A research work on the effects of the global financial crisis on the economies of developing countries in the world. A case study of the Nigerian economy. By Ojuola Tolulope Daniel. (B.sc/ed Econs) 1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

A research work on the effectsof the global financial crisis onthe economies of developingcountries in the world. A casestudy of the Nigerian economy.

By

Ojuola Tolulope Daniel.(B.sc/ed Econs)

1

2

CHAPTER ONE

1.1. INTRODUCTION

The world is facing the most severe financial crisis since thegreat depression of the last century. The current financial crisisis unprecedented in the history of the modern world and it is havinga catastrophic effect on the financial wellbeing of millions ofpeople around the world. The current crisis is rooted to themortgage loan crisis, which became heightened in the United Statesin the early 2004 until mid 2007 when it escalated. During early2004, the mortgage industry in the United States enjoyed anunprecedented boom whereby mortgage brokers enticed prospectivebuyers with inadequate income or poor credit history into takingmortgage loans with little or no down payment, Adamu. These subprimeloans were later repackage and resold to banks and other financialinstitutions which then created collaterised debt obligations (CDO)and sold these financial instruments to world wide investors whounsuspectingly relied on the strength of the sellers rather than therisk rating of the underlying financial instruments.

The crisis escalated in the mid 2007, when subprime mortgageborrowers `unable to service their loans which were then due forrefinancing began to default en-masse. The mass default triggeredthe beginning of the global credit crunch because investment bankswho sold the collaterised debt obligations could no longer servicethe huge debts packaged as purchase notes from commercial banks.

The global financial crisis began in the United States ofAmerica and the United Kingdom, where the global credit market cameto a standstill in July 2007, Avgouleas. The original root of the

3

financial crisis is the United States of America- the world’slargest military-industrial complex. No economy whether developed orunderdeveloped is so far insulated from the global credit turmoil.The crisis has already resulted into a recession in someindustrialised economies and is already having a huge impact onemerging or developing economies like Nigeria. The Monetary PolicyCommittee (2009) has observed that the Nigerian economy is beingimparted by exogenous factors. Such factors include the deepeningrecession of the industrialised economies. This is because therewould be low remittances from abroad, decline in foreign aids, lowforeign direct investment and portfolio investment.

The current crisis is affecting Africa in two ways and thesetwo ways are, firstly there could be financial contagion and spillover for stock markets. This is because stock markets in Africa havebeen showing volatility driven by a sell off by foreign investors.Secondly there is an indirect effect of volatile and fallingcommodity prices particularly oil, on export revenue and the inflowof the capital into the region.

The financial crisis is already in the Nigerian economy eventhough the financial authorities have chosen to believe that thecountry is insulated from its effects. The unabated crisis in thecapital market may likely escalate particularly the price slump inthe Nigerian Stock Exchange. The dearth of the liquidity and globalcredit squeeze is having its impact on the Nigerian Stock Exchange.The financial crisis has also affected the prices of the oil in theglobal market.

For instance, Nigeria exports 45 percent of its oil to theUnited States of America, therefore the crisis made America toreduce its demand for oil thereby causing a major price slump in theglobal market. Another indicator of the effects of the financialcrisis on Nigeria is the persistent decline in the value of thenational currency, the naira. The free fall of the naira at theForeign Exchange market climaxed with the naira being exchanged withthe dollar at =N=153.

For avoidance of doubt, the global financial crisis startedwith banks and mortgage lenders who could not follow the traditionalrule of lending. This scenario has caused bank collapse world wideand economic disaster in several countries. In Nigeria, the current

4

crisis in the capital market is traceable in parts to the aggressiveentering of banks to the financial markets. The bankingconsolidation of 2005 by the Central Banks of the Nigeria resultedin twenty one out of the twenty banks listing in e Nigerian StockExchange. The race for higher capitalisation led to several initialpublic offers which boosted the Nigerian Stock Exchange marketcapitalisation to an unprecedented level. Banks account for oversixty five percent market capitalisation at the stock exchange.Hence bank shares became actively traded and some banks inconnivance with some brokers engaged in shady practices. Theiractions coupled with the influx of foreign hedge funds lured byprospects of huge capital gains fuelled the markets and stock pricesshot up to levels unseen before. As soon as the Central Bank ofNigeria released a directive to harmonies bank year ends, the crisisescalated. Banks then went on an aggressive process of generatingliquidity to raise their balance sheet, interest rates shot upsporadically and broker’s credit lines dried up. Panic sets in andbrokers and some investors started dumping their shares to cut theirlosses thereby depressing the market.

The financial crisis is also affecting Foreign DirectInvestments and equity investments in Nigeria. While 2007 was arecord year for foreign Direct Investment, Nigeria’s equity financeis already weakening. The fall in inward investments will affectimportant sectors such as agriculture, infrastructure, development,health and education. While the effects could vary from country tocountry, but the impacts could include export revenues, furtherpressure on the current accounts, and Balance of Payment, lowerinvestments and growth rate.

1.2. BACKGROUND OF THE STUDY

The whole world is plunging into a deep recession. One nobel-laurete economist already posses the opinion that the recession isan awful beginning of second Great depression. This calls forimmediate mitigation strategy of quick recovery of the United Statesof America as well as the world economy. Unfortunately other thanthe bail out plans, there are no signs of long lasting solutionsfundamental in nature, visible enough to face the recurring businesscycle this time likely to manufacture another great depression.

5

Upheaval of the seeming second great depression raises doubtson the effectiveness of the Keynesian, post-Keynesian and monetaristprescriptions to counter the cyclical fluctuations. The reasons forthis are varied and complex, but can largely be attributed to anumber of factors in both the housing and credit market whichdeveloped over an extended period of time. Some of this include: theinability of home owners to make their mortgage payments, poorjudgment by borrowers and lenders, speculation and overbuildingduring the boom period, risky mortgage products, high personal andcorporate debt levels, financial innovations that distributed andconcealed default risks, central bank policies and regulation.

For the developing world, the rise in food prices as well asthe knock off effects from the financial instability and uncertaintyin industrialized nations is having a compounding effect. Commodity-dependent economies are exposed to considerable external shocksstemming from price booms and busts in international commoditysector have not resulted in greater stability of internationalcommodity prices. There is wide-spread dissatisfaction with theoutcomes fail to transmit reliable price signals for commodityproducers.

The crisis has gone deep in all the sectors of the Nigerianeconomy, the Nigerian external reserves for instance, was prettystrong before the time of the time of the crisis, it has nowcrumbled right before our very eyes within months. The exchange rateof the naira to all the other currencies in the world especially theUS dollar remains extremely volatile since the crisis erupted. Oilprices have gone down due to the reduced demand of oil commoditiesin the global market because consumer nations are trying to cut theconsumption of the commodities that engulfs virtually most of thespending due to the financial crisis.

The level of poverty before the crisis and now has tripled andthis is due to the fact that commodity prices are higher thanbefore, clearly showing that the rate of inflation is soaring andalso that the level of consumption of goods and services hasreduced, mostly due to the deficiency in demand, since people cannotafford this expensive commodities that would probably not be enoughfor them. Due to the reduced demand for oil in the global market,the level of revenue that was streaming in to the monoculture

6

economy of Nigeria started dwindling. And this fall was furtheraided by the level of crime and indiscriminate destruction of oilfacilities in the oil rich region of the Niger-Delta. This crisisdidn’t spare the Nigerian Stock exchange either as foreigninvestors, who realised the danger posed by the on-coming financialturmoil, withdrew their foreign hedge funds and took flight back totheir country depressing the stock market.

1.3. RESEARCH QUESTIONS.i. What are the major causes of the global financial crisis

and the Nigerian economic recession?ii. What are the strategies adopted by Nigerians to cope with

the economic meltdown?iii. What are the measures adopted by the government to reduce

or curb the effects of the global financial meltdown.

1.4. OBJECTIVES OF THE STUDY

The broad objective of this research is to analyse the effect of theglobal financial crisis on selected macroeconomic indicators onNigeria (inflation, aggregate savings, aggregate consumption,revenue).

The specific objectives are:

o To highlight the causes of the global and the Nigerianeconomic recession.

o To determine whether there is significant difference in theselected macroeconomic indicators before and during the globalfinancial crisis or not.

o To identify the different strategies being adopted byNigerians to cope with the economic meltdown.

To identify the various measures adopted by the Nigerian governmentin order to curb/reduce the effect of the financial crisis.

7

1.5. JUSTIFICATION OF THE STUDY,

This research is out to provide a detailed analysis of themajor effects of the global financial crisis in the economy ofNigeria. And as such a research of this nature could become a goodsource of raw materials for students, policy makers and economistswho may want to know the extent that the financial crisis affectedour economy in some years to come. The findings of the study isgoing to go beyond the hear say that global economic recessioncaused the present unimpressive performance of the Nigerian economy,the study intends to express quantitatively the extent that therecession has affected the various macroeconomic indicators.

1.6. RESEARCH METHODOLOGY

This section presents the model and the necessary methodologythat would be adopted for this empirical study, and such hascritically assessed the effects of the global financial crisis onthe economies of developing countries like Nigeria by usingDifference of means and multiple regression analysis. The economicmeltdown is not quantifiable and thus would be represented by thedummy variable.

1.6.1. SOURCES OF DATA

Secondary data would be obtained and as such data would besourced from the following institution, the Central Bank of Nigeriathrough the Statistical Bulletin where data showing the trend ofAggregate savings, aggregate consumption, aggregate revenue, Nigeriastock exchange transaction, Nigerian external reserves, Grossdomestic products from 1970-2007.

The National Bureau of Statistics for data showing the trendof the rate of inflation from 1970-2007. But for the purpose ofanalysis, data will be on quarterly basis, so as to capture theeffects (before and during the crisis) of the economic meltdown.

1.6.2. MODEL SPECIFICATION

AgCon=f (AgSav, AgRev, InfRa, SeT, NeR, ExNd, Gdp, Ecomel)........(1)

8

Where:

AgCon= Aggregate Consumption

AgSav= Aggregate Revenue

AgSav= Aggregate Savings

InfRa= Inflation Rate.

SeT= Stock Exchange Transaction

NeR= National External Reserves

ExNd= Exchange Rate of the naira to the dollar

Gdp= Gross Domestic Product.

Ecomel = Economic Meltdown

The functional expression of the above equation can still be putinto a more regressive form or econometric model using the ordinaryleast square method as shown below.

AgCon=0+1AgSav+2Rev+3InfRa+4SeT+5NeR+6ExNd+7Gdp+8Ecomel+U0…….(2)

Where:

0 = intercept or autonomous variable

1-8 = coefficients of the explanatory variables to beestimated.

* Other variables remain defined in equation one.

1.6.3. A’PRIORI EXPECTATION

This explains the theoretical expectation about therelationship between the included variables in the model. TheA’priori expectations are:

1 < 0 (coefficient of aggregate savings (=N=), is less than zero,this means that as aggregate savings increases, aggregateconsumption (=N=) decreases).

9

2 < 0 (coefficient of aggregate revenue (=N=), is less than zero,this means that as aggregate revenue increases, aggregateconsumption (=N=) decreases).

3 < 0 (coefficient of inflation rate (%), is less than zero, thismeans that as inflation rate increases, aggregate consumptiondecreases)

4 < 0 (coefficient of stock exchange transaction (=N=) is less thanzero, this means that as stock exchange transaction increases,aggregate consumption (=N=) decreases).

5> 0 (coefficient of national external reserves is greater thanzero, this means that as the national external reserves increases,aggregate consumption (=N=) also increases).

6 > 0 (coefficient of exchange rate of naira to the US dollar isgreater than zero, this means that as the exchange rate of nairato the US dollar increases, aggregate consumption (=N=) alsoincreases).

7 > 0 (coefficient of gross domestic product is greater than zero,this means that as the gross domestic product increases, aggregateconsumption (=N=) also increases).

1.6.4. RESEARCH HYPOTHESIS

i. H0: Economic meltdown does not influence aggregate consumptionexpenditure negatively.

H0: =0 (coefficient of aggregate consumption equal to zero)

H1: economic meltdown influences aggregate consumption expenditurenegatively.

H1: i<0 (coefficient of aggregate consumption less than zero)

ii. H0: Average exchange rate of naira is not significantly higherduring economic meltdown compared to the period before it.

H0: = (coefficient of exchange rate of naira to the USdollar during economic crisis is equal to the exchange rate ofthe naira to the US dollar before the economic crisis).

10

H1: Average exchange rate of naira is significantly higher duringeconomic meltdown compared to the period before it.

H1: > (coefficient of exchange rate of naira to the USdollar during economic crisis is greater than the exchangerate of the naira to the US dollar before the economiccrisis).

1.7. STATEMENT OF THE PROBLEM.

i. It is important to note that the global financial crisisconstitutes a huge problem to world economies and thus it is worthresearching. The global financial crisis has affected the financialsector of all major economies in the world; in fact most of theeconomies have had their financial sector totally crippled by thefinancial crisis. Most of the emerging economies, which had theirfinancial sectors closely interwoven into the financial sectors ofthe developed countries, have had their economies affected as muchas it had affected these developed countries.

ii. Another problem that is posed by the financial crisis is thepsychological effect of the crisis on the people of developingeconomies all over the world like Nigeria. Nobody is confident ofbanks or any financial institution any more. The recent crisis inthe capital market has not boosted their confidence at all, nobodywants to invest in stocks anymore.

iii. The government of different countries in the world haveresponded in different manners to the financial crisis, while someat first lived in denial of the effects of the financial crisis inthe country e.g. the United States and Nigeria, but since the thenthese countries have been able to bring in different packages tohelp curb the effects of the crisis in their economies.

1.8. SCOPE AND LIMITATIONS OF THE RESEARCH

This study essentially covers the effects (both positive andnegative) of the global financial crisis in Nigeria from when itstarted (July 2007) to its present stage, because nit is a currentphenomenon. However due to time constraints, the main limitations of

11

this study would be the gathering of data from all financialinstitutions within the limited time frame of the study. Thereforepublications of the National bureau of Statistics and the CentralBank of Nigeria would serve as major sources of data for this study.

1.9. RESEARCH OUTLINE

The study comprises of five chapters,

i. The first chapter introduces the research,ii. The second contains the review of related literature and

theoretical framework.iii. The third chapter is concerned with the research methodology

and method of data collection.iv. The fourth deals with the presentation analysis and

interpretation of collection data.v. The fifth contains the summary of findings, conclusions and

recommendations.

CHAPTER TWO

LITERATURE REVIEW AND THEORETICAL FRAMEWORK

2.0. INTRODUCTION

This research “the effect of the global financial crisis on

developing economies is handy for the review of authors in the sense

that it has the capacity to address the current issue affecting the

economic world global. Therefore the views of authors on the issue

for appraisal are varied and multi-dimensional. This is because the

financial meltdown affects countries differently and the views of

the individuals appraising the meltdown will be a function of where

they are, i.e. their country, exposure, profession and how they see

life generally in terms of finance.

Altman (1997) described the term financial crisis as the

simultaneous collapse of related financial institutions brought

about by the attempt of investors, speculators, lenders and

depositors to liquidate their assets. According to Adamu (2008), the

12

term financial crisis is broadly applied to a variety of situations

in which some financial institutions or assets suddenly loose a

large part of their value. In the 19th and 20th century, many

financial crises were associated with banking panics, and many

recessions coincide with these panics, Aliber (2005). Other

situations that are often referred to as the financial crisis

include stock market crashes and bursting of other financial

bubbles, currency crisis and sovereign defaults, Valencia (2008).

In the last few centuries there have been cases of financial

crisis that has left nations and countries despondent and in search

of solutions to prevent its reoccurrence. According to Bernstein

(1998), the first on record is the great depression which occurred

between 1873 and 1876 in the English economy when agriculture was

especially depressed resulting in the non-availability of food,

threatening the survival of people in that part of the world. The

second on record was when the world broke partly through protection

and cautious fiscal policies of national economies suppressed the

level of economic activities, Kindleberger (1986).

In addition, recent researchers have shown that the global

meltdown is an occurrence that occurs at least once in a century,

but looking at it from that perspective is to be extremely

superstitious. The last time this global phenomenon occurred, was in

the 1920s and its major cause was due to the fact that most of the

capitalist economies were laissez-faire. According to Viner (1960),

natural course, being subjected to few, if any governmental

regulations in order to give consumers complete freedom. These

assumptions according to Keynes (1926) were a set of unrealistic and

inapplicable set of theories. Keynes (1926) in his book ‘the General

theory’ that was published in the wake of the great depression

13

highlighted the solutions to which Hansen (1959) believed, saved the

post depression economies before the start of the Second World War.

The current global recession is having a catastrophic effect

on the financial well being of millions of people around the world

with the stock market collapsing where billions of shareholders and

investors funds were lost. Kaufman (2008) opined that the financial

crisis happened by the violation of two basics, the first being the

fact that self interest cannot evolve into greed to the degree that

personal material lost is sated without regard for human condition

of the neighbour and the second being the fact the production and

consumption may not persist in a manner and degree that outstrips

nature capacity to rejuvenate herself.

Adamu (2008) believes that some economic theories that

explained the causes of the financial crisis includes the world

system theory which explained the dangers and perils which

industrial nations are now facing at the end of the long economic

cycle which began after the oil crisis of 1973. Stiglitz (2008)

opined that the reasons for the crisis are varied and complex but

largely can be attributed to a number of factors in both the housing

and credit markets, which developed over an extended period of time.

Some of these includes: The inability of home owners to make

mortgage payments, poor judgment by borrowers, speculation and over

building during the boom period, risky mortgage products, high

personal and corporate debt levels, financial innovation that

distributed and concealed risks.

Avgouleas (2008) enumerated the causes of the crisis as:

breakdown in underwriting standards for sub prime mortgage flaws in

credit rating agencies, assessments of Subprime Residential mortgage

Backed Securities (RMBs) and other complex structured credit

products especially collaterised debt obligation (CDOs) and other

14

Asset-Backed Securities (ABS), risk management weakness at some

large United States and European Financial institutions and

regulatory policies including capital disclosure requirements that

failed to mitigate risk management weakness.

Answers.com (2009) attributed the cause of the financial

crisis to subprime lending claiming that the bank in use were

lending to people who cannot afford to payback their mortgages and

loans, when the housing bubble collapsed many people defaulted on

their debt and the banks failed or closed down. Pedro (2009) also

attributed the major cause of the financial crisis to subprime

lending, claiming that mortgage brokers enticed prospective buyers

with inadequate income or poor credit history into taking mortgage

loans, with no down payments, this loans were later repackaged and

sold to banks and other financial instrument to world wide investors

who unsuspectingly relied on the risk rating of the financial

instruments. The inability of the subprime mortgage borrowers to

service their loans was what triggered the global economic crisis.

The financial crisis has not left any economy unspared, more

importantly developing economies like Nigeria. According to the

monetary policy committee (2009), it has been observe that the

Nigerian economy was been impacted by external factors such as the

deepening recession of industrialized economies and the fall of

capital inflow into Nigeria through remittances and foreign

investments and the drying up of the credit lines for banks. Pedro

(2008) observed that the dearth of liquidity in the Nigerian Stock

Exchange due to the price slump which was what caused the crisis in

Nigeria.

According to Pedro (2008), the issues that metamorphosed into

the financial crisis were not unconnected to the financial errors

that were committed in the United States of America. Akyliz (2008)

15

opined that world economic growth in the next few years will depend

crucially on the impact of the crisis on the United State economy

and its global spillages. Pedro (2008) also opined that it is rather

ironic that the model capitalist economies who pride themselves as

the epitome of market discipline are the very ones plunging the

global economy into crisis through mismanagement. Iliyasu (2008)

believes that the economic crisis has its origins on the emphasis by

these countries, particularly the United States of America in

building and maintaining large but complex economically unproductive

and profitability expensive military industrial complexes with which

they have waged needless and unjustified wars around the world, in

pursuit of these, they have had to sacrifice the productive and

competitive sectors of their economies.

In view of the above, the idea of the political economy of the

United States backed up by her ideology and democratic norms could

be seen as the bane of the effects of the financial crisis on the

developing world like Nigeria. This makes it possible to justify an

assertion made, that western type of ideology on development could

be destructive to developing economies. In Schumpeter (1949)’s

views, if capitalism as a form of ideology for development is

brought to developing economies, it will first become poisonous

before it destroys what may have been on ground before its arrival.

It cannot be far from the truth to say that Schumpeter is a soothe

sayer whose ability to see the future in terms of ideology and

development is highly imaginative.

But the need to study past (history) in order to understand

the future has led Rewane (2009) to disagree with Schumpeter’s

assertion. Rewane (2009) believes that history has provided us many

examples of where the economic failure has led especially to new

policy understandings and a stronger long term recovery. He believes

16

that the only way to recover is to use the Keynesian model; that is,

to borrow to recover. Nwangwugwu (2009), also agreed with Rewane’s

assertion of borrowing, as required by the Keynesian model to

recover, he opined that the government should diversify the economy

and embrace fiscal responsibility to stem down the effects of the

global financial crisis. Egya (2009) opined the Nigerian government,

in their attempt to cushion the effect of the global financial

crisis has neglected the Nigerian factors and should not embrace

fiscal spending to try cushioning the effects of the crisis. What

this assertion means is that the earlier view may be invalid,

because most of the bail out packages the ripples created by the

crisis. It also confirms Schumpeter (1949) assertion soil dies and

becomes poisonous before it eventually dies there.

Pedro (2008) believes that the Nigerian economy would be

affected in overall ways and he predicted that the banking industry

would be directly affected. This is because Nigerian banks with

offshore credit lines may start experiencing reduction in their

lines or outright cancellation because many of their foreign

counterparts are enmeshed in the crisis. Soludo (2008) disagreed

with this assertion; he opined that the Nigerian economy and indeed

the banking sector might be immune to the global credit squeeze.

According to Soludo (2008), the bank recapitalization has

repositioned Nigerian banks and strengthened them to weather

whatever storm might rage in the financial system, such as the one

the world is currently witnessing. But as it turned out, Nigeria was

not immune to the financial crisis especially considering the loss

of substantial revenue arising from the fall in the prices of oil,

Iweala (2009). The prices of oil was at an all time peak of

145dollars per barrel and it dropped to 40 dollars per barrel in the

international market due to the fact that consumer nations of

17

petroleum products started reducing their energy requirements sue to

the expenses that were involved in the importation of oil products,

this nations are cutting their expenses, so that they would be less

vulnerable to the financial crisis, Nwokeoma (2009).

EMPERICAL REVIEW

2.1 THE FINANCIAL CRISIS AND THE UNITED STATES ECONOMY

The financial crisis of 2007-2009 has been called the worst

financial crisis since the one related to the Great Depression,

Wikipedia (2008). And it has contributed to the failure of key

businesses, decline in consumer wealth estimated in the trillions of

U.S. Dollars, substantial financial commitments incurred by

government, and a significant decline in economic activity, Akkas

(2008). Both market-based and regulatory solutions have been

implemented or are under consideration, while significant risks

remain, for the world economy.

The immediate cause of the crisis was the bursting of the

United States housing bubble which peaked in approximately 2005-

2006. According to Pedro (2008), high default rates on subprime and

adjustable rate mortgages (ARM), began to increase quickly

thereafter. An increase in loan incentives such as easy initial

terms and a long term trend of rising housing prices had encouraged

borrowers to assume difficult mortgages in the belief they would be

able to quickly refinance at more favourable terms. However, once

interest rates began to rise and housing prices started to drop

moderately in 2006-2007 in many parts of the United States of

America, refinancing became more difficult. Baker opined that

Defaults and foreclosure activity increased dramatically as easy

18

initial terms expired, home prices failed to go up as anticipated,

and adjustable rate mortgage interest rates reset higher.

According to Wikipedia (2008), in the years leading up to the

start of the crisis in 2007, significant amounts of foreign money

flowed into United States of America from fast growing economies in

Asia and oil producing economies. This inflow made it easier for the

Federal reserve to keep interest rate in the United States of

America too low from 2002-2006 which contributed to easy credit

conditions leading to the United States housing bubble, Taylor

(2008). Loans of various types (e.g. mortgage, credit card and auto)

were easy to obtain and consumers assumed an unprecedented debt

load. As part of the housing and credit booms, the amount of

financial agreements called mortgage-backed Securities (MBS), which

derive their value from mortgage payments and housing prices greatly

increased, answers.com (2009). Such financial innovation enabled

institutions and investors around the world to invest in the United

States housing market. As the housing prices declined, Avgouleas

(2008) believed that the major global financial institutions that

had borrowed and invested heavily in subprime MBS reported

significant losses. Falling prices also resulted in homes worth less

that the mortgage loan, providing a financial incentive to enter

foreclosure. The ongoing foreclosure epidemic that began in late

2006 in the United States continues to drain wealth from consumers

and erodes the financial strength of banking institutions.

Defaults and losses on other loan types also increased

significantly as the crisis expanded from the housing market to

other parts of the economy. According to Baker (2008), total losses

are estimated in the trillions of United States dollars globally.

While the housing and credit bubbles built, a series of factors

caused the financial system to both expand and become increasingly

19

fragile, Krugman (2008). Krugman (2008) opined that Policymakers did

not recognize the increasingly important role laid by financial

institutions such as investment banks and hedge funds, also known as

the shadow banking system. Foster (2009), believes these

institutions had become as important as commercial (depository)

banks in providing credit to the United State Economy, but they were

not subject to the same regulations. These institutions as well as

certain regulated banks had also assumed significant debt burdens

while providing the loans described above and did not have a

financial cushion sufficient to absorb the large loan defaults.

Krugman (2008) opined theta these losses impacted the ability of

financial institutions to lend, slowing economic activity. Concern

regarding the stability of key financial insinuations drove central

banks to provide funds to encourage lending and restore faith in the

commercial paper, markets, which are integral to funding business

operations, Foster (2009).

Governments also bailed out key financial institutions and

implemented economic stimulus programs, assuming significant

additional financial commitments.

2.2 THE FINANCIAL CRISIS AND EUROPE

The United States subprime mortgage mess impacted Europe

almost immediately after it erupted in August 2007, causing write-

down and credit losses among some of the largest European banks,

Friedman (2008). The Europe-wide cost of the subprime to date has

been $323.3 billion in asset write-down. Europe can only wish the

United States subprime crisis were the extent of its problems, the

underlying reason for Europe’s vulnerability is rooted not in the

United States subprime (that is only the proximate trigger) but

20

instead in the importance of banks to the entire European economy,

Wikipedia (2008). In the United States, the crisis might be

contained within the financial and housing sectors alone, but in

Europe, the close connections between banks and industry almost

assure a broad and deep spread of the contagion.

Unlike the United States, where the government has spent more

than a century battling to break the links among government,

industry and banks, this battle is only rarely joined in Europe,

Akkas (2208). If anything, such links (one could even say collusion)

between banks and businesses were encouraged from the very beginning

of modern European Capitalism. This allowed long-term investment

into capital-intense industries (such as automobiles and industrial

machinery) without the fear of quick investor flight should a single

quarterly report come back negative. The most famous example of this

type of cosy link are the ties between Siemens AG and Deut she Bank,

a relationship which has existed for more than 100 years, Amin

(2008). An over looping and intermingling of interests results from

this type of arrangement, insulating the system from many minor

shocks like strikes or changes in government, but making the system

less flexible in the face of major shocks like serious recessions or

credit crises. Therefore in times of global shortage of capital,

European corporations are left with few financing alternatives they

are comfortable with. In contrast, stockanalysts.com (2008), while

banks are an important source of financing in the United States,

Corporations there depend much more on the stock market for

investment. This forces American firms to compete ruthlessly for

capital and constantly seek greater and greater efficiencies.

The first issue, the global credit crunch, exacerbates all

efficiencies and underlying economic deficiencies that in capital-

rich situations would either be smoothed over a brought to a much

21

softer landing. Various European countries had such inefficiencies

long before the U.S subprime problem initiated the global credit

crunch, Friedman (2008). Many of these were caused by the post

September 11, 2009. Global credit expansion in combination with the

adoption of the euro. After the September 11 attacks, many feared

the end was nigh. To tackle these sentiments, all monetary

authorities (European Central bank included) flooded money into the

system dropped interest rates to 1 percent, and the ECB dropped them

to 2 percent, stock analyst.com (2008).

The euro’s adoption granted this low interest arte

environment, which normally only a state of Germany’s strength and

heft could sustain, to the entire euro zone. This easy credit

environment echoed by affiliation to most of the smaller and poorer

9and newer) European Union members as well. Cheap credit led to

consumer spending boom, which was stronger in the traditionally

credit-poor smaller, poorer, newer economies leading not only to an

overall economic boom that even without the subprime issue and the

global credit crunch, was going to burst, Foster (2009). Underneath

the global credit crunch looms the second problem: the European

subprime crisis. The issue is particularly acute in places like

Spain and Ireland that have recently experienced a lending boom

propped up by Euro’s law interest rates. The adoption of the euro in

Spain, Portugal, Italy and Ireland spread low interest rates

normally reserved for the highly developed, low inflation economy of

Germany to typically credit starved countries like Spain and

Ireland, granting consumers there cheap credit for the first time,

Avgouleas (2008).

The subsequent real estate boom, Spain built more homes in

2006 than Germany, France and the United Kingdom combined, led to

the growth of banking and construction industry. Banks pushed for

22

more lending by giving out liberal mortgage terms, in Ireland the

no-down payment 110percent mortgage was a popular product and in

Spain credit cheques were often waived creating a pool of mortgages

that might soon become as unstable as the U.S. Subprime pool.

The poorer, smaller and newer European countries gorged more

deeply than the Baltic and Balkan countries, leading to the third

problem: Baltic and Balkan over exposure. Growth rates approached 15

percent in the Baltic’s, surpassing even East Asian possibilities,

bbc.co.uk (2008). This scorching growth caused double-digit

inflation, which will now make it more difficult for the Baltic

States to take warnings to services their enormous trade imbalances.

The only reason that growth rates were less impressive in the

Balkans is because these countries either came later to EU

membership as with Bulgaria and Romania, or have not yet joined at

all. In the case of Croatia and Serbia, so they did not experience

the full credit-expanding effect of being associated with the

European Union.

Fuelling the surges were Italian, French, Austrian, Greek and

Scandinavian banks. Limited as they were by their local domestic

markets, they pushed aggressively into their Eastern neighbours,

stockanalyst.com (2008), the Scandinavians banks rushed into the

Baltic countries and the Greek and Austrian banks focused on the

Balkans, while the Italians and French also went to Russia. Europe’s

inability to address. The challenge goes well beyond the issue that

different portions of European capitals to deal with the crisis

varies greatly, but the core concern lies in the fact that, it is

the capitals, not Brussels, that must do dealing, Geithner (2008).

When the Maastricht Treaty was signed in 1992, EU member state

agreed to form a common currency, but they refused to surrender

control over their individual financial and banking sectors.

23

European banks therefore are not regulated at the continental level,

hugely limiting the possibilities of any soot of coordinated action

like the US$ 700 billion till bail out plan.

As the crisis unfolded disagreements on the member state level

were immediately evident, with France and Italy both saddled with

large and growing budget deficits and national debts, are the two

major states most in need of such a bail our. But Germany and the

United Kingdom, the more fiscally healthy states that would have

been expected to pay for the bulk of plan, quickly voted to end the

idea. The Europeans then decided to go with an EU-wide set of

measures that the individual member states liquidity injection

packages. At the EU level, the only actual proposal have been two

steps: a broad reduction in interest rates and an increase in the

minimum government guaranteed bank deposit form 20, 000 euros ($27,

000) to 50, 000 euros ($68, 300), stockanalyst.com(208). It is

worth nothing that many individual European countries are now

guaranteeing all personal deposits to share up depositor confidence.

2.3 THE FINANCIAL CRISIS AND DEVELOPING COUNTRIES.

The global financial crisis that emerged in the financial

sector in developed countries has spread to the real sector in both

developed and developing countries. The global economy is showing

signs of recovery, but poor countries are still suffering the

consequences of the financial crisis and global recession. The

poorest countries according to overseas development institutes,

(2008) need additional help to move beyond the global recession.

These countries can play a key role in helping to boost global

demand, but they will need access to financing for years to come.

24

Export market demand in the poorest countries has dropped

between 5 – 10% in 2009, due to a downturn in trade, Adamu (2008).

Private capital flows to the poorest countries are projected to drop

to $13 billion in 2009, declining form $21 billion in 2008 and $30

billion in 2007, ODI (2008). Remittances to the poorest countries

are anticipated to fall between 5 and 7% in 2009, recovering only

modestly in 2010, stratchan.com (2009). A global crisis needs a

global response, while the global economy is showing tentative signs

of recovery poor countries are still suffering the consequences of

the global recession.

The global financial crisis is already causing a considerable

slowdown in most developed countries. Governments around the world

are trying to contain the crisis, but many suggest that the worst is

not yet over. Stock markets are down than 40% from their recent

highs, stockanalyst.com (2008). Investment banks have collapsed,

rescue packages are drawn up involving more than a trillion US

dollars, and interest rates have been cut around the world in what

looks like a coordinated response.

Leading indicators of global economic activity, such as

shipping rates, are declining at alarming rates. What does the

turmoil mean for developing countries?

Many developing country economies are still growing strongly,

but forecast have been down graded substantially in the space of a

few months, statfor.com (2008). With a recession already underway in

the UK, Germany, and France: the USA and other developed countries,

it is quite startling to hear countries like Malawi and Nigeria

believe that they are insulated form the crisis, Nwokeoma(2008).

The U.S.A is going through the greatest financial crisis since

the 1930s, but as financial times (2008) opined, Lagos is not

25

Lehman. Nigeria, held back by decades of economic mismanagement, is

growing at nearly 9%. Leaders in China suggest that they can help

the world by offering growth rates of up to 10% and many African

countries still gain significantly form this (they are growing at 6-

7%), Velde (2008) believed that growth performances vary

substantially among developed and developing countries. African

growth is diverging as much as it did during the last significant

global economic downturn in the early 1990s, OECD (2009). The

relationship between OECD GDP and Africa’s GDP has weakened as a

result of the emergence of countries such as China as well as

structural changes in African economies.

According to the IMF, world Economic outlook report in April

2008, a decline in world growth of one percentage point would lead

to a 0.5 percentage point in Africa’s GDP, so the effects of the

global terminal in Africa (via trade, FDI, aid) would be quite high.

The correlation between African GDP and world GDP since 1980 is 0.5,

but between 2000 and 2007, it was only 0.2, ODI (2008). As there

have been significant structural changes (and a move into services

that were able to withstand competition much better) as well as the

rise of China, African growth has temporarily decoupled form OECD’s

GDP, Velde (2008).

Several Asian countries have built up healthy government

reserves, and a solid export performance has helped their strong

current account position. Latin American countries are currently in

much better fiscal and external position compared to the 1990s, the

decade in which several financial crises struck. However, there are

several wearying signs. The combination of high food prices and high

oil prices has meant that while the current account of oil and food

importers was in balance by 2003, it was in deficit by 4% in 2007,

inflationdata.com (2009).

26

Inflation has doubted, therefore many developing countries are

in bad position to face another crisis, Friedman (2008). The terms

of trade shock tend to be the highest in small importing countries

such as Fiji, Dominica, and Swaziland. However African countries

such as Kenya, Malawi, Tanzania are projected to have faced terms of

trade shocks of greater than 5% of GDP, World Bank paper, 2008).

2.4 THE FINANCIAL CRISIS AND AFRICA

The impact of the global financial crisis on Africa’s economy

is still evolving. However, early assessments indicate that the

crisis could undermine decades of economic of progress marked by

economic growth and investment, worldbankgroup (2008). Stanley

Devarajan (2009) opines that Africa’s banking system is not

threatened by the current global financial crisis, but the region

could see a decrease in private investment flows. Such a decrease

would compromise the financing of many infrastructure projects on

the continent. Devarajan (2009) proposes however that sovereign

wealth funds may now turn to Africa as an attractive place to

invest, given the United States and European markets.

Recent trends in global financial markets, in particular the rapidly

diminishing availability of capital experience worldwide; are having

an increasingly adverse impact on African countries and on the

Bank’s clients, Friedman (2008). The African Development Bank (ADB)

Group has been at the forefront of efforts at analyzing the crisis’

impact an Africa. The developed economies can help African exports.

Indeed, recovery in the developed and emerging markets will help

Africa out of the crisis by increasing African exports and capital

inflows, Stanley (2008). Discouraging protectionist practices in

trade and capital flows. Supporting increased provision of

27

confessionals financing and grants to African countries through

Bilateral and Multilateral mechanisms. Providing adequate funding

for African low income countries as well as supporting funding for

programs aimed at enhancing response to vulnerability, Iweala (2009)

considering the severity of the crisis and the Bank’s capacity as

the continent’s premier development finance institution, the ADB is

also providing support to institutions.

2.5 THE CAUSES OF THE GLOBAL FINANCIAL CRISIS IN NIGERIA

According to answers.com (2009), the causes of the Crisis in

Nigeria are numerous and they are listed below.

i. Overdependence of the nation on petroleum as source of income,

according to Sanusi (2009), Nigeria gets over 95% of her

revenue form oil.

ii. Resource Mismanagement (not just Petroleum, but natural gas as

well), countries like Malaysia and Singapore in the 1970s had

the same revenue with Nigeria but it is not so today, Babajide

(2008)

iii. Niger-Delta militant activities, this factors has worsened

the situation, as barrels of crude-oil produced per day, has

dropped due to militant activities in kidnapping, stopping

operations and damage to oil wells.

iv. High rate of importation: this has always been a great menace

to the Nigeria economy as many commodities are imported and on

the Longman, other economies benefit from Nigeria.

28

v. The debt game (at all levels): Nigeria as a country is still

heavily indebted to the World Bank and international monetary

fund (IMF).

vi. The changing dynamics of over-population has also affected the

Nigerian economy because adequate plan have not been put in

place for the nations’ increasing population.

vii. Outright corporate greed exhibited by various companies and

services provides also have a major contribution to the

economic situation in the country.

viii. The national relocation of employment and changing means of

labour also have a part, many people are migrating to major

cities like Lagos, Abuja, Port-Harcourt causing these cities

to be over populated and few people are left to form other

states.

ix. Growing gap between the elite and the impoverished also has

its fair share on the nation’s economic meltdown. Other

factors are erosion of human dignity, the erosion of dignity

of life.

2.6 EFFECTS OF THE FINANCIAL CRISIS IN NIGERIA

The effects of the financial crisis on the Nigerian economy

according to Adamu (2008) are as follows

i. Foreign direct investment and equity investments: these will

come under intense pressure while 2007 was record year for

foreign investment to Nigeria and other developing countries,

equity finance is under pressure, corporate and project

finance is weak, Mtango, (2008).

29

ii. Downward trend in oil price: the deteriorating global economic

outlook is likely to put further downward pressure on crude

oil prices, which are expected to remain high volatile. The

indirect affect of volatile and falling commodity prices,

cannot be over emphasized. This is because Nigeria depends on

revenue form oil to finance its budget and the countries that

were mostly affected by the crisis are primarily market for

oil. In a precautionary move, the Nigerian government reduced

the 2009 benchmark or revenue estimate to $45 per barrel form

over $ 60 per barrel, Nwokeoma, (2008).

iii. Remittances to Nigeria will be decline; there will be fewer

migrants coming to the developed countries during the

recession, so few remittance and also probably lower volumes

of remittances per-migrant. This will affect calls by

government on Nigerians in Diaspora to come and invest in the

economy, Pedro (2008).

iv. Aid: aid budgets are under pressure because of debt problems

and weak fiscal positions e.g. in the United Kingdom and other

European countries and also the United States of America.

v. Commercial lending: Banks under pressure in developing

countries may not be able to lend as much as they have done in

the past. This would unit investment in the country as

investors will find it difficult to borrow from banks.

vi. Slowdown of economic growth.

vii. Foreign currency income slump, Unemployment increase, reduced

overseas development aid, depreciation of local currency etc

will result in a set back in achieving the millennium

development goals.

30

The Nigerian government have adopted several strategies

to cope with the menace of the global economic has adopted to

curb the global affects of the global financial crisis on the

Nigerian economy. Nduwugwe (2009) note that political office

holders have had to accept huge payouts to help stem down the

huge spending of the government and the financial regulators

have earmarked for the financial crisis. Babajide (2009)

opines that the government can overcome the challenges posed

by this crisis through prudent policies; he also said that the

government must rely on the bench mark of oil fix its budgets.

The Central Bank of Nigeria (2009) expanded its discount

windows to increase lending also reduce the cash reserve ratio

from 40 to 30 percent to ensure liquidity. This measure would

help private sector initiatives if they are sustained. The

international monetary fund (2008) enumerated some economic

recipes that must be implemented to be literate the world form

the devastating effect of the global financial crisis

including that the regulatory perimeter, or scope regulation

needs to be strengthened; procyclicality in regulation and

accounting should be minimized; information gaps should be

filled and central Banks should be filled and Central Banks

should strengthen their frameworks for systemic liquidity.

2.6 APPRAISAL REVIEW

According to the pacific Westmontgate.blogspot.com (2009), the

world economy will continue to experience economic imbalances as a

result of confluence of factors at one point or the other, and at

the same time corrects itself or needs intervention or both to

obtain equilibrium. The negative impact of the financial crisis is

31

forcing many developing countries to choose between spending money

on social programmes or on debt payments and many of them are

already at risk of experiencing another debt crisis, Pedro (2009).

This supports Kimun (2009)’s argument that a debt moratorium would

liberate resources and provide counties the fiscal space to respond

to the effects of the crisis. The crisis had also highlighted the

need for state to play a larges role in the economy and in

articulating and implementing social policies.

Following the financial crisis that broke in the United States

and Western economies in late 2008, there is now serious concern

about its impact o n the developing countries, United nations

(2009).The media almost daily reports scenarios of gloom and doom,

with many predicting a deep global recession. Without much

resilience from the developing world, prospects for the world’s

richer countries would be much bloodier, Heyd (2009). The crisis

accentuates the urgent need for accelerating financial development

in developing countries, domestic financial deepening, domestic

resource mobilization, and reform of the international financial

system Naude (2009).

According to articlebase.com (2009), the United States of

America caused the crisis, by spending more than they save, their

government spending more than they made, American financial

institutions giving house loan to people who had a very weak

capacity to pay and reselling the loans to naïve and sometimes

greedy global investors while the word’s financial regulations

blindly watched. As at the close of October 2008, estimated money

lost in the current world financial turmoil is placed at US&2.8

trillion, Baker (2008). This is equivalent to N322 trillion which is

about 14, 000 years of Nigeria’s economic output, articlebase.com

(2009). Easy credit from financial institution has dried up for

32

Nigerian banks; Pedro (2008).this has raised the cost of funds

indirectly locally. Also the crisis of confidence that has plagued

the international inter bank market has impacted negatively on the

international finance operations of Nigerian banks.

The downturn in the Nigerian capital market is speculated to

have been sparked off when hedge funds withdrew about N1.5 trillion

from the market, Pedro (2008). With the current global downturn,

this capital may not return soon, meaning the market may never

regain the momentum that saw it rise to new heights. Nigeria’s

capital market is currently rated as one of the worst performing in

the world. Oil prices currently hover at a low of $43-$53, about one

third of its $150 high price in July 2008. This has had a crunching

impact on Nigeria which earns about 90 percent of its income form

sales of crude oil, Nwokeoma (2009). Drop in oil revenues means less

revenue for the government. That means less money infrastructure,

invest in new oil production and raise the foreign our reserves and

fall in the external reserves which Nigeria has consistently built

up in the last eight years. Utomi (2009). The immediate impact has

been in the steep fall in the value of the Naira against the US

dollar as Foreign exchange inflows have dried up, Nwokeoma (20009).

CHAPTER THREE

RESEARCH METHODOLOGY

3.1. INTRODUCTION

This chapter discusses in detail the methodology adopted forthis research. It presents the research model and necessarymethodology that would be adopted for this empirical study, and assuch, critically assess the effects of the global financial crisis

33

on the economy of developing countries like Nigeria. Difference ofmeans and multiple regression analysis would be adopted to achievethe specific objective of the study. The economic meltdown is notquantifiable and thus would be represented by the dummy variable.The choice of the best functional form would be based on

i. A’priori expectationii. R-2 (Adjusted R2)iii. Significance of regression coefficient.iv. The overall significance of the model.

3.2. SOURCES OF DATA

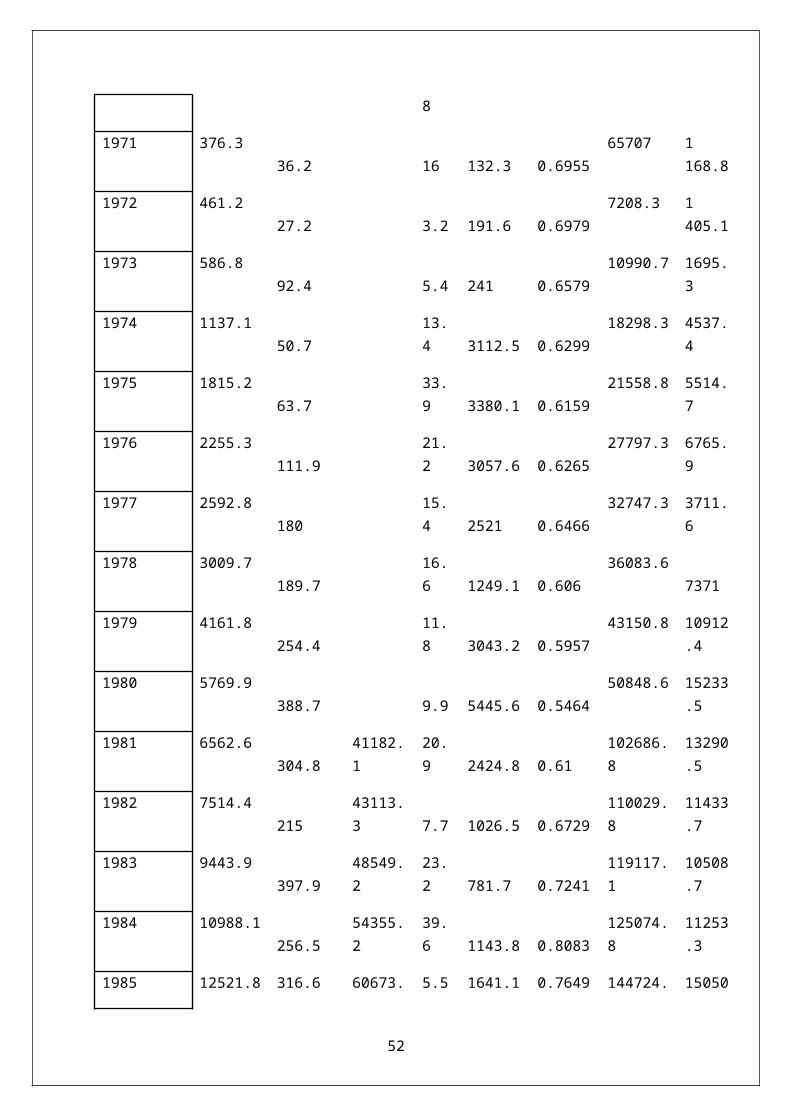

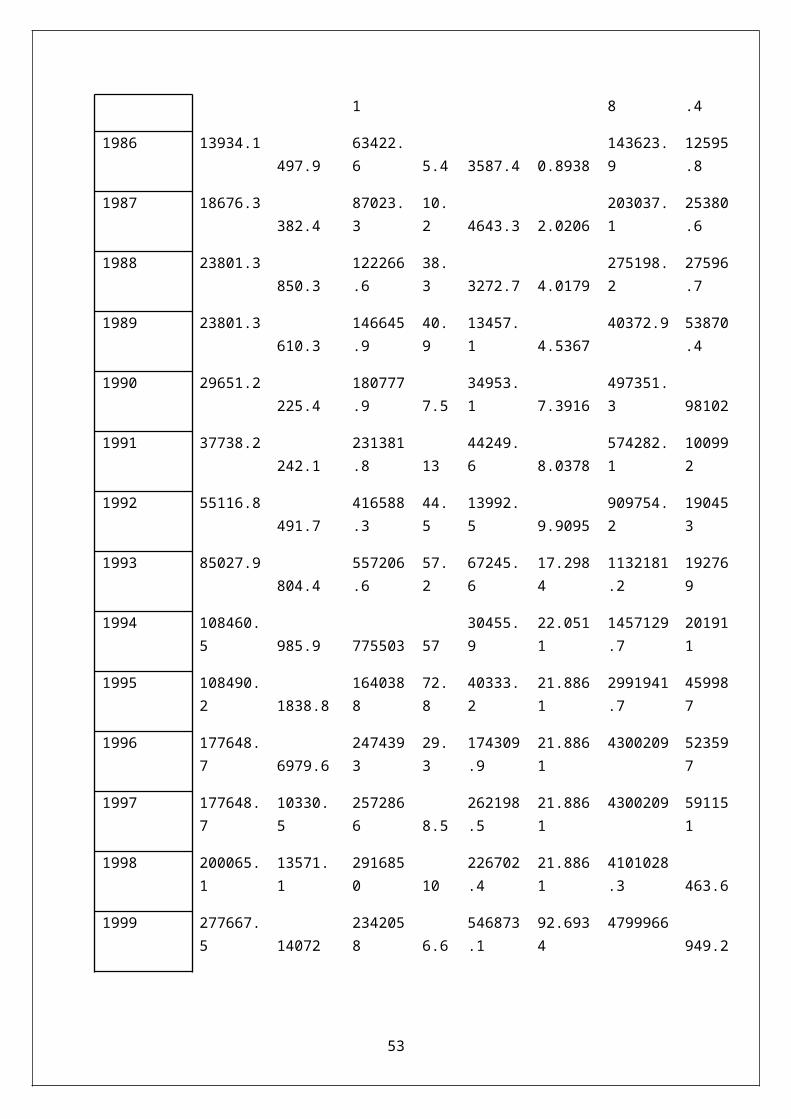

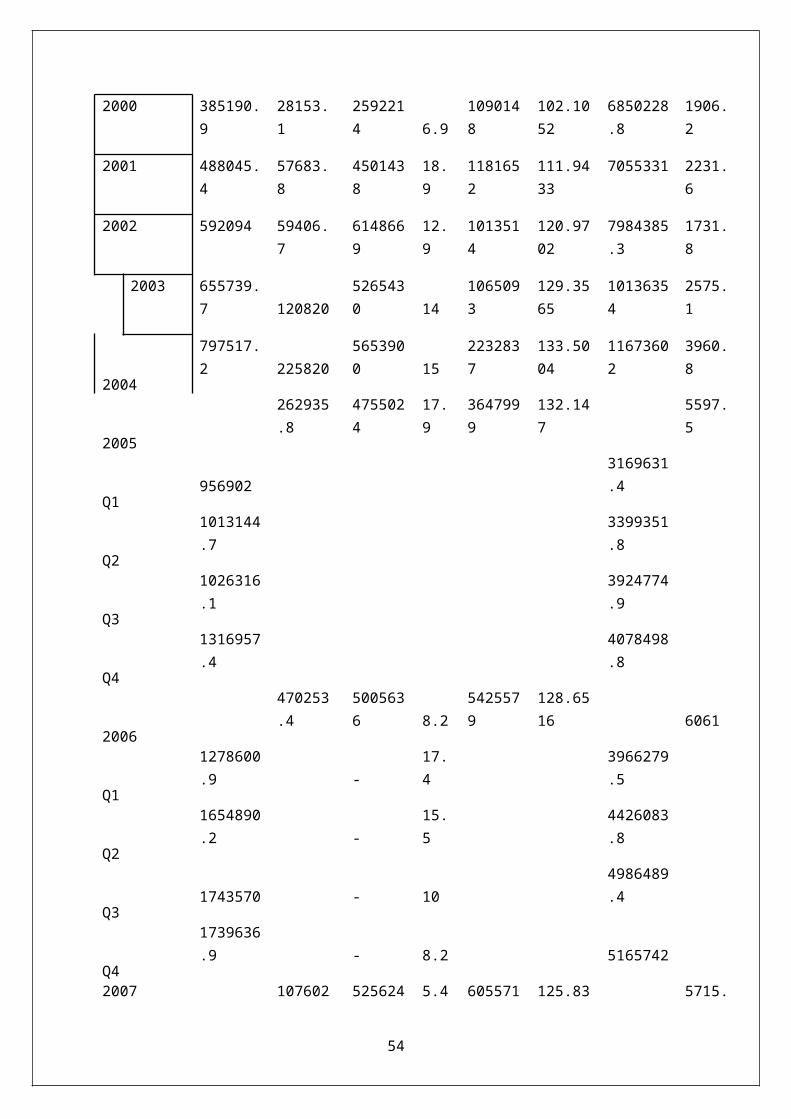

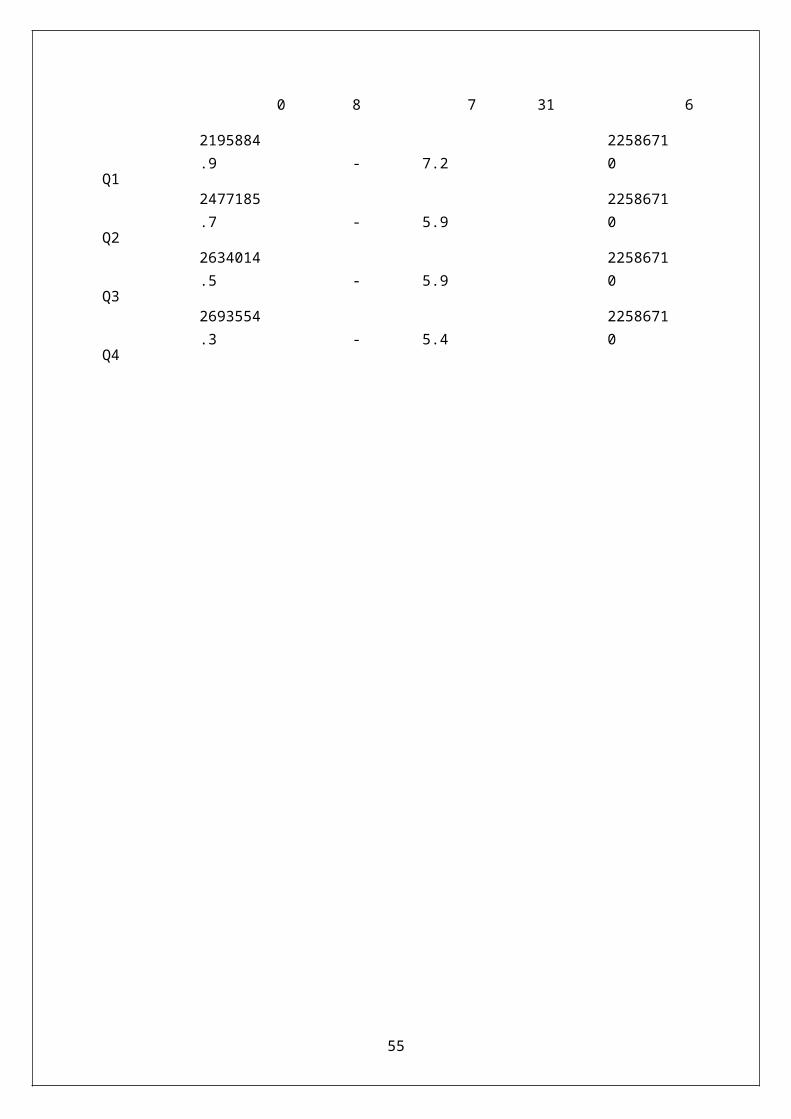

Secondary data would be obtained and as such data would be sourcedfrom the following institution, the Central Bank of Nigeria throughthe Statistical Bulletin where data showing the trend of Aggregatesavings, aggregate consumption, aggregate revenue, Nigeria stockexchange transaction, Nigerian external reserves, Gross domesticproducts from 1970-2007.

The National Bureau of Statistics for data showing the trendof the rate of inflation from 1970-2007. But for the purpose ofanalysis, data will be on quarterly basis, so as to capture theeffects (before and during the crisis) of the economic meltdown.

3.3. MODEL SPECIFICATION

a. Multiple Regression analysis would be used to achieve thespecific objectives of the study. The regression equation wasspecified explicitly in accordance with the ordinary least squareapproach as shown in equation (1) below;

AgCon=0+1AgSav+2Rev+3InfRa+4SeT+5NeR+6ExNd+7Gdp+8Ecomel+U0

Where:

AgCon= Aggregate Consumption (=N=)

AgRev= Aggregate Revenue (=N=)

AgSav= Aggregate Savings (=N=)

34

InfRa= Inflation Rate (%)

SeT= Stock Exchange Transaction (=N=)

NeR= National External Reserves (=N=)

ExNd= Exchange Rate of the naira to the dollar (=N=)

Gdp= Gross Domestic Product (=N=)

Ecomel = Economic Meltdown (dummy variable)

The data were fitted into four (4) functional forms (linear, Cobb-Douglas, Semi-log, Exponential functions) below

Linear;

AgCon=0+1AgSav+2Rev+3InfRa+4SeT+5NeR+6ExNd+7Gdp+8Ecomel+U0.......... (2)

Cobb-Douglas;

Ln(AgCon)=Ln0+1AgSav+2Ln(AgRev)+3Ln(InfRa)+4Ln(SeT)+5Ln(NeR)+6Ln(ExNd)+7Ln(Gdp)+8Ln(Ecomel)+U0..........(3)

Semi-Log;

AgCon=Ln0+1AgSav+2Ln(AgRev)+3Ln(InfRa)+4Ln(SeT)+5Ln(NeR)+6Ln(ExNd)+7Ln(Gdp)+8Ln(Ecomel)+U0.........(4)

Exponential;

Ln(AgCon)=0+1AgSav+2Rev+3InfRa+4SeT+5NeR+6ExNd+7Gdp+8Ecomel+U0.......... (5)

The selection of the lead equation (test functional form) was basedon high coefficient of determination (adjusted), statisticalsignificance of the regression coefficient and Fcal conformity of thealgebraic sign on the estimate of regression coefficients toA’priori expectation.

b. Difference of means; this is used to compare the averages of twosamples taken from the same population. This will be used to comparethe averages of Aggregate consumption, inflation rate and aggregaterevenue before and during the economic meltdown.

35

Where

= Aggregate (consumption, revenue), inflation rate, beforeeconomic meltdown.

= Aggregate (consumption, revenue), inflation rate, duringeconomic meltdown.

=

=

= Number of years before the economic meltdown.

= Number of years during the economic meltdown.

3.4. A’PRIORI EXPECTATION.

This explains the theoretical expectation about the relationshipbetween the included variables in the model. The A’prioriexpectations are:

1 < 0 (coefficient of aggregate savings (=N=), is less than zero,this means that as aggregate savings increases, aggregateconsumption (=N=) decreases).

2< 0 (coefficient of aggregate revenue (=N=), is less than zero,this means that as aggregate revenue increases, aggregateconsumption (=N=) decreases).

3< 0 (coefficient of inflation rate (%), is less than zero, thismeans that as inflation rate increases, aggregate consumptiondecreases)

36

4< 0 (coefficient of stock exchange transaction (=N=) is less thanzero, this means that as stock exchange transaction increases,aggregate consumption (=N=) decreases).

5> 0 (coefficient of national external reserves is greater thanzero, this means that as the national external reserves increases,aggregate consumption (=N=) also increases).

6> 0 (coefficient of exchange rate of naira to the US dollar isgreater than zero, this means that as the exchange rate of naira tothe US dollar increases, aggregate consumption (=N=) alsoincreases).

7> 0 (coefficient of gross domestic product is greater than zero,this means that as the gross domestic product increases, aggregateconsumption (=N=) also increases).

3.5. RESTATEMENT OF HYPOTHESIS

i. H0: Economic meltdown does not influence aggregate consumptionexpenditure negatively.

H0: 1 = 0 (coefficient of aggregate consumption equal to zero)

H1: economic meltdown influences aggregate consumptionexpenditure negatively.

H1: 1 < 0 (coefficient of aggregate consumption less than zero)

ii. H0: Average exchange rate of naira is not significantly higherduring economic meltdown compared to the period before it.

H0: = (coefficient of exchange rate of naira to the USdollar during economic crisis is equal to the exchange rate ofthe naira to the US dollar before the economic crisis).

H1: Average exchange rate of naira is significantly higher duringeconomic meltdown compared to the period before it.

H1: > (coefficient of exchange rate of naira to the USdollar during economic crisis is greater than the exchangerate of the naira to the US dollar before the economiccrisis).

37

CHAPTER FOUR

RESULT ANALYSIS

4.1 INTRODUCTION

38

This chapter is devoted to the explanation of the result ofthe analysis of the secondary data used for the study. The resultsare divided into two.

i. Difference of meansii. Multiple regression analysis

Each of these is discussed below

i. Difference of means: this analysis was used to compare theaverage of selected macro economic variables before andduring the economic meltdown. The variables are aggregateconsumption, inflation rate and aggregate revenue.

ii. Multiple regression analysis: the major reason for using themultiple regression analysis is to establish the causalrelationship between the dependent variable (aggregateconsumption) and the independent variables (aggregaterevenue, aggregate savings, inflation rate, stock exchangetransaction, national external reserves, gross domesticproduct, exchange rate of naira to the US dollar, and theeconomic meltdown).

4.2 DATA ANALYSIS

1. Using difference of means

Aggregate Consumption

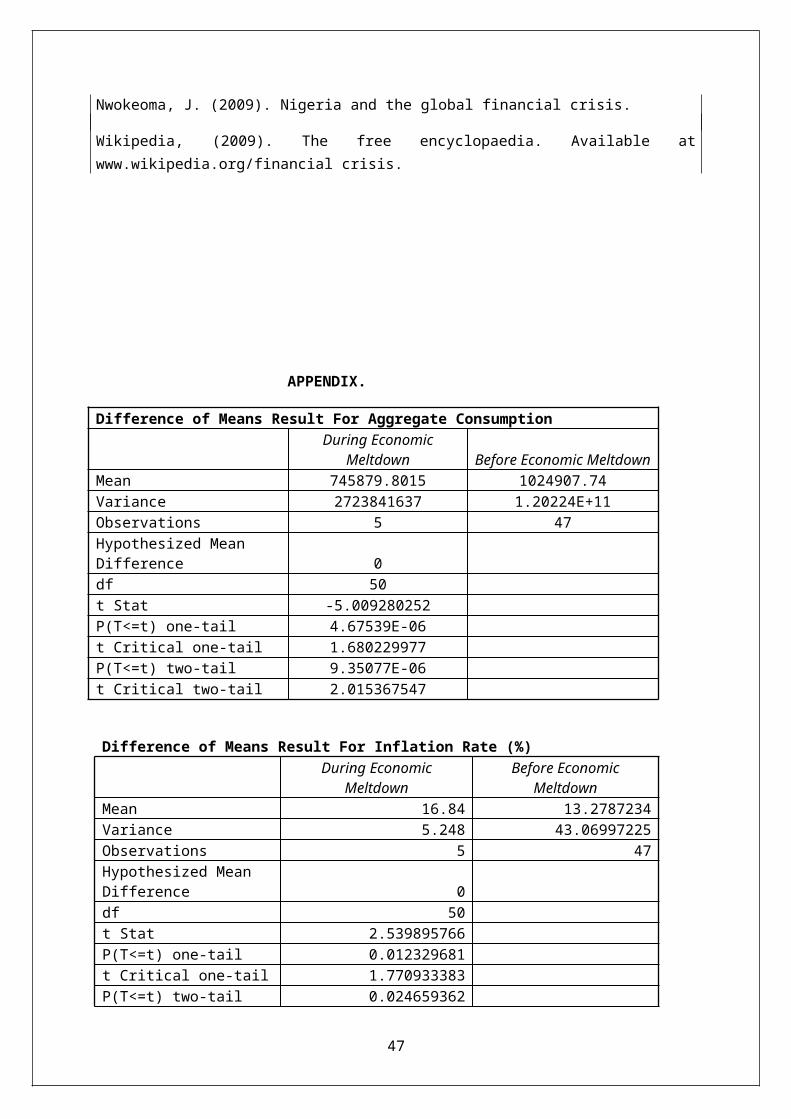

The result of the analysis shows that the absolute value of Zcal

is 5.0 while the Ztab is at 5% level of significance

H0: =

H1: >

Before economic meltdown is significantly greater duringeconomic meltdown is (1tail) 1.68, from these Zcal>Ztab. This meansthat the null hypothesis should be rejected and alternativehypothesis accepted. That is, the average aggregate consumptionbefore economic meltdown is significantly greater than averageaggregate consumption during economic meltdown. This result may beattributed to the fact that during economic meltdown, the purchasing

39

power of consumers has reduced considerably, prices of goods andservices have equally gone up.

Inflation Rate

This result shows the positive value of Zcal is 2.54, Ztab (at

1tail) is at 5% level of significance.

H0: =

H1: >

This means that inflation rate during economic meltdown is

significantly greater than inflation rate before economic meltdown.

The result corroborates the aggregate consumption result above.

Higher inflation leads to low purchasing power. The consequence of

that is that the cost of living is higher while the standard of

living continues to depreciate.

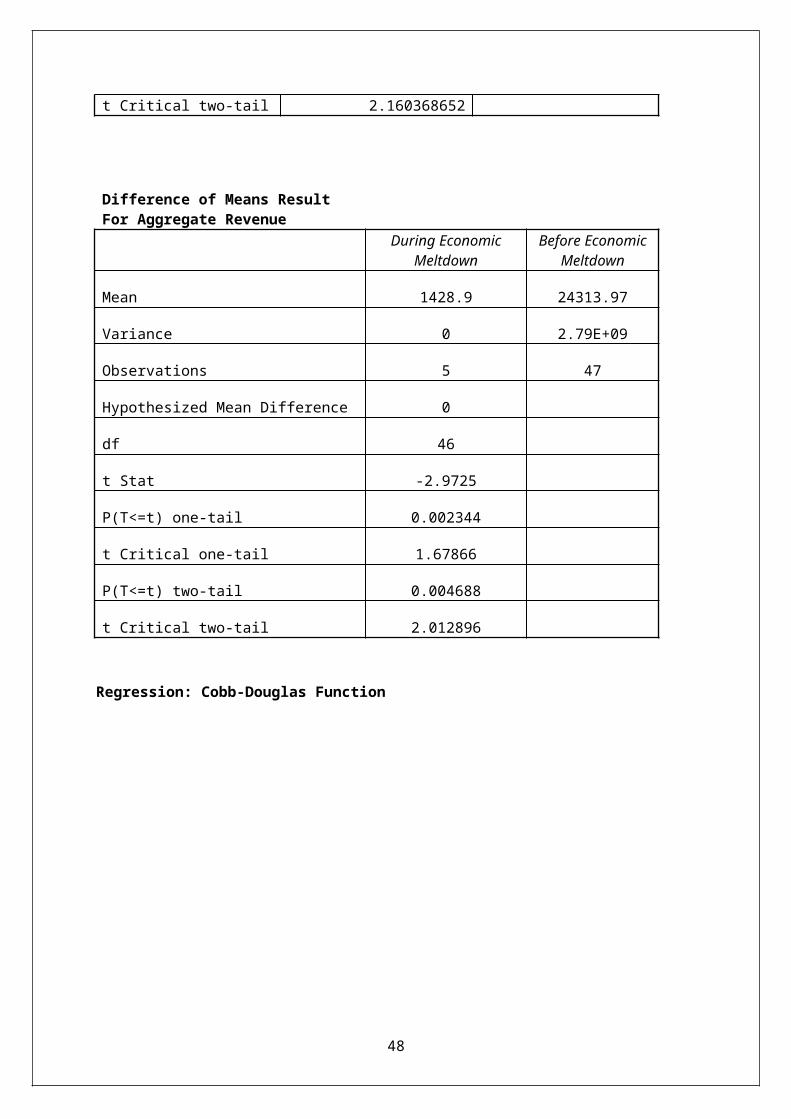

Aggregate Revenue

The absolute value of Zcal>Ztab at 5% level of significance which

means the null hypothesis is rejected while the alternative

hypothesis is accepted.

H0: =

H1: >

This means that average aggregate revenue before economic meltdown

is higher than during economic meltdown. This finding is in

agreement with what is going on in the Nigerian economy since 95% of

our revenue depends on oil. Specifically the price of crude oil

reached a peak of $145 per barrel as at July 2008 and since then it

has been dropping; the crisis in the oil rich region of Niger Delta

has not allowed Nigeria to reach its quota at OPEC. The implication

of this drastic reduction in aggregate revenue during meltdown is

40

that political office holders on whose hands lies the mantle of

power agreed on a reduction of their monthly allocation, the

government also decided to remove petroleum subsidy coupled with the

sanitization of the banking industry. The decline in aggregate

revenue also affects the external reserves which also cause the

exchange rate of the naira to the dollar to remain high, thereby

causing a reduction in the purchasing power.

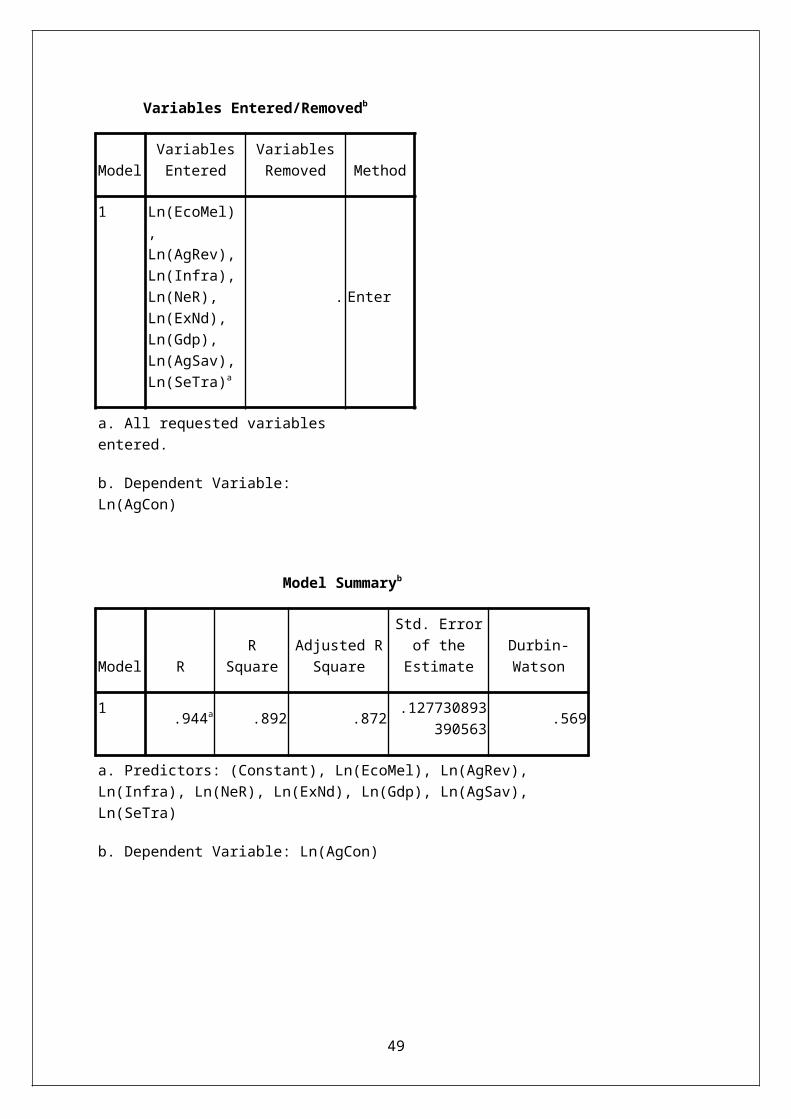

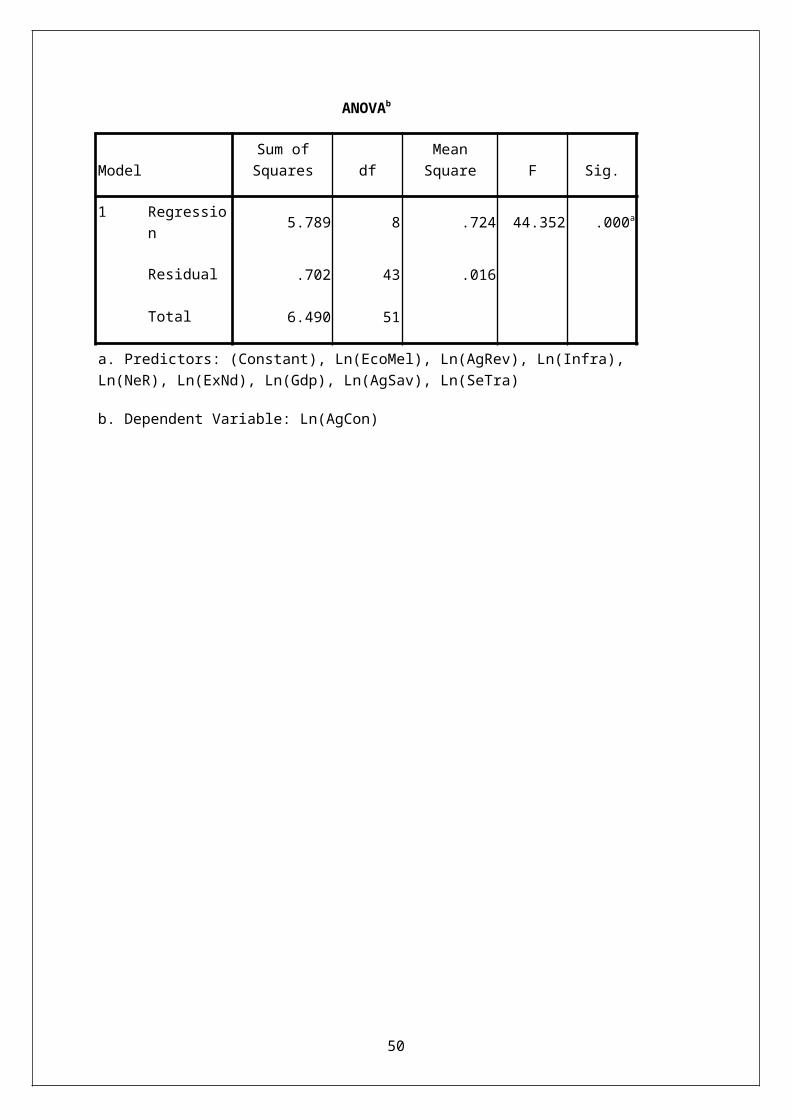

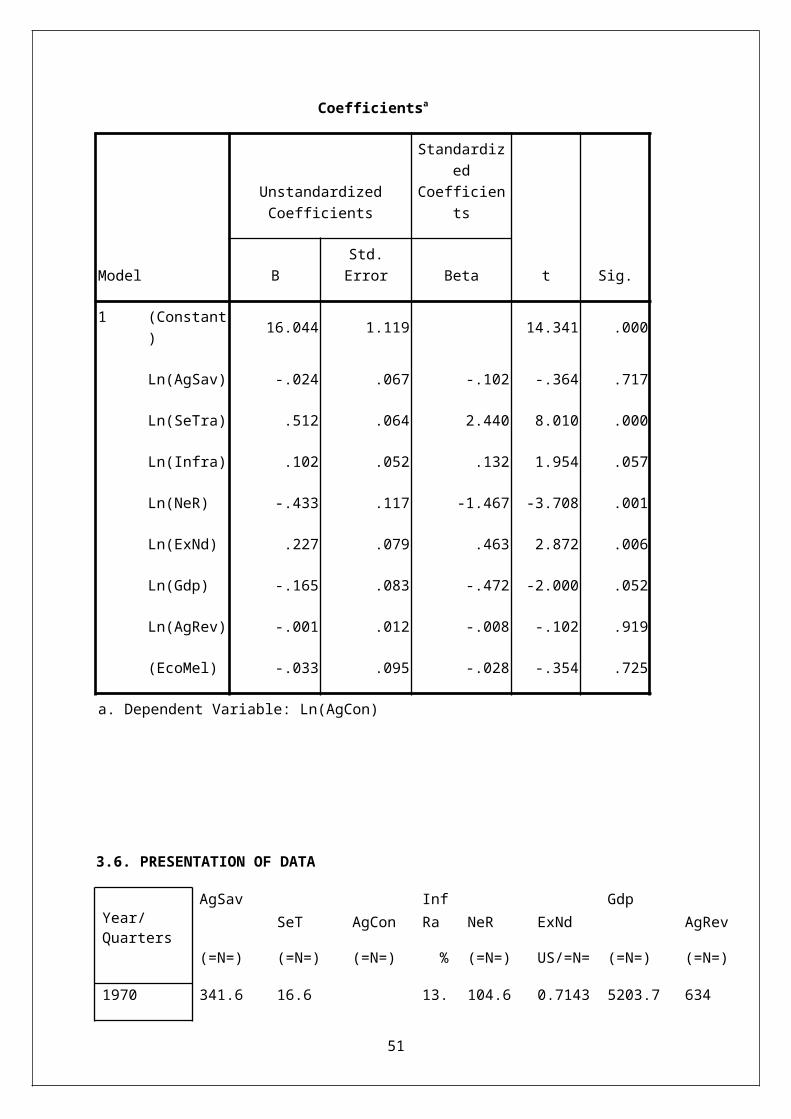

2. Using multiple regression analysis

The Cobb-Douglas functional form (equation 3) is chosen out of

the four fitted for analysis.

LnAgCon=16.04-0.024AgSav+0.51LnSeT+0.10LnInfRa-0.43LnNeR+0.23LnExNd-

0.17LnGdp-0.001LnAgRev-0.3Ecomel

Standard error: (0.067) (0.064) (0.052) (0.117) (0.079) (0.83)

(0.012) (0.095)

t. Value: (-0.364) (8.010) (1.954) (-3.708) (2.872) (-2.000) (-

0.102) (-0.354)

R-2=0.87

Fcal=44.35

Note: AgCon is dependent variable.

The choice of the Cobb-Douglas function is based on the high

adjusted coefficient at 5% level of significance and the overall

significance of the model at 1% level of significance, the

conformity of some of the algebraic sign with A’priori expectation.

4.3 INTERPRETATION OF DATA

The model shows that the economic meltdown has a negative

impact on aggregate consumption of Nigeria despite the

41

insignificance of the corresponding regression coefficient. The

insignificance of the regression coefficient may be attributed to

the high lopsidedness in the period of economic meltdown in Nigeria

(5quarters and 47 quarters) considered in this study.

4.3.1 INTERPRETATION OF THE STANDARD ERROR

The result shows that the higher the standard error, the

higher the possibility of tcal of the particular variable to be

significant.

4.3.2 INTERPRETATION OF DURBIN WATSON

The lower limit of Durbin Watson is tabulated at 1.38. And the

calculated Durbin Watson is 0.569. Since the calculated Durbin

Watson ids less then the tabulated Durbin Watson, then there is no

autocorrelation. This implies that the model is in agreement with

the fourth assumption of ordinary least square that successive value

of random variable U must be temporary independent i.e. independence

between the values of the same variables and not between two

different variables.

4.4 DISCUSSION OF FINDINGS

The adjusted coefficient of determination value revealed that

87.2% variation in aggregate consumption is explained by aggregate

consumption aggregate savings, aggregate revenue, and inflation

rate, exchange rate of naira to the US dollar, national external

reserves, stock exchange transaction, gross domestic product, and

economic meltdown. Furthermore there is overall significance of the

lead equation Fcal>Ftab at 1% level of significance. There is an

indication that not all parameters are zero. Hence there is causal

relationship between dependent variable and independent variable.

42

This result is in agreement with the difference of means

result in terms of the huge reduction in the purchasing power, cost

of production for both private and public enterprises remains high

which makes goods and services expensive therefore a burden to the

consumer.

All this can be attributed to the fact that economic meltdown

has reduced the external reserve, the inflation rate has

skyrocketed, and the effects are rather indirect. In conclusion the

economic meltdown can be a threat to the achievement of millennium

development goals and the objectives of the government to become one

of the leading economies in the world by 2020.

43

CHAPTER FIVE

SUMMARY

5.1. SUMMARY OF THE RESEARCH

The global financial crisis constitutes serious threat tomillions of people around the world, especially the poor. The crisishas spurred commitments to action from concerned institutions aroundthe world. Central Banks world over are concerned by themacroeconomic stability, maintenance of financial stability of theeconomy and ensuring the proper functioning of monetary economypayments and settlement systems.

Nigeria is presently using fiscal policies to ease thepressure of the global credit crunch. To match the efforts, theCentral Bank of Nigeria has equally put in place several measures toenable the country to cope. The economic crisis has affected theNigerian economy negatively according to the data used for thisresearch. Various economic indictors have shown significant changesin value before and during the economic meltdown. Althoughdeveloping economies are free to manage their economies usingvarious strategies, some of which may draw down to reserves tofinance sudden short falls in capital inflows and interest cuts.With depleted or no reserves, this countries will continue to feelthe brunt of the economic meltdown.

44

Developing countries like Nigeria that has been pursuingmillennium development goals prior to the outbreak of the crisis andthis decline will have their growth rates slow down to levels unseenbefore. The external reserves of Nigeria which was the pride of pastadministrations has witnessed a major decline coupled with thedecreased value of the national currency (naira) against othercurrencies in the world spells doom for Nigeria in the coming years.

5.2 IMPLICATION OF THE STUDY

The unprecedented fall by 40 percent in the internationalprice of oil, which was further compounded by the persistent crisisin the Niger-Delta region of Nigeria signals that if the financialmeltdown persists, Nigeria could suffer a major setback. The effectsof the crisis on agricultural and rural developments and indeed theNigerian economy as a whole ranges from dis-incentives to foreigninvestors, decay of the infrastructures likely to weaken the supplyside of the nations’ food market, bearish features of the capitalmarket, panic withdrawals of deposited funds from banks byentrepreneurs and industrialists in apprehension of futureuncertainties.

The current global depression has reduced energy consumptionand consequently crude oil demand. The Nigerian economy needs to berepositioned for possible shocks and fiscal adjustments. There isalso the need to deepen the economy by reinvigorating the realsector of the economy as well as revitalising the service sectors.

5.3 RECOMMENDATIONS

The study recommends the following in order to address thenegative impacts that have risen as a result of the economicmeltdown.

i. Diversification of the Nigerian economy from the monoculturecommodity of petroleum which accounts for over 95 percent ofNigeria’s revenue.

45

ii. The leakages that exist within the Nigerian economy must bebridged; the government must intensify its fight againstcorruption.

iii. There must be prudence in the external reserve spending thatis, the reserves should be spent on infrastructures ratherthan white elephant projects here and there.

iv. A lasting solution should be sought by the government tosolve the Niger-Delta crisis.

5.4 REFRENCES

Adamu, A. (2008). The effects of the global financial crisis on theNigeria economy, Ahmadu Bello University term papers.

Akkas, A. (2008). Review of the global financial crisis 2008;issues, analytical approaches and interventions.

Altman, R. (2008). The great crash, 2008/foreign affairs.

Avgouleas, E. (2008). What is the future for disclosure technique?Lessons from global financial crisis and beyond.

Bernstein, A. (2005). The capitalist manifesto: The historic,economic and philosophic case for Laissez-faire.

Iliyasu, M. (2008). Banking and currency crisis, how common aretwins?

Igbokwe, C. (2008). Reflections on Nigerian banks and globalfinancial crisis.

Kaufman, G. (2008). Financial crisis lessons from recent events, begood and grow rich.

Mtango, E. (2008). African growth financial crisis and implicationsfor TICAO IV.

Nigeriaquestion, (2009). Causes of economic meltdown in Nigeria.Available at wikianswers.com/Q/causes_of_meltdown in Nigeria.

46

Nwokeoma, J. (2009). Nigeria and the global financial crisis.

Wikipedia, (2009). The free encyclopaedia. Available atwww.wikipedia.org/financial crisis.

APPENDIX.

Difference of Means Result For Aggregate Consumption

During Economic

Meltdown Before Economic MeltdownMean 745879.8015 1024907.74Variance 2723841637 1.20224E+11Observations 5 47Hypothesized Mean Difference 0df 50t Stat -5.009280252P(T<=t) one-tail 4.67539E-06t Critical one-tail 1.680229977P(T<=t) two-tail 9.35077E-06t Critical two-tail 2.015367547

Difference of Means Result For Inflation Rate (%)

During Economic

MeltdownBefore Economic

MeltdownMean 16.84 13.2787234Variance 5.248 43.06997225Observations 5 47Hypothesized Mean Difference 0df 50t Stat 2.539895766P(T<=t) one-tail 0.012329681t Critical one-tail 1.770933383P(T<=t) two-tail 0.024659362

47

t Critical two-tail 2.160368652

Difference of Means Result For Aggregate Revenue

During Economic

MeltdownBefore Economic

Meltdown

Mean 1428.9 24313.97

Variance 0 2.79E+09

Observations 5 47

Hypothesized Mean Difference 0

df 46

t Stat -2.9725

P(T<=t) one-tail 0.002344

t Critical one-tail 1.67866

P(T<=t) two-tail 0.004688

t Critical two-tail 2.012896

Regression: Cobb-Douglas Function

48

Variables Entered/Removedb

ModelVariablesEntered

VariablesRemoved Method

1 Ln(EcoMel), Ln(AgRev),Ln(Infra),Ln(NeR), Ln(ExNd), Ln(Gdp), Ln(AgSav),Ln(SeTra)a

. Enter

a. All requested variables entered.

b. Dependent Variable: Ln(AgCon)

Model Summaryb

Model RR

SquareAdjusted R

Square

Std. Errorof the

EstimateDurbin-Watson

1 .944a .892 .872 .127730893390563 .569

a. Predictors: (Constant), Ln(EcoMel), Ln(AgRev), Ln(Infra), Ln(NeR), Ln(ExNd), Ln(Gdp), Ln(AgSav), Ln(SeTra)

b. Dependent Variable: Ln(AgCon)

49

ANOVAb

ModelSum ofSquares df

MeanSquare F Sig.

1 Regression 5.789 8 .724 44.352 .000a

Residual .702 43 .016

Total 6.490 51

a. Predictors: (Constant), Ln(EcoMel), Ln(AgRev), Ln(Infra), Ln(NeR), Ln(ExNd), Ln(Gdp), Ln(AgSav), Ln(SeTra)

b. Dependent Variable: Ln(AgCon)

50

Coefficientsa

Model

UnstandardizedCoefficients

Standardized

Coefficients

t Sig.BStd.Error Beta

1 (Constant) 16.044 1.119 14.341 .000

Ln(AgSav) -.024 .067 -.102 -.364 .717

Ln(SeTra) .512 .064 2.440 8.010 .000

Ln(Infra) .102 .052 .132 1.954 .057

Ln(NeR) -.433 .117 -1.467 -3.708 .001

Ln(ExNd) .227 .079 .463 2.872 .006

Ln(Gdp) -.165 .083 -.472 -2.000 .052

Ln(AgRev) -.001 .012 -.008 -.102 .919

(EcoMel) -.033 .095 -.028 -.354 .725

a. Dependent Variable: Ln(AgCon)