The Future of Taxes for the Business Owner Presented by: Ryan E. Miller, CPA Director Katz, Sapper & Miller, LLP 800 East 96th Street, Suite 500 Indianapolis, IN 46240 317.580.2009

The Future of Taxes for the Business Owner Presented by: Ryan E. Miller, CPA Director Katz, Sapper & Miller, LLP 800 East 96 th Street, Suite 500 Indianapolis,

Dec 25, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

The Future of Taxes

for the Business OwnerPresented by:

Ryan E. Miller, CPADirector

Katz, Sapper & Miller, LLP

800 East 96th Street, Suite 500

Indianapolis, IN 46240

317.580.2009

Place holder

Recent Tax Legislation

• HIRE Act – March 18, 2010• Patient Protection Act – March 21, 2010• 2010 Reconciliation Act – March 23, 2010• Education Jobs Act – August 10, 2010• 2010 Small Business Act – September 27, 2010• 2010 Tax Relief Act – December 17, 2010• Six Other Pieces of Legislation in December

Place holder

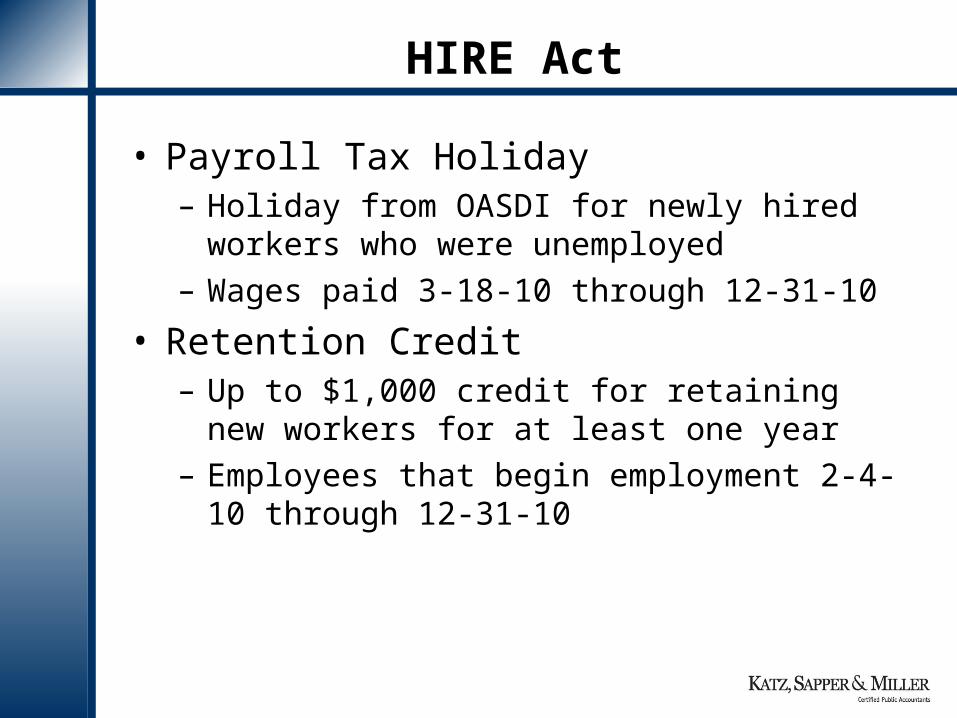

HIRE Act

• Payroll Tax Holiday– Holiday from OASDI for newly hired workers who

were unemployed– Wages paid 3-18-10 through 12-31-10

• Retention Credit– Up to $1,000 credit for retaining new workers for

at least one year– Employees that begin employment 2-4-10

through 12-31-10

Place holder

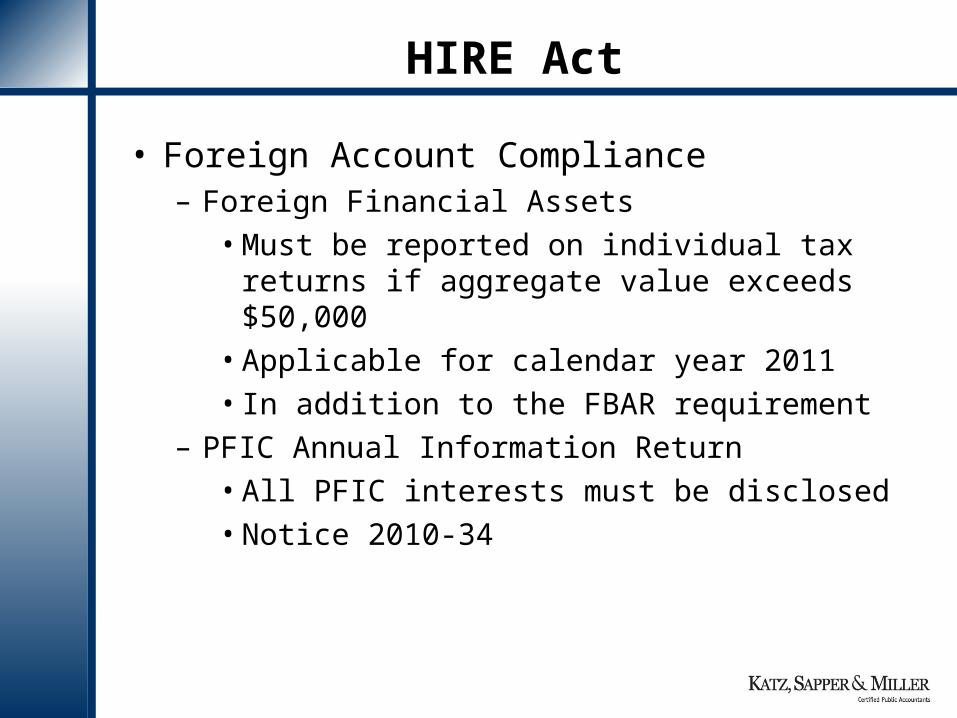

HIRE Act

• Foreign Account Compliance– Foreign Financial Assets

• Must be reported on individual tax returns if aggregate value exceeds $50,000

• Applicable for calendar year 2011• In addition to the FBAR requirement

– PFIC Annual Information Return• All PFIC interests must be disclosed• Notice 2010-34

Place holder

Health Care

• Over-the-Counter Medicines– No longer a qualified medical expense– Health FSA, HRA, HSA, and Archer MSA

• W-2 Reporting of Health Coverage– Tax years beginning in 2011

• 1099 Reporting of Payments to Corporations– Payments made in 2012 and beyond

Place holder

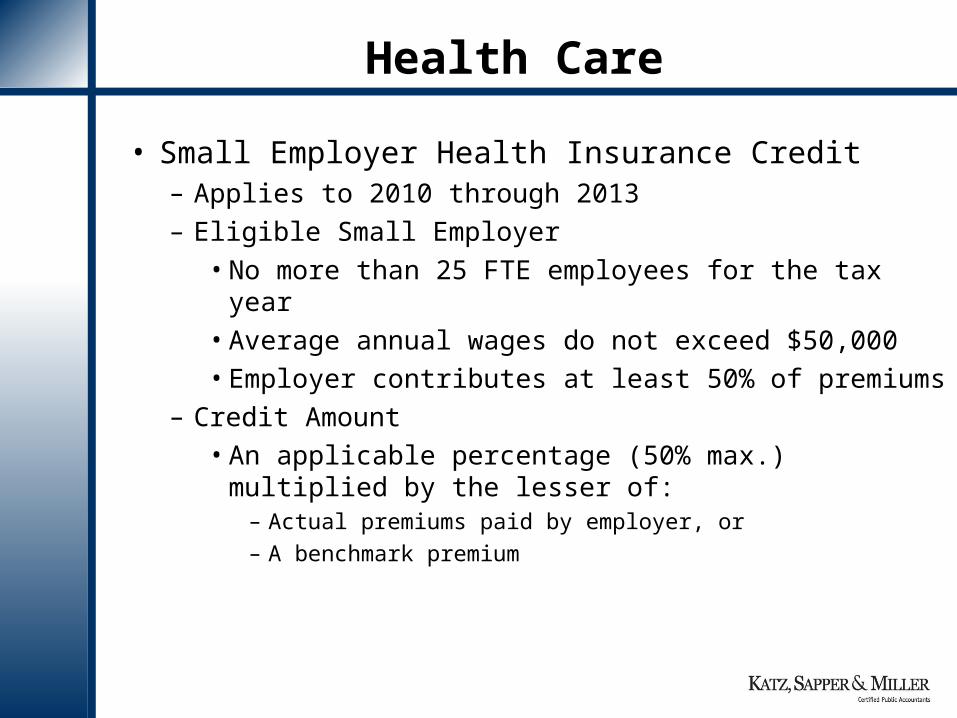

Health Care

• Small Employer Health Insurance Credit– Applies to 2010 through 2013– Eligible Small Employer

• No more than 25 FTE employees for the tax year• Average annual wages do not exceed $50,000• Employer contributes at least 50% of premiums

– Credit Amount • An applicable percentage (50% max.) multiplied

by the lesser of:– Actual premiums paid by employer, or– A benchmark premium

Place holder

Small Business Act

• 100% Gain Exclusion for QSBS– Applies for QSBS acquired after Sept. 27, 2010

and before Jan. 1, 2011– QSBS

• Domestic C Corporation other than DISCs, RICs, REITs, REMICs, or Cooperatives

• Acquired at original issue• Asset limitations

Place holder

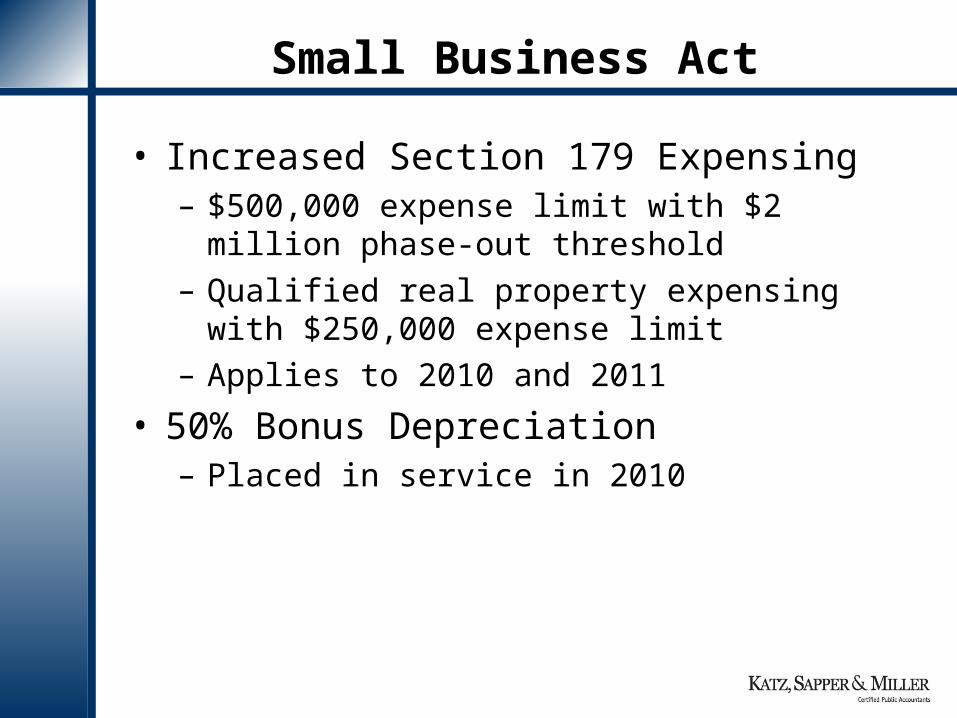

Small Business Act

• Increased Section 179 Expensing– $500,000 expense limit with $2 million phase-out

threshold– Qualified real property expensing with $250,000

expense limit– Applies to 2010 and 2011

• 50% Bonus Depreciation– Placed in service in 2010

Place holder

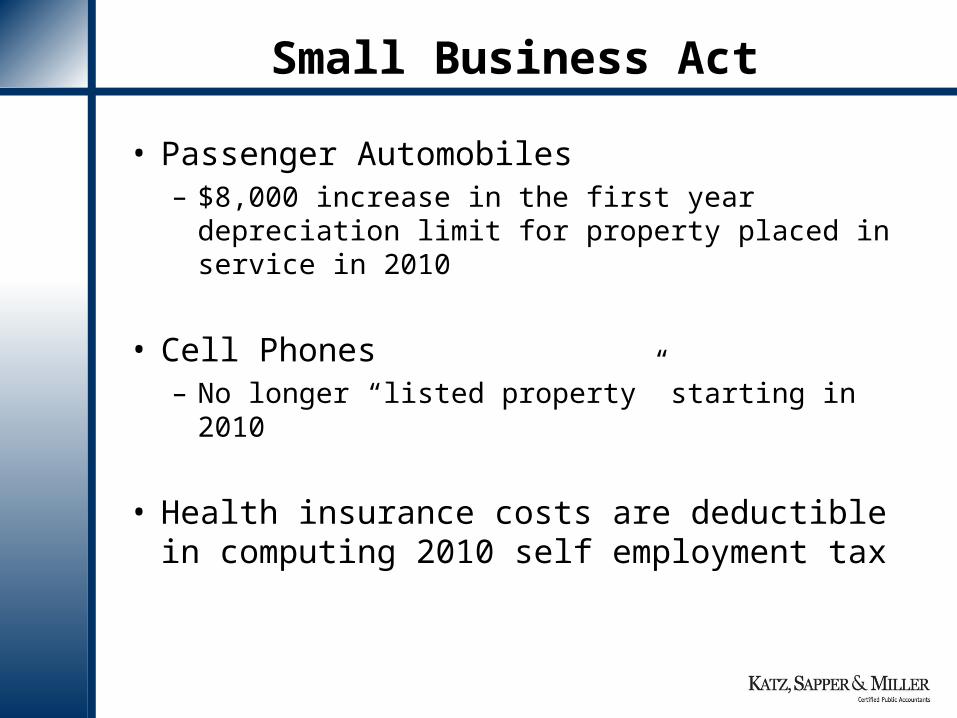

Small Business Act

• Passenger Automobiles– $8,000 increase in the first year depreciation

limit for property placed in service in 2010

• Cell Phones– No longer “listed property” starting in 2010

• Health insurance costs are deductible in computing 2010 self employment tax

Place holder

Small Business Act

• Temporary reduction in an S Corporation’s built-in gain period (from 7 to 5 years)– 10 year period returns in 2012

• 1099 reporting imposed on recipients of rental income – Deemed to be engaged in a trade or business

Place holder

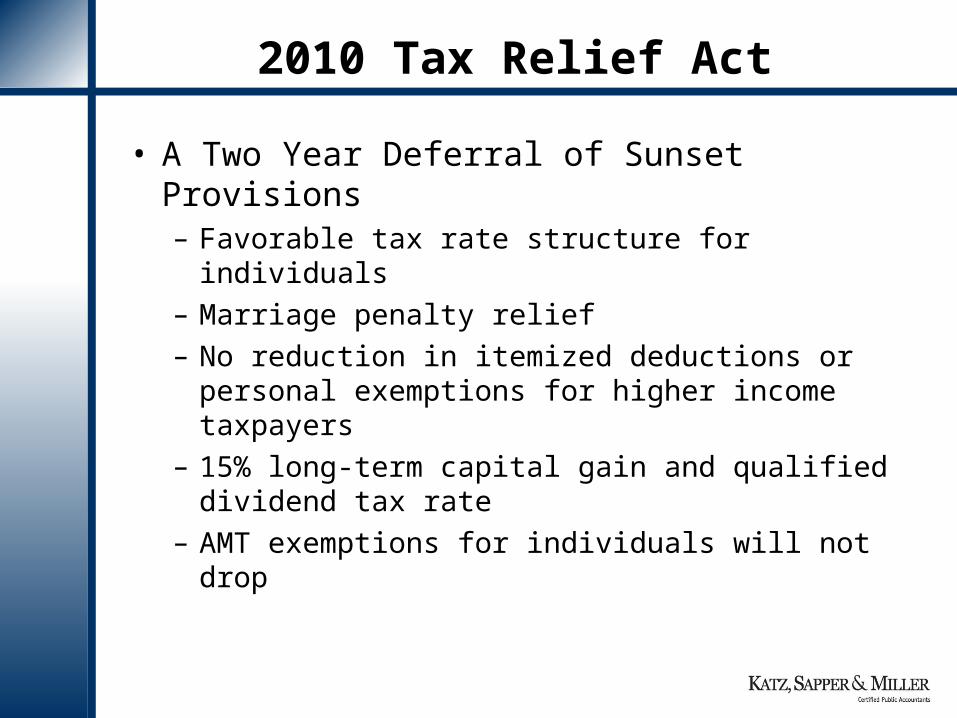

2010 Tax Relief Act

• A Two Year Deferral of Sunset Provisions– Favorable tax rate structure for individuals– Marriage penalty relief– No reduction in itemized deductions or personal

exemptions for higher income taxpayers– 15% long-term capital gain and qualified

dividend tax rate– AMT exemptions for individuals will not drop

Place holder

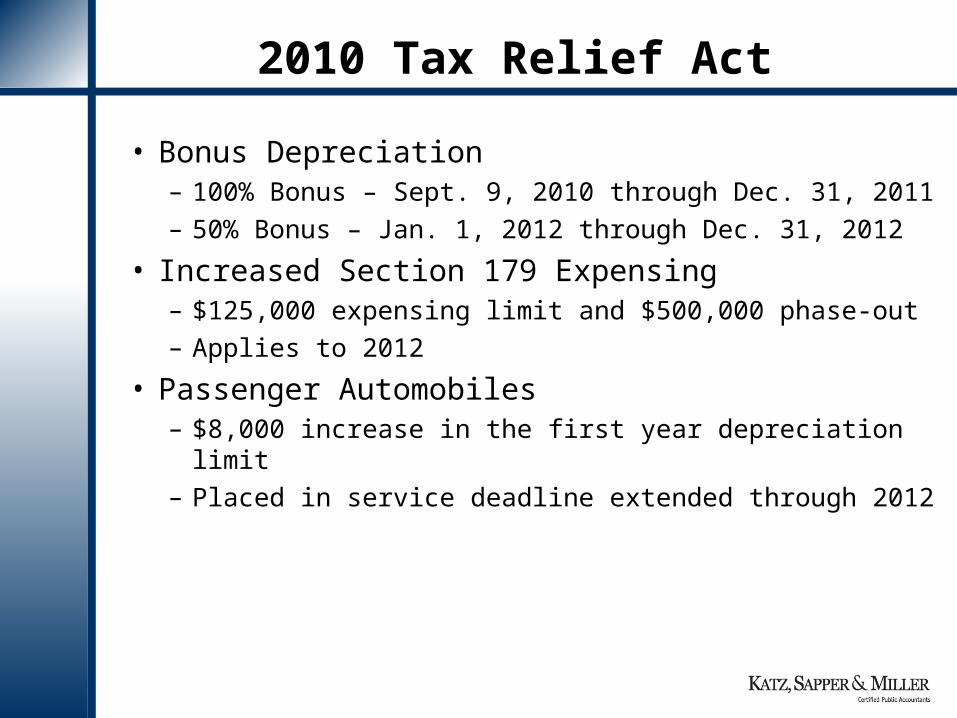

2010 Tax Relief Act

• Bonus Depreciation– 100% Bonus – Sept. 9, 2010 through Dec. 31, 2011– 50% Bonus – Jan. 1, 2012 through Dec. 31, 2012

• Increased Section 179 Expensing– $125,000 expensing limit and $500,000 phase-out– Applies to 2012

• Passenger Automobiles– $8,000 increase in the first year depreciation limit– Placed in service deadline extended through 2012

Place holder

2010 Tax Relief Act

• 2% Tax Holiday on Payroll and Self-Employment Taxes – Applies for wages paid and self-employment

income earned during calendar year 2011

• Increased Income Tax Deduction for Self-Employment Taxes– 59.6% of the OASDI tax plus 50% of the HI tax

Place holder

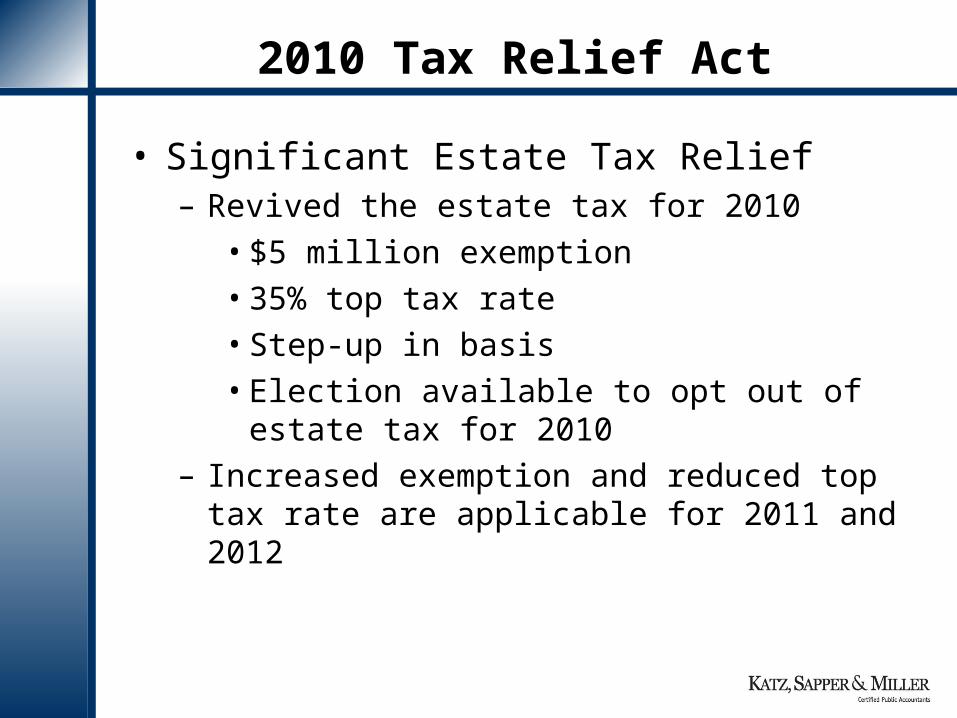

2010 Tax Relief Act

• Significant Estate Tax Relief– Revived the estate tax for 2010

• $5 million exemption• 35% top tax rate• Step-up in basis• Election available to opt out of estate tax for

2010– Increased exemption and reduced top tax rate

are applicable for 2011 and 2012

Place holder

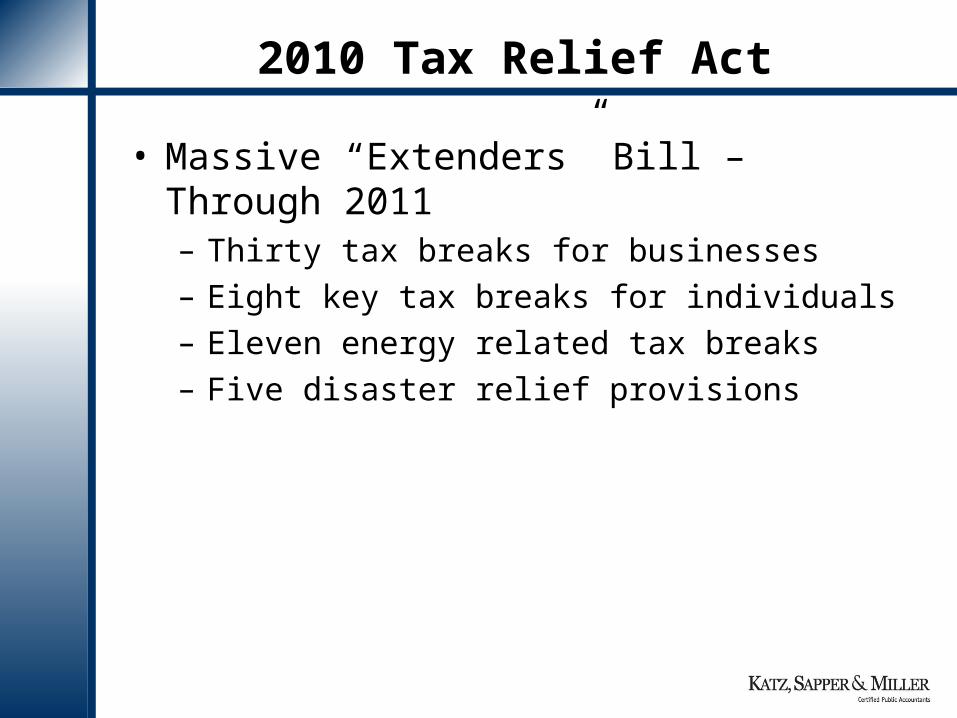

2010 Tax Relief Act

• Massive “Extenders” Bill – Through 2011– Thirty tax breaks for businesses– Eight key tax breaks for individuals– Eleven energy related tax breaks– Five disaster relief provisions

Place holder

IRA Conversions

• 2005 Legislation Referred to as TIPRA• Eliminated the income limitation• Inclusion of 2010 Conversion Income

– Pick up half in 2011 and half in 2012– Elect to pick it all up in 2010

• Undoing an IRA Conversion– Must wait 30 days before reconverting– Pick up all the conversion income in 2011

Place holder

Indiana

• Reduce the Corporate Tax Rate from 8.5% to 5%? Unclear How Much Traction This Has

• Sales Tax – Taxing Services? – Unlikely

• Sales Tax – Digital Goods– CarFax report taxable as software– Expand the definition to database access?

Place holder

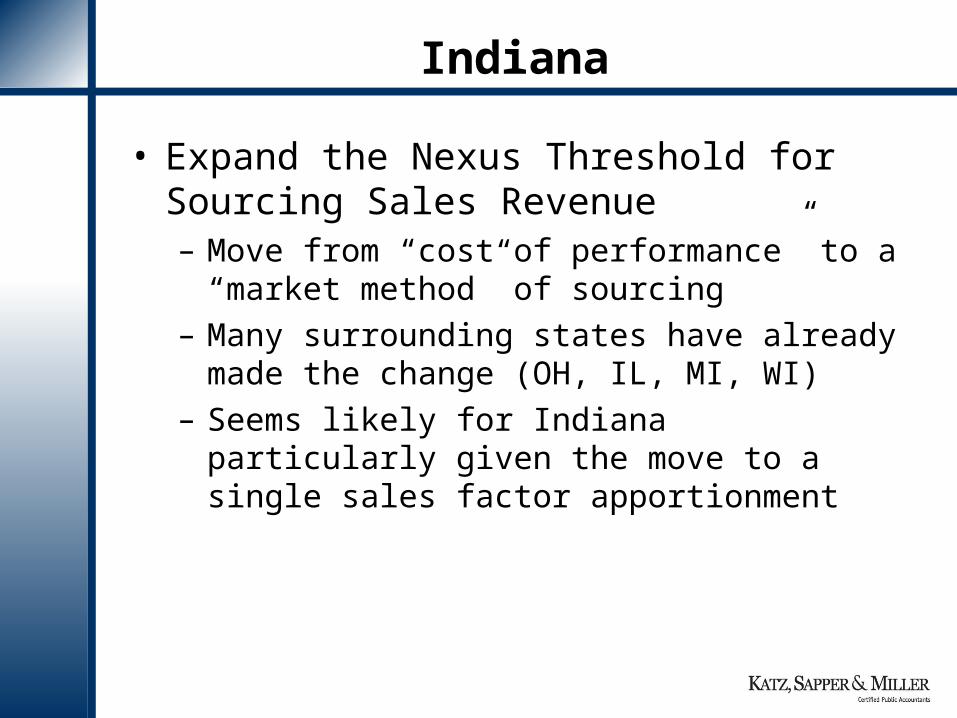

Indiana

• Expand the Nexus Threshold for Sourcing Sales Revenue– Move from “cost of performance” to a “market

method” of sourcing– Many surrounding states have already made the

change (OH, IL, MI, WI)– Seems likely for Indiana particularly given the

move to a single sales factor apportionment

Place holder

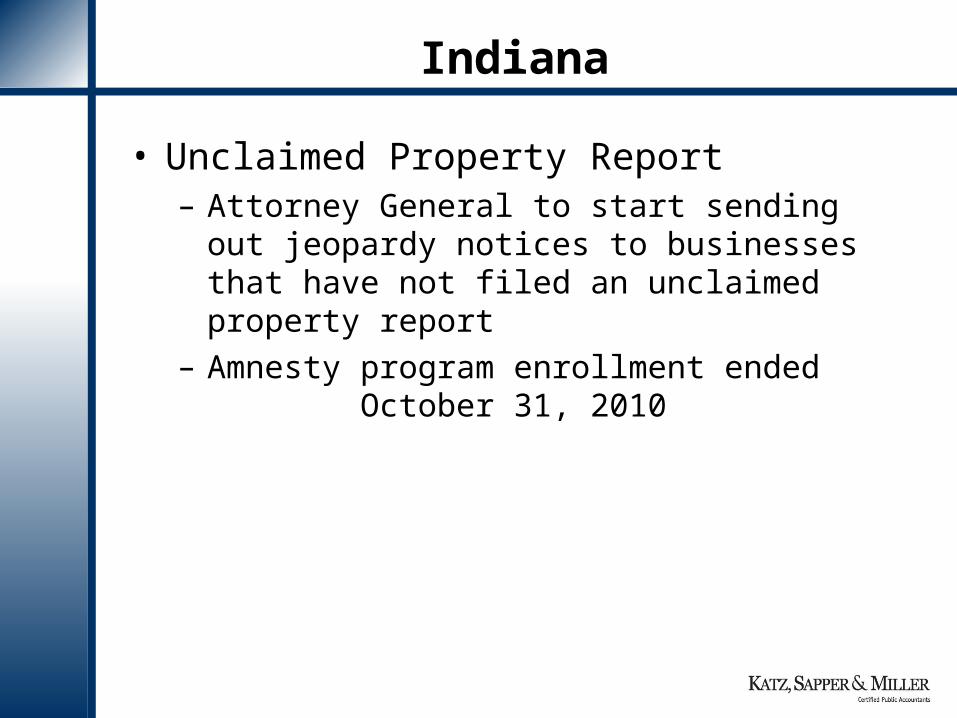

Indiana

• Unclaimed Property Report– Attorney General to start sending out jeopardy

notices to businesses that have not filed an unclaimed property report

– Amnesty program enrollment ended October 31, 2010

Place holder

ESOPs

• An Employee Stock Ownership Plan (ESOP) is an employee benefit plan that is designed to invest primarily in the sponsoring employer’s stock

Place holder

ESOP Candidate Profile

• Owner approaching retirement• Capable management team to succeed

owner• Unused debt capacity• Profits to support ESOP debt service• Company size (more cost effective benefit)• Motivated by tax advantages

Place holder

ESOP Candidate Profile

• Motivated by “ownership culture” advantages

• Desire to buy-out minority shareholder• Limited 3rd party, strategic buyers in the

market

Place holder

Indiana ESOP Initiative (IEI)

• Linked-Deposit Program– ESOP loan to Company, bank interest rate

reduced 1-2%– State links deposit to bank, CD rate reduced by

1-2%– $50 million program– Apply to the program after bank financing has

been secured

Place holder

Linked-Deposit General Guidelines

• Company must have its headquarters in Indiana, conduct significant portion of operations in Indiana, and employ majority of employees in Indiana

• Treasurer will rely on credit evaluation provided by the financial institution

• No established ESOP prior to participating in ESOP Linked-Deposit Program (ie, new ESOPs only)

Place holder

Linked-Deposit General Guidelines

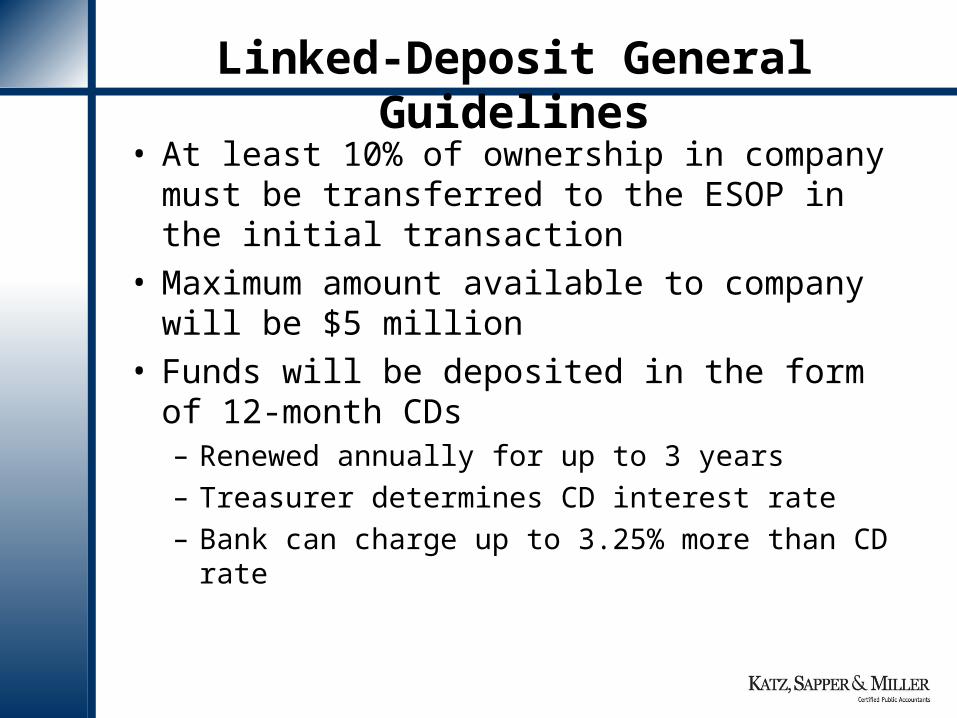

• At least 10% of ownership in company must be transferred to the ESOP in the initial transaction

• Maximum amount available to company will be $5 million

• Funds will be deposited in the form of 12-month CDs– Renewed annually for up to 3 years– Treasurer determines CD interest rate– Bank can charge up to 3.25% more than CD rate

Related Documents

![The Sapper Handbook[1]](https://static.cupdf.com/doc/110x72/553c74fb550346f92f8b49e2/the-sapper-handbook1.jpg)