The Global Crisis and The Global Crisis and LAC LAC Views from Washington Views from Washington Guillermo Calvo Guillermo Calvo Columbia University Columbia University Inter-American Development Bank, Vice Presidency for Sectors and Knowledge Research Department and the Regional Policy Dialogue, Washington, DC, April 24, 2009

The Global Crisis and LAC Views from Washington

Dec 30, 2015

The Global Crisis and LAC Views from Washington. Guillermo Calvo Columbia University. Inter-American Development Bank, Vice Presidency for Sectors and Knowledge Research Department and the Regional Policy Dialogue, Washington, DC, April 24, 2009. Main Policy Innovations. - PowerPoint PPT Presentation

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

The Global Crisis and LACThe Global Crisis and LACViews from WashingtonViews from Washington

Guillermo CalvoGuillermo CalvoColumbia UniversityColumbia University

Inter-American Development Bank, Vice Presidency for Sectors and KnowledgeResearch Department and the Regional Policy Dialogue, Washington, DC, April 24, 2009

Main Policy InnovationsMain Policy Innovations

I.I. G20 re-funding and re-founding G20 re-funding and re-founding of the Fund.of the Fund.

II.II. Pro-active monetary and Pro-active monetary and financial policy in the G7.financial policy in the G7.

III.III. G7 Stimulus packages.G7 Stimulus packages.

I. G20 Re-funding and Re-I. G20 Re-funding and Re-founding the Fundfounding the Fund

The G20 decision to substantially increase The G20 decision to substantially increase IMF funding, and the new IMF Flexible IMF funding, and the new IMF Flexible Credit Line, represent Credit Line, represent major strategic major strategic changeschanges in international financial in international financial cooperation.cooperation.The FCL offers an alternative to The FCL offers an alternative to international reserve accumulation, a costly international reserve accumulation, a costly self-insurance scheme.self-insurance scheme.The FCL could be instrumental in recycling The FCL could be instrumental in recycling Flight-to-Quality capital, and Flight-to-Quality capital, and preventing preventing BOP crisesBOP crises..

Remarkably, a US$47 billion FCL for Remarkably, a US$47 billion FCL for Mexico was approved, even though Mexico was approved, even though Mexico is not suffering from a balance-of-Mexico is not suffering from a balance-of-payments, BOP, crisis.payments, BOP, crisis.

In contrast, in 1995 Mexico got a US$50 In contrast, in 1995 Mexico got a US$50 billion package many weeks billion package many weeks afterafter BOP BOP crisis erupted – too late for preventing crisis erupted – too late for preventing major output collapse. major output collapse.

Thus, Thus, the Fund is beginning to act as a the Fund is beginning to act as a regular central bankregular central bank ( (at a global level).at a global level).

II. Pro-active Monetary and II. Pro-active Monetary and Financial Policy in the G7Financial Policy in the G7

Lowering of policy interest rates and the Lowering of policy interest rates and the many other operational innovations at the many other operational innovations at the Fed and other G7 central banks may have Fed and other G7 central banks may have contributed to:contributed to:

Protecting EMs from contagion through Protecting EMs from contagion through the capital market (as during the 1998 the capital market (as during the 1998 Russian crisis).Russian crisis).

Surge of capital flows to EMs until mid Surge of capital flows to EMs until mid 20082008

Low yields of EM bonds.Low yields of EM bonds.

Greenspan’s “conundrum”

testimony

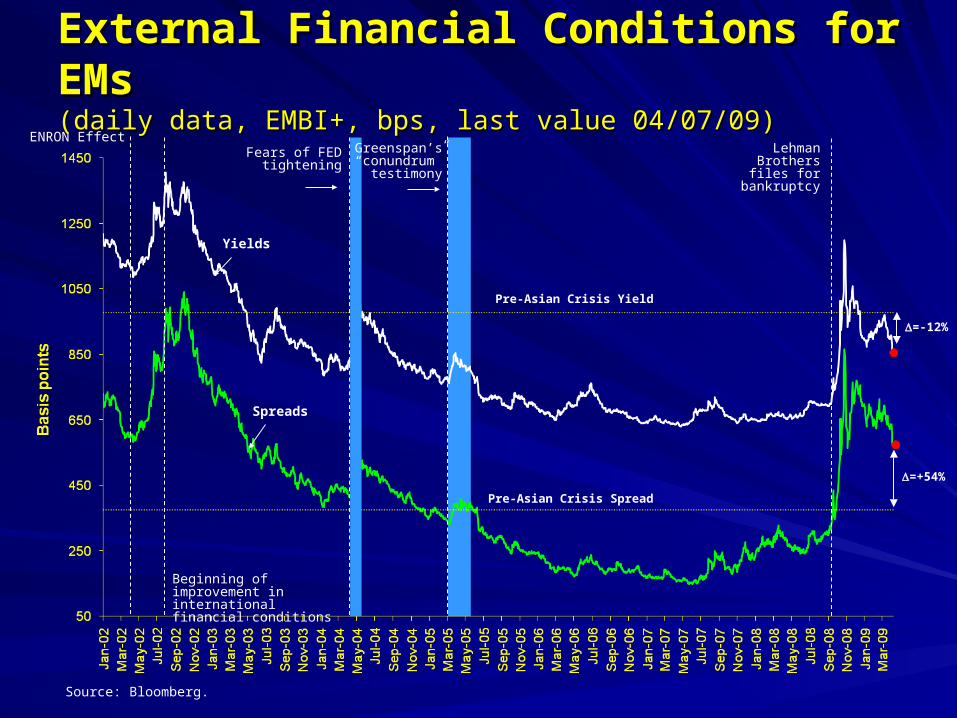

ExternalExternal Financial Conditions for EMsFinancial Conditions for EMs(daily data, EMBI+, bps, last value 04/07/09)(daily data, EMBI+, bps, last value 04/07/09)

Source: Bloomberg.

Pre-Asian Crisis Spread

Pre-Asian Crisis Yield

ENRON Effect

Spreads

Yields

Beginning of improvement in international financial conditions

Fears of FED tightening

=+54%

=-12%

Lehman Brothers files for

bankruptcy

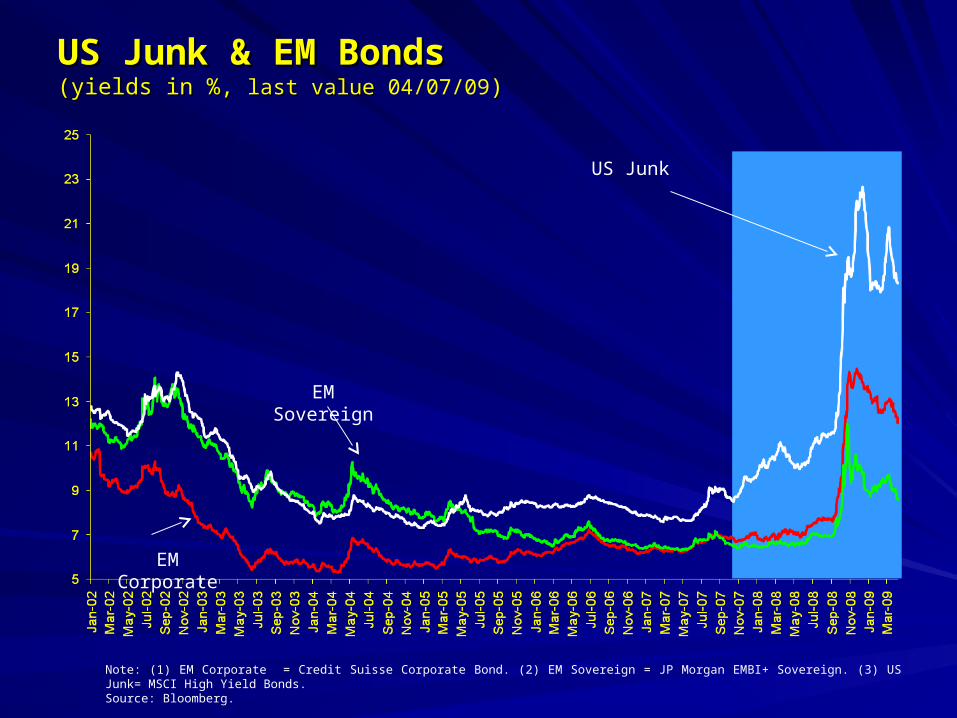

US Junk & EM BondsUS Junk & EM Bonds(yields in %, (yields in %, last value last value 04/07/09))

Note: (1) EM Corporate = Credit Suisse Corporate Bond. (2) EM Sovereign = JP Morgan EMBI+ Sovereign. (3) US Junk= MSCI High Yield Bonds.Source: Bloomberg.

EM Sovereign

US Junk

EM Corporate

III. G7 Stimulus PackagesIII. G7 Stimulus Packages

Several experts and commentators Several experts and commentators expect that effects on EM output will expect that effects on EM output will be modest.be modest.

Moreover, these packages could Moreover, these packages could contribute to further crowding out of contribute to further crowding out of capital flows from EM, especially if capital flows from EM, especially if global output takes time to react to global output takes time to react to stimulus packages.stimulus packages.

Inflation Risks in LACInflation Risks in LACInflation Risks in LACInflation Risks in LAC

Global inflation may surge as credit starts Global inflation may surge as credit starts to flow to the private sector.to flow to the private sector.Commodity prices are likely to be the first Commodity prices are likely to be the first in line to rise in line to rise – which, as experienced in 2008 Q-I, will result which, as experienced in 2008 Q-I, will result

in higher EMs’ inflation.in higher EMs’ inflation.

G7 central banks are unlikely to tighten G7 central banks are unlikely to tighten monetary policy before they see output monetary policy before they see output firmly recuperating and inflation reflected firmly recuperating and inflation reflected in their CPIs. in their CPIs.

Therefore, as inflation flares up, LACs are Therefore, as inflation flares up, LACs are likely to be on their ownlikely to be on their own

And may face a serious tradeoff between And may face a serious tradeoff between

– stopping inflation stopping inflation andand – stopping output’s rebound.stopping output’s rebound.

Commodity PricesCommodity Prices(daily data, Index 3-Sep-07= 100, last value 4/7/09)(daily data, Index 3-Sep-07= 100, last value 4/7/09)

Source: Bloomberg.

The Global Crisis and LACThe Global Crisis and LACViews from WashingtonViews from Washington

Guillermo CalvoGuillermo CalvoColumbia UniversityColumbia University

Inter-American Development Bank, Vice Presidency for Sectors and KnowledgeResearch Department and the Regional Policy Dialogue, Washington, DC, April 24, 2009

Related Documents