T HE EU ETS AND F IRM F INANCIAL P ERFORMANCE :E VIDENCE FROM THE E UROPEAN E LECTRICITY S ECTOR Master Thesis Copenhagen Business School Master of Sciences in Applied Economics and Finance Authors: Magnus Poulsen (102115) and Pontus L¨ ofgren (124590) Supervisor: Lisbeth la Cour, PhD May 15, 2020 101 pages and 147,238 characters

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

THE EU ETS AND FIRM FINANCIAL

PERFORMANCE: EVIDENCE FROM THE

EUROPEAN ELECTRICITY SECTOR

Master Thesis

Copenhagen Business School

Master of Sciences in Applied Economics and Finance

Authors: Magnus Poulsen (102115) and Pontus Lofgren (124590)

Supervisor: Lisbeth la Cour, PhD

May 15, 2020

101 pages and 147,238 characters

Abstract

Prior studies on the economic consequences of the European Union Emissions

Trading System (EU ETS) on European electricity generating firms have so far re-

lied on data from the first phase of the scheme that ended in 2007. We address

this gap and find that EU ETS emission allowance price increases (decreases) have

a positive (negative) impact on stock return by employing multifactor models with

a balanced longitudinal dataset covering thirteen European electricity generating

firms during the third phase of the EU ETS. Moreover, we find that the positive re-

lationship is stronger for firms with carbon efficient electricity generation. Based

on the Arbitrage Pricing Theory and the Efficient Market Hypothesis, we argue

that price appreciations in EU ETS emission allowances positively affect firm per-

formance for European electricity generating firms in general and carbon efficient

generators in particular. A possible explanation is that inframarginal suppliers ob-

tain regulatory rent due to the pass-through of the marginal producer’s additional

emission compliance cost to consumers. This suggests that the EU ETS is success-

ful in financially incentivizing profit maximizing firms concerned with electricity

generation to decarbonize operations, which may be of interest to policymakers

considering more stringent emission compliance costs for other sectors.

2

Acknowledgements

First and foremost, we express our gratitude and appreciation to our supervisor

Lisbeth la Cour, Professor in Time Series Econometrics at the Department of Eco-

nomics, Copenhagen Business School, for excellent guidance throughout the pro-

cess of writing this thesis. We are also grateful to Claus Vorm, Deputy Head of

Multi Assets at Nordea Investment Management, for providing important insights

into how utility stocks perform in low interest environments. We were also for-

tunate to sit down with representatives from Ørsted to learn about the electricity

sector. Lastly, we thank Julian Karst, Information Service Officer at the European

Energy Exchange (EEX) for kindly providing the data required for our empirical

analysis.

3

Contents

1 Introduction 10

1.1 Background and Problem Discussion . . . . . . . . . . . . . . . . . 10

1.2 Purpose . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

1.3 Research Question . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

1.4 Thesis Structure . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

2 Institutional Background and Literature Review 14

2.1 The European Electricity Market . . . . . . . . . . . . . . . . . . . 14

2.1.1 Infrastructure . . . . . . . . . . . . . . . . . . . . . . . . . . 14

2.1.2 Markets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

2.1.3 The European Electricity Mix . . . . . . . . . . . . . . . . . 17

2.1.4 Price-Setting and the Merit Order Curve . . . . . . . . . . . 20

2.2 The European Union Emissions Trading System . . . . . . . . . . . 21

2.2.1 Evolvement of the EU ETS . . . . . . . . . . . . . . . . . . . 22

2.2.2 Market Stability Reserve . . . . . . . . . . . . . . . . . . . . 28

2.3 Literature Review . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

2.3.1 European Union Allowances and Firm Financial Performancein the Electricity Sector . . . . . . . . . . . . . . . . . . . . 29

2.3.2 Pricing of European Union Allowances . . . . . . . . . . . . 33

3 Theory and Hypotheses 35

4

CONTENTS

3.1 Theory . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35

3.1.1 Arbitrage Pricing Theory . . . . . . . . . . . . . . . . . . . . 35

3.1.2 Efficient Market Hypothesis . . . . . . . . . . . . . . . . . . 37

3.2 Hypotheses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

4 Methodology 41

4.1 Research Approach . . . . . . . . . . . . . . . . . . . . . . . . . . . 41

4.2 Data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42

4.2.1 Firms . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42

4.2.2 Carbon Intensity . . . . . . . . . . . . . . . . . . . . . . . . 44

4.2.3 European Union Allowance Prices . . . . . . . . . . . . . . . 45

4.2.4 Market Returns . . . . . . . . . . . . . . . . . . . . . . . . . 45

4.2.5 Control Variables: Oil and Natural Gas . . . . . . . . . . . . 46

4.2.6 Transformation of Data and Frequency . . . . . . . . . . . . 46

4.3 Econometric Theory . . . . . . . . . . . . . . . . . . . . . . . . . . 47

4.3.1 OLS Estimation . . . . . . . . . . . . . . . . . . . . . . . . . 47

4.3.2 Omitted Variable Bias . . . . . . . . . . . . . . . . . . . . . 49

4.3.3 Fixed Effects Regression . . . . . . . . . . . . . . . . . . . . 50

4.3.4 Random Effects Regression . . . . . . . . . . . . . . . . . . 52

4.3.5 OLS Diagnostics . . . . . . . . . . . . . . . . . . . . . . . . 52

4.3.6 Autocorrelation . . . . . . . . . . . . . . . . . . . . . . . . . 53

4.3.7 Stationarity . . . . . . . . . . . . . . . . . . . . . . . . . . . 54

4.3.8 Econometric Methodology . . . . . . . . . . . . . . . . . . . 56

5 Results 60

5.1 Overview of the Data . . . . . . . . . . . . . . . . . . . . . . . . . . 60

5.2 Autocorrelation and Stationarity . . . . . . . . . . . . . . . . . . . 67

5

CONTENTS

5.3 Regression Results . . . . . . . . . . . . . . . . . . . . . . . . . . . 70

5.3.1 Hypothesis I . . . . . . . . . . . . . . . . . . . . . . . . . . . 70

5.3.2 Hypothesis II . . . . . . . . . . . . . . . . . . . . . . . . . . 77

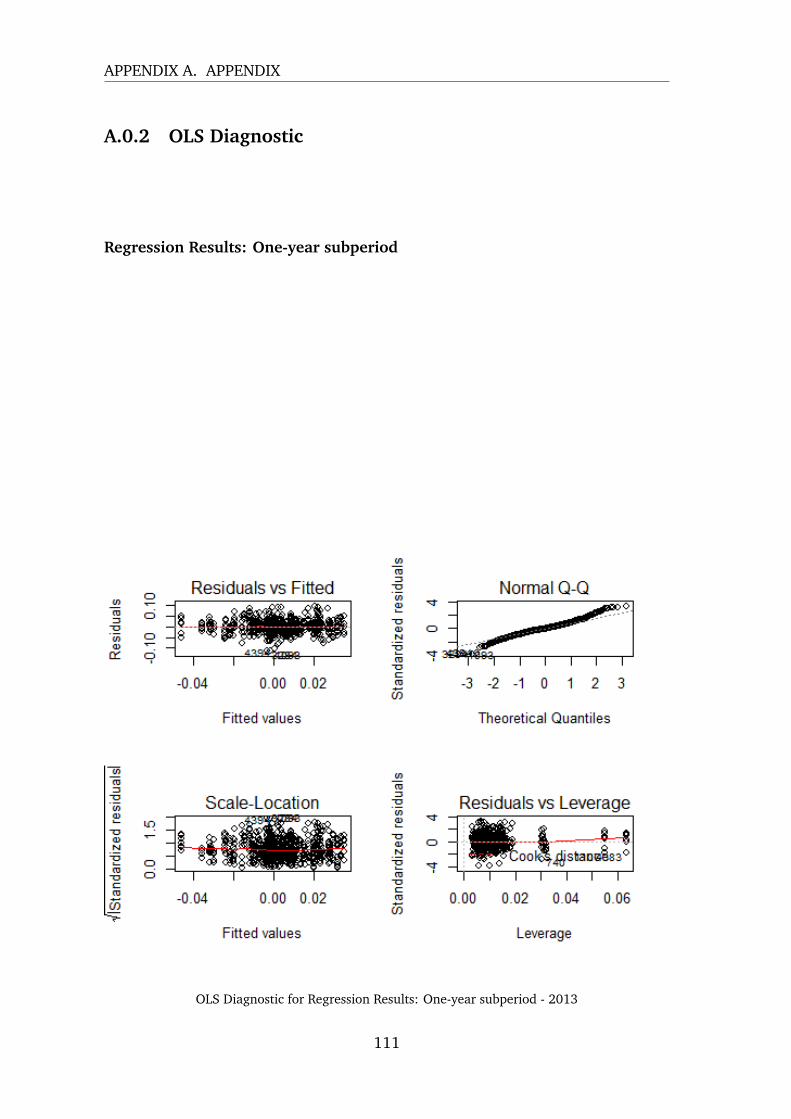

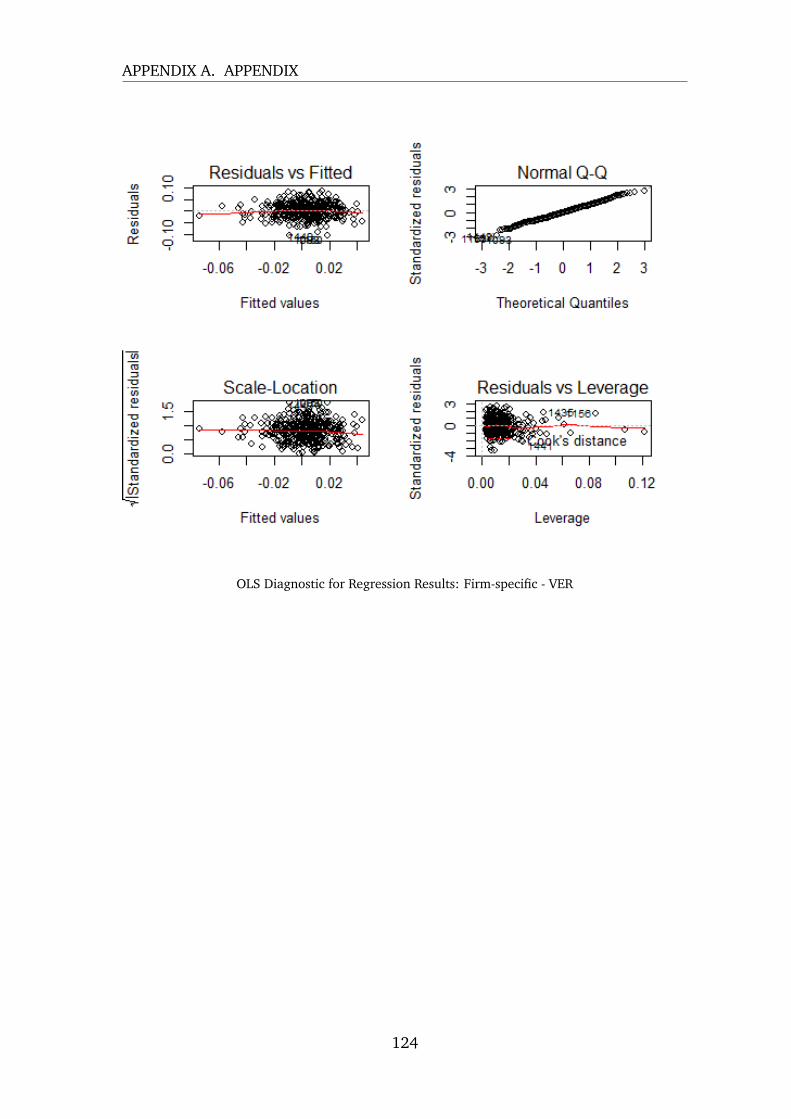

5.3.3 OLS Diagnostics . . . . . . . . . . . . . . . . . . . . . . . . 82

5.4 Summary of Findings . . . . . . . . . . . . . . . . . . . . . . . . . . 85

6 Discussion 87

6.1 EU Allowance Price Changes’ Impact on Financial Performance . . 87

6.2 Carbon Intensity and Financial Performance . . . . . . . . . . . . . 93

6.3 Practical Implications . . . . . . . . . . . . . . . . . . . . . . . . . . 95

6.4 Suggested Further Research . . . . . . . . . . . . . . . . . . . . . . 96

7 Conclusion 98

A Appendix 106

A.0.1 Autocorrelation and Stationarity . . . . . . . . . . . . . . . 106

A.0.2 OLS Diagnostic . . . . . . . . . . . . . . . . . . . . . . . . . 111

6

List of Figures

2.1 Illustration of Electricity Grid. . . . . . . . . . . . . . . . . . . . . . 15

2.2 Overview of Electricity Markets. . . . . . . . . . . . . . . . . . . . . 16

2.3 The European Electricity Mix . . . . . . . . . . . . . . . . . . . . . 18

2.4 Illustration of the European Carbon Intensity . . . . . . . . . . . . 19

2.5 Illustration of the Merit Order Curve . . . . . . . . . . . . . . . . . 20

3.1 Illustration of the Merit Order Curve with emission compliance costs 39

4.1 Carbon Intensity for sample firms . . . . . . . . . . . . . . . . . . . 44

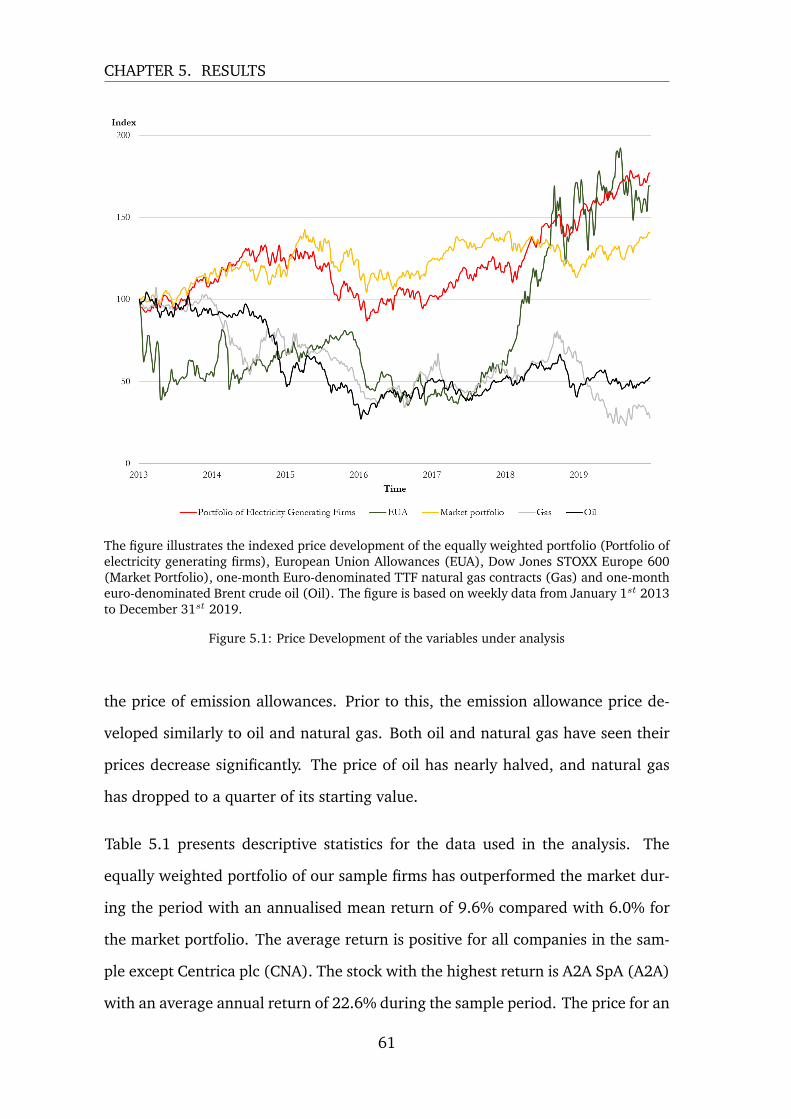

5.1 Price Development of the variables under analysis . . . . . . . . . . 61

5.2 Price development of the Portfolio of Electricity Generating Firms,the Market Portfolio and Centrica plc . . . . . . . . . . . . . . . . . 65

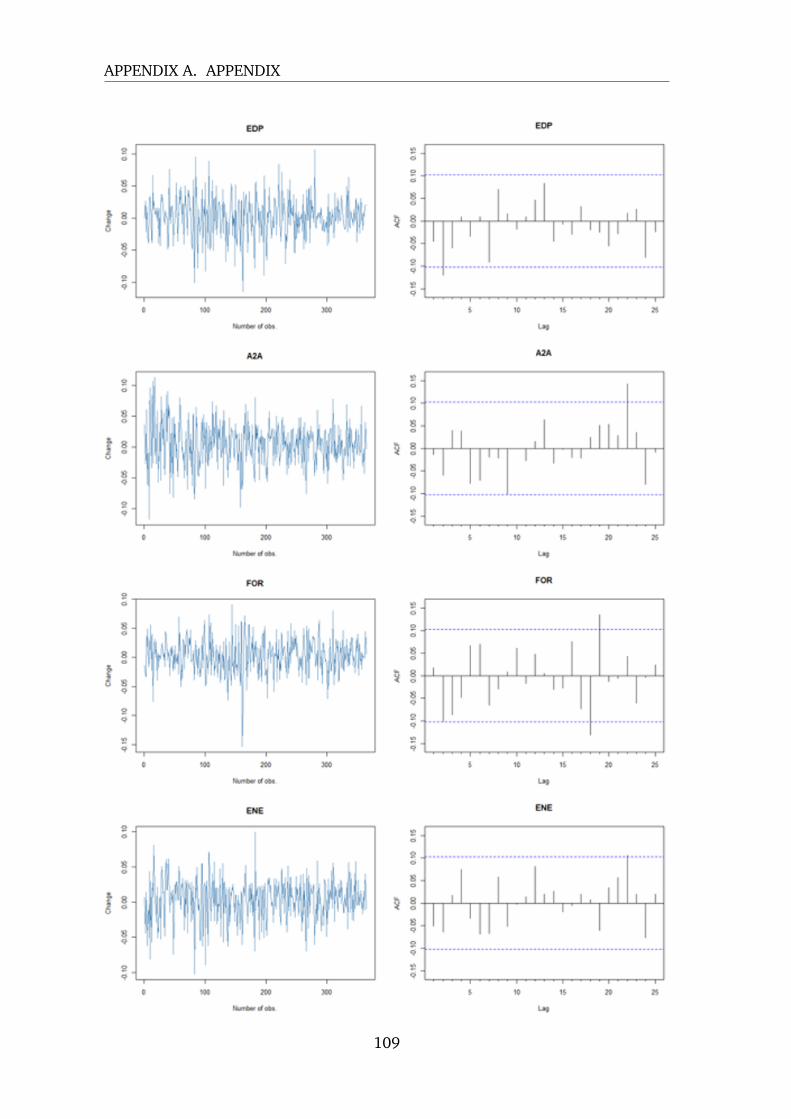

5.3 Plots of the logarithmic weekly return and the corresponding ACFplot . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 68

5.4 OLS Diagnostic - Pooled regression . . . . . . . . . . . . . . . . . . 82

5.5 OLS Diagnostic - Equally weighted portfolio . . . . . . . . . . . . . 83

5.6 OLS Diagnostic - Hypothesis II - Polluter . . . . . . . . . . . . . . . 85

6.1 Development for 10-year Government Yields for 2019 . . . . . . . 92

A.1 Plots of the logarithmic weekly return and the corresponding ACFplot . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 110

A.2 OLS Diagnostic: One-year subperiod . . . . . . . . . . . . . . . . . 117

7

LIST OF FIGURES

A.3 OLS Diagnostic: Two-year subperiod . . . . . . . . . . . . . . . . . 120

A.4 OLS Diagnostic: Firm-specific . . . . . . . . . . . . . . . . . . . . . 133

8

List of Tables

2.1 Overview of the Four Phases of the EU ETS . . . . . . . . . . . . . . 27

4.1 Overview of the companies under analysis . . . . . . . . . . . . . . 43

5.1 Descriptive statistics for variables under analysis . . . . . . . . . . . 63

5.2 Correlation matrix of returns . . . . . . . . . . . . . . . . . . . . . 64

5.3 Correlation matrix for Centrica plc . . . . . . . . . . . . . . . . . . 66

5.4 Summary of Augmented Dickey-Fuller test . . . . . . . . . . . . . . 69

5.5 Regression Results: Hypothesis I . . . . . . . . . . . . . . . . . . . 73

5.6 Regression Results: One-year subperiod . . . . . . . . . . . . . . . 75

5.7 Correlation matrix of returns for 2019 . . . . . . . . . . . . . . . . 76

5.8 Regression Results: Two-year subperiod . . . . . . . . . . . . . . . 77

5.9 Regression Results: Hypothesis II . . . . . . . . . . . . . . . . . . . 80

5.10 Regression Results: Firm-specific . . . . . . . . . . . . . . . . . . . 81

5.11 Extreme data points for Pooled regression . . . . . . . . . . . . . . 84

9

Chapter 1: Introduction

1.1 Background and Problem Discussion

The European Emission Trading System (EU ETS) was introduced in 2005 as a

policy instrument for the European Union to comply with the carbon emission re-

duction targets set out by the Kyoto protocol. Under the system, emitting entities

must surrender one European Union Allowance (EUA) per metric ton of green-

house gas emissions by year-end or face hefty fines. It is a cap-and-trade system

in which the annual number of allowances is decreasing, and firms can trade al-

lowances with one another (Chevallier, 2012). This sets a price on emissions that

serves to incentivize companies to invest in technologies that reduce emissions.

It is cost-efficient in the sense that firms with high abatement costs can purchase

emission rights from firms with cheaper ways to reduce emissions. Today, the EU

ETS is the world’s largest market for emissions and covers more than 13,500 instal-

lations, which are responsible for roughly half of the European Union’s emissions

(Hintermann et al., 2016).

The electricity sector is the largest polluter in the European Union. It is also

different from other sectors in a variety of interesting ways. Firstly, it is naturally

protected from foreign competition by means of infrastructure and regulation.

Secondly, it has a wide range of abatement options available that can substitute

10

CHAPTER 1. INTRODUCTION

carbon-intensive electricity generation. Lastly, it is currently the only sector that is

not allocated any emission allowances for free (Chevallier, 2012).

Perhaps surprising for the unversed reader, previous research has found that elec-

tricity generating firms profited from increased prices of emission allowances dur-

ing the first phase of the EU ETS that ran from 2005 to 2007, despite it constituting

an increased input cost. The phenomenon can be explained by the free allocation

method of emission allowances that was present in the first phase, combined with

a high pass-through rate of its opportunity cost to consumers (Sijm et al., 2006).

In effect, this resulted in windfall profits to the European electricity sector (Obern-

dorfer, 2009; Veith et al., 2009).

Much has changed in the last fifteen years. In terms of the regulatory nature of the

European Union Emissions Trading System, the electricity sector is now subject to

full auctioning of emission allowances, and the system itself has matured signif-

icantly (European Commission, 2015). In terms of the European electricity mix,

renewable energy production has penetrated the market, and carbon intensity has

roughly halved. As such, the results of the previous research may not hold today

and with this paper, we aim to address that gap.

1.2 Purpose

The purpose of the paper is to understand how price changes in European Union

Allowances affect financial performance for European electricity generating firms

during the third phase of the European Union Emissions Trading System. The

conclusions are relevant as it may provide important insights to European poli-

cymakers’ assessment of how to further develop the European Union Emissions

Trading System or for foreign policymakers considering implementing similar reg-

11

CHAPTER 1. INTRODUCTION

ulation. Further, it may be relevant to investors and electricity generating firms

seeking to maximize return on their investments.

1.3 Research Question

This paper seeks to deepen our understanding of how the European Union Emis-

sions Trading System’s greenhouse gas emission allowances affect firm financial

performance for European electricity generating firms during its third phase. We

define our overarching research question as follows:

How do price changes in European Union Allowances affect firm performance for

European electricity generating firms during the third phase of the EU ETS?

It will further nuance our understanding by investigating if and how these dynam-

ics change depending on the carbon intensity of the firm’s electricity production

by answering the following research question:

How does a potential impact of European Union Allowance price changes differ de-

pending on the carbon intensity of European electricity generating firms’ electricity

production during the third phase of EU ETS?

1.4 Thesis Structure

The remainder of the paper is structured as follows. Chapter II introduces the

reader to the electricity sector and the European Union Emissions Trading Sys-

tem to provide context for our overarching research question. To ensure sufficient

theoretical depth, it includes a literature review on the research of the interplay

between emission allowance price changes and firm performance for European

12

CHAPTER 1. INTRODUCTION

electricity generating firms and the price-setting forces on emission allowances.

Chapter III introduces the Arbitrage Pricing Theory and the Efficient Market Hy-

pothesis. Combined with previous research on the subject, these theories will lay

the foundation to our hypotheses. Chapter IV describes the data and the method-

ology. Chapter V will presents the empirical results discussed in Chapter VI, pre-

ceding the conclusion in Chapter VII.

13

Chapter 2: Institutional Background

and Literature Review

Chapter II begins by providing the reader with an introduction to the European

electricity sector including its infrastructure, markets, electricity mix, and price

setting mechanisms. Next, it presents an overview of the European Union Emis-

sions Trading System before providing a review of the literature covering its effect

the financial performance of European electricity generating firms as well as the

price setting forces on emission allowances.

2.1 The European Electricity Market

2.1.1 Infrastructure

The European Union has adopted a wide range of legislation aiming at achieving

the long-term goal of an integrated European energy market, in which electric-

ity is traded cross-borders competitively. Previously, each domestic energy market

was monopolistic or oligopolistic and consisted of one or a few vertically inte-

grated companies responsible for the generation, transportation, and distribution

of electricity. Today, regulation limiting the degree of vertical integration has

14

CHAPTER 2. INSTITUTIONAL BACKGROUND AND LITERATURE REVIEW

further divided the electrical sector into three participant groups: i) electricity

generators, ii) transmission system operators (TSO), and iii) distribution system

operators (DSO). The electricity grid is a network that connects electricity gen-

erators and consumers via transmission and distribution networks. Transmission

system operators are responsible for transporting electricity regionally over long

distances from power generators to distribution system operators that locally dis-

tribute electricity to households and industries. The European transmission grid

covers 300,000 km of power lines, including 355 cross-border lines. (Erbach,

2016).

Source: Erbach (2016)

Figure 2.1: Illustration of Electricity Grid.

2.1.2 Markets

Participants in the wholesale markets are electricity generators on the one side

and electricity suppliers and large industrial consumers on the other. They meet

on organized multilateral power exchanges such as Nordpool or over-the-counter.

Electricity is a unique commodity in the sense that it is essentially produced and

consumed simultaneously and that imbalances between production and consump-

tion in the grid can cause system collapse and blackouts. As such, the electricity

markets have been designed to accommodate this issue. The markets are ordered

15

CHAPTER 2. INSTITUTIONAL BACKGROUND AND LITERATURE REVIEW

sequentially starting years before the actual delivery and ending after the actual

delivery. This facilitates the balancing between supply and demand.

Source: Erbach (2016)

Figure 2.2: Overview of Electricity Markets.

In the forward and futures market, the two parties agree to the terms of the ex-

change years to weeks in advance of the transaction taking place. This allows gen-

erators to plan their output appropriately and for both parties to hedge against the

risk of fluctuating electricity prices. In the day-ahead market, electricity is traded

one day before delivery allowing electricity generators to adjust their capacity to

accommodate demand the following day. In the intra-day market, electricity is

traded on the day of delivery, and output can be fine-tuned. Lastly, in the balanc-

ing market, the Transmission System Operator will maintain system balance by

injections or take-offs of electricity (KU Leuven Energy Institute, 2015).

16

CHAPTER 2. INSTITUTIONAL BACKGROUND AND LITERATURE REVIEW

2.1.3 The European Electricity Mix

Electricity Generation Technologies

Electricity generation technologies are typically divided into three different cate-

gories: nuclear power, fossil-fueled power, and renewable electricity.

The process of generating electricity using nuclear power is thermal, in which

water is heated through nuclear fission to steam that drives a rotational turbine.

Nuclear power requires substantial initial investments, but the electricity is gener-

ated at low marginal cost and with no greenhouse gas emissions.

As with nuclear power generation, fossil-fuel power is generated through a ther-

mal process in which fuel is burned to create steam that drives a turbine. Fossil-

fuel generation can be divided into three subcategories, namely coal, natural gas,

and petroleum. Coal and natural gas fossil-fuel generation have efficiencies of

40% and 60%, respectively, meaning that a large portion of the energy is not being

transformed into electricity. These power plants are commonly operated using an

Integrated Gasification Combined Cycle procedure that allows for the use of both

fuel types as inputs. This allows the power plant to switch between fuel types de-

pending on the relative price of the input and the associated emission costs. Coal

emits, on average, approximately 2.5 times more carbon into the atmosphere than

natural gas for the same output of electricity.

Electricity generated from renewable energy sources are categorized into i) wind

power, ii) hydroelectric power, iii) biomass-based electricity, iv) photovoltaic elec-

tricity, and v) concentrating solar power.

Wind power generates electricity by exploiting wind to mechanically rotate a wind

turbine. Technological advancements have significantly increased efficiencies and

17

CHAPTER 2. INSTITUTIONAL BACKGROUND AND LITERATURE REVIEW

lowered the average cost of electricity output. Hydroelectric power exploits run-

ning water, typically from a reservoir, to drive a turbine that generates electricity.

It is a relatively stable source of electricity and can be constructed with very high

capacity. Hydroelectric power has been the primary source of renewable electric-

ity production in the European Union until recently when it ranks second to wind

power. Biomass-based electricity burns biomass, primarily wood, to create steam

that drives a turbine. Both photovoltaic and concentrating solar power use the

energy from the sun to create electricity (Rademaekers et al., 2011).

Development of the European Electricity Mix

Source: Jones (2020)

Figure 2.3: The European Electricity Mix

18

CHAPTER 2. INSTITUTIONAL BACKGROUND AND LITERATURE REVIEW

The European energy mix has undergone a significant shift towards less carbon-

intensive electricity generation. Since 2007, which was the last year of the first

phase of the EU ETS, electricity generation from coal has more than halved and

been entirely replaced by renewable energy sources, primarily wind power. In

2019, wind and solar power were responsible for a larger proportion of electric-

ity production than coal for the first time, and greenhouse gas emissions in the

electricity sector were 43% lower compared to the levels in 2007. Total electricity

generation has not changed considerably, with 3,312 TWh in 2005 and 3,227 TWh

in 2019.

Source: Jones (2020)

Figure 2.4: Illustration of the European Carbon Intensity

This transformation has been driven by multiple forces. An increased awareness

regarding global warming has increased demand for renewable energy sources,

with most electricity vendors offering “green energy” to its customers. Combined

with significant technological advancements in wind power that increase capacity

and efficiencies, investments in wind power increased substantially, often sup-

ported by government subsidies. In addition, the EU ETS’ price on emissions

has incentivized companies to invest in renewable energy production (Adabie and

19

CHAPTER 2. INSTITUTIONAL BACKGROUND AND LITERATURE REVIEW

Chamorro, 2008). Moreover, within the fossil-fuel generation, there has been a

large shift from coal to natural gas, driven by the increased cost of emissions. In

2019, for instance, a sharp increase in emission allowance prices partially drove

a significant fuel switch in thermal electricity generation from coal to natural gas

(Buck et al., 2020).

2.1.4 Price-Setting and the Merit Order Curve

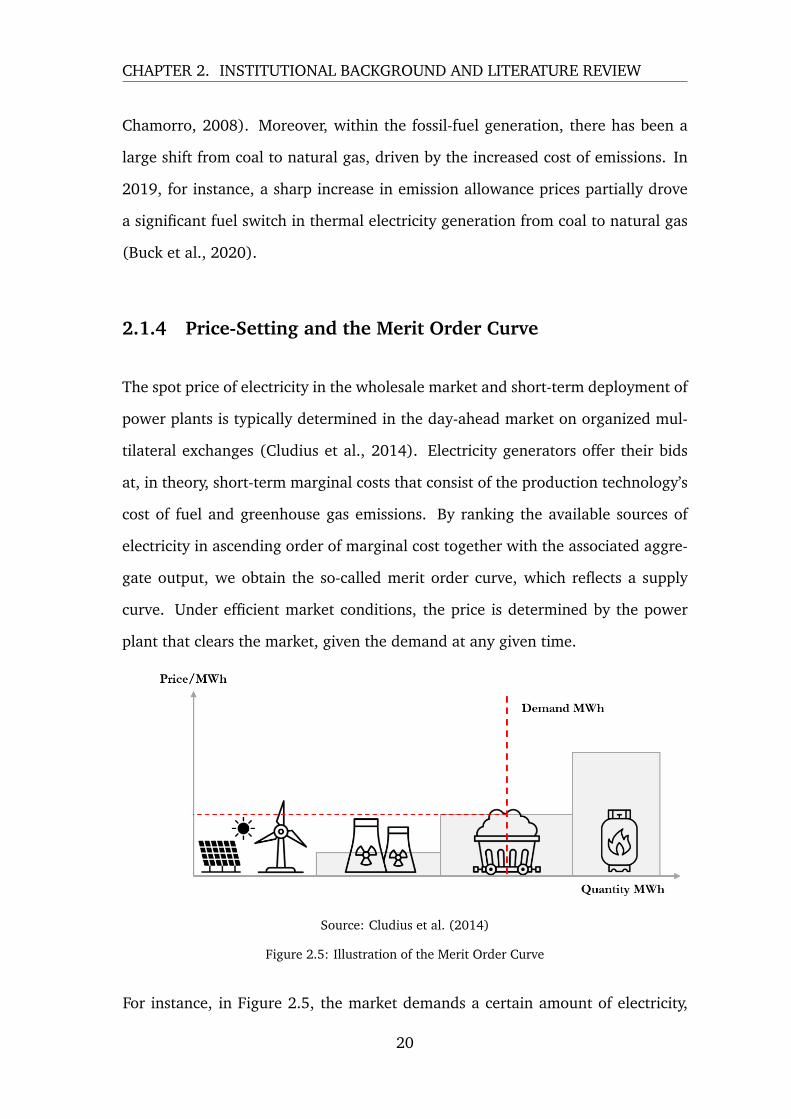

The spot price of electricity in the wholesale market and short-term deployment of

power plants is typically determined in the day-ahead market on organized mul-

tilateral exchanges (Cludius et al., 2014). Electricity generators offer their bids

at, in theory, short-term marginal costs that consist of the production technology’s

cost of fuel and greenhouse gas emissions. By ranking the available sources of

electricity in ascending order of marginal cost together with the associated aggre-

gate output, we obtain the so-called merit order curve, which reflects a supply

curve. Under efficient market conditions, the price is determined by the power

plant that clears the market, given the demand at any given time.

Source: Cludius et al. (2014)

Figure 2.5: Illustration of the Merit Order Curve

For instance, in Figure 2.5, the market demands a certain amount of electricity,

20

CHAPTER 2. INSTITUTIONAL BACKGROUND AND LITERATURE REVIEW

which makes coal clear the market. Coal is then the price-setting technology and

the marginal producer. Because renewable energy sources and nuclear power

plants have lower marginal costs, they are infra-marginal producers with positive

contribution margins.

2.2 The European Union Emissions Trading System

The first indication of a European emission trading system appeared in 2000 when

the European Commission issued Green Paper on Greenhouse Gas Emissions Trading

within the European Union (Denny Ellerman et al., 2016). The EU ETS Directive

(Directive 2003/87/EC) was adopted in 2003 and subsequently launched in 2005

across all 27 member states as a policy instrument to ensure that the European

Union would meet its legally obligated emission reduction target of the 1997 Kyoto

protocol (Chevallier, 2012).

The EU ETS is a “cap and trade” system in which a cap is set on the total amount of

greenhouse gas emissions that can be emitted during a year. Each company must

surrender enough allowances to cover its installations’ emissions by year-end, or

hefty fines will be imposed (Chevallier, 2012). Because the cap is reduced over

time, the total emissions of the European Union are reduced.

Within the cap, companies can meet on the market and trade allowances. As

such, a price on greenhouse gas emissions is formed, which serves to incentivize

profit-maximizing companies to invest in green technologies that reduce emissions

(Hintermann et al., 2016). The companies that are able to reduce their greenhouse

emissions at a lower cost than the price of carbon will be financially incentivized

to do so. Under perfect market conditions in equilibrium, the marginal abatement

cost will equal the price of carbon and will be identical for all companies. As such,

21

CHAPTER 2. INSTITUTIONAL BACKGROUND AND LITERATURE REVIEW

investments will be concentrated at the most cost-effective abatement opportuni-

ties, which leads to a reduction in emissions at the lowest economic cost.

As of 2014, more than 13,500 energy-intensive installations responsible for ap-

proximately four percent of global greenhouse gas emissions are covered by the

system (Hintermann et al., 2016) making it the largest market for greenhouse gas

emissions (European Commission, 2015). Since its inception in 2005, the system

has been successfully implemented during three distinct phases, with the fourth

phase set to begin in 2021.

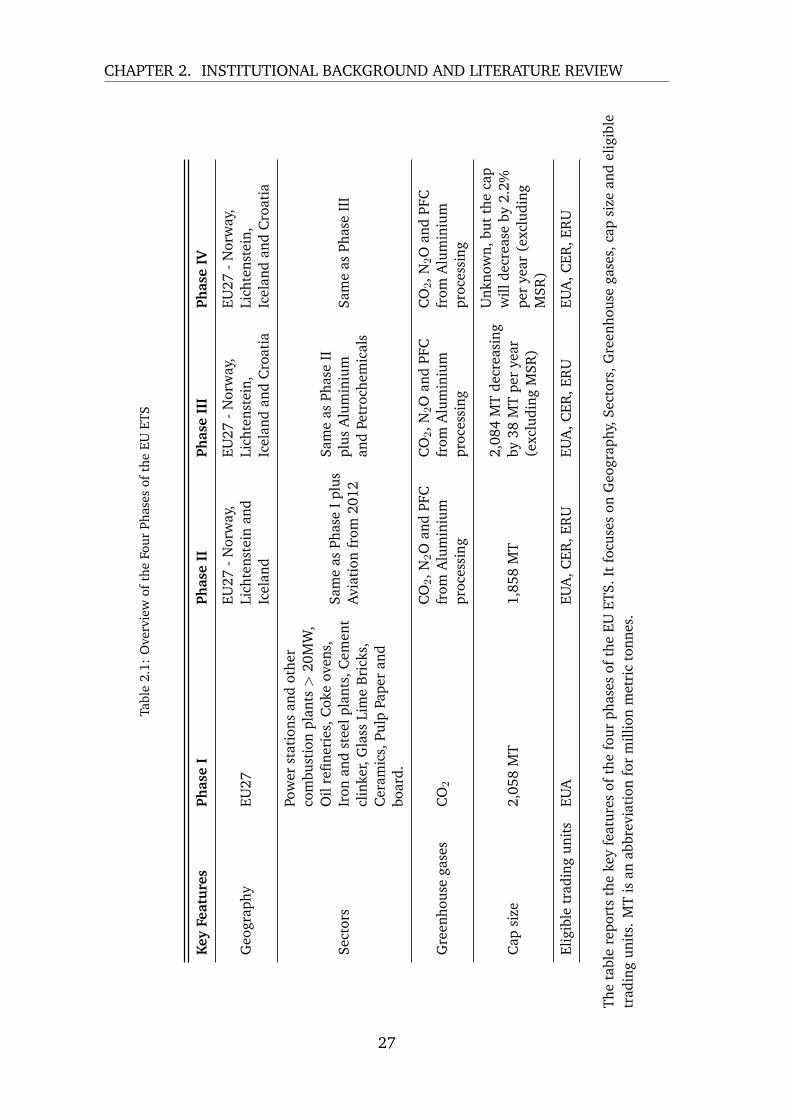

2.2.1 Evolvement of the EU ETS

Phase I: 2005 - 2007

The first phase of the EU ETS served as a “warm up phase” aimed at establishing

a price on carbon dioxide emissions, free trade in emission allowances, and the

infrastructure to monitor, report and verify emissions from installations covered

by the system (European Commission, 2013). In addition to power stations and

other combustion plants with an output above 20 MW, oil refineries, coke ovens,

iron and steel plants, cement clinkers, glass, lime, bricks, ceramics, pulp, as well as

the paper and board sectors were included in the system (European Commission,

2015). Together they covered 46% of the total CO2 emissions of EU countries with

the electricity sector being the largest emitter (Oberndorfer, 2009). Nine out of ten

allowances were allocated free-of-charge to limit the risk of adversely impacting

European competitiveness on international markets, which would result in carbon

spillover to countries outside the EU. A penalty charge to companies that failed

to sufficiently surrender allowances was set to e40 per ton of CO2. The price of

carbon dioxide reached e8 per ton in the first month (Chevallier, 2012).

22

CHAPTER 2. INSTITUTIONAL BACKGROUND AND LITERATURE REVIEW

Each covered country established its own “National Allocation Plan” that deter-

mined the amount of allowances that would be available for the country and how

they would be distributed between sectors (European Commission, 2015). The

National Allocation Plans had to comply with the criteria set out by the European

Commission in the ETS Directive to be approved. As such, the total EU cap con-

sisted of each member state’s respective national caps and would not be known

until all National Allocation Plans had been approved (Denny Ellerman et al.,

2016).

The EU had not yet gathered reliable emissions data, and the initial cap was set

based on estimates. In 2007, when the EU disclosed the emissions data compiled

from the monitoring activities, it became clear that the EU had vastly overallocated

allowances available in the market (Chevallier, 2012). At the time, an allowance

had limited temporal value as it could not be banked to the second phase that

would soon follow. This led to high volatility and spot prices plummeting dramat-

ically to a value of zero from e25-30 just months before (Aatola et al., 2013).

Phase II: 2008 - 2012

Phase II extended the EU ETS’ scope in sectors to include domestic aviation, in

geography to include Norway, Iceland, and Lichtenstein, and in emission types

by voluntary opt-in of nitrous oxide (N2O) (European Commission, 2015). The

system was linked to international carbon dioxide markets by accepting certain

Kyoto Protocol emission units under the Clean Development Mechanism (CDM)

and Joint Implementation (JI) alongside European Union Emission Allowances

(EUAs) (European Commission, 2015). These arrangements allow industrialized

countries to reduce their greenhouse gas emissions through international invest-

ments that reduce emissions in developing countries. The Kyoto credits that are

generated through CDM and JI projects are interchangeable with EUAs and can

23

CHAPTER 2. INSTITUTIONAL BACKGROUND AND LITERATURE REVIEW

thus be surrendered to offset greenhouse gas emissions subject to the regulation

(Denny Ellerman et al., 2016). The cap for these offsets during the second phase

was set to 1.3 billion (total cap in 2008 was 1.9 billion), but investments in large

hydroelectric power and forestry projects were not eligible. Although EU ETS was

the largest market for carbon dioxide and the primary driver for demand of Kyoto

credits, the use of offsets only constituted 10% of the cap despite being a perfect

substitute for EUAs (Denny Ellerman et al., 2016).

Trading volumes increased, and price volatility decreased during the second phase

due to a tighter emissions cap and because allowances were allowed to be banked

over the years (Aatola et al., 2013). Research finds that the more stringent emis-

sions cap significantly reduced emissions during the second phase (Martin & Wag-

ner, 2016).

Phase III: 2013 - 2020

The first commitment period of the Kyoto protocol ended in 2012, and it was

not followed by the Doha Amendment. In the absence of an international agree-

ment on greenhouse gas emission reduction, the third phase corresponds to the

objective of the EU’s Energy Climate Package introduced in 2008 with the goal of

reducing emissions by 20% by 2020 compared to 1990 (Chevallier, 2012).

The scope was extended in geography to include Croatia (that joined the EU in

2013), and in sectors by including the aluminium and petrochemical sectors and

in types by including N2O emissions from all installations and PFC from aluminium

production (European Commission, 2015).

A pan-EU cap for stationary installations declining by a linear factor of 1.74% com-

pared to the average total quantity of allowances issued annually in 2008 - 2012

was adopted. This corresponds to a decrease in absolute terms of 38,264,246 al-

24

CHAPTER 2. INSTITUTIONAL BACKGROUND AND LITERATURE REVIEW

lowances per year and would ensure a decrease in emissions from EU ETS covered

sectors by 21% compared to levels in 2005 (European Commission, 2015).

Although auctioning became the default allocation method in Phase III, a signif-

icant amount of allowances are still being issued for free. The power generation

sector, however, has been subject to full-auctioning since 2013 except for instal-

lations in certain countries covered by Article 10c of the EU ETS Directive. It

provided derogation from the default auctioning allocation method until 2019 to

support modernization investments that reduced the reliance on coal to generate

electricity. At the minimum, investments to diversify the energy mix and mod-

ernize their respective electricity sectors had to amount to the value of the free

allowances that were issued. Of ten eligible countries, eight states made use of the

exception: Bulgaria, Cyprus, Czech Republic, Estonia, Hungary, Lithuania, Poland

and Romania. (European Commission, 2015). The power generation sector was

considered suitable for full-auctioning due to its relatively low abatement costs to

reduce emissions and the weak exposure to international competition from firms

not covered by the EU ETS (Chevallier, 2012).

Phase IV: 2021 - 2030

The fourth phase of the EU ETS will begin from 2021 and run until 2030. To

increase the pace of the decrease in emissions, the EU will increase the annual

linear reduction rate of emissions to 2.2%, compared to 1.74% in phases III. The

purpose is to achieve a reduction in greenhouse gas emissions for sectors in the

EU ETS by 46% compared to the 2005 level. Also, the Market Stability Reserve

play a larger role in phase IV as the number of allowances put in the reserve

will temporarily double to 24% of the total number of allowances in circulation

from 2019 to 2023, after which the rate will return to 12% in 2024. The Market

Stability Reserve will be described in further detail in Section 2.2.2 but aims to

25

CHAPTER 2. INSTITUTIONAL BACKGROUND AND LITERATURE REVIEW

reduce the current overallocation of the total number of allowances in circulation.

The fourth phase will address the risk of carbon leakage by providing predictable,

robust, and a fair set of rules. The EU defines carbon leakage as an increase in

greenhouse gas emissions in one country as a product of strict climate policy in

another. The system of free allocation will be continue for another decade but will

focus on sectors at the highest risk of relocating their operations outside of the EU.

These sectors will continue receiving allowances for free, but free allocation will be

phased out to less exposed sectors by the end of phase IV. (European Commission,

2019b).

Additionally, as part of the fourth phase, there will be an increase in ”green” in-

vestments to modernize the system. The EU will set up several low-carbon fund-

ing mechanisms to help energy-intensive industrial sectors and the power sector

to meet the innovation and investment challenges facing the transition to a low

carbon economy. The two main new initiatives are an innovation fund and a mod-

ernization fund. The innovation fund will support the innovative technologies in

the industry and will be an extension of an existing fund and will correspond to a

market value of at least 450 million emission allowances. The modernization fund

will support investments in modernizing energy systems, energy efficiency, and fa-

cilitating the transition in carbon dependent regions in 10 lower-income member

states (European Commission, 2019b).

26

CHAPTER 2. INSTITUTIONAL BACKGROUND AND LITERATURE REVIEW

Tabl

e2.

1:O

verv

iew

ofth

eFo

urPh

ases

ofth

eEU

ETS

Key

Feat

ure

sPh

ase

IPh

ase

IIPh

ase

III

Phas

eIV

Geo

grap

hyEU

27EU

27-N

orw

ay,

Lich

tens

tein

and

Icel

and

EU27

-Nor

way

,Li

chte

nste

in,

Icel

and

and

Cro

atia

EU27

-Nor

way

,Li

chte

nste

in,

Icel

and

and

Cro

atia

Sect

ors

Pow

erst

atio

nsan

dot

her

com

bust

ion

plan

ts>

20M

W,

Oil

refin

erie

s,C

oke

oven

s,Ir

onan

dst

eelp

lant

s,C

emen

tcl

inke

r,G

lass

Lim

eB

rick

s,C

eram

ics,

Pulp

Pape

ran

dbo

ard.

Sam

eas

Phas

eI

plus

Avi

atio

nfr

om20

12

Sam

eas

Phas

eII

plus

Alu

min

ium

and

Petr

oche

mic

als

Sam

eas

Phas

eII

I

Gre

enho

use

gase

sC

O2

CO

2,N

2O

and

PFC

from

Alu

min

ium

proc

essi

ng

CO

2,N

2O

and

PFC

from

Alu

min

ium

proc

essi

ng

CO

2,N

2O

and

PFC

from

Alu

min

ium

proc

essi

ng

Cap

size

2,05

8M

T1,

858

MT

2,08

4M

Tde

crea

sing

by38

MT

per

year

(exc

ludi

ngM

SR)

Unk

now

n,bu

tth

eca

pw

illde

crea

seby

2.2%

per

year

(exc

ludi

ngM

SR)

Elig

ible

trad

ing

unit

sEU

AEU

A,C

ER,E

RU

EUA

,CER

,ER

UEU

A,C

ER,E

RU

The

tabl

ere

port

sth

eke

yfe

atur

esof

the

four

phas

esof

the

EUET

S.It

focu

ses

onG

eogr

aphy

,Sec

tors

,Gre

enho

use

gase

s,ca

psi

zean

del

igib

letr

adin

gun

its.

MT

isan

abbr

evia

tion

for

mill

ion

met

ric

tonn

es.

27

CHAPTER 2. INSTITUTIONAL BACKGROUND AND LITERATURE REVIEW

2.2.2 Market Stability Reserve

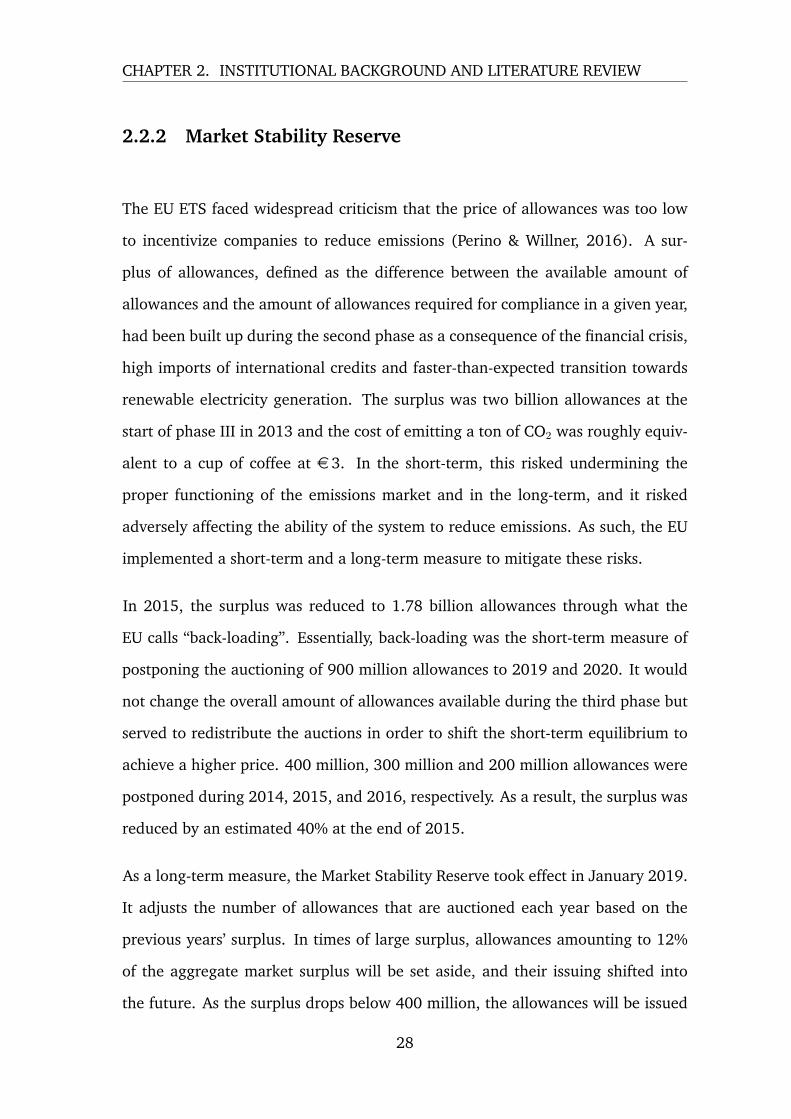

The EU ETS faced widespread criticism that the price of allowances was too low

to incentivize companies to reduce emissions (Perino & Willner, 2016). A sur-

plus of allowances, defined as the difference between the available amount of

allowances and the amount of allowances required for compliance in a given year,

had been built up during the second phase as a consequence of the financial crisis,

high imports of international credits and faster-than-expected transition towards

renewable electricity generation. The surplus was two billion allowances at the

start of phase III in 2013 and the cost of emitting a ton of CO2 was roughly equiv-

alent to a cup of coffee at e3. In the short-term, this risked undermining the

proper functioning of the emissions market and in the long-term, and it risked

adversely affecting the ability of the system to reduce emissions. As such, the EU

implemented a short-term and a long-term measure to mitigate these risks.

In 2015, the surplus was reduced to 1.78 billion allowances through what the

EU calls “back-loading”. Essentially, back-loading was the short-term measure of

postponing the auctioning of 900 million allowances to 2019 and 2020. It would

not change the overall amount of allowances available during the third phase but

served to redistribute the auctions in order to shift the short-term equilibrium to

achieve a higher price. 400 million, 300 million and 200 million allowances were

postponed during 2014, 2015, and 2016, respectively. As a result, the surplus was

reduced by an estimated 40% at the end of 2015.

As a long-term measure, the Market Stability Reserve took effect in January 2019.

It adjusts the number of allowances that are auctioned each year based on the

previous years’ surplus. In times of large surplus, allowances amounting to 12%

of the aggregate market surplus will be set aside, and their issuing shifted into

the future. As the surplus drops below 400 million, the allowances will be issued

28

CHAPTER 2. INSTITUTIONAL BACKGROUND AND LITERATURE REVIEW

to the market in intervals of 100 million per year (European Commission, 2013).

This process will continue until the surplus is depleted. The reserve operates com-

pletely based on a set of predefined rules and leaves no room for discretion to

the EU or member states. The aforementioned reintroduction of the back-loaded

allowances during 2014 to 2016 was cancelled and put in the reserve instead.

2.3 Literature Review

2.3.1 European Union Allowances and Firm Financial Perfor-

mance in the Electricity Sector

Even before the system was implemented in 2005, simulations suggested that the

EU ETS would benefit the electricity sector as a whole, as long as allowances were

distributed free of charge (Bode, 2006). A price on emissions constitutes an oppor-

tunity cost as an allowance can either be used as an input factor to cover emissions

or be sold to another firm that demands it, regardless of whether it was provided

for free or not. As such, the marginal production cost increases for companies

subject to the regulation, and profit-maximizing firms will attempt to transfer this

cost to its customers. In doing so, companies face the risk of losing market share to

competition not covered by the EU ETS. However, the electricity sector in the EU

has inherent entry barriers from foreign competition due to technical aspects that

limit the possible import penetration of electricity (Marin et al., 2018). As such,

electricity companies can transfer much of the opportunity cost that the price of

an allowance represents to its customers.

Sijm et al. (2006) combined spot and forward market prices of electricity in the

Netherlands and Germany with the price of EUA to investigate the pass-through

29

CHAPTER 2. INSTITUTIONAL BACKGROUND AND LITERATURE REVIEW

rate of the emission compliance costs to wholesale electricity prices. They find

that the pass-through rate, defined as the average increase in power price over a

certain period due to the increase in the price of an emission allowance, varied be-

tween 60 to 100% depending on the carbon intensity of the marginal production

technology. As an example, consider a typical coal power station that emits 0.95

ton of CO2 per MWh and compare it with a gas power station that emits 0.48 ton

of CO2 per MWh. The pass-through rate of the emission allowances on the whole-

sale electricity price is determined by which of the two power stations that are

currently setting the price. At a price of e20 per ton of emissions, the generation

cost per MWh for the gas plant increases by e9.6 and by e17 for the coal plant.

Consequently, the pass-through rate is higher when coal is the marginal producer.

Because allowances were allocated to electricity companies free of charge during

the first phase, electricity companies were able to reap large profits. Using numer-

ical models, Sijm et al. (2006) estimate that EU ETS induced windfall profits in

the Dutch power sector amounted to e300-600 million per year.

Because stock prices theoretically reflect firms’ future discounted cash flows, economists

often use stock-market data to estimate the impact on profits from policies (Marin

et al., 2018). Oberndorfer (2009) found that stock prices of EU electricity compa-

nies reacted positively to appreciations in EU ETS prices and negatively to depre-

ciation during the first phase of trading. Oberndorfer employed panel regressions

using an aggregated equally weighted portfolio of the most important electric-

ity stocks in the Eurozone as well as disaggregated pooled panel data regression.

The market returns, as well as oil, natural gas and electricity price returns, were

included as control variables to the regressions. The author stresses that this

is important not only because of their impact as input factors but also due to

their influence on the emission allowance price itself. The factor-beta coefficients

for emission allowances are positive at 0.02 and 0.01 for the aggregate equally

weighted portfolio and the pooled OLS, respectively, and significant with a p-value

30

CHAPTER 2. INSTITUTIONAL BACKGROUND AND LITERATURE REVIEW

below 1%. Oberndorfer argues that the positive influence is due to windfall prof-

its that occur as a result of the high pass-through rate of the opportunity cost of

the grandfathered emission allowances. Oberndorfer (2009) investigates the ef-

fect on a country-specific level and finds that the results hold true for all countries

investigated except Spain. Oberndorfer (2009) argues that Spain’s stringent price

regulation that limits the pass-through rate could be the reason for the inverse

effect. Zachmann and von Hirschhausen (2008) found that positive price shocks

in emission allowances disseminated more quickly to the final German wholesale

electricity price than negative price shocks and suggest that this price asymme-

try may be due to market power or ignorance amongst market agents due to the

immaturity of the market. This could result in increased profits but Oberndor-

fer (2009) did not find that such an asymmetry existed in stock price reactions,

indicating that market participants were either unaware of the asymmetric price

reactions in the wholesale electricity prices or that it was a German phenomenon.

Similar to Oberndorfer (2009), Veith et al. (2009) measure the EU ETS impact on

firm performance through investor expectations by employing a multifactor model

on a sample of 22 publicly traded electricity firms accounting for two-thirds of total

EU electricity generation. In line with Oberndorfer (2009), they find a positive re-

lationship between emission allowance futures prices and stock prices, indicating

financial market agents expect that electricity companies obtain higher earnings

by passing on the opportunity cost of the emission allowances to wholesale elec-

tricity prices. The authors fit the emission allowance return into their subperiod

pooled panel regressions and estimate that carbon prices positively yielded an es-

timated average stock market return by 0.8% during the first six months of the

trading system, suggesting that electricity generators may obtain regulatory rent.

As a robustness check, they again regress stock performance on overall stock per-

formance and emission allowance returns for companies that have carbon-neutral

electricity generation and thus fall outside of the system. Although these firms

31

CHAPTER 2. INSTITUTIONAL BACKGROUND AND LITERATURE REVIEW

sell the same common good as firms covered by the system, the empirical results

do not show a connection between emission allowance return and stock perfor-

mance. The authors present a lack of market power as a possible explanation, or

that investors in these entities do not consider emission price movements. In addi-

tion to regressing return on emission allowance returns and overall stock market

return, they control for commodity price impact by including the return on oil and

natural gas to a fixed effects regression model. The results regarding emission

allowance futures return remain robust with a factor-beta coefficient of 0.023 and

significant at 5%. Next, they further check for the robustness by controlling for

firm-specific characteristics in terms of fuel mix by including a dummy variable

equaling one if the company’s proportion of carbon-emitting electricity generation

is above the sample median. The binary variable is interacted with the return on

emission allowance prices to allow for both different intercept and slope. There is

no interaction effect when regressing emission allowance spot prices, but a slightly

negative coefficient when using emission allowance December 2008 futures. The

firms with a high share of fossil fuels in electricity generation lose approximately

half of the positive influence of emission allowance returns. According to the au-

thors, this indicates that investors did not consider the underlying fuel mix during

the first phase of the EU ETS that would end in December 2007 but that investors

expected future cash flows to be affected during the second phase. They argue

that investors likely anticipated and discounted adverse economic effects resulting

from a higher degree of auctioning that would be enforced during the subsequent

phase.

Bushnell et al. (2013) conducted an event study on how the large price decline in

emission allowances in April 2006 affected the stock prices of 552 European com-

panies subject to EU ETS in different sectors. They find that share prices within the

power sector decline, and that “clean” electricity companies’ share prices decline

further than their “dirty” counterparts. The authors argue that this implies that

32

CHAPTER 2. INSTITUTIONAL BACKGROUND AND LITERATURE REVIEW

the market understood that declining emission prices would reduce contribution

margins more severely for less carbon-intensive power generators. High emitting

electricity companies also experienced abnormal declines in share price, and the

authors suggest that this highlights a focus on revenue rather than costs among

investors.

To our knowledge, there has been no published research on the potential effects

of EUA price changes on firm performance among European electricity firms dur-

ing the second or third phase of the EU ETS. All the abovementioned studies lay

forward that their results may not hold true during later phases of the EU ETS,

primarily due to the end of grandfathering (Sijm et al., 2006; Oberndorfer, 2009;

Veith et al., 2009; Bushnell et al., 2013) and that the market becomes more effi-

cient as market agents become better informed (Oberndorfer, 2009; Bushnell et

al., 2013).

2.3.2 Pricing of European Union Allowances

The price of a ton of greenhouse gas emission in the EU ETS is determined by

the equilibrium between supply and demand in the market. Supply is primarily

determined by EU policy decision such as the size of the emissions cap, allocation

methods, linkages to international greenhouse gas emission markets and rules

about banking and borrowing of allowances. An example of the impact of supply

on EUA prices is the crash in 2006 when the markets realized that the EU had

oversupplied participants with allowances (Alberola et al., 2008). Hintermann

et al. (2016) review the literature of pricing during the second phase of the EU

ETS and find that demand is primarily determined by the amount of “business as

usual” emissions, which are mainly driven by the growth of the economy, its energy

efficiency and emission intensity. During times of economic growth, emissions

33

CHAPTER 2. INSTITUTIONAL BACKGROUND AND LITERATURE REVIEW

increase together with industrial production, which drives demand for allowances

resulting in price appreciations (Chevallier, 2012). Even unanticipated extreme

weather conditions drive demand for EUAs. For instance, during exceptionally

hot summer months or freezing winter months, households’ increased cooling and

heating have a short-term impact on business-as-usual emissions (Alberola et al.,

2008).

Moreover, in the Nordic region, low-marginal cost and renewable hydroelectric

power is responsible for baseload generation and constitutes more than half of

total electricity output in Sweden and Norway. As such, when water reservoir lev-

els are low, more carbon-intensive technologies must replace part of hydroelectric

power’s output leading to an increased demand for emission rights (Rickels et al.,

2012). Prices are also determined by the available abatement options and their

respective costs (Hintermann et al., 2016). As an example, coal and gas power

plants are commonly able to switch between the fuel types. Because natural gas

emits at least half as much as coal, a sector-wide switch between the two fuel types

can have an effect on the price of EUAs (Aatola et al., 2013).

34

Chapter 3: Theory and Hypotheses

The following chapter provides an explanation of the theory used to answer the

research question at hand. We will begin by explaining the Arbitrage Pricing The-

ory and then the Efficient Market Hypothesis and lastly turn to how these theories

are implemented to form testable hypotheses.

3.1 Theory

3.1.1 Arbitrage Pricing Theory

The Arbitrage Pricing Theory (APT) was developed by Ross (1976) as a multi-

factor asset pricing model that asserts a security’s expected return as a linear func-

tion of its relationship to various macroeconomic factors. The return of a risky

asset is determined by a set of common factors and an idiosyncratic risk compo-

nent:

E[ri] = α + βi,k · Fk + βi,k+1 · Fk+1 + εi (3.1)

where E[εi] = 0 by construction, whereas Cov[Fk, εi] = 0 and Cov[εi, εj] = 0 for

i 6= j by assumption. Multifactor models are tools that allow us to investigate the

ultimate source of risk and are useful to measure a risky asset’s exposure to certain

sources of uncertainty. As an example, Chen et al. (1986) identified the following

35

CHAPTER 3. THEORY AND HYPOTHESES

macroeconomic factors as significant in explaining security returns:

• Surprises in inflation

• Surprises in GDP as indicated by industrial production index

• Surprises in investor confidence due to changes in default premium in cor-

porate bonds

• Surprise shifts in the yield curve

The equation above forms a multidimensional security characteristic line (SCL)

that consists of a set of factors, whose beta-values are estimated using multivariate

regression analysis for a particular security (Bodie et al., 2011). Each beta-value

represents the security’s sensitivity to the respective factor’s systematic risk. As

such, an unexpected increase of one unit in a factor is associated with a change in

the expected return of the security equivalent to the beta-value (Berk & DeMarzo,

2017). The residual variance of the regression represents an idiosyncratic risk.

Although the arbitrage theory of capital asset pricing was developed as an alter-

native to the Capital Asset Pricing Model developed by Sharpe (1964), Lintner

(1965) and Treynor (1962), it does not assume that markets are perfectly effi-

cient Ross (1976). Hence, the market may occasionally misprice securities until

arbitrageurs exploit the anomaly, which adjusts the price to its fair value accord-

ing to the Law of One Price. As such, the APT does not assume that all investors

hold identical portfolios, namely the market portfolio identified through a mean-

variance model. Instead, investors hold highly diversified but different portfolios

that essentially have no idiosyncratic risk. In applications, however, it is assumed

that there is no idiosyncratic risk and that the equation above can explain the

expected return of a security.

36

CHAPTER 3. THEORY AND HYPOTHESES

3.1.2 Efficient Market Hypothesis

The Efficient Market Hypothesis was formalized by Fama (1970) and assumes

that security prices at any time fully reflect all available information. A market in

which prices always fully reflect all available information is efficient. There are

three levels of efficiency:

• The weak-form hypothesis states that security prices reflect all historical

trading data such as past returns, trading volumes and interest rates. This

implies that trend analysis is fruitless.

• The semi strong-form hypothesis asserts that all publicly available informa-

tion is reflected in the price of the security. Such information includes news

regarding product lines, management etc. in addition to historical trading

data.

• The strong-form version states that all information, including inside infor-

mation, is reflected in the stock price.

The dividend discount model states that the stock price is determined by the dis-

counted value of all future dividends (Berk & DeMarzo, 2017):

Pt =∞∑j=1

Dt+j

(1 + rt+j)(3.2)

Hence, any price change must be due to changes in expected future dividends or

the discount rate. Assuming markets are indeed efficient, firm performance can be

gauged through the stock price (Veith et al., 2009; Oberndorfer et al., 2012).

37

CHAPTER 3. THEORY AND HYPOTHESES

3.2 Hypotheses

This paper aims to find how changes in EUA prices affect firm performance of

European electricity generating firms. According to Arbitrage Pricing Theory, a

security’s expected return can be explained through its systematic exposure to

various macroeconomic factors, such as the return of EUA allowances. As such, a

positive effect should be revealed by a positive factor-beta coefficient on EUA price

changes through multivariate linear regression. A change in expected return, and

thereby stock price, reflects the expected future cash flows of the firm according

to the Efficient Market Hypothesis, and can, therefore, be used as a proxy for firm

financial performance.

Similar studies have already been conducted on the subject and argued for a pos-

itive effect on firm performance (Veith et al., 2009; Oberndorfer et al., 2012).

However, these studies were based on data from the first phase of the European

Union Emissions Trading System, and their results cannot be generalized to hold

during the currently active third phase of the system as there are several significant

differences. For instance, the emissions market has matured, and market agents

may have developed their understanding of the dynamics of the market. As such,

it is possible that the market has become more efficient and that participants have

changed their perceptions on how EUA price changes affect firm performance.

Moreover, multiple important policy changes may have changed the fundamental

functioning of the market. For the electricity sector, as an example, auctioning is

now the default method of emission allowance allocation and replaced free allo-

cation. Hence, one could suspect that the previously mentioned windfall profits

associated with grandfathering no longer occur. Additionally, renewable energy

sources have penetrated the European electricity market and are now responsible

for approximately one-third of electricity production output in the EU as compared

38

CHAPTER 3. THEORY AND HYPOTHESES

with a fifth just a decade ago (European Commission, 2019a). As such, the merit

curve may have been shifted in a way that changes the rent obtained by carbon

efficient inframarginal producers from its exposure to emission compliance costs.

Electricity generating technologies from the left: solar and wind power, nuclear power, thermalcoal power, and thermal natural gas power. Source: Cludius et al. (2014)

Figure 3.1: Illustration of the Merit Order Curve with emission compliance costs

We suspect that the implications of these changes apply different forces on the

relationship between EUA price changes and firm performance among electricity

generating firms. As an example, the penetration of renewable energy sources

during the last decade should arguably increase the positive effect, whereas the

end of grandfathering should have an opposite effect. These conflicting forces

notwithstanding, research shows that EUA price increases are passed on to con-

sumers in the bids of the marginal producer. As such, emission allowances do not

represent a significant regulatory burden for the marginal producer. Moreover, the

contribution margin of inframarginal producers increases with increased emission

allowance prices resulting in an overall increase in profitability that will be re-

flected in the stock prices of the respective companies. As an example, consider

the chart above, in which the dark area represents the costs of emissions for the

coal generating marginal producer. The arrow illustrates the pass-through of the

allowance price to the consumer, assuming 100% pass-through rate, resulting in

39

CHAPTER 3. THEORY AND HYPOTHESES

regulatory rents for the inframarginal producers. This leads to the first hypothesis

of the paper:

Hypothesis I: Emission allowance price increases (decreases) positively (negatively)

affected electricity generating stock returns during the sample period.

By the same logic as above, we suspect that inframarginal companies with a higher

share of low-margin renewable electricity generation obtained even larger contri-

bution margins than their more carbon-intensive counterparts. This leads to the

second hypothesis of the paper:

Hypothesis II: EU Emission allowance price increases (decreases) had a larger pos-

itive (negative) effect on carbon efficient electricity generating stock returns during

the sample period.

40

Chapter 4: Methodology

In Chapter IV, we present the data and methodology used to empirically test our

hypotheses. First, we present our research approach. Next, we introduce the data

used in our econometric analysis. Last, we present the econometric methodology.

4.1 Research Approach

This thesis is based on a deductive research approach in which we formulate a

set of hypotheses built upon existing theory and previous research. Based on the

hypotheses, we design a methodology that aims to test whether the hypotheses

hold true. Our empirical research is primarily based on the methodology of Veith

et al. (2009) and Oberndorfer (2009) that investigated the relationship between

price changes in EU emission allowances and financial performance of electricity-

generating firms during the first phase of the EU ETS. To increase reliability, fi-

nancial data is primarily retrieved from organized financial databases. Data on

firm-specific carbon intensity was obtained from a report published by PwC or

from reports published by the respective company. Price data for stocks, market

index, oil and natural gas were used to calculate weekly returns that were used

in the subsequent econometric analysis. To strengthen validity, we employ multi-

ple diagnostic tests to the data and econometric models. Additionally, robustness

is increased by controlling for commodity price impact and employing regression

41

CHAPTER 4. METHODOLOGY

models using aggregate and disaggregate stock return data as well as controlling

for firm-specific fixed effects.

4.2 Data

4.2.1 Firms

The sample selection was conducted in a series of steps. First, we identified the

largest publicly traded companies in the utility sector by market capitalization via

the Dow Jones STOXX Europe 600 Utilities index. It is the largest index of listed

utility companies in Europe. Next, we excluded companies that were not listed

in the index during the whole sample period of January 2013 to December 2019,

which left 26 companies. We then excluded companies that fell under the Water

Utility classification based on their Global Industry Classification Standard. Lastly,

we assessed whether the firm was involved in electricity generation throughout

the sample period via the information provided in their respective annual reports

for 2013 and 2018 or 2019. In the end, thirteen firms remained in the sample.

These firms are presented in Table 4.1. The stock return data of the companies

was retreived from Bloomberg.

42

CHAPTER 4. METHODOLOGY

Tabl

e4.

1:O

verv

iew

ofth

eco

mpa

nies

unde

ran

alys

is

Nam

eA

bbre

viat

ion

Tick

er(I

SIN

)C

oun

try

ofhe

adqu

arte

rC

arbo

nin

ten

sity

for

2015

(gC

O2/k

Wh)

SSE

PLC

SSE

GB

0007

9087

33U

nite

dK

ingd

om39

7En

desa

SAEL

EES

0130

6701

12Sp

ain

460*

Iber

drol

aSA

IBE

ES01

4458

0Y14

Spai

n21

7Ve

rbun

dA

GV

ERAT

0000

7464

09A

ustr

ia55

Nat

urgy

Ener

gyG

roup

SAN

TGES

0116

8703

14Sp

ain

431

Cen

tric

apl

cC

NA

GB

00B

033F

229

Uni

ted

Kin

gdom

145*

Engi

eSA

ENG

FR00

1020

8488

Fran

ce37

7El

ectr

icit

ede

Fran

ceSA

EDF

FR00

1024

2511

Fran

ce81

EDP

-Ene

rgia

sde

Port

ugal

EDP

PTED

P0A

M00

09Po

rtug

al52

0A

2ASp

AA

2AIT

0001

2334

17It

aly

436

Fort

umO

yjFO

RFI

0009

0071

32Fi

nlan

d21

Enel

SpA

ENE

IT00

0312

8367

Ital

y40

9R

WE

AG

RW

ED

E000

7037

129

Ger

man

y72

1

The

firm

-spe

cific

info

rmat

ion

has

been

colle

cted

thro

ugh

annu

alre

port

san

dB

loom

berg

term

inal

.Th

eca

rbon

inte

nsit

yw

asob

tain

edfr

omPw

C’s

Clim

ate

Cha

nge

and

Elec

tric

ity

repo

rt.

*End

esa

SAan

dC

entr

ica

plc

wer

eno

tin

clud

edin

the

Clim

ate

Cha

nge

and

Elec

tric

ity

repo

rtfr

omPw

C.

How

ever

,th

eca

rbon

inte

nsit

yfo

rEn

desa

SAan

dC

entr

ica

plc

was

obta

ined

thro

ugh

Ende

saSA

’sSu

stai

nabi

lity

Rep

ort

from

2015

and

aC

arbo

nD

iscl

osur

ePr

ojec

tfo

rC

entr

ica

from

2015

.So

urce

:En

desa

(201

5),P

wC

(201

6),C

entr

ica

(201

7)

43

CHAPTER 4. METHODOLOGY

4.2.2 Carbon Intensity

Carbon intensity is defined as the emission per unit of electricity output generated

and is usually measured in gCO2/kWh. We are concerned with the carbon inten-

sity of the firms’ portfolio of power plants located in Europe. We obtained the

carbon intensity in 2015 for the electricity-generating firms from the report Cli-

mate Change and Electricity published by PwC in 2016. The report did not include

the carbon intensity for Endesa SA and Centrica plc. Instead, carbon intensity for

Endesa SA was retreived from its 2015 annual sustainability report and the carbon

intensity for Centrica plc was obtained from a questionnaire to the organization

Carbon Disclosure Project.

Source: Endesa (2015), PwC (2016), Centrica (2017)

Figure 4.1: Carbon Intensity for sample firms

We create a binary variable that equals 1 if the company’s carbon intensity is above

the sample median and 0 otherwise. This allows us to divide our sample firms into

44

CHAPTER 4. METHODOLOGY

a carbon efficient and carbon intensive group.

Figure 4.1 shows the carbon intensity for the firms under analysis and the Eu-

ropean Union carbon intensity average. Notice that there is a large dispersion

between the firms under analysis regarding carbon intensity.

4.2.3 European Union Allowance Prices

Companies with installations subject to the EU ETS must surrender allowances

to cover their emissions by year-end. We assume that market participants are

risk-averse and that they hedge their exposure to EUA price fluctuations by taking

positions in futures December contracts. EUA futures with expiration in Decem-

ber have significantly higher volumes than emission allowances traded in the spot

market and should, therefore, reflect prices better. Moreover, futures’ prices are

less affected by short run demand and supply fluctuations and thus less noisy

(Oberndorfer, 2009). Similar studies have also been based on futures (Oberndor-

fer, 2009; Veith et al., 2009).

The futures settlement prices were received by request from the European Energy

Exchange (EEX) that kindly provides its data for academic purposes. Although

there are multiple exchanges in which EUA futures contracts are traded, prices de-

velop identically across markets (Mansanet-Bataller et al., 2007), consistent with

the Law of One Price.

4.2.4 Market Returns

The Dow Jones STOXX Europe 600 covers large, mid and small capitalization

companies across 17 European countries: Austria, Belgium, Denmark, Finland,

France, Germany, Ireland, Italy, Luxembourg, the Netherlands, Norway, Poland,

45

CHAPTER 4. METHODOLOGY

Portugal, Spain, Sweden, Switzerland and the United Kingdom. It is weighted

based on free-float market capitalization, and its composition is reviewed on a

quarterly basis. The index represents a highly diversified portfolio and will be

used as a proxy for the overall market returns.

4.2.5 Control Variables: Oil and Natural Gas

In line with Arbitrage Pricing Theory and the idea of multifactor market models,

we add additional variables to the regression model that captures other potentially

influencing macroeconomic factors. We choose to follow Veith et al. (2009) and

Oberndorfer (2009) and include the price changes of oil and natural gas in our

regression equation. This will facilitate in comparing our results with their study.

Unlike Oberndorfer (2009), however, we choose not to include electricity prices,

which did not provide explanatory power in his study.

We use the price of one-month Brent crude oil contracts because it is extracted

from the North Sea and thus the primary source of oil in Europe. As for natural

gas prices, we use the one-month TTF Natural Gas contracts. The TTF Natural gas

is the largest market for natural gas in Europe. Both time series were retreived

from Bloomberg and Euro-denominated.

4.2.6 Transformation of Data and Frequency

Economic time series often exhibit growth that is approximately exponential, mean-

ing that in the long term the series grows by a certain rate per year on average.

This may have negative implications when performing linear regressions. To miti-

gate the risks associated with this, we calculate the natural logarithm of the time

series data to transform the series to exhibit linear growth (Stock & Watson, 2015).

46

CHAPTER 4. METHODOLOGY

This transformation also is often considered to stabilize the variance in the time

series data (Woolridge, 2013).

Using weekly data frequency, rather than daily, avoids issues with error-in-variables

problems with respect to irregularities (Scholes & Williams, 1977). Although

Oberndorfer (2009) used daily frequency, he argued that weekly observations are

preferable if the sample period is large enough because it reduces noise. We calcu-

late the weekly return using the closing price of the last trading day of the week.

Our sample period stretches from the first week of 2013 to the last week of 2020

with results in more than 360 observations for each series in the data set.

4.3 Econometric Theory

The following section provides an explanation of the econometric methods that

will be used to test the hypotheses presented in Section 3.2. First, the reader

is introduced to the Ordinary Least Squares (OLS) regression estimation. Next,

we discuss issues related to OLS estimation in terms of omitted variable bias and

present a Fixed Effects regression model to mitigate these issues. The inspiration

to this section is from Stock and Watson (2015), Woolridge (2013), and Enders

(2014).

4.3.1 OLS Estimation

Ordinary Least Squares (OLS) estimation a type of linear least squares method for

estimating the unknown parameters in a linear regression model. The multivariate

regression model can be expressed in matrix notation as follows, for consistency

47

CHAPTER 4. METHODOLOGY

vectors and matrices are denoted by bold type:

Y = Xβ + U (4.1)

Where:

• Y is the n× 1 dimensional matrix of n observations on the k + 1 regressors -

including the regressor for the intercept.

• X is the n×(k+1) dimensional matrix of n observations on the k+1 regressors

- including the regressor for the intercept.

• The k + 1 dimensional column vector Xi is the ith observation on the k + 1

regressors; that is, X′i = (1X1,i . . . Xk,i), where X′i denotes the transpose of

Xi.

• U is the n× 1 dimensional vector of the n error term.

• β is the (k + 1) × 1 dimensional vector of the k + 1 unknown regression

coefficients.

For the OLS estimation to provide the best linear unbiased estimators, the follow-

ing assumptions must hold.

1. E (ui|Xi) = 0, ui has conditional mean of zero.

2. (Xi, Yi) , i = 1, . . . , n, are independently and identically distributed (i.i.d)

draws from their joint distribution.

3. Large outliers are unlikely: Xi and ui have nonzero finite fourth moments.

4. X has full column rank i.e. there is no perfect multicollinearity.

48

CHAPTER 4. METHODOLOGY

The principle of OLS estimation is to minimize the sum of squared prediction

errors over all n observations. The sum of squared predicted errors can be written

as:n∑i=1

(Yi − b0 − b1X1,i − . . .− bkXk,i)2 (4.2)

Where Yi is the observed value, which the OLS estimation predicts, b0, b1, . . . , bk are

estimates of β0, β1, . . . , βk, which minimize the sum of squared prediction errors

and X1,i and Xk,i are the regressors included in the OLS estimation. The estimates

of the coefficients that minimize the sum of squared prediction errors are called

OLS estimators and are denoted as β in matrix notation. The difference between

Yi and the predicted Yi is the OLS residual and is denoted U in matrix notation.

The OLS estimators can be estimated by a closed form solution. These are ob-

tained by taking the derivative and setting the derivatives of the sum of squared