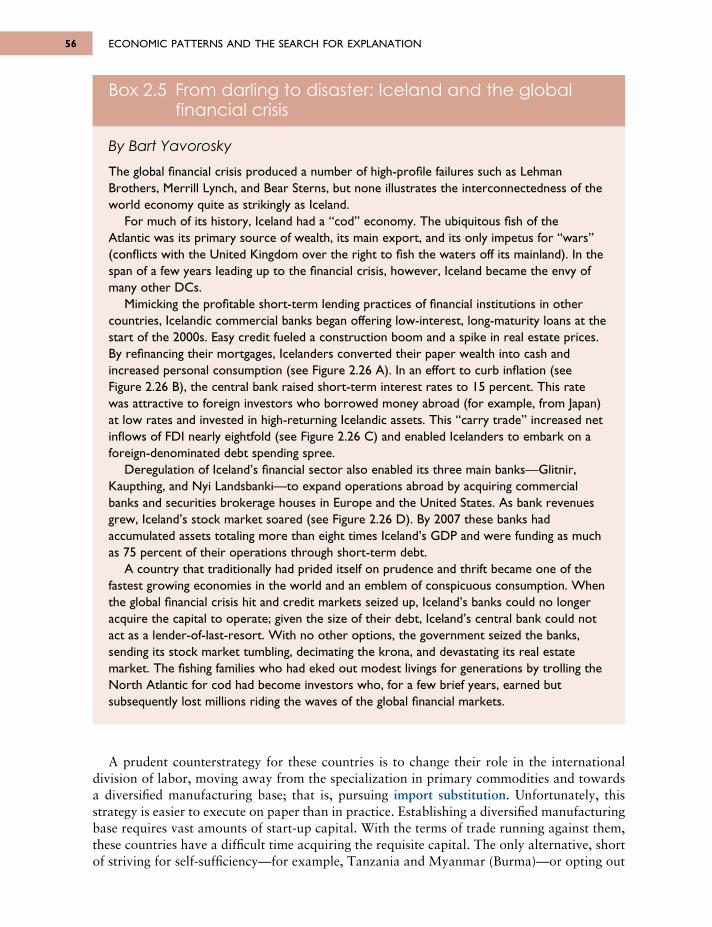

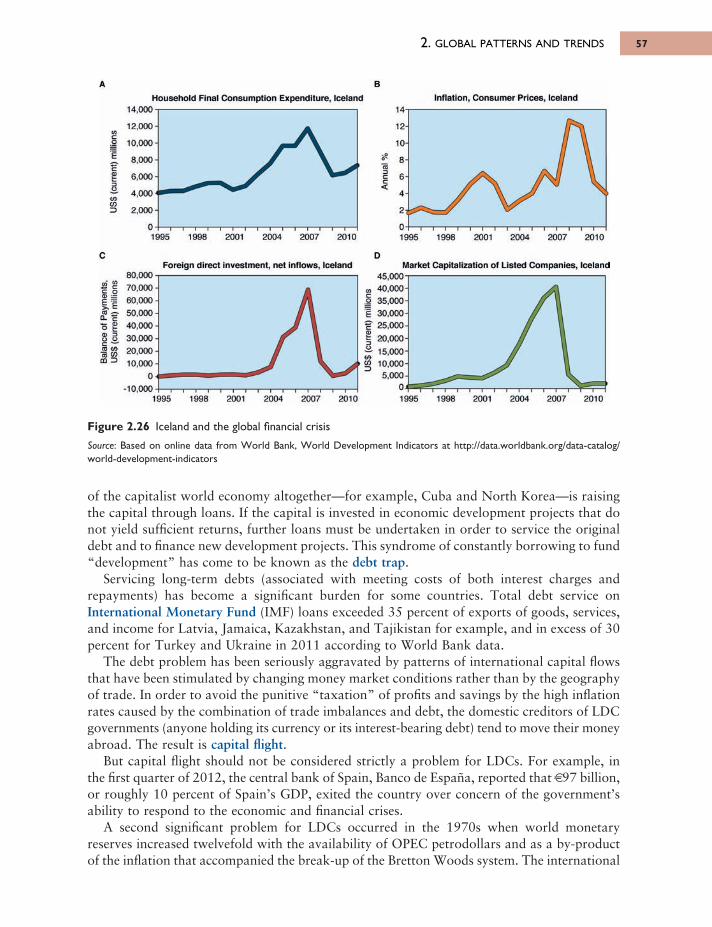

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

THE GEOGRAPHY OF THE WORLD ECONOMY

The Geography of the World Economy provides an in-depth and stimulating introduction tothe globalization of the world economy. The book offers a consideration of local, regional,national and global economic development over the long historical term. The theory and practiceof economic and political geography provide a basis for understanding the interactions withinand among the developed and developing countries of the world. Illustrated in colourthroughout, this new edition has been completely reworked and updated to take account ofrecent significant changes in the world economy.

A new companion website also accompanies the book, with additional resources for eachchapter including multiple choice and short essay questions and links to relevant websites.Figures and tables are also available for download located at www.routledge.com/cw/knox

The text is signposted throughout with an glossary of key terms, and is richly illustratedwith full-colour maps, diagrams and illustrations. It is ideal for upper level universityundergraduates and for post-graduates in a variety of specializations including geography,economics, political science, international relations and global studies.

Paul Knox, University Distinguished Professor and Senior Fellow for International Advance-ment, Virginia Polytechnic Institute and State University, USA.

John Agnew, Distinguished Professor, University of California, Los Angeles, USA.

Linda McCarthy, Associate Professor, University of Wisconsin-Milwaukee, USA.

6063 GEOGRAPHY WORLD ECON_PT_246x189 mm 22/01/2014 15:09 Page i

6063 GEOGRAPHY WORLD ECON_PT_246x189 mm 22/01/2014 15:09 Page ii

This page intentionally left blank

THE GEOGRAPHYOF THE WORLDECONOMYSixth Edition

Paul Knox, John Agnew and Linda McCarthy

6063 GEOGRAPHY WORLD ECON_PT_246x189 mm 22/01/2014 15:09 Page iii

RoutledgeTaylor & Francis Croup

LO ND O N A N D NEW YORK

First edition published in 1989 by Edward ArnoldFifth edition published in 2008 by Hodder Education

Sixth edition published in 2014by Routledge2 Park Square, Milton Park, Abingdon, Oxon OX14 4RN

and by Routledge711 Third Avenue, New York, NY 10017

Routledge is an imprint of the Taylor & Francis Group, an informa business

© 2014 Paul Knox, John Agnew and Linda McCarthy

The right of Paul Knox, John Agnew and Linda McCarthy to be identified as authors of this work has been asserted by them in accordance with sections 77 and 78 of the Copyright, Designs and Patents Act 1988.

All rights reserved. No part of this book may be reprinted or reproduced or utilised in any form or by any electronic, mechanical, or other means, now known or hereafter invented, including photocopying and recording, or in any information storage or retrieval system, without permission in writing from the publishers.

Trademark notice: Product or corporate names may be trademarks or registered trademarks, and are used only for identification and explanation without intent to infringe.

British Library Cataloguing in Publication DataA catalogue record for this book is available from the British Library

Library of Congress Cataloging in Publication DataKnox, Paul L.The geography of the world economy/Paul Knox, John Agnew and Linda McCarthy.

pages cmIncludes bibliographical references and index.1. Economic geography. 2. Economic history. I. Agnew, John A. II. McCarthy, Linda (Linda Mary) III. Title.HF1025.K573 2014330.9–dc23 2013027243

ISBN: 978-0-415-83128-4 (hbk)ISBN: 978-1-44-418470-9 (pbk)ISBN: 978-0-203-77518-9 (ebk)

Typeset in Gill Sans and Sabon by Florence Production Ltd, Stoodleigh, Devon, UK

6063 GEOGRAPHY WORLD ECON_PT_246x189 mm 22/01/2014 15:09 Page iv

List of figures viii

List of tables xi

List of boxes xiii

Acknowledgements xiv

PART 1ECONOMIC PATTERNS AND THE SEARCH FOR EXPLANATION 1

1 The changing world economy 3

1.1 Studying the world economy 51.2 Economic organization and spatial change 61.3 Spatial divisions of labor 12

Key sources and suggested reading 19

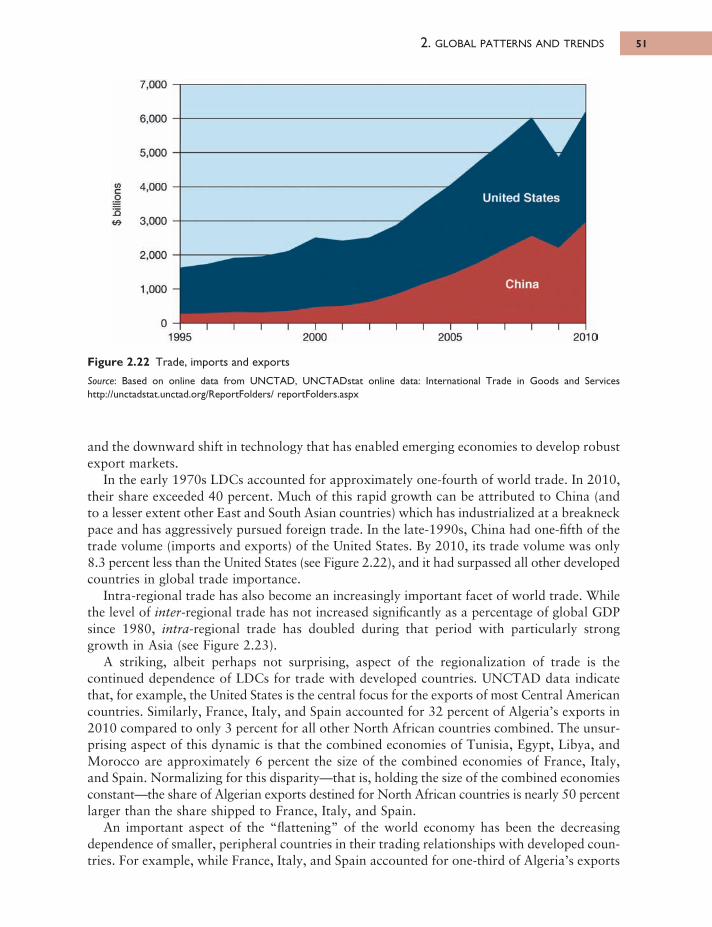

2 Global patterns and trends 20

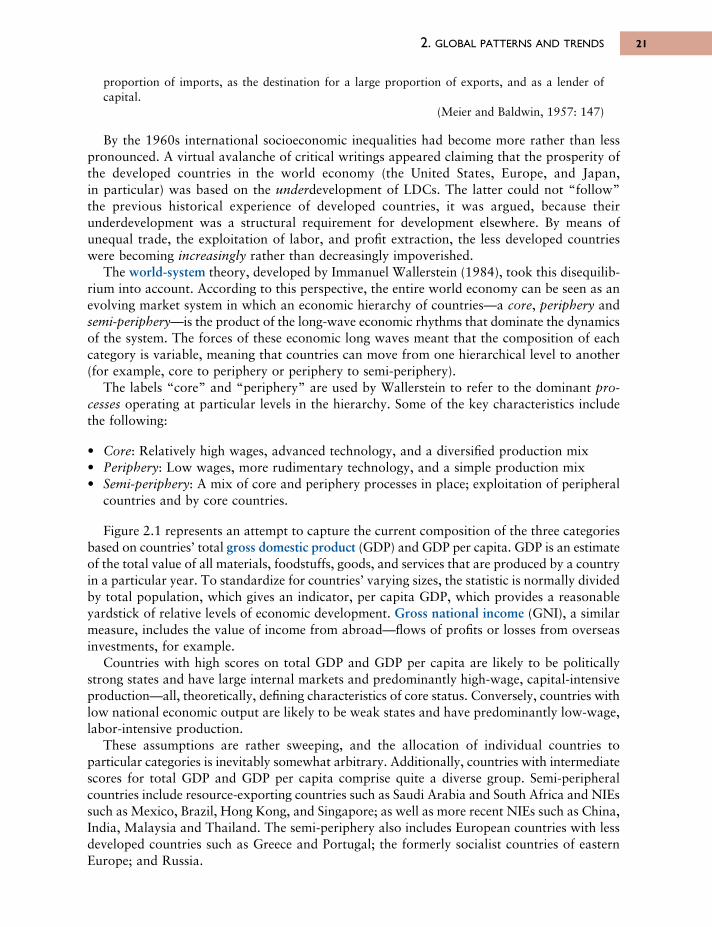

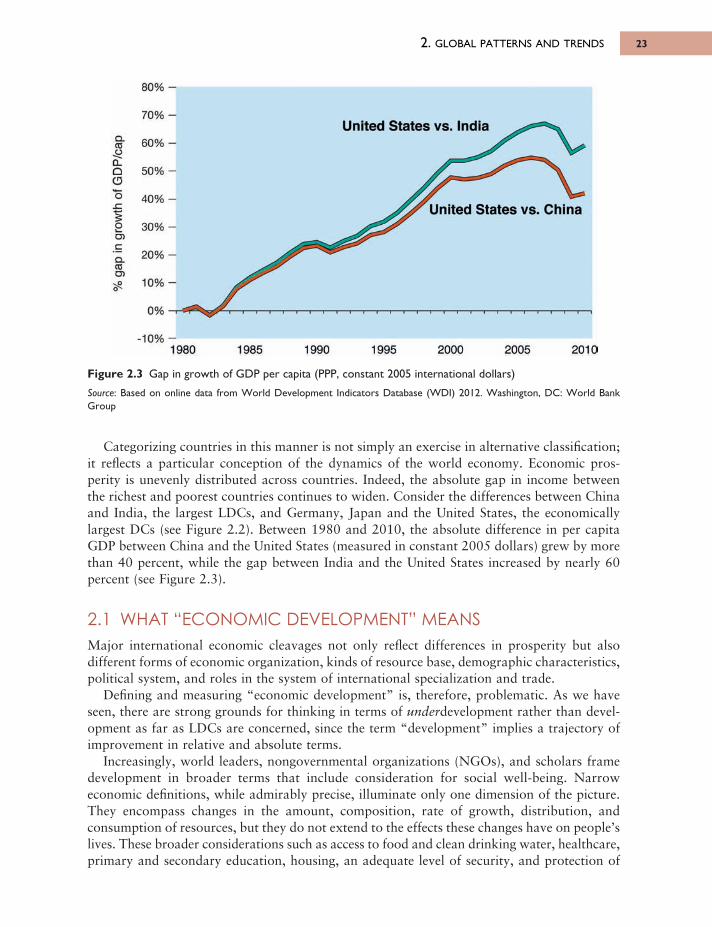

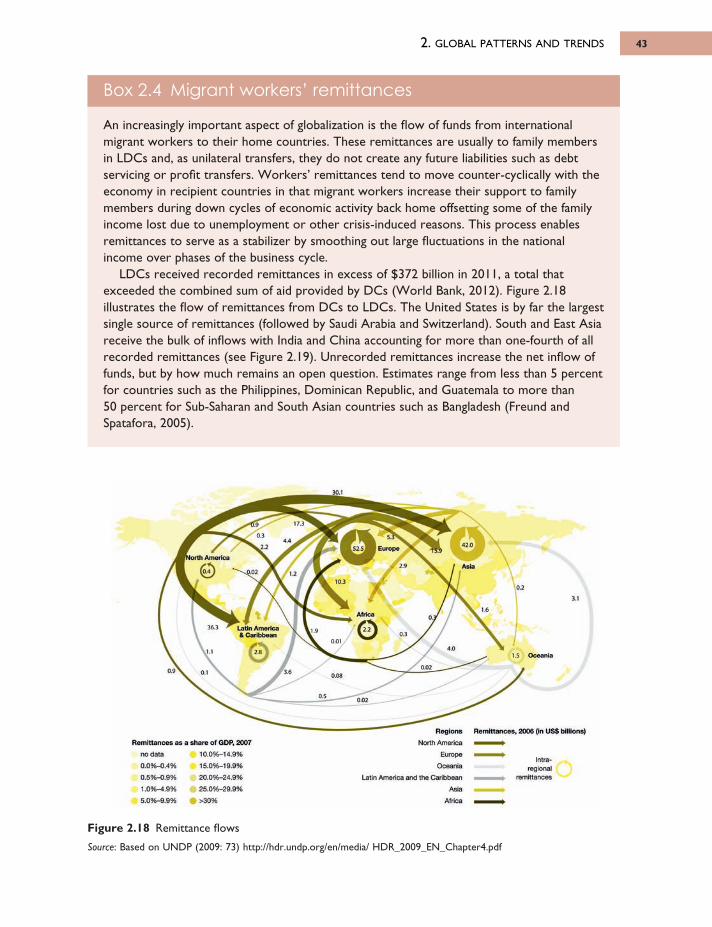

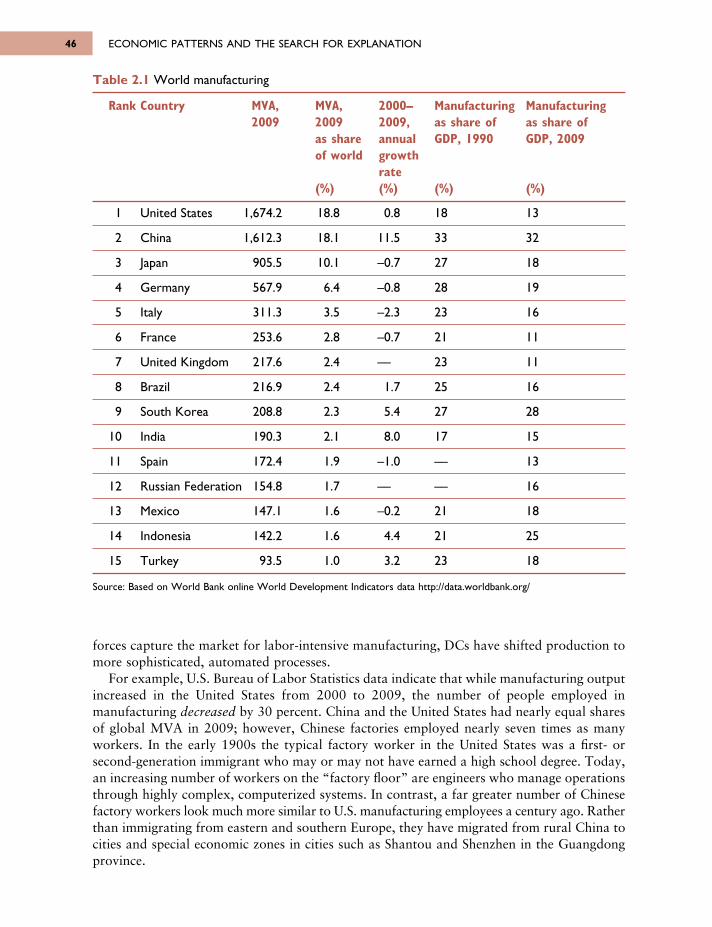

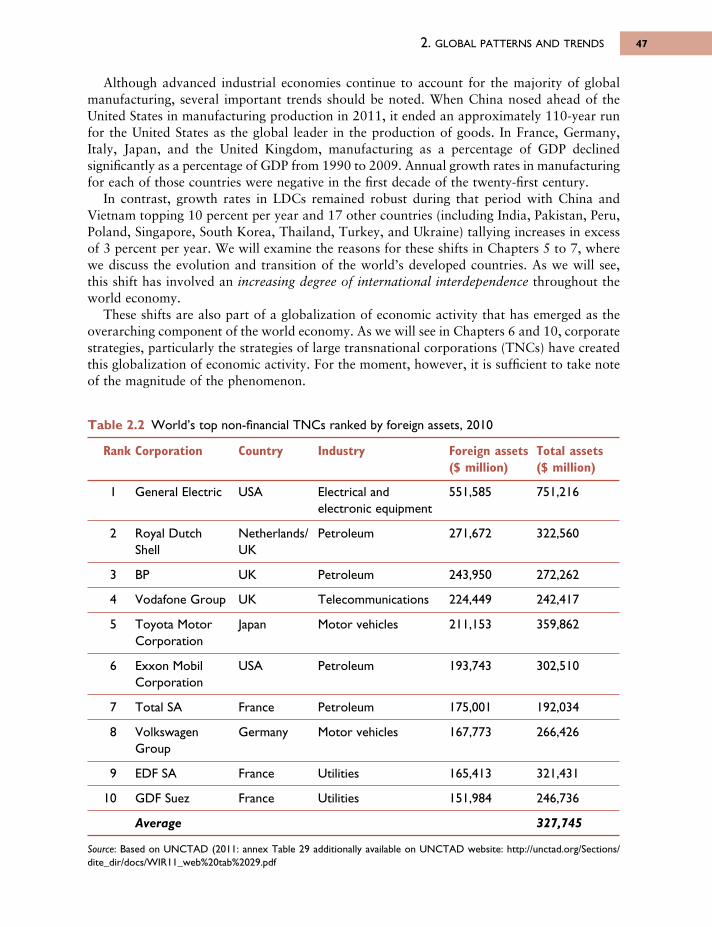

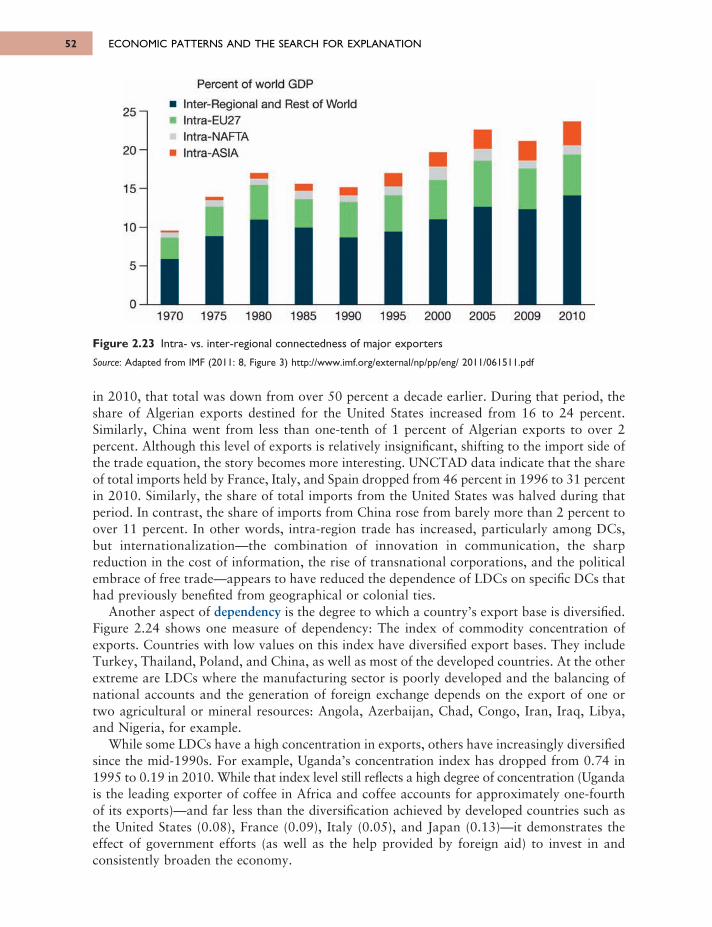

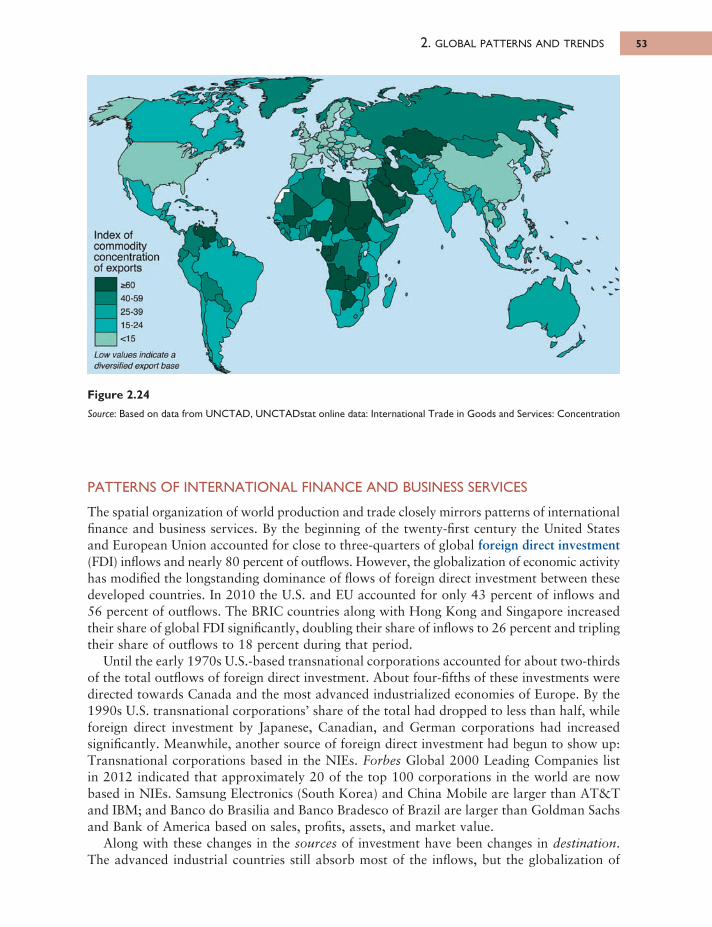

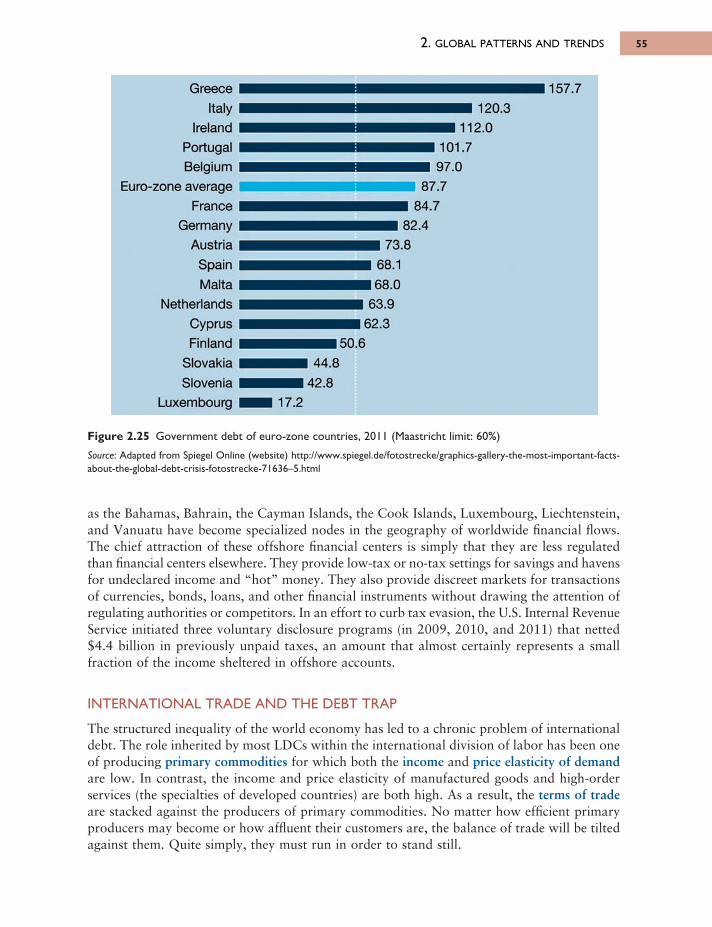

2.1 What “economic development” means 232.2 International patterns of resources and population 292.3 International patterns of industry and finance 45

Summary 59Key sources and suggested reading 60

3 Geographical dynamics of the world economy 61

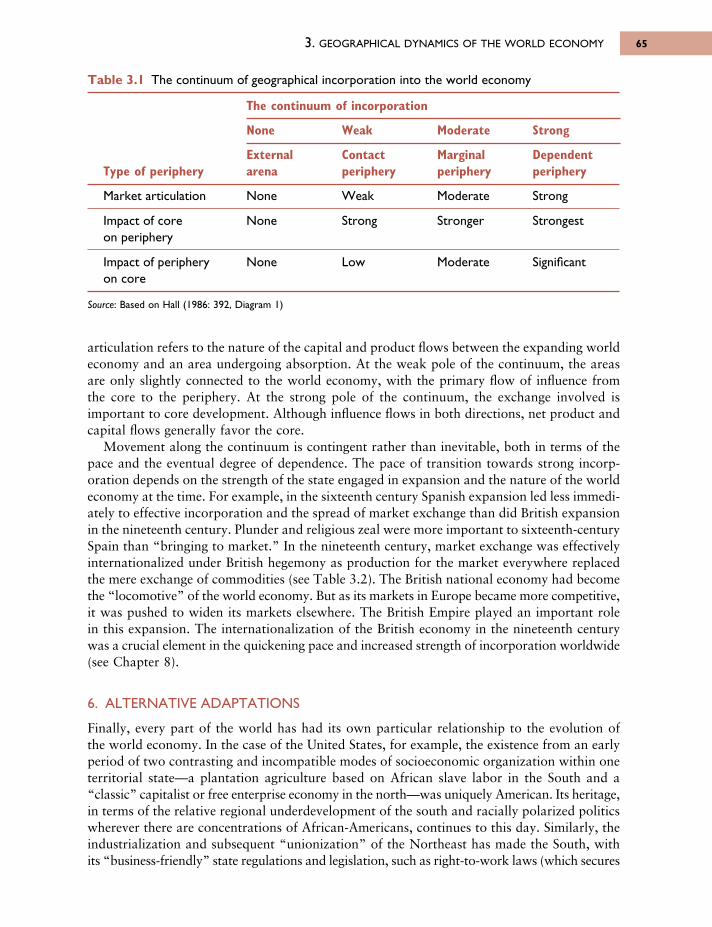

3.1 History of the world economy 623.2 States and the world economy 663.3 “Market access” and the regional motors of the world

economy 79Summary 91Key sources and suggested reading 91

PART 2RISE OF THE CORE ECONOMIES 93

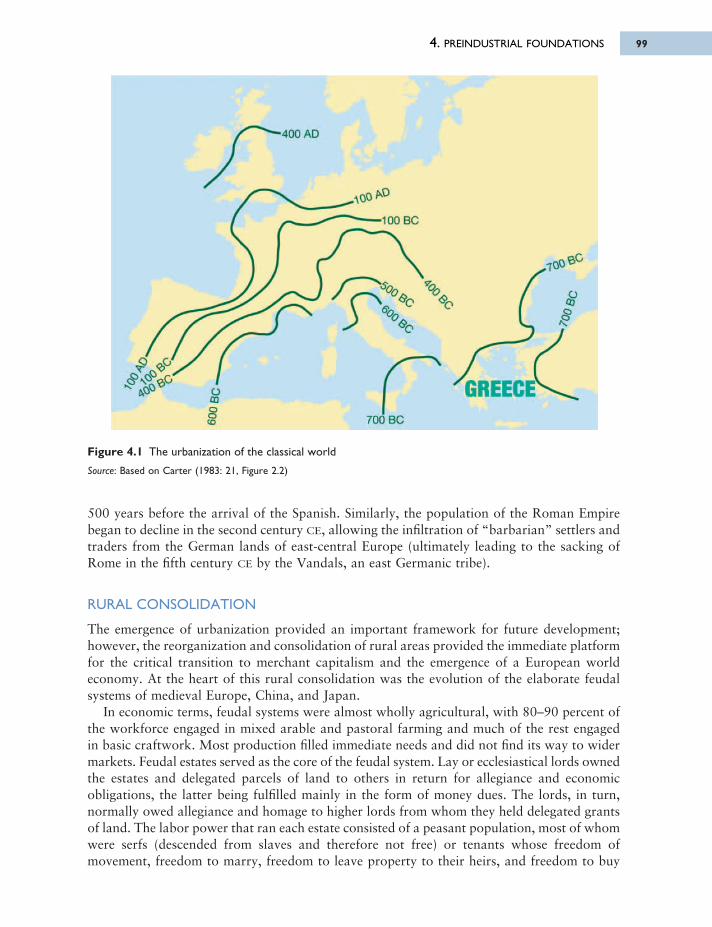

4 Preindustrial foundations 95

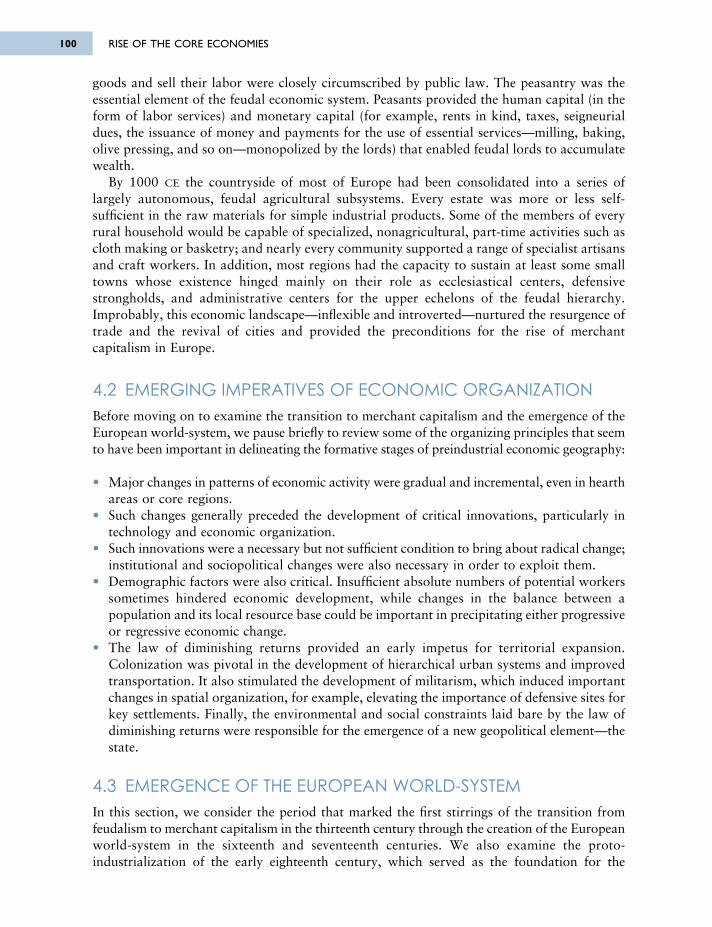

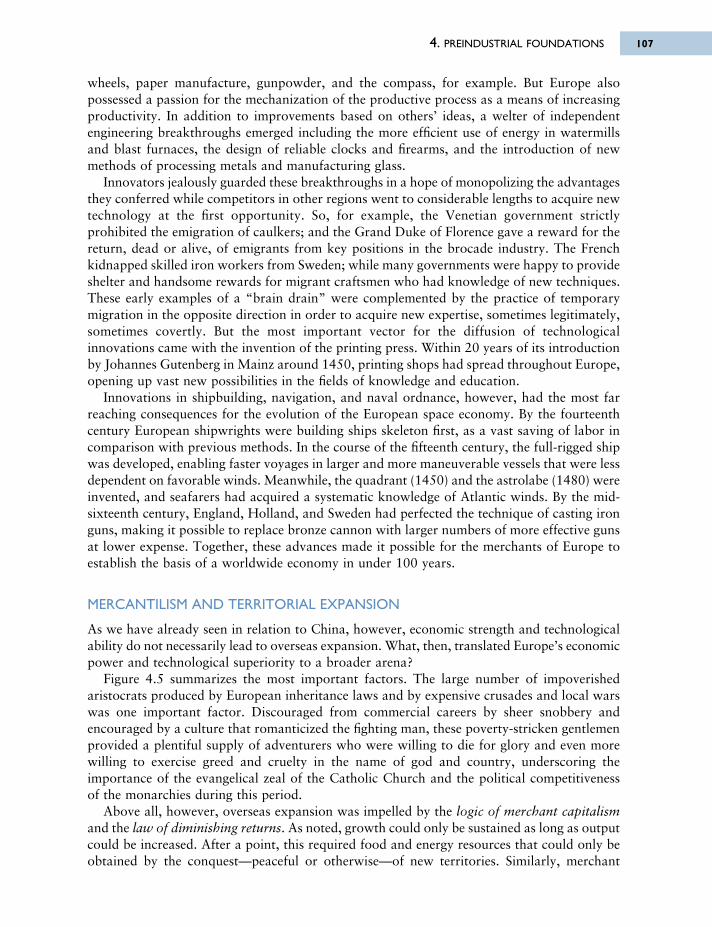

4.1 Beginnings 954.2 Emerging imperatives of economic organization 1004.3 Emergence of the European world-system 100

Summary 113Key sources and suggested reading 115

Contents

6063 GEOGRAPHY WORLD ECON_PT_246x189 mm 22/01/2014 15:09 Page v

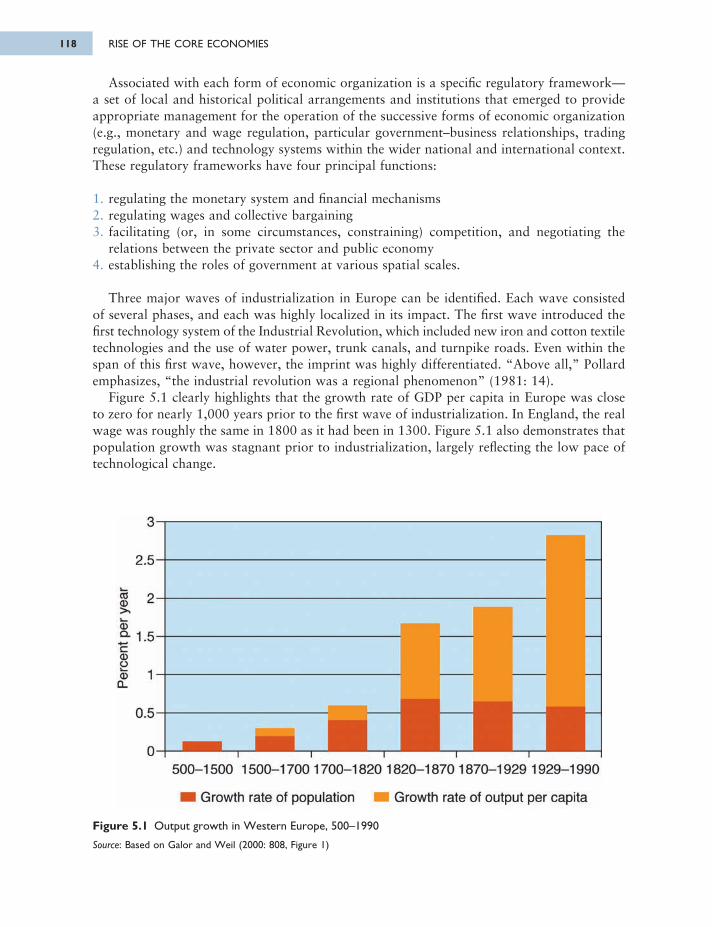

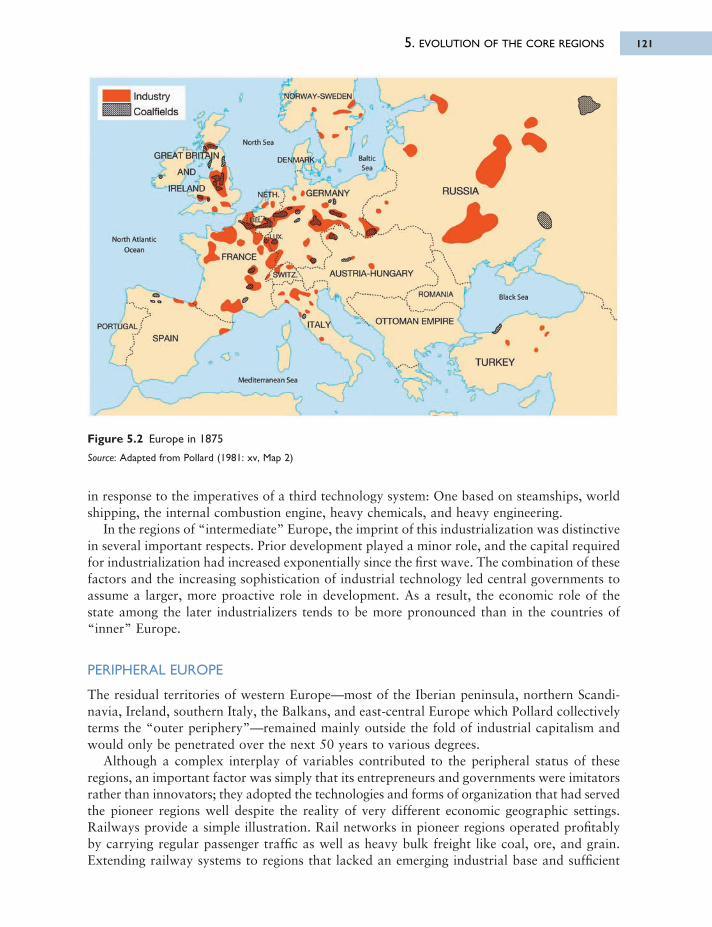

5 Evolution of the core regions 116

5.1 The Industrial Revolution and spatial change 1165.2 Machinofacture and the spread of industrialization in Europe 1175.3 Fordism and North American industrialization 1255.4 Japanese industrialization: Two economic miracles 1305.5 Emergence of “organized” capitalism 1375.6 Principles of economic geography: Summarizing lessons from the

industrial era 142Summary 144Key sources and suggested reading 144

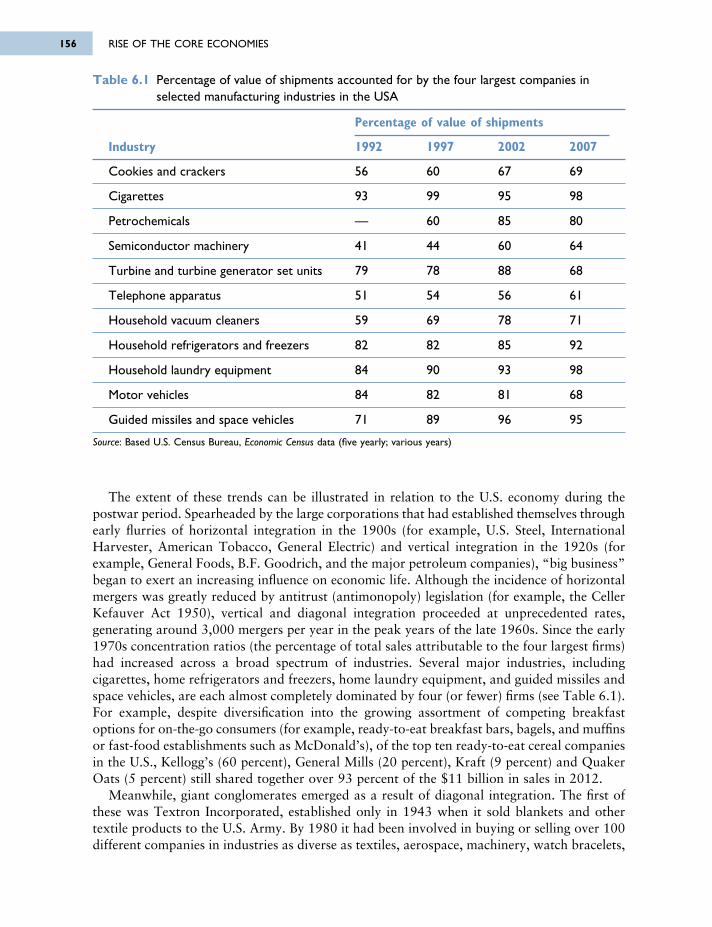

6 Globalization of economic activities 145

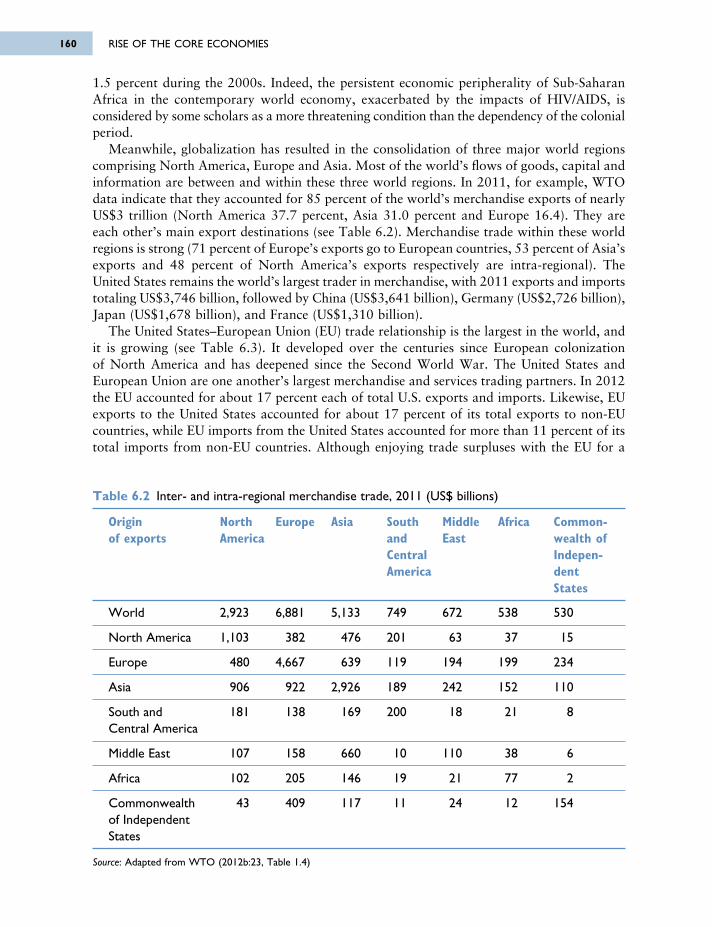

6.1 Transition to advanced capitalism 1456.2 Patterns and processes of globalization 159

Summary 174Key sources and suggested reading 174

PART 3SPATIAL TRANSFORMATION OF CORE AND PERIPHERY 177

7 Spatial reorganization of the core economies 179

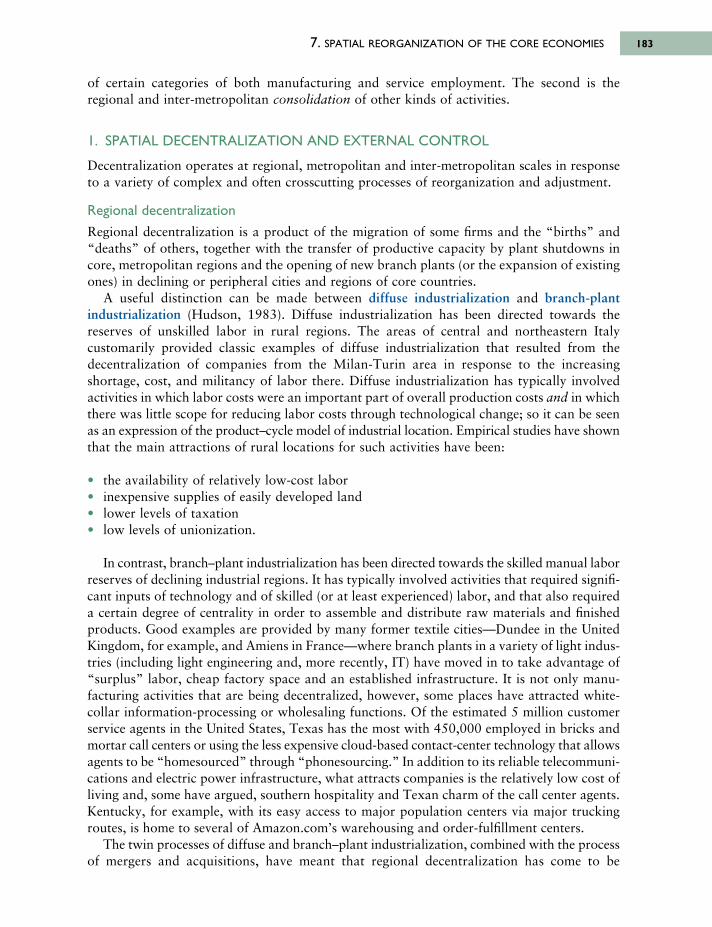

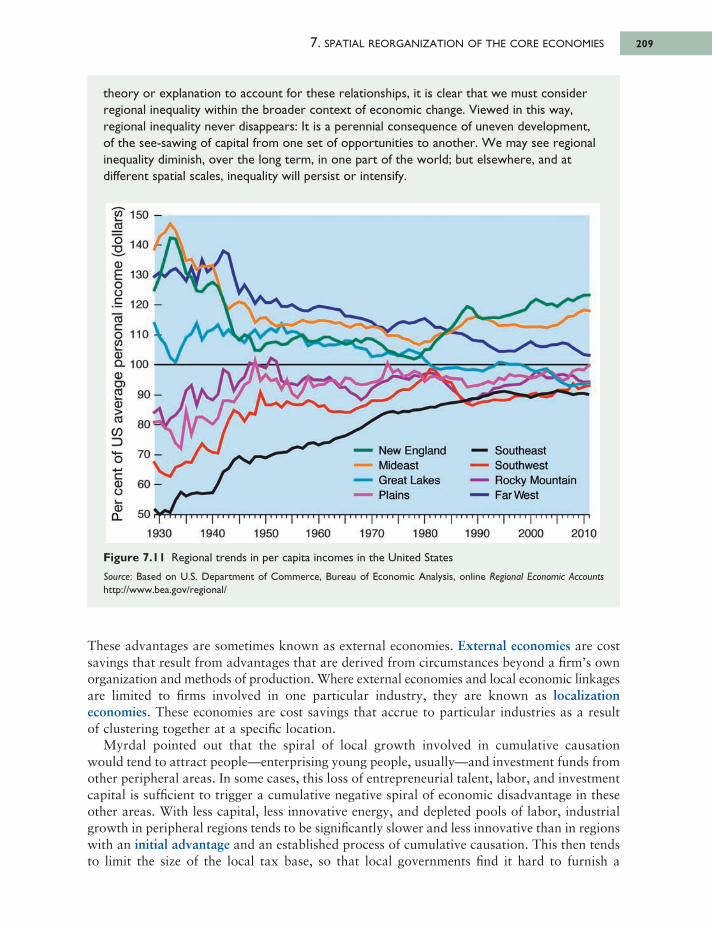

7.1 The context for urban and regional change 1807.2 Spatial reorganization of the core economies 1827.3 Old industrial spaces 1947.4 New industrial spaces 1967.5 Regional inequality in core economies 205

Summary 211Key sources and suggested reading 212

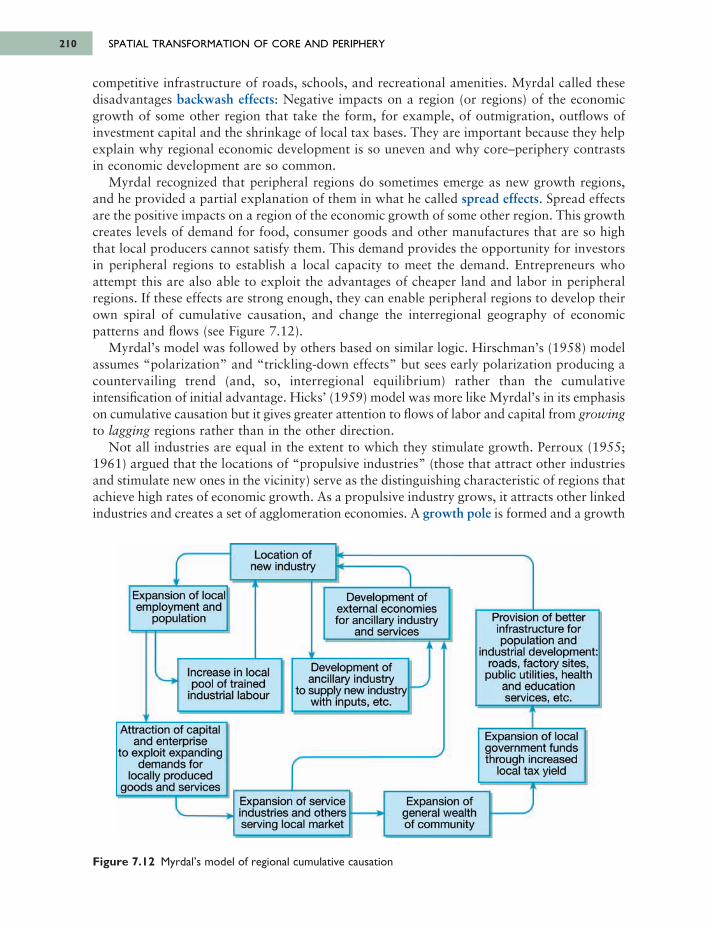

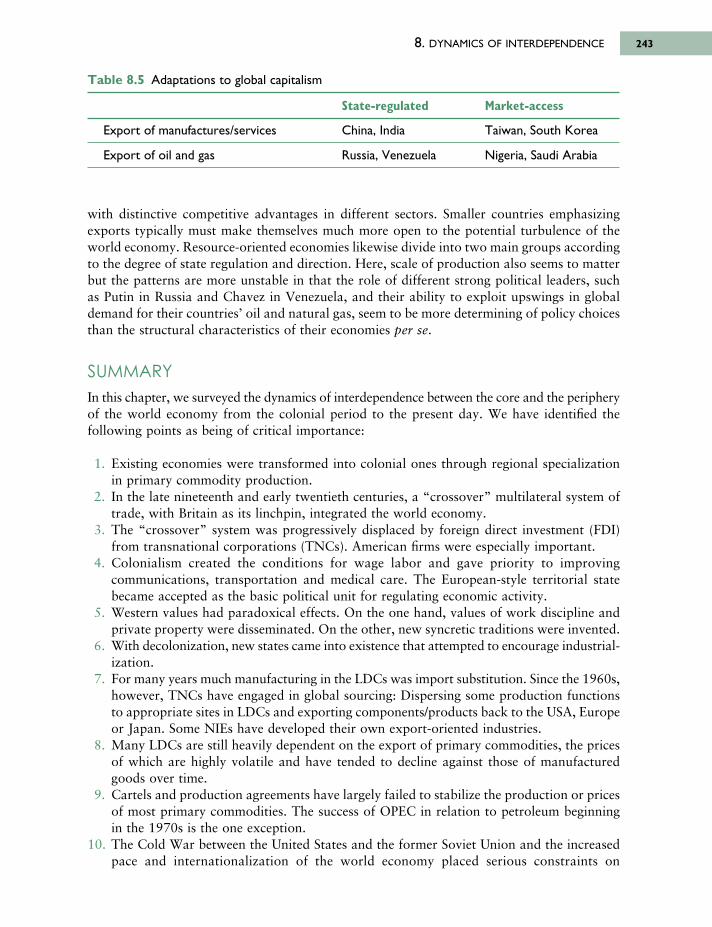

8 Dynamics of interdependence: Transformation of the periphery 213

8.1 Colonial economies and the transformation of global space 2138.2 Economic mechanisms of enmeshment and maintenance

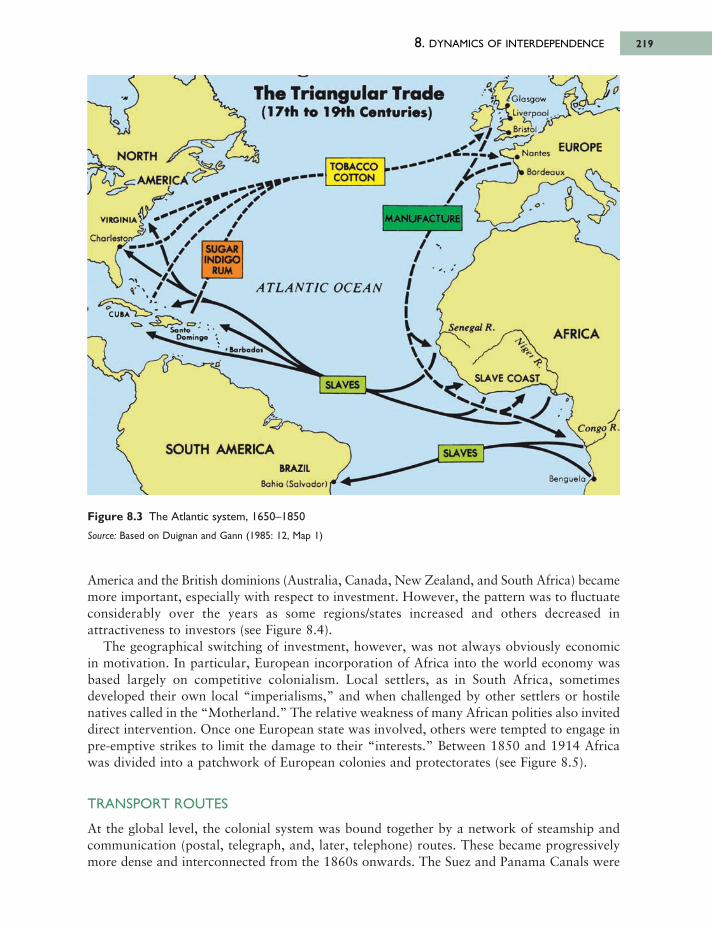

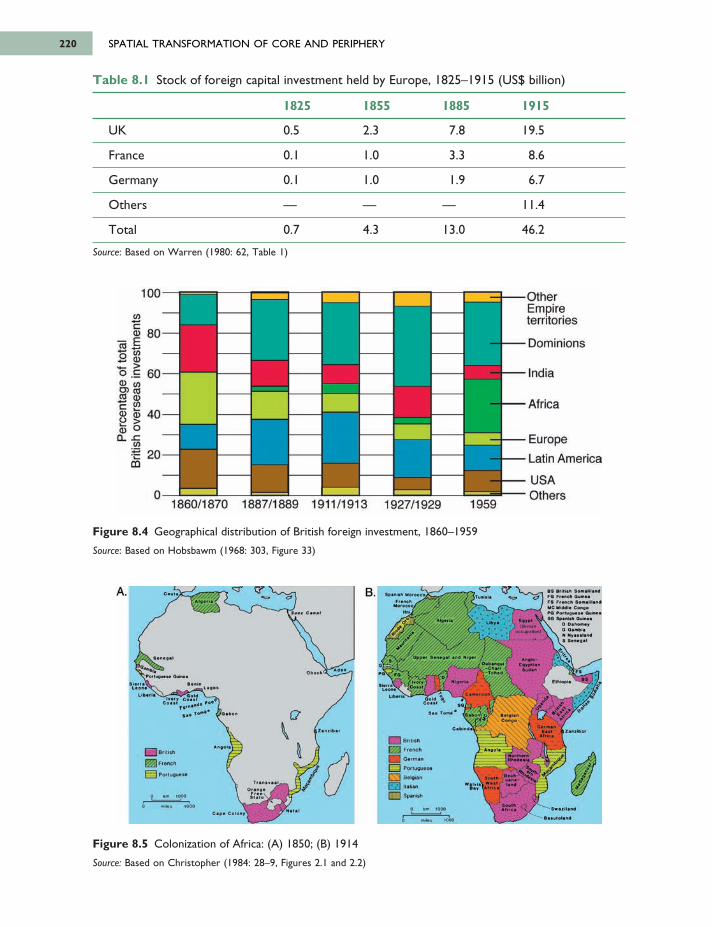

in the colonial world economy 2188.3 Influence of colonial administration on interdependence 2268.4 Mechanisms of cultural integration 2288.5 Changing global context of interdependence 2308.6 Alternative models of development? 242

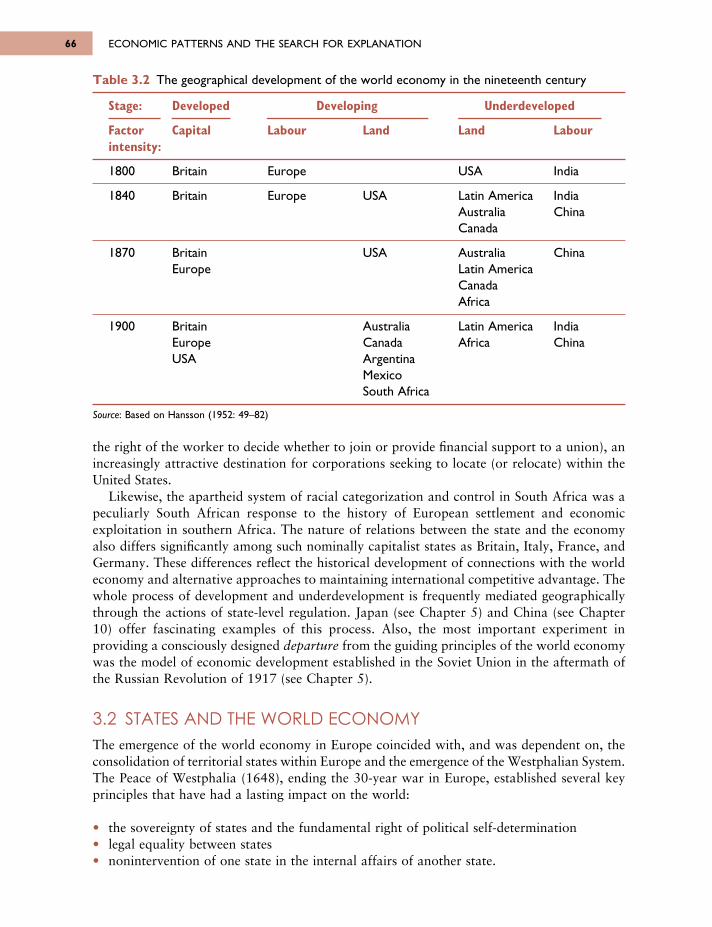

Summary 243Key sources and suggested reading 244

9 Agriculture: The primary concern? 245

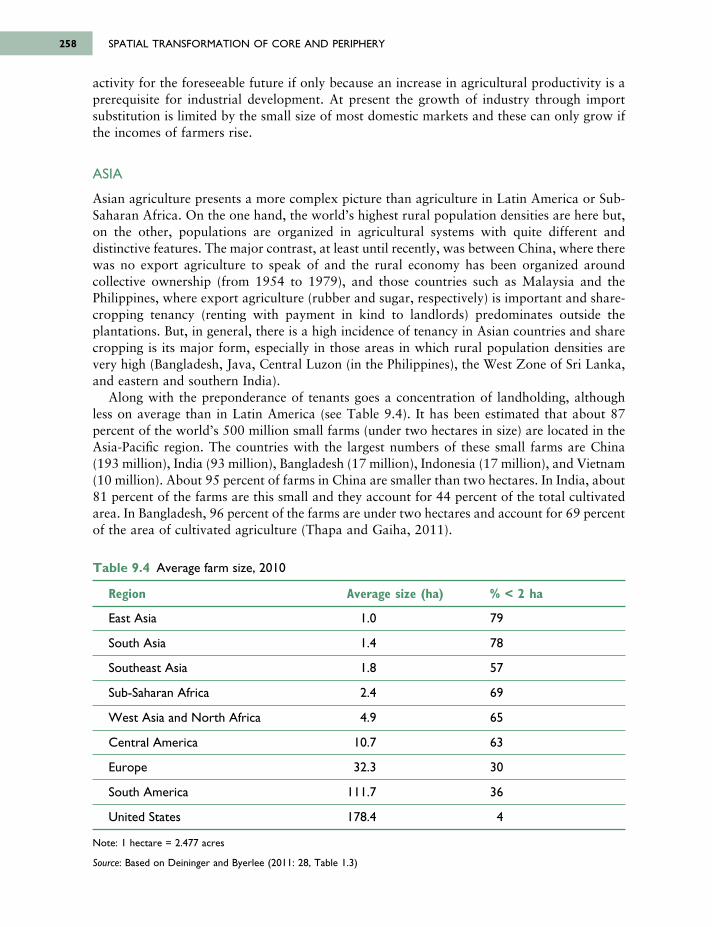

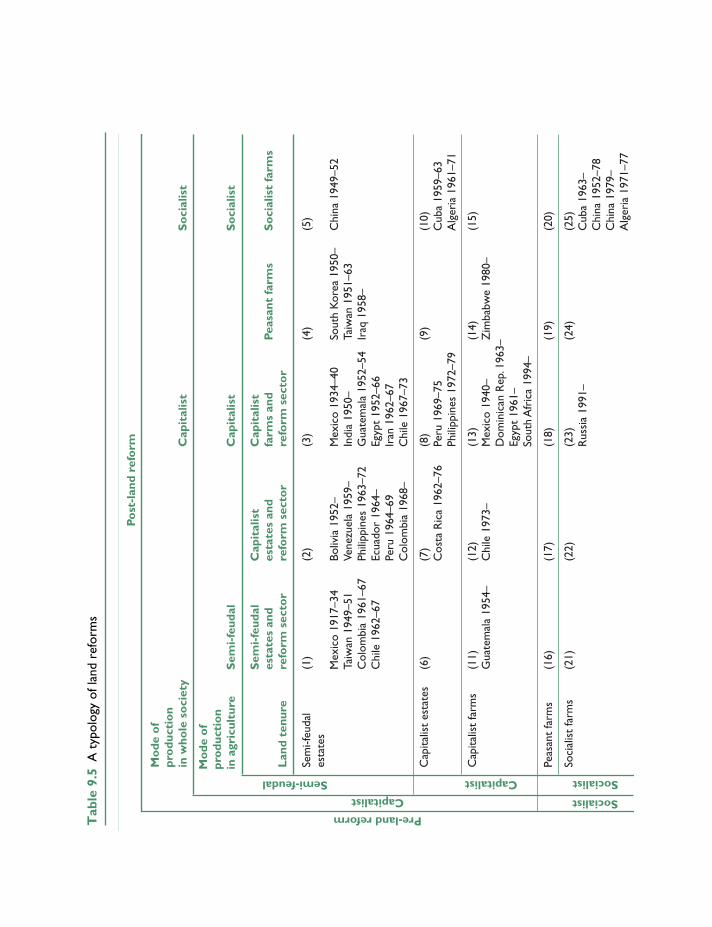

9.1 Agriculture in the periphery 2469.2 Land, labor, and capital 2519.3 Rural land reform 2609.4 Capitalization of agriculture 2629.5 Science and technology in agriculture 270

Summary 272Key sources and suggested reading 273

CONTENTSvi

6063 GEOGRAPHY WORLD ECON_PT_246x189 mm 22/01/2014 15:09 Page vi

10 Industrialization: The path to progress? 274

10.1 National and global stimuli to industrialization 27510.2 Limits to industrialization in the periphery 28010.3 Geography of industrialization in the periphery 28510.4 Rise and fall of the Soviet model of industrialization 29910.5 China’s rise in the world economy 304

Summary 310Key sources and suggested reading 312

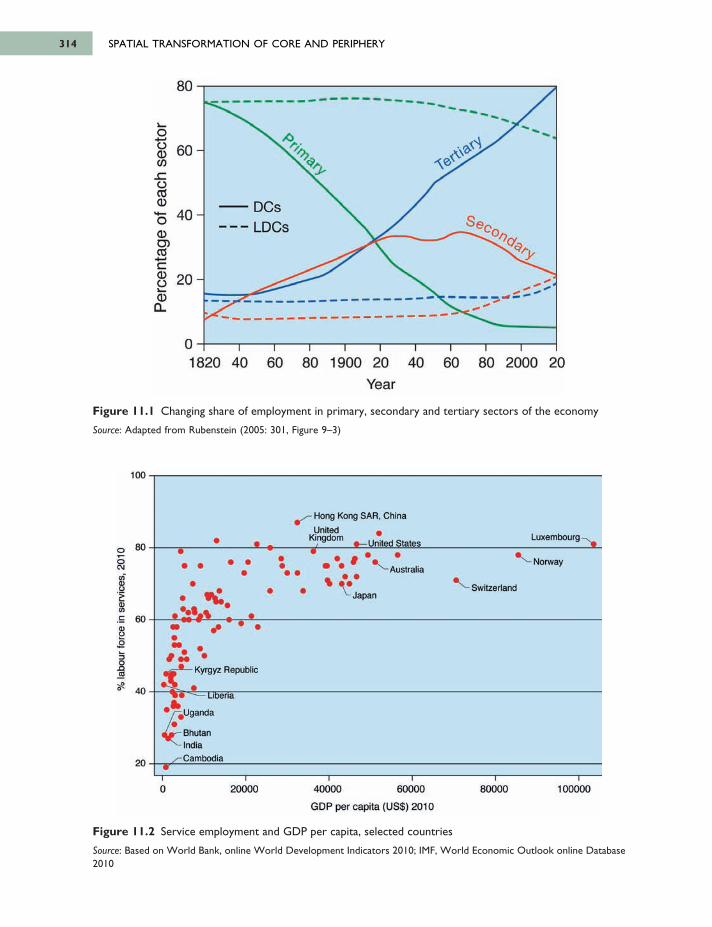

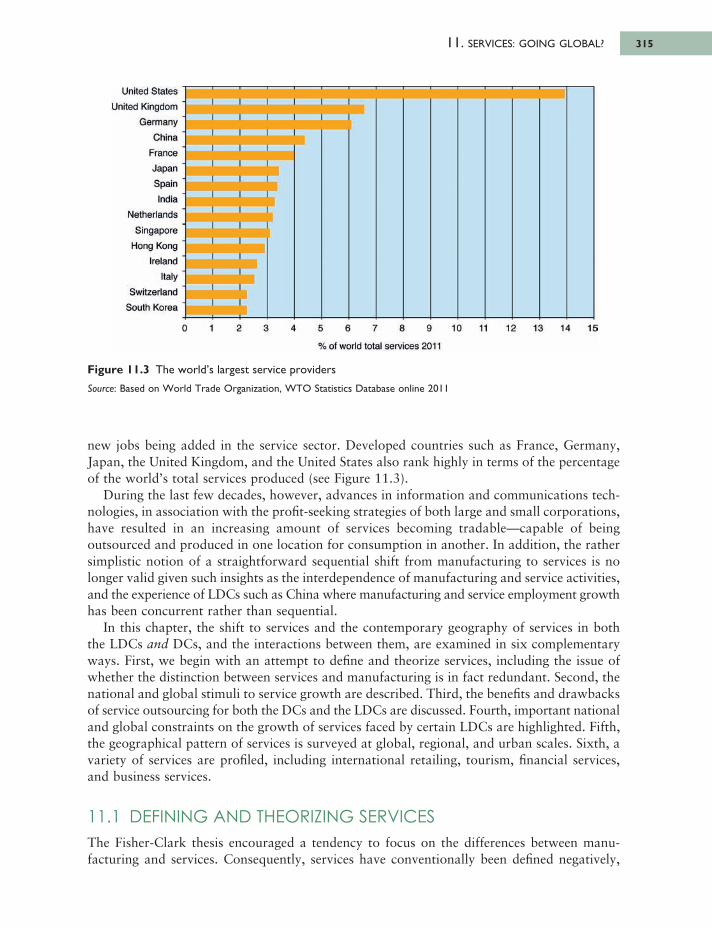

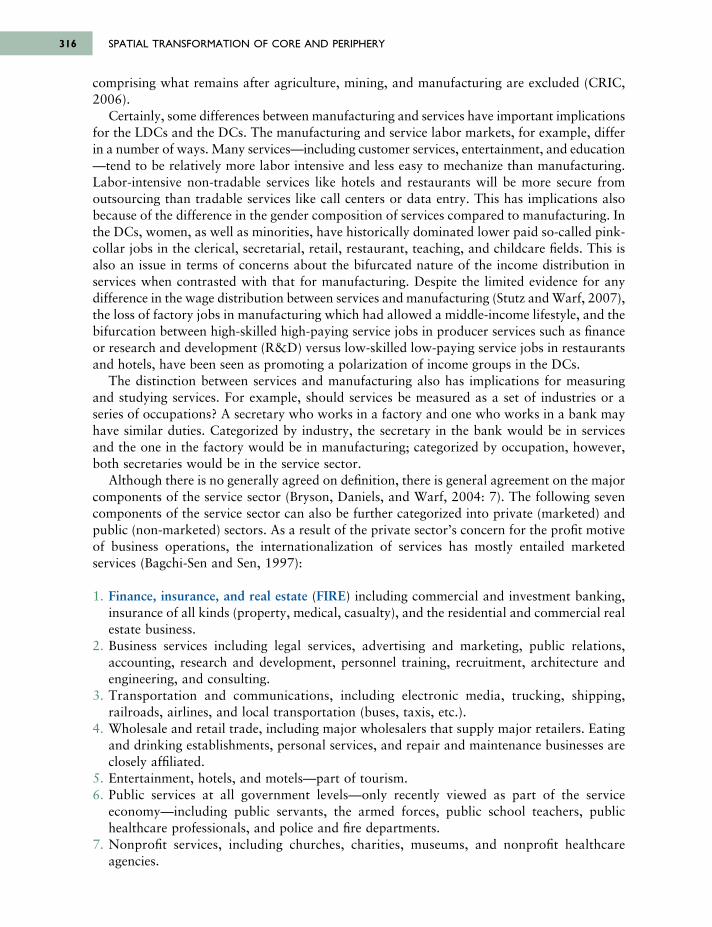

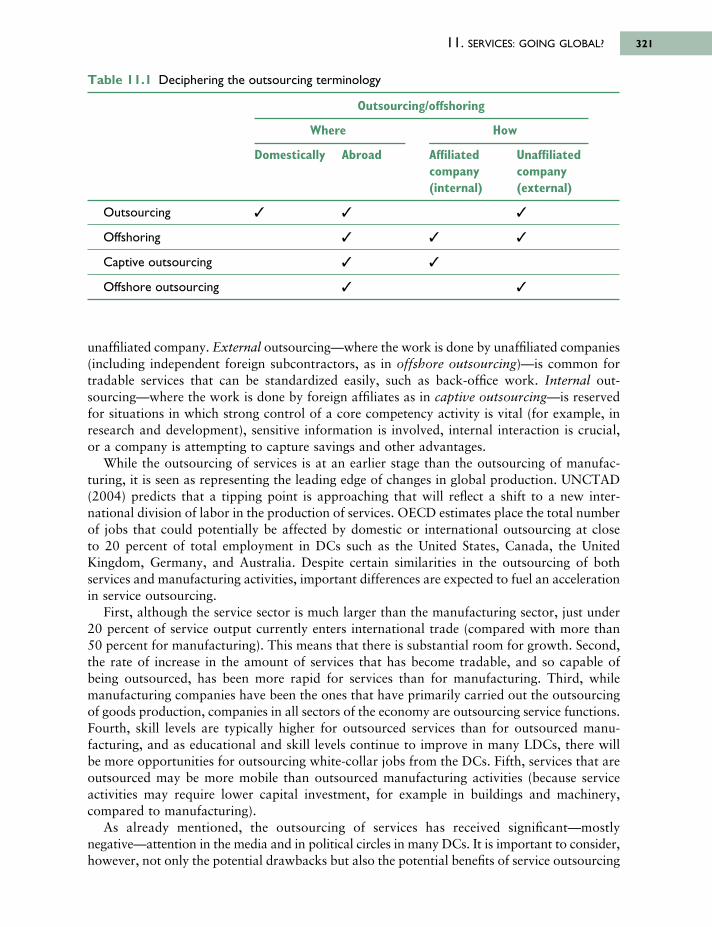

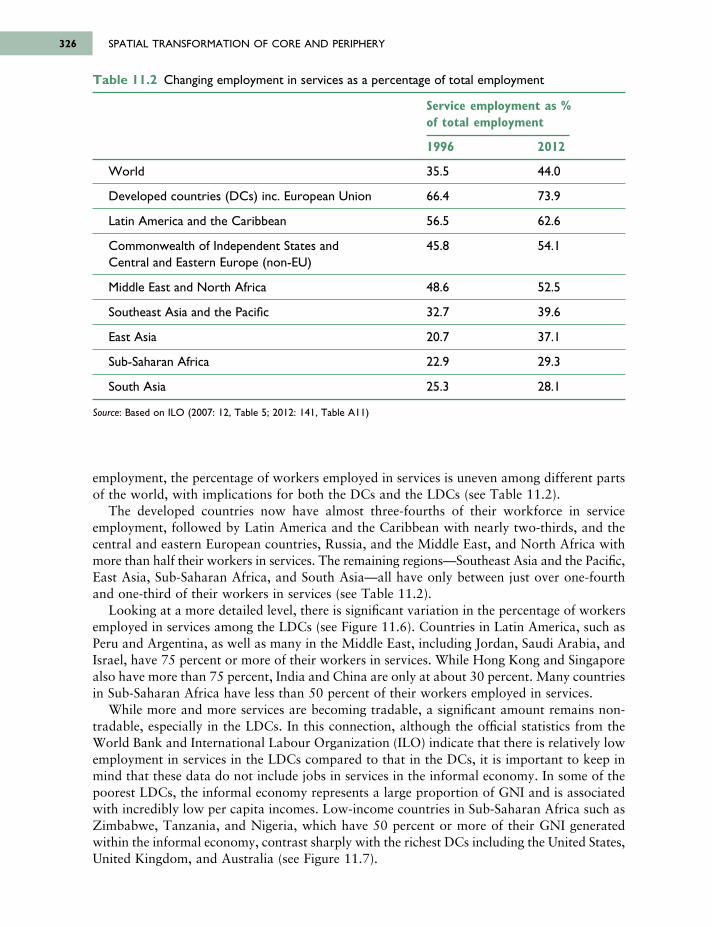

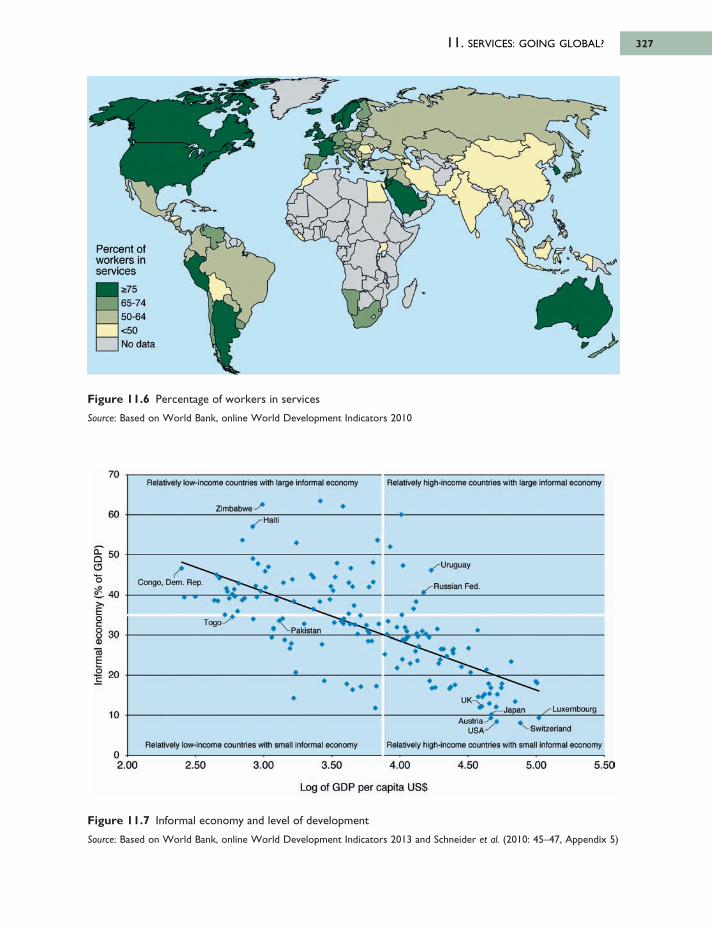

11 Services: Going global? 313

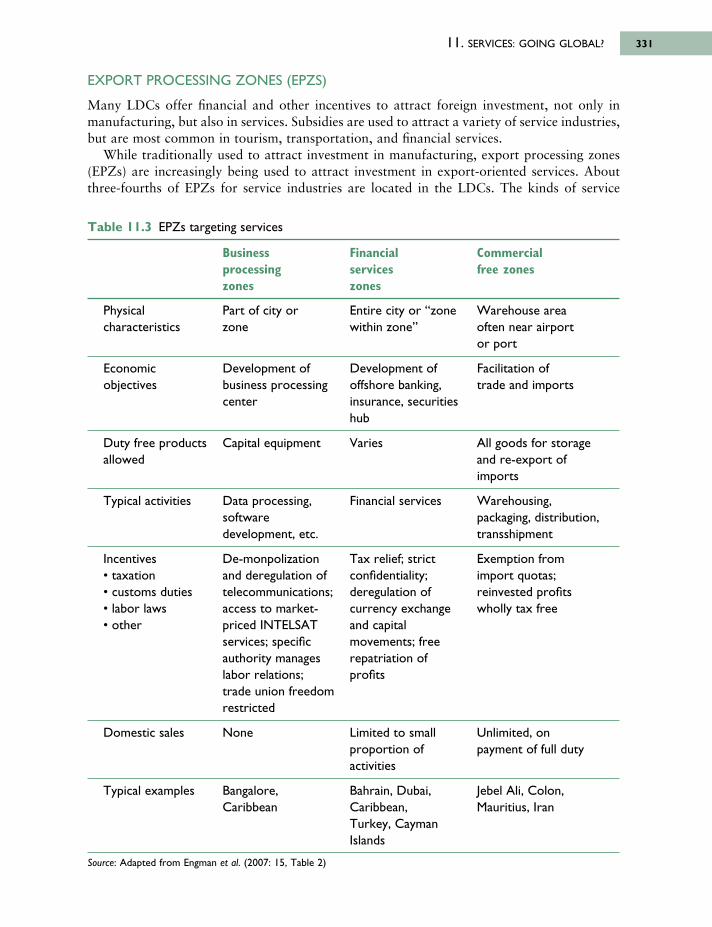

11.1 Defining and theorizing services 31511.2 National and global stimuli to the growth of services 31811.3 Services outsourcing: Benefits and drawbacks for all? 31911.4 Limits to service export growth in the semi-periphery and periphery? 32211.5 Geography of services 32511.6 Variety in the internationalization of services 332

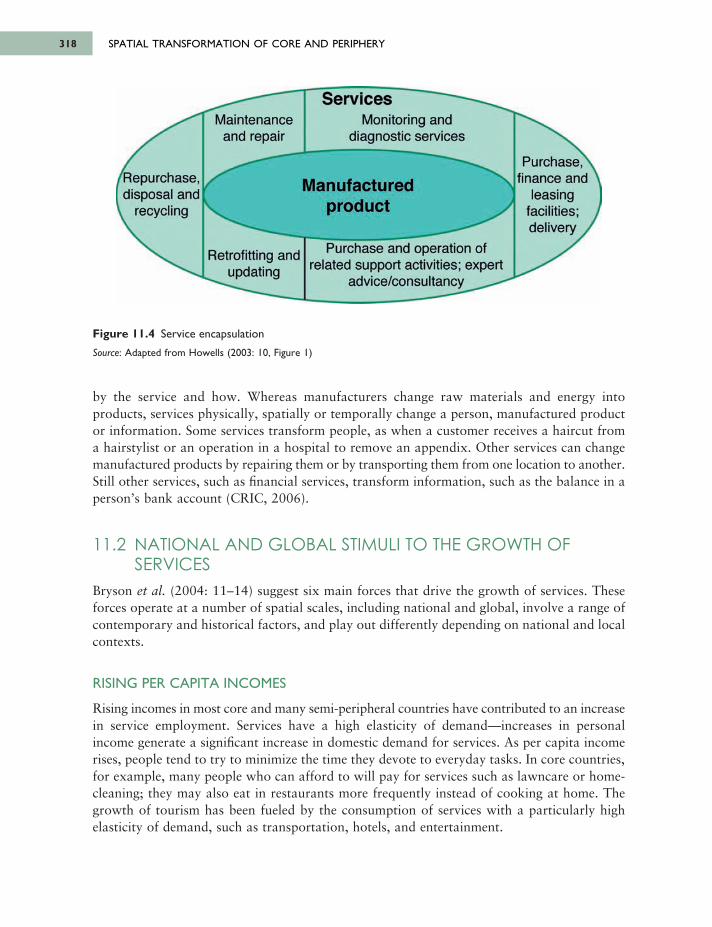

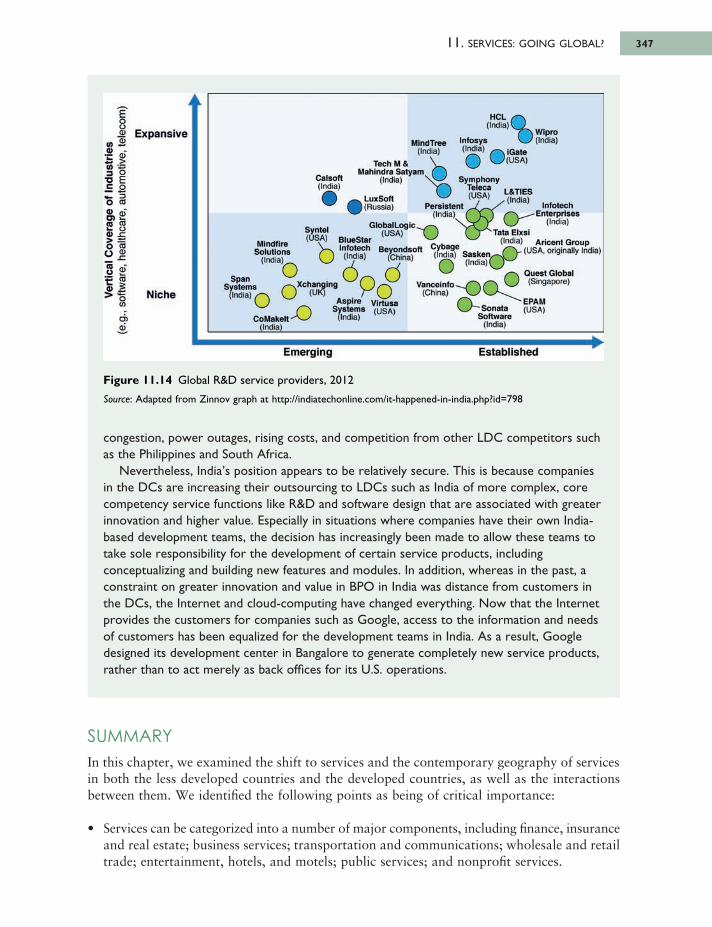

Summary 347Key sources and suggested reading 349

PART 4ADJUSTING TO THE WORLD ECONOMY 351

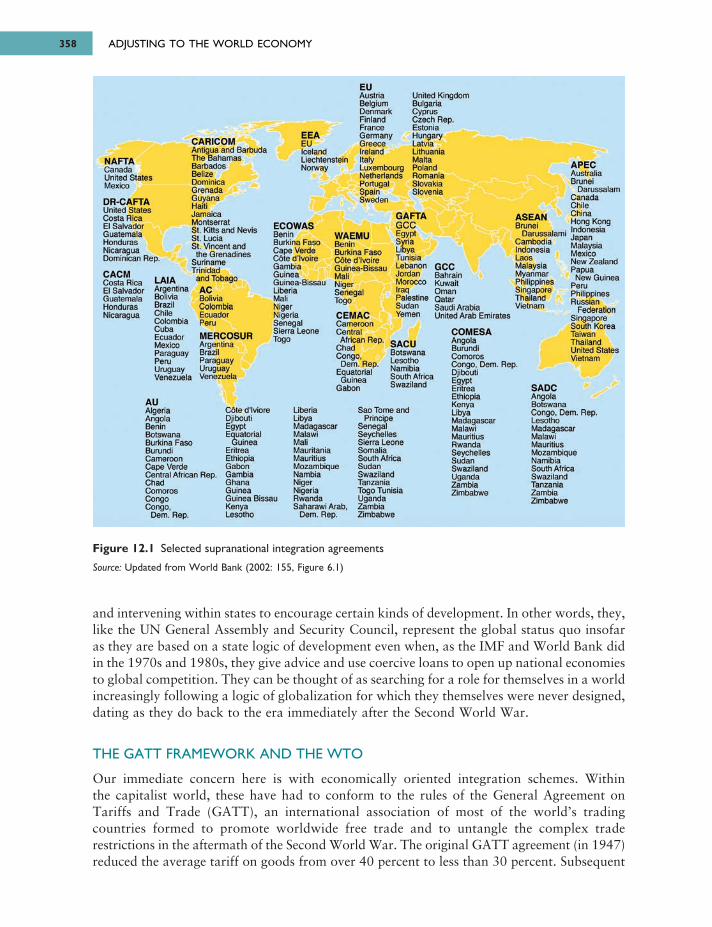

12 International and supranational institutionalized integration 353

12.1 Economic change and geopolitics 35312.2 International and supranational institutionalized integration 35612.3 Spatial outcomes of economic integration 362

Summary 377Key sources and suggested reading 378

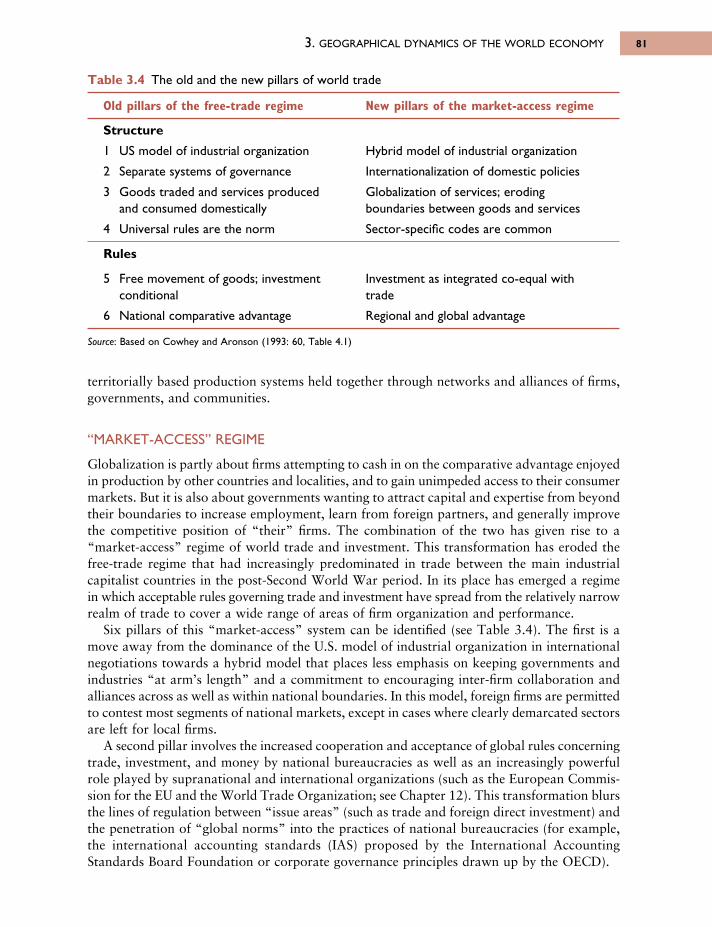

13 Reassertion of the local in the age of the global: Regions and localities within the world economy 379

13.1 Regionalism and regional policy 38013.2 Nationalist separatism 38613.3 Grassroots reactions 391

Summary 396Key sources and suggested reading 397

14 Conclusion 398

Key sources and suggested reading 401

Glossary 403

Bibliography 423

Index 453

CONTENTS vii

6063 GEOGRAPHY WORLD ECON_PT_246x189 mm 22/01/2014 15:09 Page vii

1.1 The inter-relationships surrounding economic organization and spatial change 6

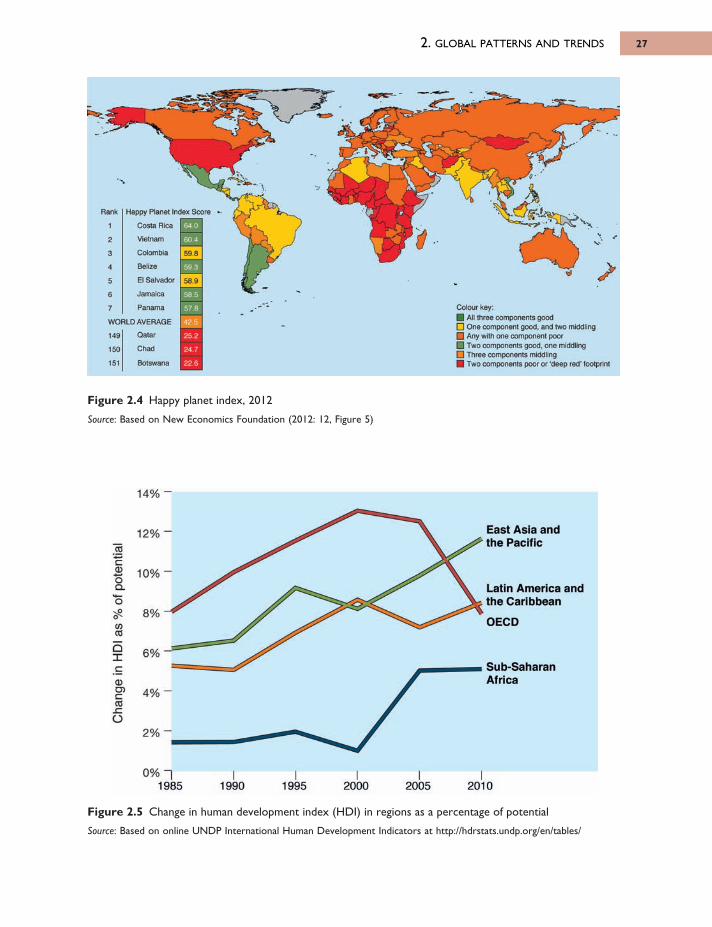

1.2 Major features of economic change in the world’s developed economies 81.3 Employment outsourcing and insourcing, United States 141.4 Basic elements of commodity chains 152.1 The world-system: core, semi-periphery and periphery 222.2 GDP per capita (PPP, constant 2005 international dollars) 222.3 Gap in growth of GDP per capita (PPP, constant 2005 international dollars) 232.4 Happy planet index, 2012 272.5 Change in human development index (HDI) in regions as a percentage

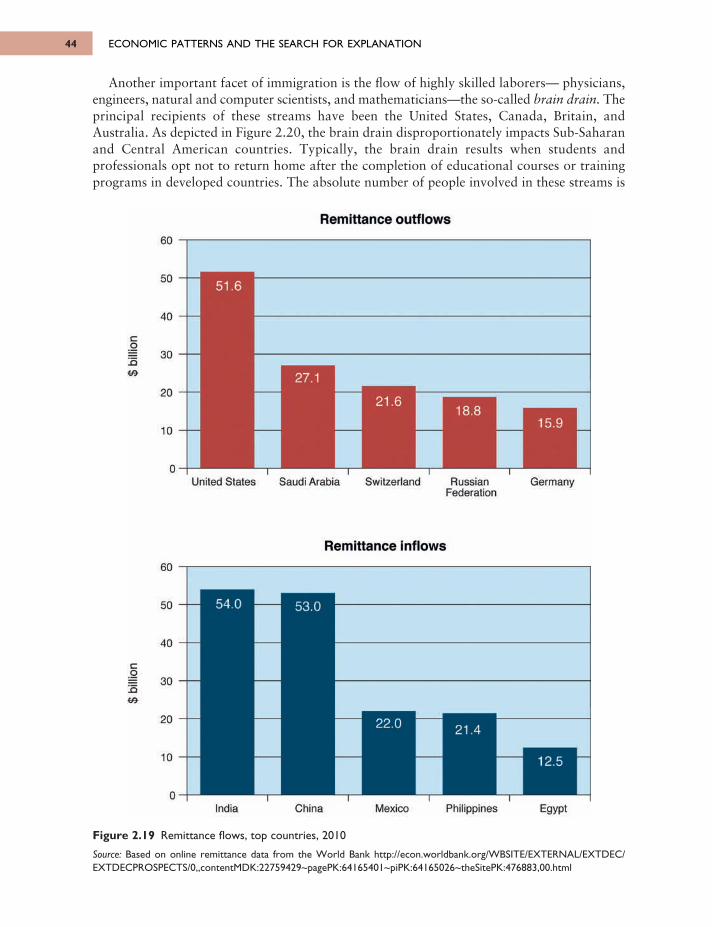

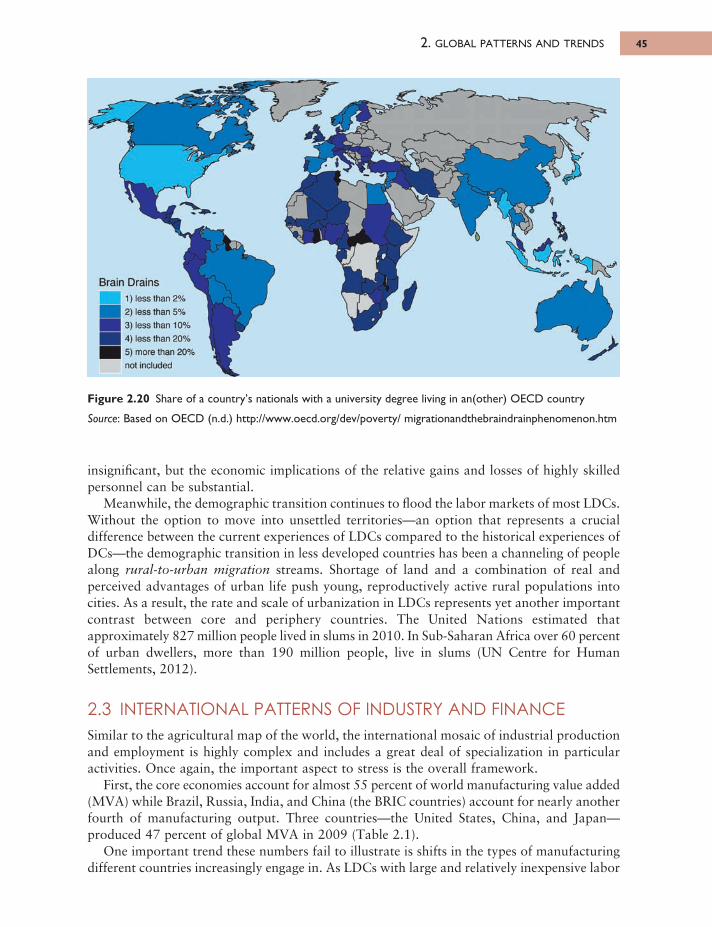

of potential 272.6 Human development index (HDI) 282.7 Human development index (HDI), 2011 282.8 North American shale plays 312.9 Estimated shale gas resources in 14 regions 312.10 Marine “dead zones” 312.11 World energy consumption by fuel, historical and projected 352.12 The world’s cultivable land 372.13 Stress on freshwater supplies, 1995 and 2025 382.14 Ecological footprint 392.15 Share of agricultural products in world merchandise exports, 1950–2009 402.16 The demographic transition 412.17 Demographic transition map of the world 422.18 Remittance flows 432.19 Remittance flows, top countries, 2010 442.20 Share of a country’s nationals with a university degree living in an(other)

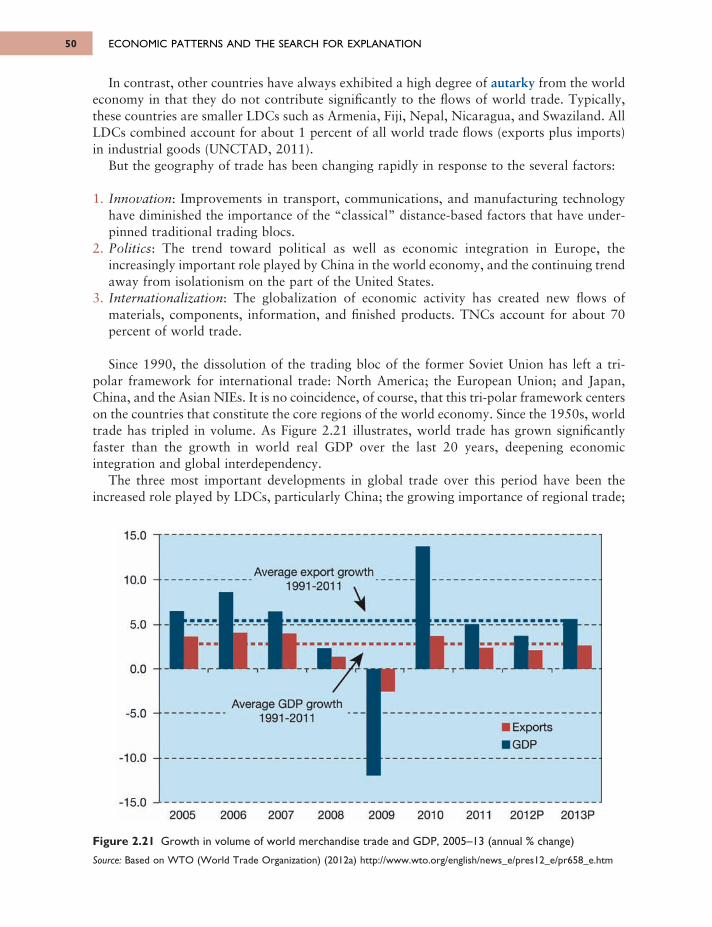

OECD country 452.21 Growth in volume of world merchandise trade and GDP, 2005–13

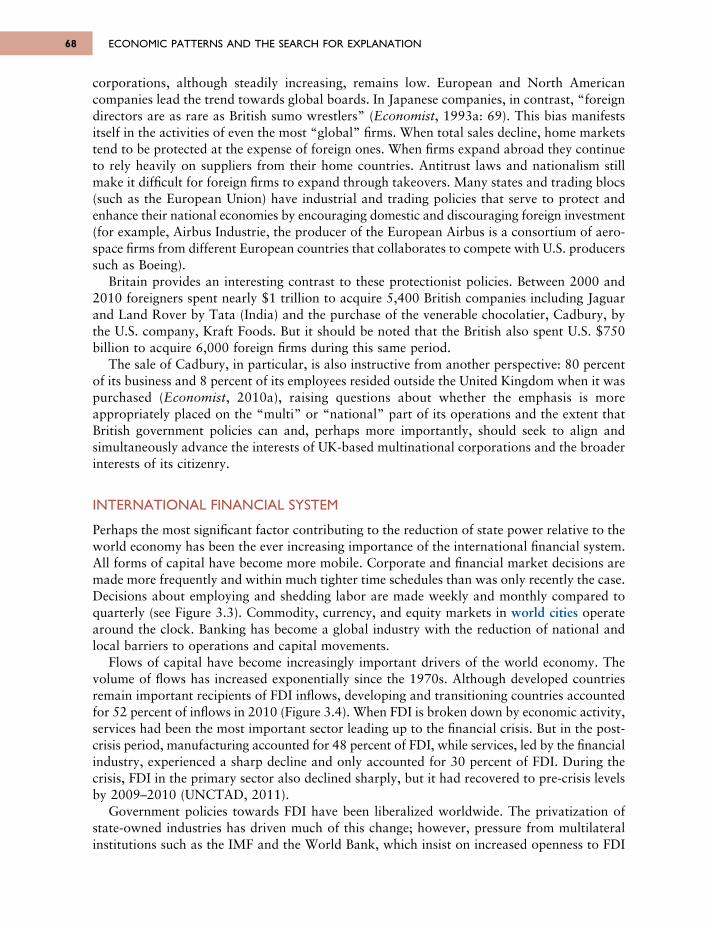

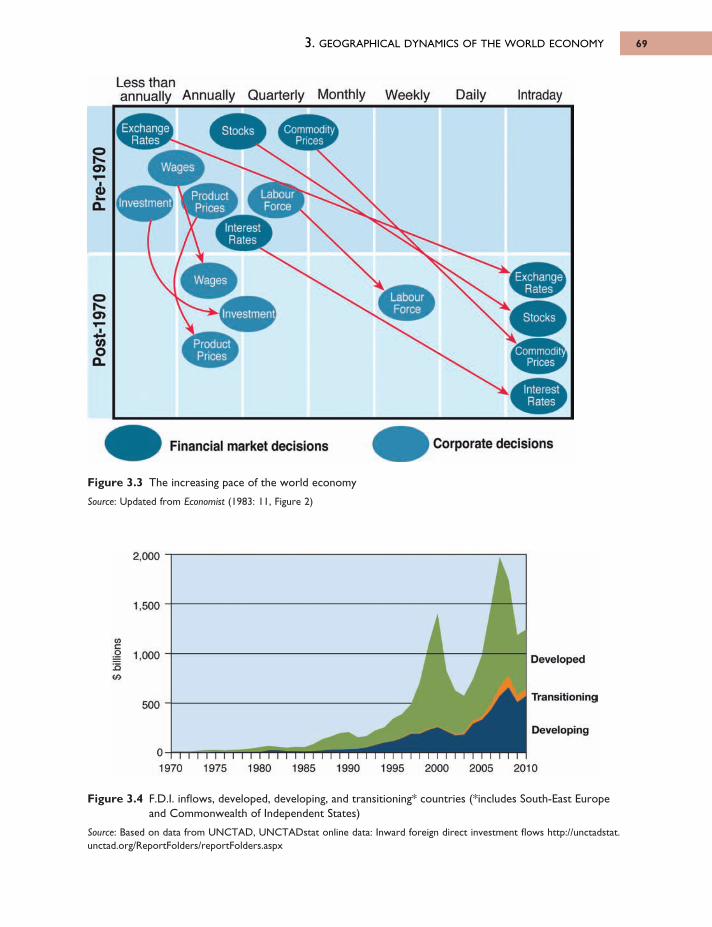

(annual % change) 502.22 Trade, imports and exports 512.23 Intra- vs. inter-regional connectedness of major exporters 522.24 Index of commodity concentration of exports, 2011 532.25 Government debt of euro-zone countries, 2011 (Maastricht limit: 60%) 552.26 Iceland and the global financial crisis 573.1 Shifting fortunes in the world economy (after Maddison) 623.2 Corruption perceptions index, 2011 633.3 The increasing pace of the world economy 693.4 F.D.I. inflows, developed, developing, and transitioning* countries

(*includes South-East Europe and Commonwealth of Independent States) 693.5 United States military expenditure 76

Figures

6063 GEOGRAPHY WORLD ECON_PT_246x189 mm 22/01/2014 15:09 Page viii

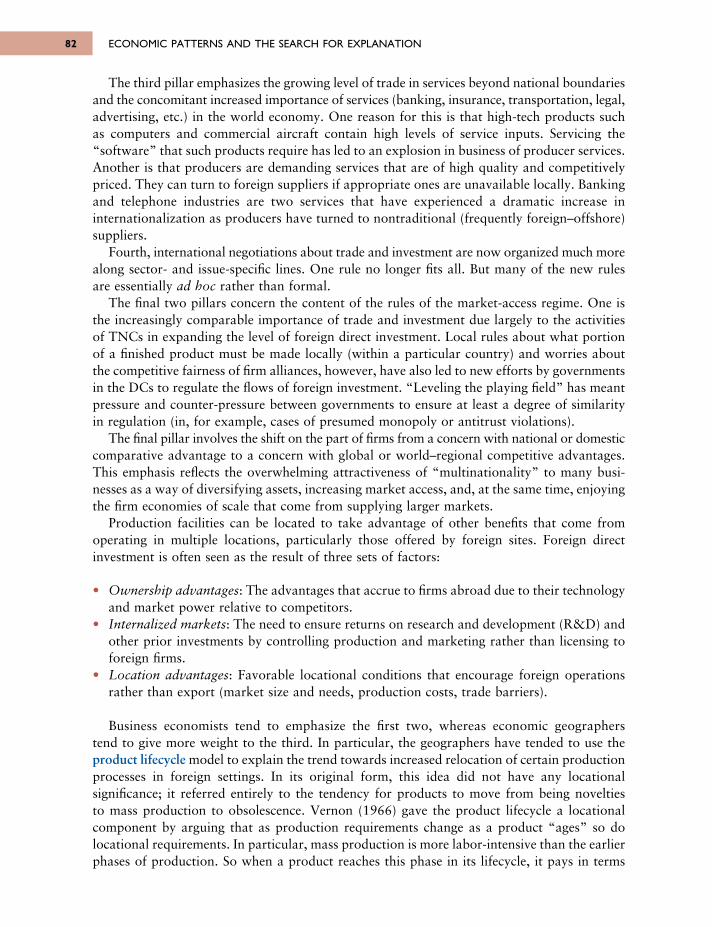

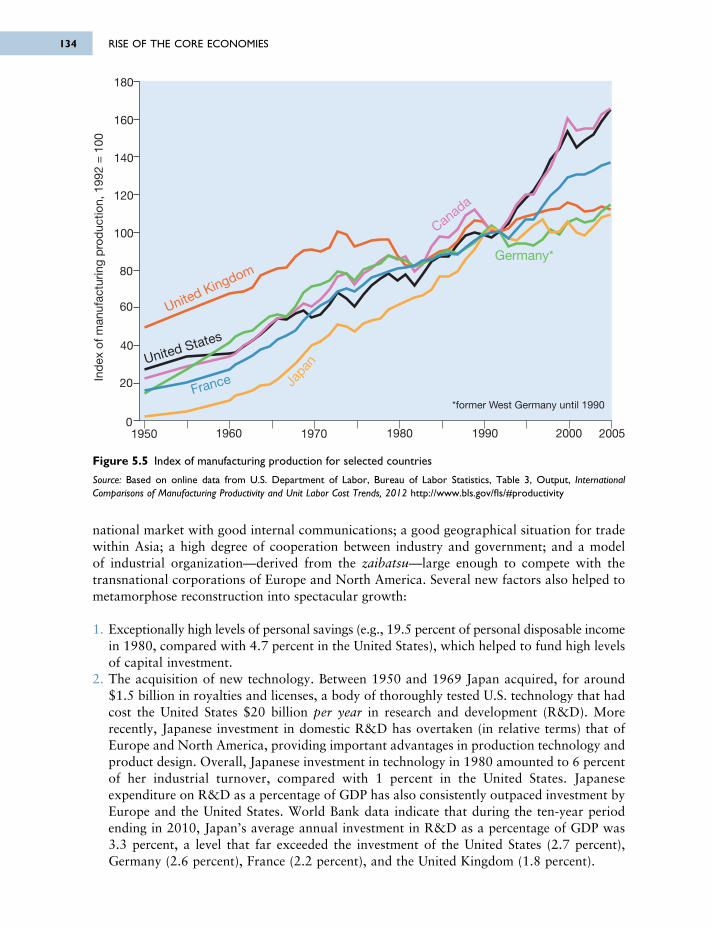

3.6 The product life cycle model and possible effects on U.S. production and trade (after Vernon, 1966) 83

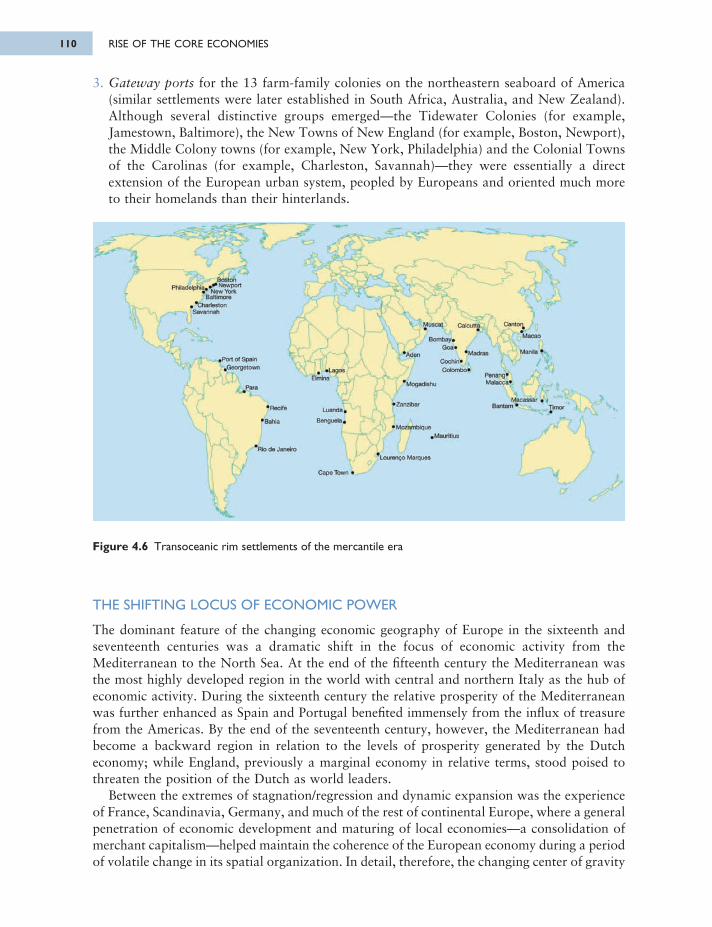

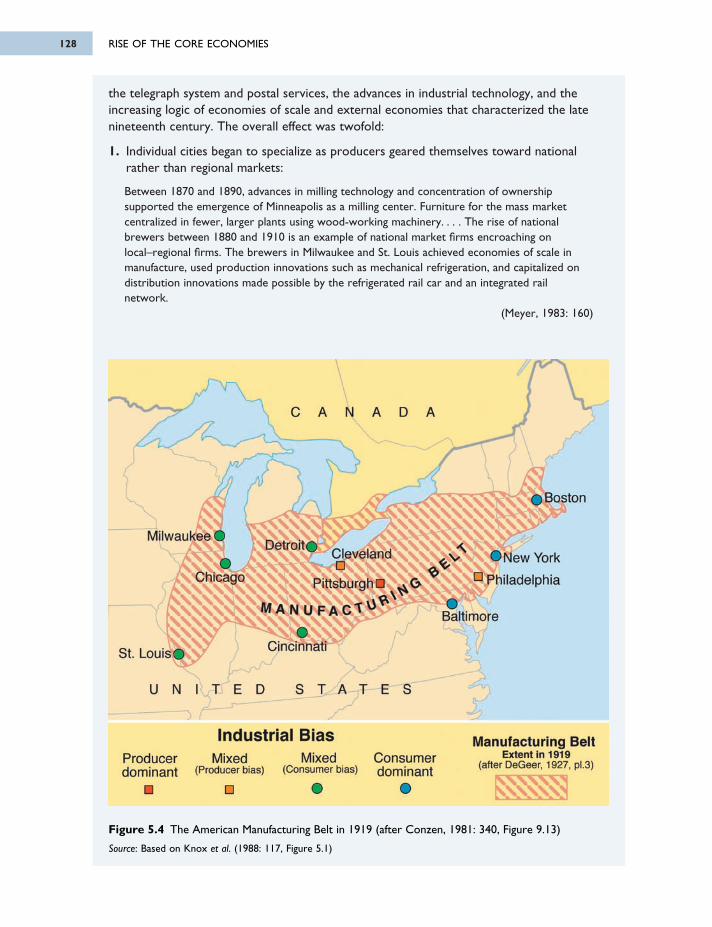

3.7 Cheaper transport and communications costs on the global highway 884.1 The urbanization of the classical world 994.2 Plan of a medieval manor 1034.3 The rise of merchant capitalism and the changing space-economy 1054.4 Towns and cities of the Hanseatic League 1054.5 The emergence of a European-based world-system 1084.6 Transoceanic rim settlements of the mercantile era 1104.7 Colonialism and urban settlement patterns 1145.1 Output growth in Western Europe, 500–1990 1185.2 Europe in 1875 1215.3 Core and periphery in Europe 1245.4 The American Manufacturing Belt in 1919 (after Conzen, 1981: 340,

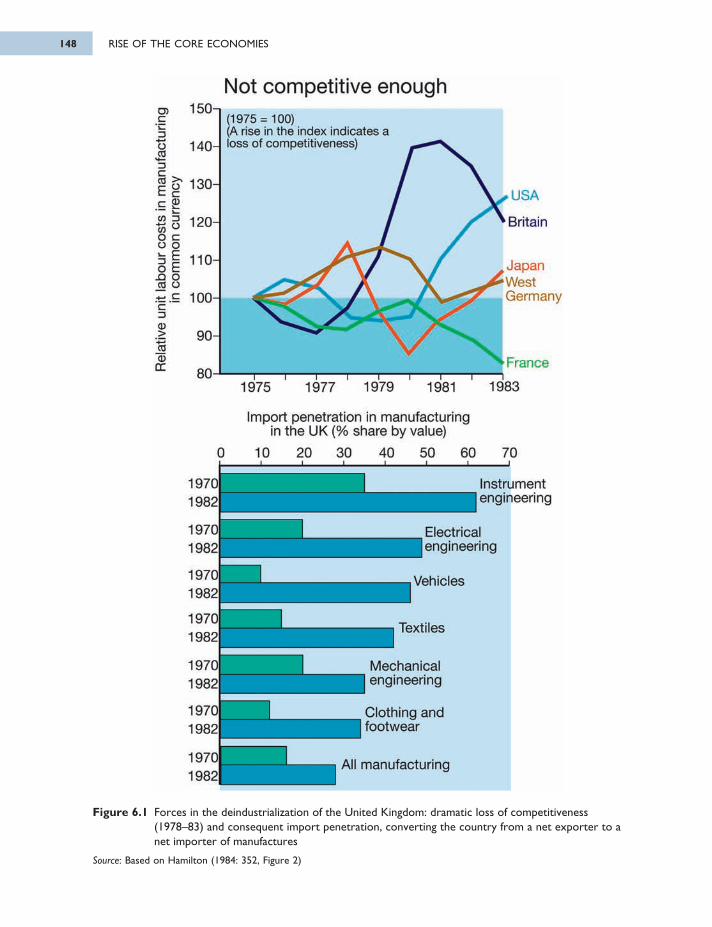

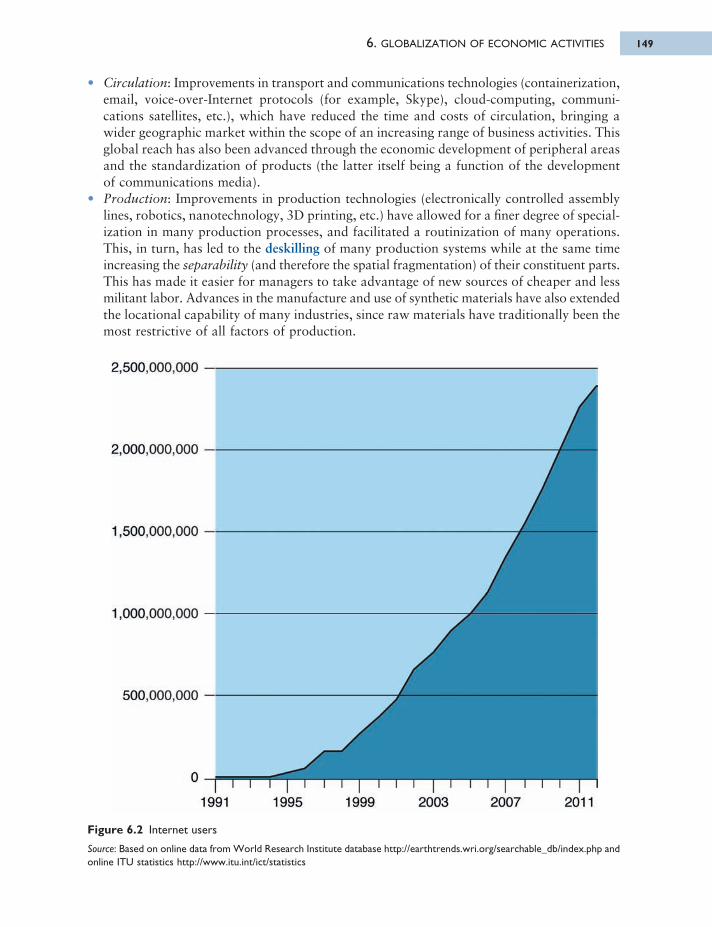

Figure 9.13) 1285.5 Index of manufacturing production for selected countries 1346.1 Forces in the deindustrialization of the United Kingdom: dramatic loss of

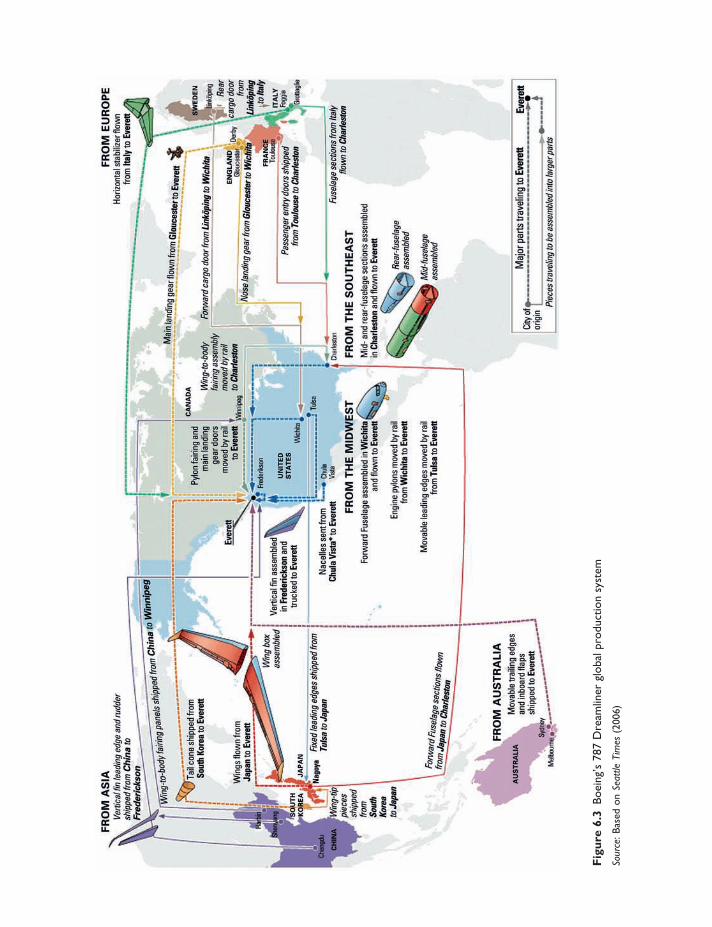

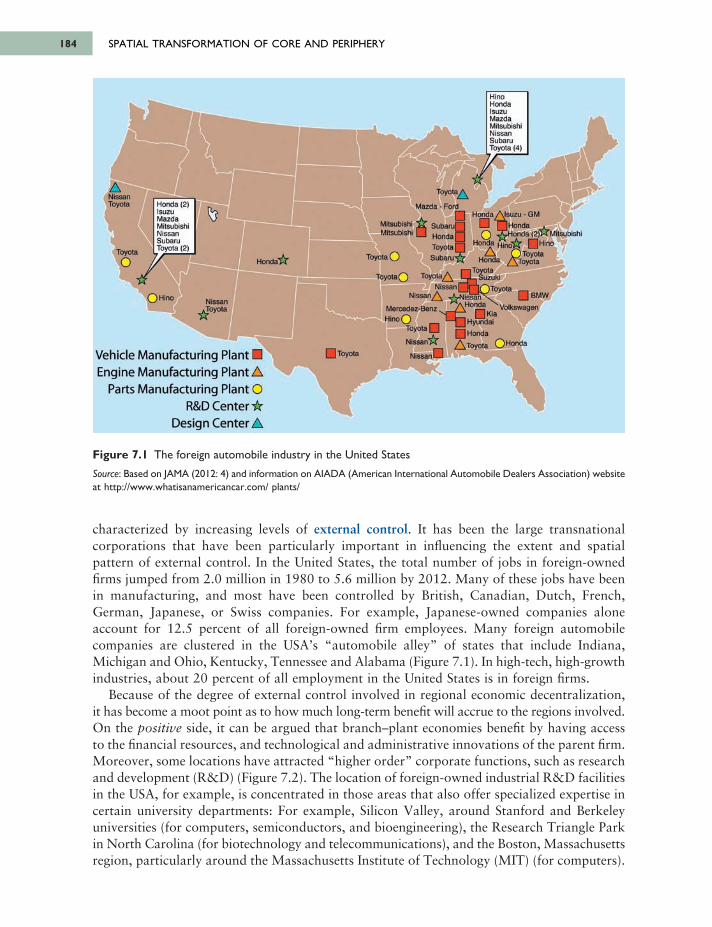

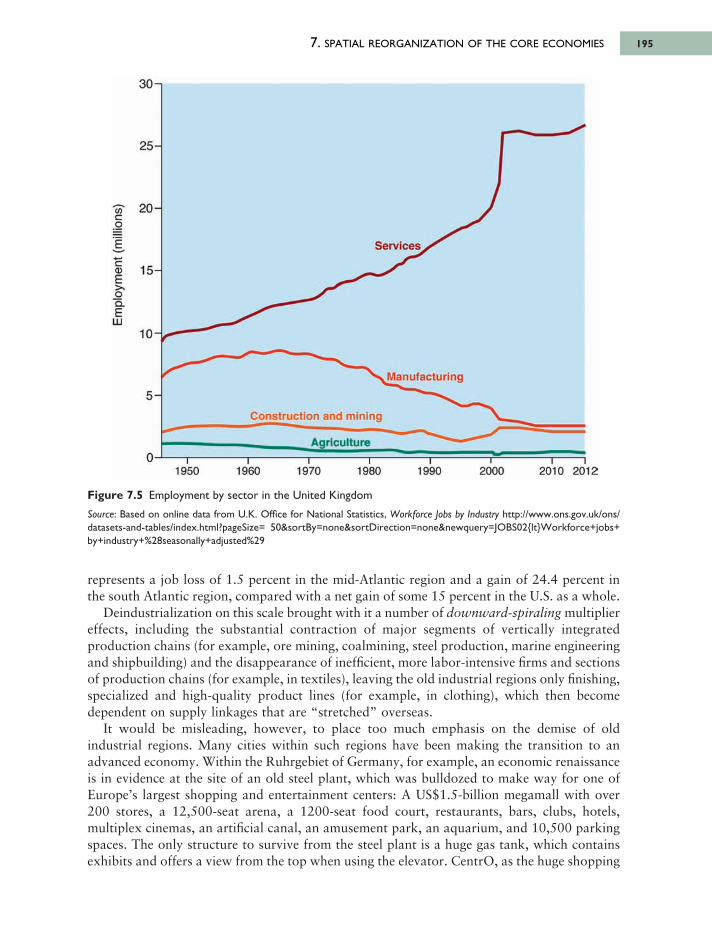

competitiveness (1978–83) and consequent import penetration 1486.2 Internet users 1496.3 Boeing’s 787 Dreamliner global production system 1656.4 The changing global geography of clothing manufacturing 1687.1 The foreign automobile industry in the United States 1847.2 Research and development (R&D) in the USA by U.S. affiliates of

foreign companies and R&D performed abroad by foreign affiliates of U.S. TNCs 185

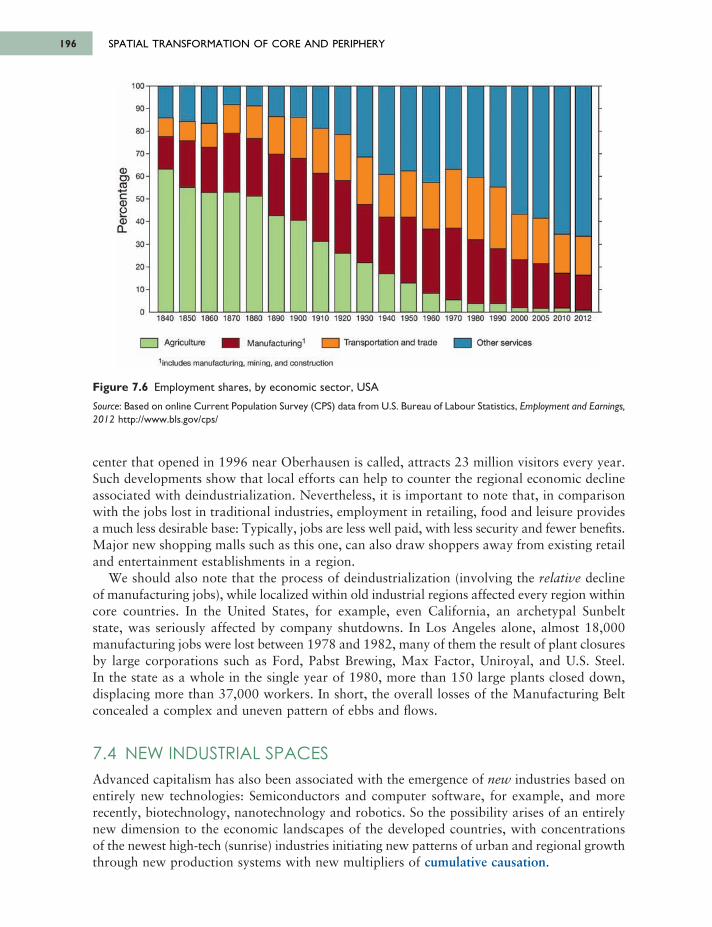

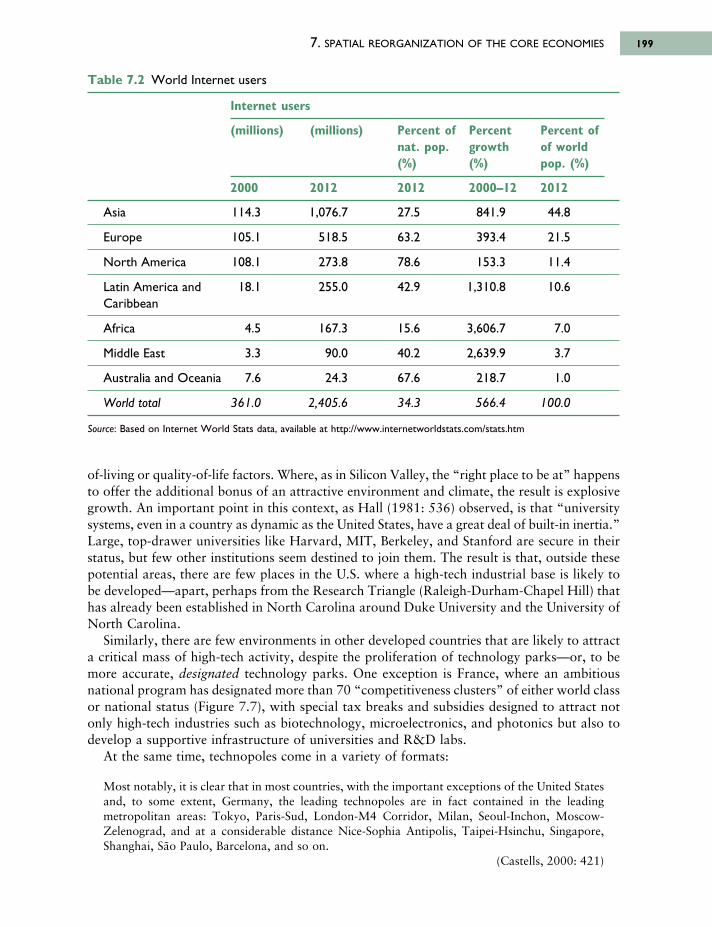

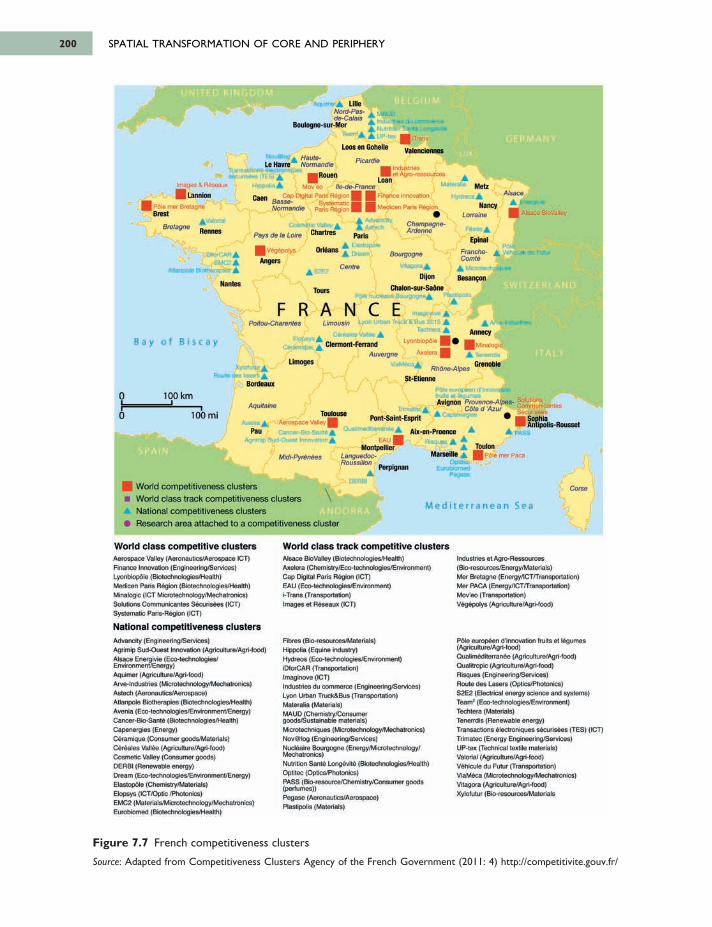

7.3 Geography of an Indian offshore services provider 1877.4 The system of world cities 1917.5 Employment by sector in the United Kingdom 1957.6 Employment shares, by economic sector, USA 1967.7 French competitiveness clusters 2007.8 Regional inequality across the European Union 2067.9 An index of deprivation in England in 2010, by district level

(average score) 2077.10 The relationship between interregional inequality and levels of economic

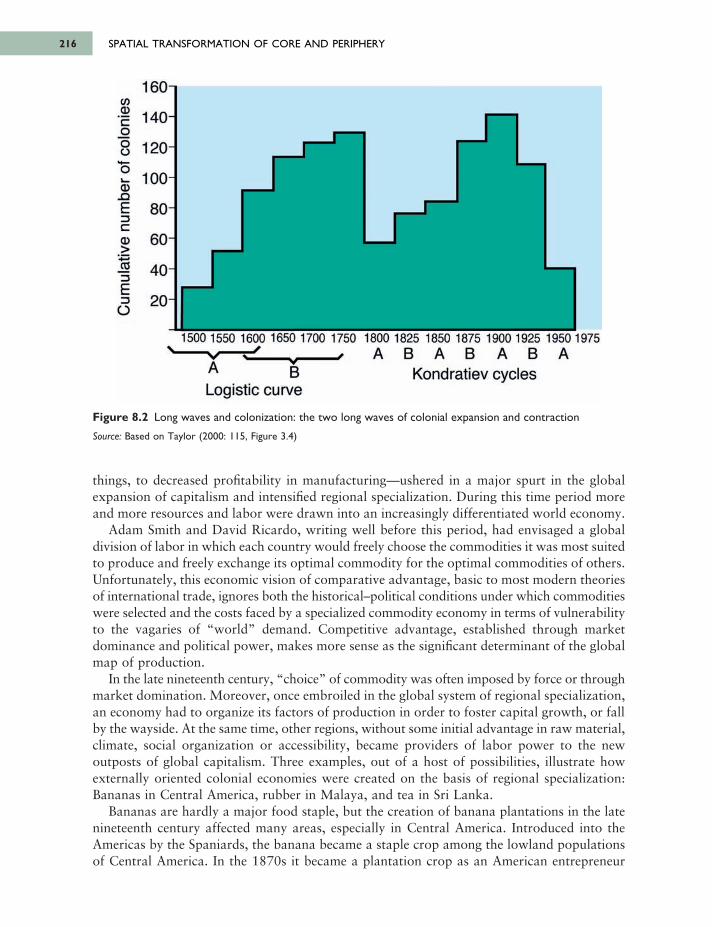

development, as posited by Williamson (1965) 2087.11 Regional trends in per capita incomes in the United States 2097.12 Myrdal’s model of regional cumulative causation 2108.1 Geographical extent of European political control, 1500–1950 2148.2 Long waves and colonization: the two long waves of colonial expansion

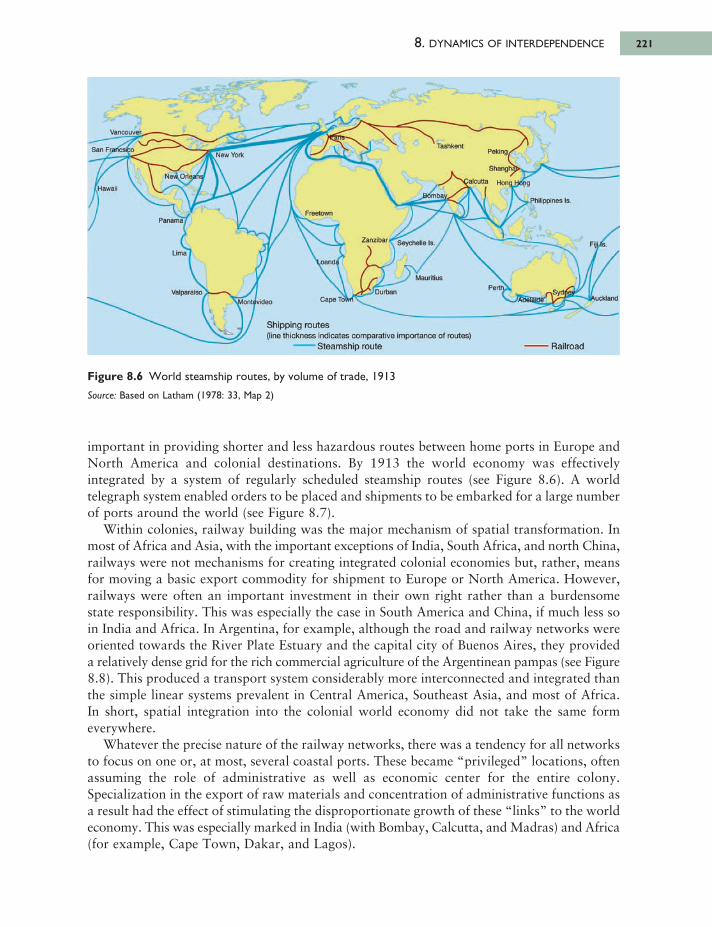

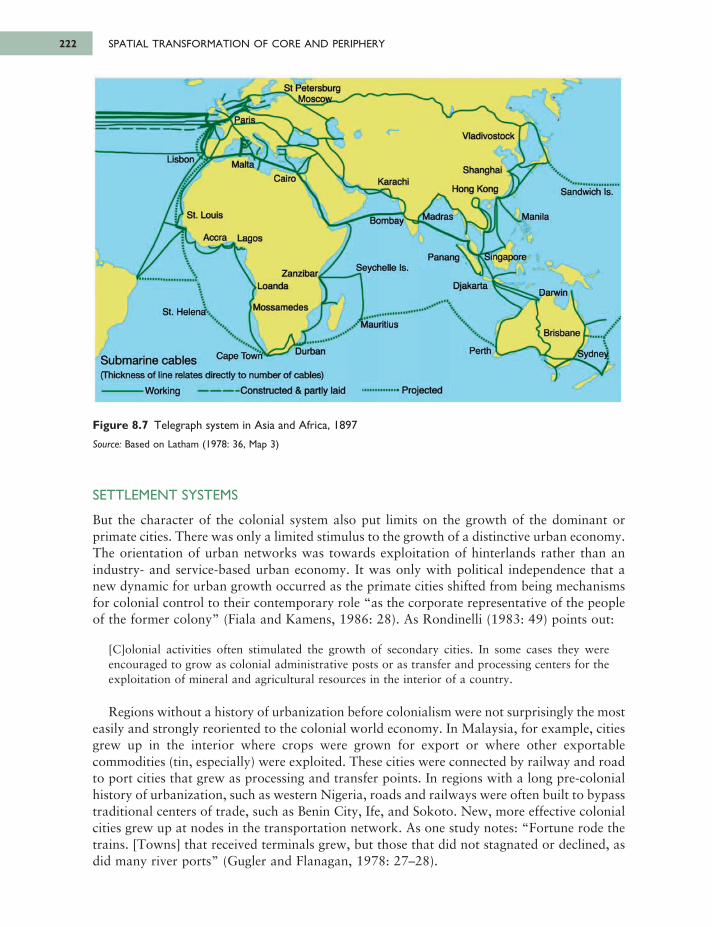

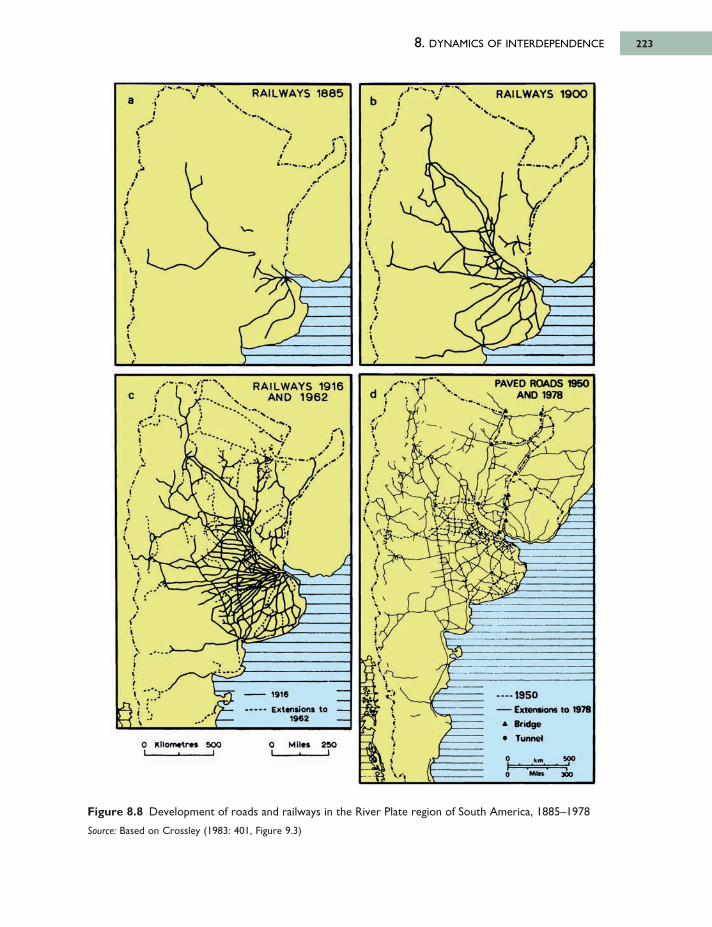

and contraction 2168.3 The Atlantic system, 1650–1850 2198.4 Geographical distribution of British foreign investment, 1860–1959 2208.5 Colonization of Africa: (A) 1850; (B) 1914 2208.6 World steamship routes, by volume of trade, 1913 2218.7 Telegraph system in Asia and Africa, 1897 2228.8 Development of roads and railways in the River Plate region of South

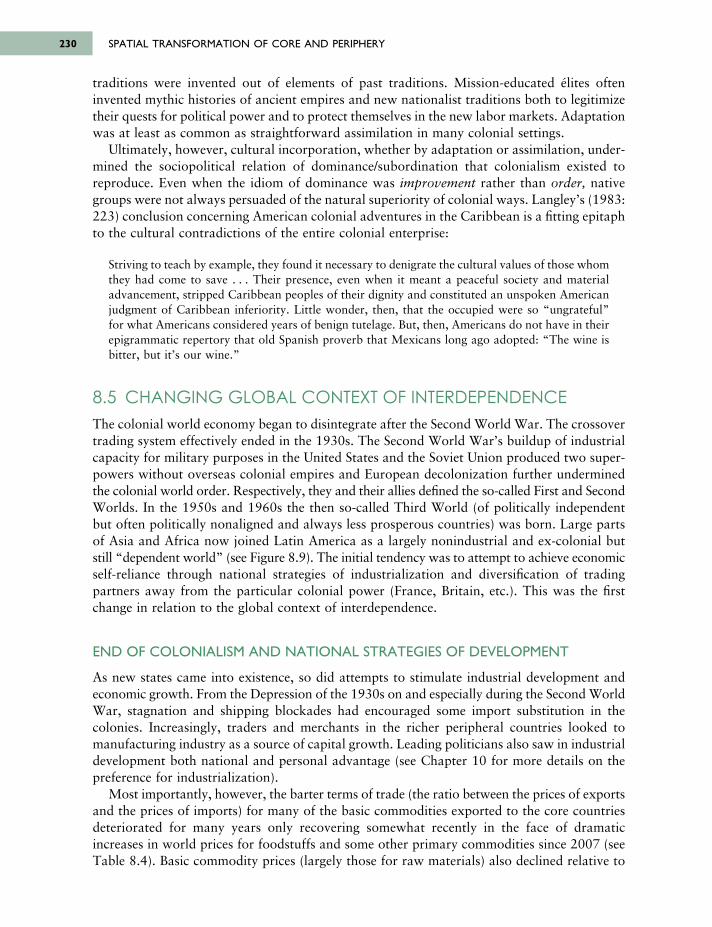

America, 1885–1978 2238.9 New states of the world since the Second World War 231

FIGURES ix

6063 GEOGRAPHY WORLD ECON_PT_246x189 mm 22/01/2014 15:09 Page ix

8.10 Exports between and from developed and less developed countries, 2001–2010 236

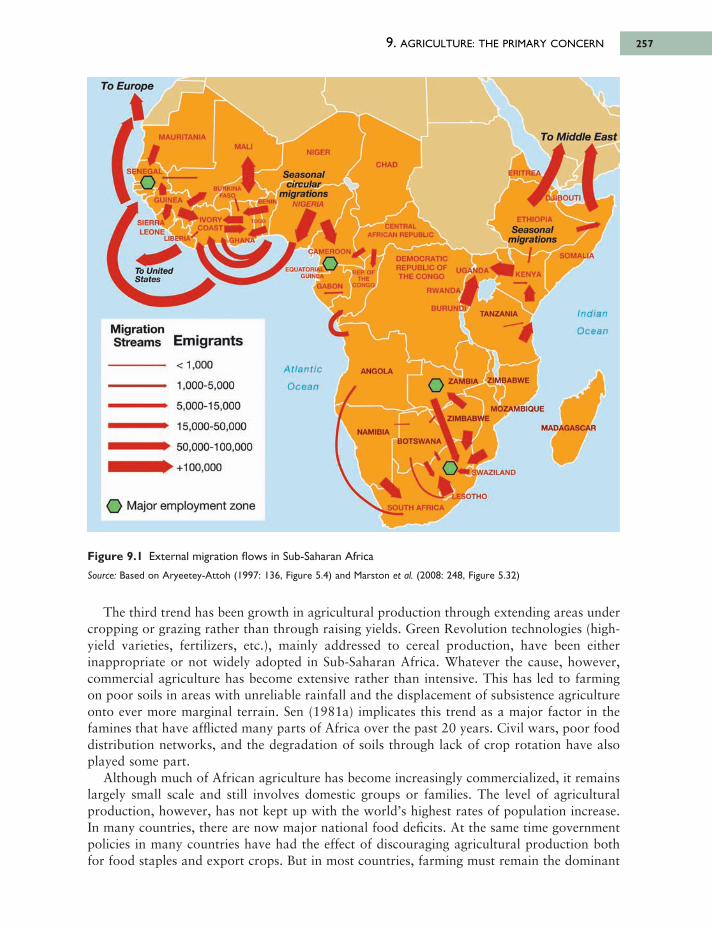

8.11 Soviet and U.S. spheres of influence, 1982 2389.1 External migration flows in Sub-Saharan Africa 257

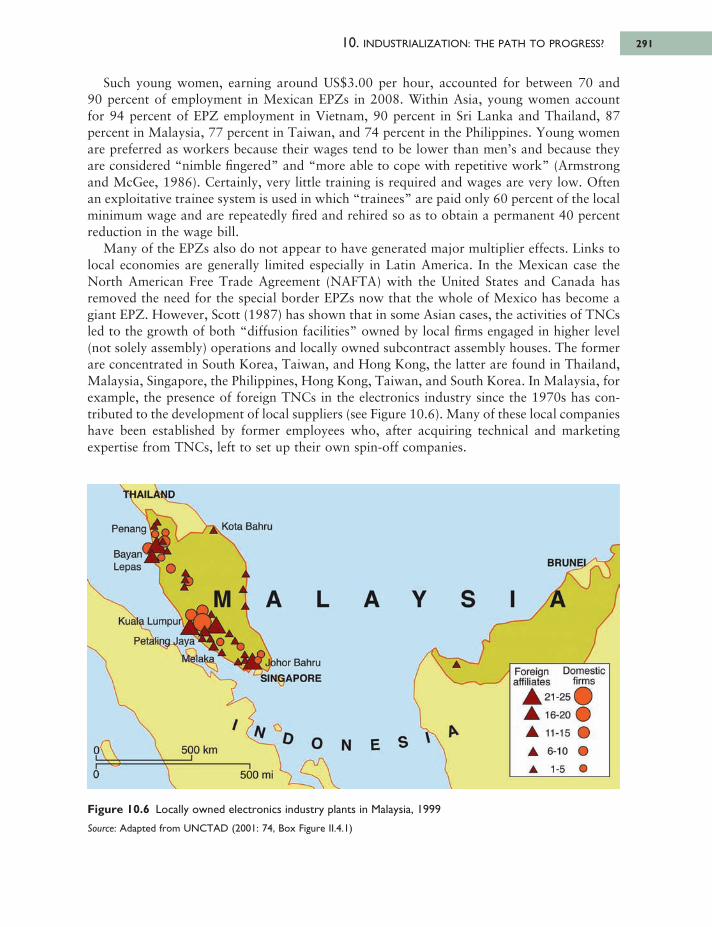

10.1 Manufacturing as a percentage of GDP, 2010 28610.2 Three “tests” of industrialization, 1975 and 2004 28710.3 The geography of growth in manufacturing output, 1995–2005 28910.4 Share of certain NIEs in total LDC exports, 2005–06 by value 28910.5 Labour processes in three manufacturing industries 29010.6 Locally owned electronics industry plants in Malaysia, 1999 29110.7 Share of U.S. and European companies’ outsourcing contracts with

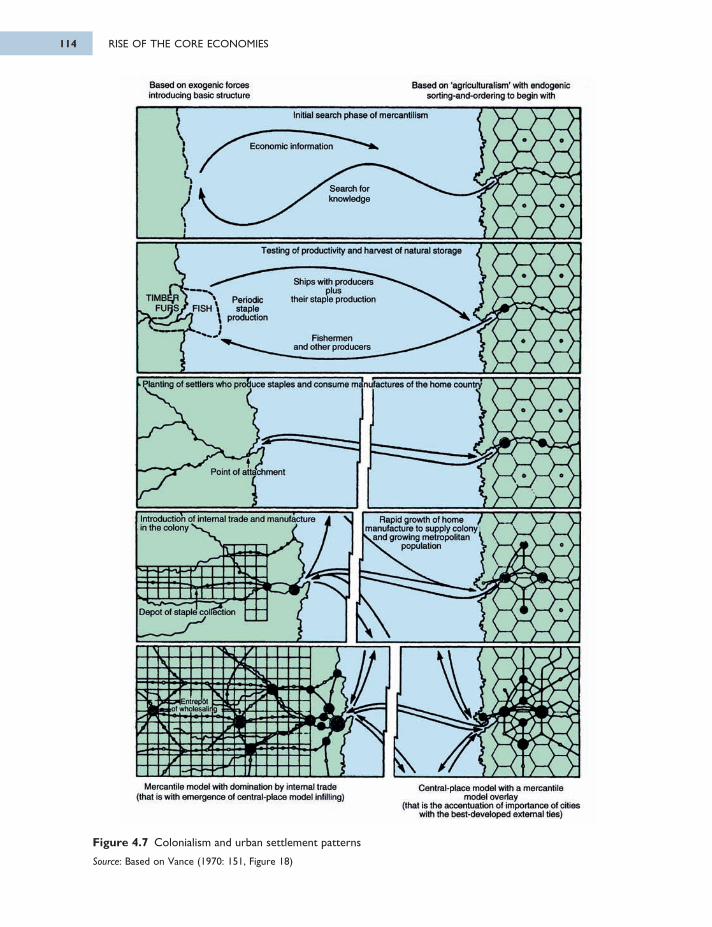

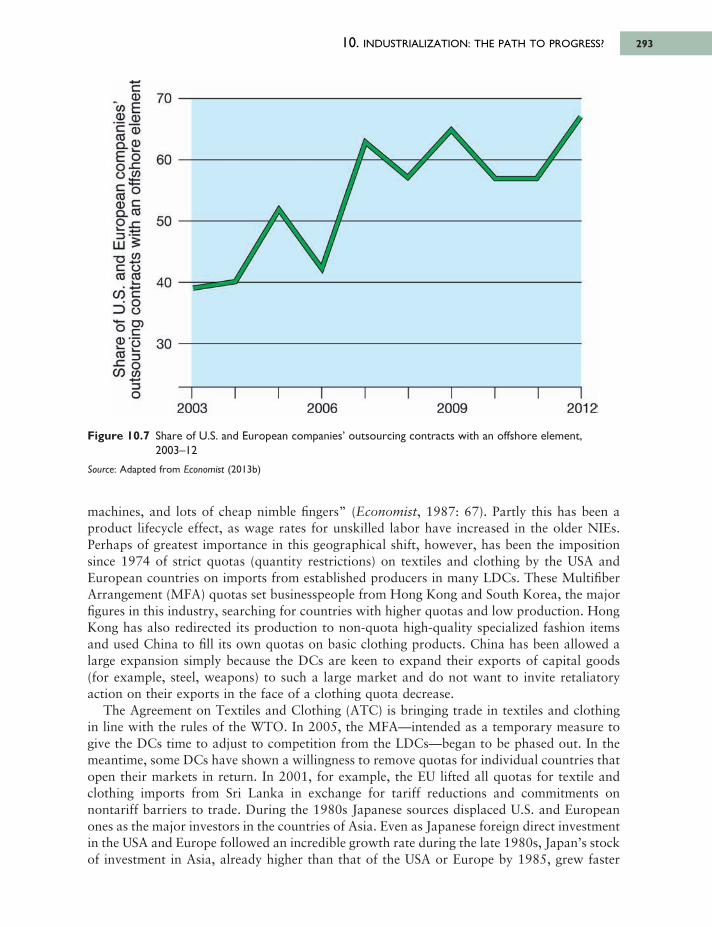

an offshore element, 2003–12 29310.8 Manufacturing establishments of the Japanese electronics industry

in Asia, 1995 29710.9 Economic and demographic growth in China 30510.10 Percentage of China’s GDP from industry and services 30711.1 Changing share of employment in primary, secondary and tertiary

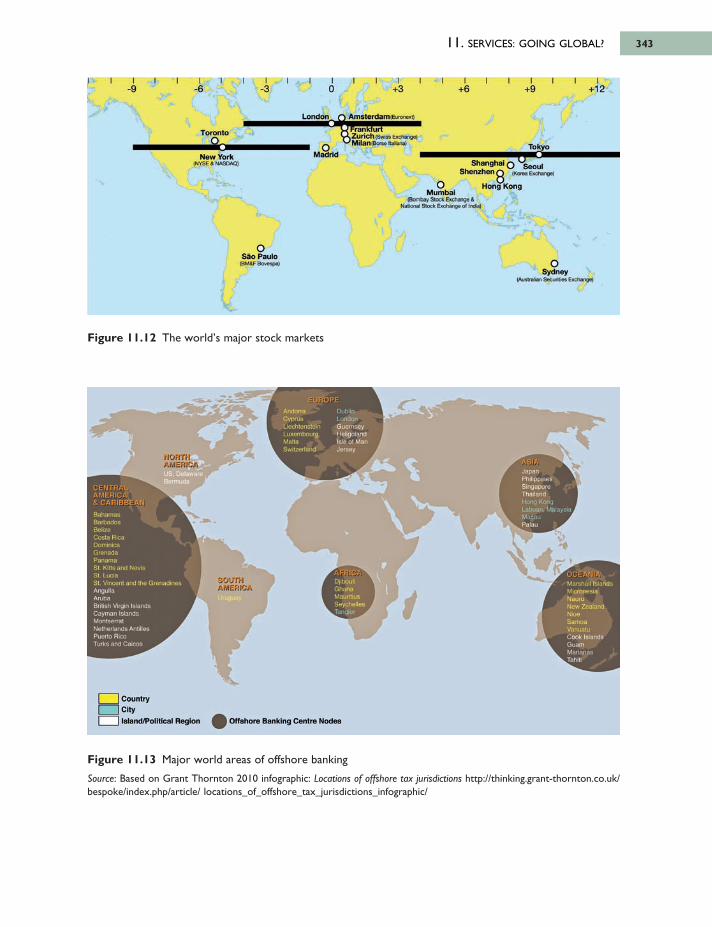

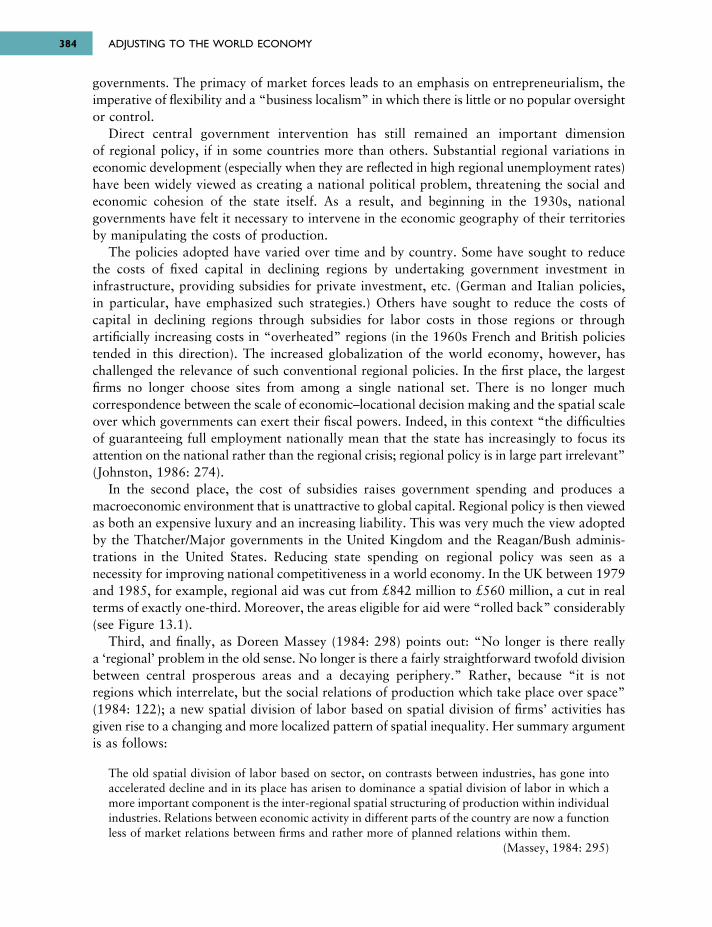

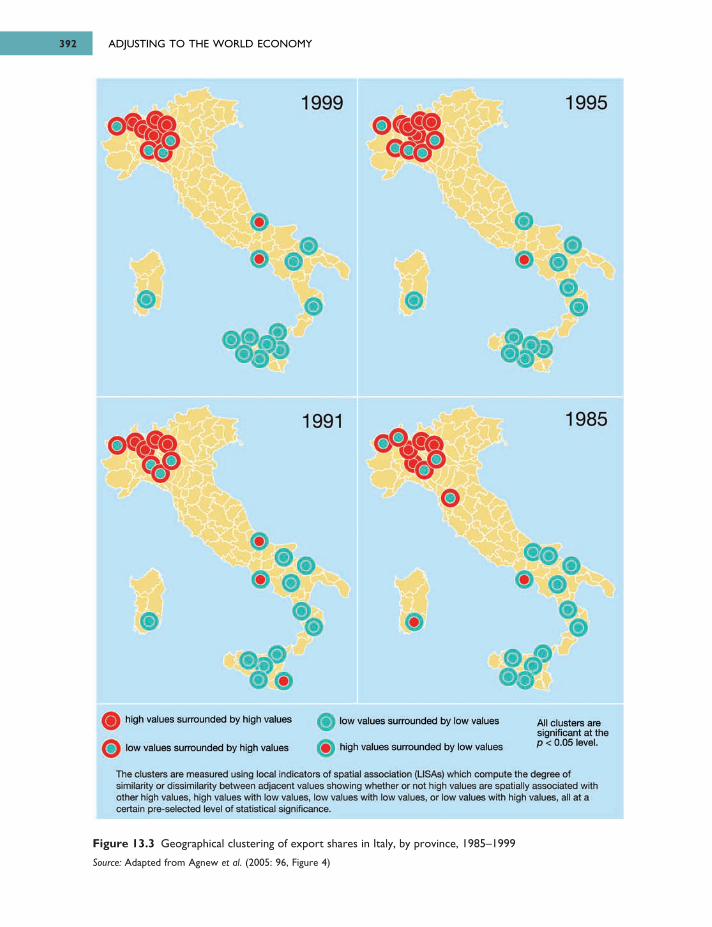

sectors of the economy 31411.2 Service employment and GDP per capita, selected countries 31411.3 The world’s largest service providers 31511.4 Service encapsulation 31811.5 Submarine fiber-optic cable network 32311.6 Percentage of workers in services 32711.7 Informal economy and level of development 327 11.8 Average annual percentage growth in services 32811.9 Service production 32811.10 Exports and imports of services, 2010 33011.11 International tourist arrivals and receipts, 2006 33711.12 The world’s major stock markets 34311.13 Major world areas of offshore banking 34311.14 Global R&D service providers, 2012 34712.1 Selected supranational integration agreements 35812.2 Enlargement of the European Union 36812.3 Regional policy in the European Union, 2007–2013 37413.1 The Thatcher government’s rolling back of regional aid, 1979–84 38513.2 Governmental decentralization of Russia, 1993 38913.3 Geographical clustering of export shares in Italy, by province, 1985–1999 39213.4 How plant size in the United States has shrunk 393

FIGURESx

6063 GEOGRAPHY WORLD ECON_PT_246x189 mm 22/01/2014 15:09 Page x

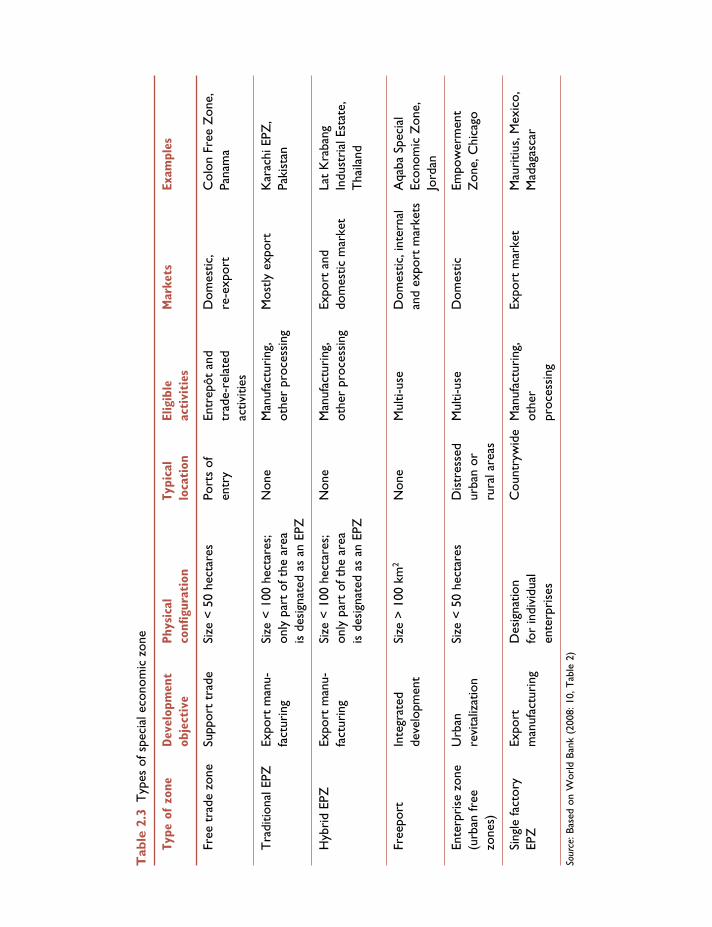

1.1 Technology systems and the evolution of the world economy 111.2 Global foreign exchange market turnover (daily averages, US$ billions) 172.1 World manufacturing 462.2 World’s top non-financial TNCs ranked by foreign assets, 2010 472.3 Types of special economic zone 483.1 The continuum of geographical incorporation into the world economy 653.2 The geographical development of the world economy in the nineteenth

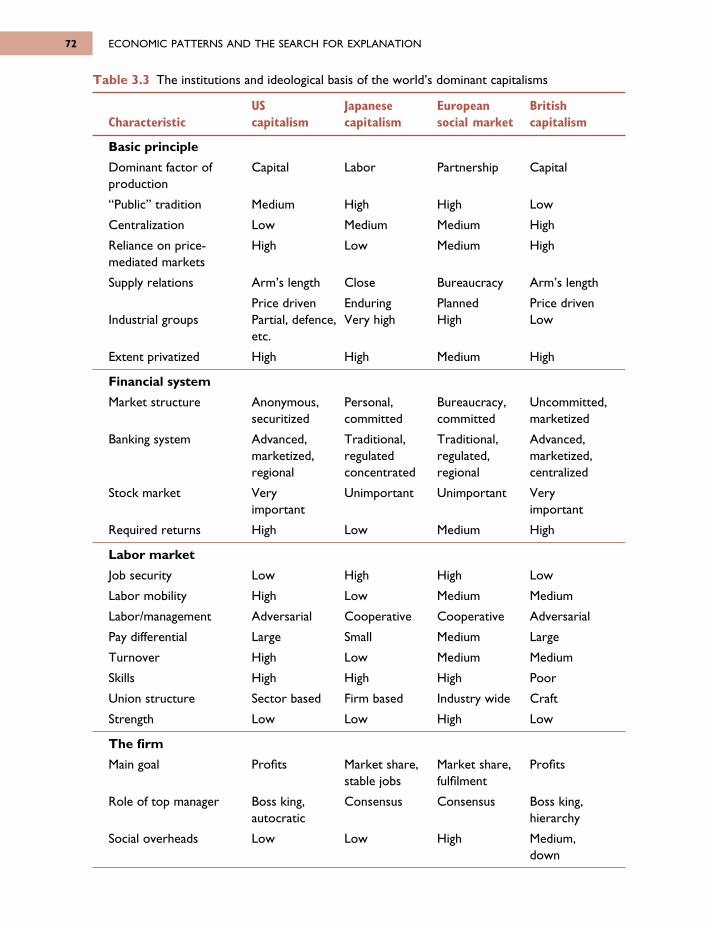

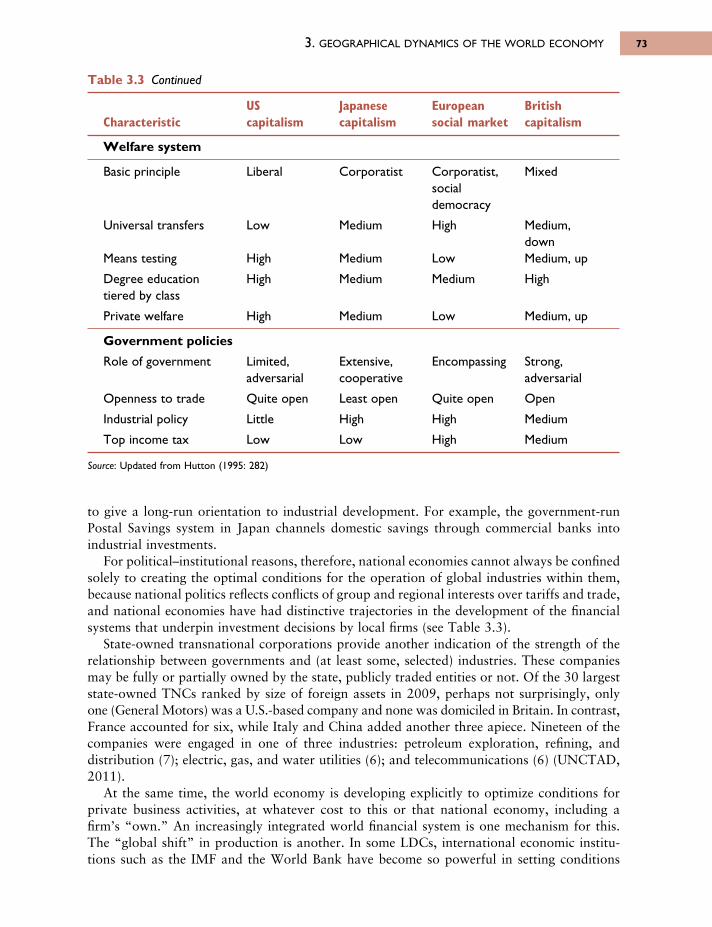

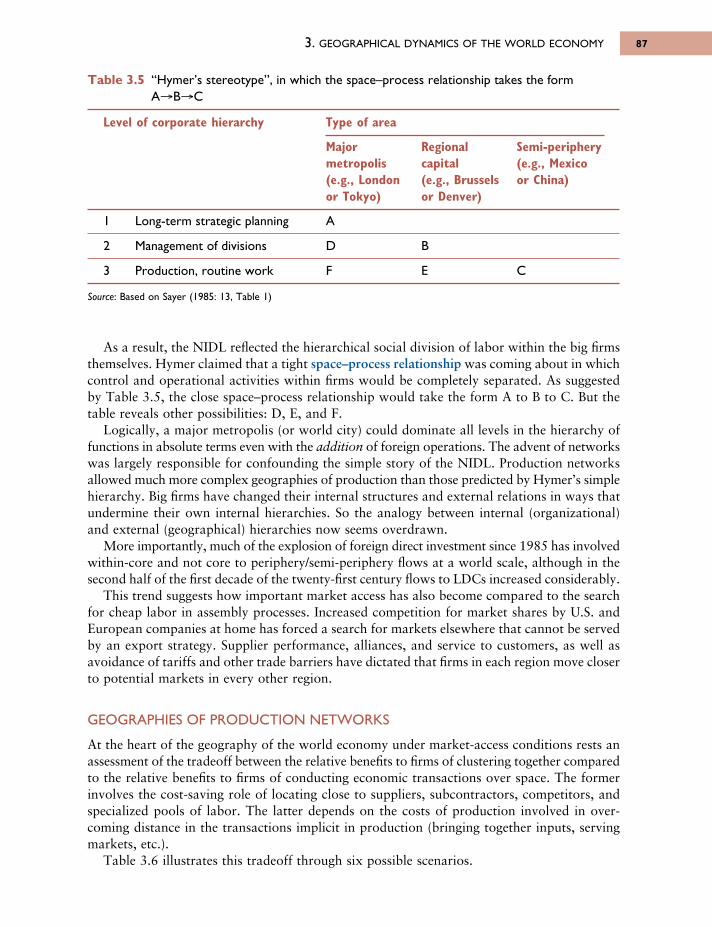

century 663.3 The institutions and ideological basis of the world’s dominant capitalisms 723.4 The old and the new pillars of world trade 813.5 “Hymer’s stereotype”, in which the space–process relationship takes

the form A→B→C 873.6 Spatial transaction costs versus externalities: six scenarios 885.1 Growth rates in Europe 1236.1 Percentage of value of shipments accounted for by the four largest

companies in selected manufacturing industries in the USA 1566.2 Inter- and intra-regional merchandise trade, 2011 (US$ billions) 1606.3 United States trade in goods and services with the European Union

(US$ billions) 1616.4 Contrasts in production and labor: Fordism versus flexible production 1637.1 Contrasts in governance: Fordism versus flexible production 1827.2 World Internet users 1997.3 Propulsive industries and new industrial spaces 2038.1 Stock of foreign capital investment held by Europe, 1825–1915

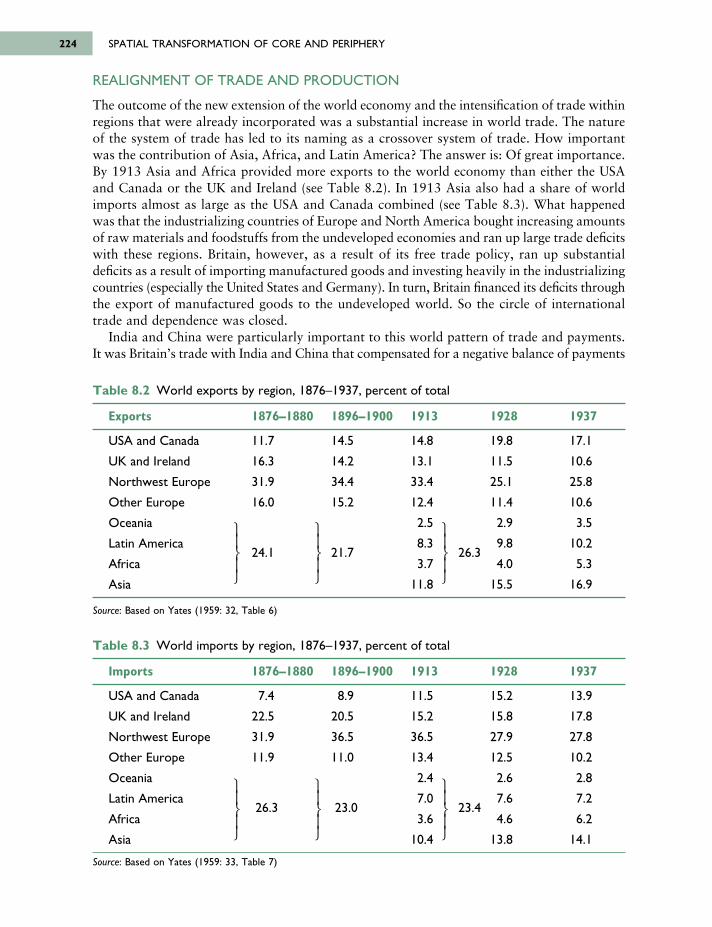

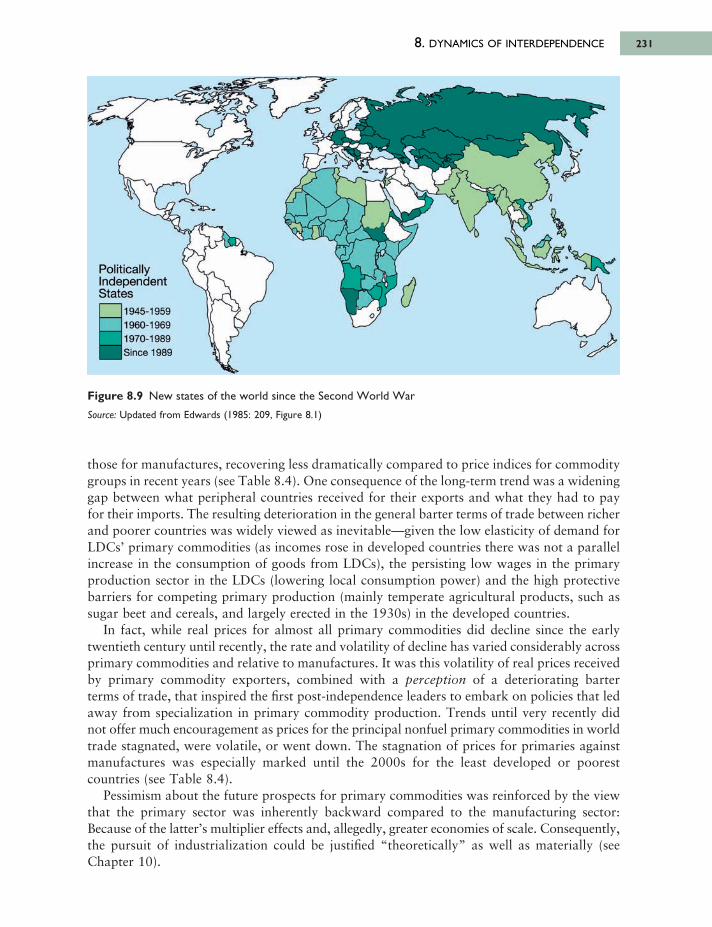

(US$ billion) 2208.2 World exports by region, 1876–1937, percent of total 2248.3 World imports by region, 1876–1937, percent of total 2248.4 Barter terms of trade and world prices for primary product commodity

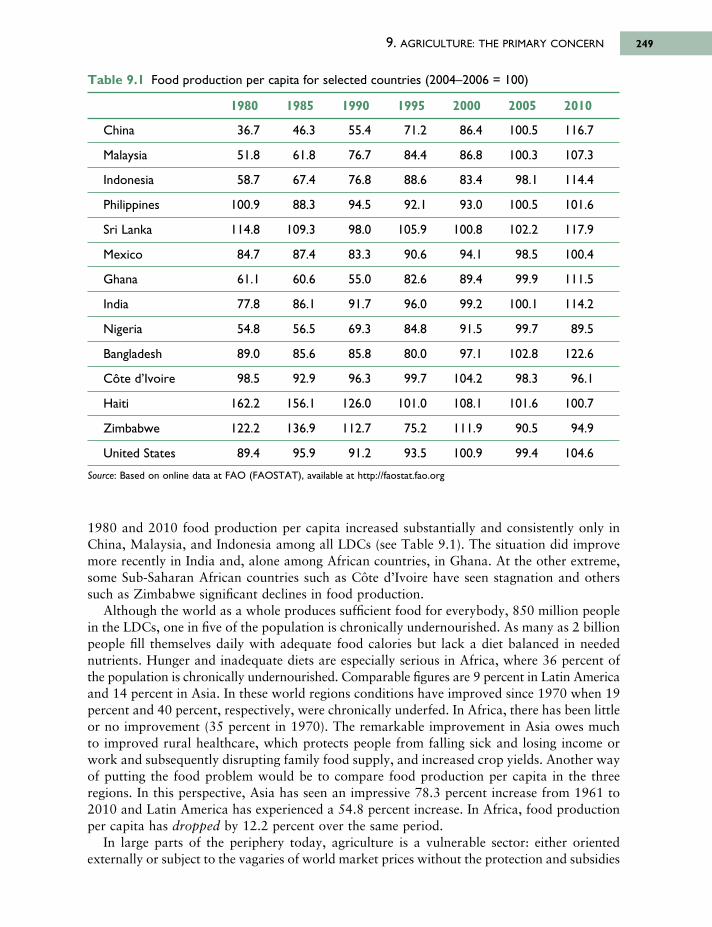

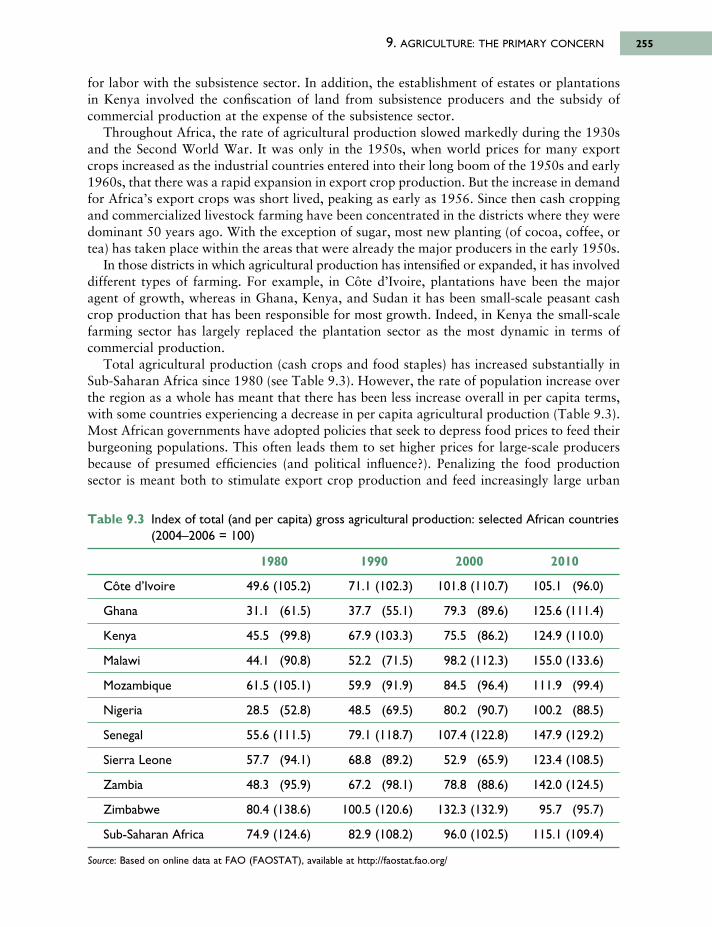

groups 2328.5 Adaptations to global capitalism 2439.1 Food production per capita for selected countries (2004–2006 = 100) 2499.2 Land, labor, capital, and markets: haciendas and plantations 2529.3 Index of total (and per capita) gross agricultural production: selected

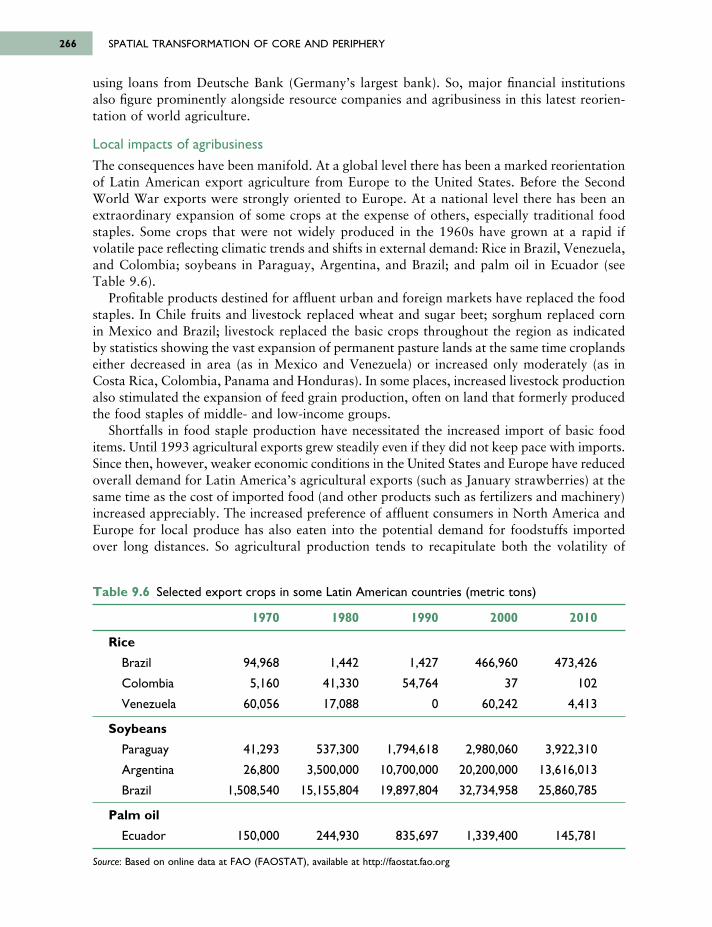

African countries (2004–2006 = 100) 2559.4 Average farm size, 2010 2589.5 A typology of land reforms 2619.6 Selected export crops in some Latin American countries (metric tons) 266

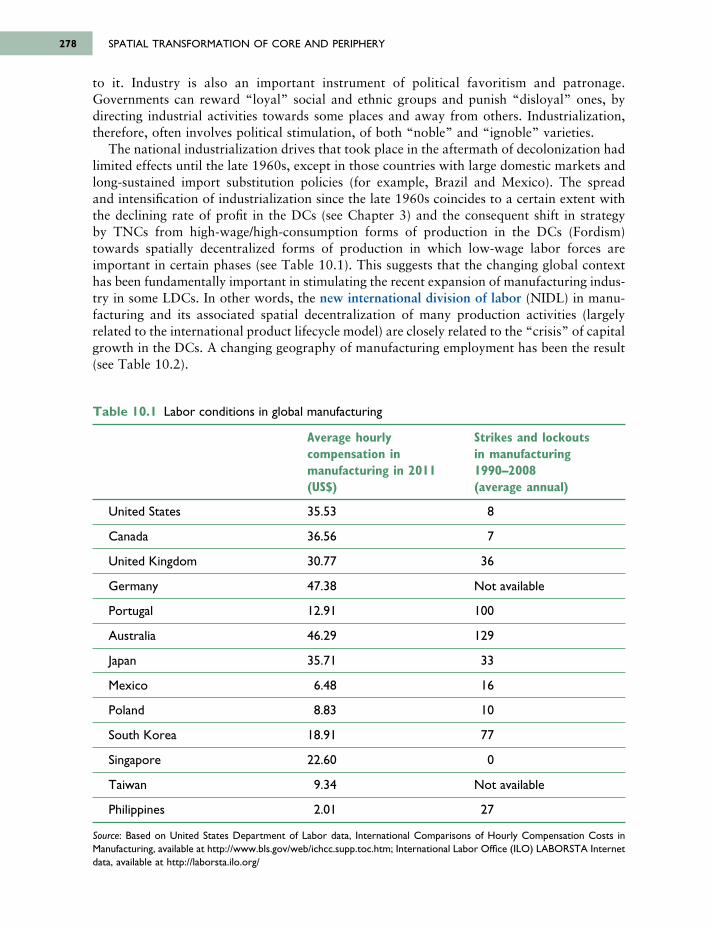

10.1 Labor conditions in global manufacturing 27810.2 Changing geography of manufacturing employment: paid employment in

manufacturing (millions of people) 279

Tables

6063 GEOGRAPHY WORLD ECON_PT_246x189 mm 22/01/2014 15:09 Page xi

10.3 International variations in the concentration of incomes (higher figures indicate greater inequality) 284

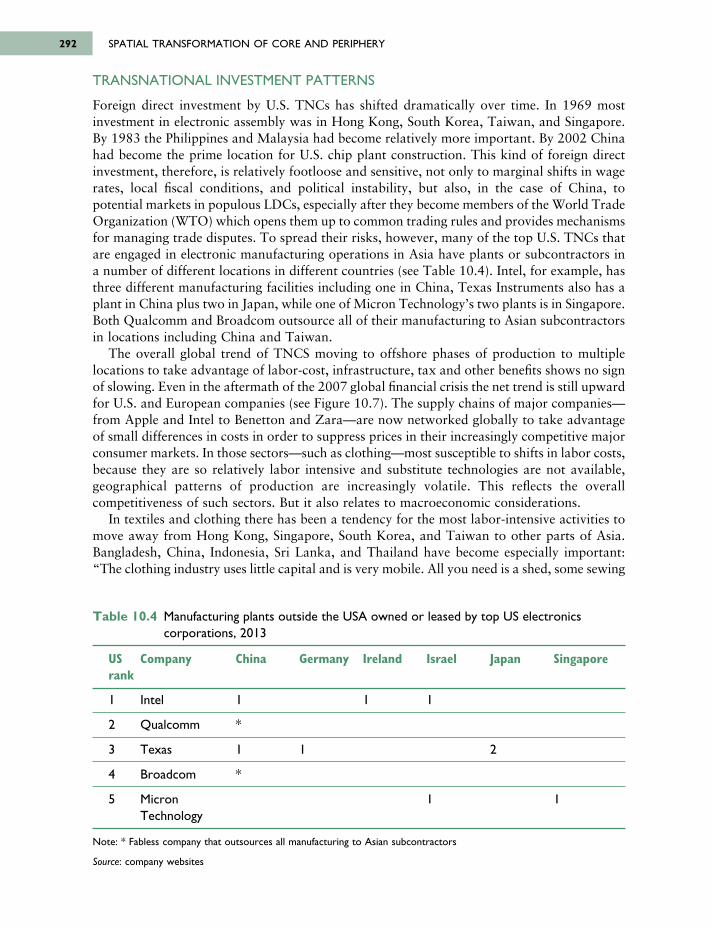

10.4 Manufacturing plants outside the USA owned or leased by top US electronics corporations, 2013 292

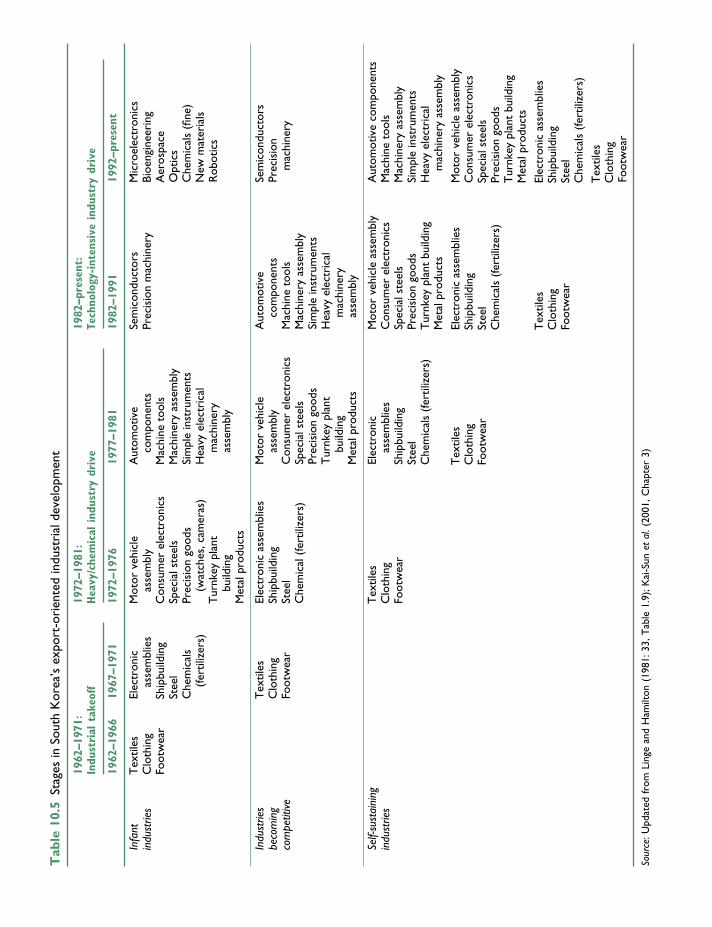

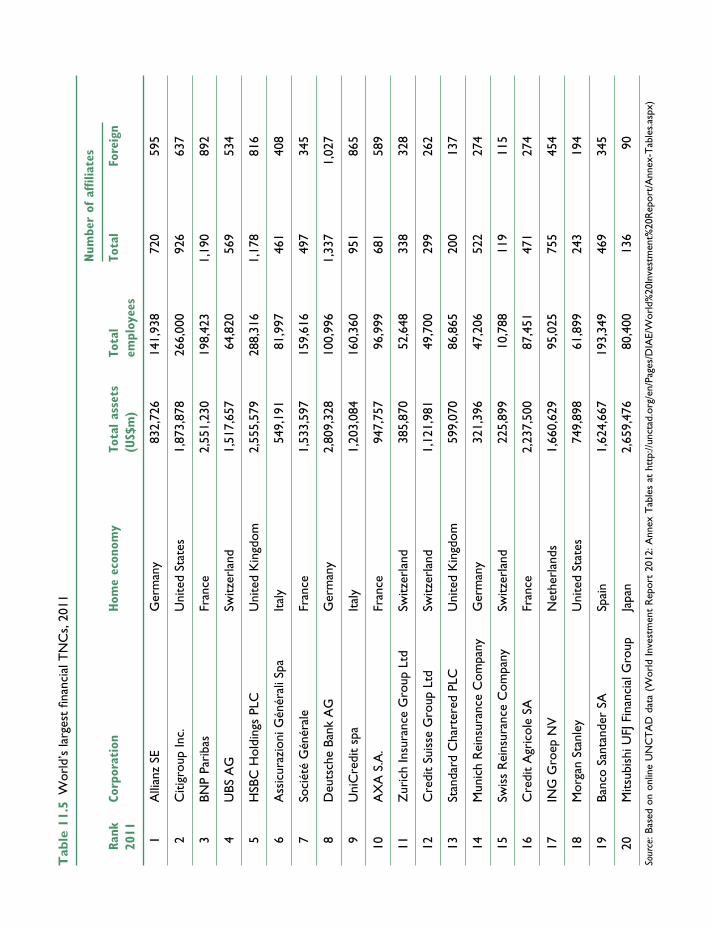

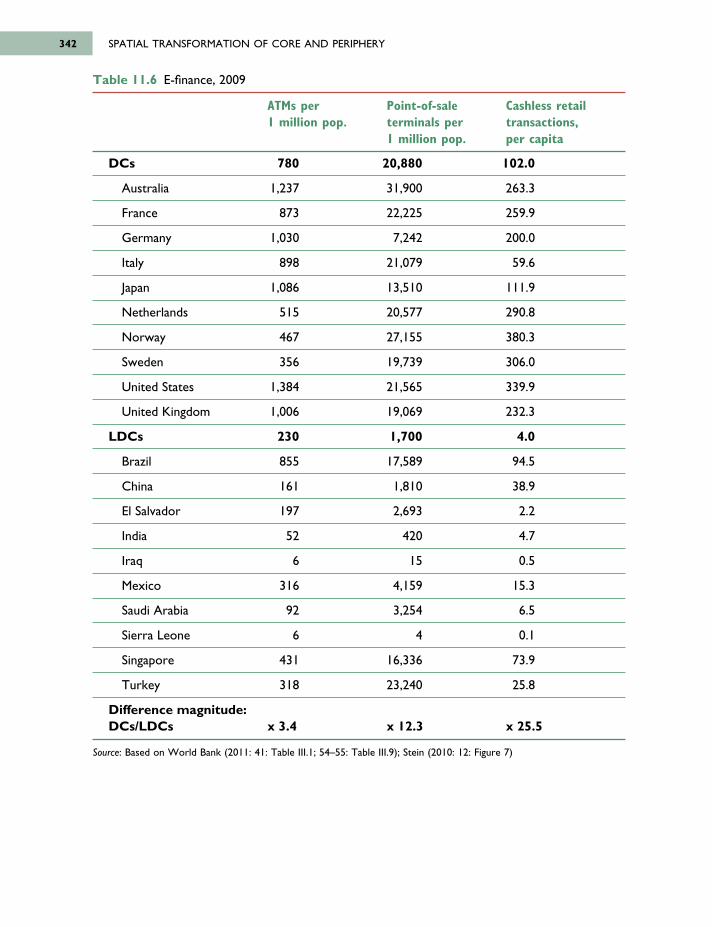

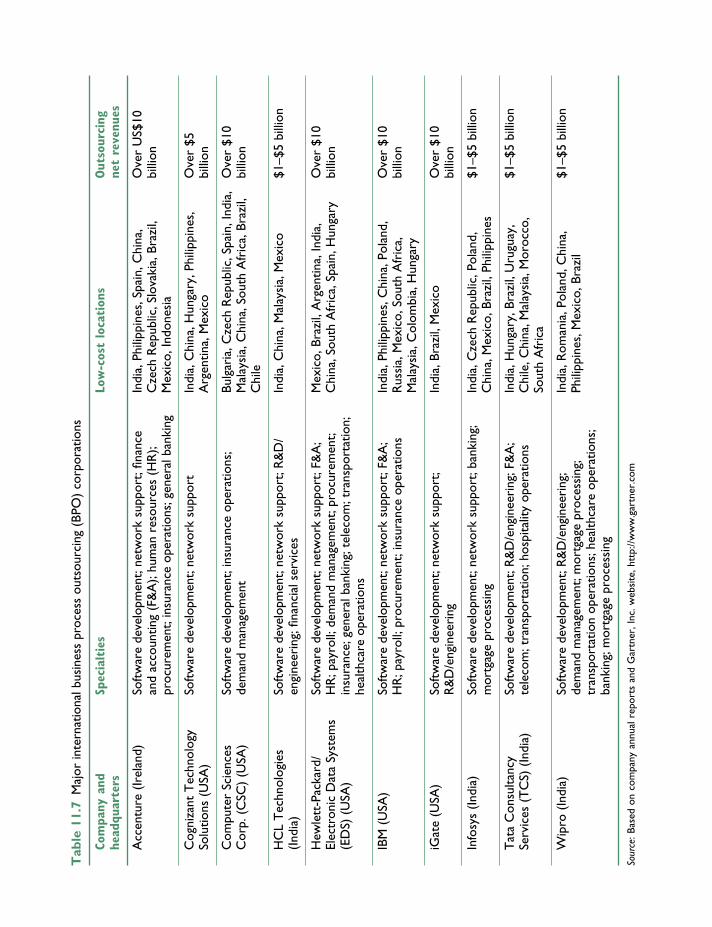

10.5 Stages in South Korea’s export-oriented industrial development 29610.6 China Mobile Limited’s cellphone global production system 29810.7 The BRIC road to economic growth 30911.1 Deciphering the outsourcing terminology 32111.2 Changing employment in services as a percentage of total employment 32611.3 EPZs targeting services 33111.4 Wal-Mart retail stores 33411.5 World’s largest financial TNCs, 2011 34111.6 E-finance, 2009 34211.7 Major international business process outsourcing (BPO) corporations 34512.1 Average tariff levels (percent) for selected countries, 1988 and 2009–2011 359

TABLESxii

6063 GEOGRAPHY WORLD ECON_PT_246x189 mm 22/01/2014 15:09 Page xii

1.1 Outsourcing and global commodity chains 141.2 Barbie: American icon and global product 162.1 HIV/AIDS and the impact on development in Sub-Saharan Africa 242.2 Indicators of well-being 262.3 E-waste and the digital divide 332.4 Migrant workers’ remittances 432.5 From darling to disaster: Iceland and the global financial crisis 563.1 Neoliberalism 773.2 The semiconductor industry and the workings of the market-access regime 845.1 Core and periphery in Europe 1245.2 The growth of the U.S. manufacturing belt 1275.3 Regional dimensions of Japanese industrialization 1356.1 Technological breakthroughs and the information economy 1506.2 Fast fashion and IT: Zara responds rapidly to changing customer demand 1546.3 The changing geography of the clothing industry 1676.4 The myth of the new industrial districts of the Third Italy? 1706.5 Coming to America? 1737.1 The Sunbelt 1887.2 Agglomeration and the “relational turn” in economic geography:

Motorsport Valley 1897.3 The digital divide 1987.4 The demise of the Celtic Tiger 2027.5 Hollywood and the cultural economy of cities 2047.6 National economic development and regional inequality 2088.1 The Asian financial crisis 2409.1 The coffee commodity chain 2489.2 From free trade to fair trade? 2509.3 Agribusiness and the developed countries 2639.4 The great land grab? 2659.5 Science and rice 271

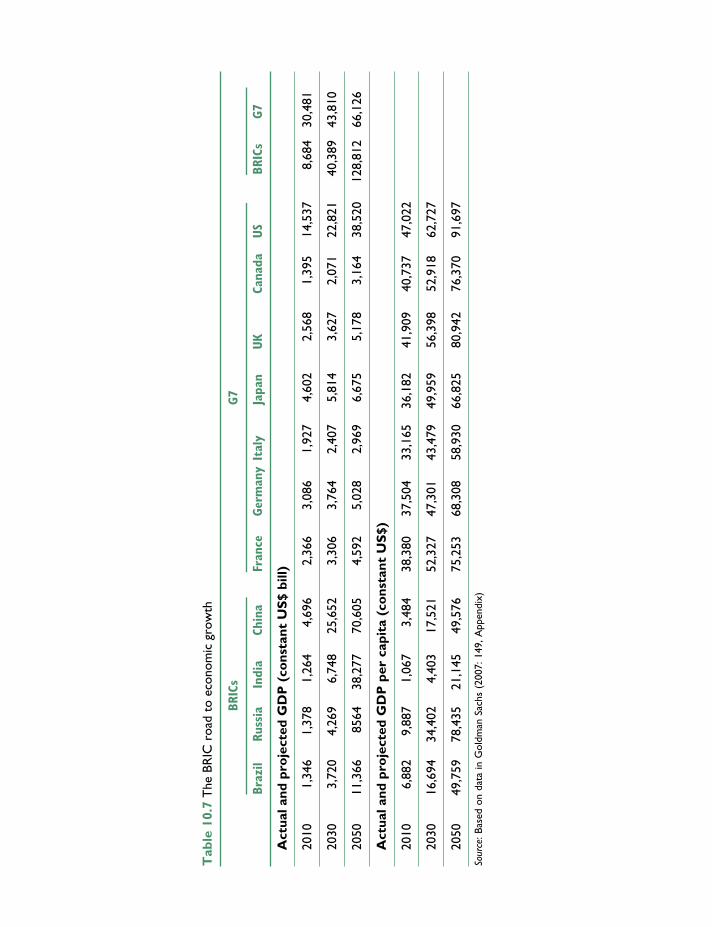

10.1 Dreaming the BRIC future 30811.1 Bucking the Fisher-Clark thesis in China? Concurrent growth of

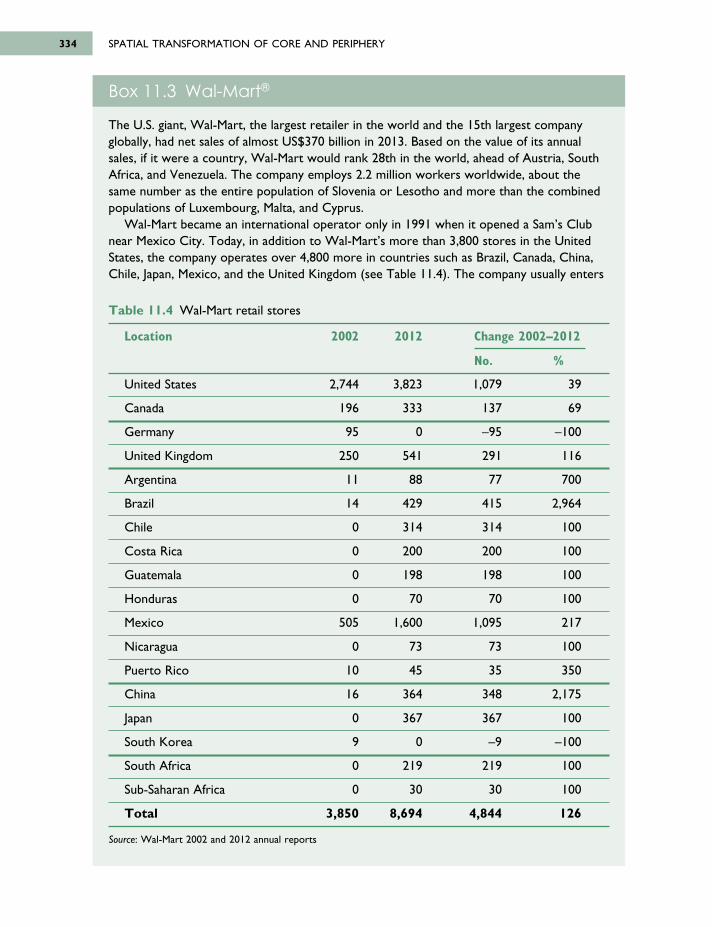

manufacturing and services 32011.2 A day in the life of a call center worker in India 32511.3 Wal-Mart® 33411.4 Abu Dhabi, a tourist Mecca? 33811.5 India’s competitive advantage in BPO 34612.1 Genetically modified foods and U.S.–EU trade 37513.1 International terrorism 389

Boxes

6063 GEOGRAPHY WORLD ECON_PT_246x189 mm 22/01/2014 15:09 Page xiii

The authors would like to thank the following organizations for permission to use the materiallisted:

Figure 1.4 from “Shifting governance structures in global commodity chains, with specialreference to the Internet,” by Gereffi, published in American Behavioral Scientist 44, 2001,with permission of Sage Publications.

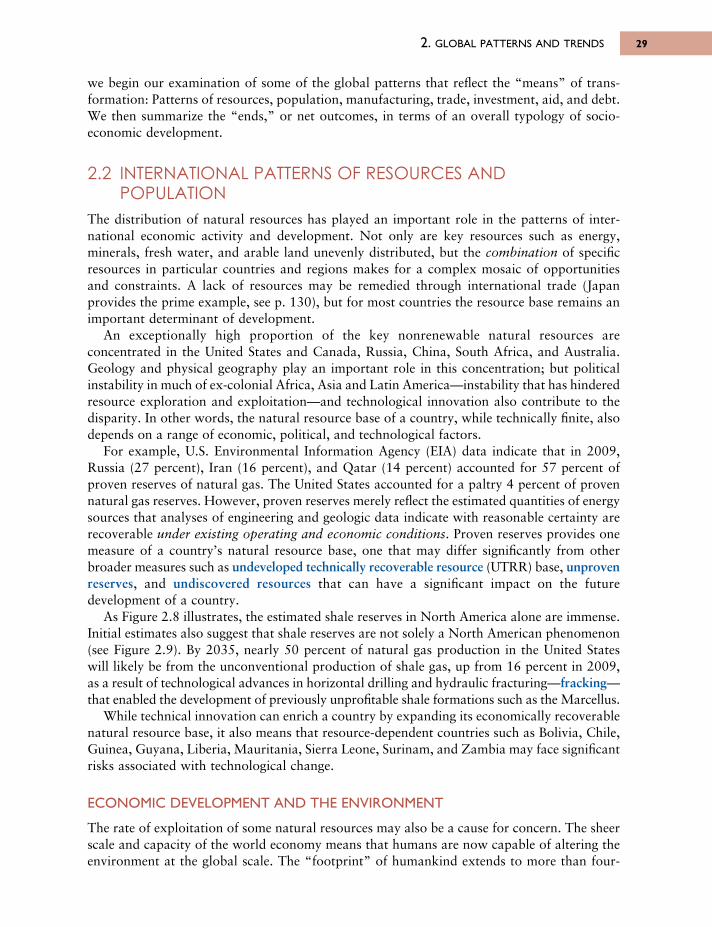

Figure 2.8 from Energy in Brief: What is shale gas and why is it important? by E.I.A. (U.S.Energy Information Administration, U.S. Department of Energy) 2012.

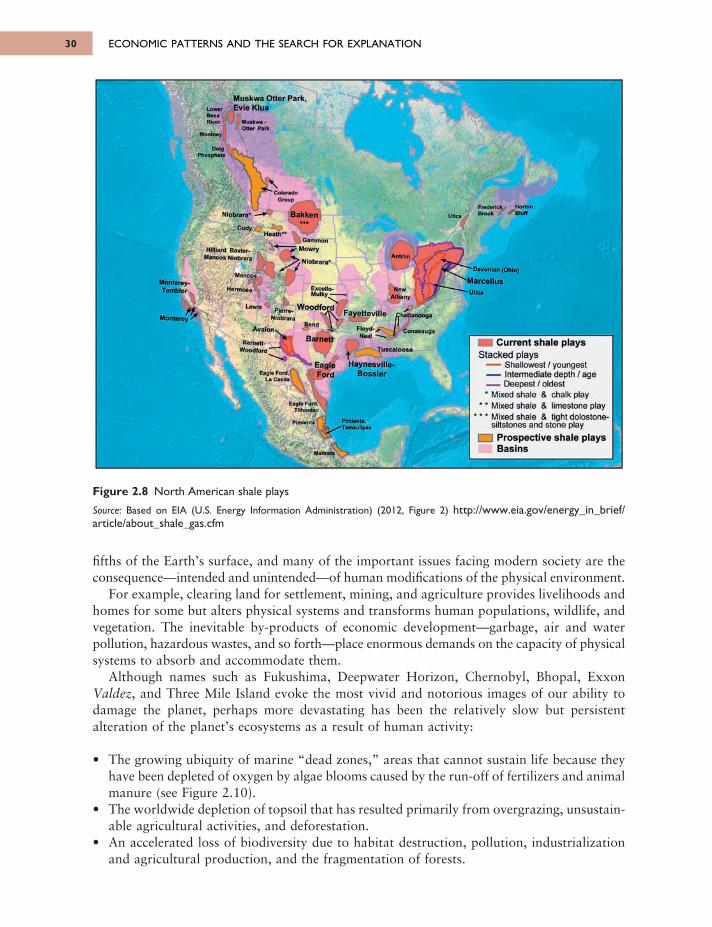

Figure 2.9 from Analysis and Projections: World shale gas resources: An initial assessment of14 regions outside the United States by E.I.A. (U.S. Energy Information Administration,U.S. Department of Energy) 2011.

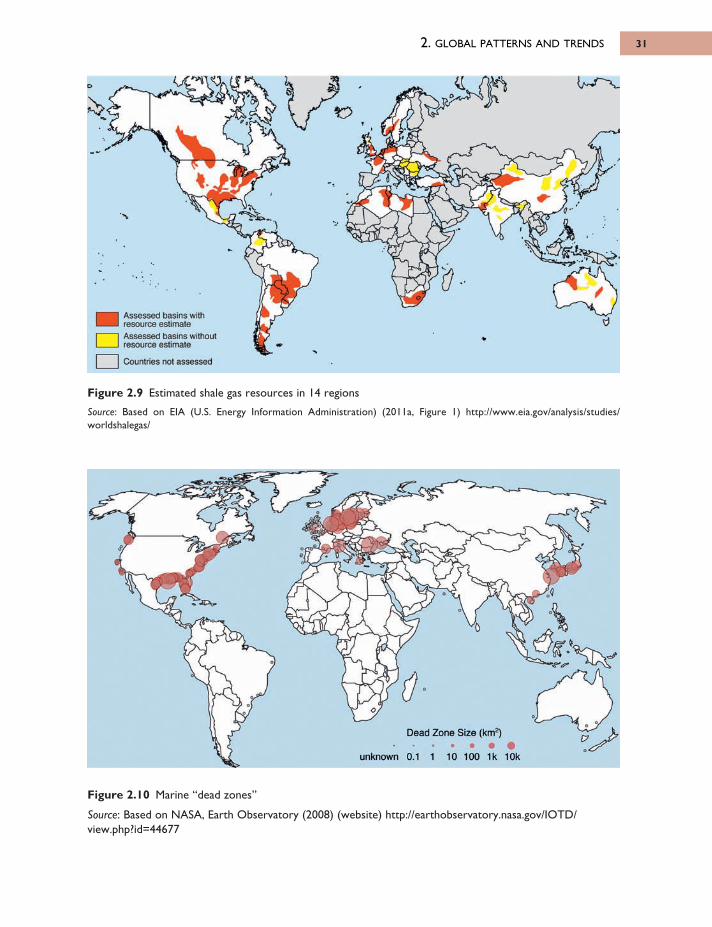

Figure 2.10 from Aquatic Dead Zones by NASA, Earth Observatory, 2008.Figure 2.13 from Vital Water Graphics: An overview of the state of the world’s fresh and

marine waters by UNEP (United Nations Environment Program) 2002.Figure 2.14 from Living Planet Report 2010: Biodiversity, biocapacity and development by

WWF (World Wide Fund for Nature) 2010.Figure 2.18 from Human Development Report 2009: Overcoming barriers: Human mobility

and development by UNDP (United Nations Development Program) 2009.Figure 2.20 from Poverty Reduction and Social Development: Migration and the brain drain

phenomenon by OECD (Organization for Economic Cooperation and Development) nd.Figure 2.21 from World Trade 2011, Prospects for 2012: Trade growth to slow in 2012 after

strong deceleration in 2011 by WTO (World Trade Organization) 2012.Figure 3.2 from Corruption Perceptions Index 2011 by Transparency International, 2012.Figure 4.1 from An Introduction to Urban Historical Geography, 1983, by Carter, with

permission from Routledge.Figure 4.2 from the Historical Atlas, 1923, by Shepherd, with permission from the Perry-

Castañeda Library Map Collection, University of Texas at Austin.Figure 5.2 from Peaceful Conquest: The industrialization of Europe, 1760–1970, 1981, by

Pollard, with permission of Oxford University Press.Figure 6.1 from “Industrial restructuring: an international problem,” by Hamilton, published

in Geoforum 15, 1984, with permission of Elsevier.Figure 6.3 from “Boeing’s outsourcing for the 787 Dreamliner,” published in Seattle Times,

2006, 29 September, with permission of Seattle Times.Figure 7.2 from Science and Engineering Indicators 2012, 2012, by National Science Board,

with permission of National Science Foundation.Figure 7.3 from The Offshore Services Value Chain, 2010, by G. Gereffi and K. Fernandez-

Stark, with permission of G. Gereffi, Duke University, North Carolina, Center onGlobalization, Governance, and Competitiveness (CGGC) http://www.cggc.duke.edu/pdfs/CGGC CORFO_The_Offshore_Services_Global_Value_Chain_March_1_2010.pdf

Acknowledgements

6063 GEOGRAPHY WORLD ECON_PT_246x189 mm 22/01/2014 15:09 Page xiv

Figure 8.8 from “The River Plate countries,” by Crossley, published in Blakemoor and Smith(eds) Latin America: Geographical perspectives, 2nd edition, 1983, with permission ofRoutledge.

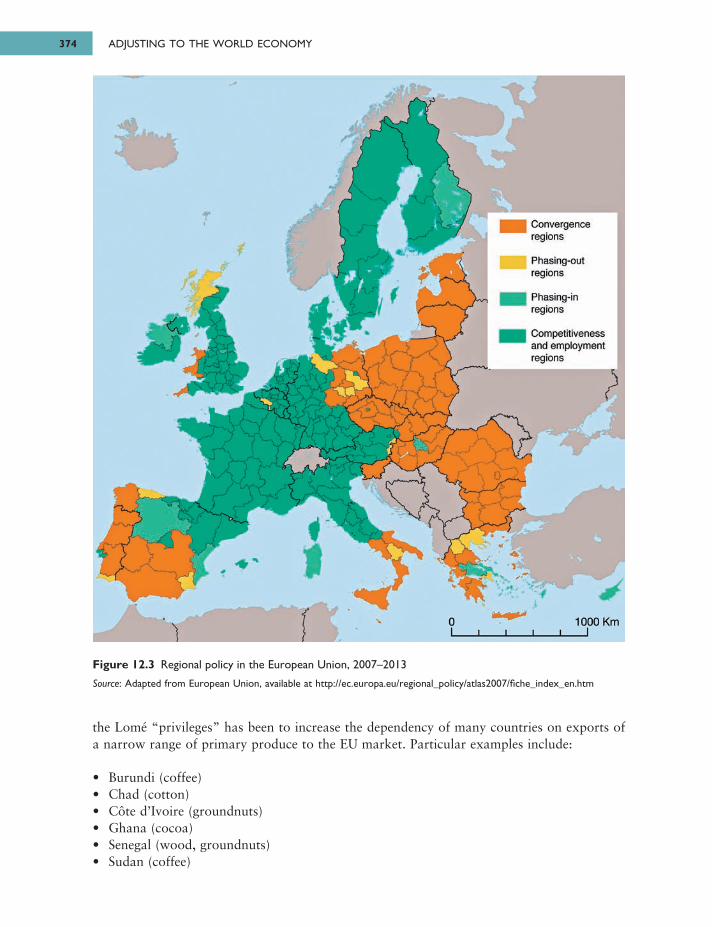

Figure 12.3 from Regional Policy—Inforegio: Cohesion policy 2007–2013 by the EuropeanCommission.

Every effort has been made to trace copyright holders of material reproduced in this book.Any rights not acknowledged here will be acknowledged in subsequent printings if notice isgiven to the publisher.

We are indebted to many of our colleagues for their advice at various stages in the conceptionand preparation of this book, and in its current revision. We would particularly like to recognizeStuart Corbridge, Raymundo Cota, Bob Dyck, Richard Grant, Larry Grossman, NaeemInayatullah, D. Michael Kirchoff, Soo-Seong Lee, Andrew Leyshon, Ragnhild Lund, SallieMarston, Ezzeddine Moudoud, Pritti Ramamurthy, Bon Richardson, Susan Roberts, David J.Robinson, Freddy Robles, Mark Rupert, David Short, Barney Warf, and Colin Warren fortheir contributions.

ACKNOWLEDGEMENTS xv

6063 GEOGRAPHY WORLD ECON_PT_246x189 mm 22/01/2014 15:09 Page xv

6063 GEOGRAPHY WORLD ECON_PT_246x189 mm 22/01/2014 15:09 Page xvi

This page intentionally left blank

Part 1

Economic patterns and thesearch for explanation

Picture credit: Linda McCarthy

In the first part of this book, we introduce the scope and complexity of our subject, establishthe salient patterns in the world’s economic landscapes, and review alternative theoreticalapproaches to understanding the development of these patterns. Chapter 1 provides the

orientation for the book by outlining the relationships between the organization of the worldeconomy and spatial change. In Chapter 2, the major dimensions of the world’s contemporarylandscapes are described. We identify dominant and recurring patterns and note the majorexceptions to these patterns. Both the patterns and the exceptions raise a number of criticalquestions about process and theory in economic geography. For example: “How should thedevelopment process be conceptualized?,” “What are the processes that initiate and sustainspatial inequalities?,” and “Why are economic activity and prosperity spread so unevenly?”These questions are pursued in Chapter 3, where we outline a broad theoretical frameworkfor under standing the interdependence of the world economy and its spatial components.

6063 GEOGRAPHY WORLD ECON_PT_246x189 mm 22/01/2014 15:09 Page 1

6063 GEOGRAPHY WORLD ECON_PT_246x189 mm 22/01/2014 15:09 Page 2

This page intentionally left blank

The perspective of this book is global. Although local, regional, and national circum -stances remain important, what happens in any given locale is increasingly influencedby its role in and relationship to systems of production, trade, and consumption that

are global in scope.In the 1970s, only a few less developed countries (LDCs) had opened their borders to trade

and investment. About one-third of the world’s labor force lived in countries with centrallyplanned economies. Another third lived in countries insulated from international markets byprotective trade barriers and currency controls.

Today, more than 7 billion people populate our planet, and most live in countries that havebeen integrated into global markets. Three population blocs—China, India, and the republicsof the former Soviet Union—account for more than 40 percent of the world’s labor force andare important participants in the global market. Many other countries such as the newlyindustrializing economies (NIEs) of Brazil, Hong Kong, Singapore, South Korea, and Taiwanhave also become vital contributors to the world economy.

More than two decades ago, Robert Reich, former U.S. Secretary of Labor, underscoredthe significance of the rapid pace of globalization:

We are living through a transformation that will rearrange the politics and economics of the comingcentury. There will be no national products or technologies, no national corporations, no nationalindustries. There will no longer be national economies, at least as we have come to understandthat concept. . . . As almost every factor of production—money, technology, factories, andequipment—moves effortlessly across borders, the very idea of a U.S. economy is becomingmeaning less, as are the notions of a U.S. corporation, U.S. capital, U.S. products, and U.S.technology.

(Reich, 1991: 3, 8)

Picture credit: Linda McCarthy

Chapter 1

The changingworld economy

6063 GEOGRAPHY WORLD ECON_PT_246x189 mm 22/01/2014 15:09 Page 3

People are not only increasingly interconnected; they are interdependent as the followingnarratives generated by the World Bank illustrate:

Joe lives in a small town in southern Texas. His old job as an accounts clerk in a textile firm,where he had worked for many years, was not very secure. He earned $50 a day, but promisesof promotion never came through, and the firm eventually went out of business as cheap importsfrom Mexico forced textile prices down. Joe went back to college to study business administrationand was recently hired by one of the new banks in the area. He enjoys a comfortable living evenafter making the monthly payments on his government-subsidized student loan.

Maria recently moved from her central Mexican village and now works in a U.S.-owned factoryin Mexico’s maquiladora sector. Her husband, Juan, runs a small car upholstery business andsometimes crosses the border during the harvest season to work illegally on farms in California.Maria, Juan, and their son have improved their standard of living since moving out of subsistenceagriculture, but Maria’s wage has not increased in years; she still earns about $10 a day but doesnot complain because she has heard rumors that the company is considering moving the factoryto China.

Xiao Zhi is an industrial worker in Shenzhen, a Special Economic Zone in China. After three difficultyears on the road as part of China’s floating population, fleeing the poverty of nearby Sichuanprovince, he has finally settled with a new firm from Hong Kong that produces garments for theU.S. market. He can now afford more than a bowl of rice for his daily meal. He makes $2 a dayand is hopeful for the future.

The complex relationships revealed in this anecdote would have been unthinkable 30 yearsago.

Although the outcomes in this tale are positive—Joe secured a position at a bank and earnsa comfortable living; Maria and her family improved their standards of living; and Xiao Zhiescaped poverty—not everyone benefits from globalization. Although the world is increasinglyflat with capital crossing borders in nanoseconds in the pursuit of the highest rate of returnand corporations locating operations where labor markets, tax codes, and regulatory regimesare most favorable, it is not necessarily increasingly fair.

In a hypothetical sequel to the World Bank narratives, the bank where Joe worked leveragedits portfolio with uncollateralized debt and had to close its doors at the height of the globalfinancial crisis. With no income and a mortgage that exceeded the value of his house, Joe wasforced to file for bankruptcy, but he still owes $830 per month on his student loans. He wasfortunate enough to find a part-time job at a Wal-Mart warehouse, but with a one-way commuteof 56 miles and gas prices nearing $4 per gallon, he cannot afford health insurance.

Juan was detained by border patrol and has joined approximately 390,000 other illegalimmigrants incarcerated indefinitely in U.S. detention centers. The recession bloated inventoriesand decreased the demand for textiles produced in the factory where Maria worked. Whenshe was laid off, she was forced to withdraw her son from school, move in with relatives, andreturn to subsistence farming.

And poor Xiao Zhi contracted a skin infection when he was forced to handle chemicals inthe factory without protective gloves. The floor manager fired him when he could no longermaintain the required pace of production. After many failed attempts to secure another jobin Shenzhen, he returned to Sichuan province but remains hopeful that the herbal remediesprescribed by the village doctor will heal him sufficiently so, one day, he will be able to earn$2 per day again.

ECONOMIC PATTERNS AND THE SEARCH FOR EXPLANATION4

6063 GEOGRAPHY WORLD ECON_PT_246x189 mm 22/01/2014 15:09 Page 4

1.1 STUDYING THE WORLD ECONOMYHow can one make sense of these stories? On the surface, cause-and-effect seem straight-forward—the demand for textiles declined; Maria lost her job—but in the undercurrent onediscovers a complex array of forces that have broad and dramatic effects that can often producesurprising and unexpected results. Deciphering the impact of those forces, interpreting theirlocal, regional, and national implications and how they alter the contours of the economiclandscape is the job of the economic geographer.

What are the implications of the Arab Spring; persistently high unemployment rates in EUcountries such as Italy and Spain; the AIDS pandemic in Africa; continued environmentaldegradation in China; increased immigration to the EU from countries in North Africa and theMiddle East; growing income inequality and increasingly polarized political landscape in theUnited States; technological advances such as fracking that enable the extraction of previouslyunprofitable carbon fuels; and the greater magnitude and frequency of natural disasters?

In addition to these headline-grabbing phenomena, what are the local, regional, andnational implications of less newsworthy but equally profound changes in the world economysuch as resource grabbing in Africa by developed countries, the rapid spread of geneticallymodified organisms (GMOs) in agricultural production, and technological advances that haveenabled cost-effective 3-D printing?

How can we interpret the significance of specific changes that have been occurring in theworld’s economic landscapes: The deindustrialization of traditional manufacturing regions (for example, the Rustbelt around the Great Lakes in the United States, northern England,the Ruhr region in Germany), the economic revival of formerly “lagging” regions (for example,New England, Bavaria), the spread of branch plants in the towns and cities of some NIEs (forexample, Taipei, Seoul), the emergence of high-technology complexes (for example, SiliconValley in California, the Research Triangle in North Carolina), the consolidation of globalfinancial and corporate control functions in a few cities (London, New York, Tokyo), and theunprecedented rates of urbanization in China’s coastal regions?

Our task is to develop an understanding of the general economic forces and socioeconomicrelationships within the world economy and of the unique features that represent local andhistorical variability.

But first we need to clarify the use of the terms “general” and “unique” as well as a thirdterm, “singular”:

• General: Widespread phenomena, such as migration or colonialism.• Unique: Distinctive phenomena—where there are no other instances of it—but its distinctive-

ness can be explained by a particular combination of general processes and individualresponses. An example of this would be the migration streams prompted by the famine in Ireland in the mid-1800s. The general processes that precipitated the famine wereenvironmental (potato blight) and governmental (laissez-faire policy); in response, manypeople emigrated, including to the United States.

• Singular: Distinctive phenomena that cannot be accounted for by combinations of generalprocesses and individual responses. An example would be the growth of the automobileindustry in Detroit. With no established pattern of manufacturing, automobile manufacturecould have developed in any number of cities; but Detroit was Henry Ford’s home town(his father had emigrated to Michigan from Ireland to flee the famine), and he put his ideasinto practice there.

With these concepts in hand, we can begin to map some of the interrelationships betweeneconomic organization and spatial change.

1. THE CHANGING WORLD ECONOMY 5

6063 GEOGRAPHY WORLD ECON_PT_246x189 mm 22/01/2014 15:09 Page 5

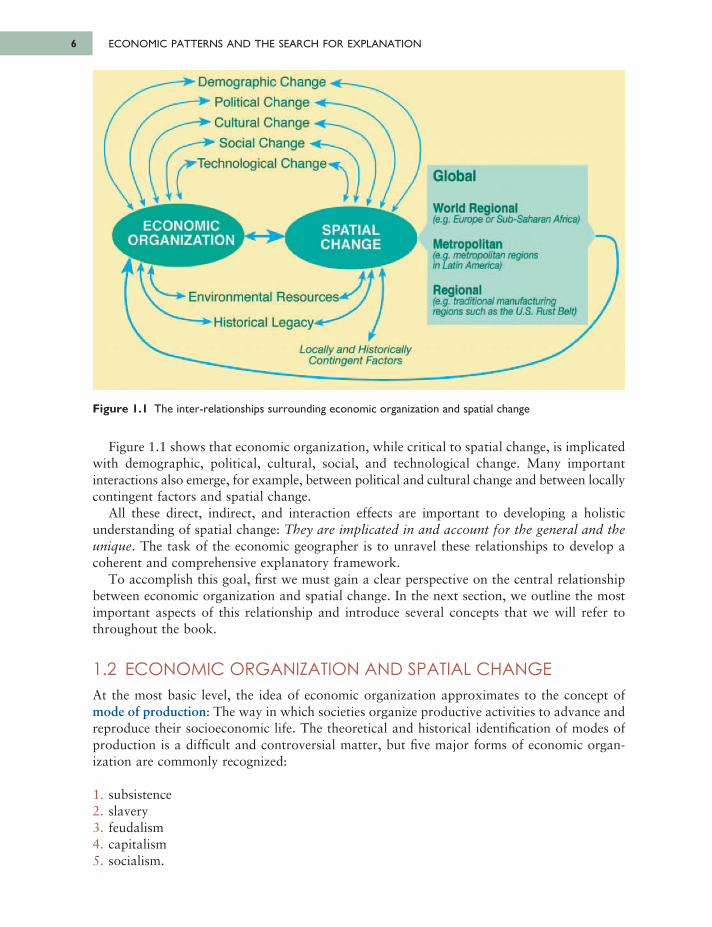

Figure 1.1 shows that economic organization, while critical to spatial change, is implicatedwith demographic, political, cultural, social, and technological change. Many importantinteractions also emerge, for example, between political and cultural change and between locallycontingent factors and spatial change.

All these direct, indirect, and interaction effects are important to developing a holisticunderstanding of spatial change: They are implicated in and account for the general and theunique. The task of the economic geographer is to unravel these relationships to develop acoherent and comprehensive explanatory framework.

To accomplish this goal, first we must gain a clear perspective on the central relationshipbetween economic organization and spatial change. In the next section, we outline the mostimportant aspects of this relationship and introduce several concepts that we will refer tothroughout the book.

1.2 ECONOMIC ORGANIZATION AND SPATIAL CHANGEAt the most basic level, the idea of economic organization approximates to the concept ofmode of production: The way in which societies organize productive activities to advance andreproduce their socioeconomic life. The theoretical and historical identification of modes ofproduction is a difficult and controversial matter, but five major forms of economic organ -ization are commonly recognized:

1. subsistence2. slavery3. feudalism4. capitalism5. socialism.

ECONOMIC PATTERNS AND THE SEARCH FOR EXPLANATION6

Figure 1.1 The inter-relationships surrounding economic organization and spatial change

6063 GEOGRAPHY WORLD ECON_PT_246x189 mm 22/01/2014 15:09 Page 6

Demographic ChangePolitical ChangeCultural ChangeSocial Change ·

Technological Change

SPATIALCHANGE

Global

World Regional(e.g. Europe or Sub-Saharan Africa)

Metropolitan(e.g. metropolitan regions in Latin America)

Regional(e.g. traditional manufacturing regions such as the U.S. Rust Belt)

ECONOMIC ORGANIZATIOr*

* Environmental Resources-

-Historical Legacy

Locally and Historically Contingent Factors

These broad categories also can be broken down into more specific forms of economicorganization. For example, scholars have often found it useful to differentiate betweenmerchant capitalism (or mercantilism), industrial (or competitive) capitalism, organizedcapitalism, and advanced (or globalized) capitalism.

What distinguishes these forms of economic organization are differences in the relationshipsbetween the factors of production such as land and other natural resources, labor, andphysical and human capital. Under slavery, for example, the laborer is private property andmay be bought and sold similar to any other instrument of production. Under feudalism (orrank redistribution), peasant laborers are legally tied to specific tracts of land. They may ownsome of the instruments of production, but the land and a percentage of the product of theirlabor is the property of the feudal lord. Under capitalism, the laborers own no instrumentsof production, but they are free to sell their labor power.

Different forms of economic organization are also characterized by different forces ofproduction (for example, technology, machinery, means of transportation) and social forma -tions (with specific proportions of participants from various social classes).

The economic “logic” of these different forms of economic organization results in sub -stantially different forms of spatial organization. Where feudalism translates into a patchworkof self-sufficient domains with little trade and, therefore, few market centers, merchantcapitalism requires a highly developed system of market towns and an inherent tendency tocolonize new territories to amass the wealth and resources necessary to sustain ever expandingmarkets.

In contrast to feudalism and mercantilism, industrial capitalism requires spatial restructuringthat enables the exploitation of new energy sources, development of increasingly efficientproduction techniques, and the adoption of new forms of corporate organization. Mining andmanufacturing towns appear, and whole regions, such as the manufacturing cities around theGreat Lakes or the Ruhr region of Germany, become specialized in certain kinds of industrialproduction.

The “classic” sequence of transformation from one form of economic organization to anotherruns from subsistence economies through slavery, feudalism, mercantilism, industrial capital -ism, and advanced capitalism.

This sequence is also distinctly European. The rise of capitalism in much of Europe andthe subsequent drive to acquire resources to propel economic growth led to different sequences of development in other regions. In North America, capitalism was imposed directly on the subsistence economies of Native American communities. In Japan, feudalismwas uprooted suddenly by state-sponsored industrial capitalism. In Russia, an embryonicindustrial capitalism was displaced by a socialism that soon gave way to state capitalism. Today,in many lesser developed countries, aspects of multiple forms of economic organization may also coexist. As a result of these variations, important regional differences have emergedin the world economy.

Spatial change and further regional differentiation also occurs with the evolution of formsof economic organization. So a regional agricultural landscape must be seen as one of a numberof possible realizations rather than a straightforward reflection of a particular form of eco -nomic organization. Each economic landscape should be interpreted, therefore, as the productof broad economic forces interacting with local social, cultural, political, and environmentalfactors: A product of the general and the unique.

1. THE CHANGING WORLD ECONOMY 7

6063 GEOGRAPHY WORLD ECON_PT_246x189 mm 22/01/2014 15:09 Page 7

ECONOMIC PATTERNS AND THE SEARCH FOR EXPLANATION8

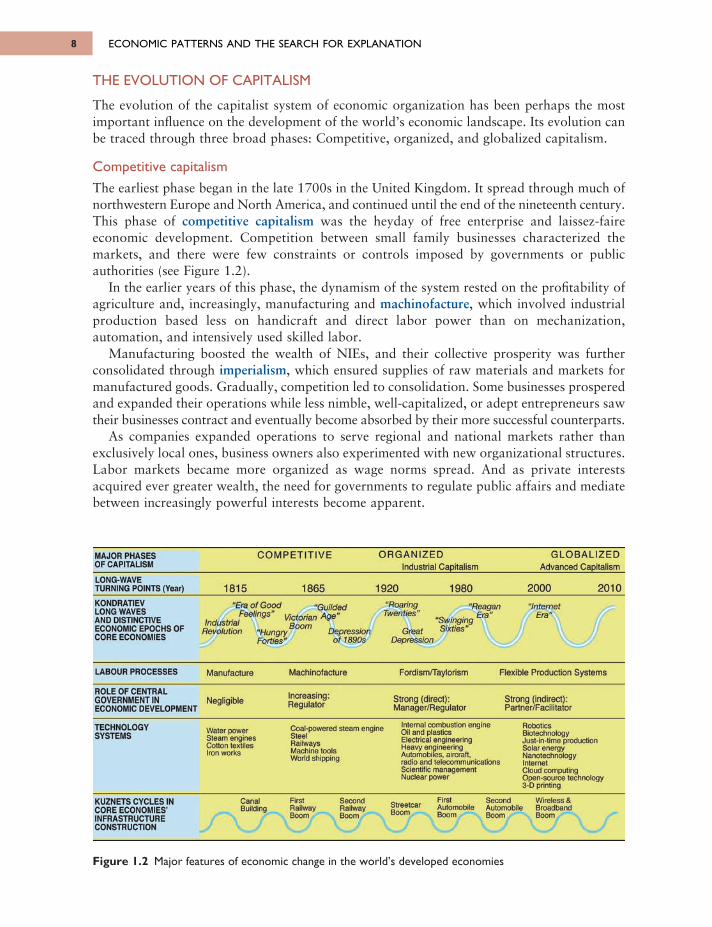

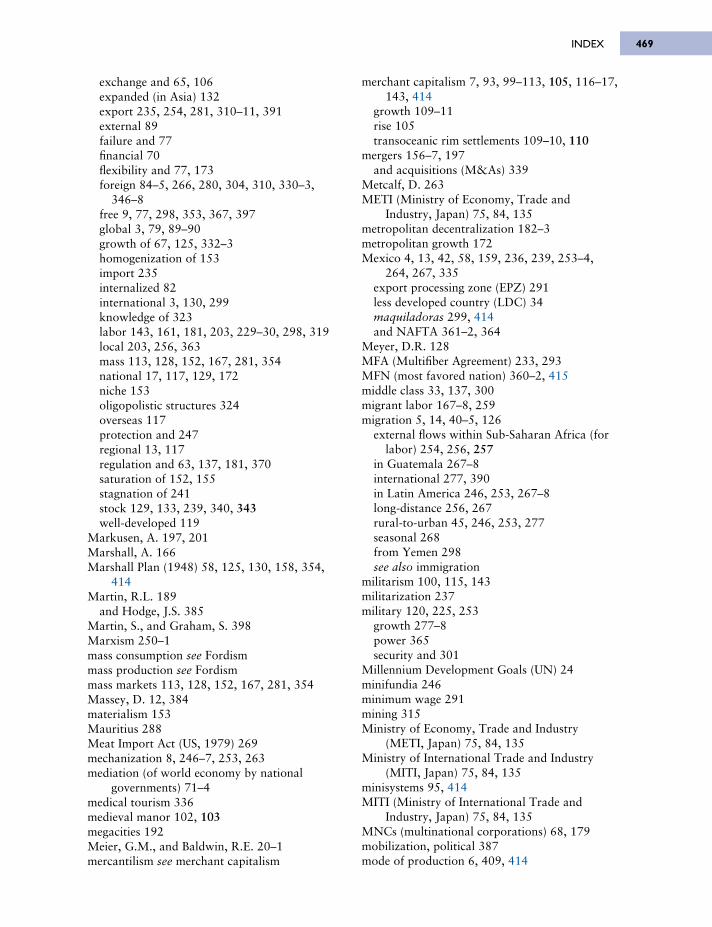

THE EVOLUTION OF CAPITALISM

The evolution of the capitalist system of economic organization has been perhaps the mostimportant influence on the development of the world’s economic landscape. Its evolution canbe traced through three broad phases: Competitive, organized, and globalized capitalism.

Competitive capitalismThe earliest phase began in the late 1700s in the United Kingdom. It spread through much ofnorthwestern Europe and North America, and continued until the end of the nineteenth century.This phase of competitive capitalism was the heyday of free enterprise and laissez-faireeconomic development. Competition between small family businesses characterized themarkets, and there were few constraints or controls imposed by governments or publicauthorities (see Figure 1.2).

In the earlier years of this phase, the dynamism of the system rested on the profitability ofagriculture and, increasingly, manufacturing and machinofacture, which involved industrialproduction based less on handicraft and direct labor power than on mechanization,automation, and intensively used skilled labor.

Manufacturing boosted the wealth of NIEs, and their collective prosperity was furtherconsolidated through imperialism, which ensured supplies of raw materials and markets formanufactured goods. Gradually, competition led to consolidation. Some businesses prosperedand expanded their operations while less nimble, well-capitalized, or adept entrepreneurs sawtheir businesses contract and eventually become absorbed by their more successful counterparts.

As companies expanded operations to serve regional and national markets rather thanexclusively local ones, business owners also experimented with new organizational structures.Labor markets became more organized as wage norms spread. And as private interestsacquired ever greater wealth, the need for governments to regulate public affairs and mediatebetween increasingly powerful interests become apparent.

Figure 1.2 Major features of economic change in the world’s developed economies

6063 GEOGRAPHY WORLD ECON_PT_246x189 mm 22/01/2014 15:09 Page 8

MAJOR PHASES OF CAPITALISM

LONG-WAVE TURNING POINTS (Year)

C O M P E T IT IV E O R G A N IZ E DIndustrial Capitalism

G L O B A L IZ E DAdvanced Capitalism

1815 1865 1920 1980 2000 2010“Era o f Good

Feelings" VictorianBoomIndustria l

Revolution "HungryForties"

"G uilded n A g e "

Depression o f 1890s

“Roaring Twenties"

GreatDepression

“Sw inging Sixties"

"Reagan6 . ·

“Internet Era"

KONDRATIEV LONG WAVES AND DISTINCTIVE ECONOMIC EPOCHS OF CORE ECONOMIES

LABOUR PROCESSES

ROLE OF CENTRAL GOVERNMENT IN ECONOMIC DEVELOPMENT

TECHNOLOGYSYSTEMS

Manufacture

Negligible

M achinofacture FordisnVTaytorism Flexible Production Systems

Strong (indirect): Partner/Facilitatoi

Strong (direct): Manager/Regulator

Increasing:Regulator

Water power Steam engines Cotton textiles Iron works

Coal-powered steam engineSteelRailwaysMachine toolsWorld shipping

Internal combustion engine Oil and plastics Electrical engineering Heavy engineering Automobiles, aircraft, radio and telecommunications Scientific management Nudear power

Robotics Biotechnology Just-in-time production Solar energy Nanotechnology InternetCloud computing Open-source technology 3-D printing

CanalBuilding

FirstRailwayBoom

SecondRailwayBoom

StreetcarBoom

FirstAutomobileBoom

SecondAutomobileBoom

Wireless S Broad barn Boom

KUZNETS CYCLES IN CORE ECONOMIES’ INFRASTRUCTURE CONSTRUCTION

Near the end of this phase of capitalism, the United States also surpassed the United Kingdomas the leading industrial economy.

Organized capitalism

By the early 1900s these trends had altered the nature of the capitalist enterprise so significantlythat a new phase—organized capitalism—was demarcated.

In the early decades of the twentieth century, profitability became increasingly dependenton new labor processes. Fordism, named after the automobile manufacturer Henry Ford,ushered in the era of mass production using assembly-line techniques. Frederick Winslow Taylor,an engineer and early critic of Fordism, also outlined the principles of scientific management(often known as Taylorism) which became central to the efficiency movement inmanufacturing.

During this period, mass production lowered the costs of many goods, and higher wagesand sophisticated advertising techniques fuelled mass consumption. In turn, mass consumptionand production initiated the race to find ever more efficient production processes and untappedmarkets.

A hallmark of this period was the emergence of a workable relationship between businessinterests and labor unions. Unions had grown in size and strength in the progressive era, andconstituted another increasingly important element of “organization.” Government alsoexpanded the scope of its activities in part to mediate the relationship between organizedbusiness and labor.

The market failures that triggered the Great Depression of 1929–1934 undermined thelegitimacy of classical economic liberalism and led to its eclipse in the New Deal era by anegalitarian liberalism that relied on the state to manage economic development and soften theunwanted side-effects of free market capitalism.

In this expanded role, government assumed responsibility for the management of thenational economy and the organization of various dimensions of social well-being. This typeof economic policy, which seeks to mitigate the deleterious effects of private market activityin aggregate through active fiscal and monetary policy, is known as Keynesianism after theeminent economist John Maynard Keynes.

Globalized capitalism

After the Second World War, another important transformation in the nature of capitalismbegan to take place and led to a third major phase: Advanced or globalized capitalism.

This period is characterized by a shift away from industrial production and toward services,particularly sophisticated financial and business services, as the basis for profitability withinthe more developed economies. Labor-intensive manufacturing declined althoughmanufacturing production continued to expand in these countries as sophisticated, technology-intensive manufacturing processes gained prominence.

The globalizing of the economy also meant that large transnational corporations (TNCs)were able to outmaneuver the national scope of governments and labor unions and contributedto a destabilization of the “organized” relationship between business, labor, and government.By the mid-1990s, the world’s largest TNCs accounted for two-thirds of international trade,and the largest ten reported total income that exceeded that of the world’s 100 poorest countries.

Meanwhile, Fordism became a victim of its own success as many markets were saturatedwith low-cost goods. As profit margins in conventional markets narrowed, many enterpriseschased revenues by catering to specialized market niches. Such specialization required flexibleproduction systems. The overall result has sometimes been labeled disorganized capitalism for

1. THE CHANGING WORLD ECONOMY 9

6063 GEOGRAPHY WORLD ECON_PT_246x189 mm 22/01/2014 15:09 Page 9

its distinct contrast to the orderly interdependence of business, labor, and government in thesystem of organized capitalism.

One of the driving forces behind growth during this phase of capitalism has been the global information (or knowledge) economy, a form of production and management whereproductivity and competitiveness rely heavily on knowledge generation and on gaining accessto and the rapid assimilation of new information.

A second critical driver of this era has been the ubiquity of high technology. In particular,the Internet has affected nearly every facet of the economy and sparked disruptive innovationthat has radically altered the dynamics of marketplaces and industries such as news and media,music, publishing, and advertising. Although the first phase of euphoric investment in Internettechnologies culminated in the bursting of the dot.com bubble in 2000, from its ashes emergeda number of robust and dynamic businesses such as Google, eBay, and Amazon.com thatcontinue to transform the economic landscape. With the expansion of broadband and wirelesstechnologies, cloud-computing, open source development tools, and the advent of Web 2.0,numerous platform technologies and social media enterprises such as YouTube, Twitter,Facebook, Flickr, and WordPress continue to change how people, companies, and institutionscollaborate, communicate, and compete with each other.

There is some question, however, about the sustainability of technological change as a driverof economic growth. We may have reached a technological plateau in which we continue toexploit yesterday’s ideas rather than develop new ones. For example, 80 percent of total growthin U.S. GDP between 1950 and 1993 came from the application of previously discovered ideasplus huge investments in education and scientific research that cannot be easily repeated inthe future. The overall rate of innovation from medieval times to the present peaked in thenineteenth century and has gone downhill since. So, we should be careful not to presume thatsomehow technological change will necessarily continue to endlessly create more growth.

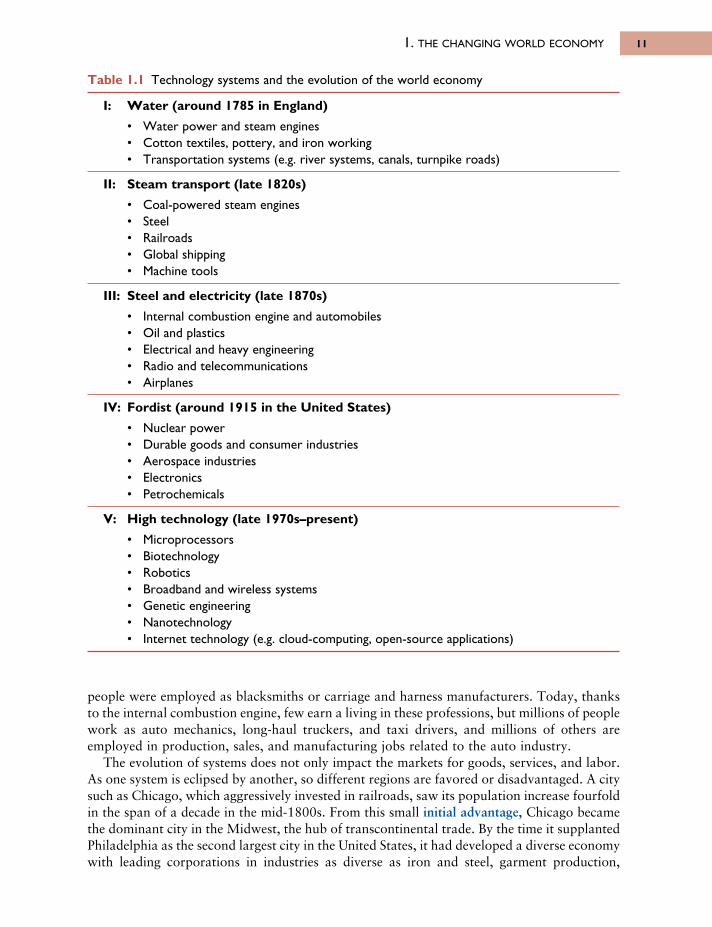

TECHNOLOGY AND ECONOMIC DEVELOPMENT

The opening up of new markets, foreign or domestic, and the organizational development fromthe craft shop and factory to such concerns as U.S. Steel illustrate the same process of industrialmutation . . . that incessantly revolutionizes the economic structure from within, incessantlydestroying the old one, incessantly creating a new one. This process of Creative Destruction is theessential fact about capitalism.

(Schumpeter, 2010/1943: 73)

Coined by the Austrian economist Joseph A. Schumpeter, the term creative destructioncaptures the essence of the capitalism system—the relentless drive to innovate in the competitionfor markets—perhaps better than any other concept.

Creative destruction is at the heart of the broad structural shifts that occur in thedevelopment of technology systems (see Table 1.1). The transportation system providesperhaps the starkest example of creative destruction at work. With each advancement newmarkets opened, industries developed, and cities were built, but not without costs. Therailroads that opened the West in the United States also effectively closed the canal systemsthat had been built in the previous decades.

Technologies also destroy old jobs even as they create new ones. Typically, more primitivetechnologies are associated with higher levels of labor inputs than are more sophisticated ones.So as technology has become more central to economic development, employment, particularlyin limited or semi-skilled jobs, has suffered. The newest technologies today require “leaner”and more skilled labor than did the older ones. By way of example, in 1900 nearly 350,000

ECONOMIC PATTERNS AND THE SEARCH FOR EXPLANATION10

6063 GEOGRAPHY WORLD ECON_PT_246x189 mm 22/01/2014 15:09 Page 10

people were employed as blacksmiths or carriage and harness manufacturers. Today, thanksto the internal combustion engine, few earn a living in these professions, but millions of peoplework as auto mechanics, long-haul truckers, and taxi drivers, and millions of others areemployed in production, sales, and manufacturing jobs related to the auto industry.

The evolution of systems does not only impact the markets for goods, services, and labor.As one system is eclipsed by another, so different regions are favored or disadvantaged. A citysuch as Chicago, which aggressively invested in railroads, saw its population increase fourfoldin the span of a decade in the mid-1800s. From this small initial advantage, Chicago becamethe dominant city in the Midwest, the hub of transcontinental trade. By the time it supplantedPhiladelphia as the second largest city in the United States, it had developed a diverse economywith leading corporations in industries as diverse as iron and steel, garment production,

1. THE CHANGING WORLD ECONOMY 11

Table 1.1 Technology systems and the evolution of the world economy

I: Water (around 1785 in England)

• Water power and steam engines• Cotton textiles, pottery, and iron working• Transportation systems (e.g. river systems, canals, turnpike roads)

II: Steam transport (late 1820s)

• Coal-powered steam engines• Steel• Railroads• Global shipping• Machine tools

III: Steel and electricity (late 1870s)

• Internal combustion engine and automobiles• Oil and plastics• Electrical and heavy engineering• Radio and telecommunications• Airplanes

IV: Fordist (around 1915 in the United States)

• Nuclear power• Durable goods and consumer industries• Aerospace industries• Electronics• Petrochemicals

V: High technology (late 1970s–present)

• Microprocessors• Biotechnology• Robotics• Broadband and wireless systems• Genetic engineering• Nanotechnology• Internet technology (e.g. cloud-computing, open-source applications)

6063 GEOGRAPHY WORLD ECON_PT_246x189 mm 22/01/2014 15:09 Page 11

publishing, banking, insurance, and mail-order retail. During this rapid period of growth, italso surpassed older and initially larger cities such as St. Louis, which depended on and wereinvested in steamboat commerce.

As this example illustrates, changes in technology are crucial to understanding the geo -graphical path dependence of economic activities, that is, the historical relationship betweenpresent economic activities associated with a place and its past experience. As new technologieseclipse old ones, industries—and sometimes entire industrial regions—are “dismantled” (or,at least, neglected) as investors shift capital to fund the creation of new centers of profitabilityand employment.

1.3 SPATIAL DIVISIONS OF LABORThe evolution of capitalism has also brought about changes in the spatial division of labor.The division of labor within and between firms and over space is not fixed; rather, it respondsto changes in the historical-structural context in which firms operate.

For example, during the Fordist period in countries such as Britain and the United States,the basic division of labor was organized primarily within regional parts of the nationaleconomy. Plant, firm, and industry were national phenomena. They were organized aroundnational markets and industries, and they created national social (class) divisions. Althoughcapital, labor, and technology were often imported and exported, these factors of productionwere subject to intensive regulation by national governments.

The internal geography of a national economy such as Britain’s reflected its position in theinternational division of labor. In the 1930s Britain specialized in certain key manufacturingindustries such as coalmining, iron and steel manufacturing, and shipbuilding. Previousinvestments in these industries and the increasing returns to scale and external economies ofscale they generated defined Britain’s trading patterns. Elsewhere, different industries, oftennewer, mass-production ones based on larger firms, also took root. As a result, trade reflectedcumulative competitive advantages in sectors where each had a “head start.”

The locational consequences in the British case are laid out by Massey (1984: 28–29) asfollows:

It was the United Kingdom’s position as an imperial power, its early lead in the growth of modern industry, and its consequent commitment to free trade and its own specialization inmanufacturing within this international division of labor, which enabled the rapid growth, up to the First World War, of these major exporting industries. The spatial structures that wereestablished by those industries were those where all the stages of production of the commodityare concentrated within single geographical areas. The comparatively low level of separation offunctions within the process of production, and the relatively small variation in locationalrequirements between such potentially separable functions, were not sufficient to make geographicaldifferentiation a major attraction.

In other words, the spatial division of labor of key industries within national economies wasbased largely on different regional industrial specializations. And agglomeration was a majorfeature of economic organization across a number of manufacturing industries.

Similarly, in the United States during this period, the northeast contained a vast array ofspecialized manufacturing clusters—steel in Pittsburgh, automobiles in Detroit, chemicals inWilmington, and photographic equipment in Rochester—as well as regional areas of special -ization in agricultural (for example, tomatoes and sweet corn in the Garden State of NewJersey, low-bush blueberries in Maine, maple syrup in Vermont), and raw materials (for

ECONOMIC PATTERNS AND THE SEARCH FOR EXPLANATION12

6063 GEOGRAPHY WORLD ECON_PT_246x189 mm 22/01/2014 15:09 Page 12

1. THE CHANGING WORLD ECONOMY 13

example, stone quarries in the “granite state” of New Hampshire). In this respect, places andregions could readily be associated with specific products.

GLOBALIZATION AND CHANGING SPATIAL DIVISIONS OF LABOR

Under the conditions of flexible production, such regional specialization has been challengedand undermined to a considerable degree. Spatial divisions of labor are now structured in avariety of ways depending on the needs and characteristics of particular industries. In additionto (1) regional specialization and (2) regional dispersal (which has characterized consumerservices such as stores, restaurants, and hospitals, and some manufacturing industries such asshoe production and food processing), four additional spatial divisions of labor can beidentified:

1. Three-tier regional functional separationa. management and research activities in major metropolitan regionsb. skilled labor in “old” manufacturing areasc. unskilled labor in regional peripheries (to exploit lower wages and non-unionized labor

forces).2. Two-tier regional functional separation

a. management and research activities in major metropolitan regionsb. semi-skilled and unskilled labor in regional peripheries.

3. Regional and global functional separationa. management, research, and skilled labor in advanced industrial regionsb. unskilled labor in the global periphery.

4. Divisions by areas of growth and declinea. some areas characterized by investment, technical change, and job expansionb. other areas characterized by stagnant and progressively less competitive production and

job loss.

These new spatial divisions of labor have been possible because transportation andcommunications technologies have created an environment in which firms can decentralizeactivities associated with primary production yet maintain central control. A firm can remainheadquartered in New York, Zürich, or Hamburg, but locate manufacturing facilities in alocation such as Chennai, India, or the Monterrey-Nuevo Laredo corridor in Mexico and reapthe benefits of non-union labor forces, easier access to concentrated regional markets, andfavorable regulatory environments.

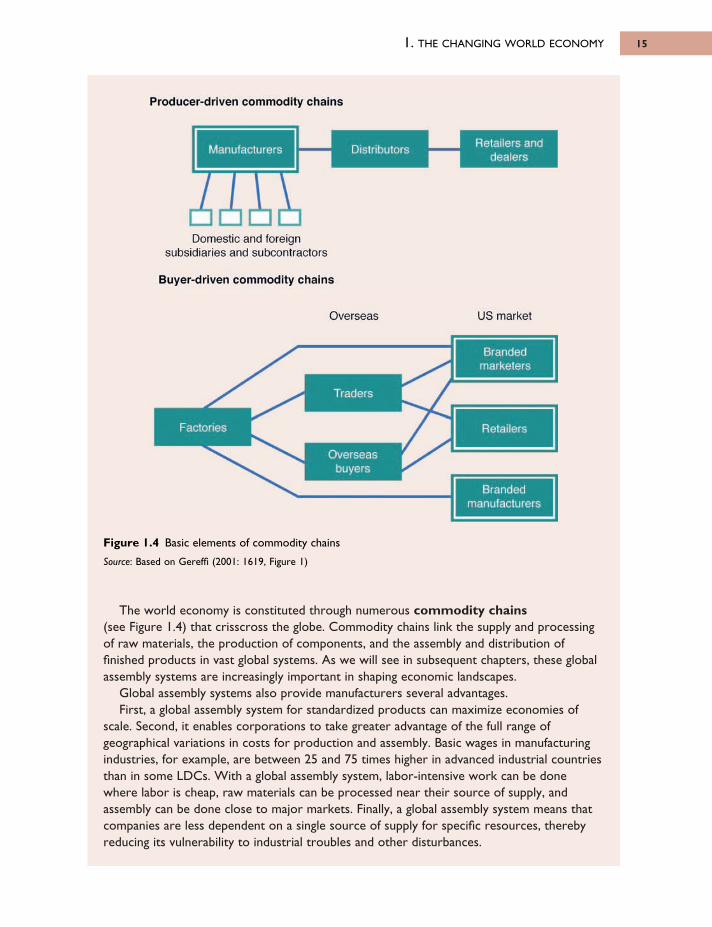

Under this new international division of labor (NIDL), investment and production are nolonger organized primarily around national economies. The process of production—mostobviously in the examples of the automobile, electronics, and software industries—is now global.Components or specific services are sourced from multiple suppliers in different countries andassembled in several locations (see Box 1.1).

In fact, many products no longer have any obvious nationality. It is difficult to distinguishsome “U.S.” from some “Japanese” cars, for example, now that U.S. car companies importvehicles under “their” names from Japan, and Japanese companies now manufacture cars inthe United States (for example, Honda in Marysville, Ohio, and Toyota in Blue Springs,Mississippi). Even manufacturing the Barbie doll, an all-American icon, includes operationsin a number of countries (see Box 1.2).

6063 GEOGRAPHY WORLD ECON_PT_246x189 mm 22/01/2014 15:09 Page 13

ECONOMIC PATTERNS AND THE SEARCH FOR EXPLANATION14

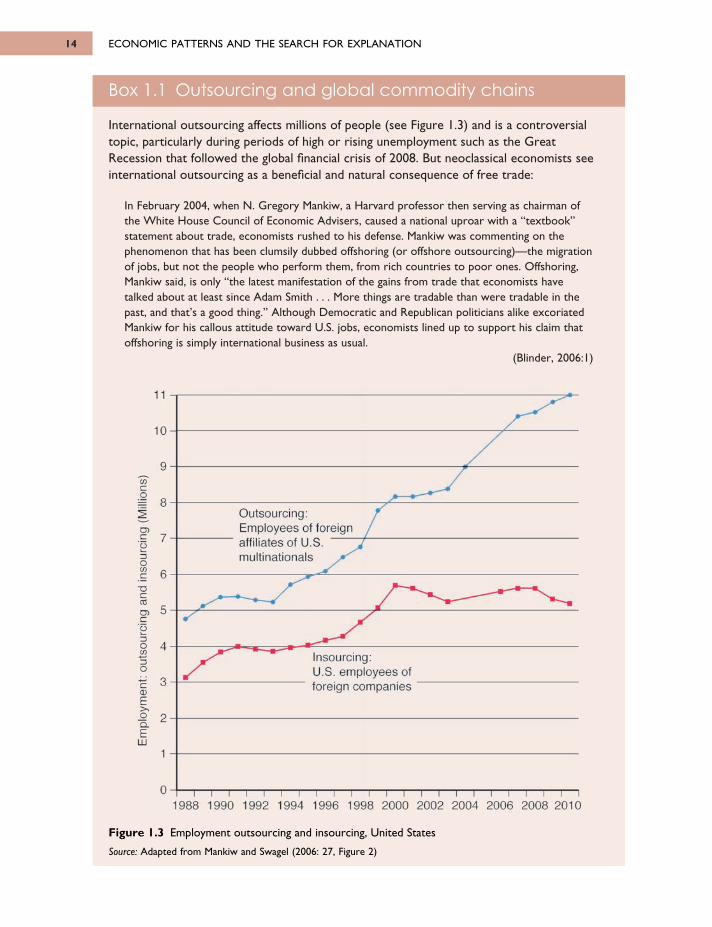

Box 1.1 Outsourcing and global commodity chains

International outsourcing affects millions of people (see Figure 1.3) and is a controversialtopic, particularly during periods of high or rising unemployment such as the GreatRecession that followed the global financial crisis of 2008. But neoclassical economists seeinternational outsourcing as a beneficial and natural consequence of free trade:

In February 2004, when N. Gregory Mankiw, a Harvard professor then serving as chairman ofthe White House Council of Economic Advisers, caused a national uproar with a “textbook”statement about trade, economists rushed to his defense. Mankiw was commenting on thephenomenon that has been clumsily dubbed offshoring (or offshore outsourcing)—the migrationof jobs, but not the people who perform them, from rich countries to poor ones. Offshoring,Mankiw said, is only “the latest manifestation of the gains from trade that economists havetalked about at least since Adam Smith . . . More things are tradable than were tradable in thepast, and that’s a good thing.” Although Democratic and Republican politicians alike excoriatedMankiw for his callous attitude toward U.S. jobs, economists lined up to support his claim thatoffshoring is simply international business as usual.

(Blinder, 2006:1)

Figure 1.3 Employment outsourcing and insourcing, United States

Source: Adapted from Mankiw and Swagel (2006: 27, Figure 2)

6063 GEOGRAPHY WORLD ECON_PT_246x189 mm 22/01/2014 15:09 Page 14

Outsourcing: Employees of foreign affiliates of U.S. multinationals У '

9

8

7

6

5

4

3

2

1

0

1

0

1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

Insourcing:U.S. employees of

" foreign companies "

(Лc0

1

O)coDoωc

~ocCO

U)cok.3oCO

Doc<D

E> .oCL

Eш

1. THE CHANGING WORLD ECONOMY 15

The world economy is constituted through numerous commodity chains(see Figure 1.4) that crisscross the globe. Commodity chains link the supply and processingof raw materials, the production of components, and the assembly and distribution offinished products in vast global systems. As we will see in subsequent chapters, these globalassembly systems are increasingly important in shaping economic landscapes.

Global assembly systems also provide manufacturers several advantages.First, a global assembly system for standardized products can maximize economies of

scale. Second, it enables corporations to take greater advantage of the full range ofgeographical variations in costs for production and assembly. Basic wages in manufacturingindustries, for example, are between 25 and 75 times higher in advanced industrial countriesthan in some LDCs. With a global assembly system, labor-intensive work can be donewhere labor is cheap, raw materials can be processed near their source of supply, andassembly can be done close to major markets. Finally, a global assembly system means thatcompanies are less dependent on a single source of supply for specific resources, therebyreducing its vulnerability to industrial troubles and other disturbances.

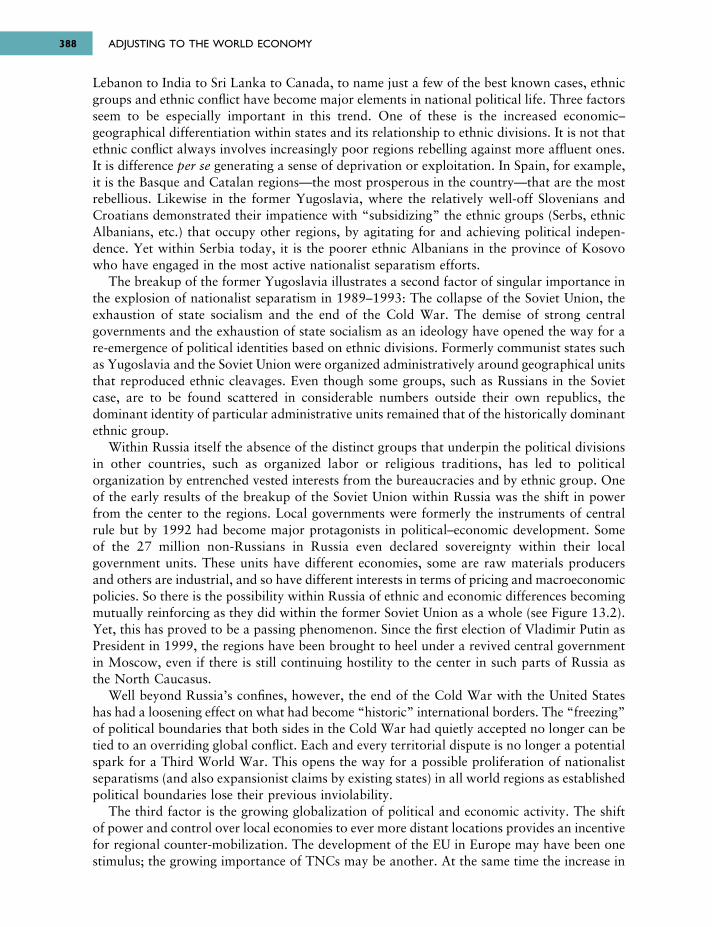

Figure 1.4 Basic elements of commodity chains

Source: Based on Gereffi (2001: 1619, Figure 1)

6063 GEOGRAPHY WORLD ECON_PT_246x189 mm 22/01/2014 15:09 Page 15

Manufacturers Distributors Retailers and dealers

Domestic and foreign subsidiaries and subcontractors

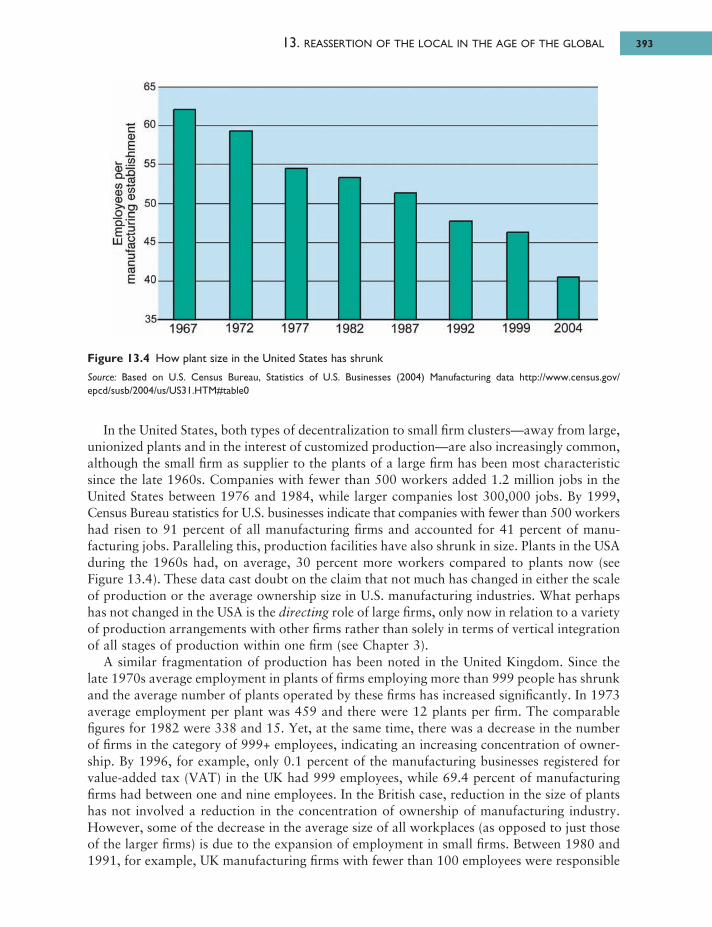

Overseas US market

Traders

Factories

Overseasbuyers

Brandedmarketers

Retailers

Brandedmanufacturers

Producer-driven commodity chains

Buver-driven commoditv chains

Producer-driven commodity chains

Buver-driven commoditv chains

ECONOMIC PATTERNS AND THE SEARCH FOR EXPLANATION16

Box 1.2 Barbie: American icon and global product

The famous (and impossible) physique of the Barbie doll says “Made in America” but thebox it comes in says “Made in China.” Tracing Barbie’s production path raises interestingquestions about how its place of origin can be identified and how the globalization ofproduction ties together disparate locations in the world economic core and the periphery(a topic that will also be covered in greater detail in the next chapter).

Although Barbie is an American icon and a team of over 100 designers, beauticians,tailors, and sculptors at the headquarters of Mattel Corporation in El Segundo, Californiacollaborate on her spring, fall, and holiday collections every year, Barbie has never beenmade in the United States. The first doll was produced in Japan in 1959. As costs rose inJapan, production was moved to other sites in Asia including Taiwan, Hong Kong, and thePhilippines. Following a strike in 1988, Mattel closed its two Philippine factories resulting inthe loss of 4,000 jobs.

Mattel closely guards its proprietary manufacturing process; however, in 1996 Los AngelesTimes staff reporter, Rone Tempest, did some sleuthing and discovered the following aboutBarbie: She is made from ethylene, refined oil imported from Saudi Arabia, which is turnedinto pellets by a firm in Taiwan. Barbie’s nylon hair comes from Japan. Her cardboardpackaging is made in the United States. The manufacturing and packaging is managed fromHong Kong.

The production story begins, however, in Mattel’s commodity management center whereinformation about commodity prices and wage rates is used to decide on the best locationsto buy the plastic resins, the cloth, the paper and other materials, and bring them togetherat a final point of assembly.

At one time, Japan and Taiwan were the main toymakers to the world economy. As their economies diversified into more capital-intensive production, they became thesuppliers of the plastics that previously had come from the United States and Europe. At that time, production shifted to lower wage sites such as China, Thailand, and Indonesia(Foek, 1997).

Making Barbie is extremely labor intensive. Workers must operate plastic molds, sewclothing, and paint the details on the dolls. A typical Barbie requires 15 separate paintstations. Machines cannot perform these tasks. So the two Barbie plants in China employabout 11,000 workers, mainly unmarried women between 18 and 23 from poor regions of interior China brought to work at the factories for two to five years (Tempest, 1996).

So, Barbie is made in China. In the trade ledgers—where country trade deficits andsurpluses are defined—Barbie is one of its exports. But a number of firms in differentcountries contributed to its production and reaped profits from the final product. Tempest estimated that Chinese firms and workers obtained only about 35 cents out of the $2 export value placed on each doll. In contrast, Barbie retails in the U.S. for$12–18.

In recent years, global sales for Barbie have fluctuated somewhat. Nevertheless, Barbiecontinues to account for $3 billion annually in retail sales for Mattel, and the secondarymarket for all things Barbie remains hotter than her “Barbie pink” toenail polish.

6063 GEOGRAPHY WORLD ECON_PT_246x189 mm 22/01/2014 15:09 Page 16

1. THE CHANGING WORLD ECONOMY 17

For many transnational corporations, national markets for capital, labor, and plant andoffice location exist only as parts of global commodity chains. Even small firms now have theopportunity to operate globally, outsourcing web development and design, production andpackaging, customer service, and nearly any other facet of its business while competing forcustomers in local, regional, and global markets. So these “new” conditions cannot be solelyidentified with multinational corporations.

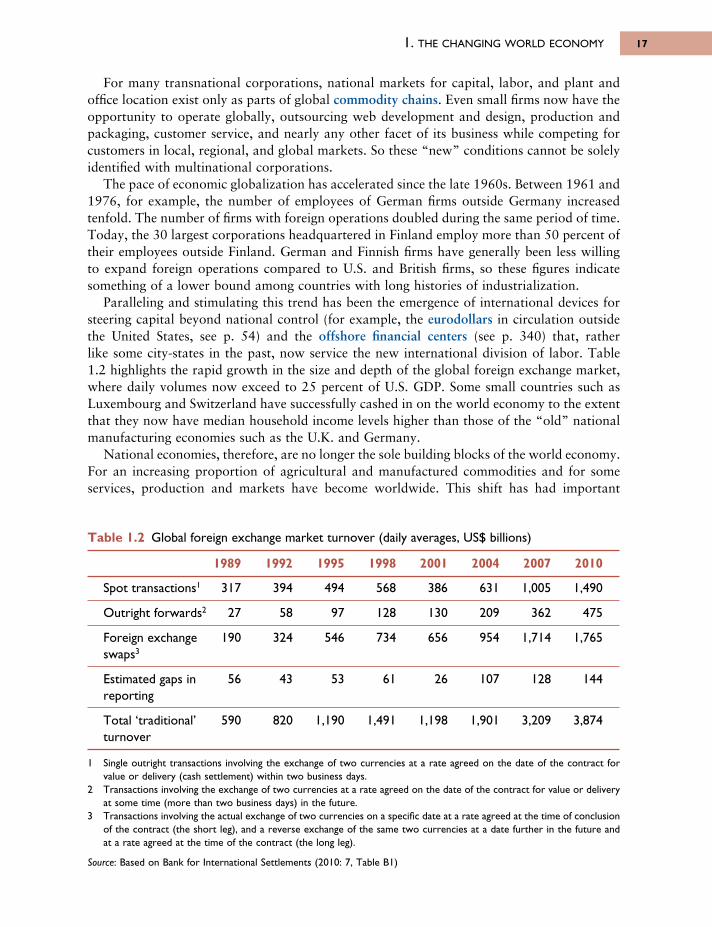

The pace of economic globalization has accelerated since the late 1960s. Between 1961 and1976, for example, the number of employees of German firms outside Germany increasedtenfold. The number of firms with foreign operations doubled during the same period of time.Today, the 30 largest corporations headquartered in Finland employ more than 50 percent oftheir employees outside Finland. German and Finnish firms have generally been less willingto expand foreign operations compared to U.S. and British firms, so these figures indicatesomething of a lower bound among countries with long histories of industrialization.

Paralleling and stimulating this trend has been the emergence of international devices forsteering capital beyond national control (for example, the eurodollars in circulation outsidethe United States, see p. 54) and the offshore financial centers (see p. 340) that, rather like some city-states in the past, now service the new international division of labor. Table1.2 highlights the rapid growth in the size and depth of the global foreign exchange market,where daily volumes now exceed to 25 percent of U.S. GDP. Some small countries such asLuxembourg and Switzerland have successfully cashed in on the world economy to the extentthat they now have median household income levels higher than those of the “old” nationalmanufacturing economies such as the U.K. and Germany.

National economies, therefore, are no longer the sole building blocks of the world economy.For an increasing proportion of agricultural and manufactured commodities and for someservices, production and markets have become worldwide. This shift has had important

Table 1.2 Global foreign exchange market turnover (daily averages, US$ billions)

1989 1992 1995 1998 2001 2004 2007 2010

Spot transactions1 317 394 494 568 386 631 1,005 1,490

Outright forwards2 27 58 97 128 130 209 362 475

Foreign exchange 190 324 546 734 656 954 1,714 1,765swaps3

Estimated gaps in 56 43 53 61 26 107 128 144reporting

Total ‘traditional’ 590 820 1,190 1,491 1,198 1,901 3,209 3,874turnover

1 Single outright transactions involving the exchange of two currencies at a rate agreed on the date of the contract forvalue or delivery (cash settlement) within two business days.

2 Transactions involving the exchange of two currencies at a rate agreed on the date of the contract for value or deliveryat some time (more than two business days) in the future.

3 Transactions involving the actual exchange of two currencies on a specific date at a rate agreed at the time of conclusionof the contract (the short leg), and a reverse exchange of the same two currencies at a date further in the future andat a rate agreed at the time of the contract (the long leg).

Source: Based on Bank for International Settlements (2010: 7, Table B1)

6063 GEOGRAPHY WORLD ECON_PT_246x189 mm 22/01/2014 15:09 Page 17

consequences for the spatial distribution of economic activities both globally and withincountries.

Globally, it has given rise to the growth of newly industrializing economies such as SouthKorea and Brazil. It has also contributed to a significant polarization of income and wealth.According to the World Bank (2010), the average per capita income in the richest 20 countriesis 47 times that of the poorest 20. Within the “core” of advanced industrial national economies,the new international division of labor has led to a reorientation in employment away frommanufacturing to services and a massive restructuring of regional economies. In Britain, forexample, three sorts of local area have fallen victim to the loss of traditional manufacturingindustries and the failure of new ones to replace them:

1. the centers of nineteenth-century industrialization in the north of England, south Wales,and central Scotland

2. the inner cities of London and other large metropolitan areas with concentrations of poorpeople and few of the unskilled jobs that they used to fill

3. the centers of the growth industries (specifically vehicles and engineering) of the 1950s and1960s in the West Midlands and northwest of England.

We will draw on this framework throughout the remainder of the book as we analyze anddescribe the geography of the world economy. In the next chapter, we establish the majordimensions of the contemporary economic landscapes within the world economy. In Chapter3, we outline a comprehensive global historical framework that serves as the context for therest of the book.

In Part 2, we trace the emergence of three of the world’s core economies—Europe, NorthAmerica and Japan—and follow their paths towards increasing scale and complexity. Part 3focuses on the rest of the world and pays special attention to the spatial transformations thathave occurred as a consequence of colonialism and global capitalism that emanated from thecore economies as well as the role of agriculture and manufacturing industries in economicdevelopment and spatial change.

Finally, in Part 4, we examine some of the reactions to the emergence of ever larger andmore powerful economic forces that have come to characterize the world economy. Inparticular, we describe the spatial consequences of transnational political and economicintegration and decentralist reactions: Nationalism, regionalism, and grassroots movementstowards economic democracy.

SUMMARYIn this introductory chapter, we provided the orientation for the book by outlining therelationships between the organization of the world economy and spatial change. We stressedhow studying the world economy involves developing an understanding of the generaleconomic forces and socioeconomic relationships within the world economy and of the uniquefeatures that represent local and historical variability. We introduced the interrelated conceptsof economic organization and spatial change and discussed the five major forms of economicorganization commonly recognized: Subsistence, slavery, feudalism, capitalism, and socialism.We established some of the basic ideas and outcomes associated with globalization includingtechnology, economic development, and changing spatial divisions of labor.

ECONOMIC PATTERNS AND THE SEARCH FOR EXPLANATION18

6063 GEOGRAPHY WORLD ECON_PT_246x189 mm 22/01/2014 15:09 Page 18

KEY SOURCES AND SUGGESTED READINGBlinder, A.S., 2006. Offshoring: The next Industrial Revolution? Foreign Affairs, March/April.Brynjolfsson, E. and McAfee, A., 2011. Race against the Machine: How the digital revolution is

accelerating innovation, driving productivity, and irreversibly transforming employment and theeconomy. Lexington, MA: Digital Frontier Press.

Cowen, T., 2011. The Great Stagnation: How America ate all the low-hanging fruit of modern history,got sick, and will (eventually) feel better. New York: Dutton.

Hughes, A. and Reimer, S. (eds.), 2004. Geographies of Commodity Chains. New York: Routledge.Johnston, R.J., Taylor, P.J., and Watts, M. (eds.), 2002. Geographies of Global Change: Remapping

the world. Cambridge, MA: Blackwell.Mankiw, N.G. and Swagel, P., 2006. The Politics and Economics of Outsourcing, Working Paper 12398,

National Bureau of Economic Research.Massey, D., 1984. Spatial Divisions of Labor. London: Methuen.O’Loughlin, J., Staeheli, L., and Greenburg, E. (eds.), 2004. Globalization and its Outcomes. New York:

Guilford Press.Schumpeter, J.A., 2010. Capitalism, Socialism and Democracy. New York: Routledge.Storper, M. and Scott, A.J. (eds.), 1992. Pathways to Industrialization and Regional Development. London:

Routledge.Venables, A.J., 2006. Shifts in Economic Geography and Their Causes, Federal Reserve Bank of Kansas

City Economic Review 31, 61–85.Wallerstein, I., 1991. Geopolitics and Geoculture. Essays on the changing world-system. Cambridge:

Cambridge University Press.

1. THE CHANGING WORLD ECONOMY 19

6063 GEOGRAPHY WORLD ECON_PT_246x189 mm 22/01/2014 15:09 Page 19

Geography is about local variability within a general context. (R.J. Johnston, 1984: 444)

In this chapter, we describe the major dimensions of the contemporary economic landscape.We identify dominant and recurring patterns and note the major exceptions to these patterns.In other words, we are concerned primarily with characterizing the general context referred

to by Johnston in our opening quote. To the extent that we identify exceptions andcontradictions, we are also concerned with local variability.

In subsequent chapters, our objective will be to uncover the processes that have contributedto these patterns—both the general and the locally distinctive or unique. As we willdemonstrate, from the interaction of the unique with the general, distinctive economic regionsemerge.

The dominant components of economic geography at the global scale are most often castin terms of core–periphery differences. Meier and Baldwin (1957) were perhaps the earliestwriters to attempt a conceptual description of this core–periphery structure on a global scale.They noted that a country is at the center of the world economy: