4 4?L4v UNDP-WORLD BANK TRADE EXPANSION PROGRAM OCCASIONAL PAPER 9 /seemh/ /s THE FISCAL IMPLICATIONS OF TRADE POLICY REFORM: THEORY AND EVIDENCE David Greenaway Chris Milner This country rport Is a product of the joint UNDP/World Bank Trade Expansion mgmm which provides technical and policy advice to countries intending to reform their trade regimes The views contained herein are those of the authors and do not necessarily refect those of the United Naions Development Program or the World Bank. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

4 4?L4v

UNDP-WORLD BANKTRADE EXPANSION PROGRAM

OCCASIONAL PAPER 9

/seemh/ /s

THE FISCAL IMPLICATIONS

OF TRADE POLICY REFORM:

THEORY AND EVIDENCE

David GreenawayChris Milner

This country rport Is a product of the joint UNDP/World Bank Trade Expansion mgmm which provides technicaland policy advice to countries intending to reform their trade regimes The views contained herein are those of theauthors and do not necessarily refect those of the United Naions Development Program or the World Bank.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

THE FISCAL IMPLICATIONS

OF TRADE POLICY REFORM:

THEORY AND EVIDENCE

David GreenawayChris Milner

November 1993

Trade Policy DivisionPolicy Research Department

World BankWashington, D.C.

Table of Contents

Page No.

Analytical links between trade reform and revenLe 1

Tariff liberalization 1Tariff simplification and consolidation 2Reductions in tariff exemptions 2Liberalization of quantitative trade restrictions 3Reductions in impediments to exports 3Exchange rate adjustment 4Decomposition of the aggregate revenue change 5

Factors that determine the revenue impact of reform 6Fiscal dependence on trade taxes 6

Cross-classification of trade tax dependence and economiccharacteristics 7Recent patterns of trade tax dependence 9Declining dependence on trade taxes 10

Expected changes in trade tax revenue 12Import and tariff rate policies 12Export and exchange rate policies 13

Experience with structural lending and fiscal yield in developing countries 14Initial conditions: experience in eleven developing countries 15Trade policy reform and fiscal yield: experience in five developing countries 16

Jamaica 19Kenya 21Mauritius 23C6te d'Ivoire 26Morocco 27

Some lessons 30

Endnotes 32

Bibliography 33

i

List of Tables

1 Country Economic Characteristics and dependence on trade taxes, 1987 82 Share of various taxes in government revenue, around 1980 113 Initial conditions in eleven countries receiving structural adjustment

loans and direction of change in trade tax revenue after reform 174 Decomposition analysis of changes in import tax revenues in five developing

countries, 1981-86 18

A.1 Trade taxes and income per capita of a sample of sixty nine countries, 1976-82 35A.2 Basic indicators, Jamaica 1980-86 36A.3 Basic indicators, Kenya 1980-86 36A.4 Basic indicators, Mauritius 1980-86 37A.5 Basic indicators, Cote d'Ivoire 1980-86 37A.6 Basic indicators, Morocco 1980-86 38

List of Boxes

1 Factors affecting the sensitivity of trade tax yield to trade policy reform 62 Summary of Trade Policy Reforms, Jamaica under SALs of 1982, 1983 and 1984 193 Trade Policy Reform in Kenya Under SALs of 1980 and 1982 224 Trade Policy Reforms in Mauritius under SALs of 1981 and 1983 245 Summary of Trade Policy Reforms in Cote d'Ivoire under SALs of 1981, 1983,

and 1986 276 Summary of Reforms in Morocco Under SALs of 1982, 1983, and 1984 29

ii

Trade interventions in developing countries frequently have multiple objectives-protectingimport competing industries, raising revenue, and altering the distribution of income. The protectiveand revenue motives are frequently at odds. Thus for example, when a tariff is at its most protective,

revenue collections are zero. Changes in the protective structure will affect revenue collections, withthe exact effect depending on the type of reform and the nature of the protective structure. Thisrelationship has important implications for a government's willingness to undertake trade policy

reform. The stronger trade taxes feature in total government revenue-and they may be veryimportant in many developing countries-the more likely the government is to be influenced by the

immediate or transitional impact (expected and actual) of the reforms on trade tax revenue.IWhat makes some countries more or less vulnerable to trade tax revenue declines in the face

of trade reform? What type of trade policy reforms are more likely to be revenue-contracting and

what type are more likely to be revenue-expanding? What guidance for the design of revenue-neutral

trade reform programs does cross-sectional or case study analysis offer?This paper constructs an analytical framework to examine how specific trade policy reforms

and country characteristics may affect government revenue in developing countries. The framework is

then extended to identify which of these characteristics can be expected to influence a country's

vulnerability to trade reform-induced revenue changes or the direction of those changes. Cross-

sectional data and material on individual countries are also used to examine the evidence on the actual

impact of trade reform on revenue.

Analytical links between trade reform and revenueTrade policy reforms are a common element of World Bank structural adjustment lending

(SAL), featuring in more than 70 percent of SAL programs. Most programs have involved some mixof the following measures: overall tariff liberalization, simplification and consolidation of import

taxation, reductions in tariff exemptions, liberalization of quantitative import restriction and reductions

in impediments to exports. The following sections examine the analytical links between government

revenue and each of these measures individually, assuming that other factors remain the same.

Tanff liberalizationIt is often taken for granted that reducing the average tariff rate will reduce tariff collections.

For example, Yagci, Kamin, and Rosenbaum (1985) argue that "tariff reduction reduces government

revenue and increases imports, which in turn increases both the budget deficit and the balance ofpayments deficit" (p. 22). The fear of revenue loss is an important impediment to tariff liberalization.

Yet it does not automatically follow that tariff reduction leads to revenue reduction.

In the case of a marginal change the revenue effect depends on the initial tariff rate and on the

elasticity of import demand over the relevant range. If the initial tariff is above the revenue-maximizing tariff rate, tariff reductions will increase tariff collections. A recent examination of tariffs

in Tanzania found that for all tariffs higher than 60 percent the collection rate averaged only 27

percent of the posted tariff rate. Thus, given appropriate elasticities, tariff revenue collections mayincrease following liberalization. In addition by reducing the incentives for smuggling, misrecording,and other ilegal activities, liberalization may improve compliance and broaden the tax base.Tanzania's recorded trade increased threefold in two years following its first SAL in the mid 1980s.Another possibility is that a tariff reduction, through a positive income effect, could initiate arightward shift in demand, reinforcing the tendency to revenue expansion.

It is nonetheless still possible, however, that liberalization will shrink tariff revenue. Thiseffect would follow if the initial tariff were below the maximum-revenue tariff. The net impact ofgeneral tariff liberalization on duty collections depends therefore on the frequency distribution ofexisting rates above and below the maximum-revenue rates on specific categories of imports, thenature of the tariff rate changes, the shares of specific imports in total imports, and the relevant ownand cross-price elasticities of demand and supply.

Tariff simplification and consolidaionTariff reforms often attempt not only to reduce tariffs across the board but also to consolidate

a variety of import taxes into a single rate that provides greater transparency. Mauritius had a systemof import taxes that included customs duties, fiscal duties, import surcharges, special import levies,and stamp duties-all of them discriminating between imports and domestic production of importsubstitutes (Greenaway and Milner, 1986 and 1989). A reform consolidating all these taxes into asingle tax should, in principle, be revenue neutral. But to the extent that greater simplicity reduces thescope for evasion or cuts administrative costs, consolidation may have a net positive impact on tariffrevenue.

Another simplification measure is to set tariffs on inputs and outputs at designated rates inorder to attain a particular rate of effective protection-as in Burundi and C6te d'Ivoire. The revenueimplications depend on initial tariff rates and elasticities and on whether the move involves tariffincreases or decreases.

Reductions in tarff exemptionsTariff exemptions are common in developing countries. Besides international organizations,

expenditures financed by project aid, and diplomatic groups, exemptions often apply to stateenterprises and any organization associated with aid projects. Exemptions are frequently discretionary,so their scope tends to widen through time. Exemptions constitute a substantial source of revenueloss. According to official estimates the tariff revenue foregone through exemptions in Tanzania in1986 was almost equivalent to the tariff revenue collected. Trade reforms that reduce exemptions willincrease revenue collections.

2

Liberalization of quantitative trade restrictions

Quantitative restrictit.us on imports are a widely used instrument of protection in developingcountries. Economic theory learly ranks the quota as an inferior protective instrument to the tariff inmost circumstances, and most SALs have conditions requiring the removal of quotas and similarrestrictions (Mosley 1987).

Removing quotas generally has fiscal implications. Adjustment loans distinguish between thedegree of protection provided to a given activity and the instrument of protection. Reform focuses on

the instrument-replacing quotas with equivalent tariffs-not on abolishing protection. As long as theequivalent tariff is not prohibitive, the switching of instruments will increase revenue collection, asquota rzntz are transferred from the foreign exporter (or local importer) to the fiscal authorities. Howmuch tariff revenues rise depends on the size of the original quota rents and the tariff rate chosen.2

Where quantitative restrictions have been pervasive, the effect on the tax base may be dramatic. Arecent study estimated that replacing quotas with equivalent tariffs in Burundi for a sample ofproducts that constituted only about 15 percent of total imports would have transferred quota rents (i

1984) to the government equivalent to total import tax revenues in that same year (Greenaway and

Milner 1990).Quantitative export restrictions are employed in many developing countries to guarantee a

minimum domestic supply of essential products. In almost all cases this often misused, anachronisticintervention can be eliminated without social cost and with negligible revenue implications.

Reductions in impediments to exportsElementary economic theory demonstrates conclusively that protection is a relative concept.

Protection of the import-substitute sector results simultaneously in disprotection of the export sector.Policy-oriented research over the last ten years or so has provided increasingly strong evidence of the

extent of this disprotection (Krueger 1981; Balassa 1982; Greenaway and Nam 1988). Mostadjustment loans include conditions intended to compensate for export disincentive effects (some 76percent of them according to Mosley 1987)-duty drawbacks, concessional finance, preferential accessto foreign exchange allocations-which is no more than a recognition that any import liberalization isfar from complete.

Even though this policy change may be motivated by allocational considerations, it has

revenue implications. Direct fiscal incentives to exporters represent a fiscal drain-a reduction in

potential fiscal revenue. This is, of course, a partial equilibrium inference. If the export supplyschedule is elastic over the relevant range, incentives could conceivably result in a net increase innontrade revenue collections or an increase in tariffs on imports finnced with the foreign exchangegenerated by the extra exports. Similarly, if a duty drawback is applied to imports that would not

have occurred in the absence of export incentives, no revenue loss is experienced.

3

Another concern is that export taxes, direct or in the form of differentials between foreignprices and prices paid to producers by public sector marketing boards with export monopolies, are a

major source of trade taxes in some developing countries. For traditional exports these taxes may notsignificantly impede the volume of exports, at least in the short run. In that case reductions in exporttaxes are likely to reduce short-term tax revenue. But it is important to note that in small open

economies the revenue impact of partial reductions depends strictly on the elasticity of export supply:

tax yield from traditional exports will be much more sensitive to variations in world prices.

Domestic policy decisions are likely to have substantially more impact in the case of

nontraditional exports. To enable these goods to compete in export markets and to reduce the

incentive to produce for the home market, exemption from export taxes is likely to be necessary.

Thus the importance of export taxes in total tax yield diminishes as the share of nontraditional

exportables in total exports increases.

Exchange rate adjustmentThe exchange rate is a critical relative price. About 16 percent of World Bank structural

adjustment loans have involved exchange rate conditions. Cross-conditionaw'y with IMF stabilization

loans give further prominence to exchange rate alignment. The need, almost invariably, is for

exchange rate depreciation in real terms. On small open economy assumptions, depreciation raises the

domestic price of imports and may reduce or augment tariff revenues (denominated in domestic

currency) depending on elasticity of demand for importables and elasticity of supply for importsubstitutes.

The overall elasticity of demand for imports depends on the share of competitive imports in

total imports. Elasticity for imports that compete with domestic production, such as foodstuffs and

consumer goods, may be quite high, while elasticity for capital goods, raw material, and intermediate

inputs for which there are no domestic substitutes wi" tend to be low.

For the least industrialized of developing countries imports are therefore likely to be price

inelastic, and devaluation is likely to boost import duties. These low-income, less industrialized

countries are also more likely to be dependent on traditional exports and export taxes. Export tax

yields in domestic currency are unambiguously increased by reducing currency overvaluation since

even if exports are perfectly inelastic in supply the domestic currency value of given foreign currency

earnings is increased by devaluation.3

Exchange rate adjustment is therefore most likely to be revenue enhancing in the case of low-

income industrializing countries. However, depreciation does not necessarily mean a loss of revenue

for more industrialized developing countries with a greater proportion of competitive imports and of

nontraditional exports because there are likely to be sufficient noncompetitive imports and quality

differences between imports and import substitutes to prevent the tax base (in domestic value terms)

4

from contracting. Revenue yield from specific duties will fall as the volume of imports falls, but if advalorem tariffs predominate revenue will be at least maintained in these cases.

Decomposition of the aggregate revenue changeAs the discussion so far makes clear, how trade tax yield is affected by trade policy reform

depends on a complex array of factors at the time of reform (reform details, price elasticities) and oncontemporaneous macroeconomic adjustments and constraints. In the absence of a highlydisaggregated, computable general equilibrium model for a large number of countries, this studyrelies on actual or revealed effects of trade policy reform programs for examining the relative revenueeffects of alternative elements of trade policy reform.

The methodology can be employed in a number of ways. First, the content and effects of

trade policy reform can be compared across a number of countries; consistent or distinctivecharacteristics may be instructive. Second, the dynamics of reform and adjustment in a restrictednumber of country case studies can be examined in detail. Last, formal decomposition analysis can beused to summarize the relative fiscal impact of the broad characteristics of import policy reform. (Thedecomposition analysis is defined in Table 4.)

The aggregate decomposition analysis considers three typee of effects on the total import taxyield: the real import effect which measures the revenue effect associated with a change in the real(dollar) value of imports: the exchange rate effect, which measures the indirect effect of a change inthe exchange rate on import tax yields through its effect on the tax base (the local currency value of a

given dollar import bill); and the tariff rate effect which measures the tariff revenue effect of a realchange in average tariff rate for a given tax base.

This type of aggregate decomposition analysis is a potentially valuable complementary tool forinvestigating the revenue effects of trade policy reform, but it has several shortcomings. Much of therichness of the earlier piecemeal analysis of tariff reform is lost in the aggregate decompositionanalysis. As established earlier, the effect on tariff revenue of lowering an individual tariff is

ambguous: it can be revenue expanding or revenue intracting, depending on whether the initial

tariff was below or above the maximum-revenue rae. Thus in measuring the tariff rte effect usingthe decomposition analysis, it is important to interpret the results carefully, in the cortext of a specific

package of trade policv reforms. A recorded change in the average rate of duty collection can be due

to a change in scheduled or operational tariff rates or to a change in the taxable base (the local

currency value of imports), so it is important to understand how trade reforms affect the average dutycollection rate. Similarly, the absence of a significant tariff rate effect in a decomposition analysis of

this type may simply mean that there are indirect tariff rate effects that are being captured by the real

import effect.

5

Factors that determine the revenue impact of reform

The interdependence of trade policy and other fiscal policy reforms is so strong that it is

impossible to consider trade policy reforms in a narrow, isolated sense. In the absence of other fiscal

reforms, trade policy reforms that reduce revenue are likely to result in fiscal problems that

undermine the sustainability of trade policy reform. The extent of this threat to sustainability in a

particular country depends on two factors:

a The country's current fiscal dependence on trade taxes and how this departure might be

expected to change.a The probability that trade policy reforms will be revenue-contracting, rather than revenue

neutral or revenue-expanding.Box 1 summarizes the factors or country characteristics that affect the sensitivity of trade tax

yields to trade policy reform and provides some testable hypotheses for the discussion presented in

this section. These hypotheses can be examined in light of the experiences of countries that have

undergone significant trade policy reform, as discussed later in this volume.

Box I Factors affecting the sensitivity of trade tax yield to trade policy reform

Thposiblityof a revenue reduction The possibilityofa revenue increase

- of import duties, inversely related - of idiport duties, dhrectly related toto the average level of nominal tariffs the eustentof tauitt see differentialsbefore reform. before reform.

- of impot4dedes,direcdly related to -of import duties, directly salated tothe smallness and newnesso ithe the share of competing imports in totalindustriaimport-substitutesector imports before reform.before reform.

- of imporidoties, directly related to - of import duties, directly related tothe share of nontraditional exports in the incidence of duty exemptions beforetotal exports before reform, reform.

- of import doties. inversely related to - of laport duties, directly related tothe extent of the foreign exchange the incidence and extent of quantitativeconstraintisasilvated by the reform. Import restrictions.

-of exoedtis,4irecdy talated to the - of exporedudles, directly related toeensorfday rearsson tradirional he anoutrcurency depreciation

expdathe impettance oftradiionlal follown th eform.

Fiscal dependence on trade taxes

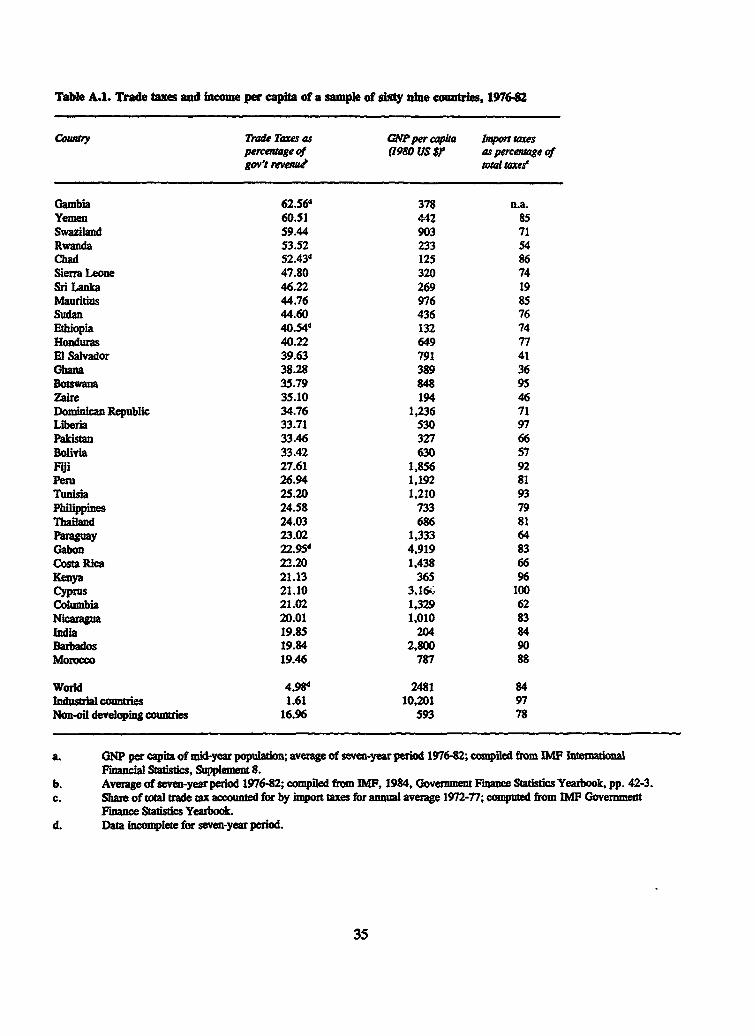

Many generalizations or "stylized facts" about developing countries cannot withstand closescrutiny. One that can, however, is that developing countries depend more heavily on trade taxes thando other countries. For developing countries in a sample of sixty-nine countries the trade tax shareover the period 1976-1982 averaged from 5 percent in Chile to 63 percent in Gambia (annex table

6

A. 1). For all developing countries that are not oil exporters the share averaged 17 percent. Dispersionaround the mean is quite high, however, and for many countries the trade tax share was substantially

higher: more than 40 percent In eleven countries and more than 20 percent in thirty-one countries.

These figures even understate the importance of trade taxes since they include only explicit import

and export taxes; foreign exchange licensing and other schemes that constitute defacto trade taxes are

excluded.

Cross-classifications of trade tax dependence and economic characteristics. For most countries

import taxes account for the largest volume (84 percent) of total trade taxes. Only in sixteen countries

does the share of import taxes in total trade taxes fall below 75 percent and only in four does it fall

below 50 percent. In general export taxes tend to be more important to economies that are heavily

dependent on exports of primary agricultural products such as El Salvador, Ghana, and Zaire. This

same consideration also influences the regional pattern of dependence on trade tax. Countries in

Africa are most heavily dependent on trade taxes, followed by those in Asia, Latin America, and the

Southern European middle-income countries (table 1). This is due in part to the more extensive use of

export taxes and in part *o the higher concentration of low-income countries in Sub-Saharan Africa.

How did this pattern of heavy dependence on trade taxes come about in developing countries?

In considering questions of tax structure, economists take into account efficiency, equity andadministration. With the exception of lump-sum levies, taxes generate by-product distortions. The

design of optimal taxes seeks to minimize the by-product distortion costs in order to minimize the

resource misallocation induced by taxation. Equity considerations include both horizontal equity

(treating like individuals or entities in a like manner) and vertical equity (allocating tax burdens in

accordance with ability to pay).Trade taxes score badly on efficiency grounds and are second-best (or worse) as revenue

raisers. Because they discriminate between domestically produced and foreign produced products,

their excess burden is greater than a revenue-equivalent sales or excise tax. Many developing

countries attempt to attain equity objectives by levying high trade taxes on luxuries. But trade taxes

do not score well from an equity standpoint because demand elasticities tend to be lower on

necessities and because domestically produced luxury substitutes frequently go untaxed. Thus on both

efficiency and equity grounds trade taxes levied for revenue purposes are unlikely to feature in a first-

best tax structure.This proposition is based on two crucial assumptions: that the country's trade is too small to

affect world prices (small country assumption) and that there are no collection costs. If the small

country assumption is relaxed, then conventional wisdom on excess burdens must be qualified.

Indeed, it can be shown that if a country has market power, an import tax may be superior on

efficiency grounds to an equal-yield Lacome tax or an equal-yield domestic production tax

(Friedlaender and Vandendorpe 1968; Georgakopoulos 1974). The tariff continues to generate

deadweight losses, but these are counteracted by the favorable shift in terms of trade. This is not,

7

Table 1. Country economic characteristics and dependence on trade taxes, 1987 (percent)7Ade tax Agriculture Government Primary Urban GDP peras share of as share consumption as products as population capita

Category tax revenue of GDP share of GDP share of GDP Share ($)

Income'Low (39) 33.8 40.7 14.0 75.0 21.0Lower-middle (34) 22.6 20.2 16.0 74.0 44.0Upper-middle (24) 9.9 13.9 16.0 58.0 60.0High-income oil (4) 3.6 2.5 22.0 90.0 76.0

Dependence on trade taxes"Low (25) 7.2 14.5 17.8 65.5 61.0 3,560Medium (29) 22.4 27.6 14.8 75.1 36.2 918High (17) 42.7 34.6 15.5 74.1 29.8 616

RegionAfrica (4) 35.8 32.3 15.6 82.4 29.9 637Asia (32) 17.7 21.8 15.8 59.8 41.3 2,636Americas (21) 22.3 15.4 14.2 71.4 54.6 1,648Europe (5) 12.3 14.2 14.2 30.2 51.2 2,786

Special categoryHighly indebted (17) 22.0 17.3 12.7 66.7 58.5 1,511Sub-Saharan Africa (35) 37.5 34.7 15.4 83.4 27.0 550

Degree of trade exposureLow (22) 28.4 34.0 13.0 72.8 33.6 782Medium (42) 19.4 26.8 15.0 72.9 42.0 1.226High (22) 21.6 18.9 16.9 61.0 46.6 2.087

World Development Report classification.For dependence categories, trade taxes constitute the following shares of total taxes: low, less than 15 percent: medium, 16-30 percent: high, more than 30 percent.

. Trade exposure categories are as follows, where exposure is defined as 1/2(X+M)/ODP: low, less than 15 percent; medium, 16-30 percent; high, more than 30 percent.

8

however, a widely applicable explanation of the greater dependence of developing countries on tradetaxes.

Relaxation of the assumption of zero collection costs turns out to be crucial for the choice oftax base in a developing country. When income per capita is low (in absolute terms), questions ofequity and efficiency are secondary to questions of administrative feasibility. Administering income-based or production-based taxes requires considerable sophistication. And even when a country hasthe required administrative superstructure, the existence of large subsistence sectors makes thedefinition and valuation of income an intractable problem. Similarly, the distribution of much ofproduction through informal markets creates insurmountable difficulties for the administration of asales tax. By contrast collection costs for taxes on international transactions are likely to be somewhatlower because the number of transactors is restricted and their identity is more obvious since all legaltransactions are channeled through a finite number of ports of entry. As Corden (1974) notes, these

characteristics apply with particular relevance to export taxes.For these reasons the cost-yield ratio could be much lower for trade taxes than for domestic

income taxes or production taxes. The World Development Report 1980 estimated the administrativecosts of trade taxes at 1 percent to 3 percent of revenue collect, compared u ith 5 percent for valueadded taxes and as high as 10 percent for income taxes. Despite these differences in the costs ofadministration, however, the social ccsts per unit of revenue raised are likely to be strongly in favorof alternatives such as consumption-based taxes (see Clarete and Whalley 1987 for an illustration).

Recent paterns of trade tax dependence. More recent information (most is for 1987) for 101developing countries was used to classify countries in ways that highlight the principal economiccharacteristics associated with heavy dependence on trade taxes (table 1).

Cross-classifying income per person and dependence on trade taxes confirms the inverserelationship between them. In low-income countries the share of trade taxes in total taxes is almost 34percent, compared with just under 10 percent in upper middle income countries and less than 4percent for high income oil exporting countries. Other factors commonly associated with low incomeper person and dependence on trade taxes also show the expected relationship: the share of agriculturein GDP varies inversely with income per person while the proportion of the total population in urbanareas varies directly. The pattern for dependence on primary products is less clear. With the exception

of the high-income oil-exporters the share of central government consumption in GDP is remarkablystable. Looking at countries classified by dependence on trade taxes (share of trade taxes in totaltaxes) shows the same relationships (second panel of table 1).

Regional cross-classification shows that trade tax dependence is heaviest in Africa, followed byCentral and South America, Asia, and Europe (third panel). In Africa, income per person and urbanpopulation share are lowest, while the share of agriculture in GDP and dependence on primaryproducts are highest. In the Southern European countries the opposite relationships hold. Countries inAsia and the Americas fall in between. Income per person is lower in the Americas than in other

9

regions except Africa, and dependence on primary products is greater. However, the share ofagriculture in GDP is lower and the share of the urban population greater than in Asia. Finally, thestability in the share of central government expenditure by continent is again notable.

Two special categories-the highly indebted countries and the Sub-Saharan African countries-show relationships for country groups that have particular problems and that have received particularscrutiny in structural adjustment loan programs. As a group the highly indebted countries-most aremiddle-income countries-fall into the medium dependence category for trade taxes, have a relativelysmall share if agriculture in GDP, and are relatively highly urbanized. By contrast, the Sub-SaharanAfrican countries are heavily dependent on trade taxes, very heavily dependent on exports of primaryproducts, and agriculturally based.

Trade exposure or openness (defined as 1/2[X + M]/GDP) appears to be directly related toincome per person and inversely related to the share of agriculture in GDP. The share of primaryproducts in GDP is lowest for the most open economies, but identical in the low and mediumexposure categories. No clear pattern emerges for dependence on trade taxes, although the mostclosed economies exhibit the greatest dependence. While one might expect the contrary to be true, itseems that the low income per person relationship with trade tax dependence (low trade exposurecountries are also low-income countries) holds sway here as elsewhere.

These cross-classifications identify very clearly the country characteristics associated withheavy dependence on trade taxes: low level of income per person, a strongly agriculturally basedeconomy, relatively heavy dependence on primary products, and not highly urbanized. The countrygroup that most closely matches these characteristics is Sub-Saharan Africa. These findings accordwell with expected relationships and suggest that sensitivity to trade policy reform is likely to bestrongest in Sub-Saharan African economies. The findings also suggest that any analysis that seeks to

define the relationship between trade liberalization and trade taxes must include the Sub-Saharan

African economies.Declining dependence on trade taxes. As per capita income grows and industrialization

proceeds, a widening of the tax phase and a shift toward a more efficient tax structure becomepossible (table 2) The collection costs of other taxes begin to fall relative to trade taxes asurbanization and the cash-based economy spread and administrative expertise grows. Severalempirical studies have investigated the relationship between fiscal dependence on trade taxes andeconomic development. The country samples in the studies examined here vary from forty-one toeighty-six and encompass various subperiods from 1954 through 1978. The studies regress the shareof trade taxes in total tax revenue on income per person and an index of openness, using the relativesize of the foreign trade sector as a proxy for taxable capacity.

The studies, although they encompass a number of time periods and a variety of countrysamples, obtained consistent results. One is the finding of a statistically significant negativerelationship for the aggregate sample between income per person and dependence on trade taxes, a

10

relationship found to be robust across time periods and for various proxies for development.Greenaway (1984), for example, used real income per person, the share of agriculture in GDP, andthe share of manufactures in GDP as :i1ernative proxies for development. Another common findingconcerns samples disaggregated by income (low income, middle income, and industrial economies).The inverse relationship holds for the middle-income countries, but it is weaker for the industrialeconomies and collapses completely for the low-income countries.' Several factors may explain thecollapse of the relationship for low-income countries. Income per capita as a proxy for development isat its most unsatisfactory in the case of low-income countries, and the pattern of trade policies amountthe least developed countries is much more varied than for other groups. Greenaway (1984) estimated

Table 2. Share of various taxes in government revenue, around 1980 (percent):raxes

Country grop (nwmber) Income and Domestic goods International Social securityprofit and services trade contributions

Industrial countries (20) 33.3 26.0 3.7 25.0Semi-industrial countries (15) 25.3 30.6 14.5 13.0Middle-income countries (55) 23.7 23.1 28.9 4.1Least developed countries (14) 17.0 21.7 41.6 1.6

Note: For a list of countries included in each group see Goode (1984, pp. 6, 91), who generally followed IMF groupings.

Source: Goode (1984, p. 91)

separate models for import and export taxes. Proxies were introduced in the export model to capturemarket power in export markets and the composition of trade effects, but neither performedsatisfactorily. For both import and export models, income per person and openness continued to bethe most important explanatory variables.

This cross-sectional work has been compleented by a little time-series work. Greenaway(1984) experimented with a sample of forty-four countries covering a period of sixteen years.Although the results are tentative, they are consistent with the cross-sectional findings. Detailed casestudy evidence is provided by Lewis (1968) and Khan (1988) for Pakistan, Idachaba (1975) forGhana, and Mulet (1979) for Ethiopia.

In summary, then, there is a clear inverse relationship between fiscal dependence on tradetaxes and economic development. a relationship that is especially strong in the case of middle-incomecountries. The least developed remain most heavily dependent on trade taxes and, therefore, the mostvulnerable to any sudden, large alteration in tariffs.

11

Expected changes in trade tax revenue

As noted earlier, trade reform may induce revenue changes in all categories of taxes, not justin trade taxes directly. The analysis here focuses on trade tax revenue only, however, both becausethe indirect tax revenue effects are difficult to identify and because they are likely to be smaller wherefiscal dependence on trade taxes is greater. The discussion, based on the relationship between tradereform and trade tax revenue developed above, considers which initial conditions (before thereform)-other conditions held constant-can be expected to result in higher or lower trade taxrevenue.

Import and tarif rate policies

The revenue effect ot reducing the overall average rate of import taxation is ambiguous,unless the effect of liberalization on individual categories of imports is known. The assumption thatall other conditions remain unchanged also gives rise to complications, since trade policy reforms arelikely to alter the composition of imports. If, for simplicity, however, it is assumed that demand andsupply elasticities are similar across broad categories of imports between developing countries, then itis possible to formulate an expected revenue effect. Since the maximum protective tariff is greaterthan the maximum-revenue tariff, countries with the highest average tariff levels can be expected tobe the most likely, through tariff reform, to move individual tariff rates toward the maximum-revenuetariff and thereby to expand tariff revenue. By contrast, if the average rate before reform lies below

the maximum-revenue tariff, tariff liberalization will tend to reduce revenue.An increase in tariff revenue can be expected, in particular, where imports . impeting with

domestically produced goods are a larger share of total imports and where the protective motive istherefore likely to have dominated the revenue motive.s Thus revenue expansion as a result ofgeneral tariff reduction would be most likely in the case of the larger, more industrialized developingcountries that have followed an inward-oriented import-substitution strategy for some time and have ahigh share of competing imports. Smaller countries or countries in the early stages of industrialization

are by contrast likely to have high shares of noncompeting (including capital and intermediate) goodsin total imports, which means that a high proportion of their import tax base is unlikely to be taxedfor protective reasons. Tariff rates are more likely to be below the revenue-maximizing level andtariff reduction is more likely to reduce tariff revenue than in the case of more industrialized

developing countries.The average maximum-revenue tariff rate for a typical developing country is of course

difficult to estimate. The rate varies by commodity according to the elasticity of import demand andthe scope for duty evasion through smuggling or false invoicing. Nonetheless, it is possible toguesstimate the order of magnitude involved as a guide for policy analysis. In the small-country casewith constant elasticity of import demand, the maximum-revenue tariff depends only on the elasticityof import demand (Johnson 1950-51). For a conservative assumption of -2 as the overall import

12

demand elasticity for developing countries, the maximum-revenue tariff rate is 100 percent.Admittedly this estimate may be upwardly biased by the constant elasticity assumption, but it is alsolikely to be downwardly biased by the specific elasticity value chosen, given developing countries'general dependence on imported fuels, intermediate goods, and capital goods.

Even if this estimated rate is adjusted for the tariff evasion likely to be induced by tariff ratesthis high, import duty collection is still likely to be significantly larger than average collection rates inmost developing countries.' The average rate of import collection (import duties as a percentage ofthe value of imports) before trade reform for the five countries considered in detail later in this study(C6te d'Ivoire, Jamaica, Kenya, Mauritius, and Morocco) was less than 20 percent and for some itwas even less than 10 percent. It is difficult to imagine that nominal scheduled rates in these countries

were higher than the maximum-revenue tariff. No doubt enforcement problems accounted for some ofthe shortfall between scheduled rates and collection rates. But it is more likely that these low averagerates of import taxation were the result of numerous tariff exemptions and the relative unimportance

of tariffs as a protective instrument, given the importance of noncompeting raw materials and

intermediate and capital goods in total imports and the pervasive use of quantitative restrictions

against competing imports.As in the case of tariff reform, so too with the reduction or removal of quantitative import

restrictions, the orientation of a country's trade strategy and the composition of its imports are likely

to be significant predictors of revenue impact. Quantitative restrictions are more likely to be pervasive

in inward-oriented economies and where import quotas and bans are a major instrument of protection

because of a high ratio of competing to total imports. Thus eliminating nontariff restrictions is likelyto be a more important way of boosting tariff revenue for the larger and more industrializeddeveloping countries than for less developed ones. Exceptions might be some of the poorest countrieswith the tightest foreign exchange constraints (in Sub-Saharan Africa, for instance), where the

rationing of scarce foreign exchange constitutes a de facto quantitative import restriction. Most of

these countries do not use auctions to ration foreign exchange, and potential revenue loss fromquantitative restrictions is likely to be greatest in relative terms the scarcer is foreign exchange. Butde facto restrictions on imports are likely to remain if the foreign exchange constraint is not

substantially alleviated by the reforms.Export and exchange rate pokcies. Many measures intended to reduce antiexport bias may

affect the government budget through other channels than trade tax revenues. Tax holidays (reducedtaxes) for firms located in export processing zones may reduce yields from profit taxes in the short to

medium term. Improving credit facilities or infrastructure for export activities will have implicationsfor the expenditure side of the budget. Direct influences on trade tax yields are likely to come through

duty drawback schemes (usually for nontraditional exports) and changes in export taxes (usually fortraditional exports). Exemption from import taxes on inputs will be revenue reducing if there were

nontraditional exports that previously received no duty drawback. The greater the share of

13

nontraditional exports in total exports and the greater the dependence of nontraditional exports onimported inputs before the reform, the greater the revenue reduction from the introdui ion of dutydrawbacks. Of course, if duty exemptions on inputs for export activities replace exemptions on inputsfor import-substitution activities and if the nontraditional export sector is smaller than the import-substitution sector, there may be no immediate revenue reduction.

Significant reduction in taxation of traditional exports is likely to reduce trade tax revenue.For nontraditional exports, export taxes are likely to be a more significant impediment to exportingthan for traditional exports, making total removal of export taxes revenue-contracting. Partial removalcould be revenue-expanding, however-albeit on a small scale-if nontraditional exports constitute asmall share of total exports, which is likely to be the case when nontraditional exports are taxed toany significant extent.

Predicting the revenue effects of exchange rate adjustment is particularly problematic. Exporttax yield is directly related to the degree of currency depreciation-and the degree of depreciationrequired to restore equilibrium is directly related to the extent of import protection. But it is also inthe most heavily protected economies that tariff reduction is most likely to increase tariff revenue.This revenue-expanding effect may therefore be offset if currency depreciation accompanies tariff ratereductions. The corollary is that currency depreciation tends to eliminate sources of revenuecontraction associated with tariff reductions.

Experience with structural adjustment lending and fiscal yield in developing countriesThe preceding section focused on an a priori appraisal of the conditions that might influence

fiscal yield following trade policy reform in the context of structural adjustment loans (SALs). Theseconditions were related to prereform tariff levels, tariff dispersion, quotas, and exemptions. Thepossible combinations of initial conditions are numerous. Moreover, the importance of reformmeasures and their impact on fis-al yield will be strongly affected by institutional constraints andfeedback effects, which may differ by country. For these reasons, this section focuses morespecifically on the detail of individual country experiences.

Three important points need to be noted in an analysis of this type. First, the sheer number of

countries that have had SALs with some trade policy components (more than forty countries)precludes a detailed analysis of the experience of all of them in a study such as this one. Second, theSAL program is only about a decade old, and many of the policy reforms they have introduced are

intended to have effects in the medium to long term. Although some fiscal effects occur quickly, itmay still be too early in many cases to evaluate the economic effects of SALs. Third, some countrieshave had more than one SAL with trade policy components.

The next section examines the initial conditions in a subsample of eleven SALcountries-Chile, C6te d'Ivoire, Ghana, Jamaica, Kenya, Mauritius, Mexico, Morocco, Panama, thePhilippines, and Tunisia-to identify any obvious patterns with respect to revenue effects following a

14

SAL program. This sample provides wide coverage of country characteristics (size, geographicallocation, and population) and economic characteristics (debt position, income per capita, and tradeorientation). The following section then focuses in greater detail on the experience of five countries,three that experienced revenue expansion-Jamaica, Kenya, and Mauritius-and two that experiencedrevenue contraction-C6te d'Ivoire and Morocco. Together, the analysis of initial conditions and thedetailed examination of experience in these countries will provide a foundation for identifying some of

the factors that influence revenue expansion or contraction with trade policy reform.

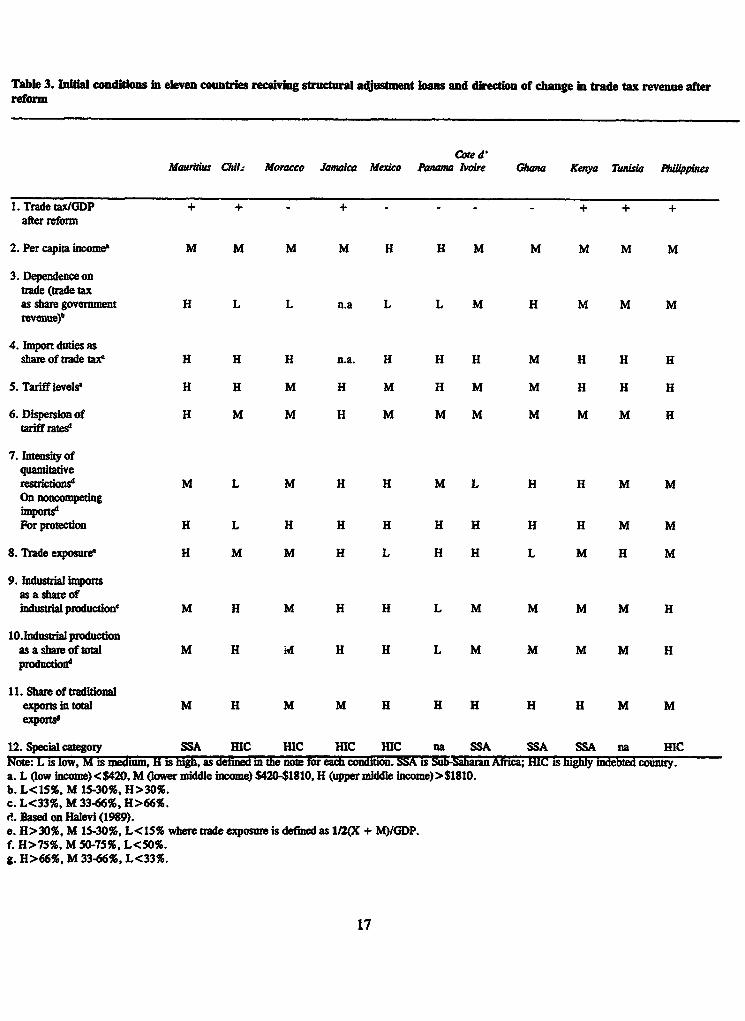

Initial conditions: experience in eleven developing countriesTable 3 summarizes initial conditions-most of them identified in the preceding section as

likely to have an important impact on fiscal yield after reform-for the eleven sample SAL countries.

Fiscal yield does not appear to vary systematically either with overall dependence on trade taxes (row3) or with the importance of import duties in trade taxes (row 4). High, low, and nedium dependencecases are found both among countries that have evidently experienced a rise in trade taxes as a shareof GDP and among those that have experienced a fall. In all but one case (Ghana) import duties are,overwhelmingly, the main source of trade taxes. Judging from this sample, the importance of import

duties in trade taxes does not appear to have a significant bearing on post-reform fiscal yield.

It was argued above that the probability that trade liberalization would result in an increase inrevenue was greater when tariffs started at a level above the maximum-revenue tariff. The difficulty

lies in estimating maximum-revenue tariffs, which are likely to vary from country to country. Onealternative is a qualitative analysis, based on a classification such as Halevi's (1989), who categorizes

tariff structures as high, medium, or low. Other things being equal, the probability that initial tariffsexceed maximum-revenue tariffs is greater the higher the initial tariffs. All six countries that

experienced revenue gains from reform (Chile, Jamaica, Kenya, Mauritius, the Philippines, and

Tunisia) had high initial tariff levels (row 5). All the other countries experienced revenue contraction

and all but one had initial tariffs in the medium range. Some caution is required in interpreting this

finding, however. Scheduled tariffs on competing imports may be high for protective purposes, but

overall or average collection rates may be relatively low if noncompeting imports predominate.Another hypothesis presented in the preceding section is that high dispersion of tariff rates is

likely to be associated with a higher probability of revenue gain. The three countries with highdispersion all achieved revenue expansion from reform; results were mixed for the other countries,which all had medium dispersion (row 6): thus the comparison of country experiences offers some

support for the validity of this relationship.The association between broad coverage of quantitative restrictions and a high potential for

revenue gains from reform that was posited above also receives some support from the case study

comparison. In all countries where revenue expansion occurred (except Chile), quantitative

restrictions were (initially) either high or medium. But they wcre also high or medium in cases where

15

revenue contraction resulted. This apparent lack of a decisive pattern arises because pervasivequantitative restrictions are a necessary but not sufficient condition fo revenue expansion. Thesufficiency condition is that any dismantled quantitative restrictions be replaced with equivalent tariffs.

Half the sum of exports plus imports as a share of GDP (trade exposure) was used as a proxyfor the trade tax base. All the case study countries with revenue gains had high or medium tradeexposure, as did three of the five revenue-contracting countries-the other two were in the lowcategory for trade exposure. Overall, the average index of trade exposure was 43 percent for therevenue gainers and 27 percent for the revenue losers. Thus the comparison suggests some tentative

association between revenue yield and trade exposure.Two other variables identified above as having an impact on revenue-the share of competing

imports in total imports and the size of the industrial sector-are difficult concepts to capture in

simple summary statistics. Industrial imports as a share of industrial production and industrialproduction as a share of total production are two possible indicators of these concepts (rows 9 and

10). There is no obvious association between revenue performance and either of these indicators,probably because these ratios can be interpreted in different ways for different countries.

Last, the analysis in the preceding section posited an association between revenue and the

share of traditional exportables in total exports for the case of export tax reductions. For the casestudy countries no obvious pattern emerges for dependence on traditional exportables (row 11).

All these patterns of country characteristics and revenue change suggest that revenue

expansion has tended to occur in economies with relatively wide dispersion of tariff rates, extensive

use of quantitative restrictions, and relatively high levels of exposure to trade. Superficially, revenueexpansion also appears to have occurred where initial tariff rates were relatively high. But, after

allowing for low or no duties on noncompeting imports and for duty-exemptions, high scheduledtariffs on competing imports may not translate into high average rates of duty. Indeed, as is discussed

in the next section, only some of the countries experiencing revenue-expansion reduced tariffs while

others actually increased tariffs overall as part of an adjustment program.

Trade policy reform and fiscal yield experience in five developing countries

So far, this section has defined the broad parameters of possible influences on revenue. Moredetailed, country-speciic analysis of initial conditions and, more important, of reform packages andactual outcomes is required to identify more precisely the outcome of what is, after all, a highlycomplicated general equilibrium process. This section focuses on the experience of five countries with

SALs that included trade reform components. In three of them-Jamaica, Kenya, and

Mauritius-revenue expansion followed SAL reforms; in the other two-C6te d'Ivoire and

Morocco-revenue contraction resulted.

16

Table 3. Initial conditions in eleven countries receiving structural adjustment loans and direction of change In trade tax revenue afterreform

Coe d'MauritiWs h. Moracco Jamaica Mexico Panama Ivoire Ghana Kenya Tunisia P*ilipines

1. Trade tax/GDP + + - + - - - - + + +after reform

2. Per capita income M M M M H H M M M M M

3. Dependence ontrade (trade taxas share government H L L n.a L L M H M M Mrevenue)

4. Import duties asshare of rade tax H H H n.a. H H H M H H H

5. Tariff levels, H H M H M H M M H H H

6. Dispersion of H M M H M M M M M M Htariff ratee

7. Intensity ofquantitativerestrictions M L M H H M L H H M MOn noncompetingimportsFor protection H L H H H H H H H M M

8. Trade exposure H M M H L H H L M H M

9. Industrial importsas a share ofindustrialproduction' M H M H H L M M M M H

10.Industrial productionas a share of total M H M H H L M M M M Hproduction

11. Share of traditionalexports in total M H M M H H H H H M Mexports'

12. Special category SSA HIC HIC HIC HIC na SSA SSA SSA na HICNote: L is low, M is medium, H is high, as defined in the note for each condition. SSA is Sub-Saharan Africa; HIC is highly indebted country.a. L (low income)<$420, M (lower middle income) $420-$1810, H (upper middle income)>$1810.b. L<15%, M 15-30%, H>30%.c. L<33%, M 33-66%, R>66%.0. Based on Halevi (1989).e. H>30%, M 15-30%, L<15% where trade exposure is defined as 1/2(X + M)/GDP.f. H>75%. M 50-75%, L<SO%.g. H>66%, M 33-66%, L<33%.

17

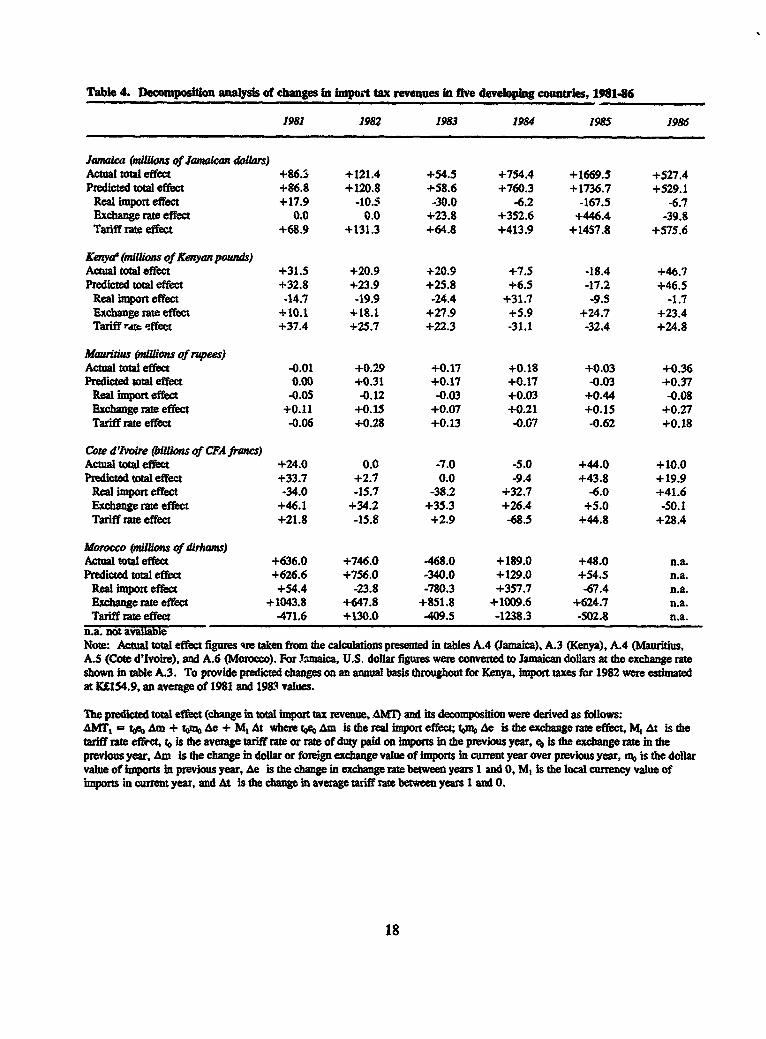

Table 4. Decomposition analysis of changes in Import tax revenues in five developing countries, 198146

1981 1982 1983 1984 1985 1986

Jamaica (millions of Jamaican dollars)Actual total effect +86.5 +121.4 +54.5 +754.4 +1669.5 +527.4Predicted total effect +86.8 +120.8 +58.6 +760.3 +1736.7 +529.1

Real import effect +17.9 -10.5 -30.0 -6.2 -167.5 -6.7Exchange rate effect 0.0 0.0 +23.8 +352.6 +446.4 -39.8Tariff rate effect +68.9 +131.3 +64.8 +413.9 +1457.8 +575.6

Kenya (milUons of Kenyan pounds)Actual total effect +31.5 +20.9 +20.9 +7.5 -18.4 +46.7Predicted total effect +32.8 +23.9 +25.8 +6.5 -17.2 +46.5

Real import effect -14.7 -19.9 -24.4 +31.7 -9.5 -1.7Exchange rate effect +10.1 +18.1 +27.9 +5.9 +24.7 +23.4Tariff rtv effect +37.4 +25.7 +22.3 -31.1 -32.4 +24.8

Mauiaus (millons of rupees)Actual total effect -0.01 +0.29 +0.17 +0.18 +0.03 +0.36Predicted total effect 0.00 +0.31 +0.17 +0.17 -0.03 +0.37

Real import effect -0.05 -0.12 -0.03 +0.03 +0.44 -0.08Exchange rate effect +0.11 +0.15 +0.07 +0.21 +0.15 +0.27Tariff rate effect -0.06 +0.28 +0.13 -0.07 -0.62 +0.18

Core d'Ivoire (illions of CPA francs)Actual total effect +24.0 0.0 -7.0 -5.0 +44.0 +10.0Predicted total effect +33.7 +2.7 0.0 -9.4 +43.8 +19.9

Real import effect -34.0 -15.7 -38.2 +32.7 -6.0 +41.6Exchange rate effect +46.1 +34.2 +35.3 +26.4 +5.0 -50.1Tariff rate effect +21.8 -15.8 +2.9 -68.5 +44.8 +28.4

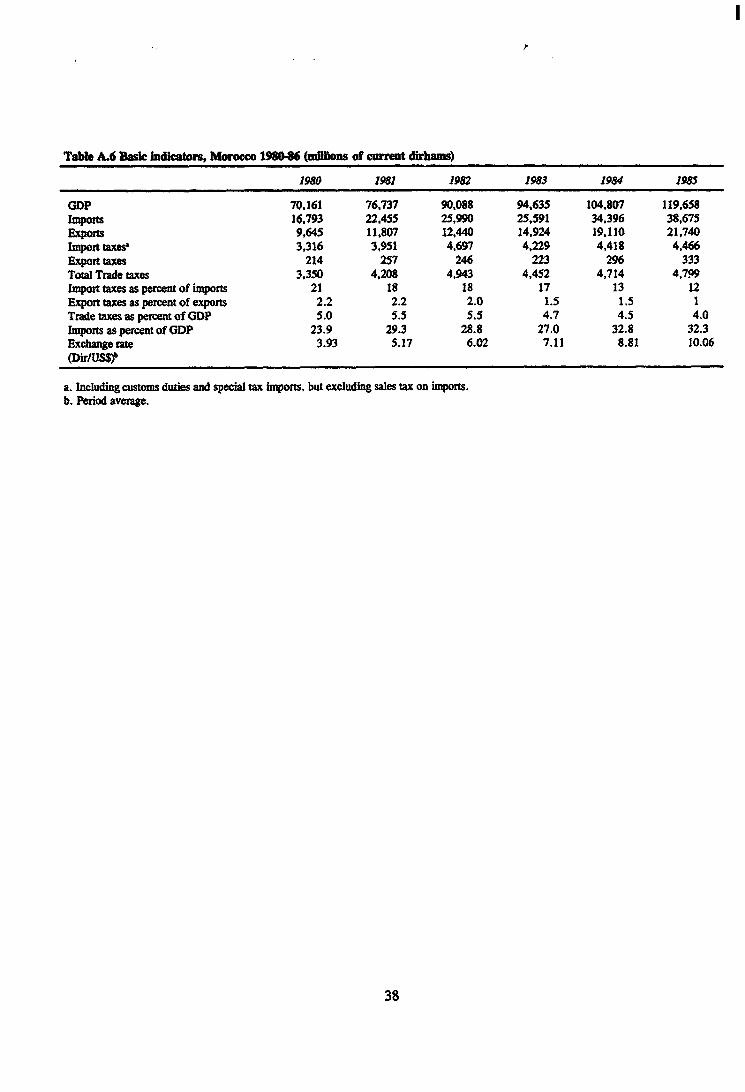

Morocco (millions of dirhams)Actual total effect +636.0 +746.0 -468.0 +189.0 +48.0 n.a.Predicted total effect +626.6 +756.0 -340.0 +129.0 +54.5 n.a.

Real import effect +54.4 -23.8 -780.3 +357.7 -67.4 n.a.Exchange rate effect +1043.8 +647.8 +851.8 +1009.6 +624.7 n.a.Tariff rate effect -471.6 +130.0 -409.5 -1238.3 -502.8 n.a.

n.a. not availableNote: Actual total effect figures re taken from the calculations presented in tables A.4 (Jamaica), A.3 (Kenya), A.4 (Mauritius,A.5 (Cote d'Ivoire), and A.6 (Morocco). For Jamaica, U.S. dollar figures were converted to Jamaican dollars at the exchange rateshown in table A.3. To provide predicted changes on an annual basis throughout for Kenya, import taxes for 1982 were estimatedat K£154.9, an average of 1981 and 1983 values.

The predicted total effect (change in total import tax revenue, AMT) and its decomposition were derived as follows:AMT, to Am + to% Ae + M, At where toev Am is the real import effect; tom Ae is the exchange rate effect, M, At is thetariff rate effect, to is the average tariff rate or rate of duty paid on imports in the previous year, e is the exchange rate in theprevious year, Am is the change in dollar or foreign exchange value of imports in current year over previous year, n), is the dollarvalue of imports in previous year, Ae is the change in exchange rate between years 1 and 0, M, is the local currency value ofimports in current year, and At is the change in average tariff rate between years 1 and 0.

18

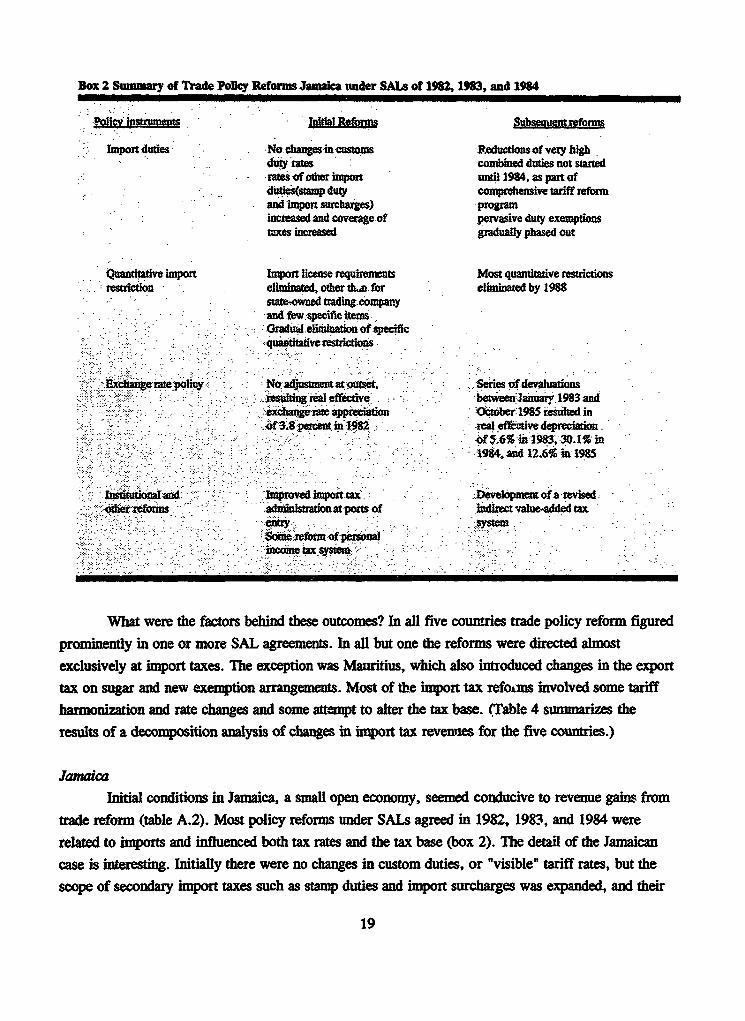

Box 2 Summary of Trade Policy Reforms Jamaica under SALs of 1982, 1983, and 1984

.olicy instrments Initial RfrsSubseounatsofouns

Import duties No changesin customs Reductionsof vey highduty rates combined duties not startedTates of other import until 1984. as part ofduties(stamp duty comprehensive tariff reformand impon surcharges) programincreased and coverageof pervasive duty exemptionstaxes increased gradually phased out

Quantitative import Import license requirements Most quantitative restrictionsrestriction eliminated, other the for eliminated by 1988

state-owned trading companyand few specific itemsGradual e -minationofspecificquatitativerestritions

Exchange rate policy Iadjustmentat tet Series of-devaluationsresulting neal ef fecive betweea January 1983 andchange rat appreciation October 1985 resulted in

fitpercent in 1982 real eMctive depreciationof 5.6% in 1983,30.1% in18. and 12.6% in 1985

Istonland Improved impoit ta Developmentof a revisedother reforms adeAinistrationat ports of indirect value-added tax

-.entry. sysemSonereftm or personaincame tax system

What were the factors behind these outcomes? In all five countries trade policy reform figured

prominently in one or more SAL agreements. In all but one the reforms were directed almost

exclusively at import taxes. The exception was Mauritius, which also introduced changes in the export

tax on sugar and new exemption arrangements. Most of the import tax refoims involved some tariff

harmonization and rate changes and some attempt to alter the tax base. (Table 4 summarizes the

results of a decomposition analysis of changes in import tax revenues for the five countries.)

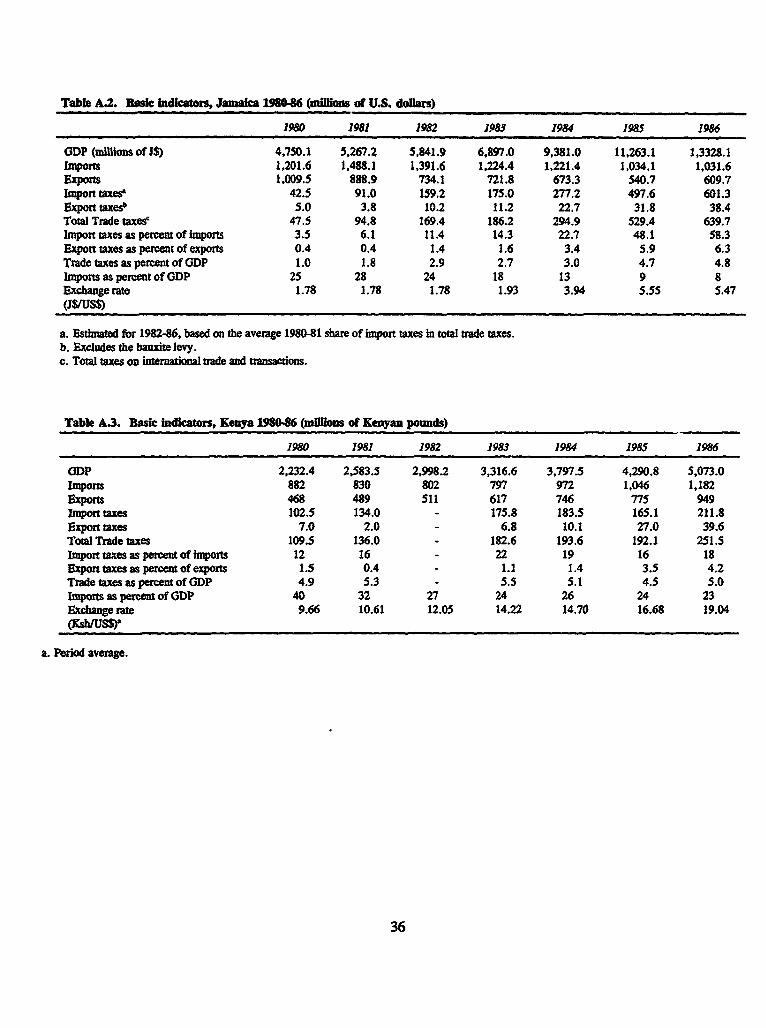

Jamaica

Initial conditions in Jamaica, a small open economy, seemed conducive to revenue gains from

trade reform (table A.2). Most policy reforms under SALs agreed in 1982, 1983, and 1984 were

related to imports and influenced both tax rates and the tax base (box 2). The detail of the Jamaican

case is interesting. Initially there were no changes in custom duties, or "visible" tariff rates, but the

scope of secondary import taxes such as stamp duties and import surcharges was expanded, and their

19

rates were increased. Exemptions to import duties-which had been pervasive prior to reform-werereduced. As a result of these measures, the overall import duty rate increased, and this increase wasassociated with increased revenue collections.

There were substantial revisions in quantitative restrictions. Before SAL I in 1982, licensingprovisions applied to all imports, and there were 364 specific quantitative restrictions. The SALsrequired that licensing be lifted for all but a few state-owned companies. In addition many quantitativerestrictions were eliminated, and by 1988 nontariff barriers affected only about 8.5 percent ofimports. No formal provisions were made for replacing the quantitative restrictions with equivalent

tariffs, although some de facto replacement occurred through an expansion of the scope of stampduties and import surcharges. Average rates of collection on imports were very low prior to the first

SAL in 1982: 3.5 percent in 1980 and 6.1 percent in 1981 (table A.2). From such low average levels,

the rise in tariff rates implicit in increases in stamp duties and surcharges would be expected to be

revenue-expanding. The view that overall rates of duty were on average below their maximum-

revenue levels prior to the reforms is supported by the results of the decomposition analysis for

Jamaica: the tariff rate effect is positive for all years covered, but increases dramatically after 1983(table 4).

Pressures for exchange rate adjustment were initially resisted. The decomposition analysisshows no exchange rate effect on revenues in 1981 and 1982. In 1983, however, parallel market

transactions were legalized. Subsequently, the parallel and official rates were anified. The Jamaican

dollar fell from J$1.78 = US$1, to J$6.4 = US$1 between 1983 and 1985 and then stabilized. With

the reduction in the over-valuation of the exchange rate and the removal of quantitative restrictions,

the structure of imports changed. For instance, the share of consumer goods in total imports doubled

(from 11 percent to 21 percent). The 300 percent currency depreciation had a major impact on thesize of the tax base as well as on its composition. While the volume and foreign currency value of

imports fell sharply after 1982, the depreciation sustained the value of imports in local currency

terms. The decomposition analysis shows substantial positive revenue effects associated with

depreciation in 1984 and 1985 (table 4).Changes in the exchange rate also affected non-trade tax-related revenues associated with

specific exports. Bauxite levy receipts, for example, rose sharply in 1984 as devaluation induced a

rise in export earnings. But the decline in bauxite production meant that the bauxite levy as a share of

GDP did not increase over the period as a whole. Other trade-related policy changes may also haveaffected revenue, in particular the cutbacks in the activities of state marketing boards in bananas,coffee, cocoa, citrus, and pimento and the introduction of a duty drawback scheme (which did notprove very effective). These changes were unlikely to have caused significant revenue-contraction.

Indeed over the period as a whole tax effort increased, rising form 26.9 percent of GDP in 1982 to

30.4 percent in 1986.

20

While Jamaica's overall progress with policy reform during this period was incomplete, the

impact on trade revenue was dramatic. The tariff collection rate (import duties as a share of total

imports) rose from 12 percent in 1982 to nearly 60 percent in 198C, despite a massive contraction in

imports as a share of GDP (from 24 percent to 8 percent). This source of shrinkage in the tax base

was (approximately) offset in absolute terms by the substantial devaluation that occurred after 1983.

The decomposition analysis shows that the negative real import effect for 1981-86 was more than

offset by a significant, positive tariff rate effect, especially in 1984-85, and by exchange rate

depreciation between 1983 and 1985. So although the import tax base contracted sharply, the rate of

import tax collection rose enough to boost trade taxes as a share of GDP from 2.7 percent in 1983 to

4.8 percent in 1986. Revenue expansion would thus appear to have resulted from an increase in

collection rates due to improved tax administration at ports of entry and the introduction of additional

import-specific taxes in 1982 as Jamaica phased out quantitative restrictions. Thus, although no

formal provisions were made to replace quantitative restrictions with equivalent tariffs, the tariff

surcharges had that effect.

KenyaKenya also experienced revenue expansion following its SAL progrms. Prior to Kenya's first

SAL in 1980 the average tariff collection rate was only 12 percent, although scheduled nominal tariff

rates ranged from zero to over 100 percent. With the relaxation of import bans in 1980-81 (see box

3), tariffs were raised on some 150 items, many of them intermediate goods (about 11 percent of

imports), and a 10 percent surcharge was imposed on all dutiable items, including many of the items

removed from the banned list.

21

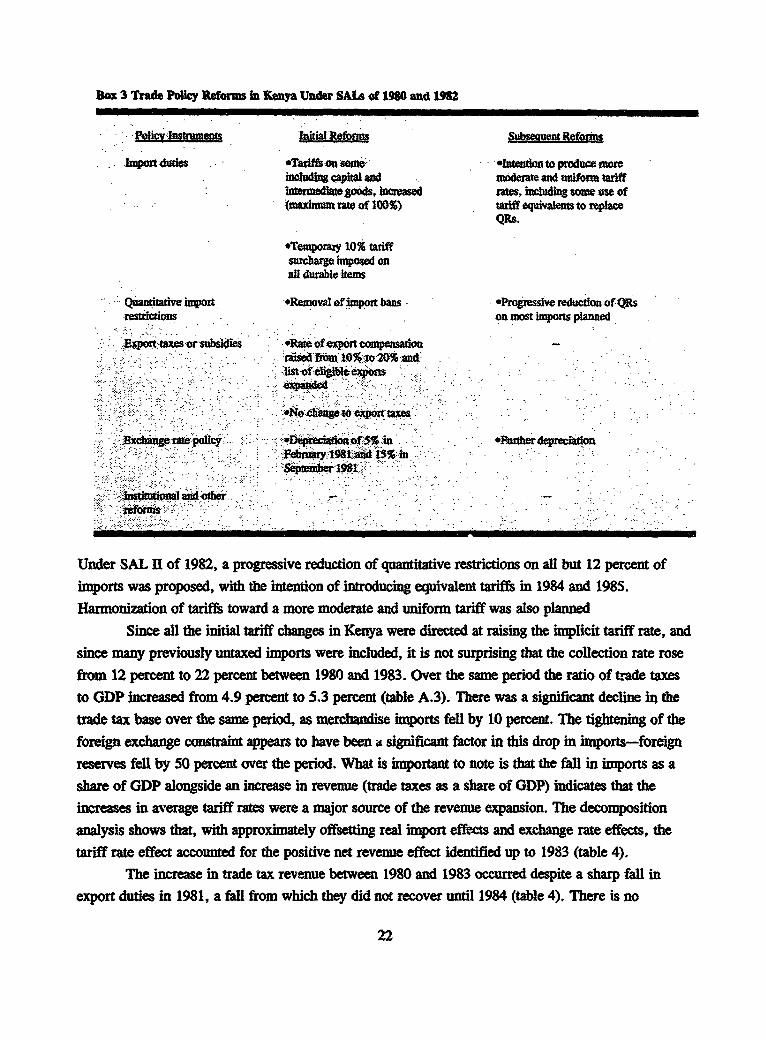

Box 3 Trade Policy Reforms in Kenya Under SALs of 1980 and 1982

oneitial Reforms Subseqent Ref*rMs

Import duties *Tadf-fson ome *Intention to produce moreincluding capital and moderate and unifouM tariffintersmediategods, increased sat, including sMe use of(maximum rate of 100%) tariff equivalents to replace

QRs.

*Temporary 10% tariff

surcharge imposed onall duraWble items

Quantitative import *Removalof import bans *Progressive reduction of QRsresuictions on most imports planned

Export taxes or subsidies *Raesof export compensationraisedirom 10% to 20% andlist of dlg il ex ions

Exchange rate policy i %in unher depreciationFebrnary 1981 ad1% inS pteberl981

Intoal and other..:foT f

Under SAL I of 1982, a progressive reduction of quantitative restrictions on all but 12 percent ofimports was proposed, with the intention of introducing equivalent tariffs in 1984 and 1985.Harmonization of tariffs toward a more moderate and uniform tariff was also planned

Since all the initial tariff changes in Kenya were directed at raising the implicit tariff rate, and

since many previously untaxed imports were included, it is not surprising that the collection rate rose

from 12 percent to 22 percent between 1980 and 1983. Over the same period the ratio of trade taxesto GDP increased from 4.9 percent to 5.3 percent (table A.3). There was a significant decline in the

trade tax base over the same period, as merchandise imports fell by 10 percent. The tightening of theforeign exchange constraint appears to have been A significant factor in this drop in imports-foreign

reserves fell by 50 percent over the period. What is important to note is that the fall in imports as ashare of GDP alongside an increase in revenue (trade taxes as a share of GDP) indicates that theincreases in average tariff rates were a major source of the revenue expansion. The decomposition

analysis shows that, with approximately offsetting real import effects and exchange rate effects, thetariff rate effect accounted for the positive net revenue effect identified up to 1983 (table 4).

The increase in trade tax revenue between 1980 and 1983 occurred despite a sharp fall inexport duties in 1981, a fall from which they did not recover until 1984 (table 4). There is no

22

evidence of changes in export tax rates, so the fall in export tax is probably reflected in the exportbase. Indeed, the value of coffee exports fell from $292 million in 1980 to $241 million in 1983,while that of tea exports fell from $172 million to $153 million.

Between 1983 and 1985 trade taxes as a share of GDP fell from 5.5 percent to 4.5 percent,with the collection rate for import taxes falling from 22 percent to 16 percent and the rate for exportduties increasing from 1.1 percent to 4.2 percent.Why did the trade tax share fall? There was somerationalization of the tariff regime during this period, but only a modest reduction of rates, and littleprogress was made in liberalizing quantitative restrictions and replacing them with equivalent tariffs.The value of merchandise imports increased by some 30 percent, and some exchange rate depreciationtook place. The principal driving force, however, appears to have been a relaxation of the foreignexchange constraint. Foreign exchange reserves rose from $281 million in 1982 to $448 million in1984, and there was a significant increase in external loans of almost $500 million in 1984. Thus,despite an expanding (import and export) tax base, the trade tax to GDP ratio fell. This fall can beattributed to the fall in collection rates on imports. The decomposition analysis shows large negativetariff-rate effects for 1984 and 1985, which were offset in 1984 (only) by the growth in imports (table

4).The increase in the trade tax to GDP ratio after 1984 can be largely explained by an

exchange-rate induced increase in the tax base. The decomposition analysis shows large positiveexchange rate effects in 1984 and 1985 for import tax revenues. In addition there was a substantialincrease in export earnings, particularly from coffee exports (up from $281 million to $479 million).Provisional estimates suggest that the rising trend for the collection rate, the trade tax ratio, and the

import base continued into 1987.Changes in the composition of the trade tax base between 1983 and 1987 may also have had

some slight effect. Among imports, the importance of fuels and lubricants fell as that of transportequipment rose, although it is not clear whether these changes were directly due to the trade policymeasures. While the impact on revenue is unclear, the direction of change should have been upward,assuming that fuels and lubricants am subject to excise duties while transportation equipment issubject to import duties. Among exports, the relative importance of coffee increased, a change thatshould also have boosted revenue. As with the change in the composition of imports, however, thischange appears to have had little to do with the trade policy measures-indeed, the share ofnontraditional exports actually fell marginally between 1980 and 1986.

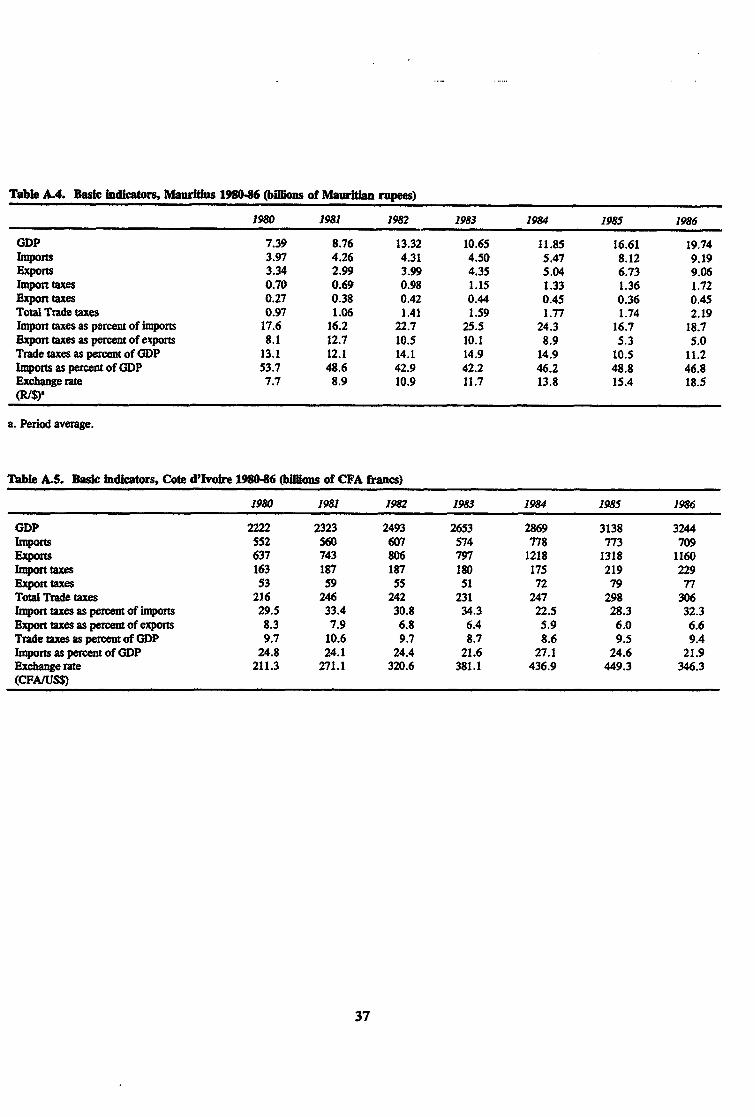

MauritiusLike Jamaica and Kenya, Mauritius also experienced revenue expansion following its SAL

programs. The SAL reforms affected both export and import duties. On the export side reformsincluded changes in exemption and assessment arrangements (see box 4). Lifting the export taxexemption ceiling for sugar and offering duty drawbacks to nontraditional exports were

23

unambiguously revenue contracting, at least in the short run. After 1994-85, however, export tax

revenue increased as the higher guaranteed price offered by the EC led to a rise in the value of sugar

exports.

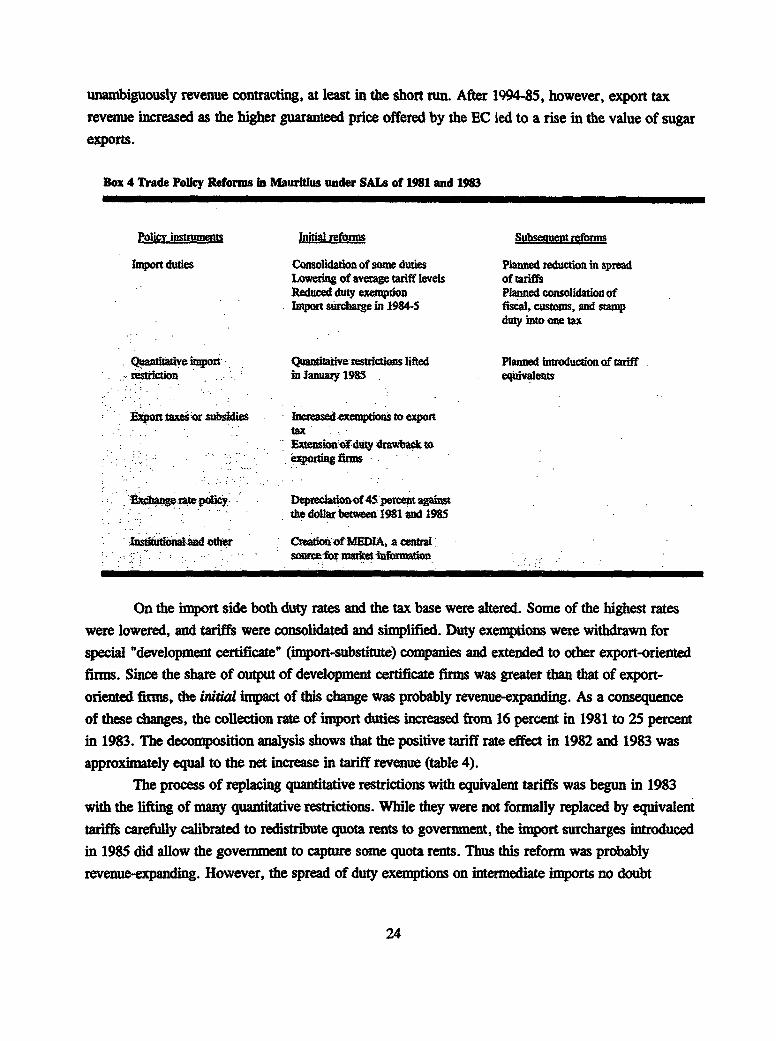

Box 4 Trade Policy Reforms In Mauritlus under SAL of 1981 and 1983

Policy instruments Initial refouns Subsequent reforms

Import dudes Consolidation of some duties Planed reduction in spreadLowering of average tariff levels of tariffsReduced duty exemption Planned consolidation ofImport surchar e in 1984-5 fiscal, customs, and stamp

duty into one tax

Quantitative import Quantitative restrictions lifted Planned introduction of tariffrestriction january 1985 equivalents

aport taxes or subsidies Increased exemptions to exporttaxExtension of duty drawback toeporting anrms

dxcange rateopolicy Depreciationof45 percent againstthe doUar between 1981 and 1985

nsdtutionatand edier Creati of MEDIA, a centralsourcefor market infornation

On the import side both duty rates and the tax base were altered. Some of the highest rates

were lowered, and tariffs were consolidated and simplified. Duty exemptions were withdrawn for

special "development certificate" (import-substitute) companies and extended to other export-oriented

firms. Since the share of output of development certificate firms was greater than that of export-

oriented firms, the initial impact of this change was probably revenue-expanding. As a consequence

of these changes, the collection rate of import duties increased from 16 percent in 1981 to 25 percent

in 1983. The decomposition analysis shows that the positive tariff rate effect in 1982 and 1983 was

approximately equal to the net increase in tariff revenue (table 4).

The process of replacing quantitative restrictions with equivalent tariffs was begun in 1983with the lifting of many quantitative restrictions. While they were not formally replaced by equivalent

tariffs carefully calibrated to redistribute quota rents to government, the import surcharges introduced

in 1985 did allow the government to capture some quota rents. Thus this reform was probably

revenue-expanding. However, the spread of duty exemptions on intermediate imports no doubt

24

contributed to the overall negative tariff rate effects in 1984 and 1985 shown in the decompositionanalysis, although the import surcharge effect is discernible in 1986 (table 4).

Mauritius introduced the strongest package of export incentives for nontraditional exportsamong the five sample countries: improvements in the duty drawback scheme, tax exemptions forexporters, and such institutional improvements as an export credit guarantee and insurance scheme, acentral source of information and market intelligence (MEDIA), and an industrial coordination unit toassist potential foreign investors. These measures, together with the increasing attractiveness ofMauritius as a location for offshore investment, contributed to the export-led growth of th; economyand to strong growth in the tax base (imports and exports) after 1982 (table A.4). The decompositionanalysis shows a positive real import effect in 1984 and 1985 and overall for the period 1981-86.

Two other important factors in the Mauritian case are changes in the exchange rate and innontrade taxes. The exchange rate was permitted to depreciate in real terms over the adjustmentperiod, resulting in a positive exchange rate effect on import duties throughout 1981-86 (table 4).

Changes in the tax system-a land development tax, a tax on seasonal residences, a land transfer tax,and a withholding tax on dividends-helped alleviate the fear of revenue-contraction from the tradereforms, thus strengthening the government's resolve to see the reforms through.

Most of the revenue effects of these changes were positive (table A.4). Between 1981 and1984 total trade taxes increased by 67 percent in nominal terms or by 23 percent relative to GDP.Revenue from both export and import taxes increased in absolute terms, but the collection rate on

exports fell by more than 40 percent, despite strong export growth, largely because of changes inexemption arrangements and export rates for sugar. By contrast the collection rate for imports

increased by 50 percent, due to changes in tariff rates and the import tax base. The rate changes wererelatively modest and in an upward direction initially, and together with the surcharges accompanyingremoval of quantitative restrictions, were probably revenue-expanding. The tax base changes-growthin the local currency value of imports and the significant reduction in exemptions-would also havebeen revenue-expanding.

The picture changes in 1985 and 1986, several years after the second SAL. Both import andexport growth remained strong, and import duty collections continued to rise in nominal terms. Butwhile duty collections rose 29 percent between 1984 and 1986, imports grew by an even faster 68percent. The drop in the collection rate from 24 percent to just under 19 percent is consistent withincreased imports of exempt and duty-free items and falling nominal rates as liberalization becameeffective. The strong growth of imports (more than 20 percent a year in real terms between 1984 and

1988), however, ensured that actual collections from imports more than doubled over the perioddespite the fall in the collection rate.

25

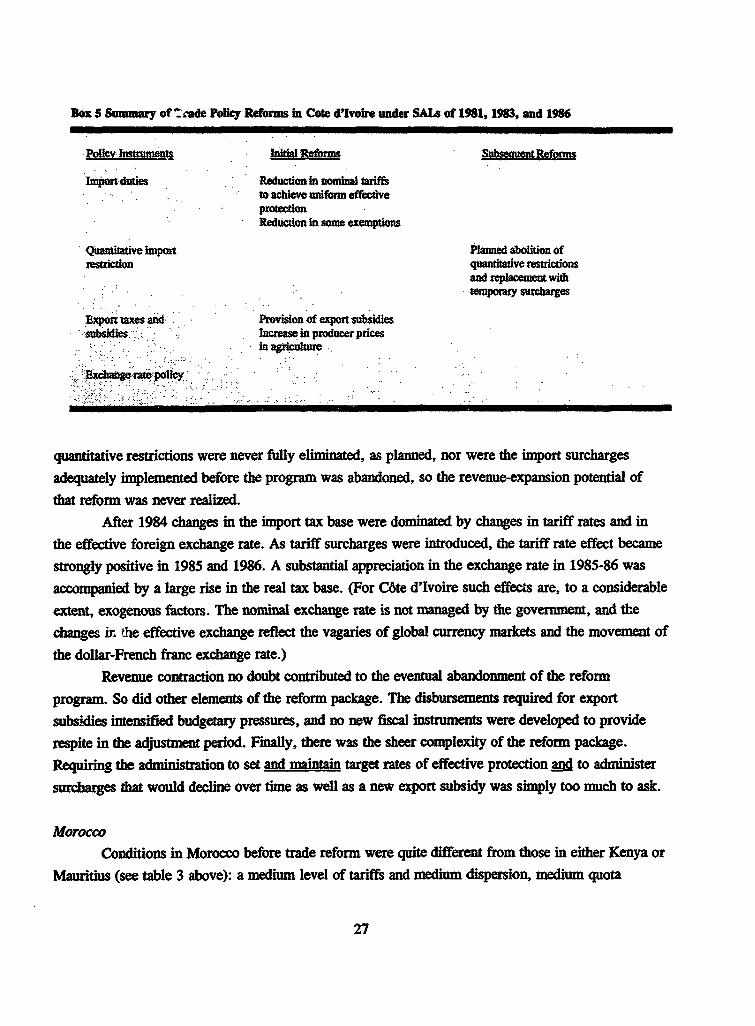

Cte d'IvoireOf the five countries considered in this section, C6te d'Ivoire proposed the most far-reaching

and ambitious reforms (box 5). The 1981 stabilization program provided for raising producer pricesin agriculture, restructuring state enterprises, and increasing nontrade taxes. Trade policy reforms

were initiated under the terms of the 1983 SAL, to be phased in over 1985-90. Nominal tariff rateswere to be lowered and their dispersion narrowed, the objective being to create a uniform effectiveprotection of 40 percent. Since effective protection rates in 1980 ranged from 14 percent to 355percent, this rep'esented a significant degree of liberalization for many industries. Export subsidies

would be granted so that exporters (of some products) would also benefit from an effective protectionrate of 40 percent. Quantitative restrictions- which had affected about 45 percent of allimports-began to be dismantled in 1985, and all quotas were to be removed by the end of 1986. Toease adjustment, temporary import surtaxes of 10 to 50 percent were proposed, to be phased out

between 1986 and 1990. Tariff exemptions were eliminated, except for domestic producers of

intermediate goods.This reform package altered both tax rates and the tax base. Nominal tariffs, which were

substantially lower than effective tariffs before reform, were reduced less than were effective tariffs.

The nominal exchange rate remained stable in the early reform period, but the effective rate againstthe dollar depreciated steadily up to 1985, in large measure because of appreciation of the dollar(table A.5). The import and export tax base contracted in real or dollar terms until 1983, then

expanded in 1984 and 1985 (as cocoa prices rose). However, import duty collection rates, which had

risen somewhat between 1980 and 1983, fell back sharply in 1984 before recovering to the prereform

rate of 30 percent in 1986. Export duty collection rates remained fairly stable in the postreform

period. Between 1981 and 1984 trade taxes as a share of GDP fell by two percentage points. The

decomposition analysis shows that the actual total change in import tax revenues in CMte d'Ivoire