary institutional fit between the national fiscaland labour market policies of each member state and EMU. Monetary policy remainsEuropeanized, yet the institutions to transmit this to the real economy remainnational, with the result that the various ECB monetary easing programmes since2011 are not having the assumed expansionary effect on domestic consumption.Banking, much like labour market policies, operate at the national, not European,level (Mody and Sandri, 2012).

Hence, the assumption that an institutional complementarity between all these sub-spheres of the economy can be achieved through the implementation of a singularmonetary policy, stricter fiscal rules and labour market liberalization is not possible if oneaccepts that there are different VoC based around distinct growth regimes in Europe. Butit does draw our attention to the complexity of decision making among diverse capitalistdemocracies in a multilevel polity during hard economic times, and it is on this point thata theory narrowly focused on the nation-state has limited explanatory power. It requiresexamining the Euro area from an international political economy perspective.

The outcome: Competitive internal devaluation

Political leaders at the national level in creditor and debtor countries are operating ina complex institutional matrix that offers competing incentives and constraints on

Regan

16 © 2015 Macmillan Publishers Ltd. 1472-4790 Comparative European Politics 1–22

their behaviour. They have to respond to the popular preferences of domesticelectorates to ensure re-election and simultaneously respond to the interests of otherpolitical leaders at the EU level, to ensure their membership of the EMU. In theaftermath of the Eurozone crisis this has become an asymmetric tension. Thosecountries with the most economic resources are in a significantly stronger bargainingposition to get other member states to comply with their interests. But simultaneouslycountries such as Germany must comply with European Union law. The outcome isthat member states in the north and south of Europe are compelled to compete withone another through competitive internal devaluations, despite the asymmetric effecton their growth regimes.

Given the structural constraints of the monetary union, the only way to do this is toreduce the price of domestic wages and enhance labour market flexibility. Theimplication, however, is that those countries who rely upon domestic consumption togenerate economic growth are now confronted with the prospect of a permanentdecline in domestic demand (no wage or credit growth), growing levels of labourmarket dualization and high levels of unemployment. All of this could be overcomethrough a rebalancing of capitalisms within the Eurozone. But the heterogeneity andpolitical interests of the social coalitions underpinning national labour and welfareinstitutions makes this highly unlikely (Höpner and Schäfer, 2012; Schimmelfennigand Winzen, 2014). It would require Germany to inflate by 5.5 per cent per annumand Spain to deflate by a similar margin (see Hans-Werner, 2012). This is notpolitically feasible, nor is it legally possible under the existing EU treaties (that is, themandate of the ECB is price stability).

The EU lacks all the pre-requisites of input legitimacy that characterize a nation-state. There are no European-wide political parties, no European-wide capacity togenerate revenue and no directly elected President or European government capableof coordinating the adjustment across debtor and creditor regions. Political cleavagesand the public sphere remain an entirely national affair. Hence, the capacity tocoordinate a European-wide solution to the Eurozone debt crisis is restricted by themultiple veto points built into sharing sovereignty in a multilevel polity. Policy-making and power relations are diffused across a wide variety of actors andinstitutions. It is for all these reasons that Scharpf (2009) has long argued that theEU is best characterized as a negative process of market-making that is structurallybiased towards the promotion of neoliberal markets. Even if policymakers wanted toturn the EU into a federal system capable of coordinating a balanced adjustmentbetween diverse growth regimes they would be incapable of doing so because ofinstitutional asymmetries. The outcome for Scharpf (2012) is a variant of Hayekiantechnocracy whereby the ECB is the only actor capable of solving problems.

The European Commission has been replaced by intergovernmental Eurozonesummits between heads of state as the main forum for political decision making. TheCommission subsequently monitors and implements the outcomes, particularly thefinancial and economic affairs commissioner, reflected in the new ‘macroeconomic

The imbalance of capitalisms in the Eurozone

17© 2015 Macmillan Publishers Ltd. 1472-4790 Comparative European Politics 1–22

imbalances and competitiveness’ scorecard. This attributes ultimate responsibility forcrisis adjustment to government executives at the national level. In a context of crisismanagement, where creditor countries in northern Europe are being requested todistribute scarce resources to deficit countries in the south, this shift to nationalbargaining should not be surprising. But it draws our attention to the asymmetricalinfluence of countries with export-led macroeconomic growth regimes in designingthe structural adjustment programmes in southern Europe. Hence, the crisis of themonetary union in Europe has exposed the absence of coordinated problem-solvingcapacity in the single currency.

The outcome is that national governments are compelled to internalize the adjustmentpressures associated with the single currency and implement national supply-sidereforms of the labour market. Debtor governments, even if they wanted to, would not beable to adopt a variegated response that would stimulate the demand side of themacroeconomic equation (either by wage increases or public spending). This could bejustified if fiscal consolidation and supply-side reforms solved the diverse economicproblems facing these countries (that is, output legitimacy). The IMF (Blanchard andLeigh, 2013), among a whole host of other commentators, has since concluded that thisis not the case. The question, therefore, is whether there are substitute instruments at thenational level that go beyond ‘supply-side’ reforms in southern Europe and can lead to arebalance of path-dependent capitalisms in the Eurozone?

Discussion: Rethinking the Political Economy of European Integration

It is worth re-examining the question on external imbalances in the EMU in order toanswer the question as to whether the imbalance of capitalisms in the euro can bestructurally reversed. The first and dominant explanation for external imbalances isthat unit labour costs increased in the south relative to Germany. In the secondexplanation, the crisis was caused by an increase in the money supply. In the firstcase, the external imbalances were caused by a loss of competitiveness that is to beresolved through supply-side reforms and pay cuts. In the second case thecompetitiveness crisis was caused by financialization. Both agree, however, thatinternal devaluation is necessary to reduce domestic prices and wages. Theseperspectives differ on the causal mechanisms through which external imbalancesoccurred, but both are premised on the classical political economy assumption thatcurrent account imbalances are the outcome of countries not selling enough ‘real’goods and services to their trading partners, and hence they both agree that money isexogenous to the real economy. But if we accept that some countries areendogenously conducive to an export-led or a domestic consumption-led capitalistgrowth regime, and that these became systematically dependent upon one anotherthrough euro-finance markets, then this classical political economy equation becomesdeeply problematic. It mistakes cause for effect.

Regan

18 © 2015 Macmillan Publishers Ltd. 1472-4790 Comparative European Politics 1–22

Membership of the EMU compels member states to adopt labour market supply-side reforms as a tool of adjustment in a recession because the implicit design of themonetary union assumes that current account imbalances are an external competive-ness problem created by wage inflation. VoC theory broadly accepts this classicalpolitical economy assumption. It differs by arguing that surplus countries haveavoided a competitiveness crisis through their coordinated wage-setting institutions(see Hancké, 2013). In the context of a fixed exchange rate, supply-side reforms,should therefore facilitate an export-led recovery (even if it comes at the expense ofincreased inequality and enhanced labour market dualization). This theory can beapplied to countries with an export-led macroeconomic growth model. But it is notapplicable to countries reliant upon domestic consumption, and inflationary tenden-cies, for economic and employment growth. In Spain, Portugal and Greece exportsaccount for between 20–25 per cent of GDP.

Many economists argue that Germany and other surplus countries should reflatetheir domestic economy and pursue a more neoliberal response to the crisis (see Buti,2012, 2014) That is, they should spend more, let banks fail and encourage preciselywhat has happened in the United States. But given the export-oriented macroeco-nomic model endogenous to the political coalition underpinning the German growthregime, this is not likely to occur. The proximate cause of Germany’s capacity tointernalize the monetary constraints of the Eurozone can be traced to wage restraintand the supply-side labour market adjustments (popularly referred to as the ‘Hartz’reforms) mentioned in the section ‘The consequence: Creditor and debtor bargainingin Europe’. These are now being explicitly used by the DG for ECFIN as the modelprescription for deficit countries with high levels of unemployment. But the coreinsight from comparative political economy on the ultimate cause of German export-competitiveness is that its growth regime is built around a path-dependent industrialinfrastructure based on highly specific price-inelastic niche export markets.

Hence, if one accepts that the EMU has joined together distinct and path-dependent capitalist growth regimes, then there are four choices facing deficitcountries if they want to retain membership of the currency union: accept tradeimbalances and finance them through an increase in capital imports, reject the focuson export competitiveness and promote a wage-led recovery through enhanceddomestic demand, spend the fiscal resources necessary to develop the productivecapacity to compete with the German export model, or carve out an autonomouseconomic and growth strategy that is distinctively ‘southern European’. Given thelegal and political constraints of the EMU, the only possible solution is to pursue thesecond and last options. Both require some variant of inflationary wage-led growth.This can only come about if European policymakers accept that the causal source ofthe euro crisis was a debt-financed boom in domestic demand, rather than a loss ofcompetitiveness in the export sectors. It is precisely the sustainability of a wage-ledrecovery that remains a crucial and unexplored part of the debate about the politicaleconomy of contemporary capitalism today.

The imbalance of capitalisms in the Eurozone

19© 2015 Macmillan Publishers Ltd. 1472-4790 Comparative European Politics 1–22

This article has argued that the attempt to join together different VoC into a singlecurrency without a central government is the real source of the Eurozone crisis.It hypothesized that the imbalance of capitalism can be traced to competing growthmodels (export and consumption) that became systematically dependent on oneanother with the onset of monetary union and financial market integration. Thedivergence in these capitalist growth regimes can be empirically observed in the capitalflows, real exchange rates and net international investment positions of deficit andcreditor countries. It is not national wage-setting institutions or competitiveness per sethat is the core problem facing the EMU, but private debt created by financial markets.The one-size-fits-all policy response of fiscal consolidation and supply-side structuralreforms perpetuates the myth of market convergence that caused the crisis because itcontinues to assume that all member states can generate the conditions for export-ledgrowth. This, however, is systematically impossible in a semi-closed trading area suchas the Eurozone. The structural effect of the single currency, therefore, is to exacerbatethe imbalance of capitalisms within the EMU of Europe. In this sense, financial marketde-regulation did not unravel the national CMEs of Europe, but it has fundamentallychanged the political economy of European integration.

About the Author

Aidan Regan is a lecturer in European political economy at the School of Politicsand International Relations (SPIRe), University College Dublin (UCD), and co-director of the Dublin European Institute (DEI).

References

Armingeon, K. and Baccaro, L. (2012a) Political economy of the sovereign debt crisis: The limits ofinternal devaluation. Industrial Law Journal 41(3): 254–275.

Baccaro, L. and Rei, D. (2007) Institutional determinants of unemployment in OECD countries: Does thederegulatory view hold water? International Organization 61(03): 527–569.

Blanchard, O. and Leigh, D. (2013) Growth Forecast Errors and Fiscal Multipliers, IMF Working PaperNo. 13/1, Washington DC: International Monetary Fund.

Blanchard, O.J., Jaumotte, F. and Loungani, P. (2014) Labor market policies and IMF advice in advancedeconomies during the great recession. ZA Journal of Labor Policy 3(1): 1–23.

Buti, M. and Carnot, N. (2012) The EMU debt crisis: Early lessons and reforms*. JCMS: Journal ofCommon Market Studies 50(6): 899–911.

Buti, M. (2014) A consistent trinity for the Eurozone. VoxEU. org, 8.Dellepiane, S. and Hardiman, N. (2012) The New Politics of Austerity: Fiscal Responses to the Economic

Crisis in Ireland and Spain (No. 201207).De Grauwe, P. and Ji, Y. (2012) Mispricing of sovereign risk and macroeconomic stability in the

Eurozone. JCMS: Journal of Common Market Studies 50(6): 866–880.DeGrauwe, P. (2013) The European Central Bank as lender of last resort in the government bond markets.

Economic Studies 59(3): 520–535.

Regan

20 © 2015 Macmillan Publishers Ltd. 1472-4790 Comparative European Politics 1–22

De la Porte, C. and Heins, E. (2014) A new era of European integration quest; governance of labour marketand social policy since the sovereign debt crisis. Comparative European Politics 3.1(2015): 8–28.

Habermas, J. (2012) The crisis of the European Union in the light of a constitutionalization of internationallaw. European Journal of International Law 23(2): 335–348.

European Commission’s Directorate General for Economic and Financial Affairs (2014) Annual macro-economic database (AMECO), http://ec.europa.eu/economy_finance/ameco/user/serie/SelectSerie.cfm,accessed February–May 2014.

EU KLEMS Database (2010) Groningen Growth and Development Centre, http://www.euklems.net,accessed by Alison Johnston, December 2009–April 2011.

Fabbrini, S. (2013) Intergovernmentalism and its limits assessing the European Union’s answer to the Eurocrisis. Comparative Political Studies 46(9): 1003–1029.

Gros, D (2012) Macroeconomic Imbalances in the Euro Area: Symptom or cause of the crisis. CEPS PolicyBrief.

Hall, P. A. (2012a) The mythology of European monetary union. Swiss Political Science Review 18(4):508–513.

Hall, P.A (2012b) The economics and politics of the Euro crisis. German Politics 21(4): 355–371.Hall, P.A. and Soskice, D. (2001) Varieties of Capitalism: The Institutional Foundations of Comparative

Advantage. Oxford: Oxford University Press.Hancké, B. (2013) Unions, Central Banks, and EMU. New York: Oxford University Press.Hans-Werner, S. (2012) Austerity, Growth and Inflation: Remarks on the Euro’s Competitiveness

Problem.Hardiman, N. and Regan, A. (2013) The politics of austerity in Ireland. Intereconomics 48(1):2013-01 4–32.Hassel, A. (2012) The paradox of liberalization – Understanding dualism and the recovery of the German

political economy. British Journal of Industrial Relations 52(1): 57–81.Hay, C. (2004) Common trajectories, variable paces, divergent outcomes? Models of European capitalism

under conditions of complex economic interdependence. Review of International Political Economy11(2): 231–262.

Hay, C. and Wincott, D. (2012) The Political Economy of European Welfare Capitalism. Basingstoke:Palgrave Macmillan.

Hemerijck, A. (2012) Changing welfare states. Oxford: Oxford University Press.Höpner, M. and Schäfer, A. (2010) A new phase of European integration: Organised capitalisms in post-

Ricardian Europe. West European Politics 33(2): 344–368.Höpner, M. and Schäfer, A. (2012) Embeddedness and regional integration: Waiting for polanyi in a

Hayekian setting. International Organization 66(03): 429–455.Höpner, M. and Lutter, M. (2014) One currency and many modes of wage formation: Why the Eurozone is

too heterogeneous for the Euro. Cologne: Max Planck Institute for the Study of Societies. MPIfGDiscussion Paper 14/14.

Iversen, T. and Soskice, D. (2013) A political-institutional model of real exchange rates, competitiveness,and the division of labor. In: A. Wren (ed.) The Political Economy of the Service Transition, Oxford:Oxford University Press, 73.

Johnston, A. (2012) European Economic and Monetary Union’s perverse effects on sectoral wageinflation: Negative feedback effects from institutional change? European Union Politics 13(3):345–366.

Johnston, A. and Regan, A. (2014) European Integration and the Incompatibility of National Varieties ofCapitalism Problems with Institutional Divergence in a Monetary Union (No. 14/15) Cologne. MPIfGDiscussion Paper.

Johnston, A. and Regan, A. (forthcoming) European Monetary Union and the Incompatibility of NationalCapitalist Systems. Journal of Common Market Studies, in press.

Jones, E (2014) Competitiveness and the European financial crisis. Conference paper presented at the 21stConference of Europeanists, Washington DC, 14–16 March.

The imbalance of capitalisms in the Eurozone

21© 2015 Macmillan Publishers Ltd. 1472-4790 Comparative European Politics 1–22

Lane, P. R. (2012) Comment on: Net foreign assets and the exchange rate: Redux revived. Journal ofMonetary Economics 49(5): 1099–1102.

Monastiriotis, V. et al (2013) Austerity measures in crisis countries—results and impact on mid-termdevelopment. Intereconomics 48(1): 4–32.

Mody, A. and Sandri, D. (2012) The Eurozone crisis: How banks and sovereigns came to be joined at thehip. Economic Policy 27(70): 199–230.

Moravcsik, A. (1998) The Choice for Europe: Social Purpose and State Power from Messina toMaastricht. Ithaca, NY: Cornell University Press.

Moravcsik, A. (2012) Europe after the crisis: How to Sustain a common currency. Foreign Affairs91(2012): 54.

Mourlon-Druol, E. (2012) A Europe Made of Money: The Emergence of the European Monetary System.Ithaca, NY: Cornell University Press.

Rosamond, B. (2002) Imagining the European Economy: ‘Competitiveness’ and the social constructionof'Europe’as an economic space. New Political Economy 7(2): 157–177.

Scharpf, F. (2009) The Double Asymmetry of European Integration. Or Why the EU Cannot be a SocialMarket Economy. Cologne: MPIfG Working Paper 09/12.

Scharpf, F. (2011) Monetary Union, Fiscal Crisis and the Preemption of Democracy. London, LEQS Paper 36.Scharpf, F. (2012) Legitimacy Intermediation in the Multilevel European Polity and Its Collapse in the

Euro Crisis. Cologne, MPIfG Discussion Paper 12/6.Schmidt, V. A. (2002) The futures of European capitalism. Oxford, UK: Oxford University Press.Schimmelfennig, F. and Winzen, T. (2014) Instrumental and constitutional differentiation in the European

Union. JCMS: Journal of Common Market Studies 52(2): 354–370.Storm, S. and Naastepad, C. W. M. (2014) Europe’s hunger games: Income distribution, cost competitive-

ness and crisis. Cambridge Journal of Economics, advance online publication 25 September,doi:10.1093/cje/beu037.

Regan

22 © 2015 Macmillan Publishers Ltd. 1472-4790 Comparative European Politics 1–22

Related Documents