The economic consequences of putting a price on carbon * Link to most recent version Diego R. Känzig † London Business School September, 2021 Abstract How does carbon pricing affect the economy? Is it successful at reducing emissions and how does it affect economic inequality? Exploiting institu- tional features of the European carbon market and high-frequency data, I estimate the aggregate and distributional effects of a carbon policy shock. I find that a shock tightening the carbon pricing regime leads to a significant increase in energy prices and a persistent fall in emissions. The drop in emis- sions comes at the cost of a temporary fall in economic activity, which is not borne equally across society: poorer households lower their consumption significantly while richer households are barely affected. My results suggest that targeted fiscal policy can reduce the economic costs of carbon pricing – without compromising emission reductions. JEL classification: E32, E62, H23, Q54, Q58 Keywords: Carbon pricing, cap and trade, emissions, macroeconomic effects, inequality, high-frequency identification * I am indebted to my advisor Paolo Surico, João Cocco, Elias Papaioannou, Lucrezia Reich- lin and Hélène Rey for their invaluable guidance and support. For helpful comments and sug- gestions, I thank Asger Andersen, Michele Andreolli, Juan Antolin-Diaz, Christiane Baumeis- ter, Jean-Pierre Benoît, Florin Bilbiie, James Cloyne, Martin Ellison, Luis Fonseca, Luca Fornaro, Jordi Galí, Garth Heutel, Yueran Ma, Joseba Martinez, Matthias Meier, Silvia Miranda-Agrippino, Tsvetelina Nenova, Luca Neri, Gert Peersman, Michele Piffer, Richard Portes, Sebastian Rast, Vania Stavrakeva, Nadia Zhuravleva, Nathan Zorzi as well as participants at the EEA-ESEM con- ference, the Young Economist Symposium, the IAAE conference, the Oxford NuCamp PhD Work- shop, the IAEE conference, the Ghent Workshop on Empirical Macro, the QCGBF conference, the QMUL Economics and Finance Workshop and the LBS Brownbag Seminar. I thank Mario Alloza for kindly sharing their fiscal policy shock series. I also thank the IAEE for the best student paper award. Finally, I am very grateful to the London Business School’s Wheeler Institute for Business and Development for generously supporting this research. † Contact: Diego R. Känzig, London Business School, Regent’s Park, London NW1 4SA, United Kingdom. E-mail: [email protected]. Web: diegokaenzig.com. 1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

The economic consequences of putting a priceon carbon*

Link to most recent version

Diego R. Känzig†

London Business School

September, 2021

Abstract

How does carbon pricing affect the economy? Is it successful at reducing

emissions and how does it affect economic inequality? Exploiting institu-

tional features of the European carbon market and high-frequency data, I

estimate the aggregate and distributional effects of a carbon policy shock. I

find that a shock tightening the carbon pricing regime leads to a significant

increase in energy prices and a persistent fall in emissions. The drop in emis-

sions comes at the cost of a temporary fall in economic activity, which is not

borne equally across society: poorer households lower their consumption

significantly while richer households are barely affected. My results suggest

that targeted fiscal policy can reduce the economic costs of carbon pricing –

without compromising emission reductions.

JEL classification: E32, E62, H23, Q54, Q58

Keywords: Carbon pricing, cap and trade, emissions, macroeconomic effects,

inequality, high-frequency identification

*I am indebted to my advisor Paolo Surico, João Cocco, Elias Papaioannou, Lucrezia Reich-lin and Hélène Rey for their invaluable guidance and support. For helpful comments and sug-gestions, I thank Asger Andersen, Michele Andreolli, Juan Antolin-Diaz, Christiane Baumeis-ter, Jean-Pierre Benoît, Florin Bilbiie, James Cloyne, Martin Ellison, Luis Fonseca, Luca Fornaro,Jordi Galí, Garth Heutel, Yueran Ma, Joseba Martinez, Matthias Meier, Silvia Miranda-Agrippino,Tsvetelina Nenova, Luca Neri, Gert Peersman, Michele Piffer, Richard Portes, Sebastian Rast,Vania Stavrakeva, Nadia Zhuravleva, Nathan Zorzi as well as participants at the EEA-ESEM con-ference, the Young Economist Symposium, the IAAE conference, the Oxford NuCamp PhD Work-shop, the IAEE conference, the Ghent Workshop on Empirical Macro, the QCGBF conference, theQMUL Economics and Finance Workshop and the LBS Brownbag Seminar. I thank Mario Allozafor kindly sharing their fiscal policy shock series. I also thank the IAEE for the best student paperaward. Finally, I am very grateful to the London Business School’s Wheeler Institute for Businessand Development for generously supporting this research.

†Contact: Diego R. Känzig, London Business School, Regent’s Park, London NW1 4SA, UnitedKingdom. E-mail: [email protected]. Web: diegokaenzig.com.

1

1. Introduction

Climate change is one of the greatest challenges of our time, posing significantthreats not only to our lives, livelihoods and the environment, but also to theglobal economy. Fighting climate change, however, has proved very difficult be-cause of its global nature and the pervasive externalities involved. As the threatsof a climate crisis are becoming more acute and visible, climate change is now akey priority for policymakers around the world. There is broad agreement thatputting a price on carbon emissions is the most effective way to mitigate climatechange and several countries have enacted national carbon pricing policies, eithervia carbon taxes or cap and trade systems. Yet, little is known about the economiceffects of such policies. While arguably beneficial in the longer term, there couldbe short-term economic costs and important distributional consequences.

This paper aims to contribute filling this gap. I propose a novel approach toestimate the dynamic causal effects of a carbon policy shock, exploiting institu-tional features of the European carbon market and high-frequency data. The Eu-ropean Union Emissions Trading System (EU ETS) is the largest and oldest carbonmarket in the world, accounting for around 40 percent of the EU’s greenhousegas (GHG) emissions. The market was established in phases and the regulationshave been updated continuously. Following an event study approach, I collected113 regulatory update events concerning the supply of emission allowances. Bymeasuring the change in the carbon futures price in a tight window around theregulatory news, I am able to isolate a series of carbon policy surprises. Reversecausality can be plausibly ruled out as economic conditions are known and pricedby the market prior to the regulatory news and unlikely to change within the tightwindow. Using the surprise series as an instrument, I estimate the aggregate anddistributional effects of a structural carbon policy shock.

I find that carbon pricing has significant effects on emissions and the econ-omy. A carbon policy shock tightening the carbon pricing regime causes a strong,immediate increase in energy prices and a persistent fall in overall GHG emis-sions. Thus, carbon pricing turns out to be successful in achieving its goal ofreducing emissions. However, this does not come without cost. Consumer pricesrise significantly and economic activity falls, which is reflected in lower outputand higher unemployment. Crucially, the fall in activity appears to be somewhatless persistent than the fall in emissions – improving the emissions intensity inthe longer term. The stock market falls for about one and a half years but thenrebounds and turns positive after. The euro depreciates in real terms and importsfall significantly. While the shock leads to somewhat heightened financial un-

2

certainty and a short-term deterioration of financial conditions, the main trans-mission channel appears to work through higher carbon prices, which passingthrough energy prices leads to lower consumption and investment. At the sametime, carbon pricing creates an incentive for green innovation, causing a signifi-cant uptick in low-carbon patenting.

Carbon policy shocks have also contributed meaningfully to historical varia-tions in prices, emissions and macroeconomic aggregates. Importantly, however,they did not account for the fall in emissions associated with the global financialcrisis – supporting the validity of the identified shock.

My results illustrate that carbon pricing is successful at reducing emissionsand mitigating climate change. However, this comes at the cost of lower eco-nomic activity today. Importantly, these costs are not equally distributed acrosssociety. Using detailed household-level data, I document pervasive heterogene-ity in the expenditure response to carbon policy shocks. While the expenditureof higher-income households only falls marginally, low-income households re-duce their expenditure significantly and persistently. These households are morehardly affected in two ways. First, they spend a larger share of their dispos-able income on energy and thus the higher energy bill leaves significantly lessresources for other expenditures. Second, they also experience the largest fall inincome, as they tend to work in sectors that are more exposed to carbon pricing.Crucially, the estimated magnitudes are much larger than what can be accountedfor by the direct effect through energy prices alone – pointing to an importantrole of indirect, general equilibrium effects via income and employment.

These findings suggest that targeted fiscal policies could be an effective wayto reduce the economic costs of carbon pricing. To the extent that energy demandis inelastic, which turns out to be the case especially for poorer households, thisshould not compromise the reductions in emissions. I also show that carbon pric-ing leads to a significant fall in the support of climate-related policies amonglow-income households. Thus, such targeted compensations may also help toincrease the public support of such policies.

A comprehensive series of sensitivity checks indicate that the results are ro-bust along a number of other dimensions including the selection of event dates,the estimation technique, the model specification, and the sample period. Im-portantly, the results are also robust to accounting for confounding news over theevent window. Controlling for such background noise using an heteroskedasticity-based estimator produces very similar results, even though the responses are a bitless precisely estimated.

3

Related literature and contribution. This paper is related to a growing litera-ture studying the effects of climate policy and carbon pricing in particular. Whilethere is mounting evidence on the effectiveness of such policies for emission re-ductions (Lin and Li, 2011; Martin, De Preux, and Wagner, 2014; Andersson, 2019;Pretis, 2019), less is known about the economic effects. A number of studies haveanalyzed the macroeconomic effects of the British Columbia carbon tax, findingno significant impacts on GDP (Metcalf, 2019; Bernard, Kichian, and Islam, 2018).Metcalf and Stock (2020a,b) study the macroeconomic impacts of carbon taxes inEuropean countries. They find no robust evidence of a negative effect of the taxon employment or GDP growth.1 In contrast, theoretical studies based on com-putable general equilibrium models tend to find contractionary output effects(see e.g. McKibbin, Morris, and Wilcoxen, 2014; McKibbin et al., 2017; Goulderand Hafstead, 2018). By way of summary, the existing evidence on the economiceffects of carbon pricing is still scarce and inconclusive. I contribute to this litera-ture by providing new estimates for the macroeconomic impact based on the EUETS, the largest carbon market in the world.

A large literature has studied the macroeconomic effects of discretionary taxchanges more generally. To address the endogeneity of tax changes, the litera-ture has used SVAR techniques (Blanchard and Perotti, 2002) and narrative meth-ods (Romer and Romer, 2010). The narrative approach in particular points tolarge macroeconomic effects of tax changes; a tax increase leads to a significantand persistent decline of output and its components (see also Mertens and Ravn,2013; Cloyne, 2013). However, it is unclear how much we can learn from theseestimates with respect to carbon pricing, which is enacted to correct a clear exter-nality and not because of past decisions or ideology. While the motivation behindcarbon pricing is arguably long-term and thus more likely unrelated to the cur-rent state of the economy – similar to the tax changes considered in Romer andRomer (2010) – it is still perceivable that regulatory decisions also take economicconditions into account.

To address this potential endogeneity in carbon pricing, I propose a novelidentification strategy exploiting high-frequency variation. From a methodologi-cal viewpoint, my approach is closely related to the literature on high-frequencyidentification, which has been developed in the monetary policy setting (Kuttner,2001; Gürkaynak, Sack, and Swanson, 2005; Gertler and Karadi, 2015; Nakamuraand Steinsson, 2018, among others) and more recently employed in the global oil

1Contrary to this paper, Metcalf and Stock (2020a,b) do not study the effects of the EU ETS butnational carbon taxes, which are present in many European countries and cover sectors that arenot included in the EU ETS.

4

market context (Känzig, 2021). In this literature, policy surprises are identified us-ing high-frequency asset price movements around policy events, such as FOMCor OPEC announcements. The idea is to isolate the impact of policy news by mea-suring the change in asset prices in a tight window around the announcements.I contribute to this literature by extending the high-frequency identification ap-proach to climate policy, exploiting institutional features of the European carbonmarket.

This paper is not the first to study regulatory news in the European carbonmarket. A number of studies have used event study techniques to analyze theeffects of regulatory news on carbon, energy and stock prices (Mansanet-Batallerand Pardo, 2009; Fan et al., 2017; Bushnell, Chong, and Mansur, 2013, amongothers). To the best of my knowledge, however, this paper is the first to exploitthese regulatory updates to analyze the economic effects of carbon pricing. Theapproach is very general and could also be employed to evaluate the performanceof other cap and trade systems.

Equipped with this novel identification strategy, I provide new direct ev-idence not only on the aggregate but also on the distributional consequencesof carbon pricing. There is growing consensus that a sustainable transition toa low-carbon economy has to be fair and equitable (see e.g. European Comis-sion, 2021). Therefore, it is crucial to understand how carbon pricing affectseconomic inequality. I find that carbon pricing in the EU has been more regres-sive than commonly thought, burdening lower-income households substantiallymore than richer ones. This stands in contrast to existing studies, which tendto find a more modest regressive impact (Beznoska, Cludius, and Steiner, 2012;Ohlendorf et al., 2021). My findings illustrate the importance of accounting forindirect, general-equilibrium effects via income and employment; solely focus-ing on the direct effects via higher energy prices can massively understate theactual distributional impact. Finally, I show that the distributional consequencesdo not only matter for inequality but also for the transmission of the policy to themacroeconomy.

Roadmap. The paper proceeds as follows. In the next section, I provide somebackground information on the European carbon market and detail relevant reg-ulatory events in this market. In Section 3, I discuss the high-frequency identifica-tion strategy and perform some diagnostic checks on the carbon policy surpriseseries. Section 4 discusses the econometric approach and introduces the exter-nal and internal instrument models. Section 5 presents the results on the aggre-gate effects of carbon pricing. I start by analyzing the instrument strength before

5

studying the effects on emissions and the macroeconomy, the historical impor-tance and potential propagation channels. Section 6 looks into the heterogeneouseffects of carbon pricing, using detailed household-level data on income and ex-penditure. I analyze the distributional impact, how heterogeneity matters for thetransmission and end with some policy implications. In Section 7, I perform anumber of robustness checks. Section 8 concludes.

2. The European carbon market

The European emissions trading system is the cornerstone of the EU’s policy tocombat climate change. It is the largest carbon market in the world and also hasone of the longest implementation histories. Established in 2005, it covers morethan 11,000 heavy energy-using installations and airlines, accounting for around40 percent of the EU’s greenhouse gas emissions.

The market operates under the cap and trade principle. Different from a car-bon tax, a cap is set on the total amount of certain greenhouse gases that can beemitted by installations covered by the system. The cap is reduced over time sothat total emissions fall. Within the cap, emission allowances are auctioned off orallocated for free among the companies in the system, and can subsequently betraded. Alternatively, companies can also use limited amounts of internationalcredits from emission-saving projects around the world. Regulated companiesmust monitor and report their emissions. Each year, the companies must surren-der enough allowances to cover all their emissions. This is enforced with heavyfines. If a company reduces its emissions, it can keep the spare allowances tocover its future needs or sell them to another company that is short of allowances.A binding limit on the total number of allowances available in the system guar-antees a positive price on carbon (see European Comission, 2020a, for more infor-mation).

There exist several organized markets where EU emission allowances (EUAs)can be traded. An EUA is defined as the right to emit one ton of carbon diox-ide equivalent gas and is traded in spot markets such as Bluenext (Paris), EEX(Leipzig) or Nord Pool (Oslo). Furthermore, there exist also liquid futures mar-kets on EUAs, such as the EEX and ICE (London). In 2018, the cumulative trad-ing volume in the relevant futures and spot markets was about 10 billion EUA(DEHSt, 2019).

A brief history of the EU ETS. The development of the EU ETS has been di-vided into different phases. The evolution of the carbon price over the phases of

6

the system is depicted in Figure 1. The first phase lasted three years, from 2005 to2007. This period was a pilot phase to prepare for phase two, where the systemhad to run efficiently to help the EU meet its Kyoto targets. In this initial phase,almost all allowances were freely allocated at the national level. In absence of reli-able emissions data, phase one caps were set on the basis of estimates. In 2007, thecarbon price fell significantly as it became apparent that the total amount of al-lowances issued exceeded total emissions significantly, and eventually convergedto zero as phase one allowances could not be transferred to phase two.

Figure 1: The carbon price in the EU

Notes: The EUA price, as measured by the price of the first EUA futures contractover the different phases of the EU ETS.

The second phase ran from 2008 until 2012, coinciding with the first commit-ment period of the Kyoto Protocol where the countries in the EU ETS had con-crete emission targets to meet. Because verified annual emissions data from thepilot phase was now available, the cap on allowances was reduced in phase two,based on actual emissions. The proportion of free allocation fell slightly, severalcountries started to hold auctions, and businesses were allowed to buy a limitedamount of international credits. The commission also started to extend the sys-tem to cover more gases and sectors; in 2012 the aviation sector was included,even though this only applies for flights within the European Economic Area.Despite these changes, EU carbon prices remained at moderate levels. This wasmainly because the 2008 economic crisis led to emissions reductions that weregreater than expected, which in turn led to a large surplus of allowances andcredits weighing down prices.

The subsequent third phase began in 2013 and ran until the end of 2020.Learning from the lessons of the previous phases, the system was changed sig-nificantly in a number of key respects. In particular, the new system relies on asingle, EU-wide cap on emissions in place of the previous national caps, auction-

7

ing became the default method for allocating allowances instead of the previousfree allocation and harmonized allocation rules apply to the allowances still allo-cated for free, and the system covers more sectors and gases, in particular nitrousoxide and perfluorocarbons in addition to carbon dioxide. In 2014, the Commis-sion postponed the auctioning of 900 million allowances to address the surplus ofemission allowances that has built up since the Great Recession (‘back-loading’).Later, the Commission introduced a market stability reserve, which started oper-ating in January 2019. This reserve has the aim to reduce the current surplus ofallowances and improve the system’s resilience to major shocks by adjusting thesupply of allowances to be auctioned. To this end, the back-loaded allowanceswere transferred to the reserve rather than auctioned in the last years of phasethree and unallocated allowances were transferred to the reserve as well.

The current, fourth phase spans the period from 2021 to 2030. The legislativeframework for this trading period was revised in early 2018. In order to achievethe EU’s 2030 emission reduction targets, the pace of annual reductions in to-tal allowances is increased to 2.2 percent from the previous 1.74 percent and themarket stability reserve is reinforced to improve the EU ETS’s resilience to futureshocks. More recently, the Commission has proposed to further revise and ex-pand the scope of the EU ETS, with the aim to achieve a climate-neutral EU by2050 (see European Comission, 2020a).

Regulatory events. Given its pioneering role, the establishment of the Europeancarbon market has followed a learning-by-doing process. As illustrated above,since the start in 2005, the system has been expanded considerably and its insti-tutions and rules have been continuously updated to address issues encounteredin the market, improve market efficiency, and reduce information asymmetry andmarket distortions.

Building on the event study literature, I collected a comprehensive list of reg-ulatory events in the EU ETS. These regulatory update events can take the formof a decision of the European Commission, a vote of the European Parliament ora judgement of an European court, for instance. Of primary interest in this paperare regulatory news regarding the supply of emission allowances. Thus, I focus onnews concerning the overall cap in the EU ETS, the free allocation of allowances,the auctioning of allowances as well as the use of international credits. Goingthrough the official journal of the European Union as well as the European Com-mission Climate Action news archive, I could identify 113 such events during theperiod between 2005 and 2018. The events as well as the sources are detailed inTable A.1 in the Appendix. In the first two phases, the key events concern de-

8

cisions on the national allocation plans (NAP) of the individual member states,e.g. the commission approving or rejecting allocation plans or a court ruling incase of legal conflicts about the free allocation of allowances. With the move toauctioning as the default way of allocating allowances, decisions on the timingand quantities of emission allowances to be auctioned became the most impor-tant regulatory news in phase three. After the pilot phase of the system, therewere also a number of important events related to the use and entitlement of in-ternational credits. Finally, there are a few events on the setting of the overall capin the system.

The selection of events is a crucial factor in event studies. As the baseline, Iuse all of the identified events, however, in Section 7, I study the sensitivity of theresults with respect to different event types in detail.

Carbon futures markets. Under the EU ETS, the right to emit a particularamount of greenhouse gases becomes a tradable commodity. The most liquidmarkets to trade these emission allowances are the futures markets at the EEXand the ICE. In this paper, I focus on data from the ICE, which has been found todominate the price discovery process in the European carbon market (Stefan andWellenreuther, 2020). The ICE EUA futures are listed on a quarterly expiry cycleand are traded up to 6 quarters out. The contract size is 1,000 EUAs and deliveryis physical.

3. High-frequency identification

Since policies to fight climate change are long-term in nature, they are likelyless subject to endogeneity concerns than other fiscal polices (Romer and Romer,2010). However, to properly address the concern that regulatory decisions in thecarbon market may take economic conditions into account, I implement a high-frequency identification approach.

The institutional framework of the European carbon market provides an idealsetting in this respect. First, as discussed above, there are frequent regulatoryupdates in the market that can have significant effects on the price of emissionallowances. Second, there exist liquid futures markets for trading emission al-lowances. This motivates the idea to construct a series of carbon policy surprisesby looking at how carbon prices change around regulatory events in the carbonmarket. By measuring the price change within a sufficiently tight window aroundthe regulatory news, it is possible to isolate the impact of the regulatory decision.Reverse causality of the state of the economy can be plausibly ruled out because

9

it is known and priced prior to the decision and unlikely to change within thetight window.

To fix ideas, the carbon policy surprise series is computed by measuring thepercentage change in the EUA futures price on the day of the regulatory event tothe last trading day before the event:

CPSurpriset,d = Ft,d − Ft,d−1, (1)

where d and t indicate the day and the month of the event, respectively, and Ft,d

is the (log) settlement price of the EUA futures contract in month t on day d.Assuming that risk premia do not change over the narrow event window, we caninterpret the resulting surprise as a revision in carbon price expectations causedby the regulatory news.2

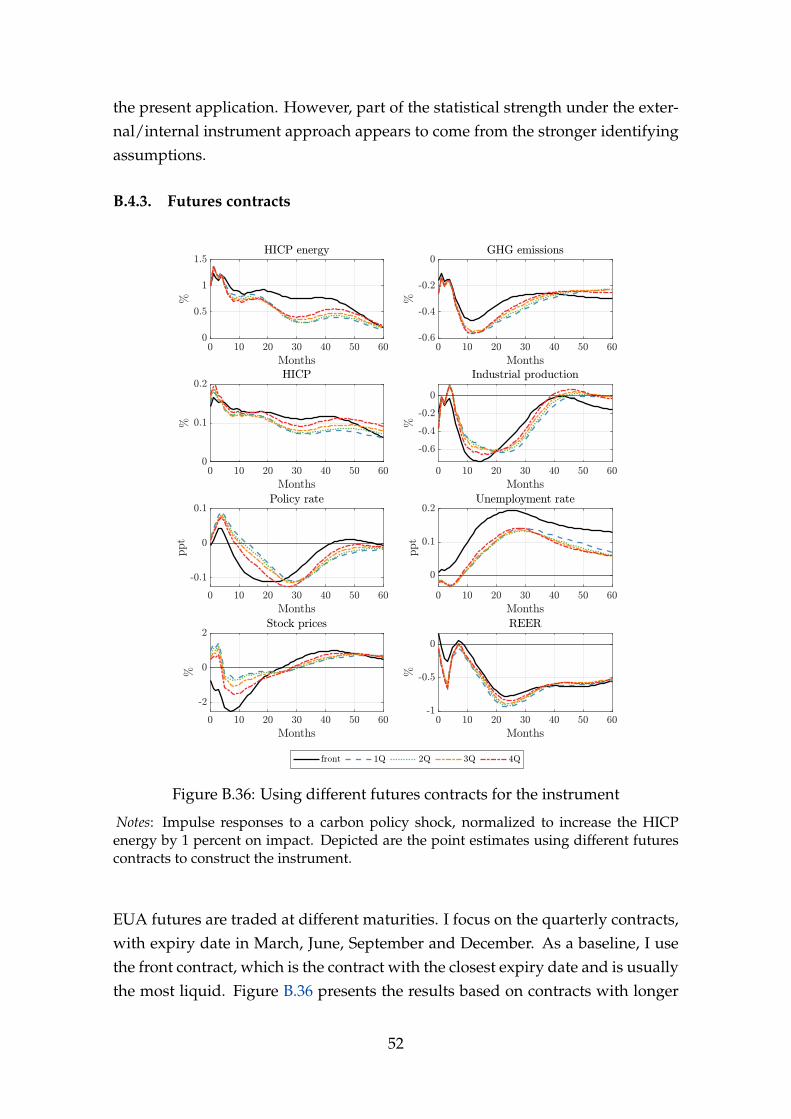

EUA futures are traded at different maturities. I focus here on the front con-tract (the contract with the closest expiry date), which is the most liquid. Im-portantly, near-dated contracts also tend to be less sensitive to risk premia thancontracts with longer maturities (Baumeister and Kilian, 2017; Nakamura andSteinsson, 2018). Thus, focusing on the front contract helps to further mitigateconcerns about time-varying risk premia.3

The daily surprises, CPSurpriset,d, are then aggregated to a monthly series,CPSurpriset, by summing over the daily surprises in a given month. In monthswithout any regulatory events, the series takes zero value.

The resulting carbon policy surprise series is shown in Figure 2. We can seethat regulatory news can have a substantial impact on carbon prices, with somenews moving prices in excess of 20 percent. In April 2007, for instance, when theCommission approved the NAPs of Austria and Hungary, carbon prices fell byaround 30 percent. Later in November, when the general court ruled on ex-postadjustments of Germany’s NAP, the carbon price rose by over 30 percent, eventhough prices were already at very low levels with the end of the pilot phase insight. Throughout the second phase, the regulatory surprises were a bit smaller,especially at the beginning. Towards the end, there were some larger surprises,for instance in November 2011 when a new regulation determining the volumeof allowances to be auctioned prior to 2013 came into force. Some very large

2While futures prices are in general subject to risk premia, there is evidence that these premiavary primarily at lower frequencies (Piazzesi and Swanson, 2008; Hamilton, 2009; Nakamura andSteinsson, 2018). If that is the case, risk premia are differenced out in the computation of the high-frequency surprise series.

3As shown in Appendix B.4, using contracts further out produces results that are at least qual-itatively similar. However, the first stage gets considerably weaker, further supporting the use ofthe front contract.

10

Figure 2: The carbon policy surprise series

Notes: This figure shows the carbon policy surprise series, constructed by mea-suring the percentage change of the EUA futures price around regulatory pol-icy events concerning the supply of emission allowances in the European carbonmarket.

surprises occurred at the beginning of the third phase. On April 16, 2013 the Eu-ropean Parliament voted against the Commission’s back-loading proposal, whichled to a massive price fall of 43 percent. In September 2013, the Commission fi-nalized the free allocation to the industrial sector in phase three, which led to aprice increase of 10 percent. And in March 2014, the Commission approved twobatches of international credit entitlement tables, sending prices down by almost20 percent, just to name a few.

A crucial choice in high-frequency identification concerns the size of the eventwindow. There is a trade-off between capturing the entire response to the an-nouncement and the threat of other news confounding the response, so-calledbackground noise (cf. Nakamura and Steinsson, 2018). Because the exact releasetimes of the regulatory news detailed in Table A.1 are mostly unavailable, it ispractically infeasible to use an intraday window. However, to mitigate concernsabout background noise when using a daily window, I also present results froma heteroskedasticity-based approach that allows for background noise in the sur-prise series (see Section 7).

Finally, to be able to interpret the resulting series as a carbon policy surprises,it is crucial that the events do not release other information such as news aboutthe demand of emission allowances or economic activity in the EU more gen-erally. To address these concerns, I put great care in selecting regulatory updateevents that were about very specific changes to the supply of emission allowancesin the European carbon market and do not include broader events such as out-comes of Conference of the Parties (COP) meetings or other international confer-

11

ences. Furthermore, I show that excluding the events regarding the overall cap,which are generally broader in scope, leads to very similar results. Likewise, ex-cluding events that overlap with broader news about the carbon market does notchange the results materially (see Section 7 for more details). Lastly, the focuson the supply of allowances is also confirmed by looking how some of the majorevents are received in the press.4

Diagnostics. To further assess the validity of the carbon policy surprise series, Iperform a number of diagnostic checks. Desirable properties of a surprise seriesare that it should not be autocorrelated, forecastable nor correlated with otherstructural shocks (see Ramey, 2016, for a detailed discussion).

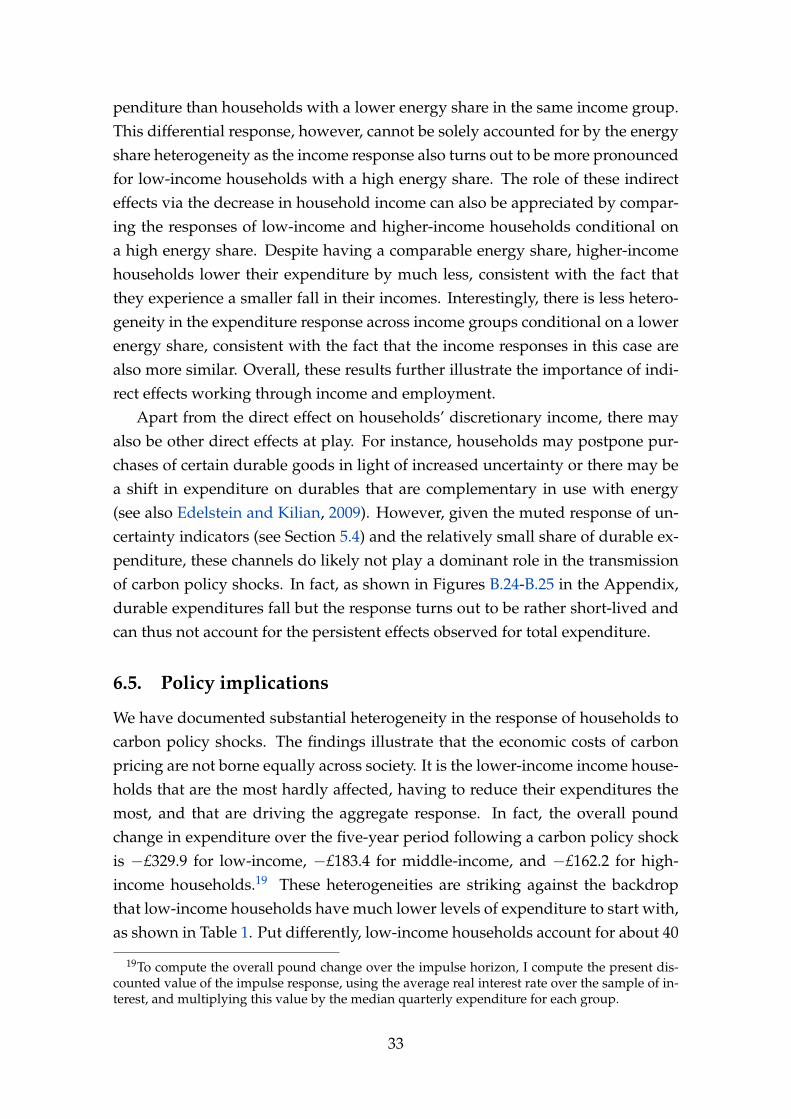

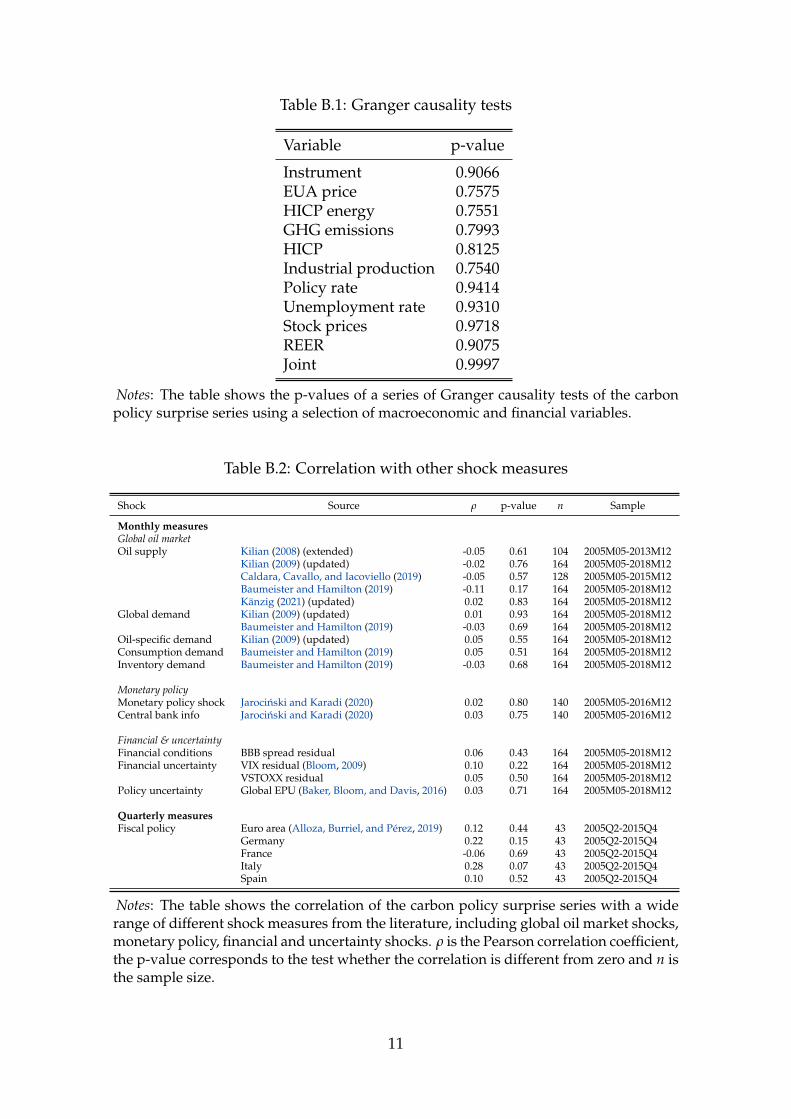

Inspecting the autocorrelation function, I find little evidence for serial corre-lation. The p-value for the Q-statistic that all autocorrelations are zero is 0.92. Ialso find no evidence that macroeconomic or financial variables have any powerin forecasting the surprise series. For all variables considered, the p-values forthe Granger causality test are far above conventional significance levels, with thejoint test having a p-value of 0.99. I also show that the surprise series is uncor-related with other structural shock measures from the literature, including oil,uncertainty, financial, fiscal and monetary policy shocks. The corresponding fig-ures and tables can be found in Appendix B.1. Overall, this evidence supportsthe validity of the carbon policy surprise series.

4. Econometric approach

As illustrated above, the carbon policy surprise series has many desirable prop-erties. Nonetheless, it is only a partial measure of the shock of interest becauseit may not capture all relevant instances of regulatory news in the carbon mar-ket and could be measured with error (see Stock and Watson, 2018, for a detaileddiscussion of this point).

Thus, I do not use it as a direct shock measure but as an instrument. Providedthat the surprise series is correlated with the carbon policy shock but uncorre-lated with all other shocks, we can use it to estimate the dynamic causal effectsof a carbon policy shock. Because of the short sample at hand, I rely on VARtechniques for estimation. For identification, I use both an external instrument(Stock, 2008; Stock and Watson, 2012; Mertens and Ravn, 2013) and an internalinstrument approach (Ramey, 2011; Plagborg-Møller and Wolf, 2019). In the ex-

4See e.g. https://www.bbc.com/news/science-environment-22167675 or https://www.argusmedia.com/en/news/2234159-eu-eyes-42pc-lrf-extended-scope-for-ets.

12

ternal instrument approach, the surprise series is used as an instrument externalto the VAR model. While this approach tends to be very efficient, it provides bi-ased estimates if the VAR is not invertible. In contrast, the internal instrumentapproach, which includes the instrument as the first variable in a recursive VAR,is robust to problems of non-invertibility.

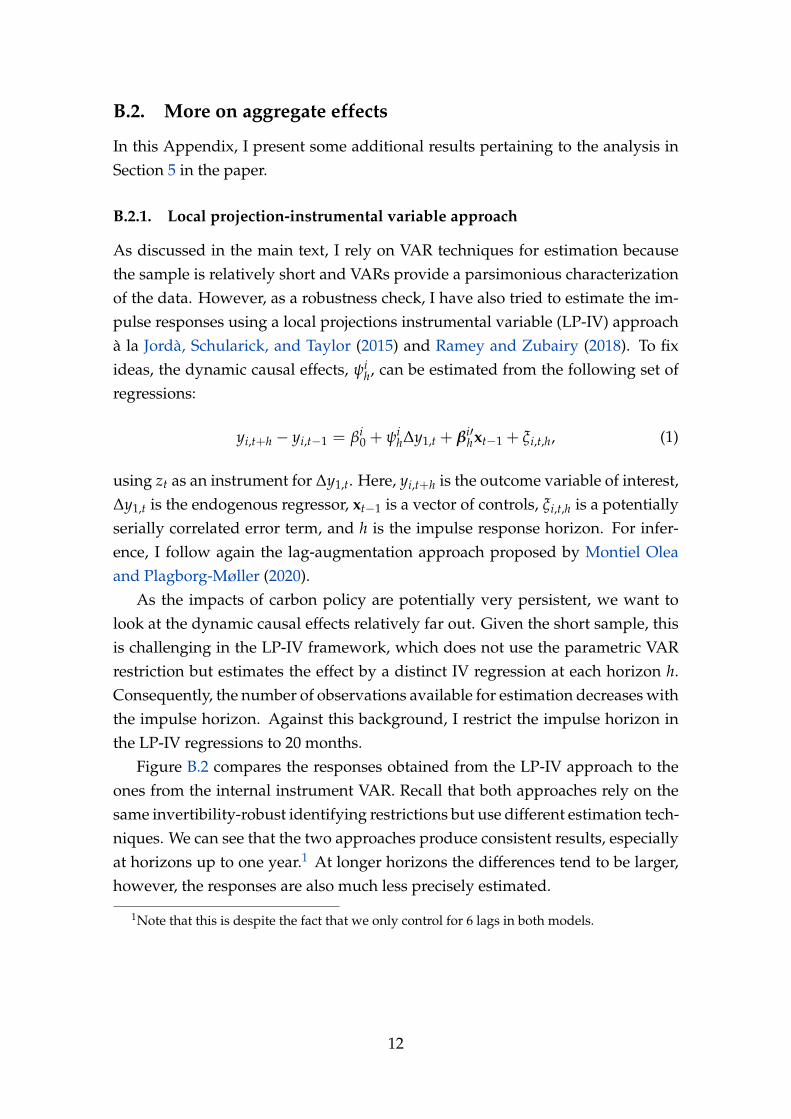

An alternative approach would be to estimate the dynamic causal effects us-ing local projections (see Jordà, Schularick, and Taylor, 2015; Ramey and Zubairy,2018). However, this approach is quite demanding given the short sample, as itinvolves a distinct IV regression for each impulse horizon. Importantly, Plagborg-Møller and Wolf (2019) show that the internal instrument VAR and the LP-IV relyon the same invertibility-robust identifying restrictions and identify, in popula-tion, the same relative impulse responses. In Appendix B.2, I compare the LP-IVto the internal instrument VAR responses in the sample at hand. Reassuringly, theresponses turn out to be similar, even though the LP responses are more jaggedand less precisely estimated.

4.1. Framework

Consider the standard VAR model

yt = b + B1yt−1 + · · ·+ Bpyt−p + ut, (2)

where p is the lag order, yt is a n× 1 vector of endogenous variables, ut is a n× 1vector of reduced-form innovations with covariance matrix Var(ut) = Σ, b is an× 1 vector of constants, and B1, . . . , Bp are n× n coefficient matrices.

Under the assumption that the VAR is invertible, we can write the innovationsut as linear combinations of the structural shocks εt:

ut = Sεt. (3)

By definition, the structural shocks are mutually uncorrelated, i.e. Var(εt) = Ω isdiagonal. From the invertibility assumption (3), we get the standard covariancerestrictions Σ = SΩS′.

We are interested in characterizing the causal impact of a single shock. With-out loss of generality, let us denote the carbon policy shock as the first shock inthe VAR, ε1,t. Our aim is to identify the structural impact vector s1, which corre-sponds to the first column of S.

External instrument approach. Identification using external instruments worksas follows. Suppose there is an external instrument available, zt. In the applica-

13

tion at hand, zt is the carbon policy surprise series. For zt to be a valid instrument,we need

E[ztε1,t] = α 6= 0 (4)

E[ztε2:n,t] = 0, (5)

where ε1,t is the carbon policy shock and ε2:n,t is a (n− 1)× 1 vector consistingof the other structural shocks. Assumption (4) is the relevance requirement andassumption (5) is the exogeneity condition. These assumptions, in combinationwith the invertibility requirement (3), identify s1 up to sign and scale:

s1 ∝E[ztut]

E[ztu1,t], (6)

provided that E[ztu1,t] 6= 0.5 To facilitate interpretation, we scale the structuralimpact vector such that a unit positive value of ε1,t has a unit positive effect ony1,t, i.e. s1,1 = 1. I implement the estimator with a 2SLS procedure and estimatethe coefficients above by regressing ut on u1,t using zt as the instrument. To con-duct inference, I employ a residual-based moving block bootstrap, as proposedby Jentsch and Lunsford (2019), and use Hall’s percentile interval to compute thebands.

Internal instrument approach. To assess potential problems of non-invertibility, I also employ an internal instrument approach. For identification,we have to assume in addition to (4)-(5) that the instrument is orthogonal toleads and lags of the structural shocks:

E[ztεt+j] = 0, for j 6= 0. (7)

In return, we can dispense of the invertibility assumption underlying equation(3).

Under these assumptions, we can estimate the dynamic causal effects byaugmenting the VAR with the instrument ordered first, yt = (zt, y′t)

′, andcomputing the impulse responses to the first orthogonalized innovation, s1 =

[chol(Σ)]·,1/[chol(Σ)]1,1. As Plagborg-Møller and Wolf (2019) show, this ap-proach consistently estimates the relative impulse responses even if the instru-ment is contaminated with measurement error or if the shock is non-invertible.

5To be more precise, the VAR does not have to be fully invertible for identification with externalinstruments. As Miranda-Agrippino and Ricco (2018) show, it suffices if the shock of interest isinvertible in combination with a limited lead-lag exogeneity condition.

14

To conduct inference, I rely again on a residual-based moving block bootstrap.

4.2. Empirical specification

Studying the macroeconomic impact of carbon policy requires modeling the Eu-ropean economy and the carbon market jointly. The baseline specification con-sists of eight variables. For the carbon block, I use the energy component of theHICP as well as total GHG emissions.6 For the macroeconomic block, I includethe headline HICP, industrial production, the unemployment rate, the policy rate,a stock market index, as well as the real effective exchange rate (REER).7 More in-formation on the data and its sources can be found in Appendix A.2.

The sample spans the period from January 1999, when the euro was intro-duced, to December 2018. Recall, that the carbon policy surprise series is onlyavailable from 2005 when the carbon market was established. To deal with thisdiscrepancy, the missing values in the surprise series are censored to zero (seeNoh, 2019, for a theoretical justification of this approach). The motivation forusing a longer sample is to increase the precision of the estimates. However, re-stricting the sample to 2005-2018 produces very similar results.8

Following Sims, Stock, and Watson (1990), I estimate the VARs in levels. Apartfrom the unemployment and the policy rate, all variables enter in log-levels. Ascontrols I use six lags of all variables and in terms of deterministics only a con-stant term is included. However, the results turn out the be robust with respectto all of these choices (see Section 7).

5. The aggregate effects of carbon pricing

5.1. First stage

The main identifying assumption behind the (external) instrument approach isthat the instrument is correlated with the structural shock of interest but uncor-related with all other structural shocks. However, to be able to conduct standardinference, the instrument has to be sufficiently strong. To analyze whether this

6Unfortunately, GHG emissions are only available at the annual frequency. Therefore, I con-struct a monthly measure of emissions using the Chow-Lin temporal disaggregation method withindicators from Quilis’s (2020) code suite. As the relevant monthly indicators, I include the HICPenergy and industrial production. The results are robust to extending the list of indicators used.

7A delicate choice concerns the monetary policy indicator. As the baseline, I use the 3-monthEuribor. Using the shadow rate or longer-term government bond yields produces similar results.

8Note that while the carbon market was only established in 2005, the EU agreed to the Kyotoprotocol in 1997 and started planning on how to meet its emission targets shortly after. Thedirective for establishing the EU ETS came into force in October 2003 (Directive 2003/87/EC).

15

is the case, I perform the weak instruments test by Montiel Olea and Pflueger(2013).

The heteroskedasticity-robust F-statistic in the first stage of the external in-strument VAR is 20.95. Assuming a worst-case bias of 20 percent with a sizeof 5 percent, the corresponding critical value is 15.06. As the test statistic liesclearly above the critical value, we conclude that the instrument appears to besufficiently strong to conduct standard inference.

5.2. The impact on emissions and the macroeconomy

Having established that the carbon policy surprise series is a strong instrument, Ipresent now the results from the external and internal instrument models. Figure3 shows the impulse responses to the identified carbon policy shock, normalizedto increase the HICP energy component by one percent on impact. Panel A de-picts the responses from the external instrument VAR and Panel B presents theresponses from the internal instrument model. I start by discussing the resultsfrom the external instrument approach.

A restrictive carbon policy shock leads to a strong, immediate increase in theenergy component of the HICP and a significant and persistent fall in GHG emis-sions. Thus, carbon pricing appears to be successful at reducing emissions andmitigating climate change. Turning to the macroeconomic variables, we can seethat the fall in emissions does not come without cost. Consumer prices, as mea-sured by the HICP, increase, industrial production falls, and the unemploymentrate rises significantly. The labor market response turns out to be particularlypronounced, consistent with reallocation frictions in the economy. However, thefall in activity and industrial production in particular appears to be less persistentthan the fall in emissions – implying an improvement in the emissions intensityin the longer run. While headline consumer prices increase persistently, the re-sponse of core HICP turns out to be more short-lived (see Appendix B.2 for moredetails). Monetary policy seems to largely look through the inflationary pressurescaused by the carbon policy shock, as reflected in the insignificant policy rate re-sponse. Stock prices fall significantly on impact but recover quite quickly andeven turn positive after about two years. Finally, the real exchange rate depreci-ates significantly.

In terms of magnitudes, a carbon policy shock increasing energy prices by 1percent causes a decrease in GHG emissions and industrial production by around0.5 percent, a rise in the unemployment rate of 0.2 percentage points and an in-crease in consumer prices of slightly more than 0.15 percent – measured at thepeak of the responses. Thus, the responses are not only statistically but also eco-

16

Panel A: External instrument approach Panel B: Internal instrument approach

Figure 3: Impulse responses to a carbon policy shock

Notes: Impulse responses to a carbon policy shock, normalized to increase the HICP energy by 1 percent on impact. The solid line is the pointestimate and the dark and light shaded areas are 68 and 90 percent confidence bands, respectively.

17

nomically significant.

The results from the internal instrument model turn out to be very similar.The signs are all consistent and the responses are also similar in shape. The maindifference lies in the response of energy prices, which turns out to be strongerand more persistent than in the external instrument model. Consequently, themagnitudes for emissions and the economic variables also turn out to be larger.It should be noted, however, that the responses are also less precisely estimated.Overall, these findings suggest that the results are robust to relaxing the assump-tion of invertibility. In the remainder of the paper, I thus use the external instru-ments model as the baseline.

By way of summary, these findings clearly illustrate the policy trade-off be-tween reducing emissions and thus the future costs of climate change and thecurrent economic costs associated with climate change mitigation policies. Myresults also point to a strong pass-trough of carbon to energy prices, as can beseen from the significant energy price response. Unfortunately, it is not possi-ble to quantify the pass-through directly, as my baseline specification does notinclude the carbon price, which only became available in 2005 when the carbonmarket was established. However, estimates from a model including the carbonprice, estimated on the shorter sample, point to a pass-through of around 20 per-cent at its peak (see Appendix B.2).

5.3. Historical importance

In the previous section, we have seen that carbon policy shocks can have sig-nificant effects on emissions and the economy. An equally important question,however, is how much of the historical variation in the variables of interest cancarbon policy account for? To this end, I perform a historical decomposition ex-ercise. To get a better idea of the average contribution, I also perform a variancedecomposition in Appendix B.2.

Figure 4 shows the historical contribution of carbon policy shocks to energyprice inflation and GHG emissions growth. We can see that carbon policy shockshave contributed meaningfully to variations in energy prices and GHG emissionsin many episodes. On average, carbon policy shocks account for about a third ofthe variations in energy prices and a quarter of the variations in emissions athorizons up to one year. Furthermore, carbon policy shocks can also explain anon-negligible share of the variations in other macroeconomic and financial vari-ables (see Appendix B.2). Importantly, we can also see that the significant fallin emissions in the aftermath of the global financial crisis was not driven by car-

18

bon policy shocks. This result is reassuring that the high-frequency identificationstrategy is working as the fall in emissions during the Great Recession was clearlydriven by lower demand and not supply-specific factors in the European carbonmarket.

Panel A: HICP energy inflation

Panel B: GHG emissions growth

Figure 4: Historical decomposition of energy inflation and emissions growth

Notes: The figure shows the cumulative historical contribution of carbon policy shocksover the estimation sample for a selection of variables against the actual evolution ofthese variables. Panel A shows the historical contribution to HICP energy inflation, PanelB presents the contribution to GHG emissions growth. The solid line is the point estimateand the dark and light shaded areas are 68 and 90 percent confidence bands, respectively.

5.4. Propagation channels

Having established that carbon policy shocks are an important driver of the econ-omy, we now analyze in more detail the underlying transmission channels.

The role of energy prices. The above results suggest that energy prices play acrucial role in the transmission of carbon policy shocks. Power producers seem to

19

pass through the emission costs to energy prices to a significant extent, which is inline with previous empirical evidence (see e.g. Veith, Werner, and Zimmermann,2009; Bushnell, Chong, and Mansur, 2013). To further corroborate this channel, Iperform an event study using daily stock market data. More specifically, I mapout the effects of carbon policy surprises on carbon futures and stock prices byrunning the following set of local projections:

qi,d+h − qi,d−1 = βi0 + ψi

hCPSurprised + βih,1∆qi,d−1 + . . . + βi

h,p∆qi,d−p + ξi,d,h,

(8)

where qi,d+h is the (log) price of asset i after h days following the event d,CPSurprised is the carbon policy surprise on event day. ψi

h measures the effect onasset price i at horizon h. For inference, I follow the lag-augmentation approachproposed by Montiel Olea and Plagborg-Møller (2020). In particular, I augmentthe controls by an additional lag and use heteroskedasticity-robust standard er-rors.

Figure 5: Carbon prices and stock market indicesNotes: Responses of carbon futures prices and stock indices for the market and the utilitysector to a carbon policy surprise. The sample spans the period from April 22, 2005 toDecember 31, 2018. As controls, I use 15 lags of the respective dependent variable.

The results are shown in Figure 5. We can see that carbon policy surpriseslead to a significant increase in carbon futures prices. The front contract increasessignificantly for about three weeks. The effect turns out to be quite persistent

20

as the price of the second contract, which expires in the following quarter, alsoincreases significantly. Turning to the stock market, we can see that the marketdoes not seem to move immediately following carbon surprises. Only after aboutone week, the index starts to fall significantly. This may reflect the fact that theEU ETS is a relatively new market and thus market participants need some timeto process the regulatory news. Looking into potential sectoral heterogeneities,I find that most sectors display a similar response to the market. Among the 11GICS sectors, utilities is the only sector that stands out, displaying a significantincrease in stock prices.

These results suggest that the European utility sector is able to profit, at leastin the short run, from a more stringent carbon pricing regime. This findingis in line with previous empirical evidence (Veith, Werner, and Zimmermann,2009; Bushnell, Chong, and Mansur, 2013) and may be explained as follows. Theutility sector is segmented due to the structure of existing transmission networks,which substantially limits import penetration from countries without a carbonprice. Thus, utility companies are able to increase their product prices withoutlosing market share. At the same time, utilities can decarbonize at relativelylow cost, for instance by switching from coal to gas-fired electricity, and sell theexcess allowances at a profit. In contrast, for industrial emitters competing ininternational product markets, passing through the cost of carbon could lead tosignificant losses in market share, and decarbonizing tends to be more costly.

The transmission to the macroeconomy. To better understand how carbon pric-ing and the associated increase in energy prices affect the economy, I study theresponses of a selection of financial and macroeconomic variables. To be able toestimate the dynamic causal effects on these variables, I extract the carbon pol-icy shock from the monthly VAR as CPShockt = s′1Σ−1ut (for a derivation, seeStock and Watson, 2018) and estimate the dynamic causal effects using simplelocal projections:

yi,t+h = βi0 + ψi

hCPShockt + βih,1yi,t−1 + . . . + βi

h,pyi,t−p + ξi,t,h, (9)

where ψih is the effect on variable i at horizon h. Importantly, we can also use this

approach to estimate the effects on variables that are only available at the quar-terly or even annual frequency. In this case, we aggregate the shock CPShockt bysumming over the respective months before running the local projections. Usingthe shock series directly in the local projections as opposed to the high-frequencysurprises increases the statistical power of these regressions, as the shock seriesis consistently observed and spans the entire sample. Note, however, that this

21

comes at the cost of assuming invertibility. Throughout the paper, I normalize theshock to increase the HICP energy component by one percent on impact. The con-fidence bands are again computed using the lag-augmentation approach (MontielOlea and Plagborg-Møller, 2020).9

Increases in energy prices can have significant effects on the macroeconomy(see e.g. Hamilton, 2008; Edelstein and Kilian, 2009). They directly affect house-holds and firms by reducing their disposable income. Given that energy de-mand is considered to be quite inelastic, consumers and firms have less moneyto spend and invest after paying their energy bills (and financing their emissionallowances). Note, however, that the magnitude of this discretionary income ef-fect is bounded by the energy share in expenditure, which is around 7 percent inEurope. In addition, increased uncertainty about future energy prices may leadto a further fall in spending and investment because of precautionary motives.

Energy prices also affect the economy indirectly through the general equilib-rium responses of prices and wages and hence of income and employment. Aftera carbon policy shock increasing energy prices, the direct decrease in households’and firms’ consumption and investment expenditure will lead to lower outputand exert downward pressure on employment and wages. The additional fall inaggregate demand induced by lower employment and wages lies at the core ofthe indirect effect.

To shed light on the different transmission channels at work, I study the re-sponses of GDP and its components in Figure 6. We can see that the shock leadsto a significant fall in real GDP. The response looks quite similar to the response ofindustrial production, both in terms of shape and magnitude. Looking at the dif-ferent components, we can see that the shock leads to a significant and persistentfall in consumption. Investment, as measured by gross fixed capital formation,also falls significantly but the response turns out to be somewhat less persistent.Finally, net exports, expressed as a share of GDP, increase significantly, in linewith the real depreciation of the euro. Inspecting the responses of exports andimports separately reveals that both exports and imports fall but imports fall bymuch more causing the significant increase in net exports.

Importantly, the magnitudes of the effects are by an order of magnitude largerthan what can be accounted for by the direct effect through higher energy prices.This suggests that indirect effects play a crucial role in the transmission of carbonpolicy shocks. In Section 6, I shed more light on the role of different transmission

9Reassuringly, the comparison of the internal and external instrument models as well as therobustness checks in Section 7 did not point to any problems of non-invertibilty. As controls inthe local projections, I use 7 lags for monthly variables, 3 lags for quarterly variables and 2 lagsfor annual variables.

22

Figure 6: Effect on GDP and components

Notes: Impulse responses of real GDP, consumption, investment and net exports ex-pressed as a share of GDP.

channels using detailed household micro data.The above results support the notion that higher energy prices and the asso-

ciated direct and indirect effects are a dominant transmission channel of carbonpricing. However, apart from the effects through energy prices, carbon pricingmay also affect the economy through other channels, for instance by affectingfinancing conditions or increased uncertainty. It turns out, however, that thesevariables respond to carbon policy shocks only with a lag, similar to stock prices,and the responses do not turn out to be very significant (see Figure B.5 in the Ap-pendix). Thus, these alternative channels are unlikely to play a dominant role inthe transmission of carbon policy shocks.

The effect on innovation. We have seen that carbon pricing is successful in re-ducing emissions but this comes at an economic cost, at least in the short term.However, there could also be positive effects in the longer term, for instance byspurring innovation in low-carbon technologies. In fact, part of the vision for theEU ETS is to promote investment in clean, low-carbon technologies (EuropeanComission, 2020a).

To analyze this channel in more detail, I study how the patenting activity inclimate change mitigation technologies is affected by the carbon policy shock.The European Patent Office (EPO) has developed specific classification tags forclimate change mitigation technologies.

23

Figure 7: Patenting in climate change mitigation technologies

Notes: Impulse responses of patenting activity in climate change mitigation technologies.Depicted is the response of the number of climate change mitigation patent filings, inabsolute terms (left panel) and as a share of all patents filed at the EPO (right panel).

The results are shown in Figure 7. We can see that the shock leads to a signifi-cant increase in low-carbon patenting, both in absolute terms and also relativeto the overall patenting activity. Thus, carbon pricing appears to be success-ful in stimulating innovation in climate change mitigation technologies. Theseresults support the findings of Calel and Dechezleprêtre (2016), who employ aquasi-experimental design exploiting inclusion criteria at the installations levelto estimate the ETS system’s causal impact on firms’ patenting, and also chimewell with the previously documented stock market response, which reboundsand even turns positive in the longer run.

6. The heterogeneous effects of carbon pricing

Recently, there has been a big debate in Europe on energy poverty and the dis-tributional effects of carbon pricing amid the European Commission’s plans ofextending the carbon market to buildings and transportation (European Comis-sion, 2021). While the commission did propose a Social Climate Fund to cushionthe adverse effects on vulnerable households, several observers have argued thatthe proposal does not do enough to ensure a fair and equitable transition.10

Against this backdrop, it is crucial to better understand the distributional im-pact of the EU ETS. If certain groups are left behind, this could ultimately under-mine the success of climate policy. To this end, I study the heterogeneous effectsof carbon pricing on households. This will help to get a better picture on howcarbon pricing affects economic inequality. Furthermore, looking into potentialheterogeneities in the consumption responses can help to better understand the

10See e.g. https://righttoenergy.org/2021/07/14/fit-for-55-not-fit-for-europes-energy-poor/.

24

transmission channels at work. There is reason to believe that there are impor-tant heterogeneities at play. First, the direct effect through energy prices cruciallydepends on the energy expenditure share, which is highly heterogeneous acrosshouseholds. Second, the indirect effects will also be heterogeneous to the extentthat individual incomes respond differently to the change in aggregate expendi-ture, for instance because of differences in the income composition or the sectorof employment. As poorer households tend to have a higher energy share andtheir income tends to be more cyclical, we expect the impact to be regressive.

6.1. Household survey data

To be able to analyze the heterogeneous effects of carbon policy shocks on house-holds, we need detailed micro data on consumption expenditure and income ata regular frequency for a sample spanning the last two decades. Unfortunately,such data does not exist for most European countries let alone at the EU level.Therefore, I focus here on the UK which is one of the few countries that has suchdata as part of the Living Costs and Food Survey (LCFS).11

The LCFS is the most significant survey on household spending in the UK andprovides high-quality, detailed information on expenditure, income, and house-hold characteristics. The survey is fielded in annual waves with interviews beingconducted throughout the year and across the whole of the UK. I compile a re-peated cross-section based on the last 20 waves, spanning the period 1999 to 2018.Each wave contains around 6,000 households, generating over 120,000 observa-tions in total. To compute measures of income and expenditure, I first express thevariables in per capita terms by dividing household variables by the number ofhousehold members. In a next step, I deflate the variables by the (harmonized)consumer price index to express them in real terms. For more information, seeAppendix A.3.

Ideally, we would like to observe how individual consumption expenditureand income evolve over time. Unfortunately, the LCFS being a repeated cross-section has no such panel dimension. To construct a pseudo-panel, it is commonto use a grouping estimator in the spirit of Browning, Deaton, and Irish (1985).

A natural dimension for grouping households is their income. However, asthe income may endogenously respond to the shock of interest, we cannot use thecurrent household income as the grouping variable. Luckily, the LCFS does not

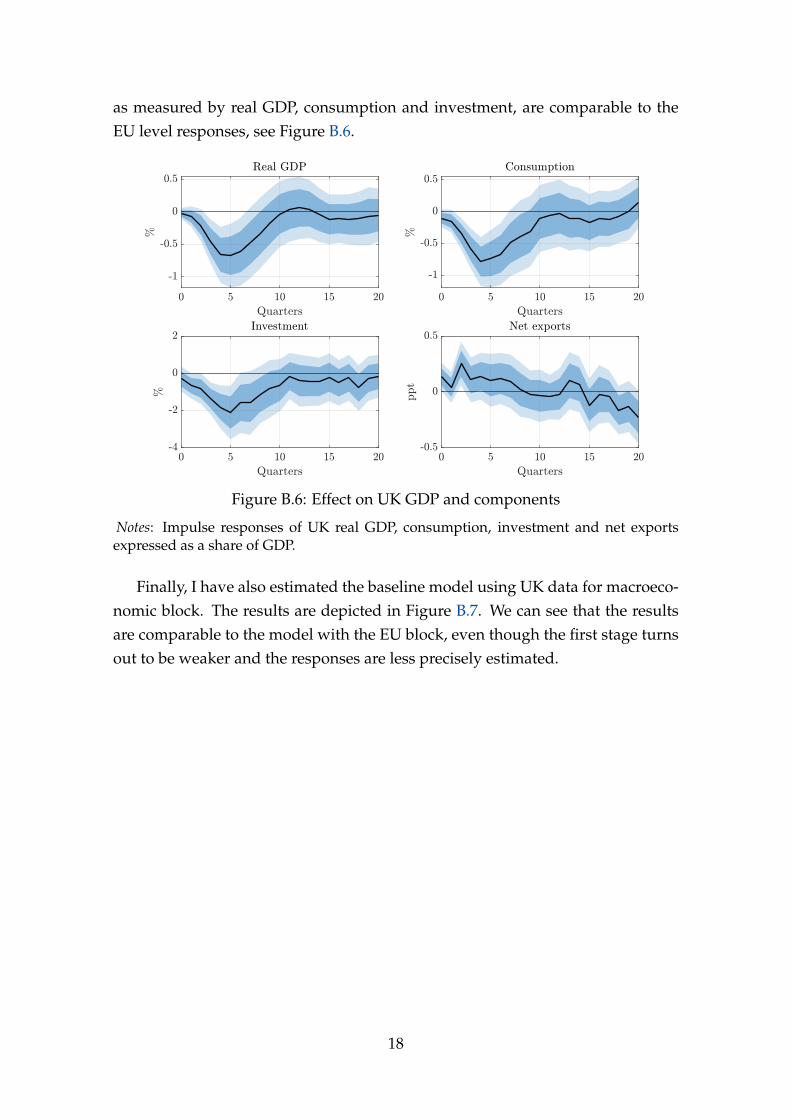

11The UK was part of the EU ETS until the end of 2020. Over the sample of interest, the ag-gregate effects in the UK are comparable to the ones documented at the EU level, see Figure B.6in the Appendix. To further mitigate concerns about external validity, I show that the results forother European countries such as Denmark and Spain are very similar, see Figure B.26.

25

only collect information about current household income but also about normalhousehold income, which should by construction not be affected by temporaryshocks.12 Thus, I use the normal disposable household income to group house-holds into three pseudo-cohorts: low-income, middle-income, and high-incomehouseholds.13 Following Cloyne and Surico (2017), I assign each household to aquarter based on the date of the interview, and create the group status as the bot-tom 25 percent of the normal disposable income distribution for low-income, themiddle 50 percent for middle-income, and the top 25 percent for high-income inevery quarter of a given year. The individual variables are then aggregated usingsurvey weights to ensure representativeness of the British population.

Table 1 presents some descriptive statistics, unconditional for all householdsas well as by conditioning on the three income groups. We can see that weeklytotal expenditure (excl. housing) and housing expenditure are both increasing inincome. While low-income households spend a large part of their budget on non-durables, richer households spend more on services and durables. Importantly,poorer households spend a significantly higher share of their expenditure on en-ergy: the (average) energy share stands at close to 9.5 percent for low-income, justabove 7 percent for middle income, and around 5 percent for high-income house-holds. Thus, to the extent that energy demand is inelastic, poorer households aremore exposed to increases in energy prices.

The different income groups turn out to be comparable in terms of their age.This can be seen from the median age which is around 50 for all groups and alsofrom Figure B.8 in the Appendix, which shows that the empirical age distributionis similar across all three income groups. As expected, high-income householdstend to be more educated, as can be seen from the larger share of households thathave completed post-compulsory education. Finally, higher-income householdstend to be homeowners, either by mortgage or outright, while among the low-income there is a large share of social renters. Importantly, all these variablesare rather slow-moving and unlikely to confound potential heterogenities in thehousehold responses to carbon policy shocks, which exploit variation at a muchhigher frequency (see Figure B.9 in the Appendix).

12While it may be affected by permanent shocks, this should not be too much of a concern forour grouping strategy as the normal income variable is very slow moving. I have also verifiedthat normal income does not respond significantly to the carbon policy shock. In contrast, currentincome falls significantly and persistently, as shown in Figure B.10 in the Appendix.

13In Appendix B.3, I use a selection of other proxies for the income level, including earnings,expenditure, and an estimate for permanent income obtained from a Mincerian-type regression.The results turn out to be robust to using these alternative measures of income for grouping.Alternatively, I tried to group households by their energy share directly. The results turn outagain to be very similar, see Figure B.21. This suggests that the energy share is a good proxy forthe level of income, with poorer households having higher energy shares (see also Table B.4).

26

Table 1: Descriptive statistics on households in the LCFS

Overall By income group

Low-income Middle-income High-income

Income and expenditureNormal disposable income 236.3 112.6 236.3 466.6Total expenditure (excl. housing) 157.3 91.6 155.4 269.6

Energy share 7.2 9.4 7.1 5.1Non-durables (excl. energy) share 49.6 55.0 49.7 44.1Services share 31.9 26.7 31.9 37.2Durables share 11.3 8.9 11.3 13.6

Housing 32.0 18.8 31.1 58.0

Household characteristicsAge 51 46 54 49Education (share with post-comp.) 33.5 25.0 29.1 51.0Housing tenure

Social renters 20.9 47.1 17.4 3.7Mortgagors 42.6 25.5 41.6 60.4Outright owners 36.6 27.4 41.0 36.0

Notes: The table shows descriptive statistics on weekly per capita income and expen-diture (in 2015 pounds), the breakdown of expenditure into energy, non-durables excl.energy, services and durables (as a share of total expenditure) as well as a selection ofhousehold characteristics, both over all households and by income group. For variablesin levels such as income, expenditure and age the median is shown while the shares arecomputed based on the mean of the corresponding variable. Note that the expenditureshares are expressed as a share of total expenditure excl. housing and thus services do notinclude housing either, and semi-durables are subsumed under the non-durable category.Age corresponds to the age of the household reference person and education is proxiedby whether a member of a household has completed a post-compulsory education.

6.2. Median effect and the response of inequality

We are now in a position to study how households’ expenditure and income re-spond to carbon policy shocks.14 As a validating exercise, we first look at themedian household expenditure response and compare it to the consumption re-sponse based on national statistics. As can be seen from the left panel of Figure 8,the median response aligns quite well with the response from national statistics,both in terms of shape and magnitude (see Figure 6).

14In the LCFS, households interviewed at time t are typically asked to report expenditure overthe previous three months (with the exception of non-durable consumption which refers to theprevious two weeks). To eliminate some of the noise inherent in survey data, I smooth the ex-penditure and income measures with a backward-looking (current and previous three quarters)moving average, as in Cloyne, Ferreira, and Surico (2020). Similar results are obtained when us-ing the raw series instead (even though the responses become more jagged and imprecise) or byusing smooth local projections as proposed by Barnichon and Brownlees (2019), see Figure B.14in the Appendix. To account for potential seasonal patterns I include a set of quarterly dummiesas controls, following again Cloyne, Ferreira, and Surico (2020).

27

Figure 8: Response of household consumption expenditure

Notes: Impulse responses of total expenditure excluding housing. The left panel showsthe median response and the right panel shows the response of consumption inequality,as measured by the Gini coefficient.

To investigate into potential heterogeneities, we also look at the Gini index forhousehold expenditure. The response is shown in the right panel of Figure 8. Wecan see that the shock leads to a significant increase in inequality, especially atlonger horizons. While this result is interesting in itself, it does not tell us whichgroups are more hardly affected than others.

6.3. Heterogeneity by household income

Having analyzed the aggregate effects as well as the effects on inequality, wenow look into the underlying heterogeneity by income group. Figure 9 showsthe responses of household expenditure and current income for the three incomegroups we consider.

We can see that there is pervasive heterogeneity in the expenditure responsebetween income groups. Low-income households reduce their expenditure sig-nificantly and persistently. In contrast, the expenditure response of higher-income households is rather short-lived and only barely statistically significant.Interestingly, the income responses turn out to be somewhat more homogeneous.While low-income households experience the largest drop in income, higher-income households also experience a non-negligible income decline, even thoughit turns out to be less persistent.15 The finding that the expenditure of high-income households does nevertheless not respond significantly points to the factthat these households have more savings and liquid assets to smooth the tempo-rary fall in their income. In contrast, the low-income households are hit twofold.

15While the income decline of the low- and middle-income households appears to be driven bya fall in earnings, high-income households also experience a fall in their financial income, whichthen however reverses and turns significantly positive – in line with the stock market response,see Figure B.15 in the Appendix.

28

Figure 9: Household expenditure and income responses by income groups

Notes: Impulse responses of total expenditure excluding housing and current total dis-posable household income for low-income (bottom 25 percent), middle-income (middle50 percent) and high-income households (top 25 percent). The households are groupedby total normal disposable income and the responses are computed based on the medianof the respective group.

29

First, they spend a larger share of their budget on energy and are thus, as energyexpenditure is highly inelastic, adversely affected by the higher energy bill. Sec-ond, they experience a larger fall in income, as they tend to work in sectors thatare more hardly affected by the carbon policy shock (see Section 6.4). At the sametime, they are more likely to be financially constrained and less able to cope withthe adverse effects on their income and budget.

At this stage, it is worth discussing a potential concern about grouping house-holds concerning selection. The assignments into the income groups are notrandom and some other characteristics may, potentially, be responsible for theheterogeneous responses I document. To mitigate these concerns, I group thehouseholds by a selection of other grouping variables, including age, educationand housing tenure. The results are shown in Figures B.16-B.18 in the Appendix.While there is not much heterogeneity by age, less educated households tendto respond more than better educated ones and social renters tend to respondmore than homeowners. However, none of the alternative grouping variablescan account for the patterns uncovered for income, suggesting that we are notspuriously picking up differences in other household characteristics.

6.4. Direct versus indirect effects

While the expenditure responses are, as expected, more pronounced the higherthe energy share, the magnitudes are much larger than what can be accounted forby the discretionary income effect alone. Assuming that energy demand is com-pletely inelastic, the direct effect is bounded by the energy share of the respectivegroup.16 However, the peak response of low-income households is around one– close to ten times the energy share of that group. This suggests that indirect,general equilibrium effects via income and employment account for a large partof the overall effect on household expenditure; a finding that is also supportedby the significant effects on unemployment documented in Section 5.2.

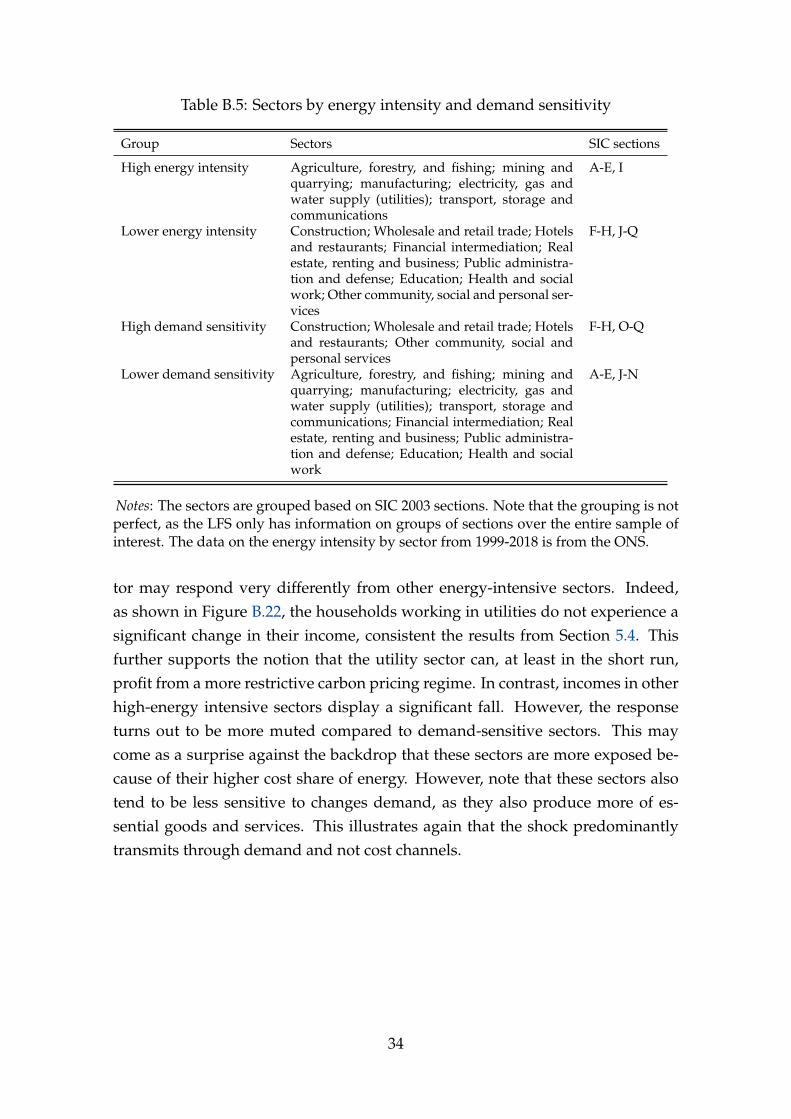

To shed more light on these indirect effects, I study how the income responsevaries by the sector of employment using data from the UK Labour Force Survey(LFS).17 I consider two dimensions to group sectors. First, I group sectors by

16Energy expenditure does indeed turn out to be pretty inelastic, especially for low-incomehouseholds, see Figures B.19-B.20 in the Appendix. While the energy share of higher-incomehouseholds does not respond significantly, the energy share of low-income households tends toincrease – reflecting the fact that their energy expenditure hardly changes while their total con-sumption expenditure falls significantly.

17Unfortunately, the LCFS does not include any information on the sector of employment.Therefore, I use data from the LFS which provides detailed information on employment sectorand income. For more information on the LFS, see Appendix A.3.

30

their energy intensity to gauge the role of the conventional cost channel. Second,I group sectors by how sensitive they are to changes in aggregate demand (seeAppendix B.3 for more information).

Table 2: Sectoral distribution of employment

Sectors Overall By income group

Low-income Middle-income High-income

Energy intensityHigh 21.8 9.8 25.8 25.9Lower 78.2 90.2 74.2 74.1

Demand sensitivityHigh 30.6 49.1 27.3 18.1Lower 69.4 50.9 72.7 81.9

Notes: The table depicts the sectoral employment distribution of households in the LFS,both overall and by income group (where income is proxied by net pay in the main andsecond job). I group sectors along two dimensions: their energy intensity and their de-mand sensitivity. The energy-intensive sectors include agriculture, utilities, transporta-tion, and manufacturing (SIC sections A–E and I). The demand-sensitive sectors includeconstruction, wholesale and retail trade, hospitality, and entertainment and recreation(SIC sections F–H and O–Q).

Table 2 presents descriptive statistics on the sectoral distribution of house-holds, both overall and by income group. We can see that only few low-incomehouseholds work in sectors with a high energy intensity such as utilities or man-ufacturing. Thus, the sectors’ energy intensity is unlikely to explain the hetero-geneous income responses that we observe. A more relevant dimension of het-erogeneity appears to be the sectors’ demand sensitivity: low-income householdswork disproportionally in sectors that tend to be more sensitive to aggregate de-mand fluctuations, such as retail or hospitality, while a large majority of higherincome households work in less demand-sensitive sectors.

In a next step, I study how the median income across different sectors changesafter a carbon policy shock. Figure 10 presents the results. It turns out that the sec-tors’ energy intensity does not appear to play a crucial role for the magnitude ofthe income response. In fact, the response in sectors with a high energy intensityis relatively comparable to the response in sectors with a lower energy intensity.18

In contrast, there is significant heterogeneity by the sectors’ demand-sensitivity:

18Note that I exclude utilities from the energy-intensive group, as there is reason to believethat the utility sector behaves differently from other energy-intensive sectors. In fact, as shownin Figure B.22 in the Appendix, the utility sector does not display a significant fall in incomes, inline with the findings from Section 5.4.

31

Figure 10: Income response by sector of employment

Notes: Impulse responses of income (pay from main and second job net of deduc-tions and benefits) in different sectors, grouped by their energy-intensity and demand-sensitivity. The response is computed based on the median income in the respectivegroup of sectors. The sector groups are described in detail in Table 2.

households working in demand-sensitive sectors experience the largest and mostsignificant fall in their income after a carbon policy shock while households inless-demand sensitive sectors face a much more muted income response.

These results support the interpretation that carbon policy shocks mainlytransmit to the economy through the demand side, and not by affecting produc-tion costs. While this may seem surprising, it is in line with previous evidence byKilian and Park (2009) on the transmission of energy price shocks. Importantly,the results also help explain why low-income households display a stronger fallin their income, as they disproportionally work in demand-sensitive sectors. Inresponse to a carbon policy shock, these sectors face a stronger decrease in de-mand than other sectors and thus react by laying off employees and cutting com-pensation.

To better disentangle these indirect effects from the direct effect via the energyshare, I look at the responses of low- and higher-income households condition-ing on the most exposed high-energy share households and households with alower energy share. The responses are shown in Figure B.23 in the Appendix. Afew observations emerge from this exercise. First, we can see that low-incomehouseholds with a high energy share display a much stronger fall in their ex-

32

penditure than households with a lower energy share in the same income group.This differential response, however, cannot be solely accounted for by the energyshare heterogeneity as the income response also turns out to be more pronouncedfor low-income households with a high energy share. The role of these indirecteffects via the decrease in household income can also be appreciated by compar-ing the responses of low-income and higher-income households conditional ona high energy share. Despite having a comparable energy share, higher-incomehouseholds lower their expenditure by much less, consistent with the fact thatthey experience a smaller fall in their incomes. Interestingly, there is less hetero-geneity in the expenditure response across income groups conditional on a lowerenergy share, consistent with the fact that the income responses in this case arealso more similar. Overall, these results further illustrate the importance of indi-rect effects working through income and employment.