The European Wireless The European Wireless Data Market Data Market Mark Holden Mark Holden Wireless Data Service Director Wireless Data Service Director Strategy Analytics Strategy Analytics [email protected] [email protected] October 1998 October 1998

The European Wireless Data Market Mark Holden Wireless Data Service Director Strategy Analytics [email protected] October 1998.

Dec 18, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

The European Wireless The European Wireless Data MarketData Market

Mark HoldenMark HoldenWireless Data Service DirectorWireless Data Service Director

Strategy AnalyticsStrategy Analytics

[email protected]@strategyanalytics.com

October 1998October 1998

October 1998 2

AGENDAAGENDA

1.1. Current Market StatusCurrent Market Status

-- Networks, devices, applications, Networks, devices, applications, usersusers

2.2. Future DevelopmentsFuture Developments

-- Cellular enhancementsCellular enhancements

3.3. Market ForecastsMarket Forecasts

-- Differences between 1997 & 1998 Differences between 1997 & 1998 forecastsforecasts

October 1998 3

Current Status - NetworksCurrent Status - Networks

Cellular the dominant wide-area technologyCellular the dominant wide-area technology Consistent SMS usage growth across EuropeConsistent SMS usage growth across Europe

Operator shift towards the verticalsOperator shift towards the verticals

Growing focus on coverage issues & service/ quality Growing focus on coverage issues & service/ quality assurance levelsassurance levels

The operator as ISPThe operator as ISP

Dedicated operators face an uncertain futureDedicated operators face an uncertain future

TETRA vs. TETRAPOLTETRA vs. TETRAPOL

Interactive paging: is there a future in Europe?Interactive paging: is there a future in Europe?

October 1998 4

Current Status - Devices/EquipmentCurrent Status - Devices/Equipment

Devices & equipment are a major user concernDevices & equipment are a major user concern Leveraging existing portable devices & systemsLeveraging existing portable devices & systems

Cost of accessories (e.g. PC cards)Cost of accessories (e.g. PC cards)

Practicalities of usePracticalities of use

Ease of operation & human computer interfaceEase of operation & human computer interface

Smart phones & hand-held computers not yet Smart phones & hand-held computers not yet widely accepted by European corporateswidely accepted by European corporates

October 1998 5

Current Status - ApplicationsCurrent Status - Applications

Key user segments are the verticalsKey user segments are the verticals Remote information access & short messagingRemote information access & short messaging

Reporting & updating functionsReporting & updating functions

Resource location & allocationResource location & allocation

Mobile professionals have similar needsMobile professionals have similar needs File transfer applications have yet to emergeFile transfer applications have yet to emerge

Fixed applications, e.g. telemetryFixed applications, e.g. telemetry

October 1998 6

Current Status - UsersCurrent Status - Users

Relatively high awareness in the verticalsRelatively high awareness in the verticals Productivity & service level imperativesProductivity & service level imperatives

Few formal corporate cellular implementationsFew formal corporate cellular implementations Evaluation & assessment of the practicalitiesEvaluation & assessment of the practicalities

Coverage, speed, reliabilityCoverage, speed, reliability

Equipment considerations, e.g. power issuesEquipment considerations, e.g. power issues

Impact on existing systems, applications & working Impact on existing systems, applications & working practicespractices

COSTCOST

October 1998

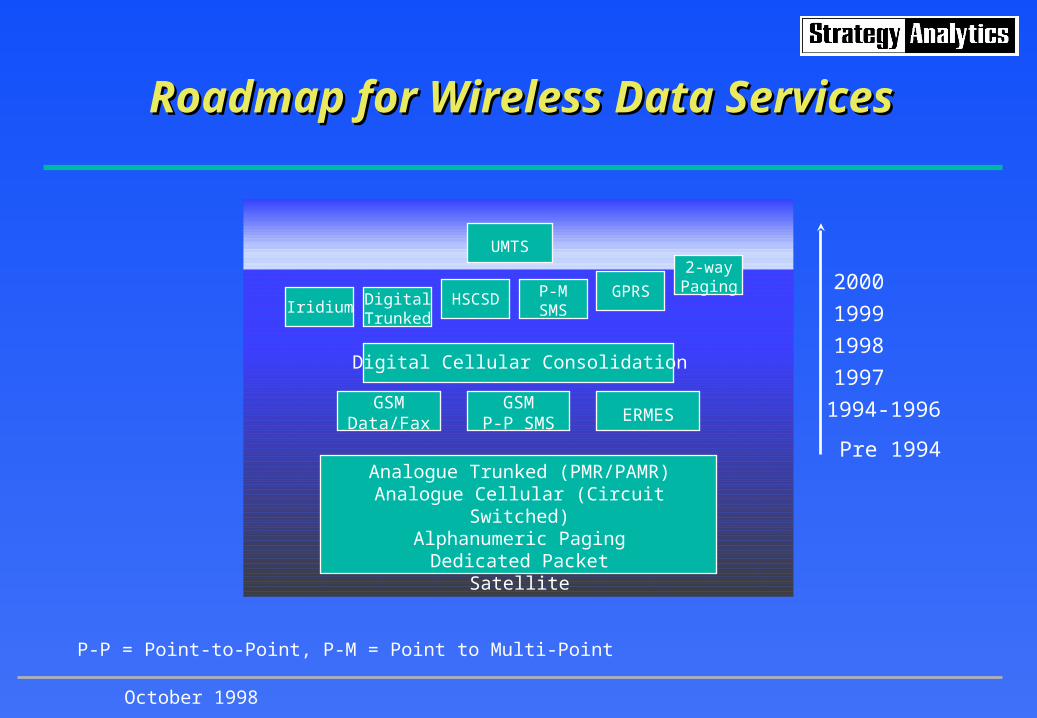

Analogue Trunked (PMR/PAMR)Analogue Cellular (Circuit Switched)

Alphanumeric PagingDedicated Packet

Satellite

1994-1996

Pre 1994

1997

1998

1999

2000

GSMData/Fax

GSMP-P SMS ERMES

Digital Cellular Consolidation

UMTS

Iridium DigitalTrunked

HSCSD GPRS

2-wayPagingP-M

SMS

P-P = Point-to-Point, P-M = Point to Multi-Point

Roadmap for Wireless Data ServicesRoadmap for Wireless Data Services

October 1998 8

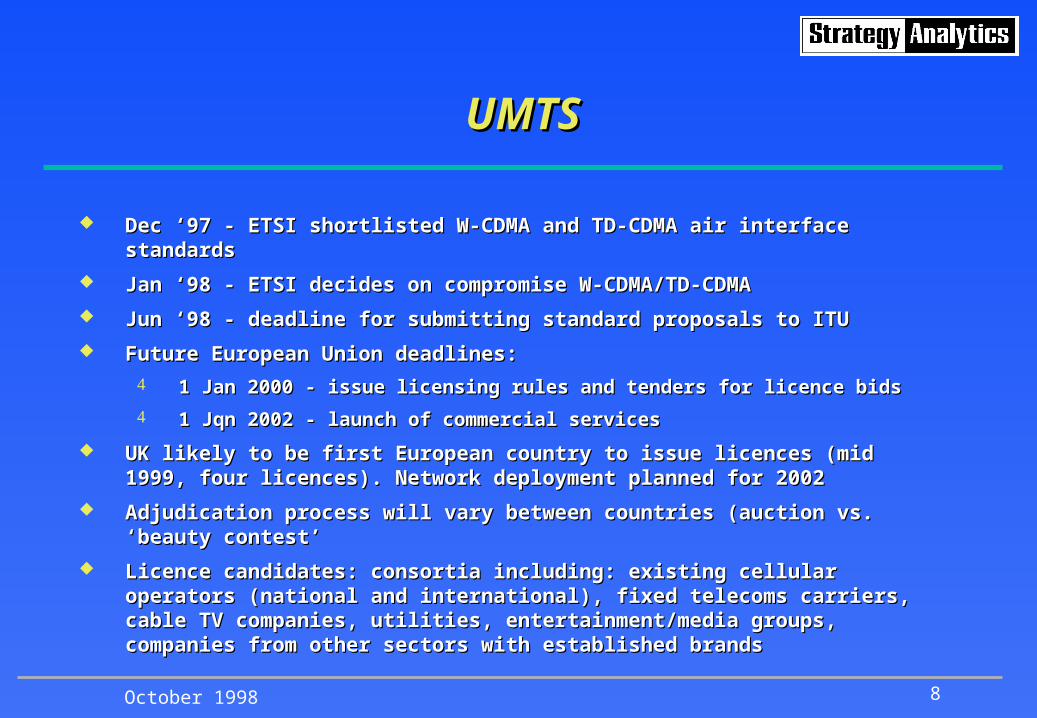

UMTSUMTS

Dec ‘97 - ETSI shortlisted W-CDMA and TD-CDMA air interface standardsDec ‘97 - ETSI shortlisted W-CDMA and TD-CDMA air interface standards

Jan ‘98 - ETSI decides on compromise W-CDMA/TD-CDMAJan ‘98 - ETSI decides on compromise W-CDMA/TD-CDMA

Jun ‘98 - deadline for submitting standard proposals to ITUJun ‘98 - deadline for submitting standard proposals to ITU

Future European Union deadlines:Future European Union deadlines:

1 Jan 2000 - issue licensing rules and tenders for licence bids1 Jan 2000 - issue licensing rules and tenders for licence bids

1 Jqn 2002 - launch of commercial services1 Jqn 2002 - launch of commercial services

UK likely to be first European country to issue licences (mid 1999, four UK likely to be first European country to issue licences (mid 1999, four licences). Network deployment planned for 2002licences). Network deployment planned for 2002

Adjudication process will vary between countries (auction vs. ‘beauty contest’Adjudication process will vary between countries (auction vs. ‘beauty contest’

Licence candidates: consortia including: existing cellular operators (national Licence candidates: consortia including: existing cellular operators (national and international), fixed telecoms carriers, cable TV companies, utilities, and international), fixed telecoms carriers, cable TV companies, utilities, entertainment/media groups, companies from other sectors with established entertainment/media groups, companies from other sectors with established brandsbrands

October 1998 9

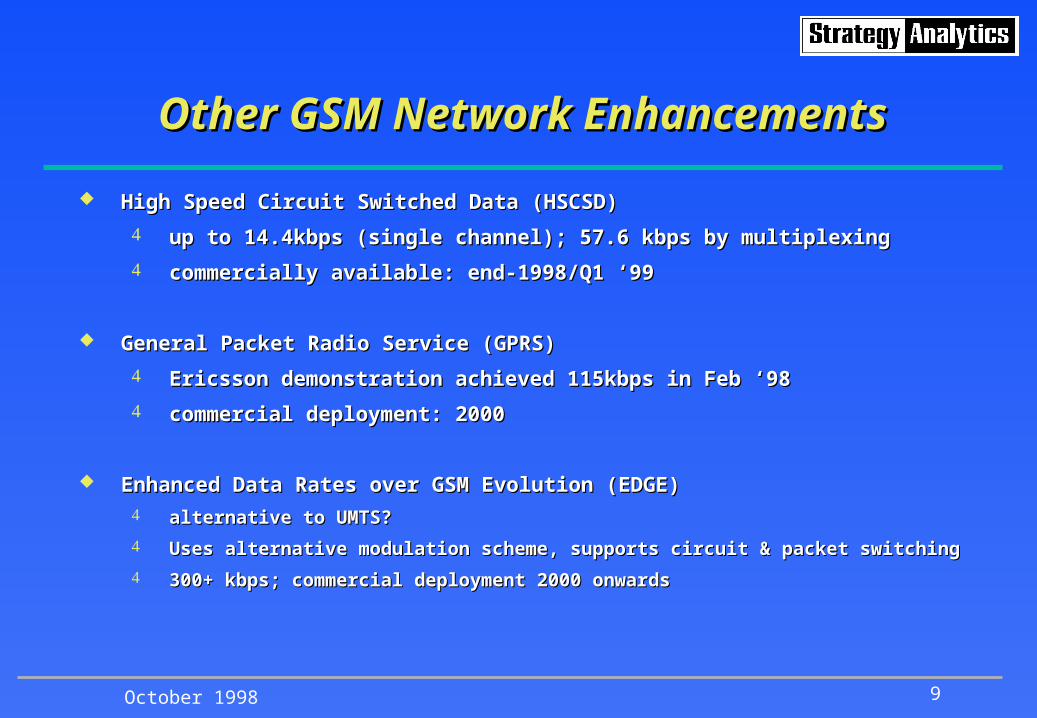

Other GSM Network EnhancementsOther GSM Network Enhancements

High Speed Circuit Switched Data (HSCSD)High Speed Circuit Switched Data (HSCSD)

up to 14.4kbps (single channel); 57.6 kbps by multiplexingup to 14.4kbps (single channel); 57.6 kbps by multiplexing

commercially available: end-1998/Q1 ‘99commercially available: end-1998/Q1 ‘99

General Packet Radio Service (GPRS)General Packet Radio Service (GPRS)

Ericsson demonstration achieved 115kbps in Feb ‘98Ericsson demonstration achieved 115kbps in Feb ‘98

commercial deployment: 2000commercial deployment: 2000

Enhanced Data Rates over GSM Evolution (EDGE)Enhanced Data Rates over GSM Evolution (EDGE) alternative to UMTS?alternative to UMTS?

Uses alternative modulation scheme, supports circuit & packet switchingUses alternative modulation scheme, supports circuit & packet switching

300+ kbps; commercial deployment 2000 onwards300+ kbps; commercial deployment 2000 onwards

October 1998 10

European Wireless Data Market to 2004European Wireless Data Market to 2004

0

1000

2000

3000

4000

5000

6000

7000

8000

1997 1998 2000 2004

Satellite

PMR

PAMR

Ded. Data

Cell. Data

2695

8824

1223783

Figures in thousands

CAAGR 1997-2004: 41%Cellular: 55%PMR: 23%

October 1998 11

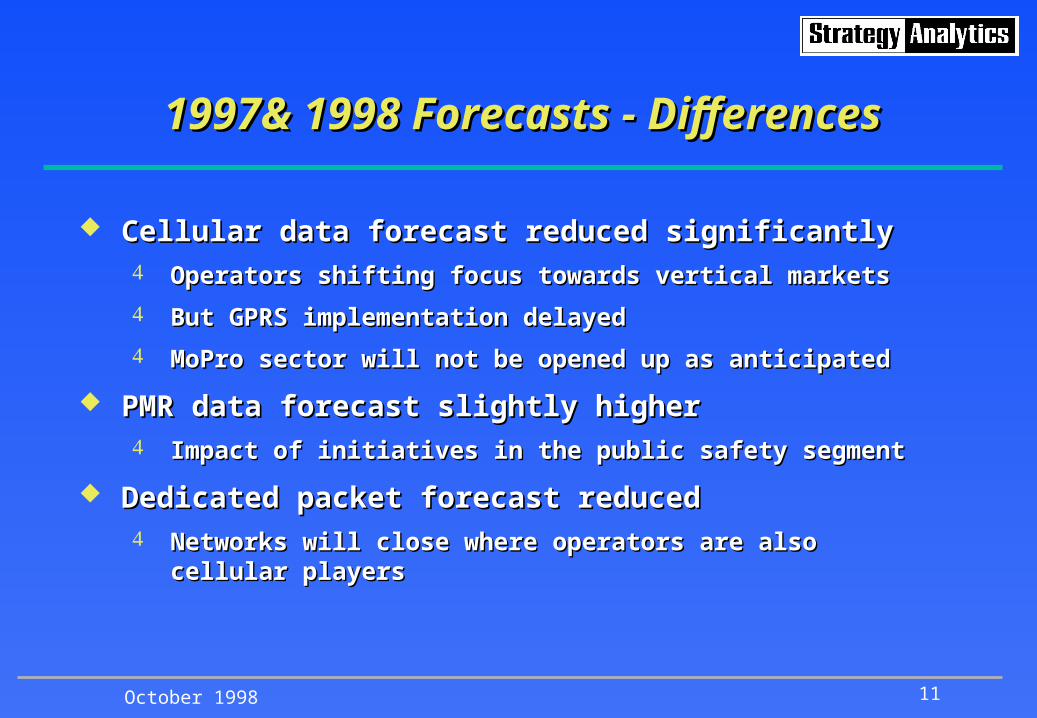

1997& 1998 Forecasts - Differences1997& 1998 Forecasts - Differences

Cellular data forecast reduced significantlyCellular data forecast reduced significantly Operators shifting focus towards vertical marketsOperators shifting focus towards vertical markets

But GPRS implementation delayedBut GPRS implementation delayed

MoPro sector will not be opened up as anticipatedMoPro sector will not be opened up as anticipated

PMR data forecast slightly higherPMR data forecast slightly higher Impact of initiatives in the public safety segmentImpact of initiatives in the public safety segment

Dedicated packet forecast reducedDedicated packet forecast reduced Networks will close where operators are also cellular Networks will close where operators are also cellular

playersplayers

October 1998 12

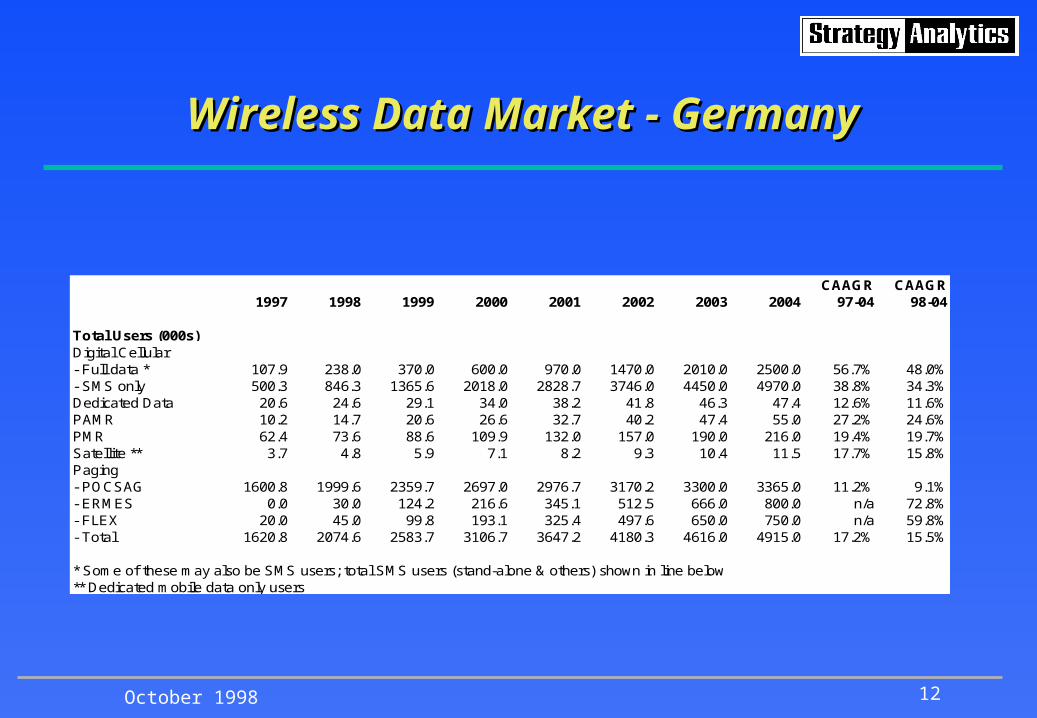

Wireless Data Market - GermanyWireless Data Market - Germany

CAAGR CAAGR1997 1998 1999 2000 2001 2002 2003 2004 97-04 98-04

Total Users (000s)Digital Cellular- Full data * 107.9 238.0 370.0 600.0 970.0 1470.0 2010.0 2500.0 56.7% 48.0%- SMS only 500.3 846.3 1365.6 2018.0 2828.7 3746.0 4450.0 4970.0 38.8% 34.3%Dedicated Data 20.6 24.6 29.1 34.0 38.2 41.8 46.3 47.4 12.6% 11.6%PAMR 10.2 14.7 20.6 26.6 32.7 40.2 47.4 55.0 27.2% 24.6%PMR 62.4 73.6 88.6 109.9 132.0 157.0 190.0 216.0 19.4% 19.7%Satellite ** 3.7 4.8 5.9 7.1 8.2 9.3 10.4 11.5 17.7% 15.8%Paging- POCSAG 1600.8 1999.6 2359.7 2697.0 2976.7 3170.2 3300.0 3365.0 11.2% 9.1%- ERMES 0.0 30.0 124.2 216.6 345.1 512.5 666.0 800.0 n/a 72.8%- FLEX 20.0 45.0 99.8 193.1 325.4 497.6 650.0 750.0 n/a 59.8%- Total 1620.8 2074.6 2583.7 3106.7 3647.2 4180.3 4616.0 4915.0 17.2% 15.5%

* Some of these may also be SMS users; total SMS users (stand-alone & others) shown in line below** Dedicated mobile data only users

October 1998 13

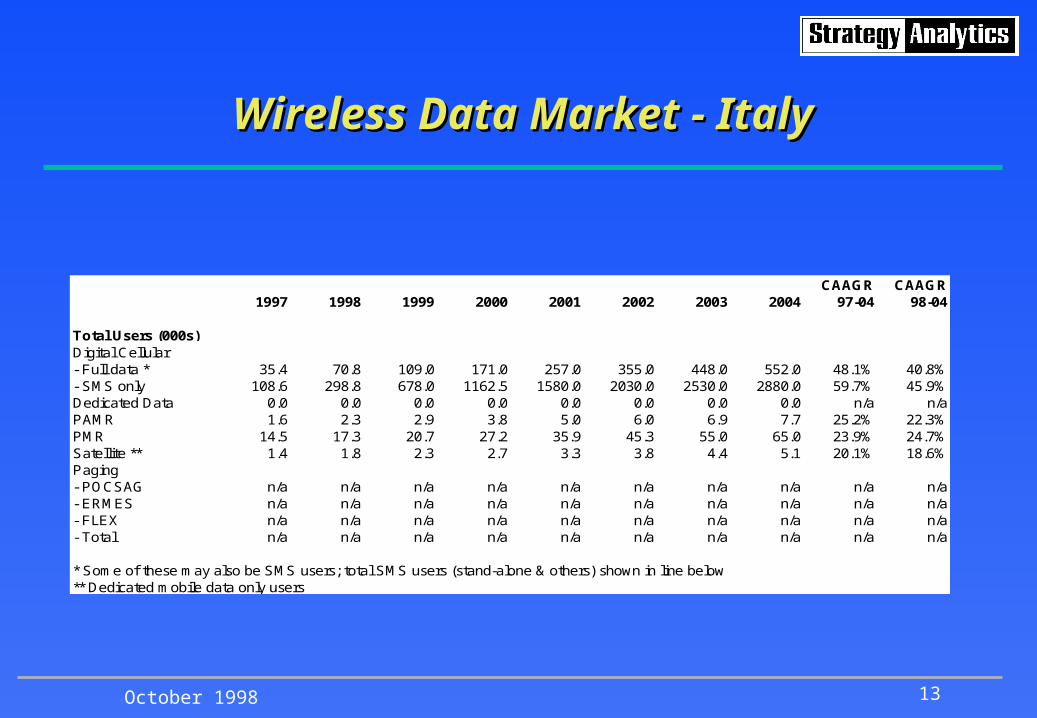

Wireless Data Market - ItalyWireless Data Market - Italy

CAAGR CAAGR1997 1998 1999 2000 2001 2002 2003 2004 97-04 98-04

Total Users (000s)Digital Cellular- Full data * 35.4 70.8 109.0 171.0 257.0 355.0 448.0 552.0 48.1% 40.8%- SMS only 108.6 298.8 678.0 1162.5 1580.0 2030.0 2530.0 2880.0 59.7% 45.9%Dedicated Data 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 n/a n/aPAMR 1.6 2.3 2.9 3.8 5.0 6.0 6.9 7.7 25.2% 22.3%PMR 14.5 17.3 20.7 27.2 35.9 45.3 55.0 65.0 23.9% 24.7%Satellite ** 1.4 1.8 2.3 2.7 3.3 3.8 4.4 5.1 20.1% 18.6%Paging- POCSAG n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a- ERMES n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a- FLEX n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a- Total n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a

* Some of these may also be SMS users; total SMS users (stand-alone & others) shown in line below** Dedicated mobile data only users

October 1998 14

Wireless Data Market - UKWireless Data Market - UK

CAAGR CAAGR1997 1998 1999 2000 2001 2002 2003 2004 97-04 98-04

Total Users (000s)Digital Cellular- Full data * 67.0 120.0 206.0 334.0 550.0 770.0 990.0 1220.0 51.4% 47.2%- SMS only 491.1 727.9 997.3 1296.5 1646.5 2058.1 2510.9 3000.0 29.5% 26.6%Dedicated Data 94.8 110.1 130.1 156.6 189.8 226.3 264.2 286.0 17.1% 17.2%PAMR 7.0 10.0 14.0 19.2 25.6 32.7 40.6 50.0 32.4% 30.8%PMR 46.2 54.4 68.0 86.4 112.3 149.3 201.6 244.0 26.8% 28.4%Satellite ** 3.1 3.6 4.3 4.8 5.4 5.9 6.5 7.0 12.4% 11.6%Paging- POCSAG 1455.0 1773.0 2123.0 2462.0 2695.0 2787.0 2814.0 2830.0 10.0% 8.1%- ERMES 0.0 12.0 37.0 110.0 260.0 494.0 741.0 940.0 n/a 106.9%- FLEX 0.0 0.0 12.0 39.0 100.0 198.0 306.9 400.0 n/a n/a- Total 1455.0 1785.0 2172.0 2611.0 3055.0 3479.0 3861.9 4170.0 16.2% 15.2%

* Some of these may also be SMS users; total SMS users (stand-alone & others) shown in line below** Dedicated mobile data only users

October 1998 15

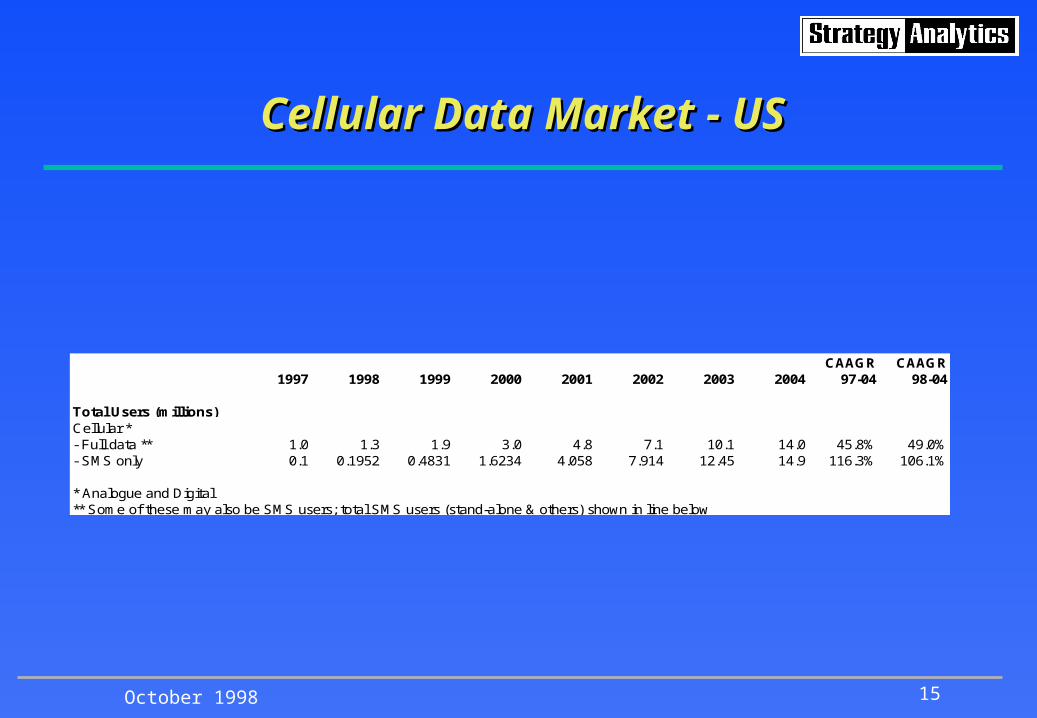

Cellular Data Market - USCellular Data Market - US

CAAGR CAAGR1997 1998 1999 2000 2001 2002 2003 2004 97-04 98-04

Total Users (millions)Cellular *- Full data ** 1.0 1.3 1.9 3.0 4.8 7.1 10.1 14.0 45.8% 49.0%- SMS only 0.1 0.1952 0.4831 1.6234 4.058 7.914 12.45 14.9 116.3% 106.1%

* Analogue and Digital** Some of these may also be SMS users; total SMS users (stand-alone & others) shown in line below

October 1998 16

ARPU & Total Data Revenues - GermanyARPU & Total Data Revenues - Germany

(1) Average Revenue Per User Per Month (ARPU - $)CAAGR CAAGR

1997 1998 1999 2000 2001 2002 2003 2004 97-04 98-04

Micro Info. Services 10.0 10.3 10.8 11.4 11.9 12.5 13.1 13.8 4.7% 5.0%Messaging Services 51.7 50.0 46.7 43.0 39.5 36.6 33.7 31.0 -7.0% -7.7%Multimedia Services 103.4 100.0 93.4 86.0 79.0 73.2 67.3 62.0 -7.0% -7.7%

(2) Total Revenues ($ Millions)CAAGR CAAGR

1997 1998 1999 2000 2001 2002 2003 2004 97-04 98-04

Micro Info. Services 60.0 104.6 177.2 275.0 404.7 562.8 702.0 823.2 45.4% 41.0%Messaging Services 66.3 139.9 201.1 297.2 436.8 606.9 754.8 855.6 44.1% 35.2%Multimedia Services 1.3 5.7 12.4 24.8 46.0 77.5 113.6 148.8 96.0% 72.2%

Total Data Revenues 127.6 250.3 390.8 597.0 887.5 1247.1 1570.4 1827.6 46.3% 39.3%

October 1998 17

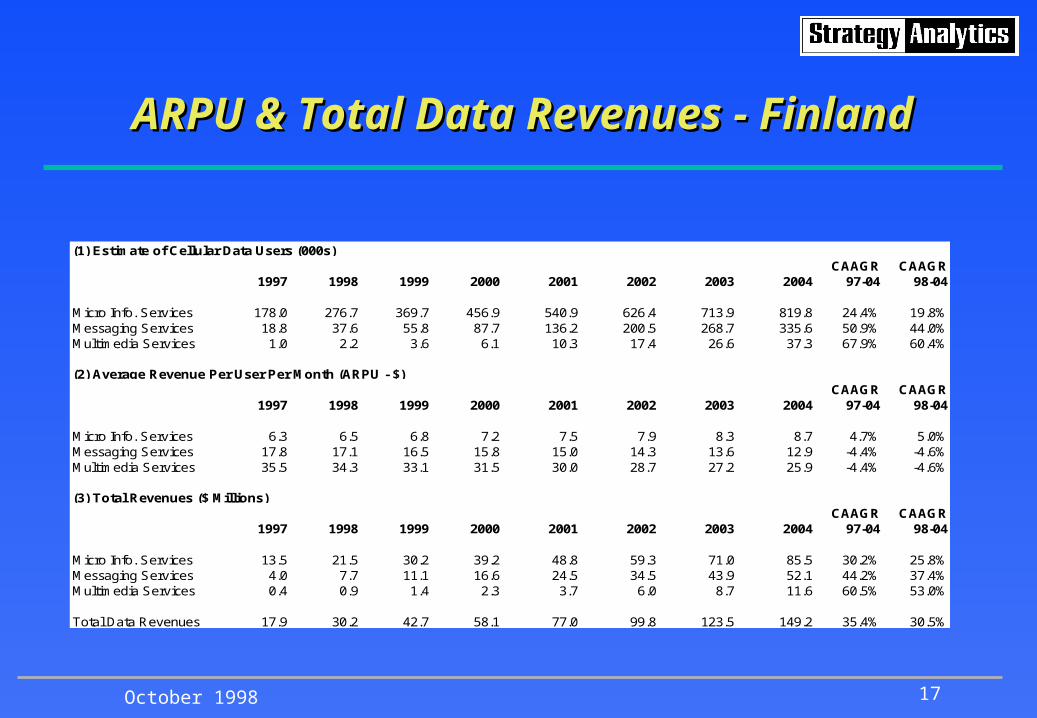

ARPU & Total Data Revenues - FinlandARPU & Total Data Revenues - Finland

(1) Estimate of Cellular Data Users (000s)CAAGR CAAGR

1997 1998 1999 2000 2001 2002 2003 2004 97-04 98-04

Micro Info. Services 178.0 276.7 369.7 456.9 540.9 626.4 713.9 819.8 24.4% 19.8%Messaging Services 18.8 37.6 55.8 87.7 136.2 200.5 268.7 335.6 50.9% 44.0%Multimedia Services 1.0 2.2 3.6 6.1 10.3 17.4 26.6 37.3 67.9% 60.4%

(2) Average Revenue Per User Per Month (ARPU - $)CAAGR CAAGR

1997 1998 1999 2000 2001 2002 2003 2004 97-04 98-04

Micro Info. Services 6.3 6.5 6.8 7.2 7.5 7.9 8.3 8.7 4.7% 5.0%Messaging Services 17.8 17.1 16.5 15.8 15.0 14.3 13.6 12.9 -4.4% -4.6%Multimedia Services 35.5 34.3 33.1 31.5 30.0 28.7 27.2 25.9 -4.4% -4.6%

(3) Total Revenues ($ Millions)CAAGR CAAGR

1997 1998 1999 2000 2001 2002 2003 2004 97-04 98-04

Micro Info. Services 13.5 21.5 30.2 39.2 48.8 59.3 71.0 85.5 30.2% 25.8%Messaging Services 4.0 7.7 11.1 16.6 24.5 34.5 43.9 52.1 44.2% 37.4%Multimedia Services 0.4 0.9 1.4 2.3 3.7 6.0 8.7 11.6 60.5% 53.0%

Total Data Revenues 17.9 30.2 42.7 58.1 77.0 99.8 123.5 149.2 35.4% 30.5%

October 1998 18

ARPU & Total Data Revenues - UKARPU & Total Data Revenues - UK

(1) Average Revenue Per User Per Month (ARPU - $)CAAGR CAAGR

1997 1998 1999 2000 2001 2002 2003 2004 97-04 98-04

Micro Info. Services 8.0 8.2 8.7 9.1 9.5 10.0 10.5 11.0 4.7% 5.0%Messaging Services 35.5 34.3 33.1 31.5 30.0 28.7 27.2 25.9 -4.4% -4.6%Multimedia Services 71.0 68.5 66.1 63.0 60.0 57.3 54.4 51.7 -4.4% -4.6%

(2) Total Revenues ($ Millions)CAAGR CAAGR

1997 1998 1999 2000 2001 2002 2003 2004 97-04 98-04

Micro Info. Services 47.1 72.0 103.5 141.3 188.5 247.4 316.9 397.5 35.6% 33.0%Messaging Services 27.1 46.6 76.8 118.0 184.1 243.5 294.1 340.6 43.6% 39.3%Multimedia Services 2.9 5.4 9.8 16.4 27.7 42.4 58.2 75.7 59.7% 55.2%

Total Data Revenues 77.1 124.0 190.1 275.8 400.3 533.3 669.1 813.8 40.0% 36.8%

October 1998 19

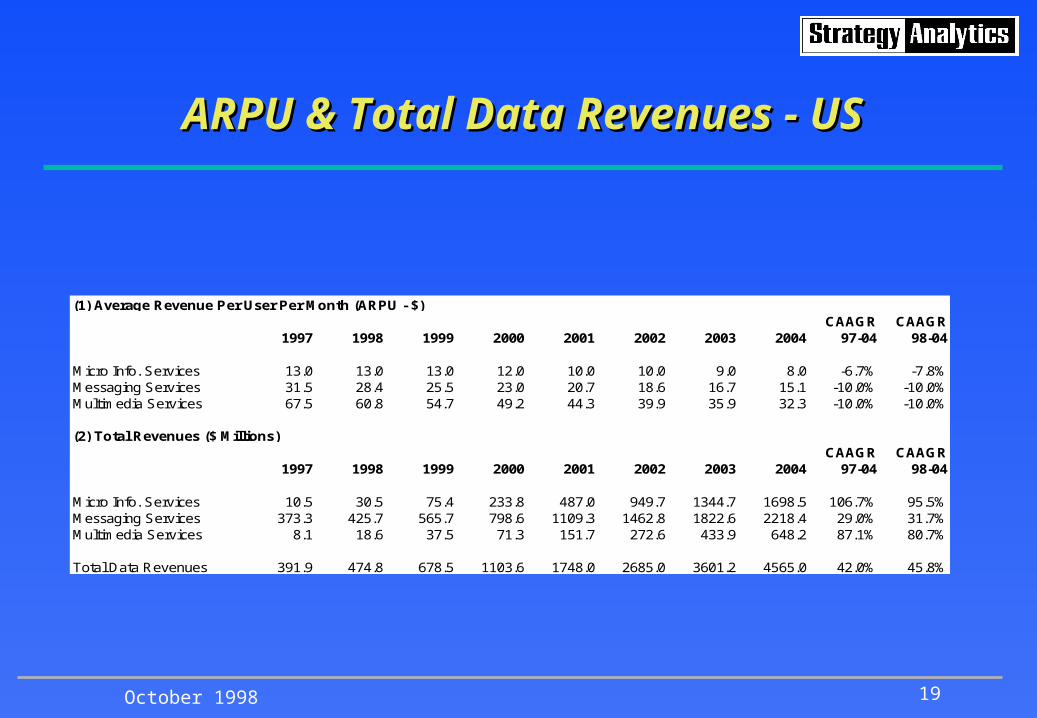

ARPU & Total Data Revenues - USARPU & Total Data Revenues - US

(1) Average Revenue Per User Per Month (ARPU - $)CAAGR CAAGR

1997 1998 1999 2000 2001 2002 2003 2004 97-04 98-04

Micro Info. Services 13.0 13.0 13.0 12.0 10.0 10.0 9.0 8.0 -6.7% -7.8%Messaging Services 31.5 28.4 25.5 23.0 20.7 18.6 16.7 15.1 -10.0% -10.0%Multimedia Services 67.5 60.8 54.7 49.2 44.3 39.9 35.9 32.3 -10.0% -10.0%

(2) Total Revenues ($ Millions)CAAGR CAAGR

1997 1998 1999 2000 2001 2002 2003 2004 97-04 98-04

Micro Info. Services 10.5 30.5 75.4 233.8 487.0 949.7 1344.7 1698.5 106.7% 95.5%Messaging Services 373.3 425.7 565.7 798.6 1109.3 1462.8 1822.6 2218.4 29.0% 31.7%Multimedia Services 8.1 18.6 37.5 71.3 151.7 272.6 433.9 648.2 87.1% 80.7%

Total Data Revenues 391.9 474.8 678.5 1103.6 1748.0 2685.0 3601.2 4565.0 42.0% 45.8%

October 1998 20

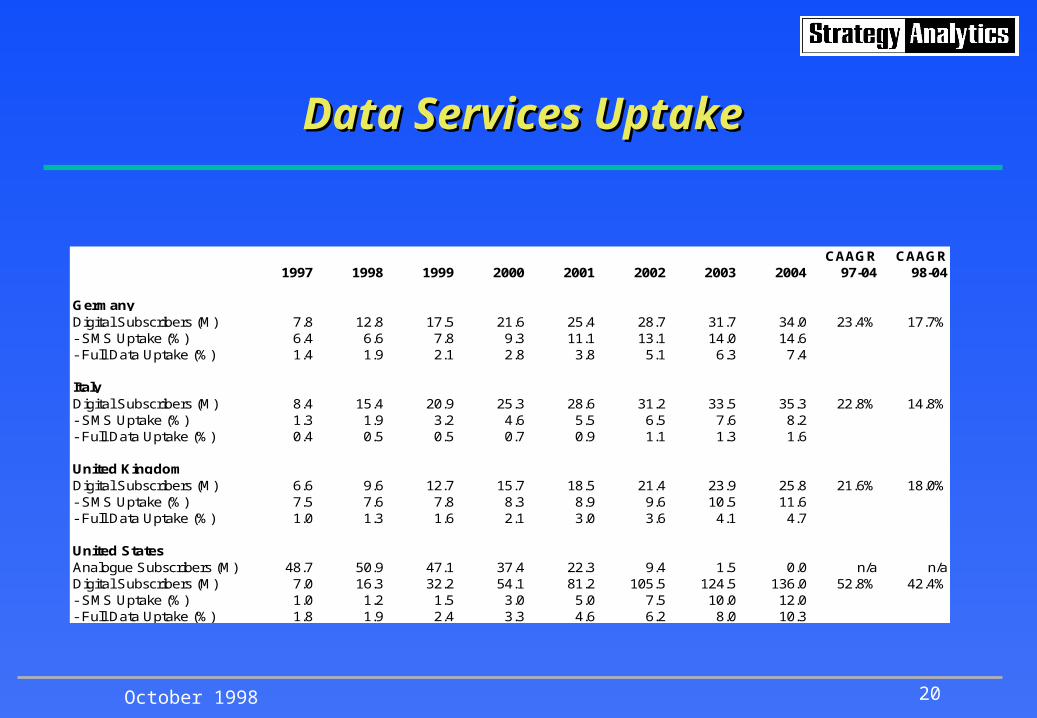

Data Services UptakeData Services Uptake

CAAGR CAAGR1997 1998 1999 2000 2001 2002 2003 2004 97-04 98-04

GermanyDigital Subscribers (M) 7.8 12.8 17.5 21.6 25.4 28.7 31.7 34.0 23.4% 17.7%- SMS Uptake (%) 6.4 6.6 7.8 9.3 11.1 13.1 14.0 14.6- Full Data Uptake (%) 1.4 1.9 2.1 2.8 3.8 5.1 6.3 7.4

ItalyDigital Subscribers (M) 8.4 15.4 20.9 25.3 28.6 31.2 33.5 35.3 22.8% 14.8%- SMS Uptake (%) 1.3 1.9 3.2 4.6 5.5 6.5 7.6 8.2- Full Data Uptake (%) 0.4 0.5 0.5 0.7 0.9 1.1 1.3 1.6

United KingdomDigital Subscribers (M) 6.6 9.6 12.7 15.7 18.5 21.4 23.9 25.8 21.6% 18.0%- SMS Uptake (%) 7.5 7.6 7.8 8.3 8.9 9.6 10.5 11.6- Full Data Uptake (%) 1.0 1.3 1.6 2.1 3.0 3.6 4.1 4.7

United StatesAnalogue Subscribers (M) 48.7 50.9 47.1 37.4 22.3 9.4 1.5 0.0 n/a n/aDigital Subscribers (M) 7.0 16.3 32.2 54.1 81.2 105.5 124.5 136.0 52.8% 42.4%- SMS Uptake (%) 1.0 1.2 1.5 3.0 5.0 7.5 10.0 12.0- Full Data Uptake (%) 1.8 1.9 2.4 3.3 4.6 6.2 8.0 10.3

October 1998 21

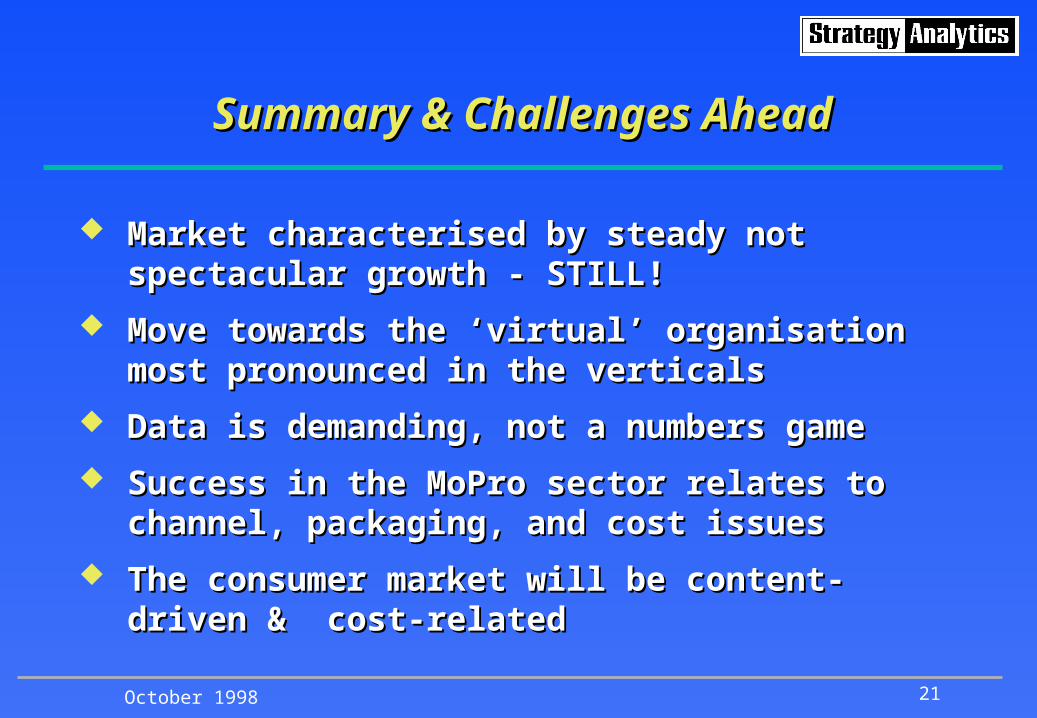

Summary & Challenges AheadSummary & Challenges Ahead

Market characterised by steady not spectacular Market characterised by steady not spectacular growth - STILL!growth - STILL!

Move towards the ‘virtual’ organisation most Move towards the ‘virtual’ organisation most pronounced in the verticalspronounced in the verticals

Data is demanding, not a numbers gameData is demanding, not a numbers game

Success in the MoPro sector relates to channel, Success in the MoPro sector relates to channel, packaging, and cost issuespackaging, and cost issues

The consumer market will be content-driven & The consumer market will be content-driven & cost-relatedcost-related

Related Documents