The Development of the Mortgage-Backed Bond Market Presented by: Renan Schiavetto and Geovany Simon

The Development of the Mortgage-Backed Bond Market Presented by: Renan Schiavetto and Geovany Simon.

Dec 13, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

The Development of the Mortgage-Backed Bond Market

Presented by: Renan Schiavetto and Geovany Simon

History

Fannie Mae (FNMA) Established in 1938 with one single purpose:

“To promote home ownership in the United States”

Ginnie Mae (GNMA) Established in 1968

First GSE to issue Mortgage-Backed Securities

Freddie Mac (FHLMC) Established in 1970

Had the power to buy mortgages from institutions under the FDIC

History (Cont’d)

Secondary Mortgage Market Enhancement Act of 1984 (SMMEA) Loose regulation for private companies

Structure

Government Policies

Alternative Mortgage Transaction Parity Act of 1982 Non-Federally chartered institutions able to sell ARM

ARM very popular in the 90’s

By 2006, almost 90% of subprime mortgages were ARM According to the Financial Crisis Inquiry Report (FCIC)

Gramm-Leach-Bliley Act Repealed the glass-stegall act

Created the shadow banking system Hedge Funds

Investment banks

Insurance Companies

Money Market funds

Financial Crisis

Moral Hazard Problem “No risky business”

Subprime Mortgage Boom MBS with risky mortgages being rated AAA by rating institutions

Moody's

Fitch

Standard and Poor’s

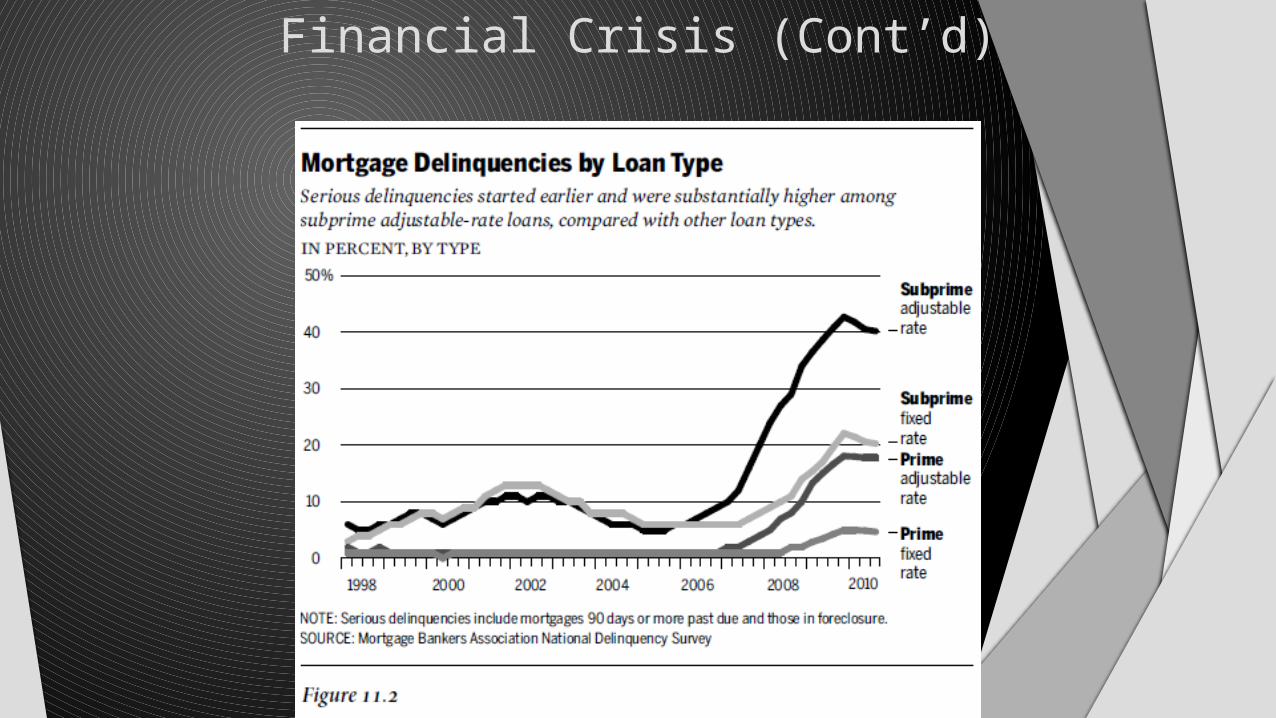

Financial Crisis (Cont’d)

Easy Lending Moral Hazard

Loose Regulations

Credit RiskNo Credit CheckFinancial Institutions Wanted to Issue as Many Mortgages as Possible

Mortgages became assets

No-Doc LoansNo proof of income was requiredVery little documentation from mortgages issued in the 2000’s

Financial Crisis (Cont’d)

Aftershocks

The average house hold in the USA lost an average of 5,800$ in income during the recession peak

The cost to the Federal government to stop the crisis was around 2,000$ on average for every household in the USA

Combined of the decreasing costs with stock values and housing values was around 100,000$ average for every household in the USA

Home values The USA lost $3.4 trillion in real estate wealth according to the Federal government

Stock value The USA lost around 7.4$ trillion in stock wealth

Jobs 5.5 million jobs were lost because of slow economic growth

Income The economic recession cost around 648$ billion dollars

Government response Federal government implemented Troubled Asset Relief Program (TARP)

that resulted a net cost to taxpayers of $73 billion

Aftershocks (Cont’d)

Aftershocks (Cont’d)

Gross Domestic product Highest decrease during the recession in the 4Q of 2008 and the 1Q of

2009 with a decrease at an annual rate of 6%

2008 ended with a GDP of -0.3%, and 2009 ended with a GDP of -3.1%

The US GDP stopped shrinking by the 3Q of 2009, and has been positively growing since then until today

In 2013, the USA GDP reached its four worst years of economic growth (2009-2013) since the 1930’s with a four year economic growth of 0.73%

Aftershocks (Cont’d)

Distribution of Wealth The Federal government conducted a survey during 2007-2009, 4000

households were surveyed

63% of the American families surveyed declared a decrease in their wealth because of the 2008 financial crisis

77% of the richest families declared a decrease in their wealth

50% of the poorest families declared a decrease in their wealth

The top 1% of USA households has netted 95% of total income from 2009 and 2013, compared with the 63% of total income netted by the top 1% of USA households between the years 1993-2013

Global Effects

Europe The European banking system failed mainly because the European banks recklessly

borrowed money in American markets to buy risky securities

The most affected countries with a declining annual growth rate in the 1 quarter of 2009 were Germany 15.2%, 7.4% in the United Kingdom, 18% in Latvia, 9.8% in the Euro area

The 2008 financial crisis later developed into an Eurozone crisis

Middle-East The least affected region in the world. Being oil producing countries, the Middle East

region had a strong currency and a stable economy due to strong oil prices

Asia Slow economic growth during 2008 and 2009 mainly because being export and import

based economies, and with the United States netting almost 1/3 of world’s consumption.

East Asia were the most affected part of Asia, specifically Singapore and Japan.

Singapore GDP’s dropped from a 14% annual growth rate in 2008 to a 1.1% in 2009 and Japan annual growth rate declined 15.2% during the first quarter of 2009.

Global Effects (Cont’d)

Economic Regulations after 2008

Two major acts were implementedA. Dodd-Frank Wall Street Reform and Consumer protection act

B. Housing and economic recovery act of 2008

Both Acts were signed by President Barrack Obama

Dodd-Frank Wall Street Reform and Consumer Protection Act

Introduced by Senator Chris Dodd in 2010, and revised by Congressman Barney Frank, signed by President Barrack Obama in 2010

Composed of 8 major regulations Regulate credit cards, loans, and mortgages

Creation of the Consumer Financial Protection Bureau

Supervise Wall Street The Financial Stability Oversight Council looks out for risks that affect the entire financial

industry

Stop banks from gambling with depository’s money The Volcker rule bans banks from using or owning hedge funds for their own profit purposes

Regulate risky derivatives Risky derivatives, like credit default swaps, be regulated by the Securities Exchange

Commission (SEC) or the Commodity Futures Trading Commission (CFTC)

Bring hedge funds trades into the light Hedge funds must register with the SEC and provide data about their trades and portfolios

Oversee credit ranging agencies Dodd-Frank created an Office of Credit Ratings at the SEC to regulate credit ratings

agencies like Moody's and Standard & Poor‘s

Increase supervision of insurance companies It created a new Federal Insurance Office (FIO) under the Treasury Department, its

mission is to identify insurance companies that create a threat to the entire system Reform the Federal Reserve

The Government Accountability Office (GAO) was permitted to audit the Fed's emergency loans during the financial crisis

Dodd-Frank Wall Street Reform and Consumer Protection Act

Housing and Economic Recovery Act of 2008

Designed to deal with the subprime mortgage crisis and restore the public’s faith in Fannie Mae and Freddie Mac

Signed by President Barrack Obama in 2008 Composed of 7 major regulations

Granting $300 billion in insurance for mortgages.

The creation of a new regulator, the Federal Housing Finance Agency. Awarded with more power to supervise operation of the 14 housing (GSEs).Fannie Mae and Freddie Mac and the 12 Federal Home Loan Bank.

Raises the dollar limit of the mortgages the government sponsored entities can purchase

Provides loans for the refinancing of mortgages for owner-occupants at risk of foreclosure The new loans must be 30-year fixed loans

Enhancements to mortgage disclosures Community assistance to help local governments buy and

renovate foreclosed properties An increase in the national debt ceiling by US$800 billion,

giving the Treasury the elasticity to support the secondary housing markets

Housing and Economic Recovery Act of 2008

Conclusion

Related Documents