THE AMERICAN BUSINESS COUNCIL OF PAKISTAN Facilitating Trade & Investment since 1984 Proposals for the consideration of The Government of Pakistan

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

THE AMERICAN BUSINESS COUNCIL OF PAKISTAN

Facilitating Trade & Investment since 1984

Proposals for the consideration of

The Government of Pakistan

Table of Contents

ABC Profile

Executive Committee Members

Agenda

Proposals by the Finance & Taxation Subcommittee

Proposals by the Industry, Trade & Logistics Subcommittee

Proposals by the Pharmaceuticals & Chemicals Subcommittee

Proposals by the IT & Innovation Subcommittee

Page 2

The core objective of The American Business Council of Pakistan is to provide a solid and dynamic platform for American Investors to leverage the vast business and economic potential that Pakistan has to offer. We are an independent, not-for-profit organization; enabling US investors in the country to collaborate since 1984.

The ABC works closely with all the relevant stakeholders, including the Government of Pakistan and the US Mission, for American Investors to help formulate Policy which is conducive to business and economic growth as well as the overall prosperity of the country. We protect and promote the interests of our members in the form of recommendations to the country’s Trade Policy, proposals for the Federal Budget, and high-profile meetings with Government officials and the US Embassy.

At the American Business Council, we are always looking ahead to the future in order to be effective and deliver impactful outcomes. Our strategy is based on a three-pronged approach:

Fostering Advocacy – dialoguing with our partners and stakeholders towards issue management and better policies.

Developing Alliances- internally, within the American business community, and externally with stakeholders in government and trade to harness cooperation and consensus;

Promoting Awareness – sharing best practices and research, as well as raising key issues that need addressing to ensure a more robust business environment;

Through this approach we believe, we are well-poised to deliver meaningful change and economic and social value to our businesses, communities, and Pakistan at large.

For over three decades, The Council has been the voice of more than 60 members, most of which are Fortune 500 companies. The United States consistently ranks among the top resources of Foreign Direct Investment (FDI) in Pakistan, and ABC members account for a significant share in that investment. More importantly, ABC Members adhere to high standards of corporate governance and transparency, and they bring cutting edge technologies and best practices to Pakistan.

Business and Trade ties are important to our shared prosperity. We want American companies to invest and thrive in Pakistan. The ABC strives to make this a reality. We’ve worked – and continue to work – to establish a level-playing field for American companies, protect US investors and promote commerce between the United States and Pakistan.

BRIEF OVERVIEW

Page 3

AmericanBusinessCouncilP A K I S T A N

The American Business Council of Pakistan

Asif Peer President The American Business Council of Pakistan

Member Company Systems Ltd.Chief Executive Officer

Company ProfileSystems Limited is a global leader of next-generation IT services and BPO solutions.

Tushna D. KandawallaMember Executive CommitteeThe American Business Council of Pakistan

Member CompanyCaptain-PQ Chemical Industries (Pvt.) Ltd.CEO

Company ProfileCaptain Industries is a leading producer of Silicates in Pakistan. Founded in 1951 in Karachi, the company today has several manufacturing facilities serving local and global customers.

Jamshed SafdarVice PresidentThe American Business Council of Pakistan

Member CompanyUniversal Logistics Services (Pvt.) Ltd/UPS Chief Executive Officer

Company ProfileUnited Parcel Service is a global leader in logistics, offering a broad range of solutions including the transportation of packages, freight, and the facilitation of international trade.

S.M. WajeehuddinSenior Vice President The American Business Council of Pakistan

Member CompanyPfizer Country Manager & Chief Executive Officer

Company ProfilePfizer is the world’s premier biopharmaceutical company engaging in the business of discovering innovative solutions to health

Page 4

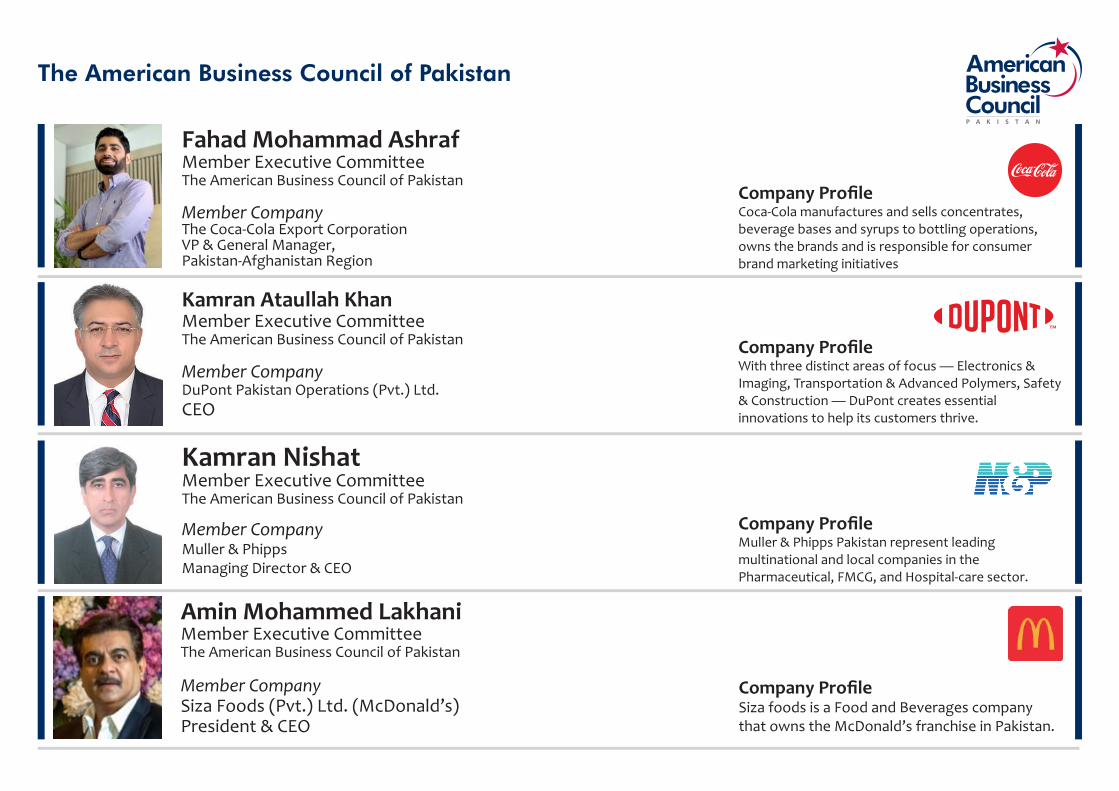

Amin Mohammed LakhaniMember Executive CommitteeThe American Business Council of Pakistan

Member CompanySiza Foods (Pvt.) Ltd. (McDonald’s)President & CEO

Company ProfileSiza foods is a Food and Beverages company that owns the McDonald’s franchise in Pakistan.

The American Business Council of Pakistan AmericanBusinessCouncilP A K I S T A N

Kamran Ataullah KhanMember Executive CommitteeThe American Business Council of Pakistan

Member CompanyDuPont Pakistan Operations (Pvt.) Ltd.CEO

Company ProfileWith three distinct areas of focus — Electronics & Imaging, Transportation & Advanced Polymers, Safety & Construction — DuPont creates essential innovations to help its customers thrive.

Fahad Mohammad AshrafMember Executive CommitteeThe American Business Council of Pakistan

Member CompanyThe Coca-Cola Export CorporationVP & General Manager, Pakistan-Afghanistan Region

Company ProfileCoca-Cola manufactures and sells concentrates, beverage bases and syrups to bottling operations, owns the brands and is responsible for consumer brand marketing initiatives

Kamran NishatMember Executive CommitteeThe American Business Council of Pakistan

Member Company Muller & PhippsManaging Director & CEO

Company ProfileMuller & Phipps Pakistan represent leading multinational and local companies in the Pharmaceutical, FMCG, and Hospital-care sector.

Page 5

Adnan AsadImmediate Past PresidentThe American Business Council of Pakistan

Member Company Venus Pakistan Chief Executive Officer

Nadeem Arshad ElahiMember Executive CommitteeThe American Business Council of Pakistan

Member CompanyTRG (Pvt.) Ltd. Managing Director & Country Head

Sami AhmedMember Executive CommitteeThe American Business Council of Pakistan

Member CompanyProcter & Gamble Pakistan (Pvt.) Ltd.Vice President

Ahmed Jamal MirMember Executive CommitteeThe American Business Council of Pakistan

Member CompanyPrestige Communications Managing Director & Chief Executive Officer

Company ProfileVenus group offers Freight Consolidation in USA, Clearing Warehouse facilities, direct distribution and are Master Franchisees of Texas Chicken and Cold Stone Creamery.

Company ProfileThe Resource Group (TRG) is an investment holding company specializing in the business process outsourcing sector.

Company ProfileProcter & Gamble (P&G) is the world's largest consumer goods company, home to 65 individual brands organized into the following categories: Fabric care, home care, baby care, feminine care, family care, grooming, oral care, personal healthcare and hair, skin & personal care.

Company ProfilePrestige is one of the oldest advertising agencies in Pakistan offering full service to an array of national and multinational clients.

The American Business Council of Pakistan AmericanBusinessCouncilP A K I S T A N

Page 6

Finance & Taxation

1. Mandating Digital Transactions beyond a certain amount

Mandate digital transactions through digital channels for transactions beyond a certain size e.g., Rs. 50,000. This

will enable FBR to have visibility into spending patterns in the market, without having to go through physical audit

of the company. Otherwise, remove the requirement for retaining a copy of CNIC from customers that perform

their transactions electronically.

2. Liability on Manufacturer Where a registered person supplies 3rd schedule (MRSP) to unregistered person in sales tax and Inactive in income tax, Supplier will be penalized rather than buyer. The responsibility of registration of unregistered and inactive person should not be the responsibility of compliant taxpayer. It is proposed to remove this penalty from registered persons.

3. Illicit cigarette Trade and Excise Duty

Moderate excise duty increase is proposed for this year coupled with increased enforcement by the multi-agency

task force (Inland Revenue Enforcement Network, Customs Enforcement and I&I) to bring the non-tax paying

manufacturers into the tax net.

4. Reduce Sales Tax on payments made through Credit Cards Merchants discourage card sale to evade taxes and hide true sales. There is no incentive to merchant to promote digitization of the economy. We propose a certain rebate to be given to merchants and the customer for accepting and using digital means of payments.

5. Federal Excise Duty on Merchant Discount Rate (MDR)

Adding FED on top of MDR further aggravates the value proposition around digital payments. FBR is requested to

waive of FED on MDR for the next 5 years to ensure adoption of digital means of payments.

Agenda

Page 7

Finance & Taxation

6. Withholding Tax amount before the actual remittance to Non-residents

The time period for deposit of withholding tax should be made consistent with local payments or at the most

reduced to the same date as the date of payment to non-resident.

7. Annual Certificate for withholding agents Rule 42, Income Tax Rules 2002

Post Finance Act 2013, such certificates are not sufficient evidence of tax collection or deduction unless it is

accompanied by CPRN. However, due to this rule the vendors require and oblige the withholding agents to issue

annual certificate of collection or deduction of income tax by virtue of the said rule. Such requirement should be

deleted.

8. Tax Amortization Period for Intangibles Intangible Assets (Intellectual properties) are main assets of IT companies, hence reduction in amortization expense due to increased useful life over which expenses shall be allowed, would significantly impact taxable profit and tax liability.

9. Exemption on COVID related products The situation of COVID is ongoing. Previously, Government granted tax exemption on import of COVID related products and extended the same for 3 months. But after September 2020, the exemption is not further granted which is ultimately increasing the price for consumer.

10. Withholding Tax on Distributors

Distribution is a high turnover business with low margins. It is recommended that the rates should be reduced by

50% and made adjustable from the minimum tax liability to ensure no revenue impact to exchequer.

Agenda

Page 8

Finance & Taxation

11. Disallowance of Input Sales Tax

Section 73(4) of the Sales Tax Act 1990 provides a threshold on taxable sales to be made to an unregistered person

i.e. Rs.10 million in a tax period or in aggregate Rs.100 million in a financial year. This provision is oppressive and is

restricting the business activity of a registered person which can result in lower collection of tax. The restriction

should be removed for registered persons.

12. Regulatory Duties on Raw and Packing Materials

Regulatory duty on certain items of raw and packing materials has been imposed due to which cost of local

production goes up for manufacturers. Regulatory duty on items of raw and packing material directly imported by

manufacturers/industrial consumers should be abolished.

13. Import Valuation

WTO guidelines should be followed for determination of custom valuation in all cases and a valuation should only

be used where there is ample evidence of under invoicing. Valuation ruling should also be made on case-to-case

basis and not on the entire class of products.

14. Tax Credit on Balancing, Modernization and Replacement – Section 65BTax credit u/s 65B should be restored as it promotes foreign direct investments in addition to incentivizing the local taxpayers into investing in long term capital projects.

15. Royalty Payments Royalty payments have been capped at 5% for over 15 years. They should be increased to 7-8%.

Agenda

Page 9

Industry, Trade & Logistics

16. Adjustment of input tax restricted for the manufacturers who are selling their product to unregistered distributors under Sales Tax Act. Since FBR has the complete data of the distributors of every registered manufacturer, they can easily register them on their own without putting implications / pressure on the manufacturers. Moreover, it has also suggested to exclude the items which fall under 3rd schedule of the Sales Tax Act.

17. 75% of Dealer Margin to be added towards Taxable Income of Manufacturer if dealer is not registered and active taxpayer with Federal Board of Revenue under Income Tax and Sales Tax. The responsibility should not lie with the manufacturer, which is already bringing the investment in the country and generating revenue for tax authorities.

18. To avert sugar crisis in Pakistan, allow sugar import for beverage industry, duty & tax free throughout the year by making it part of the Federal Budget 2021-2022 and do not ban sugar procurement from local sugar mills for industries.

19. Permit Branches of International Insurers / Attract FDI in Insurance Sector: Currently a Draft Insurance Ordinance (Amendment) Bill, 2020, has been proposed by SECP. The proposed amendments allow branches of foreign insurers to operate in Pakistan. We recommend that the matter is timely progressed and actioned as a Draft Insurance Bill has been pending since 2016.

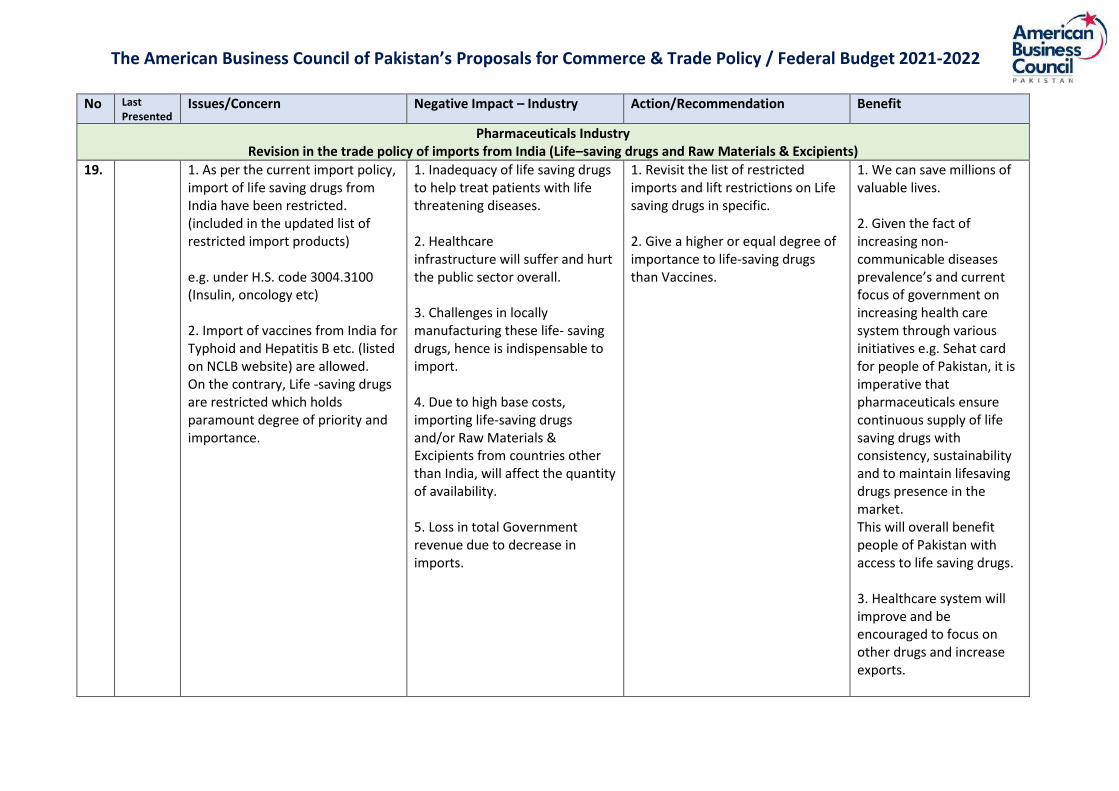

20. As per the current import policy, import of life saving drugs from India have been restricted. It is proposed to revisit the list of restricted imports, lift restrictions on Life saving drugs in specific, and give a higher or equal degree of importance to life-saving drugs.

Information Technology

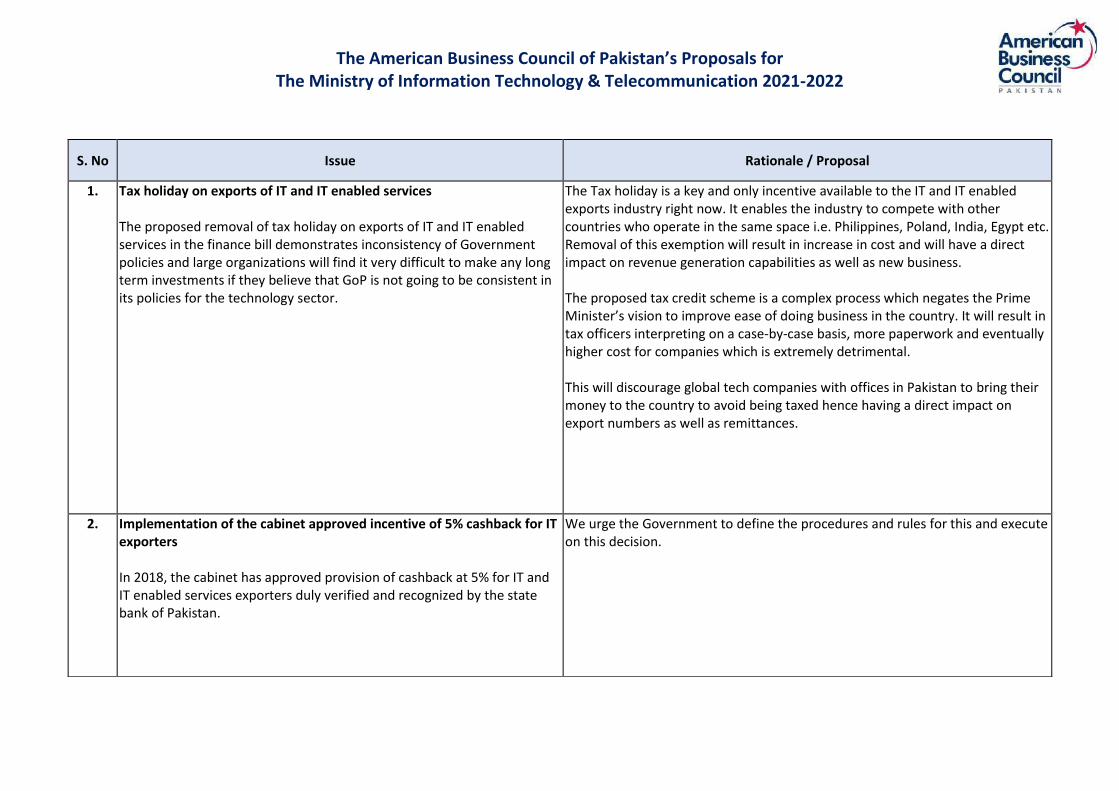

21. The proposed removal of tax holiday on exports of IT and IT enabled services in the finance bill demonstrates inconsistency of Government policies which discourages long-term investments. Removal of this exemption will result in increase in cost and will therefore have a direct impact on revenue generation capabilities as well as new businesses.

Agenda

Page 10

AgendaPharmaceuticals

22. Consistent application of a practical Pricing Regime.

23. Speedy registration/approval of new medicines: Drugs already approved by Stringent Regulatory Authorities(SRAs) should be granted speedy approval. These medicines have been extensively reviewed and evaluated by the respective SRA(s) before approval, and little value addition is expected if they go thru the same detailed process at DRAP also.

24. Patent enforcement: Approvals to generics should not be granted for molecules where originators have valid patents.

Overseas Investment

25. To encourage American citizens of Pakistan origin to invest in projects, real estate and set up bank accounts: it is suggested to change the Pakistan resident status from 3 months to 6 months (preferably 9 months); this adjustment will certainly encourage the diaspora to look towards Pakistan as a preferred investment opportunity.

26. Remove the requirements of no objection certificate, for American citizens of Pakistan origin to invest, set up and operate business in Pakistan. Any Pakistan origin citizen should be able to select his field of business just like a local Pakistan citizen. As a reference today, aviation, security, operating in cantonment zones, port related activities have a requirement of NOC.

27. To develop tourism and encourage large resort operators to invest, the government must redress the civil aviation rules and encourage foreign registered aircraft to operate in Pakistan and set up green fields/ private landing strips to develop this industry.

28. Resort properties are capital and labor intensive, to attract American operators to invest in this area, the state bank needs to offer concessional finance for 10-15 years. It is recommended that these loans are capped at 3%.

29. The TERF finance facility has been a great success, it is recommended to extend this offer through the end of 2021.

Agenda

Page 11

For the consideration of:Ministry of Finance Federal Board of Revenue (FBR)

Proposals by:The Finance & Taxation Subcommittee of The American Business Council of Pakistan

Chairman: Mr. Kamran Nishat

Page 12

The American Business Council of Pakistan’s Proposals for Ministry of Finance & FBR (Federal Board of Revenue) Federal Budget 2021-2022

We are pleased to share The American Business Council’s (ABC) proposals for the upcoming Federal Budget 2021-2022. The

proposals aim to boost investments and increase Government revenue by creating a level playing field as well as enhancing the

ease of doing business. ABC continues to play a key role in proposing economic and taxation measures for the improvement of

prevailing economic conditions and stable growth of the economy.

One of the key challenges that Pakistan faces is significantly low tax to GDP ratio. It is, therefore, imperative that the tax base of

the country must be broadened so that all segments of the economy pay their due share of taxes according to their contribution in

GDP. It is also pertinent that interests of bonafide taxpayers be safeguarded against excessive burden of high taxes (both direct &

indirect). ABC continues to strive for a robust, business friendly and transparent taxation environment and in this regard, we believe:

▪ Documentation of economy is critical for broadening of the tax base.

▪ Tax laws, procedures and regulations must be drafted precisely and clearly so that taxpayers understand their tax mandate.

▪ Moderate tax rates promote tax compliance and reduce the incidence and incentives for tax evasion; and

▪ Reliance on direct taxes should be increased as it will help in taxing the richer and will result in fair and equitable distribution

of wealth.

ABC welcomes an ongoing dialogue to help contribute towards the economic growth of the country.

Let us together make Pakistan a prosperous country.

Kamran Nishat Chairman - Finance & Taxation Subcommittee

Page 13

The American Business Council of Pakistan’s Proposals for Ministry of Finance & FBR (Federal Board of Revenue) Federal Budget 2021-2022

S. No Last Presented

Section / Clause / Rule

Proposed Amendment Rationale Revenue Impact

Broadening of Tax Base for a wider participation in revenue generation efforts

1. 2020-2021 Income Tax Ordinance 2001

Mandating digital transactions beyond a certain size e.g., Rs. 50,000 FBR had earlier mandated that any transaction beyond Rs. 50,000 would require the merchant to retain a CNIC. It may be noted that the same can be achieved if the transaction is done digitally. If a transaction is performed digitally banks have complete record of who performed the transaction at which merchant location. This will enable FBR to have visibility into spending patterns in the market, with out having to go through physical audit of the company. Mandate digital transactions through digital channels for transactions beyond a certain size e.g., Rs. 50,000. Or remove the requirement for retaining a copy of CNIC from customers that perform their transactions electronically.

By having a digital transaction FBR can ask banks to provide the CNIC Numbers against the account used to perform any particular transaction. This can bring FBR generic industry wide access instead of having to go through individual record of merchants. Furthermore, it will also protect merchants/customers from the hassle of providing and maintaining a record of CNICs.

Yes / Positive

2. 108B of the Income Tax Ordinance 2001

Liability on Manufacturer 75% of Dealer Margin to be added towards Taxable Income of Manufacturer if dealer is not registered and active taxpayer with Federal Board of Revenue under Income Tax and Sales Tax.

The responsibility should not lie with the manufacturer, which is already bringing the investment in the country and generating revenue for tax authorities. Such measures may lose the investor confidence, as the international investors are already working towards their business continuity due to fluid tax regime.

Yes / Negative

Page 14

The American Business Council of Pakistan’s Proposals for Ministry of Finance & FBR (Federal Board of Revenue) Federal Budget 2021-2022

S. No Last Presented

Section / Clause / Rule

Proposed Amendment Rationale Revenue Impact

Broadening of Tax Base for a wider participation in revenue generation efforts

3. FED Law Illicit cigarette Trade and Excise Duty The tobacco industry faces a critical challenge with the wide presence of duty-not-paid cigarettes. While contributing only 2% in tobacco excise revenues they have a market share of approx. 40%. Excessive taxation widens the price gap between tax-paid and non-tax paid cigarettes, shifting legal consumption to non-tax paid illicit cigarettes, thus negatively impacting cigarette excise revenue. Moderate excise duty increase is proposed for this year coupled with increased enforcement by the multi-agency task force (Inland Revenue Enforcement Network, Customs Enforcement and I&I) to bring the non-tax paying manufacturers into the tax net.

This will help the government to recover the lost government revenues of more than PKR 70 billion annually and encourage foreign investment.

Yes / Positive

4. Sales Tax Act 1990 Reduce Sales Tax on payments made through Credit Cards Merchants discourage card sale to evade taxes and hide true sales. There is no incentive to merchant to promote digitization of the economy, in fact they fear being taxed. We propose a certain rebate to be given to merchants and the customer for accepting and using digital means of payments. e.g., Punjab Revenue board reduced Sales tax at Restaurants to 5% if a payment was made through card.

Retailers will discourage cash sales and push customers to pay via their cards. Similarly, customers will also push for digital means of payments. This will increase documented sales and will yield higher tax collection in comparison to incentive given.

Yes / Positive

Page 15

The American Business Council of Pakistan’s Proposals for Ministry of Finance & FBR (Federal Board of Revenue) Federal Budget 2021-2022

S. No Last Presented

Section / Clause / Rule

Proposed Amendment Rationale Revenue Impact

Broadening of Tax Base for a wider participation in revenue generation efforts

5.

FED

Federal Excise Duty on Merchant Discount Rate (MDR) FBR has mandated charging a 16% FED on Merchant Discount Rate (MDR). MDR is the fee charged by banks to Merchants for accepting digital payments. Banks have to recover this fee to offset the cost of POS terminals which are being provided for free in return for MDR. Adding FED on top of MDR further aggravates the value proposition around digital payments. According to SBP, around Rs. 288 Billion were spent on purchases made through POS terminals in Pakistan. Whereaas Rs. 5.7 trillion were withdrawn through ATMs, the challenge is, no one knows where this money was spent. In case of POS terminals, we can track who has been spending, how much money at which merchant locations. This information can be useful to FBR in its effort to document the society and widening the tax base. FBR is requested to waive of FED on MDR for the next 5 years to ensure adoption of digital means of payments.

Usage of cash has been the primary factor in supporting undocumented economies. If customers shift to the use of cards instead of cash, it gives FBR more information on the sales being made through different outlets. FED on MDR further increases the cost of accepting digital payments. FBR would have more visibility on spending patterns in the country by not charging any FED on MDR and would pave the way for documentation of the economy and incremental revenues from direct taxation. As per a general estimate the total revenue impact from waiving off FED on MDR would be in the range Rs. 700 Million.

YES / Positive

Page 16

The American Business Council of Pakistan’s Proposals for Ministry of Finance & FBR (Federal Board of Revenue) Federal Budget 2021-2022

S. No Last Presented

Section / Clause / Rule

Proposed Amendment Rationale Revenue Impact

Broadening of Tax Base for a wider participation in revenue generation efforts

6. 2020-2021 Income Tax Ordinance 2001

Promoting digital mode of payment through cards in Government offices (Online and Point of Sale Terminals) It should be mandatory for all Government organizations and semi-autonomous bodies to deploy International Payment Gateways and POS terminals. Majority of the leading Government sectors where citizens transact are not enable for digital means of collections e.g., NADRA, SBP, FBR, Excise and Taxation office, Pakistan Railways, Government Hospitals, Education Institutions including Higher Education Commission (HEC) etc.

Government organizations should themselves be enabled for digitization of payments. This will increase documentation of the economy and create a halo effect in the economy. Better visibility of spending patterns in Pakistan.

Yes / Positive

7. FED Act 2005 Unmanufactured Tobacco Tax Adjustable FED of PKR 300 per kg was implemented on unmanufactured tobacco to curtail the use of tobacco for manufacture of duty-not-paid cigarettes which was reversed in Federal Budget 2019-20. It is proposed to increase adjustable FED to PKR 300 per kg of unmanufactured tobacco collected at leaf threshing stage, while maintaining the exemption on exports.

This will reduce the incidence of FED evasion at cigarette manufacturing stage.

Yes / Positive

Page 17

The American Business Council of Pakistan’s Proposals for Ministry of Finance & FBR (Federal Board of Revenue) Federal Budget 2021-2022

S. No Last Presented

Section / Clause / Rule

Proposed Amendment Rationale Revenue Impact

Broadening of Tax Base for a wider participation in revenue generation efforts

8. Customs Act 1969 Lowering/Waiving Taxes & Duties on import of POS Terminals & Cash Registers Cost of importing POS terminals and Cash Registers (HS Code: 8470.5000) is very high due to various taxes and duties to be paid by acquirers. This makes increasing POS network very capex intensive and difficult. State Bank of Pakistan (SBP) has already given a target of over 500k POS terminals to banks. It is proposed that FBR supports SBP in its initiative to digitize payments. It is proposed that any all duties and taxes levied on import of POS machines and Cash Registers may be waived for a period of 5 years.

Waiving off taxes and duties would lower the cost for acquirers and help them expand in Pakistan ultimately terminalizing more merchants. Increasing documentation of the economy.

Customs Act 1969

Page 18

The American Business Council of Pakistan’s Proposals for Ministry of Finance & FBR (Federal Board of Revenue) Federal Budget 2021-2022

S. No

Last Presented

Section / Clause / Rule

Proposed Amendment Rationale Revenue Impact

Removal of Tax distortions and anomalies

9. Rule 43B(2), Income Tax Rules 2002

Withholding Tax amount before the actual remittance to Non-residents In case of payments to non-residents, the law requires to deposit corresponding withholding tax amount before the actual remittance to the non-resident person. The time period for deposit of withholding tax should be made consistent with local payments or at the most reduced to the same date as the date of payment to non-resident.

Such requirement results in great difficulty to taxpayers in terms of applying the exchange rate that would be applicable at the time of actual payment to the non-resident and also creates mismatch at the time of subsequent filing of returns of such non-resident persons.

No impact.

10. Rule 42, Income Tax Rules 2002

Annual Certificate for withholding agents Rule 42, Income Tax Rules 2002 The said rule requires the withholding agents to issue certificates of collection or deduction of tax collected or deducted, to the person from whom tax has been collected or deducted. Post Finance Act 2013, such certificates are not sufficient evidence of tax collection or deduction unless it is accompanied by CPRN. However, due to this rule the vendors require and oblige the withholding agents to issue annual certificate of collection or deduction of income tax by virtue of the said rule. Such requirement should be deleted.

To promote ease and remove unnecessary manual requirements that can be easily automated, FBR should introduce online facility on its portal for obtaining annual tax certificate based on the payment wise CPRN data stored in its database.

No impact.

Page 19

The American Business Council of Pakistan’s Proposals for Ministry of Finance & FBR (Federal Board of Revenue) Federal Budget 2021-2022

S. No

Last Presented

Section / Clause / Rule

Proposed Amendment Rationale Revenue Impact

Removal of Tax distortions and anomalies

11. 2020-2021 Section 24 Income Tax Ordinance 2001

Tax Amortization Period for Intangibles Federal Government through Finance Act 2019 has increased useful life of Intangible Assets having indefinite useful life from 10 years to 25 to allow amortization expense. Intangible Assets (Intellectual properties) are main assets of IT companies, hence reduction in amortization expense due to increased useful life over which expenses shall be allowed, would significantly impact taxable profit and tax liability.

This will help to considerably reduce the number of litigations between the taxpayer and the tax authorities i.e. FBR & PRA and attract more investment in IT sector

Yes / Negative

12. Clause 133 of Part 1 of Second Schedule

Clarity to the Term “Export Proceeds” The said clause provides that Exports proceeds on Exports of IT and IT Enabled services are exempt if 80% of the proceeds are brought into Pakistan through normal Banking channel. However, there is no clarification or rules whether limit of 80% is with respect to per invoice, per party or for overall export of a company and no criteria is mentioned with regard to point of time of checking the said limit.

It will simplify the understanding of the conditions attached and remove any ambiguity among taxpayers and department. Further the attached condition is discouraging the expansion of operations in foreign countries to enhance exports.

No impact.

13. Sixth Schedule, Sales Tax Act, 1990

Sales tax on plant growth regulators Pesticides and seeds are exempt from sales tax. However, plant growth regulators, micro-nutrients and their active ingredients are still subject to sales tax. These should be separately included as exempt in the Sixth Schedule, Sales Tax Act 1990.

This tax exposure contradicts government's policy towards price reduction and subsidy to the farmers for betterment of agricultural sector.

Yes / Positive

Page 20

The American Business Council of Pakistan’s Proposals for Ministry of Finance & FBR (Federal Board of Revenue) Federal Budget 2021-2022

S. No

Last Presented

Section / Clause / Rule

Proposed Amendment Rationale Revenue Impact

Removal of Tax distortions and anomalies

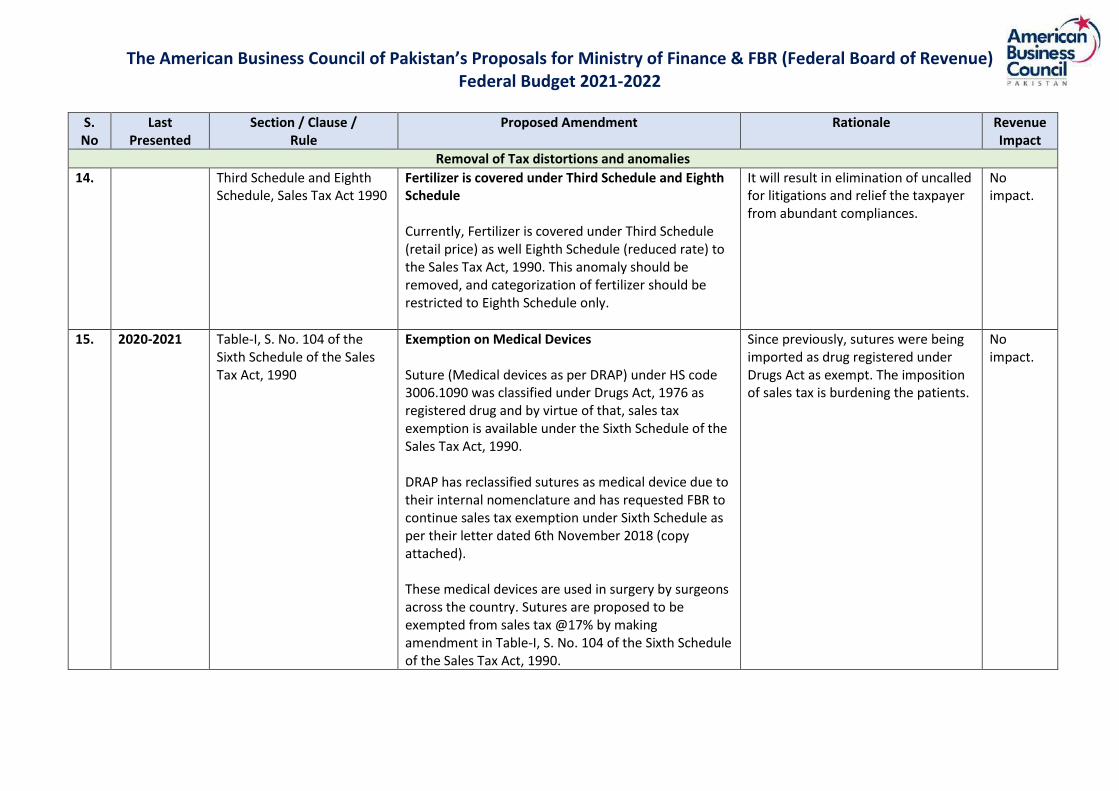

14. Third Schedule and Eighth Schedule, Sales Tax Act 1990

Fertilizer is covered under Third Schedule and Eighth Schedule Currently, Fertilizer is covered under Third Schedule (retail price) as well Eighth Schedule (reduced rate) to the Sales Tax Act, 1990. This anomaly should be removed, and categorization of fertilizer should be restricted to Eighth Schedule only.

It will result in elimination of uncalled for litigations and relief the taxpayer from abundant compliances.

No impact.

15. 2020-2021 Table-I, S. No. 104 of the Sixth Schedule of the Sales Tax Act, 1990

Exemption on Medical Devices Suture (Medical devices as per DRAP) under HS code 3006.1090 was classified under Drugs Act, 1976 as registered drug and by virtue of that, sales tax exemption is available under the Sixth Schedule of the Sales Tax Act, 1990. DRAP has reclassified sutures as medical device due to their internal nomenclature and has requested FBR to continue sales tax exemption under Sixth Schedule as per their letter dated 6th November 2018 (copy attached). These medical devices are used in surgery by surgeons across the country. Sutures are proposed to be exempted from sales tax @17% by making amendment in Table-I, S. No. 104 of the Sixth Schedule of the Sales Tax Act, 1990.

Since previously, sutures were being imported as drug registered under Drugs Act as exempt. The imposition of sales tax is burdening the patients.

No impact.

Page 21

The American Business Council of Pakistan’s Proposals for Ministry of Finance & FBR (Federal Board of Revenue) Federal Budget 2021-2022

S. No

Last Presented

Section / Clause / Rule

Proposed Amendment Rationale Revenue Impact

Removal of Tax distortions and anomalies

16. 2020-2021 Section 2 clause (44) of Sales tax act, 1990

Advances included in the definition of Supply Section 2 clause (44) of Sales Tax Act, 1990 includes advances under the definition of time of supply resulting in sales tax to be computed at payment stage. Advances should be removed from the definition of time of supply. Regulatory duty should be restricted to imports of luxurious items only or its rate should be reduced.

This will help counter inflationary pressure and promote growth of business activities.

No impact.

17. 2020-2021 Section 4B of the Income Tax Ordinance 2001

Tax rate for banks/Super Tax Banks are taxed at the rate of 35% of taxable income. Super Tax is also being charged to baking industry at the rate of 4%. Income earned on additional investment in government securities by banks are subject to additional 2.5% tax.

Tax rate should be reduced to make it in line with other industry. Super tax should be abolished for banks. Imposition of high tax rate on banking companies is discriminatory. Tax rates for business income of corporate sector have been gradually reduced from 35% to 29%. Effectively, banks are paying 10 % higher than other corporates.

Yes / Negative

Page 22

The American Business Council of Pakistan’s Proposals for Ministry of Finance & FBR (Federal Board of Revenue) Federal Budget 2021-2022

S. No Last Presented

Section / Clause / Rule

Proposed Amendment Rationale Revenue Impact

Facilitation of Taxpayers and ease of doing business

18. SRO 555(I)/2020 dated 19th June 2020

Exemption on COVID related products In the prevailing situation of COVID-19, Government has exempted sales tax on imported products related to COVID as per SRO 237(I)/2020 dated 20th March 2020 which was extended subsequently through SRO 555(I)/2020 dated 19th June 2020 for 3 months till 20th September 2020. Later on, no further extension has been granted. Resultantly, exempt products which have been imported earlier, converted into taxable which is increasing the cost to COVID patients. Keeping in view the current situation of COVID, it is proposed to extend the SRO. Further it is proposed to add Disinfectants which contains HS Code 3808.9400 in COVID related items because the same is also used frequently in COVID-19 pandemic.

This will lessen the burden on patients related to COVID-19

No impact.

19. 2019-2021 Clause 24A of Part II of 2nd Schedule of the Income Tax Ordinance, 2001 Section 153(1)ab of the Income Tax Ordinance, 2001 Section 153(1)(a) of the Income Tax Ordinance, 2001

Withholding Tax on Distributors Currently, withholding tax on distributors of pharmaceuticals is 1%, FMCG is 2% and other goods are subject to 4% withholding tax. Distribution is a high turnover business with low margins. It is proposed to bring down the withholding tax rates.

It is recommended that the rates should be reduced by 50% and made adjustable from the minimum tax liability to ensure no revenue impact to exchequer.

The relief sought will improve economic progress and more job opportunities and create balance in the distributor’s business model.

No impact.

Page 23

The American Business Council of Pakistan’s Proposals for Ministry of Finance & FBR (Federal Board of Revenue) Federal Budget 2021-2022

S. No Last Presented

Section / Clause / Rule

Proposed Amendment Rationale Revenue Impact

Facilitation of Taxpayers and ease of doing business

20. Section 73(4) of the Sales Tax Act, 1990

Disallowance of Input Sales Tax Section 73(4) provides a threshold on taxable sales to be made to an unregistered person i.e. Rs.10 million in a tax period or in aggregate Rs.100 million in a financial year. Attributable input tax would accordingly be disallowed where taxable sales would go beyond the above threshold. The above provision prior to the enactment of the Finance Act, 2020 was restricted to manufacturers only. However, vide the Finance Act, 2020 the scope of section 73(4) has been expanded to apply on all registered persons including distributors. The above provision is oppressive and is restricting the business activity of a registered person which can result in lower collection of tax. The restriction should be removed for registered persons.

Conducive for business and will assist in better collection of tax.

No impact.

Page 24

The American Business Council of Pakistan’s Proposals for Ministry of Finance & FBR (Federal Board of Revenue) Federal Budget 2021-2022

S. No Last Presented

Section / Clause / Rule

Proposed Amendment Rationale Revenue Impact

Facilitation of Taxpayers and ease of doing business

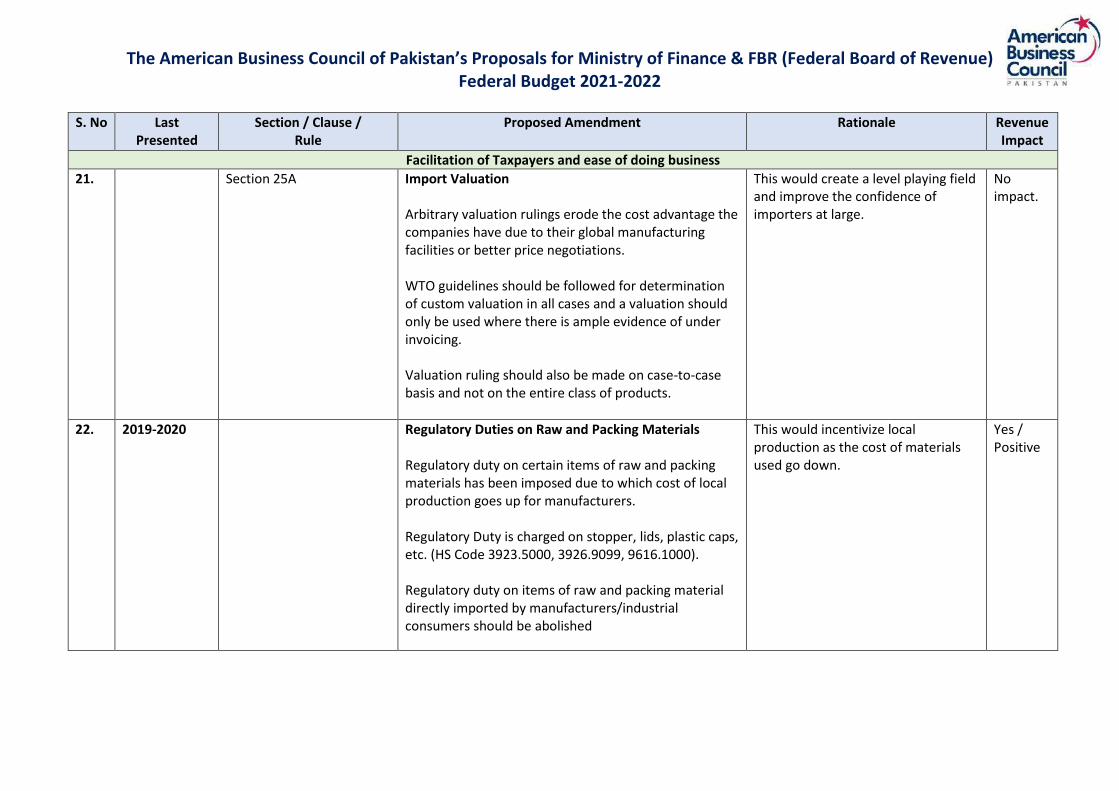

21. Section 25A Import Valuation Arbitrary valuation rulings erode the cost advantage the companies have due to their global manufacturing facilities or better price negotiations. WTO guidelines should be followed for determination of custom valuation in all cases and a valuation should only be used where there is ample evidence of under invoicing. Valuation ruling should also be made on case-to-case basis and not on the entire class of products.

This would create a level playing field and improve the confidence of importers at large.

No impact.

22. 2019-2020 Regulatory Duties on Raw and Packing Materials Regulatory duty on certain items of raw and packing materials has been imposed due to which cost of local production goes up for manufacturers. Regulatory Duty is charged on stopper, lids, plastic caps, etc. (HS Code 3923.5000, 3926.9099, 9616.1000). Regulatory duty on items of raw and packing material directly imported by manufacturers/industrial consumers should be abolished

This would incentivize local production as the cost of materials used go down.

Yes / Positive

Page 25

The American Business Council of Pakistan’s Proposals for Ministry of Finance & FBR (Federal Board of Revenue) Federal Budget 2021-2022

S. No Last Presented

Section / Clause / Rule

Proposed Amendment Rationale Revenue Impact

Facilitation of Taxpayers and ease of doing business

23. Tax holiday on exports of IT and IT enabled services The Tax holiday is a key and only incentive available to the IT and IT enabled exports industry right now. It enables the industry to compete with other countries who operate in the same space i.e. Philippines, Poland, India, Egypt etc. The proposed tax credit scheme is a complex process which negates the Prime Minister’s vision to improve ease of doing business in the country. It will result in tax officers interpreting on a case-by-case basis, more paperwork and eventually higher cost for companies which is extremely detrimental.

The proposed removal of tax holiday in the Finance Bill demonstrates inconsistency of Government policies, and large organizations will find it very difficult to make any long-term investments if they believe that GoP is not going to be consistent in its policies for the technology sector. Removal of this exemption will result in increase in cost and will have a direct impact on revenue generation capabilities as well as new business.

24. 2019-2021 Section 65B of the Income Tax Ordinance, 2001

Restoration of Section 65B Section 65B of Income Tax Ordinance, 2001 allowed a 10% tax credit to be claimed in respect of Balancing, Modernization & Replacement with respect to investment in Plant & Machinery. This was proposed to be withdrawn in Finance Act 2019, in addition to reduced rate of credit for additions made up-till June 2019 Tax credit u/s 65B should be restored as it promotes foreign direct investments in addition to incentivizing the local taxpayers into investing in long term capital projects. At a time when the economic growth has already slowed-down, restoration of 65B can help to bring about investment that stir economic growth.

It will attract FDI and will be beneficial for the economy in general.

YES / Positive

Page 26

The American Business Council of Pakistan’s Proposals for Ministry of Finance & FBR (Federal Board of Revenue) Federal Budget 2021-2022

S. No Last Presented

Section / Clause / Rule

Proposed Amendment Rationale Revenue Impact

Facilitation of Taxpayers and ease of doing business

25. Section 153(1)(b) Specified Services

Decrease in Tax Rate Specified sectors were incentivized and reduced rate of 2% was required under second schedule. Finance Act 2019 has omitted the said clause and now IT and IT enabled services are taxed at increased rate of 3% under section 153. Tax relief should be restored to attract more investment in Information Technology sector.

IT Industry is in booming phase and decreased in tax rate can make salutary effects on industry and attract more investors and sole proprietor to establish company which ultimately increase the overall tax revenue

YES / Positive

26. 2020-2021 Royalty Payments Royalty payments have been capped at 5% for over 15 years. They should be increased to 7-8%.

There are several USA – based companies who can license local production with 7-8% Royalty

YES / Positive

27. 2021-2021 STR-07 of Chapter XVIII of the Sales Tax Rules

CNIC wise entry on FBR web portal After declaration of invoices CNIC wise, taxpayer's database has increased 10 times which takes a lot of time for uploading the data on the FBR web portal. The web portal does not accept transactions more than 500 in number. FBR should increase the capacity of the web portal.

Taxpayer will be able to upload the transactions within given timelines.

No impact.

Page 27

The American Business Council of Pakistan’s Proposals for Ministry of Finance & FBR (Federal Board of Revenue) Federal Budget 2021-2022

S. No Last Presented

Section / Clause / Rule

Proposed Amendment Rationale Revenue Impact

Facilitation of Taxpayers and ease of doing business

28. STR-07 of Chapter XVIII of the Sales Tax Rules

Mandatory HS code in the form of Sales Tax return Taxpayer is required to report the transaction of sales HS code wise. Due to this, if there are different nature of goods mentioned on a single invoice, then taxpayer has to report a single invoice multiple times. Currently, portal does not accept the similar invoice number due to which taxpayers has to change the number. Resultantly, the data of buyer and seller is not matched and reconciled at month end which creates dispute between seller and buyer.HS code has been introduced by FBR when there was no mechanism to control fake input tax. The same was captured by CREST with the help of HS codes.After the introduction of STRIVE, there is no need to report HS code. Thus, it is proposed to report the transaction invoice wise rather than HS code wise.

This will simplify the current complex structure.

No impact.

29. 2020-2021 Income Tax Ordinance 2001

Exemption certificate of approved Provident and Gratuity Funds Currently exemption certificate is required for non-deduction of withholding tax on income of the approved/recognized provident fund schemes.Obtaining exemption certificates for approved/recognized provident and gratuity funds from FBR creates hardship and therefore should be eliminated.

Minimize the hardship creating ease of doing business.

No impact.

Page 28

The American Business Council of Pakistan’s Proposals for Ministry of Finance & FBR (Federal Board of Revenue) Federal Budget 2021-2022

S. No Last Presented

Section / Clause / Rule

Proposed Amendment Rationale Revenue Impact

Facilitation of Taxpayers and ease of doing business

30. 2020-2021 Rule 18 of the Sales Tax Rules

Time duration for filing Returns Last date of submission of Annexure C, payment and filing of return is 10th, 15th and 18th of each month respectively. Most companies have a 5-day working week which effectively allows only a few working days for extracting and uploading thousands of transactions. It is recommended to increase the capacity of web portal and extend the last date for submission of Annexure C, payment and return filing to 15th, 18th and 20th of each month.

This will allow easy and timely compliance by the taxpayers.

No impact.

31. 2019-2020 Serving of notices The tax department has often pursued a policy of serving notices with very short deadlines for compliance. Sometimes these notices are issued at inappropriate times (before weekends / public holidays) which further delays the receipt of the same. We propose that there should be a standard timeframe allowed for compliance and the time given for compliance should begin after the notice has been received at the taxpayers’ premises.

This will help to ensure timely compliance in addition to improving the level of trust between the department and the taxpayer.

No impact.

Page 29

The American Business Council of Pakistan’s Proposals for Ministry of Finance & FBR (Federal Board of Revenue) Federal Budget 2021-2022

S. No Last Presented

Section / Clause / Rule

Proposed Amendment Rationale Revenue Impact

Facilitation of Taxpayers and ease of doing business

32. Income Tax Ordinance 2001

Payment of refund through income tax refund bonds Through Finance Act, 2019, government has introduced refund bonds for the settlement of long outstanding income tax refunds. These refunds bonds have maturity of three years with 10% simple intertest per annum payable at maturity. However, it has been observed, despite specific directions in the Income Tax Ordinance 2001, these bonds are neither being traded freely in the market nor being discounted by the banks mainly due to low interest versus current prevailing discount rate. It is recommended to amend current fixed interest rate to floating interest rate linked with KIBOR.

Issuance of refund bond at KIBOR would make it more attractive for taxpayers. As it will provide breathing space to industry in form of liquidity and at same time will resolve government issue of encashment of accumulated refunds for last five year.

Yes / Positive

Page 30

The American Business Council of Pakistan’s Proposals for Ministry of Finance & FBR (Federal Board of Revenue) Federal Budget 2021-2022

S. No Last Presented

Section / Clause / Rule

Proposed Amendment Rationale Revenue Impact

Facilitation of Taxpayers and ease of doing business

33. 2019-2021 Section 65A and 65E of the Income Tax Ordinance, 2001

Tax credits to boost investments: Tax credit available under section 65A of the Ordinance on sales made to persons registered under Sales Tax Act, 1990 has been withdrawn vide Finance Act, 2017. It is proposed that the said credit should be restored. Tax credit on investment in plant & machinery is allowed under section 65E subject to conditions. It is suggested to extend time limit for purchase and installation of plant and machinery under section 65B and 65E from June 30, 2021 to a further period of 5 years.

Section 65A-It will promote doing business with documented and compliant sector. Section 65E-It will promote investment in local industry and will help foreign/local investors in making timely investment decisions.

YES / Positive

34. 2019-2020 26(3) of Sales Tax Act Revision of Sales Tax return: It is recommended that the process of obtaining Commissioner approval should be relaxed / abolished.

Ease of doing business and boosting investor confidence on tax authorities.

No impact.

Page 31

The American Business Council of Pakistan’s Proposals for Ministry of Finance & FBR (Federal Board of Revenue) Federal Budget 2021-2022

S. No Last Presented

Section / Clause / Rule

Proposed Amendment Rationale Revenue Impact

Facilitation of Taxpayers and ease of doing business

35. Section 3 with reference to Section 2, Sub Section 44

IT services and IT enabled Services Payment of sales tax should be applicable on realization of proceeds instead of issuance of sales tax invoice.

Sales tax is a government levy which is collected by the service provider from the service recipient and deposited in the government treasury. In case of IT services, generally the payment against invoices is made after a long time. It becomes very difficult for the entities to make payment of sales tax from its own sources prior to its collection from the customers to whom sales tax was charged. The payment of sales tax from own funds creates liquidity problem for the entities, which needs to be addressed.

No impact.

36. Section 159/ 153, Income Tax Ordinance 2001

Auto-approval of exemption application The introduction of 15 days limit for auto-approval of exemption application for public listed companies should be extended to at-least those companies that are; - active taxpayers for minimum three years; and - availing this exemption compliantly for last two years.

This measure would ease the pressure on compliant taxpayers as well as tax department. Further, extending this provision to other companies with restrictions would minimize the channel for exploitation of exemption by taxpayers and provide necessary comfort to Revenue authorities.

No impact.

Page 32

The American Business Council of Pakistan’s Proposals for Ministry of Finance & FBR (Federal Board of Revenue) Federal Budget 2021-2022

S. No Last Presented

Section / Clause / Rule

Proposed Amendment Rationale Revenue Impact

Facilitation of Taxpayers and ease of doing business

37. Section 148, Income Tax Ordinance 2001

Advance income tax @ 5.5% on Patient Assistance Programs (PAP) Imported oncology medicines worth more than tens of billions are being given to deserving patients every year by selected pharmaceutical companies under Patient Assistance Programs (PAP). Advance income tax @ 5.5% is currently being charged on import of such medicines. The advance income tax on products imported for PAP should be abolished.

As this program is for the benefit of patients and society at large, pharmaceutical companies should be relieved from this extra tax exposure, this would enable such companies to further extend these programs.

No impact.

Page 33

The American Business Council of Pakistan’s Proposals for Ministry of Finance & FBR (Federal Board of Revenue) Federal Budget 2021-2022

S. No Last Presented

Section / Clause / Rule

Proposed Amendment Rationale Revenue Impact

Facilitation of Taxpayers and ease of doing business

38. Section 23(1)(b) of the Sales Tax Act, 1990

Exemption on CNIC collection from Retailers Under section 23(1)(b) of the Sales Tax Act, 1990 law provides an exclusion to retailers for collection of CNIC on transaction value inclusive of sales tax up to 100,000 from the customers. Whereas distributors are required to collect CNICs on all transactions regardless of any threshold. Similar exclusion should also be extended to Distributors. Due to the present provisions of the law, the Distributors are facing a dilemma whereby small retailers are purchasing taxable goods valuing Rs. 100,000 from Mega stores (retailers) in order to avoid the requirement of providing the CNIC, resulting in loss of business for the Distributors who normally used to sell goods to such small retailers. FBR should extend a similar exclusion of Rs. 100,000 to distributors as well. Contrary, this is impacting the revenue of exchequer because small retailers are buying from mega stores without any implication of 3% further tax.

Ease of doing business thereby resulting in enhancement of tax revenue.

YES / Positive

Page 34

The American Business Council of Pakistan’s Proposals for Ministry of Finance & FBR (Federal Board of Revenue) Federal Budget 2021-2022

S. No Last Presented

Section / Clause / Rule

Proposed Amendment Rationale Revenue Impact

Facilitation of Taxpayers and ease of doing business

39. Federal Excise Duty/Federal Excise Act 2005

Reduction in FED rates In earlier years, the government had announced a strategy for gradual reduction in the number of items from the list of Federal Excise Duty. It was recommended that the food & beverage sector should be allowed to continue to attract new FDI investments in Pakistan. However, since 2011, the FED on Carbonated Soft Drinks have increased from 6% to 13%. In addition to sales tax, the retail taxation rate on CSDs is 30% which is one of the highest in the region. 1. Rate of FED in Serial No. 4, 5 & 6 of First Schedule of Federal Excise Act, 2005 should be reduced from 13% to 11.5%. 2. Serial no. 57 “Fruit juices, syrups and squashes, waters containing added sugar or sweetening matter” should be removed from the table in the First schedule of the Federal Excise Act, 2005.

2018-2020 → Industry volumes declined by 14% while sugar cost increased by 50%, putting further pressure on pricing. The high rate of taxation has stagnated the growth of the CSD sector as beverage companies are unable to reinvest in their systems. This has also significantly impacted the tax revenue growth for the government in recent years. Similarly in the Federal Budget 2020-21, a 5% FED was levied on fruit juices. This has again led to a negative impact on industry growth. This 5% FED must be removed to utilize the potential of the juice sector. Relief on consumer FED/ Consumer pricing is proven to immediately reflect in increased volume and sustainable FBR collection growth.

Yes / Positive

Page 35

For the consideration of:Ministry of Finance Ministry of CommerceSecurities & Exchange Commission of Pakistan (SECP)Federal Board of Revenue (FBR)

Proposals by:The Industry, Trade & Logistics Subcommittee of The American Business Council of Pakistan

Chairman: Mr. Jamshed Safdar

Page 36

The American Business Council of Pakistan’s Proposals for Commerce & Trade Policy / Federal Budget 2021-2022

Trade, Industry and Logistics are the core engine of any business development in the country. Strategic direction of its growth helps to resolve and positively develop the business foundation and its progressive environment. The American Business Council’s representation in this sector runs across several segments of business. Some of these industry representations need a focused discussion on the nuances of the speed bumps in growth. The aim of this document is to highlight select industries which can enhance the focus on the growing business by increasing the revenue base or reducing the cost impact to the country. We have nominated the following industries:

• Beverage

• Pharmaceuticals

• Tobacco

• Insurance

• Ceramics This document highlights areas for which we request a dialogue and together aim to enhance growth and stability in the business sector of Pakistan, and be a poster child for contributing growth in the country. Jamshed Safdar Chairman – Trade, Industry and Logistics subcommittee

Page 37

The American Business Council of Pakistan’s Proposals for Commerce & Trade Policy / Federal Budget 2021-2022

No Last Presented

Issues/Concern Negative Impact – Industry Action/Recommendation Benefit

Tobacco Industry – Illicit Trade in Pakistan

1. There are various cigarette packaging and labelling requirements mandated by the FBR and the Ministry of Health. Any cigarette pack that does not fulfill these requirements is not allowed to be cleared from the port or sold in Pakistan and hence must be confiscated by Customs.

Non-level playing field leading to a volume loss by the compliant industry and ultimately revenue loss for the government

Disseminate the relevant packaging and labelling requirements to the field teams at the air, dry and wet ports to ensure that non-compliant packs are confiscated and not cleared and furthermore are destroyed.

Increase in compliant industry volumes for improved excise revenue generation

Impact on country's health objectives due to lack of health warning and other packaging requirements

Conduct raids at hotspots for smuggled cigarettes to seize and destroy cigarettes which have been smuggled in through the borders.

Positive impact on public health objectives

2. Pakistan recent years has shown a spike in counterfeit cigarettes which is due to interplay of various factors including supply incentives, market demand. Illegal manufacturing of cigarettes bears a trademark without the owner`s consent are being sold with the intent of being passed off as genuine. Excise tax is rarely, if ever paid on counterfeit cigarettes.

Loss of government revenue as consumers buy non-tax paid counterfeit products

Back tracking of the supply chain from the retailers, manufacturers of counterfeit products, primary distributor of counterfeit products, manufacturers producing packing materials which are used for the production of counterfeit products.

Increase in compliant industry volumes for improved excise revenue generation.

Infringement of intellectual property right of compliant manufacturers

Protection of intellectual property rights of compliant manufacturers

Page 38

The American Business Council of Pakistan’s Proposals for Commerce & Trade Policy / Federal Budget 2021-2022

No Last Presented

Issues/Concern Negative Impact – Industry Action/Recommendation Benefit

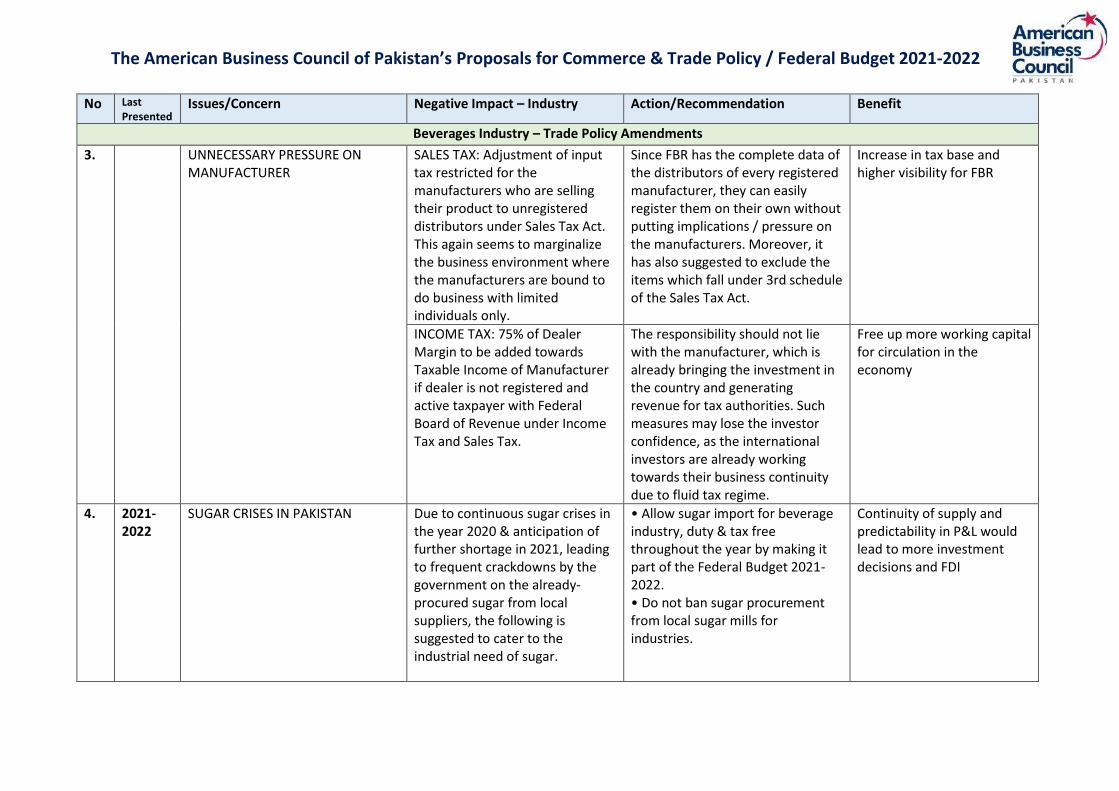

Beverages Industry – Trade Policy Amendments

3. UNNECESSARY PRESSURE ON MANUFACTURER

SALES TAX: Adjustment of input tax restricted for the manufacturers who are selling their product to unregistered distributors under Sales Tax Act. This again seems to marginalize the business environment where the manufacturers are bound to do business with limited individuals only.

Since FBR has the complete data of the distributors of every registered manufacturer, they can easily register them on their own without putting implications / pressure on the manufacturers. Moreover, it has also suggested to exclude the items which fall under 3rd schedule of the Sales Tax Act.

Increase in tax base and higher visibility for FBR

INCOME TAX: 75% of Dealer Margin to be added towards Taxable Income of Manufacturer if dealer is not registered and active taxpayer with Federal Board of Revenue under Income Tax and Sales Tax.

The responsibility should not lie with the manufacturer, which is already bringing the investment in the country and generating revenue for tax authorities. Such measures may lose the investor confidence, as the international investors are already working towards their business continuity due to fluid tax regime.

Free up more working capital for circulation in the economy

4. 2021-2022

SUGAR CRISES IN PAKISTAN Due to continuous sugar crises in the year 2020 & anticipation of further shortage in 2021, leading to frequent crackdowns by the government on the already-procured sugar from local suppliers, the following is suggested to cater to the industrial need of sugar.

• Allow sugar import for beverage industry, duty & tax free throughout the year by making it part of the Federal Budget 2021-2022. • Do not ban sugar procurement from local sugar mills for industries.

Continuity of supply and predictability in P&L would lead to more investment decisions and FDI

Page 39

The American Business Council of Pakistan’s Proposals for Commerce & Trade Policy / Federal Budget 2021-2022

No Last Presented

Issues/Concern Negative Impact – Industry Action/Recommendation Benefit

Beverages Industry – Trade Policy Amendments

5. HARMONIZATION OF STANDARDS Following the devolution of power to the provincial governments through the 18th Amendment in 2006, the provincial governments have started to create their own food standards that are not science-based, not in line with global practice, and often contradictory to each other. Prior to implementation of the 18th Amendment, Pakistan Standards and Quality Control Authority (PSQCA) as a federal body was responsible for standards setting. These standards were aligned with international standards laid out by the Food and Agricultural Organization (FAO) of the United Nations. At present, multiple standards across multiple provinces are creating operational challenges for companies operating across provinces and serving as a barrier to trade.

In December 2019, the Council of Common Interest (CCI), chaired by the Prime Minister, took the decision to form a uniform food standard. However, the implementation of the decision is pending. Furthermore, the industry expects the government to facilitate and encourage "ease of doing business" and to this regard requests the Federal Government to provide one window solution at the Federal level, as far as "registrations and licencing" is concerned.

Avoid avenues for kick backs for the field staff and ensuring consistent quality across the country

Page 40

The American Business Council of Pakistan’s Proposals for Commerce & Trade Policy / Federal Budget 2021-2022

No Last Presented

Issues/Concern Negative Impact – Industry Action/Recommendation Benefit

Beverages Industry – Trade Policy Amendments

6. 2020-2021

Federal Excise Duty: FED on beverage products is very high. Not justifiable and discriminatory. - 13% on Carbonated Drinks - 5% on Juices. Paying FED input on Concentrate @ 50%

-The levy of federal Excise duty @13% on soft drinks along with sales tax @17% has increased consumer prices. This is badly affecting revenues of beverage companies and FDI in Pakistan. - Further, levy of 5% FED on Juices is giving edge to the revenues of B-Brands which are mostly un-documented and not paying full taxes. - Only penalizing the tax compliant companies.

It should reduce to 11% in first go. Then over period of 3 years reduce to 6% as it was in past. Further, FED on Juices should be Eliminate.

It will reduce the burden on manufacturer. Consumer prices will reduce correspondingly. Increase the production and resultantly increase GOP revenue.

7. Sales Tax: Reduce the sales tax rate 17%.

- The cost of doing business has become very high. - Blockage of high cash in input taxes. - Hurdle in expanding the tax net.

FBR is implementing real time Video Monitoring for beverages industry. For successful compliance of Video monitoring project of FBR, the standard rate of Sales Tax should be reduced from 17% to 15% for beverage industry.

All revenue collection from B-brands will be enhanced, if MNCs & FBR will successfully implement video monitoring.

Page 41

The American Business Council of Pakistan’s Proposals for Commerce & Trade Policy / Federal Budget 2021-2022

No Last Presented

Issues/Concern Negative Impact – Industry Action/Recommendation Benefit

Beverages Industry – Trade Policy Amendments

8. FBR Handling: Currently, tax office is enforcing multiple audits for direct & indirect taxes in a financial year. Tax office sending illogical and unjustifiable notices.

Wastes time and money of company on litigations. This type of illogical notices creates question marks on taxation system of Pakistan in front of foreign investors. Will reduce future foreign investment. Ultimately not helping in increase of Govt. revenues.

It should be restricted to one audit in a tax year.

This will support in ease of doing business and revenue enhancement of taxpayer and FBR.

9.

Custom Duty on Plastic Resin: Currently custom duty of 8% (6+2) is imposed on Resin. Resulted in high price of imported resin. Locally there is monopoly of one company.

- Blocking the imported products, fully dependent of one company for supplies. - Charging high prices and resultantly high input cost for company

Custom duty should be waived to bring the resin price on competitive level.

It will help the manufacturer to get plastic resin at international prices. Bring the cost down and ultimately consumer price also reduces.

Page 42

The American Business Council of Pakistan’s Proposals for Commerce & Trade Policy / Federal Budget 2021-2022

No Last Presented

Issues/Concern Negative Impact – Industry Action/Recommendation Benefit

Beverages Industry – Trade Policy Amendments

10. 2020-2021

Groundwater Extraction Charges Counterfeit Products (Last year's input) Punjab Government recently passed Punjab Water Bill, which essentially defines the process for determining water tariff and other related elements. As per Supreme Court directions, other provinces should also proceed with developing legislation to govern this area.

- Counterfeit products help those companies which are not paying tax at all. - Others are same points used in last year proposal

Should be set after consultation Strict action required from authorities Reduce less than 1%. (Last year's input) This must be done in consultation with relevant stakeholders. Current impact of Rs. 1/litre will potentially result in industry closures

(Last year's input) - Provide level-playing field to all players - Protect consumers from harmful fake products in the market - Protect IPPs of companies (esp. MNCs)

Page 43

The American Business Council of Pakistan’s Proposals for Commerce & Trade Policy / Federal Budget 2021-2022

No Last Presented

Issues/Concern Negative Impact – Industry Action/Recommendation Benefit

Insurance Industry

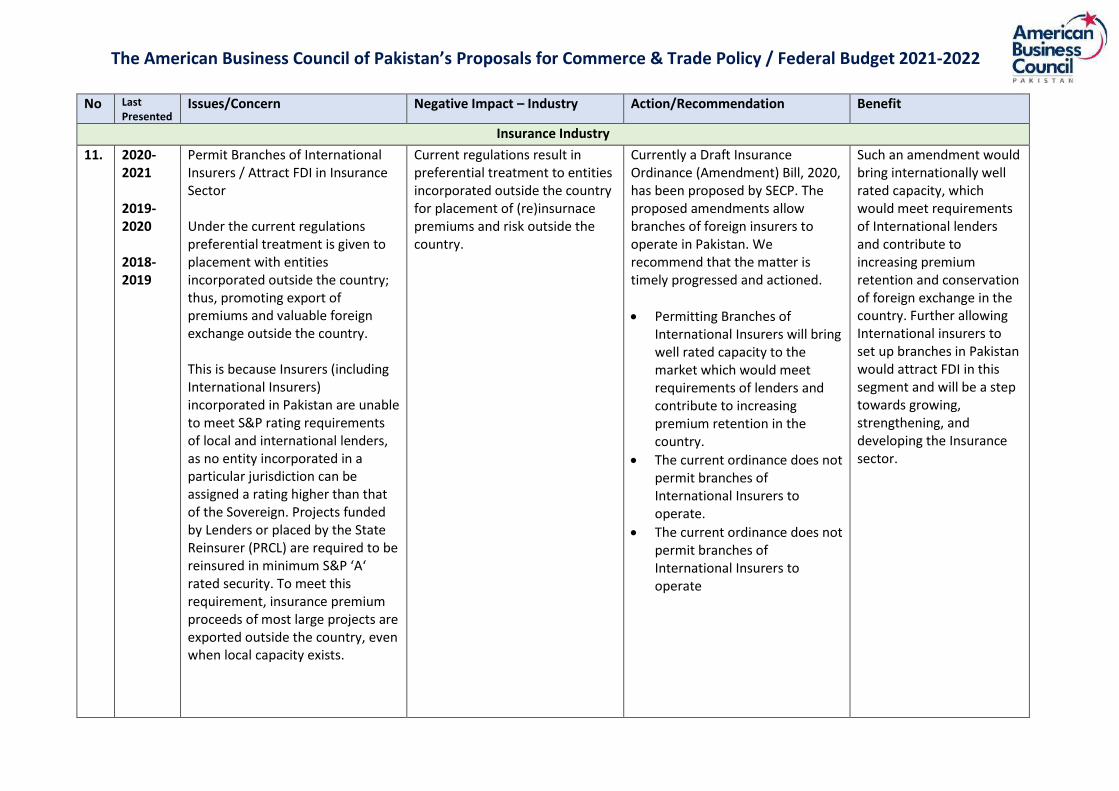

11. 2020-2021 2019-2020 2018-2019

Permit Branches of International Insurers / Attract FDI in Insurance Sector Under the current regulations preferential treatment is given to placement with entities incorporated outside the country; thus, promoting export of premiums and valuable foreign exchange outside the country. This is because Insurers (including International Insurers) incorporated in Pakistan are unable to meet S&P rating requirements of local and international lenders, as no entity incorporated in a particular jurisdiction can be assigned a rating higher than that of the Sovereign. Projects funded by Lenders or placed by the State Reinsurer (PRCL) are required to be reinsured in minimum S&P ‘A‘ rated security. To meet this requirement, insurance premium proceeds of most large projects are exported outside the country, even when local capacity exists.

Current regulations result in preferential treatment to entities incorporated outside the country for placement of (re)insurnace premiums and risk outside the country.

Currently a Draft Insurance Ordinance (Amendment) Bill, 2020, has been proposed by SECP. The proposed amendments allow branches of foreign insurers to operate in Pakistan. We recommend that the matter is timely progressed and actioned.

• Permitting Branches of International Insurers will bring well rated capacity to the market which would meet requirements of lenders and contribute to increasing premium retention in the country.

• The current ordinance does not permit branches of International Insurers to operate.

• The current ordinance does not permit branches of International Insurers to operate

Such an amendment would bring internationally well rated capacity, which would meet requirements of International lenders and contribute to increasing premium retention and conservation of foreign exchange in the country. Further allowing International insurers to set up branches in Pakistan would attract FDI in this segment and will be a step towards growing, strengthening, and developing the Insurance sector.

Page 44

The American Business Council of Pakistan’s Proposals for Commerce & Trade Policy / Federal Budget 2021-2022

No Last Presented

Issues/Concern Negative Impact – Industry Action/Recommendation Benefit

Insurance Industry

12. 2018-2019 This matter has been raised by Insurance Association

of Pakistan (IAP) in relevant Judicial forum and is currently sub

judice.

Sales Tax on Reinsurance Premium The SRB has imposed retrospectively a 13% tax on reinsurance service providers. This has created a concern in the market as SST is charged on the insurance premium – to charge SST again on the facultative reinsurance transaction acts as a double taxation on virtually the same insurance risk and adds to unnecessary administrative burden. Under the current reinsurance tax regime, premium exports outside the country are incentivized as the tax is not applicable on such transactions (emanating from elsewhere in Pakistan). Further under the proposed tax regime, the sales tax is now applicable to reinsurance provided to insurance companies in other jurisdictions – thereby making the country’s insurance industry further uncompetitive and forcing such reinsurance placements to be moved to other jurisdictions.

Makes the country's Insurance / Reinsurance segment uncompetitive as such a tax on reinsurance is exempt in comparable jurisdictions. Does not provide a level playing field to Insurers operating in Sindh, as such a tax on reinsurance is not applicable on transactions emanating in other provinces.

Reinsurance is not an independent activity that should be subject to tax. Rather it is only generated by an insurance transaction which entails sharing the risk of the original insurer and for the same perils as covered on the direct policy of insurance. Thus, the transaction does not entail any “value addition”, reinsurance only serves to spread the risk, which is the essence of the concept of insurance and hence it is recommended that this 13% sales tax be removed. It may be pertinent to mention that, on the basis of the facts aforementioned, the FBR which had earlier, imposed a similar charge withdrew it vide Finance Act 2013.

It should be noted that VAT prevalent in most European Countries including UK, Ireland, Germany, France, Finland, Italy etc. exempts reinsurance from VAT. Further in our region, Sri Lanka, UAE, Bangladesh as well as other countries of Asia, levy Sales tax only on premium, while reinsurance remains exempt. The removal of this additional levy would bring Pakistan’s structure in line with other countries. It would also enable Pakistan to offer competitive reinsurance service across borders as well. More than PKR 10 billion of premiums are exported outside the country to buy reinsurance.

Page 45

The American Business Council of Pakistan’s Proposals for Commerce & Trade Policy / Federal Budget 2021-2022

No Last Presented

Issues/Concern Negative Impact – Industry Action/Recommendation Benefit

Insurance Industry

13. (i)

2020-2021 2019-2020 2018-2019

Need for Holistic Approach to Regulations by SBP and SECP / Reinsurance from Regional Countries: 6(i) Projects financed by lenders (both International and local) contain contract clauses that require insurance claim proceeds to be deposited into offshore Trustee accounts in USD. When settling claim involving such projects, processing at the SBP is slow with unnecessary documentation being requested and, in most cases, results in a denial of permission for claim settlements outside the country. Due to inability of local Insurers to settle as per lender requirements, local and international re-insurance brokers, place reinsurance coverage with offshore Reinsurers, notwithstanding availability of local re-insurance capacity in Pakistan. As a result, there is outflow of foreign exchange from Pakistan market for business which could be catered to in Pakistan.

This ambiguity in regulations places restrictions on Insurers incorporated in Pakistan while no such restriction is made on Insurers operating elsewhere thus incentivizing placement of risks and premiums outside the country at the cost of Insurers incorporated in Pakistan. Conflicting regulatory stance and position taken by SECP and SBP, resulting in loss of regional business from neighbouring countries. The current regulations incentivise this export of premiums. Incentivising local retention of premiums will reduce premium exports / foreign exchange outflow.

6(i) SBP & SECP need to comprehensively review incorporation of Lender clauses in agreements (both local and international) and to take a holistic approach in terms of other applicable laws affecting the transactions. If SBP finds such lender clauses (requiring claim settlements in USD to offshore bank accounts) acceptable, then local insurance companies should also be enabled to be in a position to honour the agreements and be at par with foreign insurers and reinsurers.

- Higher foreign exchange earnings for Pakistan via export proceeds from Insurance Services. - Reduction in foreign exchange outflow and greater retention of Insurance business within the country. - Development of long-term business linkages between Pakistan and regional countries

Page 46

The American Business Council of Pakistan’s Proposals for Commerce & Trade Policy / Federal Budget 2021-2022

No Last Presented

Issues/Concern Negative Impact – Industry Action/Recommendation Benefit

Insurance Industry

13. (ii)

2020-2021 2019-2020 2018-2019

(Continued) Need for Holistic Approach to Regulations by SBP and SECP / Reinsurance from Regional Countries: 6(ii) Pakistan Insurance market has substantial potential to cater to some of the reinsurance requirements of markets such as Afghanistan, Bangladesh, and Sri Lanka. Due to business linkages, many clients based in these countries reach out to Insurers in Pakistan, however till date there is no clear framework to provide reinsurance services and as a result, substantial business has been lost to regional markets. A major challenge is the lack of a sound interface between SECP and SBP policies – whereas SECP permits reinsurance of risks located outside of Pakistan, SBP has no specific rules governing such transactions and therefore SBP does not permit remittance of reinsurance claim proceeds outside of Pakistan.

This ambiguity in regulations places restrictions on Insurers incorporated in Pakistan while no such restriction is made on Insurers operating elsewhere thus incentivizing placement of risks and premiums outside the country at the cost of Insurers incorporated in Pakistan. Conflicting regulatory stance and position taken by SECP and SBP, resulting in loss of regional business from neighbouring countries. The current regulations incentivise this export of premiums. Incentivising local retention of premiums will reduce premium exports / foreign exchange outflow.

6(ii) There is a need for the two regulators (SECP & SBP) to agree to a common framework in order to promote and develop insurance in the country.

- Higher foreign exchange earnings for Pakistan via export proceeds from Insurance Services. - Reduction in foreign exchange outflow and greater retention of Insurance business within the country. - Development of long-term business linkages between Pakistan and regional countries

Page 47

The American Business Council of Pakistan’s Proposals for Commerce & Trade Policy / Federal Budget 2021-2022

No Last Presented

Issues/Concern Negative Impact – Industry Action/Recommendation Benefit

Insurance Industry

14. Prequalification of Reinsurers by State Reinsurer Tender requirements of Pakistan Reinsurance Company Limited (PRCL), the State-owned reinsurer, mandates a minimum S&P ‘A’ rating for reinsurers participating in placement of reinsurance programs. Given Pakistan’s sovereign rating (which is lower than International S&P’A’) this prequalification requirement in the tender is discriminatory to entities registered in Pakistan (including International Insurers), since none of them can be rated higher than the sovereign.

Tender requirements of State Reinsurer are discriminatory towards Insurers incorporated in Pakistan.

There should be separate Tender criteria for Pakistan registered Insurance companies in accordance with their local capacity. Rationale: Pakistan has several strong local insurance companies and a foreign insurance company that can provide capacity.

Incorporating this proposal will allow greater participation from entities registered in Pakistan and will strengthen the local market by increasing premium retention and reducing foreign exchange outflow from Pakistan

Page 48

The American Business Council of Pakistan’s Proposals for Commerce & Trade Policy / Federal Budget 2021-2022

No Last Presented

Issues/Concern Negative Impact – Industry Action/Recommendation Benefit

Ceramics Industry

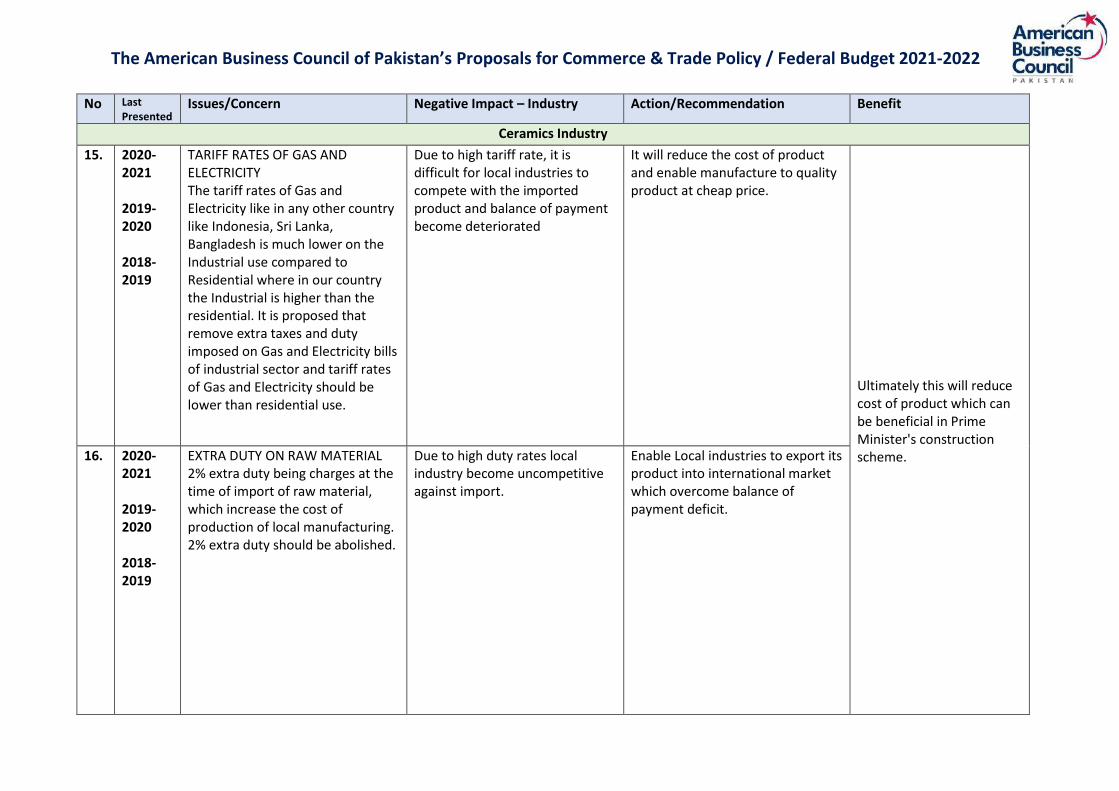

15. 2020-2021 2019-2020 2018-2019

TARIFF RATES OF GAS AND ELECTRICITY The tariff rates of Gas and Electricity like in any other country like Indonesia, Sri Lanka, Bangladesh is much lower on the Industrial use compared to Residential where in our country the Industrial is higher than the residential. It is proposed that remove extra taxes and duty imposed on Gas and Electricity bills of industrial sector and tariff rates of Gas and Electricity should be lower than residential use.