The Geography of Urban Intelligence PETER NIJKAMP in cooperation with Karima Kourtit Tinbergen Institute, Amsterdam, The Netherlands KTH Royal Institute of Technology, Stockholm, Sweden Adam Mickiewicz University, Poznan, Poland

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

The Geography of Urban Intelligence

PETER NIJKAMP

in cooperation with

Karima Kourtit

Tinbergen Institute, Amsterdam, The NetherlandsKTH Royal Institute of Technology, Stockholm, Sweden

Adam Mickiewicz University, Poznan, Poland

Features of agglomerations:

• Density

• Proximity

• Connectivity

Agents:

• People and Industries,

Empowered by:

oHuman Capital

o Cultural Capital

o Social Capital

o Technological Capital

o Environmental Capital

Motto:“interaction (often involuntary) among economic agents made possible by the lesser amount of spatial frictions that occur in concentrated location” (Capello)

Categories:MARJacobsPorter

Aim: to present a panorama on:

The Geography of Creative Industries and Cultural Heritage

THE GEOGRAPHY OF CREATIVE

INDUSTRIES AND CULTURAL HERITAGE

PETER NIJKAMP

in cooperation with

Karima Kourtit

Tinbergen Institute, Amsterdam, The NetherlandsKTH Royal Institute of Technology, Stockholm, Sweden

Adam Mickiewicz University, Poznan, Poland

AIM

To investigate the presence of creative industries in theNetherlands in relation to the presence of culturalheritage

• to analyze shares of the creative sectors and the growth rates of these shares in the national economy and in the largest cities

• to analyze its relationships with cultural heritage

COMPETION CONDITIONS

World cities are increasingly involved in fierce competition on global product

and service markets; these metropolitan areas have to create favourable

conditions for economic agents, such as:

healthy entrepreneurial climate;

specialized basis of industrial clusters;

ecologically sustainable urban environment;

high-quality research and educational infrastructure;

international accessibility through majors hubs.

(Cheshire and Magrini 2009)

URBAN MISSION

Modern cities’ mission: maximize ‘XXQ’ (the highest possible quality) in a

heterogeneous urban product market in a global system (see for a detailed

exposition of the XXQ principle, Nijkamp 2010)

URBAN CHALLENGE

Cities and regions are challenged to develop a ‘Cultural and Creative

Geographic Space’ (see Tornqvist 1983; Andersson 1985; Kourtit et al. 2011)

CREATIVE GEOGRAPHIC SPACE

MULTI-TASKING

Modern regions and cities must attract, retain and even nurture

highly mobile and (global) creative and innovative firms and

talents

GOVERNANCE OBJECTIVE

Secure economic development and competitive advantage of modern regions and cities (Peck 2005)

INTERACTIVE SPACE

Multiple agents, multiple tasks, multiple cities in a competitive setting, with many feedback mechanisms ---- Non-linear dynamics

CONTEXT AND FOCUS

CONCEPTUAL FRAMEWORKS

• New (endogenous) growth theory (Romer and Lucas)

• New economic geography (Fujita, Krugman)

• New innovation theory (Acs )

• Creativity theory (Florida, Scott)

• Complexity theory (Reggiani, Nijkamp)

STAGES EMERGING INDUSTRIES

• Service and high-tech industries

• Information industries

• Creative industries

IMPACTS

• Prompt dynamic and challenging economic sectors world-wide

• Drivers of economic development of modern cities

FOCUS

Innovative and creative firms as key actors in the economic change and transformation process of

cities and regions (see e.g. Pavitt 1990; Berry and Taggart 1996; Oakey 2007; Cooper and Park

2008) . Creative industries comprise a range of new economic activities such as advertising,

architecture, art, tourism, design, fashion, film, R&D, high-tech, games, media

Geographical market and environmental changes put

emphasis on:

• entrepreneurship

• locational decision-making (business growth

strategies; Ansoff’s model 1957)

• spatial strategies (market and spatial

segmentation)

Need for efficient and effective management

techniques; with a geographic location dimension

9

CITIES: A WEALTH OF CULTURAL HERITAGE

BERN

BUDAPEST

Rotterdam

BUCHAREST

Napels

10

THE NEXUS OF CREATIVITY AND CULTURAL HERITAGE

A wealth of cultural heritage assets can be found in many European cities, and worldwide (Africa, Asia, etc)

Cities have a wealth of cultural facilities that may attract all kind of stakeholders (visitors, residents, business sectors), in particular creative minds

Creative minds have an exceptional innovation potential in terms of both innovative ideas and practices (diversification / specialization segmentation, Ansoff 1957) creative industries

Cultural heritage is frequently used as a strategic development tool for urban policies, many current cities (Paris, Florence, Athens, Amsterdam, Marrakesh, Acapulco, etc.) derive their wealth from the abundant presence of a great diversity of cultural heritage

But which people, businesses and (economic) activities are particularly attracted by the presence of and access

to urban cultural heritage capital?

12

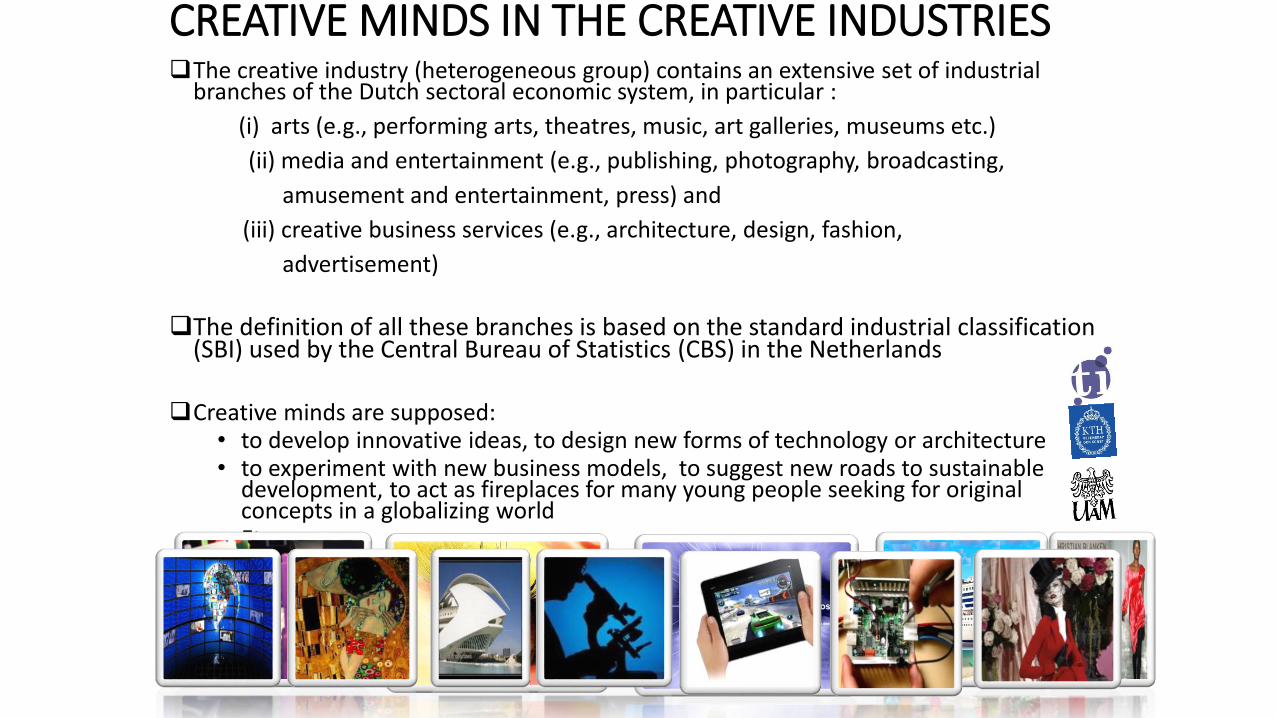

CREATIVE MINDS IN THE CREATIVE INDUSTRIES The creative industry (heterogeneous group) contains an extensive set of industrial

branches of the Dutch sectoral economic system, in particular :

(i) arts (e.g., performing arts, theatres, music, art galleries, museums etc.)

(ii) media and entertainment (e.g., publishing, photography, broadcasting,

amusement and entertainment, press) and

(iii) creative business services (e.g., architecture, design, fashion,

advertisement)

The definition of all these branches is based on the standard industrial classification (SBI) used by the Central Bureau of Statistics (CBS) in the Netherlands

Creative minds are supposed:• to develop innovative ideas, to design new forms of technology or architecture• to experiment with new business models, to suggest new roads to sustainable

development, to act as fireplaces for many young people seeking for original concepts in a globalizing world

• Etc.

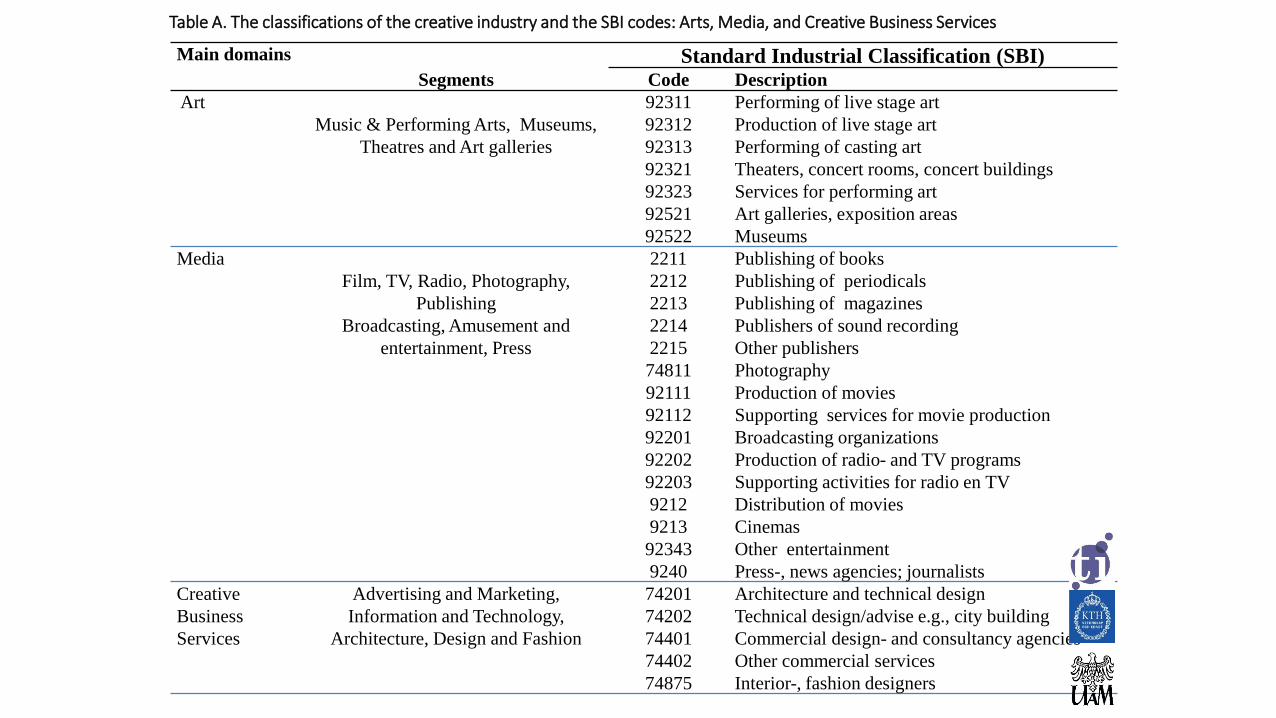

Table A. The classifications of the creative industry and the SBI codes: Arts, Media, and Creative Business Services

Main domains Standard Industrial Classification (SBI)Segments Code Description

Art

Music & Performing Arts, Museums,

Theatres and Art galleries

92311

92312

92313

92321

92323

92521

92522

Performing of live stage art

Production of live stage art

Performing of casting art

Theaters, concert rooms, concert buildings

Services for performing art

Art galleries, exposition areas

Museums

Media

Film, TV, Radio, Photography,

Publishing

Broadcasting, Amusement and

entertainment, Press

2211

2212

2213

2214

2215

74811

92111

92112

92201

92202

92203

9212

9213

92343

9240

Publishing of books

Publishing of periodicals

Publishing of magazines

Publishers of sound recording

Other publishers

Photography

Production of movies

Supporting services for movie production

Broadcasting organizations

Production of radio- and TV programs

Supporting activities for radio en TV

Distribution of movies

Cinemas

Other entertainment

Press-, news agencies; journalists

Creative

Business

Services

Advertising and Marketing,

Information and Technology,

Architecture, Design and Fashion

74201

74202

74401

74402

74875

Architecture and technical design

Technical design/advise e.g., city building

Commercial design- and consultancy agencies

Other commercial services

Interior-, fashion designers

RESEARCH QUESTIONS

Hypothesis:

Cities attract relatively more creative talent in creative industries, especially if these cities have a wealth of

cultural heritageRelated questions:

• What is the spatial distribution of firms in the creative industries?

• Is there a relationship with cultural heritage?

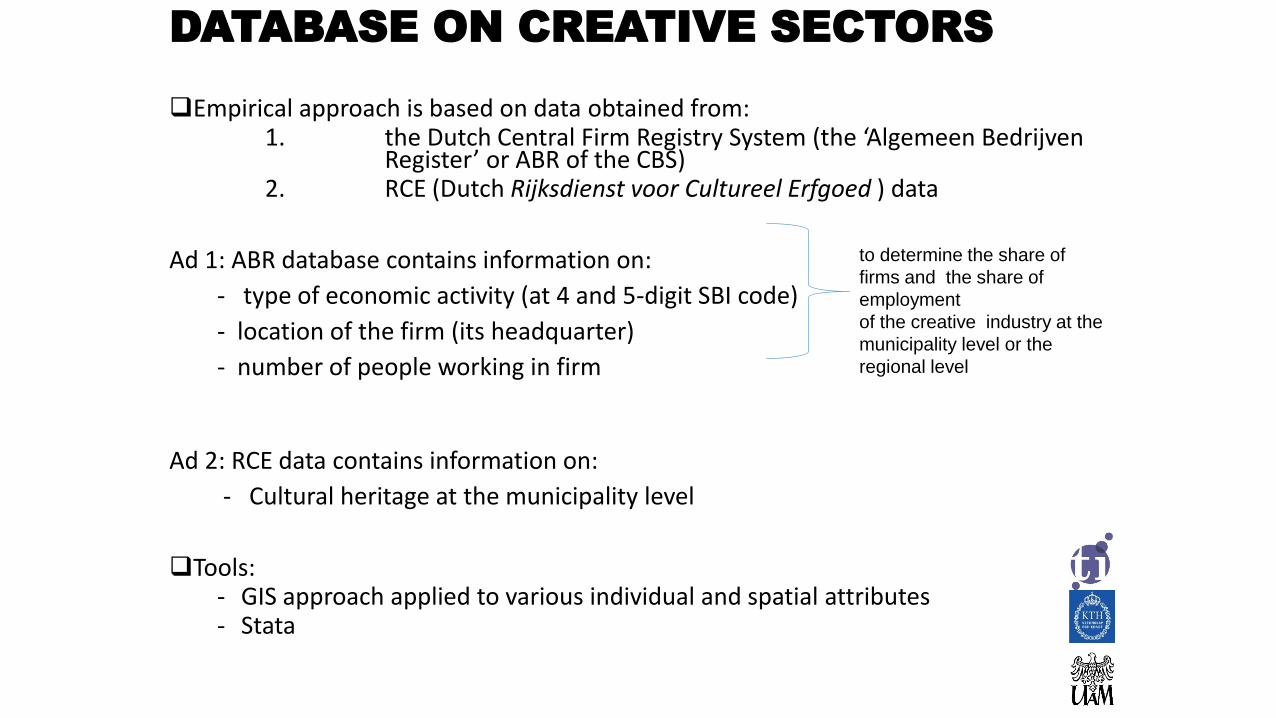

DATABASE ON CREATIVE SECTORS

Empirical approach is based on data obtained from:1. the Dutch Central Firm Registry System (the ‘Algemeen Bedrijven

Register’ or ABR of the CBS)2. RCE (Dutch Rijksdienst voor Cultureel Erfgoed ) data

Ad 1: ABR database contains information on:

- type of economic activity (at 4 and 5-digit SBI code)

- location of the firm (its headquarter)

- number of people working in firm

Ad 2: RCE data contains information on:

- Cultural heritage at the municipality level

Tools:- GIS approach applied to various individual and spatial attributes- Stata

to determine the share of

firms and the share of

employment

of the creative industry at the

municipality level or the

regional level

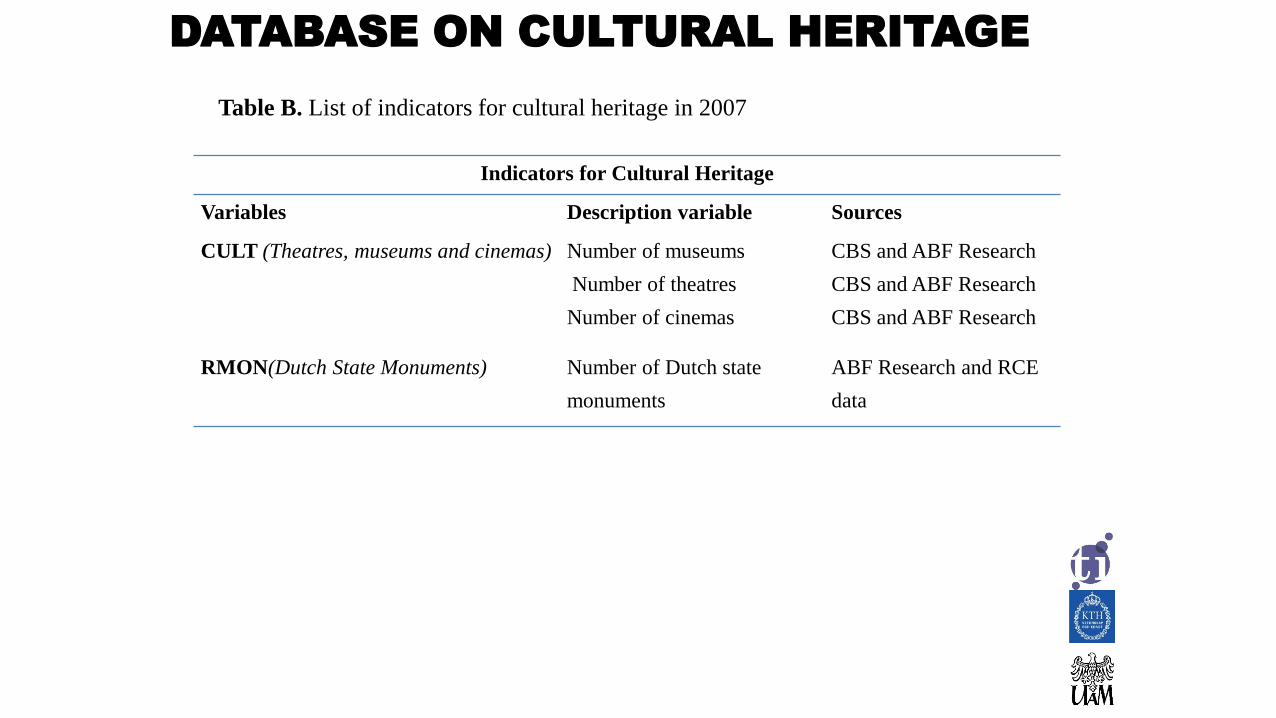

DATABASE ON CULTURAL HERITAGE

Indicators for Cultural Heritage

Variables Description variable Sources

CULT (Theatres, museums and cinemas) Number of museums

Number of theatres

Number of cinemas

CBS and ABF Research

CBS and ABF Research

CBS and ABF Research

RMON(Dutch State Monuments) Number of Dutch state

monuments

ABF Research and RCE

data

Table B. List of indicators for cultural heritage in 2007

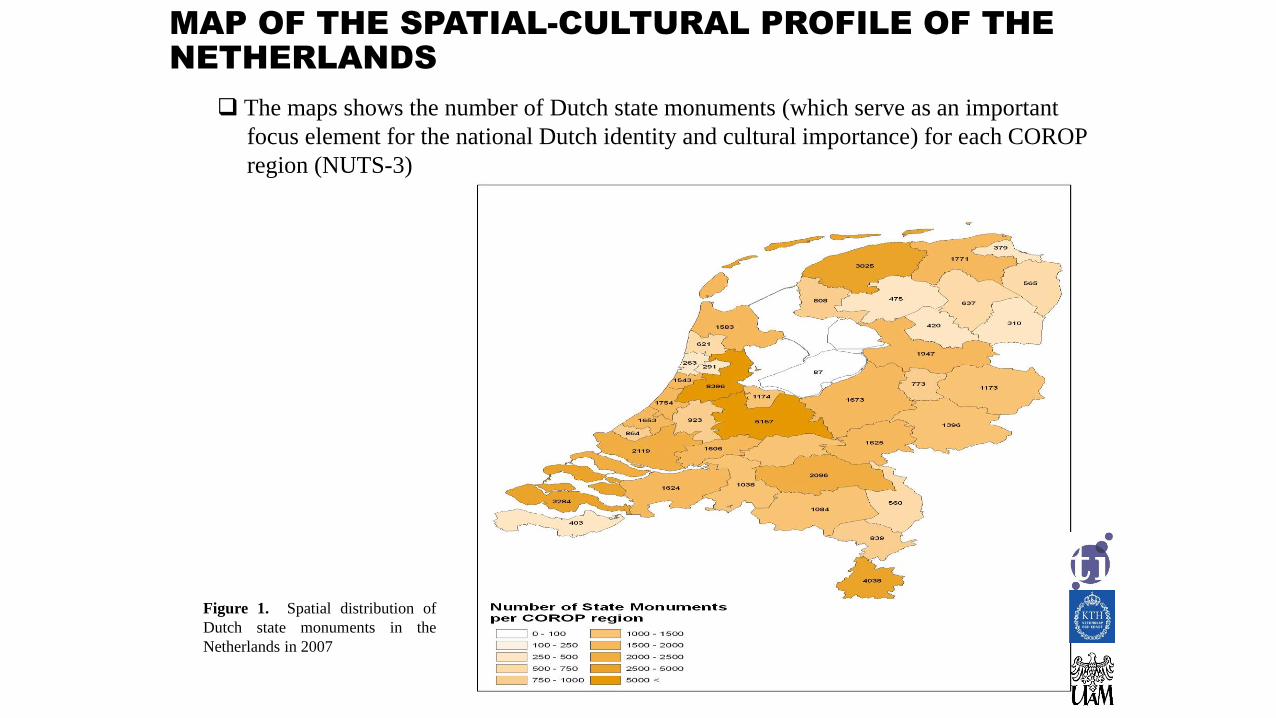

MAP OF THE SPATIAL-CULTURAL PROFILE OF THE

NETHERLANDS

The maps shows the number of Dutch state monuments (which serve as an important

focus element for the national Dutch identity and cultural importance) for each COROP

region (NUTS-3)

Figure 1. Spatial distribution of

Dutch state monuments in the

Netherlands in 2007

RESULTS

STEP 1

RESULTS:

Shares of the creative industries in the total economy of the Netherlands, in terms of the number of firms and the number of fte’s

Arts

(i)

Media

(ii)

Creative

business

services

(iii)

Creative

industries total

(%)

Share in number of firms (1994) 0.9% 1.4% 2.2% 4.5%

Share in number of firms (2009) 3.1% 2.3% 3.9% 9.2%

Share in fte’s (1994) 0.2% 0.9% 0.9% 2.0%

Share in fte’s (2009) 0.8% 1.0% 1.6% 3.4%

Table 1. Growth in importance of the creative sector (1994 and 2009)

1. The relative importance of the creative industries is rapidly rising over the period

considered (both the size of this sector and the employment in this sector)

2. Firms in the creative sector are on average smaller than firms in other sectors for

1994 as well as 2009 (the growth of the creative industry is mainly driven by the

entry of new firms)

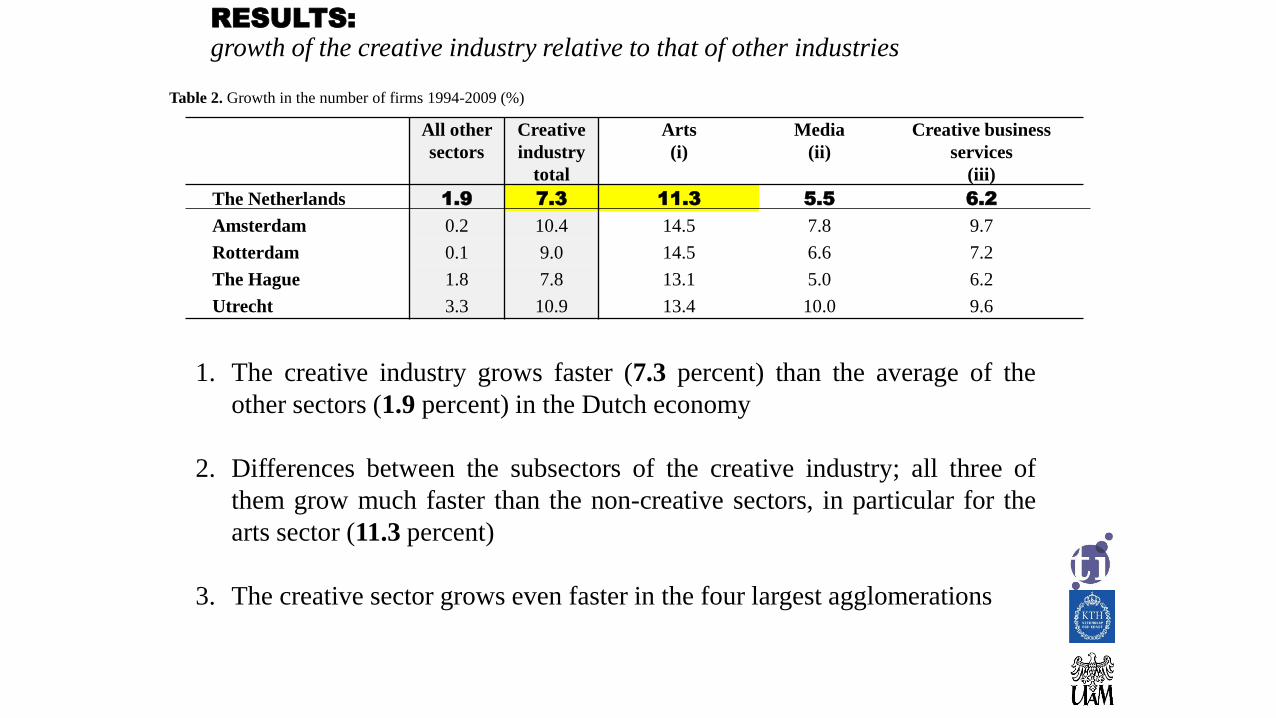

RESULTS:

growth of the creative industry relative to that of other industries

All other

sectors

Creative

industry

total

Arts

(i)

Media

(ii)

Creative business

services

(iii)

The Netherlands 1.9 7.3 11.3 5.5 6.2

Amsterdam 0.2 10.4 14.5 7.8 9.7

Rotterdam 0.1 9.0 14.5 6.6 7.2

The Hague 1.8 7.8 13.1 5.0 6.2

Utrecht 3.3 10.9 13.4 10.0 9.6

Table 2. Growth in the number of firms 1994-2009 (%)

1. The creative industry grows faster (7.3 percent) than the average of the

other sectors (1.9 percent) in the Dutch economy

2. Differences between the subsectors of the creative industry; all three of

them grow much faster than the non-creative sectors, in particular for the

arts sector (11.3 percent)

3. The creative sector grows even faster in the four largest agglomerations

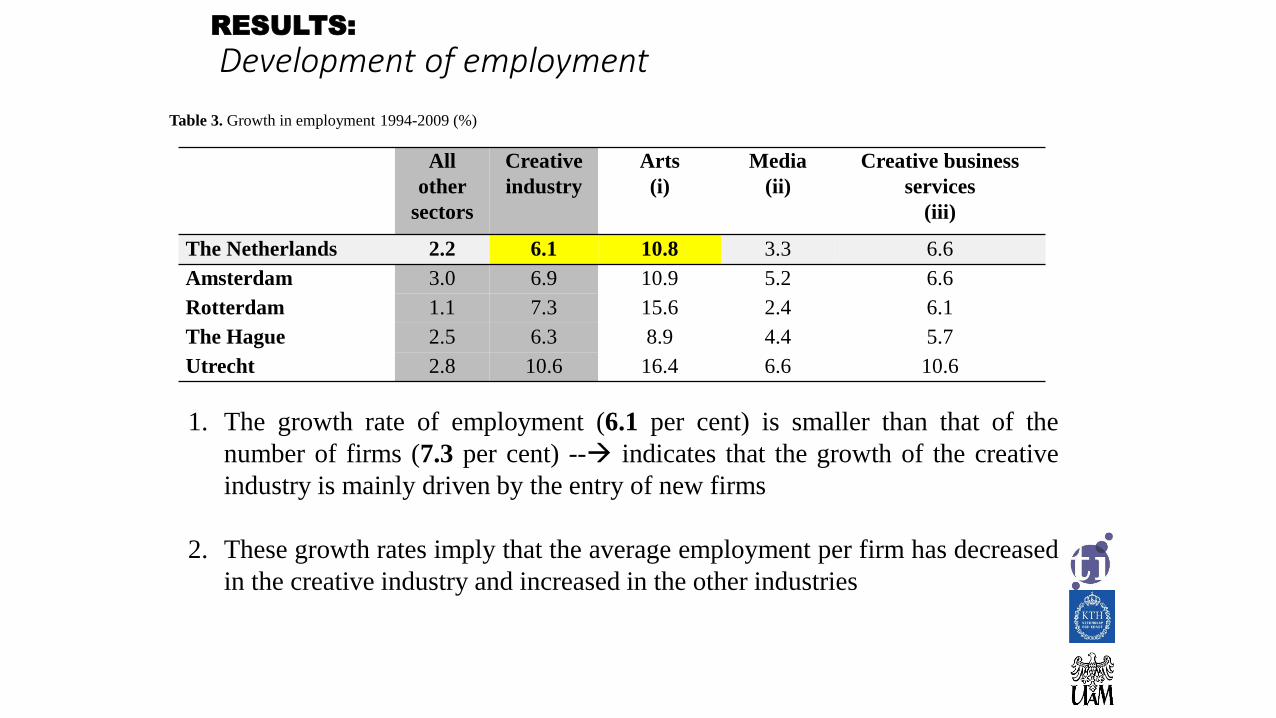

RESULTS:

Development of employment

All

other

sectors

Creative

industry

Arts

(i)

Media

(ii)

Creative business

services

(iii)

The Netherlands 2.2 6.1 10.8 3.3 6.6

Amsterdam 3.0 6.9 10.9 5.2 6.6

Rotterdam 1.1 7.3 15.6 2.4 6.1

The Hague 2.5 6.3 8.9 4.4 5.7

Utrecht 2.8 10.6 16.4 6.6 10.6

Table 3. Growth in employment 1994-2009 (%)

1. The growth rate of employment (6.1 per cent) is smaller than that of the

number of firms (7.3 per cent) -- indicates that the growth of the creative

industry is mainly driven by the entry of new firms

2. These growth rates imply that the average employment per firm has decreased

in the creative industry and increased in the other industries

RESULTS:

Evolution of employment growth and the increase in the number of firms in the creative sector

Figure 2. Number of firms (left axis, 1994 = 100) and fte’s per firm (right axis)

1. In the period 1994 – 2009, the number of firms in the creative industry has almost

tripled, while the increase in the number of firms in the other sectors was modest

2. The average employment generated by firms in the creative industry is about 3 fte,

while firms in other sectors employ on average 7 fte

3. Firms in the creative industry are on average much smaller than firms in other sectors

RESULTS

STEP 2

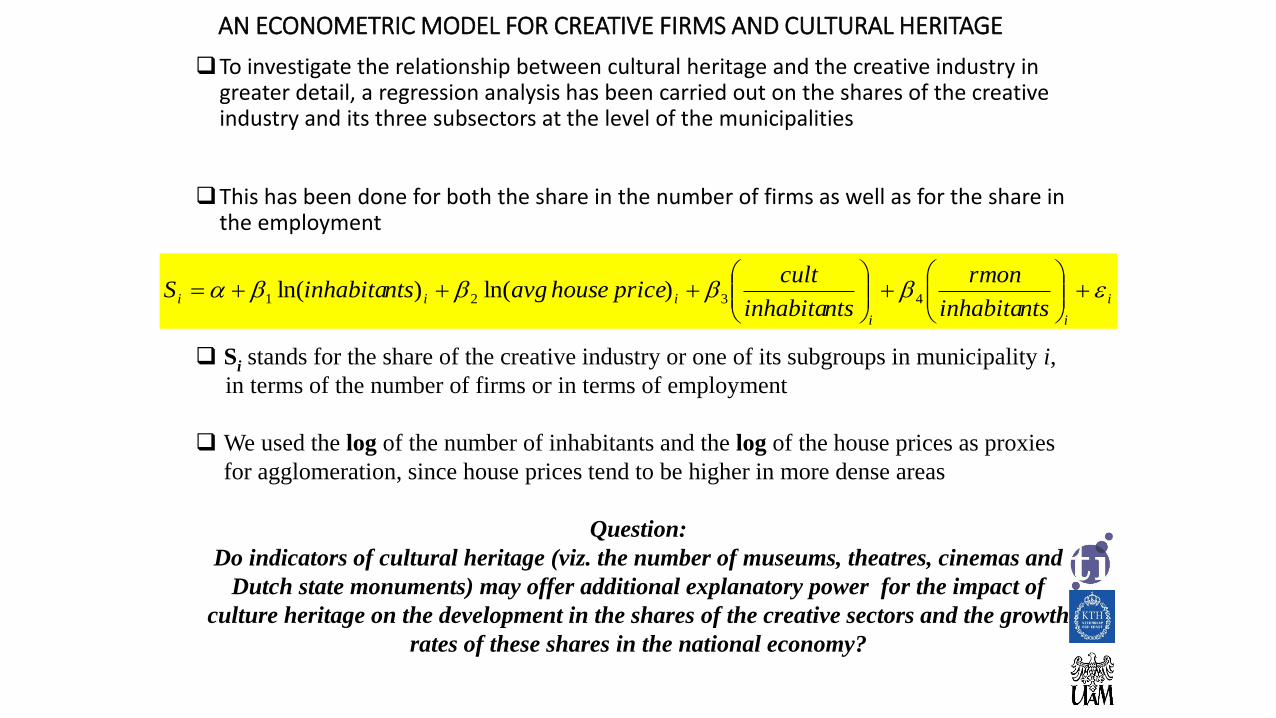

AN ECONOMETRIC MODEL FOR CREATIVE FIRMS AND CULTURAL HERITAGE

To investigate the relationship between cultural heritage and the creative industry in greater detail, a regression analysis has been carried out on the shares of the creative industry and its three subsectors at the level of the municipalities

This has been done for both the share in the number of firms as well as for the share in the employment

i

ii

iiintsinhabita

rmon

ntsinhabita

cultpricehouseavgntsinhabitaS

4321 )ln()ln(

Si stands for the share of the creative industry or one of its subgroups in municipality i,

in terms of the number of firms or in terms of employment

We used the log of the number of inhabitants and the log of the house prices as proxies

for agglomeration, since house prices tend to be higher in more dense areas

Question:

Do indicators of cultural heritage (viz. the number of museums, theatres, cinemas and

Dutch state monuments) may offer additional explanatory power for the impact of

culture heritage on the development in the shares of the creative sectors and the growth

rates of these shares in the national economy?

Creative industry

Coef. (Std. Err)

Arts

(i)

Coef. (Std. Err)

Media

(ii)

Coef. (Std. Err)

Creative Business

Services (iii)

Coef. (Std. Err)

Const -.496 (.054) -.108 (.024) -.169 (.019) -.219 (.021)

Log (#inhabitants) .015*** (.001) .006*** (.001) .004*** (.001) .005*** (.001)

Log (house price) .034*** (.004) .006*** (.002) .012*** (.002) .016*** (.002)

Theatres etc. per inhabitant 10.106 (9.511) 12.327*** (4.263) 3.183 (3.232) -5.404 (3.700)

Monuments per inhabitant 1.283*** (.220) .683*** ( .0987) .356*** (.0748) .244*** (.086)

Observations 436 436 436 436

R2 0.33 0.26 0.27 0.34

Method OLS OLS OLS OLS

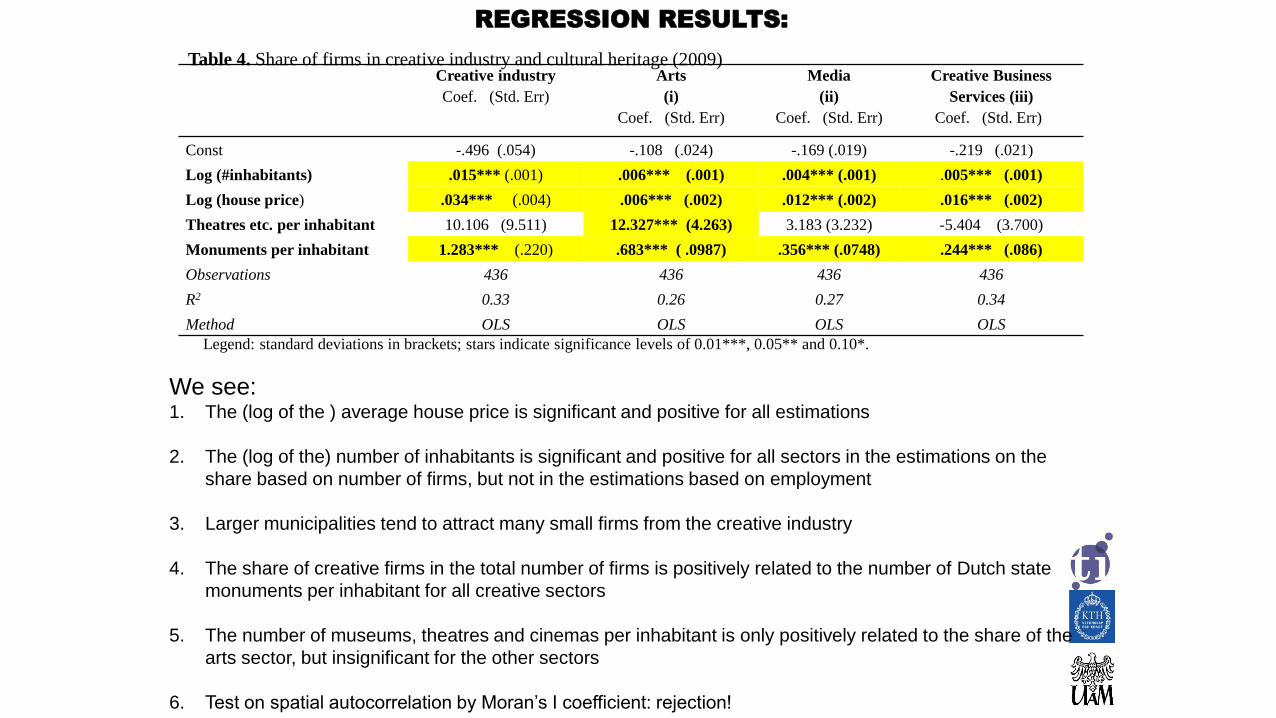

Table 4. Share of firms in creative industry and cultural heritage (2009)

Legend: standard deviations in brackets; stars indicate significance levels of 0.01***, 0.05** and 0.10*.

REGRESSION RESULTS:

We see:1. The (log of the ) average house price is significant and positive for all estimations

2. The (log of the) number of inhabitants is significant and positive for all sectors in the estimations on the

share based on number of firms, but not in the estimations based on employment

3. Larger municipalities tend to attract many small firms from the creative industry

4. The share of creative firms in the total number of firms is positively related to the number of Dutch state

monuments per inhabitant for all creative sectors

5. The number of museums, theatres and cinemas per inhabitant is only positively related to the share of the

arts sector, but insignificant for the other sectors

6. Test on spatial autocorrelation by Moran’s I coefficient: rejection!

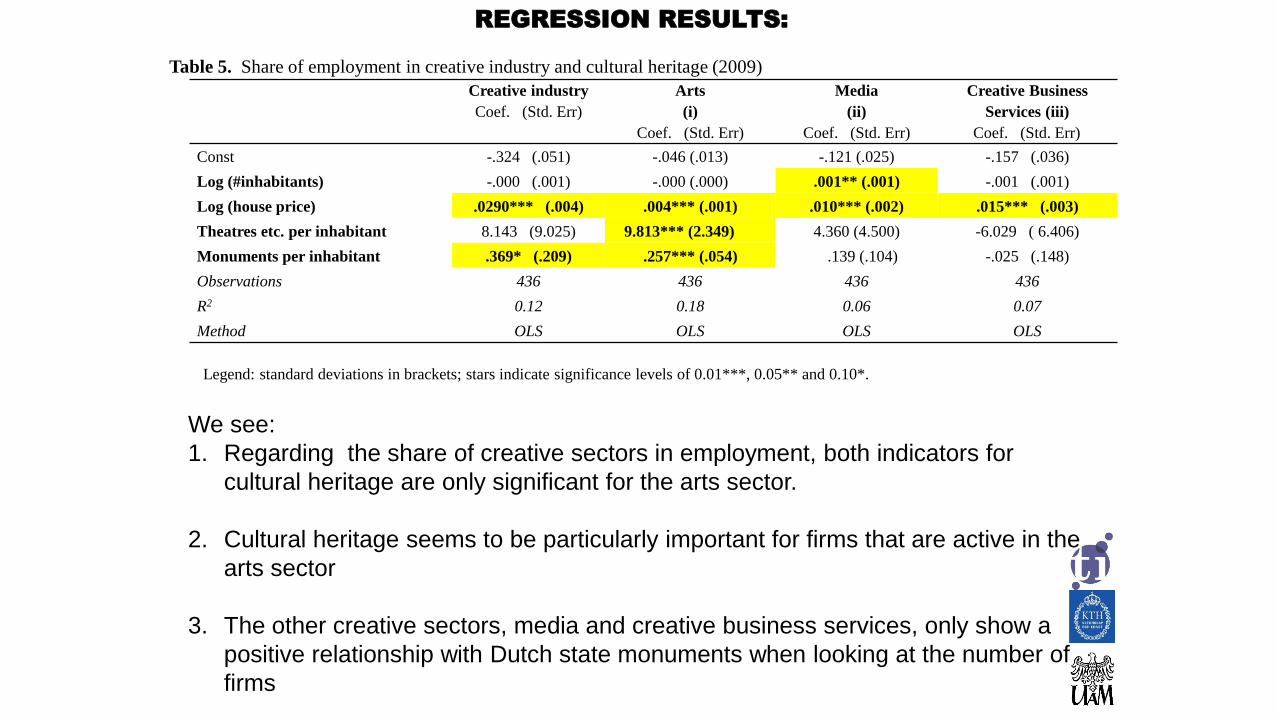

Creative industry

Coef. (Std. Err)

Arts

(i)

Coef. (Std. Err)

Media

(ii)

Coef. (Std. Err)

Creative Business

Services (iii)

Coef. (Std. Err)

Const -.324 (.051) -.046 (.013) -.121 (.025) -.157 (.036)

Log (#inhabitants) -.000 (.001) -.000 (.000) .001** (.001) -.001 (.001)

Log (house price) .0290*** (.004) .004*** (.001) .010*** (.002) .015*** (.003)

Theatres etc. per inhabitant 8.143 (9.025) 9.813*** (2.349) 4.360 (4.500) -6.029 ( 6.406)

Monuments per inhabitant .369* (.209) .257*** (.054) .139 (.104) -.025 (.148)

Observations 436 436 436 436

R2 0.12 0.18 0.06 0.07

Method OLS OLS OLS OLS

Table 5. Share of employment in creative industry and cultural heritage (2009)

REGRESSION RESULTS:

Legend: standard deviations in brackets; stars indicate significance levels of 0.01***, 0.05** and 0.10*.

We see:

1. Regarding the share of creative sectors in employment, both indicators for

cultural heritage are only significant for the arts sector.

2. Cultural heritage seems to be particularly important for firms that are active in the

arts sector

3. The other creative sectors, media and creative business services, only show a

positive relationship with Dutch state monuments when looking at the number of

firms

FURTHERMORE

• In order to investigate the relationship between the annual change in the creative sector and the presence of cultural heritage, we also regressed the change in the share of firms in the creative sector and the three subsectors on the same set of explanatory variables (Table 6)

• This allows us to assess whether the creative sector will grow faster than the non-creative sector in municipalities with a relatively high density of cultural heritage

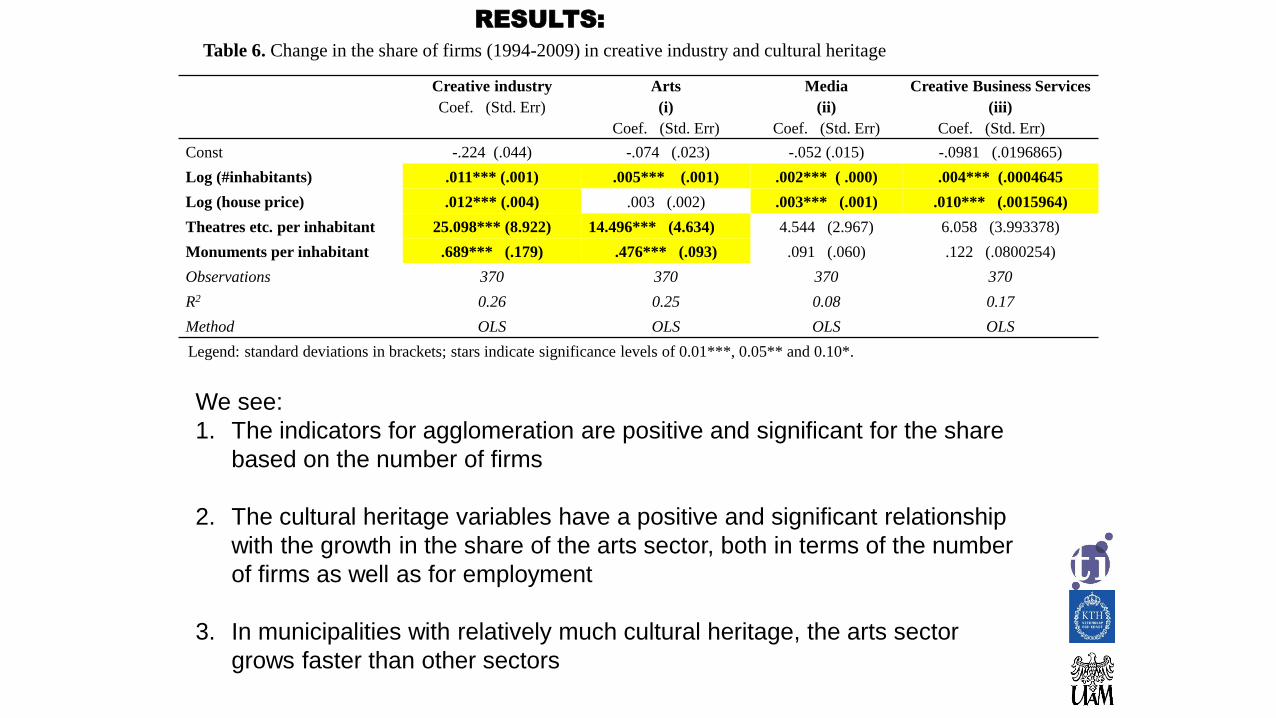

Creative industry

Coef. (Std. Err)

Arts

(i)

Coef. (Std. Err)

Media

(ii)

Coef. (Std. Err)

Creative Business Services

(iii)

Coef. (Std. Err)

Const -.224 (.044) -.074 (.023) -.052 (.015) -.0981 (.0196865)

Log (#inhabitants) .011*** (.001) .005*** (.001) .002*** ( .000) .004*** (.0004645

Log (house price) .012*** (.004) .003 (.002) .003*** (.001) .010*** (.0015964)

Theatres etc. per inhabitant 25.098*** (8.922) 14.496*** (4.634) 4.544 (2.967) 6.058 (3.993378)

Monuments per inhabitant .689*** (.179) .476*** (.093) .091 (.060) .122 (.0800254)

Observations 370 370 370 370

R2 0.26 0.25 0.08 0.17

Method OLS OLS OLS OLS

Table 6. Change in the share of firms (1994-2009) in creative industry and cultural heritage

Legend: standard deviations in brackets; stars indicate significance levels of 0.01***, 0.05** and 0.10*.

We see:

1. The indicators for agglomeration are positive and significant for the share

based on the number of firms

2. The cultural heritage variables have a positive and significant relationship

with the growth in the share of the arts sector, both in terms of the number

of firms as well as for employment

3. In municipalities with relatively much cultural heritage, the arts sector

grows faster than other sectors

RESULTS:

Creative industry

Coef. (Std. Err)

Arts

(i)

Coef. (Std. Err)

Media

(ii)

Coef. (Std. Err)

Creative Business

Services (iii)

Coef. (Std. Err)

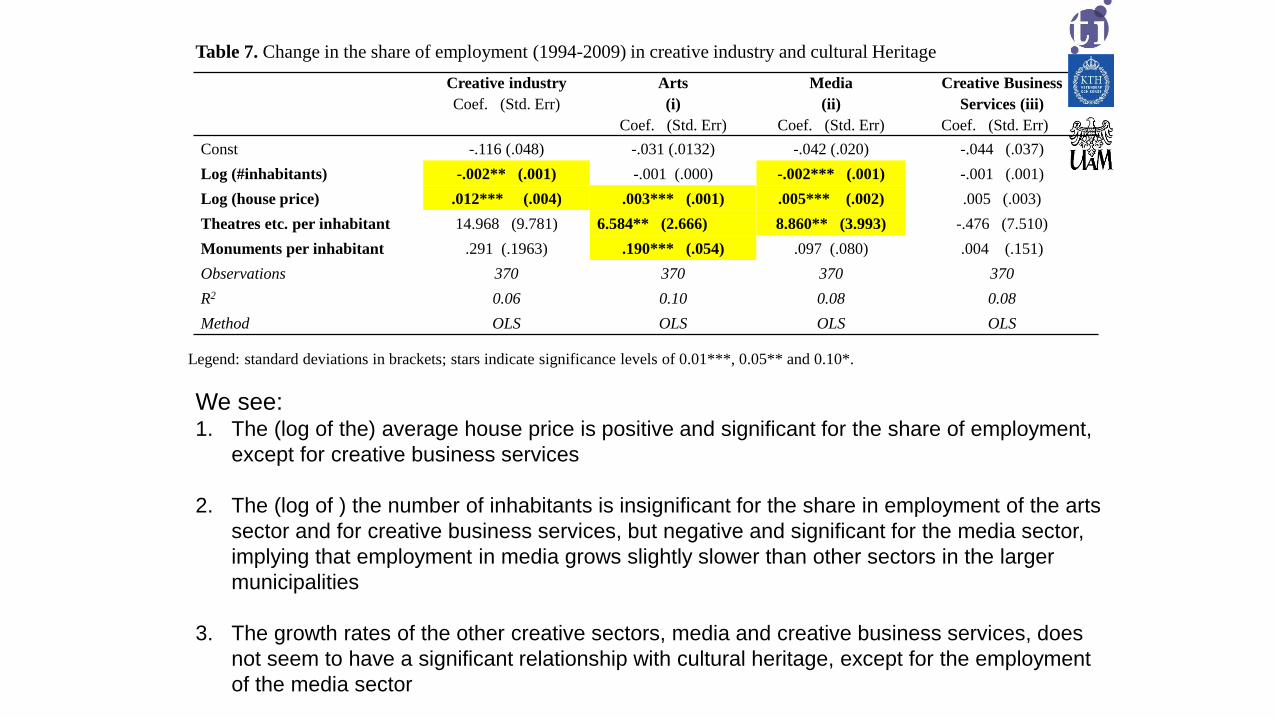

Const -.116 (.048) -.031 (.0132) -.042 (.020) -.044 (.037)

Log (#inhabitants) -.002** (.001) -.001 (.000) -.002*** (.001) -.001 (.001)

Log (house price) .012*** (.004) .003*** (.001) .005*** (.002) .005 (.003)

Theatres etc. per inhabitant 14.968 (9.781) 6.584** (2.666) 8.860** (3.993) -.476 (7.510)

Monuments per inhabitant .291 (.1963) .190*** (.054) .097 (.080) .004 (.151)

Observations 370 370 370 370

R2 0.06 0.10 0.08 0.08

Method OLS OLS OLS OLS

Table 7. Change in the share of employment (1994-2009) in creative industry and cultural Heritage

Legend: standard deviations in brackets; stars indicate significance levels of 0.01***, 0.05** and 0.10*.

We see: 1. The (log of the) average house price is positive and significant for the share of employment,

except for creative business services

2. The (log of ) the number of inhabitants is insignificant for the share in employment of the arts

sector and for creative business services, but negative and significant for the media sector,

implying that employment in media grows slightly slower than other sectors in the larger

municipalities

3. The growth rates of the other creative sectors, media and creative business services, does

not seem to have a significant relationship with cultural heritage, except for the employment

of the media sector

OVERAL CONCLUSION

1. Our results demonstrate that at the level of the municipality, cultural heritage such as Dutch state monuments can play a role in both the level as well as the change of the share of creative firms and employment in creative firms

2. This relationship is mainly caused by the arts sector, and is less prominent in the other creative sectors

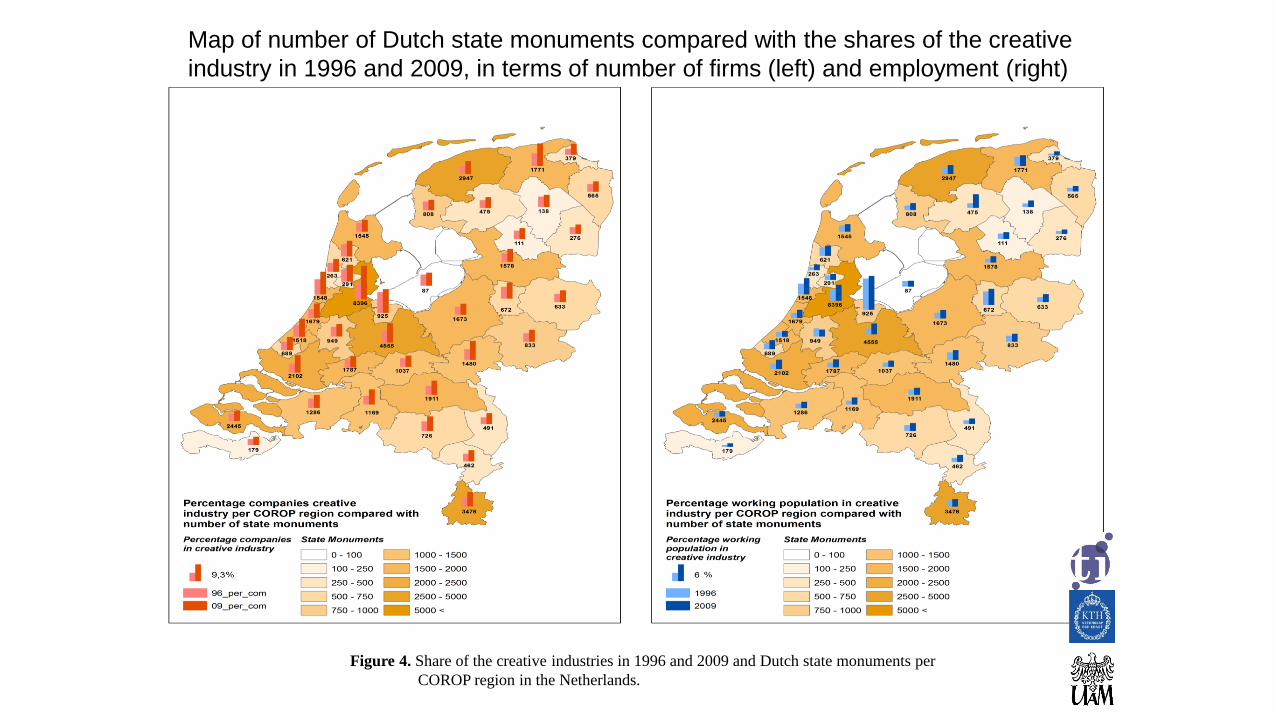

Figure 4. Share of the creative industries in 1996 and 2009 and Dutch state monuments per

COROP region in the Netherlands.

Map of number of Dutch state monuments compared with the shares of the creative

industry in 1996 and 2009, in terms of number of firms (left) and employment (right)

Concluding RemarksOur research has explored the relationship between urban cultural heritage and the level and

growth of various branches of the creative sector, with a particular view to urban agglomerations in the Netherlands:

1. The creative sector in the Netherlands appears to grow – in terms of both the number of firms and the number of jobs – significantly faster than other industries over the period 1994-2009; especially the high entry rates of new firms plays a critical role here

2. The creative industry appears to be mainly concentrated - and to have the highest growth rates – in urban areas. Agglomeration externalities are apparently an essential element here. Especially Amsterdam appears to have a strong creativity profile

3. The four urban agglomerations in the Netherlands turn out to offer favourableseedbed conditions for a strongly operating creative industry , especially when there is abundant presence of cultural capital, and more in particular cultural heritage (monuments, performing arts etc.). This holds in particular for the arts sector, and less for the media sector and the creative business services

Our results suggest a clear relationship between cultural heritage and creative industries, but further research is necessary to determine whether there is a causal relationship

Thank you for your attention

Related Documents