SMB CAPITAL OPTIONS TRAINING PROGRAM

THE GREEKS Options prices are always based on market supply and demand. However predictive models have been developed to measure effect on changes.

Dec 27, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

SMB CAPITAL OPTIONS TRAINING PROGRAM

THE GREEKS

SESSION FOUR

Options prices are always based on market supply and demand.

However predictive models have been developed to measure effect on changes in price, time and volatility.

These measurement are known as “the greeks”.

Options Greeks

Delta--Effect of movement of underlying stock or index on an option’s price.

Gamma—Rate of change of delta. Vega—Effect of fear of future price volatility

on an option’s price. Theta—Effect of passage of time on an

option’s price. Rho—Effect of interest rates on an option’s

price.

Options greeks predict changes in prices of options

Delta=statistical chance that option will expire in the money.

Delta also equals the predicted price change of the option based on a 1 point change in the underlying.

Long calls and short puts and actual shares of stock have positive deltas.

Short calls, long puts and short stock have negative deltas.

DELTA

OUT OF THE MONEY DELTAS

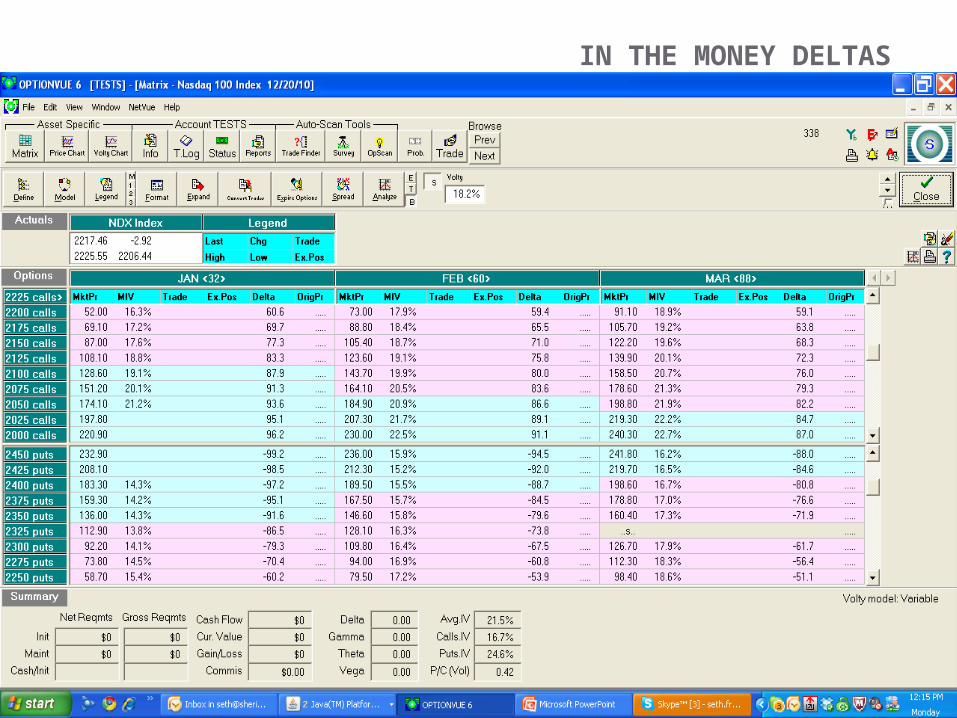

IN THE MONEY DELTAS

ATM CALLS OR PUTS HAVE ABOUT 50 DELTAS—50% CHANCE OF EXPIRING IN THE MONEY.

THE SUM OF A CALL AND A PUT AT THE SAME STRIKE SHOULD BE APPROXIMATELY 100%--PROBABILITIES OF EXPIRING ITM.

BACK MONTH OPTIONS HAVE HIGHER DELTAS THAN THE SAME STRIKE FRONT MONTH OPTION—GREATER CHANCE OF EXPIRING IN THE MONEY AS OPTION IS AT RISK LONGER.

AS OPTIONS GO FARTHER OTM THE DELTA DROPS. AS OPTIONS GO DEEPER ITM THE DELTA INCREASES. DISTANCE BETWEEN DELTAS WIDENS CLOSER TO

EXPIRATION.

PROPERTIES OF DELTAS

The second derivative of price. It’s the “delta of the delta”—the rate of change of delta.

Each 1 point move in underlying changes delta by amount of gamma.

You ADD gamma to delta if the underlying moves up to arrive at the new delta.

You SUBTRACT gamma from delta if the underlying moves down 1 point.

So call deltas get more positive in rallies and put deltas get more negative in sell-offs.

GAMMA

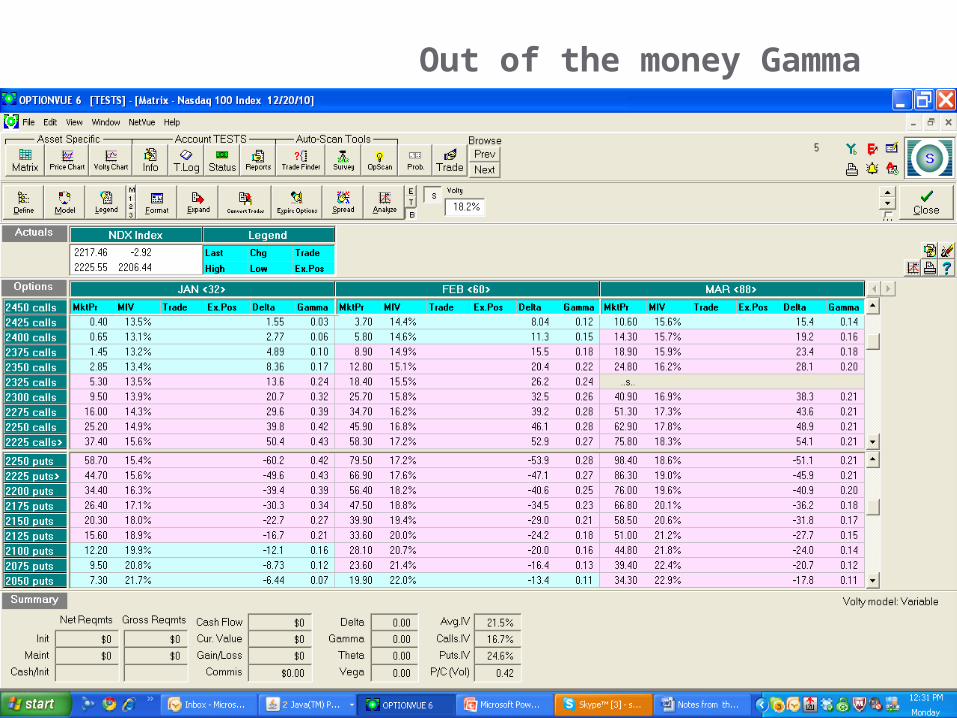

Out of the money Gamma

In the money Gamma

Gamma is highest for ATM options or nearest options to ATM

Gamma gets very high as expiration nears so deltas can change very quickly which is dangerous if you are short options (chances of expiring ITM changes dramatically near expiration as price moves because of gamma)

Front month gamma is higher than back month nearer to the money-reverse for far OTM.

PROPERTIES OF GAMMA

Measures daily deterioration of extrinsic value in long options.

Theta of an option is the predicted deterioration of its time premium (extrinsic value) in one trading day.

This is the key to income trading—we are net sellers of options-- taking advantage of their deterioration in value over time.

Any long option automatically reduces theta of an options position.

Selling a long option automatically increases theta of the position.

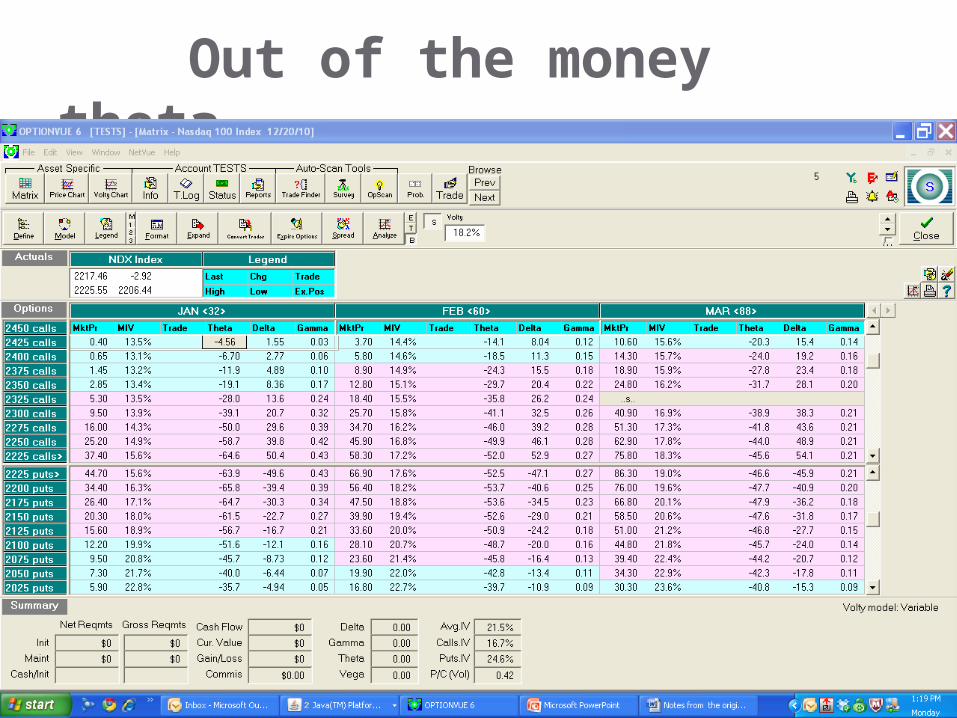

Theta

Out of the money theta

In the money theta

At the money options burn off theta fastest. So short ATM options have the opportunity for the quickest appreciation.

Back month ATM options have much less theta than front month ATM options.

Back month OTM options have more theta than front month OTM options at the same strike.

ATM options theta increases rapidly as expiration approaches.

Farther out options theta decelerates towards expiration.

Properties of theta

Measures how an option reacts to changes in market price volatility.

An option changes by the vega amount given a one point move in “implied volatility (IV)”.

Implied volatility is the one standard deviation range of prices (68.3%) for the stock or index over the next 365 days.

Vega

Out of the money vega

In the money vega

ATM options have the most vega and Back month options have more vega than

front month options primarily because there is more time premium impacted by the increase in volatility.

As options approach expiration, vega decreases as less time premium is present.

Vega goes to zero at on expiration day.

Properties of vega

Measures effect of changes in interest rates on

A 1% change in interest rates will cause an option to change value by the value of its rho.

This has the greatest effect on leap options (long term options).

Rho

The essence of income options trading is to take advantage of theta decay by being short options.

All of the other greeks create risk while theta creates the reward.

The game is to control the risk of the “risk” greeks so as to maximize the reward of the “reward” greek which is theta.

Our next session will expand on this quite a bit.

Why are the greeks important?

Go into Optionvue and pull up the Options Chain for fifteen stocks of your choice of the S and P 500 priced greater than $75. (google “components SPX index”).

Select 5 of those stocks and go back in time through backtrader until you get to 30 days before any month’s expiration. Pull up the options chain for that expiration. For each stock sell a 10 lot at-the-money call 30 days out. Mark down the delta, gamma, vega and theta every three days until expiration of those options. Note how they change as time passes and market price and volatility changes.

Select 5 different stocks and pull up the options chain from a recent expiration 60 days prior to that expiration. Buy a 10 lot put spread with a delta at around 10 or a bit lower ( a far OTM put). Mark down the delta, gamma, vega and theta every six days until expiration. Note how they change as time passes and market price changes.

Select the remaining 5 stocks and pull up the options chain for 45 days out from a recent expiration. For each stock buy a 10 lot call with a delta of 90 or greater (deep in the money call). Note how they change as time passes and market price changes.

Homework

Related Documents