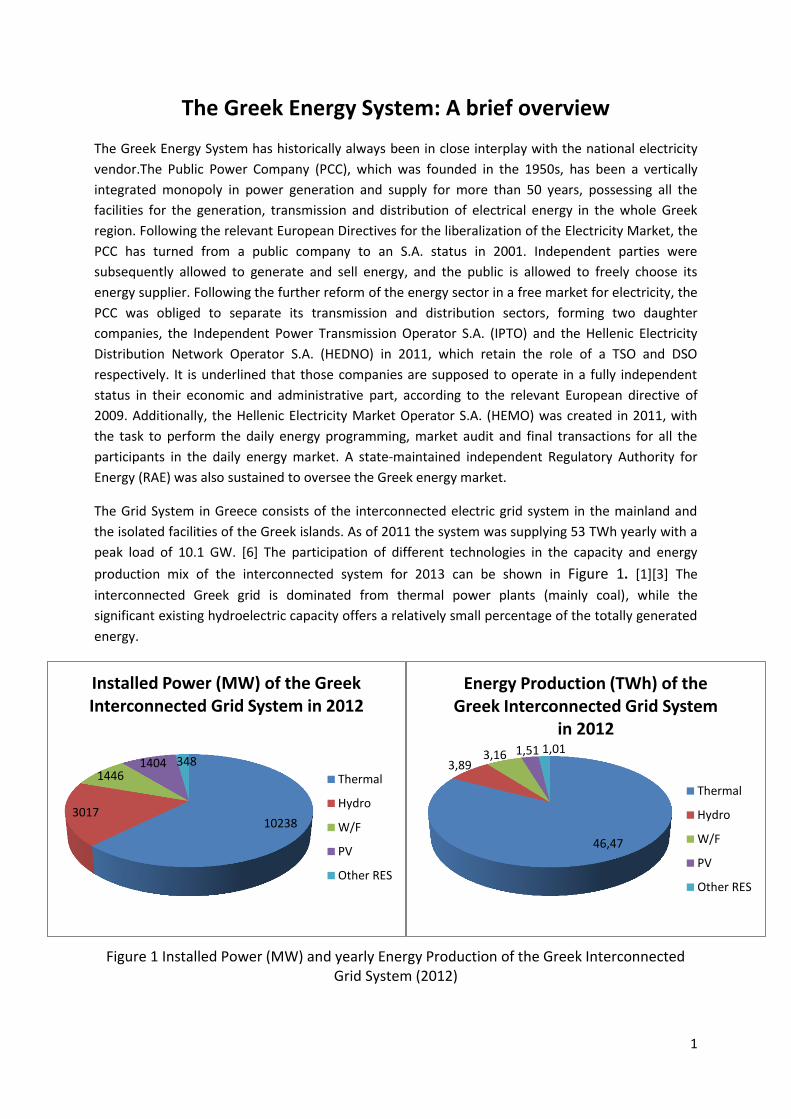

1 The Greek Energy System: A brief overview The Greek Energy System has historically always been in close interplay with the national electricity vendor.The Public Power Company (PCC), which was founded in the 1950s, has been a vertically integrated monopoly in power generation and supply for more than 50 years, possessing all the facilities for the generation, transmission and distribution of electrical energy in the whole Greek region. Following the relevant European Directives for the liberalization of the Electricity Market, the PCC has turned from a public company to an S.A. status in 2001. Independent parties were subsequently allowed to generate and sell energy, and the public is allowed to freely choose its energy supplier. Following the further reform of the energy sector in a free market for electricity, the PCC was obliged to separate its transmission and distribution sectors, forming two daughter companies, the Independent Power Transmission Operator S.A. (IPTO) and the Hellenic Electricity Distribution Network Operator S.A. (HEDNO) in 2011, which retain the role of a TSO and DSO respectively. It is underlined that those companies are supposed to operate in a fully independent status in their economic and administrative part, according to the relevant European directive of 2009. Additionally, the Hellenic Electricity Market Operator S.A. (HEMO) was created in 2011, with the task to perform the daily energy programming, market audit and final transactions for all the participants in the daily energy market. A state-maintained independent Regulatory Authority for Energy (RAE) was also sustained to oversee the Greek energy market. The Grid System in Greece consists of the interconnected electric grid system in the mainland and the isolated facilities of the Greek islands. As of 2011 the system was supplying 53 TWh yearly with a peak load of 10.1 GW. [6] The participation of different technologies in the capacity and energy production mix of the interconnected system for 2013 can be shown in Figure 1. [1][3] The interconnected Greek grid is dominated from thermal power plants (mainly coal), while the significant existing hydroelectric capacity offers a relatively small percentage of the totally generated energy. Figure 1 Installed Power (MW) and yearly Energy Production of the Greek Interconnected Grid System (2012) 10238 3017 1446 1404 348 Installed Power (MW) of the Greek Interconnected Grid System in 2012 Thermal Hydro W/F PV Other RES 46,47 3,89 3,16 1,51 1,01 Energy Production (TWh) of the Greek Interconnected Grid System in 2012 Thermal Hydro W/F PV Other RES

The Greek Energy System - A Brief Overview v 3 0

Feb 14, 2016

Summary of the characteristics of the Greek energy system

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

The Greek Energy System: A brief overview

The Greek Energy System has historically always been in close interplay with the national electricity

vendor.The Public Power Company (PCC), which was founded in the 1950s, has been a vertically

integrated monopoly in power generation and supply for more than 50 years, possessing all the

facilities for the generation, transmission and distribution of electrical energy in the whole Greek

region. Following the relevant European Directives for the liberalization of the Electricity Market, the

PCC has turned from a public company to an S.A. status in 2001. Independent parties were

subsequently allowed to generate and sell energy, and the public is allowed to freely choose its

energy supplier. Following the further reform of the energy sector in a free market for electricity, the

PCC was obliged to separate its transmission and distribution sectors, forming two daughter

companies, the Independent Power Transmission Operator S.A. (IPTO) and the Hellenic Electricity

Distribution Network Operator S.A. (HEDNO) in 2011, which retain the role of a TSO and DSO

respectively. It is underlined that those companies are supposed to operate in a fully independent

status in their economic and administrative part, according to the relevant European directive of

2009. Additionally, the Hellenic Electricity Market Operator S.A. (HEMO) was created in 2011, with

the task to perform the daily energy programming, market audit and final transactions for all the

participants in the daily energy market. A state-maintained independent Regulatory Authority for

Energy (RAE) was also sustained to oversee the Greek energy market.

The Grid System in Greece consists of the interconnected electric grid system in the mainland and

the isolated facilities of the Greek islands. As of 2011 the system was supplying 53 TWh yearly with a

peak load of 10.1 GW. [6] The participation of different technologies in the capacity and energy

production mix of the interconnected system for 2013 can be shown in Figure 1. [1][3] The

interconnected Greek grid is dominated from thermal power plants (mainly coal), while the

significant existing hydroelectric capacity offers a relatively small percentage of the totally generated

energy.

Figure 1 Installed Power (MW) and yearly Energy Production of the Greek Interconnected Grid System (2012)

10238 3017

1446 1404 348

Installed Power (MW) of the Greek Interconnected Grid System in 2012

Thermal

Hydro

W/F

PV

Other RES

46,47

3,89 3,16 1,51 1,01

Energy Production (TWh) of the Greek Interconnected Grid System

in 2012

Thermal

Hydro

W/F

PV

Other RES

2

Within this report, the main aspects of the Greek electricity system and market will be analyzed. This

is to be achieved with a targeted reference to a series of features. More specifically, the topics

presented will cover the recent developments in the Greek electricity market, the present changes

regarding the generation and consumption sectors, the state and development of the Transmission

and Distribution network, the integration of RES in the system, the regulatory framework and

relevant legislation related to the RES, and finally the prospects of the integration of storage

technology.

1. The electricity market in Greece

Although the liberalization of the energy markets of the member states was clearly introduced in the

European Directives of 1996, 2003, 2009, the liberalization of the Greek market is still in progress. In

an effort to promote competition and avoid unfair market asymmetries, the electricity industry of

Greece has been unbundled in the Sectors of Generation, Transmission, Distribution and Supply.

However, there has been limited success in the effort for an increase of market participants. More

specifically, although between 2004 and 2014 numerous participants have been introduced in the

generation area, as of today the PPC still holds 68% of the installed capacity. The prospect is even

worse in the supply sector. Two major supply companies that had managed to gain access to a high

number of end customers were suspended from the market in 2012 after participating in major

scandals. At this point of time several other companies are engaged in the supply sector, but

maintain a minor share of the supply market (1.5%). Recently, the retail tariffs have been effectively

unbundled, separating charges for monopolistic and competitive activities to the end user, adding

some transparency into the competition of the market. [7]

On the other hand, the Market Operator established operates effectively a wholesale (mandatory

electricity pool) market where a Daily Energy Planning takes place, after the producers/importers and

suppliers/exporters submit offers for their total generation/demand, forming the System Marginal

Price. No individual contracts between generators and suppliers are allowed. [10] Specific HV

costumers are reported to be allowed to take part in the Daily Energy Planning to cover their own

demand directly. Apart from the PCC, three major independent energy firms and two industrial firms

possess generation plants and participate with 9 generating units in the HEMO records. The

independent suppliers possess only gas fired power plants which, although cost efficient, allow the

PCC to be the only company in possession of low cost coal plants, maintaining its predominant

position in the market. At this point of time, HEMO is still under the complete ownership of the

Greek government. [7] In real time conditions, the HEMO is of course not responsible for real time

dispatch, emergency dispatch and import and ancillary services. The TSO is responsible for those

actions along with measurement and definition of deviations from the supposed Daily Planning.

Those deviations are transferred also to HEMO, who is responsible for the necessary corrections in

predefined transactions. [11]

The Regulatory Authority for Energy, although initially having only a consulting character, has

gradually gained independency from the ministry control (2011), and is currently related to the

licensing procedure for new generation units. It is also considered the referee guaranteeing the

proper operation of the electricity market, especially when it comes to fair competition and safety of

energy supply. The State cannot interfere with its decisions, but RAE is financed and manned by the

relevant Ministry of Environment, Energy and Climate Change (MEECC).

3

The Greek government has a high involvement in the electricity market through the actions of

MEECC. The ministry has often participated in regulatory decisions for the electricity market that

would normally not be under its jurisdiction, making the electricity market susceptible to political

influence. In the past, the publicly owned utility has constituted an important tool in the hands of the

government, used for the application of social policies, through the application of low retail tariffs for

specific social teams. The PPC often sets retail prices really low for specific customer categories

making competition very difficult, and existing suppliers are active into the supply of very small

profitable parts of the market, leaving the other market segments to the PPC. In general, the PCC’s

objectives have many times not led by the concepts of profit and value maximization, rather the

application of social and political aims. At this point of time, the liberalization process is seen by the

government as a clash between EU agenda and local Unions of Workers, with the Greek government

being rather reluctant to promote it, in fear of losing significant political power.

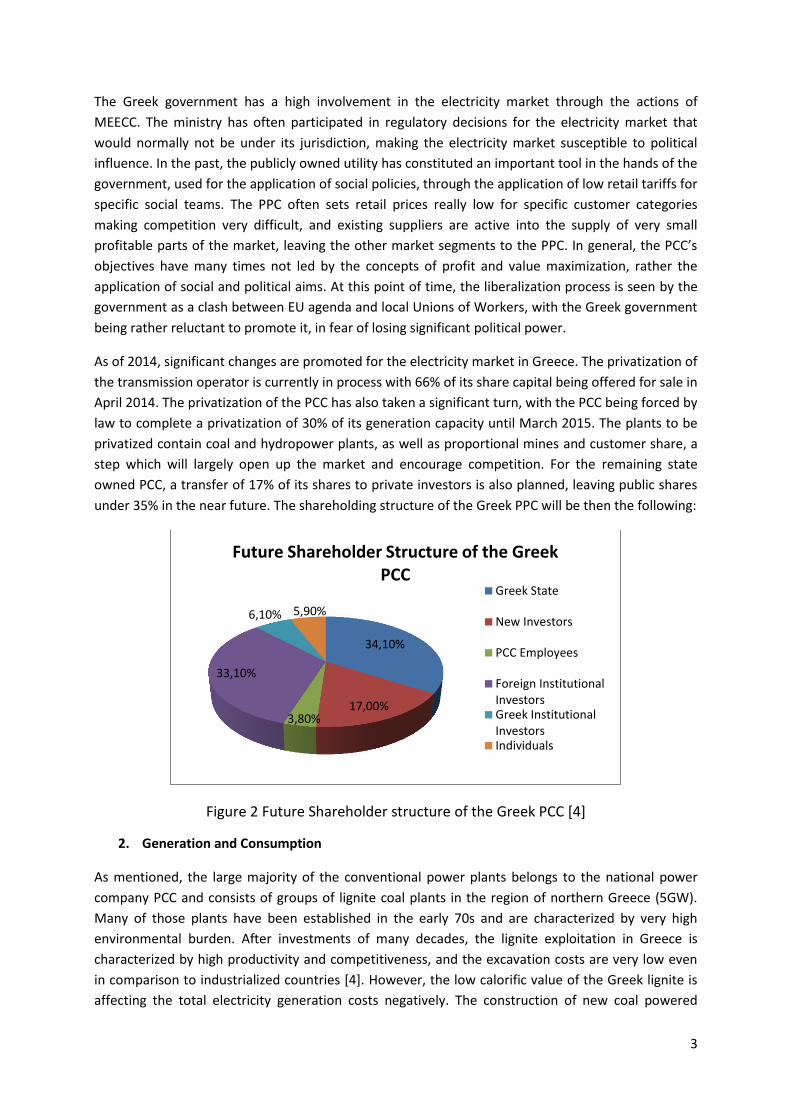

As of 2014, significant changes are promoted for the electricity market in Greece. The privatization of

the transmission operator is currently in process with 66% of its share capital being offered for sale in

April 2014. The privatization of the PCC has also taken a significant turn, with the PCC being forced by

law to complete a privatization of 30% of its generation capacity until March 2015. The plants to be

privatized contain coal and hydropower plants, as well as proportional mines and customer share, a

step which will largely open up the market and encourage competition. For the remaining state

owned PCC, a transfer of 17% of its shares to private investors is also planned, leaving public shares

under 35% in the near future. The shareholding structure of the Greek PPC will be then the following:

Figure 2 Future Shareholder structure of the Greek PCC [4]

2. Generation and Consumption

As mentioned, the large majority of the conventional power plants belongs to the national power

company PCC and consists of groups of lignite coal plants in the region of northern Greece (5GW).

Many of those plants have been established in the early 70s and are characterized by very high

environmental burden. After investments of many decades, the lignite exploitation in Greece is

characterized by high productivity and competitiveness, and the excavation costs are very low even

in comparison to industrialized countries [4]. However, the low calorific value of the Greek lignite is

affecting the total electricity generation costs negatively. The construction of new coal powered

34,10%

17,00% 3,80%

33,10%

6,10% 5,90%

Future Shareholder Structure of the Greek PCC

Greek State

New Investors

PCC Employees

Foreign InstitutionalInvestorsGreek InstitutionalInvestorsIndividuals

4

plants has not yet been halted completely, with at least another 1.5 GW of capacity to be developed

in the near future.

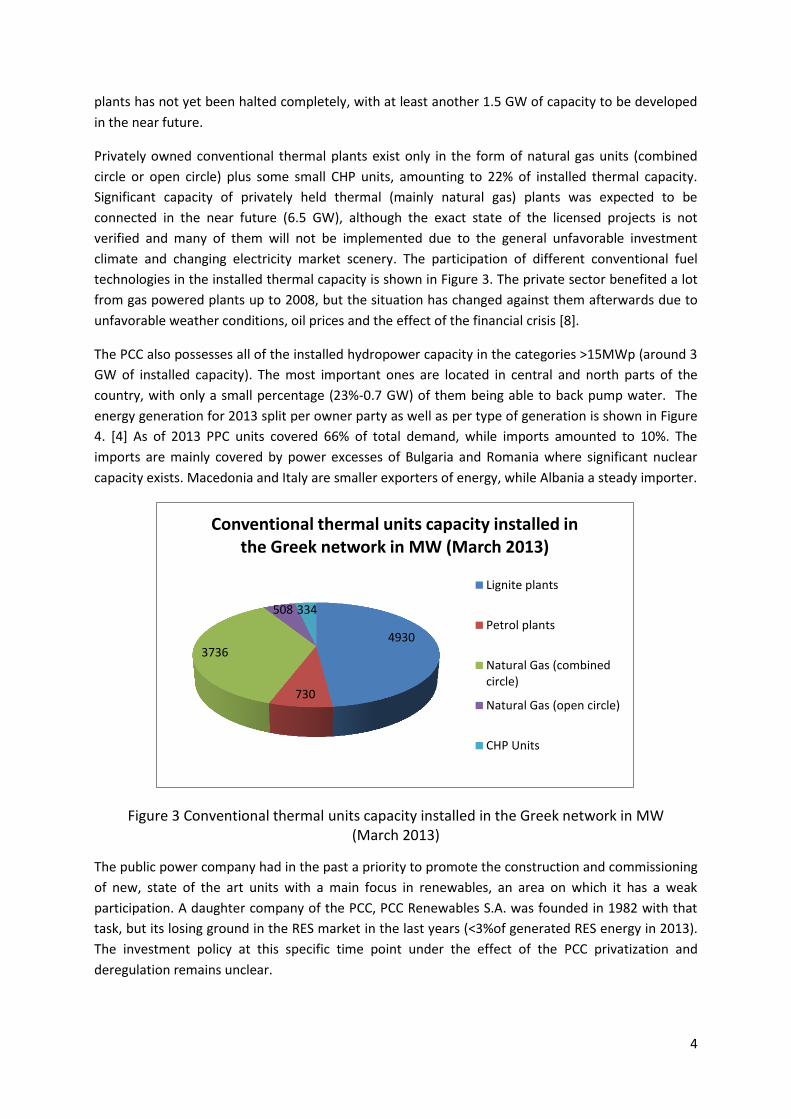

Privately owned conventional thermal plants exist only in the form of natural gas units (combined

circle or open circle) plus some small CHP units, amounting to 22% of installed thermal capacity.

Significant capacity of privately held thermal (mainly natural gas) plants was expected to be

connected in the near future (6.5 GW), although the exact state of the licensed projects is not

verified and many of them will not be implemented due to the general unfavorable investment

climate and changing electricity market scenery. The participation of different conventional fuel

technologies in the installed thermal capacity is shown in Figure 3. The private sector benefited a lot

from gas powered plants up to 2008, but the situation has changed against them afterwards due to

unfavorable weather conditions, oil prices and the effect of the financial crisis [8].

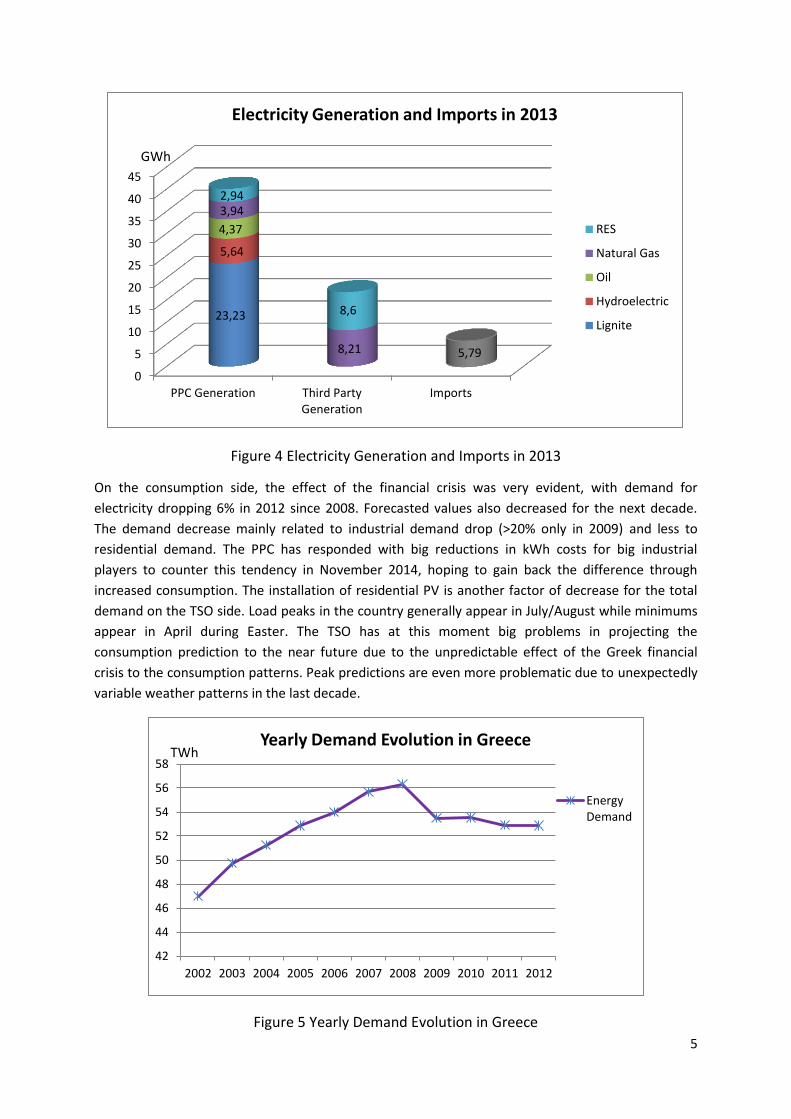

The PCC also possesses all of the installed hydropower capacity in the categories >15MWp (around 3

GW of installed capacity). The most important ones are located in central and north parts of the

country, with only a small percentage (23%-0.7 GW) of them being able to back pump water. The

energy generation for 2013 split per owner party as well as per type of generation is shown in Figure

4. [4] As of 2013 PPC units covered 66% of total demand, while imports amounted to 10%. The

imports are mainly covered by power excesses of Bulgaria and Romania where significant nuclear

capacity exists. Macedonia and Italy are smaller exporters of energy, while Albania a steady importer.

Figure 3 Conventional thermal units capacity installed in the Greek network in MW (March 2013)

The public power company had in the past a priority to promote the construction and commissioning

of new, state of the art units with a main focus in renewables, an area on which it has a weak

participation. A daughter company of the PCC, PCC Renewables S.A. was founded in 1982 with that

task, but its losing ground in the RES market in the last years (<3%of generated RES energy in 2013).

The investment policy at this specific time point under the effect of the PCC privatization and

deregulation remains unclear.

4930

730

3736

508 334

Conventional thermal units capacity installed in the Greek network in MW (March 2013)

Lignite plants

Petrol plants

Natural Gas (combined circle)

Natural Gas (open circle)

CHP Units

5

Figure 4 Electricity Generation and Imports in 2013

On the consumption side, the effect of the financial crisis was very evident, with demand for

electricity dropping 6% in 2012 since 2008. Forecasted values also decreased for the next decade.

The demand decrease mainly related to industrial demand drop (>20% only in 2009) and less to

residential demand. The PPC has responded with big reductions in kWh costs for big industrial

players to counter this tendency in November 2014, hoping to gain back the difference through

increased consumption. The installation of residential PV is another factor of decrease for the total

demand on the TSO side. Load peaks in the country generally appear in July/August while minimums

appear in April during Easter. The TSO has at this moment big problems in projecting the

consumption prediction to the near future due to the unpredictable effect of the Greek financial

crisis to the consumption patterns. Peak predictions are even more problematic due to unexpectedly

variable weather patterns in the last decade.

Figure 5 Yearly Demand Evolution in Greece

0

5

10

15

20

25

30

35

40

45

PPC Generation Third PartyGeneration

Imports

23,23

5,64

4,37

3,94

8,21

2,94

8,6

5,79

Electricity Generation and Imports in 2013

RES

Natural Gas

Oil

Hydroelectric

Lignite

GWh

42

44

46

48

50

52

54

56

58

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Yearly Demand Evolution in Greece

EnergyDemand

TWh

6

3. Transmission System

Generally, the backbone of the Greek transmission system has been a three line 400 kV system,

transporting power from the 5 coal factory sites in North Greece to the highly loaded area around

Athens. The system is dominated by overhead lines both in 400 kV and 150 kV levels on shore, while

some 150 and 66 kV cable systems are used for the interconnection of a limited number of islands.

Traditionally the system operator has faced problems due to this high imbalance between north and

south, especially during extended periods of very hot summers. However, it is claimed by the TSO

that the problem has been partially tackled with new grid infrastructure, increase of generation in

Southern Greece, and the increased introduction of RES locally.

Reactive power compensation takes places mainly in the MV side of step down substations with

static capacitor banks on the medium voltage side of the 150kV/MV substations (4200 MVar).

Compensation with shunt reactors is applied to submarine cable systems. No reference exists in the

TSO reports to the use of flexible AC transmission system schemes. The residential peak loads of

summer are mainly inductive, and create a need for reactive power compensation in the big city

centers. The TSO reports the installation of several PLC equipped automation systems, for the

optimal control of the installed capacitor banks. [1]

Most 150kV/MV step down and step up substations (Distribution, RES connection, conventional

plants connections) also belong to the TSO, apart from a small number in the area around Athens

(belonging to the DSO). All 400kV/150 kV step down and step up sites belong to the TSO.

Decreased demand and increase in the integration of RES has led to a decrease/postponement of

projects in the area of transmission systems (load demand related) especially concerning the large

cities. As a result, projects related with an additional 400kV line across the country as well as two

major HV substations have been postponed. Still however the 400kV system is being expanded in the

regions of Thrace and Peloponnesus, with the latter being really important to ensure system stability

and increase power transfers from the energy producing region. Some 150 kV lines constructions and

upgrades are being reported in order to integrate wind farms and new thermal power plants and

better service big city centers. The TSO reports high delays in a high number of projects due to lack of

public acceptance and a slow licensing procedure. It is repeatedly reported, that lack of public

acceptance is a significant obstacle in Greece transmission system projects.

Still various grid expansions and upgrades are essential for RES integration. Sources support that the

mainland electricity grid of the country can support the integration of 5000-5500 MW of wind power

capacity without major stability problems. Even so, the target of 7500 MW until 2020 will definitely

need major change in structure and operation of production and transmission. [3] Such projects have

already been described in the Ten Year National TSO plan of 2014. The TSO states that those

infrastructure projects will be enough to cover the power transmission tasks related with high RES

integration of 2020. [1] It is understood that the participation of the private sector in network

construction is very limited, as those projects are mostly assigned by the TSO to the PPC. An increase

of participation on the technical realization side as well as on the co-financing side of new projects

would benefit network reinforcement/expansion.

The TSO reports several projects related with constructing and upgrading HV lines and substations,

new line connections with nearby countries, projects for the connection to the system of new

customers and energy generators. The TSO is fully responsible for funding and realization of the first

7

two project categories and the cost is reflected to the fees paid by all the users of theTSO’s

infrastructure. For projects of the third category the relevant user is responsible for financing and the

implementation is either done by the TSO or the user. Either way after construction, the new

infrastructure belongs to the TSO in a form of a natural monopoly.

At the time of speaking, numerous RES projects have all the necessary licenses and an obligatory

allocation of transmission capacity from the TSO side but are not implemented. This results in

reservation of unused transmission capacity and a subsequent turning down of a high number of

further applications. In other regions high concentration of RES capacity threatens the transmission

capability. Regions that are considered very highly saturated are Evvoia, Thrace, Peloponnese, Kilkis

and numerous islands. Additionally, existence of saturated grids in areas of high potential, creates a

unwanted shift in investment towards areas of moderate or low wind potential [3].

The interconnection of more islands to the central system is also of high priority for the TSO, in order

to bring down costs and increase safety and reliability of supply. The interconnection of the island of

Crete is of extremely high importance due to the existence of significant loads and RES potential

locally, but is also considered expensive and technically challenging. It is considered to be completed

until the end 2019. Interconnection of some of the islands nearby to Athens is also a point of high

focus, and is expected to be completed until 2016. The autonomous island systems amount to 10% of

the total consumption and are considered very expensive and environmentally unfriendly (petrol).

Interconnection of autonomous islands would also be very beneficial due to their very high wind

potential.

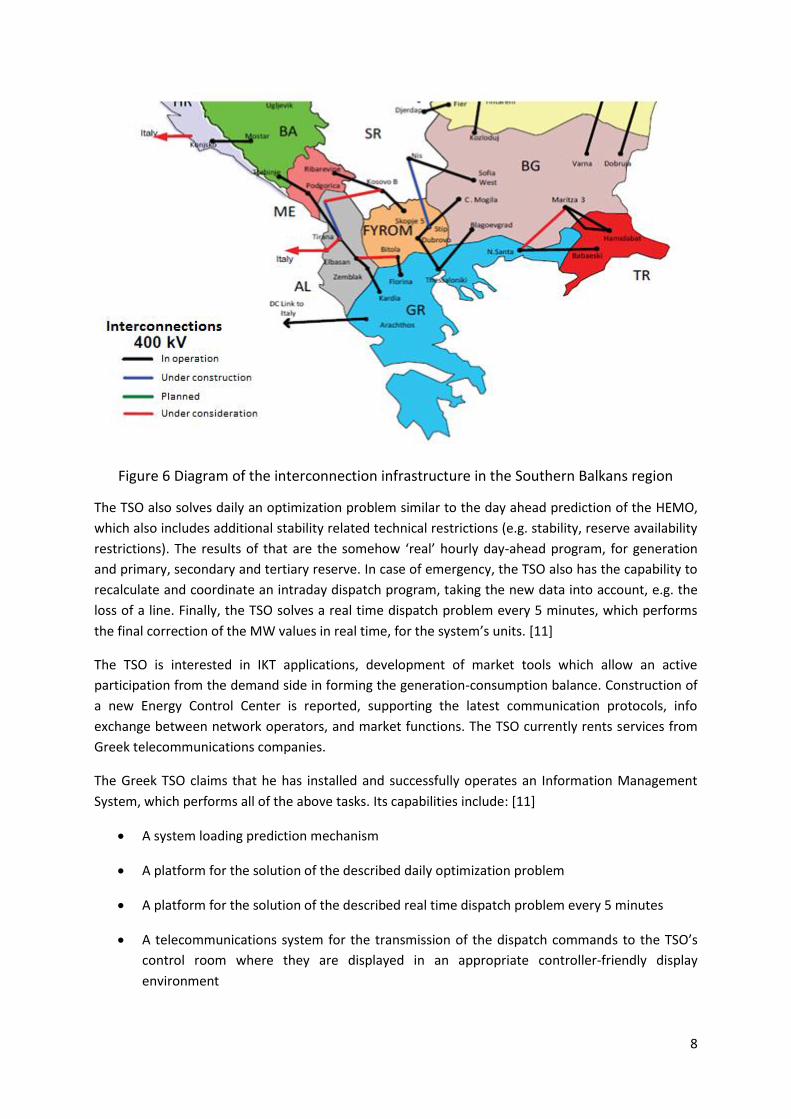

The Greek TSO is a member of ENTSO-E since 2004 and operates in synchronization with the

European interconnected system, which is also mainly responsible for generally guiding transmission

system planning after 2025. This is achieved by synchronized interconnection through (mainly) 400

kV lines with Albania, Macedonia, Bulgaria and recently Turkey, and unsynchronized interconnection

with Italy (submarine HVDC 500 MW cable). The Greek TSO has interest in the development of

interconnection projects in Southeastern Europe as well as the creation of transmission projects from

within the European continent. However, it is noted that the poor grid situation in the northern

neighboring countries are a significant restriction to the beneficial effect of interconnection. Existing

and planned 400 kV interconnections are depicted in Figure 6.

The ancillary services prescribed in the ENTSO-E are implemented by the TSO in coordination with

the energy producers. Those services include primary, secondary and tertiary frequency response

and backup availability. The TSO currently maintains a SCADA system, which is part of its Energy

Management System. Real time measurements of voltage and power flows from the system

substations are collected and used to perform the real time system state estimation process, the

results of whom are used along with results from load flow and voltage stability analysis tools in

various TSO coordination actions. The most common control action is reactive power compensation

with the target to dangerous voltage drops. Such drops are usually encountered through

disconnection of reactor banks, energizing of static capacitor banks in MV and then in HV, control

actions for synchronous compensation units (not FACTS) and changes in the positions of

autotransformers taps, in that specific order. Other collected information is related to the availability

and operating condition of generation units, availability of interconnections and possible important

issues of the distribution grid side. [11]

8

Figure 6 Diagram of the interconnection infrastructure in the Southern Balkans region

The TSO also solves daily an optimization problem similar to the day ahead prediction of the HEMO,

which also includes additional stability related technical restrictions (e.g. stability, reserve availability

restrictions). The results of that are the somehow ‘real’ hourly day-ahead program, for generation

and primary, secondary and tertiary reserve. In case of emergency, the TSO also has the capability to

recalculate and coordinate an intraday dispatch program, taking the new data into account, e.g. the

loss of a line. Finally, the TSO solves a real time dispatch problem every 5 minutes, which performs

the final correction of the MW values in real time, for the system’s units. [11]

The TSO is interested in IKT applications, development of market tools which allow an active

participation from the demand side in forming the generation-consumption balance. Construction of

a new Energy Control Center is reported, supporting the latest communication protocols, info

exchange between network operators, and market functions. The TSO currently rents services from

Greek telecommunications companies.

The Greek TSO claims that he has installed and successfully operates an Information Management

System, which performs all of the above tasks. Its capabilities include: [11]

A system loading prediction mechanism

A platform for the solution of the described daily optimization problem

A platform for the solution of the described real time dispatch problem every 5 minutes

A telecommunications system for the transmission of the dispatch commands to the TSO’s

control room where they are displayed in an appropriate controller-friendly display

environment

9

An automated generation control unit, automatically regulating units that allow a distant

control of their real power generation

State estimation software

A SCADA system, its relevant control system and relevant databases

The participants in the electric market can also connect through the internet to a part of this system

related with interchange of information regarding the energy market. The TSO apart from internet

and telephone communication, utilizes a power line carrier option allowing uninterruptible

communication with the users and the DSO. The TSO is responsible for defining the alarm state and

implement the necessary countermeasures in case of emergency of the system.

4. RES information

The amount of production by RES in the share of national final energy consumption is set at 18% for

2020 by EU Directive 2009/28/EC. The Greek Parliament has turned the Directive into a law, setting a

target of 40% for RES electricity compared to the gross national electricity consumption for 2020.

At the end of 2012, RES contributed around 26% of electricity demand, with 11% from large

hydropower, 7% wind, 8% from photovoltaic plants, small hydro (run of river) and biogas. It is

reported that the already interconnected capacity of RES generation does not overcome the 2014

mid-targets of the 2020 plan. [1] On PV, the situation is far more better, with the operating and

planned-to-be-connected capacity already overcoming the target for 2020. This is attributed to the

previously existing support scheme on PV, the decreased PV projects development cost and a

decrease in burocrasy for licensing, especially for installations <100kW. [2] The high penetration of

PV is expected to affect the loading patterns for the transmission system, with the loading peaks for

the grid shifting towards the night hours. There are reported effects from wind farm surplus during

the night and/or midday peaks due to PV. [1] As of 2014, nooffshore wind parks exist in Greece [2].

RES integration has created the need for distributed, quickly dispachable, conventional fuel units to

cover the changing demand as well as the need for more pumping stations on existing hydropower

plants. The TSO recognizes the need for changes in operational level to ensure safety in a system

with high RES penetration without further comments. [1] Other sources also suggest the need for

more availability of such dispatchable plants in order to work in close collaboration with the wind

farms. Since significant investment in gas fired power plants already exists today, it remains to be

seen how this issue will evolve and how the classic problems from the coordination of gas and RES

that occurred in central Europe will be tackled in the Greek system.

Wind farms are usually connected at the 150 kV voltage level. The main investment in windpower is

in non-dispersed high power units with a capacity in the range of 20 MW. Smaller wind farms in the

area of 8 MW and small hydroelectric plants under 5 MW are connected in MV. There is very high

potential for small hydropower plants in the mountain regions, but the distances are prohibiting for

installation of new MV lines. The Greek TSO has licensed projects on renewable energy for more than

25 GW totally. At the end of 2013, however only 3,9 GW were installed. The Greek TSO claims that

the sum of the RES projectsunder the status of Binding Connection Offers will be sufficient in order to

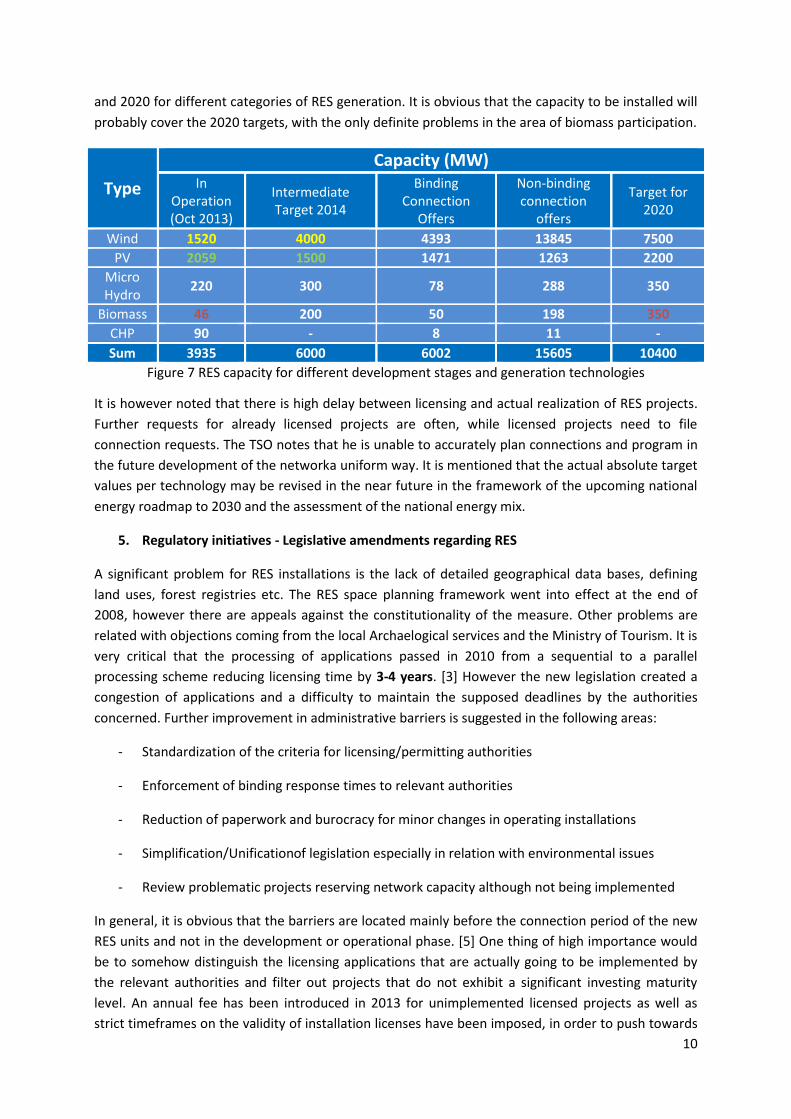

cover the targets of 2020. Figure 7shows the already installed capacity, the capacity of RES projects

under Binding and Non-Binding Connection Offers in comparison with the target capacity for 2014

10

and 2020 for different categories of RES generation. It is obvious that the capacity to be installed will

probably cover the 2020 targets, with the only definite problems in the area of biomass participation.

Type

Capacity (MW)

In Operation (Oct 2013)

Intermediate Target 2014

Binding Connection

Offers

Non-binding connection

offers

Target for 2020

Wind 1520 4000 4393 13845 7500

PV 2059 1500 1471 1263 2200

Micro Hydro

220 300 78 288 350

Biomass 46 200 50 198 350

CHP 90 - 8 11 -

Sum 3935 6000 6002 15605 10400

Figure 7 RES capacity for different development stages and generation technologies

It is however noted that there is high delay between licensing and actual realization of RES projects.

Further requests for already licensed projects are often, while licensed projects need to file

connection requests. The TSO notes that he is unable to accurately plan connections and program in

the future development of the networka uniform way. It is mentioned that the actual absolute target

values per technology may be revised in the near future in the framework of the upcoming national

energy roadmap to 2030 and the assessment of the national energy mix.

5. Regulatory initiatives - Legislative amendments regarding RES

A significant problem for RES installations is the lack of detailed geographical data bases, defining

land uses, forest registries etc. The RES space planning framework went into effect at the end of

2008, however there are appeals against the constitutionality of the measure. Other problems are

related with objections coming from the local Archaelogical services and the Ministry of Tourism. It is

very critical that the processing of applications passed in 2010 from a sequential to a parallel

processing scheme reducing licensing time by 3-4 years. [3] However the new legislation created a

congestion of applications and a difficulty to maintain the supposed deadlines by the authorities

concerned. Further improvement in administrative barriers is suggested in the following areas:

- Standardization of the criteria for licensing/permitting authorities

- Enforcement of binding response times to relevant authorities

- Reduction of paperwork and burocracy for minor changes in operating installations

- Simplification/Unificationof legislation especially in relation with environmental issues

- Review problematic projects reserving network capacity although not being implemented

In general, it is obvious that the barriers are located mainly before the connection period of the new

RES units and not in the development or operational phase. [5] One thing of high importance would

be to somehow distinguish the licensing applications that are actually going to be implemented by

the relevant authorities and filter out projects that do not exhibit a significant investing maturity

level. An annual fee has been introduced in 2013 for unimplemented licensed projects as well as

strict timeframes on the validity of installation licenses have been imposed, in order to push towards

11

quick realization of RES projects. In the same direction, laws allowing overcoming the congestion

limit by 20% from the TSO when granting connection offers have been enacted. The effect of those

measures is not yet clear. [2]

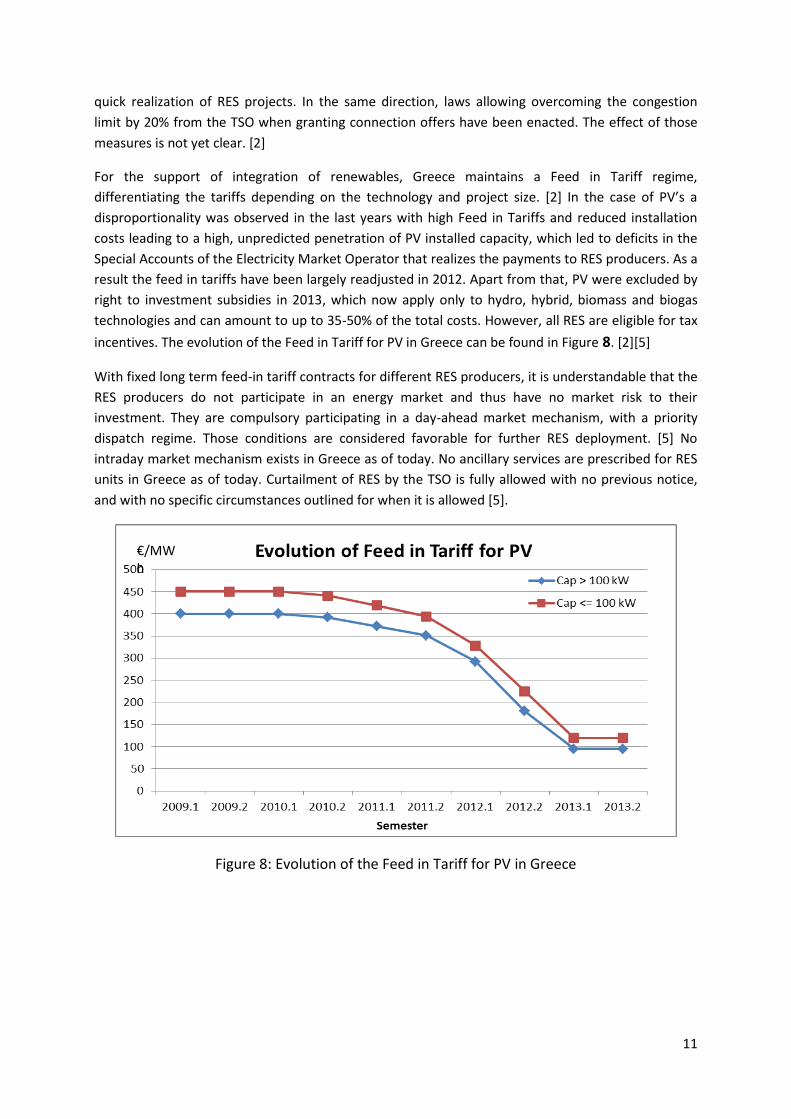

For the support of integration of renewables, Greece maintains a Feed in Tariff regime,

differentiating the tariffs depending on the technology and project size. [2] In the case of PV’s a

disproportionality was observed in the last years with high Feed in Tariffs and reduced installation

costs leading to a high, unpredicted penetration of PV installed capacity, which led to deficits in the

Special Accounts of the Electricity Market Operator that realizes the payments to RES producers. As a

result the feed in tariffs have been largely readjusted in 2012. Apart from that, PV were excluded by

right to investment subsidies in 2013, which now apply only to hydro, hybrid, biomass and biogas

technologies and can amount to up to 35-50% of the total costs. However, all RES are eligible for tax

incentives. The evolution of the Feed in Tariff for PV in Greece can be found in Figure 8. [2][5]

With fixed long term feed-in tariff contracts for different RES producers, it is understandable that the

RES producers do not participate in an energy market and thus have no market risk to their

investment. They are compulsory participating in a day-ahead market mechanism, with a priority

dispatch regime. Those conditions are considered favorable for further RES deployment. [5] No

intraday market mechanism exists in Greece as of today. No ancillary services are prescribed for RES

units in Greece as of today. Curtailment of RES by the TSO is fully allowed with no previous notice,

and with no specific circumstances outlined for when it is allowed [5].

Figure 8: Evolution of the Feed in Tariff for PV in Greece

€/MWh

12

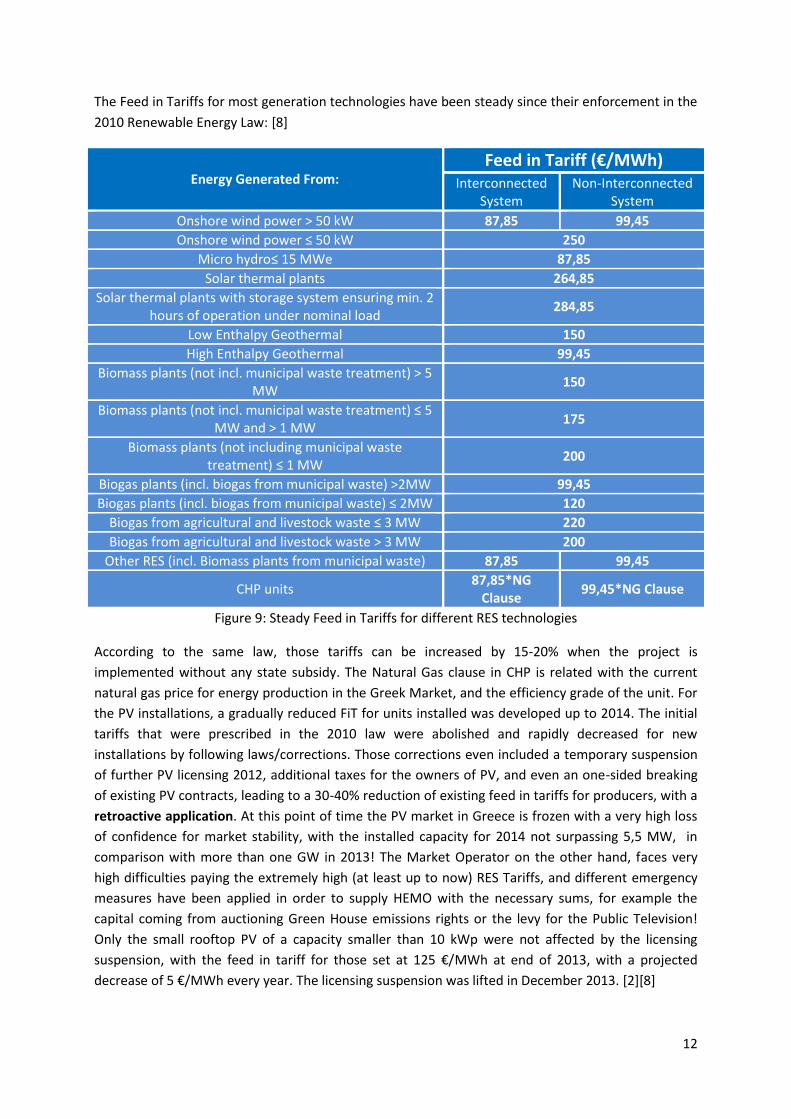

The Feed in Tariffs for most generation technologies have been steady since their enforcement in the

2010 Renewable Energy Law: [8]

Energy Generated From: Feed in Tariff (€/ΜWh)

Interconnected System

Non-Interconnected System

Onshore wind power > 50 kW 87,85 99,45

Onshore wind power ≤ 50 kW 250

Micro hydro≤ 15 ΜWe 87,85

Solar thermal plants 264,85

Solar thermal plants with storage system ensuring min. 2 hours of operation under nominal load

284,85

Low Enthalpy Geothermal 150

High Enthalpy Geothermal 99,45

Biomass plants (not incl. municipal waste treatment) > 5 MW

150

Biomass plants (not incl. municipal waste treatment) ≤ 5 MW and > 1 MW

175

Biomass plants (not including municipal waste treatment) ≤ 1 MW

200

Biogas plants (incl. biogas from municipal waste) >2MW 99,45

Biogas plants (incl. biogas from municipal waste) ≤ 2MW 120

Biogas from agricultural and livestock waste ≤ 3 MW 220

Biogas from agricultural and livestock waste > 3 MW 200

Other RES (incl. Biomass plants from municipal waste) 87,85 99,45

CHP units 87,85*NG

Clause 99,45*NG Clause

Figure 9: Steady Feed in Tariffs for different RES technologies

According to the same law, those tariffs can be increased by 15-20% when the project is

implemented without any state subsidy. The Natural Gas clause in CHP is related with the current

natural gas price for energy production in the Greek Market, and the efficiency grade of the unit. For

the PV installations, a gradually reduced FiT for units installed was developed up to 2014. The initial

tariffs that were prescribed in the 2010 law were abolished and rapidly decreased for new

installations by following laws/corrections. Those corrections even included a temporary suspension

of further PV licensing 2012, additional taxes for the owners of PV, and even an one-sided breaking

of existing PV contracts, leading to a 30-40% reduction of existing feed in tariffs for producers, with a

retroactive application. At this point of time the PV market in Greece is frozen with a very high loss

of confidence for market stability, with the installed capacity for 2014 not surpassing 5,5 MW, in

comparison with more than one GW in 2013! The Market Operator on the other hand, faces very

high difficulties paying the extremely high (at least up to now) RES Tariffs, and different emergency

measures have been applied in order to supply HEMO with the necessary sums, for example the

capital coming from auctioning Green House emissions rights or the levy for the Public Television!

Only the small rooftop PV of a capacity smaller than 10 kWp were not affected by the licensing

suspension, with the feed in tariff for those set at 125 €/ΜWh at end of 2013, with a projected

decrease of 5 €/ΜWh every year. The licensing suspension was lifted in December 2013. [2][8]

13

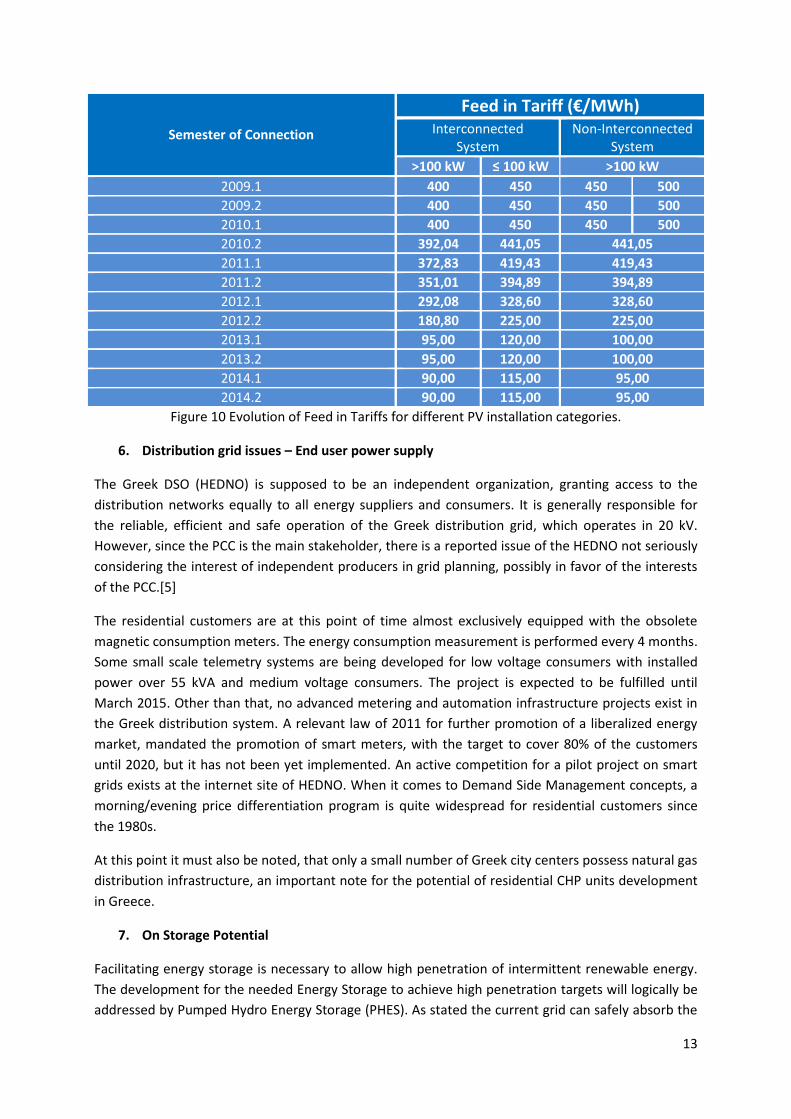

Semester of Connection

Feed in Tariff (€/ΜWh)

Interconnected System

Non-Interconnected System

>100 kW ≤ 100 kW >100 kW

2009.1 400 450 450 500

2009.2 400 450 450 500

2010.1 400 450 450 500

2010.2 392,04 441,05 441,05

2011.1 372,83 419,43 419,43

2011.2 351,01 394,89 394,89

2012.1 292,08 328,60 328,60

2012.2 180,80 225,00 225,00

2013.1 95,00 120,00 100,00

2013.2 95,00 120,00 100,00

2014.1 90,00 115,00 95,00

2014.2 90,00 115,00 95,00

Figure 10 Evolution of Feed in Tariffs for different PV installation categories.

6. Distribution grid issues – End user power supply

The Greek DSO (HEDNO) is supposed to be an independent organization, granting access to the

distribution networks equally to all energy suppliers and consumers. It is generally responsible for

the reliable, efficient and safe operation of the Greek distribution grid, which operates in 20 kV.

However, since the PCC is the main stakeholder, there is a reported issue of the HEDNO not seriously

considering the interest of independent producers in grid planning, possibly in favor of the interests

of the PCC.[5]

The residential customers are at this point of time almost exclusively equipped with the obsolete

magnetic consumption meters. The energy consumption measurement is performed every 4 months.

Some small scale telemetry systems are being developed for low voltage consumers with installed

power over 55 kVA and medium voltage consumers. The project is expected to be fulfilled until

March 2015. Other than that, no advanced metering and automation infrastructure projects exist in

the Greek distribution system. A relevant law of 2011 for further promotion of a liberalized energy

market, mandated the promotion of smart meters, with the target to cover 80% of the customers

until 2020, but it has not been yet implemented. An active competition for a pilot project on smart

grids exists at the internet site of HEDNO. When it comes to Demand Side Management concepts, a

morning/evening price differentiation program is quite widespread for residential customers since

the 1980s.

At this point it must also be noted, that only a small number of Greek city centers possess natural gas

distribution infrastructure, an important note for the potential of residential CHP units development

in Greece.

7. On Storage Potential

Facilitating energy storage is necessary to allow high penetration of intermittent renewable energy.

The development for the needed Energy Storage to achieve high penetration targets will logically be

addressed by Pumped Hydro Energy Storage (PHES). As stated the current grid can safely absorb the

14

energy of WF capacity in the area of 5 GW. Even for this restricted amount, increased curtailments

will be unavoidable, exceeding 20% in 2020 scenarios, calling for installation of sufficient storage

capacity. [6] The author of [6] supports pumped storage as the most realistic, reliable and mature

technology for large scale systems in Greece. The probability of the utilization of Battery Storage

Systems remains unknown. For the targets of 2020 at least 1GW of PHES capacity is required

(existing 0.7 GW) by the existing national roadmap directives. The author of [6] considers this

amount insufficient and believes that it will not be able to absorb more than 25% of the excess

energy on 2020.

Bibliography:

[1]: Independent Power Transmission Operator,Ten Year Network Development Plan 2014-2023,

March 2013.

[2]: Ministry of Environment Energy and Climate Change, Second Progress Report on the Promotion

and Use of Energy from Renewable Sources in Greece, 2014

[3]: Greek Association of RES electricity producers, Overcoming RES Permitting and Grid Access

Barriers in Greece, January 2012

[4]: ArthourosZervos: Chairman & Chief Executive Officer of PPC, Annual Ordinary General Meeting

of Shareholders, June 2014

[5]: Eclareon GmbH, Öko-Institute.V., Integration of electricity from renewables to the electricity grid

and to the electricity market – RES Integration, March 2012

[6]: John Anagnostopoulos, Dimitris Papantonis, Overview of the electricity system status and its

future development scenarios – Assessment of the energy storage needs, February 2013

[7]: Nikolaos Danias, John Kim Swales, Peter McGregor: The Greek Electricity Market Reforms:

Political and Regulatory Considerations, July 2013

[8]: The Greek Goverment, Law3851/2010: Accelerating the development of Renewable Energy to

address climate change and other provisions relating to the jurisdiction of the Ministry of

Environment, Energy and Climate Change, June 2010,

[9]: The Greek Goverment, Law3851/2011: On the operation of Energy Markets for electricity and

gas in the areas of research, production and transmission of Hydrocarbons and other settings, August

2011

[10]: Hellenic Electric Market Operator: Electric Power Transactions Code Manual, August 2013

[11]: Independent Power Transmission Operator: Dispatch Manual, November 2012

Related Documents