THE EFFECT OF THE EXTERNAL LABOR MARKET ON THE GENDER PAY GAP AMONG EXECUTIVES CRISTINA QUINTANA-GARCI ´ A AND MARTA M. ELVIRA* To date, few empirical studies have explored potential differences in the effects of external labor market hiring on the compensation of male and female managers. Using longitudinal data from a sam- ple of public high-technology firms on individual top executives’ total compensation in the United States, and the separate compo- nents of base and variable pay, the authors study the effects of being an external hire for men and women. The results suggest that women who are external labor market hires are disadvantaged, in both base and variable compensation, compared with internal placements. The analyses also provide some evidence that having greater representation of women in top positions reduces the disad- vantaging effects for women of being an external hire. W omen’s representation in top management is the subject of ample research (e.g., Reskin and McBrier 2000; Kalev, Dobbin, and Kelly 2006). Far less is known about gender differences in work outcomes once women reach top executive positions (Gayle, Golan, and Miller 2012; Shin 2012). As has been stressed recently, ‘‘access to high-paying jobs and the rewards that await workers once they are hired are important factors in studying the gender pay gap’’ (Kahn 2014: 285). Specifically, a significant pay gap exists between male and female executives that is attributable to unobserved factors, with estimates varying between 5% and 16% (Bertrand and Hallock 2001; Blau and Kahn 2006; Mun ˜oz-Bullo ´n 2010; Elkinawy and Stater 2011, but see Gayle et al. 2012 for contrary evidence). The still unex- plained portion of pay differentials is usually interpreted as evidence of gender inequality (Elvira and Saporta 2001; Elkinawy and Stater 2011), *CRISTINA QUINTANA-GARCI ´ A is an Associate Professor of Management and Director of the Santander Center for Corporate Social Responsibility at the University of Ma ´laga (Spain). MARTA M. ELVIRA is the Puig Chair Professor of Global Leadership Development and Associate Dean for Research at IESE Business School. The study has been partially supported by the aforementioned center. We gratefully acknowledge the feedback received from Emilio Castilla, Lisa Cohen, Olav Sorenson, Miguel Canela, participants in the EGOS colloquium in Rotterdam (2014), the ILR School of Cornell University confer- ence ‘‘Increasing Inclusion/Reducing Discrimination: What Works?’’ in New York City (2015), IESE’s Entrepreneurship Research Workshop, and anonymous reviewers of earlier versions of this manuscript. Correspondence can be sent to the authors at [email protected] or [email protected]. KEYWORDs: gender pay gap, executive compensation, external recruitment, inequality ILR Review, 70(1), January 2017, pp. 132–159 DOI: 10.1177/0019793916668529. Ó The Author(s) 2016 Journal website: ilr.sagepub.com Reprints and permissions: sagepub.com/journalsPermissions.nav

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

THE EFFECT OF THE EXTERNAL LABOR MARKET

ON THE GENDER PAY GAP AMONG EXECUTIVES

CRISTINA QUINTANA-GARCIA AND MARTA M. ELVIRA*

To date, few empirical studies have explored potential differencesin the effects of external labor market hiring on the compensationof male and female managers. Using longitudinal data from a sam-ple of public high-technology firms on individual top executives’total compensation in the United States, and the separate compo-nents of base and variable pay, the authors study the effects of beingan external hire for men and women. The results suggest thatwomen who are external labor market hires are disadvantaged, inboth base and variable compensation, compared with internalplacements. The analyses also provide some evidence that havinggreater representation of women in top positions reduces the disad-vantaging effects for women of being an external hire.

Women’s representation in top management is the subject of ampleresearch (e.g., Reskin and McBrier 2000; Kalev, Dobbin, and Kelly

2006). Far less is known about gender differences in work outcomes oncewomen reach top executive positions (Gayle, Golan, and Miller 2012; Shin2012). As has been stressed recently, ‘‘access to high-paying jobs and therewards that await workers once they are hired are important factors instudying the gender pay gap’’ (Kahn 2014: 285). Specifically, a significantpay gap exists between male and female executives that is attributable tounobserved factors, with estimates varying between 5% and 16% (Bertrandand Hallock 2001; Blau and Kahn 2006; Munoz-Bullon 2010; Elkinawy andStater 2011, but see Gayle et al. 2012 for contrary evidence). The still unex-plained portion of pay differentials is usually interpreted as evidence ofgender inequality (Elvira and Saporta 2001; Elkinawy and Stater 2011),

*CRISTINA QUINTANA-GARCIA is an Associate Professor of Management and Director of the SantanderCenter for Corporate Social Responsibility at the University of Malaga (Spain). MARTA M. ELVIRA is thePuig Chair Professor of Global Leadership Development and Associate Dean for Research at IESEBusiness School. The study has been partially supported by the aforementioned center. We gratefullyacknowledge the feedback received from Emilio Castilla, Lisa Cohen, Olav Sorenson, Miguel Canela,participants in the EGOS colloquium in Rotterdam (2014), the ILR School of Cornell University confer-ence ‘‘Increasing Inclusion/Reducing Discrimination: What Works?’’ in New York City (2015), IESE’sEntrepreneurship Research Workshop, and anonymous reviewers of earlier versions of this manuscript.Correspondence can be sent to the authors at [email protected] or [email protected].

KEYWORDs: gender pay gap, executive compensation, external recruitment, inequality

ILR Review, 70(1), January 2017, pp. 132–159DOI: 10.1177/0019793916668529. � The Author(s) 2016

Journal website: ilr.sagepub.comReprints and permissions: sagepub.com/journalsPermissions.nav

although we need to understand fully how various employment practicesaffect compensation. For example, in recent decades external market forcesare increasingly influencing the organizational distribution of work andrewards (Bidwell, Briscoe, Fernandez-Mateo, and Sterling 2013). Becausemuch research on gender inequality has focused on internal promotions,little is known about the impact of external hiring on pay differentials(Fernandez and Abraham 2011).

In this study, we explore the effects of adopting an external labor market(ELM) strategy on gender differences in executive compensation. The the-ory of incomplete information, social capital, and the opportunity structurefor discrimination framework serve as the study’s foundation. On the onehand, promotion within the firm differs from external hiring in the level ofinformation that a firm has about employees (Granovetter 1981; Halaby1988). Differences in access to such information might affect the character-istics of workers who enter jobs through hiring versus internal promotionand, consequently, their pay levels (Bidwell 2011). On the other hand, forexecutives, base salary is complemented by variable pay, usually subject toless formalization and more subjective valuation, which opens a structuralopportunity for differential treatment in compensation between male andfemale executives.

At the management level, to our knowledge, few studies explore theeffect of ELM moves on male and female managers’ compensation. Someresearch suggests that the process of changing companies explains much ofthe observed gender gap. Brett and Stroh (1997) studied a sample of man-agers at different levels from 20 Fortune 500 companies. Examining onlycash compensation while controlling for human capital and industry, thisstudy showed that male managers who changed companies between 1989and 1991 improved their compensation relative to those who remained intheir firms. This effect was not observed for female managers. Researchinga sample of 1992 MBA graduates and considering practically the same vari-ables as above, Dreher and Cox (2000) also concluded that pay differentialsamong graduates who changed employers were a white male phenomenon.Similarly, using data from U.S. managers and professionals collectedthrough surveys in 1991 and 1999, Lam and Dreher (2004) found that cashcompensation levels (base salary plus bonus) were significantly higheramong males who followed an ELM strategy than among men whoremained with the same firm (stayers). Again this pattern does not appearamong female managers, for whom cash compensation was similar betweenstayers and movers.

Some contradictory evidence exists: Valcour and Tolbert (2003), using asample of primarily managerial and professional employees in dual-earnercouples in the United States, found no gender earnings differences forintra- and interorganizational mobility. For both men and women, movingbetween organizations tends to depress earnings while job changes withinan organization relate to increased earnings. More recently, Kronberg

EXTERNAL LABOR MARKET’S EFFECT ON EXECUTIVE GENDER PAY GAP 133

(2013) found that in the 1990s externalization closed the gender gap mostlyamong workers who already occupied good positions (such as executivejobs) and left a firm voluntarily.

Overall, most prior studies have considered cash compensation as theoutcome variable, have lacked information about employers (i.e., firm char-acteristics and organizational practices), and have mixed managers belong-ing to different organizational levels (though pay components typicallydiffer across levels). Regarding the first issue, a large (if not the largest) por-tion of executives’ total compensation comes from long-term components(i.e., restricted stock awards, stock options, and other long-term incentivepayouts) (Elkinawy and Stater 2011; Gayle et al. 2012; Shin 2012). The useof stock options, incentive bonuses, and other components of variable com-pensation may widen the pay gap between women and men (Elvira andGraham 2002; Munoz-Bullon 2010). Base pay is determined largely by thelevel of an individual’s occupational category whereas variable pay is setthrough a less formalized process.

Given prior research limitations, our study aims to advance understand-ing of how ELM moves relate to the gender gap in executive compensationby 1) focusing on top executives, who may constitute a relatively homoge-neous group in terms of pay elements, work experience, skills and abilities,and education (Bell 2005); 2) taking into account the total direct compen-sation awarded to executives, while analyzing the gender pay gap separatelyfor base salary and variable pay; and 3) including organizational variablessuch as the proportion of women in top executive positions, in addition toconsidering individual human capital and firm-level factors. For the empiri-cal setting, we have chosen firms from the high-technology sectors, whichshow an increasing influence of external market forces on labor practices(DiPrete, Goux, and Maurin 2002; Siegel and Hambrick 2005) and thatoperate in similar labor market conditions, allowing for relative datahomogeneity.

Women Executives’ Compensation and External Managerial Recruitment

Research shows a persistent gender wage gap, which has been explainedfrom various perspectives. Human capital theory (Becker 1964; Hashimoto1981) predicts that earnings differences emerge from variation in the broadarray of individual abilities and educational investments among workers. Acommon empirical finding is that women have inadequate firm-specifichuman capital, different educational backgrounds, shorter tenures, andmore interrupted careers than do men. These variables partially explain thegender wage gap (Blau and Beller 1988). Nevertheless, the evidence for thishuman capital hypothesis is mixed. For instance, Petersen and Saporta(2004) indicated that initial gender differences in job levels and salariesdecrease to the extent of disappearing as seniority increases. This equaliza-tion may happen because, with seniority, it becomes harder to discriminate

134 ILR REVIEW

and also because more information is available about employees. Such adeclining gap should mean that once women break the glass ceiling andbecome top executives, their compensation would equal that of their malecounterparts.

Few articles on the executive pay gap have measures of education or workexperience. Gayle et al. (2012) showed that female executives have back-grounds and experiences that differ from male executives and that womenare paid more and have higher pay-for-performance sensitivity than do menwith a similar rank, background, and experience. They also found thatwomen are promoted internally more quickly than men are (as long as theyremain in the firm), which results in their having significantly less job expe-rience than male executives have.

We wonder whether the gender gap might widen with the increasing reli-ance on external hiring. Firms using internal labor markets (ILMs) torecruit and promote managers should have access to accumulated perfor-mance information to help place competent internal employees (female ormale) with suitable human capital in executive positions (Bidwell 2011).Then individuals would be promoted and rewarded according to their abil-ity and skills, if and when they were assigned to a more senior position (Fee,Hadlock, and Pierce 2006).

Consistent with the theory of incomplete information, the trend towardmarket-based employment has reduced the influence of firm-specifichuman capital on pay and thus, the rewards to seniority. As a result, exter-nally hired managers may obtain a salary premium relative to those who arepromoted internally. Employers have incomplete information about outsidepotential employees. Because many higher-level jobs are subject to greatuncertainty and demand a threshold level of performance, firms mayrequire stronger visible credentials from outside hires than from those peo-ple promoted from within (Fee et al. 2006; Bidwell 2011). The purchase ofskills valuable to the firm requires the provision of extra rewards in order toattract employees and to obtain their agreement to this sort of transactionalemployment relationship (Valcour and Tolbert 2003). Another potentialreason for higher pay is that experienced managers receiving an ELM offermay anticipate short-term employment. Companies that tend to hire man-agers from outside the organization do not emphasize career developmentor security. Consequently, expectations of short-term employment may leadto greater compensation in exchange for the lack of employment security(Brett and Stroh 1997).

Research indicates that ELM career moves generally lead to compensa-tion advantages for men but not for women (Brett and Stroh 1997; Dreherand Cox 2000; Lam and Dreher 2004). For women at the executive level,several factors may result in a cumulative career disadvantage attributable toELM career strategies. Because less is known at the point of hire comparedwith the time of promotion, the decision on which working conditions (e.g.,pay) to offer is usually highly subjective. As a result, differential treatment in

EXTERNAL LABOR MARKET’S EFFECT ON EXECUTIVE GENDER PAY GAP 135

setting salaries is more likely to affect new hires than long-tenure employ-ees, whose actual performance has been observed (Gerhart 1990). The sta-tus of a new hire leaves women more vulnerable to differential treatmentbecause such an approach is easier to justify when less information is avail-able (Petersen and Saporta 2004; Kronberg 2013).

Some employers may even stereotype women as less sophisticated negoti-ators and offer them lower salaries and/or take a harder bargainingapproach (Dreher and Cox 2000). If women are less inclined to negotiatetheir wage upward (Babcock and Laschever 2003), then their pay maydecline more when negotiations are more frequent, such as in externaltransitions. Additionally, female managers may be disadvantaged in theELM because they are less well connected than male managers to formaland informal social networks that provide access to career opportunitiesand information. The use of such networks, especially for external hiring,has grown over time (Marsden and Hurlbert 1988; Moss and Tilly 2001).Network-based hiring generates gender inequality in access to jobs andfavors the persistence of differential allocation to higher levels (Fernandezand Sosa 2005; Gorman and Kmec 2009).

Overall, incomplete information and social capital research suggestpotential mechanisms that disadvantage women in external mobility. Thus,a growing emphasis on ELMs among executives may lead to higher com-pensation levels for men and generate more opportunities for gender paygap increases. Our baseline hypothesis is as follows.

Hypothesis 1: The compensation penalty for female executives relative to menrecruited through the external labor market will be larger than that of internallypromoted employees.

Beyond gender-specific characteristics, organizational structures offervarying opportunities for unjustified differential treatment of men andwomen. The opportunity structure for discrimination refers to the structuralconditions under which discrimination is feasible and successful, focusingon dimensions that may inhibit or facilitate differential treatment (seePetersen and Saporta 2004). We surmise that the increasing use of incentiveand performance-based compensation may unwittingly open the door togender biases. Base pay, the fixed component of compensation, is deter-mined largely by the individual’s job rank rather than job performance.Differential treatment of men and women in base salary for the same posi-tion is presumably easy to document, the evidence is mostly unambiguous,and the potential complainant is clear (the woman discriminated against).The opposite holds when compensation depends not only on the positionoccupied but also on the employee’s productivity, qualifications, or merit.Bonuses, stock options, and other long-term components of compensationare more often performance-based and thus subject to greater uncertainty

136 ILR REVIEW

and lower transparency. These variable pay elements could justify pay differ-ences within jobs that can be hard to assess (Petersen and Saporta 2004).

The limited formalization of setting variable pay gives firms greater dis-cretion in designing pay plans and criteria for pay allocation (Elvira andGraham 2002). For instance, women are considered to be more risk-averseand less confident than men, so they are expected to behave in ways thatare different from men during pay negotiations. These expectations mayreinforce the gender gap by encouraging women to choose less risky paypackages (Kulich et al. 2011). Therefore, relative to base salary, variable paymay represent a structural opportunity for differential treatment (Petersenand Saporta 2004), which might be more likely to occur during hiring thanduring promotion because it is harder for external candidates to detect andchallenge discrimination (Bidwell et al. 2013).

Empirical evidence indicates that the gender earnings gap is greater forvariable pay than for base salary. Chauvin and Ash (1994) found that mostof the unexplained difference in total pay between male and female busi-ness school graduates was attributable to gender differences in theperformance-contingent portion of pay (commissions, bonuses, and profitsharing). Using data from all full-time employees of a financial corporation,Elvira and Graham (2002) reported that women in the same occupationsand with similar characteristics (tenure and performance rating) receivedlower bonuses than men. Studies of U.S. firms’ top executives found that asubstantial part of the estimated gap in total pay was because of differencesin variable pay (Elkinawy and Stater 2011; Munoz-Bullon 2010).

In short, existing research suggests that the use of incentive pay couldwiden the earnings gap between women and men, so we hypothesize thefollowing.

Hypothesis 2: The penalty for female executives relative to men will be larger forvariable than for fixed compensation, especially among employees recruitedthrough the ELM.

Another organizational characteristic typically related to the gender wagegap is the sex composition of organizations, occupations, or work groups.Regarding executives, the proportion of women in top management hasgrown substantially, even as women continue to be underrepresented. Datasuggest that women’s pay increases in jobs with a higher proportion ofwomen employed in that type of job. As women advance through the ranks,any differences in the treatment of men and women that arise from imper-fect information about women’s abilities will narrow (Bell 2005).Furthermore, social identity theory suggests that people have a tendency toevaluate in-group members more favorably than out-group members and todevelop mutual liking and attraction (Tajfel and Turner 1979). Consistentwith these processes, male decision makers are more likely than theirfemale counterparts to hire and promote male candidates (Beckman and

EXTERNAL LABOR MARKET’S EFFECT ON EXECUTIVE GENDER PAY GAP 137

Phillips 2005; Gorman 2006). Thus an increasing female presence in topcorporate jobs may help reduce the gender gap in executive pay (Shin2012). Wages would also be higher because the higher proportion ofwomen would give them more organizational power (Pfeffer 1981) andwould potentially facilitate actions in favor of other women on the top man-agement team (TMT), for example, in job allocation and compensationdecisions.

A higher representation of women in the TMT can have a positive impacton female executives’ pay. Evidence suggests that women across an organi-zation earn more when they have female managers (Hultin and Szulkin1999) or a female CEO (Cardoso and Winter-Ebmer 2010; Flabbi, Macis,Moro, and Schivardi 2014). Bertrand and Hallock (2001) found that as theparticipation of women in top managerial jobs grew, the gender compensa-tion gap declined. Expectations that women are risk-averse and less confi-dent than men when negotiating their pay may increase the gender gap byencouraging women to accept a lower variable compensation (Byrnes,Miller, and Schafer 1999; Kulich et al. 2011). Such expectations may causenegative reactions toward those women who do not comply with genderstereotypes. For example, women are penalized socially more than men arefor negotiating for higher pay (Bowles and Babcock 2012). A higher pro-portion of women in the TMT may help increase the bargaining power ofother females, encouraging them to negotiate for desirable job conditions(Beckman and Phillips 2005). When a higher proportion of female manag-ers are employed, women are more likely to be negotiating the terms oftheir employment with other women and to have a greater likelihood ofsuccess (Rousseau 2005; Cohen and Broschak 2013). The presence ofwomen in the TMT and in other top corporate jobs can also be a proxy forsome of the firm’s cultural and institutional climate, such as female-friendliness or an egalitarian environment (Shin 2012).

The board of directors, which often includes some members of the TMT,directly influences the design of compensation packages for top executives,as it is legally responsible for monitoring, rewarding and, if necessary, firingtop executives. A greater proportion of female directors on the board couldbe associated with a more favorable evaluation of female executives andgreater access to compensation information for executives generally, thuspotentially reducing the gender gap in pay. In fact, evidence does supportthat having more female board members is associated with a smaller gendergap in executive compensation (Shin 2012). Using various data samplesfrom ExecuComp over the long term, Bell (2005), Elkinawy and Stater(2011), and Carter, Franco, and Gine (2015) found that female representa-tion in the boardroom mitigates the gender pay gap among executives.

We expect these female representation effects to be magnified for exter-nal hires, for whom negotiations may take center stage in the recruiting pro-cess from the start and are typically more visible than for internallypromoted candidates whose career follows an accepted path.

138 ILR REVIEW

Therefore, we hypothesize the following.

Hypothesis 3: The pay penalty for female executives will be reduced in firms with ahigher proportion of women at the firm’s top levels, especially among employeesrecruited through the ELM.

Methods

Data and Sample

Our research question is especially salient in settings such as high technol-ogy and other growing sectors in which employment relationships relyincreasingly on ELMs, as manifested by the decline in average employmenttenure (DiPrete et al. 2002). Moreover, the high-technology sectors arecharacterized by a flatter wage-tenure profile among the more highly edu-cated workers than in more traditional industries (DiPrete et al. 2002).These features make it easier to analyze the dynamics of the ELM relative toindustries that still rely heavily on ILMs. Focusing on high-technology manu-facturing firms also enables relatively homogeneous data to be obtainedbecause such firms operate in similarly dynamic environments, with the cor-responding consequences for executive rewards compared with relativelystable settings (Siegel and Hambrick 2005).

Specifically, we study a panel data set of U.S. public high-technology man-ufacturing firms. We use the executive year as the level of analysis and cre-ate a database using different sources of information. The panel of U.S.public high-technology firms is drawn from Thomson Reuters Datastream’sASSET4 ESG, the world’s largest environmental, social, and governance rat-ing database. It contains objective and systematic quantitative and qualita-tive company-level data on public companies worldwide for at least fouryears for most companies, with 2007 to 2011 being the most commonperiod. Therefore, we identify a panel of firms with available informationon organizational practices that are explanatory variables in this study forthe stated period. Variables drawn from this database include the percent-age of women on the board of directors and a range of diversity manage-ment practices. ASSET4 ESG contains data on 167 U.S. public high-technology manufacturing companies.1

Having selected the companies, we draw information concerning com-pensation of their top executives from the ExecuComp database. For thehighest-paid executives of the U.S. public companies, ExecuComp containscomprehensive information on base salary and variable components ofcompensation (bonuses, total value of restricted stock grants, total value ofstock options granted, long-term incentive payouts, and so forth) as

1The high-technology manufacturing sectors identified from the ASSET4 ESG are aerospace/defense;biotechnology/medical research; biotechnology/pharmaceuticals; communications equipment; comput-ers/office equipment; healthcare equipment/suppliers; and semiconductors/semiconductor equipment.This selection derives directly from the OECD definition of high-technology sectors (OECD 2011).

EXTERNAL LABOR MARKET’S EFFECT ON EXECUTIVE GENDER PAY GAP 139

reported in the proxy statements required by the U.S. Securities andExchange Commission (SEC). The percentage of women among top execu-tives is also estimated using ExecuComp. Biographical information (includ-ing whether hiring was from the internal or the external labor market) oneach executive is obtained from the annual meeting proxy statements orForm 10-K, which are filed with the SEC. The SEC requires firms to followstrict format guidelines, producing a high level of consistency across reports.Regarding other firm-level variables, performance data (return on assets)and firm size (number of employees) come from Form 10-K’s financialinformation.

As a result of this selection process, data availability constraints (missingdata for one or more variables regarding organizational practices or person-nel information for executives), and the elimination of two outlier observa-tions (two CEOs whose total direct compensation is zero), our final sampleincludes 2,600 executive-year observations (814 unique individuals) from atotal of 105 high-technology firms for the period 2006 to 2011 (with a maxi-mum of five-year observations for each firm).

Measures

Dependent Variables

‘‘Total direct compensation’’ derives from the measure reported as TDC2by ExecuComp. TDC2 represents ex post total compensation consisting ofsalary, bonus, other annual compensation, total value of restricted stockgrants, long-term incentive payouts, all other compensation, and the valueof options exercised. This measure appears in thousands of 2011 constantdollars. We use a logarithmic transformation of TDC2 to account for itsskewed distribution. To estimate the two dependent variables useful for test-ing Hypotheses 2 and 3, we disaggregate total direct compensation into twoforms of pay: ‘‘base salary,’’ which is the part of TDC2 that does not dependon the individual’s job performance, and ‘‘variable pay,’’ which includes theremaining components of TDC2 (bonus, other annual compensation, totalvalue of restricted stock grants, and so forth). We also take these variables inthousands of 2011 constant dollars and use their logarithmic transformation.

Independent Variables

The first independent variable used in the regression analysis is ‘‘femaleexecutive,’’ measured by a dummy variable that assumes value 1 if the exec-utive is female, and 0 otherwise. Then, we include in the models anotherindependent variable called ‘‘executive hired through the ELM,’’ coded asa dummy variable with value 1 when the executive (male or female) washired externally. These executives remain coded as an external hire in sub-sequent years, which allows us to compare the compensation with the exec-utives who reached the TMT position through internal promotion. ‘‘Female

140 ILR REVIEW

executive hired through the ELM’’ is the main variable, an interactionbetween the two previously described values.

Finally, to test Hypothesis 3, three independent variables concerningwomen’s representation are included: ‘‘percentage of women in the topmanagement team,’’ ‘‘percentage of women on the board,’’ and ‘‘femaleCEO,’’ which is a dummy variable taking value 1 when the CEO is a woman,and 0 otherwise.

Control Variables

We control for several individual and firm-level variables that may influenceexecutive compensation. Concerning human capital, we consider four attri-butes: ‘‘occupation title,’’ ‘‘age,’’ ‘‘firm tenure,’’ and ‘‘job tenure.’’ We con-struct occupational categories based on the annual title variable inExecuComp. More than 13,100 unique occupation titles are in this data-base, and many of these titles represent similar occupations. Based on previ-ous studies (Bertrand and Hallock 2001; Munoz-Bullon 2010), we construct11 broad occupational titles: chief executive officer (CEO)/chair, vice chair,president, chief financial officer (CFO), chief operating officer (COO),other chief officers, executive vice president, senior vice president, groupvice president, vice president, and other occupations. These occupationaltitles are operationalized as dummy variables that take value 1 when theexecutive occupied such a function, and 0 otherwise. We also include exec-utives’ age, firm tenure (number of years at their firm of employment), andjob tenure (number of years in the current occupation) as proxies for expe-rience that affect compensation (Munoz-Bullon 2010; Kulich et al. 2011).Information related to other human capital variables (e.g., education, expe-rience in the industry, total number of companies for which the executivehas worked) is not reported consistently for a large portion of the sample,so we omit it from the analysis.

Executive pay is a function of firm size, which in turn has been proxiedby various measures (Renner, Rives, and Bowlin 2002). We have operation-alized ‘‘firm size’’ as the logarithm of the number of employees. Finally, ifmanagers are paid for performance, compensation should increase as prof-itability rises (Munoz-Bullon 2010). To control for firm performance, weuse return on assets (ROA).

Gender pay differences may be reduced in companies that implementdiversity practices to promote a diverse workplace, enhancing perceptionsof organizational justice and inclusion (Reskin and McBrier 2000; Kalevet al. 2006). Thus, we include controls for six organizational practices: theexistence of a diversity and equal opportunity policy, the promotion of posi-tive discrimination, the existence of a work–life balance policy, the provisionof flexible working hours that promote work–life balance, support foremployee skill training or career development, and the provision of regularstaff and business management training for managers. These variables are

EXTERNAL LABOR MARKET’S EFFECT ON EXECUTIVE GENDER PAY GAP 141

included in the ASSET4 ESG database in terms of yes/no descriptions. Wecode the variables 1 when the practice is present in a firm (yes), and 0otherwise.

We apply the generalized estimating equation (GEE) regression method,which is particularly suited to control for firm heterogeneity. The GEE algo-rithm accounts for correlation between records within the same cluster(data collected about the same firm during successive periods of time), thusproviding improved standard error estimates and more efficient parameterestimators than fixed- and random-effects models (Liang and Zeger 1986;Zorn 2001; Castilla 2007). The GEE approach is less computationally inten-sive than either fixed effects or random effects. Therefore, it often provesless subject to instability and convergence problems.

Results

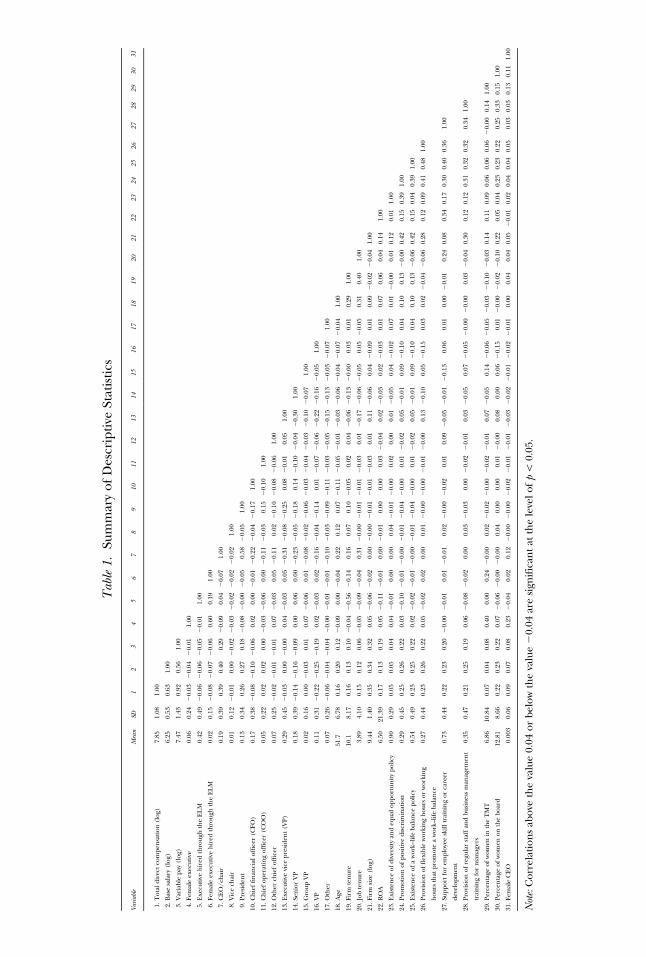

Table 1 reports descriptive statistics (mean, standard deviations, and corre-lations) for the variables used in the analyses.

Concerning women’s representation in top executive positions, 64 out of814 executives in the sample (7.86%) are female. Female executives repre-sent 174 out of 2,600 executive-year observations in the study (6.69%). Weobtained information for 2,564 executive observations related to the labormarket used to recruit them (174 female and 2,390 male executives). Outof 167 firms in the sample, 48 have at least one woman in their TMTs(28.74% of the sample). Only four women are CEOs in this sample, consis-tent with the known number in this sector. The ELM was used to hire38.50% of all female executives compared with 42.34% of male executives.This tendency has been changing in recent years as ELM career strategiesgrow in importance. We have identified 253 new executive recruitments inour database over the past six years: 13 out of 25 new female executives(52.00%) were recruited externally, compared with 150 out of 228 newmale executives (65.79%). In absolute values, the mean of variable pay is$4,340,700 compared with a base salary mean of $593,800. The substantiveamount of variable compensation validates the significance of the gendergap in this component.

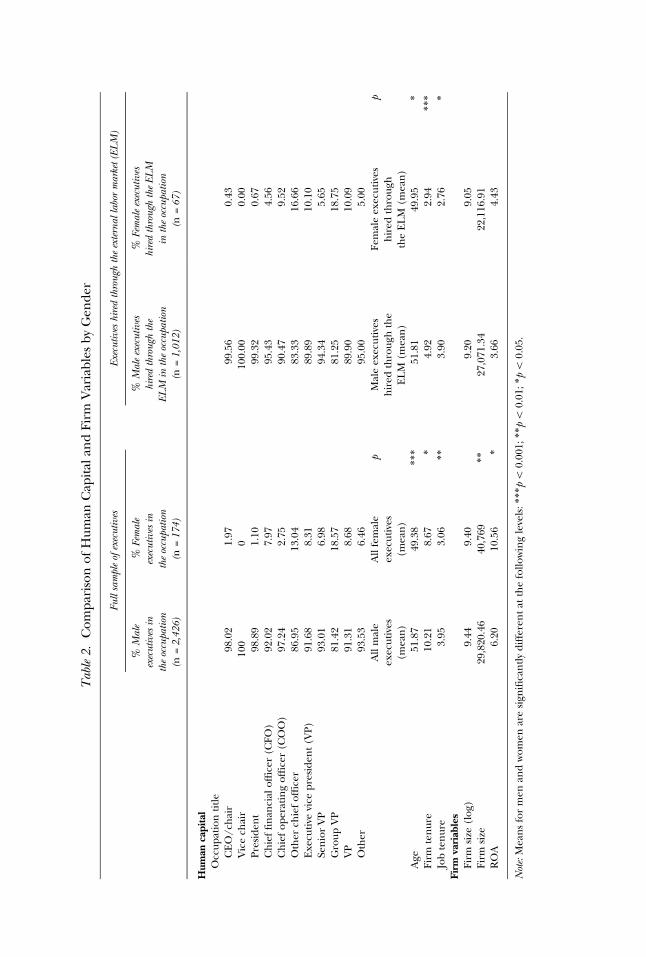

Table 2 presents descriptive statistics regarding gender differences inhuman capital, as well as firm size and profitability, first for the full sampleand then for the subsample of externally recruited executives. Concerningthe share of women in each occupation, the low proportion of women inthe top three occupational categories (CEO/chair, vice chair, and presi-dent) is remarkable. Women in the sample and the subsample were abouttwo years younger than the men, had about two fewer years of seniority inthe firms, and had one fewer year in the current position. The difference inindividual characteristics is small but statistically significant, so these mightrelate to the gender gap. Female executives work in significantly larger firmsthan their male counterparts do (in terms of number of employees).

142 ILR REVIEW

Tab

le1.

Sum

mar

yof

Des

crip

tive

Stat

isti

cs

Vari

able

Mea

nSD

12

34

56

78

910

1112

1314

1516

1718

1920

2122

2324

2526

2728

2930

31

1.T

otal

dire

ctco

mpe

nsa

tion

(log

)7.

851.

081.

00

2.B

ase

sala

ry(l

og)

6.25

0.53

0.63

1.00

3.V

aria

ble

pay

(log

)7.

471.

430.

920.

561.

00

4.Fe

mal

eex

ecut

ive

0.06

0.24

20.

032

0.04

20.

011.

00

5.E

xecu

tive

hir

edth

roug

hth

eE

LM

0.42

0.49

20.

062

0.06

20.

052

0.01

1.00

6.Fe

mal

eex

ecut

ive

hir

edth

roug

hth

eE

LM

0.02

0.15

20.

082

0.07

20.

060.

600.

191.

00

7.C

EO

/ch

air

0.19

0.39

0.39

0.40

0.29

20.

090.

042

0.07

1.00

8.V

ice

chai

r0.

010.

122

0.01

0.00

20.

022

0.03

20.

022

0.02

20.

021.

00

9.Pr

esid

ent

0.13

0.34

0.26

0.27

0.18

20.

082

0.00

20.

050.

582

0.05

1.00

10.C

hie

ffi

nan

cial

offi

cer

(CFO

)0.

170.

382

0.08

20.

102

0.06

0.02

0.00

20.

012

0.22

20.

042

0.17

1.00

11.C

hie

fop

erat

ing

offi

cer

(CO

O)

0.05

0.22

0.02

0.02

0.00

20.

032

0.06

0.00

20.

112

0.03

0.15

20.

101.

00

12.O

ther

chie

fof

fice

r0.

070.

252

0.02

20.

012

0.01

0.07

20.

030.

052

0.11

0.02

20.

102

0.08

20.

061.

00

13.E

xecu

tive

vice

pres

iden

t(V

P)0.

290.

452

0.03

0.00

20.

000.

042

0.03

0.05

20.

312

0.08

20.

250.

082

0.01

0.05

1.00

14.S

enio

rV

P0.

180.

392

0.14

20.

162

0.09

0.00

0.06

0.00

20.

232

0.05

20.

180.

142

0.10

20.

042

0.30

1.00

15.G

roup

VP

0.02

0.16

0.00

20.

030.

010.

072

0.06

0.01

20.

082

0.02

20.

062

0.03

20.

042

0.03

20.

102

0.07

1.00

16.V

P0.

110.

312

0.22

20.

252

0.19

0.02

20.

030.

022

0.16

20.

042

0.14

0.01

20.

072

0.06

20.

222

0.16

20.

051.

00

17.O

ther

0.07

0.26

20.

062

0.04

20.

042

0.00

20.

012

0.01

20.

102

0.03

20.

092

0.11

20.

032

0.05

20.

152

0.13

20.

032

0.07

1.00

18.A

ge51

.76.

780.

160.

200.

122

0.09

0.00

20.

040.

220.

120.

072

0.11

20.

052

0.01

20.

032

0.06

20.

042

0.07

20.

041.

00

19.F

irm

ten

ure

10.1

8.17

0.16

0.13

0.10

20.

042

0.56

20.

140.

160.

070.

102

0.05

0.02

0.04

20.

062

0.13

20.

000.

030.

010.

291.

00

20.J

obte

nur

e3.

894.

100.

150.

120.

062

0.05

20.

092

0.04

0.31

20.

002

0.01

20.

012

0.03

0.01

20.

172

0.06

20.

050.

052

0.05

0.31

0.40

1.00

21.F

irm

size

(log

)9.

441.

400.

350.

340.

320.

052

0.06

20.

020.

002

0.00

20.

012

0.01

20.

030.

010.

112

0.06

0.04

20.

090.

010.

092

0.02

20.

041.

00

22.R

OA

6.50

21.3

90.

170.

130.

190.

052

0.11

20.

010.

002

0.01

0.00

0.00

0.03

20.

040.

022

0.03

0.02

20.

030.

010.

070.

060.

040.

141.

00

23.E

xist

ence

ofdi

vers

ity

and

equa

lopp

ortu

nit

ypo

licy

0.90

0.29

0.05

0.05

0.04

0.04

20.

010.

000.

000.

042

0.01

20.

000.

020.

000.

012

0.05

0.04

20.

020.

070.

012

0.00

0.01

0.12

0.01

1.00

24.P

rom

otio

nof

posi

tive

disc

rim

inat

ion

0.29

0.45

0.25

0.26

0.22

0.03

20.

102

0.01

20.

002

0.01

20.

042

0.00

0.01

20.

020.

052

0.01

0.09

20.

100.

040.

100.

132

0.00

0.42

0.15

0.39

1.00

25.E

xist

ence

ofa

wor

k–lif

eba

lan

cepo

licy

0.54

0.49

0.23

0.25

0.22

0.02

20.

022

0.01

20.

002

0.01

20.

042

0.00

0.01

20.

020.

052

0.01

0.09

20.

100.

040.

100.

132

0.06

0.42

0.15

0.04

0.39

1.00

26.P

rovi

sion

offl

exib

lew

orki

ng

hou

rsor

wor

kin

g

hou

rsth

atpr

omot

ea

wor

k–lif

eba

lan

ce

0.27

0.44

0.23

0.26

0.22

0.05

20.

020.

020.

000.

012

0.00

20.

002

0.01

20.

000.

132

0.10

0.05

20.

150.

030.

022

0.04

20.

060.

280.

120.

090.

410.

481.

00

27.S

uppo

rtfo

rem

ploy

eesk

illtr

ain

ing

orca

reer

deve

lopm

ent

0.73

0.44

0.22

0.23

0.20

20.

002

0.01

0.01

20.

010.

022

0.00

20.

020.

010.

092

0.05

20.

012

0.13

0.06

0.01

0.00

20.

010.

240.

080.

340.

170.

300.

400.

361.

00

28.P

rovi

sion

ofre

gula

rst

aff

and

busi

nes

sm

anag

emen

t

trai

nin

gfo

rm

anag

ers

0.35

0.47

0.21

0.25

0.19

0.06

20.

082

0.02

0.00

0.03

20.

030.

002

0.02

20.

010.

032

0.05

0.07

20.

052

0.00

20.

000.

032

0.04

0.30

0.12

0.12

0.31

0.32

0.32

0.34

1.00

29.P

erce

nta

geof

wom

enin

the

TM

T6.

8610

.84

0.07

0.04

0.08

0.40

0.00

0.24

20.

000.

022

0.02

20.

002

0.02

20.

010.

072

0.05

0.14

20.

062

0.05

20.

032

0.10

20.

030.

140.

110.

090.

060.

060.

062

0.00

0.14

1.00

30.P

erce

nta

geof

wom

enon

the

boar

d12

.81

8.66

0.22

0.23

0.22

0.07

20.

062

0.00

20.

000.

040.

000.

000.

012

0.00

0.08

0.00

0.06

20.

150.

012

0.00

20.

022

0.10

0.22

0.05

0.04

0.23

0.23

0.22

0.25

0.33

0.15

1.00

31.F

emal

eC

EO

0.00

30.

060.

090.

070.

080.

232

0.04

0.02

0.12

20.

002

0.00

20.

022

0.01

20.

012

0.03

20.

022

0.01

20.

022

0.01

0.00

0.04

0.04

0.05

20.

010.

020.

040.

040.

050.

030.

030.

130.

111.

00

Not

e:C

orre

lati

ons

abov

eth

eva

lue

0.04

orbe

low

the

valu

e2

0.04

are

sign

ific

ant

atth

ele

velo

fp\

0.05

.

Tab

le2.

Com

pari

son

ofH

uman

Cap

ital

and

Firm

Var

iabl

esby

Gen

der

Full

sam

ple

ofex

ecut

ives

Exec

utiv

eshi

red

thro

ugh

the

exte

rnal

labo

rm

arke

t(EL

M)

%M

ale

exec

utiv

esin

the

occu

patio

n(n

=2,

426)

%Fe

mal

eex

ecut

ives

inth

eoc

cupa

tion

(n=

174)

%M

ale

exec

utiv

eshi

red

thro

ugh

the

ELM

inth

eoc

cupa

tion

(n=

1,01

2)

%Fe

mal

eex

ecut

ives

hire

dth

roug

hth

eEL

Min

the

occu

patio

n(n

=67

)

Hum

anca

pita

lO

ccup

atio

nti

tle

CE

O/c

hai

r98

.02

1.97

99.5

60.

43V

ice

chai

r10

00

100.

000.

00Pr

esid

ent

98.8

91.

1099

.32

0.67

Ch

ief

finan

cial

offi

cer

(CFO

)92

.02

7.97

95.4

34.

56C

hie

fop

erat

ing

offi

cer

(CO

O)

97.2

42.

7590

.47

9.52

Oth

erch

ief

offi

cer

86.9

513

.04

83.3

316

.66

Exe

cuti

vevi

cepr

esid

ent

(VP)

91.6

88.

3189

.89

10.1

0Se

nio

rV

P93

.01

6.98

94.3

45.

65G

roup

VP

81.4

218

.57

81.2

518

.75

VP

91.3

18.

6889

.90

10.0

9O

ther

93.5

36.

4695

.00

5.00

All

mal

eex

ecut

ives

(mea

n)

All

fem

ale

exec

utiv

es(m

ean

)

pM

ale

exec

utiv

esh

ired

thro

ugh

the

EL

M(m

ean

)

Fem

ale

exec

utiv

esh

ired

thro

ugh

the

EL

M(m

ean

)

p

Age

51.8

749

.38

***

51.8

149

.95

*

Firm

ten

ure

10.2

18.

67*

4.92

2.94

***

Job

ten

ure

3.95

3.06

**

3.90

2.76

*

Firm

vari

able

sFi

rmsi

ze(l

og)

9.44

9.40

9.20

9.05

Firm

size

29,8

20.4

640

,769

**

27,0

71.3

422

,116

.91

RO

A6.

2010

.56

*3.

664.

43

Not

e:M

ean

sfo

rm

enan

dw

omen

are

sign

ific

antl

ydi

ffer

ent

atth

efo

llow

ing

leve

ls:*

**p\

0.00

1;**p\

0.01

;*p\

0.05

.

Female executives work for companies with significantly higher accountingperformance, an important determinant of executive compensation.Analyzing the subsample of executives hired through the ELM, however, wesee no significant difference in firm size and corporate performancebetween female and male executives’ companies.

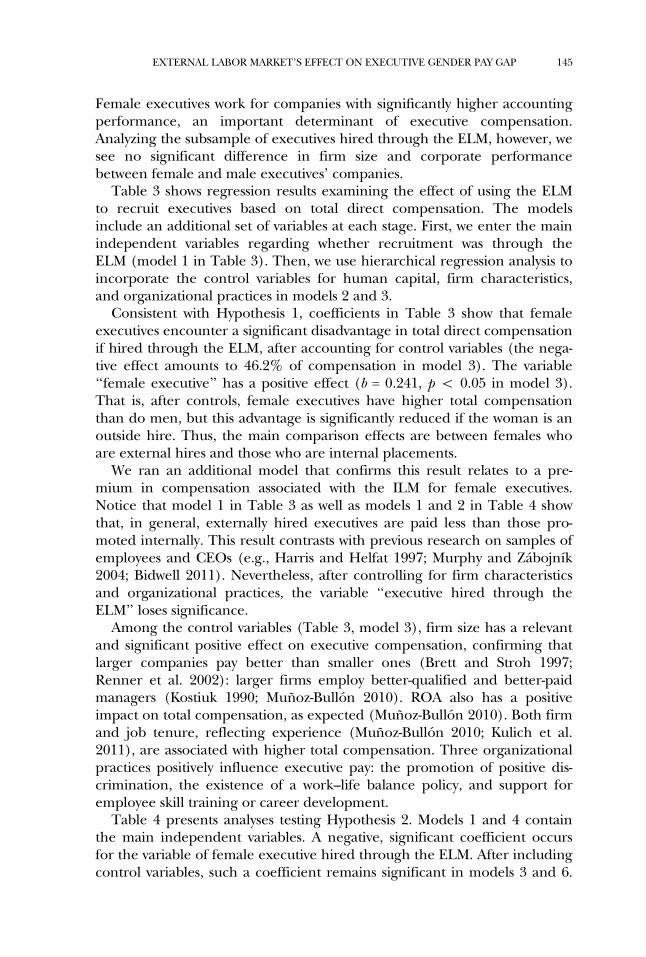

Table 3 shows regression results examining the effect of using the ELMto recruit executives based on total direct compensation. The modelsinclude an additional set of variables at each stage. First, we enter the mainindependent variables regarding whether recruitment was through theELM (model 1 in Table 3). Then, we use hierarchical regression analysis toincorporate the control variables for human capital, firm characteristics,and organizational practices in models 2 and 3.

Consistent with Hypothesis 1, coefficients in Table 3 show that femaleexecutives encounter a significant disadvantage in total direct compensationif hired through the ELM, after accounting for control variables (the nega-tive effect amounts to 46.2% of compensation in model 3). The variable‘‘female executive’’ has a positive effect (b = 0.241, p \ 0.05 in model 3).That is, after controls, female executives have higher total compensationthan do men, but this advantage is significantly reduced if the woman is anoutside hire. Thus, the main comparison effects are between females whoare external hires and those who are internal placements.

We ran an additional model that confirms this result relates to a pre-mium in compensation associated with the ILM for female executives.Notice that model 1 in Table 3 as well as models 1 and 2 in Table 4 showthat, in general, externally hired executives are paid less than those pro-moted internally. This result contrasts with previous research on samples ofemployees and CEOs (e.g., Harris and Helfat 1997; Murphy and Zabojnık2004; Bidwell 2011). Nevertheless, after controlling for firm characteristicsand organizational practices, the variable ‘‘executive hired through theELM’’ loses significance.

Among the control variables (Table 3, model 3), firm size has a relevantand significant positive effect on executive compensation, confirming thatlarger companies pay better than smaller ones (Brett and Stroh 1997;Renner et al. 2002): larger firms employ better-qualified and better-paidmanagers (Kostiuk 1990; Munoz-Bullon 2010). ROA also has a positiveimpact on total compensation, as expected (Munoz-Bullon 2010). Both firmand job tenure, reflecting experience (Munoz-Bullon 2010; Kulich et al.2011), are associated with higher total compensation. Three organizationalpractices positively influence executive pay: the promotion of positive dis-crimination, the existence of a work–life balance policy, and support foremployee skill training or career development.

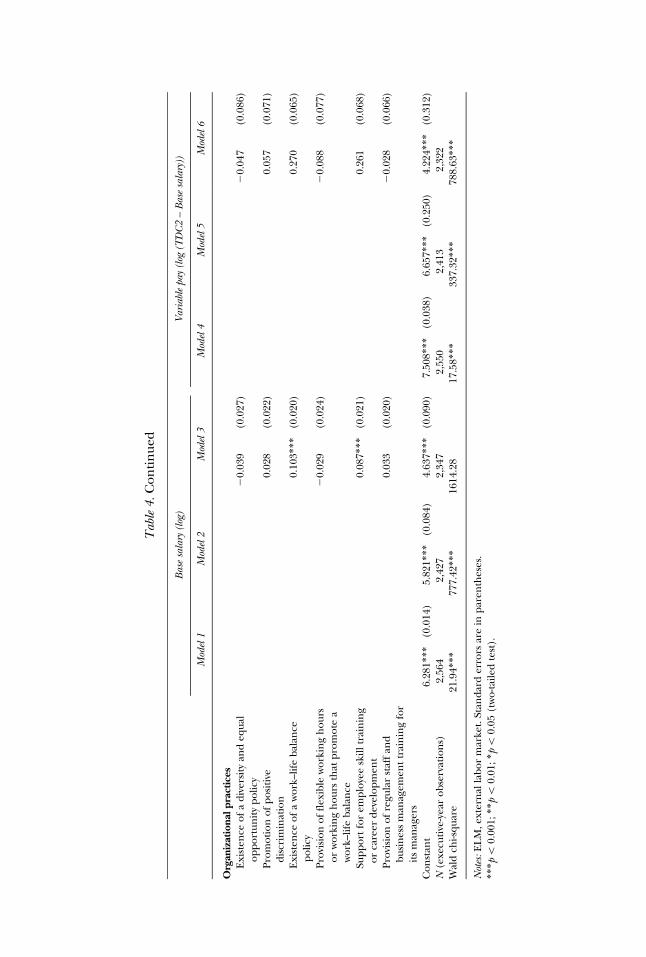

Table 4 presents analyses testing Hypothesis 2. Models 1 and 4 containthe main independent variables. A negative, significant coefficient occursfor the variable of female executive hired through the ELM. After includingcontrol variables, such a coefficient remains significant in models 3 and 6.

EXTERNAL LABOR MARKET’S EFFECT ON EXECUTIVE GENDER PAY GAP 145

Table 3. GEE Regression Results on Total Direct Compensation

Total Direct Compensation (log TDC2)

Model 1 Model 2 Model 3

Female executive 0.097 (0.107) 0.315** (0.101) 0.241* (0.093)Executive hired through the ELM 20.112* (0.044) 20.045 (0.050) 0.055 (0.047)Female executive hired through the

ELM (interaction: female executive3 executives hired through theELM)

20.587** (0.173) 20.554** (0.157) 20.462** (0.145)

Human capitalOccupation title

CEO/chair 0.834*** (0.086) 0.874*** (0.079)Vice chair 20.220 (0.161) 20.263 (0.149)President 0.031 (0.074) 0.053 (0.068)Chief financial officer (CFO) 0.025 (0.054) 0.031 (0.050)Chief operating officer (COO) 0.214* (0.101) 0.328*** (0.093)Other chief officer 0.045 (0.082) 0.142 (0.076)Executive vice president (VP) 0.018 (0.074) 20.044 (0.069)Senior VP 20.245** (0.081) 20.119* (0.075)Group VP 0.031 (0.138) 20.029 (0.127)VP 20.630*** (0.089) 20.420*** (0.082)Other 20.274** (0.095) 20.317*** (0.088)

Age 0.010** (0.003) 0.003 (0.003)Firm tenure 0.009** (0.003) 0.008*** (0.003)Job tenure 0.000 (0.005) 0.010* (0.005)

Firm variablesFirm size (log) 0.211*** (0.016)ROA 0.004*** (0.000)

Organizational practicesExistence of a diversity and equal

opportunity policy20.045 (0.060)

Promotion of positivediscrimination

0.101* (0.049)

Existence of a work–life balancepolicy

0.224*** (0.045)

Provision of flexible working hoursor working hours that promote awork–life balance

20.062 (0.053)

Support for employee skill trainingor career development

0.198*** (0.047)

Provision of regular staff andbusiness management training forits managers

20.025 (0.045)

Constant 7.897*** (0.028) 7.169*** (0.176) 5.177*** (0.216)N (executive-year observations) 2,561 2,424 2,333Wald chi-square 26.05*** 652.18*** 1309.45***

Notes: ELM, external labor market. Standard errors are in parentheses. After controls, female executiveshave higher total compensation than do men, but this advantage is significantly reduced if the womanis an outside hire. Thus, the main comparison effects are between females who are external hires andthose who are internal placements.***p \ 0.001; **p \ 0.01; *p \ 0.05 (two-tailed test).

146 ILR REVIEW

Tab

le4.

GE

ER

egre

ssio

nR

esul

tson

Bas

eSa

lary

and

Var

iabl

ePa

y

Bas

esa

lary

(log

)Va

riab

lepa

y(l

og(T

DC

2–

Bas

esa

lary

))

Mod

el1

Mod

el2

Mod

el3

Mod

el4

Mod

el5

Mod

el6

Fem

ale

exec

utiv

e2

0.02

2(0

.052

)0.

083

(0.0

48)

0.04

8(0

.042

)0.

179

(0.1

44)

0.38

5**

(0.1

43)

0.26

9*(0

.134

)E

xecu

tive

hir

edth

roug

hth

eE

LM

20.

053*

(0.0

21)

20.

053*

(0.0

24)

20.

008

(0.0

21)

20.

107

(0.0

59)

20.

053

(0.0

71)

0.07

1(0

.068

)Fe

mal

eex

ecut

ive

hir

edth

roug

hth

eE

LM

(in

tera

ctio

n:f

emal

eex

ecut

ive3

exec

utiv

esh

ired

thro

ugh

the

EL

M)

20.

205*

(0.0

84)

20.

190*

(0.0

75)

20.

142*

(0.0

66)

20.

722*

*(0

.232

)2

0.69

7**

(0.2

24)

20.

536*

(0.2

11)

Hum

anca

pita

lO

ccup

atio

nti

tle

CE

O/c

hai

r0.

402*

**

(0.0

41)

0.42

2***

(0.0

36)

0.91

3***

(0.1

23)

0.99

1***

(0.1

15)

Vic

ech

air

20.

063

(0.0

76)

20.

077

(0.0

68)

20.

371

(0.2

32)

20.

370

(0.2

19)

Pres

iden

t0.

059

(0.0

35)

0.09

5**

(0.0

31)

20.

055

(0.1

05)

20.

028

(0.0

99)

Ch

ief

finan

cial

offi

cer

(CFO

)2

0.00

1(0

.026

)0.

003

(0.0

23)

0.01

5(0

.077

)0.

029

(0.0

72)

Ch

ief

oper

atin

gof

fice

r(C

OO

)0.

037

(0.0

48)

0.08

6*(0

.042

)0.

147

(0.1

42)

0.31

3*(0

.135

)O

ther

chie

fof

fice

r0.

030

(0.0

39)

0.07

2*(0

.034

)0.

077

(0.1

16)

0.22

3*(0

.110

)E

xecu

tive

vice

pres

iden

t(V

P)0.

023

(0.0

35)

20.

016

(0.0

31)

0.07

9(0

.106

)0.

019

(0.0

99)

Sen

ior

VP

20.

158*

**

(0.0

38)

20.

093*

*(0

.034

)2

0.21

4(0

.115

)2

0.04

7(0

.108

)G

roup

VP

20.

095

(0.0

65)

20.

126*

(0.0

57)

0.14

8(0

.194

)0.

097

(0.1

82)

VP

20.

348*

**

(0.0

42)

20.

238*

**

(0.0

37)

20.

681*

**

(0.1

26)

20.

418*

**

(0.1

19)

Oth

er2

0.08

0(0

.045

)2

0.09

7*(0

.040

)2

0.25

9(0

.135

)2

0.28

8*(0

.127

)A

ge0.

008*

**

(0.0

01)

0.00

4**

(0.0

01)

0.01

3*(0

.004

)0.

005

(0.0

04)

Firm

ten

ure

0.00

0(0

.001

)2

0.00

1(0

.001

)0.

005

(0.0

04)

0.00

8(0

.004

)Jo

bte

nur

e0.

001

(0.0

02)

0.00

7**

(0.0

02)

20.

018*

(0.0

07)

20.

008

(0.0

07)

Firm

vari

able

sFi

rmsi

ze(l

og)

0.12

4***

(0.0

07)

0.25

5***

(0.0

23)

RO

A0.

000*

(0.0

00)

0.00

7***

(0.0

01)

(con

tinue

d)

Tab

le4.

Con

tin

ued

Bas

esa

lary

(log

)Va

riab

lepa

y(l

og(T

DC

2–

Bas

esa

lary

))

Mod

el1

Mod

el2

Mod

el3

Mod

el4

Mod

el5

Mod

el6

Org

aniz

atio

nalp

ract

ices

Exi

sten

ceof

adi

vers

ity

and

equa

lop

port

unit

ypo

licy

20.

039

(0.0

27)

20.

047

(0.0

86)

Prom

otio

nof

posi

tive

disc

rim

inat

ion

0.02

8(0

.022

)0.

057

(0.0

71)

Exi

sten

ceof

aw

ork–

life

bala

nce

polic

y0.

103*

**

(0.0

20)

0.27

0(0

.065

)

Prov

isio

nof

flex

ible

wor

kin

gh

ours

orw

orki

ng

hou

rsth

atpr

omot

ea

wor

k–lif

eba

lan

ce

20.

029

(0.0

24)

20.

088

(0.0

77)

Supp

ort

for

empl

oyee

skill

trai

nin

gor

care

erde

velo

pmen

t0.

087*

**

(0.0

21)

0.26

1(0

.068

)

Prov

isio

nof

regu

lar

staf

fan

dbu

sin

ess

man

agem

ent

trai

nin

gfo

rit

sm

anag

ers

0.03

3(0

.020

)2

0.02

8(0

.066

)

Con

stan

t6.

281*

**

(0.0

14)

5.82

1***

(0.0

84)

4.63

7***

(0.0

90)

7.50

8***

(0.0

38)

6.65

7***

(0.2

50)

4.22

4***

(0.3

12)

N(e

xecu

tive

-yea

rob

serv

atio

ns)

2,56

42,

427

2,34

72,

550

2,41

32,

322

Wal

dch

i-squ

are

21.9

4***

777.

42***

1614

.28

17.5

8***

337.

32***

788.

63***

Not

es:E

LM

,ext

ern

alla

bor

mar

ket.

Stan

dard

erro

rsar

ein

pare

nth

eses

.***

p\

0.00

1;**p\

0.01

;*p\

0.05

(tw

o-ta

iled

test

).

Also, the compensation penalty for female executives hired through theELM is larger for variable pay (b = 0.536) than for base salary (b = 0.142),confirming Hypothesis 2. Externally recruited women made less in variablepay than their male counterparts, even after considering occupation, age,tenure, firm characteristics, and organizational practices.

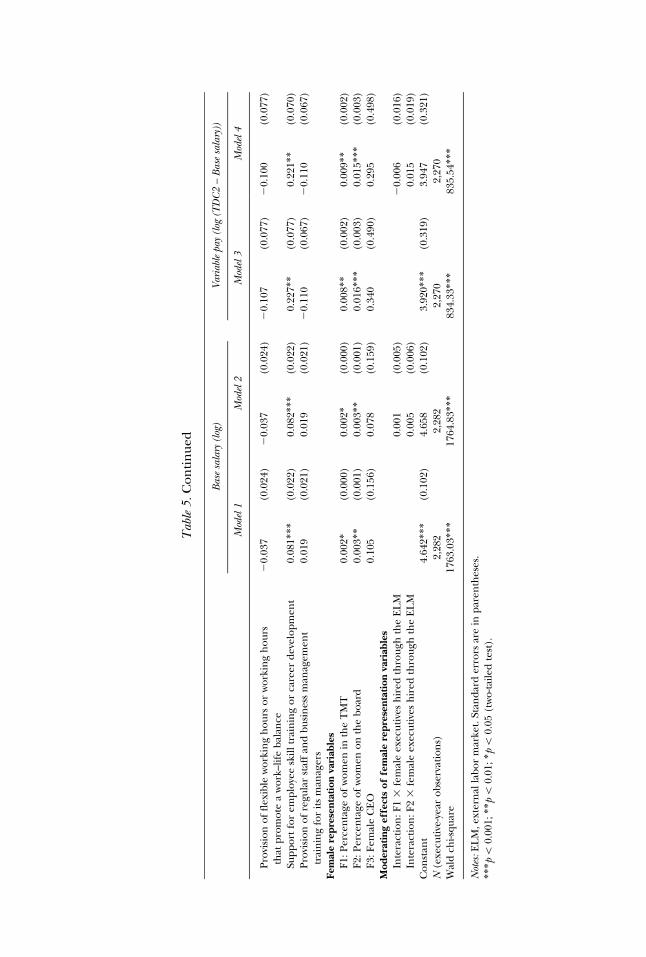

To test Hypothesis 3, we conduct regression analyses relating women’srepresentation in top executive levels to base salary and variable compensa-tion. The results appear in Table 5.

The gender penalty for female executives hired through the ELM losessignificance for base salary (see model 1) and is reduced for variable com-pensation, but remains significant after the inclusion of female representa-tion. (The gap falls by about 20%, from 20.536 to 20.446 as model 3 inTable 5 shows.) For fixed and variable components of compensation, onlytwo practices have a statistically significant effect on variable pay: the exis-tence of a work–life balance policy and support for employee skill trainingor career development. Models 2 and 4 in Table 5 include the interactionterms between the significant variables related to female representation(the percentage of women in the TMT and on the board) and female exec-utives hired through the ELM. The results indicate that such interactionsare not statistically significant. Hence, women’s representation variables donot seem to have a moderating effect.

To understand these results better, we run supplementary analyses thatoffer suggestive evidence for Hypothesis 3. As shown in Table 6, we separatethe base salary and variable pay of executives recruited through the ELM bygender. This exploration offers a more accurate and direct analysis abouthow the different measures of representation of women in top positionsseparately influence the variable compensation for men and women. Forexternally hired executives, the presence of women on the board has a sig-nificant impact on the base salary of both women and men. Nevertheless,the value of the coefficients is very close to zero. Note that for the variablepay of externally recruited female executives, the coefficient of the percent-age of women in the TMT is positive and significant. By contrast, the per-centage of women in the TMT and as CEO have a negative and significantinfluence on compensation for their male counterparts. Consistent withHypothesis 3, a higher level of female representation in top positions mayrepresent a useful mechanism to reduce the gender gap in the compensa-tion component, for which the penalty is larger.

Finally, to check the robustness of our results, we include in all previouslyestimated models a control regarding the gender composition of the execu-tive occupations, measured by the proportion of women in each occupa-tion. This analysis should help identify whether a potential source of thedifferential treatment is the devaluation of individual women relative tomen in the same occupation (Elvira and Graham 2002). The results (avail-able on request) show that such control is not significant and does not alterour prior findings, perhaps because women are underrepresented in all

EXTERNAL LABOR MARKET’S EFFECT ON EXECUTIVE GENDER PAY GAP 149

Tab

le5.

GE

ER

egre

ssio

nR

esul

tson

Bas

eSa

lary

and

Var

iabl

ePa

y(l

og)

wit

hFe

mal

eR

epre

sen

tati

onV

aria

bles

Bas

esa

lary

(log

)Va

riab

lepa

y(l

og(T

DC

2–

Bas

esa

lary

))

Mod

el1

Mod

el2

Mod

el3

Mod

el4

Fem

ale

exec

utiv

e2

0.00

7(0

.046

)2

0.00

4(0

.046

)2

0.00

2(0

.145

)0.

002

(0.1

46)

Exe

cuti

veh

ired

thro

ugh

the

EL

M0.

000

(0.0

21)

0.00

0(0

.021

)0.

107

(0.0

68)

0.10

7(0

.068

)Fe

mal

eex

ecut

ive

hir

edth

roug

hth

eE

LM

(in

tera

ctio

n:f

emal

eex

ecut

ive

3ex

ecut

ive

hir

edth

roug

hth

eE

LM

)2

0.12

9(0

.067

)2

0.25

1(0

.165

)2

0.44

6*(0

.212

)2

0.50

5(0

.524

)

Hum

anca

pita

lO

ccup

atio

nti

tle

CE

O/c

hai

r0.

405*

**

(0.0

37)

0.40

5***

(0.0

37)

0.99

8***

(0.1

19)

0.99

9***

(0.1

18)

Vic

ech

air

20.

090

(0.0

72)

20.

090

(0.0

72)

20.

311

(0.2

30)

20.

312

(0.2

30)

Pres

iden

t0.

095*

*(0

.032

)0.

093*

*(0

.032

)2

0.05

2(0

.100

)2

0.05

6(0

.100

)C

hie

ffin

anci

alof

fice

r(C

FO)

0.00

5(0

.023

)0.

004

(0.0

23)

0.04

0(0

.073

)0.

039

(0.0

73)

Ch

ief

oper

atin

gof

fice

r(C

OO

)0.

079

(0.0

43)

0.07

9(0

.044

)0.

327*

(0.1

37)

0.33

5*(0

.138

)O

ther

chie

fof

fice

r0.

072*

(0.0

35)

0.07

1*(0

.035

)0.

263*

(0.1

11)

0.26

4*(0

.111

)E

xecu

tive

vice

pres

iden

t(V

P)2

0.02

0(0

.032

)2

0.02

1(0

.032

)0.

031

(0.1

01)

0.02

9(0

.101

)Se

nio

rV

P2

0.09

7**

(0.0

35)

20.

097*

*(0

.035

)2

0.01

3(0

.110

)2

0.01

5(0

.110

)G

roup

VP

20.

149*

(0.0

58)

20.

151*

(0.0

58)

0.05

0(0

.183

)0.

047

(0.1

83)

VP

20.

227*

**

(0.0

38)

20.

229*

**

(0.0

38)

20.

326*

*(0

.120

)2

0.33

0**

(0.1

20)

Oth

er2

0.09

4*(0

.041

)2

0.09

4*(0

.041

)2

0.24

1(0

.128

)2

0.24

1(0

.128

)A

ge0.

004

(0.0

01)

0.00

4**

(0.0

01)

0.00

4(0

.004

)0.

004

(0.0

04)

Firm

ten

ure

20.

000

(0.0

01)

20.

000

(0.0

01)

0.01

1*(0

.004

)0.

011*

(0.0

04)

Job

ten

ure

0.00

7**

(0.0

02)

0.00

7**

(0.0

02)

20.

007

(0.0

07)

20.

007

(0.0

07)

Firm

vari

able

sFi

rmsi

ze(l

og)

0.12

6***

(0.0

07)

0.12

6***

(0.0

07)

0.26

7***

(0.0

24)

0.26

5***

(0.0

24)

RO

A0.

000*

(0.0

00)

0.00

0*(0

.000

)0.

007*

**

(0.0

01)

0.00

7***

(0.0

01)

Org

aniz

atio

nalp

ract

ices

Exi

sten

ceof

adi

vers

ity

and

equa

lopp

ortu

nit

ypo

licy

20.

043

(0.0

27)

20.

043

(0.0

27)

20.

079

(0.0

87)

20.

079

(0.0

87)

Prom

otio

nof

posi

tive

disc

rim

inat

ion

0.02

1(0

.023

)0.

022

(0.0

23)

0.03

1(0

.072

)0.

029

(0.0

72)

Exi

sten

ceof

aw

ork–

life

bala

nce

polic

y0.

102*

**

(0.0

20)

0.10

2***

(0.0

20)

0.25

7***

(0.0

65)

0.25

8***

(0.0

65)

(con

tinue

d)

Tab

le5.

Con

tin

ued

Bas

esa

lary

(log

)Va

riab

lepa

y(l

og(T

DC

2–

Bas

esa

lary

))

Mod

el1

Mod

el2

Mod

el3

Mod

el4

Prov

isio

nof

flex

ible

wor

kin

gh

ours

orw

orki

ng

hou

rsth

atpr

omot

ea

wor

k–lif

eba

lan

ce2

0.03

7(0

.024

)2

0.03

7(0

.024

)2

0.10

7(0

.077

)2

0.10

0(0

.077

)

Supp

ort

for

empl

oyee

skill

trai

nin

gor

care

erde

velo

pmen

t0.

081*

**

(0.0

22)

0.08

2***

(0.0

22)

0.22

7**

(0.0

77)

0.22

1**

(0.0

70)

Prov

isio

nof

regu

lar

staf

fan

dbu

sin

ess

man

agem

ent

trai

nin

gfo

rit

sm

anag

ers

0.01

9(0

.021

)0.

019

(0.0

21)

20.

110

(0.0

67)

20.

110

(0.0

67)

Fem

ale

repr

esen

tatio

nva

riab

les

F1:P

erce

nta

geof

wom

enin

the

TM

T0.

002*

(0.0

00)

0.00

2*(0

.000

)0.

008*

*(0

.002

)0.

009*

*(0

.002

)F2

:Per

cen

tage

ofw

omen

onth

ebo

ard

0.00

3**

(0.0

01)

0.00

3**

(0.0

01)

0.01

6***

(0.0

03)

0.01

5***

(0.0

03)

F3:F

emal

eC

EO

0.10

5(0

.156

)0.

078

(0.1

59)

0.34

0(0

.490

)0.

295

(0.4

98)

Mod

erat

ing

effe

cts

offe

mal

ere

pres

enta

tion

vari

able

sIn

tera

ctio

n:F

13

fem

ale

exec

utiv

esh

ired

thro

ugh

the

EL

M0.

001

(0.0

05)

20.

006

(0.0

16)

Inte

ract

ion

:F2

3fe

mal

eex

ecut

ives

hir

edth

roug

hth

eE

LM

0.00

5(0

.006

)0.

015

(0.0

19)

Con

stan

t4.

642*

**

(0.1

02)

4.65

8(0

.102

)3.

920*

**

(0.3

19)

3.94

7(0

.321

)N

(exe

cuti

ve-y

ear

obse

rvat

ion

s)2,

282

2,28

22,

270

2,27

0W

ald

chi-s

quar

e17

63.0

3***

1764

.83*

**

834.

33***

835.

54***

Not

es:E

LM

,ext

ern

alla

bor

mar

ket.

Stan

dard

erro

rsar

ein

pare

nth

eses

.***

p\

0.00

1;**p\

0.01

;*p\

0.05

(tw

o-ta

iled

test

).

Tab

le6.

GE

ER

egre

ssio

nR

esul

tson

Var

iabl

ePa

y(l

og)

ofE

xecu

tive

sH

ired

thro

ugh

the

EL

M

Bas

esa

lary

offe

mal

eex

ecut

ives

hire

dth

roug

hth

eEL

M

Bas

esa

lary

ofm

ale

exec

utiv

eshi

red

thro

ugh

the

ELM

Vari

able

pay

offe

mal

eex

ecut

ives

hire

dth

roug

hth

eEL

M

Vari

able

pay

ofm

ale

exec

utiv

eshi

red

thro

ugh

the

ELM

Hum

anca

pita

lO

ccup

atio

ntit

leC

EO

/ch

air

0.16

6*0.

071

0.05

5***

(0.0

15)

20.

021

(0.1

05)

1.40

3***

(0.2

93)

Vic

ech

air

—2

0.03

7(0

.032

)2

0.07

1(0

.204

)2

0.83

9(0

.570

)Pr

esid

ent

—0.

025*

(0.0

12)

0.01

8(0

.089

)2

0.29

2(0

.249

)C

hie

ffi

nan

cial

offi

cer

(CFO

)0.

000

(0.0

20)

0.00

1(0

.009

)2

0.04

5(0

.064

)0.

220

(0.1

80)

Ch

ief

oper

atin

gof

fice

r(C

OO

)0.

269*

**

(0.0

55)

20.

000

(0.0

18)

0.14

8(0

.121

)2

0.32

6(0

.339

)O

ther

chie

fof

fice

r2

0.02

3(0

.019

)0.

017

(0.0

15)

0.27

9**

(0.0

98)

20.

226

(0.2

74)

Exe

cuti

vevi

cepr

esid

ent

(VP)

0.24

4***

(0.0

47)

0.00

2(0

.013

)0.

196*

(0.0

90)

20.

386