THE EMPLOYER’S ROLE IN MEDICARE Henry de Vos Lawrie, Jr. Kathryn J. Greenlief McGuire Woods Battle USAA & Boothe LLP

THE EMPLOYER’S ROLE IN MEDICARE Henry de Vos Lawrie, Jr.Kathryn J. Greenlief McGuire Woods BattleUSAA & Boothe LLP.

Dec 29, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

THE EMPLOYER’S ROLE IN MEDICARE

Henry de Vos Lawrie, Jr. Kathryn J. Greenlief McGuire Woods Battle USAA & Boothe LLP

2

TRADITIONAL MEDICARE

Defined Benefit Fee-For-Service Out-of-Pocket

– Part A (Hospital) $768 (1-60)

– Part B (Medical) $100 Deductible 20% Co-Pay

3

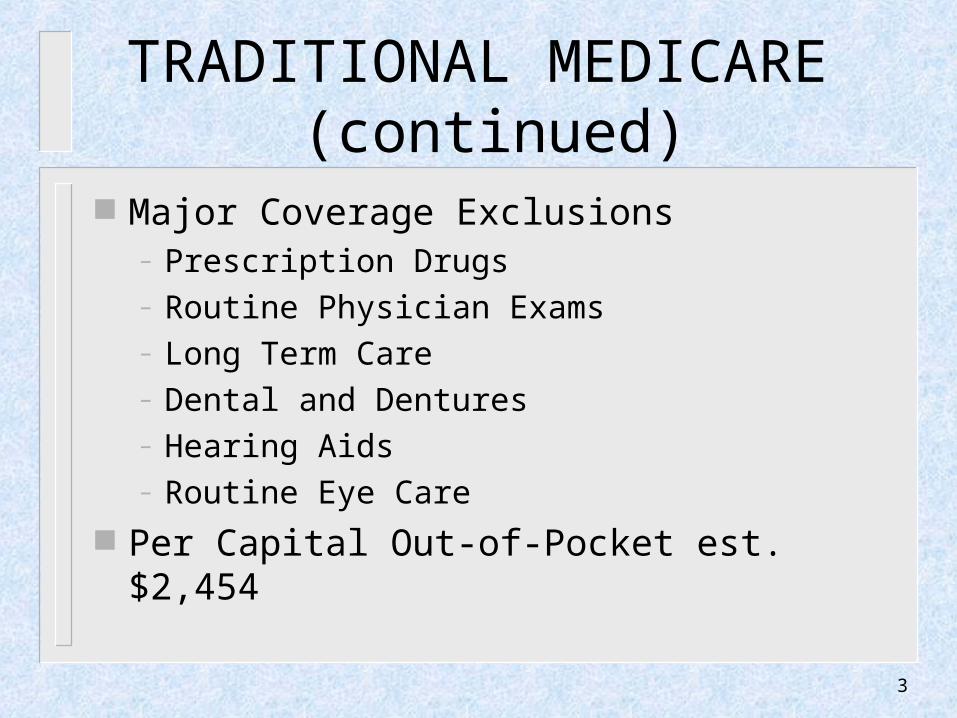

TRADITIONAL MEDICARE (continued)

Major Coverage Exclusions– Prescription Drugs– Routine Physician Exams– Long Term Care– Dental and Dentures– Hearing Aids– Routine Eye Care

Per Capital Out-of-Pocket est. $2,454

4

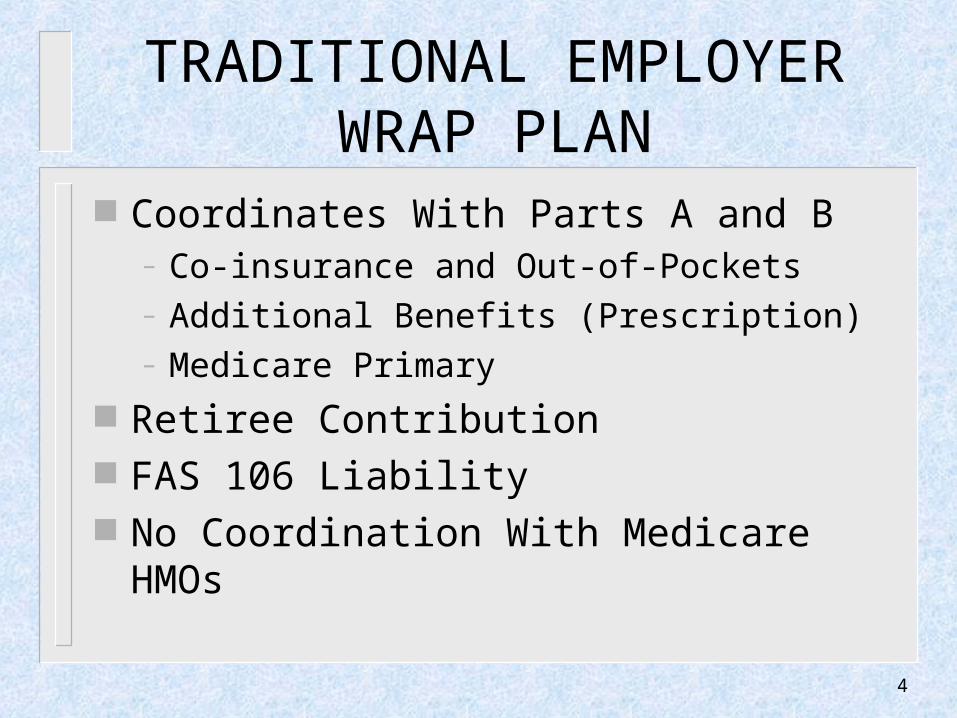

TRADITIONAL EMPLOYER WRAP PLAN

Coordinates With Parts A and B– Co-insurance and Out-of-Pockets– Additional Benefits (Prescription)– Medicare Primary

Retiree Contribution FAS 106 Liability No Coordination With Medicare HMOs

5

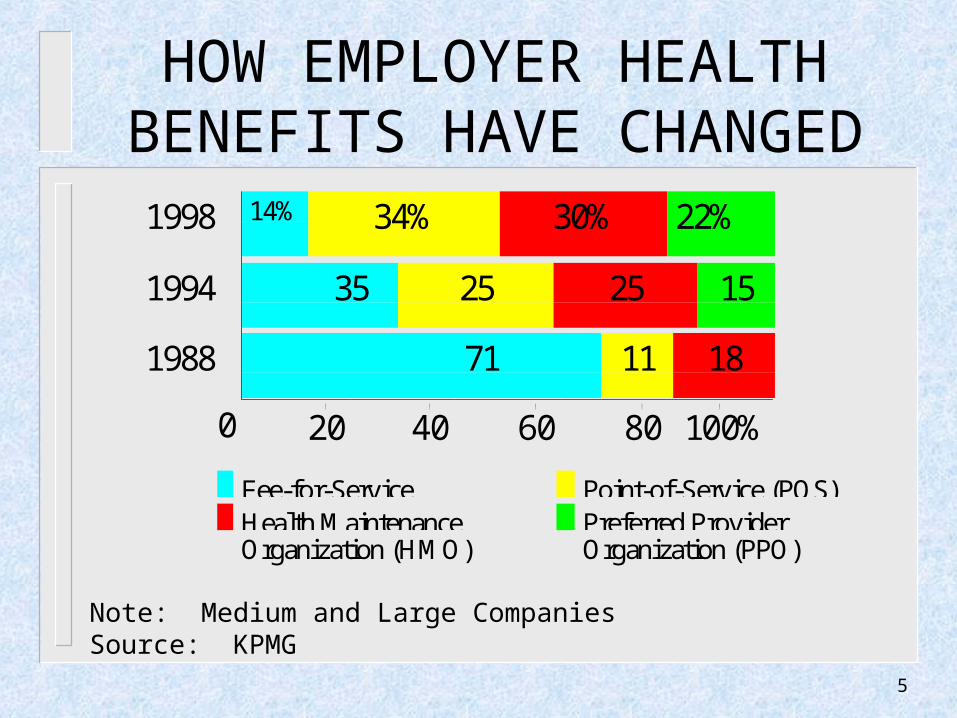

HOW EMPLOYER HEALTH BENEFITS HAVE CHANGED

1998 14% 34% 30% 22%

1994 35 25 25 15

1988 71 11 18

0 2'0 4'0 6'0 8'0 10'0%

Fee-for-Service Point-of-Service (POS)Health Maintenance Preferred ProviderOrganization (HMO) Organization (PPO)

Note: Medium and Large CompaniesSource: KPMG

6

BALANCED BUDGET ACT OF 1997

Fewer Dollars for Providers More Managed Care Effective 1999 Introduces Medicare Part C

7

MEDICARE + CHOICE(Part C of Medicare)

More Coordinated Care Plans (HMO, PPO, PSO or POS)

Private Fee-for-Service Plan MSA Plan Parts A & B Remain Alternatives

8

MEDICARE RISK HMOs

Introduced in 1985 Enrollment Quadrupled to 14% Since 12/93 Current Primary Vehicle Under Medicare +

Choice

9

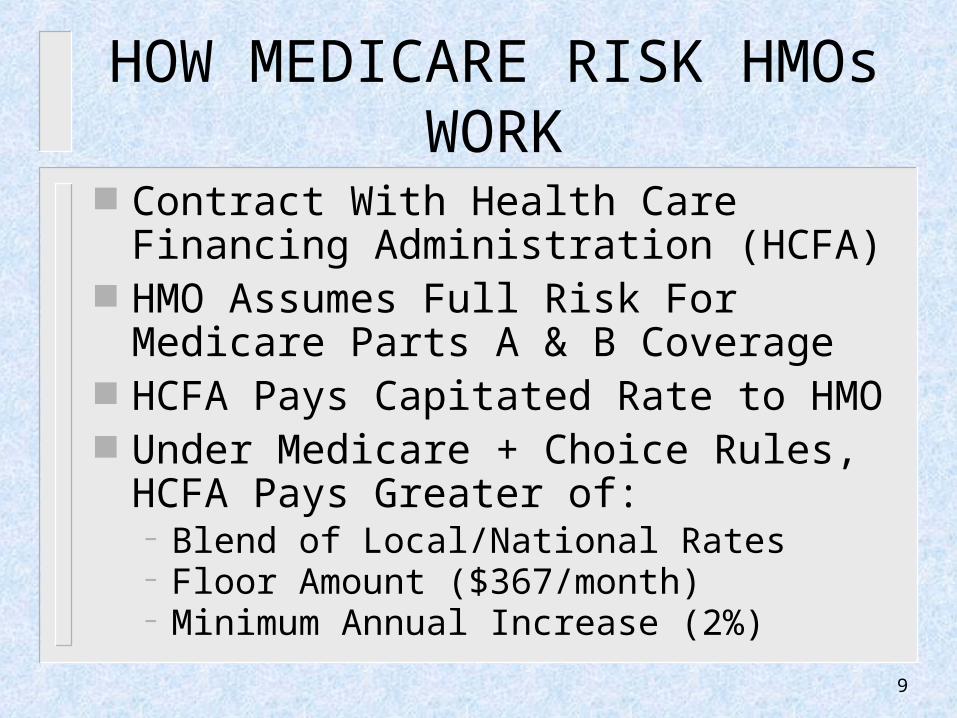

HOW MEDICARE RISK HMOs WORK

Contract With Health Care Financing Administration (HCFA)

HMO Assumes Full Risk For Medicare Parts A & B Coverage

HCFA Pays Capitated Rate to HMO Under Medicare + Choice Rules, HCFA

Pays Greater of:– Blend of Local/National Rates– Floor Amount ($367/month)– Minimum Annual Increase (2%)

10

HOW MEDICARE RISK HMOs WORK (continued)

Normal HMO Coordinated Care Features– Defined Geographic Area– Gatekeeper– Network Limitations– Possibly POS Option

11

ADVANTAGES OF MEDICARE RISK HMOs

Lower Cost or Higher Benefit Level at Same Cost

More Predictable, Budgetable Expense

12

THE CURRENT HMO MARKET

Reduced or No Out-of-Pockets Some Zero Premium Plans Offer Additional Benefits Pricing Too Good to Be True?

13

VARIATIONS IN SAVINGS

Vendor Network Effectiveness Plan Location Enrollment Employer/Employee Contributions for

Existing Medicare Coverage

14

FAS 106 RELIEF

Estimate of Total Liability Driven By Current and Anticipated Expense Impact of Migration to Medicare Managed

Care

15

CHOICES FOR THE EMPLOYER

Whether to Embrace or Merely Tolerate Medicare + Choice

Strategy for Encouraging Migration Extent of Plan Redesign

16

INITIAL EMPLOYER ISSUES

Coverage Availability in Employer’s Area Benefit and Price Differences Among

Available Options Quality of Service Due Diligence Determine Likelihood of Acceptability of

Managed Care to Current and Future Retiree Population

17

DESIGN ISSUES

Medicare + Choice as Alternative or Mandate

Single or Multiple Coordinated Care Options Supply Benefit Enhancement to Encourage

Migration to Managed Care Limitations on Transfers Among Alternative

Choices

18

DESIGN ISSUES(continued)

Define the Employer’s Subsidy Develop Communications and Enrollment

Strategies

19

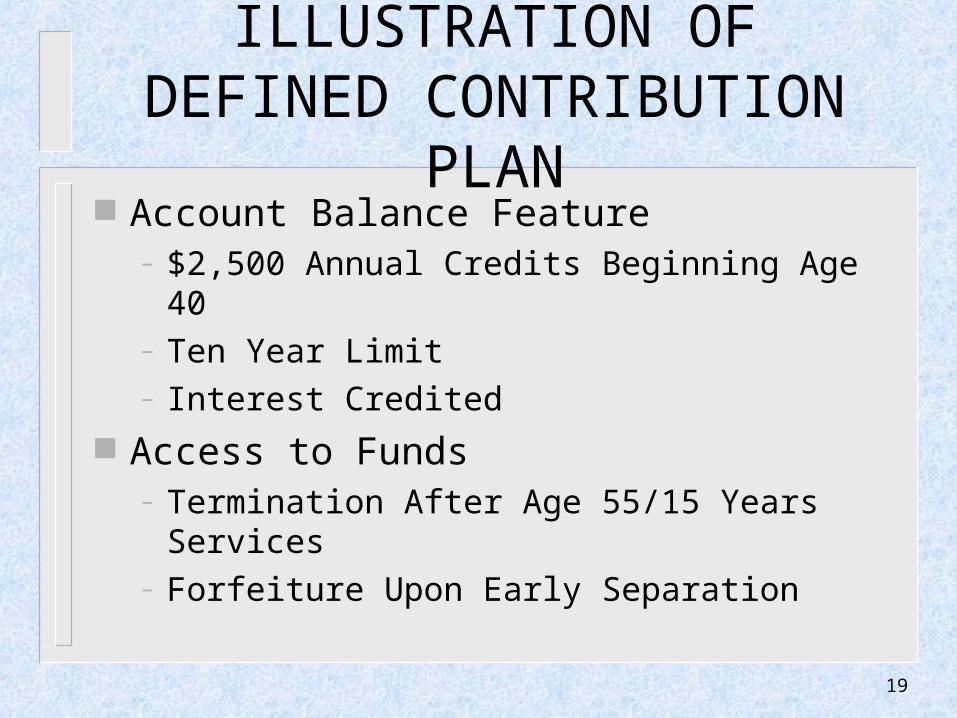

ILLUSTRATION OF DEFINED CONTRIBUTION PLAN

Account Balance Feature– $2,500 Annual Credits Beginning Age 40– Ten Year Limit– Interest Credited

Access to Funds– Termination After Age 55/15 Years Services– Forfeiture Upon Early Separation

20

ILLUSTRATION OF DEFINED CONTRIBUTION PLAN

(continued)

Use of Funds– Premiums For Range of Plans– Retiree Elects Annual Allocation Amount– Individual Contributions Permitted– Eligible Dependents– Premiums Only; No Cash

21

ILLUSTRATION OF DEFINED CONTRIBUTION PLAN

(continued) Advantages of Program

– Coordinates Well With Medicare + Choice– High Employee Visibility– Rewards for Service, Not Age– Employee Flexibility– FAS 106 Relief

Related Documents

![PARTIES: LAWRIE, Delia Phoebe LAWLER, John TITLE … · lawrie v lawler [2015] ntsc 19 . parties: lawrie, delia phoebe . v . lawler, john . title of court: supreme court of the northern](https://static.cupdf.com/doc/110x72/5ad464727f8b9a1a028bce85/parties-lawrie-delia-phoebe-lawler-john-title-v-lawler-2015-ntsc-19-parties.jpg)